First passage upwards for state dependent-killed spectrally negative Lévy processes

Abstract.

For a spectrally negative Lévy process , killed according to a rate that is a function of its position, we complement the recent findings of [9] by analysing (in greater generality) the exit probability of the one-sided upwards-passage problem. When is strictly positive, this problem is related to the determination of the Laplace transform of the first passage time upwards for that has been time-changed by the inverse of the additive functional . In particular our findings thus shed extra light on related results concerning first passage times downwards (upwards) of continuous state branching processes (spectrally negative positive self-similar Markov processes).

Key words and phrases:

Spectrally negative Lévy processes; first passage upwards; killing; time-changes2010 Mathematics Subject Classification:

Primary: 60G51; Secondary: 60J25, 60G441. Introduction

Let be a spectrally negative Lévy process (snLp) under the probabilities . This means that is a càdlàg, real-valued process with no positive jumps and non-monotone paths, which, under , a.s. vanishes at zero and has stationary independent increments; furthermore, for each , the law of under is that of under . We refer to [1, 8, 3, 10] for the general background on (the fulctuation theory of) Lévy processes and to [1, Chapter VII] [8, Chapter 8] [3, Chapter 9] [10, Section 9.46] for snLp in particular. As usual we set . For denote next by the first hitting time of the set by the process . Further, let and let be an exponentially with mean distributed random variable ( a.s.) independent of (under for all ). Finally, let be Borel measurable and locally bounded. Then, for real , we will be interested in the quantity111Throughout we will write for , for , for ( an event) and for ( a sub--field).

| (1.1) |

This may be interpreted as the ultimate passage probability of , killed at , over the level , when started at , under “-killing”, i.e. when is killed (in addition to being killed at the time ) according to a rate that depends on the position of and that is given by the function . Of course , but it will be convenient to keep the independent exponential killing separate.

Assume now that is strictly positive everywhere. Our main motivation for the interest in (1.1) comes from its involvement in the solution of the first passage problem upwards for the process that we will denote by , and that is defined as follows. Setting (see [4] for conditions on the finiteness/divergence of this integral in the case , i.e. ), then

| for , , where is some “cemetery” state, whilst for , , | (1.2) |

with

Notice that is continuous (because is strictly positive, and hence strictly increasing) and it is strictly increasing where it is finite (because is locally bounded, and hence continuous). Thus the paths of up to are the same as the paths of up to – modulo the random time change . Also, if is any filtration relative to which is adapted and has independent increments, with independent of , then thanks to the strong Markov property of and the memoryless property of the exponential distribution, the process is Markovian with state space and life-time under the probabilities and in the filtration , in the precise sense that it is -adapted and that for any Borel measurable , and any , , a.s.-, . (Of course if in addition one has a such that for all a.s.-, then as a consequence is also simply Markovian with state space and infinite life-time.)

By way of example, when and , then, under the probabilities , is a spectrally negative positive self-similar Markov process (pssMp) absorbed at the origin, with index of self-similarity , associated to via the Lamperti transform for pssMp [8, Theorem 13.1]. And, for , on , is the first time that hits the set , the latter time being on the complement of . See Example 6. Similarly, for , with for and again , becomes, under the probabilities , a continuous state branching process (csbp) stopped on hitting the set , where is the csbp associated to under the Lamperti transform for csbp [8, Theorem 12.2].222We are forced to stop at in order to remain in the setting of a locally bounded , which is an assumption that remains in force throughout this paper. And, on , is the first time hits , the latter time being on the complement of . See Example 8.

More generally, denote for , by the first hitting time of the set by the process . Then, for , and real , under , the Laplace transform of on , at the point , is given simply by

| (1.3) |

Moreover, knowledge of this expression automatically furnishes also the joint Laplace transform of and : if further , then .

Literature-wise, fluctuation results for the “-killed” snLp have been the subject of the substantial recent study of [9] to which the reader is referred for a further review of existing and related results as well as extra motivation for considering such processes.

Our contribution is only a small complement to the findings of [9], but still one that seems to deserve recording. To be precise, [9] provides information on the one-sided upwards passage problem when is constant on (see [9, Section 2.4]); we will extend this to a far more general class of functions . In this class, the solution to (1.1) will be given in terms of a function that will be found to solve (uniquely) a natural convolution equation on the real line involving the -scale function of (Theorem 2). In contrast to the two-sided exit problem, where the pertinent convolution equation is on the nonnegative half-line [9, Eq. (1.2)], this introduces some extra finiteness issues, making the analysis slightly more delicate. The function will also be associated with a family of (local) martingales involving the process (Proposition 12).

To avoid unnecessary repetition we turn to the results and their proofs presently in Section 3, after briefly introducing some necessary further notation and recalling some known facts in Section 2. Section 4 concludes by illustrating the findings in the context of determining the optimal level at which to sell an asset whose price process is given by the exponential of the process from (1.2).

2. Further notation and some preliminaries

We denote by the Laplace exponent of , for ; and by its right-continuous inverse, for ; is strictly convex and continuous, and is the largest zero of . For real recall the classical identity [8, Eq. (3.15)]

| (2.1) |

Further, for , will be the -scale function of , characterized by being continuous on , vanishing on , and having Laplace transform

| (2.2) |

In particular we set . The reader is referred to [7] for further background on scale functions of snLp; we note explicitly only the asymptotic behavior [7, Eq. (33), Lemmas 2.3 and 3.3]

| (2.3) |

that we shall use repeatedly in what follows (here when , and otherwise ; is the scale function of an Esscher transformed process – its precise character is unimportant, what matters is only the monotone convergence).

Convolution on the real line will be denoted by a : for Borel measurable ,

whenever the Lebesgue integral is well-defined.

Finally, it will be convenient to introduce the following concepts.

Definition 1.

For a function , we will (i) say that it has a bounded left tail (resp. left tail that is bounded below away from zero) if is bounded (resp. bounded below away from zero) on for some ; (ii) for further , say that it has a left tail that is -subexponential provided that for some , some , and then all , one has ; and (iii) say simply that it has a subexponential left tail if, for some , it has a left tail that is -subexponential.

3. Results and their proofs

Here is now the main result of this note.

Theorem 2.

There exists a unique function satisfying (the arbitrary normalization condition) such that

| (3.1) |

The function enjoys the following properties.

-

(I)

It is nondecreasing (hence locally bounded), continuous, and it is strictly increasing provided .

-

(II)

For each the following holds: implies for some ; this being if .333 means the function . More generally, throughout this text, given an expression defined for we will write for the function .

-

(III)

If are both locally bounded and Borel measurable with (resp. ), then (resp. ) on and (resp. ) on (of course ).

-

(IV)

For real , , in particular for all , so that has a left tail that is -subexponential.

Furthermore, if is finite-valued for all , then for some unique , satisfies the convolution equation

| (3.2) |

More specifically:

-

(i)

If moreover has a left tail that is bounded and bounded below away from zero, then satisfies the (homogeneous) convolution equation

(3.3) -

(ii)

If even is finite-valued, in particular if has a subexponential left tail, then is the unique locally bounded Borel measurable function admitting a left tail that is -subexponential and satisfying the (inhomogeneous) convolution equation

(3.4) where

(3.5) This function is given as , where and recursively for .

After some remarks and examples we turn to the proof of this theorem on p. 3.

Remark 3.

Since , (3.3) may be rewritten as . For the same reason, when , then automatically .

Remark 4.

Because of (2.3) cases i and ii are seen to be mutually exclusive (but they are not exhaustive). Of course is finite-valued for all iff is finite-valued for all , in which case, for each , falls under the provisos of ii. For the resulting convolution equation (3.4) we then have suitable uniqueness of the solution as well as an explicit recursion to (at least in principle) produce it. At the same time, by bounded convergence in (3.1)-(1.1), .

Example 5.

Example 6.

When , with and , a case that falls under ii, one obtains using (2.2)

| (3.6) |

with the series converging to finite values. (As usual the empty product is interpreted as being equal to .) Of course when , then from (3.1), by spatial homogeneity, , . Note that this reproduces (up to trivial transformations) Patie’s scale functions from the fluctuation theory of spectrally negative pssMp [8, Section 13.7]. One also identifies the limit (3.5) as .

Remark 7.

Example 8.

Let , and for . Using the result for csbp of [5, Theorem 1] we identify up to a multiplicative constant;

where is arbitrary but fixed. Note that this falls neither under i nor under ii, but it does fall under (3.2). In fact, while it is not so obvious, an easy computation shows that (3.2) is verified in this case with .

Example 9.

Let , , and for . Except possibly when , we then automatically have, because of the asymptotic properties of , see (2.3), that is finite-valued, and in any event we assume now that this is so. Then note, using (2.2), that, for , and for , , which implies . Hence, letting , by monotone convergence, . Thus the recursion of ii allows us to identify , up to a proportionality constant, as an infinite series of iterated integrals;

Remark 10.

In connection to the results of [9]:

- (a)

-

(b)

In [9, Eq. (2.25)], for real , the “-resolvent” identity is formally asserted only for the case when is constant, but it prevails of course in full generality (with our replacing the there): the proof consists only in using the resolvent identity for the two-sided exit problem [9, Eq. (2.15)] and the fact that . For this reason we omit reproducing the expression here.

- (c)

Proof of Theorem 2.

Let be real numbers. Since has no positive jumps, then -a.s. on , and it follows by the strong Markov property of applied at the time and the memoryless property of the exponential distribution, that one has the multiplicative structure

Furthermore, it is clear that for all real . As a consequence we may unambiguously define (with a preemptive choice of notation) for real , . In short, then, , , and (3.1) holds. It is clear that is unique in having the preceding properties.

Statements I-II-III, apart from the continuity of , follow immediately from (3.1)-(1.1) and simple comparison arguments. To prove continuity of note that for real , as , and that further for , by quasi-left-continuity and regularity of for , -a.s. also (on and hence everywhere) as . Then use bounded convergence in (3.1)-(1.1), exploiting the facts that is locally bounded and that the law of the overall supremum has no finite atoms, which implies that a.s.- on also for all that are sufficiently close to . (That the law of has no finite atoms follows for instance from (2.1) and the continuity of .) For IV, notice that by (2.1), for real .

We now prove i. Since the homogeneous convolution equation (3.3) may be checked “locally”, separately on each for , we may assume (replacing by if necessary) that is bounded by a . Also, there is an such that is bounded below away from zero on by some . Let again be real numbers. Then, using the resolvent [7, Theorem 2.7(ii)]

as well as the classical identity (2.1) , it follows via the marked Poisson process technique of [9] – letting be the arrival times of a homogeneous Poisson process of intensity , marked by an independent sequence of i.i.-uniformly on -d. random variables – that

| (3.7) |

Next, plugging (3.1) into (3.7), multiplying both sides by and letting , we obtain by monotone convergence using (2.3) that

with ; a priori this limit must exist in . Now convolute both sides of the preceding display by , exploiting the relations (which is a direct consequence of (2.2)) and (which may be checked by taking Laplace transforms and again using (2.2)) that together imply , to obtain

Then the estimate for implies (via (2.2) and the local boundedness of and ) that is finite-valued and upon subtracting finite quantities we obtain (3.3). This concludes the proof of i.

Suppose now is finite-valued for all . From i, for each and , one has, for all ,

| (3.8) |

We now first pass to the limit as follows. In (3.1)-(1.1) monotone (for the integral against the Lebesgue measure) and bounded (for the expectation) convergence yield as . Then in (3.8) monotone (for the integrals on ; recall III) and dominated (for the integrals on ; using the assumed integrability condition and the estimate for ) convergence produce

| (3.9) |

Let us next write, for the purposes of the remainder of this proof only, and for short. We proceed to pass to the limit . In (3.1)-(1.1), similarly as before, by bounded (for the integral against the Lebesgue measure; recall is locally bounded) and monotone (for the expectation) convergence, we obtain that as . Then in (3.9), , as , by monotone (for the integral on ; recall III) and bounded (for the integral on ; use the facts that is nondecreasing, that is bounded in bounded given a fixed , and that and are locally bounded) convergence. Finally we consider

a priori this limit must exist in . We show that does not depend on , thus demonstrating that (3.2) is indeed satisfied for some, necessarily unique, .

Now, since is locally bounded, since is nondecreasing, and since is bounded in bounded given a fixed real , it is clear that for any choice of ,

Suppose now first that . Then, given any we may (2.3) choose this to be (for simplicity) and such as to render for all . Consequently, since (using the estimate for ) , we conclude that in fact does not depend on . For the case when , i.e. the case , we have that for any . We argue that for that are (again for simplicity) , which will complete the verification that does not depend on . Indeed, since for , we have that .

We have, regarding uniqueness of the solutions to (3.4), the following

Lemma 11.

Suppose is finite-valued (which obtains if has a subexponential left tail). Let be Borel measurable and locally bounded with a left tail that is -subexponential. Then:

-

(i)

.

-

(ii)

implies .

-

(iii)

Let now further be locally bounded Borel measurable with a left tail that is -subexponential. Suppose and . Then , where the are given recursively: and for .

Proof.

i. We have . Since has a left tail that is -subexponential and since it is locally bounded it follows that there is a such that for all (say). Therefore, for , , which is by assumption. Now by (2.3) is nonincreasing to as . Thus the conclusion follows by dominated convergence.

ii. Denote, for , . Note this quantity is finite because has a tail that is -subexponential and because it is locally bounded. Then implies that for all one has . By i as , so there is an such that for all . At the same time, the above estimate implies , hence , which forces to vanish on . Let us now shift all the functions by for (notational) convenience; to wit and are Borel measurable, locally bounded and . From this we obtain finally that by the following argument. Fix and let be an upper bound for on . We may choose such that . Denote . Then, for each , and (2.2) imply . Again this renders , and completes the proof of ii.

As is to be expected, the solution to (1.1) is associated to a family of (local) martingales. Recall the process from (1.2).

Proposition 12.

Let , . Define the processes and as follows:

and

Let further be any filtration relative to which is adapted and has independent increments. Then:

-

(i)

The stopped process is a bounded càdlàg martingale in the filtration under for each ; for real the -terminal value of this martingale is .

-

(ii)

Assume is strictly positive and is independent of (under for each ). Then the stopped process is a càdlàg bounded martingale in the filtration under for each .

Remark 13.

As a check, since has a constant expectation, we recover (1.3) in the limit as time goes to infinity.

Proof.

We may assume .

i. Let . Then in Markov process theory parlance (for notational simplicity only; ultimately no shift operators are of course needed here) and -a.s. , which establishes the first claim.

ii. For all real , , applying the optional sampling theorem to the process at the times and , we obtain

i.e., because on , since is the inverse of , and by the independence of from ,

This implies that stopped at is a martingale in the filtration under , because this process is constant on , and since for , with the equality of the trace -fields holding true. Replacing with shows the same is true of the process stopped at . ∎

Apart from the solutions presented in Examples 5, 6, 8 and 9, it seems difficult to come up with “nice” for which is given explicitly (in terms of and , say), at least for a general . However, based on Example 6, we can “reverse-engineer” a class of for which is explicit, in the precise sense of

Proposition 14.

Let be a probability measure on the Borel sets of whose support is compactly contained in . Denote, for , and . Then and , where and, for , and .

Proof.

The fact that has a bounded support ensures that is locally bounded. We know for each . Integrating both sides against we obtain via Tonelli’s theorem (relevant measurabilities follow from the explicit form of the given in Example 6) . At the same time, for , so has a left tail that is -subexponential. Next, because the support of is bounded from below away from zero, has a subexponential left tail. By Lemma 11 we obtain . But we also have , hence , and the proof is complete. ∎

Another fairly general class of that can be handled with some success is considered in

Remark 15.

Let be a real polynomial, and . Suppose for all . Then the recursion of Theorem 2ii can, on , be successively computed in essentially closed form: one obtains algebraic expressions involving only and its higher-order derivatives. This is because, together with the Laplace transform of (2.2) that is given in terms of , one obtains, by successive differentiation, also expressions for its higher order derivatives. In a similar vein, if and for , then one gets iterated integrals involving (cf. Example 9).

4. Application to a model for the price of a financial asset

Assume . We consider the process defined by

as a model for the price of a (speculative) financial asset (here is the process from (1.2)). When , then , on , and is nothing but the classical exponential Lévy model for the price of a risky asset (defaulted at ), see [11] for a recent review. The idea with allowing a more general is that the asset price may “move faster or slower along its trajectory”, depending on the price level, destroying the stationary independent increments property of the log-returns, but preserving their Markovian character.

Using time changed Lévy processes to model financial assets is of course not new, see e.g. [2, 6]. We set , , for convenience.

Suppose then in this setting that we are interested in the simple problem of the determination of the optimal level at which to sell the asset, having bought it at the level , under an inflation/impatience rate . In other words, if we let denote the first hitting time of the set by the process , then we would like a solution to the problem

| (4.1) |

(More generally we may simply be interested in itself, if we are predetermined to sell at the level .) But, for , since on ,

Hence (4.1) is intimately related to the determination of the quantity (1.1).

Now if , then, of course, because of the martingale property of and the optional sampling theorem, is monotone in , and the problem is trivial. However, for a general this is no longer the case, as we will see on an example shortly.

Let indeed and : as a possible rationale for such a choice, one may imagine that the asset moves faster along its trajectory at smaller price levels, reflecting that the investors are then more jittery, increasing the velocity of the trades. In this case we can be quite explicit about the nature of , as follows. Denote , and by the Patie scale function (3.6) of Example 6, so that and

where we have set for . Then on , while for ,

| (4.2) |

where

| (4.3) |

As in the proof of Lemma 11 one sees that, on , where and then recursively for , the latter convolution being now on . Taking Laplace transforms on in (4.2) (denoting them by a hat) and using (2.2), it is also true that and hence

| (4.4) |

(using Theorem 2III and the known solution for it is easily checked that for ).

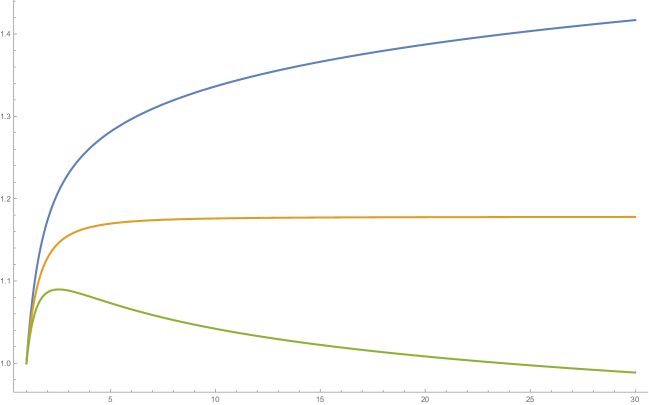

Now if , then a comparison argument (with ) shows that as . However, in general, it does not seem obvious how to determine an optimal analytically, nor is it our intent to pursue this further here; we content ourselves by demonstrating how may fail to be monotone in . This transpires already in the (presumably simplest) case when , , corresponding to being a multiple (by the factor ) of Brownian motion, and , . Under the latter specifications, and , while and (via (4.3)) , , where . Inverting the Laplace transform (4.4) for we obtain

see Figure 1.

References

- [1] J. Bertoin. Lévy Processes. Cambridge Tracts in Mathematics. Cambridge University Press, Cambridge, 1996.

- [2] P. Carr and L. Wu. Time-changed Lévy processes and option pricing. Journal of Financial Economics, 71(1):113 – 141, 2004.

- [3] R. A. Doney. Fluctuation Theory for Lévy Processes: Ecole d’Eté de Probabilités de Saint-Flour XXXV - 2005.

- [4] Leif Döring and A. E. Kyprianou. Perpetual integrals for Lévy processes. Journal of Theoretical Probability, 29(3):1192–1198, 2016.

- [5] X. Duhalde, C. Foucart, and C. Ma. On the hitting times of continuous-state branching processes with immigration. Stochastic Processes and their Applications, 124(12):4182 – 4201, 2014.

- [6] S. Klingler, Y. S. Kim, S. T. Rachev, and F. J. Fabozzi. Option pricing with time-changed Lévy processes. Applied Financial Economics, 23(15):1231–1238, 2013.

- [7] A. Kuznetsov, A. E. Kyprianou, and V. Rivero. The theory of scale functions for spectrally negative Lévy processes. In Lévy Matters II: Recent Progress in Theory and Applications: Fractional Lévy Fields, and Scale Functions, pages 97–186. Springer Berlin Heidelberg, Berlin, Heidelberg, 2013.

- [8] A. E. Kyprianou. Fluctuations of Lévy Processes with Applications: Introductory Lectures. Springer-Verlag, Berlin Heidelberg, 2014.

- [9] B. Li and Z. Palmowski. Fluctuations of Omega-killed spectrally negative Lévy processes. Stochastic Processes and their Applications, 2016.

- [10] K. I. Sato. Lévy Processes and Infinitely Divisible Distributions. Cambridge studies in advanced mathematics. Cambridge University Press, Cambridge, 1999.

- [11] P. Tankov. Pricing and hedging in exponential Lévy models: Review of recent results. In Paris-Princeton Lectures on Mathematical Finance 2010, pages 319–359. Springer Berlin Heidelberg, Berlin, Heidelberg, 2011.