Moment Inequalities in the Context of Simulated and Predicted Variables

Abstract

This paper explores the effects of simulated moments on the performance of inference methods based on moment inequalities. Commonly used confidence sets for parameters are level sets of criterion functions whose boundary points may depend on sample moments in an irregular manner. Due to this feature, simulation errors can affect the performance of inference in non-standard ways. In particular, a (first-order) bias due to the simulation errors may remain in the estimated boundary of the confidence set. We demonstrate, through Monte Carlo experiments, that simulation errors can significantly reduce the coverage probabilities of confidence sets in small samples. The size distortion is particularly severe when the number of inequality restrictions is large. These results highlight the danger of ignoring the sampling variations due to the simulation errors in moment inequality models. Similar issues arise when using predicted variables in moment inequalities models. We propose a method for properly correcting for these variations based on regularizing the intersection of moments in parameter space, and we show that our proposed method performs well theoretically and in practice.

Keywords: Simulated moments, Moment inequalities, Smoothable convex functions

1 Introduction

Recently, estimating with moment inequalities rather than traditional equalities has proven increasingly popular (Tamer, 2010). Even in contexts when a model is difficult or even impossible to compute exactly, economic theory may provide inequalities that are amenable to estimation. Thus, many of the examples in which moment inequalities are attractive are also examples in which computing the model is complex. This model complexity also leads the author to use simulation techniques, often to address the calculation of integrals over complex objects. However, the role of simulation in moment inequality estimation has been largely unexplored.

In this paper, we argue that using simulation or predicted values in the context of moment inequalities has important implications both for determining identified sets and for inference. We show that simulated moment inequality estimators suffer from small sample bias, which is a result of the irregular nature of the estimator. This irregularity is introduced by the following mechanism. Rather than finding optimal parameters through some kind of extremum estimator, moment inequality estimators typically build the estimated identified set or confidence region through level set computations, such as in Chernozhukov et al. (2007) and Andrews & Barwick (2012). The level set is defined by the intersection of moments, and at these intersections, the objective function may depend on the underlying moments in an irregular way. That is, at such intersections, the distribution of the objective function can be particularly sensitive to perturbations to the underlying moments. Since these intersections often define the maximum or minimum of the confidence interval in a particular direction, they determine the range of parameters in the confidence interval, and thus the intersections are often of greatest interest. Whereas approximation error (for instance, due to simulation) in moment equality estimators for small samples is of second order importance, we show that irregular objective functions promote approximation error in small samples to first order importance.

In this paper, we first describe formally the phenomena that we are interested in. A starting place is the well-known result for moment equalities that estimation that requires simulation is consistent, even for a fixed number of draws (McFadden, 1989; Pakes & Pollard, 1989). Moment inequality estimators are similar to moment equalities because they take means over simulated or predicted variables before transforming them into an objective function. Simulated moment functions are consistent (and asymptotically unbiased) for their population counterparts for a finite number of draws. This ensures that level-set estimators of identified sets (Chernozhukov et al., 2007) are also consistent in the Hausdorff distance.

We show that the similarity breaks down when it comes to inference in finite samples, due to the irregular feature of the objective function. We explore this phenomenon in two Monte Carlo experiments. The first one focuses on estimation of the point of intersection of multiple simulated moment inequalities, and is meant to maximize the scope of the problem we discuss. The second is a more realistic treatment: We study an entry game in the spirit of Ciliberto & Tamer (2009). Moment inequalities are generated by the lower and upper bounds of entry probabilities conditional on covariates that are classified into a finite number of bins. In our Monte Carlo experiments, we find that the coverage probabilities of the confidence regions are distorted severely when there are bins with a limited number of observations and a small number of simulation draws is used. The presence of such bins is common in empirical applications. Therefore, inference methods that properly account for the effects of simulation are needed.

We propose a new solution to the problems associated with the irregularity of the objective function, including those due to simulated moments. The key is that the commonly used objective functions involve smoothable convex functions (Beck & Teboulle, 2012). Our method “regularizes” or smoothes the objective function, and we show that this method leads to a straightforward bias correction method. While the idea of regularization appears in some other contexts, such as Haile & Tamer (2003), Chernozhukov et al. (2015) and Masten & Poirier (2017), we formally show that this approach has uniform validity in the context of inference with simulated variables. Our regularization method is based on the class of -smooth approximations studied in the non-smooth optimization literature (Nesterov, 2005; Beck & Teboulle, 2012). We provide conditions on the choice of approximating functions and regularization parameters that ensure the uniform validity of an inference procedure that combines the proposed regularization scheme with a straightforward bootstrap resampling. In addition to being attractive theoretically, we show that this approach performs well in practice, even relative to techniques that implement bias correction via the adjustment of the critical value such as Andrews & Soares (2010) and Chernozhukov et al. (2013). Specifically, our Monte Carlo experiments show that the proposed method controls the size well and is often less conservative than the existing methods.

Before moving on, we want to stress that simulation is common in many well-known applications of moment inequalities. For instance, Haile & Tamer (2003) simulate bids in order to place bounds on the value of participants in an auction. Ciliberto & Tamer (2009) simulate an entry game to determine upper and lower bounds for the probability of a firm entering under different equilibrium selection mechanisms. Ho (2009) uses inequalities to study network formation between hospitals and insurers, and uses predicted profit from a network as an explanatory variable for the firm’s choices. The profit function is based on a random coefficient logit demand function as in Berry et al. (1995), which involves simulation. Eizenberg (2013) studies firms choosing product characteristics, and also relies on simulated demand predictions drawn from a Berry et al. (1995) demand system. Kawai & Watanabe (2013) simulates market effects in a model of strategic voting that uses moment inequalities to address unobserved beliefs about other voters. Although not strictly moment inequalities, the method of Bajari et al. (2007) uses simulation in the context of a minimum distance estimator based on inequalities to study dynamic oligopoly games. Well-known applications are Ryan (2012) and Fowlie et al. (2015).

While our paper focuses on simulation as a source of small-sample bias, the same problem is introduced by using predicted values from some prior estimation stage. For example, Holmes (2011) studies the diffusion of Walmart using moment inequalities, and Houde et al. (2017) take a similar approach to study the locations of Amazon’s fulfillment centers. Both papers use profits or revenues as explanatory variables in their moment inequalities, where revenues and profits are constructed from estimated models. Although neither of these papers use simulation in any stage of their estimation, the fact that there is estimation error associated with these variables brings up similar issues to the approximation error introduced by simulation.

Our paper follows in a long line of research on problems with using simulation and prediction in estimation procedures. For instance, Hausman (1983) terms using predicted or simulated values in non-linear estimation procedures the “Forbidden Regression,” and Gourieroux & Montfort (1996) shows that simulated Maximum Likelihood is inconsistent for any fixed number of samples due to the non-linearity of maximum likelihood estimator. Our result is in fact not due to non-linearity, as moment inequality estimators are not inherently non-linear. Indeed, we show consistency even for a fixed number of samples. Rather, our result emphasizes the irregularity of the level set estimator in a moment inequalities context, which makes the confidence interval irregular at important points. Interestingly, Bajari et al. (2007) show in Table 5 that their inequalities estimator may be inferior to an estimator based on moment equalities (as in Pakes et al., 2007) if one can be implemented. They ascribe this to the non-linearity of the second-stage estimator.111For example, on page 1362, Bajari et al. (2007) write: “The results above suggest that the inequality estimator may exhibit bias in small samples. This bias arises because the second-stage objective function is nonlinear in the first-stage estimates.” Our paper provides an alternative explanation, which is the irregularity of the level-set estimator in the context of first-stage simulation.

2 Setup

2.1 Simulated moments and motivating examples

Let be a random vector, be a structural parameter and be a function known up to the parameter. Consider the (unconditional) moment inequality restrictions:

| (1) |

We call the set of parameter values satisfying these restrictions an identified set and denote it by . In models where is difficult to evaluate analytically, simulation methods are often employed to obtain its approximation. Throughout, we consider the setting where can be written

| (2) |

for some known function and a conditional distribution , which may also depend on the parameter. This allows one to draw simulated samples from the conditional distribution and approximate by a simulation counterpart . We use the subscript to denote statistics constructed from simulated samples. This setting parallels the classical method of simulated moments (MSM) (McFadden, 1989; Pakes & Pollard, 1989) except that the moment conditions in (1) involve inequality restrictions.

For making inference for the structural parameter or its identified set (the set of s satisfying (1)), level-sets of criterion functions are commonly used (Chernozhukov et al., 2007; Andrews & Soares, 2010). Following the literature, we consider set estimators and confidence regions of the form:

| (3) |

where is a test statistic (properly scaled sample criterion function), and is a possibly data-dependent critical value. The variable is the number of observations in our sample, and the subscript n denotes statistics constructed from that sample. Throughout, we consider criterion functions that can be written as

| (4) |

for some index function , which aggregates the vector of sample moments normalized by an estimator of the asymptotic covariance matrix. Examples include and

A key observation is that the level sets commonly used in the literature may depend on the underlying moments and hence simulation errors in an irregular manner. We illustrate this point using simplifications of well-known examples in the literature.

Example 1 (Intersection bounds).

Let be a scalar parameter, let be random variables, and let moment inequalities be given by

| (5) | |||

| (6) |

where follows a known distribution . That is, the upper bound for is the minimum of two expectations of draws from separate Bernoulli distributions. While these moment restrictions may appear overly simple, they capture some of the common features shared by empirical examples. These include (i) key parameters are restricted through an intersection of multiple bounds; and (ii) simple frequency simulators can be used to approximate individuals’ or firms’ choice probabilities represented by the expectation of the indicator functions.

For each , let . Taking , one may then construct a confidence interval for with level as follows:

| (7) |

where is a suitable critical value.222For example a critical value based on the least favorable configuration where the two constraints bind, i.e. solves where is the distributional limit of . A refined critical value based on moment selections can also be used. The simulated variables are drawn from for each . As shown in (7), the right end point of the confidence interval is given by the minimum of the sample moments (shifted by the critical value).

The next example is an entry game based on Bresnahan & Reiss (1991); Berry (1992); Tamer (2003); Ciliberto & Tamer (2009).

Example 2 (Entry game).

Consider a binary-response static game of complete information with two players. For each player let , , and denote s binary action, observed and unobserved characteristics respectively. For each let denote a parameter vector. The players’ payoffs are summarized as follows.

|

|

Suppose that any outcome observed by the econometrician is a pure strategy Nash equilibrium and that the opponent’s entry negatively affects a player’s payoff, i.e. for . Then, without further assumptions, the model restricts the conditional probabilities of outcomes as follows:

| (8) | ||||

| (9) | ||||

| (10) | ||||

| (11) | ||||

where follows a conditional distribution specified by the researcher, e.g. mean zero bivariate normal with correlation . The inequality restrictions (10)-(11) arise because the model predicts multiple equilibria for some values of exogenous variables, while an equilibrium selection mechanism is left unspecified (Tamer, 2003). Suppose for simplicity that has a finite support, and its distribution is known. The right hand side of (8)-(11) can be approximated by simulators. For example, the probability can be approximated by its analog , where for each , a sample of simulated payoff shifters are drawn from the conditional distribution . It is straightforward to rewrite the restrictions in (10)-(11) as unconditional moment inequalities as in (1) for a suitable moment function with .

Whereas Ciliberto & Tamer (2009) places inequalities on the probability of equilibrium outcomes, our next example follows the approach of Pakes et al. (2011) to generate inequalities directly from agent utility functions and revealed preference. This approach has been utilized to study strategic environments such as product introductions (Eizenberg, 2013) and network formation (Ho, 2009). In both of these binary choice examples, the researchers estimate variable profits in a pre-stage and use the moment inequalities to estimate the fixed cost associated with a positive choice.333Similar examples are Nosko (2014), Wollmann (2014), Crawford & Yurukoglu (2012), and Gowrisankaran et al. (2014). To the extent that variable profits are estimated with some error, this approach introduces analogous problems to the ones we highlight in the context of simulation. The problem is particularly clear if the variable profits are based on simulation estimators. That is the case for Eizenberg (2013) and Ho (2009), which utilize a simulated demand system (i.e. Berry et al., 1995) in the pre-stage. We provide an example here, based on Eizenberg (2013):

Example 3 (Product introductions).

Consider a binary-response static game of complete information with two players. For each player , let denote player ’s action, let denote the profits to from the choice of , conditional on the choice of the other firm . Let be the fixed cost associated with , so the payoff to adoption is . Let , where is observed by the firm and not the researcher, and . The firms play a Nash Equilibrium. We take as observed and our goal is to estimate .

If firm chooses , revealed preference implies that . And similarly, observing implies . We further impose finite bounds on , denoted and , so we have upper and lower bounds for that we apply to every observation in the data. Note that it is common to interact moment inequalities with instrument matrices, and functions of these instruments, to obtain more moments. We do not explore that here. Thus, we have the following moment inequalities for :

If , and are observed, it is straightforward to construct the sample analog of these inequalities. However, in practice, these are rarely observed, especially profits for . Eizenberg (2013) estimates a structural demand system and pricing game in a pre-stage in order to construct and how it varies with . Central to the paper is the use of simulation to construct and . Thus, all of the explanatory variables are approximations and are subject to prediction and simulation error.

We start with an observation that, similar to moment equalities, level-set estimators that use simulation are consistent even for a fixed number of draws. This similarity arises because estimators of the moments take means over simulated variables before transforming them into an objective function and level-set estimators depend on the estimated moments in a continuous way. For each , let and let . Then, it holds under mild regularity conditions (Assumption A.1 in Appendix A) that

uniformly in as for any fixed .444Moreover, under the assumption of Proposition 2.1, the estimated moments are asymptotically unbiased in the sense that the empirical process converge weakly to a Gaussian process with zero mean.

We state the Hausdorff consistency of level-set estimators as a proposition under a set of assumptions similar to those in Chernozhukov et al. (2007). For this, let denote the Hausdorff distance between two sets .

Proposition 2.1.

While simulation based level-set estimators are consistent, the similarity to moment equalities breaks down when it comes to inference. In models characterized by moment equalities, finite simulation draws affect a confidence region primarily through the asymptotic variance of a point estimator. However, with moment inequalities, this is no longer the case. A noteworthy feature of the level sets based on moment inequalities is that its boundary may depend on the sample moments in a non-standard manner. To see this, in Example 1, write the boundary of the level set as

| (12) |

where, for each , . Note that is a nonlinear function that is not differentiable at points such that . While this function is still directionally differentiable, the (directional) derivative of at can be shown to depend on the underlying data generating process in a discontinuous manner. This has important consequences on inference. Namely, even if the simulators for the moments are consistent (with a fixed simulation size), they may introduce finite sample biases to the boundary of the level-set, which in turn may affect the performance of inference in non-trivial ways. Below, we show numerically that this can sometimes result in severe size distortions in empirically relevant settings.

The non-standard nature of inference in moment inequality models and its finite-sample properties have been extensively studied in the recent literature (Andrews & Guggenberger, 2009; Andrews & Soares, 2010; Hirano & Porter, 2012; Chernozhukov et al., 2013; Fang & Santos, 2014). However, to our knowledge, its consequence in relation to simulation-based inference has not been explored. One of our goals here is to quantify the effects of simulation in the context of moment inequalities and provide a practical guidance for empirical studies.

2.2 The effects of simulated variables

We start with a simple numerical experiment. Slightly generalizing Example 1, consider moment inequality restrictions on a scalar parameter :

| (13) |

The goal of the experiment is to compare the performance of two types of confidence intervals for : one that computes the moment above analytically and the other that approximates the moment by simulation. Let be generated as an i.i.d. random vector following a -dimensional standard normal distribution. For each and , let be generated as a -dimensional standard normal vector independent of . For the simulation-based confidence region, we draw, for each , a random sample of size .

For each define

| (14) | ||||

| (15) |

where is the cumulative distribution function of a standard normal distribution. The first confidence region computes the moments analytically, while the second confidence region computes them using simulation. To investigate the effect of simulation on the test statistic only, we use a common critical value for both confidence intervals. This critical value is calculated as the quantile of the maximum of independent normal random variables with mean and variance , which corresponds to the limiting distribution of under the least favorable configuration (i.e. for all ). Note that this critical value does not account for the fact that a finite number of draws is used in (15).

Below, we report the probabilities of the confidence intervals covering the upper bound of the identified set.555 For the one-sided confidence intervals in (14)-(15), covering the upper bound of the identified set is the least favorable event for covering the identified set or covering each point in the identified set. Table 1 shows the coverage probabilities of the confidence intervals for a nominal level of . We report simulation results based on sample size , the number of simulation draws , and the number of moment inequalities . For each setting, we generate Monte Carlo replications. Here, the experiments are designed to investigate the performance of the confidence intervals when relatively small numbers of draws are used. However, note that the number of simulation draws in this range is used in practice (see e.g Ciliberto & Tamer, 2009).

| Analytical | Simulated | ||||

| Panel A: () | |||||

| 0.948 | 0.734 | 0.904 | 0.919 | 0.933 | |

| 0.954 | 0.733 | 0.916 | 0.916 | 0.945 | |

| 0.949 | 0.738 | 0.906 | 0.925 | 0.933 | |

| Panel B: () | |||||

| 0.940 | 0.583 | 0.882 | 0.908 | 0.930 | |

| 0.952 | 0.604 | 0.881 | 0.920 | 0.935 | |

| 0.948 | 0.666 | 0.894 | 0.913 | 0.933 | |

| Panel C: () | |||||

| 0.931 | 0.481 | 0.853 | 0.904 | 0.920 | |

| 0.939 | 0.467 | 0.868 | 0.908 | 0.925 | |

| 0.937 | 0.487 | 0.853 | 0.896 | 0.919 | |

| Panel D: () | |||||

| 0.939 | 0.245 | 0.811 | 0.888 | 0.923 | |

| 0.935 | 0.266 | 0.803 | 0.878 | 0.917 | |

| 0.946 | 0.235 | 0.810 | 0.881 | 0.912 | |

The coverage probabilities of the confidence intervals depend on the number of simulation draws and the number of inequalities in non-trivial ways. For any and , reducing the number of draws lowers the coverage probability below the nominal level, resulting in a size distortion. This distortion is particularly severe when the number of inequality restrictions is large. For example, consider the case with inequalities. This setting is relevant for empirical examples that involve moderate to many inequalities. In this case, even for , the simulation based confidence intervals have coverage probabilities significantly below the nominal level: 0.235 (=1), 0.810 (=5), 0.881 (=10), and 0.912 (=20) respectively. The size distortion is particularly severe when only one simulation draw is used for each . The size distortions are not as severe as this case when the number of inequalities is relatively low (e.g. =2 and 5). However, the coverage probabilities are still below the nominal level in all cases.666We note that the analytical confidence interval is also undersized when is large. This is due to the fact that the critical value is also calculated by a simulation based approximation. However, the magnitude of the distortion is limited (at most 2%).

This experiment shows that simulation errors can have nontrivial impacts on the finite sample performance of the confidence intervals. In particular, size distortions can be severe in models with moderate to many moment inequalities. Heuristically, the size distortion arises because the boundary of the confidence interval is an irregular transformation of the underlying moment functions. When the analytical moment is replaced with the simulation counterpart , an approximation error (of order ) remains. To see the effect of this, write the right end point of as

| (16) |

where . Taking the minimum introduces a downward bias to the estimated boundary. In other words, the right end point of the confidence interval gets pushed inward, reducing the coverage probability. This bias tends to be more severe when there are many binding moment inequalities with non-negligible approximation errors. The naive critical value does not take this into account. In finite samples, where the variation of is not negligible, ignoring the effect of the simulation error may therefore result in misleading inference.

Predicted variables

Predicted variables have similar effects on inference. Slightly modifying Example 1, consider the restrictions

where is an unknown function, which can be estimated separately. As discussed earlier, it is common in empirical practice to estimate some functions (such as the profit function in Example 3) before conducting inference based on the moment inequalities. Let denote the number of observations used to estimate in the first stage and let be the first-stage estimator of . If is known up to a finite-dimensional parameter , it can be estimated by a parametric first-stage estimator . It can also be estimated nonparametrically or with simulation. Replacing with its prediction introduces an approximation error , which often satisfies for some .777The rate depends on the estimator and assumptions imposed on . For parametric problems, it is common to have , while is common for nonparametric problems. Therefore, ignoring the variation of the first-stage error can have a consequence similar to the one discussed above.

The magnitude of the first-stage error is of order , which must be evaluated in context. For instance, the total number of observations in the first stage may be large, but if the first stage uses location fixed effects, the relevant is the number of observations in each location, which may be quite small in some cases. Note that in recognition that first-stage estimation error may be an issues, Holmes (2011) and Houde et al. (2017) implement a procedure similar to the first procedure we discuss (in Section 3.1).

Comparison to MSM

We note that the irregularity mentioned above does not arise in classical moment equality models. For comparison purposes, we briefly discuss this point. Suppose that is the unique solution to the moment equality restrictions:

| (17) |

for . A method of simulated moments (MSM) estimator is defined as

| (18) |

where . Confidence regions can be constructed around . Under regularity conditions that ensure asymptotic normality, the MSM estimator depends on the sample moments in a regular manner.

Let and . It is well-known that, under regularity conditions, the MSM estimator is asymptotically linear in the sense that

| (19) |

where the influence function has zero mean and measures the (first-order) effect of each observation on the variation of the estimator and hence determines the asymptotic variance of (see e.g Newey & McFadden, 1994; Gourieroux & Montfort, 1996). In sum, the first-order effect of simulation enters only the asymptotic variance of the estimator.

To see the effect of simulation on confidence intervals, consider a slight modification of Example 1 where solves

| (20) |

It is straightforward to show that an MSM estimator with equal weights on the moment conditions is given by . A one-sided confidence interval on can be constructed as

| (21) |

where is the quantile of the asymptotic (normal) distribution of the MSM estimator. The form of the confidence interval shows that (i) the boundary of the confidence interval depends on the sample moments in a smooth manner; and hence (ii) simulation errors in the MSM estimator affects , but it can easily be accounted for by adjusting That is, the increased variance of the MSM estimator can be accommodated using a suitable estimator of the asymptotic variance that accounts for being finite. For moment inequalities, however, it turns out that this type of variance correction is not enough. As we show in Section 3, one also needs to account for a potential bias in the estimated boundary.

The effects of simulation and a common empirical feature

Before proceeding further, we illustrate a common feature of empirical examples that can potentially cause serious size distortions if simulation is used naively. The distortion can be particularly severe when the number of draws is small. To highlight this, we design a data generating process based on the entry game in Example 2.

Let collect the observable characteristics of the two firms. We let be generated as a discrete random vector supported on a finite set . Table 2 gives the distribution and support of . In empirical studies, it is a common practice to classify continuous state variables into a finite number of bins. When such discretization is used, some bins may contain a limited number of observations. The distribution in Table 2 emulates this feature by assigning low probabilities to some bins.

Note: and are independent.

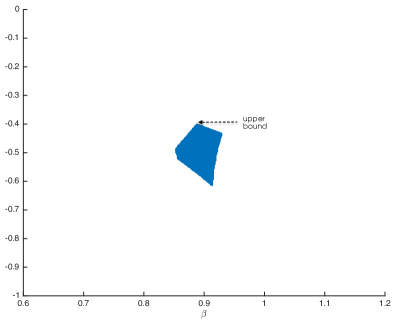

We generate unobservable characteristics as a bivariate standard normal vector independent of . For simplicity, we assume symmetry between the firms and set . For some values of , the model predicts both and as multiple equilibria. If this is the case, we select the equilibrium with probability (independent of ). The knowledge on the selection mechanism is not used for inference, and hence the agnosticism about the equilibrium selection rule leads to partial identification of parameters. Figure 1 shows the identified set for based only on the moment inequalities (10)-(11).888To focus on the non-standard effects through the moment inequalities, we drop the moment equality restrictions in this exercise. Due to the presence of covariates with 15 support points, there are a total of unconditional moment inequalities. In what follows, we report coverage probabilities on one of the extreme points of , which gives the upper bound on the competitive effect parameter .

Using the specification above and instrument functions , we transform the conditional moment inequalities in (10)-(11) into the following unconditional moment inequalities:

| (22) | ||||

where the entry probabilities

| (23) | ||||

| (24) |

are calculated using either an analytical expression or a frequency simulator. For example, using the parametric specification, may be computed analytically as . Alternatively, using a simulator one may compute the same object as , where are drawn from the bivariate standard normal distribution.

Our benchmark inference procedure is implemented as follows. The confidence region takes the form: , where is the statistic proposed by Rosen (2008) and further refined by Andrews & Barwick (2012):

where is a suitable estimator of the asymptotic variance of the moments. The critical value is computed using a bootstrap procedure combined with the generalized moment selection (GMS) procedure (Andrews & Soares, 2010; Andrews & Barwick, 2012).999We use , where and . We set for the GMS parameter. For details on the GMS procedure, we refer to the references above, but we briefly describe its mechanism to highlight the potential effects of simulation on this procedure. The key idea of the GMS is to compute the critical value by selecting the moments that are relevant to the asymptotic null distribution of the test. For example, in an implementation of the GMS, the -th moment inequality is “selected” and used to calculate if the studentized moment is smaller than a tuning parameter , i.e. , where is the -th diagonal element of . The critical value is then computed as the quantile of the bootstrapped statistic where the sample moments are replaced with the bootstrap analog of the selected moments. We note here that the simulated moments could also potentially affect the GMS step, but its consequence is not immediately clear.

| Analytical | Simulated | ||||

|---|---|---|---|---|---|

| Panel A: () | |||||

| Coverage prob | |||||

| of times differ in selection | |||||

| Panel B: () | |||||

| Coverage prob | |||||

| of times differ in selection | |||||

| Panel C: () | |||||

| Coverage prob | |||||

| of times differ in selection | |||||

| Panel D: () | |||||

| Coverage prob | |||||

| of times differ in selection | |||||

Table 3 reports simulation results based on sample size and the number of simulation draws . We simulate datasets for each setting. The coverage probabilities of the confidence regions with nominal level are evaluated for the true upper bound .

The main finding is that, for small sample size and simulation size, the coverage probabilities of the confidence region are distorted in a significant way. In particular, with , the coverage probabilities of the simulation-based confidence regions vary from 39.1% to 45.3%, significantly below the nominal level. Even for a moderate sample size, these confidence regions exhibit size distortions when the number of draws is small. For example, for , the coverage probabilities of the simulated-based confidence region is 75.6% when only a single draw is used. However, this gets improved (to 93.5%) with draws. Table 3 suggests that, with , the coverage probabilities of simulation based confidence regions are close to those of of the analytical ones in relatively large samples ().

This experiment suggests that the test statistic may not be able to benefit from averaging of the simulation errors when the number of observations in each bin is small. Combined with the irregular nature of the test statistic, this can result in a severe size distortion. The presence of bins with small numbers of observations is common in empirical settings. In such cases, care must be taken.101010We conjecture that the same comment applies to conditional moment inequality models if the essential sample size is small (i.e. small and bandwidth ). One possibility may be to increase the number of simulation draws for such bins. However, the choice of the number of draws becomes an arbitrary component of inference. Another possibility is to modify the procedure to explicitly account for the effects of the simulation. In the next section, we explore several possibilities along this line.

As a final remark, we note that the simulation not only affects the value of the test statistic but also the general moment selection procedure. Table 3 reports the number of times (out of 1000) the set of the selected moments differ between the simulated and analytical methods. This difference arises because the simulation adds perturbation to the studentized moment. With a limited number of draws, this effect on the GMS may not be negligible. As a result, some of the “selected” inequalities (i.e. ) according to the GMS based on the analytical moment may be discarded (i.e. ) under the GMS based on the simulated moment, and vice versa.

3 Inference methods with corrections for simulation errors

We consider two methods to account for the simulation errors. One is to correct the critical value. The other is to correct or “regularize” the test statistic. The former method closely follows the recent development on the moment inequality literature, and hence we keep its discussion minimal. The second method is a novel approach and has several attractive features for simulation based methods. It combines a simple bias correction method with a bootstrap critical value based on a regular (and differentiable) functional of a random vector that is asymptotically normal. To our knowledge, the uniform validity of such a method in the context of simulation-based inference is new to the literature.

3.1 Critical value correction methods

Commonly used inference methods provide approximations to the distribution of the test statistic in (26). Many of these methods are based on resampling techniques. As we saw in the previous section, ignoring the variation due to simulation can result in poor inference. Recall that, in the numerical experiment in Section 2.2, the size distortion occurred because the naive critical value did not take into account the bias that was due to the extra variation from the approximation error (in (16)). A straightforward way to correct this effect is to adjust the critical value. One can achieve this by a bootstrap critical value that resamples the simulated variables along with the original sample across bootstrap replications. Specifically, let be a bootstrap sample drawn with replacement from the empirical distribution. For each , let be drawn from .

We then let be the simulation approximation to the (conditional) moment function in the -th bootstrap sample. Define

| (25) |

This resampled moment is constructed so that it mimics the behavior of including the variation due to the simulated variables. The final step is to use the resampled moment above when one applies an existing method for computing the critical value.111111Due to the non-standard nature of , consistently approximating the limiting distribution of uniformly over a large class of DGPs is not possible in general. Hence, the existing methods resort to conservative distortions. For example, consider the generalized moment selection (GMS) in Andrews & Soares (2010). Let and let be an estimator of the correlation matrix, i.e. This procedure uses the quantile of the following statistic

| (26) |

where is the bootstrapped empirical process, and is a vector whose components are

| (27) |

The generalized moment selection (GMS) function then selects the inequalities that are relevant for the inference for based on (see Andrews & Soares (2010) for details). The resulting confidence region is

| (28) |

In Example 1, applying this method with a -test based GMS function ( if and otherwise) yields the following confidence interval

| (29) |

where the critical value is the quantile of the bootstrapped statistic121212The critical value and the standard deviations in this example are not indexed by because the re-centered moment functions in the test statistic do not depend on .

| (30) |

The confidence interval in this example is the intersection of the sample (upper) bounds that are suitably expanded. The amount of the expansion accounts for the variation of each simulated moment. This type of confidence interval is also considered in the context of conditional moment restrictions in Chernozhukov et al. (2013).

Remark 3.1.

The method described above accounts for the simulation variation contained in the sample moment . Hence, one can expect that it mitigates the problem we saw in Section 2.2. However, it does not account for the second channel through which simulation can affect the performance of the confidence region. This is through the rescaled moments used in the GMS function. As we saw in Table 3, the effect of simulation on the selected set of moments is nontrivial. However, since the critical value may depend on in a discontinuos manner (see the -test based on GMS above), the analysis of the effect of the simulation error on the coverage probability through this channel is complex. We therefore do not pursue the correction of the effect of simulation through . In contrast, our alternative inference method in the next section admits a straightforward way to correct the effect of simulation.

3.2 Regularization of test statistics

In addition to the modification of the existing methods, we propose a novel and computationally simple inference procedure that accounts for simulation. The key idea is as follows. Recall that commonly used test statistics take the form: whose irregular behavior arises due to the non-smoothness of . Our procedure replaces by a smooth approximation , which satisfies certain regularity conditions. This approach has several attractive features. First, the proposed method has a uniform approximation property. That is, for any , for a known uniform constant and the degree of smoothness , which is chosen by the researcher. Accounting for the approximation error is then straightforward because is known. Second, the approximated test statistic obeys standard limit theorems uniformly over a large class of DGPs and over a range of values for . This in turn allows one to employ a standard resampling method such as bootstrap to calculate the critical value. Finally, smooth approximations to a wide class of non-smooth convex functions are available thanks to the recent developments in the non-smooth convex optimization literature (see e.g. Nesterov, 2005; Beck & Teboulle, 2012). Using these results, we provide functional forms of smooth approximations to some of the commonly used test statistics. The idea of regularizing test statistics (or estimated bounds) also appears in related contexts (Haile & Tamer, 2003; Chernozhukov et al., 2015; Kaido, 2017; Masten & Poirier, 2017). Our contribution here is to show its uniform validity in the context of inference with simulated variables. A potential price for this computationally simple method is the possibility of inference becoming conservative for some choice of the smoothing parameter. We will examine this point numerically in Section 4.

Below, we illustrate our approach using Example 1.

Example 1 (Intersection bounds (continued)).

Recall the confidence interval in (7):

| (31) |

where . Consider replacing with a smooth approximation. Specifically, for , define

| (32) |

where replaces the maximum function. We then calculate our critical value by

| (33) |

This critical value consists of two terms. The first term, , is an approximation to the quantile of the root (centered and rescaled statistic):131313In this example, does depend on . Hence, its quantile does not depend on either.

| (34) |

The second term in (33) is a bias-correction term that accounts for the approximation error (or population-level bias) that arises when we replace by its smooth counterpart . The quantile can be approximated by a bootstrap procedure that resamples an analog of in (34) (see Algorithm 1 below).

The confidence interval in (32) is asymptotically valid over a wide class of data generating processes and choices of . We sketch the argument below and defer the formal proof to the sequel.

Let be the upper boundary point of the identified set. Then, Let Then, uniformly in and in over a class of distributions specified below, the (least favorable) coverage probability is

| (35) | ||||

| (36) |

where we used (34), with (see Table 4). The convergence in the last step follows from the argument below.

Note that is differentiable with the following derivative:

| (37) |

It can be shown that is Lipschitz continuous in with a Lipschitz constant Hence, by the mean-value theorem,

| (38) | ||||

| (39) |

where uniformly in as with fixed. Hence, converges in distribution to some limit uniformly in over a compact set (not containing 0).

Now, let us compare this to a method without any regularization of . The coverage probability of the confidence interval in (31) is

| (40) |

The transformation is not differentiable but can be shown to be directionally differentiable with the following directional derivative:

| (41) |

Observe that the directional derivative is non-linear in (but only positively homogeneous). More importantly, the directional derivative depends on and hence the underlying data generating process in a discontinuous manner. This is because the set of “active” inequalities, , depends on discontinuously. This in turn implies that the limiting distribution of the test statistic is discontinuous in the underlying DGP.141414This follows from a -method for directionally differentiable functions (Shapiro, 1991). The discontinuity in the limiting distribution of the statistic can be shown without using the directional derivative (Andrews & Soares, 2010). We use the directional derivative to make a comparison to the method based on the -smooth approximation and standard -method. Hence, a small perturbation of the underlying data generating process may result in a significant change in the distribution of the statistic. When simulation is used to replace the population moments, this therefore could affect the behavior of the statistic in non-trivial ways. This feature motivated the vast literature on moment inequalities that corrects the critical value whenever this type of discontinuity is a concern (see e.g Andrews & Soares, 2010; Chernozhukov et al., 2013; Fang & Santos, 2014; Romano et al., 2014).

In contrast, our approach first replaces the by a smooth approximation , while correcting for the population level bias. Since the limiting distribution of depends on the underlying distribution in a smooth manner, there is no need to correct the critical value . In short, our approach regularizes the behavior of the statistic, while the vast literature regularizes the critical value to ensure the uniform validity of inference.

The motivations for this approach are two-fold. First, it is straightforward to show that the proposed method is uniformly valid under the large asymptotics with a fixed simulation size . The proposed method combines the standard -method with a bias correction (at the population level). The method and its uniform validity may be of independent interest outside the context of simulation based inference. Second, the inference method is simple and can be implemented by a standard bootstrap procedure. This is attractive as accounting for the effects of simulation errors on moment selection procedures or Bonferroni-correction methods in the existing literature may be non-trivial.

In general, we define our confidence set by

| (42) |

where the test statistic and the critical value are calculated as follows

| (43) | ||||

| (44) |

where is an estimate of the quantile of

| (45) |

Here, is an approximation to , which has smoothness properties that are useful for analyzing and correcting the behavior of the test statistic in the presence of simulated variables. We introduce the following notion of approximation based on Beck & Teboulle (2012).151515The third condition in Definition 3.1 is not required in Beck & Teboulle (2012) but is satisfied by all -smooth approximations we use in this paper and is useful for establishing asymptotic results.

Definition 3.1 (-smooth approximation).

Let be a closed and proper convex function and let be a closed convex set. A function is said to be a -smooth approximation of with parameters if the following conditions hold:

(i) for some satisfying ;

(ii) has a derivative such that

| (46) |

for some and ;

(iii) For each , is continuous.

Definition 3.1 (i) requires that has a uniform approximation property, which is the key condition for bias correction. Definition 3.1 (ii) requires that ’s derivative is Lipschitz continuous, which plays a role in making the limiting distribution of depend continuously on the underlying DGP. Given this definition, we require and to satisfy the following condition. For this, let be the set of symmetric positive semi-definite matrices.

Assumption 3.1.

(i) The index function satisfies Assumptions in Andrews & Soares (2010). For any and , for a proper convex function with , where ; (ii) For each , the map is such that for any and , for a -smooth approximation of .

In what follows, we also call the -smooth approximation of . Table 4 gives the index functions we consider and their -smooth approximations with associated parameters. Details are provided in Appendix A. These functions satisfy Assumption 3.1.161616It is also possible to consider the index function considered in Rosen (2008) whose -smooth approximation is given by with . However, the statistic based on this approximation requires a second-order -method to obtain a valid limiting distribution, which makes the analysis more complicated. As such, we leave this possibility for future research.

| (i) | |||

|---|---|---|---|

| (ii) |

In summary, we propose the following procedure to construct confidence regions.

Algorithm 1:

- Step 1

-

: Choose . Calculate using a -smooth approximation of in Table 4 and simulated samples of size . For each observation , also draw a larger simulated sample with from the law for .

- Step 2

-

: Bootstrap.

-

•

Let be drawn from the empirical distribution of (with replacement).

-

•

For each bootstrapped observation , draw a simulated sample from the law for .

-

•

Compute the quantile of the root:

(47)

-

•

- Step 3

-

: Calculate the critical value in (44) by introducing the correction term for the approximation bias.

- Step 4

-

: For each , conduct steps 1-3 and report

Similar to the consistent estimation of the asymptotic covariance matrix in the MSM literature, we use a simulation sample of larger size in the algorithm (see e.g. Gourieroux & Montfort, 1996, Section 2.3). This is to re-center the bootstrapped root at an object that tends to the population counterpart and mimic the behavior of the root in (45) by the bootstrap sample. While needs to be large for the asymptotic approximation to be valid, this simulation needs to be done only once.

Below, we establish the asymptotic validity of the inference procedure described above. For each , we let and , where . We then let denote the gradient of the map Let be the set of -by- correlation matrices with for some . We make the following assumption on the model.

Assumption 3.2.

The model for satisfies the following conditions.

(i)

(ii) for some

(iii) is an i.i.d. sample from ;

(iv) for and ;

(v) ;

(vi) for some and ;

(vii) For any , for some and for all .

Assumption 3.2 (i)-(vi) are based on the conditions in Andrews & Guggenberger (2009); Andrews & Soares (2010). In (iii), we assume an i.i.d. sample. With this assumption, the following estimator of the asymptotic covariance can be used:171717While we establish validity of inference for i.i.d. samples, one could potentially relax this assumption and allow for strictly stationary and strongly mixing data by adopting an alternative estimator of the asymptotic covariance and modifying the bootstrap procedure properly. See Andrews & Guggenberger (2009) for the inference framework that allows such data.

| (48) |

We then let . For the purpose of stating an assumption, let us also define an infeasible estimator of as follows:

This estimator can be computed only if simulation is not required. We then let .

In Assumption 3.2 (v), contains all correlation matrices whose determinant is bounded from below by . This condition is required for one of the index functions used in Andrews & Soares (2010). In our setting, we use this condition to ensure that the limiting distribution of is continuously distributed. With additional notation, this assumption can be relaxed so that the lower bound on the determinant is required only for the correlation matrix of a suitable subset of the moment functions.181818See Kaido et al. (2017) for generalization of the condition along this line. Or it can be dropped entirely at the price of an additional tuning parameter to handle a potentially discontinuos limiting distribution.

Assumption 3.2 (vii) is an additional condition, which we add to the standard set of assumptions. It requires that the gradient of the smoothed index function does not vanish. This allows us to use the (first-order) -method. For the functions in Table 4, the condition is satisfied when is continuous and are uniformly bounded away from 0.

The following theorem ensures that the proposed confidence region controls the asymptotic confidence size uniformly over the parameter space .

4 Monte Carlo Experiments

In this section, we show results of main Monte Carlo simulations to examine the performance of the methods that account for the simulation error.

4.1 Performance of methods with correction for simulation errors

Following our example on the intersection bounds in Section 2.2, we first use the method that corrects the critical value described in Section 3.1. We construct confidence intervals for with level using:

| (49) |

where is the estimated standard deviation of the -th simulated moment, and is a critical value computed as the quantile of

| (50) |

where is the bootstrap quantities corresponding to , and is as defined in (27) with . When is computed, we redraw simulation draws to account for simulation variations when simulating the bootstrap samples.

We also consider our inference procedure based on the regularized statistic. Specifically, we use to approximate used in computing the confidence region in equation (15). We then construct confidence intervals for with level using:

| (51) |

where is an estimated critical value in (44). We also redraw simulation draws when simulating the bootstrap samples. In the experiments, we use to compute in the bootstrap step (Step 2 in Algorithm 1). For both confidence intervals, Monte Carlo replications are generated.

Table 6 reports the probabilities of the confidence intervals covering the upper bound of the identified set using the critical value correction. The coverage probabilities of the confidence intervals are all above the nominal level after correcting the critical value. This can be contrasted with the coverage probabilities of the confidence intervals without any correction. The critical value correction method tends to make the confidence interval somewhat conservative when is small. In some cases, the coverage probability is very close to 1 and the corrected confidence interval is substantially longer than the one based on the regularization method as we discuss below.

Table 6 reports the coverage probabilities of the confidence intervals based on the -smooth approximation. We set the smoothing parameter to and in our Monte Carlo experiments. The coverage probabilities of are all above those of the confidence intervals without correction and close to the nominal level in many cases. These results indicate that the inference procedure with the -smooth approximation is an effective method for correcting the size distortion caused by the finite number of draws.

Tables 8 and 8 report the median length of the confidence intervals. The median length of a one-sided confidence interval is computed as the difference between the median of the upper bound of the confidence interval and the right end point of the identified set. Table 8 shows that the confidence interval with the critical value correction is often much longer than the confidence interval without any correction, which is consistent with the robust size control property. The difference between the two shrinks as gets large. Comparing the two tables, one can see that the regularization based confidence intervals are often significantly shorter than . A close inspection of the simulation results showed that this was because the regularized statistic had a smaller variance that that of the non-regularized statistic, which led to shorter confidence intervals even after the bias correction.191919This may be a generic feature of the -smooth approximation method. We leave its general analysis for future work.

The overall pattern remains the same even in the presence of locally slack constraints. Tables 10-12 report the coverage probabilities and excess length of the confidence intervals when some of the constraints are slack. The slack constraints are introduced by shifting ’s mean by for the first constraints. One can see that both correction methods achieve valid coverage across all values of simulation draws. The regularization based confidence interval becomes slightly more conservative in terms of coverage probabilities compared to the case without the slack constraints. However, its length is still shorter than that of the critical value correction confidence interval across all cases.

In sum, the simulation results show that the regularization based confidence interval works well both in terms of size and length. Its size is controlled reasonably well even under some DGPs that make simulated confidence intervals without correction severely undersized. The critical value correction method also achieves robust size control. However, it tends to be overly conservative when is small.

5 Concluding remarks

This paper explores the effects of simulated moments on the performance of inference methods based on moment inequalities. Due to the irregularity of the boundary of the confidence regions, simulation errors can affect the performance of inference in non-standard ways. This can result in a severe distortion especially when the number of inequality restrictions is large and the essential sample size is small. To account for the effect of the simulation error, we propose a novel way to construct confidence regions using regularized statistics and establish an asymptotic size control result. The simulation results confirm the robust size control property of the proposed method. An interesting avenue for future research is on the choice of the smoothing parameter that accounts for the trades-off between the amount of bias correction and variance of the regularized statistic.

| Simulated (No correction) | CV correction: | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| A: () | |||||||||

| 0.583 | 0.882 | 0.908 | 0.930 | ||||||

| 0.604 | 0.881 | 0.920 | 0.935 | ||||||

| 0.666 | 0.894 | 0.913 | 0.933 | ||||||

| B: () | |||||||||

| 0.481 | 0.853 | 0.904 | 0.920 | ||||||

| 0.467 | 0.868 | 0.908 | 0.925 | ||||||

| 0.487 | 0.853 | 0.896 | 0.919 | ||||||

| C: () | |||||||||

| 0.245 | 0.811 | 0.888 | 0.923 | ||||||

| 0.266 | 0.803 | 0.878 | 0.917 | ||||||

| 0.235 | 0.810 | 0.881 | 0.912 | ||||||

| Regularization: () | Regularization: () | ||||||||

| A: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| B: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| C: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| Simulated (No correction) | CV correction: | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| A: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| B: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| C: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| Regularization: () | Regularization: () | ||||||||

| A: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| B: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| C: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| Simulated (No correction) | CV correction: | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| A: () | |||||||||

| 0.620 | 0.899 | 0.920 | 0.935 | ||||||

| 0.647 | 0.903 | 0.933 | 0.945 | ||||||

| 0.700 | 0.911 | 0.927 | 0.944 | ||||||

| B: () | |||||||||

| 0.533 | 0.875 | 0.920 | 0.938 | ||||||

| 0.520 | 0.886 | 0.922 | 0.935 | ||||||

| 0.535 | 0.879 | 0.917 | 0.933 | ||||||

| C: () | |||||||||

| 0.301 | 0.833 | 0.911 | 0.940 | ||||||

| 0.324 | 0.840 | 0.895 | 0.933 | ||||||

| 0.280 | 0.833 | 0.905 | 0.926 | ||||||

| Regularization: () | Regularization: () | ||||||||

| A: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| B: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| C: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

Note: Among moment inequalities, of them are slack.

| Simulated (No correction) | CV correction: | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| A: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| B: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| C: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| Regularization: () | Regularization: () | ||||||||

| A: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| B: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

| C: () | |||||||||

| 100 | |||||||||

| 250 | |||||||||

| 1000 | |||||||||

Note: Among moment inequalities, of them are slack.

References

- Andrews & Guggenberger (2009) Andrews, D. W. & Guggenberger, P. (2009). Validity of subsampling and plug-in asymptotic inference for parameters defined by moment inequalities. Econometric Theory, 25(03), 669–709.

- Andrews & Soares (2010) Andrews, D. W. & Soares, G. (2010). Inference for parameters defined by moment inequalities using generalized moment selection. Econometrica, 78(1), 119–157.

- Andrews & Barwick (2012) Andrews, D. W. K. & Barwick, P. J. (2012). Inference for parameters defined by moment inequalities: A recommended moment selection procedure. Econometrica, 80(6), 2805 – 2826.

- Bajari et al. (2007) Bajari, P., Benkard, L., & Levin, J. (2007). Estimating dynamic models of imperfect competition. Econometrica, 75, 1331–1370.

- Beck & Teboulle (2012) Beck, A. & Teboulle, M. (2012). Smoothing and first order methods: A unified framework. SIAM Journal on Optimization, 22(2), 557–580.

- Berry (1992) Berry, S. (1992). Estimation of a model of entry in the airline industry. Econometrica, 60, 889–917.

- Berry et al. (1995) Berry, S., Levinsohn, J., & Pakes, A. (1995). Automobile prices in market equilibrium. Econometrica, 63, 841–890.

- Bresnahan & Reiss (1991) Bresnahan, T. & Reiss, P. (1991). Entry and competition in concentrated markets. Journal of Political Economy, 99, 977–1009.

- Chernozhukov et al. (2007) Chernozhukov, V., Hong, H., & Tamer, E. (2007). Estimation and confidence regions for parameter sets in econometric models. Econometrica, 75(5), 1243 – 1284.

- Chernozhukov et al. (2015) Chernozhukov, V., Kocatulum, E., & Menzel, K. (2015). Inference on sets in finance. Quantitative Economics, 6(2), 309–358.

- Chernozhukov et al. (2013) Chernozhukov, V., Lee, S., & Rosen, A. (2013). Intersection bounds: Estimation and inference. Econometrica, 81, 667–737.

- Ciliberto & Tamer (2009) Ciliberto, F. & Tamer, E. (2009). Market structure and multiple equilibria in airline markets. Econometrica, 77, 1791–1828.

- Crawford & Yurukoglu (2012) Crawford, G. S. & Yurukoglu, A. (2012). The welfare effects of bundling in multi-channel television markets. American Economic Review, 102, 643–685.

- Eizenberg (2013) Eizenberg, A. (2013). Upstream innovation and product variety in the U.S. home PC market. Unpublished Manuscript, Hebrew University.

- Fang & Santos (2014) Fang, Z. & Santos, A. (2014). Inference on directionally differentiable functions. arXiv preprint arXiv:1404.3763.

- Fowlie et al. (2015) Fowlie, M., Reguant, M., & Ryan, S. P. (2015). Market-based emissions regulation and industry dynamics. Journal of Political Economy, forthcoming.

- Gourieroux & Montfort (1996) Gourieroux, C. & Montfort, A. (1996). Simulation-Based Econometric Methods. Oxford University Press.

- Gowrisankaran et al. (2014) Gowrisankaran, G., Nevo, A., & Town, R. (2014). Mergers when prices are negotiated: Evidence from the hospital industry. The American Economic Review, 105(1), 172–203.

- Haile & Tamer (2003) Haile, P. A. & Tamer, E. (2003). Inference with an incomplete model of english auctions. Journal of Political Economy, 111, 1–51.

- Hausman (1983) Hausman, J. A. (1983). Specification and estimation of simultaneous equation models. Handbook of econometrics, 1, 391–448.

- Hirano & Porter (2012) Hirano, K. & Porter, J. R. (2012). Impossibility results for nondifferentiable functionals. Econometrica, 1769–1790.

- Ho (2009) Ho, K. (2009). Insurer-provider networks in the medical care market. American Economic Review, 99, 393–430.

- Holmes (2011) Holmes, T. J. (2011). The diffusion of Wal-Mart and economies of density. Econometrica, 79, 253–302.

- Houde et al. (2017) Houde, J.-F., Newberry, P., & Seim, K. (2017). Economies of density in e-commerce: A study of amazons fulfillment center network. NBER Working Paper.

- Kaido (2017) Kaido, H. (2017). Asymptotically efficient estimation of weighted average derivatives with an interval censored variable. Econometric Theory, 1–24.

- Kaido et al. (2017) Kaido, H., Molinari, F., & Stoye, J. (2017). Confidence intervals for projections of partially identified parameters. arXiv preprint arXiv:1601.00934.

- Kawai & Watanabe (2013) Kawai, K. & Watanabe, Y. (2013). Inferring strategic voting. American Economic Review, 103(2), 624 – 662.

- Masten & Poirier (2017) Masten, M. A. & Poirier, A. (2017). Inference on breakdown frontiers. Discussion Paper, Duke University.

- McFadden (1989) McFadden, D. (1989). A method of simulated moments for estimation of discrete response models without numerical integration. Econometrica: Journal of the Econometric Society, 995–1026.

- Nesterov (2005) Nesterov, Y. (2005). Smooth minimization of non-smooth functions. Mathematical Programming, 103(1), 127–152.

- Newey & McFadden (1994) Newey, W. K. & McFadden, D. (1994). Large sample estimation and hypothesis testing. Handbook of econometrics, 4, 2111–2245.

- Nosko (2014) Nosko, C. (2014). Competition and quality choice in the cpu market. Discussion Paper, Harvard University.

- Pakes et al. (2007) Pakes, A., Ostrovsky, M., & Berry, S. (2007). Simple estimators for the parameters of discrete dynamic games (with entry/exit examples). RAND Journal of Economics, 38, 373–399.

- Pakes & Pollard (1989) Pakes, A. & Pollard, D. (1989). Simulation and the asymptotics of optimization estimators. Econometrica, 57, 1027–1057.

- Pakes et al. (2011) Pakes, A., Porter, J., Ho, K., & Ishii, J. (2011). Moment inequalities and their application. Unpublished Manuscript, Columbia University.

- Politis et al. (1999) Politis, D. N., Romano, J. P., & Wolf, M. (1999). Subsampling: Springer series in statistics. Berlin: Springer.

- Rockafellar & Wets (2009) Rockafellar, R. T. & Wets, R. J.-B. (2009). Variational analysis, volume 317. Springer Science & Business Media.

- Romano et al. (2014) Romano, J. P., Shaikh, A. M., & Wolf, M. (2014). A practical two-step method for testing moment inequalities. Econometrica, 82(5), 1979–2002.

- Rosen (2008) Rosen, A. M. (2008). Confidence sets for partially identified parameters that satisfy a finite number of moment inequalities. Journal of Econometrics, 146(1), 107–117.

- Ryan (2012) Ryan, S. (2012). The costs of environmental regulation in a concentrated industry. Econometrica, 80, 1019–1062.

- Shapiro (1991) Shapiro, A. (1991). Asymptotic analysis of stochastic programs. Annals of Operations Research, 30(1), 169–186.

- Tamer (2003) Tamer, E. (2003). Incomplete simultaneous discrete response model with multiple equilibria. Review of Economic Studies, 70(1), 147–165.

- Tamer (2010) Tamer, E. (2010). Partial identification in econometrics. Annual Review of Economics, 2, 167–195.

- Van Der Vaart & Wellner (1996) Van Der Vaart, A. W. & Wellner, J. A. (1996). Weak Convergence and Empirical Processes with Applications to Statistics. Springer.

- Wollmann (2014) Wollmann, T. (2014). Trucks without bailouts: Equilibrium product characteristics for commercial vehicles. Working Paper, Chicago-Booth.

Appendix A Proofs

A.1 Hausdorff consistency

Below, we let be a random vector that stacks and . We then let . For each , let be defined as in (48) and let . We use the following assumption to establish consistency of in Proposition 2.1.

Assumption A.1.

The following conditions hold.

-

(i)

The parameter space is a nonempty compact subset of ;

-

(ii)

: is jointly measurable in , where is a neighborhood of ;

-

(iii)

For each , the collection is a -Donsker class. is an i.i.d. sample;

-

(iv)

There exist positive constants and such that for all ,

-

(v)

uniformly in when with fixed, where is a diagonal matrix with positive diagonal elements and is continuous for all

The imposed conditions are analogous to Condition M.1 in Chernozhukov et al. (2007) (see Section 3.2 in their paper for details). A key modification is that we assume that is -Donsker instead of being -Donsker. This ensures that the sample moments converge to the population counterpart even with a finite number of draws. This condition is satisfied when is a -Donsker class, which holds for a wide class of functions (Pakes & Pollard, 1989; Van Der Vaart & Wellner, 1996). Assumption A.1 (v) requires that the estimators of the asymptotic variance converge with a finite number of draws. This holds under mild regularity conditions. A more primitive condition is given in Assumption 3.2.

Proof of Proposition 2.1.

The result follows almost immediately from Theorems 3.1 and 4.2 of Chernozhukov et al. (2007) (CHT below). Hence, we briefly sketch the argument below.

Under the imposed assumptions, Condition C.1 (a)-(c) in CHT follows. This step is the same as in the proof of Theorem 4.2 in CHT. For Condition C.1-(d), note that

By being -Donsker, it follows that

for a fixed and . Together with the uniform convergence of the weighting matrix (Assumption A.1 (v)) and the continuous mapping theorem, it implies Condition C.1-(d) of CHT.

Again by the Donskerness, uniformly over

where the last equality follows because of the Donskerness and on . Hence, one may take . The conclusion of the proposition then follows from Theorem 3.1 in CHT. ∎

A.2 Auxiliary results for regularization based confidence regions

For each and , define

| (52) | ||||

| (53) |

In what follows, we denote the covariance matrix of the moment function under distribution by and we let . Similarly, we let the correlation matrix be . Here is a set of high-level conditions for the asymptotic size control.

Condition A.1.

There exist , , and such that are closed intervals, and the following conditions hold:

(i) If a sequence satisfies , and , then

| (54) |

for all continuity points of whose distribution is determined by . The cumulative distribution function is strictly increasing at the quantile.

(ii) for the sequence defined above,

| (55) |

where is the quantile of .

Under this condition, we obtain the following generic size control result, which we will apply to establish Theorem 3.1.

Proposition A.1.

Suppose that is a -smooth approximation to . Suppose Condition A.1 holds. Let . Then, for any ,

| (56) |

Proof.

Let Note that we have where and are as in (52)-(53). Therefore, we may restate the coverage of by the confidence region as follows:

| (57) |

where the last step follows from Definition 3.1 (i).

Let the asymptotic confidence size be Then, there is a sequence such that , , and By compactness of and , there is a further subsequence along which and . For notational simplicity, we use the same index for the subsequence. By Condition A.1 (ii) and passing to a further subsequence, one has almost surely. Again by Condition A.1 (i), we then obtain

| (58) |

| (59) |

We may therefore conclude ∎

A.3 Proof of Theorem 3.1

Proof of Theorem 3.1.

Below, we show Condition A.1.

First, by Assumption 3.1 (ii),

| (60) |

where . The last equality in (60) follows from the mean value theorem (applied componentwise), and is a point between and , which may be different across components.

Let . This is a compact subset of due to Assumption 3.2 (vi). Note that, there exists a such that, uniformly over ,

| (61) |

where and denote the operator and Frobenius norms of a matrix respectively, and the last inequality follows from , , and being uniformly bounded by the continuity of (by Definition 3.1) and compactness of . As we show below, the asymptotic variance of is then bounded by . Below, we let be the quantile of a mean-zero normal distribution with variance , which will serve as the uniform upper bound for the critical value.

By Assumption 3.2 (vi) and Minkowski’s inequality, for some uniform constant . Together with Assumption 3.2 (iii), we may then apply Lemma 2 in Andrews & Guggenberger (2009), which uses a triangular-array LLN and CLT to obtain

| (65) |

where is a multivariate normal random vector with covariance matrix . By being a -smooth approximation and Definition 3.1 (ii),

| (66) |

where the last equality follows from being between and and the uniform law of large numbers applied to , which again follows from Lemma 2 in Andrews & Guggenberger (2009). By Definition 3.1 (iii), Assumption 3.2 (vi), and the extended continuous mapping theorem (Van Der Vaart & Wellner, 1996, Theorem 1.11.1), we obtain

| (67) |

Note that is a mean zero normal distribution with variance . By Assumption 3.2 (v) and (vii) and a continuity argument, and is positive definite. Hence, the variance of is bounded away from 0. This ensures that the cumulative distribution function of is continuous and strictly increasing at its quantile. This establishes Condition A.1 (i).

Next, we show Condition A.1 (ii). Let a sequence be given, fix , and let be the set of sequences such that and for some and . In what follows, we write and . In Part (i), we have shown that

| (68) |

where is a metric that metrizes the weak convergence (e.g. the bounded Lipschitz metric). For each be the empirical distributions of . Let denote the joint distribution of , where ’s law is the empirical distribution based on the original sample , while ’s conditional law is known. The bootstrap sample is drawn from the empirical distribution, while for each , is drawn from . Therefore, can be viewed as a sample from

Define

| (69) |

where for each ,

| (70) | ||||

| (71) |

We then let where . Note that differs from the root we compute in Algorithm 1 as the centering term in (69) is not based on any simulation (or it can be viewed as the limit with ). Below, we first show that there is a subsequence such that almost surely. We then apply Theorem 1.2.1 in Politis et al. (1999) to establish bootstrap consistency for this infeasible bootstrap. Bootstrap consistency for Algorithm 1 is then established by showing that replacing with has asymptotically negligible effects as

Under Assumption 3.2 and arguing as in (65), we may apply Lemma 2 in Andrews & Guggenberger (2009), which ensures that

| (72) |

and

| (73) |

Hence, for any subsequence of these sequences that are converging in probability, one also has a further subsequence along which convergence in (72) and (73) hold almost surely under (instead of in probability) for all . Therefore with probability 1. By Theorem 1.2.1 in Politis et al. (1999), it then holds that with probability 1. Since the choice of the original subsequence was arbitrary, this in turn implies

| (74) |

Now consider the root we compute in Algorithm 1. For each , let Below we take to be the bounded Lipschitz metric. Then,

| (75) |

Arguing as in (60)-(62), one has

| (76) |

where , and is a point between and . The last equality follows by the assumption on . Note that, conditional on , is uniformly integrable, and hence it converges in by (76). Therefore, by (75), it follows that

| (77) |

Combining (68), (74) and (77), we conclude that

| (78) |

For any subsequence, one can then find a further subsequence for which (78) holds almost surely. Mimicking the argument in the proof of Theorem 1.2.1 in Politis et al. (1999) and being strictly increasing at its quantile, the bootstrap critical value along the subsequence then satisfies

| (79) |

with probability 1. Since this holds for arbitrary subsequence, we have

| (80) |

for the original sequence. This establishes Condition A.1 (ii).

The conclusion of the theorem now follows by applying Proposition A.1 with and . ∎

Appendix B -smooth approximations of index functions

We show below that the functions given in Table 4 and footnote 16 are the -smooth approximations of the corresponding index functions.

For , is the sum of functions . For each , it has a -smooth approximation function with parameters . By Lemma in Beck & Teboulle (2012), has the following -smooth approximation function

| (81) |

with parameters .

For , . By Theorem in Beck & Teboulle (2012), this suggests has a -smooth approximation function with parameters .

For the function in footnote 16, is constructed through an operation called inf-convolution (see e.g Rockafellar & Wets, 2009). Let and let be defined by

| (82) |

Define the infimal convolution of and by

| (83) |