Soft-Robust Actor-Critic Policy-Gradient

Abstract

Robust Reinforcement Learning aims to derive an optimal behavior that accounts for model uncertainty in dynamical systems. However, previous studies have shown that by considering the worst case scenario, robust policies can be overly conservative. Our soft-robust framework is an attempt to overcome this issue. In this paper, we present a novel Soft-Robust Actor-Critic algorithm (SR-AC). It learns an optimal policy with respect to a distribution over an uncertainty set and stays robust to model uncertainty but avoids the conservativeness of robust strategies. We show the convergence of SR-AC and test the efficiency of our approach on different domains by comparing it against regular learning methods and their robust formulations.

1 INTRODUCTION

Markov Decision Processes (MDPs) are commonly used to model sequential decision making in stochastic environments. A strategy that maximizes the accumulated expected reward is then considered as optimal and can be learned from sampling. However, besides the uncertainty that results from stochasticity of the environment, model parameters are often estimated from noisy data or can change during testing [Mannor et al., 2007; Roy et al., 2017]. This second type of uncertainty can significantly degrade the performance of the optimal strategy from the model’s prediction.

Robust MDPs were proposed to address this problem [Iyengar, 2005; Nilim and El Ghaoui, 2005; Tamar et al., 2014]. In this framework, a transition model is assumed to belong to a known uncertainty set and an optimal strategy is learned under the worst parameter realizations. Although the robust approach is computationally efficient when the uncertainty set is state-wise independent, compact and convex, it can lead to overly conservative results [Xu and Mannor, 2012; Yu and Xu, 2016; Mannor et al., 2012, 2016].

For example, consider a business scenario where an agent’s goal is to make as much money as possible. It can either create a startup which may make a fortune but may also result in bankruptcy. Alternatively, it can choose to live off school teaching and have almost no risk but low reward. By choosing the teaching strategy, the agent may be overly conservative and not account for opportunities to invest in his own promising projects. Our claim is that one could relax this conservativeness and construct a softer behavior that interpolates between being aggressive and robust. Ideally, the soft-robust agent should stay agnostic to outside financing uncertainty but still be able to take advantage of the startup experience.

This type of dilemma can be found in various domains. In the financial market, investors seek a good trade-off between low risk and high returns regarding portfolio management [Mitchell and Smetters, 2013]. In strategic management, product firms must choose the amount of resources they put into innovation. A conservative strategy would then consist of innovating only under necessary conditions [Miller and Friesen, 1982].

In this paper, we focus on learning a soft-robust policy (defined below) by incorporating soft-robustness into an online actor-critic algorithm and show its convergence properties. Existing works mitigate conservativeness of robust MDP either by introducing coupled uncertainties [Mannor et al., 2012, 2016] or by assuming prior information on the uncertainty set [Xu and Mannor, 2012; Yu and Xu, 2016]. They use dynamic programming techniques to estimate a robust policy. However, these methods present some limiting restrictions such as non-scalability and offline estimation. Besides being computationally more efficient than batch learning [Wiering and van Otterlo, 2012], the use of an online algorithm is of significant interest in robust MDPs because it can detect non-adversarial state-actions pairs along a trajectory and result in less conservative results, something which cannot be performed when solving the planning problem [Lim et al., 2016]. Other works have attempted to incorporate robustness into an online algorithm for policy optimization [Tamar et al., 2015; Mankowitz et al., 2018]. Although these approaches can deal with large domains, a sampling procedure is required for each critic estimate in Tamar et al. [2015], which differs from the strictly-speaking actor-critic. In Mankowitz et al. [2018], the authors introduce a robust version of actor-critic policy-gradient but its convergence results are only shown for the actor updates. Moreover, these works target the robust solution which may be too conservative. We review all existing methods in Section 7 and compare them to our approach.

To the best of our knowledge, our proposed work is the first attempt to incorporate a soft form of robustness into an online algorithm that has convergence guarantees besides being computationally scalable. We deal with the curse of dimensionality by using function approximation that parameterizes the expected value within a space of much smaller dimension than the state space. By fixing a distribution over the uncertainty set, the induced soft-robust actor-critic learns a locally optimal policy in an online manner. Under mild assumptions on the set of distributions and uncertainty set, we show that our novel Soft-Robust Actor-Critic (SR-AC) algorithm converges. We test the performance of soft-robustness on different domains, including a large state space with continuous actions. As far as we know, no other work has previously incorporated robustness into continuous action spaces.

Our specific contributions are: (1) A soft-robust derivation of the objective function for policy-gradient; (2) An SR-AC algorithm that uses stochastic approximation to learn a variant of distributionally robust policy in an online manner; (3) Convergence proofs of SR-AC; (4) An experiment of our framework to different domains that shows the efficiency of soft-robust behaviors in a continuous action space as well. All proofs can be found in the Appendix.

2 BACKGROUND

In this section, we introduce the background material related to our soft-robust approach.

Robust MDP A robust MDP is a tuple where is a finite state-space, is a finite set of actions, is the immediate reward function which is deterministic and bounded and is a set of transition matrices. We assume that is structured as a cartesian product , which is known as the rectangularity assumption [Nilim and El Ghaoui, 2005]. Given a state , the uncertainty set is a family of transition models we represent as vectors in which the transition probabilities of each action are arranged in the same block. For and , denote by the probability of getting from state to state given action .

At timestep , the agent is in state and chooses an action according to a stochastic policy that maps each state to a probability distribution over the action space, denoting the set of distributions over . It then gets a reward and is brought to state with probability .

Policy-Gradient Policy-gradient methods are commonly used to learn an agent policy. A policy is parametrized by and estimated by optimizing an objective function using stochastic gradient descent. A typical objective to be considered is the average reward function

where is the reward at time , an aperiodic and irreducible transition model under which the agent operates and is the stationary distribution of the Markov process induced by under policy . The gradient objective has previously been shown to be

where is the expected differential reward associated with state-action pair . This gradient is then used to update the policy parameters according to: , with a positive step-size [Sutton et al., 2000].

Actor-Critic Algorithm Theoretical analysis and empirical experiments have shown that regular policy-gradient methods present a major issue namely high variance in the gradient estimates that results in slow convergence and inefficient sampling [Grondman et al., 2012]. First proposed by Barto et al. [1983], actor-critic methods attempt to reduce the variance by using a critic that estimates the value function. They borrow elements from both value function and policy-based methods. The value function estimate plays the role of a critic that helps evaluating the performance of the policy. As in policy-based methods, the actor then uses this signal to update policy parameters in the direction of a gradient estimate of a performance measure. Under appropriate conditions, the resulting algorithm is tractable and converges to a locally optimal policy [Konda and Tsitsiklis, 2000; Bhatnagar et al., 2009].

Deep Q-networks Deep Q-Networks (DQNs) have proven their capability of solving complex learning tasks such as Atari video games [Mnih et al., 2013]. The Q-learning of Watkins and Dayan [1992] typically learns a greedy or -greedy policy by updating the Q-function based on a TD-error. In Deep Q-learning [Mnih et al., 2013, 2015], a non-linear function such as a neural network is used as an approximator of the Q-function. It is referred to as a Q-network. The agent is then trained by optimizing the induced TD loss function thanks to stochastic gradient descent. Like actor-critic, DQN is an online algorithm that aims at finding an optimal policy. The main difference with actor-critic is that it is off-policy: it learns a greedy strategy while following an arbitrary behavior [Mnih et al., 2013].

Deep Deterministic Policy-Gradient Since DQN acts greedily at each iteration, it can only handle small action spaces. The Deep Deterministic Policy-Gradient (DDPG) is an off-policy algorithm that can learn behaviors in continuous action spaces [Lillicrap et al., 2016]. It is based on an actor-critic architecture that follows the same baseline as in DQN. The critic estimates the current Q-value of the actor using a TD-error while the actor is updated according to the critic. This update is based on the chain rule principle which establishes equivalence between the stochastic and the deterministic policy gradient [Silver et al., 2014].

3 SOFT-ROBUSTNESS

3.1 SOFT-ROBUST FRAMEWORK

Unlike robust MDPs that maximize the worst-case performance, we fix a prior on how transition models are distributed over the uncertainty set. A distribution over is denoted by and is structured as a cartesian product . We find the same structure in Xu and Mannor [2012]; Yu and Xu [2016]. Intuitively, can be thought as the way the adversary distributes over different transition models. The product structure then means that this adversarial distribution only depends on the current state of the agent without taking into account its whole trajectory. This defines a probability distribution over independently for each state.

We further assume that is non-diffuse. This implies that the uncertainty set is non-trivial with respect to in a sense that the distribution does not affect zero mass to all of the models.

3.2 SOFT-ROBUST OBJECTIVE

Throughout this paper, we make the following assumption:

Assumption 3.1.

Under any policy , the Markov chains resulting from any of the MDPs with transition laws are irreducible and aperiodic.

Define as the stationary distribution of the Markov chain that results from following policy under transition model .

Definition 3.1.

We call soft-robust objective or soft-robust average reward the function .

The distribution introduces a softer form of robustness in the objective function because it averages over the uncertainty set instead of considering the worst-case scenario. It also gives flexibility over the level of robustness one would like to keep. A robust strategy would then consist of putting more mass on pessimistic transition models. Likewise, a distribution that puts all of its mass on one target model would lead to an aggressive behavior and result in model misspecification.

The soft-robust differential reward is given by where

Similarly, we introduce the quantity

with We will interchangeably term it as soft-robust expected differential reward or soft-robust value function.

3.3 SOFT-ROBUST STATIONARY DISTRIBUTION

The above performance objective cannot as yet be written as an expectation of the reward over a stationary distribution because of the added measure on transition models. Define the average transition model as . It corresponds to the transition probability that results from distributing all transition models according to . In analogy to the transition probability that minimizes the reward for each given state and action in the robust transition function [Mankowitz et al., 2018], our average model rather selects the expected distribution over all the uncertainty set for each state and action. Under Assumption 3.1, we can show that the transition as defined is irreducible and aperiodic, which ensures the existence of a unique stationary law we will denote by .

Proposition 3.1 (Stationary distribution in the average transition model).

Under Assumption 3.1, the average transition matrix is irreducible and aperiodic. In particular, it admits a unique stationary distribution.

As in regular MDPs, the soft-robust average reward satisfies a Poisson equation, as it was first stated in the discounted reward case in Lemma 3.1 of Xu and Mannor [2012]. The following proposition reformulates this result for the average reward.

Proposition 3.2 (Soft-Robust Poisson equation).

This Poisson equation enables us to establish an equivalence between the expectation of the stationary distributions over the uncertainty set and the stationary distribution of the average transition model, naming with Indeed, we have the following:

Corollary 3.1.

Recall the stationary distribution for the average transition model . Then

The goal is to learn a policy that maximizes the soft-robust average reward . We use a policy-gradient method for that purpose.

4 SOFT-ROBUST POLICY-GRADIENT

In policy-gradient methods, we consider a class of parametrized stochastic policies with and estimate the gradient of the objective function with respect to policy parameters in order to update the policy in the direction of the estimated gradient of . The optimal set of parameters thus obtained is denoted by

When clear in the context, we will omit the subscript in for notation ease. We further make the following assumption, which is standard in policy-gradient litterature:

Assumption 4.1.

For any , the mapping is continuously differentiable with respect to .

Using the same method as in Sutton et al. [2000], we can derive the gradient of the soft-robust average reward thanks to the previous results.

Theorem 4.1 (Soft-Robust Policy-Gradient).

For any MDP satisfying previous assumptions, we have

In order to manage with large state spaces, we also introduce a linear approximation of we define as . Sutton et al. [2000] showed that if the features satisfy a compatibility condition and the approximation is locally optimal, then we can use it in place of and still point roughly in the direction of the true gradient.

In the case of soft-robust average reward, this defines a soft-robust gradient update that possesses the ability to incorporate function approximation, as stated in the following result. The main difference with that of Sutton et al. [2000] is that we combine the dynamics of the system with distributed transitions over the uncertainty set.

Theorem 4.2 (Soft-Robust Policy-Gradient with Function Approximation).

Let be a linear approximator of the soft-robust differential reward . If minimizes the mean squared error

and is compatible in a sense that , then

We can further improve our gradient estimate by reducing its variance. One direct method to do so is to subtract a baseline from the previous gradient update. It is easy to show that this will not affect the gradient derivation. In particular, Bhatnagar et al. [2009] proved that the value function minimizes the variance. It is therefore a proper baseline to choose. We can thus write the following:

| (1) |

where is the soft-robust advantage function defined by .

5 SOFT-ROBUST ACTOR-CRITIC ALGORITHM

In this section, we present our SR-AC algorithm which is defined as Algorithm 1. This novel approach incorporates a variation of distributional robustness into an online algorithm that effectively learns an optimal policy in a scalable manner. Under mild assumptions, the resulting two-timescale stochastic approximation algorithm converges to a locally optimal policy.

5.1 SR-AC ALGORITHM

An uncertainty set and a nominal model without uncertainty are provided as inputs. In practice, the nominal model and the uncertainty set can respectively be an estimate of the transition model resulting from data sampling and its corresponding confidence interval. A distribution over the uncertainty set is also provided. It corresponds to our prior information on the uncertainty set. The step-size sequences consist of small non-negative numbers properly chosen by the user (see Appendix for more details).

At each iteration, samples are generated using the nominal model and the current policy. These are utilized to update the soft-robust average reward (Line 5) and the critic (Line 7) based on an estimate of a soft-robust TD-error we detail further. In our setting, the soft-robust value function plays the role of the critic according to which the actor parameters are updated. We then exploit the critic to improve our policy by updating the policy parameters in the direction of a gradient estimate for the soft-robust objective (Line 8). This process is repeated until convergence.

5.2 CONVERGENCE ANALYSIS

We establish convergence of SR-AC to a local maximum of the soft-robust objective function by following an ODE approach [Kushner and Yin, 1997].

Consider and as unbiased estimates of and respectively. Calculating (Line 6 in Algorithm 1) requires an estimate of the soft-robust average-reward that can be obtained by averaging over samples given immediate reward and distribution (Line 5). In order to get an estimate of the soft-robust differential value , we use linear function approximation. Considering as a -dimensional feature extractor over the state space , we may then approximate as , where is a -dimensional parameter vector that we tune using linear TD. This results in the following soft-robust TD-error:

where corresponds to the current estimate of the soft-robust value function parameter.

As in regular MDPs, when doing linear TD learning, the function approximation of the value function introduces a bias in the gradient estimate [Bhatnagar et al., 2009]. Denoting it as , we have (see Appendix). This bias term then needs to be small enough in order to ensure convergence.

Convergence of Algorithm 1 can be established by applying Theorem 2 from Bhatnagar et al. [2009] which exploits Borkar’s work on two-timescale algorithms [1997]. The convergence result is presented as Theorem 5.1.

Theorem 5.1.

Under all the previous assumptions, given , there exists such that for a parameter vector obtained using the algorithm, if , then the SR-AC algorithm converges almost surely to an -neighborhood of a local maximum of .

6 NUMERICAL EXPERIMENTS

We demonstrate the performance of soft-robustness on various domains of finite as well as continuous state and action spaces. We used the existing structure of OpenAI Gym environments to run our experiments [Brockman et al., 2016].

6.1 DOMAINS

Single-step MDP We consider a simplified formulation of the startup vs teaching dilemma described in Section 1. The problem is modeled as a 7-state MDP in which one action corresponds to one strategy. An illustration of this construction is given in Figure 1. At the starting state , the agent chooses one of three actions. Action [corresponds to the startup adventure] may lead it to a very high reward in case of success but can be catastrophic in case of failure. Action [corresponds to the teaching carrier] leads it to low positive reward in case of success with no possibility of negative reward. Action [corresponds to an intermediate strategy] can lead to an intermediate positive reward with a slight risk of negative reward. Depending on the action it chose and if it succeeded or not, the agent is brought to one of the six right-hand states and receives the corresponding reward. It is brought back to at the end of each episode. We assume the probability of success to be the same for all three actions.

Cart-Pole In the Cart-Pole system, the agent’s goal consists of balancing a pole atop a cart in a vertical position. It is modeled as a continuous MDP in which each state consists of a 4-tuple which represents the cart position, the cart speed, the pole angle with respect to the vertical and its angular speed respectively. The agent can make two possible actions: apply a constant force either to the right or to the left of the pole. It gets a positive reward of 1 if the pole has not fallen down and if it stayed in the boundary sides of the screen. If it terminates, the agent receives a reward of 0. Since each episode lasts for 200 timesteps, the maximal reward an agent can get is 200 over one episode.

Pendulum In the inverted pendulum problem, a pendulum starts in a random position and the goal is to swing it up so that it stabilizes upright. The state domain consists in a 2-tuple which represents the pendulum angle with respect to the vertical and its angular velocity. At each timestep, the agent’s possible actions belong to a continuous interval which represents the force level being applied. Since there is no specified termination, we establish a maximal number of steps for each episode.

6.2 UNCERTAINTY SETS

For each experiment, we generate an uncertainty set before training. In the single-step MDP, we sample from different probabilities of success using a uniform distribution over . In Cart-Pole, we sample 5 different lengths from a normal distribution centered at the nominal length of the pole which we fix at . We proceed similarly for Pendulum by generating 10 different masses of pendulum around a nominal mass of . Each corresponding model thus generates a different transition function. We then sample the average model by fixing as a realization of a Dirichlet distribution. A soft-robust update for the actor is applied by taking the optimal action according to this average transition function.

6.3 LEARNING ALGORITHMS

We trained the agent on the nominal model in each experiment. The soft-robust agent was learned using SR-AC in the single-step MDP. In Cart-Pole, we run a soft-robust version of a DQN algorithm. The soft-robust agent in Pendulum was trained using a soft-robust DDPG.

Soft-Robust AC We analyze the performance of SR-AC by training a soft-robust agent on the single-step MDP. We run a regular AC algorithm to derive an aggressive policy and learn a robust behavior by using a robust formulation of AC which consists in replacing the TD-error with a robust TD-error, as implemented in Mankowitz et al. [2018]. The derived soft-robust agent is then compared with the resulting aggressive and robust strategies respectively.

Soft-Robust DQN Robustness has already been incorporated in DQN [Di-Castro Shashua and Mannor, 2017]. The Q-network addressed there performs an online estimation of the Q-function by minimizing at each timestep the following robust TD-error:

where is a discount factor.

In our experiments, we incorporate a soft-robust TD-error inside a DQN that trains a soft-robust agent according to the induced loss function. The soft-robust TD-error for DQN is given by:

We use the Cart-Pole domain to compare the resulting policy with the aggressive and robust strategies that were obtained from a regular and a robust DQN respectively.

Soft-Robust DDPG Define as the estimated deterministic policy at step . We incorporate robustness in DDPG by updating the critic network according to the following robust TD-error:

Similarly, we incorporate soft-robustness in DDPG by using the soft-robust TD-error:

We compare the resulting soft-robust DDPG with its regular and robust formulations in the Pendulum domain.

6.4 IMPLEMENTATION

For each experiment, we train the agent on the nominal model but incorporate soft-robustness during learning. A soft-robust policy is learned thanks to SR-AC in the single-step MDP. We use a linear function approximation with 5 features to estimate the value function. For Cart-Pole, we run a DQN using a neural network of 3 fully-connected hidden layers with 128 weights per layer and ReLu activations. In Pendulum, a DDPG algorithm learns a policy based on two target networks: the actor and the critic network. Both have 2 fully-connected hidden layers with 400 and 300 units respectively. We use a activation for the actor and a Relu activation for the critic output. We chose the ADAM optimizer to minimize all the induced loss functions. We used constant learning rates which worked well in practice. Each agent was trained over episodes for the single-step MDP and Cartpole and tested over episodes per parameter setting. For Pendulum, the agents were trained over episodes evaluated over episodes per parameter setting. Other hyper-parameter values can be found in the Appendix.

6.5 RESULTS

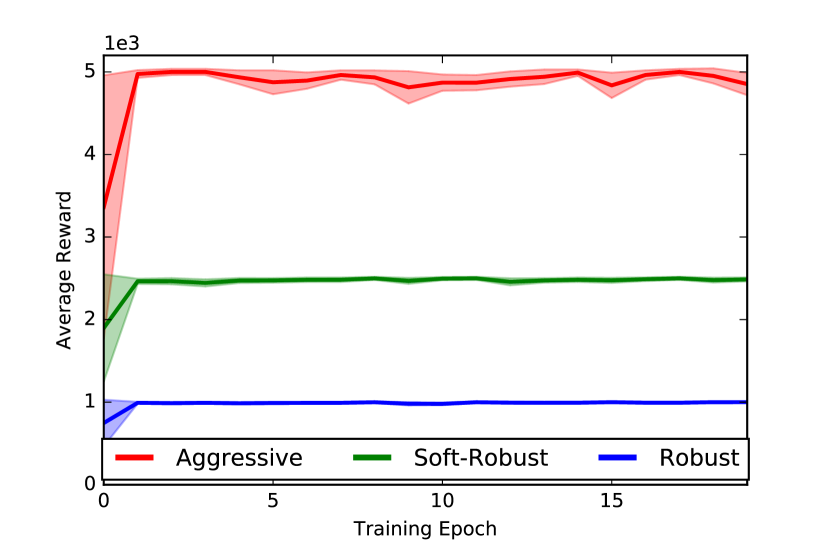

Single-step MDP Figure 2 shows the evolution of the performance for all three agents during training. It becomes more stable along training time, which confirms convergence of SR-AC. We see that the aggressive agent performs best due to the highest reward it can reach on the nominal model. The soft-robust agent gets rewards in between the aggressive and the robust agent which performs the worst due to its pessimistic learning method.

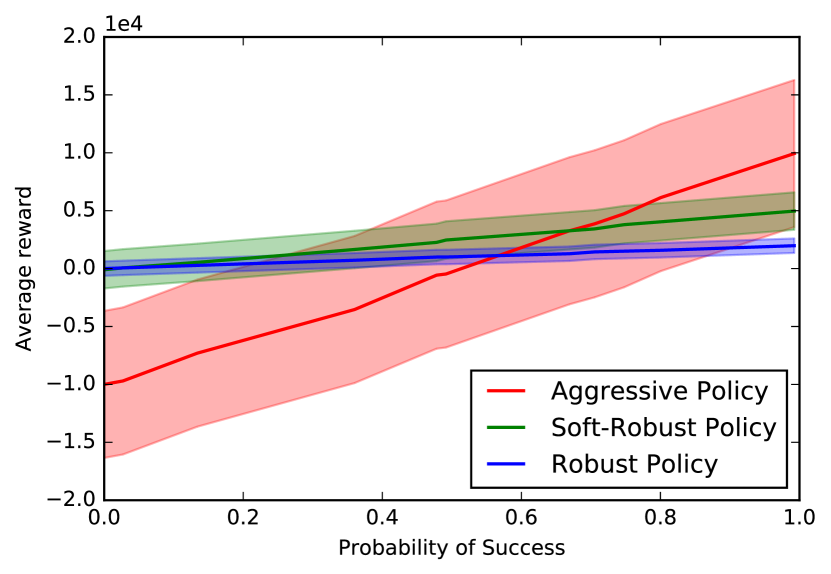

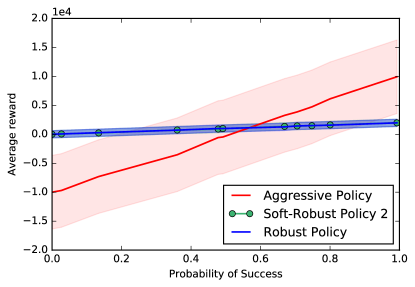

The evaluation of each strategy is represented in Figure 3. As the probability of success gets low, the performance of the aggressive agent drops down below the robust and the soft-robust agents, although it performs best when the probability of success gets close to 1. The robust agent stays stable independently of the parameters but underperforms soft-robust agent which presents the best balance between high reward and low risk. We noticed that depending on the weighting distribution initially set, soft-robustness tends to being more or less aggressive (see Appendix). Incorporating a distribution over the uncertainty set thus gives significant flexibility on the level of aggressiveness to be assigned to the soft-robust agent.

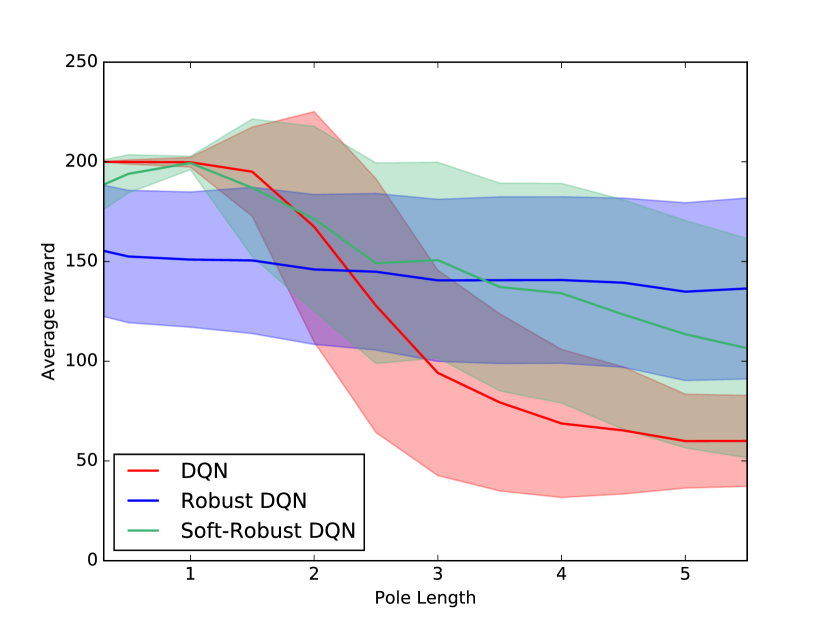

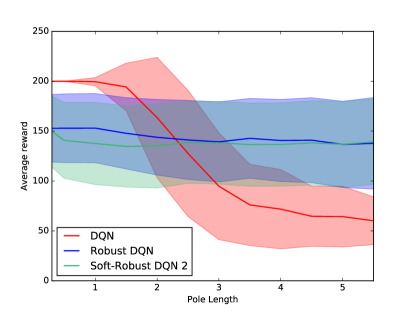

Cart-Pole In Figure 4, we show the performance of all three strategies over different values of pole length during testing. Similarly to our previous example, the non-robust agent performs well around the nominal model but its reward degrades on more extreme values of pole length. The robust agent keeps a stable reward under model uncertainty which is consistent with the results obtained in Di-Castro Shashua and Mannor [2017]; Mankowitz et al. [2018]. However, it is outperformed by the soft-robust agent around the nominal model. Furthermore, the soft-robust strategy shows an equilibrium between aggressiveness and robustness thus leading to better performance than the non-robust agent on larger pole lengths. We trained a soft-robust agent on other weighting distributions and noted that depending on its structure, soft-robustness interpolates between aggressive and robust behaviors (see Appendix).

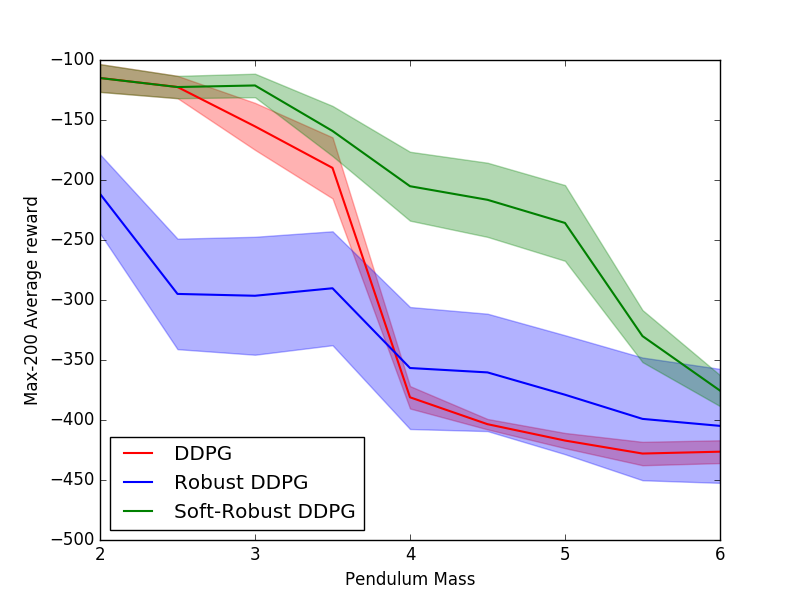

Pendulum Figure 5 shows the performance of all three agents when evaluating them on different masses. Since the performance among different episodes is highly variable, we considered the best -episodes average reward as a performance measure. As seen in the figure, the robust strategy solves the task in a sub-optimal fashion, but is less affected by model misspecification due to its conservative strategy. The aggressive non-robust agent is more sensitive to model misspecification compared to the other methods as can be seen by its sudden dip in performance, below even that of the robust agent. The soft-robust solution strikes a nice balance between being less sensitive to model misspecification than the aggressive agent, and producing better performance compared to the robust solution.

7 RELATED WORK

This paper is related to several domains in RL such as robust and distributionally robust MDPs, actor-critic methods and online learning via stochastic approximation algorithms. Our work solves the problem of conservativeness encountered in robust MDPs by incorporating a variational form of distributional robustness. The SR-AC algorithm combines scalability to large scale state-spaces and online estimation of the optimal policy in an actor-critic algorithm. Table 1 compares our proposed algorithm with previous approaches.

| Reference | Scalable | Actor- Critic | Softly- Robust |

|---|---|---|---|

| SR-AC (this paper) | ✓ | ✓ | ✓ |

| Mankowitz et al. [2018] | ✓ | ✗ | ✗ |

| Lim et al. [2016] | ✗ | ✗ | ✗ |

| Yu and Xu [2016] | ✗ | ✗ | ✓ |

| Mannor et al. [2016, 2012] | ✗ | ✗ | ✗ |

| Tamar et al. [2015] | ✓ | ✗ | ✗ |

| Xu and Mannor [2012] | ✗ | ✗ | ✓ |

| Bhatnagar et al. [2009] | ✓ | ✓ | ✗ |

Many solutions have been addressed to mitigate conservativeness of robust MDP. Mannor et al. [2012, 2016] relax the state-wise independence property of the uncertainty set and assume it to be coupled in a way such that the planning problem stays tracktable. Another approach tends to assume a priori information on the parameter set. These methods include distributionally robust MDPs [Xu and Mannor, 2012; Yu and Xu, 2016] in which the optimal strategy maximizes the expected reward under the most adversarial distribution over the uncertainty set. For finite and known MDPs, under some structural assumptions on the considered set of distributions, this max-min problem reduces to classical robust MDPs and can be solved efficiently by dynamic programming [Puterman, 2009].

However, besides becoming untracktable under large-sized MDPs, these methods use an offline learning approach which cannot adapt its level of protection against model uncertainty and may lead to overly conservative results. The work of Lim et al. [2016] solutions this issue and addresses an online algorithm that learns the transitions that are purely stochastic and those that are adversarial. Although it ensures less conservative results as well as low regret, this method sticks to the robust objective while strongly relying on the finite structure of the state-space. To alleviate the curse of dimensionality, we incorporate function approximation of the objective value and define it as a linear functional of features.

First introduced in Barto et al. [1983] and later addressed by Bhatnagar et al. [2009], actor-critic algorithms are online learning methods that aim at finding an optimal policy. We used the formulation of Bhatnagar et al. [2009] as a baseline for the algorithm we proposed. The key difference between their work and ours is that we incorporate soft-robustness. This relates in a sense to the Bayesian Actor-Critic setup in which the critic returns a complete posterior distribution of value functions using Bayes’ rule [Ghavamzadeh and Engel, 2007; Ghavamzadeh et al., 2015, 2016]. Our study keeps a frequentist approach, meaning that our algorithm updates return point estimates of the average value-function which prevents from tracktability issues besides enabling the distribution to be more flexible. Another major distinction is that the Bayesian approach incorporates a prior distribution on one model parameters whereas our method considers a prior on different transition models over an uncertainty set.

In Tamar et al. [2015]; Mankowitz et al. [2018], the authors incorporate robustness into policy-gradient methods. A sampling procedure is required for each critic estimate in Tamar et al. [2015], which differs from the strictly-speaking actor-critic. A robust version of actor-critic policy-gradient is introduced in Mankowitz et al. [2018] but its convergence guarantees are only shown for robust policy-gradient ascent. Both of these methods target the robust strategy whereas we seek a soft-robust policy that is less conservative while protecting itself against model uncertainty.

8 DISCUSSION

We have presented the SR-AC framework that is able to learn policies which keep a balance between aggressive and robust behaviors. SR-AC requires a stationary distribution under the average transition model and compatibility conditions for deriving a soft-robust policy-gradient. We have shown that this ensures convergence of SR-AC. This is the first work that has attempted to incorporate a soft form of robustness into an online actor-critic method. Our approach has been shown to be computationally scalable to large domains because of its low computational price. In our experiments, we have also shown that the soft-robust agent interpolates between aggressive and robust strategies without being overly conservative which leads it to outperform robust policies under model uncertainty even when the action space is continuous. Subsequent experiments should test the efficiency of soft-robustness on more complex domains.

The chosen weighting over the uncertainty set can be thought as the way the adversary distributes over different transition laws. In our current setting, this adversarial distribution stays constant without accounting for the rewards obtained by the agent. Future work should address the problem of learning the sequential game induced by an evolving adversarial distribution to derive an optimal soft-robust policy. Other extensions of our work may also consider non-linear objective functions such as higher order moments with respect to the adversarial distribution.

Acknowledgements

This work was partially funded by the Israel Science Foundation under contract 1380/16 and by the European Community’s Seventh Framework Programme (FP7/2007-2013) under grant agreement 306638 (SUPREL).

References

- Barto et al. [1983] Andrew G. Barto, Richard S. Sutton, and Charles W. Anderson. Neuronlike adaptive elements that can solve difficult learning control problems. IEEE Transactions on Systems, Man, and Cybernetics, SMC-13(5):834 – 846, 1983.

- Bhatnagar et al. [2009] Shalabh Bhatnagar, Richard Sutton, Mohammad Ghavamzadeh, and Mark Lee. Natural Actor-Critic Algorithms. Automatica, elsevier edition, 2009.

- Borkar [1997] Vivek S. Borkar. Stochastic Approximation with Two Timescales. Systems and Control Letters, 29:291–294, 1997.

- Brockman et al. [2016] Greg Brockman, Vicki Cheung, Ludwig Pettersson, Jonas Schneider, John Schulman, Jie Tang, and Wojciech Zaremba. OpenAI Gym. arXiv:1606.01540v1, 2016.

- Di-Castro Shashua and Mannor [2017] Shirli Di-Castro Shashua and Shie Mannor. Deep Robust Kalman Filter. arXiv preprint arXiv:1703.02310v1, 2017.

- Ghavamzadeh and Engel [2007] Mohammad Ghavamzadeh and Yaakov Engel. Bayesian Actor-Critic Algorithms. Proceedings of the 24th international conference on Machine learning, pages 297–304, 2007.

- Ghavamzadeh et al. [2015] Mohammad Ghavamzadeh, Shie Mannor, Joelle Pineau, and Aviv Tamar. Bayesian Reinforcement Learning: A Survey. Foundations and Trends in Machine Learning, 8(5-6):359–492, 2015.

- Ghavamzadeh et al. [2016] Mohammad Ghavamzadeh, Yaakov Engel, and Michal Valko. Bayesian Policy Gradient and Actor-Critic Algorithms. Journal of Machine Learning Research, 17(66):1–53, 2016.

- Grondman et al. [2012] Ivo Grondman, Lucian Busoniu, Gabriel A.D. Lopes, and Robert Babuska. A Survey of Actor-Critic Reinforcement Learning: Standard and Natural Policy Gradients. IEEE Transactions on Systems, Man, and Cybernetics—Part C: Applications and Reviews, 42(1291-1307), 2012.

- Iyengar [2005] Garud N. Iyengar. Robust Dynamic Programming. Mathematics of Operations Research, 30(2):257–280, 2005.

- Konda and Tsitsiklis [2000] Vijay R. Konda and John N. Tsitsiklis. Actor-Critic Algorithms. In Advances in Neural Information Processing Systems, volume 12, 2000.

- Kushner and Clark [1978] Harold J. Kushner and Dean S. Clark. Stochastic Approximation Methods for Constrained and Unconstrained Systems. Springer Verlag, 1978.

- Kushner and Yin [1997] Harold J. Kushner and G. George Yin. Stochastic Approximation Algorithms and Applications. Springer Verlag, New York, 1997.

- Lillicrap et al. [2016] Timothy P. Lillicrap, Jonathan J. Hunt, Alexander Pritzel, Nicolas Heess, Tom Erez, Yuval Tassa, David Silver, and Daan Wierstra. Continuous Control with Deep Reinforcement Learning. arXiv:1509.02971, US Patent App. 15/217,758, 2016.

- Lim et al. [2016] Shiau Hong Lim, Huan Xu, and Shie Mannor. Reinforcement Learning in Robust Markov Decision Processes. Mathematics of Operations Research, 41(4):1325–1353, 2016.

- Mankowitz et al. [2018] Daniel J Mankowitz, Timothy A Mann, Shie Mannor, Doina Precup, and Pierre-Luc Bacon. Learning Robust Options. In AAAI, 2018.

- Mannor et al. [2007] Shie Mannor, Duncan Simester, Peng Sun, and John N. Tsitsiklis. Bias and Variance Approximation in Value Function Estimates. Management Science, 53(2):308–322, 2007.

- Mannor et al. [2012] Shie Mannor, Ofir Mebel, and Huan Xu. Lightning Does Not Strike Twice: Robust MDPs with Coupled Uncertainty. In ICML, 2012.

- Mannor et al. [2016] Shie Mannor, Ofir Mebel, and Huan Xu. Robust MDPs with k-Rectangular Uncertainty. Mathematics of Operations Research, 41(4):1484–1509, 2016.

- Miller and Friesen [1982] Danny Miller and Peter H. Friesen. Innovation in conservative and entrepreneurial firms: Two models of strategic momentum. Strategic Management Journal, 1982.

- Mitchell and Smetters [2013] Olivia S. Mitchell and Kent Smetters. The Market for Retirement Financial Advice. Oxford University Press, first edition edition, 2013.

- Mnih et al. [2013] Volodymyr Mnih, Koray Kavukcuoglu, David Silver, Alex Graves, Ioannis Antonoglou, Daan Wierstra, and Martin Riedmiller. Playing Atari with Deep Reinforcement Learning: Technical Report. DeepMind Technologies, arXiv:1312.5602, 2013.

- Mnih et al. [2015] Volodymyr Mnih, Koray Kavukcuoglu, David Silver, Andrei A. Rusu, Joel Veness, Marc G. Bellemare, Alex Graves, Martin Riedmiller, Andreas K. Fidjeland, Georg Ostrovski, Stig Petersen, Charles Beattie, Amir Sadik, Ioannis Antonoglou, Helen King, Dharshan Kumaran, Daan Wierstra, Shane Legg, and Demis Hassabis. Human-level control through deep reinforcement learning. Nature, 518:529–533, 2015.

- Nilim and El Ghaoui [2005] Arnab Nilim and Laurent El Ghaoui. Robust control of Markov decision processes with uncertain transition matrices. Operations Research, 53(5):783–798, 2005.

- Puterman [2009] Martin L. Puterman. Markov decision processes: Discrete stochastic dynamic programming, volume 414. Wiley Series in Probability and Statistics, 2009.

- Roy et al. [2017] Aurko Roy, Huan Xu, and Sebastian Pokutta. Reinforcement learning under Model Mismatch. 31st Conference on Neural Information Processing Systems, 2017.

- Silver et al. [2014] David Silver, Guy Lever, Nicolas Heess, Thomas Degris, Daan Wierstra, and Martin Riedmiller. Deterministic Policy Gradient Algorithms. ICML, 2014.

- Sutton et al. [2000] Richard S. Sutton, David McAllester, Satinger Singh, and Yishay Mansour. Policy Gradient Methods for Reinforcement Learning with Function Approximation. In Advances in Neural Information Processing Systems, volume 12, pages 1057–1063, 2000.

- Tamar et al. [2014] Aviv Tamar, Shie Mannor, and Huan Xu. Scaling up robust mdps using function approximation. ICML, 32:1401–1415, 2014.

- Tamar et al. [2015] Aviv Tamar, Yinlam Chow, Mohammad Ghavamzadeh, and Shie Mannor. Policy gradient for coherent risk measures. In Advances in Neural Information Processing Systems, pages 1468–1476, 2015.

- Watkins and Dayan [1992] Christopher J. C. H. Watkins and Peter Dayan. Q-learning. Machine Learning, 8:279–292, 1992.

- Wiering and van Otterlo [2012] Marco Wiering and Martijn van Otterlo. Reinforcement Learning: State-of-the-Art. 12. Springer-Verlag Berlin Heidelberg, 2012.

- Xu and Mannor [2012] Huan Xu and Shie Mannor. Distributionally Robust Markov Decision Processes. Mathematics of Operations Research, 37(2):288–300, 2012.

- Yu and Xu [2016] Pengqian Yu and Huan Xu. Distributionally Robust Counterpart in Markov Decision Processes. IEEE Transactions on Automatic Control, 61(9):2538 – 2543, 2016.

Appendix: Soft-Robust Actor-Critic Policy-Gradient

Appendix A Proofs

A.1 Proposition 3.1

Proof.

Fix . For any policy , we denote by the probability of getting from state to state , which can be written as . Since is non-diffuse, there exists such that . Also, by Assumption 3.1, there exists an integer such that . We thus have

which shows that is irreducible. Using the same reasoning, we show and then use the fact that is aperiodic to conclude that is aperiodic too. ∎

A.2 Proposition 3.2

This recursive equation comes from the same reasoning as in Lemma 3.1 of Xu and Mannor [2012]. We apply it to the average reward criterion.

Proof.

For every , we can apply the Poisson equation to the corresponding model:

By integrating with respect to we obtain:

We then use the statewise independence assumption on to make the recursion explicit. We thus have

where results from the rectangularity assumption on . Since is an element of vector that only depends on the uncertainty set at state and depends on the uncertainty set at state , we can split the integrals. We slightly abuse notation here because a state can be visited multiple times. In fact, we implicitly introduce dummy states and treat multiple visits to a state as visiting different states. More explicitely, we write as where , being the distribution at state . This representation is termed as the stationary model in Xu and Mannor [2012]. ∎

A.3 Corollary 3.1

Proof.

According to Proposition 3.2 and summing up both sides of the equality with respect to the stationary distribution , we have

Since is stationary with respect to , we can then write

It remains to simplify both sides of the equality in order to get the result. ∎

A.4 Theorem 4.1

We use the same technique as in Sutton et al. [2000]; Mankowitz et al. [2018] in order to prove a soft-robust version of policy-gradient theorem.

Proof.

where occurs thanks to the soft-robust Poisson equation. Multiply both sides of the Equation by . Since is stationary with respect to , we have that . ∎

A.5 Theorem 4.2

Proof.

Recall the mean squared error:

with respect to the soft-robust state distribution . If we derive this distribution with respect to the parameters and analyze it when the process has converged to a local optimum as in Sutton et al. [2000], then we get:

Additionally, the compatibility condition yields:

Subtract this quantity from the soft-robust policy gradient (Theorem 4.1). We then have:

∎

A.6 Convergence Proof for SR-AC

We define as soft-robust TD-error at time the following random quantity:

where and are unbiased estimates that satisfy and respectively. We can easily show that this defines an unbiased estimate of the soft-robust advantage function [Bhatnagar et al., 2009]. Thus, using equation (1), an unbiased estimate of the gradient can be obtained by taking

Similarly, recall the soft-robust TD-error with linear function approximation at time :

where corresponds to the current estimate of the soft-robust value function parameter.

As in regular MDPs, when doing linear TD learning, the function approximation of the value function introduces a bias in the gradient estimate Bhatnagar et al. [2009].

Define the quantity

where is an estimate of the value function upon convergence of a TD recursion, that is . Also, define as the associated error upon convergence:

Similarly to Lemma 4 of Bhatnagar et al. [2009], the bias of the soft-robust gradient estimate is given by

that is . This error term then needs to be small enough in order to ensure convergence of the algorithm.

Let denote as the linear approximation to the soft-robust differential value function defined earlier, where is a matrix and each feature vector corresponds to the column in . We make the following assumption:

Assumption A.1.

The basis functions are linearly independent. In particular, has full rank. We also have for all value function parameters where is a vector of all ones.

The learning rates and (Lines 7 and 8 in Algorithm 1) are established such that slower than as . In addition, and . We also set the soft-robust average reward step-size for a positive constant . The soft-robust average reward, TD-error and critic will all operate on the faster timescale and therefore converge faster. Eventually, define a diagonal matrix where the steady-state distribution forms the diagonal of this matrix. We write the soft-robust transition probability matrix as:

where and designates the average transition model. By denoting the column vector of rewards where is a numbered representation of the state-space and using the following operator , we can express the soft-robust Poisson equation as:

The soft-robust average reward iterates (Line 5) and the critic iterates (Line 7) defined in Algorithm 1 converge almost surely, as stated in the following Lemma which is a straightforward application of Lemma 5 from Bhatnagar et al. [2009].

Lemma A.1.

For any given policy and as in the soft-robust average reward and critic updates, we have and almost surely, where

is the average reward under policy and is the unique solution to

Thanks to all the previous results, convergence of Algorithm 1 can be established by applying Theorem 2 from Bhatnagar et al. [2009] which exploits Borkar’s work on two-timescale algorithms [1997]. For simplicity, we assume that the iterates resulting from the actor update (Line 10 of Algorithm 1) in SR-AC remain bounded, although one could prove convergence without such an assumption by incorporating an operator that projects any policy parameter to a compact set, as described in Kushner and Clark [1978]. The resulting actor update would then be the projected value of the predefined iterate. The convergence result is presented as Theorem A.1.

Theorem A.1.

Under all the previous assumptions, given , there exists such that for a parameter vector obtained using the algorithm, if , then the SR-AC algorithm converges almost surely to an -neighborhood of a local maximum of .

Appendix B Experiments

B.1 One-step MDP

| Model Parameters | Value |

|---|---|

| Nominal probability of success | |

| Uncertainty set for probabilities of success | |

| Weighting Distribution 1 | |

| Weighting Distribution 2 | |

| Aggressive rewards | |

| Soft robust rewards | |

| Robust rewards |

| Hyperparameters | Value |

| Critic Learning rate | 5e-3 |

| Actor Learning rate | 5e-5 |

| Step size | |

| Number of linear features | |

| Number of episodes for training | |

| Number of episodes for testing |

B.2 Cart-Pole example

| Hyperparameters | Value |

| Discount factor | |

| Learning rate | 1e-4 |

| Mini-batch size | 256 |

| Final epsilon | 1e-5 |

| Target update interval | |

| Max number of episodes for training | |

| Number of episodes for testing |

We trained a soft-robust agent on a different weighting over the uncertainty set. Figure 7 shows the performance of the resulting strategy that presents a similar performance as the robust agent. This stronger form of robustness demonstrates the flexibility we have on the way we fix the weights, which leads to more or less aggressive behaviors.

B.3 Pendulum

| Hyperparameters | Value |

| Discount factor | |

| Actor learning rate | 1e-5 |

| Critic learning rate | 1e-3 |

| Mini-batch size | 64 |

| Soft target update | |

| Max number of episodes for training | |

| Number of episodes for testing |