A Mean Field Game of Optimal Portfolio Liquidation.

Abstract

We consider a mean field game (MFG) of optimal portfolio liquidation under asymmetric information. We prove that the solution to the MFG can be characterized in terms of a FBSDE with possibly singular terminal condition on the backward component or, equivalently, in terms of a FBSDE with finite terminal value, yet singular driver. Extending the method of continuation to linear-quadratic FBSDE with singular driver we prove that the MFG has a unique solution. Our existence and uniqueness result allows to prove that the MFG with possibly singular terminal condition can be approximated by a sequence of MFGs with finite terminal values.

AMS Subject Classification: 93E20, 91B70, 60H30

Keywords: mean field game, portfolio liquidation, continuation method, singular FBSDE

1 Introduction and overview

Mean field games (MFGs) are a powerful tool to analyse strategic interactions in large populations when each individual player has only a small impact on the behavior of other players. In the economics literature, mean-field-type (or anonymous) games were first considered by Jovanovic and Rosenthal [33] and later analyzed by many authors including [8, 20, 29]. In the mathematical literature MFGs were independently introduced by Huang, Malhamé and Caines [31] and Lasry and Lions [37]. MFGs have been successfully applied to various economic problems, ranging from systemic risk management [15] to principal agent problems [22, 39] and from portfolio optimization [36] to optimal exploitation of exhaustible resources [18].

In a standard MFG, each player chooses an action from a given set of admissible controls that minimizes a cost functional of the form

| (1.1) |

subject to the state dynamics

| (1.2) |

Here, are independent Brownian motions, and are independent and identically distributed random variables with law that are independent of the Brownian motions. All stochastic processes and random variables are defined on an underlying filtered probability space555We assume throughout that all filtrations are augmented by the null sets. . The vector denotes the action profile, and denotes the empirical distribution of the individual players’ states at time . It is usually assumed that the players observe their own initial state and know the common distribution of the other player’s initial states.

The existence of approximate Nash equilibria for large populations can be established using a representative agent approach.The idea is to approximate the dynamics of the empirical distribution of the states by a deterministic measure-valued process, and then to consider the optimization problem of a representative player subject to the equilibrium constraint that the distribution of the representative player’s state process under her optimal strategy coincides with the pre-specified measure-valued process. More precisely, denoting by the space of probability measures on , by the law of a stochastic process and by a random initial state with distribution the resulting MFG can be formally described as follows:

| (1.3) |

Let be a solution to the above fix point problem and let be the representative player’s optimal response to given . Then for some measurable function from into a suitable function space, and each individual player’s optimal response to given her initial state is . Under suitable assumptions the homogeneous action profile forms an -equilibrium in the original game if is large enough.

There are basically four approaches to solve mean field games. In their original paper [37], Lasry and Lions followed an analytic approach. They analyzed a coupled forward-backward PDE system, where the backward component is the Hamiltion-Jacobi-Bellman equation arising from the representative agent’s optimization problem, and the forward component is a Kolmogorov-Fokker-Planck equation that characterizes the dynamics of the state process; see also [25]. Merging the forward backward system into a single master equation, the dynamics of the MFG can alternatively be described in terms of some form of second order PDE on the space of probability measures; see [9, 12, 19, 21] for details. A more probabilistic approach was introduced by Carmona and Delarue in [11]. Using a maximum principle of Pontryagin type, they showed that the fixed point problem reduces to solving a McKean-Vlasov FBSDEs; see also [6, 17]. A relaxed solution concept to MFGs was introduced by Lacker in [35] and later extended by various authors including [14, 23]. In this paper we apply a probabilistic approach to analyze a novel class of MFGs arising in models of optimal portfolio liquidation under market impact. Our existence and uniqueness of equilibrium result is based on a new existence of solutions result for FBSDE systems with singular drivers.

1.1 Single player models of optimal portfolio liquidation

Single-player portfolio liquidation models have been extensively analyzed in recent years. Their main characteristic is a singularity at the terminal time of the Hamilton-Jacobi-Bellmann equation. The majority of the optimal liquidation literature assumes that only absolutely continuous trading strategies are allowed; see e.g. [3, 28] and references therein. In such models the controlled state sequence follows a dynamics of the form

where is the initial portfolio that a trader needs to unwind, and is the trading rate. The set of admissible controls is confined to those processes that satisfy almost surely the liquidation constraint

It is typically assumed that the unaffected benchmark price process follows a one-dimensional Brownian motion (or some Brownian martingale) and that the trader’s transaction price is given by

where is a (sufficiently regular) stochastic volatility process. The integral term accounts for permanent price impact, i.e. the impact of past trades on current prices, while the term accounts for the instantaneous impact that does not affect future transactions. The expected cost functional is typically of the linear-quadratic form

where and are one-dimensional bounded adapted and non-negative processes. The process describes the trader’s degree of risk aversion or her belief about the volatility process; it penalizes slow liquidation. The process describes the degree of market illiquidity; it penalizes fast liquidation. The process describes the impact of past trades on current transaction prices.

There are basically two approaches to overcome the challenges resulting from the terminal state constraint. The majority of the literature, including Ankirchner et al. [3], Graewe et al. [27], Kruse and Popier [34] and Popier [42, 43] considers finite approximations of the singular terminal value, and then shows that the minimal solution to the value function with singular terminal condition can be obtained by a monotone convergence argument. A second approach, originally introduced in Graewe et al. [28] and further generalised in Graewe and Horst [26] is to determine the precise asymptotic behaviour of a potential solution to the HJB equation at the terminal time, and to characterize the value function in terms of a PDE or BSDE with finite terminal value yet singular driver, for which the existence of a solution in a suitable space can be proved using standard fixed point arguments.

If the transactions are not directly observable, then it is natural to assume that the permanent impact is driven by the market’s expectation about the trader’s transactions as in [5], given the publicly observable information. It leads to a mean field control problem, which is not the focus of our paper.

1.2 A MFG of optimal portfolio liquidation

We consider a MFG of optimal portfolio liquidation among asymmetrically informed players. In order to introduce the game, we fix a probability space that carries independent standard Brownian motions with in one dimension and in dimension and independent and identically distributed one-dimensional random variables with law that are independent of the Brownian motions. The Brownian motion drives the unaffected benchmark price process. We assume that is observable by all agents. The Brownian motion is private information to player and determines that player’s cost function. We may think of as measuring a player’s individual degree of market impact and/or subjective belief about the price volatility. The random variables specify the respective players’ initial portfolios. We assume that each player observes the realization of her initial portfolio and knows the distribution of all the other initial portfolios.

Following [10] we assume that the transaction price for each player is given by

In particular, the permanent price impact depends on the players’ average trading rate. Given her initial portfolio the optimization problem of player is to minimize the cost functional

| (1.4) |

subject to the state dynamics

| (1.5) |

Here, is the vector of strategies of all the players. We assume that the one-dimensional cost coefficients have the same distribution across players and are adapted to the filtration

| (1.6) |

Remark 1.1.

As pointed above, we assume that all players observe the Brownian motion that drives the unaffected benchmark price process; this motivates the individual information sets. Although we strongly believe that all our results carry over to the more general case where the agents observe only the price process itself, we prefer to work under the stronger assumption that is observable to simplify the analysis.

Our game is different from the majority of the MFG literature in at least three respects. First, as in [16, 25] the players interact through the impact of their strategies rather than states on the other players’ payoff functions. Second, all players observe the common Brownian motion that drives the benchmark price process. Hence, ours is a MFG with common noise. While MFGs with common noise have been investigated before (see, e.g. [14]) the nature of both the common and the idiosyncratic noise in our model is very different from the existing literature. Third, the individual state dynamics are subject to a terminal state constraint arising from the liquidation requirement. MFGs with terminal state constraint have been considered before in the literature by means of so-called mean field (game) planning problems (MFGP) introduced by Lions in his lectures at Collège de France (2009-2010). In these problems the terminal state constraint is given by a target density of the state at the terminal time. While our problem formally belongs to the literature on MFGP, see e.g. [1, 24, 44] and the references therein, ours seems to be the first paper that considers a MFG with strict terminal state constraint.

1.2.1 The MFG

In order to specify the resulting MFG, let and be independent Brownian motions of dimension and , respectively666The same as player game, we may interpret as the common information to all players and as the private information to the representative player., and be an independent one-dimensional random variable with law defined on some probability space, again denoted . Let with be the filtration generated by and let with The MFG associated with the -player game (1.4) and (1.5) is then given by:

| (1.7) |

where is the optimal strategy from 2 and the processes are adapted to the filtration . We denote by a solution to the fixed point problem in Step 3.

We apply the probabilistic method to solve the MFG with terminal constraint (1.7). In a first step we show how the analysis of our MFG can be reduced to the analysis of a conditional mean-field type FBSDE. The forward component describes the optimal portfolio process; hence both its initial and terminal condition are known. The backward component describes the optimal trading rate; its terminal value is unknown. Making an affine ansatz, we show that the mean-field type FBSDE with unkown terminal condition can be replaced by a coupled FBSDE with known initial and terminal condition, yet singular driver. Proving the existence of a small time solution to this FBSDE by a fixed point argument is not hard. The challenge is to prove the existence of a global solution on the whole time interval. Under a weak interaction condition that has been used in the game theory literature before (see, e.g. [29]) we prove the existence and uniqueness of a global solution by a generalization of the method of continuation established in [30, 41] to linear-quadratic FBSDE systems with singular driver. Under the additional assumption that all players share the same cost structure, i.e. that

for bounded measurable functions we prove that each player’s best response to the mean-field equilibrium is of the form

for some function and that the resulting homogeneous action profile forms an -equilibrium in the original -player game.

The common information case where all the cost coefficients are measurable with respect to the common factor can be analysed in greater detail. When different players hold different initial portfolios, then the optimal portfolio processes are given as weighted averages of the players’ initial portfolios and the differences of their own and the average initial portfolio. In this case, we show that if the average initial portfolio is positive and a player holds an above average initial portfolio, then her optimal portfolio process is always positive. If, however, a player holds a positive yet well below average initial portfolio, then it is optimal to quickly unwind the position, to then take a negative position and to buy the stock back by the end of the trading period. This is intuitive as players with negative portfolios benefit from the negative price trends generated by other players while the cost of unwinding a small portfolio is low. As such, our result suggests that traders with small portfolios act as liquidity providers in equilibrium even if their initial holds are positive.

The benchmark case of deterministic coefficients can be solved in closed form. For this case we show that when the strength of interaction in (1.7) is large and all players share the same initial portfolio, the players initially trade very fast in equilibrium to avoid the negative drift generated by the mean field interaction. Our model thus provides a possible explanation for large price drops in markets with many strategically interacting homogenous investors. We also show that the deterministic case is equivalent to a single player model with suitably adjusted cost terms.

Under mild additional assumptions on the market impact parameters we further prove that the solution to the MFG can be approximated by the solutions to a sequence of MFGs where the liquidation constraint is replaced by an increasing penalization of open positions at the terminal time. The convergence result can be viewed as a consistency result for both, the unconstrained and the constrained problem.

The three papers closest to our model are Cardaliaguet and Lehalle [10], Carmona and Lacker [16], Huang, Jaimungal and Nourin [32]. In [16], the authors propose a specific portfolio liquidation model where each players portfolio is subject to exogenous fluctuations (customer flow) described by independent Brownian motions. As such, their model is much closer to a standard MFG than ours, but no liquidation constraint is possible in their framework. The papers [10] and [32] consider mean field models parameterized by different preferences and with major-minor players, respectively. Again, no liquidation constraint is allowed. The model introduced in [10] is extended to portfolios of correlated assets in [38] where the effect of trading flows on naive estimates of intraday volatility and correlations is analyzed.

The remainder of the paper is organized as follows. In Section 2 we state and prove our existence and uniqueness of solutions result for the MFG (1.7) and establish additional results on the equilibrium trading strategies and portfolio processes if all the players share the same information. In Section 3 we prove that the solution to the MFG yields an -Nash equilibrium in the -player game. In Section 4 we prove that the MFG with singular terminal condition can be approximated by MFGs that penalize open positions at the terminal time under additional assumptions on the market impact term.

1.2.2 Notation and notational conventions

Throughout, we adopt the convention that denotes a constant which may vary from line to line. Moreover, for a filtration , denotes the sigma-field of progressive subsets of and for , which could be a subset of , or , we consider the set of progressively measurable processes w.r.t. :

We define the following subspaces of :

Whenever the notation appears in the definition of a function space we mean the set of all functions whose restriction satisfy the respective property on for any , e.g., by , we mean for any . For notational convenience, we put

For a positive stochastic process we denote its upper and lower bound by and , respectively.

2 The mean-field game

In this section, we state and prove an existence and uniqueness of solutions result for the MFG (1.7). The set of admissible controls for the representative player’s liquidation problem is given by

For a given process , the corresponding cost and value functions are given by

and

respectively. The Hamiltonian is

and the stochastic maximum principle suggests that the solution to the optimization problem can be characterised in terms of the FBSDE

| (2.1) |

where is a -dimensional Brownian motion. The process is called the adjoint process to the controlled state process . The liquidation constraint results in a singularity of the value function at liquidation time; see [3, 28]. As a result, the terminal condition for cannot be determined a priori. In particular, the first equation holds on while the second equation holds on . A standard approach yields the candidate optimal control

| (2.2) |

Taking the equilibrium condition into account suggests that the analysis of the MFG reduces to the analysis of the following conditional mean-field type FBSDE:

| (2.3) |

We establish the existence and uniqueness of a solution to the preceding FBSDE in the following space of weighted stochastic processes.

Definition 2.1.

For , we introduce the space

which is endowed with the norm

and the space

which is endowed with the norm

Fact 2.2.

The following facts are readily verified:

-

•

For any , with .

-

•

If , with , then a.s.

-

•

If and , then .

The first two properties also hold for the space .

We assume throughout that the cost coefficients are bounded and that the dependence of an individual player’s cost function on the average action is weak enough. The weak interaction condition is consistent with the game theory literature on mean-field type games where some form of moderate dependence condition is usually required to prove the existence and uniqueness of Nash equilibria; see [29] and references therein. The condition is also consistent with the monotonicity condition for FBSDE systems originally proposed by [30, 41] and the generalization to mean-field type FBSDEs established in [7]. Specifically, we assume that the following condition is satisfied.

Assumption 2.3.

-

i)

The processes , , , and belong to and is independent of and .

-

ii)

There exists a constant such that

(2.4)

The following quantity will be important in our subsequent analysis:

| (2.5) |

We are now ready to state our first major result.

Theorem 2.4.

Under Assumption 2.3, there exists a unique solution

to the FBSDE (2.3). Moreover, the process is an optimal control for the representative player, is the optimal state process and the aggregation effect given by

| (2.6) |

is the unique solution to the MFG (1.7). Finally, the value function is given by

| (2.7) |

2.1 General existence and uniqueness of solutions

In this section we prove our existence and uniqueness of equilibrium result for the MFG (1.7). Decoupling the FBSDE (2.3) by yields the following system of Riccati type equations:

| (2.8) |

The existence of a unique solution to the first equation is established in Lemma A.1 in the appendix. Namely, there exists a unique process such that , , the dynamics is given on any interval , by the first equation of (2.8) and . Moreover satisfies the a priori estimate (A.1) in Lemma A.1 in the appendix, from which it also follows that

| (2.9) |

for any , where is given by (2.5). Hence we need to solve the following FBSDE:

| (2.10) |

Our approach is based on an extension of the method of continuation that accounts for the singularity of the process at the terminal time and hence for the singularity in the driver of the FBSDE. We apply the method of continuation to the triple rather than the pair , and search for solutions

where was defined in (2.5) and is any constant

Specifically, the method of continuation will be applied to the FBSDE

| (2.11) |

where , . We emphasise that the first two equations hold on , while the third equation holds on .

In a first step, we provide an a priori estimate for the processes and .

Lemma 2.5.

Assume that and that there exists a solution to (2.11) such that

Then

and there exists a constant such that

and such that for each

In particular, is a true martingale on and is a true martingale on , for each .

Proof.

Since and there exists a constant that is independent of such that

Let us notice that

Since , this implies

Thus, by Doob’s maximal inequality,

Similarly, for each ,

∎

In a second step, we now prove an existence of solutions result for the FBSDE (2.11) with .

Lemma 2.6.

For there exists for every given data a unique solution to (2.11). It is given by

and and are given by the martingale representation theorem.

Proof.

For the process solves a linear ODE and the pair solves a linear BSDE. Hence, the explicit representations follow from the respective solution formulas. It remains to establish the desired integration properties. To this end, let us recall that has positive values. Thus we first apply Hölder’s inequality in order to obtain,

Using Doob’s maximal inequality, Jensen’s inequality and the fact that we conclude that,

From (2.9), the solution formula for and using that we obtain that because

In view of (A.1) and the previously established properties of and we have with

| (2.12) |

For any , integration by part implies that

The positivity of the process along with the definition of the process yields Thus, taking expectations on both sides of the above equation, letting and using yields

Together with the inequality (2.12) for this shows that

∎

In a third step we now establish the continuation result for the FBSDE (2.11) from which we shall then deduce the existence of a unique global solution to our original MFG.

Lemma 2.7.

If for some the FBSDE (2.11) is for every data uniquely solvable in , then this holds also for with small enough (independent of and ).

Proof.

Let us fix , and and consider the following system:

| (2.13) |

Then

Thus, by assumption there exists a unique solution

to (2.13), and . This defines a mapping from to and hence also a mapping on . In what follows we prove that this second mapping is a contraction for some . For the unique fixed point the system (2.13) reduces to the system (2.11) with replaced by . This then yields the desired result.

In order to establish the contraction property, we denote for two processes by and the corresponding processes defined by (2.13) and put

For any integration by part yields that

and

Taking the sum of these two equations and using that

yields

Taking expectations on both sides drops the martingale part. Then we can pass to the limit as to drop the term because , and , . Furthermore, since for any , we obtain:

and

All these inequalities imply that for any

In view of Assumption 2.3 we can choose a such that

which implies that there exists a constant depending only on the coefficients , and , such that

Thus, when is small enough,

for some . We notice that the bound on only depends on , and .

Now using the definition of and the solution formula for linear BSDEs yields

Thus

Since , Doob’s maximal inequality along with the previously established bounds yields

Now using the dynamics of and we obtain

Hence this leads to

Proposition 2.8.

From the equations (2.10), (2.2) and recalling , where is from Proposition 2.8, we obtain the following candidates of the optimal portfolio process and the optimal trading strategy for the representative player:

| (2.14) |

By construction, and hence is an admissible liquidation strategy. The following proposition shows that it is indeed the optimal liquidation strategy and that its conditional expectation defines the desired equilibrium for our MFG. In particular, it proves Theorem 2.4.

Proposition 2.9.

Proof.

Let be the solution given by Proposition 2.8. For any , let be the corresponding state process. Then it holds that,

| (2.15) |

Indeed, since , for any

With this, we can now show that is a best response against . In fact, for each , the convexity of the Hamiltonian yields

Furthermore, integration by part implies that for any ,

| (2.16) |

Therefore,

The equation (2.15) does indeed yield

Using the Lebesgue convergence theorem and taking , we obtain

In other words . Finally, (2.15) and (2.16) again yield

Now assume is another equilibrium, i.e. there is an optimal control such that for any , and . Note that is strictly convex for . Thus, there is a unique optimal control, which must satisfy , where is the solution to (2.1) with replaced by . By the uniqueness of the solution of (2.3), it must hold that as well as . ∎

Remark 2.10.

If we suppose that is a deterministic initial value of the state process at time , then we can define the space of admissible controls as

where is the filtration generated by and . Assuming that the cost coefficients satisfy Assumption 2.3 with replaced by , the same arguments as before show that the FBSDE

has a unique solution with and is a solution of the MFG starting at time . Moreover the value function is given by:

Since and ,

Since as tends to , we get the following terminal condition for the value function:

2.2 Common information environments

The benchmark case where all players share the same information, except for their initial value can be analyzed in greater detail. In this section we therefore assume that all randomness is generated by the common Brownian motion and the initial value .

Assumption 2.11.

The processes , , and belong to .

The weak interaction condition (2.4) is not required in this section. Under the common information assumption the conditional mean-field FBSDE (2.3) reduces to the following FBSDE:

| (2.17) |

2.2.1 Common initial portfolio

In this subsection we further assume that the initial portfolio is common to all players, i.e. . In this case all processes are -adapted and the mean-field FBSDE (2.17) simplifies to the regular FBSDE

| (2.18) |

In this setting, we can check that is given by where

| (2.19) |

This singular terminal condition on is necessary to satisfy the constraint . This equation has a unique solution, due to Corollary A.2 in the appendix. By (2.18),

The candidate of the optimal strategy is , where is the solution to (2.18). Since both and are -adapted, the consistency condition (2.6) reads .

Lemma 2.12.

Under Assumption 2.11, the processes , , and have the same sign as . Moreover

Proof.

Let . Due to Lemma A.1 in the appendix, the following estimate holds for any :

Hence the process is bounded from below by:

| (2.20) |

Hence (2.9) holds:

The conclusion on can be deduced immediately. Again from Lemma A.1 in the appendix, is bounded from above:

Thus we get an upper bound on :

Collecting all inequalities we get that and

A similar inequality holds for . ∎

It follows from the preceding lemma that is a non-negative or non-positive supermartingale so the limit of at the terminal time exists and is finite. Since , we deduce that . Moreover, the process belongs to for any .

The following theorem verifies that is optimal. The proof is the similar to Proposition 2.9.

2.2.2 Private initial portfolio

Let us now return to the problem (2.17). Theorem 2.4 implies there exists a unique soluton to (2.17). From the solution to (2.18), we deduce that

where solves the BSDE (2.19). Since is given by , we obtain (see equation (2.8) in Section 2.1) that

| (2.22) |

Note that and are -adapted. Thereby we have an explicit solution: for

Again from the general analysis of Section 2.1, the system (2.22) has a unique solution; similar arguments as in the proof of Proposition 2.9 can be applied to verify that the optimal state process for a given initial position is given by:

| (2.23) |

Thus, if different players hold different initial portfolios, then a trader’s optimal position consists of a weighted sum of the competitors’ average portfolio size and the deviation of the own initial position from that average.

Remark 2.14.

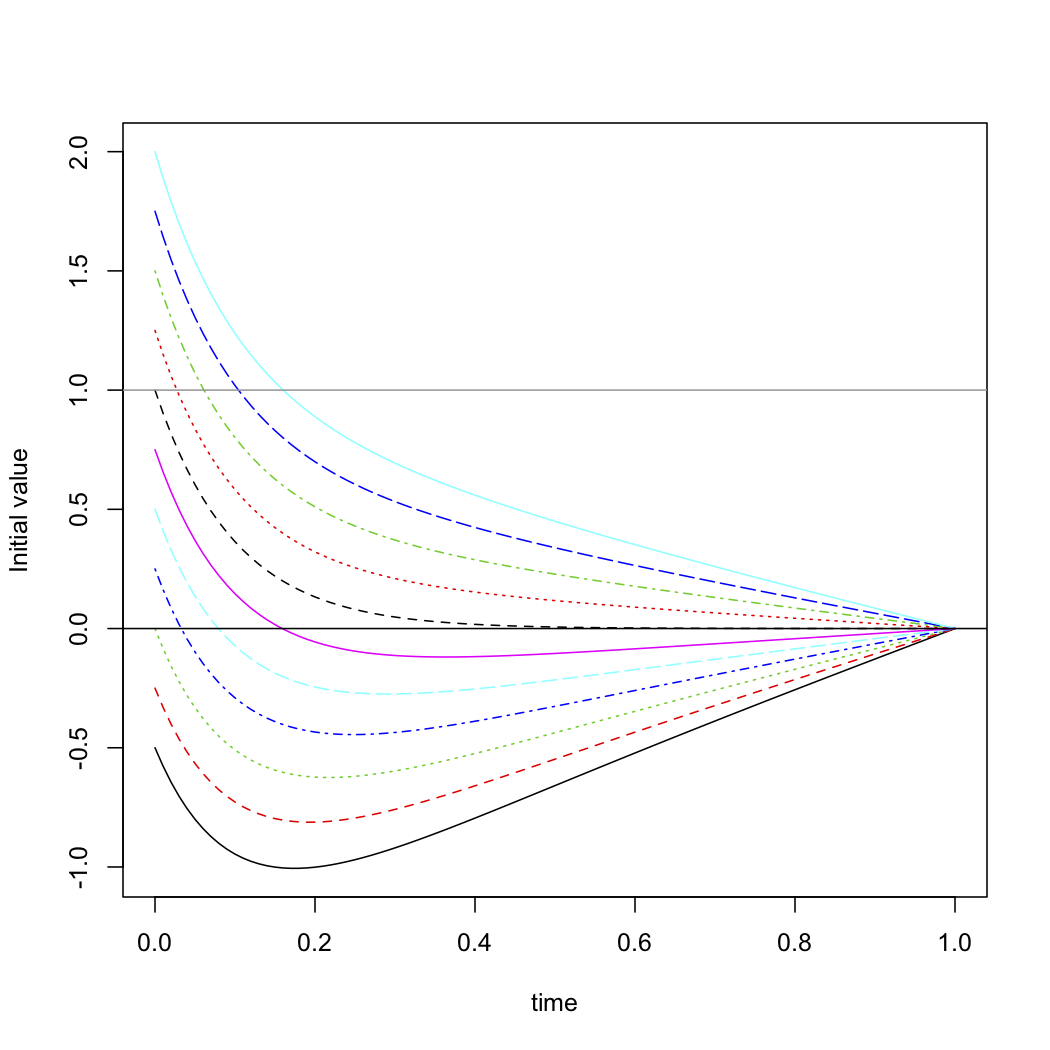

The preceding remark shows that the dependence of the optimal portfolio process on decreases if . It also suggests that - contrary to the previous case - the sign of the optimal portfolio process may change on the interval . In fact, if and , then remains non-negative on . However, if where , then becomes negative shortly after the initial time; see also Figure 2 below.

2.2.3 Constant cost coefficients

In this section, we consider a deterministic benchmark example that can be solved explicitly.

Assumption 2.15.

The processes , , are positive constants.

Under the preceding assumption, the Riccati equation (2.19) reduces to

Its explicit solution is given by

where

If all players share the same initial portfolio (see Subsection 2.2.1), then the optimal portfolio process is given by

| (2.24) |

and the optimal liquidation rate is given by

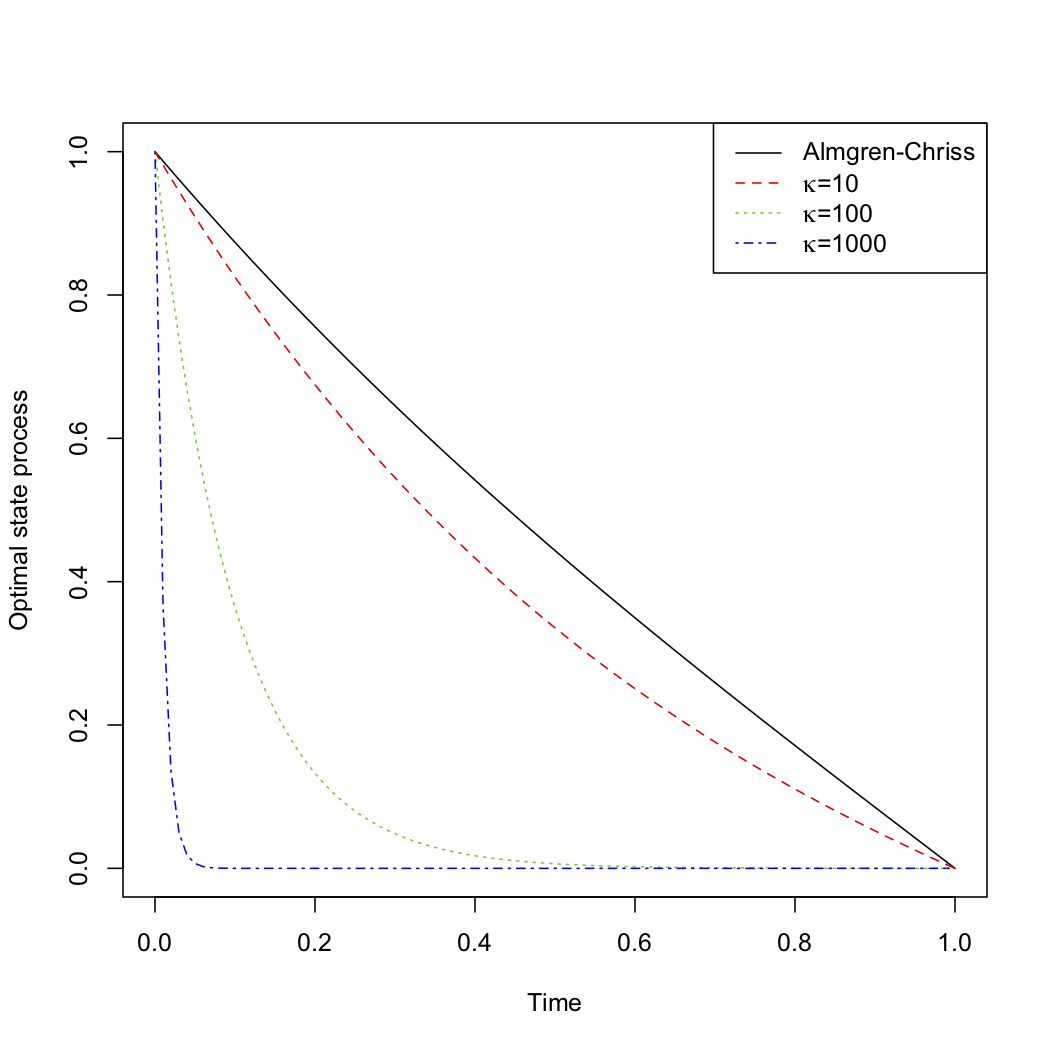

When , then with . This corresponds to the benchmark model in [2]. This convergence can also be seen from Figure 1. Furthermore, we see that—as in the corresponding single player models—the optimal liquidation rate is always positive, i.e., round trips are not beneficial. Moreover, we notice that the portfolio process (2.24) corresponds to the optimal portfolio process in an Almgren–Chriss model with adjusted risk aversion and with additional exponential decay of rate .

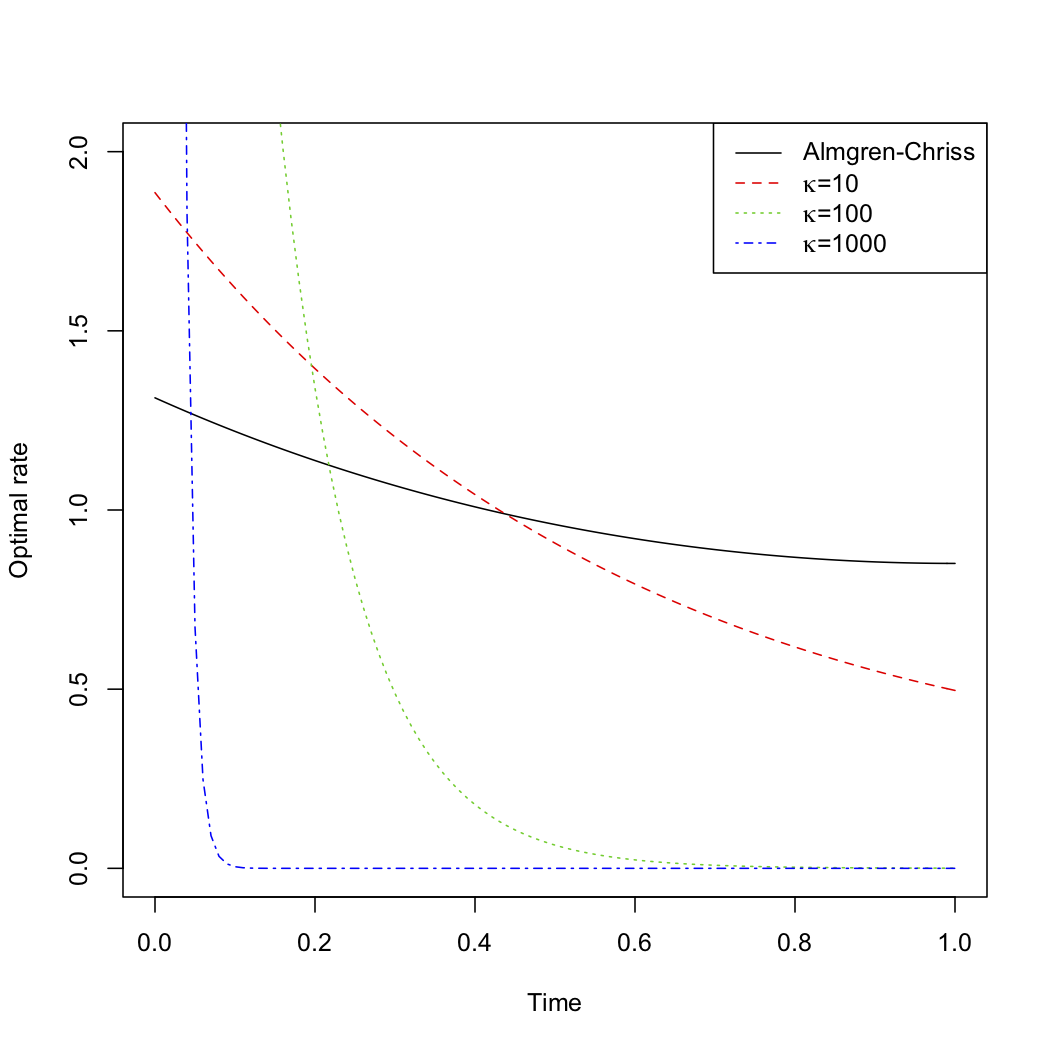

When , then while for . That is, when the impact of interaction is very strong, then the players trade very fast initially and very slowly afterwards. The intuitive reason is that in this case an individual player would benefit from trading fast slightly before his competitors start trading in order to avoid the negative drift generated by the mean-field interaction. As all the players are statistically identical, they “coordinate” on an equilibrium trading strategy as depicted in Figure 2. Thus, our model provides a possible explanation for large price increases or decreases in markets with strategically interacting players with similar preferences.

If the players hold different initial portfolios (Subsection 2.2.2), then (2.23) shows that the optimal portfolio process is given by

Figure 2 confirms that the sign of is indeed changing when is small.

3 Approximate Nash Equilibrium

In this section we show that an -Nash equilibrium for the player portfolio liquidation game can be constructed from the solution to the MFG (1.7) when the number of players is large if all players share the same cost structure.

Assumption 3.1.

Assume for any , , and admit the following expression

for some non-negative deterministic bounded and measurable functions , and .

The next result is an adaptation to the Yamada-Watanabe result for FBSDE. The proof follows from the same arguments given in, e.g. [13] and [4].

Lemma 3.2.

In view of the above lemma, under Assumption 3.1 each player’s unique best response to the mean-field equilibrium can be represented in terms of the function as in (3.1). In particular, each individual action has the same distribution as the mean-field equilibrium:

| (3.2) |

Proposition 2.8 guarantees the existence of a constant such that

| (3.3) |

and Lemma 3.2 yields a real-valued function , which is independent of , such that

| (3.4) |

Before we prove the main result of this section, we recall the cost functional from (1.4).

Theorem 3.3.

Proof.

By the symmetry of the player game, it is sufficient to show the result for Player . We first estimate the following term:

Using (3.3) and (3.4), the second term is bounded by . For the first term, if , then the conditional expectation reduces to the expectation and since and are conditionally independent given for ,

If , then we see from Lemma 3.2 that

for some real-valued function . Using again conditional independence and (3.2) we see that this term vanishes as well. As a result,

| (3.5) |

We are now ready to the prove the -equilibrium property of . By (3.4), we have that . For a given strategy , let be the corresponding state process and let be Player 1’s cost function when the average trading rate is replaced by the mean-field equilibrium. By Proposition 2.9, , which implies:

For the first difference , using (3.5) we have that

For the second difference , again using (3.5), we have that

This proves the assertion. ∎

4 Approximation by unconstrained MFGs

In this section, we prove that the solution to our singular MFG can be approximated by the solutions to non-singular MFGs under additional assumptions on the market impact parameter. Specifically, we consider the following unconstrained MFGs:

| (4.1) |

We will need the following assumption on the solution to the first equation in (2.8) with the terminal condition . It implies in particular that .

Assumption 4.1.

There exists a constant such that for any

The following result is proven in the appendix.

Lemma 4.2.

Assumption 4.1 holds under each of the following conditions:

-

•

is deterministic;

-

•

is a positive martingale;

-

•

has uncorrelated multiplicative increments, namely for any

Using the same arguments as in Section 2, the unconstrained control problem leads to the following conditional mean field FBSDE:

| (4.2) |

where

| (4.3) |

The existence of a solution to the BSDE (4.3) can be deduced from Lemma A.3. By the same lemma the sequence is a non-decreasing sequence converging pointwise to and there exists a constant such for any ,

where the space is defined as

and endowed with the norm

We shall also need the following analogs to the space :

endowed with the norm

The next result can be obtained using similar arguments as in the proof of Theorem 2.8. In fact, we have a slightly stronger result.

Theorem 4.3.

Assume that Assumption 2.3 holds and that is a square integrable random variable. Then, for any fixed and , there exists a unique solution

to the following FBSDE system:

| (4.4) |

In order to establish the convergence of the value functions of the unconstrained problems to the value function of the constrained problem we need a uniform norm estimate for the sequence .

Lemma 4.4.

Proof.

The proof is split into three steps.

Step 1.

Step 2.

Suppose that for some , the solution to (4.4) satisfies

for some independent of . Then there exists independent of such that the solution to (4.4) with replaced by satisfies the same estimate for some :

| (4.6) |

To prove this assertion, we introduce for any given the FBSDE system

| (4.7) |

Arguing as in the proof of Theorem 4.3, there exists a unique solution to (4.7). This defines a mapping

on . We now show the has a unique fixed point and that this fixed point belongs to , the subset of such that the -norm is bounded by .

By the same arguments as in the proof as Lemma 2.7 we have

where does not depend on and is small enough but independent of and of . Taking , we have

Note that corresponds to the solution to (4.4) with . By assumption,

Thus, if we assume ,

This implies that is a mapping from to itself. Since is a Banach space the unique fixed point belongs to . This yields the desired estimate for .

Let be the solution corresponding to and . Then, by Hölder’s inequality,

Doob’s maximal inequality yields that

Hence,

and

Step 3.

Since is independent of , by iteration for only finitely many times, we have the solution for (4.2) with and with the uniform estimate (4.5). ∎

Under Assumption 4.1, the value appearing in the estimate of Theorem 2.8 is equal to one. That is

| (4.8) |

This allows us to prove the convergence of the optimal position and control.

Lemma 4.5.

Proof.

Using the same arguments as in the proof of Lemma 2.7, we have for each

| (4.9) |

The two terms in the above summation admit the following estimates

respectively,

Letting go to zero in (4.9), by Theorem 2.8 and Lemma 4.4 we get

Hence we obtain the desired limit for and . By the expression for , we have

Let us recall that is a non-decreasing sequence converging to . This leads to

∎

Let us denote by the value function associated with the penalized problem (4.1). The next theorem shows the convergence of to the value function associated with the constrained MFG.

Proof.

Let be the solution in Theorem 4.3. Recall that is the optimal strategy for the penalized problem with degree and the related optimal process is equal to . Thus, with fixed, the optimal strategy for the constraint optimization is an admissible control for the penalized optimization. We denote by the optimal state process related to (Proposition 2.9 and Equation (2.14)). Let us define

From Lemma 4.5, Recalling that

we have

Hence we deduce that

thus

Again by Lemma 4.5,

∎

Remark 4.7.

As a by-product of the proof, we get that . Moreover

The proof of convergence of the value function simplifies substantially under the common information assumption (Subsection 2.2.1). In particular, Assumption 4.1 is not necessary here. In this case, where

and

The optimal strategy and the resulting portfolio process are given by, respectively,

Since the sequence is non-decreasing and converges to , we deduce that converges to a.s. and that converges to a.e. a.s.. Moreover, for fixed , is suboptimal to the penalized optimization. This implies that

For any , it holds

Hence, the monotone convergence theorem implies

| (4.10) |

Moreover,

which is bounded uniformly in , due to Lemma 4.4. Vitali convergence implies

| (4.11) |

The convergence (4.10) and (4.11) yields the desired result.

Appendix A Appendix

In this appendix we recall an existence of solutions result for a stochastic Riccati equation with singular terminal condition and prove Lemma 4.2. We assume throughout that , and are bounded.

A.1 Stochastic Riccati equations with singular terminal value

Lemma A.1.

Corollary A.2.

Proof.

Let . Then,

| (A.2) |

Hence, the assertion follows from the preceding lemma. ∎

Lemma A.3.

For each , there exists a unique solution to the BSDE

| (A.3) |

Moreover, the sequence is non-decreasing and converges to . There exists a constant such that for any :

Proof.

The first and second assertions are results of [3, Proposition 3.1,Theorem 3.2], respectively. For any , and , we have

Let us denote by the solution of the BSDE with generator and terminal condition . By the comparison principle for BSDEs, we have and by the solution formula for linear BSDEs,

Hence

Thus , that is . ∎

A.2 On Assumption 4.1

Assumption 4.1 states that there exists a constant such that a.s. for any

The left-hand side is equal to the optimal state process of the control problem studied in [3, 28] with initial value equal to 1 at time . In particular from the proof of [3, Theorem 4.2], the process defined on by

is a non-negative local martingale with . Hence for any

Since is also a non-negative supermartingale converges almost surely as goes to and the limit satisfies . Therefore Assumption 4.1 does not strike us as overly restrictive.

Acknowledgments.

Financial support by the Berlin Mathematical School (BMS), the TRCRC 190 Rationality and competition: the economic performance of individuals and firms and the Tier 2 grant “Nonstandard BSDEs in Mathematical Finance: Theory, Application, Numerical Methods” is gratefully acknowledged. We thank participants of the IPAM workshop “Mean Field Games” for valuable comments and suggestions. We also thank seminar participants at various places for helpful comments and discussions.

References

- [1] Y. Achdou, F. Camilli, and I. Capuzzo-Dolcetta. Mean field games: numerical methods for the planning problem. SIAM Journal on Control and Optimization, 50(1):77–109, 2012.

- [2] R. Almgren and N. Chriss. Optimal execution of portfolio transactions. Journal of Risk, 3:5–40, 2001.

- [3] S. Ankirchner, M. Jeanblanc, and T. Kruse. BSDEs with singular terminal condition and a control problem with constraints. SIAM Journal on Control and Optimization, 52(2):893–913, 2014.

- [4] K. Bahlali, B. Mezerdi, M. N’zi, and Y. Ouknine. Weak solutions and a Yamada-Watanabe theorem for FBSDEs. Random Operators and Stochastic Equations, 15(3):271–285, 2007.

- [5] M. Basei and H. Pham. A weak martingale approach to linear-quadratic McKean-Vlasov stochastic control problems. J. Optim. Theory Appl., 181(2):347–382, 2019.

- [6] A. Bensoussan, K. Sung, P. Yam, and S. Yung. Linear-quadratic mean field games. Journal of Optimization Theory and Applications, 169(2):496–529, 2016.

- [7] A. Bensoussan, S.C.P. Yam, and Z. Zhang. Well-posedness of mean-field type forward-backward stochastic differential equations. Stochastic Processes and their Applications, 125(9):3327–3354, 2015.

- [8] M. Blonski. Anonymous games with binary actions. Games and Economic Behavior, 28(2):171–180, 1999.

- [9] P. Cardaliaguet, F. Delarue, J.-M. Lasry, and P.-L. Lions. The master equation and the convergence problem in mean field games, volume 201 of Annals of Mathematics Studies. Princeton University Press, Princeton, NJ, 2019.

- [10] P. Cardaliaguet and C. Lehalle. Mean field game of controls and an application to trade crowding. Mathematics and Financial Economics, 12(3):335–363, 2018.

- [11] R. Carmona and F. Delarue. Probabilistic analysis of mean-field games. SIAM Journal on Control and Optimization, 51(4):2705–2734, 2013.

- [12] R. Carmona and F. Delarue. The master equation for large population equilibriums. In Stochastic analysis and applications 2014, volume 100 of Springer Proc. Math. Stat., pages 77–128. Springer, Cham, 2014.

- [13] R. Carmona and F. Delarue. Probabilistic theory of mean field games with applications. II, volume 84 of Probability Theory and Stochastic Modelling. Springer, Cham, 2018. Mean field games with common noise and master equations.

- [14] R. Carmona, F. Delarue, and D. Lacker. Mean field games with common noise. Annals of Probability, 44(6):3740–3803, 2016.

- [15] R. Carmona, J. Fouque, and L. Sun. Mean field games and systemic risk. Communications in Mathematical Sciences, 13(4):911–933, 2015.

- [16] R. Carmona and D. Lacker. A probabilistic weak formulation of mean field games and applications. Annals of Applied Probability, 25(3):1189–1231, 2015.

- [17] R. Carmona and X. Zhu. A probabilistic approach to mean field games with major and minor players. Annals of Applied Probability, 26(3):1535–1580, 2016.

- [18] P. Chan and R. Sircar. Fracking, renewables, and mean field games. SIAM Review, 59(3):588–615, 2017.

- [19] J.-F. Chassagneux, D. Crisan, and F. Delarue. A probabilistic approach to classical solutions of the master equation for large population equilibria. Forthcoming in Memoirs of the AMS., 2015.

- [20] C. Daskalakis and C. Papadimitriou. Approximate Nash equilibria in anonymous games. Journal of Economic Theory, 156:207–245, 2015.

- [21] F. Delarue, D. Lacker, and K. Ramanan. From the master equation to mean field game limit theory: a central limit theorem. Electronic Journal of Probability, 24(51):1–54, 2019.

- [22] R. Elie, T. Mastrolia, and D. Possamaï. A tale of a principal and many, many agents. Mathematics of Operations Research, 44(2):440–467, 2019.

- [23] G. Fu and U. Horst. Mean field games with singular controls. SIAM Journal on Control and Optimization, 55(6):3833–3868, 2017.

- [24] D. A. Gomes and T. Seneci. Displacement convexity for first-order mean-field games. Minimax Theory and its Applications, 3(2):261–284, 2018.

- [25] D. A. Gomes and V. K. Voskanyan. Extended mean field games. Izv. Nats. Akad. Nauk Armenii Mat., 48(2):63–76, 2013.

- [26] P. Graewe and U. Horst. Optimal trade exection with instantaneous price impact and stochastic resilience. SIAM Journal on Control and Optimization, 55(6):3707–3725, 2017.

- [27] P. Graewe, U. Horst, and J. Qiu. A non-Markovian liquidation problem and backward SPDEs with singular terminal conditions. SIAM Journal on Control and Optimization, 53(2):690–711, 2015.

- [28] P. Graewe, U. Horst, and E. Séré. Smooth solutions to portfolio liquidation problems under price-sensitive market impact. Stochastic Processes and their Applications., 128(3):979–1006, 2018.

- [29] U. Horst. Stationary equilibria in discounted stochastic games with weakly interacting players. Games and Economic Behavior, 51(1):83–108, 2005.

- [30] Y. Hu and S. Peng. Solution of forward-backward stochastic differential equations. Probability Theory and Related Fields, 103(2):273–283, 1995.

- [31] M. Huang, R. Malhamé, and P. Caines. Large population stochastic dynamic games: closed-loop McKean-Vlasov systems and the Nash certainty equivalence principle. Communications in Information and Sytems, 6(3):221–252, 2006.

- [32] X. Huang, S. Jaimungal, and M. Nourian. Mean-field game strategies for optimal execution. Applied Mathematical Finance, 26(2):153–185, 2019.

- [33] B. Jovanovic and R. Rosenthal. Anonymous sequential games. Journal of Mathematical Economics, 17(1):77–87, 1988.

- [34] T. Kruse and A. Popier. Minimal supersolutions for BSDEs with singular terminal condition and application to optimal position targeting. Stochastic Processes and their Applications, 126(9):2554–2592, 2016.

- [35] D. Lacker. Mean field games via controlled martingale problems: Existence of Markovian equilibria. Stochastic Processes and their Applications, 125(7):2856–2894, 2015.

- [36] D. Lacker and T. Zariphopoulou. Mean field and n-agent games for optimal investment under relative performance criteria. Mathematical Finance, 29(4):1003–1038, 2019.

- [37] J.-M. Lasry and P.-L. Lions. Mean field games. Japanese Journal of Mathematics, 2(1):229–260, 2007.

- [38] C.-A. Lehalle and C. Mouzouni. A mean field game of portfolio trading and its consequences on perceived correlations, 2019.

- [39] M. Nutz and Y. Zhang. A mean field competition. Math. Oper. Res., 44(4):1245–1263, 2019.

- [40] É. Pardoux. BSDEs, weak convergence and homogenization of semilinear PDEs. In Nonlinear analysis, differential equations and control (Montreal, QC, 1998), volume 528 of NATO Sci. Ser. C Math. Phys. Sci., pages 503–549. Kluwer Acad. Publ., Dordrecht, 1999.

- [41] S. Peng and Z. Wu. Fully coupled forward-backward stochastic differential equations and applications to optimal control. SIAM Journal on Control and Optimization, 37(3):825–843, 1999.

- [42] A. Popier. Backward stochastic differential equations with singular terminal condition. Stochastic Processes and their Applications, 116(12):2014–2056, 2006.

- [43] A. Popier. Backward stochastic differential equations with stopping time and singular terminal condition. Annals of Probability, 35(3):1071–1117, 2007.

- [44] A. Porretta. On the planning problem for the mean field games system. Dynamic Games and Applications, 4(2):231–256, 2014.