Renewal Monte Carlo:

Renewal theory based reinforcement learning

Abstract

In this paper, we present an online reinforcement learning algorithm, called Renewal Monte Carlo (RMC), for infinite horizon Markov decision processes with a designated start state. RMC is a Monte Carlo algorithm and retains the advantages of Monte Carlo methods including low bias, simplicity, and ease of implementation while, at the same time, circumvents their key drawbacks of high variance and delayed (end of episode) updates. The key ideas behind RMC are as follows. First, under any reasonable policy, the reward process is ergodic. So, by renewal theory, the performance of a policy is equal to the ratio of expected discounted reward to the expected discounted time over a regenerative cycle. Second, by carefully examining the expression for performance gradient, we propose a stochastic approximation algorithm that only requires estimates of the expected discounted reward and discounted time over a regenerative cycle and their gradients. We propose two unbiased estimators for evaluating performance gradients—a likelihood ratio based estimator and a simultaneous perturbation based estimator—and show that for both estimators, RMC converges to a locally optimal policy. We generalize the RMC algorithm to post-decision state models and also present a variant that converges faster to an approximately optimal policy. We conclude by presenting numerical experiments on a randomly generated MDP, event-triggered communication, and inventory management.

Index Terms:

Reinforcement learning, Markov decision processes, renewal theory, Monte Carlo methods, policy gradient, stochastic approximationI Introduction

In recent years, reinforcement learning [1, 2, 3, 4] has emerged as a leading framework to learn how to act optimally in unknown environments. Policy gradient methods [5, 6, 7, 8, 9, 10] have played a prominent role in the success of reinforcement learning. Such methods have two critical components: policy evaluation and policy improvement. In policy evaluation step, the performance of a parameterized policy is evaluated while in the policy improvement step, the policy parameters are updated using stochastic gradient ascent.

Policy gradient methods may be broadly classified as Monte Carlo methods and temporal difference methods. In Monte Carlo methods, performance of a policy is estimated using the discounted return of a single sample path; in temporal difference methods, the value(-action) function is guessed and this guess is iteratively improved using temporal differences. Monte Carlo methods are attractive because they have zero bias, are simple and easy to implement, and work for both discounted and average reward setups as well as for models with continuous state and action spaces. However, they suffer from various drawbacks. First, they have a high variance because a single sample path is used to estimate performance. Second, they are not asymptotically optimal for infinite horizon models because it is effectively assumed that the model is episodic; in infinite horizon models, the trajectory is arbitrarily truncated to treat the model as an episodic model. Third, the policy improvement step cannot be carried out in tandem with policy evaluation. One must wait until the end of the episode to estimate the performance and only then can the policy parameters be updated. It is for these reasons that Monte Carlo methods are largely ignored in the literature on policy gradient methods, which almost exclusively focuses on temporal difference methods such as actor-critic with eligibility traces [3].

In this paper, we propose a Monte Carlo method—which we call Renewal Monte Carlo (RMC)—for infinite horizon Markov decision processes with designated start state. Like Monte Carlo, RMC has low bias, is simple and easy to implement, and works for models with continuous state and action spaces. At the same time, it does not suffer from the drawbacks of typical Monte Carlo methods. RMC is a low-variance online algorithm that works for infinite horizon discounted and average reward setups. One doesn’t have to wait until the end of the episode to carry out the policy improvement step; it can be carried out whenever the system visits the start state (or a neighborhood of it).

Although renewal theory is commonly used to estimate performance of stochastic systems in the simulation optimization community [11, 12], those methods assume that the probability law of the primitive random variables and its weak derivate are known, which is not the case in reinforcement learning. Renewal theory is also commonly used in the engineering literature on queuing theory and systems and control for Markov decision processes (MDPs) with average reward criteria and a known system model. There is some prior work on using renewal theory for reinforcement learning [13, 14], where renewal theory based estimators for the average return and differential value function for average reward MDPs is developed. In RMC, renewal theory is used in a different manner for discounted reward MDPs (and the results generalize to average cost MDPs).

II RMC Algorithm

Consider a Markov decision process (MDP) with state and action . The system starts in an initial state and at time :

-

1.

there is a controlled transition from to according to a transition kernel ;

-

2.

a per-step reward is received.

Future is discounted at a rate .

A (time-homogeneous and Markov) policy maps the current state to a distribution on actions, i.e., . We use to denote . The performance of a policy is given by

| (1) |

We are interested in identifying an optimal policy, i.e., a policy that maximizes the performance. When and are Borel spaces, we assume that the model satisfies the standard conditions under which time-homogeneous Markov policies are optimal [15]. In the sequel, we present a sample path based online learning algorithm, which we call Renewal Monte Carlo (RMC), which identifies a locally optimal policy within the class of parameterized policies.

Suppose policies are parameterized by a closed and convex subset of the Euclidean space. For example, could be the weight vector in a Gibbs soft-max policy, or the weights of a deep neural network, or the thresholds in a control limit policy, and so on. Given , we use to denote the policy parameterized by and to denote . We assume that for all policies , , the designated start state is positive recurrent.

The typical approach for policy gradient based reinforcement learning is to start with an initial guess and iteratively update it using stochastic gradient ascent. In particular, let be an unbiased estimator of , then update

| (2) |

where denotes the projection of onto and is the sequence of learning rates that satisfies the standard assumptions of

| (3) |

Under mild technical conditions [16], the above iteration converges to a that is locally optimal, i.e., . In RMC, we approximate by a Renewal theory based estimator as explained below.

Let denote the stopping time when the system returns to the start state for the -th time. In particular, let and for define

We call the sequence of from to as the -th regenerative cycle. Let and denote the total discounted reward and total discounted time of the -th regenerative cycle, i.e.,

| (4) |

where . By the strong Markov property, and are i.i.d. sequences. Let and denote and , respectively. Define

| (5) |

where is a large number. Then, and are unbiased and asymptotically consistent estimators of and .

From ideas similar to standard Renewal theory [17], we have the following.

Proposition 1 (Renewal Relationship)

The performance of policy is given by:

| (6) |

□

Proof

For ease of notation, define

Using the formula for geometric series, we get that . Hence,

| (7) |

Differentiating both sides of Equation (6) with respect to , we get that

| (9) |

Therefore, instead of using stochastic gradient ascent to find the maximum of , we can use stochastic approximation to find the root of . In particular, let be an unbiased estimator of . We then use the update

| (10) |

where satisfies the standard conditions on learning rates (3). The above iteration converges to a locally optimal policy. Specifically, we have the following.

Theorem 1

Let , , and be unbiased estimators of , , , and , respectively such that and .111The notation means that the random variables and are independent. Then,

| (11) |

is an unbiased estimator of and the sequence generated by (10) converges almost surely and

□

Proof

In the remainder of this section, we present two methods for estimating the gradients of and . The first is a likelihood ratio based gradient estimator which works when the policy is differentiable with respect to the policy parameters. The second is a simultaneous perturbation based gradient estimator that uses finite differences, which is useful when the policy is not differentiable with respect to the policy parameters.

II-A Likelihood ratio based gradient based estimator

One approach to estimate the performance gradient is to use likelihood radio based estimates [18, 12, 19]. Suppose the policy is differentiable with respect to . For any time , define the likelihood function

| (12) |

and for , define

| (13) |

In this notation and . Then, define the following estimators for and :

| (14) | ||||

| (15) |

where is a large number.

Proposition 2

and defined above are unbiased and asymptotically consistent estimators of and . □

Proof

Let denote the probability induced on the sample paths when the system is following policy . For , let denote the sample path for the -th regenerative cycle until time . Then,

Therefore,

| (16) |

Note that can be written as:

Using the log derivative trick,222Log-derivative trick: For any distribution and any function , we get

| (17) |

where follows from (16), follows from changing the order of summations, and follows from the definition of in (13). is an unbiased and asymptotically consistent estimator of the right hand side of the first equation in (17). The result for follows from a similar argument. ■

To satisfy the independence condition of Theorem 1, we use two independent sample paths: one to estimate and and the other to estimate and . The complete algorithm in shown in Algorithm 1. An immediate consequence of Theorem 1 is the following.

Corollary 1

The sequence generated by Algorithm 1 converges to a local optimal. □

Remark 1

Remark 2

Remark 3

It has been reported in the literature [22] that using a biased estimate of the gradient given by:

| (18) |

(and a similar expression for ) leads to faster convergence. We call this variant RMC with biased gradients and, in our experiments, found that it does converge faster than RMC. □

II-B Simultaneous perturbation based gradient estimator

Another approach to estimate performance gradient is to use simultaneous perturbation based estimates[23, 24, 25, 26]. The general one-sided form of such estimates is

where is a random variable with the same dimension as and is a small constant. The expression for is similar. When , the above method corresponds to simultaneous perturbation stochastic approximation (SPSA) [23, 24]; when , the above method corresponds to smoothed function stochastic approximation (SFSA) [25, 26].

Substituting the above estimates in (11) and simplifying, we get

The complete algorithm in shown in Algorithm 2. Since and are estimated from separate sample paths, defined above is an unbiased estimator of . Then, an immediate consequence of Theorem 1 is the following.

Corollary 2

The sequence generated by Algorithm 2 converges to a local optimal. □

III RMC for Post-Decision State Model

In many models, the state dynamics can be split into two parts: a controlled evolution followed by an uncontrolled evolution. For example, many continuous state models have dynamics of the form

where is an independent noise process. For other examples, see the inventory control and event-triggered communication models in Sec V. Such models can be written in terms of a post-decision state model described below.

Consider a post-decision state MDP with pre-decision state , post-decision state , action . The system starts at an initial state and at time :

-

1.

there is a controlled transition from to according to a transition kernel ;

-

2.

there is an uncontrolled transition from to according to a transition kernel ;

-

3.

a per-step reward is received.

Future is discounted at a rate .

Remark 4

As in Sec II, we choose a (time-homogeneous and Markov) policy that maps the current pre-decision state to a distribution on actions, i.e., . We use to denote .

The performance when the system starts in post-decision state and follows policy is given by

| (19) |

As before, we are interested in identifying an optimal policy, i.e., a policy that maximizes the performance. When and are Borel spaces, we assume that the model satisfies the standard conditions under which time-homogeneous Markov policies are optimal [15]. Let denote the stopping times such that and for ,

The slightly unusual definition (using rather than the more natural ) is to ensure that the formulas for and used in Sec. II remain valid for the post-decision state model as well. Thus, using arguments similar to Sec. II, we can show that both variants of RMC presented in Sec. II converge to a locally optimal parameter for the post-decision state model as well.

IV Approximate RMC

In this section, we present an approximate version of RMC (for the basic model of Sec. II). Suppose that the state and action spaces and are separable metric spaces (with metrics and ).

Given an approximation constant , let denote the ball of radius centered around . Given a policy , let denote the stopping times for successive visits to , i.e., and for ,

Define and as in (4) and let and denote the expected values of and , respectively. Define

Theorem 2

Given a policy , let denote the value function and (which is always less than ). Suppose the following condition is satisfied:

-

(C)

The value function is locally Lipschitz in , i.e., there exists a such that for any ,

Then

| (20) |

□

Proof

We follow an argument similar to Proposition 1.

| (21) |

where uses the strong Markov property. Since is locally Lipschitz with constant and , we have that

Substituting the above in (21) gives

Substituting and rearranging the terms, we get

The other direction can also be proved using a similar argument. The second inequality in (20) follows from and . ■

Theorem 2 implies that we can find an approximately optimal policy by identifying policy parameters that minimize . To do so, we can appropriately modify both variants of RMC defined in Sec. II to declare a renewal whenever the state lies in .

For specific models, it may be possible to verify that the value function is locally Lipschitz (see Sec. V-C for an example). However, we are not aware of general conditions that guarantee local Lipschitz continuity of value functions. It is possible to identify sufficient conditions that guarantee global Lipschitz continuity of value functions (see [29, Theorem 4.1], [30, Lemma 1, Theorem 1], [31, Lemma 1]). We state these conditions below.

Proposition 3

Let denote the value function for any policy . Suppose the model satisfies the following conditions:

-

1.

The transition kernel is Lipschitz, i.e., there exists a constant such that for all and ,

where is the Kantorovich metric (also called Kantorovich-Monge-Rubinstein metric or Wasserstein distance) between probability measures.

-

2.

The per-step reward is Lipschitz, i.e., there exists a constant such that for all and ,

In addition, suppose the policy satisfies the following:

-

3.

The policy is Lipschitz, i.e., there exists a constant such that for any ,

-

4.

.

-

5.

The value function exists and is finite.

Then, is Lipschitz. In particular, for any ,

where

□

V Numerical Experiments

We conduct three experiments to evaluate the performance of RMC: a randomly generated MDP, event-triggered communication, and inventory management.

V-A Randomized MDP (GARNET)

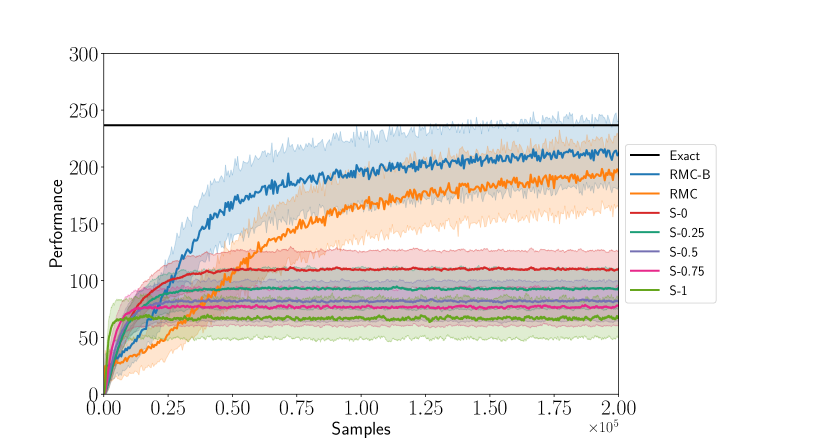

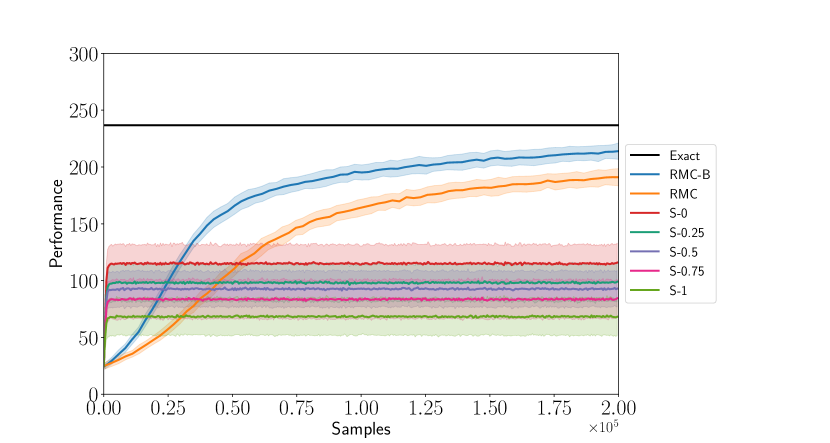

In this experiment, we study a randomly generated model [32], which is an MDP with states, actions, and a branching factor of (which means that each row of all transition matrices has non-zero elements, chosen and normalized to add to ). For each state-action pair, with probability , the reward is chosen , and with probability , the reward is . Future is discounted by a factor of . The first state is chosen as start state. The policy is a Gibbs soft-max distribution parameterized by (states actions) parameters, where each parameter belongs to the interval . The temperature of the Gibbs distribution is kept constant and equal to .

We compare the performance of RMC, RMC with biased gradient (denoted by RMC-B, see Remark 2), and actor critic with eligibility traces for the critic [3] (which we refer to as SARSA- and abbreviate as S- in the plots), with . For both the RMC algorithms, we use the same runs to estimate the gradients (see Remark 2 in Sec. II). Each algorithm333For all algorithms, the learning rate is chosen using ADAM [33] with default hyper-parameters and the parameter of ADAM equal to for RMC, RMC-B, and the actor in SARSA- and the learning rate is equal to for the critic in SARSA-. For RMC and RMC-B, the policy parameters are updated after renewals. is run times and the mean and standard deviation of the performance (as estimated by the algorithms themselves) is shown in Fig. 1(a). The performance of the corresponding policy evaluated by Monte-Carlo evaluation over a horizon of steps and averaged over runs is shown in Fig. 1(b). The optimal performance computed using value iteration is also shown.

The results show that SARSA- learns faster (this is expected because the critic is keeping track of the entire value function) but has higher variance and gets stuck in a local minima. On the other hand, RMC and RMC-B learn slower but have a low bias and do not get stuck in a local minima. The same qualitative behavior was observed for other randomly generated models. Policy gradient algorithms only guarantee convergence to a local optimum. We are not sure why RMC and SARSA differ in which local minima they converge to. Also, it was observed that RMC-B (which is RMC with biased evaluation of the gradient) learns faster than RMC.

V-B Event-Triggered Communication

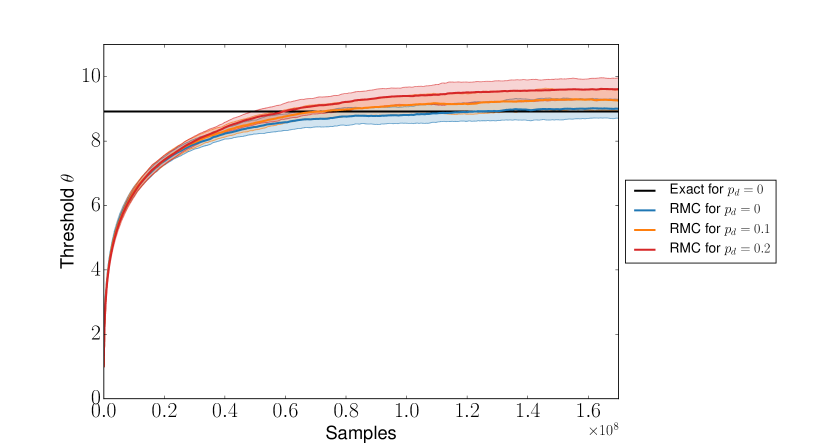

In this experiment, we study an event-triggered communication problem that arises in networked control systems [34, 35]. A transmitter observes a first-order autoregressive process , i.e., , where , and is an i.i.d. process. At each time, the transmitter uses an event-triggered policy (explained below) to determine whether to transmit or not (denoted by and , respectively). Transmission takes place over an i.i.d. erasure channel with erasure probability . Let and denote the “error” between the source realization and it’s reconstruction at a receiver. It can be shown that and evolve as follows [34, 35]: when , ; when , if the transmission is successful (w.p. ) and if the transmission is not successful (w.p. ); and . Note that this is a post-decision state model, where the post-decision state resets to zero after every successful transmission.444Had we used the standard MDP model instead of the post-decision state model, this restart would not have always resulted in a renewal.

The per-step cost has two components: a communication cost of , where and an estimation error . The objective is to minimize the expected discounted cost.

An event-triggered policy is a threshold policy that chooses whenever , where is a design choice. Under certain conditions, such an event-triggered policy is known to be optimal [34, 35]. When the system model is known, algorithms to compute the optimal are presented in [36, 37]. In this section, we use RMC to identify the optimal policy when the model parameters are not known.

In our experiment we consider an event-triggered model with , , , , , and use simultaneous perturbation variant of RMC555An event-triggered policy is a parametric policy but is not differentiable in . Therefore, the likelihood ratio method cannot be used to estimate performance gradient. to identify . We run the algorithm 100 times and the result for different choices of are shown in Fig. 2.666We choose the learning rate using ADAM with default hyper-parameters and the parameter of ADAM equal to 0.01. We choose , and in Algorithm 2. For , the optimal threshold computed using [37] is also shown. The results show that RMC converges relatively quickly and has low bias across multiple runs.

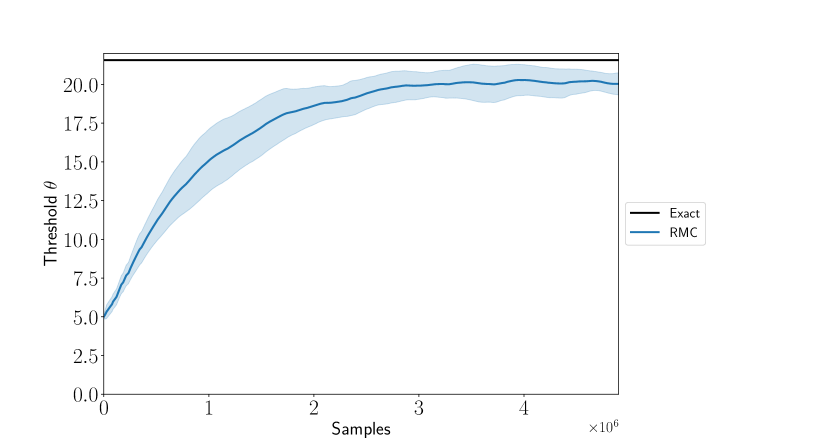

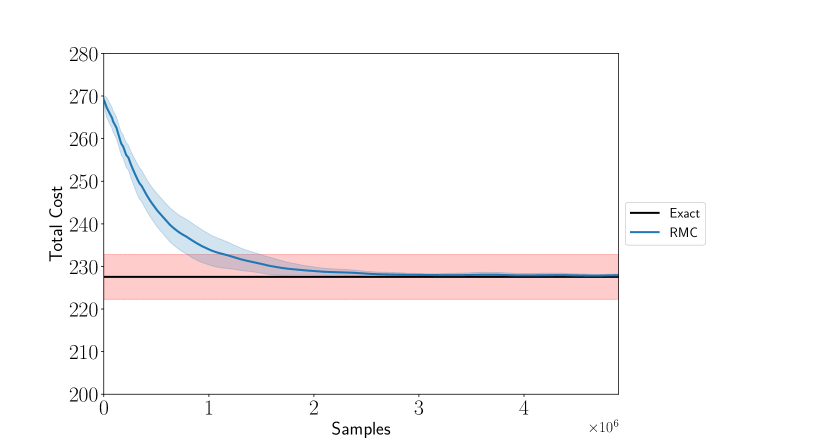

V-C Inventory Control

In this experiment, we study an inventory management problem that arises in operations research [38, 39]. Let denote the volume of goods stored in a warehouse, denote the amount of goods ordered, and denotes the demand. The state evolves according to .

We work with the normalized cost function:

where is the procurement cost, is the holding cost, and is the backlog cost (see [40, Chapter 13] for details).

It is known that there exists a threshold such that the optimal policy is a base stock policy with threshold (i.e., whenever the current stock level falls below , one orders up to ). Furthermore, for , we have that [40, Sec 13.2]

| (22) |

So, for , the value function is locally Lipschitz, with

So, we can use approximate RMC to learn the optimal policy.

In our experiments, we consider an inventory management model with , , , with , start state , discount factor , and use simultaneous perturbation variant of approximate RMC to identify . We run the algorithm times and the result is shown in Fig. 3.777We choose the learning rate using ADAM with default hyper-parameters and the parameter of ADAM equal to 0.25. We choose , , and in Algorithm 2 and choose for approximate RMC. We bound the states within . The optimal threshold and performance computed using [40, Sec 13.2]888For demand, the optimal threshold is (see [40, Sec 13.2]) is also shown. The result shows that RMC converges to an approximately optimal parameter value with total cost within the bound predicted in Theorem 2.

VI Conclusions

We present a renewal theory based reinforcement learning algorithm called Renewal Monte Carlo. RMC retains the key advantages of Monte Carlo methods and has low bias, is simple and easy to implement, and works for models with continuous state and action spaces. In addition, due to the averaging over multiple renewals, RMC has low variance. We generalized the RMC algorithm to post-decision state models and also presented a variant that converges faster to an approximately optimal policy, where the renewal state is replaced by a renewal set. The error in using such an approximation is bounded by the size of the renewal set.

In certain models, one is interested in the peformance at a reference state that is not the start state. In such models, we can start with an arbitrary policy and ignore the trajectory until the reference state is visited for the first time and use RMC from that time onwards (assuming that the reference state is the new start state).

The results presented in this paper also apply to average reward models where the objective is to maximize

| (23) |

Let the stopping times be defined as before. Define the total reward and duration of the -th regenerative cycle as

Let and denote the expected values of and under policy . Then from standard renewal theory we have that the performance is equal to and, therefore , where is defined as in (9). We can use both variants of RMC prosented in Sec. II to obtain estimates of and use these to update the policy parameters using (10).

Acknowledgment

The authors are grateful to Joelle Pineau for useful feedback and for suggesting the idea of approximate RMC.

References

- [1] D. Bertsekas and J. Tsitsiklis, Neuro-dynamic Programming, ser. Anthropological Field Studies. Athena Scientific, 1996.

- [2] L. P. Kaelbling, M. L. Littman, and A. W. Moore, “Reinforcement learning: A survey,” Journal of Artificial Intelligence Research, vol. 4, pp. 237–285, 1996.

- [3] R. S. Sutton and A. G. Barto, Reinforcement learning: An introduction. MIT Press, 1998.

- [4] C. Szepesvári, Algorithms for reinforcement learning. Morgan & Claypool Publishers, 2010.

- [5] R. S. Sutton, D. A. McAllester, S. P. Singh, and Y. Mansour, “Policy gradient methods for reinforcement learning with function approximation,” in Advances in Neural Information Processing Systems, Nov. 2000, pp. 1057–1063.

- [6] S. M. Kakade, “A natural policy gradient,” in Advances in Neural Information Processing Systems, Dec. 2002, pp. 1531–1538.

- [7] V. R. Konda and J. N. Tsitsiklis, “On actor-critic algorithms,” SIAM Journal on Control and Optimization, vol. 42, no. 4, pp. 1143–1166, 2003.

- [8] J. Schulman, S. Levine, P. Abbeel, M. Jordan, and P. Moritz, “Trust region policy optimization,” in Proceedings of the 32nd International Conference on Machine Learning (ICML-15), June 2015, pp. 1889–1897.

- [9] J. Schulman, F. Wolski, P. Dhariwal, A. Radford, and O. Klimov, “Proximal policy optimization algorithms,” arXiv preprint arXiv:1707.06347, 2017.

- [10] D. Silver, J. Schrittwieser, K. Simonyan, I. Antonoglou, A. Huang, A. Guez, T. Hubert, L. Baker, M. Lai, A. Bolton, Y. others Chen, T. Lillicrap, F. Hui, L. Sifre, G. van den Driessche, T. Graepel, and D. Hassabis, “Mastering the game of go without human knowledge,” Nature, vol. 550, no. 7676, p. 354, 2017.

- [11] P. Glynn, “Optimization of stochastic systems,” in Proc. Winter Simulation Conference, Dec. 1986, pp. 52–59.

- [12] ——, “Likelihood ratio gradient estimation for stochastic systems,” Communications of the ACM, vol. 33, pp. 75–84, 1990.

- [13] P. Marbach and J. N. Tsitsiklis, “Simulation-based optimization of Markov reward processes,” IEEE Trans. Autom. Control, vol. 46, no. 2, pp. 191–209, Feb 2001.

- [14] ——, “Approximate gradient methods in policy-space optimization of Markov reward processes,,” Discrete Event Dynamical Systems, vol. 13, no. 2, pp. 111–148, 2003.

- [15] O. Hernández-Lerma and J. B. Lasserre, Discrete-time Markov Control Processes: Basic Optimality Criteria. Springer Science & Business Media, 1996, vol. 30.

- [16] V. Borkar, Stochastic Approximation: A Dynamical Systems Viewpoint. Cambridge University Press, 2008.

- [17] W. Feller, An Introduction to Probability Theory and its Applications. John Wiley and Sons, 1966, vol. 1.

- [18] R. Y. Rubinstein, “Sensitivity analysis and performance extrapolation for computer simulation models,” Operations Research, vol. 37, no. 1, pp. 72–81, 1989.

- [19] R. J. Williams, “Simple statistical gradient-following algorithms for connectionist reinforcement learning,” Machine learning, vol. 8, no. 3-4, pp. 229–256, 1992.

- [20] E. Greensmith, P. L. Bartlett, and J. Baxter, “Variance reduction techniques for gradient estimates in reinforcement learning,” Journal of Machine Learning Research, vol. 5, no. Nov, pp. 1471–1530, 2004.

- [21] J. Peters and S. Schaal, “Policy gradient methods for robotics,” in International Conference on Intelligent Robots and Systems, 2006 IEEE/RSJ. IEEE, Oct. 2006, pp. 2219–2225.

- [22] P. Thomas, “Bias in natural actor-critic algorithms,” in International Conference on Machine Learning, June 2014, pp. 441–448.

- [23] J. C. Spall, “Multivariate stochastic approximation using a simultaneous perturbation gradient approximation,” IEEE Trans. Autom. Control, vol. 37, no. 3, pp. 332–341, 1992.

- [24] J. L. Maryak and D. C. Chin, “Global random optimization by simultaneous perturbation stochastic approximation,” IEEE Trans. Autom. Control, vol. 53, no. 3, pp. 780–783, Apr. 2008.

- [25] V. Katkovnik and Y. Kulchitsky, “Convergence of a class of random search algorithms.” Automation and Remote Control, vol. 33, no. 8, pp. 1321–1326, 1972.

- [26] S. Bhatnagar, H. Prasad, and L. Prashanth, Stochastic Recursive Algorithms for Optimization: Simultaneous Perturbation Methods. Springer, 2013, vol. 434.

- [27] B. Van Roy, D. P. Bertsekas, Y. Lee, and J. N. Tsitsiklis, “A neuro-dynamic programming approach to retailer inventory management,” in 36th IEEE Conference on Decision and Control, 1997, vol. 4, Dec. 1997, pp. 4052–4057.

- [28] W. B. Powell, Approximate Dynamic Programming: Solving the Curses of Dimensionality, 2nd ed. John Wiley & Sons, 2011.

- [29] K. Hinderer, “Lipschitz continuity of value functions in Markovian decision processes,” Mathematical Methods of Operations Research, vol. 62, no. 1, pp. 3–22, Sep 2005.

- [30] E. Rachelson and M. G. Lagoudakis, “On the locality of action domination in sequential decision making,” in 11th International Symposium on Artificial Intelligence and Mathematics (ISIAM 2010), Fort Lauderdale, US, Jan. 2010, pp. pp. 1–8.

- [31] M. Pirotta, M. Restelli, and L. Bascetta, “Policy gradient in Lipschitz Markov decision processes,” Machine Learning, vol. 100, no. 2, pp. 255–283, Sep 2015.

- [32] S. Bhatnagar, R. Sutton, M. Ghavamzadeh, and M. Lee, “Natural actor-critic algorithms,” Department of Computing Science, University of Alberta, Canada, Tech. Rep., 2009.

- [33] D. Kingma and J. Ba, “Adam: A method for stochastic optimization,” arXiv preprint arXiv:1412.6980, 2014.

- [34] G. M. Lipsa and N. Martins, “Remote state estimation with communication costs for first-order LTI systems,” IEEE Trans. Autom. Control, vol. 56, no. 9, pp. 2013–2025, Sep. 2011.

- [35] J. Chakravorty, J. Subramanian, and A. Mahajan, “Stochastic approximation based methods for computing the optimal thresholds in remote-state estimation with packet drops,” in Proc. American Control Conference, Seattle, WA, May 2017, pp. 462–467.

- [36] Y. Xu and J. P. Hespanha, “Optimal communication logics in networked control systems,” in 43rd IEEE Conference on Decision and Control, Dec. 2004, pp. 3527–3532.

- [37] J. Chakravorty and A. Mahajan, “Fundamental limits of remote estimation of Markov processes under communication constraints,” IEEE Trans. Autom. Control, vol. 62, no. 3, pp. 1109–1124, Mar. 2017.

- [38] K. J. Arrow, T. Harris, and J. Marschak, “Optimal inventory policy,” Econometrica: Journal of the Econometric Society, pp. 250–272, 1951.

- [39] R. Bellman, I. Glicksberg, and O. Gross, “On the optimal inventory equation,” Management Science, vol. 2, no. 1, pp. 83–104, 1955.

- [40] P. Whittle, Optimization Over Time: Dynamic Programming and Optimal Control. John Wiley and Sons, Ltd., 1982.