∎

22email: libo.li@unsw.edu.au 33institutetext: Dai Taguchi 44institutetext: Graduate School of Engineering Science, Osaka University, 1-3, Machikaneyama-cho, Toyonaka, Osaka, Japan,

44email: dai.taguchi.dai@gmail.com

On a positivity preserving numerical scheme for jump-extended CIR process: the alpha-stable case.

Abstract

We propose a positivity preserving implicit Euler-Maruyama scheme for a jump-extended Cox-Ingersoll-Ross (CIR) process where the jumps are governed by a compensated spectrally positive -stable process for . Different to the existing positivity preserving numerical schemes for jump-extended CIR or CEV (Constant Elasticity Variance) process, the model considered here has infinite activity jumps. We calculate, in this specific model, the strong rate of convergence and give some numerical illustrations. Jump extended models of this type were initially studied in the context of branching processes and was recently introduced to the financial mathematics literature to model sovereign interest rates, power and energy markets.

2010 Mathematics Subject Classification:

60H35; 41A25; 60H10; 65C30

Keywords:

Implicit scheme

Euler-Maruyama scheme

alpha-CIR models

Lévy driven SDEs

Hölder continuous coefficients

Spectrally positive Lévy process

Introduction

In this article, we study the strong approximation of the alpha-CIR process. This class of models was first studied in the context of continuous state branching processes with interaction or/and immigration, see Li and Mytnik LiMy , Fu and Li FL and the references within, and was recently introduced by Jiao et al. JMS JMSS to the mathematical finance literature to model sovereign interest rates, power and energy markets. The alpha-CIR process is an extension of the classic diffusion Cox-Ingersoll-Ross process to include jumps which are governed by a compensated spectrally positive -stable Lévy process for . More specifically, given a positive initial point , the alpha-CIR process satisfies the following stochastic differential equation (SDE),

| (1) |

where , are non-negative and . The diffusion and the jump coefficient are given by and . The process is a Brownian motion and is a compensated spectrally positive -stable process, independent of , of the form

where is a compensated Poisson random measure with its Lévy measure denoted by . In other words, the process is a Lévy process with the characteristic triple , where . In general, under some monotonicity conditions on the jump coefficient, the above SDE will have a unique non-negative strong solution for any integrable compensated spectrally one-sided Lévy process , see FL LiMy . Here we mainly focus our attention on the -stable case. In the special case where , the solution to (1) is termed the stable-CIR, see Li and Ma LiMa .

The CIR and the CEV processes are theoretically non-negative and are widely used in the modelling of interest rates, default rates and volatility, e.g. Duffie et al. DFS DPS . Therefore, in practice, for consistency reasons the ability to simulate a positive sample path is very important. The study of positivity preserving strong approximation schemes for CIR/CEV type processes has received a great deal of attention in the literature. For the classic diffusion case we mention the works of Alfonsi Alf Alf2 , Berkaoui et al. BBD , Brigo and Alfonsi BA , Dereich et al. DNS , Neuenkirch and Szpruch NeSz and the references within. The jump-extended case (with and without delays) has recently received increasing attention, we refer to Yang and Wang YW , and the recent working papers of Fatemion Aghdas FHT and Stamatiou ST . To the best of our knowledge, for jump-extended CIR/CEV models, the existing results have all focused on the case of finite activity jumps (the jumps are governed by a Poisson process) and results on positivity preserving strong approximation schemes in the case of infinite activity jumps have yet to be obtained.

The common approach in devising a positivity preserving simulation scheme for jump-extended CIR or diffusion CIR models is to first transform the solution to remove the diffusion coefficient and then combine an existing positivity preserving scheme for the Itô diffusions, such as the backward Euler-Maruyama scheme, with the jumps of the Poisson process to create a jump-adapted scheme. The first order convergence rate obtained in for example YW is very attractive, however schemes of this type can suffer from high computational costs when the intensity rate is high.

Unfortunately, the existing techniques for Poisson jumps do note translate well into the case of infinite activity. This is because, in the infinite activity case, one can not simulate individually the small jumps and transform methods will usually lead to extra jump terms, which, due to presence of the small jumps are impossible to simulate. Depending on the application, one possible alternative is to consider weak approximation schemes by using a gaussian approximation of the small jumps as done in Asmussen and Rosinski AR or Kohatsu-Higa and Tankov KHT .

In the case of the alpha-CIR process, one is able to obtain some results in this direction. We propose an implicit approximation scheme in (4), which extends the scheme proposed in Alfonsi Alf and Brigo and Alfonsi BA for the classic diffusion CIR process. This method depends strongly on the fact that the diffusion coefficient is a square root, which allows one to device a positivity preserving implicit scheme by solving a quadratic equation.

Although the derivation of the current scheme follows closely the idea presented in Alf BA , the inclusion of an infinite activity jump process makes the scheme behave very differently to the classic implicit scheme for the diffusion CIR model, and the proof of convergence is technically more difficult.

In the diffusion case, the discriminate of the previously mentioned quadratic equation is non-negative if the condition is satisfied. In the proposed scheme, the support of the discriminate is bounded below only in the case where has finite activity jumps (Type A) or is of finite variation and has infinite activity jumps (Type B). In the case where is of infinite variation (Type C) and therefore has infinite activity jumps, there is no hope of finding a set of conditions on the parameters , and the grid size such that the discriminate is non-negative. This issue is resolved by taking the absolute value of the constant term in the quadratic equation, which ensures the non-negativity of the discriminate and thus the existence of an unique positive root (Descartes' Sign Rule).

We point out that in the diffusion case, by using more advanced techniques, c.f. Hefter and Herzwurm HH , it is possible to relax the condition . However, it is not clear if these techniques can be translated to the jump-extended setting. Here the condition is essential in controlling the probability that the discriminate is negative in Lemma 2.1. The case is not studied in this work, this is because for the alpha-CIR can be reduced to the diffusion CIR (see Jiao et al. JMS ) and one can refer to previously mentioned works on the diffusion case.

Unfortunately, depending on the integrability of , in order to obtain strong convergence of the proposed scheme, our methodology requires one to first modify the jump coefficient and the rate of convergence is obtained in two steps. That is we first truncate and consider the bounded jump coefficient given by , for some arbitrarily large constant , and then compute the strong rate of convergence in Theorem 2.7 for the approximation scheme of the truncated alpha-CIR process , i.e. the solution to (1) with jump coefficient . Then we compute in Theorem 2.8 the strong rate of convergence of the truncated alpha-CIR process towards the alpha-CIR process as . Finally, by carefully selecting as a function of the grid size, we obtain for the overall rate of convergence in Corollary 2.9.

To this end, it is worth pointing out that the jump coefficient is truncated for purely technical reasons. In fact, to the best of our knowledge, there are no results on Euler-Maruyama schemes for (symmetric) -stable processes with unbounded jump coefficient, e.g. Hashimoto Ha and Hashimoto and Tsuchiya HaTsu . On the other hand, we note that truncation of the jump coefficient is not needed in the case where is square integrable. For example, when is compensated Poisson process or a compensated spectrally positive tempered -stable process for .

Finally, we mentioned that the current problem can potentially be treated using the symmetrized Euler-Maruyame scheme studied Diop DA , Berkaoui et al. BBD and Bossy and Diop BD . However, local time techniques used in BBD BD DA do not translate well to our setting. This is due to the lack of a suitable version of the Itô-Tanaka formula for -stable process or in general, Lévy processes of infinite variation.

Notations and Assumptions

We work on a usual filtered probability space with a filtration , and we assume that all the processes considered are adapted to this filtration. For any , the integral with upper limit and lower limit is understood as a integral over the interval . Given the terminal time , we consider an equally spaced grid and set for . In addition, for , we require the condition that where . Given a process , the negative part of is denoted by and for , we set . The Lévy measure of will be denoted by and the drift of is denoted by . For general results on Lévy processes we refer to Sato SK and Applebaum AD . In estimation, we often use , , , or to denote constants, which may change from line to line. Subscripts will be used to indicate dependence of the constant on other parameters.

1 An implicit scheme for the truncated alpha-CIR process

Given a positive initial point , we let , for some arbitrarily large constant , we consider the solution to the stochastic differential equation

| (2) |

where , are non-negative parameters with , , . The process is a Brownian motion and is a compensated spectrally positive -stable Lévy process with Lévy measure , independent of . In order to derive a positivity preserving scheme for the truncated process , we take our inspiration from Alfonsi Alf or more generally Milstein et al. MRT by considering the implicit scheme, , for

| (3) |

where the extra term stems from the quadratic variation of and .

Remark 1.

In equation (3), the discretisation scheme is made implicit in the drift and the diffusion coefficient, but not in the jump coefficient . It is important that the scheme is not implicit in the jump coefficient. Otherwise there will be another extra adjustment term stemming from the quadratic variation of and , which can not be simulated unless the time and size of each individual jump can be simulated.

For every , by setting in (3), one can obtain the following quadratic equation in ,

which has a unique non-negative solution if the discriminate is non-negative, or under a slightly strong condition, the process

is non-negative. However the above can be negative as the drift of is negative.

In the case where is a compensated spectrally positive -stable process, or in general a Lévy process of infinite variation (Lévy process of Type C), the support of the process is not bounded below (see Theorem 24.10 (iii) in Sato SK ). Therefore it is not possible to select parameters so that the discriminate is non-negative. To overcome this, we take the absolute value and consider the following scheme, and for each ,

| (4) | ||||

The goal in the rest of this article is to derive the strong rate of convergence under the assumption that and . We must point out that can be replaced by any compensated spectrally positive integrable Lévy process and one can show that the scheme converges given good estimates on and .

Remark 2.

The difficulty of the current work lies in that a compensated spectrally positive -stable process is a Lévy process of infinite variation (Type C). In the case where has finite activity (Type A) or has infinite activity and is of finite variation (Type B), (see Definition 11.9 in SK ), it is possible to find a set of conditions on the parameters to ensure that the process is non-negative. To see this, suppose that the support of the Lévy measure contains , (see page 148 of SK for the definition and properties of the support of a measure). From Theorem 24.10 (iii) in Sato SK , we know that the support of is almost surely contained in , where the drift is given by . Therefore, we obtain

By considering the convex function over the domain and applying Jensen's inequality, we see that for all in the interval . Since lies in this interval, this inequality holds for . Applying this inequality to the above expression gives,

which is positive if and are both positive. Hence, we arrive at a set of sufficient conditions on the parameters, given by

| (5) |

If is equal to zero, then the second condition becomes , which is the same as the conditions imposed on the diffusion CIR process to be strictly positive.

Therefore it is worth mentioning that if is the compensated Poisson process, then one does not need to truncate the jump coefficient or modify the discriminate once the condition given in (5) is satisfied.

2 Strong convergence

To show that the proposed scheme converges, we expand the implicit scheme given in (4) around the Euler-Maruyama scheme and then apply the Yamada-Watanabe approximation technique. More explicitly, by expanding the quadratic in (4), using the identity and adding/subtracting the appropriate terms we obtain

| (6) |

where and (change in the remainder process) is given by

| (7) | ||||

The term is given by

and the fact that is a martingale increment in the filtration can be quick checked as

which is equal to zero. Hence we can conclude that .

The next step is to compute the semimartingale decomposition of . The second term on the right hand side of (7) is given by

and for the last term of (7), we can write . Finally, by collecting terms appropriately, we can express where

The terms in are martingale differences and is a predictable process.

Finally, the discrete time scheme (6) can be then extended to continuous time by setting where

The extension of the martingale part of the remainder process to continuous time is done by setting for .

2.1 Auxiliary estimates

In this subsection, we present some auxiliary estimates which are needed to prove the strong convergence of the proposed scheme.

Lemma 2.1.

For and

where is some positive constant depending on , , and .

Proof.

See subsection 4.3 of the Appendix. ∎

Lemma 2.2.

For , we have .

Proof.

Taking the expectation of the scheme given in (6) to obtain, for some ,

To continue the calculation, by using the fact that is positive, we obtain

By taking the expectation above, applying Hölder's inequality with where , , we obtain

where in the second inequality, we have used the fact that is independent from and Jensen's inequality (as ). In the last inequality, we have used the fact that . Therefore by using the Lemma 2.1,

for some . From the above we recover the recursive equation

for some . This gives . ∎

Lemma 2.3.

For all , there exists positive constants and such that

and .

Proof.

Lemma 2.4.

For , we have

Proof.

To estimate , we proceed by setting and we note that it can be estimated by

The right hand side of the above inequality can be estimated using the fact that , and are independent and . Therefore, by Lemma 2.2 and Lemma 2.3, the expectation of the right hand side above is bounded by an integrable random variable multiplied by . ∎

Lemma 2.5.

The remainder process satisfies or more specifically, the process and satisfies

where is some constant depending on .

Proof.

Using Lemma 2.1, that is is exponentially small with respect to the discretisation grid, we obtain

Recall that the martingale differences can be expressed as

where we set

In order to estimate , we note that for

By taking the absolute value, applying the Cauchy-Schwarz inequality, Jensen's inequality and the -isometry to the martingale increment , we obtain

where follows from Lemma 2.1 and Lemma 2.3. On the other hand, from Lemma 2.4

and the result follows by taking the square root. ∎

Lemma 2.6.

Let be the scheme defined in (4) then

2.2 Strong rate of convergence for the truncated alpha-CIR

We present in the following the strong rate of convergence of the positivity preserving approximation scheme to the truncated alpha-CIR process as . The proof relies on a careful application of the Yamada-Watanabe approximation technique. For readers who are unfamiliar with the approximation technique, we included some useful results in section 4.2 of the appendix.

Before proceeding, we point out that the Yamada-Watanabe approximation technique can not be applied directly to as done in Alfonsi Alf . This is due to the presence of the remainder process . The differences/difficulties that we faced here are the following, (i) the martingale representation property do not hold and one can not hope to obtain estimates from an direct application of the Itô formula for Lévy processes, see for example Applebaum AD , as the explicit form of the martingale is not known. (ii) Even in the case where can be computed or is square integrable and therefore martingale representation property holds, the monotone increasing condition on the jump coefficients (which is crucial in the proof of strong uniqueness in LiMy and FL ) may not be satisfied. To overcome the above mentioned issues, we notice that the strong error can be decomposed into . The estimate of the process is readily available in Lemma 2.5, and we need only to apply the Yamada-Watanabe approximation technique to the process .

Theorem 2.7.

Let , then the strong rate of convergence is given by

Let , then the strong rate of convergence is given by

Proof.

Let and . We define and denote the jumps of by . By applying Itô's formula to the Yamada-Watanabe function , see equation (16), we obtain

where we have set

The local martingale term will disappear after applying the standard localization argument and taking the expectation. In the following, we suppose that all integrals are appropriately stopped, and to simplify notation, we do not explicitly write the localizing sequence of stopping times and will focus on obtaining upper estimates of , and which are independent of the localizing sequence.

To estimate , we write it into two terms where

We observe that if then . Therefore we can apply Lemma 4.2 with and , since is non-decreasing. We obtain for any ,

| (8) |

where in the second last inequality, we used the fact that is -Hölder continuous.

By applying (4.3) in Lemma 4.3, with and , and the fact that is bounded, can be bounded as follows

| (9) | |||

By writing , from Lemma 2.5 and Lemma 2.6

| (10) |

Therefore, by taking the expectation of the both hand sides of inequality (9), we obtain for some ,

| (11) |

To estimate the term , we again apply Lemma 2.6 to obtain

To estimate the term , we write

which by Lemma 2.6 or (10) shows that

Putting this together, we obtain

Recall that and we choose and . Then by Gronwall's inequality we conclude that

In the case , we choose and we have

Then by using Gronwall's inequality, the fact that and choosing where , we obtain

It is clear that the upper bound is independent of the localizing sequence of stopping times, the final result then holds by Fatou's Lemma. ∎

Remark 4.

The condition that the jump coefficient is bounded is only used in the estimation of in equation (11). The boundedness condition is used to make up for the lack of knowledge on the integrability of for . We claim that if one can show for , that for then the strong rate of convergence can be obtained for certain range of values of without first having to truncate the jump coefficient. However, it appears that uniform bound on the -th moment of the approximation process is difficult to obtain, however for the theoretical process and , one can show that for all we have and . This result is given in Lemma 4.1 and is needed in the next subsection to study the convergence of the truncated alpha-CIR towards the alpha-CIR process as .

2.3 Convergence of the truncated alpha-CIR to the alpha-CIR

Theorem 2.8.

Assume that , and then there exists such that for any ,

Assume that , and then for any , there exists such that for any ,

where converges to infinity as .

Proof.

Let and . We define and denote the jumps of by . By a similar arguments of the proof of Theorem 2.7, we obtain

where we have set

By applying (4.3) in Lemma 4.3, with and , can be bounded as follows

The assumption implies for any we have . From Lemma 4.1, and has -th moment, thus we have

for some which explodes as (see (14) in Lemma 4.1). Therefore, is bounded by

| (13) |

To estimate and , we write

Putting this together, we obtain

By choosing and , and using Gronwall's inequality,

Similarly, for , , we choose , where ,

where again the constant explodes as . It is clear that the upper bound is independent of the localizing sequence of stopping times, the final result then holds by Fatou's Lemma. ∎

Corollary 2.9.

Assume that , and . We let , then there exists such that

Assume that , and then for any , then there exists such that

where and , and the constant convergences to infinity as .

Remark 5.

It is slightly unpleasant to have restriction on the parameter and, in the case where , to present convergence rates which depend on the parameter . However we want to point out that these are again technical issues. The restriction on and the dependence of are due to estimate (13), where one is forced to use moment estimates in Lemma 4.1 as one has little information on the distribution of or .

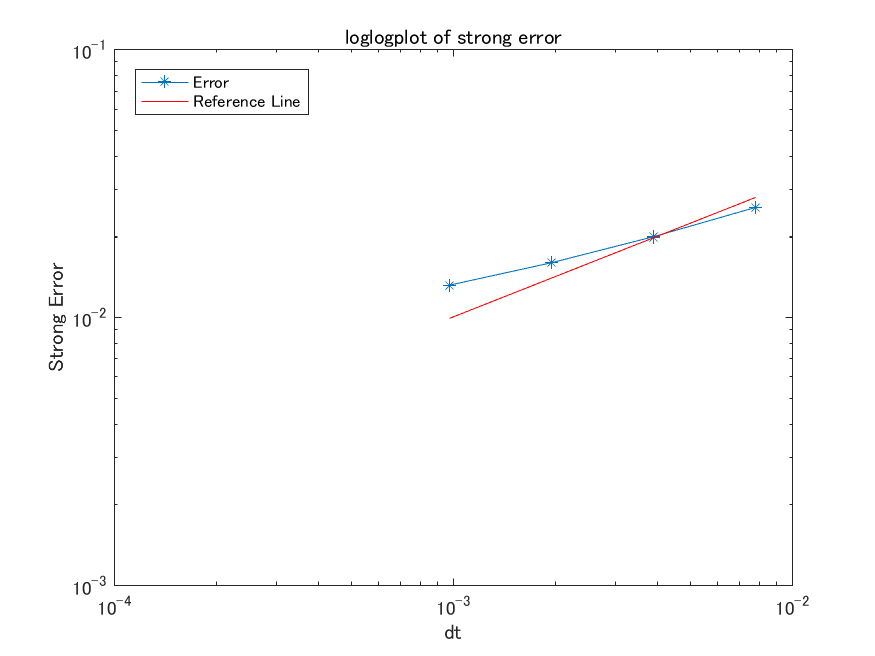

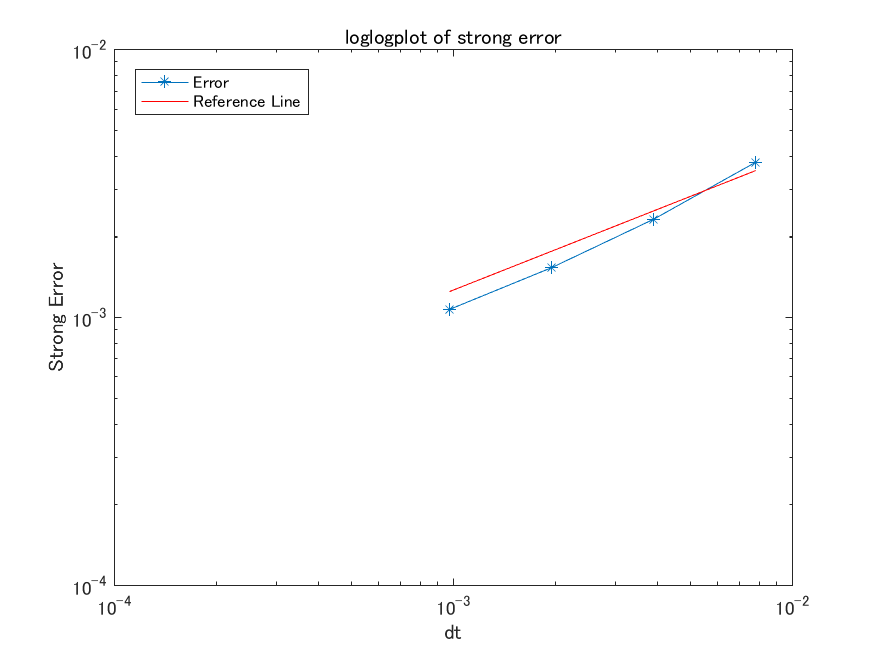

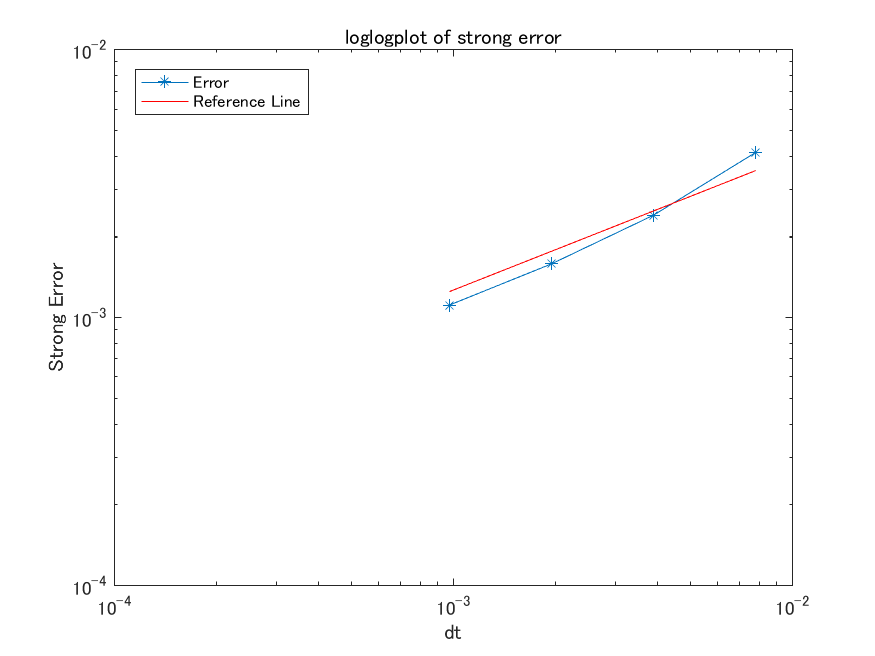

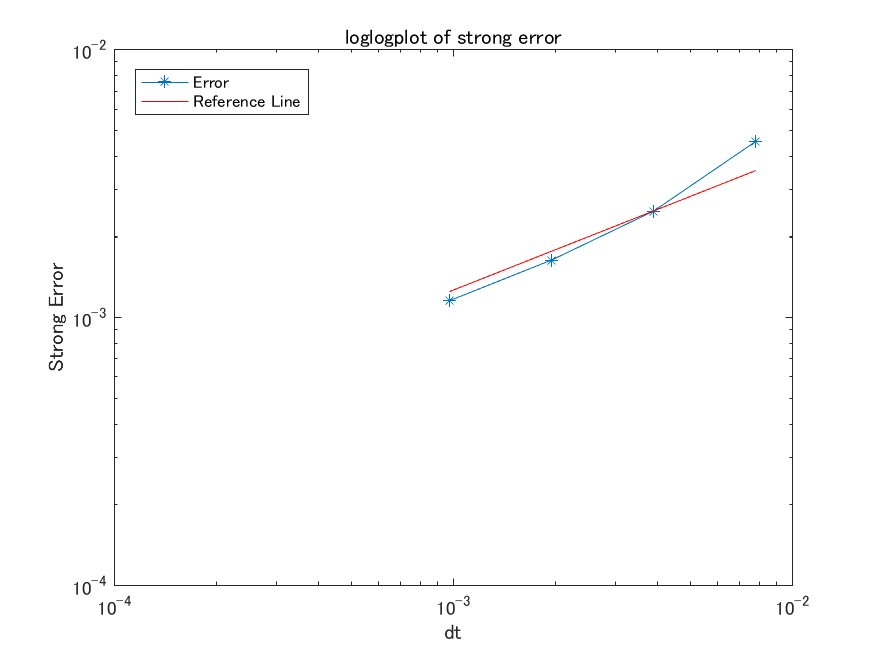

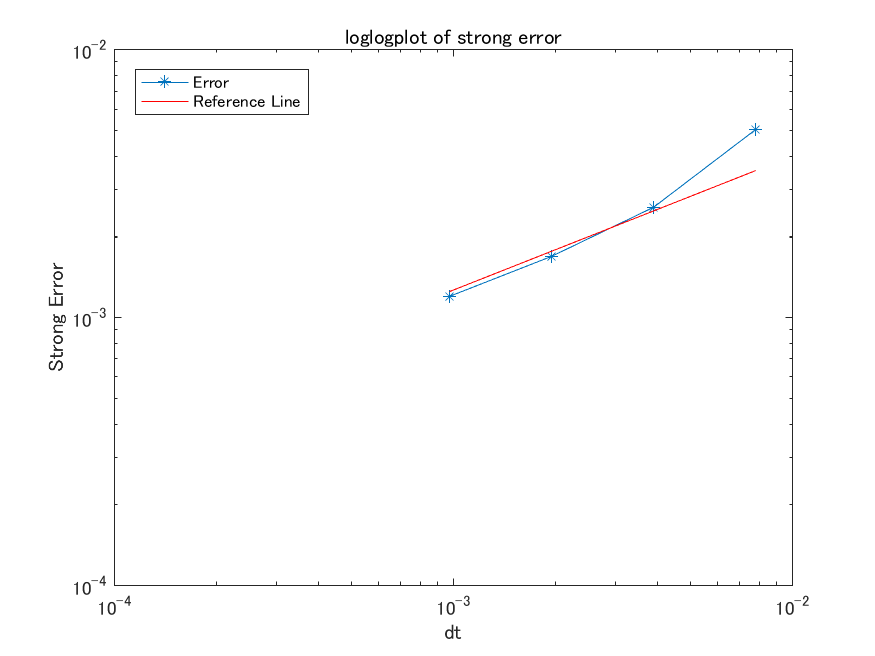

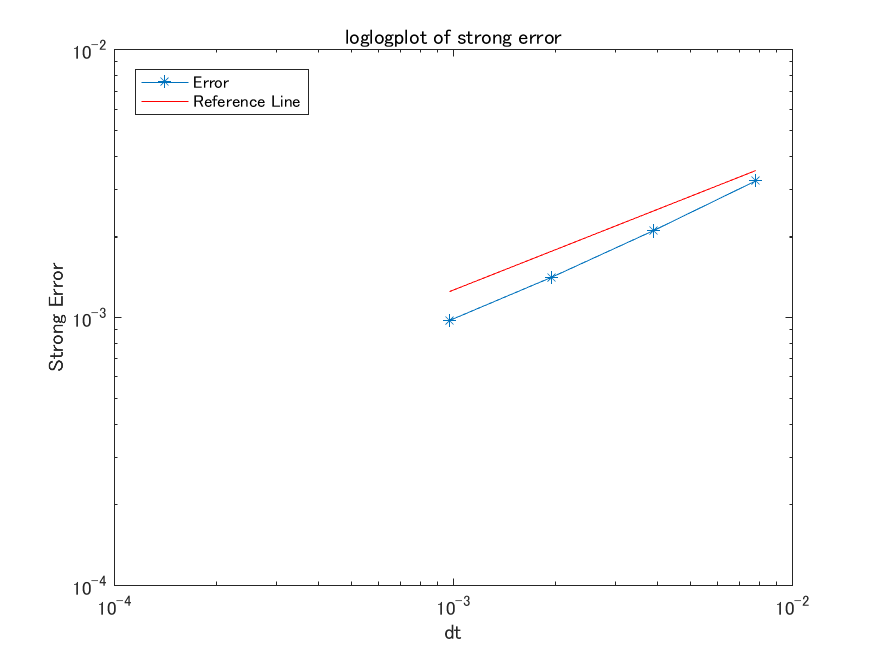

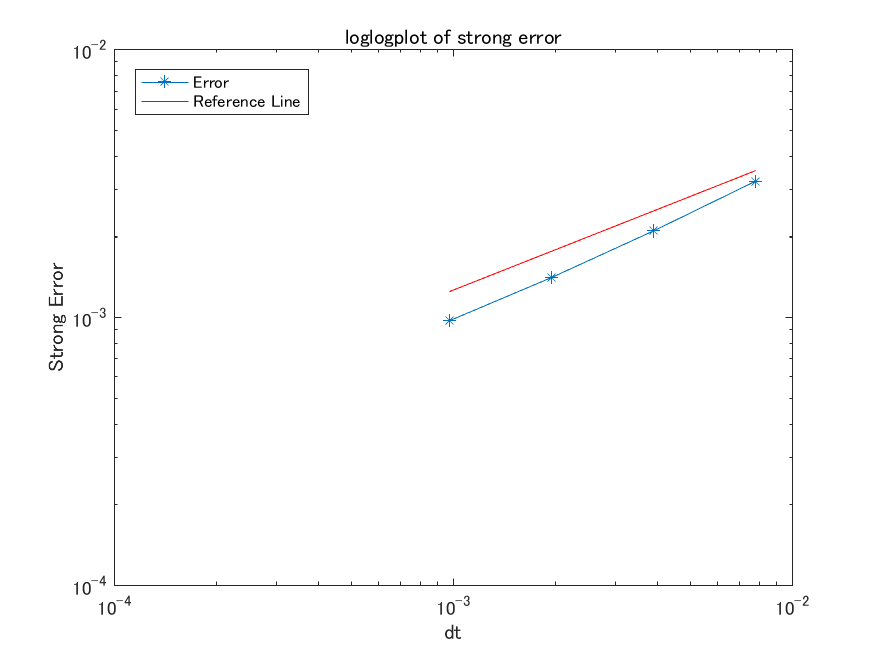

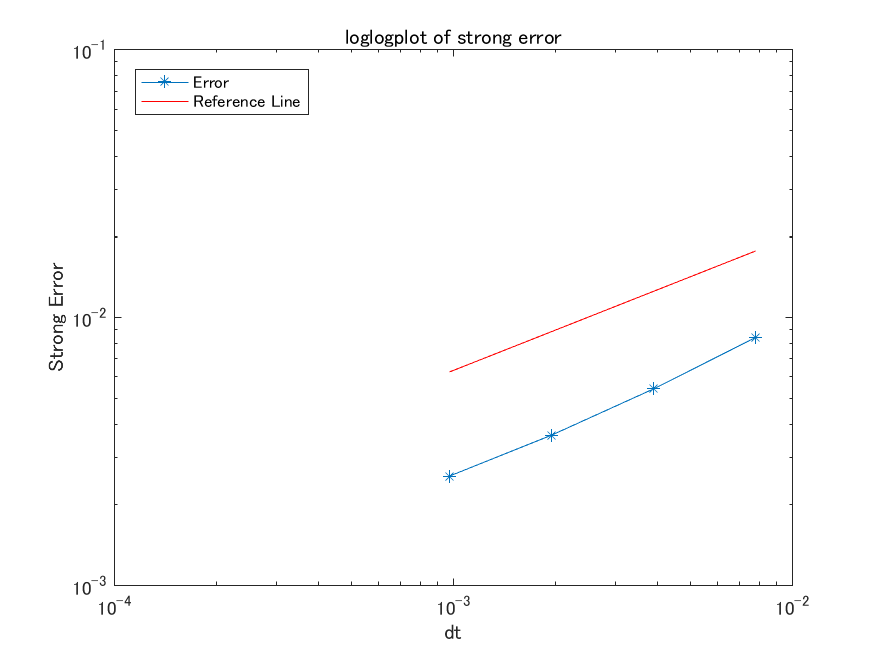

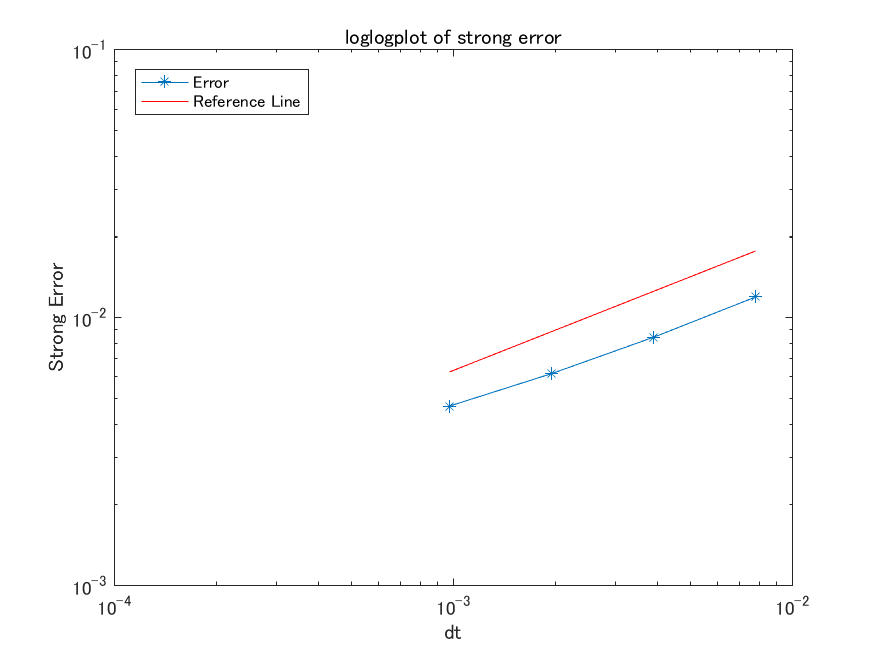

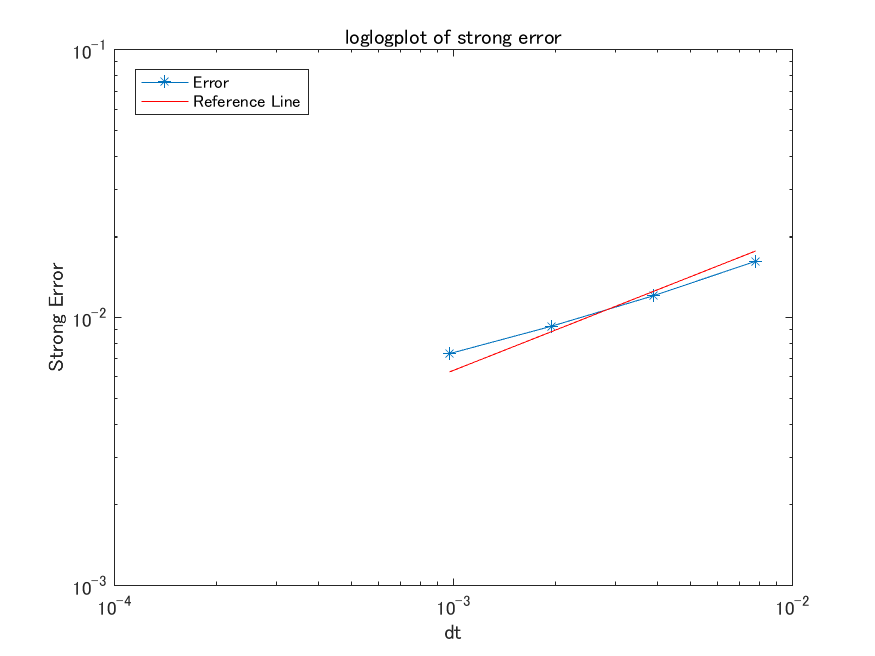

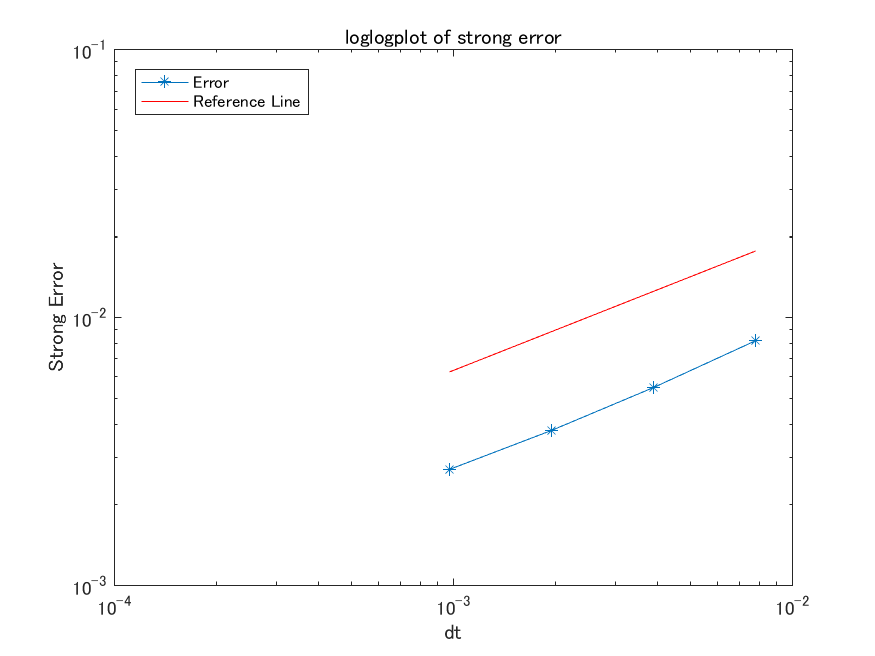

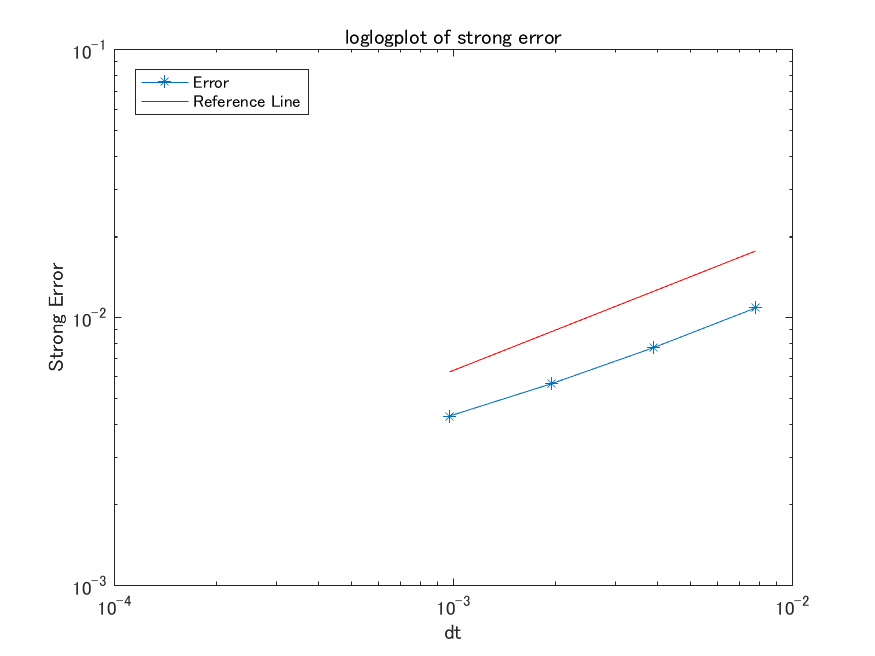

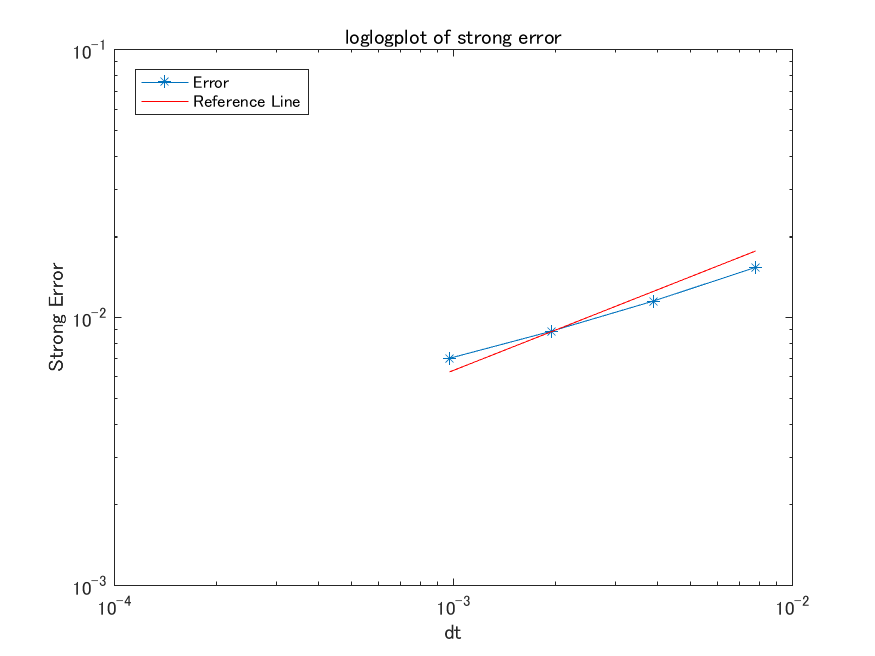

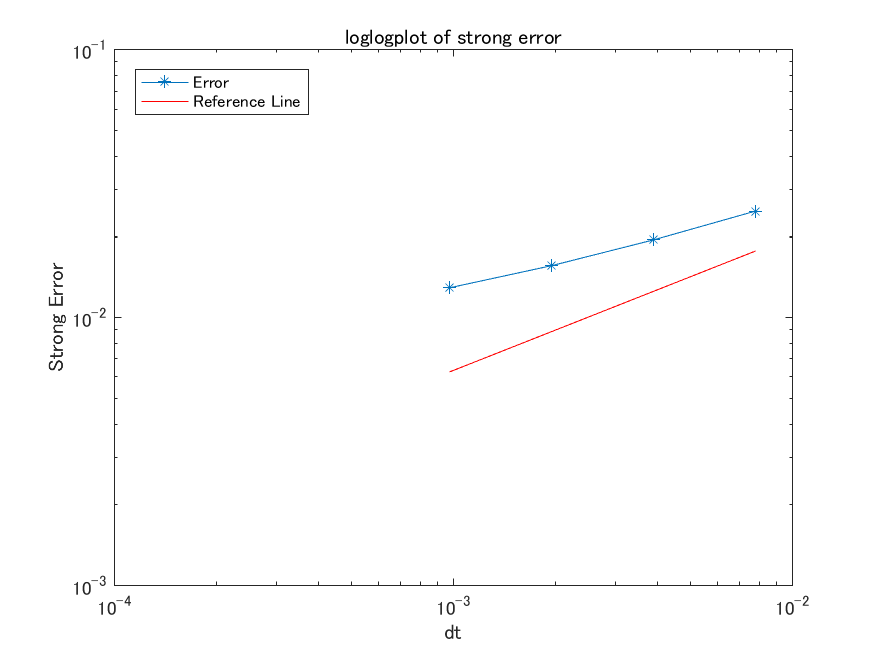

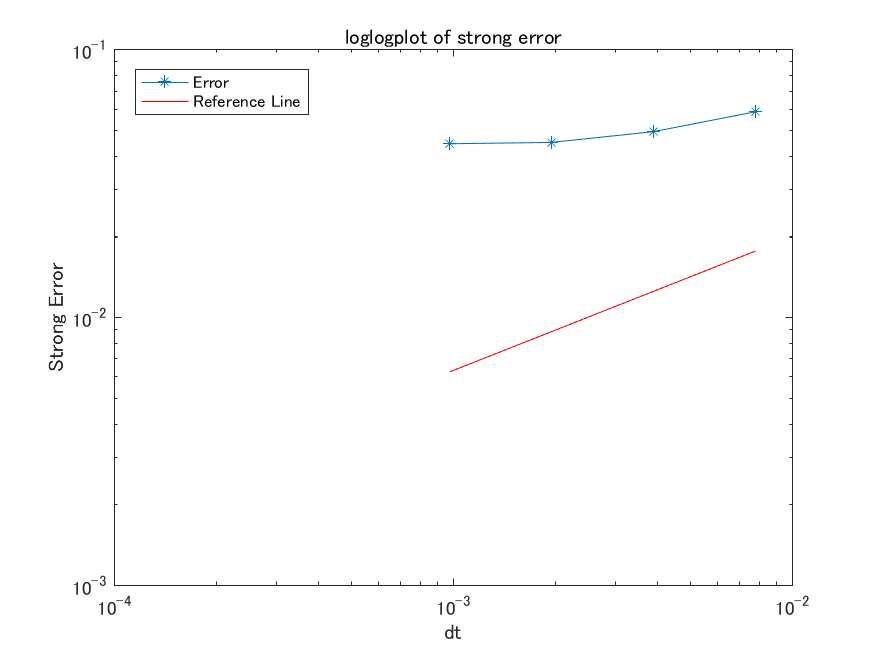

3 Numerical experiments

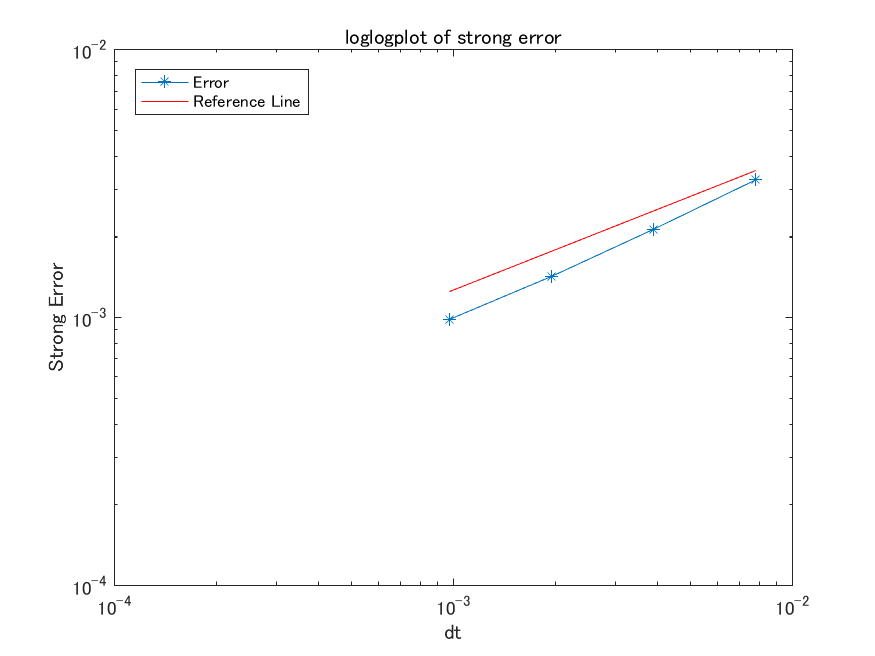

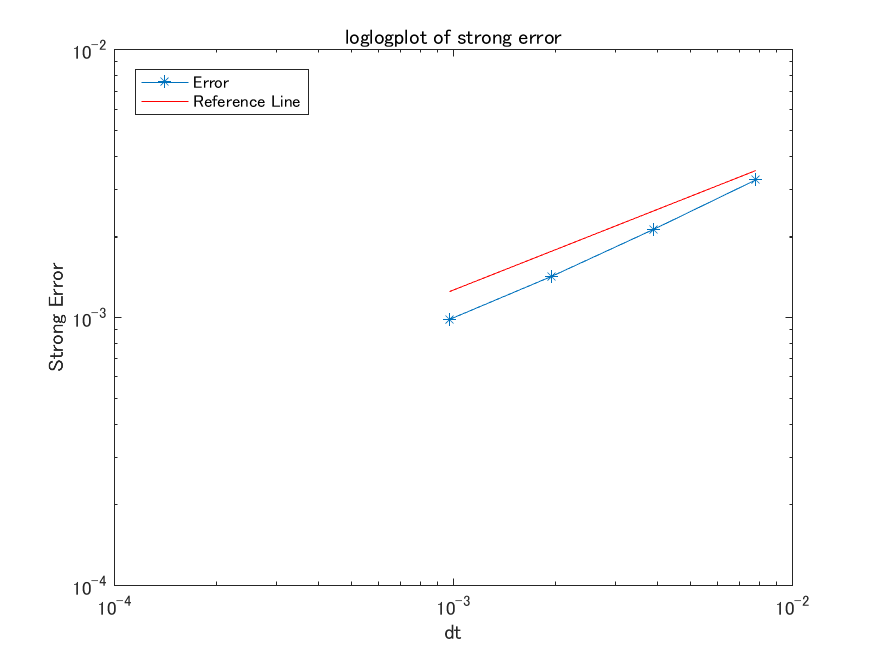

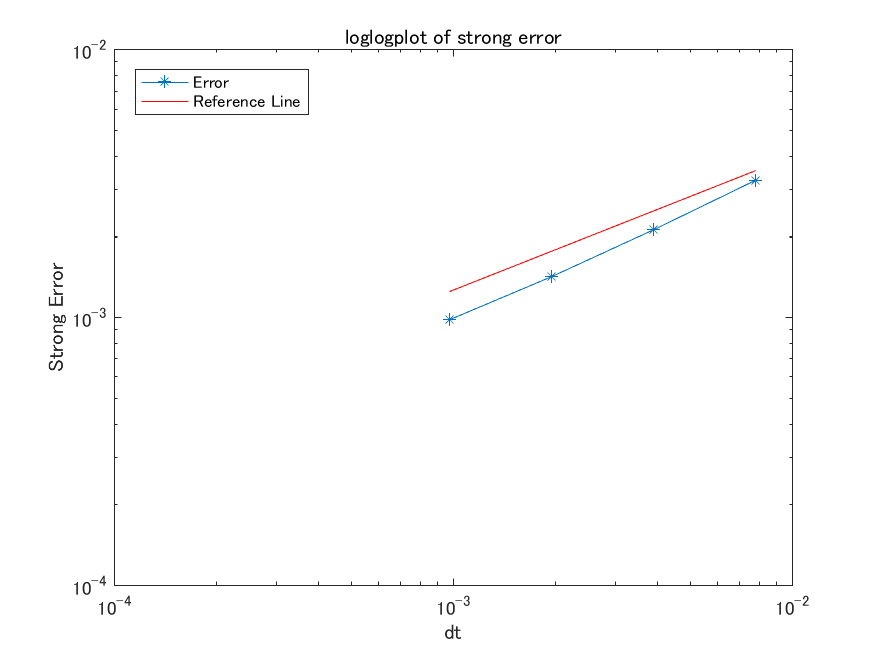

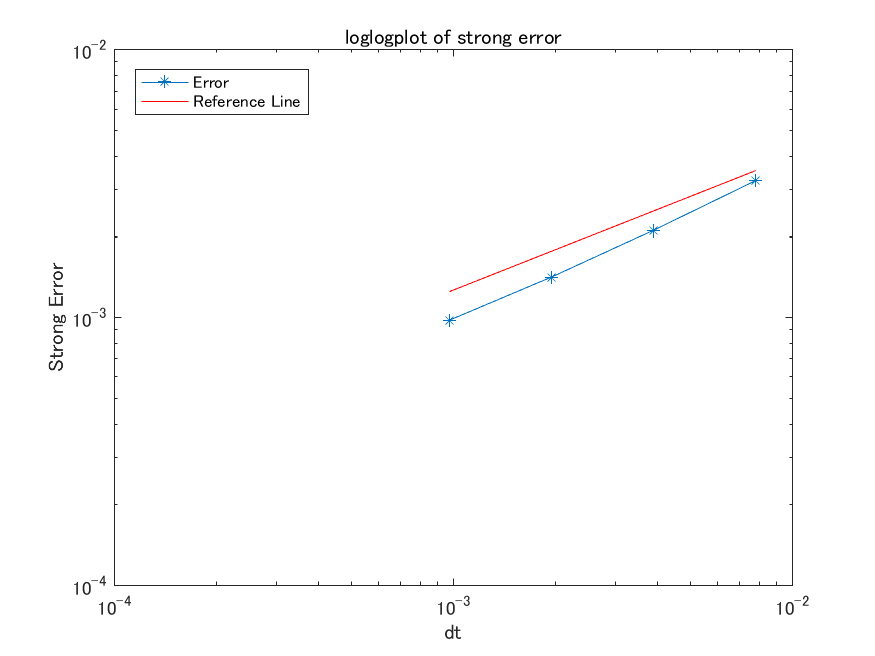

Numerical experiments were performed to study the strong rate of convergence of the implicit approximation scheme give in (4). Note that here we ignored the truncation constant , since one is bounded, by design, by the largest number possible on a given computer architecture. In the following, the terminal time is and to illustrate the rate of convergence we compute

using . The implicit scheme is simulated using , for . The log-log plots of the error against grid size are given for some parameter values.

|

We observe in the above that the rate of convergence appears lower for larger values of . This observation is intuitive, since the rate of convergence for the diffusion CIR, i.e. , , is of order , and on the other hand, Theorem 2.7 tells us that in the jump case, i.e. , , the rate of convergence decreases as . Therefore, when combined, the worst rate should prevail. Unfortunately, due to the limitation in techniques, we are unable to identify this theoretically when and , and this will be the focus of future works. For experimental purposes, in the following pages, we present some graphs on the strong rate of convergence for different parameter regimes.

Conclusion

In this work, we devised a positivity preserving numerical scheme for the alpha-CIR process. We show that the scheme convergences and numerical experiments indicated that the strong rate is likely to be of order when is small and decreases as .

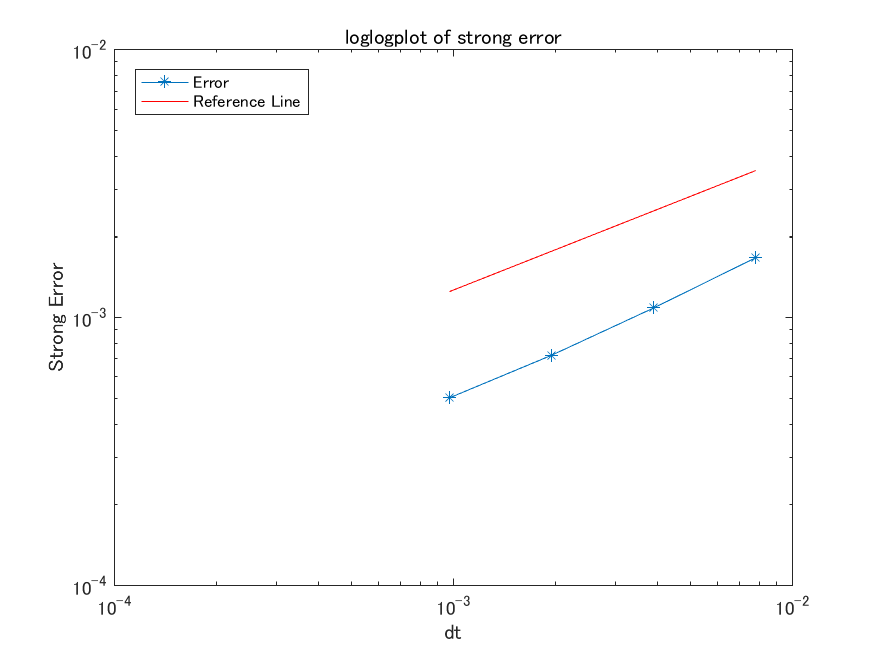

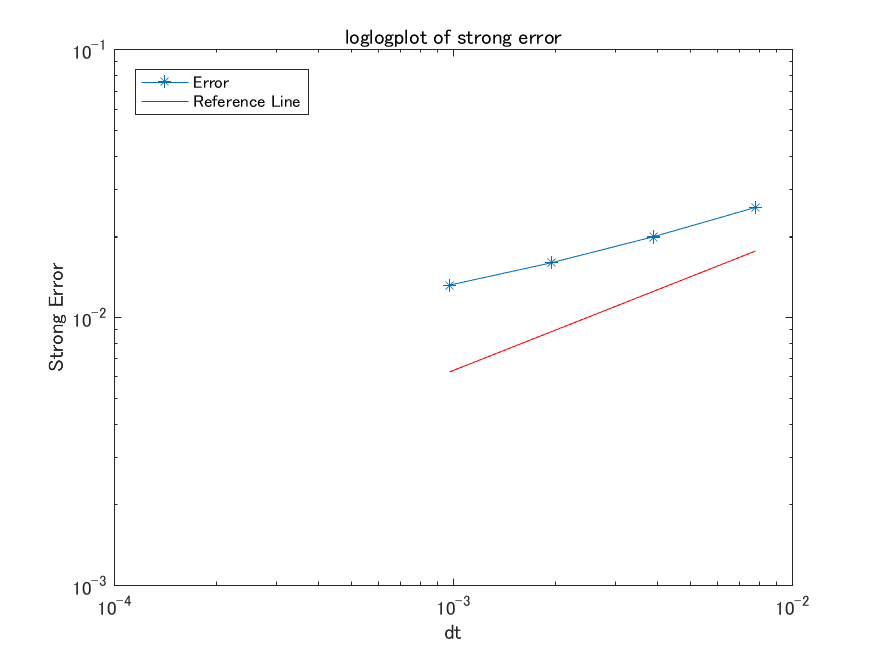

Numerical experiments - Graphs on the rate of convergence

The effect of increasing

|

|

|

|

|

|

Remark 3.1.

In the above, we investigate the effect of increases in . We observe that a increase in increases the magnitude of the log-error. The numerical experiments suggests that the strong rate is when and are relatively small.

The effect of increasing when is small

|

|

|

|

|

|

Remark 3.2.

In the above graphs, we investigate the effect of increases in in the case where is small. We observe that when is small then the increase in (when is relative small) have little effect to no effect on the rate of convergence or the magnitude of the log-error.

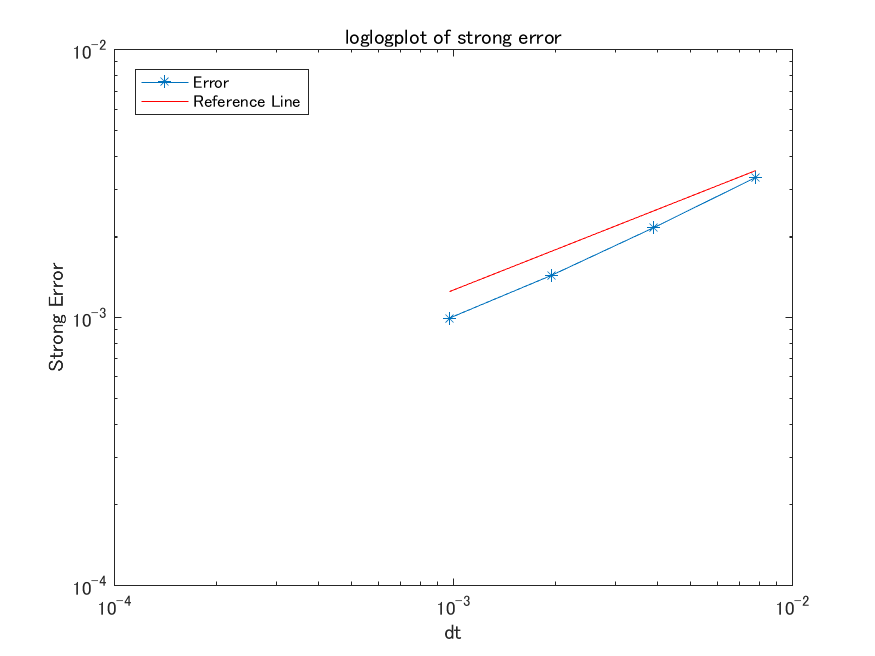

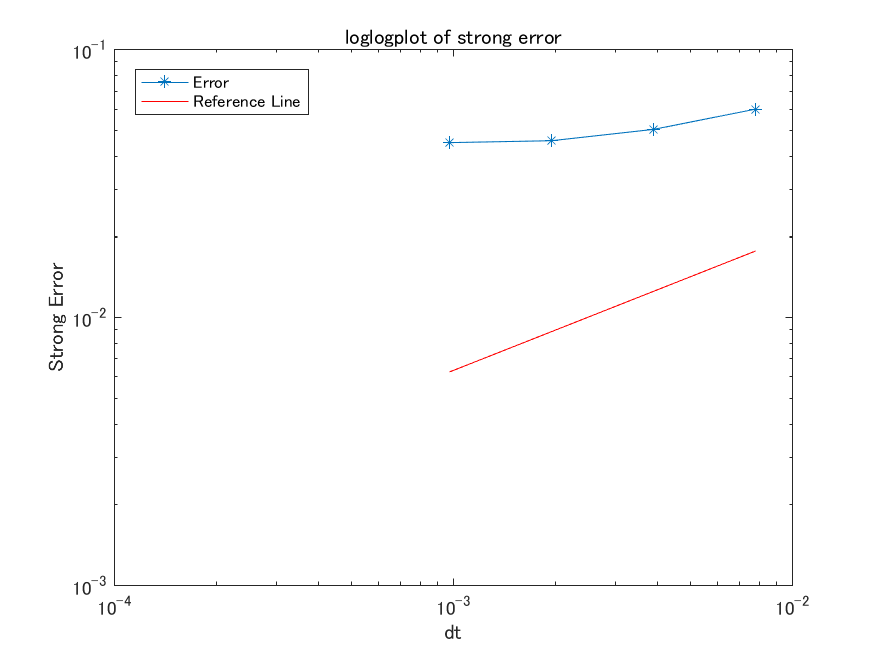

The effect of increasing when and are large and are of the same magnitude

|

|

|

|

|

|

Remark 3.3.

In the above graphs, we investigate the effect of increases in when and are of the same magnitude and are relatively large. We observe when is close to two the rate of convergence decreases and the magnitude of the log-error also increases (note that the range of the -axis is from to ).

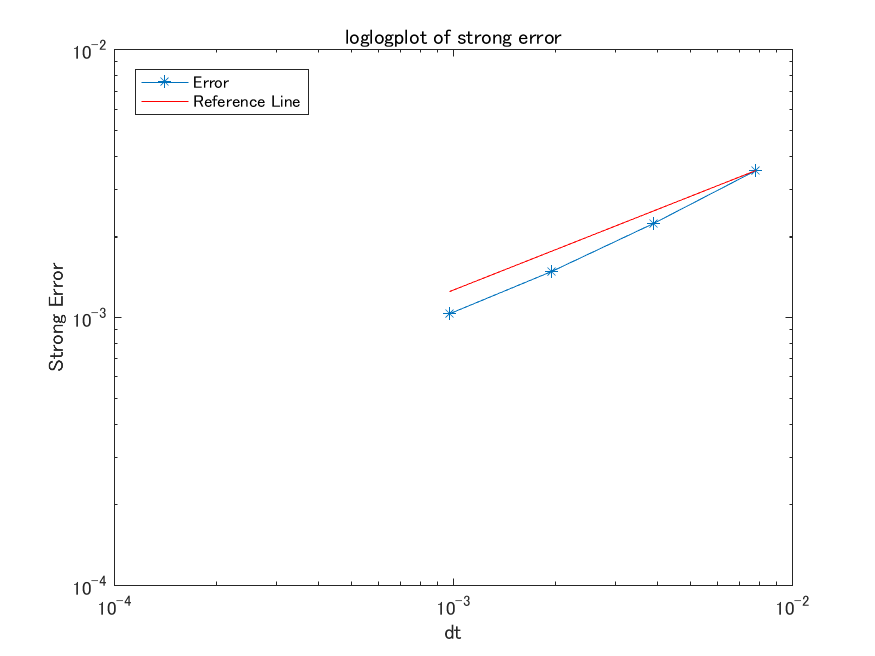

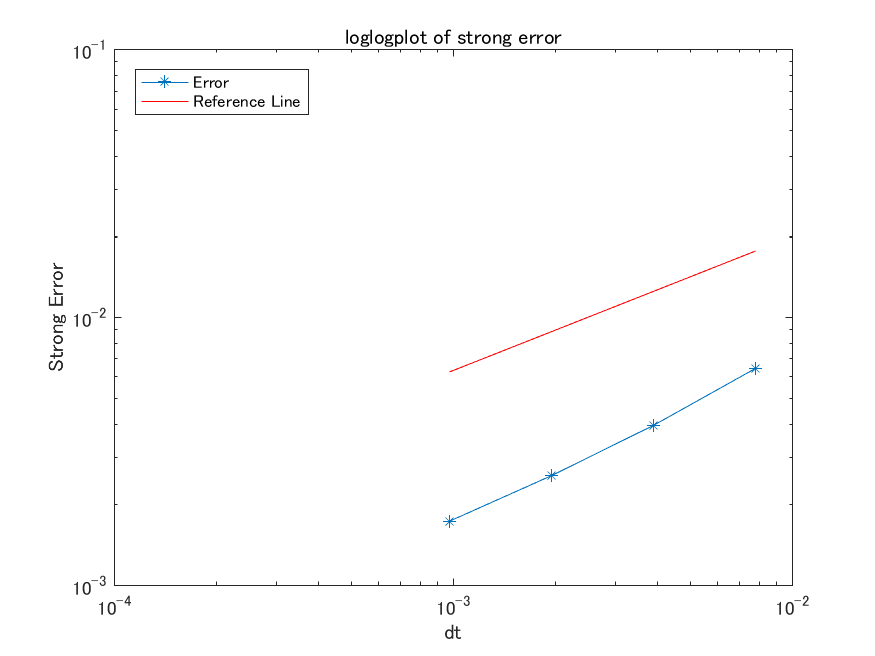

The effect of increasing when is large and

|

|

|

|

|

|

Remark 3.4.

In the above graphs, we investigate the effect of increases in when and is relatively large. The numerical results here are similar to those presented in Figure 4 where we observe that increases in reduces the rate of convergence and the magnitude of the log-error also increases (note that the range of the -axis is from to ). This is consistent with Theorem 2.7, where in the case , the strong rate of convergence decreases as .

4 Appendix

4.1 Moment estimate of

In this subsection, we show that for the solution of (2) has -th moment for .

Lemma 4.1.

For , the -th moment of is finite or more explicitly, there exists a constant such that

| (14) |

Proof.

In the following, let be a localizing sequence of stopping times so that when stopped at , all local martingales are martingales. By apply the Itô formula to , we obtain

| (15) |

where we have set

The martingale term can be removed after taking the expectation. Next we consider . For , by the second order Taylor's expansion for the map , we have

For , by the first order Taylor's expansion for the map and the Hölder continuity of the map , we have

Hence, the expectation of is bounded by

Since , then and there exists a constant such that . Then by taking expectation on (15), and using the fact that , we see that there exists such that

By Gronwall's inequality, we obtain

Finally, we conclude by using Fatou's lemma. ∎

4.2 Yamada-Watanabe Approximation Technique

We introduce below the Yamada and Watanabe approximation technique. For each and , we select a continuous function with support of belongs to and is such that

We define a function by setting

| (16) |

It is straight forward to verify that has the following useful properties:

Lemma 4.2 (Lemma 1.3 in LT ).

Suppose that the Lévy measure satisfies . Let and . Then for any , with and , it holds that

Lemma 4.3 (Lemma 1.4 in LT ).

Suppose that the Lévy measure satisfies . Let and . Then for any , and , it holds that

| (17) |

In particular, if , then

| (18) | ||||

4.3 Estimates of the probability that is negative

In the case where is an -stable compensated Lévy process with , where for , the moment generating function is given by

see Jiao et al. JMS . The support of is not bounded below and it is not possible to find conditions on the parameters which guarantee that the process is non-negative.

Proof of Lemma 2.1.

One can estimate the conditional probability using the conditional Laplace transform, and for any ,

By setting as the solution to

we eliminate from the above expression, giving the upper bound

∎

Acknowledgement: The authors wish to thank the anonymous referees for their careful readings and valuable advices on the writing of this article. The first author also wishes to thank Allan Loi for interesting discussions. The second author was supported by JSPS KAKENHI Grant Number 17H066833.

References

- (1) Asmussen, S. and Rosinski, J.: Approximations of small jumps of Levy processes with a view towards simulation, J. Appl. Probab 38 (2), 482–493 (2001).

- (2) Applebaum, D.: Lévy Process and Stochastic Calculus, second edition, Cambridge University Press, (2009).

- (3) Alfonsi, A.: On the discretization schemes for the CIR (and Bessel squared) processes, Monte Carlo Methods Appl. 11 (4), 355–384 (2005).

- (4) Alfonsi, A.: Strong order one convergence of a drift implicit Euler scheme: Application to the CIR process, Statist. Probab. Lett. 83 (2), 602–607 (2013).

- (5) Berkaoui, A., Bossy, M and Diop, A.: Euler scheme for SDEs with Non-Lipschitz Diffusion coefficient: Strong Convergence, ESAIM Probab. Stat. 12, 1–11 (2008).

- (6) Bossy, M and Diop, A.: An efficient discretisation scheme for one dimensional SDEs with a diffusion coefficient function of the form , . Doctoral dissertation, INRIA (2007).

- (7) Brigo, D. and Alfonsi, A.: Credit default swap calibration and derivatives pricing with the SSRD stochastic intensity model, Finance Stoch. 9 (1), 29–42 (2005).

- (8) Dereich. S, Neuenkirch, A and Szpruch, L.: An Euler-type method for the strong approximation of the Cox-Ingersoll-Ross process, Proc. R. Soc. A. The Royal Society, 468 (2140), 1105–1115 (2011).

- (9) Diop, A.: Sur la discrétisation et le comportement à petit bruit d'EDS multidimensionnelles dont les coeffcients sont à dérivées singuliéres, PhD Thesis, INRIA (2003).

- (10) Duffie, D., Filipović, D. and Schachermayer, W.: Affine processes and applications in finance, Ann. Appl. Probab. 13 (3), 984–1053 (2003).

- (11) Duffie, D., Pan, J., Singleton, K.: Transform analysis and asset pricing for affine jump-diffusions, Econometrica 68 (6), 1343–1376 (2000).

- (12) Fatemion Aghdas, A. S., Hossein, S. M. and Tahmasebi, T.: Convergence and non-negativity preserving of the solution of balanced method for the delay CIR model with jump, arXiv:1712.03206, Working paper 2017.

- (13) Fu, Z. and Li, Z.: Stochastic equations of non-negative processes with jumps, Stoch. Process. Appl. 120 (3), 306–330 (2010).

- (14) Hashimoto, H.: Approximation and Stability of Solutions of SDEs Driven by a Symmetric -Stable Process with Non-Lipschitz Coefficients. In: Donati-Martin C., Lejay A., Rouault A. (eds) Séminaire de probabilités XLV. Lecture Notes in Mathematics, 2078, Springer, Heidelberg, 181–199 (2013).

- (15) Hashimoto, H. and Tsuchiya, T.: On the convergent rates of Euler-Maruyama schemes for SDEs driven by rotation invariant -stable processes, RIMS Kokyuroku, 229–236 (2013), in Japanese.

- (16) Hefter, H. and Herzwurm, A.: Strong convergence rates for Cox-Ingersoll-Ross processes - Full parameter range, J. Math. Anal. Appl. 459(2), 1079–1101, (2018).

- (17) Jiao, Y., Ma, C. and Scotti, S.: Alpha-CIR model with branching processes in sovereign interest rate modelling, Finance Stoch. 21 (3), 789–813 (2017).

- (18) Jiao, Y., Ma, C. and Scotti, S. and Sgarra, C.: A Branching Process Approach to Power Markets, Accepted for publication in Energy Econ. (2018).

- (19) Li, Z. and Mytnik, L.: Strong solutions for stochastic differential equations with jumps, Ann. Inst. H. Poincaré Probab. Statist. 47 (4), 1055–1067 (2011).

- (20) Li, Z. and Ma, C.: Asymptotic properties of estimators in a stable Cox-Ingersoll-Ross model, Stoch. Process. Appl. 125 (8), 3196–3233 (2015).

- (21) Li, L. and Taguchi, D.: On the Euler-Maruyama scheme for spectrally one-sided Lévy driven SDEs with Hölder continuous coefficients, Stat. Probab. Lett. 146, 15–26, (2019).

- (22) Milstein, G. N., Repin, Y. M., and Tretyakov, M. V.: Numerical methods for stochastic systems preserving symplectic structure, SIAM J. Numer. Anal., 40 (4), 1583–1604 (2002).

- (23) Neuenkirch, A. and Szpruch, L., First order strong approximations of scalar SDEs defied in a domain, Numer. Math. 128 103–136. (2014).

- (24) Stamatiou, I.: An explicit positivity preserving numerical scheme for CIR/CEV type delay models with jump, arXiv:1803.00327, Working Paper 2018.

- (25) Sato, K.: Lévy Processes and Infinitely Divisible Distributions, Cambridge University Press (2011).

- (26) Kohatsu-Higa, A. and Tankov, P.: Jump-adapted discretization schemes for Lévy-driven SDEs, Stoch. Process. Appl. 120 (11), 2258–2285, (2010).

- (27) Yamada, T. and Watanabe, S.: On the uniqueness of solutions of stochastic differential equations, J. Math. Kyoto Univ. 11, 155–167 (1971).

- (28) Yang, X. and Wang, X.: A transformed jump-adapted backward Euler method for jump-extended CIR and CEV models, Numer. Algor. 74 (1), 39–57 (2017).