Quantile correlation coefficient: a new tail dependence measure

Ji-Eun Choi and Dong Wan Shin111Corresponding author. Mailing Address: Dept. of Statistics, Ewha University, Seoul, Korea. Tel: 82-2-3277-2614; Fax: 82-2-3277-3606; E-mail address: shindw@ewha.ac.kr (D.W. Shin)

Department of Statistics, Ewha University

March 16, 2018

Abstract. We propose a new measure related with tail dependence in terms of correlation: quantile correlation coefficient of random variables X, Y. The quantile correlation is defined by the geometric mean of two quantile regression slopes of X on Y and Y on X in the same way that the Pearson correlation is related with the regression coefficients of Y on X and X on Y. The degree of tail dependent association in X, Y, if any, is well reflected in the quantile correlation. The quantile correlation makes it possible to measure sensitivity of a conditional quantile of a random variable with respect to change of the other variable. The properties of the quantile correlation are similar to those of the correlation. This enables us to interpret it from the perspective of correlation, on which tail dependence is reflected. We construct measures for tail dependent correlation and tail asymmetry and develop statistical tests for them. We prove asymptotic normality of the estimated quantile correlation and limiting null distributions of the proposed tests, which is well supported in finite samples by a Monte-Carlo study. The proposed quantile correlation methods are well illustrated by analyzing birth weight data set and stock return data set.

Keywords Quantile correlation; quantile regression; tail dependence; conditional quantile

MSC classification: 62H20

1 Introduction

Correlation coefficient is a standard statistical tool for measuring relationship between two variables. There are several versions of correlation coefficient such as the Pearson correlation coefficient, the Spearman’s rank correlation coefficient, the Kendall’s tau rank correlation coefficient, and others. The most common of these is the Pearson correlation coefficient, which is a measure for linear association. However, these correlation coefficients fail to measure tail-specific relationships.

Recently, interests in associations of random variables in tail parts have grown up in various fields. In finance, recurrent global finance crises have shown that a risky status of one financial institution causes a series of bad impacts on other financial institutions or on the total financial system. Hence, many studies on the measures for tail dependence have been conducted in the recent literature: CoVaR (co-value at risk) of Adrian and Brunnermeier (2016) and Giradi and Ergun (2013), volatility spillover index of Diebold and Yilmaz (2012) and many others. Other statistical tools were considered for tail dependence analysis. Copular is considered by many authors, see Joe et al. (2010), Nikoloulopoulos et al. (2012) and Kollo et al. (2017).

In environment, as frequency of abnormal climate has increased, importance for identifying associations of environmental factors in extreme tail part is accentuated. Accordingly, statistical analysis for association between abnormal climate and other factors using quantile regression have been conducted by many authors: Sayegh et al. (2014) for concentration; Meng and Shen (2014) for extreme temperature; Vilarini et al. (2011) for heavy rainfall and others.

We therefore need a measure which captures tail-specific relations. We define a new correlation coefficient, called “quantile correlation coefficient”, as a measure related to tail dependence in the context of correlation of random variables and . There is already a measure named “quantile correlation coefficient”, say, proposed by Li et al. (2015) which is the Pearson correlation of the indicator of the event and with -quantile of random variable , . Clearly, is not symmetric in in that . Moreover, the measure is a compound measure of sensitivity of conditional probability to change in and heterogeneity of conditional expectations and , which make it difficult to get a clear interpretation related with tail dependence, see Sections 2, 6. In fact, fails to reflect the degree of tail dependent association as illustrated in Examples 2.1, 2.2 below. Therefore, it is necessary to define a new quantile correlation coefficient which capture well the degree of tail dependent association and allows a clear interpretation for tail dependence.

The -quantile correlation coefficient of two random variables , is defined by the geometric mean of the two -quantile regression slopes of X on Y and of Y on X. Note that the Pearson correlation coefficient is the geometric mean of the two linear regression slopes of X on Y and of Y on X. The geometric mean indicates overall sensitivity of conditional mean of a variable with respect to change of the other variable. Similarly, the quantile correlation coefficient has the meaning of overall sensitivity of conditional -quantile of one variable with respect to change of the other variable.

Our quantile correlation coefficient will be shown to have many advantages of clear meaning and easy estimation. The quantile correlation coefficient satisfies the basic features of correlation coefficient: being zero for independent random variables; being for perfectly linearly related random variables; commutativity; scale-location-invariance; being bounded by 1 in absolute value for a general class of . This allows quantile correlation coefficient to be interpreted as a correlation coefficient.

The quantile correlation coefficient can be applied diversely. First, we can compare how sensitive lower, upper, median conditional quantile of one variable is to unit change of the other variable. For example, we can identify the fact that a stock return is more affected in lower tail conditional quantiles by change of another stock return than in upper tail conditional quantiles or than in conditional median. Second, it can be used to determine the order of variables which have high sensitivity in tail conditional quantiles with respect to change of the specific variable. For example, in environment, we can use it in primary screening of environmental factors which cause abnormal climate, such as high concentration of fine dust, heavy snow, heat wave and many others.

An estimation method is implemented for the quantile correlation coefficient giving us the sample quantile correlation coefficient. Based on the sample quantile correlation coefficient, we construct new measures and tests for differences between -quantile correlation and the median correlation and between left -quantile correlation and right -quantile correlation. We derive the asymptotic distributions of the sample quantile correlation coefficient and the asymptotic null distributions of the proposed tests.

A Monte-Carlo experiment shows finite sample validity of asymptotic distribution of the sample quantile correlation coefficient through its stable confidence interval coverage. The experiment also demonstrates that the proposed tests have reasonable sizes and powers. The proposed quantile correlation coefficient methods are well demonstrated by analyzing birth weight data set and stock return data set for investigating the relations between mother’s weight gained during pregnancy and birth weight and between the US S&P 500 index return and the French CAC 40 index return .

The remaining of the paper is organized as follows. Section 2 defines quantile correlation coefficient. Section 3 implements an estimation method. Section 4 establishes asymptotic distributions. Section 5 contains a finite sample Monte-Carlo simulation. Section 6 applies the quantile correlation coefficient methods to real data sets. Section 7 gives a conclusion.

2 Quantile correlation coefficient

In Section 2.1, quantile correlation coefficient is defined for a random vector which addresses -tail specific relation of and , . Meaning of is discussed to be a sensitivity measure of conditional -quantile of a variable with respect to change of the other variable. The proposed is shown to satisfy the properties what the Pearson correlation coefficient does. In Section 2.2, two examples illustrate that tail-dependent relations of and are well reflected in -dependent shape of . Measures of tail-dependency and tail asymmetry are proposed.

2.1 Definition and properties

The quantile correlation is motivated from the relationship between linear regression coefficients and correlation coefficient. Let be a random vector having finite second moment. Let , , . We observe that is the minimizing the expected squared error loss and is the minimizing . Note that is the geometric mean of the two linear regression coefficients. This correlation coefficient measures sensitivity of conditional mean of a random variable with respect to change of the other variable. The correlation is modified to measure sensitivity of conditional quantile rather than of conditional mean by considering -quantile regressions of minimizing the expected losses of -quantile regression, , rather than linear regressions of minimizing the expected square error losses: the -quantile correlation coefficient is defined to be the geometric mean of the two -quantile regression coefficients and of Y on X and X on Y.

In order to see what tells us, we first review what the Pearson correlation coefficient tells us. Assume temporarily linearities of and . Note that is the amount of change of with respect to unit change in and so is the amount of change of with respect to unit change in . The regression coefficients and are sensitivities of conditional expectations with respect to changes of conditioning variables. When the linearities of conditional expectations are violated, and are overall sensitivities of changes of conditional expectations with respect to changes of conditioning variables. Therefore, their geometric mean tells us overall sensitivity of conditional mean of a variable with respect to change of the other variable: the larger , the more sensitive the conditional mean of one variable to change of the other variable in an overall sense. By the same reasoning, the median correlation is an overall sensitivity measure of conditional median of one variable with respect to change of the other variable: the larger , the more overally sensitive the conditional median of a random variable to change of the other variable.

Similarly, for given , the larger , the more sensitive overally the conditional -quantile of a random variable to change of the other variable. Therefore, comparison of for different is meaningful. For example, if , it means that the conditional 0.1-quantile of a random variable is overally more sensitive to change of the other variable than the conditional median of it. If , it means the left conditional 0.1-quantile of a random variable is overally more sensitive to change of the other variable than the right conditional 0.1-quantile of it. Therefore, we can say that is an overall sensitivity measure of conditional -quantile of one variable with respect to change of the other variable.

On the other hand, the quantile correlation , of Li et al. (2015) has complicated implication, where is the -quantile of and is the indicator function of an event A. Assume linear conditional expectations for and . We have , , . Note that is the change of the conditional probability associated with unit change in and that . Therefore, large indicates (i) strong sensitivity of the conditional probability of being highly sensitive to change in or (ii) strong heterogeneity of conditional mean of having large difference in mean depending on or . Therefore, is a compound measure of sensitivity of conditional probability to change in and heterogeneity of conditional expectations and , see Section 6.1 for a real data illustration. It is hard to get a simple sensitivity interpretation from . Moreover, it is obvious that lacks symmetry in that . Furthermore, tail dependent association of , , if any, is not well reflected in as illustrated in Examples 2.1, 2.2. Unlike , our quantile correlation has well reflection of the degree of association of , as demonstrated in Examples 2.1, 2.2, has symmetry in and has a clear sensitivity interpretation.

Our -quantile regressions of on and on are defined by minimizing the expected loss,

| (1) |

respectively, where

is the loss function of the -quantile regression. Let be given and let

| (2) |

Note that these coefficients are more general than the “usual quantile regression coefficient” which minimizes the conditional loss function under the linearity assumption of the -conditional quantiles of given , see Koenker (2005, Section 4.1.2). Our quantile regression coefficient is defined without imposing the linearity assumption. If the -quantile of Y given X is linear in , is the same as the “usual -quantile regression coefficients” as shown in Theorem 2.3 below.

We define the quantile correlation for a random vector and study its basic properties.

Definition 2.1.

Let be a random vector having finite first order moment. Let and be defined in (2). Given , the -quantile correlation coefficient between X and Y is defined as

If relation between and is heterogeneous in that they have different degrees of association depending on left tails of , right tails of and other , then the heterogeneity is reflected on . Therefore, can be regarded as a tail-dependence measure. This point will be more investigated in Examples 2.1, 2.2, below.

If , is not defined. However, the following theorem shows that the proposed quantile correlation is always well-defined.

Theorem 2.2.

For all , .

The following theorem states that under the linear quantile function conditions, the quantile regression coefficients are the same as the “usual quantile regression coefficient” of Koenker (2005, Section 4.1.2) and many others. Let be the conditional -quantile of given and let be that of given :

Note that minimizes the conditional expected loss . Similarly, minimizes .

Theorem 2.3.

Assume and are both linear in and , respectively, that is,

| (3) |

for some and . Then .

Basic properties of such as commutativity, scale-location-equivariance, and others are given below.

Theorem 2.4.

Assume has finite first moment. We have

(i) ,

(ii) if ,

(iii) if and , ,

(iv) if and are independent, .

Thanks to Theorem 2.4 (i), we can write by , which will be adopted in the remaining of the paper. According to properties (ii) - (iv), we have for perfectly linearly related (, ) and for independent and we know that is invariant under linear transforms of or of with positive slopes. The following theorem shows that for a wide class of distributions. We therefore can say that is a correlation measure of for such class.

Theorem 2.5.

Assume has finite first moment. We have if either (i) or (ii) , , where , , , , .

The condition of Theorem 2.5 for needs to be discussed. We have if , if , if or if . The first one is the case in which conditional -quantile of a random variable is negatively associated with the other variable. From the second condition, we have in any case. The third one is a kind of symmetry of the residuals and , which is satisfied for the usual symmetric bivariate distributions such as bivariate normal, bivariate t, bivariate uniform and many others. We finally discuss the last condition . For skewed distributions having , we have for . This is a satisfactory aspect. For the distributions with , left tails of the distributions of , are heavier than right tails. Special important such examples are financial asset returns. For such distributions with heavier left tails, people are more interested in dependence in left tails than in right tails. For distribution having , even though Theorem 2.5 does not guarantee for , it does not mean for .

The following theorem characterizes a situation in which the -quantile correlation coefficient is identical with the Pearson correlation coefficient .

Theorem 2.6.

Assume the conditional distribution of Y given X depend on only through and is linear in X. Assume the same one for the conditional distribution of X given Y. Then for all .

An important special random vector satisfying the conditions of Theorem 2.6 is the bivariate normal random vector for which we hence have . Such random vector satisfying the conditions of Theorem 2.6 has no tail-specific dependence because association between X and Y is exhausted out by the linear conditional expectations and .

2.2 Local dependence measure

This subsection starts with a couple of illustrative examples having -dependent quantile correlation coefficient whose shape reflects the tail-dependent degree of association between and . Next, it proposes tail dependence measure and of tail asymmetry measure based on .

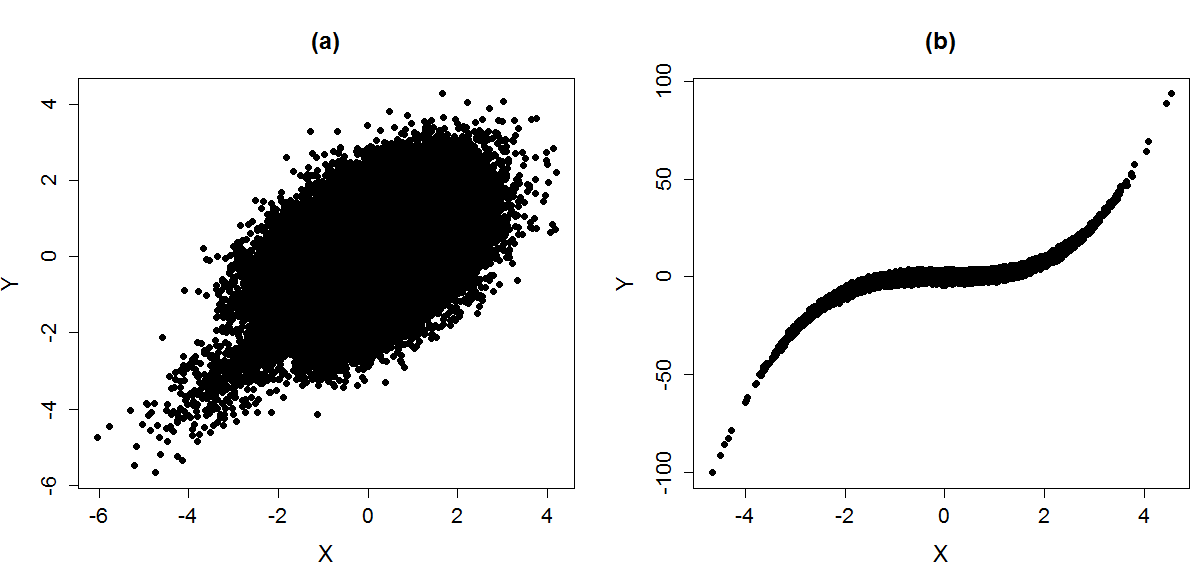

Example 2.1.

(A rocket-type bivariate distribution) Let . Let be independent of . Let

| (4) |

where . Note that the bivariate normal random variables are contaminated by a common error in the lower left area of . Figure 1 (a) displays scatter plot of . The figure shows that has a rocket-type scatter plot with stronger correlation in the lower left area than in the other area owing to the contaminating common term for X and Y in the lower left area.

Table 1 provides values of quantile correlation coefficient , Pearson correlation for and the quantile correlation coefficients , of Li et al. (2015). We approximate by a Monte-Carlo simulation average of 100 independent obtained by minimizing the averaged losses and with independently generated . By taking large enough, by the law of the large numbers, we can make the averaged loss be close enough to the expected loss and and hence the approximated value be close enough to the true value . We take .

Table 1. Quantile correlation , , and correlation for in (4)

| 0.553 | 0.539 | 0.526 | 0.499 | 0.500 | 0.500 | 0.500 | 0.506 | |

| 0.192 | 0.231 | 0.289 | 0.393 | 0.292 | 0.232 | 0.135 | ||

| 0.192 | 0.231 | 0.287 | 0.397 | 0.290 | 0.236 | 0.135 | ||

The most interesting point is that reflects well the degree of association of , shown in Figure 1 (a). Stronger association of in lower tails of , matches up well with larger values of for than those for , but reversely matches up with smaller values of for than that for . Moreover, the fact that , have similar degrees of association at center and at high tails by construction is in conflict with different values of for and for close to 1. We can say the shape of is in harmony with the degree of tail-dependent associaiton of , while that of is not.

The table shows tail dependent features of : the lower quantile correlations and are greater than the median correlation ; and the median correlation is almost the same as the upper quantile correlations and . This is in harmony with the fact that has stronger conditional correlation in the area of (low tail of , low tail of ) than the other area of as observed from Figure 1 (a). The fact tells that, in the overall sense, the 1% conditional quantile of one random variable varies more sensitively according to change of the other variable than the conditional median. This is a consequence of the higher correlation of in the lower left part than in the other part: in the former which, for example, the conditional 0.1-quantile of a variable change overally more sensitively than the conditional median according to change of the other variable because of higher correlation of lower tail , than other , . The fact that tells that all the conditional median, 99% quantile, and mean of a random variable vary similarly with change of the other variable.

Example 2.2.

(A cubic relation) Let and let and be independent standard normal random variables. Figure 1 (b) shows scatter plot of . We find a tail specific relation between and : steeper linear relation at tails than at the center. We provide the values of quantile correlation coefficient and Pearson correlation coefficient for in Table 2, which are approximated by a Monte-Carlo Simulation, similar to that in Example 2.1. We note that has similar tail specific feature as the tail specific relation between and : for tail is larger than . This harmonic feature of and degree of association of , is not shared by , in that is larger at tails than at center and .

Table 2. Quantile correlation , , and correlation for ,

| 0.815 | 0.745 | 0.711 | 0.688 | 0.711 | 0.745 | 0.815 | 0.750 | |

| 0.489 | 0.560 | 0.537 | 0.404 | 0.541 | 0.565 | 0.497 | ||

| 0.265 | 0.469 | 0.559 | 0.547 | 0.559 | 0.470 | 0.266 | ||

The fact that means that, in an overall sense, the conditional median of one variable varies less sensitively with change of the other variable than its conditional mean. From we find that the left and right 1% conditional quantiles of a variable vary more strongly with change of the other variable than its conditional median, which is a consequence of stronger correlation between and in tails than other .

The above two examples illustrate that tail-dependent correlation of is well reflected in but not well in , . Now, we define a new tail dependent correlation measure, which measures how far -quantile correlation is away from the median correlation .

Definition 2.7.

Let be given. The - tail dependent correlation measure is defined as

If , we can say that, the conditional -quantile of a variable is differently sensitive to change in the other variable than the conditional median of the variable.

Definition 2.8.

Tail correlation asymmetry measure is defined as

It is obvious that the symmetric distributions stated in Theorem 2.6 having no tail specific correlation have 0 for both of and as formally presented in the following theorem.

Theorem 2.9.

For random vector satisfying the conditions of Theorem 2.6, , for all .

Example 2.3.

Consider the in Example 2.1 and Example 2.2. Values of and are computed using constructed by the Monte-Carlo methods in Examples 2.1, 2.2. Table 3 presents the result.

Consider first the random vectors in Example 2.1. We see tail-dependent values : for and for . This means that, compared with the conditional median, as a variable changes, the left tail conditional quantile of the other variable varies more sensitively, but the right tail conditional quantile varies similarly. We see a highly asymmetric feature by the value for . Consider next in Example 2.2. We observe that and are the same for , which are larger for more extreme tails, telling stronger dependency of for deeper tail of , . We note that has value zero, indicating that is symmetric and hence symmetric tail dependent relation of in lower tails and in upper tails.

Table 3. Tail dependent correlation measure (), tail correlation asymmetry measure () for Example 2.1 and Example 2.2

| 0.01 | 0.05 | 0.1 | 0.5 | 0.9 | 0.95 | 0.99 | |

| Example 2.1 | , | ||||||

| 0.05 | 0.04 | 0.03 | 0.00 | 0.00 | 0.00 | 0.00 | |

| 0.05 | 0.04 | 0.03 | - | - | - | - | |

| Example 2.2 | |||||||

| 0.13 | 0.06 | 0.02 | 0.00 | 0.02 | 0.06 | 0.13 | |

| 0.00 | 0.00 | 0.00 | - | - | - | - | |

3 Estimation

This section constructs an estimator of from the sample quantile regressions, which in turn gives us estimators of and . Standard errors for them are presented here, whose theoretical validation is provided in Section 4 and finite sample validation is given in Section 5.

Let , be two random variables whose tail dependence is of interest. Suppose that a sample of realizations of is given. The sample may be an iid (independent and identically distributed) one or may be possibly non-iid one having linear quantile functions

| (5) |

Note that, for iid samples, we do not need the linearity assumption of (5). Let be given. The -quantile correlation is estimated from the sample quantile correlation coefficients as given by

| (6) |

where are the estimated quantile regression slopes of ( on , on ) obtained by minimizing the averaged losses

that is,

| (7) |

which are the same as the usual -quantile regression coefficient estimates. The minimization is usually performed by linear programming, see Koenker (2005, p.181). The estimator in (6) will be termed as the sample -quantile correlation coefficient. The sample quantile correlation can be easily computed from estimated quantile regression estimates using any statistical software for quantile regression estimation such as “quantreg” in R package, “proc quantreg” in SAS, and others. For iid sample, is consistent for with defined by (2) and for possibly non-iid sample having linear quantile functions of (5), is consistent for with defined by (5), see Theorem 4.3 below.

In finite samples, it may happen that or greater than 1 for some . For large samples, the probability of goes to 0 as , as will be demonstrated in Corollary 4.2 in Section 4 below.

Section 4 below will show that is asymptotically normal,

| (8) |

for in (11) below. We present the standard error of based on a consistent estimator of the asymptotic variance . Let and and be two given values. Let and and let

Given two values of and a density functions , we define

| (9) |

| (10) |

which is assumed to exist. Then, with , , , , , as will be shown in Section 4, we have

| (11) |

where if ; otherwise, and are the conditional densities of given and given , respectively.

The results (8)-(11) enable us to construct a standard error of . We need a consistent estimator of the asymptotic variance for which we need estimators of the parameter values , and conditional density values , evaluated of and . We use the consistent estimators for the corresponding parameter values. Given estimators and of and , the obvious estimator of is

| (12) |

where,

and

| (13) |

We now have the standard error of ,

Note that estimators of the conditional densities and evaluated at and are required for variance estimator (12) but not for the quantile correlation coefficient estimator . For the estimated conditional kernel density values and in (13), two strategies are available. The first strategy is using nonparametric conditional density estimators, and , say, of Hyndman et al. (1996) for iid sample. Since are iid, we can omit subscript as in and . The conditional kernel density estimator of Hyndman et al. (1996) is

| (14) |

where

, , , are bandwidths, and is a kernel function. Optimal choices of the bandwidths are given in Bashtannyk and Hyndman (2001), which will be employed in (24) in Section 5 below. The estimator (14) is consistent for iid sample but not for non-iid sample. The other strategy is using the estimated values of the conditional densities at the quantiles, for example by Hendricks and Koenker (1991). For possibly non-iid smaple, we can use the method of Hendricks and Koenker (1991) who estimated the values of the conditional densities at the estimated quantiles under the linearity assumption that quantile of is linear in and so is :

| (15) | |||

where is a small positive constant and is a bandwidth. Optimal bandwidth parameter is found in Bofinger (1975) and Koenker (2005, p.115), which will be adopted in a Monte-Carlo study in (25) in Section 5. The estimator (15) is consistent for some non-iid samples under some regularity conditions such as linearity of quantile functions and . Performances of these two strategies will be compared in Section 5.

The tail dependent correlation measure and the tail asymmetry measure are estimated by

| (16) |

For standard errors of the estimated measures and , we need the asymptotic variance of in , , as will be demonstrated in Section 4, where

| (17) | ||||

A consistent estimator of is

| (18) |

where and . The standard errors of and are

| (19) |

4 Asymptotic theory and statistical inference

Let realizations of two random variables , be given. We establish asymptotic normality for and other estimators in Section 3, which enable us to construct confidence intervals and tests for , , . Let and be the vectors of -quantile regression coefficients defined in (2) or (5) for iid sample or for possibly non-iid sample, respectively. The asymptotic distribution of is established under the following conditions.

Condition A1. We have either

(i) are iid having finite second moment or

(ii) are possibly non-iid; is linear in and is linear in as in (5); is a martingale difference with respect to satisfying

| (20) |

| (21) |

Note that, for iid sample of condition A1(i), linearity is not assumed for the quantile functions and (20)-(21) are automatically satisfied with as proved in the proof of Lemma 4.1. Thanks to (20)-(21), the probability limits in (9)-(10) are well defined for true , . Sequence of random vectors having GARCH-type conditional heteroscedasticity satisfy the condition of A1(ii), for which the asymptotic results of this section hold. Therefore, our quantile correlation method is applicable for tail-dependent analysis of financial return data sets.

Condition A2. Let be given. The conditional distribution function of given is absolutely continuous, with continuous conditional density uniformly bounded away from 0 and at . The conditional distribution function of given by satisfies the similar conditions with conditional density .

Condition A3. Let be given.

(i) are bounded,

(ii) and ,

Conditions A2-A3 are similar to those assumed in quantile regression asymptotic analysis, see Section 4.2 of Koenker (2005). Thanks to Condition A2, the asymptotic variance of is expressed in terms of the conditional densities through the terms in Condition A3(i).

Let . In Lemma 4.1, we first derive the asymptotic distribution of the vectors of estimated quantile regression coefficients .

Lemma 4.1.

Let be given. Assume conditions A1 - A3. Then, as , we have

| (22) |

where and .

Corollary 4.2.

Let be given. Assume conditions A1 - A3. Then, as ,

From Lemma 4.1 and Corollary 4.2, applying the multivariate -method, we get the limiting normality of .

Theorem 4.3.

Assume conditions A1 - A3. As , given , we have

Theorem 4.3 is useful in constructing the statistical inference for the quantile correlation such as statistical significance of and hypothesis tests. One can compute the p-value of the sample -quantile correlation coefficient by where is the distribution function of the standard normal distribution. A valid -confidence interval of will be

| (23) |

where is the -quantile of the standard normal distribution. Furthermore, we can develop tests for tail dependence and asymmetry.

With or , the tests of the tail dependence and tail correlation asymmetry are constructed from the asymptotic distribution of which is derived easily by applying the multivariate -method to the limiting distribution of as given in Lemma 4.4.

Lemma 4.4.

Let be given. Assume conditions A1- A3 for . Then as ,

Theorem 4.5.

Under the same conditions for Lemma 4.4, as , we have

From Theorem 4.5, given , valid tests for the tail independent correlation and for the tail correlation symmetry are

respectively, where and are given in (19). Under the null hypotheses, both of the two tests converge to the standard normal distribution as stated in the following corollaries.

Corollary 4.6.

Let be given. Assume conditions A1 - A3 hold for , . Assume with , , , are consistent for . Then, under , as ,

Corollary 4.7.

Let be given. Assume conditions A1 - A3 hold for , . Assume with , , , are consistent for . Then, under , as ,

The conditional density estimators , of Hyndman et al. (1996) are consistent under some mild conditions on , , , and and of Hendricks and Koenker (1991) are consistent under some mild conditions on and the additional linearity condition (3) on and . For more discussion on the consistency, see Hyndman et al. (1991) and Koenker (2005, p.77)

5 Simulation

We investigate finite sample validity of the asymptotic distribution of the sample quantile correlation in Theorem 4.3 and finite sample performances of the proposed tests and . The first one is checked by finite sample coverages of the confidence interval (CI) of the quantile correlation . According to Theorem 4.3, this CI is asymptotically valid. The second one is verified by size and power performances of the tests.

We consider

from which the data are generated, . In , GARCH (1,1) model is given as and . The normal and t random variables are generated by “rmvnorm” and “rmvt” in the R package.

Note that from , , , is a sequence of iid random variable satisfying condition A1(i) and that from is a sequence of non-iid martingale difference satisfying condition A1(ii). According to Theorem 2.6, has constant quantile correlation for all and almost so has with for . Other DGPs have tail-dependent : has asymmetric tail dependent quantile correlation; has symmetric tail dependent quantile correlation; has and for . For each of the five distributions, independent , and the corresponding CIs of are constructed, .

In order to construct the CIs and test statistics, we need estimators and of the conditional density values for which we consider the two strategies of (14) by Hyndman et al. (1996) and (15) by Hendricks and Koenker (1991). The conditional kernel density of Hyndman et al. (1996) is (14) with the Gaussian kernel,

and bandwidths

| (24) |

where

and are the sample variances of and , respectively. The other bandwidth parameters , are computed by interchanging , in (24). According to Bashtannyk and Hyndman (2001), the bandwidths are estimated values of the optimal bandwidths for bivariate normal distributions.

The estimated conditional density values proposed by Hendricks and Koenker (1991) are (15) with and bandwidth

| (25) |

where and are pdf and cdf of the standard normal distribution, respectively. According to Bofinger (1975) and Koenker (2005, p.115), is optimal under normality of .

Empirical coverage probability of CI of the quantile correlation coefficient is

| (26) |

where is the indicator function of an event . The true values for and are given in Table 1 and Table 2, those for and are .

Table 4 shows the coverages and lengths of the 90% CIs. Consider first the results with the conditional kernel density in (14) of Hyndman et al. (1996). Except for with , for all five DGPs, the proposed CI of has coverages not much deviated from the given value 90% even though there are some under-coverages for , which generally improve to the nominal coverage 90% as increases from 100 to 500 and next to 2500. The under-coverage problems is caused by inefficient estimate of conditional density values due to the small number of sample in tails especially for . The degree of under-coverage is similar to that the CI of the coefficient of the quantile regression , reported in the Monte-Carlo studies of Koenker (2005, Section 3.10) and Kocherginskty et al. (2005, Section 4).

Consider next the results with the conditional kernel density values in (15) of Hendricks and Koenker (1991). Except for , for all , considered here, coverage of the proposed CI of is generally acceptable and is better than the corresponding coverage based on the other conditional density estimator . Regarding average lengths of CIs, that based on tends to be shorter in tails and longer in center than that based on , which however dues to smaller coverage of them in tails and larger coverage in center. Therefore, none of and are better than the other one in average length of CI.

Table 4. Empirical coverages (%) and lengths of the 90% confidence intervals of quantile correlation coefficients

| Coverage (%) | Length | ||||||||||||

| DGP | |||||||||||||

| 100 | , Normal | 83.8 | 93.4 | 87.5 | 88.5 | 91.3 | 91.2 | 0.31 | 0.34 | 0.35 | 0.38 | 0.32 | 0.42 |

| , | 83.5 | 93.1 | 86.9 | 91.0 | 87.8 | 92.4 | 0.35 | 0.35 | 0.39 | 0.47 | 0.29 | 0.52 | |

| , Example 2.1 | 77.5 | 93.8 | 88.5 | 85.2 | 90.6 | 91.0 | 0.33 | 0.35 | 0.35 | 0.40 | 0.32 | 0.41 | |

| , Example 2.2 | 66.8 | 91.7 | 70.5 | 82.0 | 72.3 | 85.3 | 0.25 | 0.27 | 0.27 | 0.44 | 0.16 | 0.48 | |

| : GARCH(1,1) | 83.8 | 92.0 | 87.2 | 89.4 | 88.5 | 91.6 | 0.32 | 0.34 | 0.36 | 0.40 | 0.31 | 0.44 | |

| 500 | : Normal | 87.0 | 93.5 | 88.0 | 90.1 | 91.6 | 91.1 | 0.15 | 0.15 | 0.15 | 0.16 | 0.14 | 0.17 |

| : | 86.6 | 92.5 | 88.0 | 91.5 | 87.2 | 92.4 | 0.16 | 0.15 | 0.17 | 0.19 | 0.13 | 0.20 | |

| : Example 2.1 | 85.5 | 93.1 | 87.7 | 88.8 | 90.4 | 90.0 | 0.17 | 0.15 | 0.15 | 0.19 | 0.14 | 0.16 | |

| : Example 2.2 | 82.2 | 91.8 | 82.9 | 81.0 | 66.9 | 81.9 | 0.16 | 0.11 | 0.16 | 0.17 | 0.06 | 0.17 | |

| : GARCH(1,1) | 86.3 | 91.4 | 87.0 | 90.1 | 87.9 | 90.5 | 0.15 | 0.14 | 0.15 | 0.17 | 0.13 | 0.17 | |

| 2500 | : Normal | 89.1 | 92.6 | 88.3 | 91.0 | 91.2 | 90.6 | 0.07 | 0.06 | 0.07 | 0.07 | 0.06 | 0.07 |

| : | 88.7 | 91.0 | 88.5 | 92.5 | 85.8 | 92.4 | 0.08 | 0.06 | 0.08 | 0.09 | 0.06 | 0.09 | |

| : Example 2.1 | 88.7 | 91.7 | 89.1 | 90.9 | 89.8 | 90.5 | 0.08 | 0.06 | 0.07 | 0.09 | 0.06 | 0.07 | |

| : Example 2.2 | 86.8 | 90.6 | 86.6 | 76.3 | 64.9 | 76.6 | 0.08 | 0.05 | 0.08 | 0.06 | 0.03 | 0.06 | |

| : GARCH(1,1) | 87.8 | 89.6 | 87.5 | 90.6 | 85.9 | 90.4 | 0.07 | 0.06 | 0.07 | 0.08 | 0.06 | 0.08 | |

Note: is conditional kernel density of Hyndman et al. (1996). is conditional kernel density of Hendricks and Koenker (1991).

Finite sample size and power studies of the proposed tests and , are made. Rejection rates of the tests out of independent replications are reported in Table 5. For and , the rejection rates of and are both sizes; for , those for and are powers; and for and , that for is size and that for is power.

Except for for , the table shows reasonable sizes, which improves to the given level 5% as in increases from 100 to 500 and next to 2500. For , size of based on is poor for , which however improves rapidly as increases from 100 to 500 and on. This bad performance of for is a consequence of inefficiency of . Since is consistent, the bad coverage of for disappears as increases to 500. On the other hand, for , size of based on is not so bad for , but is bad for . The bad performance for is a consequence of nonlinearity of the quantile functions of .

The table shows the proposed tests have powers which increases as increases from 100 to 2500. The power values are not large even for . This implies that we need a large sample in order to detect tail dependency or tail asymmetry if any.

Table 5. Sizes (%) and powers (%) of level 5% tests n DGP size/power size/power 100 : Normal size 3.9 3.3 size 6.4 3.6 : size 4.5 3.1 size 7.6 2.6 : Example 2.1 power 5.6 4.5 power 8.8 4.9 : Example 2.2 power 13.2 10.6 size 29.5 8.2 : GARCH(1,1) power 4.0 3.6 size 6.6 3.3 500 : Normal size 4.8 4.2 size 6.2 4.3 : size 5.0 3.9 size 6.2 3.1 : Example 2.1 power 7.7 6.4 power 8.8 5.8 : Example 2.2 power 10.7 15.4 size 10.5 9.2 : GARCH(1,1) power 6.4 5.7 size 6.4 4.2 2500 : Normal size 4.8 4.5 size 5.5 4.4 : size 5.3 4.2 size 5.4 3.3 : Example 2.1 power 18.8 17.0 power 17.7 14.9 : Example 2.2 power 17.1 31.1 size 7.6 14.5 : GARCH(1,1) power 12.4 11.8 size 5.0 3.8

Note: is conditional kernel density of Hyndman et al. (1996). is conditional kernel density of Hendricks and Koenker (1991).

We discuss relative performance of and . Consider first . The density estimator gives always-acceptable coverages for the CI and sizes for the tests , , while the other one gives poor coverages for CI and sizes for for . Consider next . We observe stable coverages of the proposed CIs and sizes of the proposed tests and for the last four DGPs, , , , , except for for even though we have used the conditional density value estimators . For samples of not small size, we recommend the always-consistent , but, for samples of small size, one may better use .

We summarize the results of this Monte-Carlo simulation. First, the confidence interval of has reasonable finite sample coverages and the proposed tests , have generally acceptable sizes and power for the bivariate distributions with tail dependent correlation considered here. This fact confirms both finite sample validity of the asymptotic theory and usefulness of the proposed methods based on . Second, among the two conditional density value estimators considered here, for samples of not small size, those by Hyndman et al. (1996) provide the confidence intervals and tests with better finite sample coverage and sizes than the other one by Hendricks and Koenker (1991), while, for samples of small size, is better than .

6 Real data set analysis

The proposed quantile correlation methods are applied a couple of field data sets: birth weight data set and stock return data set. The data analysis illustrates well the tail-dependent sensitivity of the conditional quantile of one variable with respect to change of the other variable.

6.1 Birth weight data

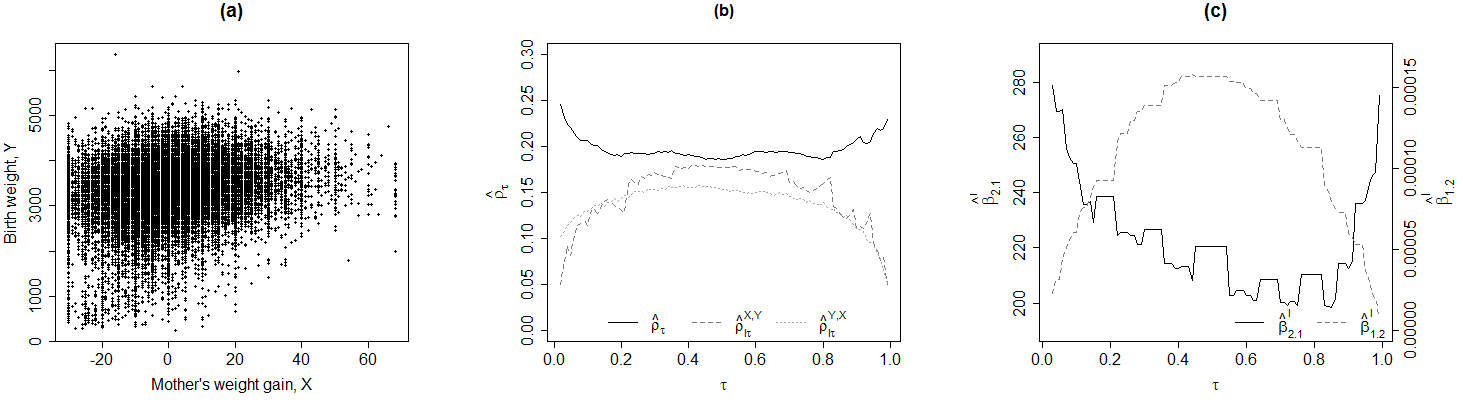

We first analyze the birth weight data set considered by Abreveya (2001) and Koenker (2005) for identifying impact factors on the birth weight. The data set is the natality data published by the US national center for health statistics in June 2017. We investigate the relationship between mother’s weight gained during pregnancy and birth weight . We have . The sample may be regarded to be iid satisfying condition A1(i). Figure 2 (a) displays a scatter plot of birth weight and mother’s weight gain. The figure shows an overall positive correlation.

We compute sample quantile correlation . We also compute the sample quantile correlations of Li et al. (2015), which are the Pearson correlations of and and of and , respectively, where and are the -quantiles of and .

Figure 2 (b) shows the sample quantile correlation coefficient , , which is superimposed on . We note a tail-dependent convex feature that , in tails of are greater than . This means that conditional tail quantile, , , of one variable varies more sensitively with change of the other variable than the conditional median of the variable. The other quantile correlations and tell a quite different story having concave shapes. Figure 2 (b) shows that and are closer to 0 at tails than at center. This indicates that the indicator and or and the indicator have stronger association at center.

Concavity of is a compound result of convexity of and concavity of , the slope of in the regression of on , whose plots are given in Figure 2 (c). Note that is heterogeneity in conditional means, is sensitivity of the conditional probability to change of , and they are reversely shaped. Therefore, it is hard to get a simple interpretation from and so is from .

Table 6. Estimated and , and t-tests statistics and estimate t-stat p-value estimate t-stat p-value estimate t-stat p-value 0.034 4.733 0.020 4.126 0.006 1.687 0.006 0.684 0.494 -0.001 -0.179 0.858 0.003 0.660 0.509

Table 6 provides estimated measures and , their t-test statistics, and their p-values of the test and , in which the conditional density estimator is used according to the recommendation of Section 5 for not small. The differences between median quantile correlation and lower and upper quantile correlation shown in Figure 2 (b) are significant with p-value of . Note that is symmetric in that lower quantile and upper quantile are not significantly different from each other having p-values of larger than 0.05, for .

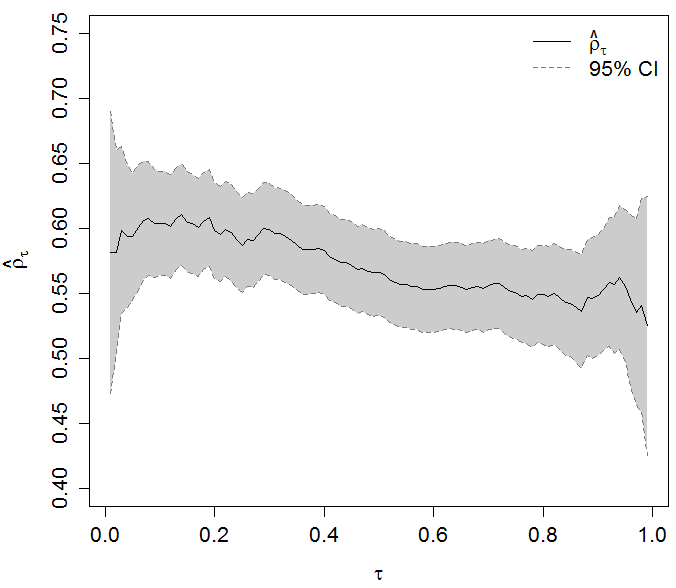

6.2 Stock return data

We next analyze asymmetric tail dependent relations of pairs of log returns of two stock price indices for the period of 01/03/2000 - 11/30/2017: the US S&P 500 index and the French CAC 40 index. The stock price data sets are obtained from the Oxford-Man realized library (http://realized.oxford-man.ox.ac.uk). We have . The sample may be regarded from a martingale difference satisfying condition A1(ii). Confidence intervals of for closer to 0 or 1 are wider than those of for close to 0.5. This implies that for closer to 0 or 1 has larger standard error than for closer to 0.5.

Figure 3 reports the sample quantile correlation coefficient and 95% confidence interval for constructed from (23), in which is used according to the recommendation of it for not small. We see strongly tail-dependent : roughly, . This implies that the left conditional quantile of one stock return is more sensitive to change of the other return than its conditional median and the right conditional quantile is less sensitive than its conditional median. For example, the 5% conditional VaR (value-at-risk) of one stock return is more sensitive to change of the other stock return than its conditional median. The left 5% conditional VaR of one stock return is more sensitive to the other stock return than the right 5% conditional VaR.

Table 7. Estimated and , and t-tests statistics and

| estimate | t-stat | p-value | estimate | t-stat | p-value | estimate | t-stat | p-value | |

|---|---|---|---|---|---|---|---|---|---|

| 0.027 | 1.263 | 0.207 | 0.037 | 2.144 | 0.032 | 0.021 | 1.807 | 0.071 | |

| 0.038 | 1.248 | 0.212 | 0.055 | 2.176 | 0.030 | 0.036 | 2.261 | 0.024 | |

This asymmetric feature of is demonstrated by measures and and tests and reported in Table 7, . We see positive values for all and , indicating more sensitive for left conditional quantile of a return to change of the other return than its conditional median return and than the corresponding right conditional quantile of the return, respectively. The p-values of and show significant tail dependence and asymmetry in the quantile correlation at the tails. Insignificance of and at may be a consequence of the reduced sample sizes for the deep left tail of .

7 Conclusion

We have proposed a new correlation measure in which tail dependence is reflected, called quantile correlation coefficient. It is defined to be the geometric mean of two quantile regression slopes of X on Y and Y on X. The proposed correlation coefficient is shown to share the basic properties of the usual Pearson correlation coefficient: zero for independent pairs of random variables, for perfectly linearly related pairs, scale-location equivariance, and being bounded by in absolute value for general class of random pairs. Tail-dependent association of , , if any, is well captured by the proposed quantile correlation coefficient. The new measure allows us to measure sensitivity of conditional quantile of one variable with respect to change the other variable. The quantile correlation coefficient is easy to estimate and clear to interpret. Based on the quantile correlation coefficient, we proposed measure of tail dependent correlation and of tail correlation asymmetry and their statistical tests. We established asymptotic normalities for the sample quantile correlation coefficient and for the proposed tests under null hypothesis. A Monte-Carlo study confirms the asymptotic normality of the quantile correlation and shows reasonable sizes and powers for the proposed tests. Birth weight data set and stock return data set were analyzed by the proposed quantile correlation methods to have tail dependent correlations. The analysis reveals that degrees of sensitivity for lower, upper, median conditional quantiles of one variable to change in other variable are different.

Appendix - proofs

In the proofs of the theorems in Section 2, we use the following property: for any and , , and we use , for simplicity of notation.

Proof of Theorem 2.2. Assume Let and . Then

which is a contradiction because for all . For and , the same contradiction is derived. Hence, .

Proof of Theorem 2.3. By linearity assumption, and for and which minimize for any and for any , respectively. Note that and do not depend on and . Therefore, and minimize and , respectively, and hence ,

(ii) Applying Koenker (2005, Theorem 2.3), we have

(iii) Since , for all , minimizes to . Similarly, from , minimizes to and we get the desired result.

(iv) From independence of and , we have and , which are the conditional -quantiles of and , respectively. By Theorem 2.3, and hence

Let (ii) hold that , . Then

| (27) |

because of , where and . Then, the assumption is a contradiction because and . Therefore,

We complete the proof by showing the inequality in (27). It is easy to show

Therefore,

if . We have (27) because, with , and the condition of Theorem 2.4, we have .

Proof of Theorem 2.6. Let and be the distribution functions of given , given , respectively. Then, is free from and is free from . By the assumption, and for some . Then,

By Theorem 2.3, , and hence

Proof of Theorem 2.9. For random vector satisfying the conditions of Theorem 2.6, we have for all . We therefore have for all and hence and .

Proof of Lemma 4.1. Let be block matrix and , . We define

Note that and are convex and are uniquely minimized at and respectively. We show

| (28) |

for some and that is uniquely minimized by whose distribution is (22). Then we get the desired result from uniqueness of the minimizers

It remains to prove (28). Let , , , , , Applying the Knight (1998)’s identity, we can write

where

and

| (29) | ||||

We will show

| (30) |

| (31) |

We then have (28) with which is minimized by having the distribution (22).

We prove (30). Let condition A1(i) for iid-ness of hold. Then by the following argument. Noting that minimizes , is the -quantile of . Therefore, . Note that minimizes which is differentiable with respect to . Therefore, . Note that, the function is Lebesgue-integrable with respect to the probability measure of the joint distribution of , and for almost all , the derivative exists for almost all . Note that a.s. which is integrable. Therefore, the Leibniz’s rule is applicable to change the order of integration and derivation as in . Therefore, , and similarly , arriving at . Since are iid, (20) holds automatically.

Let condition A1(ii) for possibly non-iid sample hold. Then . Therefore, under condition A1(i) or A1(ii) with conditions A2 and A3, applying the martingale central limit theorem to the martingale with (20), we get (30).

Note that and . By (32), essentially for large , . Therefore, by (32) and condition A3 (ii),

Therefore, and similarly , arriving at (30).

Proof of Corollary 4.2. By Lemma 4.1, we have and by Theorem 2.2, for all . We therefore get the desired result.

Proof of Theorem 4.3. From Lemma 4.1, the result is derived easily by applying the multivariate -method.

Proof of Lemma 4.4. From Lemma 4.1, the result can be obtained by extending the asymptotic normality of four parameter estimators to eight parameter estimators . We redefine block matrix . By Lemma 4.1, it suffices to show

Applying the Knight (1998)’s identity, we can write

and we get the desired result by showing

| (33) |

| (34) |

Proofs of (33) and (34) are the same as those for (30) and (31).

Acknowledgements

This study was supported by a grant from the National Research Foundation of Korea (2016R1A2B4008780).

References

Abreveya, J. 2001. The effects of demographics and maternal behavior on the distribution of birth outcomes, Empirical Economics, 26, 247-257.

Adrian, T., Brunnermeier, M. K. 2016. CoVaR, American Economic Review, 106, 1705-1741.

Bashtannyk, D. M., Hyndman, R. J. 2001. Bandwidth selection for kernel conditional density estimation, Computational Statistics & Data Analysis, 36, 279-298.

Bofinger, E. 1975. Estimation of a density function using order statistics, Australian Journal of Statistics, 17, 1-7.

Diebold, F. X., Yilmaz, K. 2012. Better to give than to receive: Predictive direction measurement of volatility spillovers, International Journal of Forecasting, 28, 57-66.

Girardi, G., Ergun, T. 2013. Systemic risk measurement: Multivariate GARCH estimation of CoVaR, Journal of Banking & Finance, 37, 3169-3180.

Hendricks, W., Koenker, R. 1991. Hierarchical spline models for conditional quantiles and the demand for electricity, Journal of the American Statistical Association, 87, 58-68.

Hyndman, J. R, Bashtannyk, D. M., Grunwald, G. K. 1996. Estimating and visualizing conditional densities, Journal of Computational and Graphical Statistics, 5, 315-336.

Joe, H., Li, H., Nikoloulopoulos, A. K. 2010. Tail dependence functions and vine copulas, Journal of Multivariate Analysis, 101, 252-270.

Knight, K. 1998. Limiting distributions for regression estimators under general conditions, Annals of Statistics, 26, 755-770.

Kocherginsky, M., He, X., Mu, Y. 2005. Practical confidence intervals for regression quantiles, Journal of Computational and Graphical Statistics, 14, 41-55.

Koenker, R. 2005. Quantile Regression, New York, Cambridge University Press.

Kollo, T., Pettere, G., Valge, M. 2017. Tail dependence of skew t-copulas, Communications in Statistics - Simulation and Computation, 46, 1024-1034.

Li, G., Li, Y., Tsai, C-L. 2015. Quantile correlations and quantile autoregressive modeling, Journal of the American Statistical Association, 110, 246-261.

Meng, L., Shen, Y. 2014. On the relationship of soil moisture and extreme temperatures in east China, Earth Interactions, 18, 1-20.

Nikoloulopoulos, A. K., Joe, H., Li, H. 2012. Vine copulas with asymmetric tail dependence and applications to financial return data, Computational Statistics & Data Analysis, 56, 3659-3673.

Sayegh, A. S., Munir, S., Habeebullah, T. M. 2014. Comparing the performance of statistical models for predicting concentration, Aersol and Air Quality Research, 14, 653-665.

Villarini, G., Smith, J. A., Baeck, M. L., Vitolo, R., Stephenson, D. B., Krajewski, W. F. 2011. On the frequency of heavy rainfall for the Midwest of the United States, Jounral of Hydrology, 400, 103-120.