Abstract

We consider estimating an expected infinite-horizon cumulative discounted cost/reward contingent on an underlying stochastic process by Monte Carlo simulation. An unbiased estimator based on truncating the cumulative cost at a random horizon is proposed. Explicit forms for the optimal distributions of the random horizon are given, and explicit expressions for the optimal random truncation level are obtained, leading to a full analysis of the bias-variance tradeoff when comparing this new class of randomized estimators with traditional fixed truncation estimators. Moreover, we characterize when the optimal randomized estimator is preferred over a fixed truncation estimator by considering the tradeoff between bias and variance. This comparison provides guidance on when to choose randomized estimators over fixed truncation estimators in practice. Numerical experiments substantiate the theoretical results.

Keywords: Simulation; unbiased estimation; simulation optimization; computing budget allocation; cumulative costs

Optimal Unbiased Estimation for Expected Cumulative Discounted Cost

Zhenyu Cui 111School of Business, Stevens Institute of Technology, Hoboken, NJ-07030, United States of America; zcui6@stevens.edu, Michael C. Fu 222R.H. Smith School of Business, University of Maryland, College Park, MD-20742, United States of America; mfu@umd.edu, Yijie Peng 333Department of Industrial Engineering and Management, Peking University, Beijing, 100871, People’s Republic of China; pengyijie@pku.edu.cn, Lingjiong Zhu 444Department of Mathematics, Florida State University, 1017 Academic Way, Tallahassee, FL-32306, United States of America; zhu@math.fsu.edu.

1 Introduction

Motivation and Problem Formulation. We consider estimating an expected cumulative cost

where is the underlying stochastic process defined on a metric space (e.g. or ), and is a real-valued function of both the underlying process and time. This covers the special case , which is frequently used in asset pricing, where is the discount factor, and is referred to as cumulative discounted cost. For example, can be the expected present value of a discounted cumulative cash flow contingent on the future value of an underlying asset, where is the discount factor, the cash flow rate contingent on the asset value at time .

In finance, this is related to simulating a cumulative (discounted) cash flow of a stochastic perpetuity (Fox and Glynn (1989); Blanchet and Sigman (2011)) or a mortgage-backed security (MBS) (Glasserman and Staum (2003)). In steady-state simulation, corresponds to the expected long-run behavior of the sample time-average, e.g., average waiting time in a queueing system (Whitt (2002)). In project management, this corresponds to the accumulated present value of a project, and is a useful metric to decide between capital projects. This generic form also appears in the optimal lifetime consumption problem studied by Merton (1969).

In our setting, is assumed to be unavailable in closed form, but Monte Carlo simulation can be used to estimate . It is computationally infeasible to simulate the cumulative cost over an infinite horizon. Thus, a truncation technique is needed to estimate , and batching is typically used to construct a confidence interval (Alexopoulos et al. (2016)). However, truncating at a fixed horizon generally leads to bias, which is difficult to quantify in statistical inference. We propose a randomized estimator that truncates at a random horizon to retrieve the unbiasedness. By doing so, an asymptotically valid confidence interval can be obtained by sampling i.i.d. sample paths of cumulative cost truncated at the random horizon, which can be justified by a classical central limit theorem. Since variability is introduced by the random horizon, the unbiasedness of the estimator may come at the cost of a larger variance, which motivates us to ask the following question:

What is the optimal randomized unbiased estimator, and in what sense is it optimal?

Throughout, “optimal” means that within the class of unbiased estimators constructed based on a randomized truncation level, we are searching for the estimator satisfying some optimal criteria. More specifically, we consider three such criteria common in comparing Monte Carlo estimators: minimizing the variance with a linear penalty on the computational cost, minimizing variance with a fixed cost, and minimizing the work-variance product (see Glynn and Whitt (1992)).

The proposed estimator truncates the cumulative cost at a random horizon following a distribution independent of the underlying stochastic process. Our goal is to find an optimal distribution for the random horizon. We consider both a constrained optimization problem where the variance of the estimator is minimized subject to a fixed expected simulation cost/work, and an unconditional optimization problem where we seek to minimize the work-variance product (see e.g. Glynn and Whitt (1992)) of the estimator. These are infinite-dimensional functional optimization problems over all possible distributions, which are difficult to solve numerically in general. However, we derive explicit forms for the optimal distributions of the random horizon by using the maximum principle for an optimal control problem (see e.g. Bryson and Ho (1975)). The optimal distributions are in a shifted distribution class. For a discounted continuous cumulative cost contingent on an exponential Lévy process, the optimal randomization distributions are shifted exponential distributions. Glynn (1983) considers a similar cumulative cost estimation problem; however, since the objective there is to minimize the asymptotic variance of a randomized (unbiased) estimator, the focus is on asymptotic results, whereas we focus on the finite simulation budget setting. In particular, our results show that the optimal randomization distribution in the setting of Glynn (1983) is not necessarily optimal in any of the fixed computational budget settings we consider.

Although the proposed randomized estimator eliminates bias, it inevitably increases the variance. We define a utility function as a linear combination of bias and variance. With a positive weight on the variance, we show that the optimal randomized estimator is less favorable than the fixed truncation estimator when the computational budget is sufficiently small. A threshold function of the computational budget for the weight of variance is provided, and the advantage of the optimal randomized estimator can be justified if the weight of the variance is less than this threshold.

Related Literature. Related work on using randomization in other settings to recover unbiasedness includes McLeish (2011); Rhee and Glynn (2015) for stochastic differential equation (SDE) models. Rhee and Glynn (2015) use an infinite sum truncated at a random horizon independent of the underlying SDE to obtain an unbiased estimator of the path functionals associated with the SDE. They also derive an optimal distribution for the random horizon, but their objective is to minimize the asymptotic variance of the estimator, which assumes the computational budget goes to infinity, whereas we consider the setting of a fixed (finite) computational budget. As a result, solving for the optimal randomization distribution in their setting leads to a discrete optimization problem, whereas our formulation leads to a continuous-time functional optimal control problem that can be solved analytically by applying the maximum principle. Other work using randomization to eliminate bias includes unbiased estimation of Markov chain equilibrium expectations (Glynn and Rhee (2014)), unbiased stochastic optimization (Blanchet et al. (2015)), unbiased Bayesian inference (Lyne et al. (2015)), and unbiased maximum likelihood inference (Jacob et al. (2015)). None of the previous work provides analysis comparing randomized unbiased Monte Carlo (RUMC) method with traditional Monte Carlo (MC), e.g., a fixed truncation estimator, by taking both bias and variance into account. There is some recent work studying the choice of the optimal randomization distribution in the setting of unbiased estimation involving the solution of a SDE. Cui et al. (2019) proposed an approach based on the dual formulation, and Kahale (2019) proposed a method based on convex hulls. As far as we know, this is the first work dealing with RUMC from an optimal control perspective.

Closely related to the RUMC method is the multi-level Monte Carlo (MLMC) method introduced in Giles (2008, 2015), which combines biased estimators of different step sizes to improve the convergence rate of traditional MC method. There is also recent interest in combining RUMC and MLMC for developing an unbiased MLMC method, which can be found in Vihola (2018); Zheng and Glynn (2017).

Contribution. The contributions of our paper are three-fold:

-

1.

We propose an optimal randomized unbiased estimator for estimating the expected (infinite) cumulative cost/reward in a fixed computational budget setting.

-

2.

We provide explicit forms for the optimal randomization distributions balancing the trade-off between variance and computational cost.

-

3.

We offer theoretical justification for the advantage/disadvantage of RUMC over traditional MC by explicitly considering the tradeoff between bias and variance.

MLMC focuses on improving convergence rate rather than eliminating bias, and the existing RUMC work only minimizes the asymptotic variance of the randomized estimator. To the best of the authors’ knowledge, this is the first work resulting in explicit forms for the optimal distribution of an unbiased randomized estimator and comparing randomization with fixed truncation taking both bias and variance into consideration. In an example for the general class of exponential Lévy processes, the explicit forms can be calculated analytically, and the condition that the optimal RUMC outperforms traditional MC is given analytically. The explicit structure of the distribution function of the optimal random truncation level is particularly useful for “post-estimation” analysis, and allows us to carry out a full diagnosis of the bias-variance tradeoff.

Organization. The remainder of the paper is organized as follows. Section 2 proposes the randomized unbiased estimator with three optimal randomization distributions. We compare the optimal randomized estimator and fixed truncation estimator in Section 3. Numerical experiments are presented in Section 4. Section 5 concludes the paper.

2 Unbiased Randomized Estimator

We consider estimating the cumulative cost/reward: , which is assumed to be well-defined and finite. Here is the underlying stochastic process.

Let be a random horizon independent of the underlying stochastic process , and be the distribution of , which satisfies

The proposed randomized unbiased estimator is

| (2.1) |

Note that here in the second expression there is the indicator random variable , and for the third expression the random variable appears in the upper integration range. Thus we can name this estimator also as a random truncation estimator.

Due to the independence of and , the unbiasedness of the proposed estimator can be established straightforwardly by applying Fubini’s theorem:

In the main body of the paper, we ignore the technicality induced by possible discretization for simulating the continuous-time cost process. We consider the following three optimization problems arising from RUMC:

-

1.

minimize the variance of the estimator subject to a linear penalty on the computational cost/work;

-

2.

minimize the variance of the estimator subject to a fixed pre-specified level of computational cost/work;

-

3.

minimize the work-variance product of the estimator.

Previous work on RUMC considered three similar optimization problems with the variance replaced by asymptotic variance (Rhee and Glynn (2015)). Large (small) computational cost/work corresponds to small (large) bias. The three optimizations are natural formulations of the tradeoff between bias and variance. It turns out that solving the first optimization problem helps solving the succeeding optimization problem(s). Throughout the paper, we assume the expectations and variances of all estimators are finite and well-defined to avoid the problems of interest becoming meaningless.

2.1 Minimizing Variance with Penalty

We want to optimize over all possible distributions in order to minimize the variance of the estimator with a penalty for the computational cost:

| (2.2) |

This is inherently an infinite-dimensional optimization problem. The following lemma rewrites the optimization problem (2.2) in a form that is more amenable for analysis.

Lemma 1.

Proof.

Notice that

By Fubini’s theorem and the independence between and , we have

Since is independent of , we can drop it in the optimization, which leads to the conclusion. ∎

Following a similar procedure in the proof of Lemma 1, we have . The random truncation increases the variance by noticing , but the increased variance is compensated by a decreased computational cost. The objective of the optimization problem (2.3) is a functional of , , and . Thus, we expect the optimal randomization distribution for the optimization problem (2.3) should be determined by and . Intuitively, captures how fast the cost process decays after time , while is the unit cost for computing the cumulative cost.

Assumption 1.

is a non-negative and strictly decreasing smooth function.

The non-negativity and monotonicity in Assumption 1 can be justified if the cost process is non-negative (or non-positive) and is non-increasing in . In the case where the cost process has both positive and negative parts, we can decompose it into the difference of two non-negative processes and estimate the cumulative cost of both processes separately. Under Assumption 1, we have an explicit form for the optimal distribution given in the following theorem.

Theorem 1.

Proof.

For the optimization problem (2.3), we have

where

Notice that the function decreases for and increases for . In addition, for any , is required to decrease from to as goes from to . Then, we can calculate

Combining the arguments above leads to the conclusion. ∎

Remark 1.

It is straightforward to establish that if , then and if , then and . We can see the following insight from the explicit form of the optimal distribution : large and small correspond to small , which means the distribution of the random truncation concentrates on the domain where is small. This insight intuitively makes sense. Large unit cost for computing the cumulative cost favors a small truncation size. Small roughly indicates that the cost process decays fast after time , which thus encourages us to put more computational effort before time . If is non-monotone, the optimal can be solved by an optimal control problem, which can be found in the appendix.

In the following, we consider the exponential Lévy process, which includes geometric Brownian motion (GBM) as a special case; see e.g. Fu et al. (2017). Let be a Lévy process with the characteristic triplet , and its characteristic exponent is given by , which is uniquely characterized by the Lévy-Khintchine formula: . Then, is an exponential Lévy process. Let , where for a fixed , so .

Define

| (2.5) |

and assume that and in order for the relevant integrals to be well-defined. Then, we have

and

Corollary 1.

If is an exponential Lévy process with characteristic exponent and , then under the optimal randomization distribution , is a shifted exponential random variable with the probability density function given by

where the optimal shift is given by:

where and are given by (2.5).

Proof.

Note that for , . Otherwise, , so that

We conclude that the optimal is given by

which completes the proof by differentiation. ∎

2.2 Constrained Optimization

In this section, we consider the second optimization problem, in which we minimize the variance of the randomized estimator given that the computational budget is fixed at a level :

| (2.6) |

An explicit characterization for the optimal distribution is obtained in the following theorem by using the maximum principle of an optimal control problem.

Theorem 2.

(i) If , then

where is the unique positive solution to the following equation:

and the minimum variance is given by

(ii) If , then

| (2.7) |

and the minimum variance is given by

Proof.

Consider the following infinite horizon optimal control problem:

| (2.8) | ||||

We introduce the Hamiltonian:

where is an adjoint variable. For , the optimal control satisfies the following maximum principle, see e.g. Halkin (1974):

From the adjoint equation, we know there exists such that for . For , control on satisfies the optimal condition, but it cannot satisfy the state constraint in (2.8). Thus, we have . As in the proof of Theorem 1, the optimal condition implies

where . By the state constraint in (2.8),

we have and

From Remark 1, we know that if , then , which implies

if , then and , which implies

or equivalently,

Define

We have , and

Thus, equation has a unique solution on if and only if , or equivalently,

Summarizing the above arguments, the maximum principle and state constraint in (2.6) offer a unique on , which is the optimal control.

Remark 2.

Optimization problem (2.2) can also be viewed as an optimal control problem but without a state constraint in (2.8), which is imposed by the computational budget constraint. When the computational budget is smaller than a threshold, i.e., , we have , so that the distribution given by (2.7) is supported on . Increasing the computational budget on the range would make the tail of the distribution heavier, which indicates that the distribution of the optimal randomization shifts more weight toward the domain when is large as the computational budget increases. When the computational budget is larger than a threshold, i.e., , we have , which indicates that the truncation size would be almost surely larger than a certain threshold under the optimal randomization if the computational budget is larger than a certain threshold.

As an illustration, we then show the optimal distribution for the optimization (2.6) when is an exponential Lévy process.

Corollary 2.

If is an exponential Lévy process with characteristic exponent and , then when , the optimal distribution is given by

for any . On the other hand, when , the optimal is given by

where is given by (2.5).

Proof.

Let us recall that , and we have

Therefore, when

the optimal is given by

When , the optimal is given by

where and

which implies that

and thus

This completes the proof. ∎

2.3 Minimization of the Work Variance Product

In this section, we consider the third optimization problem, which is to minimize the product of the variance and the expected value of , i.e.,

| (2.9) |

A key observation is that this optimization problem is equivalent to first minimizing over the variance conditional on and then minimizing over all possible values of fixed levels . The main idea is that we can first conditional on the value of , and then exhaust all possible values of to search for the optimum. We have the following equivalence in the two optimization problems:

or equivalently by plugging in the corresponding expressions, i.e.,

We first establish the following lemma before proving the main result of this section.

Lemma 2.

Under Assumption 1,

Proof.

By definition, we have

noticing that . This completes the proof. ∎

Theorem 3.

Proof.

We have

where the second equality is justified by Theorem 2, and we recall that

Let

Our goal is to minimize , and we have that the optimal solution must satisfy the first-order condition:

Recall that , and thus the first-order condition is equivalent to

Denote

and we have . Noticing that , we have . Then,

where the last inequality is due to Lemma 2. In addition,

Thus, there exits a unique solution for , which minimizes . Then, we can calculate

where the second equality is justified by the definition of . This completes the proof. ∎

Remark 3.

From the proof of Theorem 2, we know is increasing with respect to . Therefore, there exists a unique such that

which is the optimal computational budget for minimizing the work-variance product. Notice that the support of the optimal distribution is always shifted away from zero for minimizing the work-variance product.

Corollary 3.

If is an exponential Lévy process with characteristic exponent and , then

where and is defined by (2.5), and is the unique positive solution to the following transcendental algebraic equation:

which can be solved in a closed form:

where is the Lambert-W function and and are defined by (2.5). Furthermore,

Proof.

In the case of exponential Lévy process, we have , then the first-order condition is equivalent to

| (2.10) |

In order to solve (2.10), we denote , then we can rewrite the algebraic equation into the following equivalent form:

| (2.11) |

and note that the right-hand side is positive due to the Lévy-Khintchine theorem and Jensen’s inequality, i.e., always holds. By the definition of the Lambert-W function, we can recognize that the solution to (2.11) is given explicitly by , and here . Then we have the desired solutions of and . Note that , and the Lambert-W function is uniquely defined, then this establishes the uniqueness of . Applying the results of Theorem 3 completes the proof. ∎

3 Randomization Vs. Fixed Truncation

As discussed in the last section, randomization inevitably increases the variance, although it eliminates the bias. Obviously, small bias and variance are desirable in practice. Basically, whether the optimal randomization is favorable or not depends on the tradeoff between bias and variance. Thus, we consider a utility function as follows:

where is an estimator of subject to the computational budget . A large indicates more weight on the variance and less weight on the bias in the tradeoff of these two factors. We denote the optimal randomized estimator with computational budget as and the fixed truncation estimator with computational budget as defined by

Then, we have the following result.

Proposition 1.

For any , when is sufficiently small,

Proof.

When is sufficiently small, the inequality is satisfied and as , and on the other hand, as , we have , which proves the conclusion. ∎

Remark 4.

The proposition indicates that as long as the variance is of concern to a practitioner, the optimal randomized estimator would not be favored if the computational budget is small enough. When is small, the distribution of must be very skewed in order to make and the estimator unbiased at the same time. Specifically, is small for , which leads to a very large variance, because appears in the denominator of the expression .

In general, we define the following threshold level:

such that for all . This threshold represents the maximum weight that a practitioner can put onto the variance such that the optimal randomized estimator is more favorable than the fixed truncation estimator. Similar to the proof in Proposition 1, it is straightforward to show that . As discussed previously,

In the case where and are positively correlated, then , which implies that is well defined and non-negative.

Proposition 2.

If is an exponential Lévy process with characteristic exponent and , then

where

and and are given by (2.5).

Proof.

Recall that

and

We have

and

In addition,

For the optimal randomized estimator, from the result in Corollary 2, we have two cases. If , then the optimal is given by

and

If , then the optimal is given by

and

Then, it is straightforward to prove the conclusion. ∎

Next we offer an explicit expression for for the Cox-Ingersoll-Ross (CIR) process, which is an affine stochastic process not belonging to the class of exponential Lévy processes. The CIR process is governed by the following SDE:

where is a standard Brownian motion. The CIR process is mean reverting to , and governs the speed of the mean reversion. According to the calculation in the appendix, we have

where

Proposition 3.

For the CIR process, we have

where

and . Here is the unique positive solution to the following equation:

The proof of Proposition 3 can be found in the Appendix.

MSE Comparison for Exponential Lévy Process

Define

The randomized estimator is unbiased, so its MSE is just its variance.

Proposition 4.

For the exponential Lévy process, for all ,

The proof of Proposition 4 can be found in the Appendix.

4 Numerical Experiments

In this section, we present numerical experiments illustrating the main theoretical results. We choose the form of the discounted cost to be with denoting the continuous discount rate. Here refers to the cost or reward at time , and we adopt the form motivated from the power utility function commonly used in decision theory and economics. As for the choice of the underlying stochastic process , we consider geometric Brownian motion (GBM) and the Cox-Ingersoll-Ross (CIR) process, which were also considered by Rhee and Glynn (2015) in their numerical experiments.

We first consider the example of discounted cost () with being the geometric Brownian motion (GBM) model, which is a special case of the exponential Lévy process. The GBM model is governed by the following SDE:

Then, we have . In addition, we can compute

and

From Corollary 3, we know that the optimal randomization distribution is a shifted exponential distribution. The survival function of the shifted exponential distribution family is given by

The variance-work product of the shifted exponential distribution family can be expressed as a function of and :

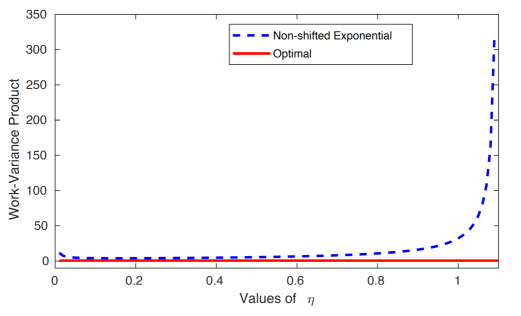

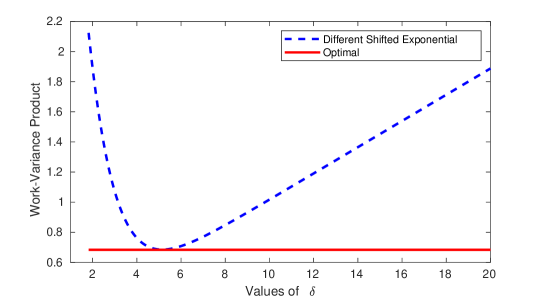

Let , which is the rate in the optimal randomization distribution. We set the parameters by , , , , . In this case, , , , and the minimum work-variance product value is .

In Figure 1, the red line is the minimum work-variance product, and the blue line is the work-variance product function of a non-shifted exponential distribution, i.e., with . We can see the variance-work product of the non-shifted exponential distribution family is strictly larger than the minimum work-variance product, which is consistent with the Theorem 3 result that the support of the optimal randomized distribution is always shifted away from zero. The work-variance product increases tremendously when grows larger than . A large would lead to a light tail for the survival function, which causes a large variance.

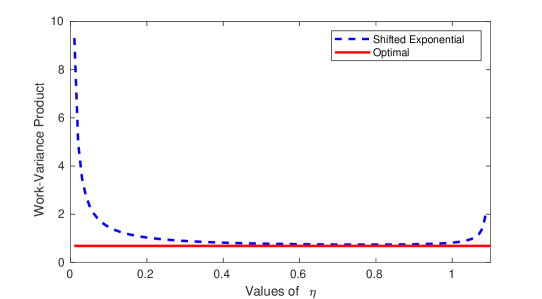

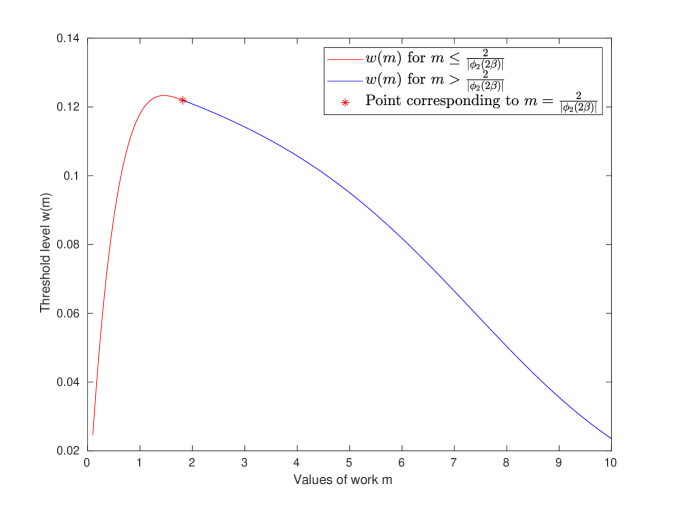

In Figure 2, the blue line in the top graph plots the work-variance product function with , while the blue line in the bottom graph is the work-variance product function with . We can see the two work-variance product functions deviate from the optimal value except at the optimal point. The right panel in Figure 2 also substantiates the uniqueness of in Theorem 3.

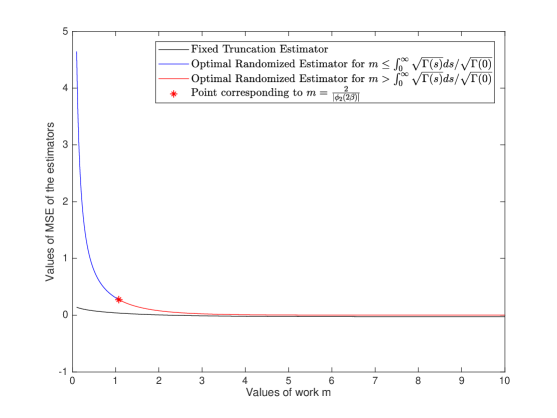

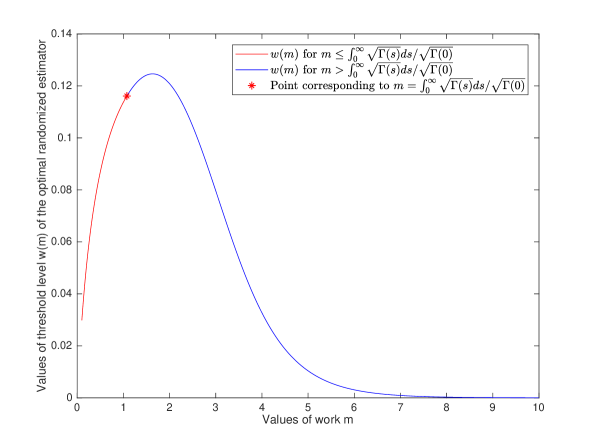

Then, we plot the threshold level given by Proposition 2 for this example. From Figure 3, we can see that even the optimal weight for all computational budget , which is the level of threshold , is less than . This indicates that the advantage of the optimal randomized estimator over the fixed truncation estimator can only be justified under the scenario where the bias is the paramount concern.

For in , this utility corresponds to the mean squared error (MSE), which is a widely used metric for the efficiency of an estimator. Figure 3 implies that the MSE of the optimal randomized estimator is always larger than the MSE of the fixed truncation estimator. Moreover, we prove in the Appendix that this conclusion holds for all exponential Lévy processes. The numerical results for the CIR process can be found in the appendix, which are similar to those for the exponential Lévy process.

5 Conclusion

In this paper, we propose a randomized unbiased estimator for simulating an expected cumulative cost/reward. We derive an explicit form for the optimal distribution of an unbiased randomized estimator balancing the trade-off between variance and computational cost. The optimal distributions are in a shifted distribution class. To the best of the authors’ knowledge, this is the first work resulting in explicit forms for the optimal randomization distribution. For a discounted continuous cumulative cost contingent on an exponential Lévy process, the optimal randomization distributions are shifted exponential distributions. The explicit structure of the distribution function of the optimal random truncation level is particularly useful for “post-estimation” analysis, and allows us to carry out a full diagnosis of the bias-variance tradeoff. Moreover, we justify the advantage of the optimal randomized estimator via a utility function taking both bias and variance into consideration. Our results are limited to simulating expected cumulative cost/reward. Future research lies in deriving the optimal randomized distribution and threshold level in the utility function for more general RUMC problems. Optimal control theory offers a new perspective to address such RUMC problems.

Acknowledgments.

We are grateful to the editor and two anonymous referees for their careful reading of the paper and very helpful suggestions. This work was supported in part by the National Science Foundation (NSF) under Grants CMMI-1362303, CMMI-1434419, and DMS-1613164, by the National Science Foundation of China (NSFC) under Grants 71901003, 71720107003, 91846301, 71790615, 71690232, and by the Air Force of Scientific Research (AFOSR) under Grant FA9550-15-10050.

References

- Alexopoulos et al. (2016) Alexopoulos, C., Goldsman, D., Tang, P., Wilson, J.R., 2016. SPSTS: A sequential procedure for estimating the steady-state mean using standardized time series. IIE Transactions 48, 864–880.

- Blanchet et al. (2015) Blanchet, J.H., Chen, N., Glynn, P.W., 2015. Unbiased Monte Carlo computation of smooth functions of expectations via taylor expansions, in: Proceedings of the Winter Simulation Conference, IEEE. pp. 360–367.

- Blanchet and Sigman (2011) Blanchet, J.H., Sigman, K., 2011. On exact sampling of stochastic perpetuities. Journal of Applied Probability 48, 165–182.

- Bryson and Ho (1975) Bryson, A.E., Ho, Y.C., 1975. Applied Optimal Control: Optimization, Estimation and Control. CRC Press.

- Cui et al. (2019) Cui, Z., Lee, C., Zhu, L., Zhu, Y., 2019. On the optimal design of the randomized unbiased Monte Carlo estimators. Available at SSRN 3362534 .

- Fox and Glynn (1989) Fox, B.L., Glynn, P.W., 1989. Simulating discounted costs. Management Science 35, 1297–1315.

- Fu et al. (2017) Fu, M.C., Li, B., Li, G., Wu, R., 2017. Option pricing for a jump-diffusion model with general discrete jump-size distributions. Management Science 63, 3961–3977.

- Giles (2008) Giles, M., 2008. Multilevel Monte Carlo path simulation. Operations Research 56, 607–617.

- Giles (2015) Giles, M., 2015. Multilevel Monte Carlo methods. Acta Numerica 24, 259–328.

- Glasserman and Staum (2003) Glasserman, P., Staum, J., 2003. Resource allocation among simulation time steps. Operations Research 51, 908–921.

- Glynn (1983) Glynn, P.W., 1983. Randomized Estimators for Time Integrals. Technical Report. Mathematics Research Center, University of Wisconsin, Madison.

- Glynn and Rhee (2014) Glynn, P.W., Rhee, C.H., 2014. Exact estimation for Markov chain equilibrium expectations. Journal of Applied Probability 51, 377–389.

- Glynn and Whitt (1992) Glynn, P.W., Whitt, W., 1992. The asymptotic efficiency of simulation estimators. Operations Research 40, 505–520.

- Halkin (1974) Halkin, H., 1974. Necessary conditions for optimal control problems with infinite horizons. Econometrica , 267–272.

- Jacob et al. (2015) Jacob, P.E., Thiery, A.H., et al., 2015. On nonnegative unbiased estimators. The Annals of Statistics 43, 769–784.

- Kahale (2019) Kahale, N., 2019. Optimal unbiased estimators via convex hulls. arXiv preprint:1909.02876 .

- Lyne et al. (2015) Lyne, A.M., Girolami, M., Atchade, Y., Strathmann, H., Simpson, D., et al., 2015. On Russian roulette estimates for Bayesian inference with doubly-intractable likelihoods. Statistical Science 30, 443–467.

- McLeish (2011) McLeish, D., 2011. A general method for debiasing a Monte Carlo estimator. Monte Carlo Methods and Applications 17, 301–315.

- Merton (1969) Merton, R., 1969. Lifetime portfolio selection under uncertainty: The continuous-time case. Review of Economics and Statistics , 247–257.

- Rhee and Glynn (2015) Rhee, C.h., Glynn, P.W., 2015. Unbiased estimation with square root convergence for SDE models. Operations Research 63, 1026–1043.

- Vihola (2018) Vihola, M., 2018. Unbiased estimators and multilevel Monte Carlo. Operations Research 66, 448–462.

- Whitt (2002) Whitt, W., 2002. Stochastic-Process Limits: An Introduction to Stochastic-Process Limits and their Application to Queues. Springer Science & Business Media.

- Zheng and Glynn (2017) Zheng, Z., Glynn, P.W., 2017. A CLT for infinitely stratified estimators, with applications to debiased MLMC. ESAIM: Proceedings and Surveys 59, 104–114.

Appendix

Optimal Randomization for Non-Monotone

Let . Then, finding the optimal distribution can be viewed as finding the state corresponding to the following optimal control problem:

Notice that the constraint makes sure the state is non-increasing. The maximum principle gives a necessary condition of the optimal control:

where

The necessary and sufficient condition for the optimal control can be given by the following Hamilton-Jacobi-Bellman (HJB) partial differential equation:

subject to the terminal condition .

Proof of Proposition 4

Proof.

If , we have

Note that we can expand the term

Plugging in this expression into the above, we can further simplify the above expression to

Then we group the above terms by those related to and those related to , and we have

From the Lévy-Khintchine formula and Jensen’s inequality, it is easy to establish that always holds. Thus we have

or equivalently we have

Using this fact, we have

| (5.1) |

We further divide the discussion into two cases:

Above all, we have proved that we always have .

If , we have

Note that we can expand the term

Plugging in this expression into the above, we can further simplify the above expression to

where in the second last inequality, we have utilized the assumption that , and in the last inequality we have used the fact that .

Then we group the above terms by those related to and those related to :

From the Lévy-Khintchine formula and the Jensen inequality, it is easy to establish that always holds. Thus we have

Thus we have

| (5.2) |

Derivations for the CIR process

We can compute that

We have the following expression for its cross moment for

Define the process , then we have

For , we have

| (5.3) |

Here we have to determine the sufficient conditions to be imposed onto the parameters in order to have the Assumption 1 to be satisfied. A sufficient condition is given by

which is equivalent to requiring

Then we calculate the ingredients for the determination of the optimal randomization distribution. For example, in the case of solving the optimization problem (2.2), from the result in Theorem 1, we have

where .

In the case of solving the constrained optimization when we are given the expected computational work , from the characterization in Theorem 2, we have

where

For the minimization of the variance-work product, from Theorem 3, we have

where is the unique positive solution to the following equation:

| (5.4) |

We can simplify the equation (5.4) as

To calculate the optimal work-variance product, recall that the optimal level of is given by

Then the optimal work-variance product in the case of the CIR process is given by

Note that in the second equality above we have utilized the defining equation characterizing .

Proof of Proposition 3

Proof.

We have the following calculations:

and

| (5.5) |

For the first term of the right hand side of (5.5), we have

The second term on the right hand side of (5.5) can be calculated as

For the optimal randomized distribution, we have

We divide the discussion into two cases:

(i) If , then we have

where we have utilized the characterization equation of in the part (i) of the (modified) Theorem 2 for the constrained optimization.

(ii) If , then we have

Then it is straightforward to prove the conclusion. ∎

Numerical Results for CIR Process

We consider a CIR process, and use the following parameter sets: , , , , . In Figure 4, the MSE of the optimal randomized estimator is larger than the MSE of the fixed truncation estimator. In Figure 5, the threshold function is plotted, and we can see that the threshold function first increases and then decreases with the optimal value less than .