On the sample autocovariance of a Lévy driven moving average process when sampled at a renewal sequence

Abstract

We consider a Lévy driven continuous time moving average process sampled at random times which follow a renewal structure independent of . Asymptotic normality of the sample mean, the sample autocovariance, and the sample autocorrelation is established under certain conditions on the kernel and the random times. We compare our results to a classical non-random equidistant sampling method and give an application to parameter estimation of the Lévy driven Ornstein-Uhlenbeck process.

Mathematics subject classification: 60F05, 60G10, 62D05.

Key words: central limit theorem, continuous time moving average process, Lévy process, Ornstein-Uhlenbeck process, renewal sampling, sample autocovariance, sample autocorrelation, sample mean, stationarity.

1 Introduction

The present paper analyzes the distributional limit of sample mean and sample autocovariance function of a Lévy driven moving average process when sampled at a renewal sequence. More precisely, let be a continuous time moving average process of the form

| (1.1) |

where is a two-sided -valued Lévy process, , and a deterministic function, called kernel, for which the integral exists.

Moving average processes as in (1.1) are the natural continuous time analogue of discrete time moving average processes, whose distributional limits for sample mean and sample autocorrelation have been studied by Brockwell and Davis [5], Davis and Mikosch [7], and Hannan [10], and many others.

A popular example of a Lévy driven moving average process is given by the Ornstein-Uhlenbeck (OU) process used to model the volatility of a financial asset, see [1], or the intermittency in a turbulence flow, see [2]. The OU process is in fact a tractable mathematical model that can adequately describe the fluctuations of the price and the velocity field on different time scales.

The process is infinitely divisible, as shown in Rajput and Rosinski [11], and strictly stationary meaning that its finite dimensional joint distributions are shift-invariant, i.e. for all and all it holds

We study a renewal sampling of the process in (1.1). We select a sequence of increasing random times such that almost surely (abbreviated a.s.). More in detail, we assume that is an i.i.d. sequence of positive supported random variables independent of the driving Lévy process and such that . We then define by

| (1.2) |

and the sampled process via

| (1.3) |

We are interested in studying the sample moments of the process . We do this for different reasons. First of all, continuous processes are often used in time series analysis because they can be sampled at non-equidistant points in time and therefore provide a model for non-equidistant data which are often available for statistical inference. Secondly, several authors (Cohen and Lindner [6], Drapatz [8], and Spangenberg [13]) analyze the asymptotic distribution of the sample mean and sample autocovariance function when is sampled on a lattice for but results for non-equidistant sampling schemes have not yet been shown.

The central limit theorems presented in the paper generalize the results of Cohen and Lindner [6] at the cost of slightly more restrictive moment conditions. In fact, in the latter, the asymptotic normality of the sample mean and the sample autocovariance function is shown under the assumption of finite second and fourth moments of the driving Lévy process, respectively, whereas we achieve the asymptotic normality by requiring and , respectively, to be finite.

As an application of the developed theory, we present a parameter estimation of the mean reverting parameter of a Lévy driven OU process

| (1.4) |

sampled at a Poisson process, i.e. a sequence where is a sequence of i.i.d. exponentially distributed random variables. We then compare the efficiency of our estimator with an estimator based on the results of Cohen and Lindner [6] for an equidistant sampling.

The paper is organized as follows. In Section 2 we give some preliminary results regarding strict stationarity of a process sampled at a renewal sequence and the mixing property that it fulfills. Section 3 is concerned with establishing a central limit theorem for the sample mean of a renewal sampled continuous time moving average process as Section 4 does for the sample autocovariance and sample autocorrelation functions. Finally in Section 5, we show the parameter estimation of a Lévy driven OU process, and Section 6 concludes.

2 Preliminaries

We start with some preliminary results on the continuous time moving average process and its renewal sampled processes needed in the upcoming sections. As a first results, we prove that a strictly stationary process sampled at a renewal sequence inherits the strict stationarity. In particular, this shows that the sampled process (1.3) is strictly stationary.

Denote with equality in distribution and with the transpose of a matrix .

Proposition 2.1.

Let be an -valued strictly stationary process and let be a sequence of random times defined as in (1.2) independent of . Then the -valued process defined by , , is strictly stationary. More generally, the process is strictly stationary.

Proof.

Observe that is strictly stationary if and only if is strictly stationary, and the latter implies strict stationarity of . Hence, it suffices to show that is strictly stationary. Let , , the Borel--algebra on , and denote with the finite dimensional distribution of a random vector . Define

Conditioning and using the strict stationarity of , we obtain

where in the last line we used that the integrand does not depend on . Using that , the latter is equal to

showing the strict stationarity of . ∎

In order to prove central limit theorems, we recall the concept of mixing: on a probability space for any two -algebras the following measures of dependence can be defined

We say that a strictly stationary sequence of random vectors is

for the -algebras and , cf. Bradley [4].

Recall that a process is called an -dependent process when and are independent for each .

Proposition 2.2.

Let be for some an -valued -dependent strictly stationary process and defined by with as in (1.2) independent of . Then is strongly mixing with exponentially decreasing mixing coefficients . More generally, is strongly mixing with exponentially decreasing mixing coefficients.

Proof.

Let , . Let and so large such that . First, we show that the two -algebras and defined as above are independent under the conditional probability measure . Therefore, let and be of the form for some , , and , and for some , , and , respectively. Then, by the Doob-Dynkin lemma and the -dependence of ,

Observe that since for and are independent. A calculation like the one above for , i.e. , gives

such that all together we obtain

| (2.1) |

Similarly we can obtain (2.1) for for , , and , and for , , and . Observe that sets of the form generate the -algebra and sets of the form generate the -algebra and both are -stable. Thus, we conclude that (2.1) is true for all and . Using measure theoretic induction, and

we obtain that where the supremum is taken over all and .

Since and , it follows, from a remark between Theorem 1.2 and Theorem 1.3 in Bradley [3], that

Since is supported on and , there exists an such that and hence , where for denotes the smallest integer so that . Denote . Then, as long as , we obtain . For set for . Then, by the i.i.d. property of ,

and

| (2.2) |

showing that and hence are strongly mixing with exponentially decreasing mixing coefficients.∎

We give some results on when a Lévy driven continuous time moving average process is well-defined. Moreover, we show under which conditions finiteness of the moments of the process is achieved.

An -valued Lévy processes , i.e. a stochastic process with independent and stationary increments, càdlàg sample paths and almost surely, which is continuous in probability, is characterized by its characteristic triplet due to the Lévy-Khintchine formula, i.e. if denotes the infinitely divisible distribution of , then its characteristic function is given by

Here, is the Gaussian covariance, a measure on which satisfies and , called the Lévy measure, and .

For a detailed account on Lévy processes we refer to the book of Sato [12].

In the following theorem, we recall the multivariate extension of Theorem 2.7 in Rajput and Rosinski [11], which characterizes the continuous time moving average process.

Theorem 2.3.

Let be a Lévy process on with characteristic triplet and be a measurable function. Denote with the unit ball in . Then

(a) is -integrable i.e. integrable with respect to the Lévy process as a limit in probability in the sense of Rajput und Rosinski [11] if and only if

(i) ,

(ii) , and

(iii) .

(b) If is -integrable, the distribution of is infinitely divisible with characteristic triplet given by

Corollary 2.4.

The next lemma shows, for a process as in (1.1), finiteness of the -moment under certain conditions on the Lévy process and the kernel function .

We use the notation .

Lemma 2.5.

Let be defined by where and is a one-dimensional Lévy process with zero mean.

(a) If , and ,

then for all .

(b) If , , and , then for all and, for , for all .

Proof.

W.l.o.g. . It is enough to show the assertions for , for which . By the strict stationarity of , we obtain the result.

(a) By Corollary 2.4, is infinitely divisible with triplet given by Theorem 2.3 (b). By Corollary 25.8 of Sato [12], we know that , if . To see that this is indeed true, observe that for . Hence, by the given assymptions,

(c) Observe that is equivalent to and that implies . Henceforth we obtain

This gives for all . Using the strict stationarity of and the Cauchy-Schwarz inequality yields

which gives the result. ∎

Remark 2.6.

Throughout the paper, we assume that the Lévy process has zero mean. This assumption can be dropped in many cases. For example, if , we define with , , another Lévy process with mean zero and the same variance such that

and has mean .

3 Sample Mean

In this section, we show the asymptotic normality of the sample mean

| (3.1) |

To do so, we consider a certain truncated continuous time moving average process. Therefore, let be a kernel function with compact support, and be defined by

| (3.2) |

where is a Lévy process with zero mean and , , and . Then the process is an -dependent process. Moreover, is strictly stationary and, by Proposition 2.1, so is the sequence defined by

| (3.3) |

where is defined as in (1.2) independent of .

The following proposition states a result on the convergence of the covariances of towards the ones of . By Proposition 2.1, the process is strictly stationary.

Proposition 3.1.

Proof.

We denote with the -algebra generated by some random variable . Clearly, for all . Then, by conditioning on and Fubini’s theorem,

| (3.6) |

Further, observe that

| (3.7) |

Define

then obviously . But, since is independent of , it holds

since . Hence as for all and all .

Define . Then such that, since , we obtain by the dominated convergence theorem for (3.7)

| (3.8) |

Now we are in the position to prove the asymptotic normality of in (3.1). We denote with convergence in distribution.

Theorem 3.2.

Let be defined as in (1.1) such that , has expectation zero and , , and . Let be defined by (1.3) with as in (1.2) independent of . Assume that

| (3.9) |

Then

(a) exists in , is absolutely convergent, and

| (3.10) |

(b) as .

Proof.

Define such that with due to the strict stationarity of and since , we obtain a sequence with expectation zero. Hence, w.l.o.g. .

(a) Observe that since and has finite second moment. Further, by (3.5) and (3.9) together with the dominated convergence theorem

| (3.11) |

This gives the absolute summability of and a similar calculation without the modulus gives (3.10).

(b) Let , where the sequence is defined as in (3.3) via the -dependent process given in (3.2). The assumptions on and imply, by Lemma 2.5 (b), .

Observe that fulfils the assumptions of Proposition 2.2 and it is therefore strongly mixing with exponentially decreasing mixing coefficient . Hence, due to (2.2), as . Hence, by Corollary 10.20 (c) in Bradley [4], we obtain

| (3.12) |

where exists in and is absolutely convergent.

By Proposition 3.1, we have that as and, since

by (3.11) and , we conclude with the dominated convergence theorem that . Hence,

| (3.13) |

Define for , . Then is strictly stationary, by Proposition 2.1. Further, by Cauchy-Schwarz’s inequality,

as since . Since, by (3.11),

the dominated convergence theorem yields .

Hence, by Theorem 7.1.1 in Brockwell and Davis [5],

Chebychef’s inequality then gives

Together with (3.12) and (3.13), the claim follows by a variant of Slutsky’s Lemma, cf. Proposition 6.3.9 of Brockwell and Davis [5]. ∎

Remark 3.3.

When is deterministic, i.e. for and some , Cohen and Lindner [6, Theorem 2.1] established the asymptotic normality of the sample mean under the conditions , , , and

| (3.14) |

Observe that (3.14) implies (3.9) since

So, Theorem 3.2 generalizes Theorem 2.1 in [6] to the case of a renewal sampling sequence , albeit at the cost of the slightly more restrictive conditions and .

Remark 3.4.

Condition (3.9) is satisfied, for example, for with and .

To see this, observe that for some

| (3.15) |

Hence,

| (3.16) |

The first sum in (3.16) converges since, as it was shown in the proof of Proposition 2.2, for all , and , if , it holds . Otherwise for , set such that .

For establishing the convergence of the second sum, observe that

| (3.17) |

4 Sample Autocovariance

In this section, we present a multivariate central limit theorem for the autocovariance and autocorrelation functions when the process is sampled at a renewal sequence. We start by considering the strictly stationary, mean zero process

| (4.1) |

As in the previous section, let be a sequence of random times defined by (1.2), and the sampled process for . Recall that for a mean zero process,

| (4.2) |

is a natural estimator for the autocovariance function.

In analogy to the proof of the asymptotic normality of the sample mean, we first show that, for the truncated sequence as in (3.3) and (3.2) with , the asymptotic normality can be proved. At this point, we need a series of lemmas that allows us to compute the -order cumulants of the processes and .

Part (a) in the lemma below generalizes expression (3.5) in Cohen and Lindner [6] to non-lattice times and presents a different and quicker proof.

Lemma 4.1.

Let , and be a Lévy process with expectation zero and finite fourth moment. Denote , , and . Then the following statements hold:

(a) For , we have for all

| (4.3) |

(b) Let additionally , then we have for all

Proof.

Since , , , and all have expectation zero, the order joint cumulant of is given by

| (4.4) |

see Proposition 4.2.2 in Giraitis et al. [9]. On the other hand,

cf. Definition 4.2.1 of Giraitis et al. [9]. Let , then it holds , and, since , we obtain which yields by Corollary 2.4 that is infinitely divisible with characteristic triplet , by Theorem 2.3 (b). This and the well-known fact yield

The latter together with (4) yields (a).

For (b) just observe that also such that with we obtain that also is infinitely divisible by Corollary 2.4. Similar argumentations as above give the demanded result. ∎

In the following lemma we give a similar expression as (4.1) when the deterministic times , and are replaced by random times.

Lemma 4.2.

Let be a Lévy process with expectation zero and finite fourth moment, be defined by (4.1), with , and the processes is defined by (1.3) with as in (1.2). Denote and , and let . Let , then

(a)

(b) If , then .

Proof.

(a) Due to the definition of it follows that . Conditioning on the random times yields, by the independence of and and Lemma 4.1 (a),

where A, B, C, and D correspond to the parts arising from the decomposition in (4.1). Then, by Fubini’s theorem,

Since for all , we obtain

Likewise

With the definition of , the assertion follows.

(b) Observe that, since , by independence of the sequence ,

which gives the result. ∎

From Lemma 4.2, the following proposition gives the expression of as needed in the upcoming central limit theorem.

Proposition 4.3.

Proof.

From Lemma 4.2 (a), since , and by the stationarity of , we have

which is (4.7). Equation (4.8) is an immediate consequence of Lemma 4.2 (b). For the proof of (4.9), by (4.7) and (4.8), it is enough to show that . To see this, observe that

The first of these summands is finite by (4.5) and the second is finite since, by using Cauchy-Schwarz’s inequality twice,

which is finite by (4.6). The same argument yields finiteness of the third summand, showing (4.9).

To see (4.10), observe that by the stationarity of , with ,

Since by (4.9), the latter converges to as by the dominated convergence theorem, which together with (4.7) and (4.8) finishes the proof of (4.10). ∎

Remark 4.4.

(a) If or , it is easy to see that for all . Hence, the second summand in (4.10) disappears.

(b) If we choose to be deterministic, i.e. for and some , it is easy to see that (4.5) and (4.6) are implied by assumptions (3.2) and (3.11) of Cohen and Lindner [6] to establish the asymptotic normality of the sample autocovariance of the moving average process sampled on a lattice. (4.5) then reduces to (3.10) of [6], which was shown to be implied by (3.2) of [6].

Remark 4.5.

The next proposition shows that similar results as obtained in Proposition 4.3 are valid for the truncated sequence .

Proposition 4.6.

Proof.

That (4.5) and (4.6) also hold for is clear since , as is . Since and as , the dominated convergence theorem shows (4.11) and (4.12). And (4.13) then follows from (4.11), (4.12), and (4.10) again by the dominated convergence theorem. ∎

Now, we can establish the multivariate asymptotic normality of the sample autocovariance and sample autocorrelation.

Theorem 4.7.

Let be a Lévy process with expectation zero and such that . Denote and . Let , suppose that , , and assume that (4.5) and (4.6) hold for all .

(b) If additionally

| (4.14) |

hold, and we denote by

the sample autocovariance, then we have for each

where as defined in (a).

(c) Let and for . Suppose that on a set of positive Lebesgue measure. Then, under the assumptions of (a), we have for each

where is given by

If additionally (4.14) is satisfied, then it also holds

Proof.

(a) Let be as in (3.3) and (3.2) with and for and . Define . Then is obviously strictly stationary and we have

where as in Proposition 4.6.

By the assumptions on and , we obtain, by Lemma 2.5 (c), , and so , by the Cauchy-Schwarz inequality. Therefore also for all .

Observe that is strongly mixing for each with for all , by Remark 1.8 (b) of Bradley [4], such that is exponentially decreasing. Hence, by Corollary 10.20 (c) of Bradley [4] it follows

By the Cramér-Wold theorem, we deduce that

Here , where is given by

with and as in Proposition 4.6.

Also by Proposition 4.6, , where Proposition 4.3 gives the form and finiteness of , the entries of . Henceforth, as , where .

By Proposition 6.3.9 of Brockwell and Davis [5], the claim will follow if we can show that

Since and , this will follow from Chebychef’s inequality if we can show that

But since

by Proposition 4.6, it remains only to show that

| (4.15) |

In doing so, denote and . Observe first that from Lemma 4.1 (b), similar to the proof of Lemma 4.2 (a), by conditioning on , , and , that for , we have

Further, as in the proof of Lemma 4.2 (b), it follows that

Denoting

we hence have

Next, observe that as in the proof of Proposition 4.6, since , for all ,

By stationarity, we obtain for

Applying Lebesgue’s dominated convergence theorem once then gives

and applying it a second time gives

which is (4.15). This finishes the proof of (a).

(b) This follows if we can show that in probability for and . The latter can be done in exactly the same way as in the proof of Proposition 7.3.4 in Brockwell and Davis [5] with replaced by in connection with the observation that, by Theorem 3.2, converges in distribution to a normal random variable as , and hence must converges to in probability as .

(c) Follows readily as in the proof of Theorem 7.2.1 in Brockwell and Davis [5]. ∎

Remark 4.8.

(a) Due to the form of , there seems to be no simplification for possible. Also observe that in general depends on as seen in Theorem 3.5 (c) of Cohen and Lindner [6].

(b) Part (a) of Theorem 4.7 in particular applies if for some and which can be seen by Remark 4.5.

(c) Similarly, part (b) of Theorem 4.7 applies if for some and as shown in Remark 3.4.

5 An Application to Parameter Estimation of the Ornstein-Uhlenbeck Process

In this section, we present a parameter estimation of a Lévy driven Ornstein-Uhlenbeck (OU) process sampled at a Poisson process. An OU process is a continuous time moving average process with kernel function and mean reverting parameter . This yields , where is a Lévy process with zero mean and . We define , , where is given by (1.2) with a sequence of i.i.d. random variables independent of and such that , .

By Proposition 2.1, is strictly stationary, , and . Then we obtain, by Proposition 3.1,

as the autocovariance function of the process . Further , and the autocorrelation function . In particular, and we can determine the mean reverting parameter by

| (5.1) |

We define an estimator for , assuming being a known parameter of the distribution of , as , where with . We can then give the following theorem.

Theorem 5.1.

Let be a Lévy process with mean zero, and , and , be defined as in (1.2) such that for some , and an OU process with parameter . Then

where

| (5.2) |

Proof.

As usual, , , and , , , and hence . Observe that , since is exponentially distributed and it has positive support. Further, is obvious as is , and, since clearly for some and , it follows, by Remark 4.5, that (4.5) and (4.6) are satisfied. Therefore, by Theorem 4.7 (c), we have

where

with for given as in Theorem 4.7 (a).

Thus, under our assumptions on the distribution of , an easy but tedious calculation yields that is given by (5.2).

To complete the proof, define such that and the delta-method, cf. Proposition 6.4.3 in Brockwell and Davis [5], yields

where . ∎

Next, we consider the case when the parameter of is unknown. Since, in addition to the observations , we also have the observation times , we also observe the waiting times , , and hence can define , which by the strong law of large numbers is a strongly consistent estimator for , since .

By (5.1), this suggests the estimator . Since and are consistent estimators, so is . The asymptotic normality of is given in the following theorem.

Theorem 5.2.

Proof.

For define and . Then the sequences and are both strictly stationary by Proposition 2.1 and the latter is also strongly mixing with exponentially decreasing mixing coefficients by Proposition 2.2.

Proceeding exactly as in the proof of Theorem 4.7, i.e. establishing first a central limit theorem for the truncated sequences and then letting tend to infinity, shows that

where

An easy but tedious calculation then shows that

with , , and as in Theorem 4.7 (a).

To complete, we define such that

Henceforth, by the delta-method, cf. Proposition 6.4.3 in Brockwell and Davis [5], we obtain

where by a straightforward calculation,

and the result follows. ∎

Remark 5.3.

Note that the shrinking phenomenon observed in the asymptotic variance of the estimator with respect to the asymptotic variance of depends on the non zero asymptotic covariance between the sample autocovariance and the estimator .

Next, we compare our results to an equidistant sampling method, more precisely to the one of Cohen and Lindner [6]. Sampling at equidistant times for , leads to an autocovariance function

from which we conclude that and hence

| (5.3) |

For an estimator of , i.e. for , where , , by Theorem 3.5 of Cohen and Lindner [6] we have

| (5.4) |

where

with given as in Proposition 3.1 of Cohen and Lindner [6].

Knowing this, we suggest as an estimator of given in (5.3) . A simple calculation of for the specific kernel and the specific autocovariance function, and an application of the delta-method then leads to

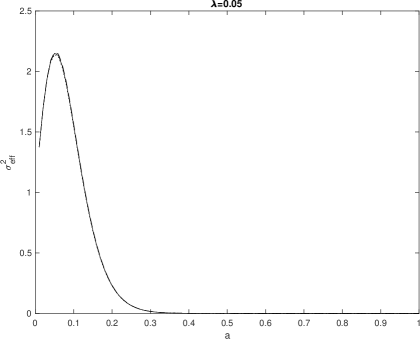

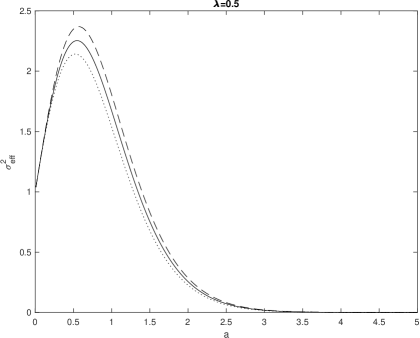

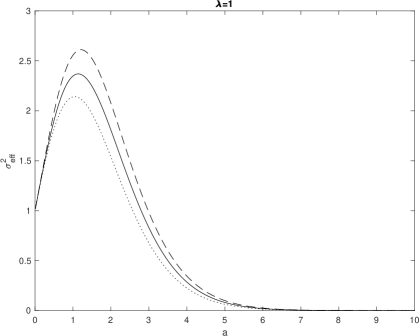

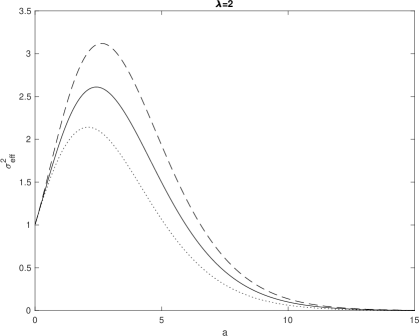

For comparing the asymptotic variances of the estimators and , we select different time scales by choosing . We remind that in the renewal sampling case the expected waiting times between two sample times and is given by . Then the asymptotic relative efficiency is given by

where given as in (5.2).

We plot in Figure 1 the relative efficiency with respect to the mean reverting parameter . The dotted line belongs to , the solid line to and the dashed line to .

The estimator is more efficient than as tends to infinity. Table 1 shows, depending on and , the smallest value of for which . For values of less than , the estimator based on an equidistant sampling is more efficient than unless the sampling frequency is greater than .

We see that the non-equidistant sampling performs worse as the kurtosis of the driving Lévy process increases. The best scenario across all time scales is observed for which corresponds to the Brownian motion case.

6 Conclusion

In this paper, we studied distributional limits for the sample mean and the sample autocovariance and autocorrelation functions of a Lévy driven continuous time moving average process. We achieved these results by assuming slightly more restrictive conditions with respect to the work of Cohen and Lindner [6] and gave an application of the theory in estimating the mean reverting parameter of a Lévy driven OU process.

Of particular interest is investigating the asymptotic behavior of the sample moments when the renewal sampling is not independent of the driving Lévy process which we hope to address in future work.

Acknowledgment

We would like to deeply thank Alexander Lindner for many hours of discussion and his helpful comments and remarks.

References

- [1] Barndorff-Nielsen, O.E. and Shephard, N. (2001). Modelling by Lévy processes for financial econometrics. In Lévy Processes: Theory and Applications, ed. O.E. Barndorff-Nielsen, T. Mikosch, S. Resnick. Birkhäuser, Boston, 283–318.

- [2] Barndorff-Nielsen, O.E. and Schmiegel, J. (2007). Ambit processes; with applications to turbulence and tumour growth. In Stochastic Analysis and Applications: Abel Symposium 2005, ed. F. E. Benth et al. Springer, Berlin, 93–124.

- [3] Bradley, R.C. (1990). On -mixing except on small sets. Pacific J. Math. 146, No. 2, 217–226.

- [4] Bradley, R.C. (2007). Introduction to Strong Mixing Conditions, Volume 1, Kendrick Press, Utah.

- [5] Brockwell, P.J. and Davis, R.A. (2006). Time Series: Theory and Methods, 2nd ed., Springer, New York.

- [6] Cohen, S. and Lindner, A. (2013). A central limit theorem for the sample autocorrelations of a Lévy driven continuous time moving average process. J. Stat. Plan. Inference 143, 1295–1306.

- [7] Davis, R.A. and Mikosch, T. (1998). The sample autocorrelation of heavy-tailed processes with applications to ARCH. Ann. Stat. 26 (5), 2049–2080.

- [8] Drapatz, M. (2017). Limit theorems for the sample mean and sample autocovariances of continuous time moving averages driven by heavy-tailed Lévy noise. ALEA, Lat. Am. J. Probab. Math. Stat. 14, 403–426.

- [9] Giraitis, L., Koul, H.L., and Surgailis, D. (2012). Large Sample Inference for Long Memory Processes, Imperial College Press, London.

- [10] Hannan, E.J. (1976). The asymptotic distribution of serial covariances. Ann. Stat. 4 (2), 396–399.

- [11] Rajput, B.S. and Rosinski, J. (1989). Spectral representations of infinitely divisible processes. Probab. Theory Related Fields 3, 451–487.

- [12] Sato, K. (2013). Lévy Processes and Infinitely Divisible Distributions, Cambridge University Press, Cambridge.

- [13] Spangenberg, F. (2015). Limit theorems for the sample autocovariance of a continuous-time moving average process with long memory. ArXiv Mathematics e-prints, arXiv:1206.0982v1.