Sparse Bayesian Factor Analysis when the Number of Factors is Unknown111Several research report versions of this paper were circulated that did not address variance identification. A June 2009 Chicago Booth School of Business Research Report selected the number of factors in a sparse Bayesian factor models under the positive lower triangular constraints. In (Frühwirth-Schnatter and Lopes, 2010), we introduced sparse Bayesian factor models with the generalized lower triangular constraints. This final version of the paper extends the later work by fully addressing variance identification. The first author would like to thank James J. Heckman for many inspiring discussions about this subject. The paper in its various forms was presented on many occasions, such as the 2010 SBIES Meeting at UT Austin, the 25th Anniversary Celebration of the Department of Statistical Science at Duke University (2012), the 2014 ESOBE Meeting in Paris, the 30rd International Workshop on Statistical Modelling in Linz (2015) and the 2016 CFE Meeting in Seville, and we acknowledge helpful comments from many people, in particular Remi Piatek und Sylvia Kaufmann.

Abstract

Despite the popularity of sparse factor models, little attention has been given to formally address identifiability of these models beyond standard rotation-based identification such as the positive lower triangular constraint. To fill this gap, we provide a counting rule on the number of nonzero factor loadings that is sufficient for achieving uniqueness of the variance decomposition in the factor representation. Furthermore, we introduce the generalised lower triangular representation to resolve rotational invariance and show that within this model class the unknown number of common factors can be recovered in an overfitting sparse factor model. By combining point-mass mixture priors with a highly efficient and customised MCMC scheme, we obtain posterior summaries regarding the number of common factors as well as the factor loadings via postprocessing. Our methodology is illustrated for monthly exchange rates of 22 currencies with respect to the euro over a period of eight years and for monthly log returns of 73 firms from the NYSE100 over a period of 20 years.

Keywords: Hierarchical model; identifiability; sparsity; Cholesky decomposition; rank deficiency; point-mass mixture priors; fractional priors; Heywood problem; rotational invariance; reversible jump MCMC, marginal data augmentation; ancillarity-sufficiency interweaving strategy (ASIS).

JEL classification: C11, C38, C63

1 Introduction

For many decades, factor analysis has been a popular method to model the covariance matrix of correlated, multivariate observations of dimension , see e.g. Anderson (2003) for a comprehensive review. Assuming uncorrelated factors, a factor model yields the representation , with a factor loading matrix and a diagonal matrix . The considerable reduction of the number of parameters compared to an unconstrained covariance matrix is a main motivation for the application of factor models in economics and finance, especially, if is large, see e.g. Fan et al. (2008) and Forni et al. (2009). Beyond that, the goal of factor analysis is often to estimate the loading matrix to understand the driving forces behind the correlation between the features observed through .

The recent years have seen considerable research in the area of sparse Bayesian factor analysis which achieves additional sparsity beyond the natural parsimonity of factor models in two different ways. One strand of literature considers sparse factor models through continuous shrinkage priors on the factor loadings, see e.g. Bhattacharya and Dunson (2011), Ročková and George (2017) and Kastner (2018), among others. Alternatively, following the pioneering paper by West (2003), many authors considered sparse factor models with point mass mixture priors on the factor loadings, including basic factor models (Carvalho et al., 2008), dedicated factor models with correlated (oblique) factors (Conti et al., 2014) and dynamic factor models (Kaufmann and Schuhmacher, 2018).

Sparse Bayesian factor analysis with point mass mixture priors assumes that (many) elements of the factor loading matrix are 0, without being specific as to which elements are concerned. Inference with respect to zero loadings is considered as a variable selection problem and there are several reasons, why variable selection is of interest in sparse Bayesian factor analysis. First of all, sparse Bayesian factor analysis allows to identify “simple structures” where in each row only a few nonzero loadings are present (Anderson and Rubin, 1956). Identifying simple structures has been a long standing issue in factor analysis, in particular in psychology, and was implemented recently through sparse Bayesian factor analysis in Conti et al. (2014). A second motivation is identifying irrelevant variables in which are uncorrelated with the remaining variables, meaning that for these variables the entire row of the factor loading matrix is zero. The possibility to identify such variables within the framework of sparse Bayesian factor analysis is of high relevance in economic analysis, given the recent practice to include as many variables as possible (Stock and Watson, 2002; Boivin and Ng, 2006), and was implemented through sparse Bayesian factor analysis in Kaufmann and Schuhmacher (2017).444Identifying irrelevant variables also of importance in areas such as bioinformatics, where typically only a few out of potentially ten thousands of genes may be related to a certain physiological outcome (Lucas et al., 2006).

The present paper contributes to the literature on sparse Bayesian factor models using point mass mixture priors in several ways. As a first major contribution, we explicitly address identifiability issues that arise in sparse Bayesian factor analysis. In the econometrics literature, identifiability is often reduced to solving rotational indeterminacy, see e.g. Geweke and Singleton (1980). However, for sparse Bayesian factor models identification goes beyond this problem and concerns uniqueness of the variance decomposition in the covariance matrix . This problem which has been known for a long time (Anderson and Rubin, 1956) went largely unnoticed in the literature on sparse Bayesian factor analysis, both in bioinformatics as well as in econometrics, and was addressed only recently by Conti et al. (2014) in the context of dedicated sparse factor models. Our paper provides a major achievement in this respect. We reverse the two-step identification strategy of Anderson and Rubin (1956) and first force a structure on the loading matrix that solves rotational invariance up to trivial rotations. To this aim, we introduce the class of generalized lower triangular (GLT) factor models where the loading matrix is a generalized lower triangular matrix. Given a GLT structure, we introduce in a second step a simple counting rule for the nonzero factor loadings as a sufficient condition for verifying variance identification.

As a second contribution, we operate in a sparse overfitting Bayesian factor model to yield inference with respect to the number of unknown factors. Selecting the number of factors has been known since long to be a very difficult issue. Bai and Ng (2002) define information criteria to choose the number of factors. Lee and Song (2002) and Lopes and West (2004) were among the first to address this issue in a careful Bayesian manner using marginal likelihood. More recently, Conti et al. (2014) use Bayesian variable selection in an overfitting model to determine the number of factors in a dedicated factor model. However, the recent econometric literature on Bayesian factor analysis, including Aßmann et al. (2016), Chan et al. (2018), and Kaufmann and Schuhmacher (2018), does not provide any intrinsically Bayesian solution for determining the number of factors. In the present paper, we discuss identification in an overfitting sparse factor model from a formal viewpoint. We gain very useful insights into the structure of the loading matrix in an overfitting model, if we confine ourselves to the class of GLT factor models. Using a point-mass mixture prior in an overfitting sparse factor model, we are able to identify the number of factors by postprocessing posterior draws and exploiting “column sparsity”, i.e. by counting the number of nonzero columns among the variance identified factor loading matrices.

As a final contribution, we design an efficient Markov chain Monte Carlo (MCMC) procedure that delivers posterior draws from an overfitting sparse factor model under point mass priors which is know to be particularly challenging, see e.g. Pati et al. (2014). In addition, we carefully discuss prior specifications on all levels of the model, including a prior for the idiosyncratic variances that avoids the well-known Heywood problem and a fractional prior for the unrestricted factor loadings.

The rest of the paper is organized as follows. Section 2 discusses identification issues for sparse factor models and introduces the class of GLT factor models. Section 3 discusses Bayesian inference and selecting the number of factors for GLT factor models. Section 4 considers applications to exchange rate data and NYSE100 returns. Section 5 concludes. Mathematical proofs and technical details are summarized in a comprehensive Web-Appendix.

2 Identification issues in sparse Bayesian factor analysis

A basic factor model relates each observation in a random sample of observations to a latent -variate random variable , the so-called common factors, through:

| (1) |

where is the unknown factor loading matrix with factor loadings . is called the number of factors. Throughout the paper, the common factors are assumed to be orthogonal:

| (2) |

A basic assumption in factor analysis is that , , , and are pairwise independent for all . Furthermore, the following assumption is made concerning the idiosyncratic errors :

| (3) |

Assumption (3) implies that conditional on the elements of are independent, hence all dependence among these variables is explained through the common factors. For the basic factor model, assumption (3) together with (2) implies that the observations arise from a multivariate normal distribution, , with zero mean and a covariance matrix with the following constrained structure:

| (4) |

For a sparse Bayesian factor model, a binary indicator is introduced for each element of the factor loading matrix which takes the value , iff , and is unconstrained otherwise. This yields a binary indicator matrix of 0s and 1s of the same dimension as . In sparse Bayesian factor analysis, the indicators are unknown and are inferred from the data, using point-mass mixture priors (also called spike-and-slab priors), see Subsection 3.1.1 for more details.

2.1 Identification of sparse basic factor models

In the present paper, we explicitly address identifiability issues that arise in sparse Bayesian factor analysis with respect to uniqueness of the variance decomposition. Assume that is of full column rank () and let be the smallest number compatible with representation (4). Identification means that for any satisfying (4), that is:

| (5) |

where is a diagonal matrix and a loading matrix, it follows that and .

Well-known identification problems arise for factor models, meaning that additional structure is necessary to achieve identifiability. A rigorous approach toward identification of factor models was first offered by Anderson and Rubin (1956). They considered identification as a two-step procedure, the first step being identification of the variance decomposition, i.e. identification of from (4), which implies identification of , and the second step being subsequent identification of from , also know as solving the rotational identification problem.

The econometric literature typically reduces identification of factor models to the second problem and focuses on rotational identification, taking variance identification for granted, see e.g. Geweke and Zhou (1996). However, uniqueness of the factor loading matrix of given does not imply identification. Variance identification is easily violated in particular for sparse factor analysis, as following considerations illustrate. Consider a sparse one-factor model for measurements, for which rotational invariance is not an issue, with two different loading matrices. In the first case all but two factor loadings are 0 (e.g. , ), whereas in the second case all but three factor loadings are 0 (e.g. , ), implying, respectively, the following covariance matrices :

As only the diagonal elements of depend on , the factor loadings can be identified only via the off-diagonal elements of . For the first model, only is nonzero, whereas all remaining covariances are equal to zero, hence, only the three sample moments , , and are available to identify the four parameters , , , and . Therefore, a sparse factor model with only two nonzero factor loadings is not identified, since infinitely many different parameters , , , and imply the same distribution for the observed data . For the second model the three covariances , , and are nonzero and in total six sample moments are available to identify the six parameters , . From these considerations, it is evident that a one-factor model is identifiable only, if at least 3 factor loadings are nonzero, which has been noted as early as Anderson and Rubin (1956).

For a basic factor model with at least two factors, uniqueness of the variance decomposition, i.e. the identification of the idiosyncratic variances in from the variance decomposition (4) of has to be verified in addition to solving rotational invariance. More precisely, given any pair and satisfying (4) and (5), under which condition does this imply that and ? In the present paper, we rely on the row deletion property of Anderson and Rubin (1956) to ensure variance identification. Anderson and Rubin (1956, Theorem 5.1) prove that the following condition is sufficient for the identification of and from the marginal covariance matrix given in (4):

-

AR.

Whenever an arbitrary row is deleted from , two disjoint submatrices of rank remain.

In standard factor analysis, where all rows of are nonzero and the factor loadings are unconstrained except for dedicated zeros that are introduced to resolve the rotation problem (see Subsection 2.4), condition AR is typically satisfied, if the following upper bound for the number of factors holds:

| (7) |

i.e. . From condition AR it is apparent that for a sparse factor model a minimum number of three nonzero elements has to be preserved in each column, despite variable selection, to guarantee uniqueness of the variance decomposition and identification of . Hence, too many zeros in a sparse factor loading matrix may lead to non-identifiability of and , and subsequently to a failure to identify . This issue is hardly ever addressed in the literature on sparse Bayesian factor analysis. In Theorem 2 in Subsection 2.3, we introduce a counting rule (which will be called the 3-5-7-9-… rule for obvious reasons) that provides a sufficient condition to verify the row deletion property AR for sparse Bayesian factor models.555A less restrictive bound than (7) which is widely used in psychological research is the Lederman bound (Ledermann, 1937). However, for the time being we did not succeed in formulating a sufficient counting rule within this class of factor models.

The identifiability of guarantees that is identified. The second step of identification is then to ensure uniqueness of the factor loadings, i.e. unique identification of from . As is well-known, without imposing constraints on , the model is invariant under transformations of the form and , where is an arbitrary orthogonal matrix (i.e. ), since evidently,

| (8) |

A special case of rotational invariance is the following trivial rotational invariance,

| (9) |

where the permutation matrix corresponds to one of the ! permutations and the reflection matrix to one of the ways to switch the signs of the columns of . Often, identification rules are employed that guarantee identification of only up to such column and sign switching, see e.g. Conti et al. (2014). Any structure obeying such an identification rule represents a whole equivalence class of matrices given by all possible trivial rotations of defined in (9).

The usual way of dealing with rotational invariance is to constrain in such a way that the only possible rotation in (8) is the identity . For orthogonal factors as defined in (2), at least restrictions on the elements of are needed to eliminate rotational indeterminacy (Anderson and Rubin, 1956). The common constraint both in econometrics (Geweke and Zhou, 1996) and statistics (West, 2003; Lopes and West, 2004) is to consider positive lower triangular (PLT) matrices, i.e. to constrain the upper triangular part of to be zero and to assume that the main diagonal elements of are strictly positive. Although the PLT constraint is pretty popular, it is often too restrictive in practice. It induces an order dependence among the responses, making the appropriate choice of the first response variables an important modeling decision (Carvalho et al., 2008). Difficulties arise in particular, if one of the true factor loadings is equal or close to 0, see e.g. Lopes and West (2004).

Alternative strategies have been suggested, for instance by Kaufmann and Schuhmacher (2017) who exploit the single value decomposition of to solve rotational invariance. In Subsection 2.2, we introduce a new identification rule based on generalized lower triangular (GLT) structures. It should be emphasised that constraints imposed on to solve rotational invariance do not necessarily guarantee uniqueness of the variance decomposition.666Consider, for instance, a PLT loading matrix where in some column only two factor loading are nonzero: the diagonal element which is nonzero by definition and a second factor loading in some row . Such a loading matrix obviously violates the necessary condition for variance identification that each column contains at least three nonzero elements. This issue is hardly ever addressed explicitly in the econometric literature, an exception being Conti et al. (2014).777Conti et al. (2014) investigate identification of a dedicated factor model, where equation (1) is combined with correlated (oblique) factors, , and the factor loading matrix has a perfect simple structure, i.e. each observation loads on at most one factor. They prove a condition that implies uniqueness of the variance decomposition as well as uniqueness of the factor loading matrix and, consequently, the 0/1 pattern of the indicator matrix , namely: the correlation matrix is of full rank () and each column of contains at least three nonzero loadings. Variance identification for sparse Bayesian factor models is discussed in detail in Subsection 2.3.

2.2 Solving rotational invariance through GLT structures

In this paper, we relax the PLT constraint by allowing to be a generalized lower triangular (GLT) matrix:

-

GLT.

Let be a factor loading matrix and let (for each ) denote the row index of the top nonzero entry in the th column of (i.e. ). is a generalized lower triangular matrix, if and for .

For a GLT matrix , the leading indices satisfy and need not lie on the main diagonal. Obviously, the class of GLT matrices contains PLT matrices as that special case where for . This generalization is particularly useful, if the ordering of the response variables is in conflict with the PLT assumption. Since is allowed to be 0, response variables different from the first ones may lead the factors. Indeed, for each factor , the leading variable is the response variable corresponding to the leading index . An example of such a GLT matrix is displayed in the left-hand side of Figure 1. Evidently, all loadings above the leading element are zero by definition. A sparse GLT matrix results, if in addition some factor loadings below the leading element are zero as well. The condition prevents sign switching and can be substituted by the condition for any row with a nonzero factor loading in column . Condition GLT resolves rotational invariance, provided that the leading indices are ordered: evidently, for any two GLT matrices and with identical leading indices the identity holds, iff .

Any GLT structure represents a whole equivalence class of unordered GLT matrices given by all possible trivial rotations of defined in (9). Any unordered GLT structure has (unordered) leading indices , occupying different rows, see the right-hand side of Figure 1. The corresponding (ordered) GLT structure is recovered from the order statistics of by a trivial rotation and has leading indices .

In practice, the leading indices of a GLT structure are unknown and need to be identified from the data for a given number of factors . This is achieved in sparse Bayesian factor analysis by introducing an indicator matrix that obeys a GLT structure. Hence, we need to identify the entire 0/1 pattern in from , including the leading indices. Given variance identification, i.e. assuming that is identified, a particularly important issue for the identification of a sparse factor model is whether the 0/1 pattern in is uniquely identified. In general, is not uniquely identified from , because non-trivial rotations might exist that change the zero pattern in .

In the context of GLT structures, assume that an unordered GLT matrix exist with leading indices being possibly different from the leading indices of the loading matrix and both matrices solve . Then, Theorem 1 shows that the entire GLT structure including the leading indices and all zero loadings is uniquely identified from , up to trivial rotations, i.e. , meaning in particular that the sets of leading indices and are identical.

Theorem 1.

For a sparse GLT structure, is uniquely identified, provided that uniqueness of the variance decomposition holds, i.e.: if and are sparse GLT matrices, respectively, with leading indices and that satisfy , then . Hence, the leading indices as well as the entire 0/1 pattern of and are identical.

See Appendix A.1 for a proof. While the assumption of a GLT structure resolves the rotational invariance, it does not guarantee uniqueness of the variance decomposition.888Consider, for instance, a GLT matrix with the leading index in column being equal to . The loading matrix has at most two nonzero elements in column and violates the necessary condition for variance identification that each column contains at least nonzero three elements. In particular, an upper bound on the leading indices is necessary for AR to hold.

-

GLT-AR.

Let be an unordered GLT structure with leading indices . The following condition is necessary for condition AR:

(10) where is the rank of in the ordered sequence . For an ordered GLT structure, (10) reduces to .

For sparse GLT structures with zeros below the leading elements, GLT-AR is only a necessary, but not a sufficient condition for AR999A GLT structure obeying (10) with and , for instance, contains only two nonzero loadings in column and violates the necessary condition for variance identification that each column contains at least nonzero three elements. and variance identification has to be verified explicitly. An efficient procedure for dealing with this challenge is introduced in the following subsection.

2.3 Verifying the row deletion property for sparse factor loading matrices

For sparse Bayesian factor analysis, conditions for verifying directly from the zero pattern in the factor loading matrix, whether the row deletion property AR holds, would be very useful, but so far only necessary conditions have been provided. Anderson and Rubin (1956), for instance, prove the following necessary conditions for AR: for every nonsingular -dimensional square matrix , the matrix contains in each column at least 3 and in each pair of columns at least 5 nonzero factor loadings. Sato (1992, Theorem 3.3) extends these necessary conditions in the following way: every subset of columns of contains at least nonzero factor loadings.

Extending the results of Sato (1992), we prove in the following Theorem 2 that for unordered GLT factor matrices it is sufficient (and not only necessary) for AR that such a counting rule holds for the indicator matrix for a single trivial rotation of the factor loading matrix (and not for every nonsingular matrix ).

Theorem 2 (The 3-5-7-9-… counting rule).

Consider the following counting rule for an unordered GLT structure corresponding to an ordered GLT structure :

-

CR

For each and for each submatrix consisting of column of , the number of nonzero rows in this sub-matrix is at least equal to .

Condition CR is both necessary and sufficient for the row deletion property AR to hold for .

See Appendix A.1 for a proof. Theorem 2 operates on the indicator matrix which is very convenient for verifying variance identification in sparse Bayesian factor analysis. Most importantly, condition CR extends the 3-5 counting rule of Anderson and Rubin (1956) to a more general 3-5-7-9-… rule for the indicator matrix corresponding to the factor loading matrix. Obviously, if CR is violated for a single subset of columns of , then AR is violated for . For as well as for the corresponding counting rules can be easily verified from simple functionals of the indicator matrix , see Corollary 6 in Appendix A.2.1. Hence, for factor models with up to 4 factors () it is trivial to verify, if the 3-5-7-9-… counting rule and hence variance identification holds.

For models with more than four factors (), these simple counting rules are necessary conditions that quickly help to identify indicator matrices where CR (and hence AR) is violated. If the simple counting rules of Corollary 6 hold, then CR could be verified by iterating over all subsets of columns of ; a number rapidly increasing with . The following Theorem 3 shows that verifying AR greatly simplifies, if the loading matrix has a block diagonal representation. In this case, CR has to be checked only up to the maximum block size, rather than for the entire loading matrix.

Theorem 3.

Let be a factor loading matrix of full column rank, with nonzero rows. Assume that has following block diagonal representation after suitable permutations of rows and columns, with and being the corresponding permutation matrices:

| (15) |

where , , are -dimensional matrices such that and . Assume that are of full column rank . Then the following holds:

-

(a)

If all sub matrices satisfy the row deletion property AR with , then the entire loading matrix satisfies the row deletion property AR with .

-

(b)

If the submatrix violates the row deletion property AR with , then the row deletion property AR is violated for the entire loading matrix .

See Appendix A.1 for a proof. Part (a) of Theorem 3 is useful to verify that AR holds for sparse loading matrices that have a block diagonal representation as in (15). Part (b) of Theorem 3 is useful to quickly identify indicator matrices where AR does not hold. In Appendix A.2.2, Algorithm 3 is discussed that derives representation (15) sequentially and is useful for verifying variance identification in practice.

2.4 Identification of irrelevant variables

Irrelevant variables are observation for which the entire row of

the factor loading matrix is zero. This implies that is uncorrelated

with the remaining variables. As argued by Boivin and

Ng (2006), it is useful to identify such variables.

Within the framework of sparse Bayesian factor analysis, such irrelevant variables can be identified

by exploring the 0/1 pattern of the indicator matrix with respect to zero rows, see Kaufmann and

Schuhmacher (2017).

In Lemma 4 formal identification of irrelevant variables from is proven,

provided that the number of factors satisfies a more general upper bound than (7).

This commonly used upper bound is based on the assumption that all rows of are nonzero and

a different upper bound is needed, if we want to learn the position of the

zero rows from a sparse factor analysis applied to all variables. The corresponding bound

is derived from the fact that we need at least nonzero rows for the row deletion

property AR to hold.

Lemma 4.

Assume that a factor loading matrix contains zero rows and that the number of factors satisfies following upper bound:

| (16) |

If uniqueness of the variance decomposition holds, then the position of the zero rows in is uniquely identified, that is, any other -factor loading matrix satisfying has exactly the same set of zero rows.

See Appendix A.1 for a proof.

2.5 Identification in overfitting factor models

Assume that the data are generated by the basic factor model (1) with the corresponding variance decomposition in (4) being unique, however, the true number of factors is not known. In this case, a common procedure is to perform exploratory factor analysis based on a model with increasing number of factors ,

| (17) |

where is a loading matrix with elements and is a diagonal matrix with strictly positive diagonal elements. As before, we allow the elements of in this potentially overfitting sparse factor model to be zero, with the corresponding indicator matrix being denoted by . Factor analysis based on model (17) yields the extended variance decomposition

| (18) |

instead of the true variance decomposition (4). If model (17) is not overfitting, that is , then variance identification implies that and for some orthogonal matrix .

However, if , then model (17) is, indeed, overfitting and additional identifiability issues have to be addressed for such overfitting factor models. In particular, identifiability of and from (18) is lost, as infinitely many representations with exist that imply the same covariance matrix as . This identifiability problem has been noted earlier by Geweke and Singleton (1980) and Tumura and Sato (1980). Consider, e.g., a model that is overfitting with . Then infinitely many representations can be constructed that imply the same covariance as , namely:

| (23) |

where is an arbitrary factor loading satisfying and is an arbitrary row index different from the leading indices in . The last column of corresponds to a so-called spurious factor which loads only on a single observation. Hence, factor analysis in an overfitting model with may yield factor loading matrices of rank , containing a spurious factor, rather than loading matrices of rank with a zero column. For arbitrary , Tumura and Sato (1980) provide a general representation of the factor loading matrix in an overfitting factor model. Suppose that has a decomposition as in (4) with factors and for some with , or equivalently,

| (24) |

the following extended row deletion property holds:

-

TS

Whenever rows are deleted from , then two disjoint submatrices of rank remain.

If has another decomposition such that where is a -matrix of rank with , then Tumura and Sato (1980, Theorem 1) show that there exists an orthogonal matrix of rank such that

| (26) |

where the off-diagonal elements of are zero. Hence, is a so-called spurious factor loading matrix that does not contribute to explaining the correlation in , since

While (26) is an important result, without imposing further structure on the factor loading matrix it is of limited use in applied factor analysis, as the separation of into the true factor loading matrix and the spurious factor loading matrix is possible only up to a general rotation of .

The following Theorem 5 shows that extended identification in overfitting sparse factor models can be achieved within the class of unordered GLT structures as introduced in this paper. If in model (17) is constrained to be an unordered GLT structure, then can be easily recovered from (26). First, all rotations in (26) are equal to trivial rotations , only. Hence, the columns of the spurious loading matrix appear in between the columns of . Second, the spurious loading matrix is easily identified as an unordered spurious GLT matrix, where in each column the leading element is the only nonzero loading. This powerful result is exploited subsequently in our MCMC procedure to navigate through overfitting models with varying the number of factors, by adding and deleting spurious factors.

Theorem 5.

Assume that is a GLT factor loading matrix with leading indices that obeys the extended row deletion property TS for some . If in the extended variance decomposition is restricted to be an unordered GLT matrix with leading indices , then the following holds:

-

(a)

and can be represented in terms of , , and as in (26) up to trivial rotations .

-

(b)

is a spurious GLT structure with leading indices with exactly one nonzero loading in each column. Furthermore, all leading indices are different from the leading indices of .

-

(c)

The leading indices of are identical to the leading indices of the matrix .

See Appendix A.1 for a proof. For an unordered GLT structure, TS implies a constraint on the leading indices of which extends GLT-AR:

-

GLT-TS.

Let be an unordered GLT structure with nonzero columns with leading indices . The following condition on the leading indices is necessary for condition TS:

(27) where is the rank of in the ordered sequence .

3 Bayesian inference

Bayesian inference is performed in the overfitting sparse factor model (17) where satisfies the upper bound (24) for a given degree of overfitting . Both as well as are user-selected parameters. The maximum number of potential factors is chosen large enough that zero and spurious columns will appear during posterior inference. We found it useful to allow for at least spurious columns.

3.1 Prior specifications

Let be the indicator matrix corresponding to the loading matrix in model (17). Within our sparse Bayesian factor analysis, a joint prior for , and the variances is selected, taking the form

3.1.1 The prior on the indicators

Following common hierarchical point mass mixture prior on the indicator matrix is applied:

| (28) | |||

where all indicators are independent a priori given .101010Alternative priors (which are not pursued in the present paper) have been considered e.g. by Conti et al. (2014) and Kaufmann and Schuhmacher (2018). Since the true number of factors is unknown, we employ a prior on that implies column sparsity apriori. To this goal, the hyperparameters of prior (28) are chosen such that the number of nonzero columns in is random apriori, taking values less than with high probability. In this case, the model is overfitting and we are able to learn the number of factors . Hyperparameters that exclude zero columns in apriori are prone to overfit the number of factors. Prior (28) can be rewritten as:

| (29) |

where is the number of potential factors. For , prior (29) converges to the two-parameter Beta prior introduced by Ghahramani et al. (2007) in Bayesian nonparametric latent feature models which can be regarded as a factor model with infinitely many columns. However, if exceed the upper bound (24), variance identification can no longer be achieved. For this reason, we stay within the framework of factor models with finitely many columns in the present paper, but exploit column sparsity as explained above.

Following Ghahramani et al. (2007), we choose values considerably smaller than 1 (a sticky prior) to allow apriori zero columns for factor models where the number of factors is unknown. The choice of (or ) is guided by the apriori expected simplicity of the factor loading matrix, where is the number of nonzero loadings in each row which is typically smaller than . This leads to following choice for and :

| (30) |

As common in statistics and machine learning, the prior on does not account explicitly for identification. To deal with rotational invariance, an unordered GLT structure as introduced in Subsection 2.2 is imposed on during MCMC estimation, by sampling only indicator matrices where the leading indices of the nonzero columns of satisfy condition GLT-TS given in (27) for the specified value of , i.e. prior is constrained implicitly to unordered sparse GLT structures. The unordered GLT structure enforced during MCMC estimation breaks the invariance of the procedure with respect to the ordering of the data. However, it is less sensitive to the ordering of the data than the PLT constraint.

3.1.2 The prior on the idiosyncratic variances

When estimating factor models using classical statistical methods, such as maximum likelihood (ML) estimation, it frequently happens that the optimal solution lies outside the admissible parameter space with one or more of the idiosyncratic variances s being negative, see e.g. Bartholomew (1987, Section 3.6). An empirical study in Jöreskog (1967) involving 11 data sets revealed that such improper solutions are quite frequent and this difficulty became known as the Heywood problem. The introduction of a prior on the idiosyncratic variances within a Bayesian framework, typically chosen from the inverted Gamma family, that is

| (31) |

naturally avoids negative values for . Nevertheless, there exists a Bayesian analogue of the Heywood problem which takes the form of multi-modality of the posterior of with one mode lying at 0. This is likely to happen, if a small value and fixed hyperparameters are chosen in (31), as common in Bayesian factor analysis.

Subsequently, we select and in such a way that Heywood problems are avoided. Heywood problems typically occur, if the constraint

| (32) |

is violated, where the matrix is the covariance matrix of defined in (4), see e.g. Bartholomew (1987, p. 54). It is clear from inequality (32) that has to be bounded away from 0. For this reason, improper priors on the idiosyncratic variances such as (Martin and McDonald, 1975; Akaike, 1987) are not able to prevent Heywood problems. Similarly, proper inverted Gamma prior with small degrees of freedom such as (Lopes and West, 2004) allow values too close to 0.

As a first improvement, we choose in (31) large enough to bound the prior away from 0, typically . Second, we reduce the occurrence probability of a Heywood problem which is equal to where through the choice of . The smaller , the smaller is this probability. However, since , a downward bias may be introduced, if is too small. We choose as the largest value for which inequality (32) is fulfilled by the prior expectation and is substituted by an estimator . This yields the following prior:

| (33) |

Inequality (32) introduces an upper bound for , the proportion of variance not explained by the common factors, which is considerably smaller than 1 for small idiosyncratic variances . Hence, our prior is particularly sensible, if the communalities are rather unbalanced across variables and the variance of some observations is very well-explained by the common factors, while this is not the case for other variables. Our case studies illustrate that this prior usually leads to unimodal posterior densities for the idiosyncratic variances.

An estimator of the inverse of the marginal covariance matrix is required to formulate prior (33). If , then the inverse of the sample covariance matrix could be used, i.e. . However, this estimator is unstable, if is not small compared , and does not exist, if . Hence, we prefer a Bayesian estimator which is obtained by combining the sample information with the inverted Wishart prior :

| (34) |

If the variables are standardized over , then is a sensible choice.

3.1.3 The prior on the factor loadings

Finally, conditional on and , a prior has to be formulated for all nonzero factor loadings. Since the likelihood function factors into a product over the rows of the loading matrix, prior independence across the rows is assumed. For a given , let be the vector of unconstrained elements in the th row of . The variance of the prior of is assumed to depend on , because this allows joint drawing of and and, even more importantly, sampling the model indicators without conditioning on the model parameters during MCMC estimation, see Algorithm 1 in Subsection 3.2.

For each row with nonzero elements, the standard prior takes the form

| (35) |

where, typically, (Lopes and West, 2004; Ghosh and Dunson, 2009; Conti et al., 2014). In addition, a fractional prior in the spirit of O’Hagan (1995) is introduced in this paper for sparse Bayesian factor models which can be interpreted as the posterior of a non-informative prior and a small fraction of the data. This yields a conditionally fractional prior for the “regression model”

| (36) |

where and . is a regressor matrix constructed from the latent factors (see Appendix B.1.2 for details). The fractional prior is then defined as a fraction of the full conditional likelihood, derived from regression model (36):

This yields the following fractional prior:111111Similar conditionally conjugate fractional priors have been applied by several authors for variable selection in latent variable models (Smith and Kohn, 2002; Frühwirth-Schnatter and Tüchler, 2008; Tüchler, 2008; Frühwirth-Schnatter and Wagner, 2010).

| (37) |

where and are the posterior moments under the non-informative prior :

| (38) |

Concerning the choice of the fraction , in general, larger values of extract more information from the likelihood than smaller values, which reduces the influence of the sparsity prior as increases, leading to a larger number of estimated factors. Depending on the relation between , , and , small values such as , or yield sparse solutions. In total, observations are available to estimate free elements in the coefficient matrix for a GLT structure.

If is considerably smaller than , then the variable selection literature suggests to choose . This is in particular the case, if the potential number of factors is considerably smaller than . On the other hand, if is in the order of , then implies a fairly small penalty and may lead to overfitting models. Following Foster and George (1994), the risk inflation criterion can be applied in this case. For a GLT sructure, implies a stronger penalty than , if .

3.2 MCMC estimation

We use MCMC techniques to sample from the posterior (with of the overfitting model (17), given the priors introduced in Subsection 3.1. As noted by many authors, e.g. Pati et al. (2014), MCMC sampling for sparse Bayesian factor models is notoriously difficult, since sampling the indicator matrix corresponds to navigating through an extremely high dimensional model space. This is even more challenging, if the sparse factor model is overfitting.

In this paper, a designer MCMC scheme is employed which is summarized in Algorithm 1, where several steps have been designed specifically for sparse Bayesian factor models under the GLT constraint when the number of factors is unknown. This designer MCMC scheme delivers posterior draws of and with a varying number of nonzero columns. An unordered GLT structure is imposed on the nonzero columns and by requiring that the leading indices obey condition GLT-TS given in (27). Non-identification with respect to trivial rotations introduces column and sign switching during MCMC sampling. Hence, the sampler produces draws that fulfill various necessary conditions for identification, while the more demanding sufficient conditions are assessed through a scanning of the posterior draws during postprocessing, see Subsection 3.3.3.

Algorithm 1 (MCMC estimation for sparse Bayesian factor models with unordered GLT structures).

Choose initial values121212See Appendix B.2.4 for details. for , iterate times through the following steps and discard the first draws as burn-in:

-

(F)

Sample the latent factors conditional on the model parameters and from .

-

(A)

Perform a boosting step based either on ASIS or marginal data augmentation.

-

(R)

Perform a reversible jump MCMC step to add or delete spurious columns in and .

-

(L)

Loop over all nonzero columns of the indicator matrix in a random order and sample the leading index conditional on the remaining columns , the factors , and without conditioning on the model parameters and .

-

(D)

Loop over all nonzero columns of the indicator matrix in a random order. Sample for each column all indicators below the leading index (i.e. with ) conditional on the remaining columns , the factors , and (without conditioning on the model parameters and ) jointly using Algorithm 6 in Appendix B.1.5.

-

(H)

Sample , where is the number of nonzero factor loadings in column .

-

(P)

Sample the model parameters and jointly conditional on the indicator matrix and the factors from .

The most innovative part of this MCMC scheme concerns sampling the indicator matrix . Updating for sparse exploratory Bayesian factor analysis without identification constraints on is fairly straightforward, see e.g. Carvalho et al. (2008) and Kaufmann and Schuhmacher (2018), among many others. However, a more refined approach is implemented in the present paper to address the econometric identification issues for sparse factor models discussed in Section 2. The nonzero columns of and are instrumental for estimating the number of factors during postprocessing, see Subsection 3.3.1. To increase and decrease the number of nonzero columns in and , Step (R) exploits Theorem 5 to add and delete spurious factors through a reversible jump MCMC step described in Subsection 3.2.2. Similarly as in Conti et al. (2014), it is much easier to introduce new latent factors into the model through these spurious factors, compared to alternative approaches that would split existing factors or add new ones only under the condition that enough nonzero elements are preserved. To force the unordered GLT structure on the nonzero columns of and , Step (L) performs MH steps to navigate through the space of all admissible leading indices that satisfy GLT-TS, see Subsection 3.2.1. To implement Step (D) efficiently, a method for sampling an entire set of indicators in a particular column in one block is developed in Appendix B.1.5.

Step (F) and Step (P) operate in a “confirmatory” factor model where certain loadings are constrained to zeros according to the indicator matrix . Although these steps are standard in Bayesian factor analysis (see e.g. Lopes and West (2004) and Ghosh and Dunson (2009)) improvements are suggested such as multi-move sampling of all unknown model parameters , and in Step (P), see Appendix B.1.1 and B.1.3 for futher details. Finally, the boosting Step (A) is added to improve mixing of the MCMC scheme, see Subsection 3.2.3 and Appendix B.3 for more details.

3.2.1 Special MCMC moves for unordered GLT structures

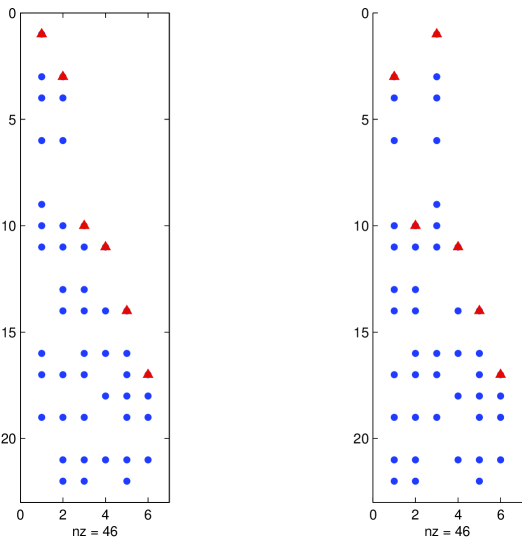

Step (L) in Algorithm 1 implements moves that explicitly change the position of the leading indices in the nonzero columns of (including spurious columns), without violating GLT-TS. Let be the set of leading indices. Since an unordered GLT structure has to be preserved, the leading index in column is not free to move, but restricted to a subset which depends on the leading indices of the other columns and the maximum degree of overfitting .131313See Subsection B.2.1 for a definition of . We scan all nonzero columns of in a random order and propose to change the position of in a selected column using one of four local moves, namely shifting the leading index, adding a new leading index, deleting a leading index and switching the leading elements (and all indicators in between) between column and a randomly selected column ; see Figure 2 for illustration and Subsection B.2.3 for further details.

3.2.2 Split and merge moves for overfitting models

For overfitting factor models, Step (R) in Algorithm 1 is a dimension changing move that explicitly changes the number of nonzero columns in and by adding and deleting a spurious column. If a spurious column is identified among the nonzero columns of , then as demonstrated in Subsection 2.5 it can be substituted by a zero column without changing the likelihood function, by adding to . On the other hand, any zero column in can be turned into an (additional) spurious column without changing the likelihood function either, see (23). This is the cornerstone of our procedure, however, while the likelihood is invariant to these moves, the prior is not and simply adding or deleting spurious columns would lead to an invalid MCMC step. A reversible jump MCMC step as implemented in Step (R) can correct for that.

The split and merge moves outlined above form a reversible pair that operates in the latent variable model (17) conditional on all parameters, except the hyperparameter which is integrated out of prior (28). Split and merge moves are local moves operating between the two following factor models:

| (39) | |||

| (40) |

where model (40) contains a spurious column with being the only nonzero loading in this column. If in model (40), then model (39) results. However, if , then, as discussed in Subsection 2.5, model (40) is not identified and can take any value such that . By integrating model (40) with respect to the spurious factor , it can be easily verified that both models imply the same distribution .

The split move turns one of the zero columns in (39) into a spurious column, by selecting a row not occupied by any other leading index and splitting the variance of the idiosyncratic error between the new variance and the spurious factor loading such that

Splitting is achieved by sampling from a distribution with support [-1,1] and defining:141414Specific choices for the distribution of are discussed in Appendix B.2.2. For instance, sampling from a uniform distribution on [0,1] worked pretty well in many situation.

Given and , new factors are proposed for the spurious column , independently for , from the conditional density which takes a very simple form (see Appendix B.2.2 for details):

By reversing the split move, the merge move sets the only nonzero factor loading in row of a spurious columns in (40) to zero, while increasing the idiosyncratic variance at the same time. Deleting the spurious column determines and in the following way:

Since column is turned into a zero column, new factors are proposed from the prior, i.e. for all .

At each sweep of the MCMC scheme, a decision has to be made whether a split or a merge move is performed. Evidently, no merge move can be performed, whenever the current factor loading matrix contains no spurious columns. Similarly, no split move can be performed, whenever no additional spurious columns can be introduced. This happens if no more zero columns are present or if the number of spurious columns is equal to . Otherwise, split and merge move are selected randomly, see Appendix B.2.2 which also contains details on the acceptance rates both for split and merge moves.

3.2.3 Boosting MCMC

Step (F) and Step (P) in Algorithm 1 perform full conditional Gibbs sampling for a confirmatory factor model corresponding to the current indicator matrix , by sampling the factors conditional on the loadings and idiosyncratic variances and sampling the loadings and idiosyncratic variances conditional on the factors. Depending on the signal-to-noise ratio of the latent variable representation, such full conditional Gibbs sampling tends to be poorly mixing. For the basic factor model (17), where , the information in the data (the “signal”) can be quantified by the matrix in comparison to the identity matrix (the “noise”) in the filter for (see Appendix B.1.1):

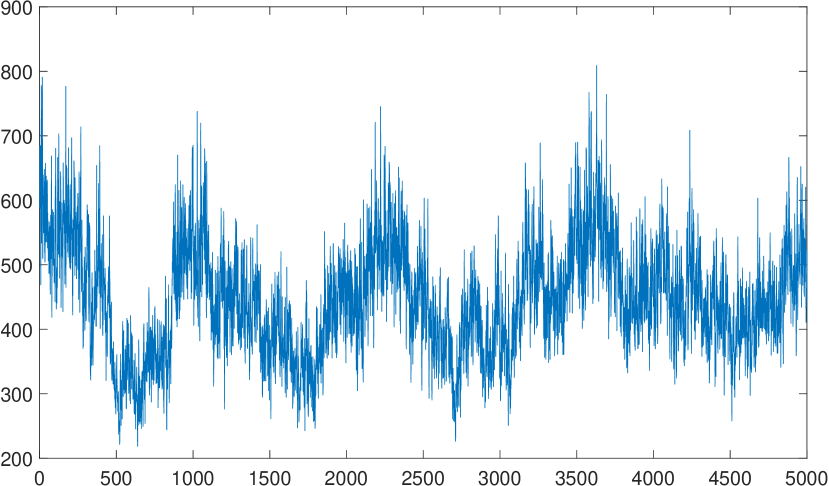

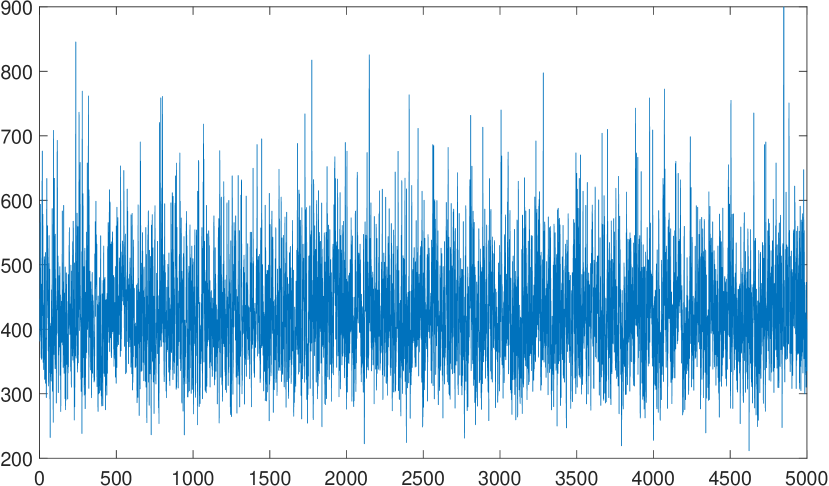

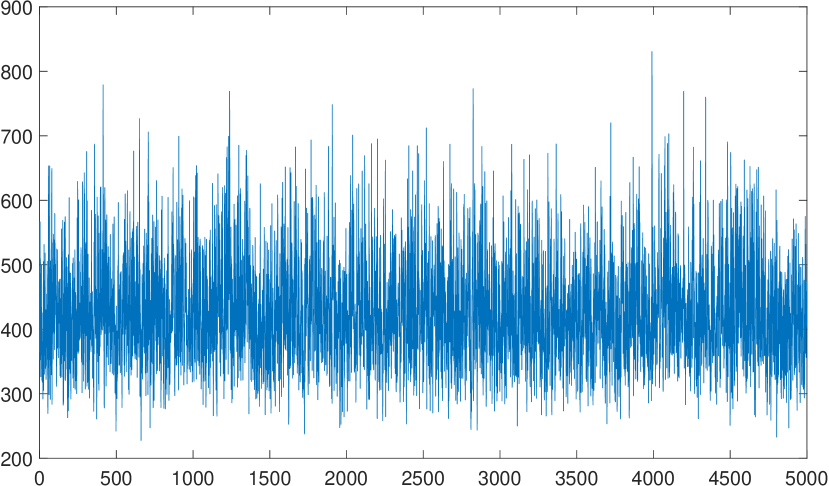

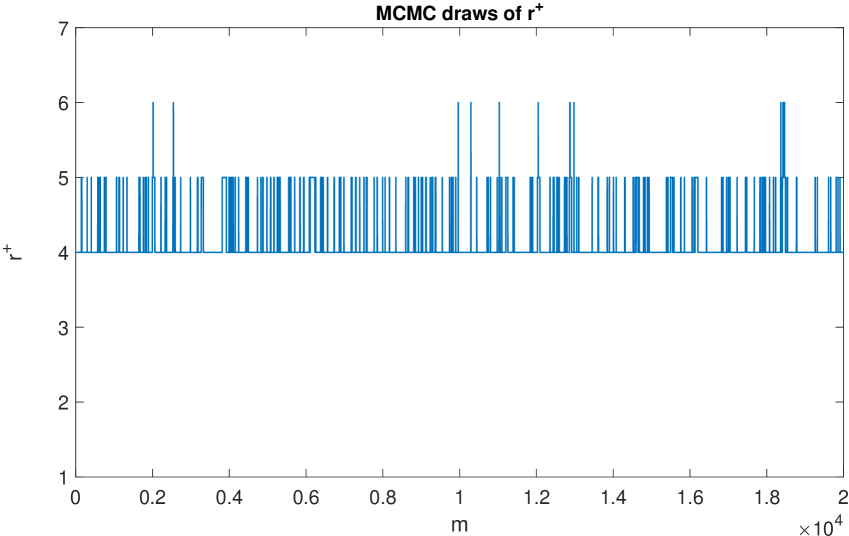

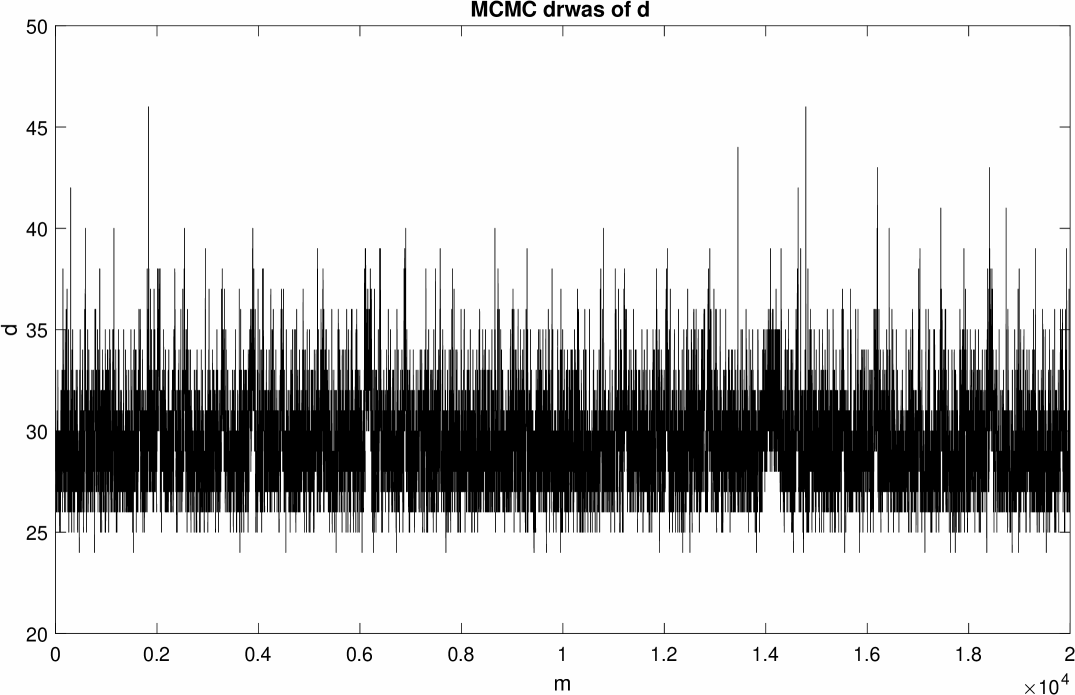

In particular for large factor models with many measurements, one would expect that the data contain ample information to estimate the factors . However, this is the case only, if the information matrix increases with , hence if most of the factor loadings are nonzero. For sparse factor models many columns with quite a few zero loadings are present, leading to a low signal-to-noise ratio and, as a consequence, to poor mixing of full conditional Gibbs sampling, as illustrated in the left-hand panel in Figure 3 showing posterior draws of without boosting Step (A) for the exchange data to be discussed in Subsection 4.1.

|

|

|

Hence, for sparse factor models it is essential to include boosting steps to obtain MCMC scheme with improved mixing properties, while keeping all priors unchanged. Popular boosting algorithms are the ancillarity-suffiency interweaving strategy (ASIS), introduced by Yu and Meng (2011), and marginal data augmentation (MDA), introduced by van Dyk and Meng (2001).151515ASIS has been applied to SV models (Kastner and Frühwirth-Schnatter, 2014), TVP models (Bitto and Frühwirth-Schnatter, 2016), and factor SV models (Kastner et al., 2017); MDA has been applied to factor models by Ghosh and Dunson (2009); Conti et al. (2014); Piatek and Papaspiliopoulos (2018). There are numerous examples in the literature, where boosting enhances mixing at the cost of changing the prior, an example being the MDA algorithm applied by Ghosh and Dunson (2009) to the basic factor model. However, changing the prior of the factor loading matrix in the original model is undesirable in any variable selection context and is avoided by the boosting strategies applied in the present paper.

Both for ASIS and MDA, boosting is based on moving from model (17) where to an expanded model with a more general prior:

where is diagonal. The relation between the two systems is given by following transformation:

| (41) |

Note that the nonzero elements in have the same position as the nonzero elements in . An important aspect of applying boosting in the context of sparse Bayesian factor models is the following. The transformation (41) has to be a one-to-one mapping for any kind of boosting based on parameter expansion to be valid. For sparse Bayesian factor models, this is true only for the nonzero columns of , whereas for any zero column , (41) would be satisfied for arbitrary values and many different expanded systems would map into the original system.161616Applying a boosting step to an unobserved factor has the undesirable effect that the prior of is no longer a normal distribution. Rather, it is a scale mixture of Gaussian distributions with the mixing distribution being equal to the distribution of . For instance, if follows an inverted Gamma distribution as in marginal data augmentation, then moving to the expanded model by rescaling the factors for all would lead to a model where follows a -prior rather than a normal distribution with scale . Hence, we set for all zero columns of and, for nonzero columns , choose in a deterministic fashion for ASIS and sample from a working prior for MDA.

For boosting based on ASIS, a nonzero factor loading is chosen in each nonzero column , to define the current value of as . This creates a factor loading matrix in the expanded system where for all nonzero columns , whereas for . For MDA, is sampled from a working prior , which is independent both of and . Our assumption of prior independence between the working parameter and the remaining parameters and guarantees that the prior distribution of remains unchanged, despite moving between the two models. For both boosting strategies, Step (A) in Algorithm 1 is implemented as described in detail in Algorithm 8 in Appendix B.3. For illustration, Figure 3 shows considerable efficiency gain in the posterior draws of for the exchange data, when a boosting strategy is applied, both for ASIS (middle panel) as well as MDA (right-hand panel).

3.3 Bayesian inference through postprocessing posterior draws

MCMC estimation through Algorithm 1 delivers draws from the posterior that are not identified in the strict sense discussed in Subsection 2.1. The only quantity that can be inferred from the posteriors draws, without caring at all about identification, is the marginal covariance matrix . For posterior inference beyond such as estimating the number of factors and posterior identification of and , it is essential to consider only posterior draws for which the variance decomposition is unique. While most papers ignore this important aspect, variance identification for sparse Bayesian factor models is fully addressed in the present paper during post-processing. Due to the point-mass mixture prior employed in this paper, the posterior draws of contain valuable information both concerning the sparsity and identifiability of the factor loading matrix, as the point-mass mixture prior allows exact zeros in the factor loading matrix both apriori as well as aposteriori.

All posterior draws obtained from Algorithm 1 are post-processed, to verify if the nonzero column of satisfy the row-deletion property condition AR with . For draws with , the simple counting rules outlined in Corollary 6 in Appendix A.2.1 are applied. For draws with , a very efficient procedure is applied that derives a block diagonal representation as in Theorem 3 for sequentially and applies the 3-5-7-9-… rule to the corresponding subblocks, see Algorithm 3 in Appendix A.2.2 for more details. Any further Bayesian inference is performed for the variance identified draws, only.

3.3.1 Identification of the number of factors

Given posterior draws of and , the challenge is to estimate the number of factors , if the model is overfitting. A common procedure to identify the number of factor is to apply an incremental procedure, by increasing step by step, and to use model selection criteria such as information criteria (Bai and Ng, 2002) or Bayes factors (Lee and Song, 2002; Lopes and West, 2004) to choose the number of factors.

Alternatively, a number of authors suggested to estimate the number of factors in one sweep together with the parameters. Carvalho et al. (2008), for instance, infer from the columns from , after removing columns with a few nonzero elements in a heuristic manner. Bhattacharya and Dunson (2011) employ a procedure which increasingly shrinks factor loadings toward zero with increasing column number. The number of factors is changed during sampling by setting an entire column of the loading matrix to zero, if all factor loadings are close to 0. Kaufmann and Schuhmacher (2018) estimate a sparse dynamic factor model with an increasing number of potential factors and use so-called “extracted factor representation” during MCMC post-processing procedure to select the number of factors.

However, any such heuristic method of inferring the number of factors from the nonzero columns from in an overfitting model without checking uniqueness of variance decomposition is prone to be biased. Instead, our procedure relies on the mathematically justified representation of the loading matrix in an overfitting factor model given by Theorem 5 and provides a new, non-incremental approach for selecting the number of factors. We identify through a one-sweep MCMC procedure which is based on purposefully overfitting the number of potential factors within the framework of sparse Bayesian factor analysis as implemented above. A related strategy was also applied in Conti et al. (2014) within the framework of dedicated Bayesian Factor analysis.

Evidently, zero columns (if any) in can be removed, since , where contains the nonzero columns of . As outlined in Section 2.5, the number of nonzero columns is the equal to the number of factors , if the variance decomposition is unique for . This is no longer true, if uniqueness of the variance decomposition does not hold for . In an overfitting factor model with , many draws with nonzero columns will have a representation as in Theorem 5 and contain a submatrix with spurious columns, each of which has exactly one nonzero element. Hence, these draws violate even the most simple condition for variance identification. For such posterior draws , overestimates since, according to Theorem 5, , or equivalently: . Hence, methods of inferring the number of factors from the nonzero columns of the unconstrained posterior draws in an overfitting factor model with are prone to overestimate the number of factors, in particular, if many draws violate simple conditions for variance identification.

As opposed to this, we rely on uniqueness of variance decomposition and discard draws from the posterior sample that violate uniqueness of the variance decomposition for . For the remaining draws, the number of nonzero columns of can be considered as a posterior draw of the number of factors . The entire (marginal) posterior distribution can be estimated from these draws, using the empirical pdf of the sampled values for . The posterior mode of provides a point estimator of the number of factors . This inference is valid, even if the rotation problem for is not solved, as only uniqueness of the variance decomposition is essential.

It should be noted that point mass mixture priors are particularly useful in identifying spurious factors, since these priors are able to identify exact zeros in the columns corresponding to spurious factors. Under continuous shrinkage priors, see e.g. Bhattacharya and Dunson (2011); Ročková and George (2017), it is not straightforward, how to identify spurious factors.

3.3.2 Further inference for unordered variance identified GLT draws

In addition to estimating the number of factors as in Subsection 3.3.1, further Bayesian inference can be performed for the variance identified draws without resolving trivial rotation. Evidently, posterior inference is possible for all idiosyncratic variances in . Functionals of , such as the trace of and as well as the (log) determinant of are useful means of assessing convergence of the MCMC sampler. Furthermore, for each variable inference with respect to the proportion of the variance explained by the common factors (also known as communalities ) is possible:

| (42) |

In addition, due to Lemma 4, irrelevant variables can be identified through the position of zero rows. This allows to estimate the (marginal) posterior probability for all variables by counting the frequency of the event during MCMC sampling for each row . Finally, overall sparsity in terms of the number of nonzero elements in ,

| (43) |

can be evaluated. Posterior draws of are particularly useful to check convergence and assessing efficiency of the MCMC sampler, as captures the ability of the sampler to move across (variance identified) factor models of different dimensions.

3.3.3 Resolving trivial rotation issues

For all unordered GLT draws that are variance identified, the factor loading matrix and the corresponding indicator matrix are uniquely identified from the nonzero columns and of and the corresponding indicator matrix by Theorem 1. Since the MCMC draws and are trivial rotations of and , column and sign switching are easily resolved. First, the columns of are ordered such that the leading indices obey ; i.e. . Then, the sign of the entire column of is switched if the leading element is negative; i.e. . In addition, the factors corresponding to the nonzero columns of are reordered through for . Finally, is also used to reorder the draws of the hyperparameter of the prior .

The draws of are exploited in various ways. Their leading indices are draws from the marginal posterior distribution allowing posterior inference w.r.t to . In particular, the identifiability constraint visited most often is determined together with its frequency which reflects posterior uncertainty with respect to choosing the leading indices. The number of elements in provide yet another estimator of the number of factors. Furthermore, the highest probability model (HPM), i.e. the indicator matrix visited most often, its frequency (an estimator of the posterior probability of the HPM), its model size , and its leading indices are of interest, and whether coincides with .

Bayesian inference with respect to the loading matrix is performed conditional on , to avoid switches between different leading indices. Averaging over the corresponding MCMC draws provides an estimate of and the marginal inclusion probabilities for all elements of the corresponding indicator matrix. Also, the median probability model (MPM) , obtained by setting each indicator to one whenever , and its model size are of interest.

4 Applications

All computations are based on the designer MCMC algorithm introduced in Algorithm 1, with boosting in Step (A) being based on ASIS with choosing as the largest loading (in absolute values) in each nonzero column (see Appendix B.3), choosing as proposal in Step (R) (see Appendix B.2.2) and choosing in Step (L) (see Appendix B.2.3).

4.1 Sparse factor analysis for exchange rate data

To analyze exchange rates with respect to the Euro, data was obtained from the European Central Bank’s Statistical Data Warehouse and ranges from January 3, 2000 to December 3, 2007. It contains exchange rates listed in Table 1 from which we derived monthly returns, based on the first trading day in a month. The data are demeaned and standardized.171717A similar set of exchange rates (however with daily returns) was studied in Kastner et al. (2017).

|

|

Since the number of factors is unknown, an overfitting factor model is applied with maximum degree of overfitting and the maximum number of factors obeying inequality (24). The hyperparameter of the prior (28) for the indicators is chosen as , while is chosen such that a prior simplicity of is achieved. This implies in the parameterization (29). This prior introduces column sparsity, see the corresponding prior distributions for the number of nonzero columns reported in Table 2, with most of the prior mass being considerably smaller than .181818This prior distributions was determined by simulating indicator matrices from the prior (28), restricted to GLT structures, and rejecting all draws that did not fulfill condition AR for the nonzero columns.

The prior (33) on the idiosyncratic variances is selected with and being estimated from (34) with and . To study sensitivity to further prior choices, we consider fractional priors (37) with . Since , choosing is the recommended choice. In addition, the standard prior (35) is considered with , and (Lopes and West, 2004).

| 0-1 | 2 | 3 | 4 | 5 | 6 | 7 | 8- 9 | ||

| 0.0434 | 0.112 | 0.231 | 0.2642 | 0.1996 | 0.1106 | 0.0336 | 0.0054 | 27.4 | |

| 0 | 0 | 0.96 | 0.04 | 0 | 0 | 0 | 0 | 58.2 | |

| 0 | 0 | 0.36 | 0.63 | 0 | 0 | 0 | 74.1 | ||

| 0 | 0 | 0.04 | 0.95 | 0 | 0 | 0 | 80.6 | ||

| 0 | 0 | 0.88 | 0.11 | 0 | 0 | 58.9 | |||

| 0 | 0 | 0 | 0.63 | 0.34 | 0.02 | 0 | 42.9 | ||

| LW | 0 | 0 | 0 | 0.19 | 0.47 | 0.29 | 0.05 | 22.1 | |

| no varide | |||||||||

| 0 | 0 | 0.89 | 0.10 | 0 | 0 | 0 | |||

| 0 | 0 | 0.40 | 0.54 | 0.06 | 0 | 0 | |||

| 0 | 0 | 0.04 | 0.80 | 0.15 | 0 | ||||

| 0 | 0 | 0.54 | 0.38 | 0.08 | |||||

| 0 | 0 | 0 | 0.28 | 0.44 | 0.23 | 0.05 | |||

| LW | 0 | 0 | 0 | 0.05 | 0.27 | 0.43 | 0.24 | ||

Algorithm 1 is run for draws after a burn-in of draws. To verify convergence, independent MCMC chains were started respectively with and nonzero columns. As discussed in Subsection 3.2, this sampler navigates in the space of all unordered GLT structures with an unknown number of nonzero columns and unknown leading indices, without forcing variance identification. Apart from no further parameters are identifiable from the unrestricted draws, and as outlined in Subsection 3.3, we screen for variance identified draws during post-processing. The fraction of variance identified draws is reasonably high, as reported in Table 2 for each prior.

We use only variance identified draws for further inference. Most importantly, for these draws the number of nonzero columns of may be regarded as draws of the number of factors. Table 2 reports the posterior distribution for all priors under investigation and the left-hand side of Figure 4 shows posterior draws of for the fractional prior for illustration. All fractional priors based on point at a four factor solution. The fractional prior with introduces too strong shrinkage leading to a three factor model, whereas the standard prior of Lopes and West (2004) leads to an overfitting model with six factors.

Our designer MCMC scheme shows good mixing across models of different dimension, as illustrated by Figure 4 showing posterior draws of and the model size for the fractional prior , with an inefficiency factor of roughly 8 for . This good behaviour is particularly due to the RJMCMC Step (R) in Algorithm 1, which has an acceptance rate of 18.9% for a split and 30.8% for a merge move.

As outlined in Subsection 3.3, the variance identified draws can be post-processed further. For instance, it is possible to investigate, if some measurements are uncorrelated with the remaining measurements. This is investigated in Table 3 through the posterior probability , where is the row sum of . Various currencies appear to be uncorrelated with the rest, namely Swiss franc (CHF), Czech koruna (CZK), the Mexican peso (MXN), the New Zealand dollar (NZD ), the Romania fourth leu (RON), and the Russian ruble (RUB).

| Currency | CHF | CZK | MXN | NZD | RON | RUB | remaining |

|---|---|---|---|---|---|---|---|

| 0.98 | 0.95 | 0.98 | 0.85 | 0.97 | 0.97 | 0 | |

| 0.96 | 0.89 | 0.94 | 0.75 | 0.90 | 0.91 | 0 | |

| 0.93 | 0.82 | 0.91 | 0.68 | 0.78 | 0.81 | 0 | |

| 0.83 | 0.59 | 0.78 | 0.44 | 0.56 | 0.51 | 0 | |

| 0.28 | 0.64 | 0.35 | 0.76 | 0.59 | 0.73 | 0 | |

| LW | 0.14 | 0.01 | 0.11 | 0.01 | 0.02 | 0 | |

| Prior | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 3 | 21 | 2709 | 42.8 | (1,2,5) | 20 | (1,2,5) | 88.5 | 3 | 20 | |

| 4 | 24 | 10809 | 10.6 | (1,2,5,7) | 20 | (1,2,5,7) | 49.7 | 4 | 20 | |

| 4 | 27 | 19198 | 11.9 | (1,2,5,7) | 26 | (1,2,5,7) | 85.5 | 4 | 26 | |

| 4 | 29 | 42906 | 2.9 | (1,2,5,7) | 26 | (1,2,5,7) | 65.3 | 4 | 26 | |

| 4 | 32 | 50920 | 0.5 | (1,2,5,7) | 26 | (1,2,5,7) | 37.3 | 4 | 27 | |

| LW | 6 | 59 | 32921 | 0.01 | (1,2,3,4,5,6) | 56 | (1,2,3,4,5,6) | 11.2 | 6 | 52 |

Further Bayesian inference is reported in Table 4, including the posterior mode estimator , the posterior mean of the model size defined in (43), the total number of visited GLT structures, the identifiability constraint visited most often together with its frequency (in percent), as well as the frequency (in percent), the leading indices and model size of the highest probability model (HPM) . For all priors, coincides with . For all 4-factor models, the GLT constraint turns out to be the most likely constraint, whereas for the 3-factor models the GLT constraints is preferred. Once more we find that a standard prior as in Lopes and West (2004) leads to an overfitting model both in terms of the factors as well in terms of the model size. Too many models are visited, leading to a very small posterior probability for the HPM.

As a final step, the factor loadings and the MPM are identified for a 4-factor model. This inference is based on all posterior draws where the leading indices of (after reordering) coincide with the GLT constraint . From these draws, the marginal inclusion probabilities and the corresponding median probability model (MPM) are derived. Its model size is reported in Table 4 for all priors.

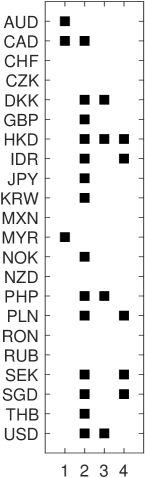

For most fractional priors, the HPM and the MPM coincide. Table 5 reports the marginal inclusion probabilities for the fractional prior and Figure 5 displays both models for illustration. The resulting model indicates considerable sparsity, with many factor loadings being shrunk toward zero. Factor 2 is a common factor among the correlated currencies, while the remaining factors are three group specific, for the most part dedicated factors.

| Currency | Factor 1 | Factor 2 | Factor 3 | Factor 4 |

|---|---|---|---|---|

| AUD | 1 | 0 | 0 | 0 |

| CAD | 1 | 1 | 0 | 0 |

| CHF | 0.01 | 0.12 | 0 | 0 |

| CZK | 0.01 | 0.21 | 0 | 0 |

| DKK | 0.02 | 1 | 1 | 0 |

| GBP | 0.07 | 1 | 0.05 | 0 |

| HKD | 0.01 | 1 | 0.97 | 1 |

| IDR | 0.04 | 1 | 0.03 | 1 |

| JPY | 0.13 | 1 | 0.01 | 0.02 |

| KRW | 0.01 | 1 | 0.06 | 0.02 |

| MXN | 0.01 | 0.16 | 0.01 | 0.01 |

| MYR | 1 | 0.06 | 0.01 | 0.01 |

| NOK | 0.01 | 1 | 0.01 | 0.02 |

| NZD | 0.09 | 0.42 | 0.04 | 0.01 |

| PHP | 0.01 | 1 | 0.95 | 0.04 |

| PLN | 0.01 | 1 | 0.02 | 0.73 |

| RON | 0.14 | 0.06 | 0.24 | 0.01 |

| RUB | 0.27 | 0.11 | 0.09 | 0.16 |

| SEK | 0.01 | 1 | 0.01 | 0.99 |

| SGD | 0.03 | 1 | 0.03 | 0.99 |

| THB | 0.01 | 1 | 0.01 | 0.02 |

| USD | 0.02 | 1 | 1 | 0.01 |

Finally, Table 6 shows the posterior mean of the factor loading matrix, the idiosyncratic variances and the communalities, obtained by averaging over all draws where the leading indices of coincide with . Sign switching in the posterior draws of is resolved through the constraint , , , and . As expected, nonzero factors loading have relatively high communalities for the different currencies, whereas for zero rows the communalities are practically equal to zero.

| Factor loadings | Communalities | ||||||||

| Currency | |||||||||

| AUD | 0.96 | 0 | 0 | 0 | 88 | 0 | 0 | 0 | 0.12 |

| CAD | 0.39 | 0.6 | 0 | 0 | 17 | 39 | 0 | 0 | 0.42 |

| CHF | -0.02 | 0 | 0 | 0.36 | 0 | 0 | 0.98 | ||

| CZK | 0.04 | 0 | 0 | 0.96 | 0 | 0 | 0.98 | ||

| DKK | 1.1 | 0.22 | 0 | 95 | 4.2 | 0 | 0.01 | ||

| GBP | 0.01 | 0.57 | -0.01 | 0 | 0.39 | 32 | 0.27 | 0 | 0.70 |

| HKD | 0.5 | 0.39 | 0.76 | 22 | 14 | 49 | 0.17 | ||

| IDR | 0.01 | 0.8 | -0.01 | 0.42 | 58 | 16 | 0.29 | ||

| JPY | 0.02 | 0.93 | 0.35 | 76 | 0.27 | ||||

| KRW | 1.1 | 0.01 | 96 | 0.01 | |||||

| MXN | 0.03 | 0.65 | 0.98 | ||||||

| MYR | 0.79 | 61 | 0.40 | ||||||

| NOK | 0.89 | 70 | 0.33 | ||||||

| NZD | 0.025 | 0.11 | -0.01 | 0.75 | 3.2 | 0.29 | 0.95 | ||

| PHP | 0.55 | -0.42 | 0.01 | 29 | 18 | 0.14 | 0.56 | ||

| PLN | 1 | 0.12 | 86 | 1.9 | 0.14 | ||||

| RON | 0.04 | -0.08 | 1.3 | 0.11 | 3 | 0.95 | |||

| RUB | -0.09 | 0.02 | 0.03 | 0.05 | 3.2 | 0.35 | 0.84 | 1.6 | 0.94 |

| SEK | 0.98 | 0.31 | 82 | 8.5 | 0.11 | ||||

| SGD | 0.75 | 0.39 | 51 | 14 | 0.37 | ||||

| THB | 0.59 | 33 | 0.7 | ||||||

| USD | 1.1 | 0.22 | 95 | 4.2 | 0.01 | ||||

4.2 Sparse factor analysis for NYSE100 returns

To show that our approach also scales to higher dimensions, we consider monthly log returns from firms from NYSE100 observed for months from January 1992 to December 2011. Again, the data are standardized. Since the number of factors is unknown, an overfitting factor model is applied with the maximum degree of overfitting and being considerably smaller than the upper bound given by (24). The hyperparameters of the prior (28) for the indicators are chosen as and , implying a prior simplicity of and in parameterization (29). The prior (33) is chosen for with and being estimated as in (34), with and . Since , we consider fractional priors with , where . Further tuning is exactly as in Subsection 4.1.

The designer MCMC scheme outlined in Algorithm 1 is used to obtain draws after a burn-in of draws starting, respectively, with and . Functionals of the posterior draws were used to monitor MCMC convergence. The fraction of MCMC draws satisfying AR is smaller than in the previous subsection but, being in the order of 8 to 11%, still acceptable. Although the prior is fairly wide-spread, the posterior distribution derived from all variance identified draws turns out to be strongly centered on for all three fractional priors, see Table 7.

| 12 | 13 | 14 | 15 | ||||

|---|---|---|---|---|---|---|---|

| 0 | 0.98 | 0.02 | 0 | 0 | 0 | 7.6 | |

| 0 | 0.70 | 0.27 | 0.02 | 0 | 0 | 10.7 | |

| 0 | 0.56 | 0.35 | 0.09 | 0 | 0 | 9.4 | |

| no varide | |||||||

| 0 | 0.88 | 0.12 | 0.01 | 0 | 0 | ||

| 0 | 0.30 | 0.45 | 0.22 | 0.03 | 0 | ||

| 0 | 0.21 | 0.52 | 0.23 | 0.04 | 0 | ||

The MCMC scheme shows good mixing, despite the high dimensionality, as illustrated by Figure 6 showing draws from the posterior distributions and for . The RJMCMC Step (R) in Algorithm 1 has an acceptance rate of 8.6% for a split and 14.7% for a merge move and the inefficiency factor for is equal to 8.

| (1,2,3,4,5,6,7,8,9,14,15,26) | 12 | 10.3 | |

| (1,2,3,4,5,6,7,8,9,14,15,26) | 12 | 9.9 | |

| (1,2,3,4,5,6,7,8,9,14,15,26) | 12 | 9.8 | |

| (1,2,3,4,5,6,7,8,9,14,15,26) | 12 | 10.8 | |

| (1,2,3,4,5,6,7,14,15,19,25,26) | 12 | 19.0 | |

| (1,2,3,4,5,6,7,9,14,15,25,26) | 12 | 25.2 |

In Table 8, the identifiability constraint visited most often is reported together with its frequency for all three priors for both runs. Also points at a 12-factor model for all priors and coincides for both runs for and . Further inference with respect to and is based on all posterior draws where the leading indices of (after reordering) are equal to . The corresponding median probability model (MPM) is shown for in Figure 7 and is extremely sparse with only nonzero loadings. The MPM clearly indicates that all returns are correlated191919This confirmed by the posterior probabilities which are equal to 1 for all firms. and one main factor is present which loads on all returns. The remaining factors are for the most part dedicated factors that capture cross-sectional correlations between specific firms.

5 Concluding remarks

We have characterised, identified and estimated (from a Bayesian viewpoint) a fairly important and highly implemented class of sparse factor models when the number of common factors is unknown. More specifically, we have explicitly and rigorously addressed identifiability issues that arise in this class of models by going well beyond and much deeper than simply applying rotation for identification and seeking instead uniqueness of the variance decomposition.