Limits of multiplicative inhomogeneous random graphs and Lévy trees: The continuum graphs

Abstract

Motivated by limits of critical inhomogeneous random graphs, we construct a family of sequences of measured metric spaces that we call continuous multiplicative graphs, that are expected to be the universal limit of graphs related to the multiplicative coalescent (the Erdős–Rényi random graph, more generally the so-called rank-one inhomogeneous random graphs of various types, and the configuration model). At the discrete level, the construction relies on a new point of view on (discrete) inhomogeneous random graphs that involves an embedding into a Galton–Watson forest. The new representation allows us to demonstrate that a processus that was already present in the pionnering work of Aldous [Ann. Probab., vol. 25, pp. 812–854, 1997] and Aldous and Limic [Electron. J. Probab., vol. 3, pp. 1–59, 1998] about the multiplicative coalescent actually also (essentially) encodes the limiting metric: The discrete embedding of random graphs into a Galton–Watson forest is paralleled by an embedding of the encoding process into a Lévy process which is crucial in proving the very existence of the local time functionals on which the metric is based; it also yields a transparent approach to compactness and fractal dimensions of the continuous objects. In a companion paper, we show that the continuous Lévy graphs are indeed the scaling limit of inhomogeneous random graphs.

1 Introduction

Motivation and results. In this paper, we construct a family of sequences of measured metric spaces that we call continuous multiplicative graphs. A companion paper [9] is dedicated to showing that these objects are indeed the scaling limits of critical (rank-one) inhomogeneous random graphs. More generally, continuous multiplicative graphs are expected to be the scaling limits of all of models of graphs that are related to the multiplicative coalescent [2, 3] which includes the classical Erdős–Rényi random graphs (as a special case of rank-one inhomogeneous random graphs) and the configuration model.

The (metric space) scaling limits for critical random graphs have been constructed and limit theorems have been proved for a number of models. At level of discrete objects, the general strategy consists in designing a suitable exploration of the graphs that yields a decomposition into a random function describing a spanning forest, together with relatively few additional “decorations” indicating where to add additional edges in order to obtain the graph. By “suitable”, we mean that the random function should both encode the metric relatively transparently, and be tractable when the time comes to taking limits. So, the random function should take advantage of the independence underlying the random graph construction, and for example should whenever possible remain close to some kind of random walk. Except in very specific cases, this constraint implies that the metric of the spanning forest cannot be a very simple functional of the random function. The natural representations, which go back to the treatment of scaling limits, encode the metric as a (discrete) local-time functional of the random function.

For a general class of random graphs related to the multiplicative coalescent, Aldous [2] and Aldous & Limic [3] have devised natural explorations that are suitable for taking limits, and that allowed them to study the scaling limits of the sequence of sizes of the connected components111to be precise, [3] deals with “masses” for a suitable measure on the vertices that is not the counting measure.. However, it remains so far unclear how to deal with the metric structure from that approach for two reasons. First, the exploration does not directly yield a nice connection with the metric. Sometimes, a slight modification of the exploration gives access to the metric without changing the law of the random function; this is for instance the case for the Erdős–Rényi random graphs: the breadth-first exploration used by Aldous is not convenient for the analysis of the metric, but the depth-first version used in [1] has the same law. One could envision that such a slight modification of the general exploration of Aldous & Limic, say from a breadth-first to a depth-first approach, would both give a handle on the metric and leave the processes unchanged in distribution (and thus suitable for taking limits). However, in general, the processes in [3] are only semi-martingales for which the relevant continuum local-time functionals are now known to exist.

The present paper addresses the issues of the previous paragraph. At the discrete level of finite graphs, we choose a very specific model that is most convenient for the construction of the limit objects. The graphs that we consider are not oriented, without either loops or multiple edges: is therefore a set consisting of unordered pairs of distinct vertices. Let and let be a set of vertex weights: namely, it is a set of positive real numbers such that . For all , we let . Then, the random graph is said to be -multiplicative if and if the random variables , are independent and for each we have

We call this graph multiplicative because as observed by Aldous, its connected components provide a natural representation of the multiplicative coalescent: see Aldous [2] and Aldous & Limic [3] for more details.

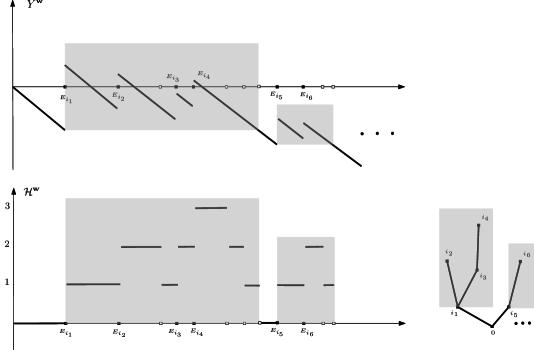

The first result of the paper (Theorem 2.1) shows that is coded by a natural depth-first exploration process that gives access to the metric and that is explained in terms of the following queueing system: a single server serves at most one client at a time applying the Last In First Out policy (LIFO, for short); exactly clients will enter the queue and each client is labelled with a distinct integer of ; Client enters the queue at a time and requires a time of service ; we assume that the are independent and exponentially distributed r.v. such that . The LIFO-queue yields the following tree whose vertices are the clients: the server is the root (Client ) and Client is a child of Client in if and only if Client interrupts the service of Client (or arrives when the server is idle if ). We claim that the subtrees of that stem from the root are spanning trees of the connected components of (and thus, captures a large part of the metric of ). If one introduces

then, is the load of the server (i.e. the amount of service due at time ) and is the number of clients waiting in the queue at time (see Figure 1). The process is a contour (or a depth-first exploration) of and codes its graph-metric: namely, the distance between the vertices/clients served at times and in is . We obtain by adding to a set of surplus edges that is derived from a Poisson point process on of intensity as follows: an atom of this Poisson point process corresponds to the surplus edge , where is the client served at time and is the client served at time . Then, Theorem 2.1 asserts that the resulting graph is a -multiplicative graph.

In order to define the scaling limits of the previous processes and of -multiplicative graphs, the second main idea of the paper consists in embedding into a Galton-Watson tree by actually embedding the queue governed by into a Markovian queue that is defined as follows: a single server receives in total an infinite number of clients; it applies the LIFO policy; clients arrive at unit rate; each client has a type that is an integer ranging in ; the amount of service required by a client of type is ; types are i.i.d. with law . If and stand for resp. the arrival-time and the type of the -th client, then, the Markovian LIFO queueing system is entirely characterised by that is a Poisson point measure on with intensity , where stands for the Lebesgue measure on . The Markovian queue yields a tree that is defined as follows: the server is the root of and the -th client to enter the queue is a child of the -th one if the -th client enters when the -th client is being served. To simplify our explanations, let us focus here on the (sub)critical cases where . Then, is a sequence of i.i.d. Galton–Watson trees glued at their root and whose offspring distribution is , , that is (sub)critical. The tree is then coded by its contour process : namely, stands for the number of clients waiting in the Markovian queue at time and it is given by

| (1) |

is the (algebraic) load of the Markovian server: namely is the amount of service due at time . Note that is a compound Poisson process and let us mention that the possible scaling limits of are well-understood.

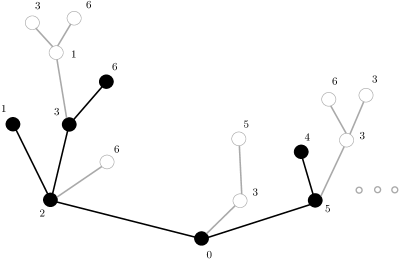

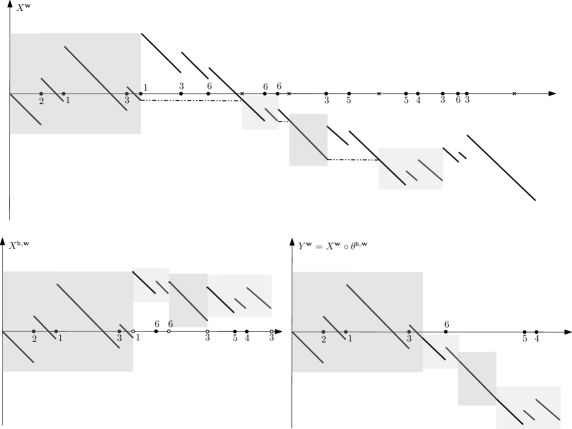

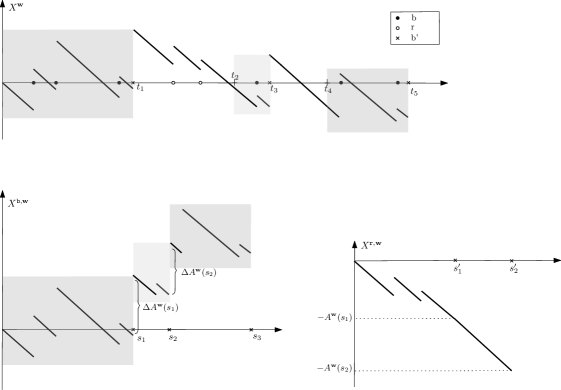

The queue governed by is then obtained by pruning clients from the Markovian queue in the following way. We colour each client of the queue governed by in blue or in red according to the following rules: if the type of the -th client already appeared among the types of the blue clients who previously entered the Markovian queue, then the -th client is red; otherwise the -th client inherits her/his colour from the colour of the client who is currently served when she/he arrives (and this colour is blue if there is no client served when she/he arrives: namely, we consider that the server is blue): see Figure 2. We claim (see Proposition 2.2 and Lemma 2.3) that if we skip the periods of time during which red clients are served in the Markovian queue, we get the queue governed by that can be therefore viewed as the blue sub-queue. Namely, if is the set of times when a blue client is served, then one sets and the above mentioned embedding is formally given by the fact that a.s. for all , (see Figure 3).

As proved in a companion paper [9], the only possible scaling limits of processes like that are relevant for our purpose are the processes already introduced in Aldous & Limic [3]. These processes are parametrized by , where , , and satisfies , and , and they are informally defined by

| (2) |

Here, is a standard linear Brownian motion, the are exponentially distributed with parameter and and the are independent (see (36) and Remark 2.2 for more details). To define the analogue of , we proceed in an indirect way that relies on a continuous version of the embedding of into a Markov process. More precisely, the scaling limits of are Lévy processes without negative jump, whose law is characterized by their Laplace exponent of the form

To simplify the explanation we focus in this introduction on the (sub)critical cases where . As proved in Le Gall & Le Jan [15] and Le Gall & D. [10], if , then there exists a continuous process such that for all , the following limit holds in probability:

that is a local time version of (28). We refer to as to the height process of and is the continuous analogue of . The third main result of the paper (Theorem 2.5 and Theorem 2.6) asserts that, as in the discrete setting, there exists a time-change, namely an increasing positive process and a continuous process that is adapted with respect to and such that a.s. for all , .

Then continuous versions of multiplicative graphs are obtained as in the discrete setting: we first define , the random continuum tree coded by , namely correspond to points in that are at distance and to obtain the -continuum multiplicative graph , we identify points in thanks to a Poisson point process on with intensity as in the discrete setting: we refer to Sections 2.2.2 and 2.2.3 for a precise definition. Specifically, our construction shows that can be embedded into the tree coded by , namely a -Lévy tree. It yields a transparent approach to the main geometric properties of : an explicit condition for compactnes and the fact that Hausdorff and packing dimensions of and -Lévy trees are the same, as shown in Proposition 2.7. Let us mention that, as shown in the companion paper [9], the -continuum multiplicative graphs introduced in this paper are the scaling limits of -multiplicative subgraphs.

Background and related work. Let us make briefly the connection with previous articles.

Entrance boundary of the multiplicative coalescent. The work [3] of Aldous and Limic already revealed a deep connection between as in (2) and the multiplicative coalescent processes. This work also suggests that the family of continuous multiplicative graphs we construct indeed contains all the possible limits of random graphs related to the multiplicative coalescent. To be precise, a stochastic process is considered in [3]. Its law is characterised by three parameters: , and . This is actually a rescaled version of the -process defined in (2), simply because

| (3) |

Then Aldous and Limic show (Theorem 2 & Theorem 3 in [3]) that there is a one-to-one correspondence between the laws of the excursion lengths of and the marginals of the extremal eternal versions of the multiplicative coalescent. This connection origins from a representation of the (finite-state) coalescent process in terms of the graph, first observed in Aldous [2]. The work [2] and [3] is the primary motivation for us to consider these particular classes of random graphs and part of their results (in particular the convergence of the excursion lengths) have figured in our proof of the limit theorems in [9]. See Section 2.3.4 in [9] for more details.

Graph limits as instances of continuous multiplicative graphs. As important examples of the family of -multiplicative graphs, let us mention that

-

–

in the scaling limit of the Erdős–Rényi graphs we find a continuous multiplicative graph with , and . This result is due to Addario-Berry, Goldschmidt & B. [1]. Let us also mention that as shown by Bhamidi, Sen & X. Wang in [6], the same limit object appears in the -multiplicative graphs which are in the basin of attraction of the Erdős–Rényi graph.

-

–

in the scaling limit of the multiplicative graphs with power-law weights, we find continuous multiplicative graphs parametrised by , , and , for all . This result is due to Bhamidi, van der Hofstad & Sen [7]. Let us also mention that Conjecture 1.3 right after Theorem 1.2 in [7] is solved by our Proposition 2.7 that asserts the following: if , , and , then (which corresponds to in [7]) and

where and stand respectively for the Hausdorff and for the packing dimensions.

Plan of the paper. The paper is organized as follows. Section 2 is dedicated to a detailed exposition of the setting and results: we start with a motivation using the setting of discrete objects, and move towards the continuum objects. The proofs in the discrete setting, namely of the main respresentation theorem and of the embedding of multiplicative graphs into a Galton–Watson forest are found in Sections 3 and 4. In Section 5, we give the proofs concerning the continuum objects together with the relevant background on Lévy trees: here, this is mainly about proving the continuum analog of the embedding into a forest. Finally, Appendix A contains auxiliary results used to deal with the fractal dimensions.

2 Exposition of the main results

2.1 Exploration of discrete multiplicative random graphs

We briefly describe the model of discrete random graphs that are considered in this paper and we discuss a combinatorial construction thanks to a LIFO-queue. Unless the contrary is specified, all the random variables that we consider are defined on the same probability space . The graphs that we consider are not oriented, without either loops or multiple edges: is therefore a set consisting of unordered pairs of distinct vertices.

Let and let be a set of weights: namely, it is a set of positive real numbers such that . We shall use the following notation.

| (4) |

The random graph is said to be -multiplicative if and if

| (5) |

In the entire article, for a stochastic process we use interchangeably and depending on which is more convenient or readable.

2.1.1 A LIFO queueing system exploring multiplicative graphs.

Let us first explain how to generate a -multiplicative graph thanks to the queueing system that is described as follows: there is a single server; at most one client is served at a time; the server applies the Last In First Out policy (LIFO, for short). Namely, when a client enters the queue, she/he interrupts the service of the previously served client (if any) and the new client is immediately served. When the server completes the service of a client, it comes back to the last arrived client whose service has been interrupted (if there is any). Exactly clients will enter the queue; each client is labelled with a distinct integer of and stands for the total amount of time of service that is needed by Client who enters the queue at a time denoted by ; we refer to as the time of arrival of Client ; we assume that are distinct. For the sake of convenience, we label the server by and we set . The single-server LIFO queueing system is completely determined by the (always deterministic) times of service and the times of arrival , that are random variables whose laws are specified below. We introduce the following processes:

| (6) |

The load at time (namely the time of service still due by time ) is then . We shall sometimes call the algebraic load of the queue. The LIFO queue policy implies that Client arriving at time will leave the queue at time , namely the first moment when the service load falls back to the level right before her/his arrival. We shall refer to the previous queueing system as the -LIFO queueing system.

The exploration tree. Denote by the label of the client who is served at time if there is one; namely, if the server is idle right after time , we set (see Section 3 for a formal definition). First observe that and that is càdlàg. By convenience, we set . Next note that and that is the label of the client who was served when Client entered the queue. Then, the -LIFO queueing system induces an exploration tree with vertex set and edge set that are defined as follows:

| (7) |

The tree is rooted at , which allows to view it as a family tree: the ancestor is (the server) and Client is a child of Client if Client enters the queue while Client is served. In particular, the ancestors of Client are those waiting in queue while is being served. See Figure 1 for an example.

Additional edges. We obtain a graph by adding edges to as follows. Conditionally given , let

| (8) |

Note that a.s. the number of atoms is finite since is null eventually. We set:

| (9) |

Note that is well-defined since . We then derive from and by setting: and , where

| (10) |

Note that is necessarily an ancestor of ; in other words, is in the queue at time . Moreover, we have a.s, since . It follows that the endpoints of an edge belonging to necessarily belong to the same connected component of . Note that is not a vertex of ; we call the set of surplus edges. When is suitably distributed, is distributed as a -multiplicative graph: this is the content of the following theorem that is the key to our approach.

Theorem 2.1

Keep the previous notation; suppose that are independent exponential r.v. such that , for all . Then, is a -multiplicative random graph as specified in (5).

Proof: see Section 3.

Height process of the exploration tree. For all , let be the number of clients waiting in the line at time . Recall that by the LIFO rule, a client entered at time is still in the queue at time if and only if . In terms of , is defined by

| (11) |

We refer to as the height process associated with . Note that is also the height of the vertex in the exploration tree . Actually, this process is a specific contour of the exploration tree and we easily check that it (a.s.) codes its graph-metric as follows:

| (12) |

See Figure 1 for more details.

The connected components of the -multiplicative graph. The above LIFO-queue construction of the -multiplicative graph has the following nice property: the vertex sets of the connected components of coincide with the vertex sets of the connected components of , since surplus edges from are only added inside the connected components of the latter. We equip with the measure that is the push-forward measure of the Lebesgue measure via the map restricted to the set of times . Denote by the number of connected components of that are denoted by , , ; here indexation is such that

Note that for all , corresponds to a connected component of such that

Let and be the respective graph-metrics of and of and denote by the restriction of to . Then, and completely encode the sequence of connected components viewed as measured metric spaces. Indeed, we will see that each excursion of above zero corresponds to a connected component of , the length of the excursion interval is and corresponds to pinching times that fall in this excursion interval. A formal description of this requires some preliminary work on the measured metric spaces and is therefore postponed to Section 2.2.2.

2.1.2 Embedding the exploration tree into a Galton–Watson tree

A Markovian LIFO queueing system. We embed the -LIFO queueing system governed by into the following Markovian LIFO queueing system:

-

A single server receives in total an infinite number of clients; it applies the LIFO policy; clients arrive at unit rate; each client has a type that is an integer ranging in ; the amount of service required by a client of type is ; types are i.i.d. with law .

Let be the arrival-time of the -th client and let be the type of the -th client. Then, the Markovian LIFO queueing system is entirely characterised by that is a Poisson point measure on with intensity , where stands for the Lebesgue measure on . We also introduce the following.

| (13) |

Then, is the load of the Markovian LIFO-queueing system and is called the algebraic load of the queue. Note that is a spectrally positive Lévy process with initial value whose law is characterized by its Laplace exponent given for all by:

| (14) |

Here, recall from (4) that . Note that if , then , a.s. and the queueing system is recurrent: all clients are served completely; if , then , a.s. and the queueing system is transient: the load tends to and infinitely many clients are not served completely. In what follows we shall refer to the following cases:

| (15) |

Colouring the clients of the Markovian queueing system. In critical or subcritical cases, we recover the -LIFO queueing system governed by from the Markovian one by colouring each client in the following recursive way.

-

Colouring rules. Clients are coloured in red or blue. If the type of the -th client already appeared among the types of the blue clients who previously entered the queue, then the -th client is red. Otherwise the -th client inherits her/his colour from the colour of the client who is currently served when she/he arrives (and this colour is blue if there is no client served when she/he arrives: namely, we consider that the server is blue).

Note that the colour of a client depends in an intricate way on the types of the clients who entered the queue previously. For instance, a client who is the first arriving of her/his type is not necessarily coloured in blue; see Figure 2 for an example. In critical or subcritical cases, one can check that exactly clients are coloured in blue and their types are necessarily distinct. While a blue client is served, note that her/his ancestors (namely, the other clients waiting in the line, if any) are blue too. Actually, we will see that the sub-queue constituted by the blue clients corresponds to the previous -LIFO queue in critical and subcritical cases.

In supercritical cases, however, we could end up with (strictly) less than blue clients so the blue sub-queue is only a part of the -LIFO queue governed by . To deal with this problem and to get a definition of the blue/red queue in a way that can be extended to the continuous setting, we proceed as follows. We first introduce the two following independent random point measures on :

| (16) |

that are Poisson point measures with intensity , where stands for the Lebesgue measure on and where . From , we extract the -LIFO queue (without repetition) that generates the desired graph and we explain below how to mix and in order to get the coloured Markovian queue seen at the beginning of the section. To that end, we first set:

| (17) |

Consequently, and are two independent spectrally positive Lévy processes, both with Laplace exponent given by (14). For all and all , we next set:

| (18) |

Thus, the are independent homogeneous Poisson processes with jump-rate and the r.v. are i.i.d. exponentially distributed r.v. with unit mean. Note that . Thanks to the "blue" r.v. contained in , we next define the processes coding the -LIFO queue (without repetition) that generates the exploration tree of the graph:

| (19) |

Thanks to and , we reconstruct the Markovian LIFO queue as follows: we first define the "blue" time-change that is the increasing càdlàg process defined for all by:

| (20) |

with the convention that . Note that iff that is a.s. finite in supercritical cases (and is a.s. infinite in critical and subcritical cases). Standard results on spectrally positive Lévy processes (see e.g. Bertoin’s book [4] Ch. VII.) assert that is a subordinator (that is defective in supercritical cases) whose Laplace exponent is given for all by:

| (21) |

We set that is the largest root of . Note that has at most two roots since it is convex: in subcritical or critical cases, is the only root of and in supercritical cases, the roots of are and . Note that is continuous and strictly increasing and that it maps onto . As a consequence of (21), in supercritical cases is exponentially distributed with parameter . We then set:

| (22) |

In critical and subcritical cases, and only takes finite values. In supercritical cases, a.s. and we check that . Imagine that the bi-coloured Markovian LIFO queue has a set of two clocks which never run simultaneously (as in chess clocks): one clock for the blue queue and one for the red. Then is the (global) time that has been spent when the clock for the blue queue shows . If we denote by (resp. ) the set of times when blue (resp. red) clients are served, then we can derive these service times from as follows (recalling that the server is considered as a blue client)

| (23) |

Note that is a countably infinite union of intervals in critical and subcritical cases and that it is a finite union in supercritical cases since . We next introduce the inverse time-changes and as follows:

| (24) |

The processes and are continuous, nondecreasing and a.s. . In critical and subcritical cases, we also get a.s. and for all . However, in supercritical cases, for all and a.s. for all , . We next derive the load of the Markovian queue from and as follows.

Proposition 2.2

Let and be as in (16). Let and be defined by (17) and let and be given by (24). We define the process by:

| (25) |

Then, has the same law as and : namely, it is a spectrally positive Lévy process with Laplace exponent as defined in (14). Furthermore, recall from (19) the definition of and recall from (22) the definition of the time ; then, we also get:

| (26) |

Tree embeddings. Recall from (11) the definition of the height process :

| (27) |

Recall that is the number of clients waiting in the -LIFO queue (without repetition) governed by and that it is the contour process of the exploration tree . Similarly, we denote by the number of clients waiting in the Markovian LIFO queue governed by the process given in Proposition 2.2: is defined as follows.

| (28) |

We shall refer to as the height process associated with . The process is the contour process of a tree that is given as follows: vertices are the clients and the server is viewed as the root; the -th client to enter the queue is a child of the -th one if the -th client enters when the -th client is served. It is easy to check that in critical and subcritical cases, this tree is made of a forest of i.i.d. Galton–Watson trees whose roots are all joined to a common vertex representing the server, and the common offspring distribution is given by:

| (29) |

Observe that . Thus, in critical and subcritical cases, the Galton–Watson trees are a.s. finite and fully explores the whole tree. In supercritical cases, we can still think of a sequence of i.i.d. Galton–Watson trees whose offspring distribution is given by (29), but we only see in a subsequence of these trees up to (part of) the first infinite member. Namely, the exploration of does not go beyond the first infinite line of descent. The embedding of the tree coded by into the Galton–Watson tree coded by is given by the following lemma.

Lemma 2.3

Proof. See Section 4.

Although the law of is complicated, (30) allows to define its height process in a tractable way which can then be passed to the limit. Note that the embedding is not complete in supercritical cases; however, it is sufficient to characterise the law of in terms of .

Remark 2.1

Note that the height process of is actually distinct from . Although related to , the tree coded by is not relevant to our purpose.

2.2 The multiplicative graph in the continuous setting

2.2.1 The continuous exploration tree and its height process

Notations and conventions. Recall that stands for the set of nonnegative integers and that . We denote by the set of weights. By an obvious extension of Notation (4), for all and all , we set . We also introduce the following:

Let be a filtration on that is specified further. A process is said to be a -Lévy process with initial value if a.s. is càdlàg, and if for all a.s. finite -stopping time , the process is independent of and has the same law as .

Let be a sequence of càdlàg -martingales that are in -summable and orthogonal: namely, for all , and if . Then stands for the (unique up to indistinguishability) càdlàg -martingale such that for all and all , , by Doob’s inequality.

Blue processes. We fix the following parameters.

| (31) |

These quantites are the parameters of the continuous multiplicative graph: plays the same role as in the discrete setting, is a drift coefficient similar to , is a Brownian coefficient and the interpretation of is explained later.

Next, let , , be processes that satisfy the following.

-

is a -real valued standard Brownian motion with initial value .

-

For all , is a -homogeneous Poisson process with jump-rate .

-

The processes , , are independent.

The blue Lévy process is then defined by

| (32) |

Clearly is a -spectrally positive Lévy process with initial value whose law is characterized by the Laplace exponent given for all by:

| (33) |

If , then a.s. and if , then a.s. . By analogy with the discrete situation of the previous section, we distinguish the following cases:

| (34) |

Most of the time, we shall assume that:

| (35) | either or . |

This assumption is equivalent to the fact that has infinite variation sample paths.

We next introduce the analogues of and defined in (19). To that end, note that . Since , it makes sense to set the following.

| (36) |

Remark 2.2

To view as in (6), set , note that and check that where is a centered -martingale such that (indeed, , where ). Since , it makes sense to write for all :

| (37) | |||||

Namely the jump-times of are the and . Let us quickly mention that the process appears in the Aldous–Limic’s approach to the exit boundary problem for general multiplicative processes [3].

Lemma 2.4

Proof. See Section 5.2.1.

Red and bi-coloured processes. We next introduce the red process that satisfies the following.

-

is a -spectrally positive Lévy process starting at and whose Laplace exponent is as in (33).

-

is independent of the processes and .

To keep the filtration minimal, we may assume that is the completed sigma-field generated by , and , . We next introduce the following processes:

| (38) |

with the convention: . For all , we set and that is a.s. finite in supercritical cases and that is a.s. infinite in critical or subcritical cases. Note that iff . Again, standard results on spectrally positive Lévy processes (see e.g. Bertoin’s book [4] Ch. VII.) assert that is a subordinator (that is defective in supercritical cases) whose Laplace exponent is given for all by:

| (39) |

We set that is the largest root of . Again, note that has at most two roots since it is convex: in subcritical or critical cases, is the only root of and in supercritical cases, the roots of are and . Note that is continuous and strictly increasing and that it maps onto . As a consequence of (39), in supercritical cases is exponentially distributed with parameter . We then set:

| (40) |

In critical and subcritical cases, and only takes finite values. In supercritical cases, a.s. and we check that . We next introduce the following.

| (41) |

The process is continuous, nondecreasing and in critical and subcritical cases, we also get a.s. and for all . However, in supercritical cases, a.s. for all and a.s. for all , . We next prove the analogue of Proposition 2.2.

Theorem 2.5

Let be as in (31). Assume that (35) holds. Recall from (32) the definition of and recall from (41) the definition of and . Then, is continuous, nondecreasing and a.s. . Furthermore, if we set

| (42) |

then, is a spectrally positive Lévy process with initial value and Laplace exponent as in (33). Namely, , and have the same law. Moreover,

| (43) |

Height process and pinching points. We next define the analogue of . To that end, we assume that defined in (33) satisfies the following:

| (44) |

Le Gall & Le Jan [15] (see also Le Gall & D. [10]) prove that there exists a continuous process such that the following limit holds true for all in probability :

| (45) |

Note that (45) is a local time version of (28). We refer to as the height process of .

Remark 2.3

Let us mention that in Le Gall & Le Jan [15] and Le Gall & D. [10], the height process is introduced only for critical and subcritical spectrally positive processes. However, it easily extends to supercritical cases thanks to the following fact that is proved e.g. in Bertoin’s book [4] Ch. VII: denote by the space of càdlàg functions equipped with Skorokhod’s topology; then for all and for all nonnegative measurable functional ,

| (46) |

where stands for a subcritical spectrally Lévy process with Laplace exponent .

Our main result, given below, introduces the analogue of in the continuous setting.

Theorem 2.6

Let be as in (31). Assume that (44) holds, which implies (35). Recall from (36) the definition of and ; recall from (38) the definition of ; recall from (40) the definition of ; recall from (42) the definition of and recall from (45) how is derived from .

Then, there exists a continuous process such that for all , is a.s. equal to a measurable functional of and such that

| (47) |

We refer to as the height process associated with .

Proof. See Section 5.2.4.

We next define the pinching times as in (9): we first set

| (48) |

Then, conditionally given , let

| (49) |

Then, set

| (50) |

In the next section, after some necessary setup on the coding of graphs, we will see that the triple completely characterises the continuous version of the multiplicative graph.

2.2.2 Coding graphs

Our primary goal here is to introduce the notions on measured metric spaces which will allow us to build the continuum graph from the processes . We will actually consider a slightly more general situation, which permits to include the coding for discrete graphs as well.

Coding trees. First let us briefly recall how functions (not necessarily continuous) code trees. Let be càdlàg and such that

| (51) |

For all , we set

| (52) |

Note that satisfies the four-point inequality: for all , one has

Taking shows that is a pseudometric on . We then denote by the equivalence relation and we set

| (53) |

Then, induces a true metric on the quotient set that we keep denoting by and we denote by the canonical projection. Note that is not necessarily continuous.

Remark 2.4

The metric space is tree-like but in general it is not necessarily connected or compact. However, we shall consider the following cases.

-

takes finitely many values.

-

is continuous.

In Case , is not connected but it is compact; is in fact formed by a finite number of points. In particular, is in this case: by (12), the exploration tree as defined in (7) is actually isometric to , that is the tree coded by the height process that is derived from by (11).

In Case , is compact and connected. Recall that real trees are metric spaces such that any pair of points is joined by a unique injective path that turns out to be a geodesic and recall that real trees are exactly the connected metric spaces satisfying the four-point condition (see Evans [13] for more references on this topic). Thus, is a compact real tree in this case.

The coding function provides two additional features: a distinguished point that is called the root of and the mass measure that is the pushforward measure of the Lebesgue measure on induced by on : for any Borel measurable function ,

| (54) |

Pinched metric spaces. We next briefly explain how additional “shortcuts” will modify the metric of a graph. Let be a metric space and let where , , are pairs of pinching points. Let that is interpreted as the length of the edges that are added to (if , then each is identified with ). Set and for all , set and . A path joining to is a sequence of such that , and , for all . For all , we then define its length by if or is equal to some ; otherwise we set . The length of a path is given by , and we set:

| (55) |

It can be readily checked by standard arguments that is a pseudo-metric. We refer to Section A for more details. Denote the equivalence relation by ; the -pinched metric space associated with is then the quotient space equipped with . First note that if is compact or connected, so is the associated -pinched metric space since the canonical projection is -Lipschitz. Of course when , on is a true metric, and is the identity map on .

Coding pinched trees. Let be a càdlàg function that satisfies (51) and or in Remark 2.4; let where , for all and let . Then, the compact measured metric space coded by and the pinching setup is the -pinched metric space associated with and the pinching points , where stands for the canonical projection. We shall use the following notation:

| (56) |

We shall denote by the composition of the canonical projections ; then and stands for the pushforward measure of the Lebesgue on via .

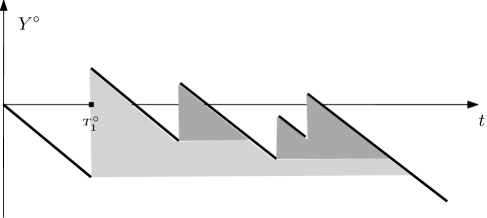

Coding -multiplicative graphs. Recall from Section 2.1 that , are the connected components of . Here, is the total number of connected components of ; is equipped with its graph-metric and with the restriction of the measure on ; the indexation satisfies . Let us briefly explain how the excursions of above code the measured metric spaces .

First, denote by , , the excursion intervals of above , that are exactly the excursion intervals of above its infimum process . Namely,

| (57) |

Here, we set and thus ; moreover, if , then we agree on the convention that ; excursions processes are then defined as follows:

| (58) |

We next define the sequences of pinching points of the excursions: to that end, recall from (8) and (9) the definition of the sequence of pinching points of ; observe that if , then ; then, it allows to define the following for all :

| (59) |

Then, for all , we easily see that is coded by as defined in (56). Namely,

| (60) |

Here, isometric means that there is a bijective isometry from onto sending to . This implies in particular that .

2.2.3 The continuous multiplicative random graph. Fractal properties.

We fix as in (31) and we assume that (44) holds true. By analogy with the discrete coding, we now define the -continuous multiplicative random graph, the continuous version of -multiplicative graph.

First, recall from (36) the definition of ; recall from Theorem 2.6 the definition of , the height process associated with ; recall from (48) the notation, , . Lemma 5.11 (see further in Section 5.2.4) asserts that the excursion intervals of above and the excursion intervals of above are the same; moreover Proposition 14 in Aldous & Limic [3] (recalled further in Proposition 5.8, Section 5.2.3), asserts that and that these excursions can be indexed in the decreasing order of their lengths. Namely,

| (61) |

where the sequence , decreases. This proposition also implies that has no isolated point, that for all and that the continuous function can be viewed as a sort of local-time for the set of zeros of . We refer to Sections 5.2.3 and 5.2.4 for more details. These properties allow to define the excursion processes as follows.

| (62) |

The pinching times are defined as follows: recall from (49) and (50) the definition of . If , then note that , by definition of . For all , we then define:

| (63) |

The connected components of the -continuous multiplicative random graph are then defined as the sequence of random compact measured metric spaces coded by the excursions and the pinching setups . Namely, we shall use the following notation: for all ,

| (64) |

The above construction of the continuous multiplicative random graph via the height process highlights the intimate connection between the graph and the Lévy trees that are the continuum trees coded by the excursions of above , where is the height process associated with the Lévy process . We conclude this section with a study of the fractal properties of the graphs where this connection with the trees plays an essential role. Indeed, as a consequence of Theorem 2.6, each component of the graph can be embedded in a Lévy tree whose branching mechanism is derived from by (33); roughly speaking the measure is the restriction to of the mass measure of the Lévy tree; this measure enjoys specific fractal properties and as a consequence of Theorem 5.5 in Le Gall & D. [11], we get the following result.

Proposition 2.7

Let as in (31). Assume that (44) holds true, which implies (35). Let be the connected components of the continuous -multiplicative random graph as defined in (64). We denote by the Hausdorff dimension and by the packing dimension. Then, the following assertions hold true a.s. for all ,

-

If , then .

-

Suppose , which implies by (35). Then, set:

that tends to as . We next define the following exponents:

(65) In particular, if varies regularly with index , then .

Then, if , we a.s. get

Proof. See Section 5.2.5.

2.3 Limit theorems for the multiplicative graphs

The family of continuous multiplicative random graphs, as defined previously, appears as the scaling limits of the -multiplicative graphs. This convergence is proved in [9]. We give here a short description of the main results of this paper.

Recall from Section 2.1 the various coding processes for the discrete graphs: for the Markovian queue/Galton–Watson tree, and for the graph, and is the time-change so that . Then recall from 2.2 their analogues in the continuous setting. Let , be a sequence of weights. The asymptotic regime considered in [9] is determined by two sequences of positive numbers . More precisely, we prove in [9] (Theorem 2.4) the following convergence of the coding processes:

| (66) |

weakly on equipped with the product of the Skorokhod and the continuous topologies, then the following joint convergence

| (67) |

holds weakly on equipped with the product topology.

For (66) to hold, it is necessary and sufficient that (see Le Gall & D. [10])

| (68) |

Above, stands for a Galton–Watson Markov chain with offspring distribution (as defined in (29)) and with initial state . In [9], for each satisfying the conditions (31) and (44), we construct examples of for (68) to take place, so that every member of the continuous multiplicative graph family appears in the limits of discrete graphs. Our construction there employs a sufficient condition for in (68) which can be readily checked in a wide range of situations. Moreover, in the near critical regime where and when large weights persist to the limit, [9] shows that -spectrally Lévy processes are the only possible scaling limits of the . Thus, in some sense, -continuum multiplicative graphs as introduced in this paper, are the only possible non-degenerate scaling limits of near critical multiplicative graphs.

In terms of the convergence of the graphs, (67) implies the following. Recall from (60) the graph encoded by . Put another way, forms the sequence of the connected components of sorted in decreasing order of their -masses: . Analogously, recall from (64) the connected components of the -continuous multiplicative random graph (ranked in decreasing order of their -masses). Completing the finite sequence with null entries, we have that (Theorem 2.8 in [9])

| (69) |

holds weakly with respect to the product topology induced by the Gromov–Hausdorff–Prokhorov distance. Moreover, the same type of convergence holds if we replace in (69) the weight-measure by the counting measure , where . We can also list the connected components of in the decreasing order of their numbers of vertices. Then again, Theorem 2.13 in [9] asserts that under the additional assumption that , we have this (potentially) different list of connected components converging to the same limit object. Theorem 2.8 in the companion paper [9] completes the previous scaling limits of truely inhomogeneous graphs due to: Bhamidi, Sen & X. Wang [6], Bhamidi, Sen, X. Wang & B. [5], Bhamidi, van der Hofstad & van Leeuwaarden [8] and Bhamidi, van der Hofstad & Sen [7]. We refer to [9] for a more precise discussion on the previous works dealing with the scaling limits of inhomogeneous graphs.

3 Proof of Theorem 2.1.

Let be a graph with . We suppose that has connected components that are listed in an arbitrary (deterministic way): let us say that the components are listed in the increasing order of their least vertex; namely, . Let be a set of strictly positive weights; we set that is a measure on .

We call the set of the atoms of a Poisson point measure a Poisson random set. We then define a law on as follows. Let be independent Poisson random subsets of with rate for all non-empty subset we set (in particular , for all ). Then is a Poisson random set with rate . For all , we then define by:

Namely, is the -th order statistic of . We denote by the joint law of and we easily check:

| (70) | ; | ||||

where is the unique permutation of such that , for all . The following lemma, whose elementary proof is left to the reader, provides a description of the law of conditionally given . Let us mention that it is formulated with specific notation for further use.

Lemma 3.1

Let be a finite graph with connected components; let be strictly positive weights; let . We fix . Then, we set and ; we equip with the set of weights , and we set . Let and be independent r.v. such that is exponentially distributed with unit mean and such that has law . We set

Then, for all ,

Next we briefly recall how to derive a graph from the LIFO queue (and from an additional point process) as discussed in Section 2.1.1. Let a finite set of vertices (or finite set of labels of clients) associated with a set of strictly positive weights denoted by (recall that the total amount of service of Client is ); let be the times of arrival of the clients. We assume that the clients arrive at distinct times and that no client enters exactly when another client leaves the queue. These restrictions correspond to a Borel subset of for that has a full Lebesgue measure. We next set

| (71) |

We then define such that is the label of the client who is served at time : since only increases by jumps, for all , we get the following:

-

either is empty and we set ,

-

or there exists such that and we set .

Note that if the server is idle. Observe that is càdlàg. As mentioned in Section 2.1.1, the LIFO-queue yields an exploration forest whose set of vertices is and whose set of edges are

Additional edges are created thanks to a finite set of points in as follows. For all , define . Then, the set of additional edges is defined by

Then the graph produced by , and is .

Theorem 2.1 asserts that if and have the appropriate distribution, then is a -multiplicative graph, whose law is denoted by given as follows: for all graphs such that ,

| (72) |

We actually prove a result that is slightly more general than Theorem 2.1 and that involves additional features derived from the LIFO queue. More precisely, denote by the number of excursions of strictly above its infimum and denote by , the corresponding excursion intervals listed in the increasing order of their left endpoints: (of course, this indexation does not necessarily coincide with the indexation of the connected components of the graph in the increasing order of their least vertex, nor with the decreasing order of their -measure). Then, we set:

| (73) |

From the definition of as a deterministic function of as recalled above, we easily check the following: has connected components (recall that they are listed in the increasing order of their least vertex: namely, ). Then, we define the permutation on that satisfies for all . Observe that and that the excursion codes the connected component . The quantity is actually the total amount of time during which the server is idle before the -th connected component is visited, and is the first visited vertex of the -th component. We denote by the (deterministic) function that associates to :

| (74) |

We next prove the following theorem that implies Theorem 2.1.

Theorem 3.2

We keep the notation from above. We assume that are independent exponentially distributed r.v. such that , for all . We assume that conditionally given , is a Poisson random subset of with intensity . Let be derived from by (74). Then, for all graphs whose set of vertices is and that have connected components, we get

| (75) | ; | ||||

Proof. We proceed by induction on the number of vertices of . When has only one vertex, then (75) is obvious. We fix an integer and we assume that (75) holds for all such that and all sets of positive weights .

Then, we fix such that ; we fix that are strictly positive weights and we also fix in ; we assume that in the corresponding LIFO queue, clients arrive at distinct times and that no client enters exactly when another client leaves the queue. We next set and . Let be the number of excursions of strictly above its infimum process ; let be as in (73): namely and , where is the -th excursion interval of strictly above listed in the increasing order of their left endpoint (namely, ).

The main idea for the induction is to shift the LIFO queue at the time of arrival of the first client (with label ) and to consider the resulting graph. More precisely, we set the following.

| (76) |

Let and be derived from and as in (71). Then observe that

| (77) |

Note that . Then, the alarm clock lemma implies the following.

-

(I)

Suppose that are independent exponentially distributed r.v. such that , for all . Then, is an exponentially distributed r.v. with unit mean, , for all , and are independent and under the conditional probability , , as defined in (76), are independent exponentially distributed r.v. such that , for all (where a.s. ).

We next fix and , two discrete (i.e. without limit-point) subsets of that yield the additional edges in a specific way that is explained later; let us mention that eventually and are taken random and distributed as independent Poisson point processes whose intensity is Lebesgue measure on . We first set:

| (78) | |||||

We next define and from to and we define a set of points by:

| (79) | |||||

| and |

We check the following (see also Fig. 4).

-

(II)

Fix ; suppose that and are two independent Poisson random subsets of with intensity . Then, is a Poisson random subset of with intensity .

Indeed, observe that and form a partition of . Then, note that is piecewise affine with slope in both coordinates on the excursion intervals of strictly above , and that that is affine with slope in both coordinates. Standard results on Poisson subsets entail that is a Poisson random subset on with intensity and by (76) , which implies (II).

Recall notation (74). We next introduce the two following graphs:

| (80) |

Then, the previous construction of combined with (77) easily implies the following:

-

(III)

Fix and . Then, is obtained by removing the vertex from : namely, and .

We next consider which connected components of are attached to in . To that end, recall that the (resp. the ) are the connected components of (resp. of ) listed in the increasing order of their least vertex; recall that (resp. ) is the permutation on (resp. on ) such that for all (resp. for all ). We first introduce

| (81) |

with the convention . The graph is the graph where the first (in the order of visit) connected component has been removed. Note that is possibly empty: it has connected components. We easily check that . Here again, we recall that the connected components of are listed in the increasing order of their least vertex: . Then, when , denote by the permutation of such that

| (82) |

We also set:

| (83) |

Suppose that are fixed, then we also check that

| (84) |

We now explain how additional edges are added to connect to . For all , let ; is the set of times during which Client is served; we easily check that is a finite union of disjoint intervals of the form whose total Lebesgue measure is : namely, .We also set:

Note that if and , then . Combined with elementary results on Poisson random sets, it implies the following.

-

(IV)

Fix and ; suppose that is a Poisson random subset of with intensity . Then, the are independent and is a Poisson random subset of with rate , where is such that .

We next introduce the following.

-

We set if there is such that .

-

We set if .

-

We set .

-

For all non-empty , we set .

We claim the following.

-

(V)

Fix . Then,

Proof of (V). The argument is deterministic and elementary. Suppose that . There are two cases to consider.

(Case 1): is part of the exploration tree generated by which means that . Namely, it means that because , by definition of ; since and by (77), it is equivalent to: . It implies that is the left endpoint of an excursion of strictly above its infimum; therefore, there exists such that and , by (73); thus which implies that (since as we are in the case where ).

Conversely, let be such that . It implies that and the previous arguments can be reversed verbatim to prove that is an edge of that is part of the exploration tree generated by .

(Case 2): is an additional edge of . Then, there exists such that and , where . Note that implies that since and since is the first visited vertex (or the first client). Also observe that implies . It also implies that lies in the first excursion interval of strictly above its infimum, which entails that . Then, we set and, thanks to (77), we rewrite the previous conditions in terms of and as follows: and , which is equivalent to: and . This proves that there is (as defined in (78)) such that as defined in (79). Since and form a partition of , and this proves that there is such that and which implies .

Conversely, suppose that and that . Then, and the previous arguments can be reversed verbatim to prove that is an (additional) edge of , which completes the proof of (Va).

Let us prove (Vb). Let . By definition . Let : namely, there exists such that , and . But implies that . Since , we get . By definition of , , which entails .

Let (if any) and let . Necessarily, , which entails , by definition. Then there exists such that , and . Note that is included in the excursion interval of strictly above its infimum whose left endpoint is , which implies that , for all . Thus . This proves that , which completes the proof of (Vb).

We now complete the proof of Theorem 3.2 as follows: let be independent exponentially distributed r.v. such that for all . We then fix and we work under ; under , by (76), we get , and for all , and . Under , we take and as two independent Poisson random subsets of with intensity ; and are also supposed independent of . Recall from (78) and (79) the definitions of and and from (80) the definition . By (I), under has the required distribution so that the induction hypothesis applies to : namely, under , has law (as defined in (72)) and conditionally given , has law as defined in (70) (namely, (75) holds).

By (IV), under and conditionally given , the are independent and is a Poisson random subset of with rate , where is such that . Since, conditionnally given , the r.v. has law , the definition of combined with elementary results on Poisson processes imply the following key point.

-

(VI)

Under and conditionally given , the are independent and is a Poisson random subset of with rate ; therefore, under , the are independent of and the very definition of implies that for all ,

Consequently, under , by (Va) and (VI), only depends on and on the , . This, combined with elementary results on Poisson processes, implies that is independent from and from ; (Va) and (VI) also imply that under , the events , , are independent and occur with probabilities . Then, note that . Thus, under , has law and it is independent from .

Recall from (81), (82), (83) and (84) notation , and . Then, observe that under and conditionally given , (Vb) and (VI) imply that has conditional law , where . Then, under and conditionally given , Lemma 3.1 applies and (84) entails that

| ; | ||||

Since , it implies that for all graph whose set of vertices is and that has connected components, we get

| ; | ||||

This completes the proof of Theorem 3.2 by induction on the number of vertices.

4 Embedding the multiplicative graph in a GW-tree

We recall from Section 2.1.2 the definition of the Markovian algebraic load process that is derived from the blue and red processes and as in (25). Namely recall from (16) that and are two independent Poisson random point measures on with intensity , where stands for the Lebesgue measure on and where . Recall from (17) the following notations

For all and all , recall from (18) that and that ; the are independent homogeneous Poisson processes with jump-rate and the r.v. are i.i.d. exponentially distributed r.v. with unit mean. Note that . Then recall from (19) that

| (86) |

Thanks to and we reconstruct the Markovian LIFO queue as follows. First recall from (20) the definition of the "blue" time-change : for all ,

| (87) |

with the convention that . Note that iff that is a.s. finite in supercritical cases (and is a.s. infinite in critical and subcritical cases). We also need to recall from (22) the definition of

| (88) |

In critical and subcritical cases, and only takes finite values. In supercritical cases, a.s. and we check that . We next recall from (23) the definition of and that are the sets of times during which blue and red clients are served (recall that the server is considered as a blue client):

| (89) |

Note that the union defining is countably infinite in critical and subcritical cases and that it is a finite union in supercritical cases since . We next recall from (24) the definition of the time-changes and :

| (90) |

The processes and are continuous and nondecreasing and a.s. . In critical and subcritical cases, we also get a.s. and for all . However, in supercritical cases, is eventually constant and equal to and a.s. for all , . We next recall from (25) the definition of the load of the Markovian queue :

| (91) |

We next prove Lemma 2.3. To that end we need the following lemma.

Lemma 4.1

Almost surely, for all such that , we get for all

| (92) |

Thus, a.s. for all , . Moreover, a.s. for all such that , then

| (93) |

We next introduce the red time-change:

| (94) |

Then, for all , and if , then .

Proof. As defined by (91), the process is obtained by concatenating alternatively successive parts of and as follows: recall from (86) that is the sum of the jumps of that already occurred once; it is therefore a nondecreasing process; denote by the -th jump-time of and to simplify, set (note that in supercritical cases, may be infinite). Let us agree on saying that the colour of the queue is defined by the colour of the client currently served. We then introduce a sequence which corresponds to the times when the queue switches its colour. For convenience, we first set and then we introduce

| (95) |

See also Fig. 5. Next set (that is infinite in the subcritical and the critical cases). Then, for all and . Fix . Then, note that , that and observe that (91) can be rewritten as follows.

| (96) |

Moreover, we get and . Namely,

Next fix . Note that and that . Thus, for all , . Namely, for all , we get and if , then we also get , which completes the proof of (92).

Clearly, (92) implies that a.s. for all , . We next prove (93): let such that , which implies that . We have proved that for all ; since by construction, , we also get . This implies that . Since , we get . But we have proved also that for all : therefore, , which entails (93).

We now complete the proof of the lemma. Since is the identity map, we get , which shows that is super-linear. Next observe that if , then there exists such that and . Thus, we get , which completes the proof of the lemma.

Proof of Lemma 2.3. Namely, we prove a.s. that for all , . To that end, we fix and we set where . By the definition (27) of , we get . For any , we next set where . By the definition (28), we get . Then, it is sufficient to prove that is one-to-one from onto .

We first prove: . First observe that , which implies that, when , we also have . Let and suppose that . By (93), we get . Moreover, since , . Suppose that , then (92) would easily entail that . Thus, and lies therefore in the interior of ; therefore for all sufficiently small , , and thus, . This implies that and it completes the proof that .

Conversely, let us prove that . Let . To simplify notation we set . Note that . We first prove that lies in the interior of . Indeed, suppose the contrary: namely suppose that lies in the closure of ; then we would get and , and (92) would entails that and thus, , which contradicts . Thus, lies in the interior of . Consequently, for all sufficiently small , and (93) entails , which implies that because

We have proved that . But recall that we have also proved that is included in the interior of on which is one-to-one, by definition. Consequently, we get , which proves Lemma 2.3.

Remark 4.1

By (92), we actually get , where we have set and .

End of the proof of Proposition 2.2. It remains to prove that has the same law as (or ). To that end, we first define a point measure that records the successive jump-times of , along with their types and their colours. Actually, here it will be convenient to distinguish three colours: (blue) for the jumps of , (repeated blue) for the jumps of and (red) for the jumps of . More precisely, set (that is infinite in the critical or subcritical cases). Recall from (16) that . Let us fix .

-

Colour :

If is a jump-time of , then is in the interior of : namely, . On the interior of , is continuous. Thus, if is a jump-time of , then corresponds to the jump-time of .

-

Colour :

If is a jump-time of , then is an endpoint of a connected component of : namely, , is a time when the queue changes its colour and the corresponding jump-time in is . By the definition (95) of the times , there exists such that and .

- Colour :

We then define as follows the increasing sequence of jump-times , of , the corresponding types and their colour .

See Fig. 5 for an example. We get:

To prove Proposition 2.2, it is then sufficient to prove that is a Poisson point measure on with intensity .

To that end, we introduce the following notation: let be a point measure on and let ; then, we denote by the restriction of on and we denote by the -time shifted measure .

Lemma 4.2

We fix an integer . Then, conditionally given and , the shifted measures and are independent Poisson point measures on with intensity .

Proof. We introduce that counts the number of red jump-times of the process among its first jump-times. For all , we introduce the events and .

We first observe that on , and . Namely, , , and . To simplify, denote by the sigma-field generated by and . By elementary properties of Poisson point measures, conditionally given , and are independent Poisson point measures on with intensity . Then, remark that belongs to . Thus, we get

| (98) |

Next observe that on , and , where is given by (87). Thus, , , and . Then, for all , denote by (resp. ) the sigma-field generated by (resp. ). Note that for all , is a-stopping time and by standard results, conditionally given under , and are independent and the conditional law of is that of a Poisson point measure on with intensity . To simplify, denote by the sigma-field generated by and . Note that , that and are -measurables and that conditionally given , and are distributed as two independent Poisson point measures on with intensity . Thus, it implies that

Since the events , form a partition of , the previous equality combined with (98) entails the desired result.

We fix and we recall notation from Lemma 4.2. Denote by the first atom of and denote by the first atom of . Recall the notation and observe that is a deterministic function of and . Then, by Lemma 4.2,

| (99) |

and , for all and all .

We next explain how (that is the first atom of ) is derived from , and . First observe that is the number of jumps of whose colour is or . Therefore, the time is the largest non-red jump-time of before (thus, if , then ). We next set . By construction of , we easily check that and that the following holds true (see also Fig. 5 for an example):

-

if .

-

if and .

-

if and .

Since are deterministic functions of , elementary properties of exponentially distributed r.v. combined with (99) entail that and are independent and that , for all and for all . This easily implies that is a Poisson point measure on with intensity . Consequently, has the same distribution as (or as ), which completes the proof of Proposition 2.2.

5 Properties of the continuous processes

5.1 The height process of a Lévy tree

In this section, we collect the various properties of the height process associated with a Lévy process that will be used later. In Section 5.1, there is no new result, the only exception being the technical Lemma 5.1.

5.1.1 Infimum process of a spectrally positive Lévy process

We first recall several results on the following specific Lévy processes : we fix , , , and we set

| (100) |

Let be a spectrally positive Lévy process with initial state and with Laplace exponent : namely, , for all . The Lévy measure of is , is its Brownian parameter and is its drift. Note that it includes the Lévy process by taking , , and .

Recall from (35) that has infinite variation sample paths if and only if either or , which is implied by the following condition:

| (101) |

that is assumed in various places in the paper.

Recall from (38) the notation: , for all , with the convention: .For all , we set and that is a.s. finite in supercritical cases and a.s. infinite in critical or subcritical cases. Observe that iff . Standard results on spectrally positive Lévy processes (see e.g. Bertoin’s book [4] Ch. VII) assert that is a càdlàg subordinator (a killed subordinator in supercritical cases) whose Laplace exponent is given for all by:

| (102) |

We set that is the largest root of . Note that iff . Let us also recall from Chapter VII in Bertoin’s book [4] the following absolute continuity relationship between a supercritical spectrally positive Lévy process and a subcritical one. More precisely, for all and for all nonnegative measurable functional ,

| (103) |

where stands for a subcritical spectrally Lévy process with Laplace exponent .

5.1.2 Local time at the supremum

We assume (35), namely that has infinite variation sample paths. For all , we set . Basic results of fluctuation theory entail that is a strong Markov process in and that is regular for and recurrent with respect to this Markov process (see for instance Bertoin [4] VI.1). We denote by the local time of at its supremum (namely, the local time of at ), whose normalisation is such that for all the following holds in probability:

| (104) |

See Le Gall & D. [10] (Chapter 1, Lemma 1.1.3 p. 21) for more details. If , then standard results about subordinators imply that a.s. for all , . We also need the following approximation of that holds when : for all , we set

| (105) |

If , then the following approximation holds true:

| (106) |

This is a standard consequence of the decomposition of into excursions under its supremum: see Bertoin [4], Chapter VI.

5.1.3 The height process

For all , we denote by that is the process reversed at time ; recall that has the same law as . Under (101), Le Gall & Le Jan [15] (see also Le Gall & D. [10]) prove that there exists a continuous process such that

| (107) |

As previously mentioned in Remark 2.3, this result has been established only in subcritical or critical cases. By (103), it easily extends to the supercritical case. In particular, one can show that

| (108) |

We next derive from the two approximations of mentionned in Section 5.1.2, similar approximations for the height process . For all real numbers , we first introduce the following:

| (109) |

Then we easily derive from (107) and (104) that (45) holds true: namely, for all , the following limit holds in probability:

Of course, we also get the following.

| (110) |

If , then (107) and (106) easily imply that for all , in probability. Actually, a closer look at the uniform approximation (106) shows the following.

| (111) |

Thanks to approximations (110) and (111), we next prove the following lemma.

Lemma 5.1

We assume (101). Then -a.s. for all , if for all , , then for all , .

Proof. Let be such that for all , . Since has only positive jumps, it implies that ; thus, for all , we get . Moreover, for all and for all , we get . It implies for all , that which entails the desired result when by (110).

Suppose next that . By a diagonal argument and (111), there is a sequence decreasing to such that -a.s. for all and for all such that , . First observe that for all , we get and that , for all . Consequently, , for all , and thus for all since is continuous.

Let . Let be such that . Then observe that and that for all . Consequently, . Since can be arbitrarily close to , the continuity of entails that and the previous inequality implies , which completes the proof of the lemma.

5.1.4 Excursion of the height process

Let us make a preliminary remark: the results of this section are recalled from Le Gall & D. [10] Chapter 1 that only deals with the critical or subcritical cases. However, they easily extend to the supercritical cases thanks to (103).

Here we assume that (101) holds, which implies that has unbounded variation sample paths. Then, basic results of fluctuation theory entail that is a strong Markov process in , that is regular for . Moreover, is a local time at for (see Bertoin [4], Theorem VII.1). We denote by the corresponding excursion measure of above . It is not difficult to derive from the previous approximations of that only depends on the excursion of above that straddles . Moreover, the following holds true:

| (112) |

Since is a local time for at , the topological support of the Stieltjes measure is . Namely,

| (113) |

Denote by , , the connected components of the open set and set , . We set that is the lifetime of . In the supercritical cases, there is one excursion with an infinite lifetime; more precisely, there exists such that and (recall that in the supercritical case, is exponentially distributed with parameter ). Then, the point measure

| (114) |

is distributed as where is a Poisson point measure on with intensity and where . Note that is exponentially distributed with parameter that is therefore equal to . Here we slightly abuse notation by denoting the "distribution" of under . In the Brownian case, up to scaling, is Itô’s measure of positive excursion of Brownian motion and the decomposition (114) corresponds to the Poisson decomposition of a reflected Brownian motion above .

As a consequence of (112), and under have the same lifetime (that is possibly infinite in the supercritical case) that satisfies the following:

| (115) |

By (108), in the supercritical cases, -a.e. on the event , we get .

Recall from (38) the definition of the subordinator whose Laplace exponent is . Note that ; consequently, is a pure jump-process and a.s. . Thus (114) entails

| (116) |

with the convention that . We next recall the following.

| (117) |

In the critical and subcritical cases, (117) is proved in Le Gall & D. [10] (Chapter 1, Corollary 1.4.2, p. 41). As already mentioned, this result remains true in the supercritical cases: we leave the details to the reader. Note that is a bijective decreasing function. Elementary arguments derived from (108) and (117) entail the following.

| (118) |

5.2 Properties of the coloured processes

Let , , and . For all , let be a homogeneous Poisson process with jump rate ; let be a standard Brownian motion with initial value . We assume that the processes and , , are independent. Let be an independent copy of . Recall from (32) that for all , we have set

where stands for the sum of orthogonal -martingales. Then and are two independent spectrally positive Lévy processes whose Laplace exponent is defined by (100). We assume (35), namely: either or . We recall from (36) the definition of :

| (119) |

Recall from (38) the following definitions:

| (120) |

with the convention: . Recall that is a possibly killed subordinator with Laplace exponent . Recall from (40) that:

| (121) |

In critical and subcritical cases, and only takes finite values. In supercritical cases, a.s. and we check that . We next recall the following from (41):

| (122) |

The processes and are continuous and nondecreasing. In critical and subcritical cases, we get a.s. and for all . In supercritical cases, for all and is constant and equal to on .

5.2.1 Properties of

Proof of Lemma 2.4. We assume (35): either or . If , then clearly a.s. is increasing. Suppose that . With the notation of (119), observe that for all ,

Note that . Since there exists depending on and such that for all , Borel’s Lemma implies that a.s. . This easily implies that is strictly increasing. To complete the proof of the lemma, observe that under (35), has infinite variation sample paths. Since is increasing, has infinite variation sample paths.

We shall need the following estimates on in the proof of Theorem 2.5.

Lemma 5.2

Let , , and . Assume (35): namely, either or . For all we set , that is well-defined. Then, is continuous and there exists that depend on and , such that

| (123) |

Proof. By Lemma 2.4, is strictly increasing, which implies that is continuous by standard arguments. We first suppose that . Then, by (119) . This entails that tends to and therefore that is well-defined. Moreover, we get , where: . Note that is the sum of exponentially distributed r.v. with parameter , which implies that and . Thus,

If , then (35) entails . Thus, and it is then possible to choose such that (123) holds.

5.2.2 Proof of Theorem 2.5

Using stochastic calculus arguments, we provide here a proof for the first statement of Theorem 2.5, namely, has the same distribution as . See Lemma 5.4 (i) in Section 5.2.3 for the proof of the second statement.

Let us first introduce notation. We first say that a martingale is of class if

-

(a)

a.s. ,

-

(b)

is càdlàg,

-

(c)

there exists such that a.s. for all , ,

-

(d)

for all , .

Let be a class martingale with respect to a filtration . Then, stands for the predictable quadratic variation process: namely, the unique -predictable nondecreasing process (provided by the Doob–Meyer decomposition) such that is a -martingale with initial value . We shall repeatedly use the following standard optional stopping theorem:

-

Let and be two -stopping times such that a.s. and . Then, and a.s. .

Then, the characteristic measure of is a random measure on such that:

-

for all , the process is -predictable;

-

for all , is a -martingale.

(See Jacod & Shiryaev [14], Chapter II, Theorem 2.21, p. 80.) The purely discontinuous part of is obtained as the -compensated sum of its jumps: namely, the -limit as goes to of the martingales . The purely discontinuous part of is denoted by and it is a -martingale of class . The continuous part of is the continuous -martingale . Note that is also a -martingale of class . We call the characteristics of . For more detail on the canonical representation of semi-martingales, see Jacod & Shiryaev [14] Chapter II, Definition 2.16 p. 76 and §2.d, Theorem 2.34, p. 84.

Let (resp. ) be the right-continuous filtration associated with the natural filtration of the process (resp. ); then, we set , , and

By standard arguments on Lévy processes, is a -martingale. We set and we easily check that

| (124) | is a -martingale. |