Bitcoin market route to maturity? Evidence from return fluctuations, temporal correlations and multiscaling effects.

Abstract

Based on 1-minute price changes recorded since year 2012, the fluctuation properties of the rapidly-emerging Bitcoin (BTC) market are assessed over chosen sub-periods, in terms of return distributions, volatility autocorrelation, Hurst exponents and multiscaling effects. The findings are compared to the stylized facts of mature world markets. While early trading was affected by system-specific irregularities, it is found that over the months preceding Apr 2018 all these statistical indicators approach the features hallmarking maturity. This can be taken as an indication that the Bitcoin market, and possibly other cryptocurrencies, carry concrete potential of imminently becoming a regular market, alternative to the foreign exchange (Forex). Since high-frequency price data are available since the beginning of trading, the Bitcoin offers a unique window into the statistical characteristics of a market maturation trajectory.

pacs:

89.75.-k – Complex systems, 89.75.Da – Systems obeying scaling laws, 89.65.Gh – Economics; econophysics, financial markets, business and managementThroughout history, the emergence of money constitutes one of the most significant achievements of civilizations, which simultaneously conditions their further evolution. By means of a process analogous to spontaneous symmetry-breaking in physical systems, money acquires the status of a universally-demanded commodity, and with it an inherent ability to serve as medium of exchange. In the contemporary high-technology era, information can readily become a high-value commodity, and the recent invention of the Bitcoin as a candidate currency naturally reflects this fact. A question that urgently needs addressing is whether, and to what extent, the emerging Bitcoin market exhibits the stylized statistical features which universally characterize mature global markets. Such question is important both theoretically, in reference to our understanding of the emergence of money, and practically, with immediate implications for policy-making. Here, it is demonstrated that over the recent months the Bitcoin market has become truly indistinguishable from mature markets according to the most important complexity characteristics, related to the return distribution, temporal correlations and multi-scaling effects, even including their generalization to discrete scale invariance, which manifests itself through log-periodic oscillations accompanying the large-scale trend reversals.

I Introduction

Money is the most liquid economic asset: it serves as a universal medium of exchange, with an inherent ability to buy, store wealth and act as unit of account. The origin of money and what precisely makes moneyness out of different economic assets and commodities remain an active area of interdisciplinary research menger1892 ; bak2001 ; lapavitsas2005 . Capturing the sheer complexity of the collective dynamics at play in the global foreign exchange (Forex) market represents a substantial challenge for traders, economists and physicists alike ghashghaie1996 ; drozdz2010 ; kwapien2012 . In recent years, arguably the most important advances in this area have come from agent–based computational economics models yasutomi1995 ; yasutomi2003 ; samanidou2007 ; gorski2010 ; oswiecimka2015 .

The commodity-based currency is a nearly extinct concept nowadays, with fiat currency relentlessly propelling financial markets around the clock. Over the last decades, the advent of electronic banking and trading, and eventually algorithmic trading, has drastically increased the frequency and security of trading, weaving complex relationships between information/events and fluctuations, and furthermore supporting the development of more and more abstracted derivative products. In 2008, Satoshi Nakamoto – a pseudonym for the anonymous inventor(s) whose identity remains unconfirmed – put forward a cryptographic protocol allowing peer–to–peer payments without need for endorsement or endowment by any third–party entity. Its monetary unit, known as the Bitcoin (BTC), accordingly needs not be issued by any central bank or government berentsen2018 . This disruptively new concept has become a topic of substantial social and scientific interest, even concern, with potentially deep implications for market regulation and stability kristoufek2013 . At the time of writing, more than a thousand electronic currency and transaction protocols using classical asymmetric cryptography technology have emerged, including for example the Ethereum, Ripple, Bitcoin Cash and Litecoin. Moreover, the currently huge volatility of the BTC market, together with its large capitalization, is very likely to spearhead the emergence of other comparably strong cryptocurrencies, with potentially substantial impact on the global trading system.

The most informative measures of any market dynamics are derived from the statistical features of the corresponding price fluctuations . These include return distributions for a given time-lag , temporal dependences of unsigned return distributions reflecting volatility correlations, the market’s susceptibility to persistence as quantified by the Hurst exponents, as well as more subtle non-linear correlations which may manifest as scale-free relationships kwapien2012 . Here, a comprehensive account of the emerging BTC market from these perspectives is provided, and references to the notion of “mature market” are understood in an econophysics sense kertesz1999 ; cont2001 ; zheng2014 . Namely, they refer to the statistical features that are empirically-identified and ubiquitous in all well-established, large-capitalization and high-liquidity world markets. These features include: i) fat-tailed return distributionlux1996 ; dacorogna2001 , which for sufficiently small is to a good approximation scale-free with scaling exponent gopi1998 ; gopi1999 , is therefore known as the inverse cubic power-law gabaix2003 , ii) temporal autocorrelation of returns that almost instantly decays to zero fama1965 ; gopi1999 ; drozdz2010 ; kwapien2012 , iii) volatility autocorrelation which, by contrast, remains positive over long periods of time gopi1999 ; mantegna2000 , iv) Hurst exponent fluctuating close to 0.5 grech2004 ; matteo2005 ; cajueiro2006 ; tabak2006 , and v) multiscaling effects halsey1986 in the temporal organization of returns, which manifest as broad singularity spectra oswiecimka2005 ; drozdz2010 ; oh2012 ; shahzad2017 , reflecting the presence of nonlinear correlations in this organization calvet2002 ; kwapien2012 .

II Bitcoin returns and volatility

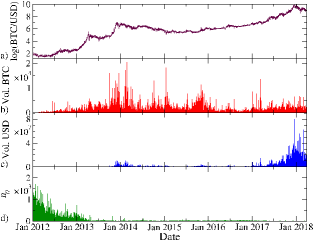

Publicly-available BTC trading data were downloaded from the Bitstamp exchange (Luxembourg) data2018 , and span the period from Jan 01, 2012 to Mar 31, 2018 with a sampling frequency of 1 minute. The corresponding price changes, volume traded expressed in terms of number of Bitcoins exchanged, BTC value in United States Dollars (USD) and number of consecutive 1-minute bins with zero returns are charted in Fig. 1. During the early trading phase, frequent and extended time intervals with no price change, on the order of min, are observed, and plausibly reflect the absence of any transactions. Contrariwise, the most recent data at the time of writing indicate that BTC volume traded expressed in USD is suddenly entering a new regime, characterized by an average increase of about one order of magnitude.

II.1 Distribution of return fluctuations

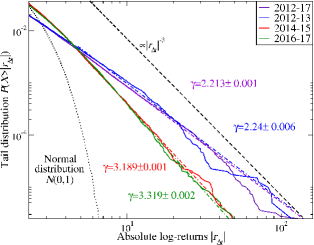

It is a well-established fact that, in contemporary mature markets (stock, commodities, Forex), the distribution of return fluctuations on relatively short time-lags follows to a good approximation an inverse cubic power-law gopi1998 ; gopi1999 ; kwapien2012 , i.e. the large-event tails of the return distributions follow where denotes the normalized returns (, denote mean and standard deviation) and . Such law is understood to reflect positive correlations between large market’s movements and the trades of large participants gabaix2003 ; gabaix2006 ; rak2013 . In the case of the BTC, as shown in Fig. 2 for , such relationship unequivocally emerges insofar as the early trading phase, i.e. the first two years 2012-2013 in our dataset, is excluded. In these two years, develops significantly heavier power-law tails having . It is noteworthy that these two years dominate the tail thickness, since remains essentially unchanged when the entire 2012-2017 period is taken into account. The tail thickness approaches the inverse cubic power-law when either of the two more recent biennia is considered: for years 2014-2015 is observed, and similarly for years 2016-2017 is observed. These values are very close, for example, to those observed over the period from Jan 2, 2018 to Mar 30, 2018, for the rates EUR/USD, GBP/USD and GBP/JPY, for which respectively , and .

II.2 Volatility autocorrelation

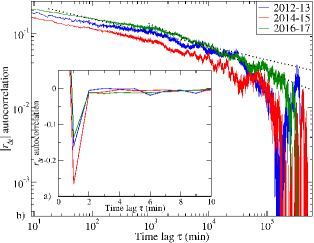

When applied to returns series in the existing markets, the autocorrelation function , where denotes average over , knowingly drops to zero almost immediately kwapien2012 , reflecting a very quick disappearance of correlations in the signs of returns. As shown in Fig. 3a, the same applies to the BTC market, which even develops a “correlation hole”, i.e. drops below zero. Such effect can also be seen in other currencies xu2003 ; drozdz2010 as well as in the stock markets fama1965 ; palagyi1999 , revealing the tendency for returns to change sign between adjacent time-steps.

On the other hand, as visible in Fig. 3b the autocorrelation of unsigned returns, , that is, of volatility, develops long-range, power law-like correlations which extend over an interval on the order of minutes, i.e. two months. This phenomenon originates from the so-called volatility clustering typical of other financial markets, and the sudden fall of for at time horizons beyond minutes reflects the average time-span of the underlying volatility clusters drozdz2009 . Attention needs to be drawn to the fact that autocorrelation is strongest and most persistent during the most recent trading period under consideration, i.e. years 2016-2017. As volatility is a nonlinear (i.e., modulus as here) function of returns, the volatility autocorrelation encodes correlations that are nonlinear in time from the perspective of returns.

III Nonlinear temporal correlations

At present, the most efficient and accurate methods to study diverse temporal correlations, including nonlinear and multifractal correlations calvet2002 , in single time-series as well as among multiple time-series, are based on inspecting the scaling properties of the varying-order moments of fluctuations, evaluated after appropriate detrending. The most general of these methods, termed Multifractal Cross-Correlation Analysis (MFCCA), consists of the steps described below kantelhardt2002 ; podobnik2008 ; zhou2008 ; oswiecimka2014 .

III.1 Methods based on detrending

Given two time-series , where , the signal profile is separately calculated for each of them according to

| (1) |

where denotes averaging over the entire time-series. These signal profiles are subsequently split into disjoint segments of length starting both from the beginning and the end of the profile, where and where in each segment , the assumed trend is estimated by fitting a polynomial of order , namely for and for . In typical cases, provides an optimal choice oswiecimka2006 . By subtracting this trend from the series, the detrended cross-covariance within each segment is obtained

| (2) |

which can in turn to be used to define the th-order covariance function oswiecimka2014

| (3) |

where denotes the sign of . Fractal cross-dependencies between given time-series and then manifest themselves in scaling relations of the form

| (4) |

where and is the corresponding scaling exponent, whose dependence on reflects a richer, multifractal character of correlations in the time-series as compared to the monofractal case, for which is -independent.

The conventional MFDFA procedure kantelhardt2002 of calculating the singularity spectra for single time-series is a special case of the above MFCCA procedure, wherein . The Eq. (3) then reduces to

| (5) |

and, as in Eq. (4), multifractality and monofractality are reflected in

| (6) |

where denotes the generalized Hurst exponent, and is its ordinary case. The singularity spectrum , also referred to as the multifractal spectrum, can thereafter be computed from the following relations

| (7) |

where denotes the Hölder exponent characterizing the singularity strength, and reflects the fractal dimension of support of the set of data points whose Hölder exponent equals .

In the case of multifractals, the shape of the singularity spectrum typically resembles an inverted parabola; furthermore, the degree of complexity is straightforwardly quantified by the width of , simply defined as , where and correspond to the opposite ends of the values as projected out by different -moments (Eq. (5)). Another important feature of is its asymmetry (skewness), which can be quantified by the asymmetry index drozdz2015 where and , and corresponds to the maximum on the spectrum. Positive and negative values of reflect, respectively, left- and right-sided asymmetry of , which correspond to more developed multifractality on the level of large or small fluctuations in the time-series.

Lastly, a family of the fluctuation functions defined by Eq. (3) can also be used to introduce a -dependent detrended cross-correlation (DCCA) kwapien2015 coefficient

| (8) |

which allows quantifying the degree of cross-correlation between two time-series and after detrending, over varying time-scales and, by varying the parameter , identifying the range of detrended fluctuation amplitudes which are most strongly correlated between the two signals kwapien2015 ; kwapien2017 .

III.2 Hurst exponent

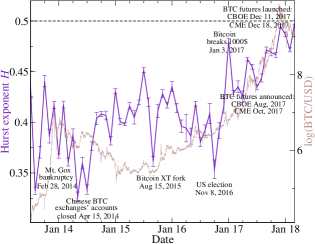

One of the principal statistical properties of time-series is the Hurst exponent, which quantifies the degree of persistence and as such has particular relevance in the context of financial time-series ausloos2000 . Here, the Hurst exponent was estimated as following the procedure prescribed by Eqs. (5) and (6) over 1-month time windows, each one comprising data points, limiting estimation error, and starting from Jul 2013; earlier windows contain excessive consecutive zero returns, which bias the procedure unacceptably. As charted in Fig. 4, during the early trading period the Hurst exponent for the BTC/USD price takes values , hallmarking the strong anti-persistence which is expected for such high-risk emerging market; it thereafter gradually approaches 0.5 from below, recently becoming very close to this value, which is interpreted as a strong indication that the market is approaching maturity matteo2003 . By comparison, over the period from Jan 2, 2018 to Mar 30, 2018, for the rates EUR/USD, GBP/USD and GBP/JPY, one observes respectively , and . It is noteworthy that, during the maturation process, the Hurst exponent of the BTC dropped sharply as a consequence of events apparently causing uncertainty, in particular the bankruptcy of the Mt. Gox Bitcoin exchange, following it the closure of the Chinese BTC exchange accounts accompanied by related regulatory changes kristoufek2015 , and finally a fork in the Bitcoin software and the 2016 United States presidential elections. On the other hand, events which appear to be correlated positively with the maturation process include the successful breaking of a psychological USD barrier in early 2017, followed by the announcement and subsequently launch of BTC future contracts in fall of that year.

III.3 Multiscaling

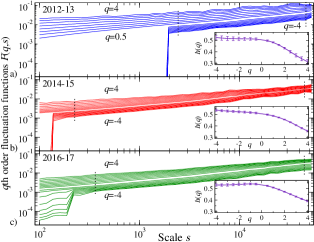

The formalism presented in Section III.A allows studying even more subtle quantitative characteristics related to the nonlinear correlations in time-series, which are encoded in the scale-dependence of the fluctuation functions . These function are shown, separately for the BTC return time-series in each of the three two-year time periods and given , in Fig. 5. From the earliest through the most recent trading period, the quality of scaling systematically improves, and the range of scales over which scaling-like behavior of is observed extends. The -dependence of the corresponding generalized Hurst exponents estimated from the chosen scaling range for each trading period, denoted by the dashed vertical lines, is shown in the corresponding panels within Fig. 5.

The most relevant behavior of the fluctuation functions pertains to the negative values of , which filter out the small fluctuations. As shown in Fig. 5a, due to number of consecutive 1-minute bins with zero returns in the earliest trading biennium (years 2012-2013) the fluctuation functions even become singular up to the scales . Only after that point scaling becomes detectable, but the corresponding function shows essentially no -dependence. In the intermediate biennium (years 2014-2015), the singularity regime shrinks by about one order of magnitude, and in the most recent biennium (years 2016-2017), it largely disappears, with only some residual distortions originating from trading around the time of the US presidential election. Nevertheless, multifractal scaling does not emerge, even in the regime of satisfactory scaling.

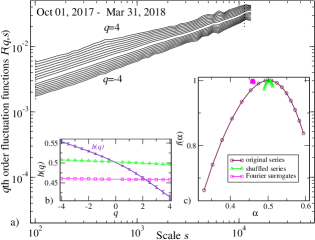

In striking contrast, fully developed multifractality can be readily appreciated for the most recent semester, i.e. Oct 1, 2017 to Mar 31, 2018. The corresponding fluctuation functions and the resulting multifractal spectrum are shown in Fig. 6 (circles). In all respects, these results resemble remarkably closely those obtained for mature markets kwapien2012 , and in particular for the Forex drozdz2010 . Namely, the scaling regime comprises the whole span of scales considered before, and multifractality is convincingly reflected both in the -dependence of and in the singularity spectrum , which has a somewhat left-sided asymmetry (). The latter is almost universally characteristic of mature markets, and can be explained by the fact that small price changes, as filtered out by the negative -values, are by their nature more noisy and their hierarchical organization is poorer drozdz2015 . Importantly, all these multiscaling effects, as it is also shown in Fig. 6, completely disappear on surrogate time-series schreiber2000 , obtained from the original BTC return time-series by shuffling (squares), or by Fourier phase randomization (triangles). Since the latter preserves the linear correlations, the location of the corresponding reflects the average Hurst exponent characteristic to the period considered. In the randomly shuffled series all correlations are removed, and consequently is centered exactly at 0.5. The non-zero width seen in in this case is an artifact of the finite length of the time-series considered, and is a known effect drozdz2009 for the uncorrelated fat-tailed series.

III.4 Volatility vs. volume traded

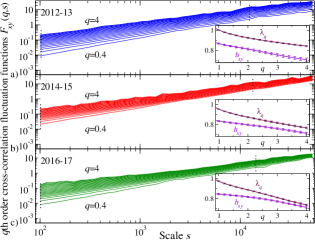

Large fluctuations in mature markets are typically characterized by cross-correlations, even multifractal ones, between volatility and the volume traded rak2015 . Within a novel, more advanced approach which is able to detect the degree of synchrony between the two multifractal time-series and , the corresponding measures are quantified in terms of the cross-correlation fluctuation functions of Eq. (4) oswiecimka2014 . When these functions develop scaling, the corresponding scaling exponent can be determined. Their closeness as regards the average generalized Hurst exponents reflects the degree of cross-correlation. Maximal multifractal synchrony corresponds to oswiecimka2014 . The development of such cross-correlations between the volume traded and volatility for the BTC market is shown, for each biennium, in Fig. 7. The cross-correlation is identified and reaches maximum synchrony during the most recent period, at large fluctuations ( between 3 and 4). For , which probes smaller fluctuations, the functions in the present case fluctuate between positive and negative values, thus exhibit no scaling and therefore are not shown in Fig. 7. This indicates the entire disappearance of cross-correlations on the level of smaller fluctuations. Notably, no such cross-correlation effects, nor even trace of scaling in for any -value, is observed when volatility is replaced by returns.

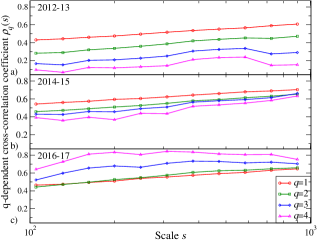

A complementary view on this aspect of the BTC market is offered by the coefficient (Eq. (8)). The result of its application to the present BTC volume traded and volatility time-series is shown in Fig. 8 for time-scales between and min. While in the first biennium the correlations are relatively weak, especially on the level of large fluctuations (), they gradually become much stronger, and in the most recent period the situation becomes opposite, as the large fluctuation cross-correlations dominate.

In view of the theoretical concepts supporting the validity of the inverse cubic power-law, demonstrated for the BTC in Section II A, and based on correlations between the large market’s movements and the trades of large participants gabaix2003 ; gabaix2006 , these observations provide further arguments for the onset of maturity characteristics in the BTC market.

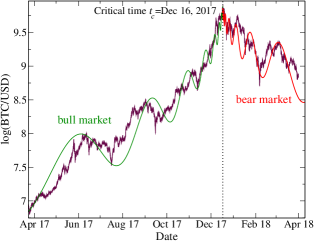

III.5 Log-periodic Bitcoin price patterns

As shown in Fig. 9, mid-way through the most recent trading semester, namely on Dec 16, 2017, the Bitcoin (BTC) market experienced a spectacular trend reversal, from strongly increasing to sharply decreasing, both large trends being accompanied by well-evident, smaller-scale oscillations. Such phenomena are a well-known product of the dynamics of mature financial markets, and unavoidably emerge in all of them, including stock exchange, commodities, Forex and even the bond markets sornette2002 ; drozdz2003 ; kwapien2012 . They are, in fact, analogous to critical phenomena which accompany second-order phase transitions in other physical systems, and closely related to scale invariance. In this case, the scale invariance is however not continuous, but discrete, with a preferred scaling factor , which overlapped to the -shaped ordinary phase transition introduces log-periodic oscillations. These accumulate exactly at the critical time which indicates, in the financial context, the instant of trend reversal.

One of the simplest suitable parameterizations for the temporal evolution of price is

| (9) |

for the bubble (increasing) phase, where /. The anti-bubble (decreasing) phase corresponds to changing sign of . There is some empirical evidence that in contemporary financial markets is common, possibly universal drozdz2003 ; bartolozzi2005 . Assuming therefore , and adjusting the remaining parameters in Eq. (9), one obtains the fits shown in Fig. 9, for corresponding to Dec 16, 2017. These reproduce remarkably well the observed oscillatory patterns, providing additional evidence that the BTC market may have entered a phase of maturity. Activity prior to Apr 2017 was not considered, because the market was not yet mature prior to that point, as indicated by all other markers e.g. , and as such was not expected to obey a log-periodic relationship.

IV Commentary

The disruptiveness of cryptocurrencies, in particular of the Bitcoin (BTC), is well-evident in the striking, possibly unprecedented, rapidity of market capitalization. Around the end of year 2017, namely approximately 8 years after the “Bitcoin Pizza Day” which celebrated the time at which 10,000 BTC were worth approximately two pizzas, the same number of BTCs was valued around 20 million USD. At present, the cryptocurrency market as a whole exceeds, in both transaction volume and capitalization, many traditional and well-established financial markets.

The present study shows a perhaps more subtle, but not less impacting fact: that, in spite of its virtual nature and novelty, the Bitcoin market has recently and rapidly developed the statistical hallmarks which are empirically observed for all “mature” markets like stocks, commodities or Forex. It appears plausible that other cryptocurrencies will follow the same trajectory. This may lead to the emergence of a completely new market, analogous to the the global foreign exchange (Forex) market, wherein cryptocurrencies could hypothetically be traded even in a self-contained manner. In the authors’ view, the substantial implications of such prospect for market stability and regulation motivate very urgent research.

The Bitcoin phenomenon is also unique in that, given the availability of high-frequency trading data since its inception and the rapidity of evolution (and capitalization), it provides new windows for exploring rigorously the trajectory towards maturity of a currency market. This will in particular motivate further investigations of the entire cryptocurrency market.

References

- (1) C. Menger, On the origin of money, Economic Journal 2, 239–255 (June 1892).

- (2) P. Bak, S.F. Nørrelykke, and M. Shubik, Money and Goldstone modes, Quantitatve Finance 1, 186-190 (2001).

- (3) C. Lapavitsas, The Emergence of Money in Commodity Exchange, or Money as Monopolist of the Ability to Buy, Review of Political Economy 17, 549-569 (2005).

- (4) S. Ghashghaie, W. Breymann, J. Peinke, P. Talkner, and Y. Dodge, Turbulent cascades in foreign exchange markets, Nature 381, 767-770 (1996).

- (5) S. Drożdż, J. Kwapień, P. Oświȩcimka, and R. Rak, The foreign exchange market: return distributions, multifractality, anomalous multifractality and the Epps effect, New Journal of Physics 12, 105003 (2010).

- (6) J. Kwapień and S. Drożdż, Physical approach to complex systems, Physics Reports 515, 115–226 (2012).

- (7) A. Yasutomi, The emergence and collapse of money, Physica D 82, 180–194 (1995).

- (8) A. Yasutomi, Itinerancy of money, Chaos 13, 1148–1164 (2003).

- (9) E Samanidou, E Zschischang, D Stauffer, and T Lux, Agent-based models of financial markets, Reports on Progress in Physics 70, 409–450 (2007).

- (10) A. Z. Górski, S. Drożdż, and P. Oświȩcimka, Modelling emergence of money, Acta Physica Polonica A 117, 676–680 (2010).

- (11) P. Oświȩcimka, S. Drożdż, R. Gȩbarowski, A. Z. Górski, and J. Kwapień, Multiscaling edge effects in an agent–based money emergence model, Acta Physica Polonica B 46, 1579–1592 (2015).

- (12) A. Berentsen and F. Schär, A Short Introduction to the World of Cryptocurrencies, Federal Reserve Bank of St. Louis Review, 100(1), 1-16 (First Quarter 2018). https://doi.org/10.20955/r.2018.1-16

- (13) L. Kristoufek, BitCoin meets Google Trends and Wikipedia: Quantifying the relationship between phenomena of the Internet era, Scientific Reports 3, 3415 (2013).

- (14) J. Kertesz, I. Kondor (Eds.), Econophysics: An emerging Science, (Kluwer Academic Publishers, Dordrecht, Netherlands, 1998).

- (15) R. Cont, Empirical properties of asset returns: stylized facts and statistical issues, Quantitative Finance 1, 223-236 (2001).

- (16) B. Zheng, X.-F. Jiang, and P.-Y. Ni, A mini-review on econophysics: Comparative study of Chinese and western financial markets, Chinese Physics B 23, 078903 (2014).

- (17) T. Lux, The stable Paretian hypothesis and the frequency of large returns: an examination of major German stocks, Applied Financial Economics 6, 463-475 (1996).

- (18) M.M. Dacorogna, R. Gencay, U.A. Muller, R. Olsen, O.V. Pictet, An Introduction to High-Frequency Finance, (Academic Press, New York, USA, 2001).

- (19) P. Gopikrishnan, M. Meyer, L.A.N. Amaral, and H.E. Stanley, Inverse cubic law for the probability distribution of stock price variations, European Physical Journal B 3, 139-140 (Rapid Note) (1998).

- (20) P. Gopikrishnan, V. Plerou, L.A.N. Amaral, M. Meyer, and H.E. Stanley, Scaling of the distribution of fluctuations of financial market indices, Physical Review E 60, 5305-5316 (1999).

- (21) X. Gabaix, P. Gopikrishnan, V. Plerou, and H.E. Stanley, A theory of power-law distributions in financial market fluctuations, Nature 423, 267-270 (2003).

- (22) E. Fama, The Behavior of Stock-Market Prices, The Journal of Business 38, 34-105 (1965).

- (23) R.N. Mantegna and H.E. Stanley, An Introduction to Econophysics: Correlations and Complexity in Finance, (Cambridge University Press, Cambridge, UK, 2000).

- (24) D. Grech and Z. Mazur, Can one make any crash prediction in finance using the local Hurst exponent idea?, Physica A 336, 133-145 (2004).

- (25) T. Di Matteo, T. Aste, and M.M. Dacorogna, Long-term memories of developed and emerging markets: Using the scaling analysis to characterize their stage of development, Journal of Banking & Finance 29, 827-851 (2005).

- (26) D.O. Cajueiro and B.M. Tabak, Testing for predictability in equity returns for European transition markets, Economic Systems 30, 56-78 (2006).

- (27) B.M. Tabak and D.O. Cajueiro, Assessing inefficiency in euro bilateral exchange rates, Physica A 367, 319-327 (2006).

- (28) T.C. Halsey, M.H. Jensen, L.P. Kadanoff, I. Procaccia, and B.I. Shraiman, Fractal measures and their singularities - The characterization of strange sets, Physical Review A 33, 1141-1151 (1986).

- (29) P. Oświȩcimka, J. Kwapień, and S. Drożdż, Multifractality in the stock market: price increments versus waiting times, Physica A 347, 626-638 (2005).

- (30) G. Oh, C. Eom, S. Havlin, W.-S. Jung, F. Wang, H.E. Stanley, and S. Kim, A multifractal analysis of Asian foreign exchange markets, European Physical Journal B 85, 214 (2012).

- (31) S.J.H. Shahzad, S.M. Nor, W. Mensi, and R.R. Kumar, Examining the efficiency and interdependence of US credit and stock markets through MF-DFA and MF-DXA approaches, Physica A 471, 351-363 (2017).

- (32) L. Calvet and A. Fisher, Multifractality in asset returns: theory and evidence, The Review of Economics and Statistics 84, 381-406 (2002).

- (33) Data source: http://api.bitcoincharts.com/v1/csv/

- (34) X. Gabaix, P. Gopikrishnan, V. Plerou, and H.E. Stanley, Institutional investors and stock market volatility, The Quarterly Journal of Economics 121 (2), 461-504 (2006).

- (35) R. Rak, S. Drożdż, J. Kwapień, and P. Oświȩcimka, Stock returns versus trading volume: is the correspondence more general?, Acta Physica Polonica B 44, 2035-2050 (2013).

- (36) Z. Xu and R. Gencay, Scaling, self-similarity and multifractality in FX markets, Physica A 323, 578-590 (2003).

- (37) Z. Palagyi and R.N. Mantegna, Empirical investigation of stock price dynamics in an emerging market, Physica A 269, 132-139 (1999).

- (38) S. Drożdż, J. Kwapień, P. Oświȩcimka, and R. Rak, Quantitative features of multifractal subtleties in time-series, EPL (Europhysics Letters) 88, 60003 (2009).

- (39) J.W. Kantelhardt, S.A. Zschiegner, E. Koscielny-Bunde, S. Havlin, A. Bunde, and H.E. Stanley, Multifractal detrended fluctuation analysis of nonstationary time-series, Physica A 316, 87-114 (2002).

- (40) B. Podobnik and H.E. Stanley, Detrended cross-correlation analysis: a new method for analyzing two nonstationary time-series, Physical Review Letters 100, 084102 (2008).

- (41) W.-X. Zhou, Multifractal detrended cross-correlation analysis for two nonstationary signals, Physical Review E 77, 066211 (2008).

- (42) P. Oświȩcimka, S. Drożdż, M. Forczek, S. Jadach, and J. Kwapień, Detrended cross-correlation analysis consistently extended to multifractality, Physical Review E 89, 023305 (2014).

- (43) P. Oświȩcimka, J. Kwapień, and S. Drożdż, Wavelet versus detrended fluctuation analysis of multifractal structures, Physical Review E 74, 016103 (2006).

- (44) S. Drożdż and P. Oświȩcimka, Detecting and interpreting distortions in hierarchical organization of complex time-series, Physical Review E 91, 030902(R) (2015).

- (45) J. Kwapień, P. Oświȩcimka ,and S. Drożdż, Detrended fluctuation analysis made flexible to detect range of cross-correlated fluctuations, Physical Review E 92, 052815 (2015).

- (46) J. Kwapień, P. Oświȩcimka, M. Forczek, and S. Drożdż, Minimum spanning tree filtering of correlations for varying time scales and size of fluctuations, Physical Review E 95, 052313 (2017).

- (47) M. Ausloos, Statistical physics in foreign exchange currency and stock markets, Physica A 285, 48-65 (2000).

- (48) T. Di Matteo, T. Aste, and M.M. Dacorogna, Scaling behaviors in differently developed markets, Physica A 324, 183–188 (2003).

- (49) L. Kristoufek, What are the main drivers of the Bitcoin price? Evidence from wavelet coherence analysis, PLoS ONE 10(4), e0123923 (2015).

- (50) T. Schreiber and A. Schmitz, Surrogate times series, Physica D 142, 346–382 (2000).

- (51) R. Rak, S. Drożdż, J. Kwapień, and P. Oświȩcimka, Detrended cross-correlations between returns, volatility, trading activity, and volume traded for the stock market companies, EPL (Europhysics Letters) 112, 48001 (2015).

- (52) D. Sornette, Why Stock Markets Crash: Critical Events in Complex Financial Systems, (Princeton University Press, Princeton, USA, 2002).

- (53) S. Drożdż, F. Grümmer, F. Ruf, and J. Speth, Log-periodic self-similarity: an emerging financial law?, PhysicaA 324, 174–182 (2003).

- (54) M. Bartolozzi, S. Drożdż, D.B. Leinweber, J. Speth, A.W. Thomas, Self-similar log-periodic structures in Western Stock Markets from 2000, International Journal of Modern Physics C 16, 1347–1361 (2005).