Distributions of Historic Market Data – Implied and Realized Volatility

M. Dashti Moghaddam

Zhiyuan Liu

R. A. Serota111serota@ucmail.uc.eduDepartment of Physics, University of Cincinnati,

Cincinnati, Ohio 45221-0011

Abstract

We undertake a systematic comparison between implied volatility, as represented by VIX (new methodology) and VXO (old methodology), and realized volatility. We compare visually and statistically distributions of realized and implied variance (volatility squared) and study the distribution of their ratio. We find that the ratio is best fitted by heavy-tailed – lognormal and fat-tailed (power-law) – distributions, depending on whether preceding or concurrent month of realized variance is used. We do not find substantial difference in accuracy between VIX and VXO. Additionally, we study the variance of theoretical realized variance for Heston and multiplicative models of stochastic volatility and compare those with realized variance obtained from historic market data.

keywords:

Volatility , Implied , Realized , VIX , Fat Tails

††journal: arXiv

1 Introduction

The implied volatility index VIX was created in order to estimate, looking forward, the expected realized volatility. CBOE introduced the original VIX (now VXO) in 1986. It was based on an inverted Black-Scholes formula, where S&P 100 near-term, at-the-money options were used to calculate a weighted average of volatilities. However, the Black-Scholes formula assumes that the volatility in the stock returns equation is either a constant, or at least does not have a stochastic component, while in reality it was already understood that volatility itself is stochastic in nature. A number of well-studied models of stochastic volatility have emerged, such as Heston (HM) [1, 2] and multiplicative (MM) [3, 4]. Consequently, a need arose for an implied volatility index, which would not only be based on stochastic volatility but would also be agnostic to a particular model of the latter [5, 6].

CBOE introduced its current VIX methodology on September 22, 2003 [7] to fulfill the above requirements and was based on [8, 9], where a closed-form formula for the expected value of realized volatility [10] was derived using call and put prices. Notably, it utilized the S&P 500 index, which is far more representative of the total market, both near-term and next-term options and a broader range of strike prices. CBOE publishes historic data using both methodologies, VIX (new) and VXO (old) dating back to 1990 [11] (historic stock prices used in calculation of realized volatility can be found at [12]). Here we call 1990 through September 19, 2003 VIX Archive and VXO Archive and from September 22, 2003 through December 30, 2016 VIX Current and VXO Current.

Naturally, the question arises of whether VIX, designed to be a superior methodology, has a better track record than VXO. The short answer is that it is unclear. All-in-all, VIX/VXO is still too young to have accumulated sufficient amount of data and only time will tell how reliable it is in predicting realized volatility. Still, one of our notable observations discussed below is that the ratio of realized to implied variance (squared volatility) is best fitted with a fat-tailed (power-law) distribution, which clearly signals occasional large discrepancies between prediction and realization. This is not surprising, given that we are trying to predict the future (by pricing options) based on what we know today and thus are unaware of unexpected future events that can spike the volatility.

On the other hand, we also find that the distribution of the ratio of realized variance of the preceding month to the implied volatility, as well as of its inverse, is distributed with lognormal distribution. While the latter is heavy-tailed, this nonetheless shows that VIX is better attuned to the known volatility. We note a recent surmise that VIX can be manipulated [13, 14] and that Nasdaq is working on its own volatility index [15]. Hopefully, this work will establish a proper framework for testing implied volatility indices.

This paper is the second in a series devoted to analysis of historic market data, the other two discussing, respectively, stock returns [16] and relaxation and correlations [17]. It is organized as follows. In Section 2 we give a detailed visual and statistical comparison between realized volatility () and implied volatility represented by VIX and VXO. More precisely, we compare distributions of realized variance with and and, in particular, we analyze KS statistics of fits of and by various distributions, from normal to fat-tailed. In Section 3 we compare the variance of the distribution against the analytical results obtained using Heston and multiplicative models respectively. We conclude with the discussion of open questions and future work.

2 Comparing distributions of and

2.1 Definitions, rescaling and normality

Realized variance (index) is defined as follows

(1)

where

(2)

are daily returns and is the reference (closing) price on day . Time-averaged realized variance can be calculated from stochastic volatility [10], [16] as

(3)

Evaluation of the implied volatility is based on the evaluation of the expectation value of (3) [8, 9]. VIX uses options prices to estimate this expectation value via the generalized formula [7]

(4)

where is the time to expiration; is the forward index level desired from index option price; is the first strike below the forward index level, ; is the strike price of th out-of-money option: a call if , a put if and both a put and a call if ; is the interval between strike prices, that is half the difference between the strike on either side of , ; is the risk-free interest rate to expiration and is the midpoint of bid-ask spread for each option with strike . This formula is then used for near- and next-term options [7] and the final expression for VIX is effectively an average between the two so the latter and the sum in (4) are intended to approximate the time average in (3).

VIX and VXO were designed to measure a 30-day expected volatility. However, in their final form and are annualized by the ratio of [7]. As is clear from (1), is also annualized and for comparison with VIX/VXO, we should take , so that ; unlike VIX/VXO, RV is calculated based on the number of trading days. Accordingly, to compare the distributions of and with , we must rescale one of them with the ratio of their mean values. Table 1 lists ratios of the mean of and over the mean of . In what follows, the distributions of are rescaled with the respective ratios from Table 1. We also analyze data for VIX Current and VXO Current both in aggregate form and split nearly evenly for a period covering the financial crisis and after (see Appendix).

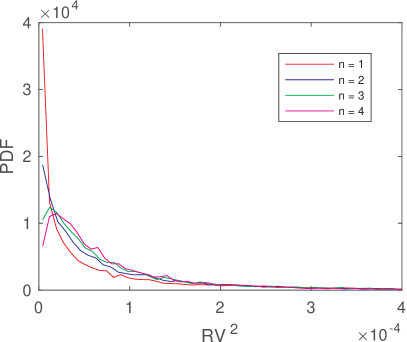

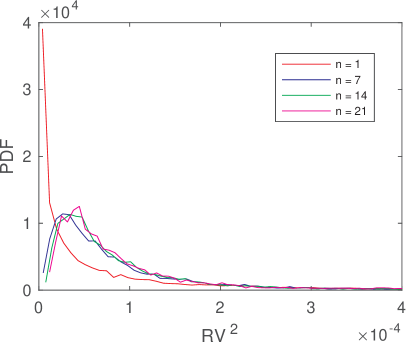

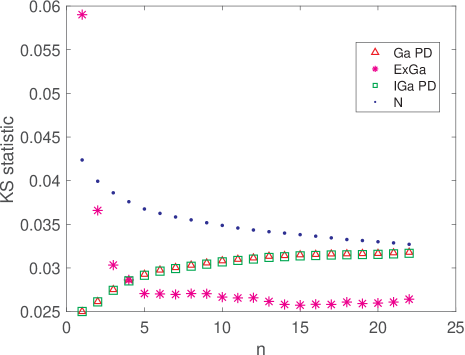

It should be emphasized that for in (1) the distribution of should be approaching normal. Fig. 1 hints at that but with an extended tail. The tail may be exponential or power-law, depending on how single-day returns are distributed. While the longer-time returns are better described by the Heston model and exponential tails [16], single-day returns is still an open question. As always, the tail behavior is hard to pinpoint, especially with smaller data sets. Fig. 2 confirms the distribution approach to modified normality.

Figure 1: PDFs of for 1,2,3,4 (left) and 1,7,14,21 (right).

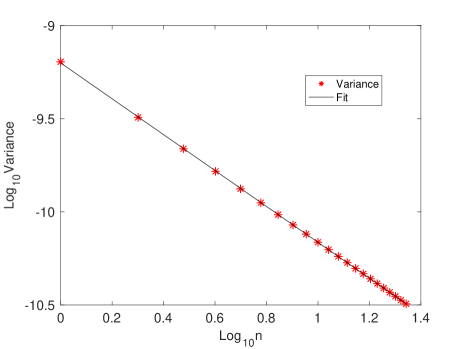

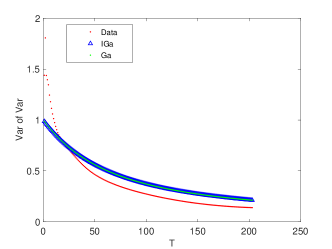

Figure 2: Left: Kolmogorov-Smirnov statistics for fitting ; lower numbers indicate a better fit. N and ExGa are normal and exGaussian distributions respectively. Ga PD and IGa PD are product distributions of gamma and inverse gamma distributions respectively and normal distribution – which describe the distributions of stock returns in the Heston and multiplicative models [16] – modified by a change of variables to squared returns. Right: Log-log plot of the variance of the distribution versus . The slope of the straight-line fit is -0.9635.

2.2 Visual comparison of realized volatility and VIX/VXO

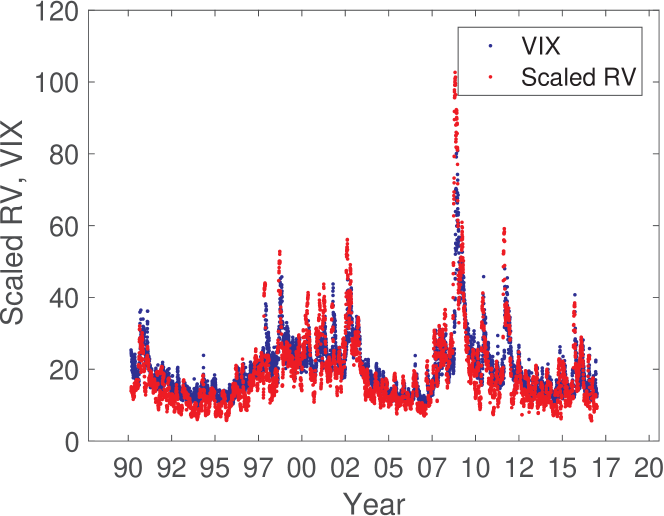

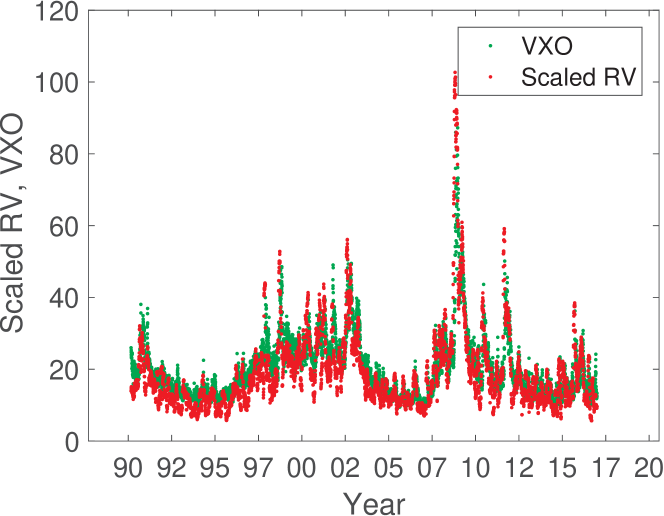

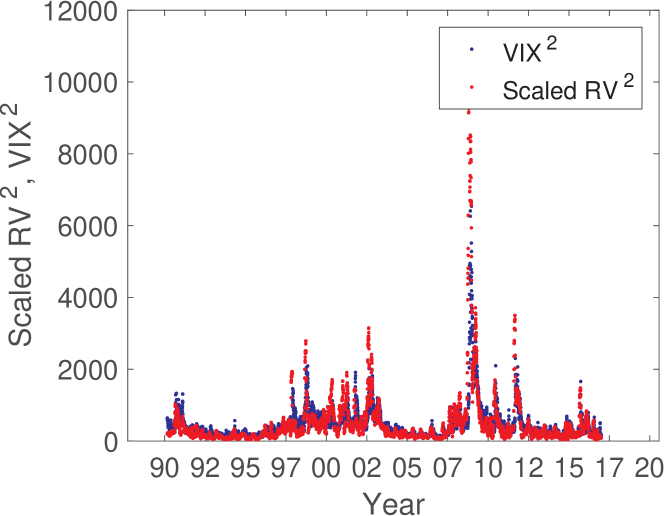

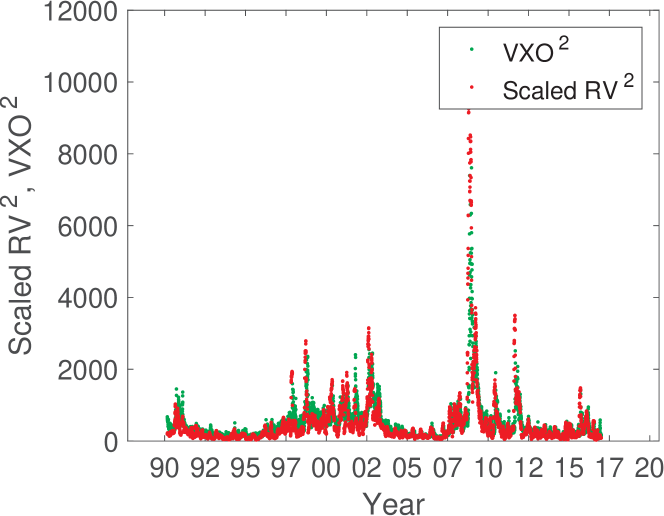

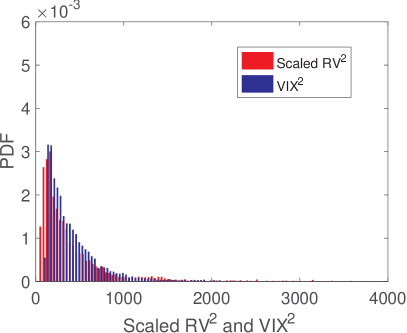

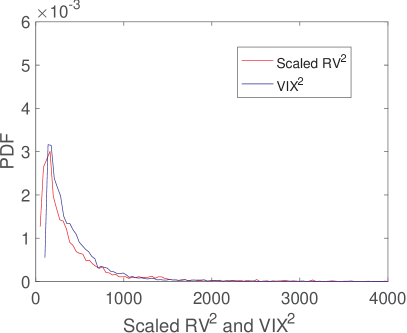

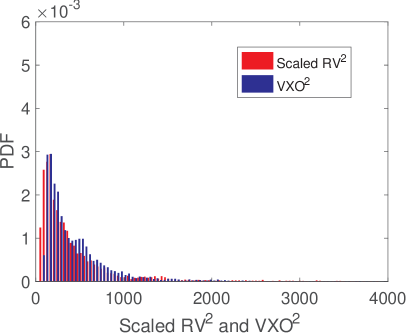

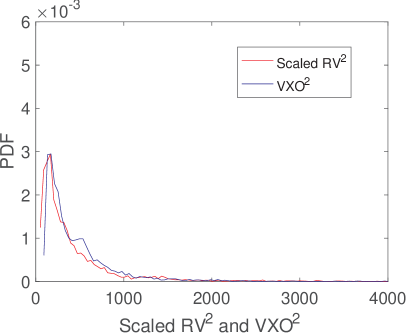

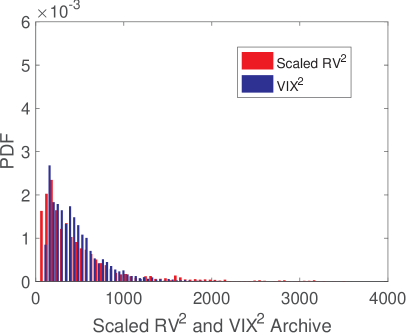

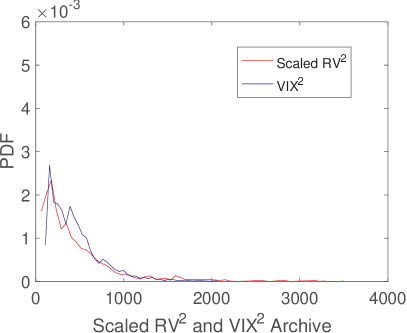

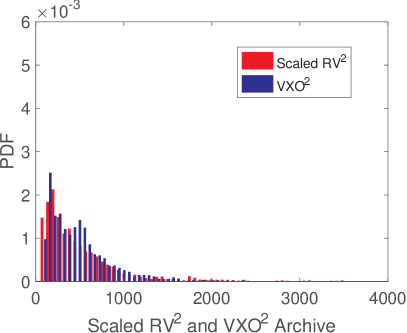

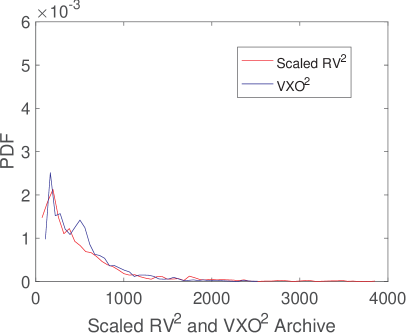

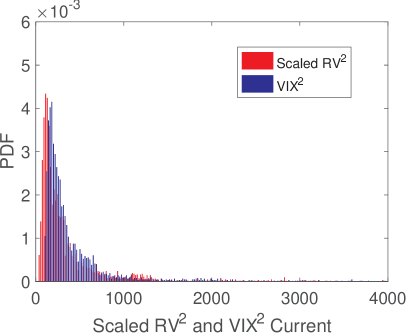

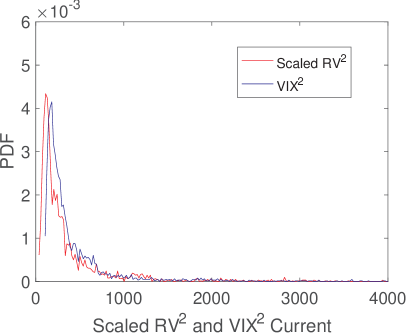

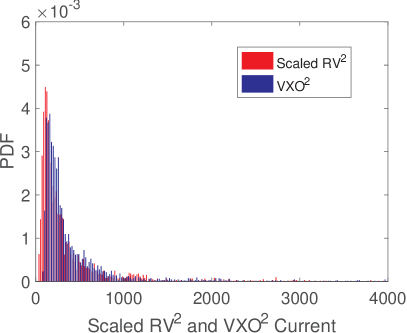

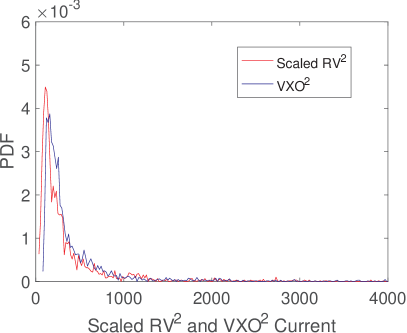

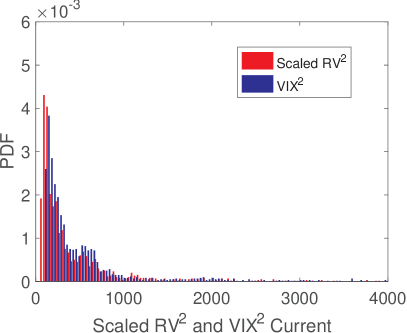

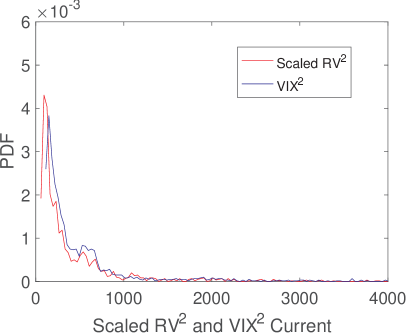

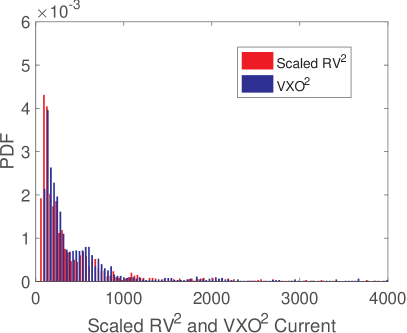

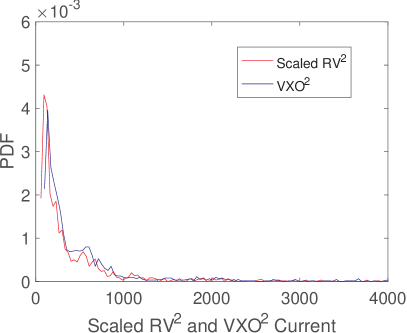

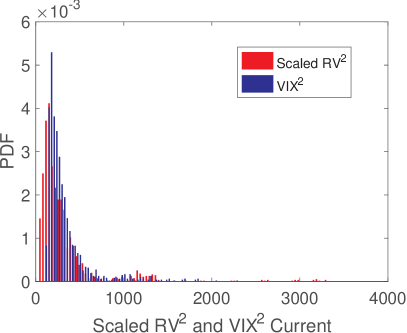

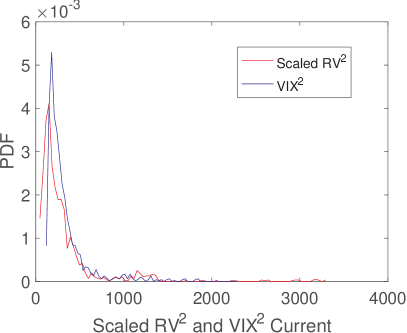

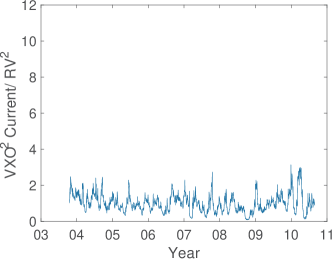

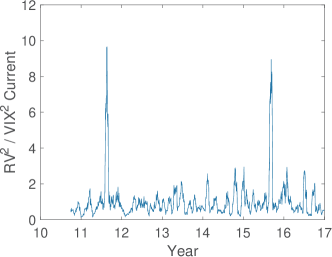

As previously mentioned, realized variance is scaled by entries in Table 1. In Figs. 3 and 4 (which is just exaggerated, squared version of 3) we show scaled RV and scaled vis-a-vis their volatility indices counterparts. In Figs. 5-10 we show histograms and their contour plots for vis-a-vis and . KS statistics for comparing the latter two with the scaled is collected in Table 2 (lower numbers correspond to a better match). Further split of the 2003-2016 data is summarized in the Appendix.

Table 1: Ratio of mean

Theory

Ratio

1.4484

1.4286

Date

Ratio

1990-2016

1.4911

1990-2003

1.6691

2003-2016

1.3446

2003-2010

1.2861

2010-2016

1.4104

Theory

Ratio

1.4484

1.4286

Date

Ratio

1990-2016

1.5257

1990-2003

1.8372

2003-2016

1.2985

2003-2010

1.2850

2010-2016

1.3097

Table 2: KS test results

Date

KS statistic

1990-2016

0.1723

1990-2003

0.1478

2003-2016

0.2394

2003-2010

0.2215

2010-2016

0.2734

Date

KS statistic

1990-2016

0.1589

1990-2003

0.1632

2003-2016

0.2157

2003-2010

0.2034

2010-2016

0.2376

Figure 3: VIX (top) and VXO (bottom) with scaled RV, from Jan 2nd, 1990 to Dec 30th, 2016.

Figure 4: (top) and (bottom) with Scaled , from Jan 2nd, 1990 to Dec 30th, 2016.

Figure 5: PDFs of scaled and from Jan 2nd, 1990 to Dec 30th, 2016.

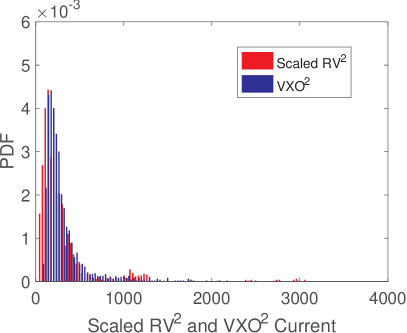

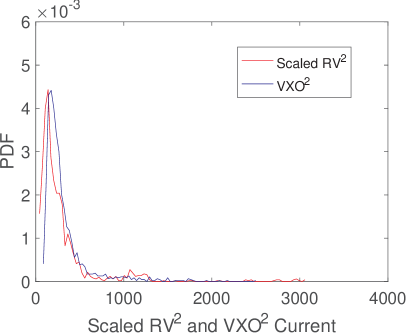

Figure 6: PDFs of scaled and from Jan 2nd, 1990 to Dec 30th, 2016.

Figure 7: PDFs of scaled and from Jan 2nd, 1990 to Sep 19th, 2003.

Figure 8: PDFs of scaled and from Jan 2nd, 1990 to Sep 19th, 2003.

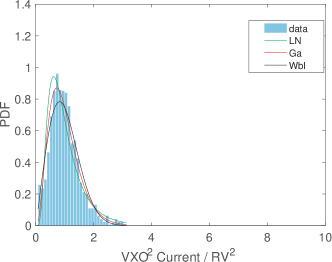

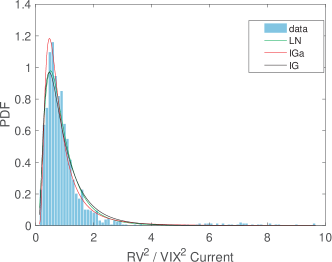

Figure 9: PDFs of scaled and from Sep 22nd, 2003 to Dec 30th, 2016.

Figure 10: PDFs of scaled and from Sep 22nd, 2003 to Dec 30th, 2016.

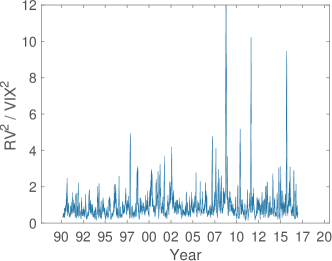

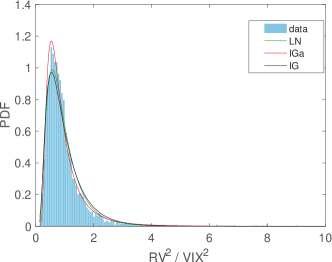

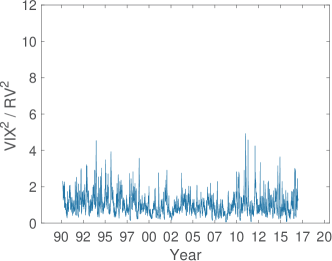

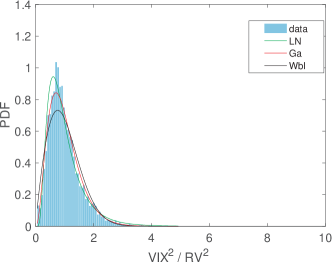

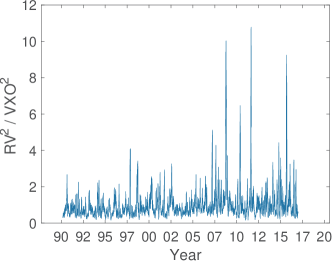

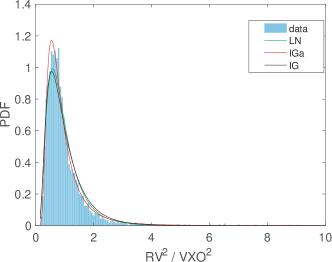

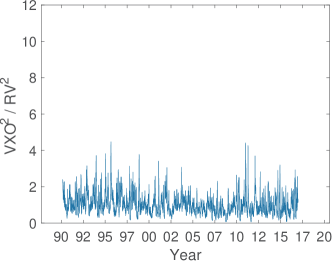

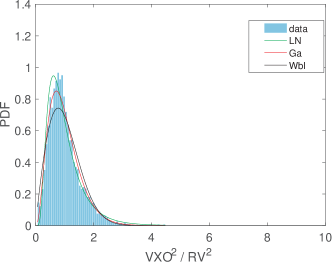

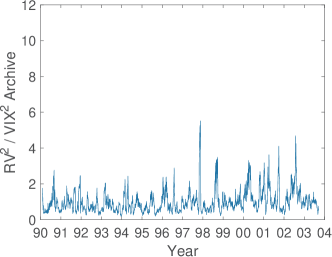

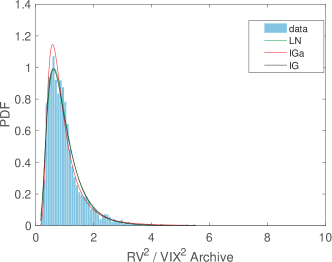

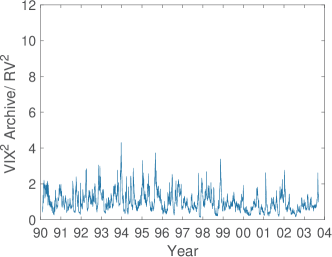

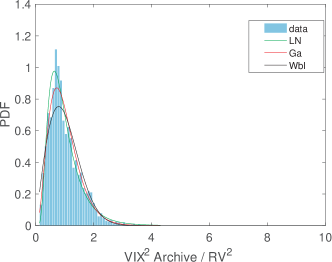

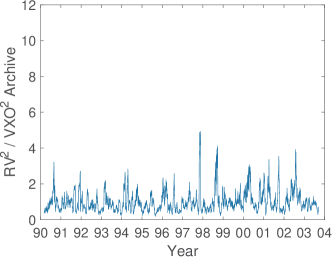

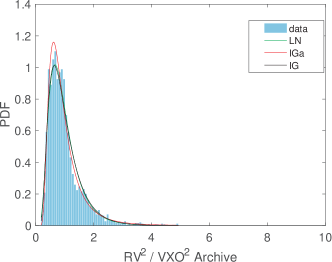

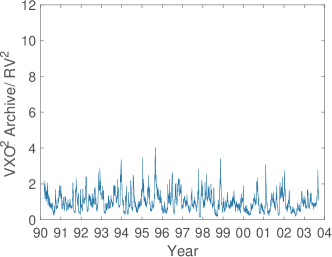

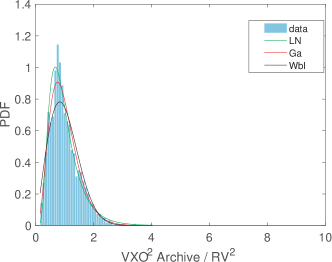

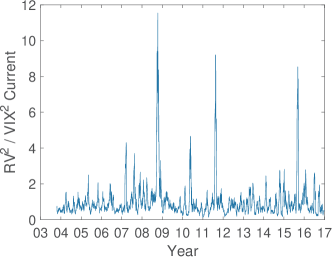

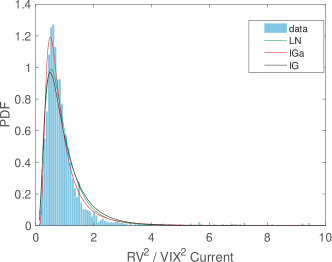

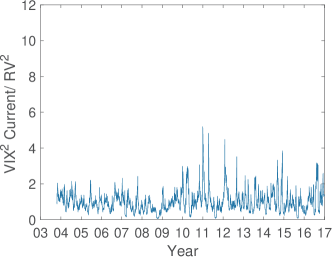

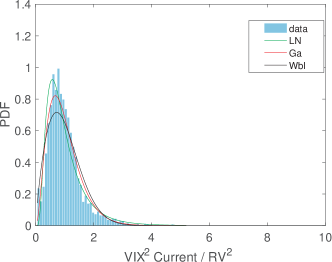

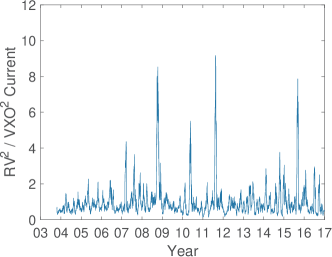

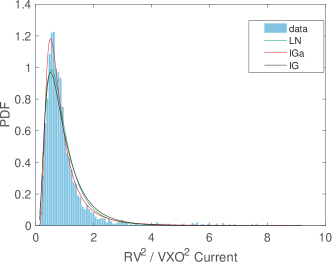

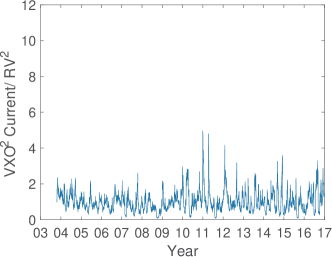

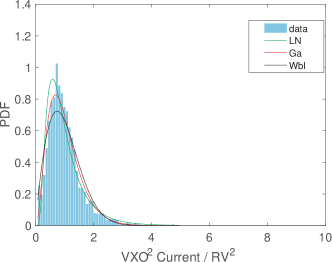

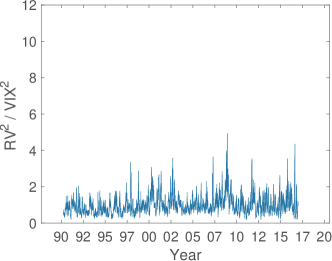

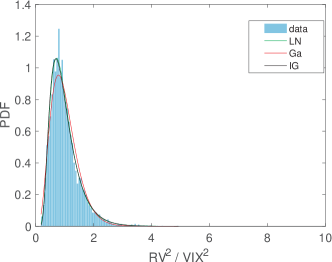

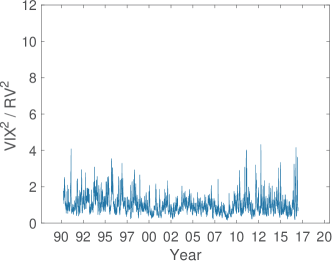

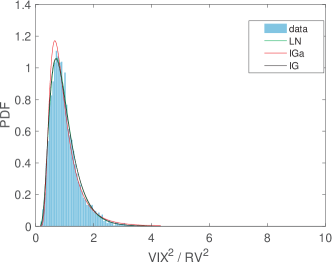

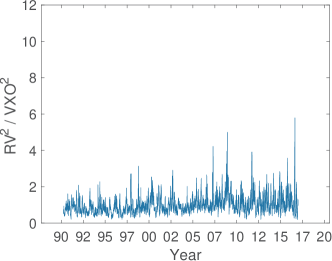

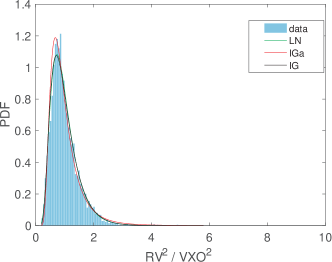

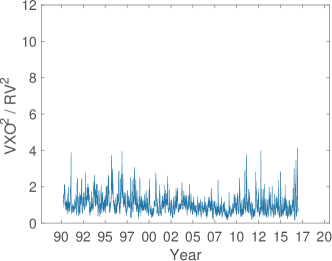

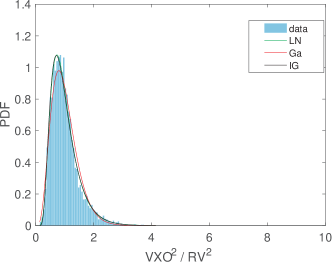

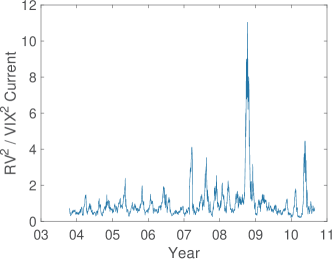

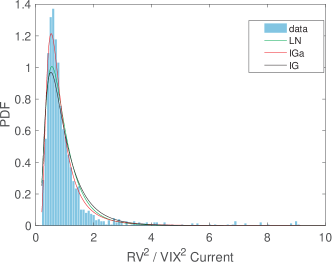

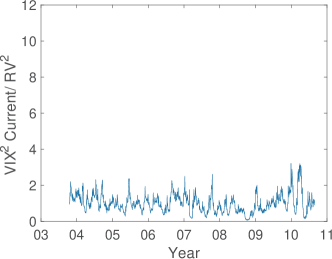

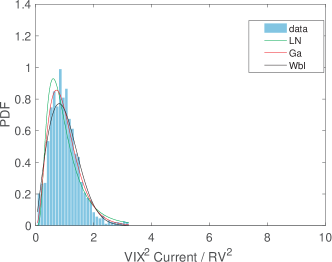

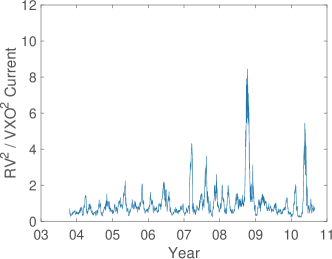

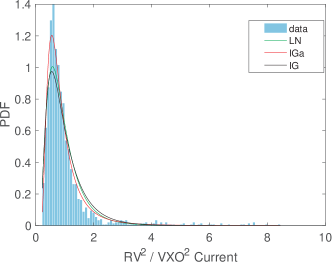

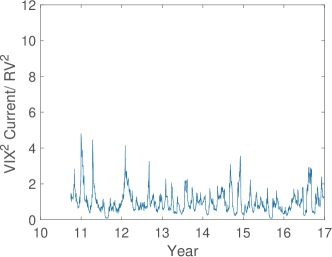

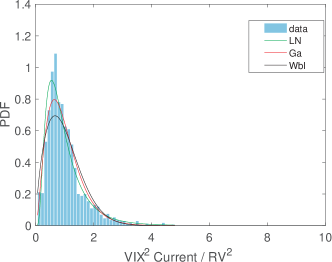

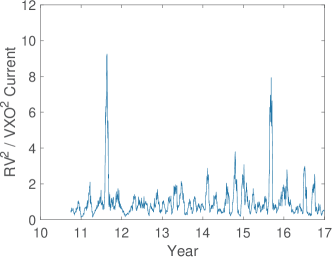

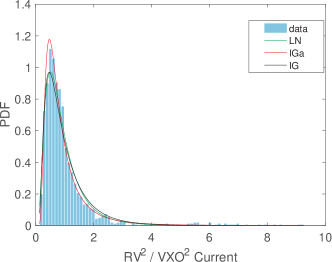

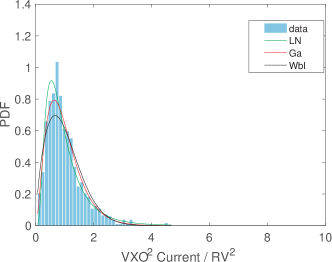

2.3 Ratio distribution

To further compare the volatilities, we examined the ratios and . In plots below we show their time series and distribution functions. The latter are fitted using maximum likelihood estimation (MLE) and the parameters of the fits and KS statistics are collected in the tables. Six functions – normal, lognormal, inverse gamma, gamma, Weibull and inverse Gaussian were used but only three best fits are shown with data PDFs. Clearly, barring VIX Archive, the fat-tailed IGa was the best fit. The hypothesis is that fat tails are due to sudden spikes in RV. The inverse distributions and are given to illustrate that there were no unexpected surges in VIX and illustrate consistency of MLE.

Figure 11: , from Jan 2nd, 1990 to Dec 30th, 2016.

Figure 12: , from Jan 2nd, 1990 to Dec 30th, 2016.

Table 3: MLE results for “” and “”

type

parameters

KS Statistic

Normal

N( 1.0000, 0.9067)

0.1940

LogNormal

LN( -0.2027, 0.5867)

0.0446

IGa

IGa( 3.3595, 2.3466)

0.0246

Gamma

Gamma( 2.6219, 0.3814)

0.0978

Weibull

Weibull( 1.1124, 1.4009)

0.1224

IG

IG( 1.0000, 2.3168)

0.0607

type

parameters

KS Statistic

Normal

N( 1.0000, 0.5626)

0.0972

LogNormal

LN( -0.1562, 0.5867)

0.0446

IGa

IGa( 2.6219, 1.8314)

0.0978

Gamma

Gamma( 3.3595, 0.2977)

0.0246

Weibull

Weibull( 1.1306, 1.8882)

0.0500

IG

IG( 1.0000, 2.3168)

0.0734

Figure 13: , Jan 2nd, 1990 to Dec 30th, 2016.

Figure 14: , from Jan 2nd, 1990 to Dec 30th, 2016.

Table 4: MLE results for “” and “”

type

parameters

KS Statistic

Normal

N( 1.0000, 0.8747)

0.1910

LogNormal

LN( -0.1973, 0.5795)

0.0449

IGa

IGa( 3.4629, 2.4438)

0.0224

Gamma

Gamma( 2.6897, 0.3718)

0.0971

Weibull

Weibull( 1.1150, 1.4256)

0.1230

IG

IG( 1.0000, 2.3981)

0.0611

type

parameters

KS Statistic

Normal

N( 1.0000, 0.5467)

0.0925

LogNormal

LN( -0.1513, 0.5795)

0.0449

IGa

IGa( 2.6897, 1.8982)

0.0971

Gamma

Gamma( 3.4629, 0.2888)

0.0224

Weibull

Weibull( 1.1308, 1.9374)

0.0499

IG

IG( 1.0000, 2.3981)

0.0729

Figure 15: , from Jan 2nd, 1990 to Sep 19th, 2003.

Figure 16: , from Jan 2nd, 1990 to Sep 19th, 2003.

Table 5: MLE results for “” and “”

type

parameters

KS Statistic

Normal

N( 1.0000, 0.6380)

0.1421

LogNormal

LN( -0.1570, 0.5460)

0.0275

IGa

IGa( 3.6963, 2.7429)

0.0358

Gamma

Gamma( 3.3420, 0.2992)

0.0640

Weibull

Weibull( 1.1310, 1.7263)

0.0913

IG

IG( 1.0000, 2.8769)

0.0344

type

parameters

KS Statistic

Normal

N( 1.0000, 0.5372)

0.1011

LogNormal

LN( -0.1413, 0.5460)

0.0275

IGa

IGa( 3.3420, 2.4800)

0.0640

Gamma

Gamma( 3.6963, 0.2705)

0.0358

Weibull

Weibull( 1.1328, 1.9825)

0.0578

IG

IG( 1.0000, 2.8768)

0.0419

Figure 17: , from Jan 2nd, 1990 to Sep 19th, 2003.

Figure 18: , from Jan 2nd, 1990 to Sep 19th, 2003.

Table 6: MLE results for “” and “”

type

parameters

KS Statistic

Normal

N( 1.0000, 0.6013)

0.1451

LogNormal

LN( -0.1404, 0.5155)

0.0349

IGa

IGa( 4.1290, 3.1633)

0.0269

Gamma

Gamma( 3.7185, 0.2689)

0.0723

Weibull

Weibull( 1.1328, 1.8135)

0.0979

IG

IG( 1.0000, 3.2759)

0.0405

type

parameters

KS Statistic

Normal

N( 1.0000, 0.5058)

0.0911

LogNormal

LN( -0.1260, 0.5155)

0.0349

IGa

IGa( 3.7185, 2.8489)

0.0723

Gamma

Gamma( 4.1290, 0.2422)

0.0269

Weibull

Weibull( 1.1326, 2.0978)

0.0536

IG

IG( 1.0000, 3.2759)

0.0481

Figure 19: , from Sep 22nd, 2003 to Dec 30th, 2016.

Figure 20: , from Sep 22nd, 2003 to Dec 30th, 2016.

Table 7: MLE results for “” and “”

type

parameters

KS Statistic

Normal

N( 1.0000, 1.0338)

0.2273

LogNormal

LN( -0.2391, 0.6201)

0.0564

IGa

IGa( 3.1107, 2.0677)

0.0360

Gamma

Gamma( 2.2436, 0.4457)

0.1178

Weibull

Weibull( 1.0981, 1.2920)

0.1344

IG

IG( 1.0000, 1.9826)

0.0814

type

parameters

KS Statistic

Normal

N( 1.0000, 0.5864)

0.0959

LogNormal

LN( -0.1693, 0.6201)

0.0564

IGa

IGa( 2.2436, 1.4914)

0.1178

Gamma

Gamma( 3.1107, 0.3215)

0.0360

Weibull

Weibull( 1.1282, 1.8115)

0.0564

IG

IG( 1.0000, 1.9827)

0.0948

Figure 21: , from Sep 22nd, 2003 to Dec 30th, 2016.

Figure 22: , from Sep 22nd, 2003 to Dec 30th, 2016.

Table 8: MLE results for “” and “”

type

parameters

KS Statistic

Normal

N( 1.0000, 0.9475)

0.2130

LogNormal

LN( -0.2263, 0.6125)

0.0595

IGa

IGa( 3.1750, 2.1454)

0.0282

Gamma

Gamma( 2.3626, 0.4233)

0.1169

Weibull

Weibull( 1.1059, 1.3451)

0.1270

IG

IG( 1.0000, 2.0837)

0.0778

type

parameters

KS Statistic

Normal

N( 1.0000, 0.5731)

0.0911

LogNormal

LN( -0.1657, 0.6125)

0.0595

IGa

IGa( 2.3626, 1.5965)

0.1169

Gamma

Gamma( 3.1750, 0.3150)

0.0282

Weibull

Weibull( 1.1289, 1.8480)

0.0486

IG

IG( 1.0000, 2.0837)

0.0930

2.4 Ratio distribution revisited

Here we repeat the calculation from the Sec. 2.3 except with the RV for the month preceding the month for which VIX/VXO is calculated. For instance, if on March 31 VIX/VXO predict RV for April, we compare them to RV for March. This is to test the hypothesis that VIX/VXO are pretty much as good a predictor as the RV they are already aware of. Indeed, LN distribution fits best both and , as well as their inverse, consistent with the fact that for a LN distribution the distribution of the inverse variable is also LN. In Sec. 2.3 we hypothesized large spikes of RV as the reason for fat tails. This is congruent with uncertainty – even with the knowledge of preceding RV – reflected in heavy LN tails.

Figure 23: , from Jan 2nd, 1990 to Dec 30th, 2016.

Figure 24: , from Jan 2nd, 1990 to Dec 30th, 2016.

Table 9: MLE results for “” and “”

type

parameters

KS Statistic

Normal

N( 1.0000, 0.4974)

0.0992

LogNormal

LN( -0.1099, 0.4689)

0.0147

IGa

IGa( 4.6889, 3.7619)

0.0431

Gamma

Gamma( 4.7110, 0.2123)

0.0381

Weibull

Weibull( 1.1325, 2.1250)

0.0672

IG

IG( 1.0000, 4.0580)

0.0215

type

parameters

KS Statistic

Normal

N( 1.0000, 0.4999)

0.1059

LogNormal

LN( -0.1104, 0.4689)

0.0147

IGa

IGa( 4.7110, 3.7796)

0.0381

Gamma

Gamma( 4.6889, 0.2133)

0.0431

Weibull

Weibull( 1.1329, 2.1186)

0.0751

IG

IG( 1.0000, 4.0580)

0.0163

Figure 25: , Jan 2nd, 1990 to Dec 30th, 2016.

Figure 26: , from Jan 2nd, 1990 to Dec 30th, 2016.

Table 10: MLE results for “” and “”

type

parameters

KS Statistic

Normal

N( 1.0000, 0.4915)

0.1064

LogNormal

LN( -0.1041, 0.4539)

0.0150

IGa

IGa( 5.0351, 4.0948)

0.0331

Gamma

Gamma( 4.9618, 0.2015)

0.0454

Weibull

Weibull( 1.1316, 2.1383)

0.0730

IG

IG( 1.0000, 4.3548)

0.0203

type

parameters

KS Statistic

Normal

N( 1.0000, 0.4768)

0.0933

LogNormal

LN( -0.1026, 0.4539)

0.0150

IGa

IGa( 4.9618, 4.0352)

0.0454

Gamma

Gamma( 5.0351, 0.1986)

0.0331

Weibull

Weibull( 1.1319, 2.2099)

0.0689

IG

IG( 1.0000, 4.3548)

0.0212

3 Variance of realized variance

The goal of this section is to evaluate the expectation value of theoretical variance of realized variance

(5)

and compare it with the market data using historic squared stock returns. Here is the stochastic variance and is the mean (expectation) value of in the mean-reverting models,

(6)

Below we discuss two such models – Heston and multiplicative [16].

3.1 Heston Model

In the Heston model the equation for stochastic variance is given by

(7)

To evaluate (5), we need to know the correlation function [17]

meaning that in the regime of strong correlations in (8) and (13), the value of the variance of realized variance does not depend on and is consistent with central limit theorem otherwise.

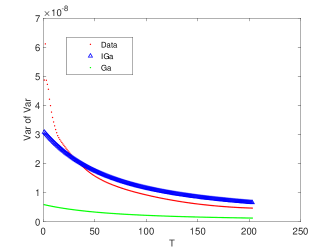

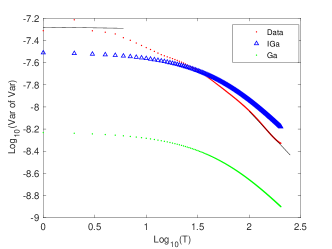

In Fig. 27 we compare the historic market data with theoretical predictions (10) and (15), including the limiting behaviors (11) and (16). To do so, we need to identify the values of parameters , and . one way to accomplish this is by fitting historic data with (6), (8) and (13) and the results are summarized in Table 11. Thus found values of parameters are close to those obtained from leverage [17], [18] and by averaging the values of parameters obtained from fitting multi-day stock returns [16], [17]. Alternatively, in Table 12 we use parameters obtained from single-day returns ( values in [16], with the same as in Table 11). While multiplicative model does better, a continuous model may not be appropriate for single-day returns.

Table 11: Parameters for Heston and multiplicative models for S&P 500

Heston model

0.041

Multiplicative model

0.041

0.25

Table 12: Parameters for Heston and multiplicative models for S&P 500 from single-day returns

Heston model

0.041

Multiplicative model

0.041

0.25

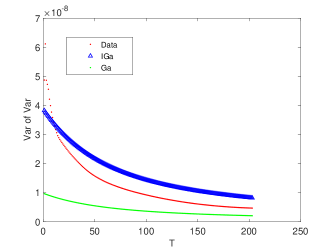

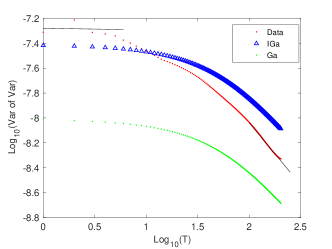

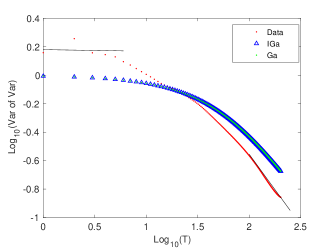

In Fig. 28 the comparison between theory and data is performed for the universal expression (17), including the limiting behaviors (18). Clearly, agreement between theory and data in Fig. 28 is quite good, while it is not as close in Fig. 27. The reason is that former depends only on one parameter , which is well established correlation and relaxation scale for mean reverting models [16]-[19].

Figure 27: Historic data vis-a-vis (10) and (15). Top row: with parameters from Table11. Bottom row: with parameters from Table12. Straight lines on the right are best data fits with slopes -0.0113 and -0.992 to compare with the limiting behaviors (10), (15) and (18).

Figure 28: Historic data vis-a-vis (17). Straight lines on the right have the same slopes as in Fig. 27.

4 Conclusions

Previously [16] we showed that the multi-day – typically longer than several weeks, to account for relaxation processes – stock returns are better described by the Heston model. Realized volatility, conversely, is calculated from single-day returns, which are presumably on the borderline between intra-day jump processes and continuous processes, such as Heston and multiplicative. Furthermore, realized volatility is square root of the realized variance, which is a sum of roughly 21 realized daily variances representing the trading month. As such, it is clear that the realized variance should be approaching normal distribution. Figs. 1-2 reflect this conjecture, with the caveat that the distribution maintains a tail similar to that of a single-day variance distribution.

Regarding the latter, we showed that an exGaussian distribution provides an excellent fit. This, however does not necessarily indicate that the tail is in fact exponential. An exGaussian is a sum of normal and exponential distributions and is an artificial construct, where all parameters are shape parameters and the distribution rescales only when all parameters rescale simultaneously. On the other hand, exGaussian has the right properties for the realized variance distribution and can be described analytically. It is quite possible that a distribution exists, which combines normality with a heavy, perhaps fat, tail that gives comparable Kolmogorov-Smirnov statistics to exGaussian. This is something we intend to study in the future.

With respect to comparison of the realized volatility to predictions of volatility indices, we found no discernible advantages between VIX and VXO. We also found that the ratio of the realized variance to squared VIX and VXO is best fitted by a fat-tailed (power-law) distribution – in this case Inverse Gamma. This most likely reflects large unexpected spikes of realized volatility not foreseen by volatility indices. The inverse distribution, which is the distribution of the inverse variable, is best fitted with an exponentially decaying distribution – in this case Gamma. This reflects no unexpected surges in volatility indices relative to realized volatility. When we use realized volatility of the preceding month, however, the ratio distributions are all best fitted with lognormal distribution. This most likely reflects the fact that while we predict future volatility based on what we presently know (past realized volatility and current information [20]), large spikes in volatility still result in heavy lognormal tails of the ratios due to uncertainty associated with such spikes. We will discuss relationship between volatility spikes and tails in a future work.

Finally, evaluation of the theoretical dependence of variance of realized variance and its limiting behaviors compares well vis-a-vis historic data, with the prediction of the multiplicative model having an edge over the Heston model. The latter may be due that single-day returns, on which realized variance is based, are better described by the Student’s distribution [16], [21]. Interestingly, 21 days, over which the realized variance is calculated, is also roughly the relaxation time of stochastic volatility, . Additionally, the mean value of the volatility in the mean-reverting models may be stochastic itself [18] – with similar time scales – which may as well affect the comparison. Ideally, one would also want to study the higher moments of the realized variance distribution. The difficulty, however, is that decoupling the higher-order correlation functions of stochastic variance into pair-wise correlation functions leads trivially to a normal distribution, which is not the case per above. This is a challenging problem that also needs to be addressed.

Appendix A VIX Current and VXO Current

Here we split 2003-2016 data in two roughly equal time periods, before and after the financial crisis.

A.1 Visual Comparison

Figure 29: PDFs of scaled and from Sep 22nd, 2003 to Aug 30th, 2010.

Figure 30: PDFs of scaled and from Sep 22nd, 2003 to Aug 30th, 2010.

Figure 31: PDFs of scaled and from Aug 31st, 2010 to Dec 30th, 2016.

Figure 32: PDFs of scaled and from Aug 31st, 2010 to Dec 30th, 2016.

A.2 Ratio Distribution

Figure 33: , from Sep 22nd, 2003 to Aug 30th, 2010.

Figure 34: , from Sep 22nd, 2003 to Aug 30th, 2010.

Table 13: MLE results for “” and “”

type

parameters

KS Statistic

Normal

N( 1.0000, 1.0244)

0.2338

LogNormal

LN( -0.2280, 0.5943)

0.0763

IGa

IGa( 3.5292, 2.4224)

0.0383

Gamma

Gamma( 2.3463, 0.4262)

0.1297

Weibull

Weibull( 1.1013, 1.3060)

0.1588

IG

IG( 1.0000, 2.1887)

0.0969

type

parameters

KS Statistic

Normal

N( 1.0000, 0.5124)

0.0613

LogNormal

LN( -0.1483, 0.5943)

0.0763

IGa

IGa( 2.3463, 1.6105)

0.1297

Gamma

Gamma( 3.5292, 0.2833)

0.0383

Weibull

Weibull( 1.1290, 2.0447)

0.0392

IG

IG( 1.0000, 2.1887)

0.1128

Figure 35: , from Sep 22nd, 2003 to Aug 30th, 2010.

Figure 36: , from Sep 22nd, 2003 to Aug 30th, 2010.

Table 14: MLE results for “” and “”

type

parameters

KS Statistic

Normal

N( 1.0000, 0.9130)

0.2237

LogNormal

LN( -0.2069, 0.5763)

0.0715

IGa

IGa( 3.6954, 2.6086)

0.0358

Gamma

Gamma( 2.5708, 0.3890)

0.1274

Weibull

Weibull( 1.1119, 1.3839)

0.1435

IG

IG( 1.0000, 2.4002)

0.0922

type

parameters

KS Statistic

Normal

N( 1.0000, 0.5009)

0.0635

LogNormal

LN( -0.1414, 0.5763)

0.0715

IGa

IGa( 2.5708, 1.8147)

0.1274

Gamma

Gamma( 3.6954, 0.2706)

0.0358

Weibull

Weibull( 1.1296, 2.0966)

0.0375

IG

IG( 1.0000, 2.4002)

0.1055

Figure 37: , from Aug 31st, 2010 to Dec 30th, 2016.

Figure 38: , from Aug 31st, 2010 to Dec 30th, 2016.

Table 15: MLE results for “” and “”

type

parameters

KS Statistic

Normal

N( 1.0000, 1.0445)

0.2245

LogNormal

LN( -0.2513, 0.6450)

0.0510

IGa

IGa( 2.8188, 1.8171)

0.0420

Gamma

Gamma( 2.1414, 0.4670)

0.1082

Weibull

Weibull( 1.0947, 1.2762)

0.1251

IG

IG( 1.0000, 1.8141)

0.0745

type

parameters

KS Statistic

Normal

N( 1.0000, 0.6306)

0.1114

LogNormal

LN( -0.1877, 0.6450)

0.0510

IGa

IGa( 2.1414, 1.3804)

0.1082

Gamma

Gamma( 2.8188, 0.3548)

0.0420

Weibull

Weibull( 1.1263, 1.7028)

0.0654

IG

IG( 1.0000, 1.8141)

0.0868

Figure 39: , from Aug 31st, 2010 to Dec 30th, 2016.

Figure 40: , from Aug 31st, 2010 to Dec 30th, 2016.

Table 16: MLE results for “” and “”

type

parameters

KS Statistic

Normal

N( 1.0000, 0.9878)

0.2060

LogNormal

LN( -0.2494, 0.6511)

0.0504

IGa

IGa( 2.7773, 1.7884)

0.0301

Gamma

Gamma( 2.1563, 0.4638)

0.1090

Weibull

Weibull( 1.0984, 1.3018)

0.1153

IG

IG( 1.0000, 1.8085)

0.0670

type

parameters

KS Statistic

Normal

N( 1.0000, 0.6258)

0.1065

LogNormal

LN( -0.1907, 0.6511)

0.0504

IGa

IGa( 2.1563, 1.3885)

0.1090

Gamma

Gamma( 2.7773, 0.3601)

0.0301

Weibull

Weibull( 1.1262, 1.7084)

0.0516

IG

IG( 1.0000, 1.8085)

0.0843

References

[1]

S. L. Heston, A closed-form solution for options with stochastic volatility

with applications to bond and currency options, The Review of Financial

Studies 6 (2) (1993) 327–343.

[2]

A. A. Dragulescu, V. M. Yakovenko, Probability distribution of returns in the

heston model with stochastic volatility, Quantitative Finance 2 (2002)

445–455.

[3]

D. Nelson, Arch models as diffusion approximations, Journal of Econometrics

45 (1990) 7.

[4]

T. Ma, R. Serota, A model for stock returns and volatility, Physica A:

Statistical Mechanics and its Applications 398 (2014) 89–115.

[5]

H. Zhou, M. Chesnes, Vix index becomes model for and based on s&p 500, Tech.

rep., Board of Governors of the Federal Reserve System (2003).

[6]

T. Bollerslev, G. Mathew, H. Zhou, Dynamic estimation of volatility risk premia

and investor risk aversion from option-implied and realized volatility, Tech.

rep., Federal Reserve Board (2004).

[7]

The CBOE volatility index - VIX, https://www.cboe.com/micro/vix/vixwhite.pdf

(2003).

[8]

K. Demeterfi, E. Derman, M. Kamal, J. Zou, More than you ever wanted to know

about volatility swaps, Tech. rep., Goldman Sachs (1999).

[9]

K. Demeterfi, E. Derman, M. Kamal, J. Zou, A guide to volatility and variance

swaps, The Journal of Derivatives 6 (4) (1999) 9–32.

[10]

O. E. Barndorff-Nielsen, N. Shephard, Econometric analysis of realized

volatility and its use in estimating stochastic volatility models, Journal of

the Royal Statistical Society: Series B (Statistical Methodology) 64 (2)

(2002) 253–280.

[11]

VIX Options and Futures Historical Data,

http://www.cboe.com/products/vix-index-volatility/vix-options-and-futures/vix-index/vix-historical-data.

[13]

J. M. Griffin, A. Shams, Manipulation in the vix?,

http://dx.doi.org/10.2139/ssrn.2972979 (May 2017).

[14]

Are traders manipulating the vix?,

https://blogs.wsj.com/moneybeat/2017/05/25/are-traders-manipulating-the-vix/

(May 2017).

[15]

Watch out vix: Nasdaq amps up volatility game,

https://www.wsj.com/articles/watch-out-vix-nasdaq-amps-up-volatility-game-1513938600

(December 2017).

[16]

Z. Liu, M. Dashti Moghaddam, R. Serota, Distributions of historic market data

– stock returns, arXiv1711.11003.

[17]

M. Dashti Moghaddam, Z. Liu, R. Serota, Distributions of historic market data

– relaxation and correlations, to be submitted to arXiv.

[18]

J. Perelló, J. Masoliver, J.-P. Bouchaud, Multiple time scales in

volatility and leverage correlations: a stochastic volatility model, Applied

Mathematical Finance 11 (1) (2004) 27–50.

[19]

Z. Liu, R. Serota, Correlation and relaxation times for a stochastic process

with a fat-tailed steady-state distribution, Physica A: Statistical Mechanics

and its Applications 474 (2017) 301–311.

[20]

B. J. Chrstensen, N. R. Prabhala, The relation between implied and realized

volaility, Journal of Financial Economics 50 (1998) 125–150.

[21]

M. A. Fuentes, A. Gerig, J. Vicente, Universal behvior of extreme price

movements in stock markets, PLoS ONE 4 (12) (2009) 1.