Deep optimal stopping111We thank Philippe Ehlers, Ariel Neufeld and Martin Stefanik for fruitful discussions and helpful comments.

Abstract

In this paper we develop a deep learning method for optimal stopping problems which

directly learns the optimal stopping rule from Monte Carlo samples. As such, it is broadly applicable

in situations where the underlying randomness can efficiently be simulated. We test the

approach on three problems: the pricing of a Bermudan max-call option, the pricing of a callable

multi barrier reverse convertible and the problem of optimally stopping a fractional Brownian motion.

In all three cases it produces very accurate results in high-dimensional situations with short

computing times.

Keywords: optimal stopping, deep learning, Bermudan option,

callable multi barrier reverse convertible, fractional Brownian motion.

1 Introduction

We consider optimal stopping problems of the form , where is an -valued discrete-time Markov process and the supremum is over all stopping times based on observations of . Formally, this just covers situations where the stopping decision can only be made at finitely many times. But practically all relevant continuous-time stopping problems can be approximated with time-discretized versions. The Markov assumption means no loss of generality. We make it because it simplifies the presentation and many important problems already are in Markovian form. But every optimal stopping problem can be made Markov by including all relevant information from the past in the current state of (albeit at the cost of increasing the dimension of the problem).

In theory, optimal stopping problems with finitely many stopping opportunities can be solved exactly. The optimal value is given by the smallest supermartingale that dominates the reward process – the so-called Snell envelope – and the smallest (largest) optimal stopping time is the first time the immediate reward dominates (exceeds) the continuation value; see, e.g., [39, 32]. However, traditional numerical methods suffer from the curse of dimensionality. For instance, the complexity of standard tree- or lattice-based methods increases exponentially in the dimension. For typical problems they yield good results for up to three dimensions. To treat higher-dimensional problems, various Monte Carlo based methods have been developed over the last years. A common approach consists in estimating continuation values to either derive stopping rules or recursively approximate the Snell envelope; see e.g., [48, 5, 15, 36, 49, 12, 14, 4, 30, 19, 11, 26, 10] or [23, 29], which use neural networks with one hidden layer to do this. A different strand of the literature has focused on approximating optimal exercise boundaries; see, e.g., [2, 20, 6]. Based on an idea of [17], a dual approach was developed by [40, 23]; see [27, 16] for a multiplicative version and [3, 13, 8, 41, 18, 7, 9, 33] for extensions and primal-dual methods. In [46] optimal stopping problems in continuous time are treated by approximating the solutions of the corresponding free boundary PDEs with deep neural networks.

In this paper we use deep learning to approximate an optimal stopping time. Our approach is related to policy optimization methods used in reinforcement learning [47], deep reinforcement learning [43, 38, 45, 35] and the deep learning method for stochastic control problems proposed by [24]. However, optimal stopping differs from the typical control problems studied in this literature. The challenge of our approach lies in the implementation of a deep learning method that can efficiently learn optimal stopping times. We do this by decomposing an optimal stopping time into a sequence of 0-1 stopping decisions and approximating them recursively with a sequence of multilayer feedforward neural networks. We show that our neural network policies can approximate optimal stopping times to any degree of desired accuracy. A candidate optimal stopping time can be obtained by running a stochastic gradient ascent. The corresponding expectation provides a lower bound for the optimal value . Using a version of the dual method of [40, 23], we also derive an upper bound. In all our examples, both bounds can be computed with short run times and lie close together.

The rest of the paper is organized as follows: In Section 2 we introduce the setup and explain our method of approximating optimal stopping times with neural networks. In Section 3 we construct lower bounds, upper bounds, point estimates and confidence intervals for the optimal value. In Section 4 we test the approach on three examples: the pricing of a Bermudan max-call option on different underlying assets, the pricing of a callable multi barrier reverse convertible and the problem of optimally stopping a fractional Brownian motion. In the first two examples, we use a multi-dimensional Black–Scholes model to describe the dynamics of the underlying assets. Then the pricing of a Bermudan max-call option amounts to solving a -dimensional optimal stopping problem, where is the number of assets. We provide numerical results for and 500. In the case of a callable MBRC, it becomes a -dimensional stopping problem since one also needs to keep track of the barrier event. We present results for and . In the third example we only consider a one-dimensional fractional Brownian motion. But fractional Brownian motion is not Markov. In fact, all of its increments are correlated. So, to optimally stop it, one has to keep track of all past movements. To make it tractable, we approximate the continuous-time problem with a time-discretized version, which if formulated as a Markovian problem, has as many dimensions as there are time-steps. We compute a solution for 100 time-steps.

2 Deep learning optimal stopping rules

Let be an -valued discrete-time Markov process on a probability space , where and are positive integers. We denote by the -algebra generated by and call a random variable an -stopping time if the event belongs to for all .

Our aim is to develop a deep learning method that can efficiently learn an optimal policy for stopping problems of the form

| (1) |

where is a measurable function and denotes the set of all -stopping times. To make sure that problem (1) is well-defined and admits an optimal solution, we assume that satisfies the integrability condition

| (2) |

see, e.g., [39, 32]. To be able to derive confidence intervals for the optimal value (1), we will have to make the slightly stronger assumption

| (3) |

in Subsection 3.3 below. This is satisfied in all our examples in Section 4.

2.1 Expressing stopping times in terms of stopping decisions

Any -stopping time can be decomposed into a sequence of 0-1 stopping decisions. In principle, the decision whether to stop the process at time if it has not been stopped before, can be made based on the whole evolution of from time until . But to optimally stop the Markov process , it is enough to make stopping decisions according to for measurable functions , . Theorem 1 below extends this well-known fact and serves as the theoretical basis of our method.

Consider the auxiliary stopping problems

| (4) |

for , where is the set of all -stopping times satisfying . Obviously, consists of the unique element , and one can write for the constant function . Moreover, for given and a sequence of measurable functions with ,

| (5) |

defines555In expressions of the form (5), we understand the empty product as . a stopping time in . The following result shows that, for our method of recursively computing an approximate solution to the optimal stopping problem (1), it will be sufficient to consider stopping times of the form (5).

Theorem 1.

Proof.

Denote , and consider a stopping time . By the Doob–Dynkin lemma (see, e.g., Theorem 4.41 in [1]), there exists a measurable function such that is a version of the conditional expectation . Moreover, due to the special form (6) of ,

is a measurable function of . So it follows from the Markov property of that is also a version of the conditional expectation . Since the events

are in , belongs to and to . It follows from the definitions of and that . Hence,

from which one obtains

Since was arbitrary, this shows that . Moreover, one has for the function given by

Therefore,

which concludes the proof. ∎

Remark 2.

Remark 3.

In many applications, the Markov process starts from a deterministic initial value . Then the function enters the representation (7) only through the value ; that is, at time , only a constant and not a whole function has to be learned.

2.2 Neural network approximation

Our numerical method for problem (1) consists in iteratively approximating optimal stopping decisions , by a neural network with parameter . We do this by starting with the terminal stopping decision and proceeding by backward induction. More precisely, let , and assume parameter values have been found such that and the stopping time

produces an expected value close to the optimum . Since takes values in , it does not directly lend itself to a gradient-based optimization method. So, as an intermediate step, we introduce a feedforward neural network of the form

where

-

•

are positive integers specifying the depth of the network and the number of nodes in the hidden layers (if there are any),

-

•

and are affine functions,

-

•

for , is the component-wise ReLU activation function given by

-

•

is the standard logistic function .

The components of the parameter of consist of the entries of the matrices and the vectors given by the representation of the affine functions

So the dimension of the parameter space is

and for given , is continuous as well as almost everywhere smooth in . Our aim is to determine so that

is close to the supremum . Once this has been achieved, we define the function by

| (8) |

where is the indicator function of . The only difference between and is the final nonlinearity. While produces a stopping probability in , the output of is a hard stopping decision given by or , depending on whether takes a value below or above .

The following result shows that for any depth , a neural network of the form (8) is flexible enough to make almost optimal stopping decisions provided it has sufficiently many nodes.

Proposition 4.

Let and fix a stopping time . Then, for every depth and constant , there exist positive integers such that

where is the set of all measurable functions .

Proof.

Fix . It follows from the integrability condition (2) that there exists a measurable function such that

| (9) | ||||

can be written as for the Borel set . Moreover, by (2),

define finite Borel measures on . Since every finite Borel measure on is tight (see e.g., [1]), there exists a compact (possibly empty) subset such that

| (10) | ||||

Let be the distance function given by . Then

defines a sequence of continuous functions that converge pointwise to . So it follows from Lebesgue’s dominated convergence theorem that there exists a such that

| (11) | ||||

By Theorem 1 of [34], can be approximated uniformly on compacts by functions of the form

| (12) |

for , and . So there exists a function expressible as in (12) such that

| (13) | ||||

Now note that for any integer , the composite mapping can be written as a neural net of the form (8) with depth for suitable integers and parameter value . Hence, one obtains from (9), (10), (11) and (LABEL:hk) that

and the proof is complete. ∎

2.3 Parameter optimization

We train neural networks of the form (8) with fixed depth and given numbers of nodes in the hidden layers777For a given application, one can try out different choices of and to find a suitable trade-off between accuracy and efficiency. Alternatively, the determination of and could be built into the training algorithm.. To numerically find parameters yielding good stopping decisions for all times , we approximate expected values with averages of Monte Carlo samples calculated from simulated paths of the process .

Let , be independent realizations of such paths. We choose such that and determine determine for recursively. So, suppose that for a given , parameters , have been found so that the stopping decisions generate a stopping time

with corresponding expectation close to the optimal value . If , one has , and if , can be written as

for a measurable function . Accordingly, denote

If at time , one applies the soft stopping decision and afterward behaves according to , the realized reward along the -th simulated path of is

For large ,

| (15) |

approximates the expected value

Since is almost everywhere differentiable in , a stochastic gradient ascent method can be applied to find an approximate optimizer of (15). The same simulations , can be used to train the stopping decisions at all times . In the numerical examples in Section 4 below, we employed mini-batch gradient ascent with Xavier initialization [21], batch normalization [25] and Adam updating [28].

Remark 6.

If the Markov process starts from a deterministic initial value , the initial stopping decision is given by a constant . To learn from simulated paths of , it is enough to compare the initial reward to a Monte Carlo estimate of , where is of the form

for and trained parameters . Then one sets (that is, stop immediately) if and (continue) otherwise. The resulting stopping time is of the form

3 Bounds, point estimates and confidence intervals

In this section we derive lower and upper bounds as well as point estimates and confidence intervals for the optimal value .

3.1 Lower bound

Once the stopping decisions have been trained, the stopping time given by (14) yields a lower bound for the optimal value . To estimate it, we simulate a new set888In particular, we assume that the samples , , are drawn independently from the realizations , , used in the training of the stopping decisions. of independent realizations , of . is of the form for a measurable function . Denote . The Monte Carlo approximation

gives an unbiased estimate of the lower bound , and by the law of large numbers, converges to for .

3.2 Upper bound

The Snell envelope of the reward process is the smallest999in the -almost sure order supermartingale with respect to that dominates . It is given101010up to -almost sure equality by

see, e.g., [39, 32]. Its Doob–Meyer decomposition is

where is the -martingale given10 by

and is the nondecreasing -predictable process given10 by

Our estimate of an upper bound for the optimal value is based on the following variant111111See also the discussion on noisy estimates in [3]. of the dual formulation of optimal stopping problems introduced by [40] and [23].

Proposition 7.

Let be a sequence of integrable random variables on . Then

| (16) |

Moreover, if for all , one has

| (17) |

for every -martingale starting from .

Proof.

For every -martingale starting from and each sequence of integrable error terms satisfying for all , the right side of (17) provides an upper bound121212Note that for the right side of (17) to be a valid upper bound, it is sufficient that for all . In particular, can have any arbitrary dependence structure. for , and by (16), this upper bound is tight if and . So we try to use our candidate optimal stopping time to construct a martingale close to . The closer is to an optimal stopping time, the better the value process131313Again, since , and are given by conditional expectations, they are only specified up to -almost sure equality.

corresponding to

approximates the Snell envelope . The martingale part of is given by and

| (18) |

for the continuation values141414The two conditional expectations are equal since is Markov and only depends on .

Note that does not have to be specified. It formally appears in (18) for . But is always . To estimate , we generate a third set151515The realizations , , must be drawn independently of , , so that our estimate of the upper bound does not depend on the samples used to train the stopping decisions. But theoretically, they can depend on , , without affecting the unbiasedness of the estimate or the validity of the confidence interval derived in Subsection 3.3 below. of independent realizations , of . In addition, for every , we simulate continuation paths , , that are conditionally independent161616More precisely, the tuples , , are simulated according to , where is a transition kernel from to such that -almost surely for all Borel sets . We generate them independently of each other across and . On the other hand, the continuation paths starting from do not have to be drawn independently of those starting from for . of each other and of . Let us denote by the value of along . Estimating the continuation values as

yields the noisy estimates

of the increments along the -th simulated path . So

can be viewed as realizations of for estimation errors with standard deviations proportional to such that for all . Accordingly,

is an unbiased estimate of the upper bound

which, by the law of large numbers, converges to for .

3.3 Point estimate and confidence intervals

Our point estimate of is the average

To derive confidence intervals, we assume that is square-integrable171717See condition (3). for all . Then

are square-integrable too. Hence, one obtains from the central limit theorem that for large , is approximately normally distributed with mean and variance for

So, for every ,

is an asymptotically valid confidence interval for , where is the quantile of the standard normal distribution. Similarly,

is an asymptotically valid confidence interval for . It follows that for every constant , one has

as soon as and are large enough. In particular,

| (19) |

is an asymptotically valid confidence interval for .

4 Examples

In this section we test181818All computations were performed in single precision (float32) on a NVIDIA GeForce GTX 1080 GPU with 1974 MHz core clock and 8 GB GDDR5X memory with 1809.5 MHz clock rate. The underlying system consisted of an Intel Core i7-6800K 3.4 GHz CPU with 64 GB DDR4-2133 memory running Tensorflow 1.11 on Ubuntu 16.04. our method on three examples: the pricing of a Bermudan max-call option, the pricing of a callable multi barrier reverse convertible and the problem of optimally stopping a fractional Brownian motion.

4.1 Bermudan max-call options

Bermudan max-call options are one of the most studied examples in the numerics literature on optimal stopping problems; see, e.g., [36, 40, 20, 12, 23, 14, 3, 13, 11, 6, 7, 26, 33]. Their payoff depends on the maximum of underlying assets.

Assume the risk-neutral dynamics of the assets are given by a multi-dimensional Black–Scholes model191919We make this assumption so that we can compare our results to those obtained with different methods in the literature. But our approach works for any asset dynamics as long as it can efficiently be simulated.

| (20) |

for initial values , a risk-free interest rate , dividend yields , volatilities and a -dimensional Brownian motion with constant instantaneous correlations202020That is, for all and . between different components and . A Bermudan max-call option on has payoff and can be exercised at any point of a time grid . Its price is given by

where the supremum is over all -stopping times taking values in ; see, e.g., [44]. Denote , , and let be the set of -stopping times. Then the price can be written as for

and it is straight-forward to simulate .

In the following we assume the time grid to be of the form , , for a maturity and equidistant exercise dates. Even though does not carry any information that is not already contained in , our method worked more efficiently when we trained the optimal stopping decisions on Monte Carlo simulations of the -dimensional Markov process instead of . Since is deterministic, we first trained stopping times of the form

for and given by (8) with and . Then we determined our candidate optimal stopping times as

for a constant depending212121In fact, in none of the examples in this paper it is optimal to stop at time . So in all these cases. on whether it was optimal to stop immediately at time or not (see Remark 6 above).

It is straight-forward to simulate from model (20). We conducted 3,00 training steps, in each of which we generated a batch of 8,192 paths of . To estimate the lower bound we simulated 096,000 trial paths. For our estimate of the upper bound , we produced ,024 paths , , of and realizations , , , of with 384. Then for all and , we generated the -th component of the -th continuation path departing from according to

Symmetric case

We first considered the special case, where , ,

for all and for all . Our results are reported in

Table 1.

Asymmetric case

As a second example, we studied model (20) with

, for all and for

all , but different volatilities .

For , we chose the specification , .

For , we set , . The results are given in

Table 2.

| Point est. | CI | Binomial | BC CI | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Point est. | CI | BC CI | ||||||

|---|---|---|---|---|---|---|---|---|

4.2 Callable multi barrier reverse convertibles

A MBRC is a coupon paying security that converts into shares of the worst-performing of underlying assets if a prespecified trigger event occurs. Let us assume that the price of the -th underlying asset in percent of its starting value follows the risk-neutral dynamics

| (21) |

for a risk-free interest rate , volatility , maturity , dividend payment time , dividend rate and a -dimensional Brownian motion with constant instantaneous correlations between different components and .

Let us consider a MBRC that pays a coupon at each of time points , , and makes a time- payment of

where is the nominal amount, a barrier, a strike price and the end of the -th trading day. Its value is

| (22) |

and can easily be estimated with a standard Monte Carlo approximation.

A callable MBRC can be redeemed by the issuer at any of the times by paying back the notional. To minimize costs, the issuer will try to find a -valued stopping time such that

is minimal.

Let be the -dimensional Markov process given by for , and

Then the issuer’s minimization problem can be written as

| (23) |

where is the set of all -stopping times and

where

Since the issuer cannot redeem at time , we trained stopping times of the form

for and given by (8) with and . Since (23) is a minimization problem, yields an upper bound and the dual method a lower bound.

We simulated the model (21) like (20) in Subsection 4.1 with the same number of trials except that here we used the lower number 024 to estimate the dual bound. Numerical results are reported in Table 3.

| Point est. | CI | Non-callable | ||||||

|---|---|---|---|---|---|---|---|---|

4.3 Optimally stopping a fractional Brownian motion

A fractional Brownian motion with Hurst parameter is a continuous centered Gaussian process with covariance structure

see, e.g., [37, 42]. For , is a standard Brownian motion. So, by the optional stopping theorem, one has for every -stopping time bounded above by a constant; see, e.g., [22]. However, for , the increments of are correlated – positively for and negatively for . In both cases, is neither a martingale nor a Markov process, and there exist bounded -stopping times such that ; see, e.g., [31] for two classes of simple stopping rules and estimates of the corresponding expected values .

To approximate the supremum

| (24) |

over all -stopping times , we denote , , and introduce the -dimensional Markov process given by

The discretized stopping problem

| (25) |

where is the set of all -stopping times and the projection , approximates (24) from below.

We computed estimates of (25) for by training networks of the form (8) with depth , and . To simulate the vector , we used the representation , where is the Cholesky decomposition of the covariance matrix of and a -dimensional random vector with independent standard normal components. We carried out 6,000 training steps with a batch size of 2,048. To estimate the lower bound we generated 096,000 simulations of . For our estimate of the upper bound , we first simulated 024 realizations , of and set . Then we produced another simulations , , , of , and generated for all and , continuation paths starting from

according to

with

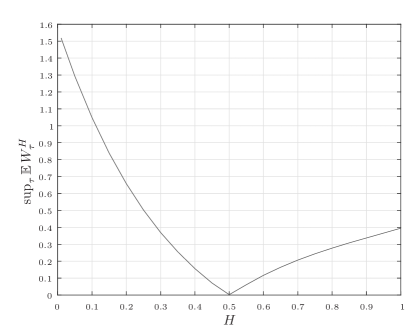

For , we chose 384, and for , 768. The results are listed in Table 4 and depicted in graphical form in Figure 1. Note that for and , our 95% confidence intervals contain the true values, which in these two cases, can be calculated exactly. As mentioned above, is a Brownian motion, and therefore, for every -stopping time . On the other hand, one has222222up to -almost sure equality , . So, in this case, the optimal stopping time is given22 by

and the corresponding expectation by

Moreover, it can be seen that for , our estimates are up to three times higher than the expected payoffs generated by the heuristic stopping rules of [31]. For , they are up to five times higher.

| Point est. | CI | |||

|---|---|---|---|---|

References

- [1] C.D. Aliprantis and K.C. Border (2006). Infinite Dimensional Analysis. 3rd Edition. Springer.

- [2] L. Andersen (2000). A simple approach to the pricing of Bermudan swaptions in the multi-factor LIBOR market model. Journal of Computational Finance 3(2), 5–32.

- [3] L. Andersen and M. Broadie (2004). Primal-dual simulation algorithm for pricing multidimensional American options. Management Science 50(9), 1222–1234.

- [4] V. Bally, G. Pagès and J. Printems (2005). A quantization tree method for pricing and hedging multidimensional American options. Mathematical Finance 15(1), 119–168.

- [5] J. Barraquand and D. Martineau (1995). Numerical valuation of high dimensional multi-variate American securities. Journal of Financial and Quantitative Analysis 30(3), 383–405.

- [6] D. Belomestny (2011). On the rates of convergence of simulation-based optimization algorithms for optimal stopping problems. Ann. Applied Probability 21(1), 215–239.

- [7] D. Belomestny (2013). Solving optimal stopping problems via empirical dual optimization. Ann. Applied Probability 23(5), 1988–2019.

- [8] D. Belomestny, C. Bender and J. Schoenmakers (2009). True upper bounds for Bermudan products via non-nested Monte Carlo. Mathematical Finance 19(1), 53–71.

- [9] D. Belomestny, J. Schoenmakers and F. Dickmann (2013). Multilevel dual approach for pricing American style derivatives. Finance and Stochastics 17(4), 717–742.

- [10] D. Belomestny, J. Schoenmakers, V. Spokoiny and Y. Tavyrikov (2018). Optimal stopping via reinforced regression. Arxiv Preprint.

- [11] S.J. Berridge and J.M. Schumacher (2008). An irregular grid approach for pricing high-dimensional American options. Journal of Computational and Applied Mathematics 222(1), 94–111.

- [12] P.P. Boyle, A.W. Kolkiewicz and K.S. Tan (2003). An improved simulation method for pricing high-dimensional American derivatives. Mathematics and Computers in Simulation 62, 315–322.

- [13] M. Broadie and M. Cao (2008). Improved lower and upper bound algorithms for pricing American options by simulation. Quantitative Finance, 8, 845–861.

- [14] M. Broadie and P. Glasserman (2004). A stochastic mesh method for pricing high-dimensional American options. Journal of Computational Finance, 7(4), 35–72.

- [15] J.F. Carriere (1996). Valuation of the early-exercise price for options using simulation and nonparametric regression. Insurance: Mathematics and Economics, 19, 19–30.

- [16] N. Chen and P. Glasserman (2007). Additive and multiplicative duals for American option pricing. Finance and Stochastics 11, 153–179.

- [17] M.H.A. Davis and I. Karatzas (1994). A deterministic approach to optimal stopping. In F.P. Kelly, editor, Probability, Statistics and Optimization: A Tribute to Peter Whittle, 455–466. J. Wiley and Sons.

- [18] V.V. Desai, V.F. Farias and C.C. Moallemi (2012). Pathwise optimization for optimal stopping problems. Management Science 58(12), 2292–2308.

- [19] D. Egloff, M. Kohler and N. Todorovic (2007). A dynamic look-ahead Monte Carlo algorithm for pricing Bermudan options. Ann. Applied Probability 17(4), 1138–1171.

- [20] D. García (2003). Convergence and biases of Monte Carlo estimates of American option prices using a parametric exercise rule. Journal of Economic Dynamics and Control 27, 1855–1879.

- [21] X. Glorot and Y. Bengio (2010). Understanding the difficulty of training deep feedforward neural networks. Proceedings of the Thirteenth International Conference on Artificial Intelligence and Statistics, PMLR 9, 249–256.

- [22] G. Grimmett and D. Stirzaker (2001). Probability and Random Processes. 3rd Edition. Oxford University Press.

- [23] M. Haugh and L. Kogan (2004). Pricing American options: a duality approach. Operations Research, 52, 258–270.

- [24] J. Han and W. E (2016). Deep learning approximation for stochastic control problems. Deep Reinforcement Learning Workshop, NIPS.

- [25] S. Ioffe and C. Szegedy (2015). Batch normalization: accelerating deep network training by reducing internal covariate shift. Proceedings of the 32nd International Conference on Machine Learning, PMLR 37, 448–456.

- [26] S. Jain and C.W. Oosterlee (2015). The stochastic grid bundling method: efficient pricing of Bermudan options and their Greeks. Applied Mathematics and Computation 269, 412–431.

- [27] F. Jamshidian (2007). The duality of optimal exercise and domineering claims: a Doob–Meyer decomposition approach to the Snell envelope. Stochastics 79, 27–60.

- [28] D. Kingma and J. Ba (2015). Adam: A method for stochastic optimization. International Conference on Learning Representations.

- [29] M. Kohler, A. Krzyżak and N. Todorovic (2010). Pricing of high-dimensional American options by neural networks. Mathematical Finance 20(3), 383–410.

- [30] A. Kolodko and J. Schoenmakers (2006). Iterative construction of the optimal Bermudan stopping time. Finance and Stochastics 10(1), 27–49.

- [31] A.V. Kulikov and P.P. Gusyatnikov (2016). Stopping times for fractional Brownian motion. Computational Management Science. Lecture Notes in Economics and Mathematical Systems 682.

- [32] D. Lamberton and B. Lapeyre (2008). Introduction to Stochastic Calculus Applied to Finance, 2nd Edition. Chapman and Hall/CRC, Boca Raton, Florida.

- [33] J. Lelong (2016). Pricing American options using martingale bases. Arxiv Preprint.

- [34] M. Leshno, V.Y. Lin, A. Pinkus and S. Schocken (1993). Multilayer feedforward networks with a non-polynomial activation function can approximate any function. Neural Networks 6, 861–867.

- [35] T.P. Lillicrap, J.J. Hunt, A. Pritzel, N. Heess, T. Erez, Y. Tassa, D. Silver and D. Wierstra (2016). Continuous control with deep reinforcement learning. International Conference on Learning Representations.

- [36] F.A. Longstaff and E.S. Schwartz (2001). Valuing American options by simulation: a simple least-square approach. Review of Financial Studies 14(1), 113–147.

- [37] B.B. Mandelbrot and J.W. van Ness (1968). Fractional Brownian motions, fractional noises and applications. SIAM Review 10 (4), 422–437.

- [38] V. Mnih, K. Kavukcuoglu, D. Silver, A.A. Rusu et al. (2015). Human-level control through deep reinforcement learning. Nature, 518, 529–533.

- [39] G. Peskir and A.N. Shiryaev (2006). Optimal Stopping and Free-Boundary Problems. Lectures in Mathematics. ETH Zurich.

- [40] L.C.G. Rogers (2002). Monte Carlo valuation of American options. Mathematical Finance 12(3), 271–286.

- [41] L.C.G. Rogers (2010). Dual valuation and hedging of Bermudan options. SIAM Journal on Financial Mathematics 1, 604–608.

- [42] G. Samorodnitsky and M.S. Taqqu (1994). Stable Non-Gaussian Random Processes. Chapman & Hall.

- [43] J. Schulman, S. Levine, P. Moritz, M. Jordan and P. Abeel (2015). Trust region policy optimization. Proceedings of Machine Learning Research 37, 1889–1897.

- [44] M. Schweizer (2002). On Bermudan options. Advances in Finance and Stochastics 257–270.

- [45] D. Silver, A. Huang, C.J. Maddison, A. Guez et al. (2016). Mastering the game of Go with deep neural networks and tree search. Nature 529, 484–489.

- [46] J. Sirignano and K. Spiliopoulos (2018). DGM: A deep learning algorithm for solving partial differential equations. Journal of Computational Physics 375, 1339–1364.

- [47] R.S. Sutton and A.G. Barto (1998). Reinforcement Learning. The MIT Press.

- [48] J.A. Tilley (1993). Valuing American options in a path simulation model. Transactions of the Society of Actuaries 45, 83–104.

- [49] J.N. Tsitsiklis and B. Van Roy (2001). Regression methods for pricing complex American-style options. IEEE Transactions on Neural Networks 12(4), 694–703.