Mixing LSMC and PDE Methods to Price Bermudan Options111SJ (RGPIN-2018-05705 and RGPAS-2018-522715) and KJ (RGPIN-2016-05637) would like to thank NSERC for partially funding this work. The authors would like to thank three anonymous referees for helpful comments that ultimately improved the paper. The first version of this paper was posted on SSRN on November 16, 2016, and is available at https://ssrn.com/abstract=2870962. This version:

SIAM J. Financial Mathematics, Forthcoming

Abstract

We develop a mixed least squares Monte Carlo-partial differential equation (LSMC-PDE) method for pricing Bermudan style options on assets under stochastic volatility. The algorithm is formulated for an arbitrary number of assets and volatility processes and we prove the algorithm converges almost surely for a class of models. We also introduce a multi-level Monte-Carlo/multi-grid method to improve the algorithm’s computational complexity. Our numerical examples focus on the single () and multi-dimensional () Heston models and we compare our hybrid algorithm with classical LSMC approaches. In each case, we find that the hybrid algorithm outperforms standard LSMC in terms of estimating prices and optimal exercise boundaries.

1 Introduction

In recent years, mixed Monte Carlo-partial differential equation (MC-PDE) methods for European options have seen an increase in research activity. In the context of stochastic volatility (SV) models with one-way coupling, these methods revolve around simulating the SV process, computing an expectation by solving a PDE conditional on the volatility path, and averaging over paths. The approach has been around for some time as in Hull and White (1987) and Lewis (2002) but has seen renewed interest in Ang (2013), Lipp et al. (2013), Loeper and Pironneau (2009), Dang et al. (2015), Dang et al. (2017) and Cozma and Reisinger (2017).

In the context of high-dimensional European option pricing problems, under stochastic volatility, finite difference methods cannot be readily applied, and the correlations between the underlying processes often make the system non-affine which rules out Fourier-based quadrature methods. Also, full Monte-Carlo (MC) methods applied to such systems suffer from high variance and computational costs. An alternative is to find a middle ground between the two approaches where one simulates the underlying volatility processes and solves the resulting lower dimensional conditional PDEs, which may often be handled efficiently. This mixed method results in dimension reduction from the PDE perspective and variance reduction from the MC perspective.

As previous research which utilizes this strategy is focused on pricing European style options and addresses the dimension and variance reduction in computing relevant expected values, we analyse the mixed MC-PDE framework for Bermudan style options. The Bermudan context requires dealing with a high dimensional PDE between exercise dates, along with a high dimensional grid for accurately locating the exercise region; the latter being an issue that arises when moving from European to Bermudan options. When pricing Bermudan options the primary object of interest is the optimal stopping policy and the exercise boundaries that it defines. We note that one can always approximate the price of an American style option by considering a Bermudan option with high number of exercise dates as discussed in Bouchard and Warin (2012).

To deal with the above issues, we develop a hybrid method which mixes the least squares Monte Carlo (LSMC) approaches of Longstaff and Schwartz (2001) and Tsitsiklis and Van Roy (2001) with PDE techniques. The essence of our version of a mixed LSMC-PDE algorithm is to

-

1.

simulate paths of the underlying SV process,

-

2.

solve the conditional expectation (using a PDE approach) along each path,

-

3.

regress these conditional expectations onto a family of basis functions over the volatility state-space.

The algorithm may be viewed as an extension of Tsitsiklis and Van Roy (2001) and reduces the monitoring of a high dimensional grid by replacing the volatility dimensions with a few regression coefficients. The approach provides variance reduction from the Monte-Carlo perspective, dimension reduction from the PDE perspective and alters the regression problems that are solved at each time step such that they are simpler than in standard LSMC. Our approach has its roots in Lipp et al. (2013) where it is very briefly mentioned, but not analysed. Our contribution is a precise development of the algorithm, proof of convergence, discussion of complexity and complexity reduction methods, followed by a series of numerical examples.

When applied to SV problems, LSMC tends to be fairly inaccurate in determining the optimal exercise boundaries. In the literature, there have been a few direct modifications to LSMC, applied to SV problems, such as in Gramacy and Ludkovski (2015), and Ludkovski (2018) that address this issue. There have also been other types of probabilistic approaches such as in Ait Sahlia et al. (2010) and Agarwal et al. (2016). The approach of Ait Sahlia et al. (2010) is specific to the Heston model and appears to be non-applicable to models outside the affine class. Agarwal et al. (2016) develops a highly efficient method for multi-scale SV models. The work of Gramacy and Ludkovski (2015), Ludkovski (2018) cast LSMC as a classification problem using various experimental designs and regression methods, and, as one of their examples, consider a one dimensional mean-reverting SV model. The approach of Jain and Oosterlee (2015) also looks promising, although it typically requires a choice of basis functions for which one can compute (or approximate) expectations in closed form, and need to be developed case-by-case. It’s also worth noting the work of Rambharat and Brockwell (2010), which deals with the related problem of Bermudan option pricing under unobservable SV.

The remainder of this paper is organized as follows. In Section 2, we set up our model and provide the basic mechanics of the algorithm. In Section 2 and 3 we develop theoretical aspects of the algorithm such as formalizing the underlying probability spaces, deriving expressions for the regression coefficients, and showing the algorithm converges almost surely for pure-SV models. Section 4 shows how Multi-Level Monte Carlo/multi-grids may be incorporated and also gives an overview of the overall algorithm’s complexity. In Section 5 we apply the algorithm to the Heston and multi-dimensional Heston model and present estimates of prices and optimal exercise boundaries. These results are also compared to finite difference and standard LSMC approaches.

2 A Hybrid LSMC/PDE algorithm

2.1 The Model

We suppose the existence of a probability space which may accommodate a dimensional stochastic process satisfying a system of SDEs with a strong, unique solution. We begin by defining mappings

and a -dimensional Brownian motion, , with correlation matrix, . The process is assumed to satisfy the following system of SDEs

where for and is element-wise product. As we shall see, our approach allows for an arbitrary (as long as it is positive semi-definite) stock-volatility correlation structure.

The above SDE classifies as a pure SV model, examples of which have been developed in Stein and Stein (1991), Heston (1993), Feng et al. (2010), and Grasselli (2017) among others. The work in this paper may also be extended easily to multi-factor pure SV models such as in Christoffersen et al. (2009). While the algorithm we discuss in this paper may conceivably be applied to SV models with a non-linear local volatility (LV) component, our derivations, numerical examples, and proof of convergence pertain to only pure SV models. Another property of is that it exhibits ‘one-way coupling’: the SDE for may be simulated independently of . We shall make this notion more precise in Section 2.4.

2.2 Bermudan Option Pricing

Let be an ordered set of exercise dates with and be our exercise function at each date. We often suppress the subscript in and to simplify notation when the context is clear. We also suppose the risk free rate is a constant, .

Valuing a Bermudan option requires developing an algorithm for evaluating where and is the set of -stopping times taking values in . By the Markov property, depends only on , and we can write for some function .

At time we have . We then define a new function, , denoted as the continuation value, at times by

By the discrete dynamic programming principle (DPP), for , we may express as the maximum of the continuation value and the immediate exercise value at :

From this point on, for notational simplicity, we condense notation and replace our subscripts with simply . We also replace arguments depending on time by subscripts.

2.3 Algorithm Overview

We now describe a hybrid-method for computing which is based on the Tsitsiklis and Van Roy (2001) approach, but uses conditional PDEs to incorporate dimensional and variance reduction. We begin by giving an intuitive explanation and provide a formal, pseudo-code based, description in A.

We simulate paths of starting from the initial value . Each path of over is represented as . Given a product set , we compute over the domain . The set is the domain of the conditional expectations that we compute; in practice, it is the grid for our numerical PDE solver. We suppose the discretized form of has points in each dimension so that there are points in total. Given the value of the option at time we proceed to compute the continuation value at . The algorithm begins at time where .

2.3.1 Solving along to obtain the pre-surface

For each simulation path (), we compute (beginning with )

| (1) |

for all . These may be computed simultaneously over for each path using a numerical PDE solver. The details of this step may be found in Section 2.4, below.

2.3.2 Regress across to obtain the completed surface

For each , from the previous step, we have realizations of the continuation value along each volatility path, i.e., .

Next, apply least-squares regression to project this onto a family of linearly independent basis functions over our volatility space. This results in a vector of coefficients of length , and provides the continuation value at for any point in the volatility space as follows:

2.3.3 Obtaining the Option Price

2.3.4 A Direct Estimate on the Time Zero Price

Since at time zero, there is only a single value for , we obtain an estimate for our time-zero prices by

which is often biased high. Following Jain and Oosterlee (2015), we call this the direct estimator.

2.3.5 A Lower Estimate on the Time Zero Price

Given our estimated regression coefficients, we obtain a sub-optimal exercise policy defined on . Thus, we may define a lower estimate via the expectation

| (2) |

In traditional LSMC, one simulates a new independent set of paths to approximate (2). In the class of models we study, simulating both and undermines the variance reduction obtained by the algorithm and we instead use a hybrid approach.

To this end, we denote the holding and exercise regions by and , respectively. We then simulate new independent paths of on , compute

| (3) |

via a PDE approach for , and take the average. To compute (3), for each , first set . Next, compute

via a PDE method for all . The option price at time is then given by

After repeating this procedure for times we obtain the lower estimate

| (4) |

for all .

2.4 Numerical Computation of Conditional Expectations

In this section we provide the details on how to numerically compute expressions of the form

using numerical solutions of PDEs. Our derivation of the conditional PDE follows the methodology of Dang et al. (2017), and our numerical method to solve the conditional PDEs is Fourier Space Time-Stepping (FST) as developed in Jackson et al. (2008).

2.4.1 Change of Variables

We begin by converting our asset price SDE into log-coordinates yielding the system

where . Next, applying the Cholesky decomposition to the matrix , we find an upper triangular matrix and Brownian motion such that and has independent components. Next, we decompose in block-form as

where

-

•

for ,

-

•

for ,

-

•

for ,

-

•

for , .

We then re-write the system as:

where is the th column of .

In this form, may be simulated first, then inserted into . To this end, define two new processes , on

and note that and . Next, define the function so that

2.4.2 Conditional PDE and Fourier Solution

Finally, we re-write our original expectation in terms of the function

treating as a deterministic path for , . By the Feynman-Kac theorem, the function may be written as the solution of the following PDE

| (5) |

where and .

Applying the Fourier transform to (5) over we obtain

| (6) |

where denotes the inner product on . For each in Fourier space, this ODE may be solved analytically to obtain the following

2.4.3 Numerical Approximation

Defining the characteristic exponent

or more compactly and using the FST’s discretization methodology with fast Fourier transforms (FFT), we have the following recursion

where are the discretizations of , respectively, and denotes the -dimensional Fast-Fourier Transform. A change of variables back to -space then provides an numerical approximation of the original expectation.

2.5 Discussion of Algorithm

We refer the reader to A for a pseudo-code based formal description.

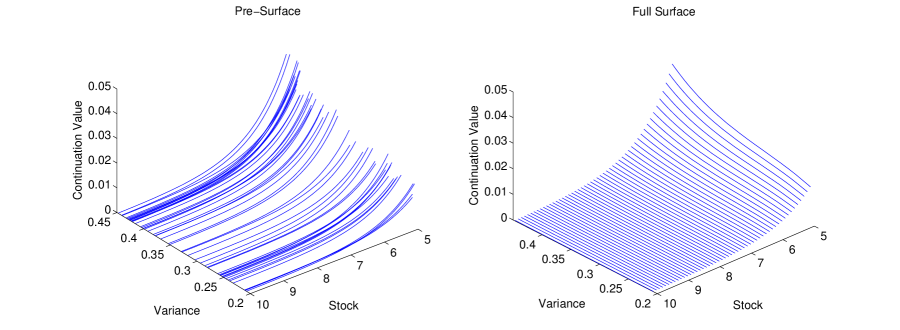

In Section 5, we show that the algorithm accurately, for a given computational budget, determines the time-zero value surface and optimal exercise regions. This may be attributed to the presence of our PDE grid, . When the conditional PDEs are solved along each path, we obtain our pre-surface as described in Subsection 2.3.1. At this point one has two choices: global or local regression. Our regression approach can be viewed as a special type of dimension reduced, local regression which is tailored to the presence of and is equivalent to local regression onto carefully chosen regions. If and , we are regressing onto families of basis functions at the cost of inverting a single matrix of size where is about , and a single matrix-multiplication for each ; the latter step introducing non-trivial costs as increases. The fact that we must only invert a single regression matrix, independent of , at each time step will be made more clear in Section 3. Also, is typically simple to fit as a function of and seems to resist the Basis Selection Problem.

Working with has other advantages as well. In comparison to standard approaches to LSMC, there is a fundamental shift in how we compare the continuation value to the exercise value and locate the exercise boundary. At time , when setting the value of for each we have

and note that is a deterministic constant as opposed to a function of a random variable. Thus, we have reduced the problem of locating the boundary from a global problem over -space to a sequence of lower dimensional problems which are simpler in nature and exhibit less noise. Also, compared to LSMC, instead of an estimate of at a single point, , one obtains a semi-global solution, i.e. a value for all and , owing to the PDE aspect of the algorithm. Obtaining a solution for all allows us to compute sensitivities with respect to with little extra computation.

Generally speaking, deriving the conditional PDE is non-trivial and to the best of our knowledge there are two approaches in the literature: the drift discretization method in Lipp et al. (2013), Cozma and Reisinger (2017), Dang et al. (2015) and the conditionally-affine decomposition of Dang et al. (2017). The drift-discretization approach is fairly general and may be applied to a wide class of models, including those with a non-linear LV component, i.e. stochastic LV models. The resulting PDEs may then be solved using a finite difference type approach as in Lipp et al. (2013). We follow the conditionally-affine approach as it applies to our pure-SV model and avoids time stepping error and drift discretization.

Finally, from the PDE perspective, we begin with a deterministic PDE problem and, using one-way coupling, we convert it to a lower-dimensional stochastic PDE (SPDE) problem. The SPDEs we solve are essentially Black-Scholes equations where the coefficients and terminal condition depend on the random simulated process, . The multi-period aspect of the problem is then handled using regression as outlined above. In light of the connection to SPDEs, in Section 4, we develop a generic Multi-Level Monte-Carlo (MLMC) scheme which completes the algorithm.

3 Theoretical Aspects of the Algorithm

In this section we provide a more theoretical perspective on the mechanics of the algorithm. We begin in Subsection 3.2, where we introduce notions that are needed for the convergence result. In Section 3.2 we derive expressions for the estimated regression coefficients. Subsection 3.4 introduces a truncation scheme to ensure the algorithm is well-defined and Subsection 3.5 shows the algorithm convergence almost surely under certain extra continuity conditions.

3.1 Notation

We denote Euclidean norms of elements or by . Given any function , we write and . Letting be an open subset of we define to be the set of continuous functions on that vanish at infinity. By vanish at infinity, we mean that for every , the set is compact. We also let be the set of compactly supported, continuous functions on .

3.2 Conditional Expectations and the Sampling Space

3.2.1 Filtrations and Conditional Probabilities

We recall the existence of a probability space which accommodates the process satisfying a system of SDEs with a strong, unique solution. In this section, we make rigorous the notion of conditioning on a volatility path.

Let , and i.e., the natural filtrations generated by and , respectively. To extend this notation, we sometimes write for some process . Given , we define a new class of (conditional) probability measures via for .

3.2.2 Conditioning on

In this Section, we make concise the notion of conditioning on a volatility path .

For a realization of and on , which we denote as , there exists a finite-dimensional statistic of the path,

such that the following Markovian-like relation holds

| (7) |

This can be seen from the solution to the derived conditional PDE in Section 2.4 which depend only on the vectors , , and . In our algorithm, when computing regression coefficients, we encounter expectations of the form

where which depend on the statistic To condense notation, we again replace with and simply write

3.2.3 Re-expressing the Conditional Expectation

Equation (7) gives rise to the mappings , defined by

| (8) |

and the conditional probability measures defined via

for . Letting denote the distribution of on our conditional expectation may be written as

so that we have the following relation

| (9) |

3.2.4 Inherited Sampling Probability Space

A consequence of one-way coupling is the ability to simulate paths of independently of . We now make sense of the notion of an iid collection of sample paths of . Since we only realize through the statistics , we only describe how to generate iid copies of .

Denote the ordered subset , and let be the corresponding intervals. Given a path on , define the dimensional matrix

This random matrix induces a measure on . Given , we introduce a new probability space equipped with a collection of independent random matrices

such that each has distribution on . This construction follows from Kolmogorov’s Extension Theorem applied to measures on (for a proof on see Durrett (2010), for more general spaces see Aliprantis and Border (2006)). It then follows that each column has distribution on . Although the process is not defined on , we can still compute relevant expectations involving this process using as defined in (8). We also recall that a random variable on corresponds to an equivalence class of mappings that agree -a.s.

3.2.5 Computing Limits

When taking limits in our algorithm, we consider expressions of the form

where is bounded, which converge to a.s. under by the Strong Law of Large Numbers (SLLN). For our purposes, however, we require convergence to

To establish the equivalence between these expressions:

| (10) |

where the second equality follows from being distributed.

3.3 Continuation Functions

We remind the reader that for each , the random variables are defined on the space and are iid (see the discussion in Section 3.2.4). For notational convenience, we suppose the risk free rate is . As our algorithm is based on the Tsitsiklis and Van Roy (2001) approach to LSMC, many of our expressions are similar.

3.3.1 Idealized Continuation Functions

For each , we consider a family of idealized continuation functions, , which are constructed by means of backwards induction. We begin by writing and for where results from regressing the random variable

for each . The coefficient vector is the vector that minimizes the mapping defined by

| (11) |

where

| (12) |

To minimize , we obtain the first order conditions and obtain the normal equations, resulting in the coefficients

where .

3.3.2 Almost-Idealized Continuation Functions

Next, for a fixed , we define a new type of continuation value, called the almost-idealized continuation functions, . These random variable are obtained by running the dynamic programming algorithm with the idealized continuation value at all times . At time step we then estimate using our paths of and future idealized continuation values. This gives us the following regression coefficients:

where . Note that involves the idealized continuation value at time .

3.3.3 Estimated Continuation Functions

The estimated continuation functions are the continuation functions produced from our algorithm: . The regression coefficients are given by

| (13) |

where

3.4 Truncation Scheme

We now state the following truncation scheme for our least-squares regression. It ensures that the coefficients produced by the algorithm are well defined and converge in a sense to be described later on.

Assumption 1 (Truncation Conditions).

-

1.

The basis functions are bounded and supported on a compact rectangle.

-

2.

The inverse of the regression matrix satisfies provided the inverse is defined.

-

3.

For each , the exercise values are bounded with compact support in .

Condition (1) may be imposed by limiting the support of on a bounded domain as they are typically smooth. By making to be a very large rectangle, the value function is essentially unaffected.

Condition (2) is imposed by replacing with where is the indicator of the event that is uniformly bounded by some constant . If then we have -a.s. Again, by making a very large constant, this has essentially no effect on the values obtained by the algorithm.

Condition (3) on the functions are always satisfied in practice as numerically solving a PDE involves truncation of ’s domain.

Lemma 1.

Given the truncation conditions, the functions defined in (11) are finite valued for all .

The proof is omitted due to its simplicity. The next lemma establishes a useful relationship between the idealized, almost idealized and estimated coefficients.

Lemma 2.

Let , . There exists a constant, , which depends on our truncation conditions, such that

where

and

| (14) |

3.5 Almost-Sure Convergence Under Pure SV Models

In this section we prove that the coefficients also converge almost surely for a class of models with certain separability conditions that are satisfied by our SV model.

Assumption 2 (Separability Conditions).

Let

-

1.

The process , for all , takes values in

-

2.

If almost surely, i.e., the process begins at at time , then where does not depend on the value of . takes values in a.s.

-

3.

The exercise function, , is continuous with compact support in . The basis functions are compactly supported and continuous on .

Condition (1) limits our analysis to assets which take only positive values such as equities and foreign exchange rates.

Condition (2) allows us to separate our future asset price as a product of its current price and return. The assumption that take values in implies that they are finite valued a.s. As a result, letting , there exists tuples , where such that

| (17) |

satisfies We also write

Given , we may find an open set such that and . By Urysohn’s Lemma/Tietze’s Extension theorem (see Munkres (2000)), there exists a map such that on , on and , i.e. a bump function supported on . In most cases, our notation will suppress dependence on .

Condition (3) allows us to apply the Stone-Weierstrass (SW) theorem which underlies the ‘separation technique’ that will be demonstrated in upcoming Lemmas. We apply the version of SW for functions on unbounded domains that vanish at infinity (See Folland (1999)). Suppose we are given the payoff function for a call option, i.e. where . To modify such that it falls within our assumption, we first truncate its support to obtain a function where is large number. Finally, we continuously extend on such that on where . A similar construction may be done for a put option payoff near 0, and payoffs on higher dimensional domains.

Under these assumptions, we have the following main result.

Theorem 1.

Let and be fixed. Then we have

-almost surely

Theorem 1 tells us that for almost every choice of sequence of paths, our coefficients based on these paths converge to the true idealized coefficient. It then follows, since , that the continuation values, option prices, and optimal exercise boundaries also converge almost surely (up to our basis assumption’s bias).

The proof borrows ideas from Tsitsiklis and Van Roy (2001) and Clément et al. (2002) and takes the following steps

-

1.

Lemma 3. Carry out a geometric construction that allows us to approximately separate functions of that are continuous and compactly supported in . The function that provides the approximate separation is denoted as .

-

2.

Lemma 4. Use the geometric construction to show the explicit relationship between and the separating functions, and thus demonstrate what is referred to as a separating estimate.

-

3.

Lemma 5. Prove the theorem for and also obtain an almost-sure separating estimate for .

- 4.

-

5.

Lemma 7. Develop an almost-sure separating estimate for for all .

- 6.

Lemma 3.

Let and be continuous and compactly supported in . Let be defined via

where results from (17). There exists a map of the form

such that and

Proof.

It follows from the properties of the mapping and compact support of and , that is compactly supported in . We also have that is continuous on .

To construct , we begin by defining the algebra of functions

and show is dense in under the uniform metric.

Given two distinct points , without loss of generality, we assume . We now find bump functions that separate , i.e., , , along with a bump function that is supported on and . Letting and , we have that separates points. Since contains bump functions supported at each point , it vanishes nowhere. ∎

Lemma 4.

Let and be continuous and supported in . Let be as in the statement of Lemma 3 and be a separable -approximation of . There exists a random variable and function such that

where for all where depend only on our truncation and separability conditions.

Proof.

We will only show the first relation as they are similar.

It then follows that for all and , where depend on our truncation and separability conditions. Finally, we set . ∎

Lemma 5.

Let . We have

a.s., where are random variables that depend on and a.s., satisfy the conditions of Lemma 4 and depends on our truncation and separability conditions.

Proof.

Given we have

By Lemma 4 we can find a constant and a separable -approximation, such that

where the last line follows from interchanging the summations, depends on our truncation and separability conditions and

By the SLLN, a.s. for all . ∎

Lemma 6.

Proof.

Lemma 7.

Proof.

We break the proof up into multiple stages.

Preliminary estimates on .

Let be as defined in (12). We begin by showing that for each that

where , with depending on our truncation conditions and separability conditions. The functions admit the representation where and . Finally . To this end, we let and have that

| (18) |

where is as in (3.5) and focus on the second term. We let

and apply Lemma 3 to find an -separating function of the form where and . This allows us to write

where and with depending on our truncation and separability conditions.

Returning to our expression in , we find

where for all , depends on our truncation and separability conditions, and

We now turn to

Equating to the term in brackets and , gives us the required form and concludes the claim for .

Now let , we have

where is as in (17) so that , and focus on the final term. By assumption, where . Letting , we are led to consider the function

where . Before carrying out a construction very similar to the case, we let Next, we note that

and find a function of the form such that , and

Finally, we write where

so that for , we have where depend on our truncation and separability conditions and Also we have that . Writing and to be the final term completes the claim for . Showing the result for is analogous to the base case and so we omit the proof.

Estimates of

We write

where and depend on our truncation conditions. We now focus on the expression within our expectations and define the function

Applying techniques that are exactly analogous to previous steps, we obtain a separating estimate for of the form where is appropriately bounded and . This leads to where again depends on our truncation conditions and

By the SLLN, for each , we have that a.s completing the proof. ∎

Proposition 1.

Let and . We have

| (19) |

a.s. where

a.s. and

almost-surely. The bounds on depend on our truncation and separability conditions and satisfy the conditions of Lemma 3.

By taking limits on both sides, and noting the properties of the random variables, mappings, and constants described, the main theorem then follows.

Proof of Proposition.

We begin by letting and by Lemma 14 and Lemma 6 we have almost-surely

| (20) | |||

| (21) |

Line (20) may be handled just as in the proof of Lemma 6. As for line (21), we use Lemma 7 and write

where a.s. and we apply the usual separation technique, the details of which we omit. We then obtain

almost-surely which corresponds to and the above random variables satisfy the necessary conditions. The remainder of the induction works exactly analogously to the base case and proofs of the previous Lemmas which establishes the Proposition. ∎

4 Overview of Complexity and Multi-Level Monte Carlo/Multi-Grids

By viewing our conditional PDEs from the SPDE perspective, we are naturally led to consider Multi-Level Monte Carlo (MLMC)/multi-grid methods as in Giles (2015) to reduce the complexity. For the direct estimator, our coefficients depend on the expectation of the solutions of our SPDEs, which may be computed using MLMC. Also, the low estimator is expressed as an expectation which may be computed using MLMC. The MLMC adjustment tends to reduce the run times by at least an order of magnitude. MLMC approaches have also appeared in the mixed MC-PDE works of Ang (2013) and Dang (2017).

A pseudo-code description of the methodology based on this idea, and outlined below, is provided in Algorithm 3 in A.

4.1 Multi-Level Monte Carlo/Multi-Grids

4.1.1 MLMC for Computing the Estimated Coefficients

Assume we have independent simulations of on , denoted , with paths where . Also, let denote the numerical solution of the conditional PDE on the th path with grid resolutions , in each dimension, over where .

Using the usual multi-level MC appoach, we may write

| (22) |

where each of is interpolated to have a resolution that matches the grid at level .

4.1.2 MLMC for Low Biased Estimates of the Time Zero Price

We again carry out independent simulations of on , denoted as , with paths where . Letting denote the numerical solution of the conditional PDE on the th path with grid resolution over where we have

where again we interpolate the lower resolution grids to match the highest resolution grid. We do not provide a pseudo-code description for this part as it is relatively simple.

4.2 An Overview of Complexity

While a complete complexity analysis lies outside the scope of this paper, we provide an overview of the sources of costs and error, along with a discussion of the complexity of our MLMC-FST scheme.

The direct estimator has three main stages: simulation of paths, solution of conditional PDEs, and the regression step. Assuming an Euler discretization for the simulation of paths, the FST method to solve the conditional PDEs, and Gauss-Jordan elimination for inverting , we obtain the following expression for the algorithm’s cost:

The terms in correspond to the costs of constructing , computing its inverse and multiplying to a length vector at each of the regression sites.

We make the following rough estimate of the algorithm’s error at a single point of our grid, ,

where determining is a topic for future papers. For other forms of LSMC, the structure of has been investigated in Glasserman et al. (2004), Stentoft (2004), Egloff (2005), Belomestny (2011). Another important question for future papers is how the quantities contribute to the error, and ought to be optimally balanced, especially in the context of MLMC that we discuss below.

In Sections 5, alongside implementing the hybrid LSMC/PDE algorithm for Heston-type models, we also investigate how the bias, variance, and cost behave on the various levels of our MLMC-FST scheme in the context of single-period expected values. By the general multi-level theorem (GMLT) (see Cliffe et al. (2011) and Giles (2015)), we are able to suggest a bound for the complexity of the MLMC-FST component in isolation from the rest of the algorithm. The choice of the highest resolution level for the PDE stage may not be optimal for the entire algorithm as the finest grid is used in the regression stage. The optimal choice of the finest grid should also take the costs and errors of the regression into account; a topic we do not fully address in this paper. On the other hand, the GMLT sheds light on the potential improvements brought about by MLMC to the main bottle-neck of the algorithm. The work of Giles (2015) also provides an optimal allocation scheme for the number of paths on each level, however, the traditional scheme is for a scalar-valued single-period problem as opposed to a vector-valued multi-period problem. While our MLMC scheme deals primarily with the grids used to solve the PDEs, one could also incorporate multiple discretization levels for the simulated paths, . Since the main bottle neck of the algorithm tends to lie with the PDE stage, we leave the paths out of our MLMC scheme for simplicity.

5 Numerical Examples

In this section, we compare the performance of our algorithm to the standard LSMC algorithm for:

-

1.

Heston model

where .

-

2.

Multi-dimensional Heston (mdHeston) model

where is a 4-dimensional Brownian motion with full correlation structure .

We price a Bermudan option with payoff function . In each case, we show results for time-zero prices and optimal exercise boundaries (OEBs). For the standard Heston model, we also implement an explicit finite difference method which we regard as a reference solution as opposed to a benchmark. Finally, we carry out the MLMC-FST tests discussed in Section 4.

5.1 Procedures and Settings for the Main Algorithm and MLMC-FST tests

We provide a brief procedure for our tests along with Tables 1–8 showing our option and model parameters.

5.1.1 Main Algorithms

-

1.

Carry out of the direct and low estimator for various grid resolutions and numbers of paths. Compute the mean prices and their standard deviations.

-

•

For the Heston model, report the reference price from the finite difference scheme.

-

•

-

2.

For each of the , using the coefficients from the direct estimator, compute the OEB. By averaging over each grid point, obtain the mean OEB.

-

•

For the Heston model, report the reference OEB from the finite difference scheme.

-

•

For the multi-dimensional Heston model, report only certain slices of the average OEB.

-

•

5.1.2 MLMC-FST Level Tests

-

1.

For each level , compute over . The quantity corresponds to the solution of the conditional PDE solved at a relatively high resolution, .

-

2.

For each level , compute over .

-

3.

For each level , measure the expected CPU time for computing , over .

| Method | Basis Functions |

|---|---|

| LSMC | for |

| , and , | |

| LSMC/PDE | for , |

| Model Type | Payoff | Exercise Frequency | ||

|---|---|---|---|---|

| Heston | 1 | |||

| mdHeston | 1 |

| 0.02 | 5 | 0.16 | 0.9 |

| 0.025 | 10 | 0.45 | 1.52 | 0.45 | 0.4 | 10 | 0.3 | 1.3 | 0.30 | 0.43 |

| 0 | 1 | 0 | 53 |

| Model Type | Basis Degree | |

|---|---|---|

| Heston | 3 | |

| mdHeston | 4 |

| Model Type | |||

|---|---|---|---|

| Heston/mdHeston | 0 | ||

| Heston/mdHeston | 1 | ||

| Heston/mdHeston | 2 |

| Model Type | Basis Degree |

|---|---|

| Heston | 3 |

| mdHeston | 3 |

| Est. Type | Run Time (s) | ||||

|---|---|---|---|---|---|

| Direct | 1.6747 (0.0011) | 1.4541 (0.0012) | 1.2598 (0.0013) | 7 | |

| Low | 1.6746 (0.0013) | 1.4540 (0.0015) | 1.2597 (0.0016) | 6 | |

| Direct | 1.6739 (0.0013) | 1.4534 (0.0014) | 1.2591 (0.0015) | 7 | |

| Low | 1.6738 (0.0012) | 1.4532 (0.0013) | 1.2588 (0.0014) | 6 | |

| Direct | 1.6735 (0.0011) | 1.4530 (0.0013) | 1.2586 (0.0014) | 7 | |

| Low | 1.6735 (0.0014) | 1.4529 (0.0016) | 1.2585 (0.0017) | 6 |

| Estimate Type | Run Time (s) | |

|---|---|---|

| Direct | 1.4494 (0.0020) | 47 |

| Low | 1.4487 (0.0023) | 38 |

| Slope Type | Estimate | |

|---|---|---|

| 2.12 | 0.9993 | |

| 4.16 | 0.9989 | |

| 0.30 | 0.9409 |

| Est Type | Run Times (s) | ||

|---|---|---|---|

| Direct | 1.1853 (0.0055) | 67 | |

| Low | 1.1852 (0.0049) | 43 | |

| Direct | 1.1834 (0.0055) | 102 | |

| Low | 1.1833 (0.0049) | 64 | |

| Direct | 1.1836 (0.0057) | 177 | |

| Low | 1.1830 (0.0060) | 105 |

| Est Type | |||||

|---|---|---|---|---|---|

| Direct | 1.2526 (0.0056) | 1.1209 (0.0054) | 1.2846 (0.0056) | 1.0931 (0.0054) | |

| Low | 1.2525 (0.0050) | 1.1208 (0.0049) | 1.2845 (0.0050) | 1.0940 (0.0048) | |

| Direct | 1.2506 (0.0055) | 1.1191 (0.0054) | 1.2826 (0.0056) | 1.0914 (0.0054) | |

| Low | 1.2506 (0.0050) | 1.1190 (0.0049) | 1.2825 (0.0050) | 1.0913 (0.0048) | |

| Direct | 1.2508 (0.0058) | 1.1194 (0.0057) | 1.2828 (0.0058) | 1.0916 (0.0056) | |

| Low | 1.2502 (0.0061) | 1.1187 (0.0059) | 1.2821 (0.0061) | 1.0910 (0.0059) |

| Estimate Type | Run Times (s) | |

|---|---|---|

| Direct | 1.2121 (0.0016) | 83 |

| Low | 1.1765 (0.0018) | 73 |

| Slope Type | Estimate | |

|---|---|---|

| 2.03 | 0.9995 | |

| 2.63 | 0.9640 | |

| 1.65 | 0.9785 |

5.2 Discussion of Results

We provide a discussion of the results from the two examples we investigated above. We first provide example-specific comments for each model, followed by comments which apply to both examples.

5.2.1 Heston model

Our choice of parameters for this problem are borrwed from Ikonen and Toivanen (2008) with a lower value for , the risk free rate, and higher maturity. We also differ in that we value a Bermudan option instead of an American.

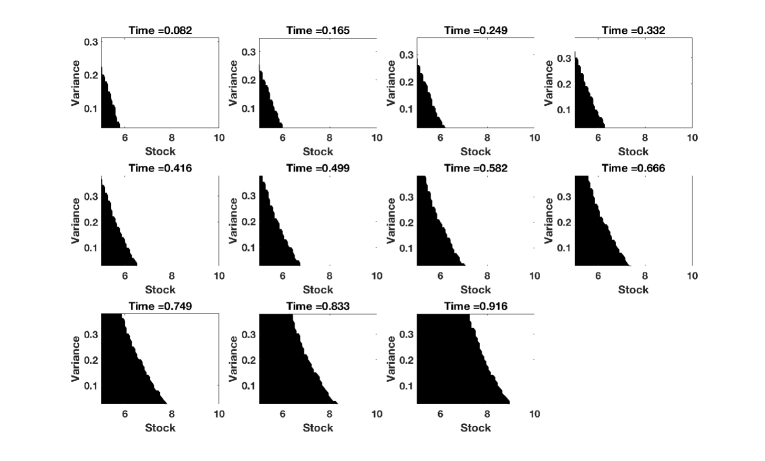

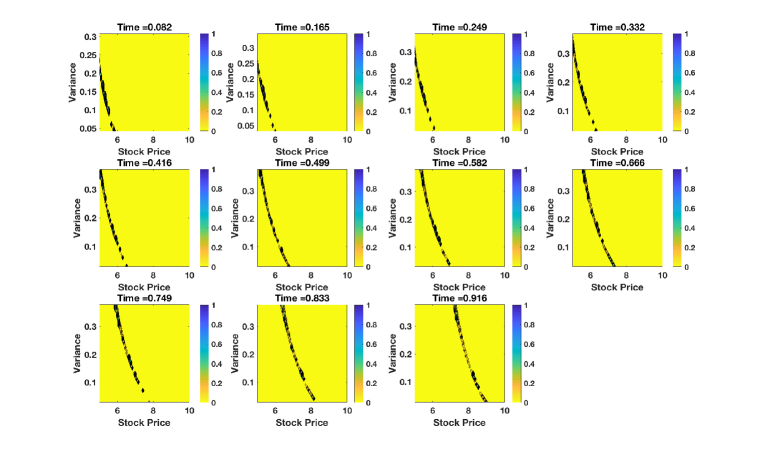

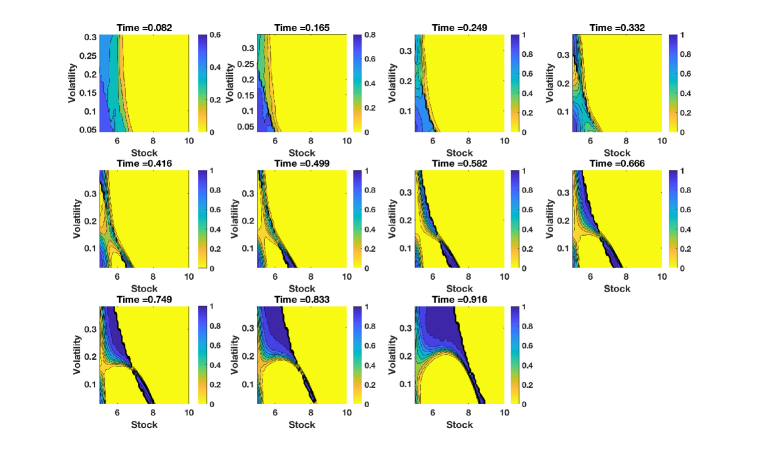

Based on Figure 3, we see the hybrid algorithm’s errors appear along the interface of the holding and exercise regions and it is able to closely approximate the true boundary across all exercise dates. The consistency arises from the comparison of the exercise value and continuation value being broken into a collection of cross-sectional comparisons for each as discussed in Section 2. At time , for each , we have an estimate of the function which is monotonically increasing in . Our goal is then to locate the points such that which is simple to compute since is a deterministic constant. We do, however, see some noise in determining across trials which is due to randomness in . From Figures 4, we see that the LSMC boundary is not particularly accurate for all exercise dates, with greater accuracy at the later dates. This is due to the accumulation of errors as one moves recursively through time and the lack of paths that are in-the-money at earlier exercise dates.

As indicated in Tables 9 and 10 the hybrid algorithm is better able to estimate time-zero prices, in comparison to the reference value. This accuracy in our prices follows from the quality of our optimal exercise boundaries (OEBs). We note that the direct estimator and low estimator are fairly close to each other and suggest that the low estimator is somewhat redundant in this case. The full LSMC algorithm also provides a direct estimate of the price that is also close to the low estimator, however, this price is biased too low as evidenced by the reference value. Since the low estimate of the LSMC-PDE algorithm is higher than the low estimate of the LSMC algorithm, by definition it is better. We also note the hybrid algorithm provides estimates for other and fixed , as opposed to a single point in LSMC. The non-ATM price estimates are of the same quality as the ATM estimate.

For run-times, we see that regardless of the choice of , the run times remain effectively unchanged which implies the conditional PDEs solved at are highly out-weighed by the work done at resolutions . We also see the direct estimator takes an extra second compared to the low estimator, roughly implying that the multi-grid PDE stage takes approximately of the run time.

Lastly, there is some discrepancy in the prices obtained by finite differences and the LSMC-PDE algorithms, mostly in the third decimal place. This discrepancy is likely due to the bias introduced from path discretization, interpolation of time-zero prices, and spatial discretization.

It is worth noting that the PDE approach is best for this example as it has lower complexity. This example is used to demonstrate the performance of the LSMC-PDE algorithm in a fully observable setting.

5.2.2 Multi-dimensional Heston model

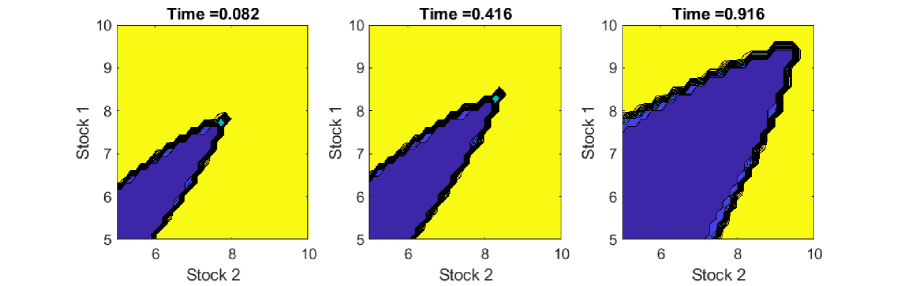

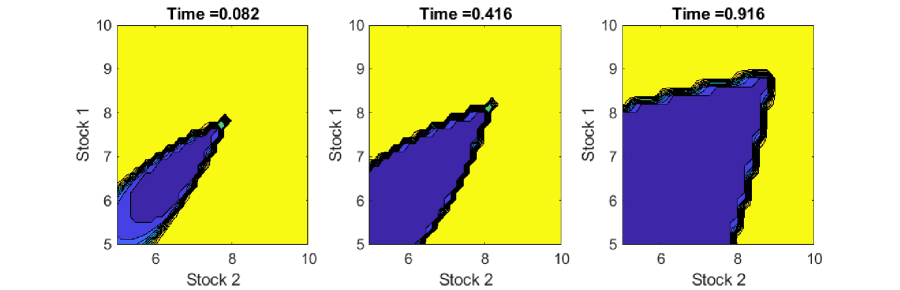

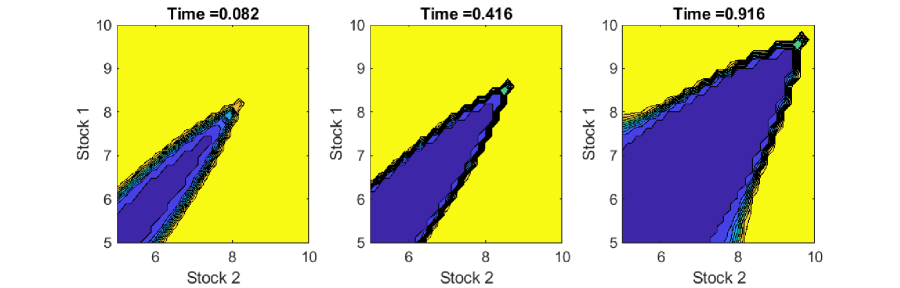

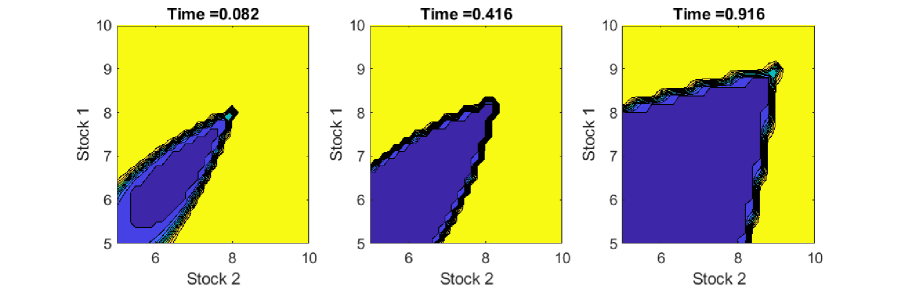

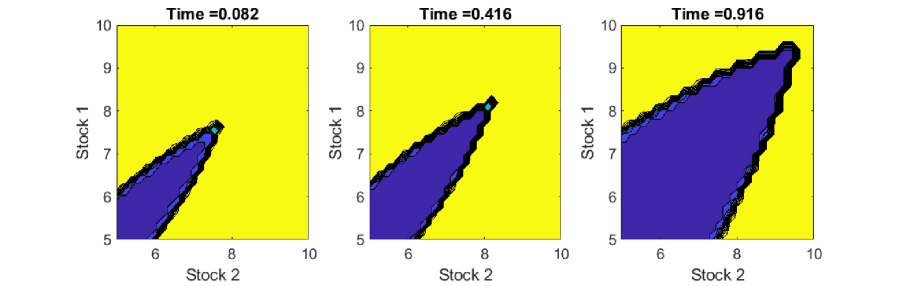

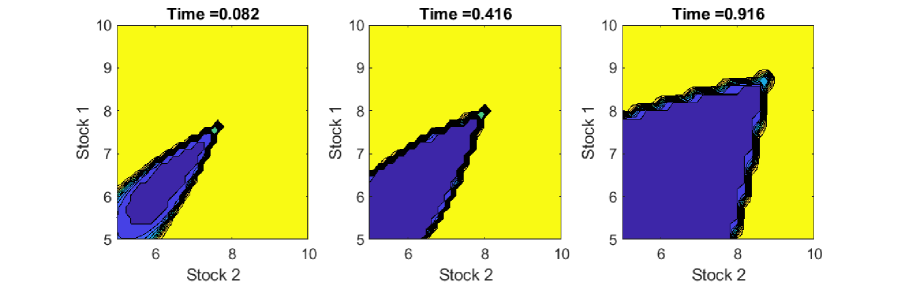

As our OEBs are four-dimensional objects, they are not fully observable; hence we show -slices of the OEB, as we have some intuition about how they should look. In Figures 5, 6, 7, we show three types of slices , the ‘central slice’, along with two other off-center slices. For brevity we show only the last, middle, and first exercise dates.

Overall the hybrid and LSMC algorithm have comparable precision in determining the region over 100 trials. However, we note that the boundaries produced by the LSMC-PDE algorithm are considerably different, just as in the standard Heston model. In looking at the price estimates in Tables 12, 13, we see that the lower estimates produced by the hybrid algorithm are generally lower, and so we are more inclined to trust the OEBs produced by the hybrid algorithm.

In terms of price estimates, the tightness of the direct and low estimator for LSMC-PDE suggest that, again, the low estimator is somewhat redundant. In this case, for LSMC, the direct estimator is considerably higher than the low estimator; indicating a relatively high degree of bias introduced by the regression scheme. We also note that, again for the hybrid algorithm, we are able to get accurate non-ATM price estimates. This suggests LSMC boundary is consistently wrong in many places.

Looking at run times, we see that unlike in the standard Heston model, the PDEs solved at resolution weigh significantly on the run times. Also, for the direct estimator, we see that the PDE stage typically takes approximately of the run time, indicating an increase in regression costs compared to the standard Heston model.

5.2.3 Overall Comments

Our choice of MLMC scheme was for simplicity and conservativeness, and hence not optimized, as alluded to before.

One issue that arises from our results is the question of whether the hybrid algorithm is more efficient. For the Heston model, we see that the hybrid algorithm provides substantial variance reduction in time zero prices and OEBs especially given that LSMC was allowed a larger computational budget. It is interesting to note, however, that while the standard deviations for prices are relatively close to each other, the OEBs for LSMC “seem” much noisier than the hybrid algorithm’s, although this is based on subjective examination. For the multi-dimensional Heston model, we note that the variance of the hybrid algorithm’s prices, for a comparable computational budget, is higher, although their boundaries have very similar levels of noisiness. This again points to a disconnect in the variance of the two estimated objects. On the other hand, it is important to note that for the hybrid algorithm, we obtain prices for all and not simply the ATM point, as in standard LSMC. Having the prices for these also allows us to compute the and of the option without any extra simulations. As a result, the hybrid algorithm provides considerably more information than standard LSMC. Also, the information provided by the hybrid algorithm tends to be more accurate in terms of quality of the boundary and bias, as noted before.

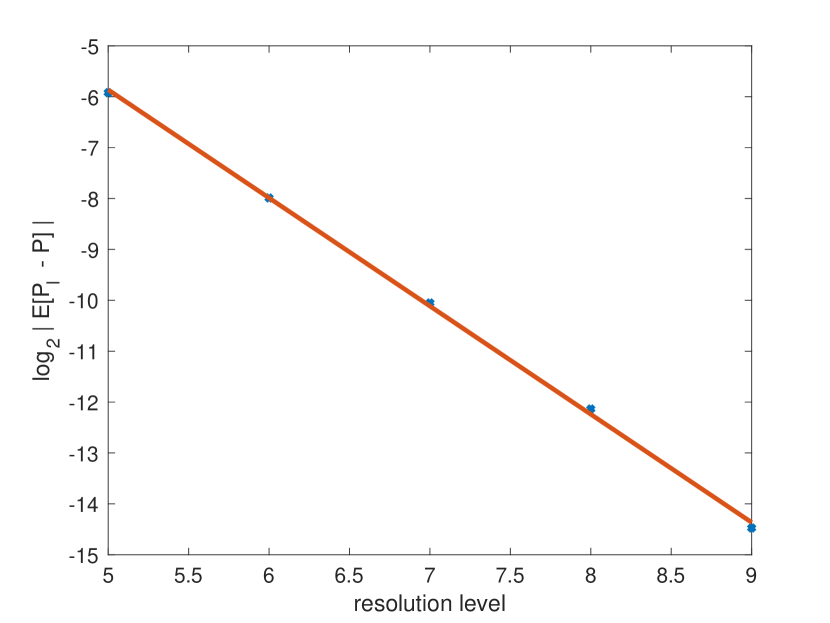

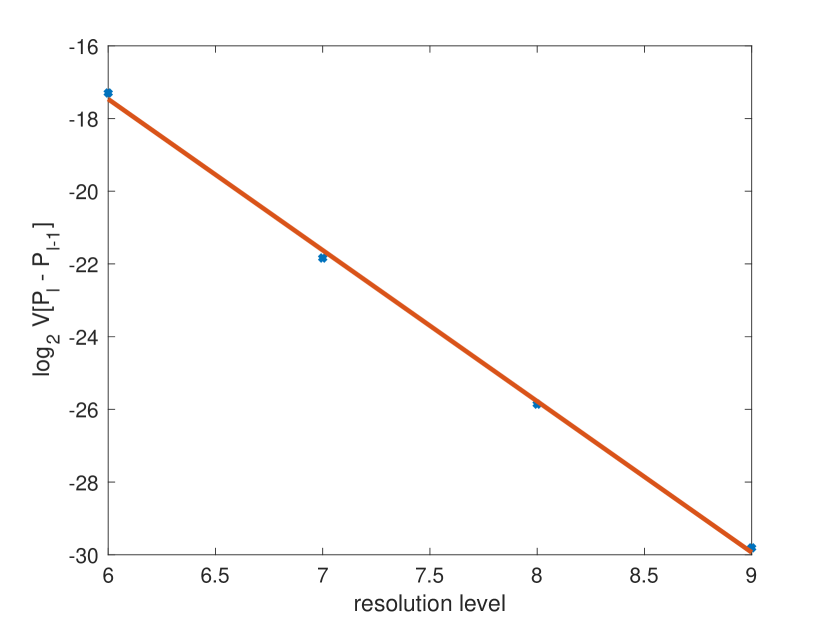

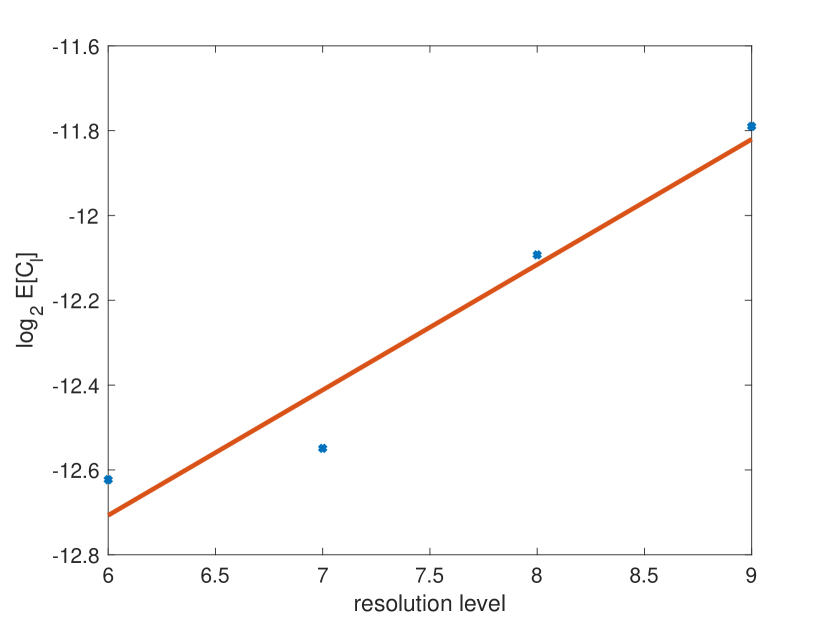

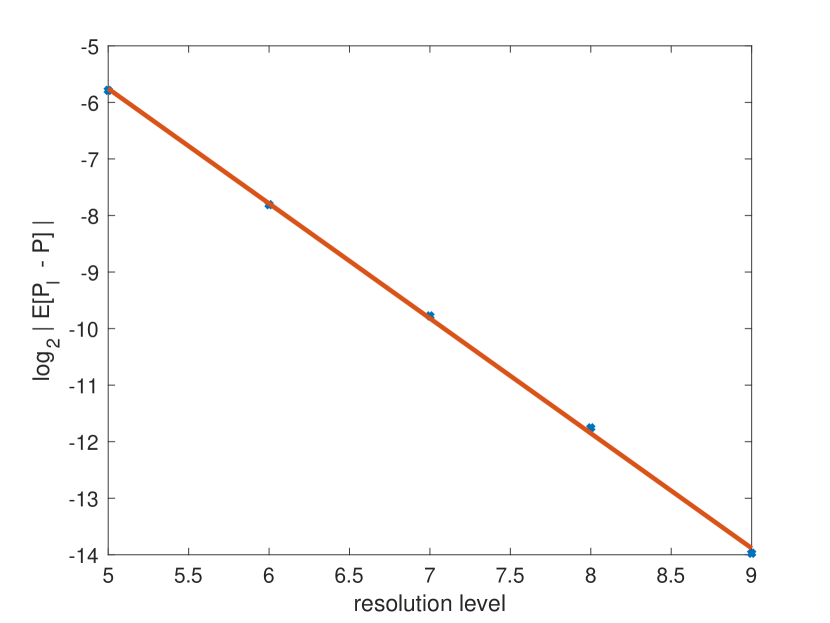

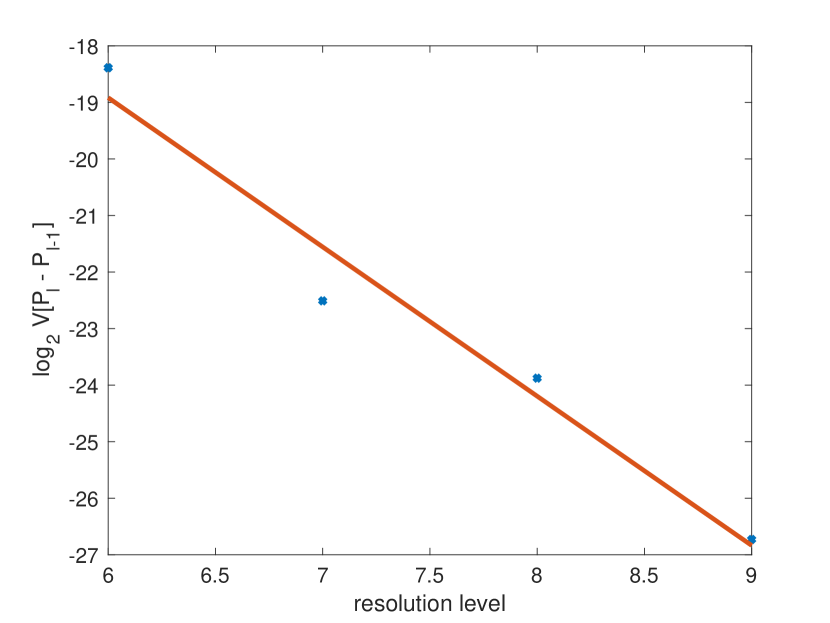

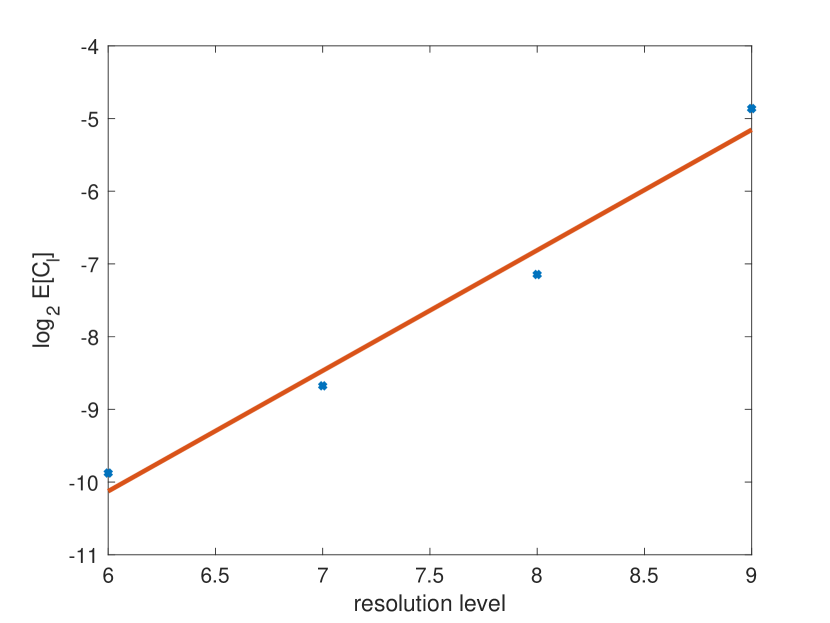

Next, we turn to our MLMC-FST tests. From Table 11 and 14 and Figures 11 to 15, by the GMLT it is suggested, since , and , that optimal complexity is attainable. That is, there exists a collection of levels and a path allocation such that one can obtain a RMSE of with cost (up to a certain time-step resolution). This, again, is for our single-period computations in isolation from the entire hybrid algorithm. As one moves from the example to the example, we see that the accuracy across levels, measured by , remains unchanged. On the other hand, the variances and costs increase considerably as we increased the number of volatility processes and dimension of . These results suggest that we may not conclude optimal complexity, via the GMLT, in the case when , analogue, although we leave this investigation to future study.

All run times were measured on a 3.60 GHz Intel Xeon CPU using Matlab 2016. For the results in Tables 9 to 13 all run-times were measured by repeating the following process three times: clearing the memory, running the algorithm, and measuring the run time. The reported run time was then taken to be the maximum of the three.

6 Conclusions

By combining conditional PDEs with the LSMC approach of Tsitsiklis and Van Roy (2001), we have developed an algorithm that improves traditional LSMC methods in the context of SV models for medium dimensional problems. The hybrid algorithm also provides an extension of PDE methods beyond lower dimensional problems, at the expense of variance and a semi-global solution.

From a theoretical perspective we provide a proof of almost-sure convergence which uses geometric arguments and requires a few modifications to the basis, regression matrix, and payoff function. The proof is also highly dependent on separability of the model. Future research into theoretical properties of the algorithm ought to search for a proof with more natural assumptions and farther reach in terms of types of SV models. Another important point is that the proof is for a stylized form of the algorithm where is a continuum rather than a finite grid of points. It seems a more appropriate proof would make assumptions on the properties of the conditional expectations, viewing them as numerical solutions of the conditional PDE. As discussed in Section 4, a major question is quantifying the rate of convergence which essentially requires a Central Limit Theorem type result as one component. To obtain this result, it would appear that our separation technique will not carry over, and so one would likely again require a more sophisticated treatment of the conditional expectation functions. Our treatment in Section 4 essentially assumes a CLT holds. With a quantification of the error associated to the regression scheme, one can then quantify the entire algorithm’s complexity; a topic for future work. Also, as alluded to before, there is a need to find an optimal allocation scheme for the MLMC component of the algorithm and prove convergence under this scheme.

7 Bibliography

References

- Agarwal et al. (2016) Agarwal, A., S. Juneja, and R. Sircar (2016). American options under stochastic volatility: control variates, maturity randomization & multiscale asymptotics. Quantitative Finance 16(1), 17–30.

- Ait Sahlia et al. (2010) Ait Sahlia, F., M. Goswami, and S. Guha (2010). American option pricing under stochastic volatility: an efficient numerical approach. Computational Management Science 7(2), 171–187.

- Aliprantis and Border (2006) Aliprantis, C. and K. Border (2006). Infinite dimensional analysis: A hitchhiker’s guide. Springer.

- Ang (2013) Ang, X. X. (2013). A mixed PDE/Monte Carlo approach as an efficient way to price under high-dimensional systems. Master’s thesis, University of Oxford.

- Belomestny (2011) Belomestny, D. (2011). Pricing Bermudan options by nonparametric regression: optimal rates of convergence for lower estimates. Finance and Stochastics 15(4), 655–683.

- Bouchard and Warin (2012) Bouchard, B. and X. Warin (2012). Monte-Carlo valuation of American options: facts and new algorithms to improve existing methods. In Numerical Methods in Finance, pp. 215–255. Springer.

- Christoffersen et al. (2009) Christoffersen, P., S. Heston, and K. Jacobs (2009). The shape and term structure of the index option smirk: Why multifactor stochastic volatility models work so well. Management Science 55(12), 1914–1932.

- Clément et al. (2002) Clément, E., D. Lamberton, and P. Protter (2002). An analysis of a least squares regression method for American option pricing. Finance and Stochastics 6(4), 449–471.

- Cliffe et al. (2011) Cliffe, K. A., M. B. Giles, R. Scheichl, and A. L. Teckentrup (2011). Multilevel Monte Carlo methods and applications to elliptic PDEs with random coefficients. Computing and Visualization in Science 14(1), 3.

- Cozma and Reisinger (2017) Cozma, A. and C. Reisinger (2017). A Mixed Monte Carlo and Partial Differential Equation Variance Reduction Method for Foreign Exchange Options Under the Heston–Cox–Ingersoll–Ross Model. Journal of Computational Finance, Forthcoming 20(3), 109–149.

- Dang (2017) Dang, D.-M. (2017). A multi-level dimension reduction Monte-Carlo method for jump–diffusion models. Journal of Computational and Applied Mathematics 324, 49–71.

- Dang et al. (2015) Dang, D.-M., K. R. Jackson, and M. Mohammadi (2015). Dimension and variance reduction for Monte Carlo methods for high-dimensional models in finance. Applied Mathematical Finance 22(6), 522–552.

- Dang et al. (2017) Dang, D.-M., K. R. Jackson, and S. Sues (2017). A dimension and variance reduction Monte-Carlo method for option pricing under jump-diffusion models. Applied Mathematical Finance, 1–41.

- Durrett (2010) Durrett, R. (2010). Probability: theory and examples. Cambridge University Press.

- Egloff (2005) Egloff, D. (2005). Monte Carlo algorithms for optimal stopping and statistical learning. The Annals of Applied Probability 15(2), 1396–1432.

- Farahany (2018) Farahany, D. (2018). Mixing Monte Carlo and Partial Differential Equation Methods for Multi-Dimensional Optimal Stopping Problems Under Stochastic Volatility. Ph. D. thesis, University of Toronto.

- Feng et al. (2010) Feng, J., M. Forde, and J.-P. Fouque (2010). Short-maturity asymptotics for a fast mean-reverting Heston stochastic volatility model. SIAM Journal on Financial Mathematics 1(1), 126–141.

- Folland (1999) Folland, G. B. (1999). Real analysis: modern techniques and their applications. Wiley.

- Giles (2015) Giles, M. B. (2015). Multilevel Monte Carlo methods. Acta Numerica 24, 259–328.

- Glasserman et al. (2004) Glasserman, P., B. Yu, et al. (2004). Number of paths versus number of basis functions in American option pricing. The Annals of Applied Probability 14(4), 2090–2119.

- Gramacy and Ludkovski (2015) Gramacy, R. B. and M. Ludkovski (2015). Sequential design for optimal stopping problems. SIAM Journal on Financial Mathematics 6(1), 748–775.

- Grasselli (2017) Grasselli, M. (2017). The 4/2 stochastic volatility model: A unified approach for the Heston and the 3/2 model. Mathematical Finance 27(4), 1013–1034.

- Haugh and Kogan (2004) Haugh, M. B. and L. Kogan (2004). Pricing American options: a duality approach. Operations Research 52(2), 258–270.

- Heston (1993) Heston, S. L. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options. The Review of Financial Studies 6(2), 327–343.

- Hull and White (1987) Hull, J. and A. White (1987). The pricing of options on assets with stochastic volatilities. The journal of finance 42(2), 281–300.

- Ikonen and Toivanen (2008) Ikonen, S. and J. Toivanen (2008). Efficient numerical methods for pricing American options under stochastic volatility. Numerical Methods for Partial Differential Equations 24(1), 104–126.

- Jackson et al. (2008) Jackson, K. R., S. Jaimungal, and V. Surkov (2008). Fourier space time-stepping for option pricing with Lévy models. Journal of Computational Finance 12(2), 1–29.

- Jain and Oosterlee (2015) Jain, S. and C. W. Oosterlee (2015). The stochastic grid bundling method: Efficient pricing of Bermudan options and their Greeks. Applied Mathematics and Computation 269, 412–431.

- Lewis (2002) Lewis, A. L. (2002). The mixing approach to stochastic volatility and jump models. Wilmott.

- Lipp et al. (2013) Lipp, T., G. Loeper, and O. Pironneau (2013). Mixing Monte-Carlo and partial differential quations for pricing options. Chinese Annals of Mathematics, Series B 34(2), 255–276.

- Loeper and Pironneau (2009) Loeper, G. and O. Pironneau (2009). A mixed PDE/Monte-Carlo method for stochastic volatility models. Comptes Rendus Mathematique 347(9), 559–563.

- Longstaff and Schwartz (2001) Longstaff, F. A. and E. S. Schwartz (2001). Valuing American options by simulation: a simple least-squares approach. Review of Financial Studies 14(1), 113–147.

- Ludkovski (2018) Ludkovski, M. (2018). Kriging metamodels and experimental design for Bermudan option pricing. Journal of Computational Finance 22(1), 37–77.

- Munkres (2000) Munkres, J. R. (2000). Topology. Prentice Hall.

- Rambharat and Brockwell (2010) Rambharat, B. R. and A. E. Brockwell (2010). Sequential Monte Carlo pricing of American-style options under stochastic volatility models. The Annals of Applied Statistics 4(1), 222–265.

- Rogers (2002) Rogers, L. C. (2002). Monte Carlo valuation of American options. Mathematical Finance 12(3), 271–286.

- Ruijter and Oosterlee (2012) Ruijter, M. J. and C. W. Oosterlee (2012). Two-dimensional Fourier cosine series expansion method for pricing financial options. SIAM Journal on Scientific Computing 34(5), B642–B671.

- Stein and Stein (1991) Stein, E. M. and J. C. Stein (1991). Stock price distributions with stochastic volatility: an analytic approach. The review of financial studies 4(4), 727–752.

- Stentoft (2004) Stentoft, L. (2004). Convergence of the least squares Monte Carlo approach to American option valuation. Management Science 50(9), 1193–1203.

- Tsitsiklis and Van Roy (2001) Tsitsiklis, J. N. and B. Van Roy (2001). Regression methods for pricing complex American-style options. IEEE Transactions on Neural Networks 12(4), 694–703.

- Wang and Caflisch (2010) Wang, Y. and R. Caflisch (2010). Pricing and hedging American-style options: a simple simulation-based approach. The Journal of Computational Finance 13(4), 95.

Appendix A Formal Algorithm Descriptions

A.1 LSMC-PDE Algorithm

A.2 MLMC/Multi-Grids

We provide guidelines for computing over the time interval in a manner that keeps the number of interpolations to a minimum. Given our coefficient matrix at level , we carry out the following.

Appendix B Optimal Exercise Boundaries

Appendix C MLMC-FST Test Plots