A Class of Solvable Stationary Singular Stochastic Control Problems

Abstract

We consider the determination of the optimal stationary singular stochastic control of a linear diffusion for a class of average cumulative cost minimization problems arising in various financial and economic applications of stochastic control theory. We present a set of conditions under which the optimal policy is of the standard local time reflection type and state the first order conditions from which the boundaries can be determined. Since the conditions do not require symmetry or convexity of the costs, our results cover also the cases where costs are asymmetric and non-convex. We also investigate the comparative static properties of the optimal policy and delineate circumstances under which higher volatility expands the continuation region where utilizing the control is suboptimal.

Keywords: stationary singular stochastic control, optimal reflection, linear diffusions.

JEL Subject Classification: G35, G31, C44, Q23.

AMS Subject Classification: 93E20, 60G10, 49J10, 49K10.

1 Introduction

Many economic and financial decision making problems can be formulated as singular stochastic control problems. For example, the determination of the harvesting policy maximizing the expected cumulative present value of the harvesting yield in the case where the harvesting effort is unbounded constitutes a singular stochastic control problem (cf. [2, 26, 40, 41, 42, 54]). Analogously, cash flow management studies investigating optimal dividend distribution, recapitalization, or both in the presence of risk neutrality result into singular control problems (cf. [3, 4, 12, 13, 27, 28, 32, 47, 49, 50, 52, 53, 58, 59]). Based on its applicability singular stochastic control has attracted much interest in mathematics and there exists a vast literature focusing on it (cf. [1, 5, 6, 7, 8, 9, 10, 16, 17, 15, 18, 19, 21, 22, 23, 24, 31, 33, 34, 35, 36, 38, 39, 43, 44, 46, 48]). However, ergodic singular stochastic control problems has not been investigated to the same extent. This is particularly surprising from the natural resource management point of view since ergodic controls play a central role in the analysis of sustainable harvesting policies (see, for example, Chapter 1 in the seminal textbook [14]). Since singular harvesting policies are associated with the situation where the admissible harvesting effort is unbounded, analyzing the optimal ergodic singular harvesting policy provides simultaneously insights on the long run sustainability of potentially bounded policies as well.

Motivated by the argument above, the objective of this study is to analyze and solve a class of ergodic singular stochastic control problems of linear diffusions. To this end, we reconsider under different assumptions the singular control problem originally introduced in [30] and analyze a class of average cumulative cost minimization problems where the controlled process is a regular linear diffusion and the costs associated with controlling the process are not necessarily symmetric nor convex. In this way, we plan to investigate how the potential asymmetry or nonconvexity of operative costs affect the optimal policy. Instead of analyzing the entire class of admissible policies at once we follow the analysis developed in [20, 53] and focus on local time control policies maintaining the controlled process between two arbitrary boundaries and derive an explicit representation of the long run expected average costs. Following then the analysis of the pioneering studies [20, 33, 57] considering the ergodic singular control of Brownian motion and [45] considering the ergodic singular control of linear diffusions in the presence of smooth costs, we also characterize the stationary value in terms of an associated free boundary problem. We solve the free boundary problem and delineate a set conditions on the cost under which the optimal policy is to reflect the underlying diffusion at two constant boundaries constituting the unique solutions of the optimality conditions. Since the conditions impose only relatively weak monotonicity and limiting conditions on the costs, our findings indicate that the optimality of ordinary reflection policies does not require the symmetry nor the convexity of costs; a result which is in line with the findings of [30]. We illustrate our general observations in explicitly parameterized examples and characterize circumstances under which our assumptions on the limiting behavior of the cost and drift coefficient can be weakened even further. Interestingly, we notice that the assumed continuity of the drift coefficient is not always needed for our findings to remain valid and illustrate this explicitly in the case where the controlled process is a Brownian motion with alternating drift. We also investigate the impact of increased volatility on the optimal policy and its value and find that the convexity of the value of the optimal policy implies that higher volatility postpones the optimal exercise of the control policy by expanding the continuation region. In order to extend previous findings based on ordinary Brownian motion and to simultaneously illustrate explicitly the positive dependence between volatility and the incentives to postpone the utilization of the control policy, we present a class of models resulting into symmetric reflection policies and characterize a special case where the optimal boundaries are linearly dependent on the volatility of the underlying. Finally, in order to cover most standard models arising in the literature applying singular control of linear diffusions, we also study the cases where the underlying can be controlled only to one direction and establish conditions under which the optimal policy can be characterized as an instantaneous reflection policy at a single optimal boundary.

It is at this point worth pointing out that the ergodic singular stochastic control of a linear diffusion has been previously studied in [60, 30, 61, 25] (see also [29] for the associated impulse control model). [60] investigates the optimal stationary singular policy minimizing the long-term average cost in a setting where the controlling costs are symmetric and the decision maker chooses optimally also the drift coefficient of the underlying. [30], in turn, investigates the optimal ergodic singular policy minimizing the long-term average cost in the presence of state-dependent costs. They delineate a set of general conditions under which the problem admits a unique solution and present a set of equations characterizing the optimal boundaries at which the underlying diffusion should be optimally reflected. One of the key findings of [30] is that the convexity of costs is not necessary for the existence of an optimal policy. [61] investigates the relationship between the value of the optimal singular policy minimizing the expected cumulative present value of the costs and the value of the optimal ergodic policy. He extends the Abelian limit result originally established in [33] for Brownian motion and states a set of general conditions under which the same conclusion is valid for a large class of linear diffusions as well. Finally, [25] investigates the optimal impulse control policy minimizing the long-term average cost in the case where the underlying is modeled as a one-dimensional diffusion. They establish conditions for the optimality of a standard -ordering policy for a large class of cost functions. The analysis in [25] is related to the one sided ergodic singular control problem considered in this study, since they also allow for potentially asymmetric holding/back-order and ordering costs within an ergodic impulse control setting. As is known from the literature on impulse control in the case where the objective is to optimize the expected cumulative present value of future revenues, the optimal exercise boundaries of impulse control policies tend towards the ones associated to singular control as the transaction/ordering costs tend to zero (cf. [46, 48]). We notice that the same conclusion is valid in the single boundary setting as well and find that the optimality conditions characterizing the optimal boundaries developed in [25] coincide with ours in the limit.

Ergodic singular stochastic control and ergodic control of singular processes has also been previously studied by relying on alternative and more general approaches than the one utilized in this study. [38] analyzes a large class of stationary control problems by extending the findings of the studies [55, 56] considering the long run average cost minimization for a broad class of processes and controls satisfying a martingale problem defined in terms of the generator of the processes. [24], in turn, investigates based on the findings of [56] the numerical implementation of an infinite-dimensional linear programming formulation of stochastic control problems involving singular stochastic processes. [39] develops conditions under which the optimal control of processes having both absolutely continuous and singular controls can be equivalently formulated as linear programs over a space of measures on the state and control spaces.

The contents of this study are as follows. The general two boundary problem is presented and solved in section 2. The results of the general analysis are then illustrated in explicitly parameterized models in Section 3. The single boundary cases are treated and illustrated in Section 4. Finally, Section 5 concludes our study.

2 The Stationary Singular Stochastic Control Problem

Let be a process defined on a complete filtered probability space and evolving on according to the dynamics characterized by the stochastic differential equation

| (2.1) |

where the drift coefficient is assumed to be continuous on . We also assume that the diffusion coefficient is continuous and satisfies the nondegeneracy condition for all and that the mapping is locally integrable on . As is known from the literature on stochastic differential equations, these conditions guarantee the existence of a weak solution defined up to an explosion time for the stochastic differential equation (2.1) in the absence of interventions (cf. [37], Section 5.5). In (2.1) denote the applied control policies. We call a control policy admissible if it is non-negative, non-decreasing, right-continuous, and -adapted, and denote the set of admissible controls as .

In accordance with the classical theory on linear diffusions, we define the differential operator representing the infinitesimal generator of the underlying diffusion as

| (2.2) |

and denote as

the density of the scale of and as

the density of the speed measure of .

Given the assumptions above, we now plan to consider the determination of the admissible pair of singular control policies minimizing the expected long run average costs

| (2.3) |

where is a continuous mapping measuring the flow of costs incurred from operating with the prevailing stock, and are known parameters which can be interpreted as the unit cost of utilizing the associated control. As usually, we assume that the costs are minimized at and, consequently, that for all .

In what follows the mappings and will play a central role in the determination of the optimal stationary policy. We will assume throughout this section that these functions satisfy the following two conditions:

-

(i)

there is a unique so that is decreasing on and increasing on , where , and

-

(ii)

.

It is worth emphasizing that in the absence of drift, that is, when , and . In that case, assumption (i) essentially states that the operating costs needs to be decreasing below and increasing above it.

Having presented the considered ergodic control problem, we now follow the approach introduced in [20] and [53] (see also [33] and [43]) and focus on the admissible reflecting barrier policies which maintain the process between two constant thresholds and . Both policies are continuous on and increase only when and , respectively. We can now establish the following auxiliary finding characterizing the expected long-run average cumulative costs as a function of the boundaries and .

Lemma 2.1.

Assume that . Then, the expected long-run average cumulative costs read as

where

| (2.4) |

Consequently, if a pair of boundaries minimizing the expected long-run average cumulative costs exists, it has to satisfy the ordinary first order conditions

| (2.5) | ||||

| (2.6) |

which can be re-expressed as

| (2.7) | ||||

| (2.8) |

Proof.

Let be an arbitrary twice continuously differentiable function and let . Applying the Doléans-Dade-Meyer change of variable formula to the function then yields

since is continuous on and the processes and increase only at the boundaries and , respectively. Reordering terms, dividing with , and taking expectations yields

since is bounded on . Since we find by letting and invoking standard ergodic results for linear diffusions that (cf. [11], pp. 36–38; see also [20], pp. 89–92)

where and . Choosing and then yields the system of equations

from which we deduce that

which proves the alleged representation (see II.6.35 on p. 36 in [11]).

In order to establish the optimality conditions, we first find that standard differentiation of yields

proving the conditions (2.5) and (2.6). Utilizing now the identity

| (2.9) |

demonstrates that the partial derivatives can be rewritten as

| (2.10) | ||||

| (2.11) |

from which the ordinary first order conditions (2.7) and (2.8) follow. ∎

Remark 2.2. It is at this point worth emphasizing that the findings of Lemma 2.1 can be extended to the state-dependent cost setting

| (2.12) |

originally considered in [30]. Focusing again on the reflecting barrier policies and yields

Consequently, if the prices and are continuously differentiable, we find that if a pair of boundaries minimizing the expected long-run average cumulative costs exists, it has to satisfy in this case the ordinary first order conditions

where and .

Before proceeding in the analysis of the considered control problem, we now connect our analysis to the free boundary value approach typically utilized in the determination of the optimal policy. To this end, let be two arbitrary constant boundaries. Our objective is now to determine the twice continuously differentiable function as well as the two boundaries and the parameter solving the free boundary problem

| (2.13) | ||||

Since

we find by integrating over the interval and invoking the boundary conditions and that

| (2.14) |

Consequently,

| (2.15) |

Finally, imposing the conditions guaranteeing the second order differentiability of the value across the boundaries implies that

| (2.16) |

which coincide with the ordinary first order optimality conditions (2.7) and (2.8). Consequently, we notice that the smoothness of the value is associated with the optimality of the boundaries. We can now establish the following existence and uniqueness result.

Theorem 2.3.

Proof.

We first observe that since

the roots are found from the set of thresholds satisfying as indicated by (2.16). It is, therefore, sufficient to focus on the function

| (2.18) |

where is defined for in appropriate subsets of .

In order to establish the sets where is well-defined, consider first the case where . If then our assumptions guarantee that there is a unique threshold so that is well-defined for all . Analogously, if , then the function is well-defined for all . Consider now instead the case where . It is then clear that our assumptions guarantee that if then we again observe that is well-defined for all . If , then is well-defined for all . Finally, if either or , then there is a unique intersection point at which and is well-defined for all and satisfies the condition .

Having characterized the sets where is well-defined, we now plan to prove that at the upper boundary of the set where is defined. Consider first the case where . Utilizing (2.9) shows

since . Consider now the case where either and or and . In those cases we find that

since . Finally, if and either or holds, then

proving the alleged positivity of at the upper boundary of the set where is defined.

We now plan to establish that equation has a unique root on by establishing that is monotonically increasing on its domain and tends to as . To this end, assume that and, therefore, that , where . Utilizing the definition of the function (2.18), as well as the identities (2.9) and yields

demonstrating that is monotonically increasing. Moreover, since

as we notice that . Combining this observation with the monotonicity and continuity of and the positivity of at the upper boundary of its domain demonstrates that equation has a unique root . Moreover, since , where , we find that the pair constitutes the unique root of the optimality conditions (2.7) and (2.8). Identity (2.17), in turn, follows directly from (2.15).

It remains to establish that the marginal value satisfies the inequality for all . It is clear that on and that on . To establish that , on , we first notice that since

we obtain by invoking the boundary condition and that

| (2.19) |

We first prove that the integral expression in (2.19) is nonpositive on . To see that this is indeed true, we first notice that if , then the integrand is always nonpositive proving the alleged nonpositivity of the integral in that case. If, however, , then our assumptions on the function guarantee that there exists a uniquely defined state . However, since the integrand is nonpositive for all and the integral is nonincreasing for we notice that the integral is nonpositive in that case as well. In order to complete the proof it is sufficient to show that

for all . To this end consider now the function

It is clear that , , and . Two cases arise. If then for all and we are done. If, however, , then for all and for all where . Consequently, we notice that for all in that case as well, completing the proof of our theorem. ∎

Remark 2.4. It is worth noticing that Theorem 2.3 implies the marginal value can be re-expressed as a convex combination

where

| (2.20) |

satisfies and .

Theorem 2.3 demonstrates that the monotonicity and limiting behavior of the functions and are the principal determinants of the pair of boundaries satisfying the first order optimality conditions (2.7) and (2.8). According to Theorem 2.3 the lower reflection boundary is situated on the set where is decreasing while the upper reflection boundary is situated on the set where is increasing. Consequently, no convexity or other second order properties are required for establishing the existence and uniqueness of a reflection. As is also clear from the proof or Theorem 2.3 the assumed limiting behavior of the functions and are sufficient for the existence of the pair of boundaries. It is, however, clear that those assumptions are not necessary and can be weakened in some circumstances. More precisely, if the function defined in (2.18) satisfies the condition , where , then a unique pair satisfying the optimality conditions (2.7) and (2.8) exists even when the limiting conditions are not satisfied. We will illustrate this point later in an explicitly parameterized example.

Having proved the existence of the pair we now demonstrate that it is optimal as well and, therefore, that deviating from it results into higher long run average cumulative costs. Our main result on this subject is summarized in the next theorem.

Theorem 2.5.

is a global minimum on and for all . Consequently, for all and constitutes an optimal singular control within the considered class of reflection policies.

Proof.

Let us first investigate the behavior of the function . If , then

It is now clear from our assumptions on that is increasing on and decreasing on as a function of . Moreover, if , then

as . Consequently, for all . Combining these observation with identity implies that has a unique root for any and for . Establishing now that is increasing on , decreasing on as a function of and satisfies for all is completely analogous. Consequently, we notice that has a unique root for any and for . Combining these observations with the uniqueness of the pair and the equations (2.10) and (2.11) completes the proof of the first claim of our theorem. The second statement then follows directly from Lemma 2.1 and (2.15). ∎

Theorem 2.5 establishes that the pair satisfying the ordinary first order conditions constitutes the global minimum of the long run average cumulative costs. Since this minimum can be attained by utilizing an admissible local time reflection policy we notice that indeed constitutes the optimal admissible policy.

It is naturally of interest to investigate how increased volatility affects the optimal policy and its value. Our main finding on that subject is summarized in the following.

Lemma 2.6.

Assume that the value is convex. Then, increased volatility expands the continuation region and increases the expected long run average costs.

Proof.

Denote as

the differential operator associated with the more volatile process characterized by the diffusion coefficient satisfying the inequality for all . If is convex, then clearly

implying that

where denotes the density of the scale and the speed density of the more volatile underlying. Since we notice that

Since this inequality is valid for all it is valid for the optimal ones as well and, consequently we have , where denotes the the expected long run average costs in the more volatile setting. Since , where denote the optimal boundaries in the more volatile setting, we notice by combining this observation with the assumed monotonicity of the mappings and that and , thus completing the proof of our lemma. ∎

In many practical economic and financial applications of singular stochastic control theory only one control policy can be endogenously determined while the other is exogenously set through the constraints affecting decision making. For example, cash flow policies may be subject to compulsory recapitalization should the prevailing reserves fall below an exogenously set critical level. In a completely analogous manner, reserve accumulation policies may be subject to obligatory redistribution should the reserves exceed a preset level. As intuitively is clear, in such situations, the considered problems constitute special cases of the general problem considered in Theorem 2.3. Our main findings focusing on these type of problems are now summarized in the next corollary of Theorem 2.3.

Corollary 2.7.

(A) Assume that the lower boundary is exogenously set. Then, there exists a unique optimal reflection boundary satisfying the first order condition

| (2.21) |

Moreover, for all .

(B) Assume that the upper boundary is exogenously set. Then, there exists a unique optimal reflection boundary satisfying the first order condition

| (2.22) |

Moreover, for all .

Proof.

(A) Utilizing (2.14) in addition to the optimality condition implies that equation (2.21) has to be satisfied. In order to establish the existence and uniqueness of , consider the function

It is clear that and for . If then

as . Comining this observation with the monotonicity of proves the existence and uniqueness of the threshold The validity of inequality for all follows from (2.19) as proved in Theorem 2.3. Establishing part (B) is completely analogous. ∎

As is clear from Theorem 2.3, the potential asymmetry of the costs affects the optimal reflection boundaries only through its effect on the functions and which depend also on the drift coefficient of the underlying dynamics. The role of the costs is naturally pronounced in the absence of a drift since in that setting and the incentives to exert the control policy are solely determined by the costs and volatility. Our findings on this special case are now summarized in the following.

Theorem 2.8.

Assume that . Then, the optimality conditions

| (2.23) | ||||

| (2.24) |

have a uniquely determined solution such that . Moreover,

-

(i)

The value is strictly convex and satisfies the inequality for all .

-

(ii)

Increased volatility expands the continuation region by decreasing the lower boundary and increasing the upper boundary.

Proof.

The first alleged result is a direct implication of Theorem 2.3. In order to establish the convexity of the value , we first notice that for all since is decreasing on and increasing on . Since is linear on and satisfies on the inequality

then proves that is convex on . This observation also implies that for all . It remains to prove that increased volatility expands the continuation region. To see that this is the case, we first observe that for all , where for all . Consequently, if for all then

for all . Since and are increasing on we notice that implying that the root of equation is below . Consequently, completing the proof of the alleged claim. ∎

Theorem 2.8 characterizes the optimal boundaries and the value explicitly in the case where the controlled diffusion constitutes a time changed Brownian motion. Interestingly, our findings indicate that the familiar conclusion on the negative effect of increased volatility on the incentives to utilize the irreversible control policy are true also in this case. The higher volatility gets, the larger the continuation region becomes. An interesting direct implication of Theorem 2.8 is now summarized in our next corollary.

Corollary 2.9.

Assume that and that the cost function is even. Then where the optimal boundary constitutes the unique positive root of equation

| (2.25) |

Proof.

The alleged result is a direct implication of Theorem 2.8. ∎

It is worth emphasizing that the optimality conditions (2.7) and (2.8) can also be re-expressed in terms of the stationary distribution of the controlled dynamics. More precisely, since the process is maintained between the boundaries and and when we notice that where is distributed according to the stationary probability measure characterized by its density (cf. [11], pp. 36–38)

Utilizing this definition shows that the optimality conditions (2.7) and (2.8) can be re-expressed as

| (2.26) | ||||

| (2.27) |

As we will later see in the analysis of single boundary control problems, the left hand side of these identities appears in the characterization of the optimal boundaries within a one-sided reflection setting. In those cases the right hand side of the optimality conditions equals zero. Consequently, we notice that in the two-boundary setting the difference between the expected long-run cost flow and its value at the boundary falls short its value in the single boundary setting. As intuitively is clear, this difference is based on the larger flexibility a decision maker has in the present setting where the underlying can be controlled both upwards as well as downwards. Since this flexibility is partially lost in the single boundary setting, the cost savings are naturally lower in that case. Our key observation on the stationary characterization of the two-boundary problem is now summarized in the following theorem how identity (2.15) arises by applying a standard reflection policy.

3 Explicit Illustrations

3.1 Example A: Controlled Brownian Motion with Drift

We now consider as an example the stationary singular stochastic control problem of the process

| (3.1) |

where and . In order to investigate how the potential asymmetries in the costs affect the optimal policy, we assume that and consider the piecewise linear cost , where are known exogenously determined positive parameters. It is clear that and satisfy the required monotonicity and limiting conditions and consequently, our results apply. Standard integration yields

| (3.2) | ||||

| (3.3) |

Now

implying that

In this case ,

and

for all . Since, we notice that equation has a unique root . The case where is of special interest, since in that case

and

Consequently, in the absence of drift the optimal boundaries read as

We notice directly that increased volatility expands the continuation region. Moreover, since we notice that the relative distance between the two optimal thresholds is inversely proportional to the marginal cost ratio . The elasticities of these thresholds with respect to changes in the marginal costs read as

where . Hence, we notice that the sensitivities of the thresholds with respect to changes in the marginal cost ratio are asymmetric as well.

It is worth noticing that in the symmetric setting where the function reads as

from which we can directly deduce that the optimal thresholds are

Invoking L’Hospital’s rule in the symmetric setting yields

demonstrating how increased volatility increases linearly the continuation region in that case.

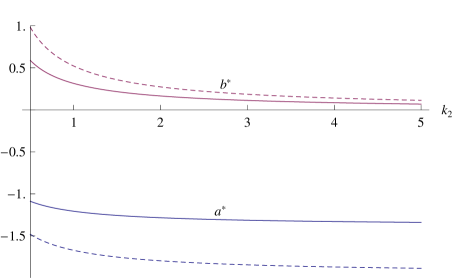

3.2 Example B: Controlled Ornstein-Uhlenbeck-process

In order to illustrate our findings in a mean-reverting setting, we now consider the stationary singular stochastic control problem of the process

| (3.4) |

where and . We again assume that and that the cost is of the piecewise linear form , where are known exogenously determined positive parameters satisfying the inequality . It is clear that now and satisfy the required monotonicity and limiting conditions and consequently, our results again apply. In this case

and

where denotes the cumulative distribution function of a standard normal random variable. As is clear from the expressions above, the auxiliary function

takes in this case a relatively complex form and is, thus, left unstated. The boundaries of the continuation region are illustrated in Figure 1 as functions of the marginal cost for two volatilities () under the assumptions that , and . As is clear from the figure, an increase in the marginal cost associated with controlling the underlying diffusion downwards decreases both boundaries. The reason for this observation is intuitively clear. As becomes larger, controlling the diffusion downwards becomes more expensive while controlling the diffusion upwards becomes relatively cheaper. In line with standard real option models of irreversible decision making our numerical illustration indicates that increased volatility expands the continuation region by rising and lowering . Interestingly, the relative impact of increased volatility appears to be stronger with respect to the boundary associated with the control policy with a lower marginal cost. This shows the intricate interaction between volatility and costs in the stationary singular stochastic control setting.

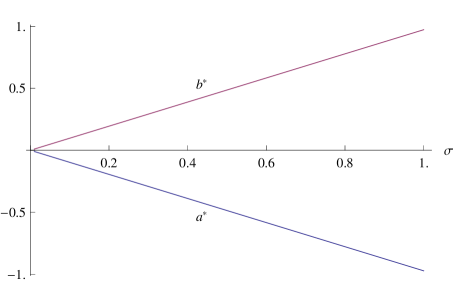

3.3 Example C: A General Symmetric Problem

In order to analyze an example leading to a symmetric control policies (in the spirit of the seminal study by [33]) we now consider the stationary singular stochastic control problem of the process

| (3.5) |

where the drift coefficient is assumed to be an odd function. In order to analyze symmetric stationary singular stochastic control policies, we assume that both the cost function as well as the volatility coefficient are even and that . It is clear that in this case for all it holds

indicating that the optimal policy is symmetric. By invoking symmetry we find that the upper optimal reflection boundary constitutes the unique root of equation , where

We illustrate the boundaries of the continuation region in the case where , and . It is clear that in this case

proving that and that , where constitutes the unique positive root of equation

The boundaries of the continuation region are illustrated in Figure 2 as functions of volatility under the assumption that (implying that ).

It is at this point worth emphasizing that as was argued after Theorem 2.3, the existence of the optimal reflection boundaries can be guaranteed even in cases where the limiting conditions on the mappings and are not satisfied. It is clear that in the present example the existence and uniqueness is guaranteed provided that , where . To illustrate such a case, assume that , , and . In that case

proving that the optimal boundary exists provided that .

Remark 3.1. The example above indicates that the assumed continuity of the drift coefficient is not necessary for the validity of our results in some circumstances since the controlled stochastic differential equation (2.1) has a weak solution also in situations where the drift coefficient is bounded but not necessarily continuous. Especially, if the underlying follows a Brownian motion with alternating drift

is an even function, and , then there exists a unique pair of optimal reflection boundaries satisfying the symmetry condition , where constitutes the unique positive root of equation

4 Optimal Reflection at a Single Boundary

In many practical applications focusing on the complete irreversibility of the implemented policy the control policy can take the controlled stock only to a single direction. Examples of such actions are, for example, rational harvesting planning or optimal dividend distribution. For the sake of completeness we will shortly focus on that class of problems in this section. More precisely, we will investigate the determination of the admissible policies and attaining the minimal expected asymptotic values

| (4.1) |

and

| (4.2) |

respectively. As is clear, our original assumptions in the two-boundary setting need to be adjusted to the problems at hand. In the case of the downward control problem (4.1) we assume in addition to our assumptions on the following:

-

(D1)

and for all

-

(D2)

.

On the other hand, in the case of the upward control problem (4.2) we assume in addition to our assumptions on the following:

-

(U1)

and for all

-

(U2)

.

It is at this point worth mentioning that assumptions (D1) and (D2) guarantee that the lower boundary is either natural or entrance (and, hence, unattainable) for the controlled diffusion in the absence of interventions. An analogous argument holds for the upper boundary under the assumptions (U1) and (U2).

Before establishing our principal existence and uniqueness results on the optimal policy, we first notice that utilizing Lemma 2.1 in addition to (2.9) and the conditions (D1), (D2), (U1), and (U2) to the problems at hand yields in the downward reflection case

for an arbitrary boundary and in the upward reflection case

for an arbitrary boundary . Define the functions and as

Standard differentiation then yields

We can now immediately establish the following result.

Theorem 4.1.

(A) The optimality condition

| (4.3) |

has a unique solution such that

Moreover,

for all .

(B) The optimality condition

| (4.4) |

has a unique solution such that

Moreover,

for all .

Proof.

(A) Consider the function

It is clear that for all and that for all . If we notice that

as . Hence, equation has a unique root constituting the global minimum of the functional and satisfying . Establishing part (B) is entirely analogous. ∎

Theorem 4.1 summarizes our main findings on the single boundary setting. It is worth noticing that the optimality condition (4.3) can be re-expressed as

Analogously, the optimality condition (4.4) can be re-expressed as

As was pointed out in the analysis of the two boundary problem, these optimality conditions are associated with the conditions (2.26) and (2.27). The main difference is naturally the absence of the term associated with the control policy acting to the opposite direction. It is also worth noticing that the optimality conditions (4.3) and (4.4) constitute the limit of the optimality condition (3.17) in Proposition 3.5 of [25] as the fixed transaction/ordering costs tend zero and the costs are linear.

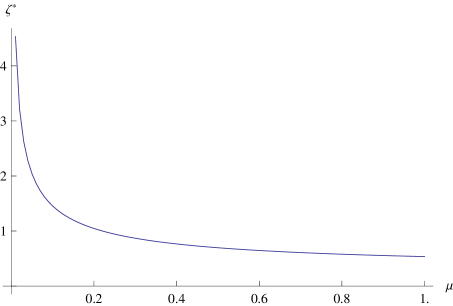

4.1 Example: Controlled Ornstein-Uhlenbeck process

In order to exemplify our general results, we now consider the downward reflection problem (4.1) in the case where , , and , where and . In that case the optimality condition reads for as

As in the two-boundary case, we again observe that the optimal boundary is linear as a function of volatility, where the ratio constitutes the root of equation

The critical ratio is illustrated in Figure 3 as a function of the drift coefficient under the assumption that .

As is clear from Figure 3, the sensitivity of the optimal boundary with respect to changes in volatility depends on the rate at which the underlying is expected to grow. The smaller the growth rate is, the higher the multiplier becomes.

5 Conclusions

We considered a class of ergodic singular stochastic control problems of a regular linear diffusion. We characterized the optimal policy and its value by relying on relatively elementary results from the classical theory of linear diffusions and ordinary optimization. Our results indicate that the convexity or symmetry of costs is not necessary for the existence of an optimal control characterized by two optimal thresholds at which the underlying diffusion should be reflected by utilizing a standard local time reflection policy. Our results also indicate that increased volatility expands the continuation region and increases the expected long run average costs whenever the value is convex; a result which is in line with results of standard models focusing on the minimization of the expected cumulative present value of the costs.

The singular stochastic control setting considered in this paper is just one class of bounded variation controls arising in the literature applying stochastic control theory. As is known, it is associated with the most flexible type of that type of policies since the decision maker can adjust the path by infinitesimal amounts at any time. In many practical situations this is unfortunately not possible due to, for example, the presence of fixed controlling costs. Such situations result into impulse control models which require a slightly different analysis. However, the recent results by [25] on inventory models indicate that analyzing that class of problems within the ergodic setting is doable at least in the single boundary setting. It would, therefore, be of interest to try to extend our findings to the two boundary impulse control setting. This is to my best knowledge a still open question left for future research.

References

- [1] Alvarez, L. H. R. A Class of Solvable Singular Stochastic Control Problems, 1999, Stochastics & Stochastics Reports, 67, 83 – 122.

- [2] Alvarez, L. H. R. and Shepp, L. A. Optimal harvesting of stochastically fluctuating populations, 1998, Journal of Mathematical Biology, 37, 155 – 177.

- [3] Alvarez, L. H. R. and Virtanen, J. A Class of Solvable Stochastic Dividend Optimization Problems: On the General Impact of Flexibility on Valuation, 2006, Economic Theory, 28, 373–398

- [4] Asmussen, S. and Taksar, M. Controlled diffusion models for optimal dividend pay-out, 1997, Insurance: Mathematics and Economics, 20, 1–15.

- [5] Baldursson, F. M. Singular Stochastic Control and Optimal Stopping, 1987, Stochastics & Stochastics Reports, 21, 1 – 40.

- [6] Bank, P. Optimal control under a dynamic fuel constraint, 2005, SIAM Journal on Control and Optimization, 44, 1529–1541.

- [7] Bather, J. A. , and Chernoff, H. Sequential decisions in the control of a spaceship, 1966, In: Proceedings of the fifth Berkeley symposium on mathematical statistics and probability, 3, 181–207.

- [8] Bayraktar, E., and Egami, M. An analysis of monotone follower problems for diffusion processes, 2008, Mathematics of Operations Research, 33, 336–350.

- [9] Benes, V. E., Shepp, L. A., Witsenhausen, H. S. Some solvable stochastic control problems, Stochastics, 1980, 4, 39–83.

- [10] Boetius, F. and Kohlmann, M. Connections between optimal stopping and singular stochastic control, 1998, Stochastic Processes and their Applications, 77, 253–281.

- [11] Borodin, A. and Salminen, P. Handbook on Brownian motion - facts and formulae, 2015, 2nd ed. (2nd printing), 685 p., Birkhäuser, Basel.

- [12] Cadenillas, A., Sarkar, S., and Zapatero, F. Optimal dividend policy with mean-reverting cash reservoir, 2007, Mathematical Finance, 17, 81–109

- [13] Choulli, T., Taksar, M., and Zhou, X. Y. A diffusion model for optimal dividend distribution for a company with constraints on risk control, 2003, SIAM Journal on Control and Optimization, 41, 1946–1979.

- [14] Clark, C. W., Mathematical bioeconomics: The mathematics of conservation, 2010, 3rd ed., John Wiley & Sons, Inc., Hoboken, NJ.

- [15] Ferrari, G. On a Class of Singular Stochastic Control Problems for Reflected Diffusions, 2017, eprint arXiv:1711.03741.

- [16] Dufour, F. and Miller, B. Singular Stochastic Control Problems, 2004, SIAM Journal on Control and Optimization, 43, 708–730.

- [17] Dufour, F. and Miller, B. Maximum Principle for Singular Stochastic Control Problems, 2006, SIAM Journal on Control and Optimization, 45, 668–698.

- [18] Guo, X., and Tomecek, P. A class of singular control problems and the smooth fit principle, 2008 (a), SIAM Journal on Control and Optimization, 47, 3076–3099.

- [19] Guo, X., and Tomecek, P. Connections between singular control and optimal switching, 2008 (b), SIAM Journal on Control and Optimization, 47, 421–443

- [20] Harrison, J. M. Brownian Motion and Stochastic Flow Systems, 1985, Wiley, New York.

- [21] Harrison, J. M., Taksar, M. I. Instantaneous control of Brownian motion, 1983, Mathematics of Operations Research, 8, 439–453.

- [22] Hausmann, U. G. and Suo, W. Singular Optimal Stochastic Controls I: Existence, 1995, SIAM Journal on Control and Optimization, 33, 916–936.

- [23] Hausmann, U. G. and Suo, W. Singular Optimal Stochastic Controls I: Dynamic Programming, 1995, SIAM Journal on Control and Optimization, 33, 937–959.

- [24] Helmes, K. and Stockbridge, R. H., Determining the optimal control of singular stochastic processes using linear programming, 2008, in Markov processes and related topics: a Festschrift for Thomas G. Kurtz, Inst. Math. Stat. (IMS) Collect., 4, 137–153.

- [25] Helmes, K. L., Stockbridge, R. H., and Zhu, C. Continuous inventory models of diffusion type: Long-term average cost criterion, 2017, Annals of Applied Probability, 27, 1831–1885

- [26] Hening, A., Nguyen, D. H., Ungureanu, S. C., and Wong, T. K. Asymptotic harvesting of populations in random environments, 2017, eprint arXiv:1710.01221

- [27] Højgaard, B. and Taksar, M. Controlling risk exposure and dividends payout schemes: Insurance company example, 1999, Mathematical Finance, 9, 153–182.

- [28] Højgaard, B. and Taksar, M. Optimal risk control for a large corporation in the presence of returns on investments, 2001, Finance & Stochastics, 5, 527–547.

- [29] Jack, A. and Zervos, M., Impulse Control of One-Dimensional Ito Diffusions with an Expected and a Pathwise Ergodic Criterion, 2006, Applied Mathematics and Optimization, 54, 71–93.

- [30] Jack, A. and Zervos, M., A Singular Control Problem with an Expected and a Pathwise Ergodic Performance Criterion, 2006, Journal of Applied Mathematics and Stochastic Analysis, 2006 (82538), 1–19.

- [31] Jacka, S. Avoiding the origin: a finite-fuel stochastic control problem, 2002, Annals of Applied Probability, 12, 1378–1389.

- [32] Jeanblanc-Picqué, M. and Shiryaev, A. N. Optimization of the flow of dividends, 1995, Russian Math. Surveys, 50, 257 – 277.

- [33] Karatzas, I. A class of singular stochastic control problems, Advances in Applied Probability, 1983, 15, 225 – 254.

- [34] Karatzas, I. Probabilistic aspects of finite-fuel stochastic control, 1985, Proceeding of the National Academy of Sciences of USA, 82, 5579–5581.

- [35] Karatzas, I. and Shreve, S. E. Connections between optimal stopping and singular stochastic control I. Monotone follower problems, SIAM J. Control and Optimization, 1984, 22, 856 – 877.

- [36] Karatzas, I. and Shreve, S. E. Connections between optimal stopping and singular stochastic control II. Reflected follower problems, SIAM J. Control and Optimization, 1985, 23, 433 – 451.

- [37] Karatzas, I. and Shreve, S. Brownian Motion and Stochastic Calculus, 1991, Springer, New York.

- [38] Kurtz, T. G. and Stockbridge, R. H. Stationary Solutions and Forward Equations for Controlled and Singular Martingale Problems, 2001, Electronic Journal of Probability, 6, 1–52.

- [39] Kurtz, T. G. and Stockbridge, R. H. Linear programming formulations of singular stochastic control problems:Time-homogeneous problems, 2017, arXiv:1707.09209

- [40] Lande, R. and Engen S. and Sæther B.-E. Optimal harvesting, economic discounting and extinction risk in fluctuating populations, 1994, Nature, 372, 88–90.

- [41] Lande, R. and Engen S. and Sæther B.-E. Optimal harvesting of fluctuating populations with a risk of extinction, The American Naturalist, 1995, 145, 728–745.

- [42] Lungu, E. M. and Øksendal, B. Optimal harvesting from a population in a stochastic crowded enviroment, 1996, Mathematical Biosciences, 145, 47 – 75.

- [43] Matomäki, P. On solvability of a two-sided singular control problem, 2012, Mathematical Methods of Operations Research, 76, 239–271.

- [44] Menaldi, J. L. and Robin, M. On some cheap control problems for diffusion processes, 1983, Transactions of the AMS, 278, 771–802.

- [45] Menaldi J. L., Robin M. Some singular control problem with long term average criterion, 1984, in: Thoft-Christensen P. (eds) System Modelling and Optimization. Lecture Notes in Control and Information Sciences, vol 59. Springer, Berlin, Heidelberg.

- [46] Menaldi, J. L. and Rofman, E. On stochastic control problems with impulse cost vanishing, 1983, Lecture notes in economics and mathematical systems, 215, Fiacco, A. V. and Kortanek, K. O. (eds.), Springer-Verlag, Berlin, 771–802.

- [47] Milne, A. and Robertson, D. Firm behaviour under the threat of liquidation, 1996, Journal of Economic Dynamics and Control, 20, 1427 – 1449.

- [48] Øksendal, B. Stochastic control problems where small intervention costs have big effects, 1999, Applied mathematics & Optimization, 40, 355–375.

- [49] Paulsen, J. Optimal dividend payments and reinvestments of diffusion processes with fixed and proportional costs, 2008, SIAM Journal on Control and Optimization, 47, 2201–2226.

- [50] Peura, S. and Keppo, J. S., Optimal Bank Capital with Costly Recapitalization, 2006, Journal of Business, 79, 2163–2201.

- [51] Protter, P. Stochastic integration and differential equations, 2004, Springer-Verlag, 2nd edition.

- [52] Sethi, S. P., and Taksar, M. I. Optimal financing of a corporation subject to random returns, 2002, Mathematical Finance, 12, 155–172.

- [53] Shreve, S., Lehoczky, J., and Gaver, D. Optimal consumption for general diffusion with absorbing and reflecting barriers, 1984, SIAM Journal on Control and Optimization, 22, pp. 55–75.

- [54] Song, Q., Stockbridge, R. H., and Zhu, C. On Optimal Harvesting Problems in Random Environments, 2011, SIAM Journal on Control and Optimization, 49, 859–889

- [55] Stockbridge, R. H., Time-average control of martingale problems: existence of a stationary solution, 1990, The Annals of Probability, 18, 190–205

- [56] Stockbridge, R. H., Time-average control of martingale problems: a linear programming formulation, 1990, The Annals of Probability, 18, 206–217.

- [57] Taksar, M. Average Optimal Singular Control and a Related Stopping Problem, 1985, Mathematics of Operations Research, 10, 63–81.

- [58] Taksar, M. Optimal risk and dividend distribution control models for an insurance company, 2000, Mathematical Methods of Operations Research, 51, 1–42.

- [59] Taksar, M. and Zhou X. Y. Optimal risk and dividend control for a company with a debt liability, 1998, Insurance: Mathematics and Economics, 22, 105–122.

- [60] Weerasinghe, A. Stationary stochastic control for Itô processes, 2002, Advances in Applied Probability, 34, 128–140.

- [61] Weerasinghe, A. An abelian limit approach to a singular ergodic control problem, 2007, SIAM Journal on Control and Optimization, 46, 714–737.