Optimality of multi-refraction dividend strategies in the dual model

Abstract.

We consider the multi-refraction strategies in two equivalent versions of the optimal dividend problem in the dual (spectrally positive Lévy) model. The first problem is a variant of the bail-out case where both dividend payments and capital injections must be absolutely continuous with respect to the Lebesgue measure. The second is an extension of Avanzi et al. [4] where a strategy is a combination of two absolutely continuous dividend payments with different upper bounds and different transaction costs. In both problems, it is shown to be optimal to refract the process at two thresholds, with the optimally controlled process being the multi-refracted Lévy process recently studied by Czarna et al. [9]. The optimal strategy and the value function are succinctly written in terms of a version of the scale function.

Numerical results are also given.

AMS 2010 Subject Classifications: 60G51, 93E20, 91B30

JEL Classifications: C44, C61, G24, G32, G35

Keywords: dividends; capital injection; Lévy processes; scale functions; dual

model

1. Introduction

In this paper, we study two equivalent optimal dividend problems. The first problem is an extension of the bail-out model where capital can be injected so as to reduce the risk of ruin. Contrary to the classical case, both dividend and capital injection strategies must be absolutely continuous with respect to the Lebesgue measure, with their densities required to be bounded by some fixed constants. Because of the restriction on capital injections, ruin may occur. The second problem pursues an optimal pair of two absolutely continuous dividend strategies with different upper bounds on the densities and with different proportional transaction costs. By incorporating the terminal payoff/cost at ruin, these two problems can easily be shown to be equivalent.

Regarding the first problem, the classical bail-out problem has been solved by Avram et al. [5] and Bayraktar et al. [6] for the spectrally negative and positive (dual) models, respectively. Without the absolutely continuous assumption on the dividend and capital injection strategies, it is optimal to reflect from below at zero and from above at some suitable barrier – the resulting surplus process becomes the doubly reflected Lévy process of Pistorius [19]. Recently, the case the dividend (and not the capital injection) strategy is absolutely continuous has been solved by Pérez et al. [17] and Pérez and Yamazaki [16], for the spectrally negative and positive models, respectively. They showed that it is optimal to reflect from below at zero and refract at a suitably chosen upper barrier, with the resulting process being the refracted-reflected Lévy process.

On the other hand, the second problem can be viewed as an extension to Avanzi et al. [4], where they considered the case a dividend strategy is composed of a singular and absolutely continuous parts with different associated transaction costs. They showed the optimality of a strategy that refracts the process at the lower threshold and reflects it at the upper barrier, similarly to the case in [16].

The objective of this current paper is to show, for both problems, the optimality of what we call the multi-refraction strategies, that refract the underlying process at two different thresholds, say , to be suitably chosen. More precisely, for the first problem, we aim to show that it is optimal to pay dividends at the maximum possible rate whenever the surplus is above while injecting capital at the maximum rate whenever it is below . For the second problem, it is optimal to activate fully one of the absolutely continuous strategies whenever the surplus is above while activating fully the other one as well if it is above .

We focus on the dual model, where the underlying (uncontrolled) surplus process follows a spectrally positive Lévy process. See Avanzi et al. [2, 3] for a more detailed motivation of this model.

Recently, Czarna et al. [9] studied a generalization of the refracted Lévy process of Kyprianou and Loeffen [14] with multiple refraction thresholds. Under a multi-refraction strategy, the resulting surplus process becomes precisely the one studied in [9], and hence the fluctuation identities obtained there can be directly used. The expected net present value (NPV) of dividends/capital injections for our problems can be written efficiently using the generalization of the scale function.

In order to solve the problems, we take the following steps:

-

(1)

Focusing on the set of multi-refraction strategies, we shall first select the two refraction thresholds and , so that the corresponding candidate value function, say , becomes smoother at these thresholds. More precisely, we choose these so that it is continuously differentiable (resp. twice continuously differentiable) for the case the underlying process has paths of bounded (resp. unbounded) variation. These conditions at and give us two equations, which we call and , respectively, in this paper. We select so that and hold if and , respectively.

-

(2)

We then show the optimality of the selected multi-refraction strategy. Toward this end, we obtain sufficient conditions for optimality (verification lemma) and show that the candidate value function indeed satisfies these.

We also conduct numerical experiments so as to confirm the obtained analytical results. We use the phase-type Lévy process of [1] whose scale function admits the form of a linear combination of (complex) exponentials (see [10]), and hence the optimal thresholds and and the value function can be computed instantaneously. We illustrate the computation procedures and also confirm the optimality of the multi-refraction strategies. Additionally, we analyze and confirm the convergence to other existing versions of the optimal dividend problems.

The rest of the paper is organized as follows. Section 2 formulates the two problems we study in this paper. We define the multi-refraction strategy and compute the expected NPV under this strategy in Section 3. In Section 4, we choose candidate optimal thresholds , whose optimality is confirmed in Section 5. We conclude the paper with numerical results in Section 6. Some proofs are deferred to the Appendix.

2. Mathematical models

In this section, we define the two problems considered in this paper.

2.1. Problem 1 (bail-out model with absolutely continuous assumptions)

Let be a Lévy process defined on a probability space , modeling the surplus of a company in the absence of control. We assume that it is spectrally positive or equivalently it has no negative jumps and is not a subordinator. For , we denote by the law of when it starts at and write for convenience in place of .

An admissible strategy is a pair of nondecreasing, right-continuous, and adapted processes (with respect to the filtration generated by ) such that where is the cumulative amount of dividends and is that of injected capital. In addition, for fixed, we require that and are absolutely continuous with respect to the Lebesgue measure of the forms and , , with and restricted to take values in, respectively, and uniformly in time. We will denote by the controlled surplus process associated with the strategy :

| (2.1) |

Assuming that is the cost per unit injected capital, the terminal payoff (if )/penalty (if ) at ruin, and the discount factor, we want to maximize

| (2.2) |

where

| (2.3) |

Hence the problem is to compute

where is the set of all admissible strategies that satisfy the constraints described above.

For this problem, we assume the following. Note that, without this condition, one can always avoid ruin by injecting enough capital.

Assumption 2.1.

We assume that process is not a subordinator.

2.2. Problem 2

We consider a variant of the problem studied in Avanzi et al. [4]. Let be a spectrally positive Lévy process, and, as in Problem 1, let be the expectation under which .

A strategy is a pair of two dividend strategies that satisfy the same properties required for of Problem 1, with the corresponding controlled surplus process

For , the unit dividend rate is while, for , proportional transaction costs are incurred and the unit dividend rate is . With the terminal payoff/penalty at ruin, one wants to maximize

| (2.4) |

where .

This can be easily transformed to Problem 1. To see this, setting the process and a strategy with

we have , (as in (2.1)), and hence (as in (2.3)). Now for all , with , (2.4) becomes

| (2.5) | ||||

In other words, the problem reduces to maximizing (2.2).

Because Problems 1 and 2 are equivalent, for the rest of the paper except for the numerical results given in Section 6, we focus on Problem 1.

3. Multi-refraction strategies

Our objective of this paper is to show the optimality of the multi-refraction strategy, say , with suitable refraction levels .

Fix . Under , dividends are paid at the maximal possible rate whenever the surplus is above while capital is injected at the maximal possible rate whenever it is below . In this case the aggregate process is given by

In order to see this is a well-defined process, note that, for all ,

| (3.1) | ||||

where

| (3.2) |

In addition, for , let

| (3.3) | ||||

which by Assumption 2.1 are spectrally negative Lévy processes (that are not the negative of subordinators).

The process is a spectrally negative multi-refracted Lévy process of [9] driven by the process with refraction thresholds , which is a unique strong solution to (3.1). It behaves like on , like on , and like on .

It is clear that the strategy is admissible and its expected NPV of the total payoff is given by

| (3.4) |

where and for , and

3.1. Scale functions

Using the results in [9], the expected NPV (3.4) under the multi-refraction strategy can be written in terms of the scale functions and of the spectrally negative Lévy processes for defined in (3.2) and (3.3).

Fix . Define the Laplace exponent of by such that

with its Lévy-Khintchine representation,

| (3.5) |

where , , and is a measure on that satisfies

We also define the Laplace exponents of for by

where .

The processes , for , have paths of bounded variation if and only if and ; in this case, we can write

where

| (3.6) |

and is a driftless subordinator.

Remark 3.1.

For the case of bounded variation, Assumption 2.1 is equivalent to .

Fix and . The -scale function of the process is defined as the continuous function on with its Laplace transform

| (3.7) |

where is the right-inverse given by . This function is unique, positive and strictly increasing and is further continuous for . We extend to the whole real line by setting for . We also define, for ,

| (3.8) | ||||

These scale functions are related by the following equalities: for ,

| (3.9) |

which can be proven by showing that the Laplace transforms on both sides are equal.

Regarding their asymptotic values as , we have, as in Lemmas 3.1 and 3.2 of [12],

| (3.10) | ||||

| (3.11) | ||||

and, as in Lemma 3.3 of [12],

| (3.12) | ||||

Here and for the rest of the paper, and , for any function , are the right-hand and left-hand derivatives, respectively, at .

Remark 3.2.

It is known that the right-hand and left-hand derivatives of the scale function always exist for all . If (and hence for as well) is of unbounded variation or the Lévy measure is atomless, it is known that is for . For more comprehensive results on the smoothness, see [8].

Finally, the following function will be important in the derivation of the results in the rest of the paper. For , we define

| (3.13) |

where the second equality holds by integration by parts. Differentiating (3.13) with respect to , we have, for ,

| (3.14) | ||||

| (3.15) |

3.2. Computation of (3.4)

Using the results obtained in [9], we present the following explicit form of the function . Its proof is deferred to Appendix A.

Lemma 3.1.

For and , we have

where

| (3.16) | ||||

| (3.17) | ||||

4. Selection of

In this section, using the smooth fit principle we choose the (candidate) optimal refraction thresholds, which we shall call . In particular, we shall choose their values so that becomes continuously differentiable (resp. twice continuously differentiable) for the case (and , ) are of bounded (resp. unbounded) variation.

We first differentiate the identities given in Lemma 3.1. The next two lemmas follow by direct differentiation and integration by parts, and hence we omit the proofs.

Lemma 4.1.

Fix . For ,

Lemma 4.2.

Fix . For , we have

By taking limits in the above identities, the following results are immediate.

Corollary 4.1.

Fix for the derivative at and for the derivative at . (i) We have

(ii) In particular, for the case of unbounded variation, we have

Corollary 4.2.

Fix for the derivative at and for the derivative at . (i) We have

(ii) In particular, for the case of unbounded variation, we have

4.1. Smooth fit

We shall now obtain the condition on the smoothness of at . By Corollaries 4.1(i) and 4.2(i) applied to Lemma 3.1,

where we define

Hence, for the case of bounded variation (with by (3.10)), the smoothness at holds if

On the other hand, for the case of unbounded variation, by Corollaries 4.1(ii) and 4.2(ii) applied to Lemma 3.1,

Hence, is twice continuously differentiable at if holds.

Similarly, we shall obtain the condition on the smoothness of at . We define, for ,

| (4.1) | ||||

Therefore, if condition is satisfied and , the continuous differentiability (resp. twice continuous differentiability) at for the case of bounded (resp. unbounded variation) holds on condition that

We shall now summarize the results below.

Lemma 4.3.

(1) Suppose is satisfied for . Then, is continuously differentiable (resp. twice continuously differentiable) at for the case of bounded (resp. unbounded) variation.

(2) Suppose in addition that is satisfied for . Then, is continuously differentiable (resp. twice continuously differentiable) at for the case of bounded (resp. unbounded) variation.

4.2. The existence of

For , in view of the above computations and the positivity of , there exists such that for and for . Hence,

-

(1)

when (or equivalently ), then is decreasing on and increasing on ;

-

(2)

when (or equivalently ), then is increasing.

Therefore, for each , is the minimizer such that

Because and , we have

Hence we have that if and only if

| (4.2) |

Lemma 4.4.

If , then is strictly decreasing to .

Proof.

In order to obtain the required smoothness for the function , we shall choose as follows. Suppose .

-

(1)

If , then we increase the value of until we attain such that (which exists and is unique by Lemma 4.4). We set , which is either zero or positive. By construction, is satisfied. When , attains a local minimum at and hence is satisfied. When , we must have

(4.3) because otherwise, by the relation 4.1, the function must attain a negative value (which contradicts with ).

-

(2)

If , we set .

Suppose . In this case, the terminal payoff dominates the perpetual dividend payoff and it is reasonably conjectured that it is optimal to liquidate as quickly possible. Hence, we set .

5. Optimality

In this section we will prove the optimality of the proposed multi-refraction strategy.

Suppose . Because in this case condition is satisfied, in view of Lemma 3.1 and using (3.14), we have, for ,

| (5.1) | ||||

On the other hand when , Lemma 3.1 gives

| (5.2) |

Theorem 5.1.

The multi-refraction strategy is optimal and the value function of the problem (2.2) is given by for all .

We call a function sufficiently smooth on if it is differentiable (resp. twice differentiable) on when is of bounded (resp. unbounded) variation.

We let be the operator acting on sufficiently smooth functions , defined by

| (5.3) |

The proof of the following lemma is deferred to Appendix B.

Lemma 5.1 (Verification lemma).

Suppose is an admissible dividend strategy such that is sufficiently smooth on and satisfies

| (5.4) | ||||

| (5.5) |

Then for all and hence is an optimal strategy.

Proposition 5.1.

(i) Suppose . The function is concave on , (with equality when ), and (with equality when ).

(ii) Suppose . The function is convex on , and for all .

Proof.

(i) (1) Let us suppose . For , differentiating (5.1) and by (3.14),

| (5.6) | ||||

and, by (3.15),

Hence, by the nonpositivity of as in (3.14), is concave on .

Note that (3.14), (4.1) and the fact that imply

Substituting the above expression and (3.15) in (5.7), we have

This is negative for all by the nonpositivity of as in (3.14).

Now, from (5.6), we deduce that and

which equals when because condition is satisfied, and is less than or equal to when , because of (4.3).

(2) Let us now suppose . Differentiating (5.2), we obtain that

| (5.8) | ||||

This implies that the function is strictly concave and hence

where the last inequality follows from (4.2).

(ii) Finally, let us consider the case . Because the equalities of (5.8) hold in this case, for , , and . This shows the result. ∎

The next result follows by a direct application of Proposition 5.1.

Lemma 5.2.

We have

Lemma 5.3.

Recall the generator as in (5.3). We have

Proof.

Recall the relationship (3.3). For and any sufficiently smooth function , let be the operator corresponding to the process , given by

| (5.9) |

First as in, for instance the proof of Theorem 2.1 in [6],

| (5.10) |

In addition, direct computation gives

| (5.11) |

On the other hand, by the proof of Lemma 4.5 of [7], we have that, for ,

| (5.12) | ||||

Now we write (5.1) as, for ,

| (5.13) | ||||

Now we have all the elements to prove Theorem 5.1.

6. Numerical Examples

We conclude the paper with numerical examples of the optimal dividend problem studied above. Here, we focus on the case

| (6.1) |

for some and . Here is a standard Brownian motion, is a Poisson process with arrival rate , and is an i.i.d. sequence of phase-type-distributed random variables with representation ; see [1]. These processes are assumed mutually independent.

The Laplace exponents of and () are then (with where )

which are analytic for every except at the eigenvalues of .

Suppose are the sets of the roots with negative real parts of the equality . We assume that the phase-type distribution is minimally represented and hence as ; see [1]. As in [10], if these values are assumed distinct, then the scale functions of for can be written, for all ,

| (6.2) |

respectively.

Let , , , , and . For the process in (6.1), we set , , and and, for , we use the phase-type distribution with that gives an approximation to the (folded) normal random variable with mean and variance (see [15] for the values of and ). For the terminal payoff , we consider Case 1 with and Case 2 with to obtain, respectively, the cases and (and ).

6.1. Computation of and

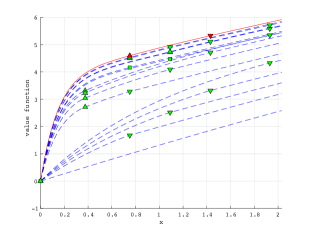

The first implementation step is the computation of the optimal thresholds . As we discussed in Section 4.2, we choose these such that and if (equivalently, (4.2) does not hold); for , we set . In both Cases 1 and 2, we have and hence . As we have shown in Section 4.2, attains its minimum at , which can be computed by bisection applied to the function . In addition, by Lemma 4.4, we can obtain the root of by another bisection method; the root becomes and . With these and , the value function becomes as in (5.1) when and (5.2) when .

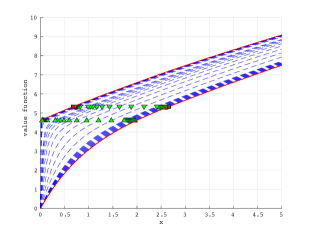

In Figure 1, we plot, for Cases 1 and 2, the mappings and for various values of . As in the proof of Lemma 4.4, is decreasing in . The value corresponds to the point (indicated by down-pointing triangles) at which attains a minimum and vanishes (if ). The curve touches and gets tangent to the x-axis at .

|

|

|

|

| Case 1 () | Case 1 () |

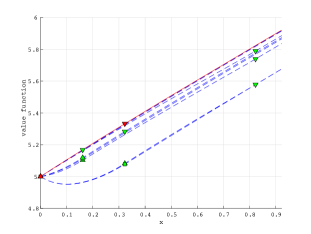

In Figure 2, we plot the corresponding value functions along with suboptimal NPVs given in Lemma 3.1 with . It can be confirmed in both Cases 1 and 2 that dominates uniformly in for .

|

|

| Case 1 () | Case 1 () |

6.2. Sensitivity and convergence

We next study the behavior of the value function with respect to the parameters that describe the problem. Here we use the same parameters as Case 1 unless stated otherwise.

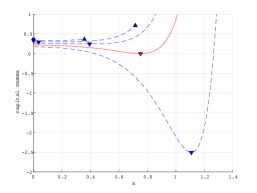

6.2.1. With respect to

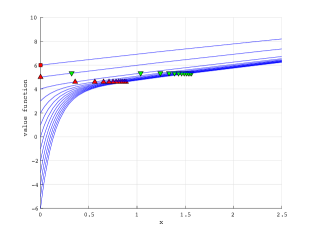

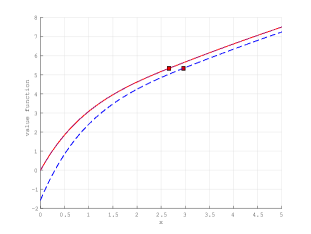

We first study the sensitivity with respect to the terminal payoff . In Figure 3, we plot along with the optimal thresholds and for ranging from to . It is clear that the value function is monotonically increasing in . When is large (), we have meaning that it is optimal to pay dividend as much as possible to enjoy quickly the terminal payoff. For the case , we have and, for the smaller values of , we have . We see that both and increase as decreases.

|

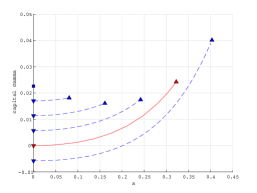

6.2.2. With respect to

We next analyze the behaviors with respect to the unit cost of capital injection . As , it becomes costly to inject capital and hence we expect that . Consequently, the value function approaches (when ) to that of Yin et al. [21] with the absolutely continuous assumption without capital injections: its optimal strategy is of threshold-type with the threshold such that

and the value function is given by

On the other hand, as and , the expected NPV of payoffs (3.4) converges to (with )

with . Its maximization corresponds to Yin et al. [21] with an additional terminal payoff . It is conjectured that the optimal strategy is of threshold-type. Consequently, we expect that as .

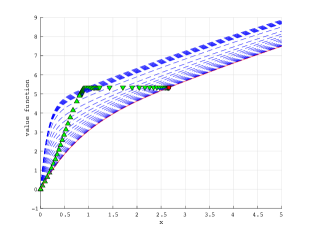

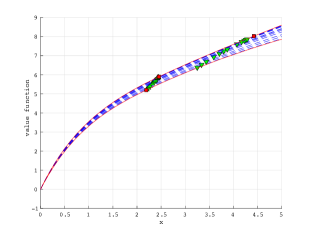

In Figure 4, we plot for various values of along with the limiting cases . It is confirmed that the value function is monotonically decreasing in . In addition, we see that, as , converges decreasingly to with and . On the other hand, as , we see that both and converge to the same value.

|

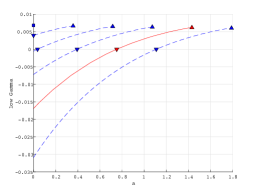

6.2.3. With respect to

We now analyze the behaviors with respect to . The case corresponds to Yin et al. [21] where, as reviewed above, its value function is with the optimal barrier . On the other hand, as , there are two possible scenarios either to let it liquidate (Case L) or to reflect the surplus to avoid ruin (Case R). It is easy to see that Case L is equivalent to the case ; in this case, because is monotonically increasing in , we have for any choice of .

Case R corresponds to Pérez and Yamazaki [16] with the absolutely continuous assumption on the dividend and classical capital injection: its value function is given by

with the optimal barrier given as the root of .

The left plot of Figure 5 shows the convergence of for Case R (the used parameters are the same as Case 1 ). Here, we plot for various values of along with the limiting case and . We see that, as , converges decreasingly to with . On the other hand, as , it converges increasingly to with and . The right plot of Figure 5 illustrates Case L (here we use the same parameters as Case 1 except that ) and shows in comparison to .

|

|

| Case R | Case L |

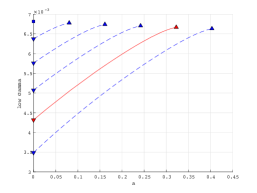

6.2.4. With respect to

For the analysis on , we consider Problem 2 that we described in Section 2.2 so as to analyze the convergence to the hybrid refracted-reflected case in Avanzi et al. [4].

Let be the value function for Problem 2 (which is equivalent to the maximal value of (2.5) with the optimal thresholds ). For the case , it reduces again to Yin et al. [21]. The value function becomes times the one reviewed above with replaced with : with the optimal threshold . On the other hand, as , the problem gets closer to the problem considered in Avanzi et al. [4] where a strategy is a combination of the absolutely continuous and singular control with transaction costs and , respectively. We refer the reader to Avanzi et al. [4] for the form of the value function and the characterization of the optimal barriers .

In Figure 6, we plot for various values of along with and . It is confirmed that is increasing in . We see that, as , the value function converges decreasingly to the limiting case with . On the other hand, as , the value function converges increasingly to with and .

|

Appendix A Proof of Lemma 3.1

Throughout this Appendix, we fix . Let us define, for ,

| (A.1) | ||||

and, for ,

| (A.2) | ||||

Let as in (3.1) and .

First, by Theorem 3 in [9], we have

| (A.3) |

On the other hand, for the expected NPV of capital injections, by Theorem 4 in [9],

Lemma A.1.

For , we have .

Proof.

Applying in (A.1) and changing variables, we obtain the result. ∎

Lemma A.2.

For , we have .

Proof.

By Lemma 14 in [9],

| (A.6) | ||||

| (A.7) |

Appendix B Proof of Lemma 5.1

By the definition of as a supremum, it follows that for all . We write and show that for all for all .

Fix , and let be the sequence of stopping times defined by . Since is a semi-martingale and is sufficiently smooth on by assumption, we can use the change of variables/Meyer-Itô’s formula (cf. Theorems II.31 and II.32 of [20]) to the stopped process to deduce under that

where is a local martingale defined in (5.8) of [4].

Note that from (2.2), and the fact that and a.s. for all , we have

References

- [1] Asmussen, S., Avram, F., and Pistorius, M.R. Russian and American put options under exponential phase-type Lévy models. Stochastic Process. Appl. 109(1), 79–111, (2004).

- [2] Avanzi, B., Gerber, H.U., and Shiu, E. Optimal dividends in the dual model. Insur. Math. Econ. 41(1), 111-123, (2007).

- [3] Avanzi, B. and Gerber, H.U. Optimal dividends in the dual model with diffusion. Astin Bull. 38(2), 653-667, (2008).

- [4] Avanzi, Pérez, J.L., Wong, B, and K. Yamazaki. On the Joint Reflective and Refractive Dividend Strategies in Spectrally Positive Lévy Models. Insur. Math. Econ. (forthcoming).

- [5] Avram, F., Palmowski, Z., and Pistorius, M.R. On the optimal dividend problem for a spectrally negative Lévy process. Ann. Appl.Probab. 17, 156-180, (2007).

- [6] Bayraktar, E., Kyprianou, A.E., and Yamazaki, K. On optimal dividends in the dual model. Astin Bull. 43(3), 359-372, (2013).

- [7] Bayraktar, E., Kyprianou, A.E., and Yamazaki, K. Optimal dividends in the dual model under transaction costs. Insur. Math. Econ. 54, 133-143, (2014).

- [8] Chan, T., Kyprianou, A.E., and Savov, M. Smoothness of scale functions for spectrally negative Lévy processes. Probab. Theory Relat. Fields 150, 691-708, (2011).

- [9] Czarna, I., Pérez, J. L., Rolski, T., and Yamazaki, K. Fluctuation theory for level-dependent Lévy risk processes. preprint.

- [10] Egami, M. and Yamazaki, K. Phase-type fitting of scale functions for spectrally negative Lévy processes. J. Comput. Appl. Math. 264, 1–22, (2014).

- [11] Egami, M. and Yamazaki, K. Precautionary measures for credit risk management in jump models. Stochastics, 85(1), 111–143, (2013).

- [12] Kuznetsov, A., Kyprianou, A.E., and Rivero, V. The theory of scale functions for spectrally negative Lévy processes. Lévy Matters II, Springer Lecture Notes in Mathematics, (2013).

- [13] Kyprianou, A.E. Fluctuations of Lévy processes with applications. Second edition, Springer, Berlin, (2006).

- [14] Kyprianou, A.E. and Loeffen, R. Refracted Lévy processes. Ann. Inst. H. Poincaré, 46(1), 24–44, (2010).

- [15] Leung, T., Yamazaki, K., and Zhang, H. An analytic recursive method for optimal multiple stopping: Canadization and phase-type fitting. Int. J. Theor. Appl. Finance 18(5), 1550032, (2015). spectrally negative Lévy processes. arXiv 1410.5341v2, (2015).

- [16] Pérez, J.L. and Yamazaki, K. Refraction-Reflection Strategies in the Dual Model. ASTIN Bulletin 47(1), 199–238, 2017.

- [17] Pérez, J.L., Yamazaki, K. and Yu, X. The bail-out optimal dividend problem under the absolutely continuous condition. arXiv 1709.06348, 2017.

- [18] Pistorius, M.R. An excursion-theoretical approach to some boundary crossing problems and the Skorokhod embedding for reflected Lévy processes. Seminaire de Probabilités XL, 287–307, (2007).

- [19] Pistorius, M.R. On doubly reflected completely asymmetric Lévy processes. Stochastic Process. Appl. 1107 (1), 131-143, (2003).

- [20] Protter, P. Stochastic integration and differential equations. 2nd Edition, Springer, Berlin, (2005).

- [21] Yin, C., Wen, Y., and Zhao, Y. On the optimal dividend problem for a spectrally positive Lévy process. ASTIN Bulletin, 44(3), 635–651, (2014).