Comparative Statics via Stochastic Orderings in a Two-Echelon Market with Upstream Demand Uncertainty

Abstract

We revisit the classic Cournot model and extend it to a two-echelon supply chain with an upstream supplier who operates under demand uncertainty and multiple downstream retailers who compete over quantity. The supplier’s belief about retail demand is modeled via a continuous probability distribution function . If has the decreasing generalized mean residual life (DGMRL) property, then the supplier’s optimal pricing policy exists and is the unique fixed point of the mean residual life (MRL) function. This closed form representation of the supplier’s equilibrium strategy facilitates a transparent comparative statics and sensitivity analysis. We utilize the theory of stochastic orderings to study the response of the equilibrium fundamentals – wholesale price, retail price and quantity – to varying demand distribution parameters. We examine supply chain performance, in terms of the distribution of profits, supply chain efficiency, in terms of the Price of Anarchy, and complement our findings with numerical results.

Keywords: Continuous Distributions, Demand Uncertainty, Generalized Mean Residual Life, Comparative Statics, Sensitivity Analysis, Stochastic Orders.

1 Introduction

The global character of modern markets necessitates the study of competition models that capture two features: first, that retailers’ cost is not constant but rather formed as the decision variable of a strategic, profit-maximizing supplier, and second that uncertainty about retail demand affects not only the retailers but also the supplier. Motivated by these considerations, in Le17 , we use a game-theoretic approach to extend the classic Cournot market in the following two-stage game: in the first-stage (acting as a Stackelberg leader), a revenue-maximizing supplier sets the wholesale price of a product under incomplete information about market demand. Demand or equivalently, the supplier’s belief about it, is modeled via a continuous probability distribution. In the second-stage, the competing retailers observe wholesale price and realized market demand and engage in a classic Cournot competition. Retail price is determined by an affine inverse demand function.

La01 studied a similar model in which demand uncertainty affected a single retailer. They identified the property of increasing generalized failure rate (IGFR) as a mild unimodality condition for the deterministic supplier’s revenue-function and then performed an extensive comparative statics and performance (efficiency) analysis of the supply chain at equilibrium. The properties of IGFR random variables were studied in a series of subsequent notes, La06 ,Ba13 and Pa05 .

In Le17 , we extended the work of La01 by moving uncertainty to the supplier and by implementing an arbitrary number of second-stage retailers. We introduced the generalized mean residual life (GMRL) function of the supplier’s belief distribution and showed that his stochastic revenue function is unimodal, if the GMRL function is decreasing – (DGMRL) property – and has finite second moment. In this case, we characterized the supplier’s optimal price as a fixed point of his mean residual life (MRL) function, see Theorem 3.1 below. Subsequently, we turned our attention to DGMRL random variables, examined their moments, limiting behavior, closure properties and established their relation to IGFR random variables, as in La06 , Ba13 and Pa05 . This study was done in expense of a comparative statistics and performance analysis, as the one in Sections 3-5 of La01 . The importance of such an analyis is underlined among others in Ac13 ,At02 ,Je18 and references therein.

1.1 Contributions – Outline:

The present paper aims to fill this gap. Following the methodology of La01 , we study the response of maket fundamentals by utilizing the closed form characterization of the equilibrium obtained in Le17 . Specifically, under the conditions of Theorem 3.1, the optimal wholesale price is the unique fixed point of the MRL function of the demand distribution . This motivates the study of conditions under which two different markets, denoted by and , can be ordered in the mrl-stochastic order, see Sh07 .

The paper is organized as follows. In Section 2, we provide the model description and in Section 3, the existing results from Le17 on which the current analysis is based. Our findings, both analytical and numerical are presented in Section 4. Section 5 concludes our analysis and discusses directions for future work.

Comparison to Related Works

Two-echelon markets have been extensively studied in the literature under different perspectives and various levels of demand uncertainty, see e.g. Be05 , Pa09 , Wu12 and Ya06 . In the present study, we depart from previous works by introducing the toolbox of stochastic orderings in the comparative statics analysis. The advantage of this approach is that we quantify economic notions, such as market size and demand variability, in various ways. Accordingly, we are able to challenge established economic intuitions by showing, for instance, that repsonses of wholesale prices to increasing market size or demand variability are not easy to perdict, since they largely depend on the notion of variability that is employed.

2 The Model: Game-Theoretic Formulation

An upstream supplier produces a single homogeneous good at constant marginal cost, normalized to , and sells it to a set of downstream retailers. The supplier has ample quantity to cover any possible demand and his only decision variable is the wholesale price which he determines prior to and independently of the retailers’ order-decisions. The retailers observe – a price-only contract (there is no return option and the salvage value of the product is zero) – as well as the market demand parameter and choose simultaneously and independently their order-quantities . They face no uncertainty about the demand and the quantity that they order from the supplier is equal to the quantity that they sell to the market (at equilibrium). The retail price is determined by an affine inverse demand function , where is the demand parameter and is the total quantity that the retailers release to the market111To simplify notation, we write or and or instead of the proper and .. Contrary to the retailers, we assume that at the point of his decision, the supplier has incomplete information about the actual market demand.

This supply chain can be represented as a two-stage game, in which the supplier acts in the first stage and the retailers in the second. A strategy for the supplier is a price and a strategy for retailer is a function , which specifies the quantity that retailer will order for any possible cost . Payoffs are determined via the strategy profile , where . Given cost , the profit function or simply , of retailer , is . For a given value of , the supplier’s profit function, is for , where depends on via .

To model the supplier’s uncertainty about retail demand, we assume that after the pricing decision of the supplier, but prior to the order-decisions of the retailers, a value for is realized from a continuous distribution , with finite mean and nonnegative values, i.e. . Equivalently, can be thought of as the supplier’s belief about the demand parameter and, hence, about the retailers’ willingness-to-pay his price. We will use the notation for the survival function and , for the support of respectively. Under these assumptions, the supplier’s payoff function becomes stochastic: . All the above are assumed to be common knowledge among the participants in the market (the supplier and the retailers).

3 Existing Results

We consider only subgame perfect equilibria, i.e. strategy profiles such that is an equilibrium in the second stage and is a best response against any for all . The equilibrium behavior of this market has been analyzed in Le17 . To proceed with the equilibrium representation, we first introduce some notation.

3.1 Generalized Mean Residual Life:

Let be a nonnegative random variable with finite expectation . The mean residual life (MRL) function of is defined as

and , otherwise, see, e.g., Be16 , Lax06 or Sh07 . In analogy to the generalized failure rate (GFR) function , where denotes the hazard rate of and the increasing generalized failure rate (IGFR) unimodality condition, defined in La01 and studied in La06 ,Ba13 , we introduce, see Le17 , the generalized mean residual life (GMRL) function , defined as , for . If is decreasing, then has the (DGMRL) property. The relationship between the (IGFR) and (DGMRL) classes of random variables is studied in Le17 .

We will use the notation DMRL for a random variable with a decreasing mean residual life function and IFR for a random variable with increasing failure rate . We say that is smaller than in the mean residual life order, denoted as , if for all , see Sh07 . Of course if and only if for all . Similarly, is smaller than in the usual stochastic (hazard rate) order, denoted as (), if () for all . The -order implies the -order. However, neither of the orders and imply the other.

Market equilibrium:

Using this terminology, we can express the supplier’s optimal pricing strategy in terms of the MRL function and formulate sufficient conditions on the demand distribution, under which a subgame perfect equilibrium exists and is unique.

Theorem 3.1 (Le17 )

Assume that the supplier’s belief about the unknown, nonnegative demand parameter, , is represented by a continuous distribution , with support inbetween and with .

-

(a)

If an optimal price for the supplier exists, then satisfies the fixed point equation

(1) -

(b)

If is strictly DGMRL and is finite, then in equilibrium, the optimal price of the supplier exists and is the unique solution of (1).

Expressing (1) in terms of the GMRL function , the supplier’s optimal price can be equivalently written as the solution of equation .

4 Comparative Statics

The closed form expression of (1) provides the basis for an extensive comparative statics and sensitivity analysis on the distribution parameters of market demand. To understand the market-equilibrium behavior under different demand (distribution) characteristics, we employ (1) and the rich theory of stochastic orders, Sh07 , Lax06 and Be16 . Based on , and Theorem 3.1, the market fundamentals at equilibrium are given in Section 4.

Here, refers to the supplier’s realized – not expected – profit, i.e. . From Section 4, it is immediate that the total quantity that is sold to the market and the retail price are monotone in . Accordingly, we restrict attention on the behavior of as the distribution parameters vary.

To obtain a meaningful comparison between different markets, we assume throughout equilibrium uniqueness. Hence, unless stated otherwise, we consider only strictly DGRML distributions with finite second moment. Since the DGMRL is particulartly inclusive, see Le17 and Ba13 and finiteness of the second moment of the demand is naturally to assume, we do not consider them as restrictive. Still, since these conditions are only sufficient and not necessary, the analysis applies to any other setting that guarantees equilibrium existence and uniqueness.

4.1 Wholesale Price Determinants:

Although immediate from Theorem 3.1, the next Lemma showcases the importance of the characterization in (1). Let and denote two markets (or two instances of the same market) with demand distributions . As stated above, are assumed to be nonnegative, strictly DGMRL random variables with finite second moment. We then have

Lemma 1

Let denote the demand in two different market instances. If , then .

Proof

Since , we have that for all , by definition. Hence, by (1), , which implies that . Since is strictly decreasing by assumption, this implies that for all . Since is the unique solution of , this in turn implies that .

Hence, the supplier charges a larger wholesale price in a market that is larger in the -order. Based on Lemma 1, the task of studying the behavior of the wholesale price largerly reduces to finding sufficient conditions that imply – or that are equivalent to – the -order. Such conditions can be found in Sh07 , and are studied below.

Re-estimating Demand:

We start with the response of the equilibrium wholesale price to transformations that intuitively correspond to a larger market. Let denote the random demand in an instance of the market under consideration. Let be a positive constant. Moreover, let denote an additional source of demand that is independent of . Let denote the equilibrium wholesale price in the initial market and the equilibrium wholesale price in the market with random demand . How does compare to and to ?

While the intuition that the larger markets and will give rise to higher wholesale prices is largely confirmed, see Theorem 4.1, the results do not hold in full generality and one needs to pay attention to some technical details. For instance, since DGMRL random variables are not closed under convolution, see Le17 , the random variable may not be DGMRL. This may lead to a multiplicity of equilibrium prices in the instance, irrespectively of whether is DGMRL or not. To focus on the economic intepretation of the comparative static analysis and to avoid an extensive discussion on the technical conditions, we assume that is a random variable such that the market has again a unique wholesale equilibrium price. However, we consider this assumption as a restriction to the applicability of statement (ii) of Theorem 4.1.

Theorem 4.1

Let be a nonnegative DGMRL random variable with finite second moment which describes the demand distribution in a market instance.

-

(i)

If is a positive constant, then .

-

(ii)

If is a nonnegative random variable with finite second moment, independent of such that remains strictly DGMRL, then .

Proof

The proof of (i) follows directly from the preservation property of the -order that is stated Theorem 2.A.11 of Sh07 . Specifically, since is the mrl function of , we have that for all

where the inequality follows from the assumption that is DGMRL. Hence, which by Lemma 1 implies that .

Statement (ii) is more involved since may not be unique in general. However, under the assumption that remains strictly DGMRL, we may adapt Theorem 2.A.11 of Sh07 and obtain the claim in a similar fashion to part (i). Although Theorem 2.A.11 is stated for DMRL random variables, the proof extends in a straightforward way to DGMRL random variables.

Another way to treat the possible multiplicity of equilibrium wholesale prices in the market and the fact that may not be DGMRL is the following. Since, is strictly DGMRL, we know that for all . Together with , this implies that for all , the following holds: , and hence that for any such that (1) holds. Hence, in this case, we can compare the with every separately and obtain that is less than any possible equilibrium wholesale price in the market . However, as mentioned above, we prefer to restrict attention to markets that preserve equilibrium uniqueness.

Closure Properties:

Next, we turn our attention to operations that preserve the -order. Let denote two different instances of the market, i.e., two different demand distributions or beliefs about it, such that . In this case, we know that . We are interested in determining transformations of that preserve the -order and hence, by Lemma 1, the ordering . Again, to avoid technicalities, we assume that are such that Theorem 3.1 applies, i.e., that they are nonnegative, strictly DGMRL and have finite second moment.

Theorem 4.2

Let denote the demand in two different market instances, such that . Then,

-

(i)

If is an increasing convex function, then .

-

(ii)

If is a nonnegative, IFR random variable with finite second moment, independent of such that and remain strictly DGMRL, then .

-

(iii)

If is strictly DGMRL for some , then .

Proof

Statements (i) through (iii) follow directly from Theorems 2.A.19, Lemma 2.A.8 and Theorem 2.A.18 respectively. The assumption that the transformed random variables remain strictly DGMRL ensures equilibrium uniqueness.

If instead of , and are ordered in the weaker -order, i.e., if and is DMRL (instead of merely IFR), then Lemma 2.A.10 of Sh07 implies that statement (ii) of Theorem 4.2 remains true. Formally,

Corollary 1

Let denote the demand in two different market instances, such that . If is a nonnegative, IFR random variable with finite second moment, independent of such that and remain strictly DGMRL, then .

Following the exposition of Sh07 , the above collection of statements can be extended to incorporate more case-specific results.

Although Theorems 4.1 and 4.2 are immediate once Theorem 3.1 and Lemma 1 have been established, their implications in terms of the economic intuitions are non-trivial. In particular, both Theorems imply that if the supplier reestimates upwards her expectations about the demand then she will charge a higher price. However, this intuitive conclusion depends on the conditions that imply the -order and does not hold in general, as discussed in Subsection 4.1 below.

Market Demand Variability:

The response of the equilibrium wholesale price to increasing (decreasing) demand variability is less straightforward. There exist several notions of stochastic orders that compare random variables in terms of their variability and depending on which we employ, we may derive different results. First, we introduce some notation.

Variability or Dispersive Orders: Let and be two nonnegative random variables with equal means, , and finite second moments. If for all , then is said to be smaller than in the convex order, denoted by . If and denote the right continuous inverses of and for all , then is said to be smaller than in the dispersive order, denoted by . Finally, if for all , then is said to be smaller than in the excess wealth order, denoted by . Sh07 show that which in turn implies that . Further insights and motivation about these orders are provided in Chapter 3 of Sh07 .

Less Variability implies Lower Wholesale Price: Under our assumptions the -order is not implied by the -order. Hence, the -order is not enough to conclude that wholesale prices are ordered according to the respective market variability, i.e., that less (more) variability gives rise to lower (higher) wholesale prices. However, if we restrict attention to the and orders, then more can be said. Recall that denotes the left end of the support of a variable . Accordingly, we will write to denote the left end of the support of variable for .

Theorem 4.3

Let be two nonnegative, DGMRL random variables with which denote the demand in two different market instances. If either , or both are DMRL and , then .

Theorem 4.3 follows directly from Theorem 3.C.5 of Sh07 . Based on its proof, the assumption that at least one of the two random variables is DMRL (and not merely DGMRL) cannot be relaxed. Be16 argue about the restricted applicability of the -order due to the difficulty in the evaluation of incomplete integrals of quantile functions and provide useful characterizations of the -order to remedy this problem.

A result of similar flavor can be obtained if we use the order instead. Again, the condition that both and are DGMRL does not suffice and we need to assume that at least one is IFR.

Theorem 4.4

Let be two nonnegative, DGMRL random variables which denote the demand in two different market instances. If either , or both are IFR and , then .

Theorem 4.4 follows directly from Theorem 3.B.20 (b) of Sh07 and the fact that the -order implies the -order. Again, more case specific results can be drawn from the analysis of Sh07 .

The main insight that we get from Theorems 4.3 and 4.4 is that less (more) variability implies lower (higher) wholesale prices. This is in sharp contrast with the results of La01 and sheds light on the effects of demand uncertainty. If uncertainty affects the retailer, then the supplier charges a higher price and captures all supply chain profits as variability reduces. Contrarily, if uncertainty falls to the supplier, then the supplier charges a lower price as variability increases. In this case, the supplier captures a lower share of system profit, see also (2) below.

The above cases correspond to two extremes: in La01 uncertainty falls solely to the retailer, whereas in the present analysis uncertainty falls solely to the supplier. Based on the aggregate findings for the two cases, the following question naturally arises: is there a way to distribute demand uncertainty among supplier and retailers to mitigate its adverse effects and to evenly distribute supply chain profits among market participants? Answering this question exceeds the scope of the comparative statics analysis. However, it highlights a interesting direction for future work.

Parametric families of distributions: To further elaborate on the effects of relative variability on the wholesale price, we may compare our analysis with the approach of La01 . Given a random variable with distribution , La01 consider the random variables with and for . They conclude that in this case, the wholesale price is dictated by the coefficient of variation, . Specifically, if , then , i.e., in their model, a lower CV, or equivalently a lower relative variability, implies a higher price.

To establish a similar comparison, we utilize the comprehensive comparison of parametric distributions in terms of stochastic orders that is provided in Section 2.9 of Be16 . For instance, consider two normal random variables and . By Table 2.2 of Be16 , if and , then and hence, by Lemma 1, . However, by choosing and appropriately, we can achieve an arbitrary ordering of relative variability, i.e. of and . The reason is that the conclusions from this approach are obscured by the fact that changing for , does not only affect the ’s but also the central location of the demand distributions. In this sense, the approach using dispersive orders seems more appropriate because, under the assumption that , it isolates the effect of the variability of the distribution on wholesale prices via stochastic orderings.

Stochastically Larger Market:

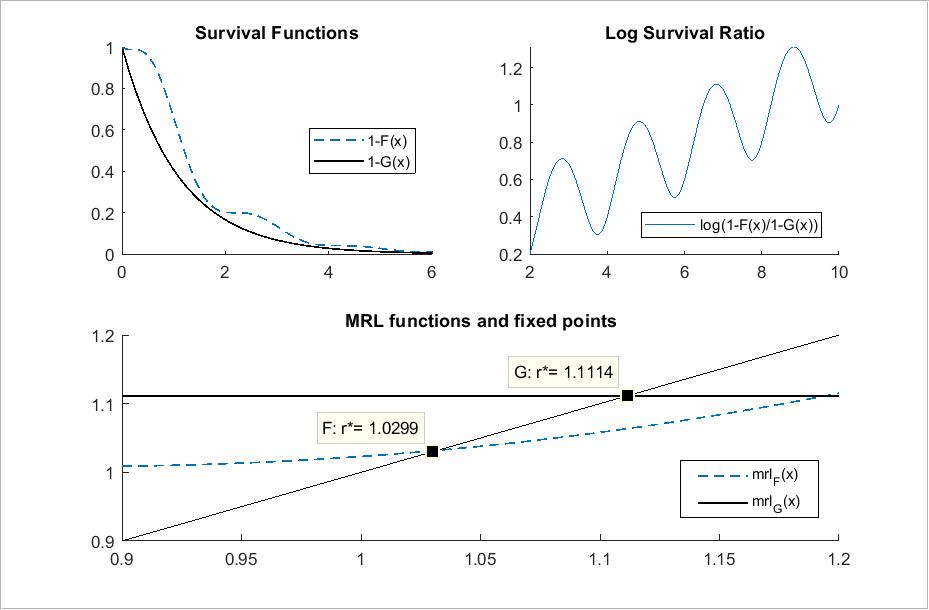

It is well known that the usual -order does not imply nor is implied by the -order, see Sh07 . This implies that in a stochastically larger market, the supplier may still charge a lower price, which is in line with the intuition of La01 that “size is not everything” and that prices are driven by different forces. Such an example is provided below. Let

for , denote the densities of a parametric family of exponentially decaying sinusoids. For , corresponds to the exponential distribution with parameter . Figure 1 depicts the survival functions , the log-survival ratio and the optimal wholesaleprices and for corresponding to and to .

Since the log-survival ratio remains throughout positive, we infer that . However, as shown in the graph below . Although, both functions have a unique fixed point, is not DMRL (nor DGMRL). Several simulations have not provided a conclusive answer to whether stochastic dominance implies also a larger price if we restrict to the DMRL (or DGMRL) class of random variables.

4.2 Supply Chain Performance:

We measure the supply chain performance in terms of the ratio which describes the division of the realized system profit between retailers and suppliers. If , then there is no transaction and the profits of all participants are equal to zero. For , we have that

| (2) |

Hence, the division of realized profit between supplier and retailers depends on the number of retailers and the wholesale price . Specifically, for a given realized demand , as or increase, the supplier captures a larger share of the system profits.

Supply Chain Efficiency:

As a benchmark, we will first determine the equilibrium behavior and performance of an integrated supply chain. Let denote the profit of an integrated firm. The integrated firms’ decision variable is now the retail price , and hence its expected profit is given by . By the same argument as in the proof of Theorem 3.1, is maximized at . In particular, the equilibrium price of both the integrated and non-integrated supplier is the same. Hence, the integrated firm’s realized profit in equilibrium is equal to .

In a similar fashion to Pe07 , we define the realized Price of Anarchy (PoA) of the system as the worst-case ratio of the realized profit of the centralized supply chain, , to the realized aggregate profit of the decentralized supply chain, . To retain equilibrium uniqueness, we restrict attention to the class of nonnegative DGMRL random variables. If the realized demand is less than , then both the centralized and decentralized chain make profits. Hence, we define the PoA as: . We then have

Theorem 4.5

The PoA of the system is given by

| (3) |

Proof

A direct substitution in the definition of PoA yields:

| (4) |

Since decreases in the ratio , the inner is attained asymptotically for . Hence, .

Theorem 4.5 implies that the supply chain becomes less efficient as the number of downstream retailers increases. Although the PoA provides a useful worst-case scenario, for a fixed and a realized demand , it is also of interest to study the response of the ratio to different wholesale prices. Specifically, for any given value of , and fixed , increases as the wholesale price increases. Hence, a higher wholesale price corresponds to worst efficiency for the decentralized chain.

Together with the observation that with a higher wholesale price, the supplier captures a larger share of the system profits, this motivates – from a social perspective – the study of mechanisms that will lead to reduced wholesale prices for fixed demand levels and fixed market characteristics (number of retailers and demand distribution). Such a study falls not within the topic of the present analysis but constitutes a promising direction for future research.

5 Conclusions

Along with Le17 , the present study provides a probabilistic and economic analysis that aims to extend the work of La01 , La06 , Pa05 and Ba13 .222The current paper and Bel18 contain preliminary results that appear in full length in Le18 ; Leo20 ; Leo21 ; Leon21 . The characterization, under mild conditions, of the supplier’s optimal pricing policy as the unique fixed point of the MRL function of the demand distribution, provides a powerful tool for a multifaceted comparative statics analysis. Theorems 4.1 and 4.2 demonstrate how stochastic orderings, coupled with this characterization, provide predictions of the response of the wholesale price in a versatile environment of various demand transformations. Based on a numerical example, Subsection 4.1 confirms La01 ’s intuition that prices are driven by different forces than market size. In Subsection 4.2 and Subsection 4.2, we show that number of second stage retailers and wholesale prices have a direct impact on supply chain performance and efficiency. A more extended version of the present study is subject of ongoing work.

References

- (1) Acemoglu, D., Jensen M. K. (2013): Aggregate Comparative Statics. Games and Economic Behavior, 81:27–49. doi:10.1016/j.geb.2013.03.009.

- (2) Athey, S. (2002): Monotone Comparative Statics under Uncertainty. The Quarterly Journal of Economics, 117(1):187–223. http://www.jstor.org/stable/2696486.

- (3) Banciu, M., Mirchandani P. (2013): Technical Note – New Results Concerning Probability Distributions with Increasing Generalized Failure Rates. Operations Research, 61(4):925–931. doi:10.1287/opre.2013.1198.

- (4) Belzunce, F., Martinez-Riquelme, C., Mulero J. (2016): An Introduction to Stochastic Orders (Chapter 2 – Univariate Stochastic Orders). Academic Press. doi:10.1016/B978-0-12-803768-3.00002-8.

- (5) Bernstein, F., Federgruen A. (2005): Decentralized Supply Chains with Competing Retailers Under Demand Uncertainty, Management Science, 51(1):18–29. doi:10.1287/mnsc.1040.0218.

- (6) Jensen M. K. (2018): Distributional Comparative Statics. The Review of Economic Studies, 85(1):581–610. doi:10.1093/restud/rdx021.

- (7) Lai, C.-D., Xie, M. (2006): Stochastic Ageing and Dependence for Reliability. Springer Science+Business Media, Inc. ISBN-10: 0-387-29742-1

- (8) Lariviere, M., Porteus, E. (2001): Selling to the Newsvendor: An Analysis of Price-Only Contracts. Manufacturing & Service Operations Management, 3(4):293–305. doi:10.1287/msom.3.4.293.9971.

- (9) Lariviere, M. (2006): A Note on Probability Distributions with Increasing Generalized Failure Rates. Operations Research, 54(3):602–604. doi:10.1007/978-1-4615-4949-9_8.

- (10) Leonardos, S., Melolidakis, C. (2020): Endogenizing the Cost Parameter in Cournot Oligopoly. International Game Theory Review, 22(02): 2040004. doi:10.1142/S0219198920400046.

- (11) Leonardos, S., Melolidakis, C. (2020): A Class of Distributions for Linear Demand Markets. arXiv e-prints. https://arxiv.org/abs/1805.06327.

- (12) Leonardos, S., Melolidakis, C. (2020): On the Equilibrium Uniqueness in Cournot Competition with Demand Uncertainty. The B.E. Journal of Theoretical Economics, 20(02): 20190131. doi:10.1515/bejte-2019-0131.

- (13) Leonardos, S., Melolidakis, C. (2021): On the Mean Residual Life of Cantor-Type Distributions: Properties and Economic Applications. Austrian Journal of Statistics, 50(04): 65–77. doi:10.17713/ajs.v50i4.1118.

- (14) Leonardos, S., Melolidakis, C., Koki C. (2021): Monopoly Pricing in Vertical Markets with Demand Uncertainty. Annals of Operations Research, 22 April. doi:10.1007/s10479-021-04067-3.

- (15) Melolidakis, C., Leonardos, S., Koki, C. (2018): Measuring Market Performance with Stochastic Demand: Price of Anarchy and Price of Uncertainty, in Belief Functions: Theory and Applications, Springer International Publishing, 163–171. doi:10.1007/978-3-319-99383-6_21.

- (16) Pan, K., Lai, K.K., Liang L., Leung S. (2009): Two-period pricing and ordering policy for the dominant retailer in a two-echelon supply chain with demand uncertainty. Omega, 36(4): 919–929. doi:10.1016/j.omega.2008.08.002.

- (17) Paul, A. (2005): A Note on Closure Properties of Failure Rate Distributions. Operations Research, 53(4):733–734. doi:10.1287/opre.1040.0206.

- (18) Perakis, G., Roels, G. (2007): The Price of Anarchy in Supply Chains: Quantifying the Efficiency of Price-Only Contracts. Management Science, 53(8):1249–1268. doi:10.1287/mnsc.1060.0656.

- (19) Shaked, M., Shanthikumar, G. (2007): Stochastic Orders. Springer Series in Statistics, New York. ISBN 0-387-32915-3.

- (20) Wu, C.-H., Chen, C.-W., Hsieh, C.-C. (2012): Competitive pricing decisions in a two-echelon supply chain with horizontal and vertical competition. International Journal of Production Economics, 135(1):265–274. doi:10.1016/j.ijpe.2011.07.020.

- (21) Yang, S.-L., Zhou, Y.-W. (2006): Two-echelon supply chain models: Considering duopolistic retailers’ different competitive behaviors. International Journal of Production Economics, 103(1): 104–116. doi:doi.org/10.1016/j.ijpe.2005.06.001.