A Continuous Time GARCH(p,q) Process with Delay

Abstract

We investigate the properties of a continuous time GARCH process as the solution to a Lévy driven stochastic functional integral equation. This process occurs as a weak limit of a sequence of discrete time GARCH processes as the time between observations converges to zero and the number of lags grows to infinity. The resulting limit generalizes the COGARCH process and can be interpreted as a COGARCH process with higher orders of lags.

We give conditions for the existence, uniqueness and regularity of the solution to the integral equation, and derive a more conventional representation of the process in terms of a stochastic delayed differential equation. Path properties of the volatility process, including piecewise differentiability and positivity, are studied, as well as second order properties of the process, such as uniform and bounds, mean stationarity and asymptotic covariance stationarity.

keywords:

[class=MSC] 60G51, 60H10, 60H20, 62M10keywords:

Lévy process; COGARCH process; continuous time GARCH process; stochastic functional differential equation;t2RSFAS, ANU College of Business and Economics. Email:adam.nie@anu.edu.au

1 Introduction

The ARCH (autoregressive conditionally heteroscedasticity) and GARCH (generalized ARCH) models, introduced by Engle [17] and Bollerslev [9], are widely used in financial econometrics to capture stylized features observed in asset return time series, including heteroscedasticity, volatility clustering and heavy tailedness. These classes of models aim to capture the conspicuous dependence between asset returns and their volatility, whereby a large fluctuation in the asset price typically causes a large fluctuation in the volatility, which persists for a period of time before reverting to a baseline level. For a review of the probabilistic properties, stationarity, and mixing properties of GARCH models, we refer to [10] and [32].

For certain applications including option pricing and the modeling of irregularly spaced or high frequency data, a model in continuous time is often preferred. For a comprehensive review of continuous time GARCH processes, we refer to Lindner [31]. The first notable attempt was due to Nelson [37], who constructed a diffusion limit from a suitably scaled sequence of GARCH(1,1) processes, akin to constructing a Wiener process from a sequence of scaled random walks. However, the resulting diffusion process loses desirable properties possessed by the approximating GARCH processes in discrete time. In particular, the diffusion limit is driven by two independent Wiener processes whereas the GARCH process is driven by a single sequence of noise, and the feedback mechanism between the price and the volatility is lost in the limit. Furthermore, Wang [42] shows that parameter estimation for the discrete time GARCH process is not equivalent to that of the diffusion limit. Nevertheless, numerous authors have studied the properties and applications of Nelson’s limit, and we refer to [12, 14, 24] and the references within.

Klüppelberg, Lindner, and Maller [27] took a significantly different approach and constructed the Continuous Time GARCH (COGARCH) process by replacing the innovation sequence in the original GARCH with the increments of a Lévy process. The resulting variance process is a generalized Ornstein-Uhlenbeck process (see [30]) driven by a single Lévy noise, and retains many of the desirable features of the original GARCH process. Kallsen and Vesenmayer [25] demonstrated that akin to the construction in [37], the COGARCH process can indeed be obtained as a weak limit of a sequence of GARCH(1,1) processes, and argued heuristically that the diffusion limit and the COGARCH limit are the only possible limits of sequences of GARCH(1,1) processes. A different discrete approximation scheme was suggested by Maller, Müller, and Szimayer [34], who provided a pseudo-maximum-likelihood estimator applicable to irregularly spaced data. Parameter estimation in the COGARCH process is considered in for instance [20, 34, 36] and the COGARCH is applied in option pricing in numerous works including [28, 29]. An analogous result to [42] for the Nelson limit was obtained in Buchmann and Müller [11].

Both the diffusion limit and the COGARCH process are Markovian processes, and the serial dependence in the variance process is implicit in the defining stochastic differential equation (SDE). Lorenz [33] on the other hand constructed a non-Markovian continuous GARCH process that explicitly specifies the serial dependence in the volatility process. Unlike the diffusion limit and the COGARCH process which are weak limits of GARCH(1,1) processes, [33] considered a sequence of GARCH volatility processes defined sequence of uniform grids of mesh size and took to infinity. A weak limit is obtained as the solution of a stochastic functional differential equation (SFDE) driven by a Wiener process, which is direct generalization of the Nelson limit.

The same idea was explored in greater depth recently in the PhD thesis of Tran [41] and the working papers of Dunsmuir, Goldys, and Tran [15, 16], where the authors considered a more general situation in which both GARCH and ARCH orders are allowed to tend to infinity as the grid becomes finer. The sequence of discrete GARCH price and volatility processes are shown to converge weakly in the Skorokhod topology to the solution of a pair of stochastic functional integral equations

where and are the return and variance processes respectively. Here, and are Borel measures representing the delay effects of higher order lags, and are semimartingales, and is the quadratic variation process of . This limit is referred to as the continuous time GARCH process with delays , or the CDGARCH process for short. Depending on how the discrete noise sequence is constructed, the limiting noise sequence could be a Brownian motion, in which case the CDGARCH generalizes Lorenz’s limit in [33], or a Lévy process, of which the COGARCH process is a special case. In this paper, we focus on the latter case of a CDGARCH process driven by a Lévy process, and compare its properties to the COGARCH and similar processes in the literature.

When and , the CDGARCH variance process satisfies an SFDE with an affine (deterministic) drift coefficient and multiplicative noise. Although this class of equations appear in the existing literature, the usual assumptions made are generally too restrictive for our case. Earlier work by Reiß, Riedle, and van Gaans [40] focuses on the existence of an invariant measure of the solution to this class of SFDEs, while the uniqueness of the invariant distribution is discussed in Hairer, Mattingly, and Scheutzow [18]. In the general case where , the resulting SFDE of the volatility process (derived in Section 4.1) has a non-deterministic drift coefficient that depends on past values of the driving noise as well as the volatility process, a case not considered in most works in the literature. The monograph Bao, Yin, and Yuan [3] collected a series of recent papers, some of which have a close connection to the CDGARCH process and the question of strict stationarity.

The rest of the paper is organized as follows. Section 2 outlines the CDGARCH process constructed in [15], motivated its resemblance to the GARCH process in discrete time. Section 3 collects some preliminary results on stochastic integration, Lévy processes, and deterministic functional differential equations. We present the main results of this paper in Section 4 and Section 5, but defer all proofs and technical lemmas to Section 6 in order to maintain the flow of our exposition.

Section 4.1 gives conditions for the existence, uniqueness and regularity of a strong solution to the CDGARCH equations, as well as differential representations of the solution in more conventional forms. Section 4.2 studies the path properties of the CDGARCH process under compound Poisson driving noise, while Section 4.3 shows that the solution in general can be approximated with solutions driven by compound Poisson processes. Section 5.1 gives uniform and bounds for the solution process, and Section 5.2 studies the second order properties of the solution, including mean stationarity and covariance structure of the volatility process as well as the return process.

2 The CDGARCH Model

The GARCH model in discrete time, with GARCH order and ARCH order , is defined in [9] as the bivariate process

| (2.1a) | ||||

| (2.1b) | ||||

Here and is a sequence of uncorrelated random variables with zero mean and unit variance. The non-negative real sequences and are the GARCH and ARCH parameters respectively. The sequence usually represents the log-return of a financial asset, while models its conditional variance.

We now introduce a form of the CDGARCH equation to be studied in this paper, motivated by its resemblance with the GARCH process in discrete time. Writing , for , the GARCH process defined above can be rewritten as

| (2.2a) | ||||

| (2.2b) | ||||

This formulation motivated [15, 16, 41] to study the following analogous setup in continuous time. Fix a filtered probability space that satisfies the usual assumptions (see [39], page 3). The CDGARCH equation with delays of length is defined by the stochastic functional integral equations

| (2.3a) | ||||

| (2.3b) | ||||

with positive initial conditions and for all , where is -measurable and is adapted. Here, is an adapted càdlàg process analogous to the term in (2.2b). The measures and are signed Borel measures with finite variations, supported on and respectively, analogous to the sequence of coefficients and . The process is a locally square integrable Lévy process adapted to , analogous to the white noise sequence , and is the quadratic variation process of analogous to the sequence . We will specify in detail in Section 3.1.

In this paper we will assume the following specification of the process and the delay measures and . The motivation behind these choices comes from their resemblance to the discrete time GARCH, as well as from the methodology in the construction of the CDGARCH process as a weak limit of discrete GARCH processes in [15, 16, 41].

Put . Let (resp. ) be the space of càdlàg functions (resp. processes) on and write and . Given an initial process , we extend it to by setting , for all . Fix a positive constant . Throughout the paper we will assume takes the form

| (2.4) |

and assume the delay measures have point masses at and are absolutely continuous with respect to the Lebesgue measure on . That is, for any ,

| (2.5) |

Here and are positive constants, and are nonnegative and continuous functions supported on and respectively, and denotes the Dirac measure at zero. Since and are supported on and , it is clear that and . We will write for either integral throughout the paper when there is no ambiguity of the meaning.

Remark 2.1.

These choices, including the signs of the constants, are very natural in that they arise as the limit of the sequences and as a sequence of GARCH processes converges weakly to the CDGARCH limit. On the other hand, we may study the CDGARCH equation as a continuous time GARCH process in its own right without constraining it to be a proper weak limit, then we have more freedom in choosing , and . ∎

Remark 2.2.

When , , and , the CDGARCH variance equation (2.3b) reduces to a stochastic differential equation

| (2.6) |

which (with a reparameterization) is the SDE specifying the COGARCH process (see [27] Proposition 3.2). On the other hand, taking to be a Brownian motion, it is possible to define a similar pair of SFDEs that generalizes Nelson’s diffusion and Lorenz’s limit. We do not pursue this setup.

Remark 2.3.

In the case where and , by Fubini’s Theorem, the variance process follows a stochastic delayed differential equation

| (2.7) |

which has an affine (delayed) drift term and multiplicative noise. A similar equation was considered in Reiß et al. [40]. Although more general in some respects, [40] assumed uniform boundedness of the diffusion coefficient, which does not apply in our situation.

3 Preliminaries

We first collect some preliminary results. We follow Jacod and Shiryaev [23], Protter [39] semimartingale theory, Applebaum [1] for Lévy processes, and Diekmann, van Gils, Lunel, and Walther [13] for deterministic delay differential equations.

3.1 Driving Lévy process

Recall and suppose we have a filtered probability space that satisfies the “usual conditions” (see Definition 12, [23]). Given a stochastic process , we write for the natural filtration of .

Let be a càdlàg, adapted martingale with respect to . We follow Protter [39] and call a square integrable martingale if for every . For a process with finite second moments, i.e. for all , write (resp. ) for the quadratic variation (resp. predictable quadratic variation) process of . Let be the set of all predictable processes such that the integral process is integrable, i.e. for each fixed . The following lemma follows from Theorems I.4.31 - I.4.40 of Jacod and Shiryaev [23].

Lemma 3.1.

Let be a semimartingale and suppose is càdlàg and predictable. Then the integral process is a càdlàg, adapted process. If furthermore is a square integrable martingale and , then is a square integrable martingale.

We assume that the space supports a càdlàg, -adapted Lévy process , such that a.s., is stochastically continuous and for all , is independent of and has the same distribution as . Put and write for the Borel sigma-algebra on . When with , write

for the Poisson random measure on associated with and write for the corresponding Lévy measure on . Write for the compensated Poisson random measure.

Recall that a Lévy measure always satisfies . Throughout the paper, we will also assume that has finite second moment and is centered, so that is a square integrable martingale with respect to , i.e., and for all . The Fourier transform of the law of is then given by the Lévy-Khintchine formula

where . Furthermore, the Lévy-Itô decomposition of gives

| (3.1) |

where is a standard Brownian motion with respect to , having , a.s. The quadratic variation process of is the subordinator

| (3.2) |

Put , so that the process defined by

| (3.3) |

is a martingale with respect to (see [1], Theorem 2.5.2). If furthermore has finite fourth moments, then and is a square integrable martingale, with predictable quadratic variation process .

3.2 Delay differential equations

Consider the deterministic functional differential equations

| (3.4) |

with initial condition for some . Here is a signed Borel measure with finite total variation on . For each initial condition , there exists a unique solution on , i.e. for all , is continuously differentiable on , and (3.4) holds on . The asymptotic stability of this solution as is governed by the roots of the so-called characteristic function of , defined as

| (3.5) |

Let be a solution to (3.4) and fix any such that on the line . Then [13] gives the following asymptotic expansion of :

| (3.6) |

where are finitely many zeros of with real part exceeding , and is a -valued polynomial in of degree less than the multiplicity of as a zero of . In particular, it’s clear from (3.6) that if is root free in the right half-plane , then the zero solution is asymptotically stable, that is, all solutions of the functional differential equation (3.4) converge to the zero solution exponentially fast as .

4 The solution process

We wish to rewrite (2.3b) into a form more commonly seen in the literature, but doing so requires some regularity of the solution . We thus start with establishing the existence, uniqueness and regularity of a strong solution to (2.3b). All proofs and supporting lemmas are deferred to Section 6 in order to maintain the flow of the exposition.

4.1 Existence, uniqueness and representations

We define the appropriate space for the solution process and give sufficient conditions for the existence of a unique solution in this space.

Definition 4.1.

For , define the maximum process and the random variable . Let be a family of semi-norms given by

| (4.1) |

We denote by the class of càdlàg processes on with finite for every . ∎

Definition 4.2.

Assumptions 4.1.

-

(a)

The initial process is adapted to , with .

-

(b)

The process as defined in (3.2) is square integrable, i.e. . ∎

Theorem 4.3.

Remark 4.1.

At this point we do not require the solution to be bounded away from zero or even positive. We give a positive lower bound for in Theorem 4.10 of Section 4.3, after deriving a more convenient representation. It is then immediate that the CDGARCH equation (2.3a) is also well defined and a semimartingale, with jumps given by . ∎

We precede Theorem 4.5 with the following useful results. Recall that the delay densities and from (2.5) are functions. Let be kernels given by

| (4.2) |

Then and are clearly Volterra type kernels on , i.e. for all . It will turn out to be useful to consider the stochastic process defined by

| (4.3) |

Proposition 4.4.

Let and be non-negative and continuous on and .

-

(a)

The kernels and are non-negative Lipschitz continuous functions on .

-

(b)

The process has locally Lipschitz continuous sample paths, with derivative

(4.4) for Lebesgue almost every . ∎

We now give two different representations of , one as a stochastic integral equation with Volterra type kernels, akin to the fractional Lévy process, and one in the form of a stochastic functional differential equation driven by the quadratic variation process .

Theorem 4.5.

Let be the unique strong solution to the CDGARCH variance equation (2.3b), with parameters specified in (2.4), (2.5) and driving noise defined in (3.2). Then the process satisfies the stochastic (Volterra) integral equation

| (4.5) |

which can be rewritten into a stochastic functional differential equation

| (4.6) |

with initial condition on . In particular, is a semimartingale and has paths of finite variation on compacts. ∎

Remark 4.2.

-

(a)

The stochastic process in (4.3) is an example of a convoluted Lévy process, studied in Bender and Marquardt [7]. In fact, with a different choice of kernel, we could recover a fractional Lévy process considered in Benassi, Cohen, and Istas [6] and Marquardt [35]. Jaber, Larsson, and Pulido [22] also considered a similar process with convolution type kernels and Brownian driving noise, with applications to modeling asset volatility.

-

(b)

Without the term , the equation (4.6) is exactly the SDE for the COGARCH process, stated previously in (2.6). We can therefore interpret the CDGARCH process as a COGARCH process with an extra stochastic delay-type drift term , which depends on the sample paths of both and . The CDGARCH process is hence not a Markovian process.

-

(c)

The process has been studied by Barndorff-Nielsen et al. in multiple works over the past few years to model stochastic volatility and turbulent flows. In particular is referred to as a volatility modulated Lévy driven Volterra (VMLV), or more specifically, a Lévy semi-stationary (LSS) process in [5]. Furthermore, these processes are special cases of a much more general class of objects called Ambit fields. We refer to Barndorff-Nielsen, Benth, and Veraart [4] and Podolskij [38] for surveys of relevant results. ∎

Remark 4.3.

Observe from (3.2) that the Brownian component of appears in as a positive drift . In light of equations (4.4) and (4.6), we could absorb this drift into the constant and the function , by replacing with and with and changing the region of integration accordingly. Therefore from here onwards, without any loss of generality, we will assume so that is a pure jump Lévy process.

4.2 Path properties of the solution

In Section 4.3 we show that the solution to (4.6) driven by a general , possibly with infinite activity, can be approximated by solutions to (4.6) driven by compound Poisson processes that approximate . We thus formulate some path properties of in the case when (and hence ) is a compound Poisson process, and compare them to the COGARCH process.

Proposition 4.6.

Let be a compound Poisson process, i.e. and the Lévy measure of has finite total mass. Let and be the jump times and sizes of .

-

(a)

The jumps of the CDGARCH variance process are driven by the jumps of the quadratic variation process , i.e.,

-

(b)

If , then on each , is continuous and is continuously differentiable, with derivative given by

Furthermore, when and , between two consecutive jump times, the CDGARCH variance process follows the deterministic delay differential equation

(4.7) In the case , i.e. when is a COGARCH process, decays exponentially between its jump times, and we have a closed form solution

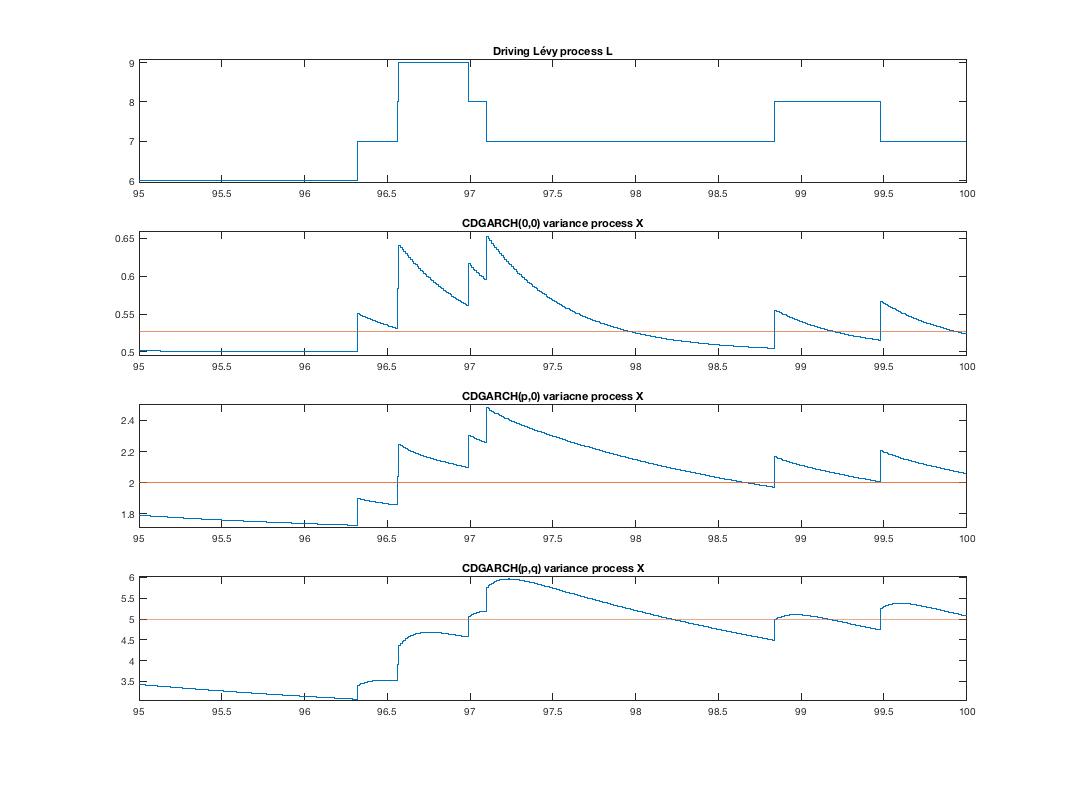

It is clear that the jump structure of the variance process is the same for the COGARCH process and the COGARCH process. However, the behavior of in between jumps is very different. In fact, from Proposition 4.6, we immediately see two levels of generalization from the COGARCH process, which decays exponentially between jumps. We illustrate this graphically by simulating sample paths of the different CDGARCH processes via a simple Euler scheme.

The top figure in Figure 1 is the simulated path of a compound Poisson process with unit intensity and jumps equal to with equal probability. The processes below are the COGARCH (or CDGARCH(0,0)), the CDGARCH(p,0) and the CDGARCH(p,q) variance processes, driven by the same realization of . The horizontal lines are the theoretical (stationary) means of the variance processes, computed in Section 5. The delay functions and are chosen to be exponential, and comparable parameters are chosen between all three processes.

In the CDGARCH case, the process follows a deterministic differential equation (given in Proposition 4.6) between the jumps of the driving noise , but the decay towards the baseline level is slower than the exponential function, indicating a longer memory effect. In the case , is no longer deterministic between jumps, but is given by a continuous process of finite variation that depends on as well as . For this particular simulated process, increases immediately after a jump, then starts decaying towards the baseline level. Depending on choices and sizes of , it is possible to have very different behaviors between jumps.

We now give conditions for the positivity of when is a compound Poisson process, which we extend to the general case in the next section.

4.3 Approximation

Following Remark 4.3, we will assume that takes the form

| (4.9) |

For each , define the approximating process by

| (4.10) |

Then is a sequence of compound Poisson processes satisfying for all and . For each , we will consider equation (4.6) driven by :

| (4.11) |

where the drift coefficient is defined as

By Theorem 4.3, Equation (4.11) has a unique solution in for each initial value satisfying Assumption 4.1(a). Similar to , we will write for the drift coefficient of (4.6) driven by .

Recall from [39] that a sequence of processes converges to uniformly on compacts in probability (ucp) if for each , converges to 0 in probability. To show approximates in the ucp topology, we will need the following set of results, which are interesting in their own right. Let be the (finite and increasing) process given by

| (4.12) |

Proposition 4.8.

-

(a)

For each , converges to in and hence in ucp.

- (b)

-

(c)

For each , the process converges to in and hence in ucp. ∎

We are now in a position to state the approximation result, which allows us to extend Proposition 4.7 to a general driving noise , thus showing positivity of the CDGARCH variance process .

Theorem 4.9.

Theorem 4.10.

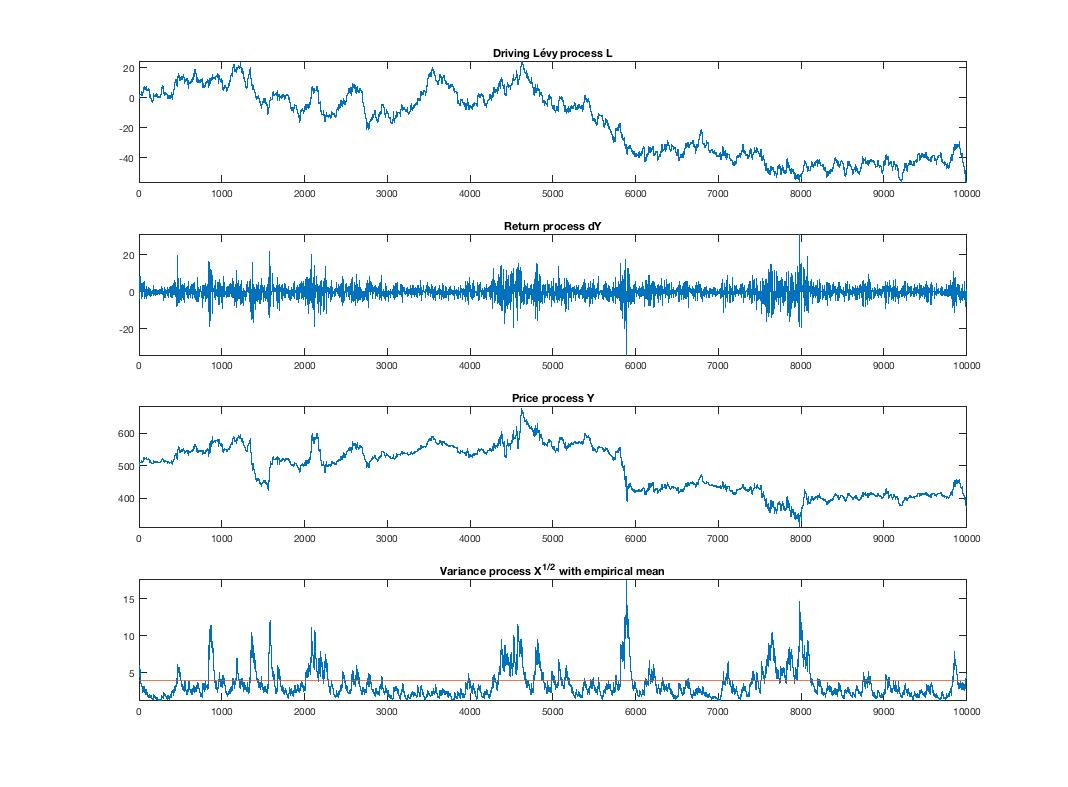

We conclude the current section with simulated paths of the CDGARCH(p,q) price and variance processes. Figure 2 shows simulated sample paths of the driving noise , the return process , the CDGARCH process and its volatility process . Note the return process visibly exhibits volatility clustering which is reflected in the process .

5 Moments

5.1 Uniform moment bounds

We first provide uniform and bounds on . Let be defined as in (2.3b) and the constants be given by

5.2 Moment processes

Let be the mean function of , i.e., , . Write for the mean function of the initial segment . For , define the segment process of the process as . For notational simplicity, we will from here onwards write and .

Theorem 5.2.

If Assumptions 4.1 are satisfied, then for any positive ,

-

(a)

The mean function is finite-valued, continuously differentiable on , and satisfies the (deterministic) functional differential equation

(5.3) with the initial condition for , where .

-

(b)

The mean function also satisfies the renewal equation

with initial condition , with convolution kernel given by

(5.4) and forcing function given by

From Theorem 5.2, we can formulate necessary and sufficient conditions for the process to be mean stationary, i.e., for for all for some , or for to be asymptotically mean stationary, i.e., for when .

Theorem 5.3.

Assume Theorem 5.2 holds so satisfies the functional differential equation (5.3) with some positive initial condition . Then

-

(a)

The mean function converges to a (positive) limit exponentially fast as , if and only if . If it exists, the limit is uniquely given by

(5.5) -

(b)

The process admits a stationary (positive) mean, i.e. for all , if and only if and on , where is given by (5.5).∎

Remark 5.1.

Here, is negative and provides a mean reversion effect, while is positive representing a positive jump in whenever there is a jump in (c.f. Proposition 4.6(a)). The functions and are positive functions representing the delayed effects of past values of and . The key condition for first order stability, , or

| (5.6) |

then has a very natural interpretation: the speed of mean reversion has to be large enough in comparison to the delay effects. ∎

In general, the second moment of the process involves the term , which is not easily evaluated. However, we can still formulate some asymptotic results.

Theorem 5.4.

Suppose condition (5.6) is satisfied so that as . For every and -measurable random variable with , we have exponentially fast as . ∎

The asymptotic behavior of the covariance function of the process is an immediate corollary to Theorem 5.4 by taking .

Corollary 5.5.

Suppose is asymptotically mean stationary and has finite fourth moments. Then for every , the covariance function tends to zero exponentially fast as . Thus, the process possesses “short memory”. ∎

We finally look at the properties of the price and return processes under the CDGARCH model. Recall the price process , and define the return process by .

Theorem 5.6.

Let be the solution to (4.6) and be defined as above. Suppose is mean stationary, with mean defined in (5.5).

-

(a)

The return process is covariance stationary, with zero mean and auto-covariance function given by .

-

(b)

Suppose has finite fourth moments. Then for any , the squared return process satisfies exponentially fast as , i.e., has short memory. ∎

6 Proofs

6.1 Existence and uniqueness of the solution

Given a signed measure on a measure space , we denote its corresponding total variation measure by , for all , where the supremum is taken over all -measurable partitions of . We also denote the total variation norm of as .

Let and be signed Borel measures on with finite total variations and be a càdlàg, adapted process with paths of finite variation. Recall from (2.4) and from (4.1). We can write the variance equation (2.3b) as , where is a linear map on given by

| (6.1) |

and for all . Using Lemma 3.1, it is easy to see that is càdlàg and adapted, whenever is càdlàg and adapted. We first obtain some norm estimates on :

Lemma 6.1.

Proof.

For notational convenience, we will define the semi-norm

Since for , by the inequality , we have

Since on , an application of the Cauchy-Schwarz inequality yields the bound

| I |

For , recall from (3.3). Using the same reasoning as above,

By similar workings as in , we have For , recall is a square integrable martingale and . Since , is clearly in , and the process is a square integrable martingale by Lemma 3.1. By Jensen’s inequality, Doob’s inequality and the Ito isometry, we have

The lemma follows immediately by collecting all terms. ∎

Proof of Theorem 4.3.

(a). Let and satisfy Assumptions 4.1 and be defined in (2.4). For the existence of a solution, we use a Picard iteration to produce a sequence of -processes that converges to a limit. Set the initial term , and define recursively for each the process . We see that the differences between each term are given by and , for .

Write , so that and , for . The first term is finite by an application of Lemma 6.1 to . Since , by Lemma 3.1 and the second bound in Lemma 6.1, is in whenever is in . Therefore by induction, for each , the difference is in and we can apply Lemma 6.1 to each .

Since is non-decreasing and non-negative on , applying Lemma 6.1 to each and expanding the recursion yields a Gronwall type inequality

The sequence is therefore Cauchy for each . Since is complete in , taking , the sequence of processes

converges in to a limit , which is also in .

It remains to show that this limit is indeed a solution to (2.3b), i.e. satisfies . First, observe that since is summable for every ,

| (6.2) |

as . Using , by the second bound from Lemma 6.1, we also have

Then by the triangle inequality, for any ,

which implies that a.s. and hence (2.3b) is satisfied on any .

To establish uniqueness, suppose and are two strong solutions to (2.3b), i.e., we have and . Let . By Lemma 6.1, for any , we have , where is defined in Lemma 6.1. By Gronwall’s inequality (Thm V.68, [39]), for all which implies that , almost surely, and the two solutions are indistinguishable.

(b). Since for any and , we have,

Hence the function is finite-valued. Since is càdlàg, by the dominated convergence theorem with as dominating functions, is a càdlàg function on for . ∎

6.2 Properties of the solution

Proof of Proposition 4.4.

(a). We first rewrite . For any and , by the triangle inequality, is Lipschitz on since

where is the sup-norm and is the Euclidean distance on . Similarly for .

(b). Since and are identically zero whenever or , we will omit the region of integration and write .

Since for almost every , is a non-decreasing càdlàg function, we will fix such an and treat the stochastic integral above as a Lebesgue-Stieljes integral with respect to the function . Since and vanishes for , by Proposition 4.4(a), for any ,

It follows that is locally Lipschitz continuous almost surely, since with probability one is locally bounded and has finite variation on compacts.

We first compute - the case of is identical and omitted. In the expression , the integrand clearly does not depend on whenever , hence is constant on these regions and . On the interval , we have so by the Fundamental Theorem of Calculus, is continuously differentiable and on the interval . We can therefore write for almost every . Clearly, is not differentiable at or , unless and are equal to zero.

We now compute the derivative of the second integral in (4.3):

| (6.3) |

The case of the first integral is similar and omitted. Again, we fix an such that is a non-decreasing càdlàg function and treat the integral as a Stieljes integral. For every , the map is in since and are locally bounded and is supported on a compact set. For every , the map is continuously differentiable in by the previous argument. For every , the derivative is locally bounded and hence also in . Then by the differentiation lemma ([26, Theorem 6.28]), is differentiable almost everywhere with derivative

| (6.4) |

The expression (4.4) then follows with a simple change of variable. ∎

Proof of Theorem 4.5.

Recalling , we have

Since and is hence locally bounded and progressively measurable, by Fubini’s theorem, exchanging the order of integration of gives

for , where the kernel is given by 4.2. The computations for the integral in (2.3b) are exactly the same and the integral equation (4.5) follows immediately.

For the functional differential equation, first observe that in (6.3) is Lipschitz and hence absolutely continuous. Hence , where is given by (6.4), with since for any . The integral involving can be differentiated in exactly the same way. The functional differential equation follows immediately.

Finally, since is of finite variation and is càdlàg, is a semimartingale with finite variations by Theorem I.4.31 of Jacod and Shiryaev [23]. ∎

Proof of Proposition 4.6.

Proof of Proposition 4.7.

Suppose for all , for some and let . Since is a compound Poisson process, almost surely and the interval is non-empty. Then by Proposition 4.6(b), is continuously differentiable in with derivative given by . Since whenever , by iterating this argument, it suffices to show that for all .

Let and suppose for a contradiction that with positive probability. Since is a.s. continuous at , necessarily and . But

almost surely, which contradicts our assumption. ∎

6.3 Approximation by processes of finite activity

Proof of Proposition 4.8.

(a). From the construction of in (4.10), we have

which in non-decreasing in . Fixing , we have

Since , the integrand is dominated by which is integrable. By the dominated convergence theorem, as . That is, approximates in each , . This clearly implies convergence in the ucp topology.

(b). Let and be càdlàg processes in , then

Since is assumed to be continuous and normalized to , integrating by parts gives

which implies that is functional Lipschitz. For each , it suffices to carry through the same computation and observe that by construction, for each and .

Proof of Theorem 4.9.

Proof of Theorem 4.10.

For a given of the form (4.9) satisfying Assumption 4.1(b), let be as defined in (4.10). By Theorem 4.3, we can set and to be unique solutions to (4.6) and (4.11) driven by and respectively.

By Theorem 4.9, converges to in ucp, which trivially implies that for each , in probability and hence in distribution. Furthermore, since each is a compound Poisson process by construction, by Proposition 4.7, for each and , we have with probability one, where is defined in (4.8). Finally, since is open in , by the Portmanteau theorem of weak convergence (Theorem 2.1 Billingsley [8]), we have for each ,

which completes the proof. ∎

6.4 Moment bounds

We precede the proof of Theorem 5.1 with the following two lemmas.

Lemma 6.2 (Lemma 8.1 - 8.2, Ito and Nisio [21]).

Suppose are continuous functions, and . For every ,

-

(a)

if , then ;

-

(b)

if , then .∎

Lemma 6.3.

Suppose Assumptions 4.1 hold, let be the unique strong solution to (4.6) with initial condition and let be as defined in (4.4). For , we have

where and .

Proof.

For the case of , by Fubini’s theorem and the Cauchy-Schwartz inequality,

The case of easily follows from the same computations. ∎

Proof of Theorem 5.1.

(a) and (b). The following proof holds for both and , with different corresponding constants. Let be a positive solution to (4.6) with . For , it follows from Ito’s Lemma ([23, Theorem I.4.57]) that (the case is trivial),

| (6.5) |

where and

Let and put and . From (6.5), we have

| (6.6) |

Let be given as in Lemma 6.3 and suppose

| (6.7) |

An exercise in calculus gives and Then for all ,

which we rearrange to get a bound for the integrand in the first integral in (6.6):

| (6.8) |

For the second integral of (6.6), Lemma 6.3 gives the bound

Combining this with (6.6) and (6.8) and writing , we have

where the constants and are given by and . Our assumed condition (6.7) gives . By Lemma 6.2 (a),

| (6.9) |

Since is non-decreasing and , an integration by parts shows

The last expression is an non-decreasing function of . Hence taking supremums in (6.9), we have

By Lemma 6.2 (b), since and for all , we have

The Theorem follows immediately. ∎

Remark.

The above arguments are partly adapted from [2], but we expand on their arguments and derive explicit bounds and constants to have explicit bounds for the first and second moments.

6.5 Moment processes

Proof of Theorem 5.2.

(a). Since , the stochastic integral process is a true martingale. Taking expectation of the equation (4.6), we get

Recalling the definitions of and before Theorem 5.2, we have the integral equation

From Theorem 4.3, we know that the function is càdlàg and hence locally bounded. Since is integrable, for any , by the dominated convergence theorem,

so the function is continuous. Furthermore,

so the function is continuous as well. Therefore is continuously differentiable and the differential equation follows.

(b). The proof is adapted from Section 6.1 of Hale and Lunel [19]. Put and and , then clearly is the solution to the linear delay equation

| (6.10) |

with initial condition on . With defined in (5.4), we can rewrite (6.10) into

For , we can separate the initial condition in (6.10) to obtain

| (6.11) |

Now, since is by construction constant for , (6.11) holds for also. Integrating by parts, we obtain a renewal equation for :

| (6.12) |

with initial condition , where . Integrating (6.12) and changing the order of integration, we obtain

Changing variables , we arrive at a renewal equation for :

| (6.13) |

with initial condition . The forcing function, , given by

| (6.14) |

is Lipschitz continuous on and constant for [13, p.18]. Since , substituting and back into (6.13) and (6.14) completes the computations. ∎

Proof of Theorem 5.3.

(a). Let , and be as defined in the proof of Theorem 5.2 (b). The characteristic function of (6.10) defined in (3.5) is given by

It’s clear from (3.6) that if is root free in the right half-plane , then all solutions of the functional differential equation (6.10) converge to zero exponentially fast as .

For sufficiency, it is enough to show that implies for any with . Let where . Then the real part of can be written as

Since and are no greater than 1 on , we have whenever , so is root free on . For necessity, the expansion (3.6) implies that 0 is the only possible limit of , which gives the uniqueness of as a limiting mean. Since we require this limit to be positive, necessarily we require .

(b). Suppose that where is defined in (5.5), and assume so that . Then is identically zero on , and the function defined in (6.14) is identically zero on . From (6.13), the centered mean process satisfies satisfies the homogeneous renewal equation

Applying the representation in Theorem 2.12 of Diekmann et al. [13] shows that the only solution to this renewal equation is for all . This gives for all . Conversely, suppose that for all , for some positive . Then (5.3) gives , which implies that is uniquely given by (5.5) and . Recall that the delay equation (5.3) has a unique solution once the initial condition is fixed. Therefore the solution for all then corresponds uniquely to the initial condition on , and the proof is complete. ∎

Proof of Theorem 5.4.

Let be an measurable random variable with for any . Since has finite variations, for any and , we have

Taking expectations and using Fubini’s theorem gives

Since is measurable and hence measurable for any , the two stochastic integrals in the last expression have zero expectation. Therefore

from which we obtain a functional differential equation,

Since we assumed , by the same argument as in the proof of Theorem 5.3 (b), we have

exponentially fast. ∎

Proof of Theorem 5.6.

(a) Since and has zero mean, we have and .

(b). Write . Since , by Ito’s lemma, it holds that , where

Then, since , we have

Now suppose so that is measurable. Taking expectations, we obtain

By Theorem 5.4 and Theorem 5.6 (a), exponentially fast as , i.e. there exists constants and such that for all . Therefore

for all , which finishes the proof. ∎

Acknowledgment

The author’s research is supported financially by the Australian Government Research Training Program (AGRTP). The author wishes to thank Prof. Boris Buchmann and Prof. Ross Maller for their help and support, as well and Prof. William Dunsmuir for all the insightful discussions.

References

- Applebaum [2009] David Applebaum. Lévy Processes and Stochastic Calculus. Cambridge University Press, Cambridge; New York, 2009.

- Bao et al. [2014] Jianhai Bao, George Yin, Chenggui Yuan, and Le Yi Wang. Exponential ergodicity for retarded stochastic differential equations. Applicable Analysis, 93(11):2330–2349, 2014. 10.1080/00036811.2014.952291.

- Bao et al. [2016] Jianhai Bao, George Yin, and Chenggui Yuan. Asymptotic Analysis for Functional Stochastic Differential Equations. SpringerBriefs in Mathematics. Springer International Publishing, 2016.

- Barndorff-Nielsen et al. [2012] Ole E. Barndorff-Nielsen, Fred Espen Benth, and Almut ED Veraart. Recent advances in ambit stochastics with a view towards tempo-spatial stochastic volatility/intermittency. arXiv preprint arXiv:1210.1354, 2012.

- Barndorff-Nielsen et al. [2013] Ole E. Barndorff-Nielsen, Fred Espen Benth, Almut ED Veraart, and others. Modelling energy spot prices by volatility modulated Lévy-driven Volterra processes. Bernoulli, 19(3):803–845, 2013.

- Benassi et al. [2004] Albert Benassi, Serge Cohen, and Jacques Istas. On roughness indices for fractional fields. Bernoulli, pages 357–373, 2004.

- Bender and Marquardt [2008] Christian Bender and Tina Marquardt. Stochastic calculus for convoluted Lévy processes. Bernoulli, 14(2):499–518, 2008. 10.3150/07-BEJ115.

- Billingsley [2013] Patrick Billingsley. Convergence of Probability Measures. John Wiley & Sons, June 2013.

- Bollerslev [1986] Tim Bollerslev. Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31(3):307–327, 1986.

- Bougerol and Picard [1992] Philippe Bougerol and Nico Picard. Stationarity of GARCH processes and of some nonnegative time series. Journal of econometrics, 52(1-2):115–127, 1992.

- Buchmann and Müller [2012] Boris Buchmann and Gernot Müller. Limit experiments of GARCH. Bernoulli, 18(1):64–99, 2012. 10.3150/10-BEJ328.

- Corradi [2000] Valentina Corradi. Reconsidering the continuous time limit of the GARCH(1,1) process. Journal of Econometrics, 96(1):145–153, May 2000. 10.1016/S0304-4076(99)00053-6.

- Diekmann et al. [2012] Odo Diekmann, Stephan A. van Gils, Sjoerd M. V. Lunel, and Hans-Otto Walther. Delay Equations: Functional-, Complex-, and Nonlinear Analysis. Springer Science & Business Media, 2012.

- Duan [1997] JC Duan. Augmented GARCH (p, q) process and its diffusion limit. Journal of Econometrics, 1997.

- Dunsmuir et al. [a] William Dunsmuir, Ben Goldys, and Cuong Viet Tran. On Limits of Continuous Time Bilinear Processes (working paper). a.

- Dunsmuir et al. [b] William Dunsmuir, Ben Goldys, and Cuong Viet Tran. Stochastic Delay Differential Equations as Weak Limits of GARCH processes (working paper). b.

- Engle [1982] Robert F. Engle. Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica, 1982.

- Hairer et al. [2011] M. Hairer, J. C. Mattingly, and M. Scheutzow. Asymptotic coupling and a general form of Harris’ theorem with applications to stochastic delay equations. Probability Theory and Related Fields, 149(1-2):223–259, 2011. 10.1007/s00440-009-0250-6.

- Hale and Lunel [2013] Jack Hale and Sjoerd M Verduyn Lunel. Introduction to Functional Differential Equations. Springer Science & Business Media, 2013.

- Haug et al. [2007] S. Haug, C. Klüppelberg, A. Lindner, and M. Zapp. Method of moment estimation in the COGARCH(1,1) model. The Econometrics Journal, 10(2):320–341, 2007. 10.1111/j.1368-423X.2007.00210.x.

- Ito and Nisio [1964] K. Ito and Makiko Nisio. On stationary solutions of a stochastic differential equation. J. Math. Kyoto Univ, 4(1):1–75, 1964.

- Jaber et al. [2017] Eduardo Abi Jaber, Martin Larsson, and Sergio Pulido. Affine Volterra processes. arXiv:1708.08796, 2017.

- Jacod and Shiryaev [2013] Jean Jacod and Albert Shiryaev. Limit Theorems For Stochastic Processes. Springer, 2nd ed edition, 2013.

- Kallsen and Taqqu [1998] Jan Kallsen and Murad S. Taqqu. Option Pricing in ARCH-type Models. Mathematical Finance, 8(1):13–26, 1998.

- Kallsen and Vesenmayer [2009] Jan Kallsen and Bernhard Vesenmayer. COGARCH as a continuous-time limit of GARCH(1,1). Stochastic Processes and their Applications, 119(1):74–98, 2009.

- Klenke [2013] Achim Klenke. Probability Theory: A Comprehensive Course. Springer Science & Business Media, 2013.

- Klüppelberg et al. [2004] Claudia Klüppelberg, Alexander Lindner, and Ross A. Maller. A continuous-time GARCH process driven by a Lévy process stationarity and second-order behaviour. Journal of Applied Probability, 2004.

- Klüppelberg et al. [2006] Claudia Klüppelberg, Alexander Lindner, and Ross Maller. Continuous time volatility modelling: COGARCH versus Ornstein–Uhlenbeck models. In From Stochastic Calculus to Mathematical Finance, pages 393–419. Springer, 2006.

- Klüppelberg et al. [2010] Claudia Klüppelberg, Ross Maller, and Alexander Szimayer. The COGARCH: A review, with news on option pricing and statistical inference. 2010.

- Lindner and Maller [2005] Alexander Lindner and Ross Maller. Lévy integrals and the stationarity of generalised Ornstein–Uhlenbeck processes. Stochastic Processes and their Applications, 115(10):1701–1722, October 2005. 10.1016/j.spa.2005.05.004.

- Lindner [2009a] Alexander M. Lindner. Continuous time approximations to GARCH and stochastic volatility models. Handbook of Financial Time Series, pages 481–496, 2009a.

- Lindner [2009b] Alexander M. Lindner. Stationarity, mixing, distributional properties and moments of GARCH (p, q)–processes. In Handbook of Financial Time Series, pages 43–69. Springer, 2009b.

- Lorenz [2006] Robert Lorenz. Weak Approximation of Stochastic Delay Differential Equations with Bounded Memory by Discrete Time Series. Phd Thesis, 2006.

- Maller et al. [2008] Ross A. Maller, Gernot Müller, and Alex Szimayer. GARCH modelling in continuous time for irregularly spaced time series data. Bernoulli, 14(2):519–542, 2008.

- Marquardt [2006] Tina Marquardt. Fractional Lévy processes with an application to long memory moving average processes. Bernoulli, 12(6), 2006.

- Müller [2010] Gernot Müller. MCMC Estimation of the COGARCH(1,1) Model. Journal of Financial Econometrics, 8(4):481–510, October 2010. 10.1093/jjfinec/nbq029.

- Nelson [1990] Daniel B. Nelson. ARCH models as diffusion approximations. Journal of Econometrics, 45(1):7–38, 1990.

- Podolskij [2015] Mark Podolskij. Ambit fields survey and new challenges. In XI Symposium on Probability and Stochastic Processes. Springer, 2015.

- Protter [2004] Philip E. Protter. Stochastic Integration and Differential Equations. Number 21 in Applications of mathematics. Springer, Berlin ; New York, 2nd ed edition, 2004.

- Reiß et al. [2006] M. Reiß, M. Riedle, and O. van Gaans. Delay differential equations driven by Lévy processes: Stationarity and Feller properties. Stochastic Processes and their Applications, 116(10):1409–1432, 2006. 10.1016/j.spa.2006.03.002.

- Tran [2013] Cuong Viet Tran. Convergence of Time Series Processes to Continuous Time Limits. Phd Thesis, University of New South Wales, 2013.

- Wang [2002] Yazhen Wang. Asymptotic nonequivalence of GARCH models and diffusions. The Annals of Statistics, 30(3):754–783, June 2002. 10.1214/aos/1028674841.