Central limit theorems from the roots of probability generating functions

Abstract

For each , let be a random variable with mean , standard deviation , and let

be its probability generating function. We show that if none of the complex zeros of the polynomials is contained in a neighbourhood of and for some , then is asymptotically normal as : that is tends in distribution to a random variable . Moreover, we show this result is sharp in the sense that there exist sequences of random variables with for which has no roots near and is not asymptotically normal. These results disprove a conjecture of Pemantle and improve upon various results in the literature. We go on to prove several other results connecting the location of the zeros of and the distribution of the random variable .

1 Introduction

Let be a random variable with mean and standard deviation and let the polynomial be its probability generating function

In this paper, we are concerned with the following general question: what can be deduced about the distribution of the random variable from information on the location of the roots of in the complex plane? For example, suppose that we are given a random variable and know only that the zeros of are real. With this knowledge at hand, we readily factor as (assuming for the moment) and notice that the roots of must be non-positive as the coefficients of are non-negative. Hence, we may write , for some . A little further thought reveals that this special expression for the probability generating function corresponds to an expression of as a sum of independent random variables , where is the -random variable, taking with probability . Thus, with an appropriate central limit theorem at hand, we see that must be approximately normal, provided the variance of is sufficiently large. In other words, from this one piece of information (albeit a strong piece of information) about the zeros of , one can quickly deduce quite a bit of information about the distribution of . The aim of this paper is to show that this assumption of real rootedness of can be related quite considerably while yielding similar results. In particular, we give three different results each of which says that “if has large variance and the roots of avoid a region in the complex plane, then is approximately normal.”

1.1 History

Before turning to our contributions, we take a brief moment to situate our results in an old and well-studied field centred around the following question: What does information about the coefficients of tell us about the distribution of the complex roots of (and vice versa)? This question has a long and rich history, reaching back to the seminal work of Littlewood, Szegő, Pólya, and perhaps even Cauchy, due to his 1829 proof [8] of the fundamental theorem of algebra, which gives explicit bounds on the magnitude of the complex roots (see [7, Theorem 1.2.1] for a modern treatment of this proof).

One line of research, initiated by the 1938 - 1943 work of Littlewood and Offord [21, 22, 23], concerns the typical distribution of roots of random polynomials. For example Kac [18] gave an exact integral formula for the number of real roots of random polynomial, with coefficients sampled independently from a normal distribution. Later, Erdős and Offord [11] showed that as almost all polynomials of the form , where , have real roots. Since these results, numerous other settings have been explored [19, Example I.2], including varied models as well as extensions to the roots of random power series [29, 32].

Deterministic results have also received considerable attention. To name a few, Bloch and Pólya [5] studied the maximum number of roots of a polynomial with coefficients in and degree . After improvements by Schur [34] and Szegő [39], this line culminated in the remarkable and celebrated result of Erdős and Turán [12] from 1950: if a polynomial has sufficiently “flat” coefficients, meaning , then the roots of are approximately “radially equidistributed”, in the sense that for every , the number of roots with is . Further refinements have been obtained by Ganelius [14], Mignotte [26] and more recently, by Erdélyi [10] and Soundararajan [36]. Also, Bilu [4] obtained a beautiful variant of the Erdős-Turán theorem for higher dimensions and with more algebraic restrictions (also see Granville [16] for some discussion).

In another direction, Odlyzko and Poonen [28] have studied the geometric properties of the set of points in the complex plane that are the zero of some polynomial with coefficents in ; they show that the closure of this set is path connected, and that it appears to exhibit a certain fractal-like structure. Beaucoup, Borwein, Boyd and Pinner [2], in a similar vein, have studied the multiple real roots of power-series with restricted coefficients.

Interestingly, and most relevant to our work here, the roots of polynomials with non-negative coefficients are also known to have several particular properties [1, 13]. To take an example in the flavour of Erdős and Turán, an old observation of Obrechkoff [27] says that if is a degree polynomial with non-negative coefficients and , then the number of zeros with is at most ; that is, “at most twice as much as the equidistributed case.”

1.2 Results

In the present work we take a slightly different perspective from many of the results above; instead of assuming “small scale” information about the coefficients (like assuming that they takes values in , say), we look to connect “large scale” distributional information of the coefficients with the distribution of the roots. Indeed, we restrict our attention to polynomials with non-negative coeffiecents and think of the polynomial as a probability generating function of a random variable.

In this line, Hwang and Zacharovas [17] showed that if a sequence of random variables is such that all of the zeros of lie on the unit circle and , then the limiting distribution of is completely determined by its fourth centralized moments . As a consequence, they gave a simple criterion for to be asymptotically normal.

Later, Lebowitz, Pittel, Ruelle and Speer (Henceforth LPRS) [20] studied a looser restriction on the roots that guarantees a central limit theorem for with large variance. They showed that if , and none of the roots of is contained in a neighbourhood of , then satisfies a central limit theorem. This lead Pemantle [30] to conjecture that a similar result holds with a weaker criterion on the variance. Namely, he conjectured that is sufficient to guarantee a central limit theorem if all the roots of avoid a neighbourhood of . We show that this conjecture is false, however the condition on the variance in the Theorem of LPRS can be considerably improved, as anticipated by Pemantle.

Theorem 1.

Let and, for each , let be a random variable with standard deviation . If all the roots of satisfy then the sequence satisfies a central limit theorem.

On the other hand, we show that for every there exists with , for which in distribution and for all roots of the polynomials . The obvious question that arises is: what is the correct variance condition in Theorem 1? It is perhaps reasonable to put forward the following modified version of Pemantle’s original conjecture.

Conjecture 2.

Let and, for each , let be a random variable with variance . If all the roots of satisfy and for every then satisfies a central limit theorem.

We note in passing that Theorem 1 also implies an improvement on the work of Ghosh, Liggett and Pemantle [15] who considered a similar situation for vector-valued random variables. Let be a sequence of random variables taking values in and let be the corresponding probability generating functions

They showed that if the polynomials are “real stable” then tends to a multivariate normal, provided the variance grows sufficiently quickly. Here, a polynomial is said to be real stable if each of its roots has at least one coordinate with imaginary part . This class of polynomials, admittedly a little strange at first blush, arise naturally in many situations [31]; indeed, the corresponding random variables can be thought of as vast generalizations of determinantal measures (see the discussion in [15] or [35, Theorem 2] together with [6, Proposition 3.2]). Our Theorem 1 implies an improvement on the variance condition in the theorem of Ghosh, Liggett and Pemantle theorem, and partially answers a question of theirs [15].

Corollary 3.

Let and for each , let be a random variable with covariance matrix and real stable probability generating function . If there exists a sequence of real numbers with and a matrix for which then

Our next result says that if all the roots of grow polynomially, that is satisfy for some fixed as , then satisfies a central limit theorem. Actually the proof of this result naturally provides a slightly stronger result.

Theorem 4.

Let and, for each , let be a random variable with standard deviation . Let be the set of roots of the probability generating function of . If and

as then satisfies a central limit theorem.

Theorem 4 is also best possible, in the sense that for every function there exists a sequence of random variables , so that , all of the roots of satisfy , and does not tend to a normal in distribution.

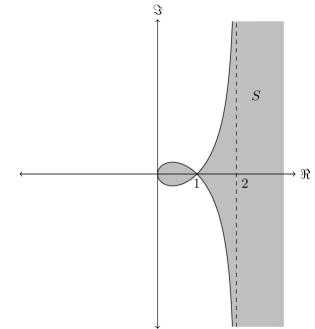

In light of Theorem 1, it is natural to ask if there is a larger neighbourhood of so that if the roots of avoid then satisfies a central limit theorem whenever . Our last theorem shows that this is true if we choose to be a neighbourhood of along with an open set containing the region , as shown in Figure 1. While this region seems to be a strange choice, it is actually quite natural; if the roots of avoid this region then each of the roots of can be thought of as contributing positively to the variance of . Moreover is the largest region for which this is true.

To state our theorem, let and let be the number of zeros of with distance at most to , where the roots are counted with multiplicity. We prove the following:

Theorem 5.

Let and let be a sequence of random variables with . If every zero of satisfies and then satisfies a central limit theorem.

1.3 Some remarks on the proofs

To prove Theorems 1 and 4, we control the rescaled characteristic functions . Our first step is to find an appropriate form of this function in terms of the roots of the polynomial . As it turns out, it is rather difficult to work directly with so we instead opt to work with for some appropriately chosen sequence . One of our main ingredients is captured in Lemma 10, which allows us to use these results to relate information about to . To control in the proof of Theorem 1, we carefully analyse how much each root contributes to our exponential representation of . The proof of Theorem 4 uses a technique from linear algebra. The proof of Theorem 6 is rather different: we use a moment method to show convergence to a normal.

It is perhaps interesting to note that our results seem to use the fact that the polynomials have non-negative coefficients in a much more central way than in previous work. To understand what is meant by this, let be an (arbitrary) polynomial with . We may formally define and and then say that a sequence of such polynomials satisfies a central limit theorem if . The results of Hwang and Zacharovas and LPRS both work work in this more general setting and, indeed, in this generalized setting, the bound on the variance [20] cannot be improved. Thus Theorems 1 and 4 depend more deeply on the hypothesis of non-negative coefficients.

2 Some Preparations

If is a real-valued random variable, we define, as is standard, the characteristic function of as the function , for . A key ingredient in our results will be the following theorem of Marcinkiewicz [24, Theorem 7.3.3] [25], which gives us some information about the structure of characteristic functions that have a specific exponential form.

Theorem 6.

Let be a polynomial. If is the characteristic function of a real-valued random variable, then .

We also use the well known fact that in distribution if and only if the associated characteristic functions converge point-wise. Thus, to show the convergence in distribution, where , it suffices to show the point-wise convergence . With this target in mind, we seek an exponential form for the polynomials .

2.1 An exponential form for

To find such an exponential expression, we take logarithms of our probability generating function in an appropriate region. We use the principal branch of the logarithm: for , write , where and . When then define . We use three simple properties of this function: that , where ; that , and that , for all with .

For a polynomial with roots , define

The following lemma gives us our desired exponential form for our polynomials.

Lemma 7.

Let , and let be a random variable with probability generating function . If all the roots of satisfy and , then for all with , we have the expression

| (1) |

where

Proof.

Let be the roots of . We write

for some non-zero constant .

We now take a logarithm of this expression for for satisfying . This is possible as all the zeros of satisfy and so we write

where is an integer valued function. Now since satisfies and there are no zeros with , we may use the Taylor expansion of the logarithmic terms. We obtain

Since , we must have

so we may write

where is an integer-valued function. We now exponentiate each side of the equation to obtain the desired result.

In the following lemma, we use the expression at (1) to obtain a exponential expression for . This lemma will ultimately be applied to the characteristic functions of our given sequence . We shall also see that this expression gives us a way of writing the cumulants of a random variable in terms of the roots of its probability generating function. Recall that if is a random variable and we put then the cumulant sequence of is defined as the coefficients in the Talyor expansion of about the origin.

Lemma 8.

Let , and let be a random variable taking values in with probability generating function . If all the roots of satisfy both and then there exists an so that for with we have

| (2) |

where , and . Moreover, the may be chosen so that convergence of the double sum is uniform for .

Anticipating the application of the Lemma 8, the reader may feel that it is far too weak for our purposes; the neighbourhood on which we have equality depends dearly on the closet root of to the unit circle and, in general, will be far too small for our application. However, this statement will be sufficient when used in tandem with the uniqueness of analytic continuations. Indeed, in the course of the proof, we will see that both expressions for are analytic in suitably sized regions and thus, from this lemma, we will be able to conclude that they are equal in these larger domains.

Proof.

The proof is straightforward; we use Lemma 7 to write in an appropriate form, use the Taylor expansion of and then exchange the order of summation. The only point at which we need to be careful is with the exchange of sums. However, we will quickly see that there is no danger as we are able to restrict to guarantee that the double sum is absolutely convergent.

Indeed, it is enough to show that the sums , , expanded from line (2), are absolutely convergent. We show the absolute convergence for the sum with the terms, and note that the proof of the other sum is analogous. Define and note that , which implies

where the exchange in sums is allowed due to the positivity of the sequence. This last sum is bounded above by , which converges absolutely whenever . Since , there exists an so that this occurs for . Free to exchange sums, we compute

Corollary 9.

In the notation above, the th cumulant of is for and for .

Proof.

Since , Lemma 8 implies that the moment generating function is analytic in some neighborhood of . Taking logarithms and equating coefficients completes the proof.

2.2 Controlling Higher Cumulants is Enough

As noted earlier, we shall use Lemma 8 to obtain an expression for the characteristic function of . So, in line with the strategy of showing convergence of the characteristic functions, we are led naturally to control the rescaled characteristic functions . It turns out this is somewhat tricky to do directly, and instead we will show that there is some appropriately chosen sequence for which we can control . The following, slightly technical lemma, tells that controlling will be sufficient for our purposes. For this lemma, define the height of a polynomial to be the magnitude of its largest coefficient .

For this lemma we require the following basic fact. If is a sequence of polynomials of bounded degree that converge to a polynomial and is a sequence of complex numbers converging to , then . We shall also use Lévy’s continuity theorem, which says that if is a sequence of characteristic functions that converges point-wise to a function then is a characteristic function provided is continuous at . See, for example, [9, Theorem 3.3.6] for a proof.

Lemma 10.

For each , let be a real-valued random variable with mean , standard deviation and with characteristic function . Let be polynomials of degree at most with bounded height and for which no subsequence tends to the zero polynomial. Let be a sequence of twice continuously differentiable functions with for and all . If there exists a sequence of positive real numbers so that

then satisfies a central limit theorem.

Proof.

We show that as for all . To show this, note that it is sufficient to show that for every infinite subsequence there is a further infinite subsequence so that . We put for each and let denote the characteristic function of .

Let be a given infinite subsequence. We now restrict to a subsequence for which converges to a polynomial of degree at most . Note that cannot be the zero polynomial by the condition on in the hypothesis. We have

for each . Put so that pointwise, and note that since is the characteristic function of and the limit is continuous at , is the characteristic function of some random variable . Thus, by Marcinkiewicz’s Theorem (Theorem 6), it follows that is a polynomial of degree at most , where we may assume that has imaginary part in the interval . We show that . It is easy to see that as . To see that , we need the following straightforward claim.

Claim 11.

We have that , for .

Proof of Claim : We observe that

and similarly for . ∎

So to see that , note that and, on the other hand, we have

which tends to as tends to infinity.

Thus we have shown that , and therefore converges to a normal random variable along the subsequence . We now need only to show that (with scaling by ) converges to a standard normal along the subsequence . To this end, we note that

| (3) |

and thus the limit of the ratio converges to some fixed number , as . Since is non-zero, we in fact have .

3 Proof of Theorem 1

It will be convenient to assume that no roots of have modulus identically equal to ; we claim that this can be assumed without loss of generality by simply perturbing the random variables slightly. Indeed, for any close to , we may define a random variable via where . Then the probability generating function of is And so we see that the roots of are simply the roots of , scaled by a factor of . Also observe that for each fixed , the functions , and are continuous functions of and take a value of at . Therefore, we may choose depending on and approaching so that 1) has a central limit theorem if and only if does 2) none of the have roots on the unit circle.

3.1 Proof of Theorem 1

To control the higher cumulants, we bound the contribution from each root individually:

Lemma 12.

For , let satisfy . Then for any , we have

| (4) |

for all satisfying .

Proof.

Note that

where are the Stirling numbers of the second kind. To see the above, note that it holds for , and proceed by applying the operator to both sides and using the recurrence relation [37, Equation (1.93)]. Applying this to the left-hand-side of (4) gives

Taking modulus of both sides and recalling and gives an upper bound of

| (5) |

By [33], the upper bound of holds for all and . Applying this bound to (5) gives a new upper bound of

for .

Corollary 13.

Let satisfy for some . Then for any , we have

| (6) |

for all satisfying .

Proof.

Apply Lemma 12 to and .

With these preparations, we are in a position to prove Theorem 1.

Proof of Theorem 1 : For some , let be a sequence of random variables for which takes values in and has mean and standard deviation . Let be the corresponding sequence of probability generating functions. Put . By the discussion at the start of the present section, we may assume without loss that no has a root on the unit circle.

We apply Lemma 8 for each to find an so that

| (7) |

for all . Put and recall that

and that

where the outer sums on the both right hand sides are over all roots of .

Claim 14.

The equality at equation (7) holds for all .

Proof of Claim : To see this, we first show that exists and is complex analytic in the domain . As is defined by a power series, we need only to show that it is bounded in this region. We apply Lemma 12 and Corollary 13 to estimate the exponent in (7). Indeed,

and therefore the right hand side of (7) is a complex analytic function in the region . On the other hand, is a polynomial and thus is an entire function of . Thus, by the identity theorem for holomorphic functions, the equation at (7) is valid for all . ∎

We now look to apply Lemma 12 to control the , for some suitable sequence . In particular, choose and recall that from Corollary 9.

Claim 15.

There exists a sequence of polynomials , and a sequence of twice continuously differentiable functions so that is not a limit point of , for all and and

Proof of Claim : Put and define

Now note that the degree and height of the polynomials are bounded, simply by definition of the . Moreover, cannot be a limit point of the as there is always an for which the the th term in is at least , in absolute value.

Moreover, this shows that for large enough , is an analytic function of in a domain containing the origin. Since uniformly tends to zero in this domain, it follows that tends to zero, in this range for all . This completes the proof of Claim 15. ∎

Thus Claim 15 allows us to apply Lemma 10 which, in turn, implies that the satisfy a central limit theorem. ∎

We now quickly obtain our improvement on the Theorem of Ghosh, Liggett and Pemantle as a corollary. To do this we use the well known theorem of Cramér and Wold (see Corollary in [15]), which says a sequence of random variables converges in distribution to a centred Gaussian if and only if for each , the projections converge in distribution to .

Proof of Corollary 3 : Let be an appropriate sequence of random variables with probability generating functions . We let be the sequence of covariance matrices, let be the sequence of means and put . Recall that we have some sequence for which and . We now show by showing that we satisfy the conditions of the Cramér-Wold Theorem.

If write and observe that the projection of , has mean and variance . Moreover, its probability generating function is exactly , which has no zeros in a neighbourhood of due to the fact that is stable ([15] Lemma 2.2). So if for some , we may apply our Theorem 1 to learn that . Therefore

If is not growing polynomially in the degree, we certainly have and thus converges to a point mass at by Chebyshev’s inequality. This is the same as . Hence we finish by applying the Cramér-Wold theorem. ∎

In the following section, we turn to give some examples which show that polynomial growth condition on the variance cannot be be replaced with a logarithmic growth condition.

3.2 An example with logarithmic variance

In this section we give class of examples that demonstrate the tightness of Theorems 1 and 4 in an appropriate sense. Let be a Poisson random variable with variance , which has been conditioned on being at most . Note that and . It is also clear that has probability generating function , where .

Curiously, the roots of these polynomials have received a considerable amount of attention going back to the work of Szegő [38], who proved the remarkable fact that the roots of converge to the curve

We refer the reader to [40] for an exposition of these results and many further results.

We shall only use the following consequence of the work of Szegő:

Lemma 16.

There exists a constant so that all of the roots of satisfy .

The following theorem contains our main construction.

Theorem 17.

For every there exists a sequence of random variables that does not satisfy a central limit theorem while , and for all the roots of the .

Proof.

We first show that if we can find a example of a sequence that satisfies Theorem 17 for some value of then we may boost the variance (that is, increase ) by adding a collection of independent Bernoulli random variables to our example. So suppose that satisfies the statement in the theorem (with and let be given. We produce a sequence with standard deviation which satisfies the statement of the theorem. For this, put and let be independent of . We define , and note that . Moreover,

tends to a linear combination , where , and is distributed as the limit of , which is not normal, by assumption. It follows that is not normal by Cramér’s Theorem [24, Theorem ].

It is also easy to calculate the roots of the probability generating function of . Indeed has probability generating function , which only adds zeros at .

We now show that the theorem holds for the constant and thus finish the proof of the theorem. We shall omit floors and ceilings in our discussion. We set and let be a Poisson random variable which has been conditioned on being at most . We define a random variable to be

a random variable with mean , standard deviation and with probability generating function . By Lemma 16, the roots of this polynomial satisfy and therefore tend uniformly to the circle of radius .

On the other hand, we have

which converges in distribution to a random variable .

With a different choice of the parameters in this construction, we demonstrate the sharpness of Theorem 4. That is, we show that there exists a sequence with that doesn’t satisfy a central limit theorem and the roots of just fail to be polynomially large in modulus.

Theorem 18.

For any , there exists a sequence , of random variables that does not satisfy a central limit theorem where , and the roots of satisfy .

Proof.

Let and define .

4 Proof of Theorem 4

In this section we prove Theorem 4, which roughly says that if the roots associated with our sequence tend to infinity at a rate polynomial in the degree of the , then we have a central limit theorem, provided . Note that Theorem 4 also yields a central limit theorem when all roots converge to sufficiently quickly; simply consider the polynomial which is the probability generating function of .

If is a polynomial with and roots , we define

for each . We begin with a lemma that says that we have a slightly stronger form of Lemma 8 when .

Lemma 19.

Let , and for each let be a random variable with probability generating function . If , then for all sufficiently large we may write

for all , where

and for each fixed and . Additionally we have, .

Proof.

Note that implies that . This gives the bound for . We write exponentially by applying Lemma 7 and using the identity . We obtain

| (8) | ||||

| (9) | ||||

| (10) |

where is defined to be the tail sum in the line above. Bound

for Utilizing and shows that this tail sum converges to zero for each fixed . The first two derivatives of are bounded by

Both sums can be shown to converge to zero for each by bounding and summing the remaining series. To show that , we need only to take logarithms of both sides at (10) and then use the definition of the cumulants and the fact that the variance of a random variable is its second cumulant.

At this point, the important observation is that the rate of growth of the large cumulants is “linearly” determined by the rate of growth of the terms . This will ultimately tells us that it is impossible for the cumulant sequence to grow fast enough to stop from tending to a function of the form , where is a polynomial. The following lemma captures the dependence between the growth of the cumulants and the growth of .

Lemma 20.

Let and let be such that every set of consecutive vectors are linearly independent and the are non-zero infinitely often. Then there exists an infinite set of integers and a sequence of real numbers so that the following hold:

-

1.

;

-

2.

is non-zero for infinitely many values of ;

-

3.

.

Proof.

Let be an infinite set for which for and for which the limit converges to some non-zero vector . In what follows, let us assume that we are only considering . Now note that there exists a sequence so that , where .

Let be the matrix with rows ; note that the linear map defined by has trivial kernel, as the vectors are linearly independent, by assumption. We express

| (11) |

and note that is non-zero and .

We now choose and note that is non-zero for infinitely many values, as is non-zero, for all . This proves Item 2. We also have that

thus proving Item 3 in the lemma.

We now combine these ingredients to prove Theorem 4.

Proof of Theorem 4 : For , let be a sequence of random variables for which converges to zero. To show convergence to a random variable , it is sufficient to prove that every subsequence has a further subsequence that converges to , as we did in the proof of Lemma 10.

We start by writing in an exponential form; Lemma 19 gives

| (12) |

where . Here we have suppressed the explicit dependence on by writing .

Set and put . Since , and , we have that and, in particular, is non-zero for infinitely many values. Also observe for every , the consecutive vectors are linearly independent: simply consider the matrix with rows ; then the columns of this matrix are which are linearly independent as are the columns of a Vandermonde matrix of full rank.

With the conditions satisfied, we apply Lemma 20 to our to find an infinite subsequence of integers and a sequence of real numbers , so that

| (13) |

as and tends to infinity, and is non-zero for infinitely many values. Since we will only be considering in what follows, we suppress the explicit dependence on .

Now, let be the smallest value for which and, anticipating an application of Lemma 10, we define

| (14) |

and split the sum at (12) according to . That is, we set

and put

The following is trivial from the definition.

Claim 21.

is a sequence of polynomials with bounded degree and height for which no subsequence converges to the polynomial.

In the remainder of the proof, we only need to control the higher order terms. That is, we show the following.

Claim 22.

We have that for all and .

Proof of Claim : We start by observing that can be bounded using the Cauchy-Schwarz inequality,

| (15) |

From the choice of at (14) and equation (13), we see that

| (16) |

and so from lines (15) and (16) we have

Applying this estimate, we see that

and that the right-hand-side of this inequality tends to zero as , due to the fact . Thus, is analytic and tends uniformly to zero in a neighbourhood of . It follows that , for all . This completes the proof of the claim. ∎

5 Roots Avoiding a Forbidden Region

Let for some taking finitely many values in . Then since has real coefficients, we may factor into conjugate pairs

where the first product is over the real roots and the second is over the non-real roots in the upper half plane. Note that each must be non-negative, as the coefficients of are non-negative. For , define and by

| (17) |

In the case of , define and and , , parallel to the above. For each , note that and that is the product of the . We now proceed as if the are probability generating functions. We define and for each define and note that and . In the case where for some , note that and . Additionally, direct calculation shows that for all we have , , and for each .

The key property is that these “central moments” behave just as if the are probability generating functions of independent random variables.

Lemma 23.

Let . Then for any we have the expansion

Proof.

Simply write

where we have used the Talyor expansion of .

Writing as a product over the ’s will give an expansion for the moments of in terms of the ’s; so to show that our random variable is normal, we only need to control the ’s. The following lemma gives us this control. It is also the point in the proof where we make use of the fact that the roots avoid the region .

Lemma 24.

Let . Then for there exists a constant so that for all satisfying , . Furthermore, if then there is a constant such that .

Proof.

In the case of , we have that where is a Bernoulli random variable in which case . We now deal with the case when .

Fix . One can see directly from the definition at (17) that as , we have and , and therefore as . Now is a continuous function of , in the region , and thus attains a maximum. That is, , for some constant .

We now turn to show the second part of the lemma, that , provided . Write . Since , a direct calculation gives

To see that if and only if , put and factor

As the denominator is always positive, the sign depends only on the numerator, which is the same expression that appears in the definition of .

So write

Since the line is contained in , we have that for all with . We bound in two steps; first for and sufficiently large, and then for sufficiently large and . Since the remaining set without these two regions is compact, the continuous function achieves a maximum on it.

We first bound for and large. Divide the numerator and denominator of the expression for by and bound the numerator by for all , . The denominator requires a bit more care. We have . Since is a compact set, we can find so that for all and we have

Then for and ,

We now bound for large and . So if we write , we bound

for sufficiently large and . Divide the numerator and denominator of the expression of by . Then for , the numerator is bounded above by

for . Similarly, the denominator over is bounded below by for and . Thus, for and , we have

Thus, we have that is bounded above for all and .

Proof of Theorem 5 : The proof is by the method of moments; Carleman’s continuity theorem tells us that convergence in distribution follows from the convergence of each moment. That is, it is sufficient to show that for each we have

since the right-hand-side is the th moment of a standard normal. Define to be the th moment of , i.e. the left-hand-side of the above equation. Since each is bounded, the expansion

converges in a neighborhood of .

By Lemma 23 and noting that , we have

| (18) |

Since for each , this means that . Expanding this product and equating coefficients—i.e. using the identity theorem—gives

| (19) |

where is the innermost sum in the line above. Since for all , it is sufficient to consider only compositions so that each part is at least .

Claim 25.

Let where and , for some . Then .

Proof of Claim : Define and and recall that . If we write it follows that

from Lemma 24 and from the assumption about the number of zeros within of our region . From Lemma 24 we also obtain an estimate for ,

| (20) |

Since is the same for all permutations of , we assume without loss of generality that is of the form with each .

Now . Thus, applying this times yields

| (21) |

Applying the triangle inequality, we see

where the last equality follows from line (20). This proves the claim. ∎

6 Acknowledgements

We would like to thank Robin Pemantle for bringing to our attention this circle of questions and Béla Bollobás and Robert Morris for comments. The second named author would like to thank Robin Pemantle and the University of Pennsylvania for hosting him while this research was conducted.

References

- [1] R.W. Barnard, W. Dayawansa, K. Pearce, and D. Weinberg. Polynomials with non-negative coefficents. Proc. Amer. Math. Soc., 113:77–85, 1991.

- [2] F Beaucoup, P Borwein, David Boyd, and Christopher Pinner. Multiple roots of [-1, 1] power series. 57:135–147, 02 1998.

- [3] P. Billingsley. Probability and measure. Wiley Series in Probability and Mathematical Statistics. John Wiley & Sons, Inc., New York, third edition, 1995. A Wiley-Interscience Publication.

- [4] Y. Bilu. Limit distribution of small points on algebraic tori. Duke Math J., 89(3), 1997.

- [5] A. Bloch and G. Pólya. On the roots of certain algebraic equations. Proc. London Math. Soc., 33:102–114, 1932.

- [6] J. Borcea, P. Brändén, and T. M. Liggett. Negative dependence and the geometry of polynomials. J. Amer. Math. Soc., 22(2):521–567, 2009.

- [7] P. Borwein and T. Erdélyi. Polynomials and polynomial inequalities, volume 161 of Graduate Texts in Mathematics. Springer-Verlag, New York, 1995.

- [8] A. L. B. Cauchy. Exercises de mathématiques, volume 3. Bure frères, 1828. p. 122.

- [9] R. Durrett. Probability: theory and examples, volume 31 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge, fourth edition, 2010.

- [10] T. Erdélyi. On the zeros of polynomials with Littlewood-type coefficient constrains. Michigan. Math. J., 49:97–111, 2001.

- [11] P. Erdős and A. C. Offord. On the number of real roots of a random algebraic equation. Proceedings of the London Mathematical Society, s3-6(1):139–160.

- [12] P. Erdős and P. Turán. On the distribution of roots of polynomials. Ann. of Math. (2), 51:105–119, 1950.

- [13] A. Eremenko and A. Fryntov. Remarks on the Obrechkoff inequality. Proc. Amer. Math. Soc., 144(2):703–707, 2016.

- [14] T. Ganelius. Sequences of analytic functions and their zeros. Ark. Mat., 3:1–50, 1954.

- [15] S. Ghosh, T. M. Liggett, and R. Pemantle. Multivariate CLT follows from strong Rayleigh property. In 2017 Proceedings of the Fourteenth Workshop on Analytic Algorithmics and Combinatorics (ANALCO), pages 139–147. SIAM, Philadelphia, PA, 2017.

- [16] A. Granville. The distribution of roots of a polynomial. In Equidistribution in Number Theory, an Introduction., pages 93–102, 2007.

- [17] H-K. Hwang and V. Zacharovas. Limit distribution of the coefficients of polynomials with only unit roots. Random Structures Algorithms, 46(4):707–738, 2015.

- [18] M. Kac. On the average number of real roots of a random algebraic equation. Bull. Amer. Math. Soc., 49(4):314–320, 04 1943.

- [19] M. Kac. Probability and related topics in physical sciences, volume 1957 of With special lectures by G. E. Uhlenbeck, A. R. Hibbs, and B. van der Pol. Lectures in Applied Mathematics. Proceedings of the Summer Seminar, Boulder, Colo. Interscience Publishers, London-New York, 1959.

- [20] J. L. Lebowitz, B. Pittel, D. Ruelle, and E. R. Speer. Central limit theorems, Lee-Yang zeros, and graph-counting polynomials. J. Combin. Theory Ser. A, 141:147–183, 2016.

- [21] J. E. Littlewood and A. C. Offord. On the number of real roots of a random algebraic equation. Journal of the London Mathematical Society, s1-13(4):288–295.

- [22] J. E. Littlewood and A. C. Offord. On the number of real roots of a random algebraic equation. II. In Mathematical Proceedings of the Cambridge Philosophical Society, volume 35, pages 133–148. Cambridge University Press, 1939.

- [23] J. E. Littlewood and A. C. Offord. On the number of real roots of a random algebraic equation. III. Rec. Math. [Mat. Sbornik] N.S., 12(54):277–286, 1943.

- [24] E. Lukacs. Characteristic functions. Hafner Publishing Co., New York, 1970. Second edition, revised and enlarged.

- [25] J. Marcinkiewicz. Sur une propriete de la lot de Gauss. Math. Zeits., 44:612–618, 1938.

- [26] M. Mignotte. Remarque sur une question relative á des fonctions conjuguées. C.R. Acad. Sci. Paris Sér. I. Math., 315(8), 1992.

- [27] N. Obrechkoff. Sur un problème de Laguerre. C. R. Acad. Sci., Paris, 177:102–104, 1923.

- [28] A.M. Odlyzko and B. Poonen. Zeros of polynomials with 0,1 coefficients. L’Enseign. Math., 39:317–348, 1993.

- [29] A. C. Offord. The distribution of the values of an entire function whose coefficients are independent random variables. Proc. London Math. Soc. (3), 14a:199–238, 1965.

- [30] R. Pemantle. Personal Communication.

- [31] R. Pemantle. Hyperbolicity and stable polynomials in combinatorics and probability. In Current developments in mathematics, 2011, pages 57–123. Int. Press, Somerville, MA, 2012.

- [32] Y. Peres and B. Virág. Zeros of the i.i.d. Gaussian power series: a conformally invariant determinantal process. Acta Math., 194(1):1–35, 2005.

- [33] B. C. Rennie and A. J. Dobson. On Stirling numbers of the second kind. J. Combinatorial Theory, 7:116–121, 1969.

- [34] I. Schur. Untersuchungen über algebraische gleichungen. Sitz. Preuss. Akad. Wiss., Phys.- Math. Kl., pages 403–428, 1933.

- [35] A. Soshnikov. Gaussian limit for determinantal random point fields. Ann. Probab., 30(1):171–187, 2002.

- [36] K. Soundararajan. Equidistribution of roots of polynomials. American Math Monthly.

- [37] R. P. Stanley. Enumerative combinatorics. Volume 1, volume 49 of Cambridge Studies in Advanced Mathematics. Cambridge University Press, Cambridge, second edition, 2012.

- [38] G. Szegő. Über eine eigenschaft der exponentialreihe. Sitzungsber Berliner Math. Gesellschaft, 23:50–64, 1924.

- [39] G. Szegő. Bemerkungen zu einem satz von E. Schmidt über algebraische gleichungen. Sitz. Preuss. Akad. Wiss., Phys.- Math. Kl., pages 86–98, 1934.

- [40] S. M. Zemyan. On the zeroes of the th partial sum of the exponential series. Amer. Math. Monthly, 112(10):891–909, 2005.