Strong formulations for quadratic optimization with M-matrices and semi-continuous variables

Abstract.

We study quadratic optimization with indicator variables and an M-matrix, i.e., a PSD matrix with non-positive off-diagonal entries, which arises directly in image segmentation and portfolio optimization with transaction costs, as well as a substructure of general quadratic optimization problems. We prove, under mild assumptions, that the minimization problem is solvable in polynomial time by showing its equivalence to a submodular minimization problem. To strengthen the formulation, we decompose the quadratic function into a sum of simple quadratic functions with at most two indicator variables each, and provide the convex-hull descriptions of these sets. We also describe strong conic quadratic valid inequalities. Preliminary computational experiments indicate that the proposed inequalities can substantially improve the strength of the continuous relaxations with respect to the standard perspective reformulation.

Keywords Quadratic optimization, submodularity, perspective formulation, conic quadratic cuts, convex piecewise nonlinear inequalities

A. Gómez: Department of Industrial Engineering, Swanson School of Engineering, University of Pittsburgh, Pittsburgh, PA 15261. agomez@pitt.edu

![[Uncaptioned image]](/html/1804.05284/assets/x1.png)

BCOL RESEARCH REPORT 18.01

Industrial Engineering & Operations Research

University of California, Berkeley, CA 94720–1777

January 2018; April 2018

1. Introduction

Consider the quadratic optimization problem with indicator variables

where , and are -vectors, is an symmetric matrix and . Binary variables indicate a selected subset of and are often used to model non-convexities such as cardinality constraints and fixed charges. (QOI) arises in linear regression with best subset selection [10], control [23], filter design [47] problems, and portfolio optimization [11], among others. In this paper, we give strong convex relaxations for the related mixed-integer set

where is an M-matrix [43], i.e., and if . M-matrices arise in the analysis of Markov chains [30]. Convex quadratic programming with an M-matrix is also studied on its own right [37]. Quadratic minimization with an M-matrix arises directly in a variety of applications including portfolio optimization with transaction costs [33] and image segmentation [27].

There are numerous approaches in the literature for deriving strong formulations for (QOI) and . Dong and Linderoth [19] describe lifted inequalities for (QOI) from its continuous quadratic optimization counterpart over bounded variables. Bienstock and Michalka [12] give a characterization linear inequalities obtained by strengthening gradient inequalities of a convex objective function over a non-convex set. Convex relaxations of can also be constructed from the mixed-integer epigraph of the bilinear function . There is an increasing amount of recent work focusing on bilinear functions [e.g., 13, 14, 35]. However, the convex hull of such functions is not fully understood even in the continuous case. More importantly, considering the bilinear functions independent from the quadratic function may result in weaker formulations for . Another approach, applicable to general mixed-integer optimization, is to derive strong formulation based on disjunctive programming [8, 17, 45]. Specifically, if a set is defined as the disjunction of convex sets, then its convex hull can be represented in an extended formulation using perspective functions. Such extended formulations, however, require creating a copy of each variable for each disjunction, and lead to prohibitively large formulations even for small-scale instances. There is also a increasing body of work on characterizing the convex hulls in the original space of variables, but such descriptions may be highly complex even for a single disjunction, e.g., see [7, 9, 31, 39].

The convex hull of is well-known for a couple of special cases. When the matrix is diagonal, the quadratic function is separable and the convex hull of can be described using the perspective reformulation [21]. This perspective formulation has a compact conic quadratic representation [2, 24] and is by now a standard model strengthening technique for mixed-integer nonlinear optimization [15, 25, 38, 48]. In particular, a convex quadratic function is decomposed as , where , and is diagonal and then each diagonal term , , is reformulated as . Such decomposition and strengthening of the diagonal terms are also standard for the binary restriction, where , , in which case [e.g. 3, 44]. The binary restriction of , where and , , is also well-understood, since in that case the quadratic function is submodular [40] and min is a minimum cut problem [28, 42] and, therefore, is solvable in poynomial time.

Whereas the set with an M-matrix is interesting on its own, the convexification results on can also be used to strengthen a general quadratic by decomposing as , where is an M-matrix, and then applying the convexification results in this paper only on the term with negative off-diagonal coefficients, generalizing the perspective reformulation approach above. We demonstrate this approach for portfolio optimization problems with negative as well as positive correlations through computations that indicate significant additional strengthening over the perspective formulation through exploiting the negative correlations.

The key idea for deriving strong formulations for is decompose the quadratic function in the definition of as the sum of quadratic functions involving one or two variables:

| (1) |

Since a univariate quadratic function with an indicator is well-understood, we turn our attention to studying the mixed-integer set with two continuous and two indicator variables:

Frangioni et al [22] also construct strong formulations for (QOI) based on decompositions. In particular, they characterize quadratic functions that can be decomposed as the sum of convex quadratic functions with at most two variables. They utilize the disjunctive convex extended formulation for the mixed-integer quadratic set

where is a general convex quadratic function. The authors report that the formulations are weaker when the matrix is an M-matrix, and remark on the high computational burden of solving the convex relaxations due the large number of additional variables. Additionally, Jeon et al [29] give conic quadratic valid inequalities for , which can be easily projected into the original space of variables, and demonstrate their effectiveness via computations. However, a convex hull description of in the original space of variable is unknown.

In this paper, we improve upon previous results for the sets and . In particular, our main contributions are () showing, under mild assumptions, that the minimization of a quadratic function with an M-matrix and indicator variables is equivalent to a submodular minimization problem and, hence, solvable in polynomial time; () giving the convex hull description of in the original space of variables — the resulting formulations for are at least as strong as the ones used by Frangioni et al. and require substantially fewer variables; () proposing conic quadratic inequalities amenable to use with conic quadratic MIP solvers — the proposed inequalities dominate the ones given by Jeon et al.; () demonstrating the strength and performance of the resulting formulations for (QOI).

Outline The rest of the paper is organized as follows. In Section 2 we review the previous results for and . In Section 3 we study the relaxations of and , where the constraints are relaxed to , and the related optimization problem. In Section 4 we give the convex hull description of . The convex hulls obtained in Sections 3 and 4 cannot be immediately implemented with off-the-shelf solvers in the original space of variables. Thus, in Section 5 we propose valid conic quadratic inequalities and discuss their strength. In Section 6 we give extensions to quadratic functions with positive off-diagonal entries and continuous variables unrestricted in sign. In Section 7 we provide a summary computational experiments and in Section 8 we conclude the paper.

Notation

Throughout the paper, we use the following convention for division by : and if . In particular, the function given by is the closure of the perspective function of the quadratic function , and is convex [e.g. 26, p. 160]. For a set , denotes the convex hull of . Throughout, denotes an M-matrix, i.e., and for .

2. Preliminaries

In this section we briefly review the relevant results on the binary restriction of and the previous results on set .

2.1. The binary restriction of

Let be the binary restriction of , i.e. . In this case, the decomposition

| (2) |

leads to , by simply taking the convex hull of each term. Indeed, the quadratic problem is equivalent to an undirected min-cut problem [e.g. 42] and can be formulated as

Decomposition (2) leading to a simple convex hull description of in the binary case is our main motivation for studying decomposition (1) with the indicator variables.

2.2. Previous results for set

Here we review the valid inequalities of Jeon et al. [29] for . Although their construction is not directly applicable as they assume a strictly convex function, one can utilize it to obtain limiting inequalities. For the inequalities of Jeon et al. are described via the inverse of the Cholesky factor of . However, for , we have or , where is a singular matrix and the Cholesky factor is not invertible.

However, if the matrix is given by with , then their approach yields three valid inequalities:

As , we arrive at three limiting valid inequalities for .

Proposition 1.

The following convex inequalities are valid for :

| (3) | ||||

| (4) | ||||

| (5) |

For completeness, we verify here the validity of the limiting inequalities directly. The validity of inequality (3) is easy to see: observe that for ; then, for , (3) reduces to the perspective formulation for the quadratic constraint , and for we have . The validity of inequality (4) is proven identically. Finally, inequality (5) is valid since it forces when , and is dominated by the original inequality for other integer values of .

3. The unbounded relaxation

In this section we study the unbounded relaxations of and obtained by dropping the upper bound on the continuous variables:

In Section 3.1 we show that the minimization of a linear function over is equivalent to a submodular minimization problem and, consequently, solvable in polynomial time. In Section 3.2, we describe and in Section 3.3 we use the results in Section 3.2 to derive valid inequalities for .

3.1. Optimization over

We now show that the optimization of a linear function over can be solved in polynomial time under a mild assumption on the objective function. Consider the problem

where is a positive definite M-matrix and . We show that (P) is a submodular minimization problem. The positive definiteness assumption on ensures that an optimal solution exists. Otherwise, if there is with , the problem may be unbounded. The assumption is satisfied in most applications (e.g., see Sections 7.1 and 7.3). If , then in any optimal solution.

Proposition 2 (Characterization 15 [43]).

A positive definite M-matrix is inverse-positive, i.e., its inverse satisfies for all .

Proposition 3.

Problem (P) is equivalent to a submodular minimization problem and it is, therefore, solvable in polynomial time.

Proof.

We assume that (otherwise in any optimal solution) and that an optimal solution exists. Given an optimal solution to (P), let , the subvector of induced by , and by the submatrix of induced by . Then, from KKT conditions, we find Thus, an optimal solution satisfies

Consequently, defining for as observe that (P) is equivalent to the binary minimization problem

Note that since is a positive definite -matrix for any , , where is a nonnegative matrix and the largest eigenvalue of is less than . By scaling, we may assume that . Moreover, [e.g. 49]. For and all let Note that . Finally, define for and the increment function .

Claim 1.

For all and , is a monotone supermodular function.

Proof.

The claim is proved by induction on .

Base case, : Let and . Note that . Thus , and for all cases except . Thus, the marginal contributions are constant and is supermodular. Monotonicity can be checked easily.

Induction step: Suppose is supermodular and monotone for all . Observe that if and otherwise. Monotonocity of follows immediately from the monotonicity of the functions . Now let and . To prove supermodularity, we check that by considering all cases:

- :

-

If then by supermodularity of functions ; if and then by monotonicity; finally, if then .

- :

-

If then by supermodularity of functions ; if and then ; finally, if then . The case is identical.

∎

As is a sum of supermodular functions, it is supermodular. Consequently, is a supermodular function and (P) is a submodular minimization problem, solvable with a strongly polynomial number of calls to a value oracle [e.g. 41]. Evaluating the submodular function for a given set , i.e., computing , requires only matrix multiplication and inversion, and can be done in strongly polynomial time. Therefore (P) is solvable in strongly polynomial time. ∎

3.2. Convex hull of

Consider the function defined as

| (6) |

and the corresponding nonlinear inequality

| (7) |

Remark 1.

Proposition 4.

Inequality (7) is valid for .

Proof.

There are four cases to consider. If , then reduces to the original quadratic inequality , thus the inequality is valid. If , then the points in satisfy and ; since , none of these points are cut off by (7). If and , then in any point in and, in particular, ; thus reduces to the original inequality. The case where and is similar. ∎

Observe that function is a piecewise nonlinear function, where each piece is conic quadratic representable. However, the pieces are not valid outside of the region where they are defined, e.g., is invalid when as it cuts off feasible points with and . Thus, inequality (7) is not equivalent to the system given by , . Nevertheless, as shown in Proposition 5 below, (7) is a convex inequality.

Proposition 5.

The function is convex on its domain.

Proof.

Let and let for be a convex combination of and . We need to prove that

| (8) |

If and , or and , inequality (8) holds by convexity of the individual functions in the definition of . Otherwise, assume, without loss of generality, that , , and . Letting , observe that

-

•

.

-

•

, which is equivalent to .

-

•

.

-

•

.

Then, we find

∎

A consequence of Proposition 5 is that the convex inequality (7) can be implemented (with off-the-shelf solvers) using subgradient inequalities as for a subgradient at a given point , we have for all points in the domain of the convex function . In particular, the linear cuts

| (9) |

provide an outer-approximation of at and are valid everywhere on the domain. A subgradient can be found simply by taking the gradient of the relevant piece of the function at . In particular, for and , a subgradient inequality is

| (10) |

The process outlined here to find subgradient cuts (9) for can be utilized for any convex piecewise nonlinear function, and will be used for other functions in the rest of the paper. Convex piecewise nonlinear functions also arise in strong formulations for mixed-integer conic quadratic optimization [5], and subgradient linear cuts for such functions were recently used in the context of the pooling problem [36].

As Theorem 1 below states, inequality (7) and bound constraints for the binary variables describe the convex hull of .

Theorem 1 (Convex hull of ).

Proof.

Consider the optimization problems

To prove the result we show that for any value of , either and are both unbounded, or there exists a solution integral in that is optimal for both problems. If , then and are both unbounded, and if then corresponds to an optimization problem over an integral polyhedron and it is easily checked that and are equivalent. Thus, the interesting case is or, by scaling, . Note that in any optimal solution of , and in any optimal solution of . If , then is optimal with corresponding integer optimal for both and . Moreover, if , then both problems are unbounded: , is feasible for any for both problems. Thus, one needs to consider only the case where and or . Without loss of generality, let and .

Optimal solutions of . There exists an optimal solution with (if , subtracting from both and does not increase the objective – and if , then swapping the values of and reduces the objective). Thus, , if and otherwise, and either or and , which is the stationary point of .

Optimal solutions of . Note that there exists an optimal solution of where at least one of the continuous variables is (if , subtracting from both variables does not increase the objective value — this operation does not change the relative order of and ). Then, we conclude that in an optimal solution (if and , then setting reduces the objective value). Moreover, when , then . Thus, in the optimal solution . Substituting in the objective, we see that simplifies to For an optimal solution, if and otherwise, and if and otherwise. And, if , then . Hence, the optimal solutions coincide. ∎

3.3. Valid inequalities for

Inequalities in an extended formulation

Let and and . Using decomposition (1) and introducing , , one can write a convex relaxation of as

Inequalities in the original space of variables

By projecting out the auxiliary variables one obtains valid inequalities in the original space of variables. By re-indexing variables if necessary, assume that to obtain the convex inequality

| (11) |

Observe that the nonlinear inequality (11) is valid only if holds. However, we can obtain linear inequalities that are valid for by underestimating the convex function by its subgradients. Let be such that and . Then, the subgradient inequality

corresponding to a first order approximation of (11) around , is valid for (regardless of the ordering of the variables).

4. The bounded set

Let be defined as

| (12) |

where is the function defined in (6). This section is devoted to proving the main result:

Theorem 2 (Convex hull of ).

Remark 2.

Observe that for the binary restriction with , , reduces to , which together with the bound constraints describe .

The rest of this section is organized as follows. In Section 4.1 we give the convex hull description of the intermediate set with two continuous variables and one indicator variable:

In Section 4.2 we use this results to prove Theorem 2. Finally, in Section 4.3 we give valid inequalities for . Unlike in Section 3, the convex hull proofs in this section are constructive, i.e., we show how is constructed from the mixed-binary description of , instead of just verifying that does indeed result in conv.

4.1. Convex hull description of

Let be given by

Proposition 6.

.

Proof.

Note that a point belongs to if and only if there exists , and such that

| (13) | |||

| (14) | |||

| (15) | |||

| (16) | |||

| (17) | |||

| (18) | |||

| (19) | |||

| (20) | |||

| (21) |

The non-convex system (13)–(21) follows directly from the definition of the convex hull. Note that a convex extended formulation of conv() could also be obtained using the approach proposed by Ceria and Soares [17]. See also Vielma [46] for a recent approach to eliminate the auxiliary variables using Cayley embedding. We now show how to project out the additional variables , to find conv in the original space of variables, which can be done directly from the non-convex formulation above.

From constraints (14) and (17) we see , from constraint (15) , from (18) , from (16) we find , and from (19) we get and . Thus, (13)–(21) is feasible if and only if , and there exists such that

The existence of such can be checked by solving the convex optimization problem

| s.t. |

The equation yields

Let be an optimal solution to (M1). Note that whenever . Moreover, , which can only happen if and , in which case . Thus, we may assume that is not equal to one of its lower bounds.

Now observe that , in which case . Additionally, if , then and in particular . Therefore, the cases , , and are mutually exclusive if , and the optimal solution of (M1) corresponds to setting , , or , respectively. By calculating the objective function of (M1) with the appropriate value of , we find . Hence, if and only if and , . ∎

4.2. Convex hull description of

We use a similar argument as in the proof of Proposition 6 to prove Theorem 2. Let be a point such that and we additionally assume that . A point belongs to if and only if there exists , , and such that

| (22) | |||

| (23) | |||

| (24) | |||

| (25) | |||

| (26) | |||

| (27) | |||

| (28) | |||

| (29) | |||

| (30) | |||

| (31) |

The system (22)–(31) corresponds to , where and . Observe that and are the convex hulls of the restrictions of , where and , respectively.

Using a similar reasoning as in the proof of Proposition 6, we find , , , , and

| s.t. | (32) | |||

| (33) |

where

Thus, to find the convex hull of , we need to compute in closed form the solutions of the optimization problem (M2).

Lemma 1.

There exists an optimal solution to (M2) such that .

Proof.

Note that if , the function is non-increasing in for any value of . Thus there exists an optimal solution where is set to one of its upper bounds, i.e., either or . Since we assume and , the case is not possible.

Now suppose that . Then observe that . Thus

in this case (substituting ). Taking the derivative, we find

Note that since in any feasible solution, and , by assumption. Additionally

-

•

since and , we find that ,

-

•

since and , we find that .

Therefore, is non-positive, i.e., is non-increasing. Then, increasing another optimal solution can be found. In particular, an optimal solution with exits. ∎

From Lemma 1 we can assume, without loss of generality, that

| (34) |

Taking partial derivatives, we find that

Lemmas 2–4 characterize the optimal solutions of (M2), depending on the values of . Note that if

| (35) |

then , independently of the values of and . Thus, any feasible point that satisfies (35) is an optimal solution of (M2), as is the case for Lemmas 2 and 3. In contrast, under the conditions of Lemma 4, no feasible point satisfies (35) as it would violate upper bound constraints.

Lemma 2.

If then , where is a sufficiently small number, and is an optimal solution to with objective

Proof.

Lemma 3.

If and , then and is an optimal solution to with objective

Proof.

Observe that is feasible as Additionally, note that . Thus, is a KKT point and, by convexity, is an optimal solution. Substituting in (34), we find the result. ∎

Lemma 4.

If and , then and is an optimal solution to with objective

Proof.

Note that since and , we have and, in particular, . Additionally, it is easily checked that all other constraints (32)–(33) are satisfied. From we find that . Now let and be the dual variables associated with constraints and , respectively. Since both constraints are satisfied at equality at , then we see that the dual variables and may take positive values without violating complementary slackness. In particular, let and . Then, Thus corresponds to a KKT point and, by convexity, is optimal. Substituting in (34) gives the result. ∎

4.3. Valid inequalities for

Similar to the discussion in Section 3.3, the description of can be used to derive strong extended convex relaxations for . In order to obtain (nonlinear) inequalities in the original space of variables, we project out the auxiliary variables for a given ordering of the continuous variables with additional restrictions corresponding to conditions in (12). Finally, to obtain linear inequalities valid independent of the conditions, we derive the first order approximations.

Suppose , and for , which holds, in particular, if . By eliminating the auxiliary variables under these conditions we obtain the inequality

| (36) |

Inequality (36) is only valid for the particular permutation of the continuous variables and when conditions for hold. Since , we can find valid subgradient inequalities by taking gradients of the left-hand-side of (36). Let and , and recall . The partial derivatives of evaluated at a point where are as follows:

Thus, since , we obtain the linear inequality

| (37) |

Observe that inequality (37) depends only on the ordering of , but not on the actual values.

Remark 3.

Consider the submodular function given by . The extreme points of the extended polymatroid [20] associated with , , correspond to the vectors in inequality (37); thus, the convex lower envelope of is described by the function [34]. Atamtürk and Bhardwaj [4] employ these polymatroid inequalities for the binary case. For the mixed-integer case, the inequality (37) is tight for the binary restriction , and the right hand side is relaxed as the distance between and increases.

5. Valid conic quadratic inequalities for

The inequalities and derived in Sections 3 and 4 for and , respectively, cannot be directly used within off-the-shelf solvers in the original space of variables as they are piecewise functions. However, since they are convex, they can be implemented using gradient outer-approximations at differentiable points (as discussed in Sections 3.3 and 4.3): given a fractional point with and a subgradient , the inequality

| (38) |

can be used as a cutting plane to improve the continuous relaxation. However, such an approach may require adding too many inequalities (38) to the formulation, possibly resulting in poor performance (see also Sections 7.1 and 7.3 for additional discussion on computations). Alternatively, an extended formulation could be used [e.g., 17, 22]; however, such formulations may require a prohibitively large number of variables, resulting in hard-to-solve convex formulations and poor performance in branch-and-bound algorithms. Therefore, in this section we give valid conic quadratic inequalities that provide a strong approximation of and can be readily used within conic quadratic solvers.

5.1. Derivation of the inequalities

Let and observe that

We now consider inequalities obtained by lifting the valid inequality for , i.e., inequalities of the form

| (39) |

for , where . We additionally require the left hand side of (39) to be convex, which is the case if and only if is convex.

Proposition 7.

Proof.

By changing the lifting order, we also get that valid inequality , or, writing the inequalities more compactly, we arrive at the convex valid inequality

| (41) |

Remark 5.

Remark 6.

For the binary case, , , inequality (41) reduces to .

5.2. Strength of the inequalities

In order to assess the strength of inequality (41), we consider the optimization problem

| s.t. | |||

| (SR) | |||

Inequalities (41) are not sufficient to guarantee the integrality of in the optimal solutions of (SR) for all values of and , since they do not describe (given in Section 4). However, we now show that optimal solutions of (SR) are indeed integral under mild assumptions on the coefficients and . First, we prove an auxiliary lemma.

Lemma 5.

If there exists an optimal solution to (SR) with for some , then there exists an optimal solution that is integral in .

Proof.

If , then clearly there is an optimal solution with , depending on the sign of . Moreover, (SR) reduces to which has an optimal integral solution in . On the other hand, if , then (SR) reduces to which, again, has an optimal integral solution in . The case with is symmetric. ∎

Proposition 8.

If have the same sign and have the same sign, then (SR) has an optimal solution that is integral in .

Proof.

Note that if , then for an optimal solution of (SR). Also, if , then in an optimal solution of (SR), in which case is integral in extreme point solutions. It remains to show that if and , then there exists an optimal solution of (SR) that is integral in .

Suppose that in an optimal solution. Then and . Thus, and (SR) reduces to

which has an optimal solution integral in .

Now suppose, without loss of generality, there is an optimal solution with (if or then by Lemma 5 the solution is integral in ). Then observe that, in this case, the functions and are non-increasing in . Since , there exists a solution where is at its upper bound, i.e., . Thus problem (SR) reduces to

Let be the dual variables associated with the constraints displayed in the order above and consider the dual feasibility conditions of problem (SR′)

Let be a KKT point with multipliers and suppose that . Then observe that for small , is also a KKT point with the same multipliers. In particular, by choosing so that , we see that there is an optimal solution with . Then, problem (SR′) further simplifies to

It remains to show that is integral. Note that

and, therefore, constraint is not binding when . So, (SR′′) is equivalent to . However, by increasing or decreasing and by the same amount it is easy to check that there exists an optimal solution where either or , and from Lemma 5 there exists an optimal integral solution. ∎

Proposition 8 provides an insight on which problems inequalities (41) may be particularly effective: if the coefficients of the binary variables and the continuous variables have the same sign, then the relaxation induced by (41) may be close to ideal; otherwise, using subgradient inequalities may be required to find strong formulations. In our computations, this simple rule of thumb indeed results in the best performance.

6. Extensions to other quadratic functions with two indicator variables

In this paper we focus on the set , i.e., a mixed-integer set with non-negative continuous variables and non-positive off-diagonal entries in the quadratic matrix. Although an in-depth study of more general quadratic functions is outside the scope of this paper, the approach used in Section 5 can be naturally extended to other quadratic functions. We briefly discuss two such extensions.

6.1. General quadratic functions

Observe that a general quadratic function can be decomposed as

Thus, stronger formulations for general quadratic functions may be obtained by studying the set with two continuous and two indicator variables and positive off-diagonal term

Proposition 9.

The proof is analogous the the proof of Proposition 7 as is omitted for brevity. Although inequality (42) is similar in spirit to (40), and that it is the strongest among inequalities of the form (39), it is not as strong as (40) for . In particular, an integrality result similar to Proposition 8 does not hold for (42).

6.2. Quadratic functions with continuous variables unrestricted in sign

Consider the set

Observe that, since the continuous variables can be positive or negative, the sign inside the quadratic expression does not matter (e.g., it can be flipped via the transformation ). Thus we assume, without loss of generality, that it is a minus sign.

Proposition 10.

Proof.

Any valid inequality for of the form (39) needs to satisfy

If , then . Else, ; in this case, the minimum is attained at if and at otherwise. Thus, we find that for . To find the strongest convex inequality, we compute , where The convex lower envelope corresponding to the one-dimensional non-convex function for is the constant function equal to . Moreover, it can be shown that

and we get the convex valid inequality for . ∎

In light of Proposition 10, inequalities (40)-(41) can be interpreted as inequalities that additionally account for the non-negativity of the continuous variables, with respect to the valid inequalities proposed by Jeon et al. [29]. Moreover, although not explicitly considered by Jeon et al., their inequalities may be particularly effective for quadratic optimization problems with indicator variables and continuous variables unrestricted in sign. Observe that inequalities (3)–(5) are indeed valid even if the variables are not required to be non-negative – in contrast with the inequalities , and (41), which account for the non-negativity of the variables and are only valid in that case.

7. Computations

In this section we report a summary of computational experiments performed to test the effectiveness of the proposed inequalities in a branch-and-bound algorithm. All experiments are conducted using Gurobi 7.5 solver on a workstation with a 3.60GHz Intel® Xeon® E5-1650 CPU and 32 GB main memory with a single thread. The time limit is set to one hour and Gurobi’s default settings are used (except for the parameter “PreCrush”, which is set to 1 in order to use cuts). Cuts (if used) are added only at the root node using the callback features of Gurobi, and the reported times include the time used to add cuts.

7.1. Image segmentation with -0 penalty

Given a finite set , functions for and for , consider

where . Problem (D) arises as the Markov Random Fields (MRF) problem for image segmentation, see [16, 32]. In the MRF context, are the deviation penalty functions, used to model the cost of changing the value of a pixel from the observed value to , e.g., with ; functions are the separation penalty functions, used to model the cost of having adjacent pixels with different values, e.g., with if pixels and are adjacent, and otherwise. Often, or is given by a suitable discretization, i.e., is a vector of integer multiples of a parameter . We consider in our computations the case , but the proposed approach can be used with any .

Problem (D) can be cast as the nonlinear dual of the undirected minimum cost network flow problem [1] and efficient algorithms exist when all functions are convex [27]. In contrast, we consider here the case where the deviation functions involve a non-convex -0 penalty, which is often used to induce sparsity, e.g., restricting the number of pixels that can have a color different from the background color. In particular, with . Thus, the problem can be formulated as

| (43) |

Instances

The instances are constructed as follows. The elements of correspond to points in a grid, thus , and separation functions are non-zero whenever the corresponding points are adjacent in the grid. The parameters for , and for each pair of adjacent points are drawn uniformly between 0 and 1. We set , where is generated as follows: first we draw uniformly between and for all , let and ; then we set . Instances generated with these parameters are observed to have large integrality gaps.

Formulations

We test the following formulations for solving problem (43):

- Basic:

-

The natural formulation

- Perspective:

-

The perspective reformulation implemented with rotated cone constraints

s.t. - Conic:

-

The formulation with the conic quadratic inequalities (41)

s.t.

Furthermore, we also test models Perspective+cuts and Conic+cuts, where the subgradient inequalities (38) are used as cutting planes to strengthen the Perspective and Conic formulations, respectively. If for some then we use the first-order expansion around instead.

Results

Table 1 shows a comparison of the performance of the algorithm for each formulation for varying grid sizes. Each row in the table represents the average for five instances for a grid size. Table 1 displays the initial gap (igap), the root gap improvement (rimp), the number of branch and bound nodes (nodes), the elapsed time in seconds (time), and the end gap at termination (egap) (in brackets, we report the number of instances solved to optimality within the time limit). The initial gap is computed as , where is the objective value of the best feasible solution found and is the objective of the continuous relaxation of Basic. The root improvement is computed as , where is the objective value of the relaxation obtained after processing the first node of the branch-and-bound tree for a given formulation, obtained by querying Gurobi’s attribute “ObjBound” at the root node using a callback.

We observe that the Basic formulation requires a substantial amount of branching before proving optimality, resulting in long solution times. The Perspective formulation results in a root gap improvement close to 50% and better times and end gaps than the Basic formulation. However, even with the Perspective formulation, instances with and larger cannot be solved to optimality leaving end gaps 15.3% or more. In contrast, formulation Conic results in root gap improvements close to 100%, and the performance of the branch-and-bound algorithm is orders-of-magnitude better than with the Basic and Perspective formulations: instances with that are not close to being solved after one hour of computation with Basic and Perspective are solved to optimality in one second; while formulation Basic is able to solve in five minutes instances with variables, formulation Conic is able to solve in the same amount of time formulations with variables, i.e., instances 250 times larger.

| igap | Basic | Perspective | Perspective+cuts | Conic | Conic+cuts | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| nodes | time | egap | rimp | nodes | time | egap | rimp | nodes | time | egap | rimp | nodes | time | egap | rimp | nodes | time | egap | |||

| 100 | 51.0 | 2,065,285 | 301 | 0.0[5] | 47.9 | 70,898 | 17 | 0.0[5] | 99.6 | 27,006 | 601 | 0.0[5] | 99.4 | 7 | 0 | 0.0[5] | 99.7 | 7 | 0 | 0.0[5] | |

| 400 | 47.7 | 9,520,774 | 3,600 | 34.0[0] | 48.6 | 5,277,876 | 3,600 | 15.3[0] | 93.2 | 305 | 2 | 0.0[5] | 99.5 | 59 | 1 | 0.0[5] | 99.5 | 58 | 1 | 0.0[5] | |

| 2,500 | 47.9 | 1,091,872 | 3,600 | 46.3[0] | 45.6 | 682,406 | 3,600 | 25.6[0] | 47.2 | 38,989 | 2,235 | 9.9[2] | 99.3 | 17,561 | 393 | 0.0[5] | 99.6 | 9,220 | 210 | 0.0[5] | |

| 10,000 | 47.4 | 167,529 | 3,600 | 47.2[0] | 45.9 | 131,986 | 3,600 | 25.9[0] | 32.4 | 25,992 | 3,600 | 0.2[0] | 99.5 | 25,842 | 3,600 | 0.1[0] | 99.6 | 26,695 | 3,600 | 0.1[0] | |

Formulation Conic+cuts results in very modest improvement in the strength of the continuous relaxation when compared with Conic (less than 0.3% additional root gap improvement) and almost no difference in terms of nodes, times or end gaps. Observe that in (43) the coefficients of the linear objective terms corresponding to the discrete and continuous variables have the same sign, and the experimental results are consistent with Proposition 8 — Conic indeed is a very close approximation of inequalities (38) in this case.

Note that if cuts are added without the approximation given by inequalities (41) (formulation Perspective+cuts), the root improvement is substantial for small instances but it degrades as the size increases. We conjecture that the required number of cuts to obtain an adequate relaxation increases with the size of the instances. Thus, for larger instances, Gurobi may stop adding cuts before obtaining a strong relaxation. Additionally, to solve second-order conic subproblems in branch-and-bound, solvers like Gurobi construct a linear outer approximation of the convex sets; adding a large number of cuts may interfere with the construction of the outer approximation, leading to weak relaxations of the convex set, which is observed for instances with . Using the approximation of the convex hull derived in Section 5 as a starting point appears to circumvent such numerical difficulties.

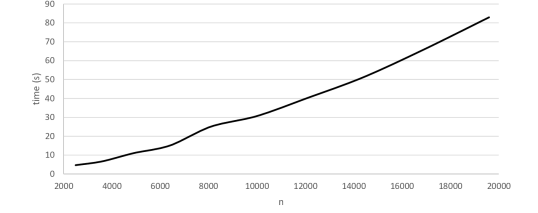

Finally, we remark that for the larger instances that are not solved to optimality by Conic, high quality solutions and tight lower bounds are found within a few seconds, but branching is ineffective to close the remaining gap. To illustrate, Figure 1 presents the time to prove an optimality gap of at most 1%, as a function of the dimension of the problem. We see that the proposed approach scales very well (almost linearly) up to . In particular, the lower bound found corresponds to the one obtained at the root node, and the feasible solutions are found within a small number (50–60) of branch-and-bound nodes. Memory limit is reached for instances with .

7.2. Portfolio optimization with transaction costs

Consider a simple portfolio optimization problem with transaction costs similar to the one discussed in [18, p.146]. However, in our case, transactions have a fixed cost and there is a restricted number of transactions. For simplicity, we first consider assets with uncorrelated returns. In this context, an M-matrix arises directly due to the buying and selling decisions. In Section 7.3 we present computations with a general covariance matrix, from which an M-matrix corresponding to the negatively correlated assets can be extracted to apply the reformulations.

Let be the set of assets, be the vectors of expected returns and standard deviations of returns. Let denote the current holdings in each asset, let be the fixed transaction costs associated with buying and selling any quantity, be the variable transaction costs and profits of buying and selling each asset, let be the upper bounds on the transactions, and let be the maximum number of transactions. Then the problem of finding a minimum risk portfolio that satisfies a given expected return with at most transactions can be formulated as the mixed-integer quadratic problem:

| s.t. | |||

where is the variance of the new portfolio, the decision variables () indicate the amount bought (sold) in asset and the variables () indicate whether asset is bought (sold). Note that the quadratic objective function is nonseparable and the corresponding quadratic matrix is positive semi-definite but not positive definite; therefore, the classical perspective reformulation cannot be used. Additionally, observe that the portfolio optimization problem can be reformulated by adding continuous variables , constraints for all to minimize the linear objective

| (44) |

Note that since each continuous variable is involved in exactly one term in the objective, the extended formulation given by (44) and constraints results in the convex envelope of .

Instances

The instances are constructed as follows. We set for all . Coefficients are drawn uniformly between and , are drawn uniformly between and , the transactions costs and profits and are drawn uniformly between and , the fixed costs and are drawn uniformly between and and , respectively. The target return is set to where is a parameter; is set to .

Formulations

We test the formulations Basic, Basic+cuts, Conic, and Conic+cuts, as defined in Section 7.1. As mentioned above, the perspective reformulation cannot be used for these instances.

Results

Table 2 shows the results for varying number of assets and values of the expected return . Observe that instances with lower values of are more difficult to solve for the Basic formulation: low results in more feasible solutions, and more branch-and-bound nodes need to be explored before proving optimality. We also see that the Basic formulation is not effective for instances with or more assets, where most instances (27 out of 30) are not solved to optimality within the time limit and leaving large end gaps at termination. On the other hand, the other three formulations achieve root improvements of over in most cases, and lead to much lower solution times and end gaps.

Observe that for the portfolio problem, the coefficients of and in the objective and return constraints have opposite signs. Thus, we expect the approximation given by Conic not to be as effective as in Section 7.1 and, therefore, the cuts to have a larger impact in closing the root gaps. Indeed, we see in these experiments that adding cuts leads to an additional 2% to 4% root improvement (compared to the 0.3% improvement observed in Section 7.1)111The root gap improvements of 95% achieved by Conic indicate that the approximation given in Section 5 is strong and considerably better than the natural continuous relaxation.. In particular, formulation Basic+cuts is able to solve all instances in seconds, even instances with low values of where all other formulations struggle.

| igap | Basic | Basic+cuts | Conic | Conic+cuts | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| rimp | nodes | time | egap | rimp | nodes | time | egap | rimp | nodes | time | egap | rimp | nodes | time | egap | |||

| 100 | 0.95 | 30.8 | 0.0 | 39,963 | 11 | 0.0[5] | 98.9 | 57 | 0 | 0.0[5] | 86.9 | 822 | 4 | 0.0[5] | 92.8 | 1,069 | 4 | 0.0[5] |

| 0.98 | 27.9 | 0.0 | 6,926 | 2 | 0.0[5] | 93.2 | 130 | 1 | 0.0[5] | 98.4 | 35 | 0 | 0.0[5] | 94.4 | 167 | 1 | 0.0[5] | |

| 1.00 | 32.7 | 0.0 | 3,229 | 1 | 0.0[5] | 97.9 | 32 | 0 | 0.0[5] | 96.9 | 49 | 0 | 0.0[5] | 97.2 | 37 | 0 | 0.0[5] | |

| Average | 0.0 | 16,706 | 5 | 0.0[15] | 96.7 | 76 | 0 | 0.0[15] | 94.1 | 302 | 2 | 0.0[15] | 94.8 | 425 | 2 | 0.0[15] | ||

| 250 | 0.95 | 32.4 | 0.0 | 5,344,016 | 3,600 | 15.0[0] | 98.8 | 176 | 0 | 0.0[5] | 94.0 | 175,859 | 2,880 | 1.7[1] | 96.0 | 233,024 | 2,880 | 1.1[1] |

| 0.98 | 26.0 | 0.0 | 4,831,484 | 3,227 | 6.2[1] | 97.8 | 210 | 1 | 0.0[5] | 99.1 | 27 | 0 | 0.0[5] | 98.4 | 50,689 | 720 | 0.3[4] | |

| 1.00 | 29.4 | 0.0 | 4,518,960 | 2,970 | 4.0[1] | 97.3 | 2,061 | 49 | 0.0[5] | 97.4 | 3,597 | 38 | 0.0[5] | 97.0 | 3,858 | 130 | 0.0[5] | |

| Average | 0.0 | 4,898,153 | 3,265 | 8.4[2] | 98.0 | 816 | 17 | 0.0[15] | 96.8 | 59,827 | 973 | 0.6[11] | 97.2 | 95,857 | 1,243 | 0.5[10] | ||

| 500 | 0.95 | 32.3 | 0.0 | 2,906,338 | 3,600 | 24.5[0] | 97.6 | 387 | 2 | 0.0[5] | 95.2 | 26,640 | 1,441 | 0.6[3] | 97.2 | 139,686 | 3,600 | 0.9[0] |

| 0.98 | 26.1 | 0.0 | 3,096,026 | 3,600 | 16.4[0] | 98.0 | 343 | 3 | 0.0[5] | 96.4 | 295 | 2 | 0.0[5] | 99.1 | 182 | 1 | 0.0[5] | |

| 1.00 | 32.8 | 0.0 | 3,076,324 | 3,600 | 18.8[0] | 97.5 | 328 | 2 | 0.0[5] | 93.4 | 330 | 2 | 0.0[5] | 97.0 | 254 | 1 | 0.0[5] | |

| Average | 0.0 | 3,026,229 | 3,600 | 19.9[0] | 97.7 | 353 | 2 | 0.0[15] | 95.0 | 9,088 | 481 | 0.2[13] | 97.7 | 46,707 | 1,201 | 0.3[10] | ||

7.3. General convex quadratic functions

The quadratic matrices used in the previous computations had specific structures, given by the applications considered. Although our results are for M-matrices, in this section, we test the strength of the formulations for more general problems, with dense matrices having positive and negative off-diagonal entries. To employ the results developed for M-matrices, we simply apply the strengthening on the pairs of variables with a negative off-diagonal entry. Toward this end, we consider the mean-variance portfolio optimization

| s.t. | |||

where the objective is to minimize the portfolio variance , where is a covariance matrix, subject to meeting a target return and satisfying sparsity constraints.

Instances

In order test the effect of positive off-diagonal elements and diagonal dominance, the matrix is constructed as follows: Let be a parameter that controls the magnitude of the positive off-diagonal entries of , and be a parameter that controls the diagonal dominance of . First, we construct a factor matrix , where each entry in in drawn uniformly from , and an exposure matrix such that with probability , and is drawn uniformly from , otherwise. Then we construct an auxiliary matrix . Then, for , we set if , and we set otherwise222The matrices generated this way have only 20.1% of the off-diagonal entries negative on average – the rest are positive if and if . The ratio of the magnitude of the negative entries vs. the total, i.e., , is on average if , if and if .. Finally, is drawn uniformly from , where , and . Observe that the auxiliary matrix represents a low-rank matrix obtained from a 20-factor model, and is a diagonal matrix representing the residual variances not explained by the factor model. The matrix is obtained by scaling the positive off-diagonals of by , and updating the diagonal entries to ensure positive definiteness by imposing diagonal dominance. Additionally, is drawn uniformly between and . Finally, we let and for “small” instances, and and for “large” instances.

Formulations

We test the same formulations as in Section 7.1. In this case, the diagonal matrix is used for the Perspective formulation. In particular, formulations Perspective+cuts, Conic and Conic+cuts are based on the decomposition of the objective function given by

| s.t. |

where for and . By construction, is positive semi-definite.

Results

Table 3 presents the results for matrices with non-positive off diagonal entries (i.e., ) and varying diagonal dominance . Table 4 presents the results for matrices with fixed diagonal dominance and varying magnitudes for positive off-diagonal entries . We see that, in all cases formulation Conic results in better root gap improvements than Perspective and Basic. The gap improvements depend on the parameters and . In Table 3 we see that Conic formulation closes an additional 30% to 40% gap with respect to Perspective (independent of the diagonal dominance ). In Table 4 we observe that, as expected, Conic formulation is more effective at closing root gaps when the magnitude for the positive off-diagonal entries is small. Nevertheless, for all instances formulations Conic and Conic+cuts result in significantly stronger root improvements than Perspective (at least 15%, and often much more) and the number of nodes required to solve the instances is decreased by at least an order of magnitude.

| igap | Basic | Perspective | Perspective+cuts | Conic | Conic+cuts | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| nodes | time | egap | rimp | nodes | time | egap | rimp | nodes | time | egap | rimp | nodes | time | egap | rimp | nodes | time | egap | ||||

| 60 | 0.1 | 88.2 | 86 | 0.0[5] | 7.2 | 99 | 0.0[5] | 19.2 | 15,230 | 544 | 0.0[5] | 43.6 | 3,704 | 107 | 0.0[5] | 43.9 | 4,653 | 154 | 0.0[5] | |||

| 0.5 | 80.2 | 103 | 0.0[5] | 28.0 | 47 | 0.0[5] | 38.9 | 3,243 | 92 | 0.0[5] | 66.1 | 1,783 | 44 | 0.0[5] | 66.6 | 1,567 | 49 | 0.0[5] | ||||

| 1.0 | 74.0 | 121 | 0.0[5] | 44.4 | 18 | 0.0[5] | 52.8 | 1,335 | 35 | 0.0[5] | 81.5 | 863 | 14 | 0.0[5] | 82.3 | 709 | 19 | 0.0[5] | ||||

| Average | 103 | 0.0[15] | 26.5 | 55 | 0.0[15] | 37.0 | 6,603 | 224 | 0.0[15] | 63.7 | 2,117 | 55 | 0.0[15] | 64.3 | 2,310 | 74 | 0.0[15] | |||||

| 80 | 0.1 | 90.3 | 3,600 | 9.7[0] | 7.2 | 3,600 | 10.1[0] | 4.0 | 31,194 | 3,600 | 16.1[0] | 37.0 | 26,657 | 2,758 | 5.7[2] | 37.3 | 36,998 | 2,776 | 4.6[2] | |||

| 0.5 | 82.8 | 3,600 | 10.5[0] | 28.2 | 2,902 | 2.8[3] | 16.8 | 29,220 | 3,017 | 4.0[2] | 60.2 | 11,367 | 1,108 | 0.0[5] | 60.4 | 13,898 | 1,208 | 0.0[5] | ||||

| 1.0 | 77.0 | 3,600 | 9.5[0] | 44.1 | 988 | 0.0[5] | 27.2 | 4,889 | 566 | 0.0[5] | 78.4 | 2,689 | 183 | 0.0[5] | 79.0 | 3,395 | 233 | 0.0[5] | ||||

| Average | 3,600 | 9.9[0] | 26.5 | 2,496 | 4.3[8] | 16.0 | 21,768 | 2,394 | 6.7[7] | 58.5 | 13,571 | 1,350 | 1.9[12] | 58.9 | 18,097 | 1,406 | 1.5[12] | |||||

| 100 | 0.1 | 90.2 | 3,600 | 30.0[0] | 6.4 | 3,600 | 29.3[0] | 2.8 | 14,855 | 3,600 | 35.8[0] | 37.1 | 19,660 | 3,600 | 19.6[0] | 37.0 | 17,047 | 3,600 | 21.6[2] | |||

| 0.5 | 83.0 | 3,600 | 27.5[0] | 25.2 | 3,600 | 18.7[0] | 12.8 | 11,912 | 3,600 | 16.4[0] | 58.6 | 16,398 | 3,432 | 7.7[1] | 58.7 | 18,645 | 3,600 | 7.9[0] | ||||

| 1.0 | 77.3 | 3,600 | 25.0[0] | 39.9 | 3,600 | 10.0[0] | 19.7 | 16,144 | 3,236 | 4.8[1] | 75.0 | 11,376 | 1,824 | 2.1[3] | 75.4 | 10,588 | 1,822 | 2.5[3] | ||||

| Average | 3,600 | 27.5[0] | 23.8 | 3,600 | 19.3[0] | 11.8 | 14,304 | 3,479 | 19.0[1] | 56.9 | 15,811 | 2,952 | 9.8[4] | 57.1 | 15,426 | 3,007 | 10.7[3] | |||||

| igap | Basic | Perspective | Perspective+cuts | Conic | Conic+cuts | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| nodes | time | egap | rimp | nodes | time | egap | rimp | nodes | time | egap | rimp | nodes | time | egap | rimp | nodes | time | egap | ||||

| 60 | 0.1 | 62.4 | 153 | 0.0[5] | 46.0 | 22 | 0.0[5] | 56.1 | 10,165 | 62 | 0.0[5] | 77.6 | 2,141 | 19 | 0.0[5] | 78.1 | 2,065 | 23 | 0.0[5] | |||

| 0.2 | 57.3 | 144 | 0.0[5] | 46.8 | 22 | 0.0[5] | 56.4 | 16,642 | 89 | 0.0[5] | 73.5 | 3,314 | 20 | 0.0[5] | 73.9 | 3,261 | 24 | 0.0[5] | ||||

| 0.5 | 51.2 | 128 | 0.0[5] | 48.0 | 19 | 0.0[5] | 53.6 | 22,526 | 137 | 0.0[5] | 65.1 | 8,635 | 36 | 0.0[5] | 65.5 | 8,742 | 60 | 0.0[5] | ||||

| Average | 142 | 0.0[15] | 46.9 | 21 | 0.0[15] | 55.4 | 16,444 | 96 | 0.0[15] | 72.1 | 4,696 | 25 | 0.0[15] | 72.5 | 4,689 | 36 | 0.0[15] | |||||

| 80 | 0.1 | 64.4 | 3,600 | 7.6[0] | 46.9 | 852 | 0.0[5] | 32.8 | 53,774 | 1,401 | 0.4[4] | 77.4 | 8,979 | 244 | 0.0[5] | 78.2 | 8,551 | 183 | 0.0[5] | |||

| 0.2 | 58.8 | 3,600 | 5.9[0] | 48.1 | 881 | 0.0[5] | 37.8 | 98,151 | 1,997 | 0.6[4] | 74.3 | 25,152 | 349 | 0.0[5] | 75.4 | 22,630 | 327 | 0.0[5] | ||||

| 0.5 | 51.8 | 3,255 | 3.2[1] | 49.7 | 391 | 0.0[5] | 43.7 | 185,839 | 2,462 | 0.4[4] | 67.8 | 66,779 | 482 | 0.0[5] | 68.5 | 64,512 | 535 | 0.0[5] | ||||

| Average | 3,485 | 5.5[1] | 48.2 | 708 | 0.0[15] | 38.1 | 112,588 | 1,953 | 0.5[12] | 73.2 | 33,637 | 358 | 0.0[15] | 74.0 | 31,898 | 349 | 0.0[15] | |||||

| 100 | 0.1 | 65.0 | 3,600 | 23.1[0] | 42.3 | 3,600 | 9.1[0] | 28.8 | 65,628 | 3,600 | 6.4[0] | 73.0 | 83,300 | 2,667 | 2.5[2] | 73.8 | 67,074 | 2,904 | 2.6[2] | |||

| 0.2 | 59.4 | 3,600 | 20.9[0] | 43.9 | 3,600 | 7.8[0] | 32.9 | 72,439 | 3,600 | 9.0[0] | 70.6 | 122,553 | 3,031 | 2.8[2] | 71.2 | 116,173 | 3,033 | 3.3[1] | ||||

| 0.5 | 52.5 | 3,600 | 17.2[0] | 46.2 | 3,600 | 5.4[0] | 39.1 | 136,082 | 3,600 | 7.7[0] | 64.4 | 261,440 | 3,327 | 3.8[1] | 64.8 | 270,701 | 3,396 | 3.7[1] | ||||

| Average | 3,600 | 20.4[0] | 44.2 | 3,600 | 7.4[0] | 33.6 | 91,383 | 3,600 | 7.4[0] | 69.3 | 155,764 | 3,008 | 3.0[5] | 69.9 | 151,316 | 3,111 | 3.2[4] | |||||

Observe that the stronger formulations of Conic and Conic+cuts do not necessarily lead to better solution times for small instances. Nevertheless, for the larger instances (), using the Conic formulation leads to faster solution times, lower end gaps and more instances solved to optimality for all values of and . As in Section 7.1, we observe little difference between Conic and Conic+cuts — consistent with Proposition 8— and that Perspective+cuts is not effective in closing the root gap. Approximating the nonlinear function with gradient inequalities appears to cause numerical issues as adding cuts weakens the relaxation contrary to expectations. Please see our comments at the end of Section 7.1.

Finally, observe that the formulations tested require adding additional variables, one for each negative off-diagonal entry in . Thus, solving the continuous relaxations may be computationally expensive for large values of . Table 5 illustrates this point for matrices with and . It shows, for the Basic, Perspective and Conic formulations, the value of the best feasible solution found (sol), the value of the lower bound after one hour of branch and bound (ebound), the value of the lower bound after processing the root node (rbound), the time used to process the root node in seconds (rtime), and the number of nodes explored in one hour (nodes). Each row represents the average over five instances, and the values of sol, ebound and rbound are scaled so that the best feasible solution found for a given instance has value . Observe that for the lower bound found by Conic at the root node is stronger than the lower bounds found by other formulations after one hour of branch-and-bound. However, the continuous relaxations of Conic are difficult to solve for large values of , leading to few branch-and-bound nodes explored and few or no feasible solutions found within the time limit.

| Basic | Perspective | Conic | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| sol | ebound | rbound | rtime | nodes | sol | ebound | rbound | rtime | nodes | sol | ebound | rbound | rtime | nodes | |

| 100 | 100.0 | 94.9 | 11.0 | 0.09 | 12,375,694 | 100.0 | 100.0 | 42.2 | 0.05 | 1,968,600 | 100.0 | 100.0 | 77.9 | 2.13 | 2,176 |

| 150 | 100.0 | 61.3 | 11.7 | 0.07 | 9,739,922 | 100.3 | 81.3 | 45.6 | 0.08 | 3,788,060 | 100.6 | 96.2 | 83.8 | 141.46 | 3,174 |

| 200 | 100.0 | 46.5 | 12.4 | 0.11 | 6,382,960 | 100.3 | 72.5 | 48.4 | 0.13 | 2,644,816 | - | 90.8 | 86.4 | 1090.73 | 1,531 |

| 250 | 100.0 | 34.7 | 11.6 | 0.22 | 4,092,948 | 100.3 | 72.5 | 48.4 | 0.21 | 1,692,204 | - | 82.7 | 82.7 | 1732.13 | 3 |

| 300 | 100.0 | 29.5 | 12.0 | 0.41 | 2,763,780 | 100.9 | 61.0 | 47.1 | 0.32 | 1,166,534 | - | 86.1 | 86.1 | 2333.81 | 1 |

A possible approach that achieves a compromise between the strength and the size of the formulation is to apply the proposed conic inequalities for a subset of the matrix: given an M-matrix Q, choose and use the formulation

| s.t. |

In particular, if , then the results in Section 7.1 suggest that the formulations would scale well. Additionally, the component corresponding to the remainder, , could be further strengthened by linear inequalities (37) (and other subgradient inequalities corresponding to points where ) in the original space of variables instead of extended reformulations. An effective implementation of such a partial strengthening is beyond the scope of the current paper.

8. Conclusions

In this paper we show, under mild assumptions, that minimization of a quadratic function with an M-matrix with indicator variables is a submodular minimization problem, hence, solvable in polynomial time. We derive strong formulations using the convex hull description of non-separable quadratic terms with two indicator variables arising from a decomposition of the quadratic function. Additionally, we provide strong conic quadratic valid inequalities approximating the convex hulls. The derived formulations generalize previous results in the binary case and separable case, and the inequalities dominate valid inequalities given in the literature. Computational experiments indicate that the proposed conic formulations may be significantly more effective compared to the natural convex relaxation and the perspective reformulation.

References

- Ahuja et al [2004] Ahuja RK, Hochbaum DS, Orlin JB (2004) A cut-based algorithm for the nonlinear dual of the minimum cost network flow problem. Algorithmica 39:189–208

- Aktürk et al [2009] Aktürk MS, Atamtürk A, Gürel S (2009) A strong conic quadratic reformulation for machine-job assignment with controllable processing times. Oper Res Lett 37:187–191

- Anstreicher [2012] Anstreicher KM (2012) On convex relaxations for quadratically constrained quadratic programming. Mathematical Programming 136:233–251

- Atamtürk and Bhardwaj [2018] Atamtürk A, Bhardwaj A (2018) Network design with probabilistic capacities. Networks 71:16–30

- Atamtürk and Gomez [2017] Atamtürk A, Gomez A (2017) Submodularity in conic quadratic mixed 0-1 optimization. arXiv preprint arXiv:170505918

- Atamtürk and Jeon [2017] Atamtürk A, Jeon H (2017) Lifted polymatroid for mean-risk optimization with indicator variables. BCOL Research Report 17.01, UC Berkeley

- Atamtürk and Narayanan [2007] Atamtürk A, Narayanan V (2007) Cuts for conic mixed integer programming. In: Fischetti M, Williamson DP (eds) Proceedings of the 12th International IPCO Conference, pp 16–29

- Balas [1985] Balas E (1985) Disjunctive programming and a hierarchy of relaxations for discrete optimization problems. SIAM Journal on Algebraic Discrete Methods 6:466–486

- Belotti et al [2015] Belotti P, Góez JC, Pólik I, Ralphs TK, Terlaky T (2015) A conic representation of the convex hull of disjunctive sets and conic cuts for integer second order cone optimization. In: Numerical Analysis and Optimization, Springer, pp 1–35

- Bertsimas et al [2016] Bertsimas D, King A, Mazumder R (2016) Best subset selection via a modern optimization lens. The Annals of Statistics 44:813–852

- Bienstock [1996] Bienstock D (1996) Computational study of a family of mixed-integer quadratic programming problems. Mathematical Programming 74:121–140

- Bienstock and Michalka [2014] Bienstock D, Michalka A (2014) Cutting-planes for optimization of convex functions over nonconvex sets. SIAM Journal on Optimization 24:643–677

- Boland et al [2017a] Boland N, Dey SS, Kalinowski T, Molinaro M, Rigterink F (2017a) Bounding the gap between the McCormick relaxation and the convex hull for bilinear functions. Mathematical Programming 162(1-2):523–535

- Boland et al [2017b] Boland N, Gupte A, Kalinowski T, Rigterink F, Waterer H (2017b) Extended formulations for convex hulls of graphs of bilinear functions. arXiv preprint arXiv:170204813

- Bonami et al [2015] Bonami P, Lodi A, Tramontani A, Wiese S (2015) On mathematical programming with indicator constraints. Mathematical Programming 151:191–223

- Boykov et al [2001] Boykov Y, Veksler O, Zabih R (2001) Fast approximate energy minimization via graph cuts. IEEE Transactions on Pattern Analysis and Machine Intelligence 23:1222–1239

- Ceria and Soares [1999] Ceria S, Soares J (1999) Convex programming for disjunctive convex optimization. Mathematical Programming 86:595–614

- Cornuejols and Tütüncü [2006] Cornuejols G, Tütüncü R (2006) Optimization Methods in Finance, vol 5. Cambridge University Press

- Dong and Linderoth [2013] Dong H, Linderoth J (2013) On valid inequalities for quadratic programming with continuous variables and binary indicators. In: Goemans M, Correa J (eds) Proc. IPCO 2013, Springer, Berlin, pp 169–180

- Edmonds [1970] Edmonds J (1970) Submodular functions, matroids, and certain polyhedra. In: Guy R, Hanani H, Sauer N, Schönenheim J (eds) Combinatorial Structures and Their Applications, Gordon and Breach, pp 69–87

- Frangioni and Gentile [2006] Frangioni A, Gentile C (2006) Perspective cuts for a class of convex 0–1 mixed integer programs. Mathematical Programming 106:225–236

- Frangioni et al [2016] Frangioni A, Gentile C, Hungerford J (2016) Decompositions of semidefinite matrices and the perspective reformulation of nonseparable quadratic programs. Report R-16-10, IASI, Rome

- Gao and Li [2011] Gao J, Li D (2011) Cardinality constrained linear-quadratic optimal control. IEEE Transactions on Automatic Control 56:1936–1941

- Günlük and Linderoth [2010] Günlük O, Linderoth J (2010) Perspective reformulations of mixed integer nonlinear programs with indicator variables. Mathematical Programming 124:183–205

- Hijazi et al [2012] Hijazi H, Bonami P, Cornuéjols G, Ouorou A (2012) Mixed-integer nonlinear programs featuring “on/off” constraints. Computational Optimization and Applications 52:537–558

- Hiriart-Urruty and Lemaréchal [2013] Hiriart-Urruty JB, Lemaréchal C (2013) Convex Analysis and Minimization Algorithms I: Fundamentals, vol 305. Springer Science & Business Media

- Hochbaum [2013] Hochbaum DS (2013) Multi-label markov random fields as an efficient and effective tool for image segmentation, total variations and regularization. Numerical Mathematics: Theory, Methods and Applications 6:169–198

- Ivănescu [1965] Ivănescu PL (1965) Some network flow problems solved with pseudo-boolean programming. Operations Research 13:388–399

- Jeon et al [2017] Jeon H, Linderoth J, Miller A (2017) Quadratic cone cutting surfaces for quadratic programs with on–off constraints. Discrete Optimization 24:32–50

- Keilson and Styan [1973] Keilson J, Styan GPH (1973) Markov chains and M-matrices: Inequalities and equalities. Journal of Mathematical Analysis and Applications 41:439–459

- Kılınç-Karzan and Yıldız [2015] Kılınç-Karzan F, Yıldız S (2015) Two-term disjunctions on the second-order cone. Mathematical Programming 154:463–491

- Kolmogorov and Zabin [2004] Kolmogorov V, Zabin R (2004) What energy functions can be minimized via graph cuts? IEEE Transactions on Pattern Analysis and Machine Intelligence 26:147–159

- Lobo et al [2007] Lobo MS, Fazel M, Boyd S (2007) Portfolio optimization with linear and fixed transaction costs. Annals of Operations Research 152:341–365

- Lovász [1983] Lovász L (1983) Submodular functions and convexity. In: Bachem A, Korte B, Grötschel M (eds) Mathematical Programming The State of the Art: Bonn 1982, Springer, Berlin, pp 235–257

- Luedtke et al [2012] Luedtke J, Namazifar M, Linderoth J (2012) Some results on the strength of relaxations of multilinear functions. Mathematical Programming 136:325–351

- Luedtke et al [2018] Luedtke J, D’Ambrosio C, Linderoth J, Schweiger J (2018) Strong convex nonlinear relaxations of the pooling problem. arXiv preprint arXiv:180302955

- Luk and Pagano [1980] Luk FT, Pagano M (1980) Quadratic programming with M-matrices. Linear Algebra and its Applications 33:15–40

- Mahajan et al [2017] Mahajan A, Leyffer S, Linderoth J, Luedtke J, Munson T (2017) Minotaur: A mixed-integer nonlinear optimization toolkit. ANL/MCS-P8010-0817, Argonne National Lab

- Modaresi et al [2016] Modaresi S, Kılınç MR, Vielma JP (2016) Intersection cuts for nonlinear integer programming: Convexification techniques for structured sets. Mathematical Programming 155:575–611

- Nemhauser et al [1978] Nemhauser GL, Wolsey LA, Fisher ML (1978) An analysis of approximations for maximizing submodular set functions I. Mathematical Programming 14:265–294

- Orlin [2009] Orlin JB (2009) A faster strongly polynomial time algorithm for submodular function minimization. Mathematical Programming 118:237–251

- Picard and Ratliff [1975] Picard JC, Ratliff HD (1975) Minimum cuts and related problems. Networks 5:357–370

- Plemmons [1977] Plemmons RJ (1977) M-matrix characterizations. I – nonsingular M-matrices. Linear Algebra and its Applications 18:175–188

- Poljak and Wolkowicz [1995] Poljak S, Wolkowicz H (1995) Convex relaxations of (0,1)-quadratic programming. Mathematics of Operations Research 20:550–561

- Stubbs and Mehrotra [1999] Stubbs RA, Mehrotra S (1999) A branch-and-cut method for 0-1 mixed convex programming. Mathematical programming 86:515–532

- Vielma [2018] Vielma JP (2018) Small and strong formulations for unions of convex sets from the cayley embedding. To appear in Mathematical Programming, arXiv preprint arXiv:1704.03954

- Wei et al [2013] Wei D, Sestok CK, Oppenheim AV (2013) Sparse filter design under a quadratic constraint: Low-complexity algorithms. IEEE T Signal Proces 61:857–870

- Wu et al [2017] Wu B, Sun X, Li D, Zheng X (2017) Quadratic convex reformulations for semicontinuous quadratic programming. SIAM Journal on Optimization 27:1531–1553

- Young [1981] Young N (1981) The rate of convergence of a matrix power series. Linear Algebra and its Applications 35:261–278