High Dimensional Causal Discovery Under Non-Gaussianity

Abstract.

We consider graphical models based on a recursive system of linear structural equations. This implies that there is an ordering, , of the variables such that each observed variable is a linear function of a variable specific error term and the other observed variables with . The causal relationships, i.e., which other variables the linear functions depend on, can be described using a directed graph. It has been previously shown that when the variable specific error terms are non-Gaussian, the exact causal graph, as opposed to a Markov equivalence class, can be consistently estimated from observational data. We propose an algorithm that yields consistent estimates of the graph also in high-dimensional settings in which the number of variables may grow at a faster rate than the number of observations, but in which the underlying causal structure features suitable sparsity; specifically, the maximum in-degree of the graph is controlled. Our theoretical analysis is couched in the setting of log-concave error distributions.

1. Introduction

Prior work shows the possibility of causal discovery with observational data in the framework of linear structural equation models with non-Gaussian errors. However, existing methods for estimation of the causal structure are applicable only in low-dimensional settings, in which the number of variables, , is small compared to the sample size, . In this paper, we develop a method which, given suitable sparsity, recovers the exact causal structure consistently in high-dimensional regimes where grows along with . Careful considerations of computational aspects make our method a practical and statistically sound exploratory tool for the intended high-dimensional settings.

Let be multivariate data from an observational study, specifically, the observations form an independent, identically distributed sample. We encode the causal structure generating dependences in the underlying -variate joint distribution by a graph with vertex set . Each node, , corresponds to an observed variable in , and each directed edge, , indicates that has a direct causal effect on . Thus, positing causal structure is equivalent to selecting a graph. We will only consider directed acyclic graphs (DAGs), directed graphs which do not contain directed cycles. Given the correspondence between a node and the random variable , we will at times let stand in for ; for instance, when stating stochastic independence relations.

Discovery of causal structure from observational data is difficult because of the super-exponential set of possible models, some of which may be indistinguishable from others. Despite this difficulty, many methods for causal discovery have been developed and have seen fruitful applications; see the recent review of Drton and Maathuis, (2017). In particular, the celebrated PC algorithm (Spirtes et al.,, 2000) is a constraint-based method which first infers a set of conditional independence relationships and then identifies the associated Markov equivalence class; this class contains all DAGs compatible with the inferred conditional independences. Kalisch and Bühlmann, (2007) show if the maximum total degree of the graph is controlled and the data is Gaussian, then the PC algorithm can consistently recover the true Markov equivalence class even in high-dimensional settings where the number of variables grows with the number of samples. Harris and Drton, (2013) extend the result to Gaussian copula models using rank correlations.

However, graphs within the same Markov equivalence class may have drastically different causal and scientific interpretations. For the graphs in Figure 1, conditional independence tests can distinguish model (a) from the rest but cannot distinguish models (b), (c), and (d) from each other. Although Maathuis et al., (2009) provide a procedure for bounding the size of a causal effect over graphs within an equivalence class, interpretation of the set of possibly conflicting graphs can remain difficult. Results on the size and number of Markov equivalence classes, which may be exponentially large, can be found e.g. in Steinsky, (2013).

In contrast, it has been shown that under various additional assumptions, the exact graph structure, not just an equivalence class, can be identified from observational data (Loh and Bühlmann,, 2014; Peters and Bühlmann,, 2014; Rothenhäusler et al.,, 2018). In particular, Shimizu et al., (2006) show this to be the case under three main assumptions: (1) the data are generated by a linear structural equation model, (2) the error terms in the structural equations are non-Gaussian, and (3) there is no unobserved confounding among the observed variables; i.e., errors are independent. These assumptions yield the linear non-Gaussian acyclic model, abbreviated as LiNGAM, which is described formally in Section 2.1. Under the LiNGAM framework, the four models from Figure 1 are mutually distinguishable. Shimizu et al., (2006) use independent component analysis to estimate the graph structure, and the subsequent DirectLINGAM (Shimizu et al.,, 2011) and Pairwise LiNGAM (Hyvärinen and Smith,, 2013) methods iteratively select a causal ordering by computing pairwise statistics. These methods are motivated by identifiability results that are derived by iteratively forming conditional expectations. In practice, the conditional expectations are estimated using larger and larger regression models. As a result, the methods become inapplicable when the number of variables exceeds the sample size.

We develop a modification of the DirectLiNGAM algorithm that is suitable for high-dimensional data and give guarantees for when our algorithm will consistently recover the true graph in high-dimensional asymptotic scenarios. Most notably, our analysis considers restricted maximum in-degree of the graph and assumes log-concave distributions. The theory also applies to hub graphs where the maximum out-degree may grow with the size of the graph, which is in contrast to the conditions needed for high-dimensional consistency of the PC algorithm (Kalisch and Bühlmann,, 2007). Hub graphs appear in many biological networks (Hao et al.,, 2012).

2. Causal discovery algorithm

2.1. Generative model and notation

We assume that the observations are independent, identically distributed replications generated from a linear structural equation model so that the elements of each random vector satisfy

| (1) |

where the are unknown real parameters that quantify the direct linear effect of variable on variable , and is an error term of unknown distribution . We assume has mean 0 and is independent of all other error terms. Our interest is in models that postulate that a particular set of coefficients is zero. In particular, the absence of an edge, , indicates that the model constrains the parameter to zero. We assume that the graph, , representing the model is a DAG, which implies that the structural equation model is recursive; i.e., there exists a permutation of the variables, , such that is constrained to be zero unless .

We denote the model given by graph by . Each distribution is induced through a choice of linear coefficients and error distributions . Let be the matrix determined by the model constraints and the chosen free coefficients. Then the equations in (1) admit a unique solution with . The error vectors are independent and identically distributed and follow the product distribution . The distribution is then the joint distribution for that is induced by the transformation of .

Standard notation has the set comprise the parents of a given node . The set of ancestors, , contains any node with a directed path from to ; we let . The set of descendants, , contains the nodes with .

2.2. Parental faithfulness

An important approach to causal discovery begins by inferring relations such as conditional independence and then determines graphs compatible with empirically found relations. For this approach to succeed, the considered relations must correspond to structure in the graph as opposed to a special choice of parameters. In the context of conditional independence, the assumption that any relation present in an underlying joint distribution corresponds to the absence of certain paths in is known as the faithfulness assumption; see Uhler et al., (2013) for a detailed discussion. For our work, we define a weaker condition, parental faithfulness. In particular, if , we require that the total effect of on does not vanish when we modify the considered distribution by regressing onto any set of its non-descendants, as detailed next.

Let be a directed path in , so for . Given coefficients , the path has weight . Let be the set of all directed paths from to . Then the total effect of on is , with if and if . The effect gives the conditional mean of under interventions on ; i.e., using the do-operator of Pearl, (2009). Total effects may be calculated by matrix inversion, .

Let be the covariance matrix of the, for convenience, centered random vector . Let be the principal sub-matrix for a non-empty set of indices . For , let be the sub-vector comprised of the entries in places for . Let

| (2) |

be the population regression coefficients when is regressed onto . The quantity is defined even if , and in general even if . A pair is parentally faithful if for any set , the residual total effect defined as

| (3) |

is nonzero. If this holds for every pair , we say that the joint distribution is parentally faithful with respect to . Parental faithfulness only pertains to the linear coefficients and error variances, and the choices for which parental faithfulness fails form a set of Lebesgue measure zero. The concept is exemplified in Figure 2.

2.3. Test statistic

Reliable determination of the causal direction between and generally requires removal of all confounding. Thus, Shimizu et al., (2011) and Hyvärinen and Smith, (2013) adjust and for all such that and . However, adjusting by an increasingly larger set of variables propagates error proportional to the number of variables, rendering high-dimensional estimation inconsistent, or impossible when the size of the adjustment set exceeds the sample size. On the other hand, restricting the size of the adjustment sets may not remove confounding completely. The method we present solves this problem via a statistic that is conservative in the sense that it does not mistakenly certify causal direction when confounding is present.

Shimizu et al., (2011) calculate the kernel-based mutual information between and the residuals of when it is regressed onto . The corresponding population information is positive if and only if or there is uncontrolled confounding between and , that is, and have a common ancestor even when certain edges are removed from the graph. Hence, the mutual information can be used to test the hypothesis that versus the hypothesis that or there is confounding between and . Unfortunately, calculating the mutual information can be computationally burdensome, so Hyvärinen and Smith, (2013) propose a different parameter . Without confounding, if and if . With confounding, however, the parameter can take either sign, so it cannot be reliably used if we remain uncertain about whether or not confounding occurs. We introduce a parameter that shares the favorable properties of the mutual information but admits computationally inexpensive estimators that are rational functions of the sample moments of , which facilitates analysis of error propagation.

The parameter we consider is motivated by the following observation. Suppose the true generating mechanism is so that and for independent of . When the causal direction is correctly specified, the linear coefficient is recovered by for all integers greater than 1 for which . Of course, letting gives the typical least squares estimator. This leads to the identity which implies , which holds even when . In general, however, when the errors are non-Gaussian and the roles of and are swapped, this identity does not hold. When there are more than 2 variables involved, we reduce the problem to a bivariate problem by conditioning on an appropriate set . To this end, define for any the residual

where are the population regression coefficients from (2). When , let .

Theorem 1.

Let be a distribution in the model given by a DAG , and let . For , two distinct nodes and , and any set , define

| (4) |

-

(i)

If and , then .

-

(ii)

Suppose with parentally faithful under the covariance matrix of . If , then for generic error moments of order .

Estimators of the parameter from (4) are naturally obtained from empirical regression coefficients and empirical moments.

In Theorem 1(ii), the term generic indicates that the set of error moments for which this statement does not hold has Lebesgue measure zero. Given that there is a finite number of sets , the union of all exceptional sets is also a null set. A detailed proof of Theorem 1 is included in the supplement. Claim (i) can be shown via direct calculation, and we give a brief sketch of (ii) here. For fixed coefficients and set , is a rational function of the error moments. Thus existence of a single choice of error moments for which is sufficient to show that the statement holds for generic error moments. As the argument boils down to showing that a certain polynomial is not the zero polynomial (Okamoto,, 1973), the choice considered need not necessarily be realizable by a particular distribution. In particular, we choose all moments of order less than equal to those of the centered Gaussian distribution with variance , but for the th moment we add an offset , so

| (5) |

where is the double factorial of . If there is no confounding between and , that is, no ancestor of is the source of a directed path to that avoids , then

| (6) |

with , by the assumed parental faithfulness. Thus, a choice of offsets with implies . A more involved but similar argument can be made in the case of confounding. Under a slightly stronger form of faithfulness, if there is confounding regardless of whether ; see supplement Remark 1.

Corollary 1.

Let and be two distributions that each have all moments up to order equal to those of some Gaussian distribution. Then there exists a graph , for which , and distributions which are parentally faithful with respect to , but for some set .

Proof.

Corollary 1 confirms that the null set to be avoided in Theorem 1(ii) contains points for which all error moments are consistent with some Gaussian distribution. Thus, our identification of causal direction requires that the error moments of order at most be inconsistent with all Gaussian distributions. In practice, we consider the case and recommend unless one is certain the errors are not symmetric. We refer readers to Hoyer et al., (2008) for a full characterization of when graphs with both Gaussian and non-Gaussian errors are identifiable.

At each step, the high-dimensional LiNGAM algorithm presented in Section 3.1 considers a sub-graph and searches for a root node, i.e., a node without any parents. Suppose ; if is not a root in the sub-graph induced by , then there must exist some with for all sets which are upstream of and . However, if is a root, then for all when . Thus, to test whether is a root in , we aggregate the various parameters corresponding to and conditioning sets . Corollary 2 describes two ways to do this aggregation. If is a root, this quantity will be , and if is not a root, it will be positive.

Corollary 2.

Let , let , and consider two disjoint sets . For a chosen non-negative integer , define

where if and if .

-

(i)

If and , then

-

(ii)

Suppose for all . If and , then for generic error moments of order up to , we have and .

Proof.

(i) The statement follows immediately from Theorem 1. (ii) Since, , but , there exists some such that . For that and any , the residual total effect is because the assumed facts and imply that for all and . We have assumed , so, by Theorem 1, generic error moments ensure that for all , which in turn implies for . ∎

When (i) is satisfied, there may be more than one set which makes all pairwise statistics . is calculated by finding a single conditioning set which minimizes the maximum pairwise statistic across all ; in contrast, allows for a different conditioning set for each . For fixed , , and , the signs, either positive or zero, of (min-max) and (max-min) will always agree, but when and both quantities are positive, . Thus, the min-max statistic may be more robust to sampling error when testing if the parameters are non-zero. However, as discussed in Section 3.1, can be computed more efficiently than .

Theorem 1(ii) requires parental faithfulness since we consider arbitrary , whereas Corollary 2(ii) only requires that since we maximize over . Use of sample moments yields estimates , which in turn yields estimates of for . In the remainder of the paper, we drop the subscript in statements that apply to both parameters/estimators. Moreover, as we always fix , we lighten notation by omitting the superscript, writing , and .

3. Graph estimation procedure

3.1. Algorithm

We now present a modified DirectLiNGAM algorithm which estimates the underlying causal structure (Algorithm 1). As in the original algorithm, we identify a root and recur on the sub-graph that has the identified root removed. After step , we have a -tuple, , which gives an ordering of the roots identified so far, and the remaining nodes . In contrast to DirectLiNGAM, the proposed algorithm does not adjust for all non-descendants, but only for subsets of limited size. This gives meaningful regression residuals also when the number of variables exceeds the sample size and limits error propagation from the estimated linear coefficients.

At each step , we consider subsets of , which we use to denote the set of possible parents for . Naively allowing is not precluded by theory, but the number of subsets such that grows at . Thus, for computational reasons, we prune nodes which are not parents of by letting

| (7) |

where , is the node selected at the previous step, and is some cut-off value. Selecting a good value for is difficult because it should depend on the unknown signal strength. However, under the assumptions of Theorem 2, if is the root selected at step and is some tuning parameter in , then letting will not mistakenly prune parents from . In Algorithm 1, we do not update after is selected as a root. Since the final cut-off, , may be larger than the cut-off used to select , a final pruning step uses the criteria from (7) with to prune away nodes in that may be ancestors but not parents.

A larger value of prunes more aggressively, decreasing the computational effort. However, setting too large could result in incorrect estimates if some parent of is incorrectly pruned from . Section 3.2 discusses selecting an appropriate and a more detailed discussion of computational savings from the pruning procedure is given in the supplement.

As discussed in Section 2.3, may be more robust to sampling error than but comes at greater computational cost. At each step, decreases by a single node and may grow by one node. If the values of have been stored, updating , the max-min, only requires testing the subsets of which include the variable selected at the previous step. Updating the min-max statistic without redundant computation would require storing the values of . In practice, we completely recompute it at each step. Section 4 demonstrates this trade-off between computational burden and robustness.

3.2. Deterministic statement

Theorem 2 below makes a deterministic statement about sufficient conditions under which Algorithm 1 will output a specific graph when given data . We assume each but allow model misspecification so that may not be in for any DAG . However, we require that the sample moments of are close enough to the population moments for some distribution . For notational convenience, for and , let denote a sample moment estimated from data , and let denote a population moment for .

Condition (C1).

For some -variate distribution , there exists a DAG with for all such that:

-

(a)

For all and with and ; if then the population quantities for satisfy .

-

(b)

For all and with and , if , then the population quantities for satisfy .

Condition (C2).

All principal submatrices of the population covariance of have minimum eigenvalue greater or equal to .

Condition (C3).

All population moments of up to degree , for , are bounded by a constant for positive integer .

Condition (C4).

All sample moments of up to degree , for , are within of the corresponding population values of .

The constraint in Condition (C3) that is only used to facilitate simplification of the error bounds and is not otherwise necessary. Condition (C1) is a faithfulness type assumption on , and in Theorem 2 we make a further assumption on which ensures strong faithfulness. However, it is not strictly stronger or weaker than the Gaussian strong faithfulness type assumption. In particular we require the linear coefficients and error moments considered to be jointly “sufficiently parentally faithful and non-Gaussian.” So for a fixed sample size, there may be cases where the linear coefficients and error covariances do not satisfy Gaussian strong faithfulness, but do satisfy the non-Gaussian condition because the higher order moments are sufficiently non-Gaussian. However, the opposite may also occur where a set of linear coefficients and error moments satisfy Gaussian strong faithfulness but not the non-Gaussian condition.

Finally, let be the subset of distributions with whenever and . Then the set of linear coefficients and error moments that induce an element of has measure zero. This set difference includes distributions which are not parentally faithful with respect to and distributions for which there exist a parent/child pair for which both error distributions have Gaussian moments up to order .

Theorem 2.

The main result of Theorem 2 is part (ii). The identifiability of a DAG was previously shown by Shimizu et al., (2006) by appealing to results for independent component analysis; however, our direct analysis of rational functions of allows for an explicit tolerance for how sample moments of may deviate from corresponding population moments of . This implicitly allows for model misspecification; see Corollary 3. The proof of Theorem 2 requires Lemmas 1-3, which we develop first. The lemmas are proven in the supplement. Recall that are the population regression coefficients from (2), and let denote the coefficients estimated from .

Recall, that . Let denote the analogous quantity for , and let .

Lemma 2.

The proof of Lemma 2 relies on the fact that the map from moments of to the quantities of interest are Lipschitz continuous within a bounded domain.

The proof of Lemma 3 is an application of the triangle inequality.

of Theorem 2.

(ii) We proceed by induction. By Lemma 3 and assuming (8), each statistic is within of the corresponding population quantity. Thus, any statistic corresponding to a parameter with value 0 is less than and, by Condition (C1) and the condition on in (8), all statistics corresponding to a non-zero parameter are greater than .

Recall that is a topological ordering of nodes. Assume for some step , that is consistent with a valid ordering of . Let so that any is a root in the subgraph induced by and is consistent with . The base case for is trivially satisfied since .

Setting does not incorrectly prune any parents, so , which implies for all that . Similarly, for any , there exists with for all . Thus, for every and . This implies the next root selected, must be in , and thus remains consistent with .

Remark.

As stated Theorem 2 concerns an explicit cut-off , whereas in practice we specify a tuning parameter that is easier to interpret and tune. If , it holds under the conditions of Theorem 2 that Algorithm 1 returns a topological ordering consistent with , but may be a superset of . However, there exists which will recover the exact graph.

To see this note that ensures that under the specified conditions, so no parents are pruned incorrectly and the estimated topological ordering is correct. This, however, may not remove all ancestors that are not parents, so the estimated edge set may be a superset of the true edge set. Letting instead

| (10) |

will correctly prune ancestors and not parents. Because all sample moments are close to their population values, the denominator must be less than and strong parental faithfulness further implies that the numerator is greater than so (10) is greater than 1. However, setting too large may result in an incorrect estimate of the ordering since a true parent may be errantly pruned. Thus, we advocate a more conservative approach of setting which is more robust to violations of strong faithfulness.

Remark.

Suppose but is not necessarily parentally faithful with respect to . If and for all , then for generic error moments a correct ordering will still be recovered consistently as .

Indeed, Corollary 2(ii) holds without parental faithfulness. So for generic error moments, there exists such that for all for all steps . However, without parental faithfulness, a parent node may be errantly pruned if . To ensure Corollary 2(i) holds, we need for all , which is satisfied by letting . For fixed , since as , there exists a so that .

3.3. High-dimensional consistency

We now consider a sequence of graphs, observations, and distributions indexed by the number of variables . For notational brevity, we do not explicitly include the index in the notation, and keep simply writing , , and for these sequences. The following corollary states conditions sufficient for the conditions of Theorem 2 to hold with probability tending to 1. We first make explicit assumptions on , with denoting the population moments of . Again, we allow for misspecification, but require control of the distance between population moments of and some .

Condition (C5).

is a log-concave distribution.

Condition (C6).

All population moments of up to degree , for , are bounded by .

Condition (C7).

Each population moment of up to degree , for , is within of the corresponding population moment of .

When is actually generated from a recursive linear structural equation model, Condition (C7) trivially holds with and log-concave errors imply that is log-concave.

Corollary 3.

Proof.

Conditions (C6) and (C7) imply Condition (C3). It remains to be shown that Condition (C4) and (8) hold for the specified in Condition (C1). Solving the inequality in Lemma 3 for shows (8) will be satisfied if the sample moments of are within of the population moments such that with less than

for defined in (9). Since , ensure that first term is the relevant term. We further simplify the expression since

Thus, the conditions of Theorem 2 will be satisfied if

Specifically, we analyze the case when and for all . If follows a log-concave distribution, we can apply Lemma B.3 of Lin et al., (2016) which states for , some degree polynomial of log-concave random variables , and some absolute constant, , if

then

Letting be the sample moments of up to degree , Condition (C6) implies the variance is bounded by . When , there are moments with degree at most , then by a union bound, when ,

when

| (12) |

In the asymptotic regime, where is increasing,

implies that the inequality in (12) will be satisfied and

Plugging in the expression for , we find

This quantity is of order when assuming that . In addition, will be satisfied if . This ratio is

which is when . ∎

4. Numerical results

4.1. Simulations: low dimensional performance

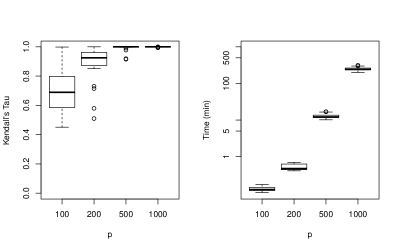

We first compare the proposed method using: (1) min-max and (2) max-min against (3) DirectLiNGAM (Shimizu et al.,, 2011) and (4) Pairwise LiNGAM (Hyvärinen and Smith,, 2013, Section 3.2). We randomly generate graphs and corresponding data with the following procedure. For each node , select the number of parents uniformly from . We include edge to ensure that the ordering is unique and draw uniformly from . The remaining parents are selected uniformly from and the corresponding edge weights are set to . The error terms for variable are generated by selecting and then drawing .

We use , fix the max in-degree , let , and let and . We set and compare performance by measuring Kendall’s between the returned ordering and the true ordering; i.e., the number of concordant pairs in the ordering minus the number of discordant pairs, normalized by the number of total pairs. The procedure is repeated 500 times for each setting of and .

Figure 3 shows that in the low-dimensional case with , the Pairwise LiNGAM and DirectLiNGAM methods outperform the proposed method, with either statistic. However, already with , our method begins to give improvements. The min-max statistic does slightly better than , the max-min. However, Figure 4 shows a large difference in computational effort; are included for further contrast. In the sequel, we use the max-min statistic, .

The proposed method compares favorably to the DirectLiNGAM method in computational effort because of the expensive kernel mutual information calculation and is comparable to the Pairwise LiNGAM. However, we refrain from a direct timing comparison because DirectLiNGAM and Pairwise LiNGAM are both implemented in Matlab while our proposed method is implemented in R and C++ (R Core Team,, 2017; Eddelbuettel and François,, 2011). In the supplement, we also provide a direct comparison between the proposed statistic and those used by Shimizu et al., (2011) and Hyvärinen and Smith, (2013).

4.2. Simulations: high-dimensional consistency

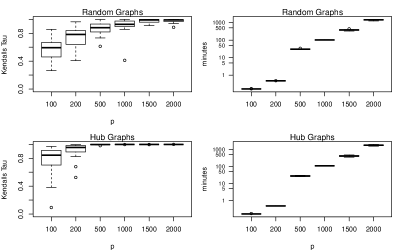

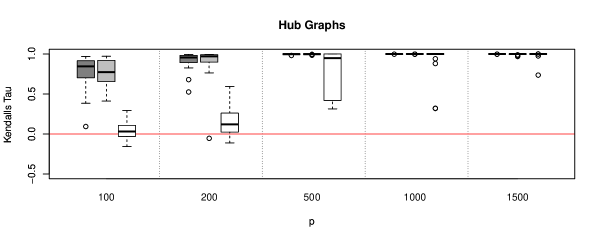

To illustrate high-dimensional consistency, we generate the graph and coefficients as in Section 4.1 but with and . We first consider random DAGs and data generated as before, but with . We also consider graphs with hubs, that is, nodes with large out-degree. These are generated by including a directed edge from to for all nodes and drawing the edge weight uniformly from . We then set nodes as hubs and include an edge with weight to each non-hub node from a randomly selected hub. Thus, the out-degree for each of the hub nodes grows linearly with , but the maximum in-degree remains bounded by . For both cases, the results for 20 runs at each value of are shown in Figure 5.

In the supplement, we show simulations with gamma errors and also consider a setting with Gaussian errors, where our method should not be consistent.

4.3. Pre-selection of neighborhoods

As with the original DirectLiNGAM procedure, any edges or non-edges known in advance can be accounted for. Such information could, for instance, be obtained by applying neighborhood selection (Meinshausen and Bühlmann,, 2006) to estimate the Markov blanket of each node. This blanket consists of parents, children, and parents of children. For sparse graphs, Hyvärinen and Smith, (2013, Section 3.3) propose first using such a pre-selection step, then directly estimating the direction of each edge using pairwise measures without any additional adjustment. To create a total ordering, Alg B and Alg C of Shimizu et al., (2006) can be used. This does not require specifying a maximum in-degree, but in general, the neighborhood selection procedure will only be consistent if the total degree is controlled.

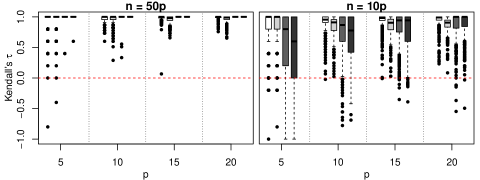

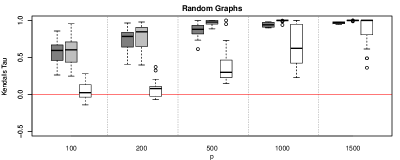

In our proposed procedure, we may incorporate estimated Markov blankets by limiting, at each step , for each remaining node , the set of potential parents, , to the intersection of the estimated Markov blanket of and the previously ordered nodes, . We do not otherwise prune the set of potential parents. Figure 6 shows results from using the pre-selection step under the setting from Section 4.2 for general random graphs. The pre-selection procedure improves the performance of our proposed high-dimensional LiNGAM procedure, but the proposed procedure without pre-selection still outperforms the two-stage procedure of Hyvärinen and Smith, (2013, Section 3.3). Similar results for the hub graph setting are shown in the supplement.

4.4. Data example: high-dimensional performance

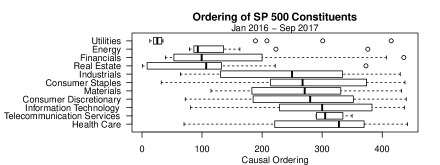

We estimate causal structure among the stocks in the Standard and Poor’s 500. Specifically, we consider the percentage increase/decrease for each share price for each trading day between Jan 2007 to Sep 2017. We consider the companies for which data is available for the entire period, and we scale and center the data so that each variable has mean 0 and variance 1. As structure may vary over time, we estimate the causal structure for each of the following periods separately with and : 2007-2009, 2010-2011, 2012-2013, 2014-2015, 2016-2017 (ending in September). Across these periods, the sample size, , ranges from 425 to 755.

The underlying structure is unlikely to be causally sufficient or acyclic. In addition, although it is common to assume that daily returns are independent, this assumption may not hold in practice. Nonetheless, the method still recovers reasonable structure. We first consider the most recent Jan 2016 - Sep 2017 period. Figure 7 shows a boxplot for the estimated ordering of the companies within each sector. The sectors are sorted top to bottom by median ordering. Near the top, we see utilities, energy, real estate, and finance. Since energy is an input for almost every other sector, intuitively price movements in energy should be causally upstream of other sectors. The estimated ordering of utilities might seem surprising; however, utility stocks are typically thought of as a proxy for bond prices. Thus, the estimated ordering may reflect the fact that changes in utility stocks capture much of the causal effect of interest rates, which had stayed constant for much of 2011-2015 but began moving again in 2016. Real estate and finance, sectors that are highly impacted by interest rates, are also estimated to be early in the causal ordering.

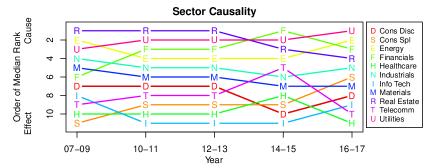

Figure 8 ranks each sector by the median topological ordering for each period. The orderings are relatively stable over time, but there are a few notable changes. In 2007, real estate was estimated to be the “root sector” while finance is in the middle. This aligns with the idea that the root of the 2008 financial crisis was actually failing mortgage backed securities in real estate, which had a causal effect on finance. However, over time, real estate has moved more downstream.

5. Discussion

We proposed a causal discovery method that was proven consistent for specific test statistics and log concave errors. Similar analyses could be given for other statistics that are Lipschitz continuous in the sample moments over a bounded domain, can distinguish causal direction, and indicate the presence of confounding. This would include a normalized version of the proposed test statistics which accounts for the scaling of the data. Log-concavity was assumed for exponential concentration of sample moments and other distributional assumptions could be considered instead if analogous concentration results can be obtained and traced throughout the analysis.

The proposed algorithm requires selecting a bound on the in-degree and a pruning parameter . The in-degree is typically unknown, but a reasonable upper bound may be used as a “bet on sparsity”. If the maximum in-degree of the true graph is larger than the specified but the “extra edges” have small enough edge-weights, the “closest” DAG with maximum in-degree is still recovered with high probability. The pruning parameter plays a similar role to the nominal level for each conditional independence test in the PC algorithm. Both parameters have an effect on the sparsity of the estimated graph and regulate the maximum size of conditioning sets.

At each step, instead of taking the minimum over all subsets of potential parents, one could also pick parents for every unordered node using a variable selection procedure and then only calculate using the selected parents. Such a procedure would also consistently estimate the causal ordering as long as the variable selection procedure is consistent. Slightly different conditions, such as a beta-min condition, would be needed when adopting standard methods based on least squares, but in practice the resulting method performs quite well as shown in simulations in the supplement. This could be explained as being due to use of only second moments for the variable selection.

In (8), we have made a key restriction that the error moments must be adequately different from the moments of any Gaussian and the edge weights must be strongly parentally faithful. In practice, this is a difficult condition to satisfy, and Uhler et al., (2013) show that strong faithfulness type restrictions can be problematic in practice. However, even if the distribution is not strongly parentally faithful, we can still consistently recover the correct ordering as long as each individual linear coefficient is non-zero and the errors are sufficiently non-Gaussian. Sokol et al., (2014) consider identifiability of independent component analysis for fixed when the error terms are Gaussians contaminated with non-Gaussian noise. In particular, when the effect of the non-Gaussian contamination decreases at an adequately slow rate, the entire mixing matrix is identifiable asymptotically. In our analysis, the measure of non-Gaussianity is treated by our assumptions on . Our results suggest that the results of Sokol et al., (2014) can also be extended, given suitable sparsity, to the asymptotic regime where the number of variables is increasing.

The modified procedure we propose retains the existing benefits of the original DirectLiNGAM procedure. In particular, the output of algorithm is independent of the ordering of the variables in the input data. Although this is typically not an issue in the low-dimensional case, in the high-dimensional setting, the output of causal discovery methods may be highly dependent on ordering (Colombo and Maathuis,, 2014).

Acknowledgment

This work was supported by the U.S. National Science Foundation under Grant No. DMS 1712535. Thomas S. Richardson gave helpful feedback on an advance copy of the manuscript.

References

- Colombo and Maathuis, (2014) Colombo, D. and Maathuis, M. H. (2014). Order-independent constraint-based causal structure learning. J. Mach. Learn. Res., 15:3741–3782.

- Drton and Maathuis, (2017) Drton, M. and Maathuis, M. H. (2017). Structure learning in graphical modeling. Annual Review of Statistics and Its Application, 4(1):365–393.

- Eddelbuettel and François, (2011) Eddelbuettel, D. and François, R. (2011). Rcpp: Seamless R and C++ integration. Journal of Statistical Software, 40(8):1–18.

- Hao et al., (2012) Hao, D., Ren, C., and Li, C. (2012). Revisiting the variation of clustering coefficient of biological networks suggests new modular structure. BMC Systems Biology, 6(1):34.

- Harris and Drton, (2013) Harris, N. and Drton, M. (2013). PC algorithm for nonparanormal graphical models. J. Mach. Learn. Res., 14:3365–3383.

- Horn and Johnson, (2013) Horn, R. A. and Johnson, C. R. (2013). Matrix analysis. Cambridge University Press, Cambridge, second edition.

- Hoyer et al., (2008) Hoyer, P. O., Hyvärinen, A., Scheines, R., Spirtes, P., Ramsey, J., Lacerda, G., and Shimizu, S. (2008). Causal discovery of linear acyclic models with arbitrary distributions. In UAI 2008, Proceedings of the 24th Conference in Uncertainty in Artificial Intelligence, Helsinki, Finland, July 9-12, 2008, pages 282–289.

- Hyvärinen and Smith, (2013) Hyvärinen, A. and Smith, S. M. (2013). Pairwise likelihood ratios for estimation of non-Gaussian structural equation models. J. Mach. Learn. Res., 14:111–152.

- Kalisch and Bühlmann, (2007) Kalisch, M. and Bühlmann, P. (2007). Estimating high-dimensional directed acyclic graphs with the pc-algorithm. J. Mach. Learn. Res., 8:613–636.

- Lin et al., (2016) Lin, L., Drton, M., and Shojaie, A. (2016). Estimation of high-dimensional graphical models using regularized score matching. Electron. J. Stat., 10(1):806–854.

- Loh and Bühlmann, (2014) Loh, P.-L. and Bühlmann, P. (2014). High-dimensional learning of linear causal networks via inverse covariance estimation. J. Mach. Learn. Res., 15:3065–3105.

- Lumley, (2017) Lumley, T. (2017). leaps: Regression Subset Selection. R package version 3.0.

- Maathuis et al., (2009) Maathuis, M. H., Kalisch, M., and Bühlmann, P. (2009). Estimating high-dimensional intervention effects from observational data. Ann. Statist., 37(6A):3133–3164.

- Meinshausen and Bühlmann, (2006) Meinshausen, N. and Bühlmann, P. (2006). High-dimensional graphs and variable selection with the lasso. Ann. Statist., 34(3):1436–1462.

- Okamoto, (1973) Okamoto, M. (1973). Distinctness of the eigenvalues of a quadratic form in a multivariate sample. Ann. Statist., 1:763–765.

- Pearl, (2009) Pearl, J. (2009). Causality. Cambridge University Press, Cambridge, second edition. Models, reasoning, and inference.

- Peters and Bühlmann, (2014) Peters, J. and Bühlmann, P. (2014). Identifiability of Gaussian structural equation models with equal error variances. Biometrika, 101(1):219–228.

- R Core Team, (2017) R Core Team (2017). R: a language and environment for statistical computing. R Foundation for Statistical Computing, Vienna, Austria.

- Rothenhäusler et al., (2018) Rothenhäusler, D., Ernest, J., and Bühlmann, P. (2018). Causal inference in partially linear structural equation models. Ann. Statist., 46(6A):2904–2938.

- Shimizu et al., (2006) Shimizu, S., Hoyer, P. O., Hyvärinen, A., and Kerminen, A. (2006). A linear non-Gaussian acyclic model for causal discovery. J. Mach. Learn. Res., 7:2003–2030.

- Shimizu et al., (2011) Shimizu, S., Inazumi, T., Sogawa, Y., Hyvärinen, A., Kawahara, Y., Washio, T., Hoyer, P. O., and Bollen, K. (2011). DirectLiNGAM: a direct method for learning a linear non-Gaussian structural equation model. J. Mach. Learn. Res., 12:1225–1248.

- Sokol et al., (2014) Sokol, A., Maathuis, M. H., and Falkeborg, B. (2014). Quantifying identifiability in independent component analysis. Electron. J. Stat., 8(1):1438–1459.

- Spirtes et al., (2000) Spirtes, P., Glymour, C., and Scheines, R. (2000). Causation, prediction, and search. Adaptive Computation and Machine Learning. MIT Press, Cambridge, MA, second edition. With additional material by David Heckerman, Christopher Meek, Gregory F. Cooper and Thomas Richardson, A Bradford Book.

- Steinsky, (2013) Steinsky, B. (2013). Enumeration of labelled essential graphs. Ars Combin., 111:485–494.

- Uhler et al., (2013) Uhler, C., Raskutti, G., Bühlmann, P., and Yu, B. (2013). Geometry of the faithfulness assumption in causal inference. Ann. Statist., 41(2):436–463.

Appendix A Proof of Theorem 1

Proof.

Statement (i): Consider any set such that and . Since we condition on all parents, for any which is not a parent of . Then,

| (13) | ||||

We then directly calculate the parameter for the set :

| (14) | ||||

The penultimate equality follows from the assumption of independent errors.∎

Statement (ii): For fixed , , and parentally faithful linear coefficients and variances, is a polynomial of the error moments of degree . Thus, selecting a single point (of error moments) where the quantity is non-zero is sufficient for showing that the quantity is non-zero for generic error moments of degree (Okamoto,, 1973). Specifically, we select that point by letting all error moments for be consistent with the Gaussian moments implied by , the variance of , but select the th degree moment to be inconsistent with the corresponding Gaussian moment. Since there are a finite number of sets such that , then the set of error moments of degree which yield for any also has Lebesgue measure zero.

Recall that the total residual effect of on given is

where is the total effect of on and . Now,

| (15) | ||||

By the parental faithfulness assumption, since , . We partition into three disjoint sets

| (16) | ||||

For generic edge weights, corresponds to ancestors of which only have directed paths to through ; corresponds to ancestors of which have directed paths to that do not pass through . For some specific edge weight values, may also include non ancestors of which have directed paths to that do not pass through if those paths do not contribute to the total effect; i.e., non-faithfulness may result in including more nodes. However, is non-empty because by the parental faithfulness assumption.

Let

so that

and

For with , let , the multinomial coefficient. Then

| (17) | ||||

so that

| (18) | ||||

We first consider the case where is empty so that the expansion above reduces to

| (19) | ||||

Let the moments of degree for of all the error terms be consistent with some Gaussian distribution. This implies that the error moments for are also consistent with some Gaussian distribution since the sum of Gaussians is also Gaussian. So and for ,

where is the double factorial of . However, let the th degree error moments be inconsistent with the specified Gaussian distribution so that for and ,

By direct calculation we see

When is odd, for all , so we are left with

| (20) | ||||

When is even, then when is odd, so we are left with

Evaluating the moments yields

Rewriting terms and a change of variables show that the first two lines cancel leaving equal to

| (21) | ||||

This is the same expression as when is odd. So for any ,

| (22) |

Since and are disjoint, we can always select the th moments of the individual error moments so that this holds.

Now consider the case when is not empty. From Equations (18), (20), and (21),

Since the unevaluated terms are fixed with respect to and , selecting values such that

| (23) | ||||

implies that .

∎

Remark.

Even if and , as long as there is some such that and (i.e., and are confounded by ), then is still non-zero for generic error moments. However, even if there is a with a directed path to both and which is not blocked by , and is not necessarily implied by parental faithfulness because may be in or .

Proof.

When , (18) reduces to

| (24) | ||||

Since the first and third term do not involve , letting

| (25) |

ensures that so that the quantity is non-zero for generic error moments. ∎

Appendix B Proof of Lemma 1

Proof.

We use to denote vector norms and to denote matrix norms. Conditions (C2) and (C3) imply that

| (26) |

Condition (C4) implies and with and . Using results from Horn and Johnson, (2013, Equation 5.8.7) for the third and fourth inequalities below yields

| (27) | ||||

The term . Since the bound in (27) is increasing in each of its arguments for ,

| (28) |

The penultimate inequality holds because by assumption and the last inequality holds because by assumption . ∎

Appendix C Proof of Lemma 2

Proof.

For , let be the multinomial coefficient. Define the map

Since is of length , there are moments we consider. By Condition (C3) and (C4), each of the sample moments of is restricted to , and as shown in (26) each of the is restricted to . In this domain, the partial derivatives of are bounded with

By the mean value theorem for some , a convex combination of and ,

where and indicate the gradient with respect to the linear coefficients and moments, respectively. The last inequality follows from Hölder’s inequality. Plugging in from Lemma 1 yields

The second inequality holds because we assumed ; the third inequality holds because we assumed ; the fourth inequality holds because we assumed and ; the fifth inequality holds because we assumed . ∎

Appendix D Proof of Lemma 3

Proof.

Similar to the previous notation where , we also allow for indicating the population moment involving . By the triangle inequality,

| (29) | ||||

Consider each of the two terms separately. For some and we have

Using the analogous argument for the second term, we can bound the entire quantity as

∎

Appendix E Pruning Procedure

At the beginning of each step in Algorithm 1, we have a set of nodes which have already been ordered, , and a set of nodes which have not yet been ordered, . To select the next node in the ordering, we calculate for each ,

where is a set of potential parents we consider for node . This requires fitting regressions which can be computationally prohibitive when is large. In order to speed up computation, rather than letting , we seek to keep small while preserving the theoretical guarantees in Theorem 2 and Corollary 3. In particular, we let

| (30) |

where and is some cut-off value. Suppose where is the root selected at step and is some tuning parameter in . Under the assumptions of Theorem 2 where is the signal strength, for all steps because . Thus, no parent of is mistakenly excluded from .

This pruning procedure can lead to large computational savings; however, the savings, even with an oracle pruning parameter , will depend on the structure of the true graph. If there is not a unique total ordering, the savings may vary from one sample to another, even if is the same, because the pruning depend on the topological ordering selected. On one extreme, if the true graph is the empty graph, then (specifically ) for all at all steps . If the graph is a single chain, i.e., , then where is the user specified maximum in-degree. However, there are also cases where the maximum in-degree is bounded, but . For the graph shown in Figure 9, in the worst case, at step , if , then . However, if , then . In general, for “upside-down” binary trees, in the worst case scenario, .

To reduce redundant computation required for the pruning procedure, we keep a running record of the minimum for each . Thus, at each new step, we only need to consider the new sets in . Since grows by at most 1 node at each step, then . Also, when calculating the pruning statistics, we avoid re-computing , which is the most expensive part, since it was already computed when calculating for some at the previous step.

Appendix F Additional Simulations

F.1. Bivariate Data

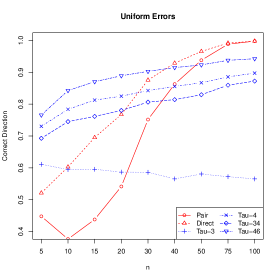

In Figure 10 we compare the proportion of times DirectLiNGAM, Pairwise LiNGAM, and the proposed procedure are able to detect the correct causal direction in bivariate data. This allows for a direct comparison of the test statistics without the additional algorithmic changes. For each simulation, we let and be either gamma or uniform with standard deviations randomly selected in . We then let and with drawn randomly from . For , we consider and also consider the sum of statistics of the form which can in some cases have more accuracy. For the uniform distribution we let and for the gamma distribution we let . For DirectLiNGAM and Pairwise LiNGAM we use the default settings in the code provided on the author’s website111https://sites.google.com/site/sshimizu06/Dlingamcode. We use simulations at each level of . We see that at the smaller sample sizes, the proposed statistics have higher accuracy, especially the sum statistics. However, as grows larger, the DirectLiNGAM and Pairwise LiNGAM methods perform better. Since the third moments of the uniform are the same as the Gaussian, is a very poor determinant of causal direction when the errors are uniform. It still does slightly better than chance because tends to have a higher variance than , but the accuracy actually decreases as increases.

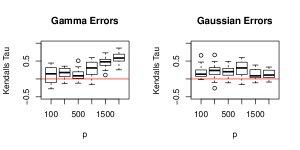

F.2. Gamma and Gaussian errors

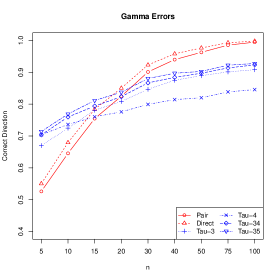

We also show two additional simulation settings with the same setup as the high-dimensional non-hub setting from Section 4.2 where . The results in the main text use uniform random variables, and here we give results for when the random variables are gamma and Gaussian. In particular, in the gamma setting, we let where is a gamma random variable with shape parameter and rate parameter so that has mean 0 and variance . In the Gaussian case, we let . In both cases, we draw uniformly from .

For the gamma case, as the theory would predict, the performance increases as the number of nodes and sample size increase. However, because the sample moments of gamma random variables concentrate slower than the uniform random variables, at each setting of and , the performance with gamma errors is worse than the uniform case.

For the Gaussian case, as the theory would predict, we see that the estimated ordering does not improve with increasing and . However, is still better than chance. We posit this is because even though the test statistic cannot determine causal direction with Gaussian errors, it can still detect uncontrolled confounding (see supplement Remark Remark). Consider, step of the procedure, where is the “already ordered” set and is the “yet to be ordered” set. When selecting a root from the subgraph induced by , node will be selected as a root (using population quantities) only if the confounders, , have already been selected into and can be used to condition . For example if nodes , share a common parent , and will still be positive because when . Thus, similar to how the PC algorithm can use v-structures to orient some edges, the proposed procedure can use confounding structures to identify some, but not all, causal orderings even in the Gaussian case.

F.3. Pre-selection with hub graphs

Figure 12 shows the results of using pre-selection with randomly generated hub graphs. We use the same data generating procedure as described in Section 4.2. Again we see that the proposed method, with or without pre-selection, outperforms the sparse Pairwise LiNGAM method.

F.4. Parent selection using best subset regression

At each step, as an alternative to picking a root by minimizing across all subsets such that , we could use a two-step procedure. Specifically, for each , we first select a set of possible parents via best subset regression so that minimizes the conditional variance

We then only calculate for that specific set of parents and select a root by

| (31) |

If the parents of the roots are consistently selected by best subset regression, this procedure may also yield consistent estimation of the causal graph. This procedure works well in simulations; however, theoretical guarantees would require slightly different assumptions, such as a beta-min condition to ensure consistent parent selection. Also, in practice, we use a branch and bound procedure (Lumley,, 2017) and implementing a pruning procedure is not as straightforward so the two-step method tends to be more computationally expensive. The simulation settings use the random graphs as described in Section 4.2 with .