Viscosity Solution for Optimal Stopping Problems of Feller Processes

Abstract.

We study an optimal stopping problem when the state process is governed by a general Feller process. In particular, we examine viscosity properties of the associated value function with no a priori assumption on the stochastic differential equation satisfied by the state process. Our approach relies on properties of the Feller semigroup. We present conditions on the state process under which the value function is the unique viscosity solution to an Hamilton-Jacobi-Bellman (HJB) equation associated with a particular operator. More specifically, assuming that the state process is a Feller process, we prove uniqueness of the viscosity solution which was conjectured in [26]. We then apply our results to study viscosity property of optimal stopping problems for some particular Feller processes, namely diffusion processes with piecewise coefficients and semi-Markov processes. Finally, we obtain explicit value functions for optimal stopping of straddle options, when the state process is a reflected Brownian motion, Brownian motion with jump at boundary and regime switching Feller diffusion, respectively (see Section 8).

Key words and phrases:

Optimal stopping; Feller process; Viscosity solutions; Hamilton-Jacobi-Bellman equation; Penalty method.2010 Mathematics Subject Classification:

Primary 60G40; 60J25; 47D07, Secondary 60J35.The authors would like to thank Bernt Øksendal for his comments and for suggesting problem in Section 8.1

1. Introduction

Optimal stopping problems for Markov processes have been extensively studied in the literature using various methods; see for example [27]. Such problems are very important due to their various applications in engineering, physics, mathematical finance and insurance. Assuming that the state process is given by a diffusion process (with non degenerate diffusion coefficient), the pioneering book [6, Chapter 3] introduces a variational inequality approach to solve optimal stopping problems. Under some weak regularity of the data the authors prove the regularity of the value function. Since then, there have been many studies on optimal stopping problems for Markov processes using the variational inequality approach, with the aim of relaxing the assumptions on the class of Markov processes and/or on the reward functional and also studying the properties of the value function. The variational inequality associated to the optimal stopping problem is often difficult to solve, unless one allows a notion of weak solution, called viscosity solution, to the Hamilton-Jacobi-Bellman (HJB) equation. In the case of a diffusion process, this approach is used for example in [2, 3, 16]; see also [22] for the jump-diffusion case.

In studying the viscosity properties of the value function, the traditional approach assumes that the generator associated with the state Markov process is given by parabolic or elliptic differential operators. Hence, one can use tools from partial differential equations to solve the problem. A natural question is what happens when the state process is given by a Markov process (for example a Feller process) for which the generator is not given by a partial differential operator but only derived from its semigroup. To the best of our knowledge, only [26] deals with existence of viscosity solution of an HJB equation when the generator is derived from a Feller semigroup.

One of the main motivation of this paper is to provide a general analytical approach that extends earlier results on properties of the value function to a more general class of processes. As such, we do not assume that the generator of the process is given by a partial differential operator. The other motivation is to establish a framework that enables to find the value function of an optimal stopping problem for a general class of processes (Feller processes) by analytically deriving the unique viscosity solution to the associated HJB equation (compare with [26]). Thus, our result completes the previous studies, in the sense that, we derive the existence and uniqueness of viscosity solutions to the HJB equation. The uniqueness was conjectured in [26]. To our knowledge, we do not know of any existing results on uniqueness of viscosity solution in this framework.

In this paper, we consider an infinite time horizon optimal stopping problems with fixed discount rate. We use the penalty method introduced in [30] and the general setting in [34]. Contrary to the traditional method which is based on calculations of the (integro) differential operators, this method is based on an efficient approximation of the value function by smooth functions. Although there are several extensions of the penalty method (see for example [23, 25, 26, 24, 33]), most of them focus on the study of the continuity of the value function except work [26] which investigates the existence of viscosity solution to the associated HJB equation. In this paper, under slightly different conditions, we show that the value function is the unique viscosity solution to the HJB equation associated with the optimal stopping problem.

We apply our result to study viscosity properties of the value functions for optimal stopping problems of Lévy processes, reflected Brownian motion, sticky Brownian motion, diffusion with piecewise coefficients and semi-Markov processes. We show that depending on the choice of the operator and its domain, the value function is the unique viscosity solution associated with the HJB equation. Let us mention that our viscosity analysis on diffusion with piecewise coefficients and semi-Markov processes are typically not investigated in the current literature on optimal stopping problems. In the former case, we will see later (confer Corollary 7.9 and Corollary 7.10) that the value function is a viscosity solution associated with a particular operator to an HJB equation. In the latter case, we first use perturbation theory (confer [9]) to transform the one-dimensional semi-Markov process to a two-dimensional Markov process. Then, we show that the value function of the problem is the unique viscosity solution to the associated HJB equation. Similar optimal stopping problem was studied in [8, 21] using iterative approach. We also use our results to explicitly derive the value function and the optimal stopping time in the case of a straddle option for the subsequent state processes: reflected Brownian motion (see Corollary 8.2); Brownian motion with jump at boundary (see Proposition 8.3) and regime switching Feller diffusion (see Corollary 8.7).

The rest of this paper is organized as follows. Section 2 introduces terminologies used throughout this paper and then formulate the optimal stopping problem. In Section 3, we study the value function as a viscosity solution to an HJB equation. Section 4 investigates uniqueness of the viscosity solution and its link to the value function under the assumption that the state space is compact. The proof relies on the comparison theorem (Theorem 4.1). Section 5 examines the extension of the uniqueness to the case of non compact state space. Section 6 studies the structure of the viscosity solution and its link to the martingale approach. In Section 7, we apply our results to study viscosity properties of value functions of optimal stopping problems for some processes satisfying our key assumptions. Section 8 is devoted to the derivation of explicit value function for optimal stopping of a straddle option.

2. Preliminaries and problem formulation

In this section, we first present some basic definitions and properties of Feller processes and Feller semigroups. Then, we formulate the optimal stopping problems and introduce our main assumptions. For more information on Feller processes, the reader may consult for example [18, Chapter 17] or [9, Chapter 1].

2.1. Preliminaries

Throughout this paper, we suppose that is a locally compact, separable metric space with metric . is the -algebra of the Borel sets of . If is not compact, we define as the one point (Alexandorff) compactification of , where is the point at infinity; otherwise, is an isolated point from . In both cases, is compact and metrizable and denotes the -algebra in generated by . We will use the following notations:

-

•

is the space of all bounded Borel measurable functions on ;

-

•

is the space of all continuous functions on ;

-

•

;

-

•

;

-

•

;

-

•

;

-

•

(respectively, ) denotes the space Borel-measurable upper (respectively, lower) semicontinuous function on .

Remark 2.1.

The above definitions imply that . Moreover, if is compact, these spaces coincide.

Let be the supremum norm that is for any ,

Equipped with the above norm, , and are Banach spaces. The relation is a partial order on the space of real valued functions on and we have if and only if for all . We now give a series of definitions.

Definition 2.2.

(Feller Semigroup) A collection of bounded linear operators is called Feller semigroups on , if it satisfies the following four properties:

-

•

, for all ; , where is the identity operator.

-

•

For each , if , , then, .

-

•

(Feller Property) for all .

-

•

(Strong Continuous Property) for .

Furthermore, a semigroup is conservative if for all .

Definition 2.3.

(Feller Process) A Feller process is a Markov process whose transition semigroup defined by

is a Feller semigroup.

Based on Definition 2.3, the transition semigroup of a Feller process is conservative.

Definition 2.4.

(Infinitesimal Generator) An infinitesimal generator of a Feller semigroup or a Feller process is a linear operator , with defined by

| (2.1) |

where the domain

Definition 2.5.

(Resolvent) A resolvent is defined by

The following resolvent identity equation is satisfied: for any and

| (2.2) |

Definition 2.6.

(Postive Maximum Principle) An operator satisfies positive maximum principle if for any with .

We now state the Hille-Yosida-Ray theorem for strongly continuous semigroup. This theorem gives the relationships among Feller semigroup, generator and resolvent (see [9, Theorem 1.30]) and will play a key role in proving the uniqueness of the viscosity solution.

Theorem 2.7.

Let be a linear operator on . is closable and its closure is the infinitesimal generator of a Feller semigroup if and only if:

-

(1)

is dense in .

-

(2)

The range of is dense in for all .

-

(3)

satisfies the positive maximum principle.

The following corollary is from the Hille-Yosida theorem (see for example [36, Proposition 4.9 and Theorem 4.10] ).

Corollary 2.8.

Let be the infinitesimal generator of some Feller semigroup. Then,

-

(1)

is closed.

-

(2)

For each , the operator is a bijection of onto and its inverse is the resolvent , that is for all and , we have

(2.3) -

(3)

For each , we have the inequality

(2.4)

Subsequently, we give the definition of the core, which enables to uniquely characterize a Feller semigroup.

Definition 2.9.

(Core) is called a core of an infinitesimal generator if it is a linear closable operator which satisfies is dense in and the closure of is , that is for any , there exists a sequence in such that

By (1) in Corollary 2.8, it follows that the infinitesimal generator of a Feller semigroup is its the core.

2.2. Problem Formulation

In this paper, we study an optimal stopping problem for a normal Markov process on the state space , where is a measurable space, is a right continuous and completed filtration, is a càdlàg stochastic process, is the shift operator and denotes the probability measure on for . Let be the family of all -stopping times. Let and be two real-valued Borel measurable functions on . Define the objective function by

| (2.5) |

where is a running benefit function, is a terminal reward function and is a constant discount factor.

We consider the following optimal stopping problem: find such that

| (2.6) |

for each . Our main goal is to study properties of the value function .

The following assumptions holds throughout this paper.

Assumption 2.10.

-

(1)

is a locally compact, separable metric space with metric .

-

(2)

is a Feller process with the state space , which has a Feller semigroup , whose generator is with a core .

-

(3)

and .

Assumption 2.10 does not make any a priori supposition on the partial differential equation satisfied by the generator of the Feller process. We first recall a result on the continuity of the value function given by (2.6). The proof of the continuity is based on the penalty method which consists in finding a sequence in that converges uniformly to the value function . More precisely, the penalty function is defined as the solution to the following equation

| (2.7) |

where . The next results which are similar to [30, Theorem I.2.1 and Theorem I.3.1] provide the continuity of the value function.

Theorem 2.11.

Proof.

See Appendix A. ∎

For more information on the continuity of the value function and its extensions; readers are referred to [23, 25, 26, 30, 33, 35]). The optimal stopping time for the above optimal stopping problem is obtained using [30, Theorem I.3.3] as follows.

Let denotes an operator with its domain. Recall that, we wish to study the link between the value function defined by (2.6) and the unique viscosity solution associated with to the corresponding Hamilton-Jacob-Bellman (HJB) equation

| (2.9) |

Thus, we first give the definition of viscosity solution:

Definition 2.13.

(Viscosity Solution) Given an operator with domain , a function (respectively, ) is a viscosity subsolution (respectively, supersolution) associated with to (2.9) if for all such that has a global minimum (respectively, maximum) at with ,

| (2.10) |

Furthermore, is a viscosity solution associated with to (2.9) if it is both a viscosity supersolution and a viscosity subsolution.

Next, let us introduce the notion of -generator:

Definition 2.14.

(-generator) Let be a Markov process on the state space . Set . An operator is called an a-supergenerator (respectively, a-subgenerator, a-generator) of , if for any , the process defined by

| (2.11) |

is a uniformly integrable supermartingale (respectively, submartingale, martingale) for all .

3. Existence of viscosity solution

In this section, we show that the value function defined by (2.6) can be described as a viscosity solution associated with the generator of the Feller process or its core .We prove that the value function defined by (2.6) is a viscosity supersolution (respectively, subsolution, solution) associated with an extended generator of the Feller process.

Theorem 3.1.

Proof.

The method used to show the existence is based on the probabilistic description of the extended generator of the Feller process . See Section 3.1 for a detailed proof. ∎

Remark 3.2.

As seeing later, enlarging the domain has the advantage that it allows to exclude functions which are viscosity solutions. Hence, we use the solution of the martingale problem to define the extended generator instead of the infinitesimal generator . The former enables us to provide more choices on the test function in . For example, can be chosen to be or could even include an unbounded function space; see for instance Section 7.1.1.

One can also show as in [10, Lemma 2.9] that if the process defined by

is a -martingale for any and , then is an -generator for when . Therefore, by Dynkin’s formula, the infinitesimal generator of the Feller process or its core is an -generator for all . In this case, Theorem 3.1 implies the following corollary:

Corollary 3.3.

The proofs of the above results is given by the following section.

3.1. Proof of Theorem 3.1

This section is devoted to the proof of Theorem 3.1. The proof is standard with a modification due to the presence of the absorbing state. The proof will be given for two classes of the initial state : the absorbing and the non-absorbing states.

We say that is an absorbing state if and only if for all almost surely under . Let be an -stopping time defined by

| (3.3) |

where and . The following lemma that can be found in [18, Lemma 17.22] provides information on the stopping time when the initial state is absorbing or not.

Lemma 3.4.

Let be a Feller process.

-

(1)

Assume is not absorbing. Then for all sufficiently small ,

-

(2)

is absorbing if and only if for all .

The subsequent lemmas are needed in the proof of the existence of the viscosity solution for absorbing initial state process. Their proofs are standard. However for the sake of completeness, we provide details.

Lemma 3.5.

Suppose Assumption 2.10 holds. Suppose in addition that the initial state is absorbing. Then the value function satisfies

| (3.4) |

Proof.

Since the initial state of the Feller process is absorbing, we have for all -a.s. For ,

If , then and the equality is attained on the set , that is, , otherwise, and the equality is attained on the set , that is, . ∎

Lemma 3.6.

Suppose Assumption 2.10 holds. For and ,

| (3.5) |

Suppose in addition that . Then there exists a constant such that for any , we have

| (3.6) |

Proof.

We now turn to the proof of Theorem 3.1.

Proof of Theorem 3.1.

(1) Viscosity Supersolution: Suppose is an -supergenerator of the Markov process . Suppose and such that and has a global maximum at . We wish to prove that

Since , it is sufficient to prove that

| (3.7) |

Case 1. Assume that is an absorbing initial state, that is for all -a.s. and define the process by

Since is absorbing, for all -a.s. Since is an -supergenerator, it follows that is a uniformly integrable supermartingale, and therefore . In addition, using Lemma 3.5, we have . The latter combines with the fact that yields (3.7).

Case 2. Assume that is not an absorbing initial value. It follows from Lemma 3.4 that for all small enough . Since and for any , (3.5) implies that

| (3.8) |

where the last inequality follows from the optional sampling theorem since is an -supergenerator. Since , dividing both sides of (3.1) by , we obtain

| (3.9) |

where . Since is bounded such that , (3.1) yields for all . Since and are in , converges pointwise to as . Hence, (3.7) is proved.

(2) Viscosity Subsolution: Assume that is an -subgenerator of the process . Choose , such that and has a global minimum at . If , we find a viscosity subsolution by setting . Since , we thus only consider the initial state satisfying . Hence, it is enough to show that

| (3.10) |

Case 1. Assume that is absorbing. Then by Lemma 3.5, . Since is an -subgenerator, applying similar arguments as in the proof of Case 1 for viscosity supersolution, we obtain . Therefore, (3.10) is satisfied.

Case 2. Assume that is not absorbing. Then by Lemma 3.4 and Lemma 3.6, there exists a constant such that for any , we have and (3.6) holds. Since and , we have

| (3.11) |

where the last inequality follows from the optional sampling theorem since is an -subgenerator. Since , dividing on both sides of (3.1), we get

| (3.12) |

for all . Then, since and belong to and is bounded, taking , we obtain the desired result. ∎

4. Uniqueness of viscosity solution for compact state space

In this section, we prove that the value function is the uniqueness of viscosity solution under the assumption that the state space is compact. Theorem 4.1 gives a comparison principle for viscosity supersolution and subsolution which is needed in the proof of the uniqueness of the viscosity solution associated with (respectively, ) (see Theorem 4.3).

Theorem 4.1.

(Comparison Principle). Suppose Assumption 2.10 holds. Suppose is compact and the constant function . Furthermore, suppose is a viscosity supersolution and is a viscosity subsolution associated with to

| (4.1) |

Then .

Proof.

See Section 4.1. ∎

Remark 4.2.

Since we suppose in the proof that all constant functions belong to or , it is natural to assume the compactness of . However, the latter is not a necessary condition to show the uniqueness of the viscosity solution and will be relaxed in the subsequent sections; see for example Section 5 and Proposition 5.1.

The following theorem constitutes the second main result of this section

Theorem 4.3.

Proof.

4.1. Proof of Theorem 4.1

We first recall that the state space is compact, (or ) contains constant functions and is the core of the infinitesimal generator . We prove Theorem 4.1 in three steps. In the first step, we define a notion of classical solution to (4.1) and show a partial comparison principle between a classical subsolution (respectively, supersolution) and a viscosity supersolution (respectively, subsolution). Second, we show that there exists a sequence of classical subsolutions (respectively, supersolutions) that converges from below (respectively, above) to the value function defined by (2.6). Finally, we use the results from steps 1 and 2 to prove Theorem 4.1.

Step 1

In this step, we first define the notion of classical subsolution (respectively, supersolution) to (4.1) and then prove a classical comparison theorem.

Definition 4.4.

A function is a classical subsolution (respectively, supersolution) associated with to (4.1), if and satisfies

| (4.2) |

Lemma 4.5.

Proof.

Let be a classical subsolution to (4.1). By contradiction, assume that is not a viscosity subsolution to (4.1). Then, there exists a function such that has a global minimum at with and

| (4.3) |

Since has a global nonnegative maximum at , the positive maximum principle yields , that is, . This together with and (4.3) gives

hence contradicting the assumption that is a classical subsolution to (4.1). Therefore is a viscosity subsolution to (4.1). The proof for the supersolution follows in the same way. ∎

We will also need the following partial comparison theorem.

Lemma 4.6 (Partial Comparison Principle).

Proof.

Let be a classical supersolution to (4.1) and be a viscosity subsolution to (4.1). Since , we have that . Since and is compact, there exists such that

By contradiction, assume that and define by

Since and has a global minimum at with , it follows that is a well defined test function for the viscosity subsolution . Moreover, by the positive maximum principle, we have . Hence,

Since is a classical supersolution, we have

Therefore,

This contradicts the fact that is a viscosity subsolution to (4.1). Thus , that is, on . Similar arguments can be used to show that , if is a viscosity supersolution to (4.1) and is a classical subsolution to (4.1). ∎

Corollary 4.7.

Step 2

We first show that there exists a sequence of classical supersolution (respectively, subsolution) that converges from above (respectively, below) to the value function .

Lemma 4.8.

Proof.

(1) Classical Supersolutions. It follows from Theorem 2.11 that the sequence defined by (2.7) converges uniformly to from below when . Thus, there exists a subsequence such that Define the sequence by

Then for

| (4.4) |

Combining (2.7) and (4.4) and using the fact that (positive maximum principle), we obtain

Since by (4.4), the above inequalities imply , that is, is a classical supersolution to (3.2). Furthermore, by (4.4), is a sequence of classical supersolutions to (3.2) that converges uniformly to from above as .

Corollary 4.9.

Proof.

We know from Lemma 4.8 that there exists a sequence of classical supersolutions associated with to (3.2) such that satisfies for . Let and choose an integer such that . Set

Then,

| (4.5) | ||||

| (4.6) |

Since is a classical supersolution to (3.2), we have

| (4.7) |

Therefore, is also a classical supersolution associated with to (3.2). Since is the core of , it follows that for , there exists a sequence in such that

| (4.8) |

In the following, we will construct a sequence of classical supersolution associated with to (4.1) that converges to from above. Since and , we have

| (4.9) |

Choose such that , then for , we have: on the one hand, using (4.1) and (4.1), is a classical supersolution to (4.1); on the other hand, using (4.5) and (4.8)

Define a new sequence by setting . Then is a classical supersolution associated with to (4.1) satisfying for any arbitrary . Therefore, converges uniformly to the value function from above as .

The case of subsolutions can be proved in a similar way. ∎

Step 3

Finally, we prove the comparison principle stated in Theorem 4.1.

Proof of Theorem 4.1.

Define the sets of classical supersolutions and subsolutions associated with to (4.1) as follows,

| (4.10) | ||||

| (4.11) |

Let be a viscosity supersolution associated with to (4.1). By Lemma 4.6, it is true that for any , and then . Similarly, let be a viscosity subsolution associated with to (4.1), then, for any and . By Corollary 4.9, there exists a sequence of classical supersolutoins (respectively, subsolutions ) associated with to (4.1) converging uniformly to the value function from above (respectively, below) as . Then for any , we have

Therefore, . The proof is completed. ∎

5. Uniqueness of Viscosity Solution for noncompact state space

Both Assumption 2.10 and compactness condition in Theorem 4.3 give sufficient conditions to prove the existence and uniqueness of the viscosity solution using probabilistic and analytical techniques. However, the compactness of is not always satisfied for some interesting Feller processes used in practice, for example Lévy processes on and one dimension diffusions on ; see Section 7.1.1 and Section 7.1.2. Thus, Theorem 4.3 is not immediately applicable for such processes. In addition, since a Feller semigroup is not necessarily conservative, its generator may not have a corresponding Feller process . In this section, we do not assume the existence of a Feller process (confer conditions (2) and (3) in Assumption 2.10) and neither do we assume the compactness of . We first extend the given Feller semigroup on to a conservative Feller semigroup on . From this we construct an associated Feller process with the aim of characterizing a viscosity solution associated with a core of any infinitesimal generator.

Recall that is the one point compactification of . We now extend the Feller semigroup on to a semigroup on defined by

| (5.3) |

where and . Here is the restriction of the function on . It follows from [18, Lemmas 17.13 and 17.14] that is a conservative Feller semigroup. Furthermore by [7, Theorem I.9.4], for a conservative Feller semigroup, there always exists a Feller process on the state space such that

| (5.4) |

This enables to link any Feller semigroup on with a Feller process whose state space is the one-point compactification of . Hence, Theorem 4.3 could also be useful in this case. We first show the relation between the infinitesimal generator of the Feller semigroup and that of its extension . We recall the definition of :

For any , has a continuous extension in . Assume that is not compact, then by one-point compactification technique, is a dense open subset of and converges to a unique limit at infinity. Thus, we can define the unique continuous extension of by

| (5.5) |

If is compact and is an isolated point, we simply define the continuous extension of by

| (5.6) |

5.1. Main Results

In this section, we present the main results. We first define the following operator defined by

| (5.7) | ||||

When is compact, it follows from (5.6) that . The proof of Theorem 5.3 relies on Theorem 4.3 and the following key result.

Proposition 5.1.

Suppose that is a core of the Feller semigroup , and (When is compact, we additionally assume that .) Then there exists a unique function with boundary condition such that is a viscosity solution associated with to

| (5.8) |

Moreover, the extension is the unique viscosity solution associated with (defined by (5.14)) to

| (5.9) |

where is the core of Feller semigoup on defined by (5.3).

Proof.

See Section 5.2.1. ∎

Remark 5.2.

The above proposition is used to show uniqueness of viscosity solution when the generator is given by a infinitesimal generator of a Feller semigroup rather than a Feller process. Let us emphasize that we need not this Feller semigroup to be conservative nor on a compact state space ; see for example Corollary 7.7.

The main results of this section are the following.

Theorem 5.3.

Proof.

See Section 5.2.2. ∎

Theorem 5.4.

Remark 5.5.

The operator in Theorem 5.3 always contains the constant function by construction. If one chooses an operator that does not contain this function, then the uniqueness might not hold as illustrated below.

Example 5.6 (Non uniqueness of viscosity solution).

Let be a standard Brownian motion on and choose as its core. By definition, the domain of this operator does not contain constant functions. Set and in the optimal stopping problem. Then, the value function defined by (2.6) is reduced to

| (5.11) |

for and the optimal stopping time strategy is . By Theorem 3.1, is a viscosity solution associated with to

Let and set . We claim that there is no such that has a global minimum equal at . Indeed assume that there exists such that

| (5.12) |

Since is of compact support, there exists such that . Choose then . This contradict the fact that has a global minimum equal at .

Since is chosen arbitrarily, it follows that for every strictly positive function , the function defined by is a viscosity subsolution.

On the other hand, let be the infinitesimal generator of the standard Brownian motion. Let and set . Let us show that is a classical supersolution associated with to

Indeed, we have

The equality follows by (2.3) and the inequality follows since . Hence by Lemma 4.5, is a viscosity supersolution associated with . Thus, it is also a viscosity supersolution associated with .

Therefore, for the function is a viscosity solution associated with . Since is arbitrarily chosen, the uniqueness is not satisfied. ∎

5.2. Proof of the Main results

5.2.1. Proof of Proposition 5.1

Before proving the main results, we need some preliminary results. We start with the following lemma that gives the relation between the infinitesimal generator of the Feller semigroup and that of its extension .

Lemma 5.8.

Let be a Feller semigroup on , whose infinitesimal generator is with a core . Given the Feller semigroup defined by (5.3), its infinitesimal generator satisfies

with

| (5.13) |

Furthermore, suppose is the restriction of on with

| (5.14) | ||||

Then is also the core of the Feller semigroup .

Proof.

See Appendix B. ∎

Since defined by (5.3) is a conservative Feller semigroup, we know [7, Theorem I.9.4] that there exists a corresponding Feller process whose transition semigroup is with the compact state space . is also a standard Markov process. Define the value function of by

| (5.15) |

One can check that all the conditions in Assumption 2.10 are fulfilled. In fact, is compact; using Lemma 5.8, defined by (5.14) is the core of the Feller process and implies . Then, by Theorem 4.3, the above value function is the unique viscosity solution associated with to

| (5.16) |

Lemma 5.9.

Suppose the assumptions in Proposition 5.1 hold. Assume that (respectively, ) is a viscosity subsolution (respectively, supersolution) associated with to (5.10). Define the extension on by

| (5.17) |

If (respectively, ), then is a viscosity subsolution (respectively, supersolution) associated with to (5.16).

Proof.

Let be a viscosity subsolution associated with to (5.8). We want to show that is also a viscosity subsolution associated with to (5.16). Let such that has a global minimum at in with , we want to show that

| (5.18) |

We distinguish two cases:

(a) Assume that (an absorbing point). Then, for all . In addition, since , (5.18) is satisfied.

(b) Assume that . Define by . Since , it follows from (5.14) that . In addition, we claim that .

To see this, we first assume that is not compact. Then and thus (since . Hence . Next, we assume that is compact. In this case, means and , that is, . Using the fact that , we obtain . Therefore, since by the compactness of and , it follows from (5.7) that . The claim is thus proved.

Next, recall that has a global minimum at in with . Hence, using and , it follows that has a global minimum at in with . Combining this with the fact that , and since is viscosity subsolution associated with to (5.8), we have

| (5.19) |

Since and , in order to prove that (5.18) holds when , it is enough to show that

| (5.20) |

It follows from (5.14) (respectively, (5.7)) that (respectively, ) and thus . That is, (5.20) becomes

| (5.21) |

Two cases are distinguished.

(i) Assume that is not compact. By the uniqueness of the extension, we have and .

(ii) Assume that is compact. By the definition of (see(5.6)), we have for any and . In addition, since has a global minimum at in and , we have for any and thus , since is compact. This indicates that has a positive maximum equal at in . Since is the core of (seeLemma 5.8), it follows from Theorem 2.7 that, satisfies the positive maximum principle and thus .

The viscosity supersolution can be proved in a similar way. ∎

Proof of Proposition 5.1.

(1) We will prove that is a viscosity solution in associated with to (5.8). We first prove that is a viscosity subsolution associated with to (5.8). Let and such that has a global minimum at with . There are two cases:

(i) Suppose that is compact. Then .

(ii) Suppose that in not compact. Since is a dense open subset of , we have .

It follows that has a global minimum at in with . Moreover, since , then by the definition (5.7) of , we have . Hence, . Therefore, by the definition (5.14) of . Since the value function defined by (5.15) is a viscosity subsolution associated with to (5.16), we have

Furthermore, since , using (5.14), we have , and using (5.7), we have . Hence, . Therefore,

We can also prove in a similar way that is a viscosity supersolution. The existence is then proved, that is, is a viscosity solution associated with to (5.8).

(2) Next, we show that is the unique viscosity solution associated with . The idea here is to prove that if is a viscosity solution associated with to (5.8), then is a viscosity solution associated with to (5.16). Hence, the result will follow since the viscosity solution associated with to (5.16) is unique. Using Lemma 5.9, if is a viscosity solution associated with to (5.8), its extension is the unique viscosity solution associated with to (5.16) which is the value function defined by (5.15). This completes the proof of the uniqueness and the proposition. ∎

5.2.2. Proof of Theorem 5.3

For compact, since , the existence and uniqueness follow Theorem 4.3. Thus, we only need to consider the case not compact.

Existence: Using Theorem 3.1, the viscosity solution associated with to (5.10) is the value function provided that is an -generator.

Let us show that is an -generator. By Dynkin’s formula and the argument preceding Corollary 3.3, we have is an -generator. Let us consider the restriction of to the space of constant functions. Since is not compact, using (5.7), we have . Hence given by (2.11) (with ) is an uniformly integrable martingale for and thus is an -generator.

Uniqueness: For the uniqueness, let be an increasing sequence in converging pointwisely to the constant function . By Dini’s theorem, converges to locally uniformly. Let . Define and . Then and are in and increasing.

Let be a viscosity solution associated with to (5.10), which satisfies , and define

By the existence proof, is a viscosity solution to

| (5.22) |

Since and in , is a viscosity supersolution to (5.22). Therefore, by Lemma 5.9, for all .

Similarly, let and and is

It is the viscosity solution to

| (5.23) |

Then, similarly, since and is the viscosity subsolution to (5.23), by Lemma 5.9, then .

Therefore, since for all , to prove the uniqueness, it is enough to show that . We have the following inequalities,

By [32, Theorem 3.2], we know that converges to locally uniformly. Then, we only need to prove that , with converges to locally uniformly. As shown in [23, Proposition 2.1], for any compact set , and , there exists a compact set such that

| (5.24) |

Therefore for any -stopping time , for all , we have

Since is compact and converges to locally uniformly, converges to as . Since , and are all arbitrarily chosen, converges to locally uniformly. Therefore, converges to locally uniformly. Similarly, we have converges to locally uniformly. This completes the proof of the uniqueness.

6. Structure of the optimal stopping value functions

In this section, we related the viscosity solution to some existing results, using martingale approach. First, we introduce some preliminary lemmas.

Lemma 6.1.

Given (respectively, ), define the process by

| (6.1) |

Suppose there exists an open subset such that is a uniformly integrable supermartingale (respectively, submartingale) for all . Then, the following claims hold.

-

(1)

For all such that has a global maximum (respectively, minimum) at with ,

(6.2) -

(2)

Additionally, suppose there exists a subset such that satisfies for some . Then for all such that has a maximum (respectively, minimum) in at with , we have

(6.3)

Proof.

The proof is similar as the proof of Theorem 3.1. Here, we only prove the statement (2) since the statement (1) follows when in the statement (2). Let such that has a maximum (respectively, minimum) in at with . Let the process be defined by

| (6.4) |

By Dynkin formula, since , is a uniformly integrable martingale. We first assume is a point not absorbing. Let and defined by (3.3). Since is a uniformly integrable supermartingale, we have

where the last inequality follows from the optional stopping theorem. Thus (6.3) is proved in an analogous way as (3.1) in Theorem 3.1. The case the non-absorbing point can be proved the same way as in Theorem 3.1. ∎

Corollary 6.2.

Proof.

Corollary 6.3.

Let be bounded from above. Suppose there exists an open subset such that its corresponding process defined by (6.1) is a submartingale.

-

(1)

If for all , then for all , where is the value function defined by (2.6).

-

(2)

Additionally, suppose there exists a subset such that satisfies for all . If for all , then for all .

Proof.

As in Lemma 6.1, we give the proof of (2) and (1) by setting . First define the function by

Since is an open subset with , is a continuous function and for , we have .

Similarly with Corollary 6.2, by Lemma 6.1, is a viscosity subsolution to

Since for all , then is a viscosity subsolution to

By the comparison principle (see Theorem 5.4), we have and then for all .

∎

Combing Corollary 6.2 and Corollary 6.3, the following result suggests that the value function characterized in the proof of [1, Theorem 3.1] coincides with the viscosity solution to (5.8).

Theorem 6.4.

Let and be an open subset. Suppose there exists a subset such that and satisfies for all . Additionally, suppose the following hold.

-

(1)

is a uniformly integrable martingale,

-

(2)

is a supermartingale,

-

(3)

and for ,

Then, for all .

The above theorem gives a classical method to find the optimal stopping value function using the martingale characterization. It is traditionally used for one-dimensional process to find explicit solution for optimal stopping for diffusion. We should mention that the martingale approach usually does not require the continuity and boundedness of the reward functions and . (See for example [4].)

7. Applications

7.1. Viscosity properties of value functions for optimal stopping problems

In this section, we apply the results to study viscosity properties for optimal stopping problems for some processes satisfying Assumption 2.10 and whose core fulfils the conditions of our main theorems. Let us mention that many traditional processes studied in the literature satisfy those assumptions. We revisit the optimal stopping using viscosity approach developed in the paper. To our knowledge, optimal stopping problems for Brownian motion jumping at boundary and semi-Markov process have not been studied in the literature using viscosity approach. Recall that the objective function is given by

| (7.1) |

Let be a space to be determined in each example. In this section, we always assume that

We will first use Theorem 3.1 to show that the value function given by (7.1) is a viscosity solution. Let us start with Lévy processes on the state space .

7.1.1. Lévy Processes

Here, we assume that is a Lévy process on . It is known (see for example [18, Theorem 17.10]) that is a Feller process. Its core is given by

| (7.2) |

for and , where is a vector, is a symmetric positive semi-definite matrix, is a positive Radon measure satisfying and denotes the space of all infinitely differentiable functions and itself and all its derivatives belong to . We have the following result from Theorem 5.3.

Proposition 7.1.

Assume that is a Lévy process whose core is described above. Then the value function given by (7.1) is the unique viscosity solution associated with to

| (7.3) |

where .

Remark 7.2.

Similar optimal stopping problem was studied in [1, 20]. In particular, the authors look at perpetual put options for one dimensional Lévy process with and , where and . More precisely, the value function has the following form

| (7.4) |

Let us note that [1] used a martingale approach similar to Theorem 6.4 to prove that the value function is solution to a martingale problem. Alternatively, we can use Proposition 7.1 to show that the value function is the unique viscosity solution to the associated HJB equation.

Let us now assume that the process is a one dimensional standard Brownian motion, that is, a Feller process with state space and core given by

| (7.5) | ||||

Theorem 3.1 gives us the freedom to choose larger domains than , for example,

| (7.6) | ||||

| (7.7) | ||||

| (7.8) |

Using Theorem 3.1 and Theorem 5.3, we have the following result:

Corollary 7.3.

Assume that is a one dimensional standard Brownian motion. Then the value function given by (7.1) is the unique viscosity solution associated with (respectively, , ) to

| (7.9) |

Proof.

Let us first observe that corresponds to and corresponds to in Theorem 5.3. Let (respectively, ). Using Itô’s formula, the process given by

is a -uniformly integrable martingale for and . Using Definition 2.14 the operator (respectively, , ) is an -generator. Hence by Theorem 3.1, the value function defined by (7.1) is a viscosity solution associated with (respectively, , ). The uniqueness follows from Theorem 5.3 since (respectively, , ) corresponds to . ∎

In the next section we consider examples of one dimensional diffusion processes on the positive half line that behave like a standard Brownian motion with different boundary behaviours at boundary .

7.1.2. Diffusion on

Let be a diffusion process on . Then the generator of is given by

| (7.10) | ||||

The operator does not satisfy the positive maximum principle at unless we add some appropriate conditions at boundary . Let us consider the following processes with appropriate domain

-

(1)

Reflected Brownian motion: ;

-

(2)

Sticking Brownian motion: ;

-

(3)

Sticky reflecting Brownian motion: , where .

-

(4)

Brownian motion with jump at the boundary: , where and is a probability measure.

We have the following result from Theorem 3.1 and Theorem 5.3:

Proposition 7.4.

Assume that is a reflected Brownian motion (respectively, sticking Brownian motion, sticky reflecting Brownian motion). Then the value function given by (7.1) is a unique viscosity solution in associated with (respectively, , , .

Proof.

It follows from the fact that the above processes are Feller processes. ∎

Now, consider the reflected Brownian motion and define

Corollary 7.5.

Assume that is a reflected Brownian motion. Then the value function given by (2.6) is the unique function in which is both a viscosity supersolution associated with and a viscosity subsolution associated with .

Proof.

Since (respectively, ), the process given by

is a uniformly integrable supermartingale (respectively, submartingale). Hence, Theorem 3.1 suggests that the value function defined by (2.6) is a viscosity supersolution (respectively, subsolution) associated with (respectively, ). As for the uniqueness, we only need to show that it holds for the operator , where

This follows from Theorem 5.3. Therefore, it leads to the desired result, since can be seen as the restriction of on . ∎

Remark 7.6.

In the above example, we consider the simplest cases of standard Brownian motion with the state space . More generally, Feller [13, 14, 15] constructs Markov processes up to a specific regular boundary point with the boundary condition given by

for with . However, we have not considered the cases in which , for example, the “Dirichlet condition” , or the “Robin condition” . The reason is that when the above Markov processes may be killed upon reaching and thus, does not coincide with Definition 2.3 of Feller process. Nevertheless, our method is still applicable as demonstrated in the following example.

Let be an operator defined by

| (7.11) | ||||

Using Proposition 5.1, we have the corollary below:

Corollary 7.7.

Suppose and . Then there exists a unique viscosity solution associated with to

where .

Proof.

Remark 7.8.

In the next section, we wish to establish viscosity properties of the value function of the optimal stopping problem (7.1), when is a diffusion with piecewise coefficients. Such problem with discontinuous function and was studied in [5, 31] using a “modified” free boundary approach. The definition of viscosity solution given in [5, Definiton 4.2 and 4.3] does not ensure that the value function is the unique solution. In this paper, assuming that and using different definition of viscosity solution, we show the viscosity property of the value function.

7.1.3. Diffusion with piecewise coefficients

We start by constructing a diffusion process with piecewise coefficients. Let , and be three bounded real valued measurable functions. Suppose and , where is a set in without cluster points and contains all the discontinuous points of the functions , and . In addition, suppose there exists such that . We know from [19, Propositions 2.1, 2.2 and 2.6] that there exists a Feller process with continuous paths whose infinitesimal generator is given by

As a consequence of Theorem 5.3, we have the following result.

Corollary 7.9.

In particular, [29, Chapter VII, Exercise 1.23] provides an example of Skew Brownian motion with parameter . Heuristically speaking, it is constructed by a Brownian motion reflected at zero which enters the positive half line with probability (respectively, the negative half with probability ) when it reaches zero. Its core is given by

| (7.13) | ||||

Again, Theorem 5.3 yields the following result

Corollary 7.10.

Remark 7.11.

Observe that in the above example does not contain any smooth function unless its derivative is . Therefore, showing that a function has the viscosity property at means test functions as described in Definition 2.13 are continuous but are not smooth at . This leads to additional technical difficulty in the proof of the uniqueness when using the traditional method. This is due to the fact that this method is based on smoothness of test function and properties of elliptic or parabolic differential equations.

7.2. Perturbation

Perturbation is a powerful method to transform a known Feller process to a new Feller process. We first introduce the following lemma which enables to construct the Feller semigroup using perturbation.

Lemma 7.12.

[9] Let be the infinitesimal generator of some Feller semigroup on . Assume that and is bounded, that is, there exists such that . Additionally suppose satisfies the positive maximum principle. Then, is the infinitesimal generator of some Feller semigroup on .

Using this method, we provide constructions of Feller processes via perturbation. The first example is the Feller process with large jumps.

7.2.1. Compound Poisson Operator

Let be a Feller process with the state space state space and core given by . Define a bounded operator by

| (7.15) |

where is a probability distribution function defined on and is the intensity parameter. Then by Lemma 7.12, is the infinitesimal generator of some Feller process . For example, let be a standard Brownian motion and be the distribution function of an exponential random variable with parameter . Let be a compound Poisson process with the intensity and the jump height following an exponential distribution with parameter . Then, in this case, one can choose as

| (7.16) |

with core , where is the natural filtration of . Thus is still a Feller process. Hence viscosity solution approach can be used to characterise the value function of the optimal stopping problem of .

7.2.2. Semi-Markov Process

Let be a sequence of independent and identical (i.i.d.) random variables with cumulative density distribution function . can be seen as the interarrival time of some random event. Additionally, let be a sequence of i.i.d random variables defined on with distribution function . Let for and the renewal process . Let be

| (7.17) |

where is the initial state. For example when the interarrival time is the exponential distribution, is a compound Poisson distribution which is a Markov process. However, if the interarrival time does not follow the exponential distribution, is not a Markov process but a semi-Markov process. We want to analyze the optimal stopping problem of

| (7.18) |

where and .

Remark 7.13.

Optimal stopping problems of semi-Markov process has been studied in [8, 21]. The work [8] provides several applications of semi-Markov processes in real life, for example, job search and shock model ( see [8, Section 1].) In this section, we want to solve optimal stopping problems using viscosity approach and not the iterative approach as in [8, 21].

Assume that is an absolutely continuous function and is its continuous density function on . Define for . In addition, assume that . Then, has a continuous extension on . Examples are:

-

(1)

Mixture exponential distribution: , where , , and is some positive integral. Its density function is given by . Thus, .

-

(2)

Generalized beta prime distribution: Here, and . Thus, for .

Let be the time from the last jumps of (for example if is the time of the last jump at time , ). Then, the two dimensional process is a Markov process (see for example [17, Lemma 2, p290]). Its infinitesimal generator is defined by

| (7.19) | ||||

Proposition 7.14.

Assume that is a semi-Markov process defined by (7.17).

-

(1)

There exists a unique viscosity solution associated with defined by (7.19) to

(7.20) where and for all and .

-

(2)

The value function can be characterized by .

-

(3)

Let be the time from the last jump. Let . Then the optimal stopping time is

(7.21)

Proof.

First, we prove that (7.19) is an infinitesimal generator of some Feller semigroup. Since is the generator of some Feller semigroup, by Lemma 7.12, we only need to prove: (i) is defines from to , (ii) is bounded and (iii) satisfies the positive maximum principle, where

| (7.22) | ||||

Let . We have

-

(i)

, where for . Then implies that follows since and .

-

(ii)

and is bounded. Then is bounded.

-

(iii)

If is the global maximum point and , .

Therefore, is a Feller generator. Furthermore, define

| (7.23) |

Since the semi-Markov process and the Markov process have the same filtration and probability measure, we have for . Since is the generator of the Feller process , we can use Theorem 5.3 to show (1) and (2) and Theorem 2.12 to show (3). ∎

Remark 7.15.

In this example, we have not derived an explicit value function for the optimal stopping problem. However, in [12], we suggest an iterative scheme to find the value function.

8. Explicit solutions

In this section, we apply the results obtained in Section 7 to explicitly derive the solution to the following optimal stopping problem: Find such that

| (8.1) |

where with and is a process to be described. can be understood as the straddle option which is the difference of two options.

8.1. Reflected Brownian Motion

In this section, let with and suppose is a reflected Brownian motion reflected at with state space with core

| (8.2) | ||||

Our aim is to find the explicit optimal stopping time of problem (8.1) based on Theorem 5.3. The following corollary is a direct consequence.

Proposition 8.1.

Proof.

This result directly follows from Theorem 5.3 by setting and for . ∎

In order to find , we first need to compute explicitly as shown below.

Corollary 8.2.

Let be a reflected Brownian motion reflected at . Let define by

| (8.4) |

where is the discount rate. Then, the value function , where

| (8.5) |

and

| (8.6) |

Additionally, the optimal stopping time is

Proof.

Let us show that defined by (8.5) is a viscosity solution. By definition of in (8.4), for . Using (8.5), we get . In what follows, we show the viscosity property for different values of .

Case 1. Assume that . It is clear from (8.5) that is twice differentiable at and we have

| (8.7) |

Since for , we have

Let such that has a maximum (respectively, minimum) at with . We first show that . Assume that . Then is an interior point. Since is twice differentiable at and has a maximum (respectively, minimum) at , we have . Assume now that . Since , we have . Using , we have . Furthermore, since has a maximum (respectively, minimum) at , it follows that . Therefore,

Hence, satisfies viscosity property at .

Case 2. Assume that Since , the viscosity subsolution property is satisfied. Then, we only need to show the viscosity supersolution property.

Let such that has a maximum at with .

Define . By (8.4) and (8.5), we have for all and .

It implies that also has a maximum at with . Hence, since is twice differentiable and is interior point, . Therefore,

Then, the viscosity supersolution property is satisfied.

Case 3 Assume that . Since , we only need to show the viscosity supersolution. It can be proved similarly with Case 1. The result follows by uniqueness of the viscosity solution (Theorem 5.3.)

Moreover, the optimal stopping time can be obtained using Theorem 2.12.

∎

Next, we consider a standard Brownian motions with jumps at the boundary .

8.2. Brownian motion with jump at boundary

Let be a standard Brownian motion which has nonlocal behavior at and state space . Then is a Feller process whose core is defined by (see for example [36])

| (8.8) | ||||

where is a positive constant and is a probability distribution function on . The process stays at zero for a positive length of exponential waiting time with parameter and then jump back to a random point in with a probability defined by the distribution function . Let be the value function of the optimal stopping problem (8.1). Then, we have the following result:

Proposition 8.3.

Suppose there exists a solution such that for , where and satisfy

-

(1)

,

-

(2)

There exists such that ,

-

(3)

is a viscosity supersolution to

-

(4)

.

Then,

| (8.9) |

Proof.

Using Theorem 5.3, we only need to show that is a viscosity solution associated to . We only prove the viscosity supersolution property and subsolution property can be shown similarily. Since , we simply need to show that for any such that and , we have simply

| (8.10) |

Case 1. Suppose . (8.10) follows by the condition (3).

Case 2. Suppose . Since has a global maximum at by condition (1) and (2) and and are twice differentiable at , we have .

Case 3. Suppose . Since for all and , (8.10) holds.

Case 4. Suppose . By the definition of , we have

where the first inequality follows from and and the last equality from condition (4). Hence, (8.10) holds when . Therefore, we conclude that is a viscosity supersolution. The case of the viscosity subsolutionccan be shown analogously. ∎

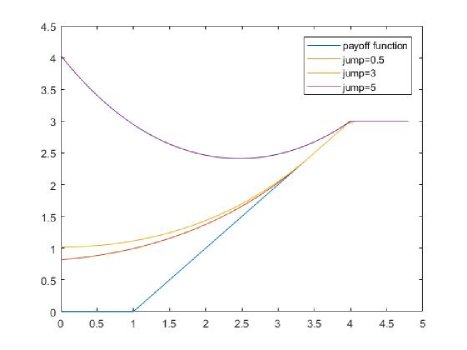

The following figure shows the evolution of the value function with fixed jump size at boundary.

In Figure 1, we assume that the jump size is fixed at (respectively and ) and the parameter . The graph shows that the value function and exercise point increases with the jump size. We can also mention that the construction of the value function by the viscosity solution can generally be used under weaker condition as compared to the smooth fit principle. Since is not differential, the smooth fit principle may failed for example if the jump size is equal to .

8.3. Regime switching boundary

In order to construct a regime switching boundary Feller diffusion, we first construct a regime switching Feller process. Let be a finite discrete space, where is a positive integer. Let be the infinitesimal generators of some Feller semigroups on . Then, define the operator as follows:

| (8.11) | ||||

where . By Hille-Yosida theorem, the above generator is the infinitesimal generator of some Feller semigroup. In addition, define the bounded operator

| (8.12) |

where and . Since satisfies the positive maximum principle and , the operator is the infinitesimal generator of some Feller semigroup.

Next, we construct a regime switching boundary Feller diffusion, that is, the boundary condition is affected by a Markov chain with the state space . The intensity matrix of the chain is given by

where . Let be a Feller process on the state space . is a one-side diffusion which behaves like Brownian motion in but is modulated at . More precisely, when touches , it either become a sticky Brownian motion or reflected Brownian motion. We denote by the state for sticky Brownian motion and the tate for reflected Brownian motion. Its infinitesimal generator is defined by:

| (8.13) | ||||

where for all . As a consequence of Theorem 5.3, we have the following characterisation of the value function for the optimal stopping problem (8.1):

Corollary 8.4.

There exists a unique pair of viscosity solution such that is a viscosity solution associated with to

and is a viscosity solution associated with to

Additionally, assume that is a viscosity supersolution to

Then, for and for . Furthermore,

is the unique viscosity solution associated with to

In order to derive explicit value function, we define fundamental solutions for optimal stopping problem. Let

| (8.14) | ||||

| (8.15) | ||||

| (8.16) | ||||

| (8.17) |

where , , , and , and and .

Lemma 8.5.

The following hold for :

-

(1)

For any , is a solution to

(8.18) -

(2)

For any , is a solution to

(8.19)

Proof.

The result simply follows from direct computations given the parameters. ∎

The subsequent result can be seen as a verification theorem for the value function.

Proposition 8.6.

Assume that there exist , , for and such that the function

| (8.20) |

satisfies

-

(1)

,

-

(2)

,

-

(3)

is a viscosity solution to

(8.21) -

(4)

is a viscosity supersolution to

(8.22)

Then, the value function .

Proof.

To show that is the viscosity solution, we divide the state space into 3 cases,

-

(i)

For , the viscosity property is given by Lemma 8.5

-

(ii)

For , the viscosity property follows from condition (3)

-

(iii)

For , the viscosity property follows from condition (1) and condition (4).

∎

Using Proposition 8.6, we need to find and such that the viscosity property is satisfied at the following points; (respectively ), and the continuity property is satisfied at the following points (respectively ).

We can then derive the explicit expression of the value function as follows:

Corollary 8.7.

Let , , , such that

| (8.23) |

and has a local minimum at and has a local minimum at . If , then is the value function.

For fixed numerical values of and , we show in the next example that we can find the above parameters and and thus derive the value function.

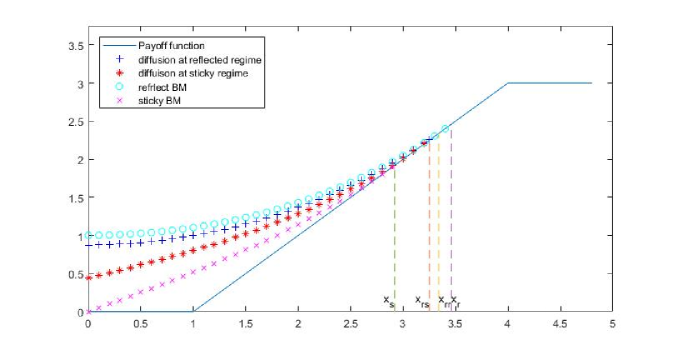

Assume that . Figure 2 depicts the evolution of the value functions

| (8.24) |

where and for regime switching diffusion with reflected boundary and sticky boundary with the intensity matrix

where state 1 represents the reflected boundary and state 2 represents the sticky boundary.

, , and are the exercise points in the cases of sticky Brownian motion, diffusion at sticky regime, diffusion at reflected regime and reflected Brownian motion, respectively. Figure 2 depicts the evolution of the value function of reflected Brownian motion and sticky Brownian motion with regime switching respectively. The sticky Brownian motion has an absorbing point at and the payoff function at equals . This means that the value function of the optimal stopping problem for sticky Brownian motion at is which is smaller than that of the reflected Brownian motion at . Therefore, the exercise points for reflected Brownian motion is larger than that of the sticky Brownian motion . The graph also shows that the value function of this regime switching process will stay between the above two value functions. This is in line with the intuition. Additionally, the graph shows that the exercise points and are between and .

Appendix A Proof of Theorem 2.11

(1) We first prove (1) in Theorem 2.11, that is, there exists a unique solution to (2.7) for each . Define the penalty function as the solution to

| (A.1) |

We start by showing that (A.1) has a unique solution in in the following lemma.

Lemma A.1.

(Equivalence here means that, the solution to one is also a solution to the other, vice versa.)

Proof.

We first show that the solution to (A.1) is equivalent to the solution to (A.2). Let be the solution to (A.1) in . Using the resolvent identity equation (2.2), we obtain

| (A.3) |

Combining (A.1) and (A.3), we have

Therefore, is also a solution to (A.2).

Now, let be a solution to (A.2). Using once more (2.2), we have

| (A.4) |

Combining (A.2) and (A) yields

Hence, is also a solution to (A.1).

In order to complete the proof, it is enough to show that (A.2) has the unique solution. Define a new operator as follows:

We have that and the resolvent operator maps from to . Let , then is also in . Furthermore, let . Using the linearity of the resolvent and the fact that for , we have

where the inequality comes from (2.4). Hence, is a contraction mapping from to . By Banach fixed point theorem, the equation (which is the same as (A.2)) has a unique solution , that we denote by . ∎

Recall that the operator is a bijection of to and its inverse is the resolvent (see Corollary 2.8). The solution to (A.1) is equivalent to the solution to (2.7). It remains to show that . We have shown that (A.1) has the unique solution in such that . Therefore, (1) in Theorem 2.11 is proved.

(2) Let be the unique solution in to (2.7) for . We prove that the sequence of penalty functions converges uniformly to the value function in as . We need the following two preliminary lemmas.

Lemma A.2.

Proof.

Let , and . Define a -optimal stopping time such that

| (A.7) |

Therefore, we have

Since is an arbitrary positive constant, . On the other hand, we can find a stopping time for such that One also obtains similarly. Therefore, we have

| (A.8) |

Then, the proof is completed. ∎

Lemma A.3.

Proof.

Let , and be a -stopping time. We know from (1) in Theorem 2.11 that . Using Dynkin’s formula and optional stopping theorem,

| (A.10) | ||||

Taking the supremum on both sides, we obtain

| (A.11) |

In order to prove the equality, define the stopping time by . Since is right continuous and and are continuous, we have . Using the preceding and (A.10), we have

Hence, (A.9) is proved. Furthermore, since , (A.9) implies for all . The proof is completed. ∎

Lemma A.4.

Proof.

Let and . Using (A.9), we get

Additionally, we have from Lemma A.3 that for all . Then,

| (A.12) |

Furthermore, since by (1) in Theorem 2.11, and thus

Hence, using (2.7) and similar argument as in (A.3), we get

| (A.13) | ||||

Thus, it follows from (A.12) that

| (A.14) |

where is a constant. Hence, converges to uniformly as . The proof of (1) in Theorem 2.11 is completed. ∎

It remains to show that the conclusion of Lemma A.4 is also true for any . Let . is dense in (see Theorem 2.7). Thus there exists a sequence in uniformly converging to as such that for any . Using Lemma A.4, the sequence of the value functions defined by (A.6) is in . Using Lemma A.2, converges to uniformly as . Therefore, .

Appendix B Proof of Lemma 5.8

Let be the Feller semigroup defined by (5.3), that is for any ,

| (B.1) |

By Definition 2.4, its infinitesimal generator can be defined by:

| (B.2) | ||||

| (B.3) |

Let be a domain defined by

| (B.4) |

We show that by double inclusion. We first prove that . Let . We have by (B.1) restricted on that

| (B.5) |

Since , we have , then the limit on the right hand side of (B.5) exists in and we can write

| (B.6) |

In addition, using (B.1) and the fact that , for all . Hence, we know that

| (B.7) |

Putting (B.6) and (B.7) together yields for any , exists in and by the definition of the extension, we get

| (B.8) |

Thus, .

Let us now prove that . Choose . Then, since for such , the limit of (B.2) exists in , it follows that the limit on the right hand side of (B.5) also exists. In addition, using (B.3) and (B.7) respectively, we have and and thus the limit

Therefore, due to the fact that , we have which means . We can conclude that and is given by (B.8), that is (5.8) and (5.13) are proved.

Then, it is reasonable to define the restriction of on by (5.14).

Let us now show that is the core of . Suppose that there is a sequence in satisfying and uniformly in . It is enough to prove that and . Using (5.14), the sequence defined by

belongs to and satisfies and uniformly in . In addition, since is the core of , it follows that and . Therefore, using (B.2), and . The proof is completed.

References

- Alili et al. [2005] Alili, L., Kyprianou, A. E., et al. (2005). Some remarks on first passage of lévy processes, the american put and pasting principles. The Annals of Applied Probability, 15(3):2062–2080.

- Bassan and Ceci [2002a] Bassan, B. and Ceci, C. (2002a). Optimal stopping problems with discontinous reward: Regularity of the value function and viscosity solutions. Stochastics: An International Journal of Probability and Stochastic Processes, 72(1-2):55–77.

- Bassan and Ceci [2002b] Bassan, B. and Ceci, C. (2002b). Regularity of the value function and viscosity solutions in optimal stopping problems for general markov processes. Stochastics: An International Journal of Probability and Stochastic Processes, 74(3-4):633–649.

- Beibel and Lerche [2001] Beibel, M. and Lerche, H. R. (2001). Optimal stopping of regular diffusions under random discounting. Theory of Probability & Its Applications, 45(4):547–557.

- Belomestny et al. [2010] Belomestny, D. V., Rüschendorf, L., and Urusov, M. A. (2010). Optimal stopping of integral functionals and a “no-loss” free boundary formulation. Theory of Probability & Its Applications, 54(1):14–28.

- Bensoussan and Lions [1978] Bensoussan, A. and Lions, J.-L. (1978). Applications des inéquations variationnelles en contrôle stochastique. Dunod.

- Blumenthal and Getoor [2007] Blumenthal, R. M. and Getoor, R. K. (2007). Markov processes and potential theory. Courier Corporation.

- Boshuizen and Gouweleeuw [1993] Boshuizen, F. A. and Gouweleeuw, J. M. (1993). General optimal stopping theorems for semi-Markov processes. Advances in applied probability, 25(4):825–846.

- Böttcher et al. [2013] Böttcher, B., Schilling, R., and Wang, J. (2013). Lévy-type processes: Construction, approximation and sample path properties. lévy matters iii. Lecture Notes in Mathematics, 2099.

- Costantini and Kurtz [2015] Costantini, C. and Kurtz, T. (2015). Viscosity methods giving uniqueness for martingale problems. Electron. J. Probab., 20:27 pp.

- Dai and Menoukeu Pamen [2018] Dai, S. and Menoukeu Pamen, O. (2018). Viscosity Solutions for Optimal Stopping Problem of Feller Process associated with Multiplicative Functionals. Work in progress.

- Dai and Menoukeu Pamen [2019] Dai, S. and Menoukeu Pamen, O. (2019). Iterative Optimal Stopping Method and its Applications. Work in progress.

- Feller [1952] Feller, W. (1952). The parabolic differential equations and the associated semi-groups of transformations. Annals of Mathematics, 55(3):468–519.

- Feller [1954] Feller, W. (1954). Diffusion processes in one dimension. Transactions of the American Mathematical Society, 77(1):1–31.

- Feller [1957] Feller, W. (1957). Generalized second order differential operators and their lateral conditions. 1(4):459–504.

- Fleming and Soner [2006] Fleming, W. H. and Soner, H. M. (2006). Controlled Markov processes and viscosity solutions, volume 25. Springer Science & Business Media.

- Gihman and Skorohod [1975] Gihman, I. and Skorohod, A. V. (1975). The theory of stochastic processes I.

- Kallenberg [2006] Kallenberg, O. (2006). Foundations of modern probability. Springer Science & Business Media.

- Lejay et al. [2015] Lejay, A., Lenôtre, L., and Pichot, G. (2015). One-dimensional skew diffusions: explicit expressions of densities and resolvent kernel. Research Report, Inria Rennes-Bretagne Atlantique; Inria Nancy-Grand Est.

- Mordecki [2002] Mordecki, E. (2002). Optimal stopping and perpetual options for lévy processes. Finance and Stochastics, 6(4):473–493.

- Muciek [2002] Muciek, B. K. (2002). Optimal stopping of a risk process: model with interest rates. Journal of applied probability, 39(2):261–270.

- Øksendal and Sulem [2007] Øksendal, B. K. and Sulem, A. (2007). Applied stochastic control of jump diffusions, volume Third. Springer, Berlin Heidelberg.

- Palczewski and Stettner [2010a] Palczewski, J. and Stettner, Ł. (2010a). Finite horizon optimal stopping of time-discontinuous functionals with applications to impulse control with delay. SIAM Journal on Control and Optimization, 48(8):4874–4909.

- Palczewski and Stettner [2010b] Palczewski, J. and Stettner, L. (2010b). Finite horizon optimal stopping of time-discontinuous functionals with applications to impulse control with delay. SIAM Journal on Control and Optimization, 48(8):4874–4909.

- Palczewski and Stettner [2011] Palczewski, J. and Stettner, Ł. (2011). Stopping of functionals with discontinuity at the boundary of an open set. Stochastic Processes and their Applications, 121(10):2361–2392.

- Palczewski and Stettner [2014] Palczewski, J. and Stettner, Ł. (2014). Infinite horizon stopping problems with (nearly) total reward criteria. Stochastic Processes and their Applications, 124(12):3887–3920.

- Peskir and Shiryaev [2006a] Peskir, G. and Shiryaev, A. (2006a). Optimal Stopping and Free-Boundary Problems. Birkhäuser.

- Peskir and Shiryaev [2006b] Peskir, G. and Shiryaev, A. (2006b). Optimal stopping and free-boundary problems. Springer.

- Revuz and Yor [2013] Revuz, D. and Yor, M. (2013). Continuous martingales and Brownian motion, volume 293. Springer Science & Business Media.

- Robin [1978] Robin, M. (1978). Contrôle impulsionnel des processus de Markov. PhD thesis, Université Paris Dauphine-Paris IX.

- Rüschendorf and Urusov [2008] Rüschendorf, L. and Urusov, M. A. (2008). On a class of optimal stopping problems for diffusions with discontinuous coefficients. The Annals of Applied Probability, 18(3):847–878.

- Schilling [1998] Schilling, R. L. (1998). Conservativeness and extensions of feller semigroups. Positivity, 2(3):239–256.

- Stettner [2011] Stettner, L. (2011). Penalty method for finite horizon stopping problems. SIAM Journal on Control and Optimization, 49(3):1078–1099.

- Stettner and Zabczyk [1980] Stettner, L. and Zabczyk, J. (1980). Stochastic version of a penalty method, pages 179–183. Springer Berlin Heidelberg, Berlin, Heidelberg.

- Stettner and Zabczyk [1983] Stettner, Ł. and Zabczyk, J. (1983). Optimal stopping for feller markov processes. Preprint, 284.

- Taira [2004] Taira, K. (2004). Semigroups, boundary value problems and Markov processes. Springer.