Fourth order compact scheme for option pricing under Merton and Kou jump-diffusion models

Kuldip Singh Patel,111Department of Mathematics, Indian Institute of Technology, Delhi, India, (kuldip@maths.iitd.ac.in) Mani Mehra222Department of Mathematics, Indian Institute of Technology, Delhi, India, (mmehra@maths.iitd.ac.in)

Abstract

In this article, a three-time levels compact scheme is proposed to solve the partial integro-differential equation governing the option prices under jump-diffusion models. In the proposed compact scheme, the second derivative approximation of unknowns is approximated by the value of unknowns and their first derivative approximations which allow us to obtain a tri-diagonal system of linear equations for the fully discrete problem. Moreover, consistency and stability of the proposed compact scheme are proved. Due to the low regularity of typical initial conditions, the smoothing operator is employed to ensure the fourth-order convergence rate. Numerical illustrations for pricing European options under Merton and Kou jump-diffusion models are presented to validate the theoretical results.

Keywords: Compact schemes; European options; jump-diffusion models; option pricing.

1 Introduction

F. Black and M. Sholes derived a partial differential equation (PDE) governing the option prices in the stock market assuming that the dynamics of the underlying asset are driven by geometric Brownian motion with constant volatility [1]. Later, numerous studies found that these assumptions are inconsistent with the market price movements. Various approaches have been considered to overcome the shortcomings of Black-Scholes model. In one of these approaches, Merton extended the Black-Scholes model to incorporate the jumps into the dynamics of the underlying asset in order to determine the volatility skews and it is known as Merton jump-diffusion model [2]. In another approach, the volatility is considered to be a stochastic process and these models are known as stochastic volatility models [3, 4]. Apart from these, the volatility is also assumed to be a deterministic function of time and stock price. This so-called deterministic volatility function approach was pioneered in [5]. Bates combined the jump-diffusion model with stochastic volatility approach to capture the typical features of market option prices [6]. Moreover, Anderson and Andreasen combined the deterministic volatility function approach with jump-diffusion model and proposed a second-order accurate numerical method for valuation of options [7]. In contrast to Merton jump-diffusion model where jump sizes follow Gaussian distribution, Kou proposed another jump-diffusion model assuming that jump sizes have double exponential distribution and it is called as Kou jump-diffusion model [8].

The prices of European options under Merton and Kou jump-diffusion models can be evaluated by solving a partial integro-differential equation (PIDE). Various numerical methods have been proposed by several authors to solve the PIDE accurately and efficiently. The viscosity solution of the PIDE is discussed in [9] and an explicit finite difference method is proposed to solve the PIDE with certain stability condition. Cont and Voltchkova proposed implicit-explicit (IMEX) scheme for pricing European and barrier options and proved the stability and convergence of the proposed scheme [10]. d’Halluin et al. proposed a second-order accurate implicit method which uses fast Fourier transform (FFT) for evaluating the convolution integral [11]. They also proved the stability and the convergence of the fixed-point iteration method. An excellent comparison of various approaches for option pricing under jump-diffusion models is given in [12]. An IMEX Runge-Kutta method for the time integration is proposed in [13] to solve the integral term of the PIDE explicitly. This method provides high-order accuracy under certain time step restriction. Sachs and Strauss used some transformation technique to eliminate the convection term from the PIDE and proposed a second-order accurate finite difference method for the solution of new PIDE [14]. A three-time levels second-order accurate implicit method using finite difference approximations is proposed in [15] for European put options under jump-diffusion models. A family of IMEX time discretization schemes is proposed in [16] to solve the PIDE under jump-diffusion models. They discussed the stability of the schemes via Fourier analysis and showed that the schemes are conditionally stable. A second-order accurate IMEX time semi-discretization scheme for pricing European and American options under Bates model is discussed in [17]. They explicitly treated the jump term using the second-order Adams-Bashforth method and rest of the terms are discretized implicitly using the Crank-Nicolson method. Recently, Kadalbajoo et al. proposed a second-order accurate IMEX schemes along with cubic B-spline collocation method for European option pricing under jump-diffusion models [18]. They discussed the stability, convergence and computational complexity of all schemes.

It is observed that the inclusion of more grid points in computation stencil in order to increase the accuracy of finite difference approximations becomes computationally expensive. Therefore, finite difference approximations have been developed using compact stencils (commonly known as compact finite difference approximations) at the expense of some complication in their evaluation. Compact finite difference approximations provide high-order accuracy and better resolution characteristics as compared to finite difference approximations for equal number of grid points [19]. Compact finite difference approximations have also been used for option pricing problems [20, 21, 22]. In particular, Lee and Sun considered the original PIDE as an auxiliary equation to derive a compact scheme for option pricing under jump-diffusion models [22]. They used IMEX schemes for temporal semi-discretization to avoid the inverse of a dense matrix and Richardson extrapolation is applied to obtain the fourth-order convergence rate. Recently, a fourth-order accurate compact scheme for option pricing under Bates model is derived in [23] and stability of the compact scheme is observed numerically. Moreover, compact schemes have been extensively studied for compressible flows problems [24] and for computational aeroacoustic problems [25]. A detailed study about various order compact finite difference approximations is given in [26].

In this article, a three-time levels compact scheme is proposed to solve the PIDE under jump-diffusion models. The novelty of the proposed compact scheme is that it does not require the original equation as an auxiliary equation unlike the compact scheme proposed in [22]. Moreover, consistency and stability of the proposed three-time levels compact scheme are proved. Since initial conditions for jump-diffusion models have low regularity, the smoothing operator given in [27] is employed to smoothen the initial conditions in order to achieve the fourth-order convergence rate. Simpson’s rule for numerical integration is used and a Toeplitz-like structure is obtained in order to use FFT for efficient matrix-vector multiplication. Moreover, the CPU times for proposed compact scheme and finite difference scheme are calculated for a given accuracy and it is shown that proposed compact scheme outperforms the finite difference scheme.

The rest of the paper is organized as follows. In Section 2, the continuous model problem is discussed. Fourth-order compact finite difference approximations for first and second derivatives along with a brief discussion on Fourier analysis are discussed in Section 3. In Section 4, three-time levels scheme for temporal semi-discretization and fourth-order compact approximations for spatial discretization are discussed for continuous PIDE. The consistency and stability of proposed three-time levels compact scheme are proved in Section 5. In Section 6, numerical examples are presented to validate the theoretical results.

2 The Continuous Problem

In this section, the mathematical model for pricing European options under jump-diffusion models is discussed. First we introduce the Lvy process in the following definition.

Definition 2.1.

Let be a probability space with filtration . A stochastic process is a Lvy process on if

-

1.

almost surely.

-

2.

It is stochastically continuous i.e. for all and for all

-

3.

For any , the distribution of does not depend on (stationary increments).

-

4.

For any and , the random variables , ,…, are independent (independent increments).

-

5.

The sample paths of are right continuous with left limits almost surely.

The Poisson process and the Brownian motion are the examples of Lvy processes. Suppose that the stock price process follows an exponential jump-diffusion model , where is the risk-free interest rate, is the stock price at and is a jump-diffusion Lvy process. The jump-diffusion Lvy process is defined as

| (1) |

where and are real constants and are independent and identically distributed random variable with density function . Furthermore, , , and are assumed to be mutually independent. In Merton jump-diffusion model, follows Gaussian distribution with density function

| (2) |

where and represents mean and standard deviation respectively. In case of Kou jump-diffusion model, follows double exponential distribution with density function

| (3) |

where is the indicator function with respect to a set , , and . The price of European options under jump-diffusion models () is obtained by solving a PIDE which is discussed in the following theorem [15].

Theorem 2.1.

Let the Lvy process has the Lvy triplet , where , and is the Lvy measure. If

then the value of European option with the payoff function is obtained by , where

is a continuous map on , on , and satisfies the following PIDE

| (4) |

on with the final condition

Let us consider the following transformation in the above PIDE (4)

Then, is the solution of the following PIDE with constant coefficients

| (5) |

where

| (6) |

is the intensity of the jump sizes and = . The initial condition for European call options is

| (7) |

and the equations describing the asymptotic behaviour of European call options are

| (8) |

Similarly, the initial condition for European put options is

| (9) |

and the asymptotic behaviour of European put options is described as

| (10) |

3 Fourth-Order Compact Finite Difference Approximations for First and Second Derivatives

Compact finite difference approximations for first and second derivatives are discussed in this section. From Taylor series expansion, second-order accurate finite difference approximations for first and second derivatives can be written as

| (11) |

where is the value of at a typical grid point . Moreover, fourth-order accurate compact finite difference approximations for first and second derivatives [19] are

| (12) |

| (13) |

where , are first and second derivatives of unknown at grid point . If first derivative is also considered as a variable then from Equation (12) we can write

| (14) |

Eliminating and from Equations (13) and (14), compact finite difference approximation for second derivative is

| (15) |

Substituting the values from Equation (11) into Equation (15), we get

| (16) |

It is observed that Equations (12) and (16) provide fourth-order accurate compact finite difference approximations for first and second derivatives. The value of in Equation (16) is obtained from Equation (12). One-sided compact finite difference approximations are discussed in [28] for non-periodic boundary conditions. It is shown in Figure 1 that lesser number of grid points are required with compact finite difference approximation as compared to finite difference approximation to obtain high-order accuracy.

3.1 Fourier analysis

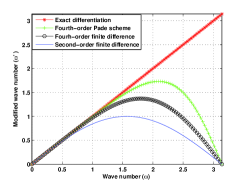

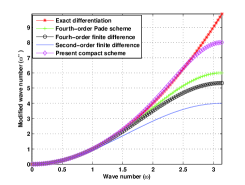

In this section, the wave numbers and the modified wave numbers for first and second derivative approximations are discussed in brief. A detailed discussion on the resolution characteristics of various order compact finite difference approximations is given in [19]. The trial function for this one on a periodic domain is , where and is known as wavenumber. The relations between (wave number), (modified wave number for first derivative) and (modified wave number for second derivative) for finite difference approximations and proposed compact finite difference approximations are given in [29]. The wave numbers versus modified wave numbers are plotted in Figures 2 and 2 for first and second derivative approximations and it is observed from figures that compact finite difference approximations have better resolution characteristics as compared to the finite difference approximations.

4 The Fully Discrete Problem

The domain of the spatial variable is restricted to a bounded interval for some fixed real number in order to solve the PIDE (5) numerically. For given positive integers and , let and and in this way we define and . Let us first introduce the numerical approximation for . The second-order accurate finite difference approximation for at each grid point is given by

| (17) |

where . The operator in Equation (6) can be written as

| (18) |

where

| (19) |

Now, the numerical approximations for the differential operator is discussed. If represents the discrete approximations for the operator then

where

| (20) |

and are the first and second derivative approximations of respectively. Substituting the value of from Equation (16) into the Equation (20), we get

| (21) |

In this way, we eliminate the compact finite difference approximations of second derivative using the unknowns and their first derivative approximations.

Now, the discrete approximation for the integral operator using fourth-order accurate composite Simpson’s rule is discussed. Integral operator given in Equation (19) is divided into two parts namely on and . The value of integration over for Merton jump-diffusion model is given as

| (22) |

where is the cumulative distribution function of standard normal distribution. Similarly, the value of integration over for Kou jump-diffusion model is given as

| (23) |

The value of integral on the interval using composite Simpson’s rule is given as

| (24) |

where . In order to write the above integral approximation (24) in matrix-vector multiplication form, we define

The matrix can be transformed into a Toeplitz matrix by transferring the coefficient to the vector as follows

and

The above matrix-vector product is obtained with complexity by embedding the matrix in a circulant matrix and using FFT for matrix-vector multiplication [30, 31]. Therefore, the discrete approximation for the integral operator is

| (25) |

If denote the discrete approximation of operator (defined in Equation (18)) then

| (26) |

The above three-time levels discretization of integro-differential operator is used for the solution of PIDE (5). We find (the approximate value of ) which is the solution of following problem

| (27) |

with suitable initial and boundary conditions. Using the value of from Equation (21) in Equation (27), we obtain

| (28) |

Re-arranging the terms, we get

| (29) |

Let us introduce the following notation

the resulting system of equations corresponding to the difference scheme (29) can be written as

| (30) |

The presence of on the right hand side of the Equation (30) bind us to use a predictor corrector method. Therefore, correcting to convergence approach is used and also summarized in the following algorithm [32].

Algorithm for Correcting to Convergence Approach

1. Start with .

2. Obtain using Equation (12).

3. Take , .

4. Correct to using Equation (29).

5. If , then .

6. Obtain using Equation (12).

7. Take , and go to step .

The stopping criterion for inner iteration can be set at in above approach. Approximately four iterations are needed at

each time interval to get . Since the proposed compact scheme (30) is three-time levels, two initial values on the zeroth and first time levels are required to start the computation. The initial condition provides the value of at and the value of at first time level is obtained by IMEX-scheme used in [10].

5 Consistency and Stability Analysis

5.1 Consistency

The consistency of the proposed three-time levels compact scheme (29) is proved in the following theorem.

Theorem 5.1.

Proof.

The second-order accurate finite difference approximation for at each grid point can be written as

| (32) |

Since the compact finite difference approximations for first and second derivatives (discussed in Section 3) are fourth-order accurate, therefore

Let us now discuss the first and second derivatives in operator . From Taylor series expansion for second derivative, we write

The following relation can be deduced for compact finite difference approximation for second derivative

From Taylor series expansion for the first derivative, we get

The compact finite difference approximation for first derivative provides the following relation

Therefore, the error between the operators and is

| (33) |

Further, Equation (24) provides the error between the integral operator and as

| (34) |

5.2 Stability

The stability of the proposed compact scheme is proved using von-Neumann stability analysis. Consider a single node

| (35) |

where , is the power of amplitude at time levels , and . The integral operator (19) can be re-written in an equivalent form as

Fourth-order accurate composite Simpson’s rule for above equation provides

where

| (36) |

The following Lemma is proved for numerical quadrature given in Equation (36).

Lemma 5.1.

The numerical quadrature satisfies the following

where is a constant.

Proof.

For the sake of simplicity, we denote and in the rest of this section. The fully discrete problem (29) can be written in terms of and as follows

| (40) |

The following relations are obtained from [33] in order to prove the stability of the proposed compact scheme (40)

| (41) |

Using Equation (41) in the difference scheme (40), we get

| (42) |

After re-arranging the terms, the above Equation (42) is written as

| (43) |

Using Equation (35) in above Equation (43), the amplification polynomial can be written as

| (44) |

where

| (45) |

The following lemma is needed to prove the stability of a three-time levels difference scheme, see [34].

Lemma 5.2.

A finite difference scheme is stable if and only if all the roots, , of the amplification polynomial satisfies the following condition:

. There is a constant such that .

. There are positive constants and such that if then is simple root and for any other root , following relation holds

as , .

Proof.

For the proof of above Lemma, see [34]. ∎

Now, we prove the above Lemma 5.2 for the proposed three-time levels compact scheme for the PIDE in the following theorem.

Theorem 5.2.

The fully discrete problem (29) is stable in the sense of von-Neumann for .

Proof.

Firstly, some properties of the coefficients and of amplification polynomial are proved. Using Lemma 5.1 in Equation (45), it is observed that

Further, the coefficient from Equation (45) can be written as

| (46) |

where

Since , which gives . Moreover, from Equations (45) and (46), we have

which implies . Now, roots of the amplification polynomial are

| (47) |

Hence, first part of the Lemma 5.2 is proved for constant . Let us assume that and are two roots of amplification polynomial and the constant which implies , then

| (48) |

If satisfies the given condition, we have

and this prove the second part of the Lemma 5.2 with . This completes the proof. ∎

6 Numerical Results

In this section, the applicability of the proposed compact scheme for pricing European options under jump-diffusion models is demonstrated. According to [27], fourth-order convergence cannot be expected for non-smooth initial conditions. Since the initial conditions given in Equations (7) and (9) have low regularity, therefore suitable smoothing operator is required to smoothen the initial conditions. For this purpose, the smoothing operator given in [27] is employed to smoothen the initial conditions and it’s Fourier transform is define as

As a result, the following smoothed initial condition is obtained

| (49) |

where is the actual non-smooth initial condition and is the grid point where smoothing is required. The smoothed initial conditions obtained from Equation (49) tends to the original initial conditions as . The parameters considered for pricing European options under Merton and Kou jump-diffusion models are listed in Table 1. The parabolic mesh ratio is fixed as in all our computations, although neither the von Neumann stability analysis nor the numerical experiments showed any such restriction. The error is used to examine the numerical convergence rate of the proposed compact scheme, where represents the solution at the step sizes and and represents the solution after halving the step sizes.

| Merton jump-diffusion model | Kou jump-diffusion model | ||

|---|---|---|---|

| Parameters | Values | Parameters | Values |

| S=90 | S=100 | S=110 | |

|---|---|---|---|

| Reference values | 9.285418 | 3.149025 | 1.401185 |

| Proposed compact scheme | 9.285420 | 3.149114 | 1.401176 |

| S=90 | S=100 | S=110 | |

|---|---|---|---|

| Reference values | 0.527638 | 4.391246 | 12.643406 |

| Proposed compact scheme | 0.527636 | 4.391244 | 12.643408 |

| S=90 | S=100 | S=110 | |

|---|---|---|---|

| Reference values | 9.430457 | 2.731259 | 0.552363 |

| Proposed compact scheme | 9.430448 | 2.731252 | 0.552361 |

| S=90 | S=100 | S=110 | |

|---|---|---|---|

| Reference values | 0.672677 | 3.973479 | 11.794583 |

| Proposed compact scheme | 0.672672 | 3.973476 | 11.794584 |

Example 1.

(Merton jump-diffusion model for European put options)

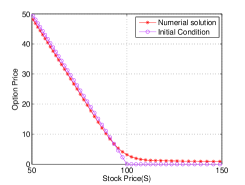

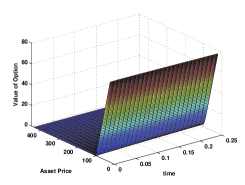

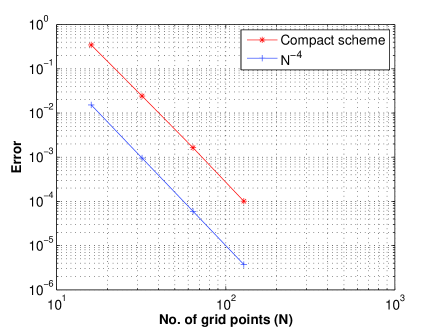

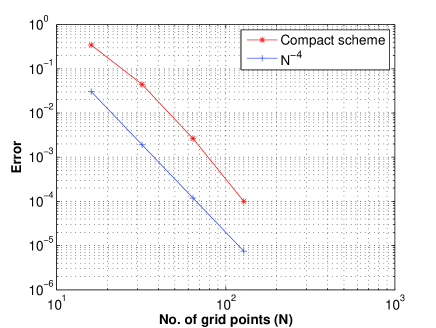

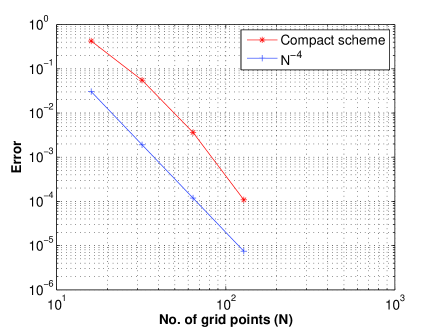

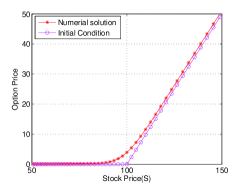

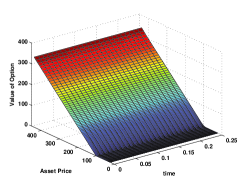

The reference values in Table 2 for European put options under Merton jump-diffusion model are obtained from the infinite series given in [2]. It can be observed from Table 2 that option prices obtained from the proposed compact scheme for different stock prices are in excellent agreement with the reference values. The initial condition and the numerical solution of the PIDE for European put option under Merton jump-diffusion model are presented in Figure 3. Moreover, the values of option as a function of stock price and time are plotted in Figure 3. The error versus number of grid points is presented in Figure 4 and it is observed that proposed compact scheme exhibit fourth-order convergence rate.

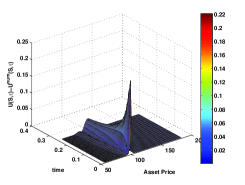

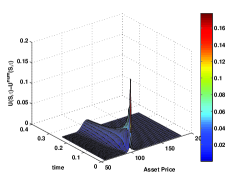

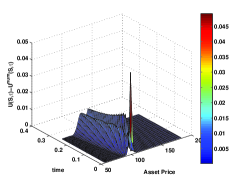

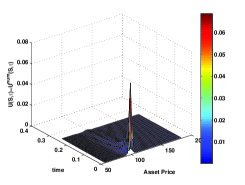

The analytic solution for European put options under Merton jump-diffusion model is obtained from [2]. The error between the analytic and numerical solution with non-smooth initial condition is presented as a function of time and stock prices in Figures 5 and 5. It is observed from the Figures 5 and 5 that proposed compact scheme provides lesser error as compared to finite difference scheme. Similarly, the error between analytic and numerical solution after applying the smoothing operator to the initial condition is plotted as a function of time and stock prices in Figures 5 and 5. It is shown in Figures 5 and 5that less oscillations are produced in the solution near the strike price with the proposed compact scheme.

Efficiency of proposed compact finite difference scheme:

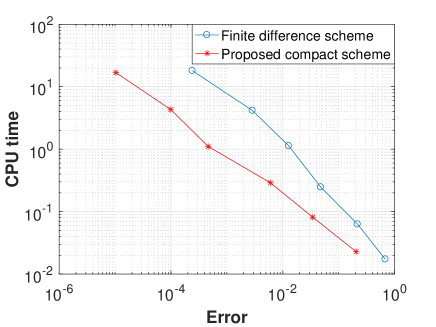

In order to compare the efficiency of the proposed compact scheme with finite difference scheme, the PIDE (27) is also solved using finite difference scheme. The error between numerical and analytic solutions in norm versus CPU time is presented in Figure 6. It is observed that proposed compact scheme is significantly efficient as compared to the finite difference scheme for a given accuracy.

Example 2.

(Merton jump-diffusion model for European call options)

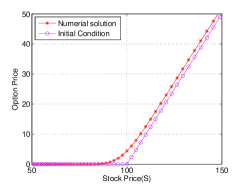

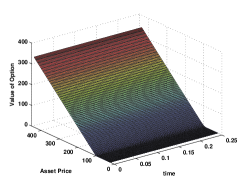

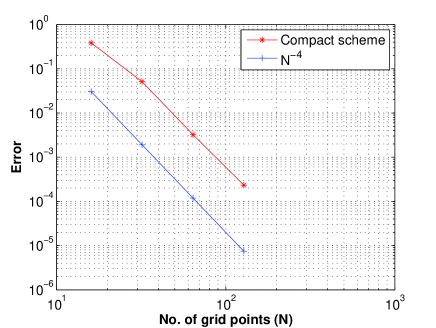

The option prices obtained from the proposed compact scheme and the reference values from [11] are given in Table 3. It can be observed from Table 3 that proposed compact scheme is accurate for pricing European call options. The error versus number of grid points is plotted in Figure 7 and fourth-order convergence of the proposed compact scheme is shown. The initial condition and numerical solution is presented in Figure 8. Moreover, the option prices as a function of stock price and time is shown in Figure 8.

Example 3.

(Kou jump-diffusion model for European put options)

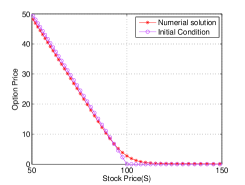

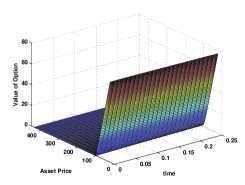

The option prices obtained from the proposed compact scheme and reference values from [15] for different stock prices are presented in Table 4. It can be observed from the Table 4 that option prices obtained from the proposed compact scheme are similar to the reference values. The initial condition and numerical solution for European put options is presented in Figure 9. The value of option as a function of stock price and time is plotted in Figure 9. Moreover, fourth-order convergence rate of the proposed compact scheme is observed from Figure 10.

Example 4.

(Kou jump-diffusion model for European call options)

The option prices obtained from the proposed compact scheme and reference values from [11] are presented in Table 5. It can be observed from the Table 5 that option prices obtained from the proposed scheme are in excellent agreement with the reference values. The initial condition and numerical solution for European call option is plotted in Figure 11. The values of option as a function of stock price and time are presented in Figure 11. Moreover, it can be observed from Figure 12 that proposed compact scheme exhibit fourth-order convergence rate.

Acknowledgement

The authors gratefully acknowledge the comments/suggestions of the referee which have greatly improved the paper. The authors also acknowledges the support provided by Department of Science and Technology, India, under the grant number .

References

- [1] F. Black and M. Scholes. The pricing of options and corporate liabilities. J. Political Econ., 81:637–654, 1973.

- [2] R. C. Merton. Option pricing when underlying stock returns are discontinous. J. Financial Econ., 3:125–144, 1976.

- [3] J. Hull and A. White. The pricing of options on assets with stochastic volatilities. J. Finance, 42:281–300, 1987.

- [4] S. L. Heston. A closed form solution for options with stochastic volatility with appliacations to bond and currency options. Rev. Financial Stud., 6:327–343, 1993.

- [5] B. Dupire. Pricing with a smile. Risk, 7:18–20, 1994.

- [6] D. Bates. Jump and stochastic volatility: exchange rate process implicit in deutsche mark options. Rev. Finan. Stud., 9:69–107, 1996.

- [7] L. Andersen and J. Andreasen. Jump-diffusion process: Volatility smile fitting and numerical methods for option pricing. Rev. Derivatives Res., 4:231–262, 2000.

- [8] S. G. Kou. A jump-diffusion model for option pricing. Manag. Sci., 48:1086–1101, 2002.

- [9] M. Briani, C. L. Chioma, and R. Natalini. Convergence of numerical schemes for viscosity solutions to integro-differential degenerate parabolic problems arising in finance theory. Numer. Math., 98:607–646, 2004.

- [10] R. Cont and E. Voltchkova. A finite difference scheme for option pricing in jump-diffusion and exponential Levy models. SIAM J. Numer. Anal., 43:1596–1626, 2005.

- [11] Y. d’Halluin, P. A. Forsyth, and K. R. Veztal. Robust numerical methods for contingent claims under jump-diffusion process. IMA J. Numer. Anal., 25:87–112, 2005.

- [12] D. J. Duffy. Numerical analysis of jump–diffusion models: A partial differential equation approach. Technical Report, Datasim, 2005.

- [13] M. Briani, R. Natalini, and G. Russo. Implicit -explicit numerical schemes for jump diffusion processes. Calcolo, 44:33–57, 2007.

- [14] E. W. Sachs and A. K. Strauss. Efficient solution of a partial integro-differential equation in finance. Appl. Numer. Math., 58:1687–1703, 2008.

- [15] Y. Kwon and Y. Lee. A second-order finite difference method for option pricing under jumps-diffusion models. SIAM J. Numer. Anal., 49:2598–2617, 2011.

- [16] S. Salmi and J. Toivanen. IMEX-schemes for pricing options under jump–diffusion models. Appl. Numer. Math., 84:33–45, 2014.

- [17] S. Salmi, J. Toivanen, and L. V. Sydow. An IMEX-scheme for pricing options under stochastic volatility models with jumps. SIAM J. Sci. Comput., 36:B817–B834, 2014.

- [18] M. K. Kadalbajoo, L. P. Tripathi, and Alpesh Kumar. Second order accurate IMEX methods for option pricing under Merton and Kou jump diffusion model. J. Sci.Comput., 65:979–1024, 2015.

- [19] S. K. Lele. Compact finite difference schemes with spectral-like resolution. J. Comput. Phys., 103:16–42, 1992.

- [20] B. During, M. Fournie, and A. Jungel. Convergence of high-order compact finite difference scheme for a nonlinear Black-Scholes equation. Math. Model. Numer. Anal., 38:359–369, 2004.

- [21] D. Y. Tangman, A. Gopaul, and M. Bhuruth. Numerical pricing of options using high-order compact finite difference schemes. J. Comput. Appl. Math, 218:270–280, 2008.

- [22] S. T. Lee and H. W. Sun. Fourth order compact scheme with local mesh refinement for option pricing in jump-diffusion model. Numer Methods Partial Differ Equ., 28:1079–1098, 2011.

- [23] B. During and A. Pitkin. High-order compact finite difference scheme for option pricing in stochastic volatility jump models. arXiv:1704.05308v1.

- [24] H. L. Meitz and H. F. Fasel. A compact-difference scheme for the Navier -Stokes equations in vorticity-velocity formulation. J. Comput. Phys., 157:371, 2000.

- [25] T. K. Sengupta, G. Ganeriwal, and S. De. Analysis of central and upwind compact schemes. J. Comput. Phys., 192:677, 2003.

- [26] M. Mehra and K. S. Patel. Algorithm 986: A suite of compact finite difference schemes. ACM Trans. Math. Softw., 44, 2017.

- [27] H. O. Kreiss, V. Thomee, and O. Widlund. Smoothing of initial data and rates of convergence for parbolic difference equations. Comm. Pure Appl. Math., 23:241–259, 1970.

- [28] K. S. Patel and M. Mehra. Fourth-order compact finite difference scheme for American option pricing under regime-switching jump-diffusion models. Int. J. Appl. Comput. Math., 3:547–567, 2017.

- [29] K. S. Patel and M. Mehra. A numerical study of Asian option with high-order compact finite difference scheme. J. Appl. Math. Comput., 2017. DOI:10.1007/s12190-017-1115-2.

- [30] R. Chan and X. Jin. An introduction to iterative Toepliz solvers. SIAM, 2007.

- [31] R. Chan and M. Ng. Conjugate gradient methods for toeplitz systems. SIAM Rev., 38:427–482, 1996.

- [32] J. D. Lambert. Numerical Methods for Ordinary Differential Systems: The Initial Value Problem. John Wiley and Sons, 1991.

- [33] K. S. Patel and M. Mehra. High-order compact finite difference scheme for pricing Asian option with moving boundary condition. Differ Equ Dyn Syst, 2017. DOI:10.1007/s12591-017-0372-8.

- [34] J. C. Strikewerda. Finite Difference Schemes and Partial Differential Equations. SIAM, 2004.