A Term Structure Model for Dividends and Interest Rates111We thank participants at the Workshop on Dynamical Models in Finance in Lausanne, the 8th General Advanced Mathematical Methods in Finance conference in Amsterdam, the 2nd International Conference on Computational Finance in Lisbon, the 11th Actuarial and Financial Mathematics Conference in Brussels, the 2018 Swiss Finance Institute Research Days in Gerzensee, the 10th Bachelier World Congress in Dublin, the 2018 Young Researchers Workshop on Data-Driven Decision Making at Cornell University, the 2019 Cambridge-Lausanne workshop, and seminars at McMaster University, New York University, Princeton University, UC Berkely, and University College Dublin, as well as Peter Carr, Jérôme Detemple (discussant), Alexey Ivashchenko (discussant), Martin Lettau, Chris Rogers (discussant), Radu Tunaru, and three anonymous referees for their comments. The research leading to these results has received funding from the European Research Council under the European Union’s Seventh Framework Programme (FP/2007-2013) / ERC Grant Agreement n. 307465-POLYTE.

forthcoming in Mathematical Finance)

Abstract

Over the last decade, dividends have become a standalone asset class instead of a mere side product of an equity investment. We introduce a framework based on polynomial jump-diffusions to jointly price the term structures of dividends and interest rates. Prices for dividend futures, bonds, and the dividend paying stock are given in closed form. We present an efficient moment based approximation method for option pricing. In a calibration exercise we show that a parsimonious model specification has a good fit with Euribor interest rate swaps and swaptions, Euro Stoxx 50 index dividend futures and dividend options, and Euro Stoxx 50 index options.

JEL Classification: C32, G12, G13

MSC2010 Classification: 91B70, 91G20, 91G30

Keywords: Dividend derivatives, interest rates, polynomial jump-diffusion, term structure, moment based option pricing

1 Introduction

In recent years there has been an increasing interest in trading derivative contracts with a direct exposure to dividends. Brennan (1998) argues that a market for dividend derivatives could promote rational pricing in stock markets. In the over-the-counter (OTC) market, dividends have been traded since 2001 in the form of dividend swaps, where the floating leg pays the dividends realized over a predetermined period of time. The OTC market also accommodates a wide variety of more exotic dividend related products such as knock-out dividend swaps, dividend yield swaps and swaptions. Dividend trading gained significant traction in late 2008, when Eurex launched exchange traded futures contracts referencing the dividends paid out by constituents of the Euro Stoxx 50. The creation of a futures market for other major indices (e.g., the FTSE 100 and Nikkei 225) followed shortly after, as well as the introduction of exchange listed options on realized dividends with maturities of up to ten years. Besides the wide variety of relatively new dividend instruments, there is another important dividend derivative that has been around since the inception of finance: a simple dividend paying stock. Indeed, a share of stock includes a claim to all the dividends paid over the stock’s lifetime. Any pricing model for dividend derivatives should therefore also be capable of efficiently pricing derivatives on the stock paying the dividends. What’s more, the existence of interest rate-dividend hybrid products, the relatively long maturities of dividend options, and the long duration nature of the stock all motivate the use of stochastic interest rates. Despite its apparent desirability, a tractable joint model for the term structures of interest rates and dividends, and the corresponding stock, has been missing in the literature to date.

We fill this gap and develop an integrated framework to efficiently price derivatives on dividends, stocks, and interest rates. We first specify dynamics for the dividends and discount factor, and in a second step we recover the stock price in closed form as the sum of the fundamental stock price (present value of all future dividends) and possibly a residual bubble component. The instantaneous dividend rate is a linear function of a multivariate factor process. The interest rates are modeled by directly specifying the discount factor to be linear in the factors, similarly as in Filipović et al. (2017). The factor process itself is specified as a general polynomial jump-diffusion, as studied in Filipović and Larsson (2020). Such a specification makes the model tractable because all the conditional moments of the factors are known in closed form. In particular, we have closed form expressions for the stock price and the term structures of dividend futures and interest rate swaps. Any derivative whose discounted payoff can be written as a function of a polynomial in the factors is priced through a moment matching method. Specifically, we find the unique probability density function with maximal Boltzmann-Shannon entropy matching a finite number of moments of the polynomial, as in Mead and Papanicolaou (1984). We then obtain the price of the derivative by numerical integration. In particular, this allows us to price swaptions, dividend options, and options on the dividend paying stock. We show that our polynomial framework also allows to incorporate seasonal behavior in the dividend dynamics.

Within our polynomial framework, we introduce the linear jump-diffusion (LJD) model. We show that the LJD model allows for a flexible dependence structure between the factors. This is useful to model a dependence between dividends and interest rates, but also to model the dependence within the term structure of interest rates or dividends. We calibrate a parsimonious specification of the LJD model to market data on Euribor interest rate swaps and swaptions, Euro Stoxx 50 index dividend futures and dividend options, and Euro Stoxx 50 index options. Our model reconciles the relatively large implied volatility of the index options with the relatively small implied volatility of dividend options and swaptions through a negative correlation between dividends and interest rates. The successful calibration of the model to three different classes of derivatives (interest rates, dividends, and equity) illustrates the high degree of flexibility offered by our framework.

Our paper is related to various strands of literature. In the literature on stock option pricing, dividends are often assumed to be either deterministic (e.g., Bos and Vandermark (2002), Bos et al. (2003), Vellekoop and Nieuwenhuis (2006)), a constant fraction of the stock price (e.g., Merton (1973), Korn and Rogers (2005)), or a combination of the two (e.g., Kim (1995), Overhaus et al. (2007)). Geske (1978) and Lioui (2006) model dividends as a stochastic fraction of the stock price. They derive Black-Scholes type of equations for European option prices, however dividends are not guaranteed to be non-negative in both setups. Chance et al. (2002) directly specify log-normal dynamics for the -forward price of the stock, with the maturity of the option. Closed form option prices are obtained as in Black (1976), assuming that today’s -forward price is observable. This approach is easy to use since it does not require any modeling assumptions on the distribution of the dividends. However, it does not produce consistent option prices for different maturities. Bernhart and Mai (2015) take a similar approach, but suggest to fix a time horizon long enough to encompass all option maturities to be priced. The -forward price is modeled with a non-negative martingale and the stock price is defined as the -forward price plus the present value of dividends from now until time . As a consequence, prices of options with maturity smaller than will depend on the joint distribution between future dividend payments and the -forward price, which is not known in general. Bernhart and Mai (2015) resort to numerical tree approximation methods in order to price options. The dependence of their model on a fixed time horizon still leads to time inconsistency, since the horizon will necessarily have to be extended at some point in time. We contribute to this literature by building a stock option pricing model that guarantees non-negative dividends, is time consistent, and remains tractable.

Another strand of literature studies stochastic models to jointly price stock and dividend derivatives. Buehler et al. (2010) assumes that the stock price jumps at known dividend payment dates and follows log-normal dynamics in between the payment dates. The jump amplitudes are driven by an Ornstein-Uhlenbeck process such that the stock price remains log-normally distributed and the model has closed form prices for European call options on the stock. The high volatility in the stock price is reconciled with the low volatility in dividend payments by setting the correlation between the Ornstein-Uhlenbeck process and the stock price extremely negative (). A major downside of the model is that dividends can be negative. Moreover, although the model has a tractable stock price, the dividends themselves are not tractable and Monte-Carlo simulations are required to price the dividend derivatives. In more recent work, Buehler (2015) decomposes the stock price in a fundamental component and a residual bubble component. The dividends are defined as a function of a secondary driving process that mean reverts around the residual bubble component. This model has closed form expressions for dividend futures, but Monte-Carlo simulations are still necessary to price nonlinear derivatives. Guennoun and Henry-Labordère (2017) consider a stochastic local volatility model for the pricing of stock and dividend derivatives. Their model guarantees a perfect fit to observed option prices, however all pricing is based on Monte-Carlo simulations. Tunaru (2018) proposes two different models to value dividend derivatives. The first model is similar to the one of Buehler et al. (2010), but models the jump amplitudes with a beta distribution. This guarantees positive dividend payments. However, the diffusive noise of the stock is assumed independent of the jump amplitudes in order to have tractable expressions for dividend futures prices. Smoothing the dividends through a negative correlation between stock price and jump amplitudes, as in Buehler et al. (2010), is therefore not possible. In a second approach, Tunaru (2018) directly models the cumulative dividends with a diffusive logistic growth process. This process has, however, no guarantee to be monotonically increasing, meaning that negative dividends can occur frequently. Willems (2019b) jointly specifies dynamics for the stock price and the dividend rate such that the stock price is positive and the dividend rate is a non-negative process mean-reverting around a constant fraction of the stock price. The model of Willems (2019b) is in fact a special case of the general framework introduced in our paper, although it is different from the LJD model and does not incorporate stochastic interest rates. We add to this literature by allowing for stochastic interest rates, which is important for the valuation of interest rate-dividend hybrid products or long-dated dividend derivatives (e.g., the dividend paying stock). Our model produces closed form prices for dividend futures and features efficient approximations for option prices which are significantly faster than Monte-Carlo simulations. In particular, we give an example of a hybrid option on the dividend-interest rate spread that can be priced efficiently in our framework. The low volatility in dividends and interest rates is reconciled with the high volatility in the stock price through a negative correlation between dividends and interest rates.

Our work also relates to literature on constructing an integrated framework for dividends and interest rates. Previous approaches were mainly based on affine processes, see e.g. Bekaert and Grenadier (1999), Mamaysky et al. (2002), d’Addona and Kind (2006), Lettau and Wachter (2007, 2011), and Lemke and Werner (2009). In more recent work, Kragt et al. (2020) extract investor information from dividend derivatives by estimating a two-state affine state space model on stock index dividend futures in four different stock markets. Instead of modeling dividends and interest rates separately, they choose to model dividend growth, a risk-free discount rate, and a risk premium in a single variable called the ‘discounted risk-adjusted dividend growth rate’. Yan (2014) uses zero-coupon bond prices and present value claims to dividend extracted from the put-call parity relation to estimate an affine term structure model for interest rates and dividends. Suzuki (2014) uses a Nelson-Siegel approach to estimate the fundamental value of the Euro Stoxx 50 using dividend futures and Euribor swap rates. We add to this literature by building an integrated framework for dividends and interest rates using the class of polynomial processes, which contains the traditional affine processes as a special case.

Finally, our work also relates to literature on moment based option pricing. Jarrow and Rudd (1982), Corrado and Su (1996b), and Collin-Dufresne and Goldstein (2002b) use Edgeworth expansions to approximate the density function of the option payoff from the available moments. Closely related are Gram-Charlier expansions, which are used for option pricing for example by Corrado and Su (1996a), Jondeau and Rockinger (2001), and Ackerer et al. (2018). Although these series expansions allow to obtain a function that integrates to one and matches an arbitrary number of moments by construction, it has no guarantee to be positive. In this paper, we find the unique probability density function with maximal Boltzmann-Shannon entropy. subject to a finite number of moment constraints. Option prices are then obtained by numerical integration. A similar approach is taken by Fusai and Tagliani (2002) to price Asian options. The principle of maximal entropy has also been used to extract the risk-neutral distribution from option prices, see e.g. Buchen and Kelly (1996), Jackwerth and Rubinstein (1996), Avellaneda (1998), and Rompolis (2010). There exist many alternatives to maximizing the entropy in order to find a density function satisfying a finite number of moment constraints. For example, one can maximize the smoothness of the density function (see e.g., Jackwerth and Rubinstein (1996)) or directly maximize (minimize) the option price itself to obtain an upper (lower) bound on the price (see e.g., Lasserre et al. (2006)). A comparison of different approaches is beyond the scope of this paper.

The remainder of the paper is structured as follows. Section 2 introduces the factor process and discusses the pricing of dividend futures, bonds, and the dividend paying stock. In Section 3 we explain how to efficiently approximate option prices using maximum entropy moment matching. Section 4 describes the LJD model. In Section 5 we calibrate a parsimonious model specification to real market data. Section 6 discusses some extensions of the framework. Section 7 concludes. All proofs and technical details can be found in the appendix.

2 Polynomial framework

We consider a financial market modeled on a filtered probability space where is a risk-neutral pricing measure. Henceforth denotes the -conditional expectation. We model the uncertainty in the economy through a factor process taking values in some state space .444We assume that has non-empty interior. We assume that is a polynomial jump-diffusion (cfr. Filipović and Larsson (2020)) with dynamics

| (1) |

for some parameters , , and some -dimensional martingale such that the generator of maps polynomials to polynomials of the same degree or less. One of the main features of polynomial jump-diffusions is the fact that they admit closed form conditional moments. For , denote by the space of of polynomials on of degree or less and denote its dimension by .555Since the interior of is assumed to be non-empty, can be identified with and therefore . Let form a polynomial basis for and denote . Since leaves invariant, there exists a unique matrix representing the action of on with respect to the basis . Without loss of generality we assume to work with the monomial basis.

Example 2.1.

If , then we have and becomes

| (2) |

From the invariance property of , one can derive the moment formula (Theorem 2.4 in Filipović and Larsson (2020))

| (3) |

for all . Many efficient algorithms exist to numerically compute the matrix exponential (e.g., Al-Mohy and Higham (2011)).

2.1 Dividend futures

Consider a stock that pays a continuous dividend stream to its owner at an instantaneous rate , which varies stochastically over time. We model the cumulative dividend process as:

| (4) |

for some parameters and such that is a positive, non-decreasing, and absolutely continuous (i.e., drift only) process. This specification for implicitly pins down , which is shown in the following proposition.

Proposition 2.2.

Remark that both the instantaneous dividend rate and the cumulative dividends load linearly on the factor process. The exponential scaling of with parameter can be helpful to guarantee a non-negative instantaneous dividend rate. Indeed, if

| (6) |

is finite, then it follows from (5) that if and only if .666We calculate explicitly for the linear jump-diffusion model studied in Section 4. Moreover, when all eigenvalues of have positive real parts, it follows from the moment formula (3) that

The parameter therefore controls the asymptotic risk-neutral expected growth rate of the dividends.

The time- price of a continuously marked-to-market futures contract referencing the dividends to be paid over a future time interval with expiry date , , is given by:

| (7) |

where we have used the moment formula (3) in the last equality. Hence, the dividend futures price is linear in the factor process. Note that the dividend futures term structure (i.e., the dividend futures prices for varying and ) does not depend on the specification of the martingale part of .

2.2 Bonds and swaps

Denote the risk-neutral discount factor by . It is related to the short rate as follows

We directly specify dynamics for the risk-neutral discount factor:

| (8) |

for some parameters and such that is a positive and absolutely continuous process. This is similar to the specification (4) of but, in order to allow for negative interest rates, we do not require to be monotonic (non-increasing). Filipović et al. (2017) follow a similar approach and specify linear dynamics for the state price density with respect to the historical probability measure . Their specification pins down the market price of risk. It turns out that the polynomial property of the factor process is not preserved under the change of measure from to in this case. However, as seen in (7), the polynomial property (in particular the linear drift) under is important for pricing the dividend futures contracts.

The time- price of a zero-coupon bond paying one unit of currency at time is given by:

Using the moment formula (3) we get a linear-rational expression for the zero-coupon bond price

| (9) |

Remark that the term structure of zero-coupon bond prices depends only on the drift of . Similarly as in Filipović et al. (2017), one can introduce exogenous factors feeding into the martingale part of to generate unspanned stochastic volatility (see e.g., Collin-Dufresne and Goldstein (2002a)), however we do not consider this in our paper.

Using the relation , we obtain the following linear-rational expression for the short rate:

When all eigenvalues of have positive real parts, it follows that

so that can be interpreted as the yield on the zero-coupon bond with infinite maturity.

Ignoring differences in liquidity and credit characteristics between discount rates and IBOR rates, we can value swap contracts as linear combinations of zero-coupon bond prices. The time- value of a payer interest rate swap with first reset date , fixed leg payment dates , and fixed rate is given by:

| (10) |

with , . The forward swap rate is defined as the fixed rate which makes the right hand side of (10) equal to zero. Note that the discounted swap value becomes a linear function of , which will be important for the purpose of pricing swaptions.

2.3 Dividend paying stock

Denote by the fundamental price of the stock, which we define as the present value of all future dividends:

| (11) |

In order for to be finite in our model, we must impose parameter restrictions. The following proposition provides sufficient conditions on the parameters, together with a closed form expression for . The latter is derived using the fact that is quadratic in , hence we are able to calculate its conditional expectation through the moment formula (3).

Proposition 2.3.

If the real parts of the eigenvalues of are bounded above by , then is finite and given by

| (12) |

where and is the unique coordinate vector satisfying

Proposition 2.3 shows that the discounted fundamental stock price is quadratic in , which means in particular that we have all moments of in closed form. Loosely speaking, the fundamental stock price will be finite as long as the dividends are discounted at a sufficiently high rate (by choosing sufficiently large). Henceforth we will assume that the assumption of Proposition 2.3 is satisfied.

The following proposition shows how the price of the dividend paying stock, which we denote by , is related to the fundamental stock price.777This relationship has been highlighted in particular by Buehler (2010, 2015) in the context of derivative pricing.

Proposition 2.4.

The market is arbitrage free if and only if is of the form

| (13) |

with a non-negative local martingale.

The process can be interpreted as a bubble in the sense that it drives a wedge between the fundamental stock price and the observed stock price. If is continuous, then applying Itô’s lemma to (13) and using the fact that is assumed to be absolutely continuous, we obtain the following risk-neutral stock price dynamics

| (14) |

where denotes the Jacobian of .888A similar, but lengthier, expression can be derived in case there are jumps in . We choose to omit it since it does not add much value to the discussion that follows. Remark that has the correct risk-neutral drift, by construction. Given dynamics for and , an alternative approach to model for derivative pricing purposes would have been to directly specify its martingale part. With such an approach, however, it is not straightforward to guarantee a positive stock price. Indeed, the downward drift of the instantaneous dividend rate could push the stock price in negative territory.999Instead of starting from dynamics for , we could have specified dynamics for the dividend yield . This would help to keep the stock price positive, but it does typically not produce a tractable distribution for . This is problematic since dividend derivatives reference notional dividend payments paid out over a certain time period. Moreover, by directly specifying the martingale part of the stock price, we are implicitly modeling a bubble because the stock price will be greater than the present value of all future dividends in general. In contrast, our approach implies a martingale part (the second term in (14)) that guarantees a positive stock price. This martingale part is completely determined by the given specification for dividends and interest rates. In case this is too restrictive for the stock price dynamics, one can always adjust accordingly through the specification of the non-negative local martingale . For example, Buehler (2015) considers a local volatility model on top of the fundamental stock price that is separately calibrated to equity option prices.

Remark 2.5.

Bubbles are usually associated with strict local martingales, see e.g. Cox and Hobson (2005). In fact, for economies with a finite time horizon, a bubble is only possible if the deflated gains process is a strict local martingale, which corresponds to a bubble of Type 3 according to the classification of Jarrow et al. (2007). For economies with an infinite time horizon, which is the case in our setup, bubbles are possible even if the deflated gains process is a true martingale. Such bubbles are of Type 1 and 2 in the classification Jarrow et al. (2007). Specifically, a (uniformly integrable) martingale corresponds to a bubble of Type 2 (Type 1).

The -forward stock price at time is defined as

If is a true martingale, then we can compute explicitly in our framework using the moment formula (3)

We finish this section with a result on the duration of the stock. We define the stock duration as

| (15) |

The stock duration represents a weighted average of the time an investor has to wait to receive his dividends, where the weights are the relative contribution of the present value of the dividends to the fundamental stock price. This definition is the continuous time version of the one used by Dechow et al. (2004) and Weber (2018). The following proposition gives a closed form expression for stock duration in our framework.

Proposition 2.6.

The stock duration is given by

| (16) |

3 Option pricing

In this section we address the problem of pricing derivatives with discounted payoff functions that are not polynomials in the factor process. The polynomial framework no longer allows to price such derivatives in closed form. However, we can accurately approximate the prices using the available moments of the factor process.

3.1 Maximum entropy moment matching

In all examples encountered below, we consider a derivative maturing at time whose discounted payoff is given by , for some , , and some function . The time- price of this derivative is given by

| (17) |

If the conditional distribution of the random variable were available in closed form, we could compute by integrating over the real line. In general, however, we are only given all the conditional moments of the random variable . We thus aim to construct an approximative probability density function matching a finite number of these moments. In a second step we approximate the option price through numerically integrating with respect to . Given that a function is an infinite dimensional object, finding such a function is clearly an underdetermined problem and we need to introduce additional criteria to pin down one particular function. A popular choice in the engineering and physics literature is to choose the density function with maximum entropy:

| (18) |

where denotes the support and denote the first moments of . Jaynes (1957) motivates such a choice by noting that maximizing entropy incorporates the least amount of prior information in the distribution, other than the imposed moment constraints. In this sense it is maximally noncommittal with respect to unknown information about the distribution.

Straightforward functional variation with respect to gives the following solution to this optimization problem:

where the Lagrange multipliers have to be solved from the moment constraints:

| (19) |

If and , then we recover the uniform distribution. For and we obtain the exponential distribution, while for and we obtain the Gaussian distribution. For , one needs to solve the system in (19) numerically, which involves evaluating the integrals numerically.101010 Directly trying to find the roots of this system might not lead to satisfactory results. A more stable numerical procedure is obtained by introducing the following potential function: . This function can easily be shown to be everywhere convex (see e.g., Mead and Papanicolaou (1984)) and its gradient corresponds to the vector of moment conditions in (19). In other words, the Lagrange multipliers can be found by minimizing the potential function . This is an unconstrained convex optimization problem where we have closed form (up to numerical integration) expressions for the gradient and hessian, which makes it a prototype problem to be solved with Newton’s method. We refer to the existing literature for more details on the implementation of maximum entropy densities, see e.g. Agmon et al. (1979), Mead and Papanicolaou (1984), Rockinger and Jondeau (2002), and Holly et al. (2011).

Remark 3.1.

By subsequently combining the law of iterated expectations and the moment formula (3), we are also able to compute the conditional moments of the finite dimensional distributions of . In particular, the method described in this section can also be applied to price path-dependent derivatives whose discounted payoff depends on the factor process at a finite number of future time points. One example of such products are the dividend options, which will be discussed below.

3.2 Swaptions, stock and dividend options

The time- price of a payer swaption with expiry date , which gives the owner the right to enter into a (spot starting) payer swap at , is given by:

where we have used (9) in the last equality. Observe that the discounted payoff of the swaption is of the form in (17) with and is a polynomial of degree one in .

The time- price of a European call option on the dividend paying stock with strike and expiry date is given by

| (20) |

where we have used (12) in the last equality. If is jointly a polynomial jump-diffusion, we can compute all moments of the random variable and proceed as explained in Section 3.1.

Remark 3.2.

If one assumes independence between the processes and , then the assumption that must jointly be a polynomial jump-diffusion is not necessarily needed. Indeed, suppose is specified such that we can compute efficiently. By the law of iterated expectations we have

where we define . The numerator in the above expression is now of the form in (17) and we proceed as before.

Consider next a European call option on the dividends realized in , expiry date , and strike price . This type of options are actively traded on the Eurex exchange where the Euro Stoxx 50 dividends serve as underlying. The time- price of this product is given by

We can compute in closed form all the moments of the scalar random variable

by subsequently applying the law of iterated expectations and the moment formula (3), see Remark 3.1. We then proceed as before by finding the maximum entropy density corresponding to these moments and computing the option price by numerical integration.

3.3 Interest rate-dividend hybrid option

We describe in this section an interest rate-dividend hybrid derivative that gives direct exposure to dividend payments and interest rate movements. Consider a tenor structure . At time , , the derivative pays the positive part of the difference between the dividends realized over , normalized by the -forward stock price, and the in-arrears compounded risk-free rate augmented with a constant spread :

where we define the in-arrears compounded risk-free rate as

This payoff structure is particularly relevant in the context of the transition of LIBOR to alternative risk-free rates (ARFRs), where term rates are constructed by compounding daily fixings of a benchmark rate based on overnight rates. In our setting, we proxy the overnight rate by the short rate and the daily compounding by continuous compounding.

The price at time is given by

We can compute in closed form all the -conditional moments of the scalar random variables

by subsequently applying the law of iterated expectations and the moment formula (3), see Remark 3.1. We then proceed as before by finding the maximum entropy density corresponding to these moments and computing the option price by numerical integration.

4 The linear jump-diffusion model

In this section we give a worked-out example of a factor process that fits in the polynomial framework of Section 2. In the following, if then denotes the diagonal matrix with on its diagonal. If , then we denote .

The linear jump-diffusion (LJD) model assumes the following dynamics for the factor process

| (21) |

where is a standard -dimensional Brownian motion, is a lower triangular matrix with non-negative entries on its main diagonal, is a compensated compound Poisson process with arrival intensity and a jump distribution that admits moments of all orders.111111For simplicity we assume a compound Poisson process with a single jump intensity, however this can be generalized (see Filipović and Larsson (2020)). Both the jump amplitudes and the Poisson jumps are assumed to be independent from the diffusive noise. The purely diffusive LJD specification (i.e., ) has appeared in various financial contexts such as stochastic volatility (Nelson (1990), Barone-Adesi et al. (2005)), energy markets (Pilipović (1997)), interest rates (Brennan and Schwartz (1979)), and Asian option pricing (Linetsky (2004), Willems (2019a)). The extension with jumps has not received much attention yet.

The following proposition verifies that is indeed a polynomial jump-diffusion and also shows how to choose parameters such that has positive components.

Proposition 4.1.

Assume that matrix has non-positive off-diagonal elements, , , and has support . Then for every initial value there exists a unique strong solution to (21) with values in . Moreover, is a polynomial jump-diffusion.

We will henceforth assume that the assumptions of Proposition 4.1 are satisfied, as it allows to derive parameter restrictions to guarantee , , and . In order to have and for all , the vectors and must have non-negative components with at least one component different from zero. The following proposition introduces a lower bound on such that .

Proposition 4.2.

Let and denote . Assume that at least one of the is non-zero, so that dividends are not deterministic. Without loss of generality we assume and , for some . If we denote by the -th column of , then we have if and only if

| (22) |

The LJD model allows a flexible instantaneous correlation structure between the factors through the matrix . This is in contrast to non-negative affine jump-diffusions, a popular choice in term structure modeling when non-negative factors are required, see, e.g., Duffie et al. (2003). Indeed, as soon as one introduces a non-zero instantaneous correlation between the factors of a non-negative affine jump-diffusion, the affine (and polynomial) property is lost. Correlation between factors can be used to incorporate a dependence between the term structures of interest rates and dividends, but also to model a dependence within a single term structure. The LJD model also allows for state-dependent, positive and negative, jump sizes of the factors. This again is in contrast to non-negative affine jump-diffusions.

The following proposition provides the eigenvalues of the corresponding matrix under the assumption of a triangular form for . Combined with Proposition 2.3, this gives sufficient conditions to guarantee a finite stock price in the LJD model.

Proposition 4.3.

If is a triangular matrix, then the eigenvalues of the matrix are

The eigenvalues of coincide with the values on the first line.

5 Numerical study

In this section we calibrate a parsimonious LJD model specification using daily market data from February to April 2015 obtained from Bloomberg. The purpose of this calibration exercise is to show that a parsimonious model specification is capable of reproducing derivative prices observed in the market. We do not specify the dynamics of the model under the historical probability measure. Hence, we do not study the evolution of risk-premia over time and focus solely on the risk-neutral pricing of derivatives. We leave a study of risk-premia for future research.

5.1 Data description

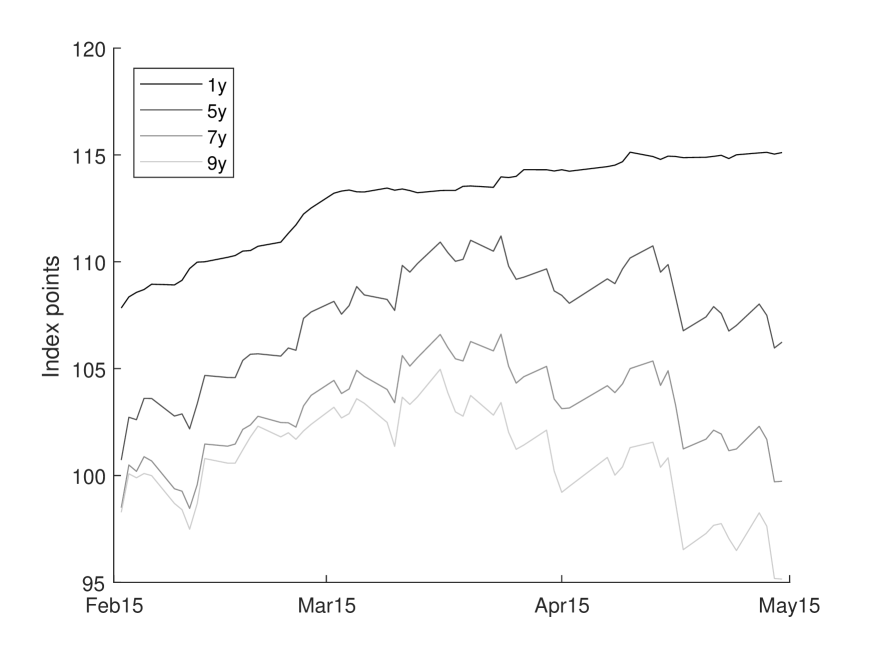

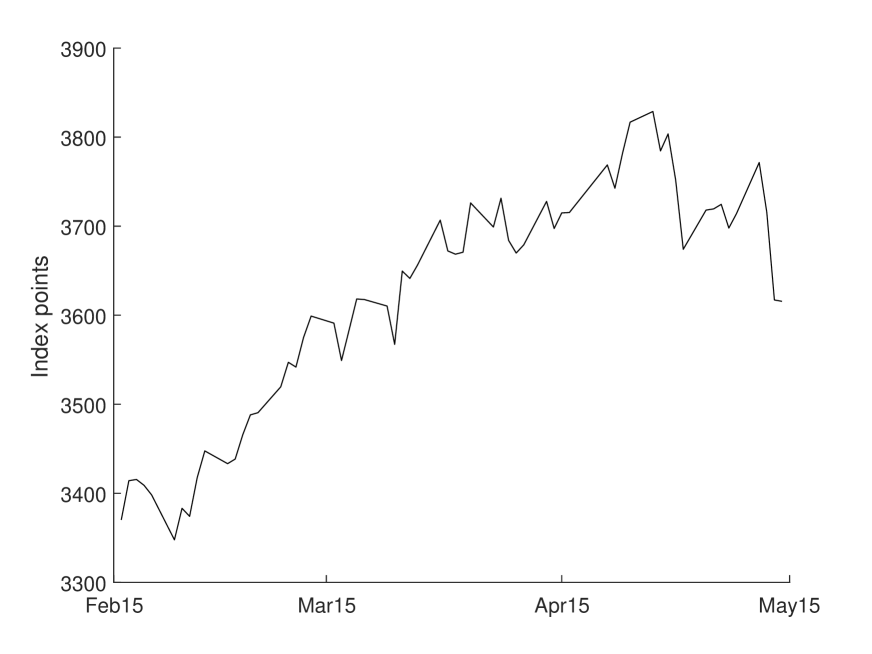

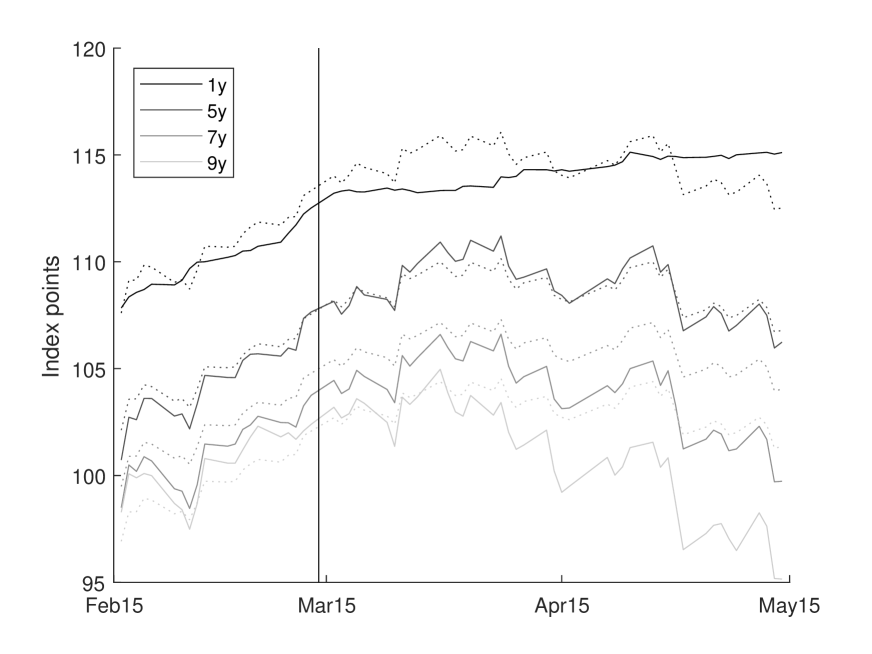

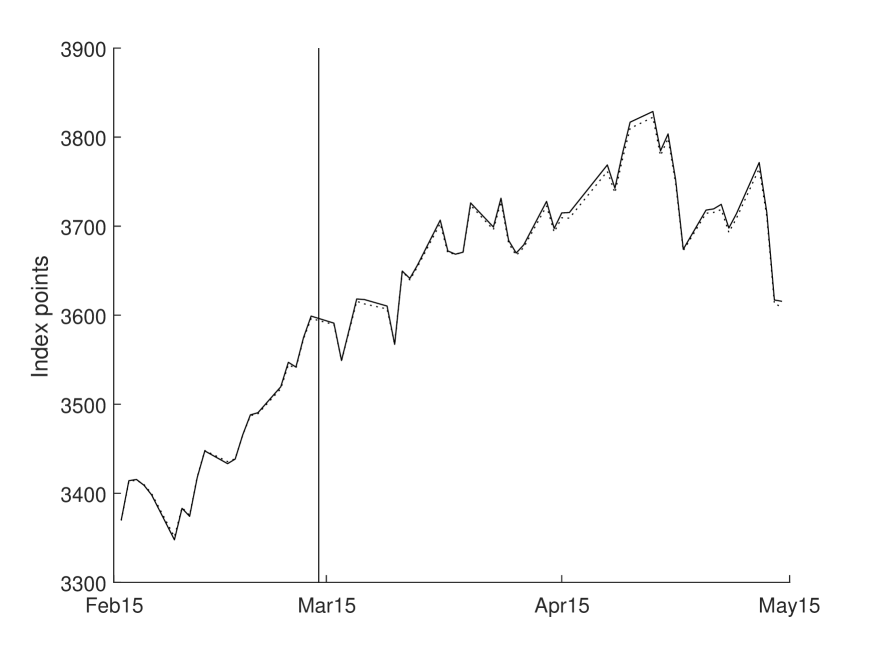

The dividend paying stock in our calibration study is the Euro Stoxx 50, the leading blue-chip stock index in the Eurozone. The index is composed of fifty stocks of sector leading companies from twelve Eurozone countries. We choose to focus on the European market because the dividend futures contracts on the Euro Stoxx 50 are the most liquid in the world and have been around longer than in any other market. Kragt et al. (2020) report an average daily turnover of more than EUR 150 million for all expiries combined. The Euro Stoxx 50 dividend futures contracts are traded on Eurex and reference the sum of the declared ordinary gross cash dividends (or cash-equivalent, e.g. stock dividends) on index constituents that go ex-dividend during a given calendar year, divided by the index divisor on the ex-dividend day. Corporate actions that cause a change in the index divisor are excluded from the dividend calculations, e.g. special and extraordinary dividends, return of capital, stock splits, etc. On every day of the sample there are ten annual contracts available for trading with maturity dates on the third Friday of December. Specifically, the -th to expire contract, , references the dividends paid between the third Friday of December and the third Friday of December . We interpolate adjacent dividend futures contracts using the approach of Kragt et al. (2020) to construct contracts with a constant time to maturity of 1 to 9 years.121212We could also calibrate the model without doing any interpolation of the data. However, in order to make the fitting errors of the sequential calibrations more comparable over time, we choose to interpolate all instruments such that they have a constant time to maturity. In the calibration we use the contracts with maturities in 1, 2, 3, 4, 5, 7, and 9 years. Figure 1(a) plots the interpolated dividend futures prices with 1, 5, 7, and 9 years to maturity.

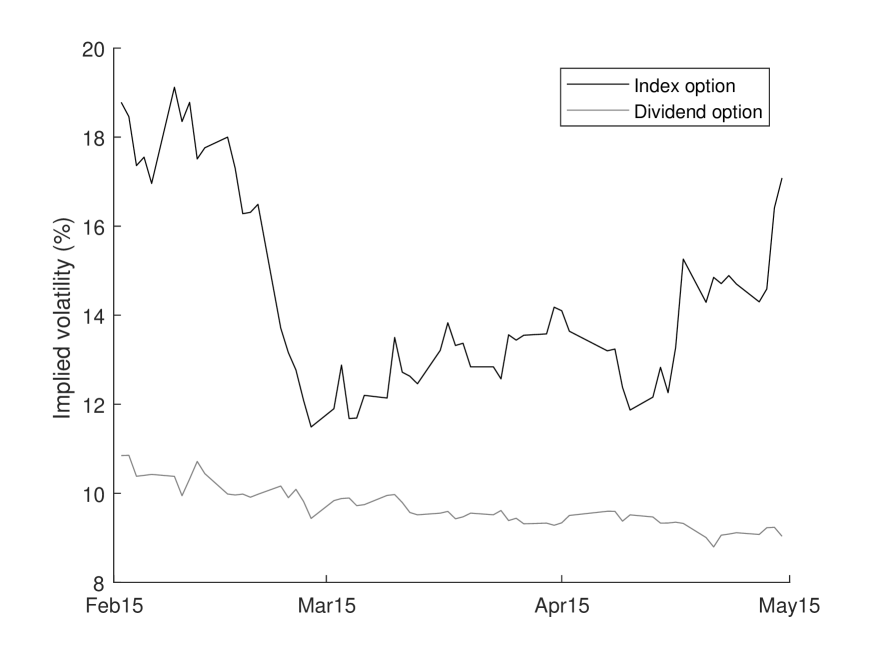

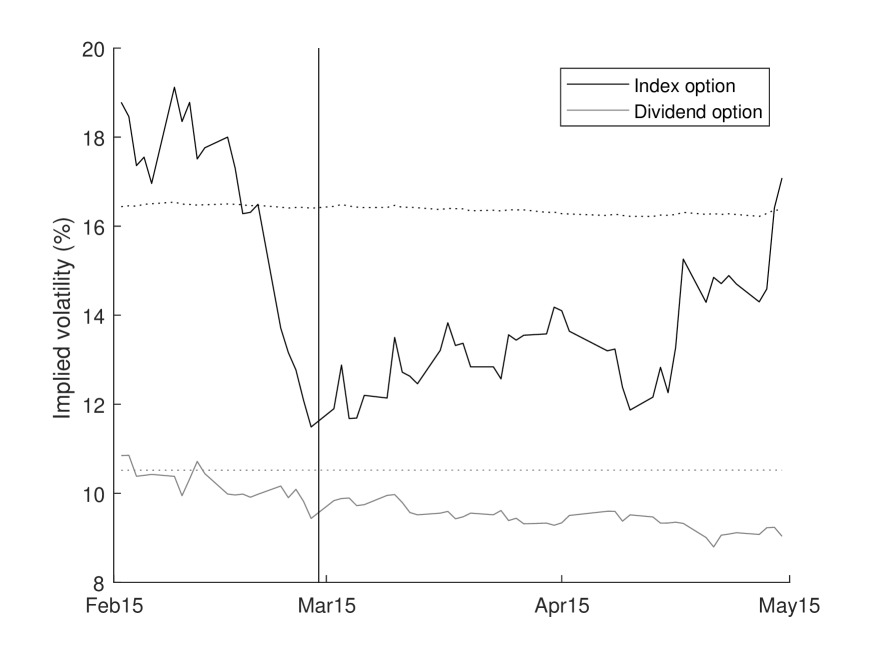

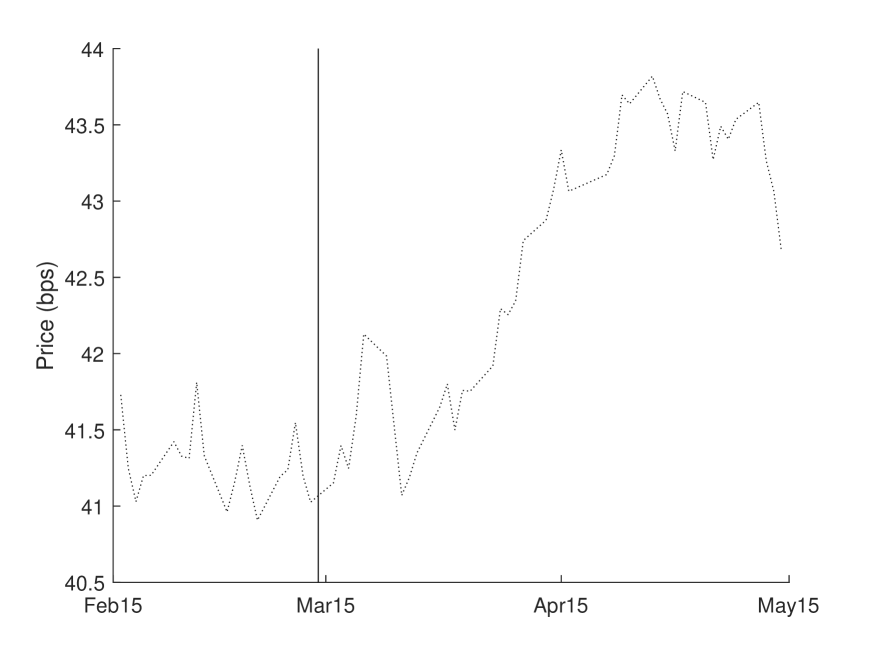

Next to the Euro Stoxx 50 dividend futures contracts, there also exist exchange traded options on realized dividends. The maturity dates and the referenced dividends of the options coincide with those of the corresponding futures contracts. At every calibration date, we consider the Black (1976) implied volatility of an at-the-money (ATM) dividend option with 2 years to maturity. Since dividend option contracts have fixed maturity dates, we interpolate the implied volatility of the second and third to expire ATM option contract.131313We linearly interpolate the total implied variance , where denotes the implied volatility and the maturity of the option. Figure 1(b) plots the implied volatilities of the dividend options over time.

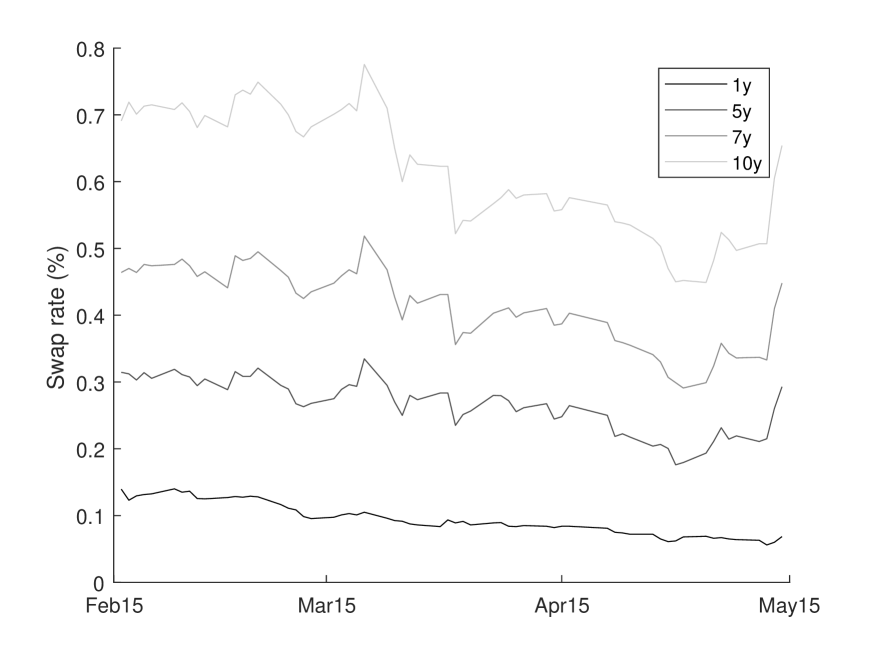

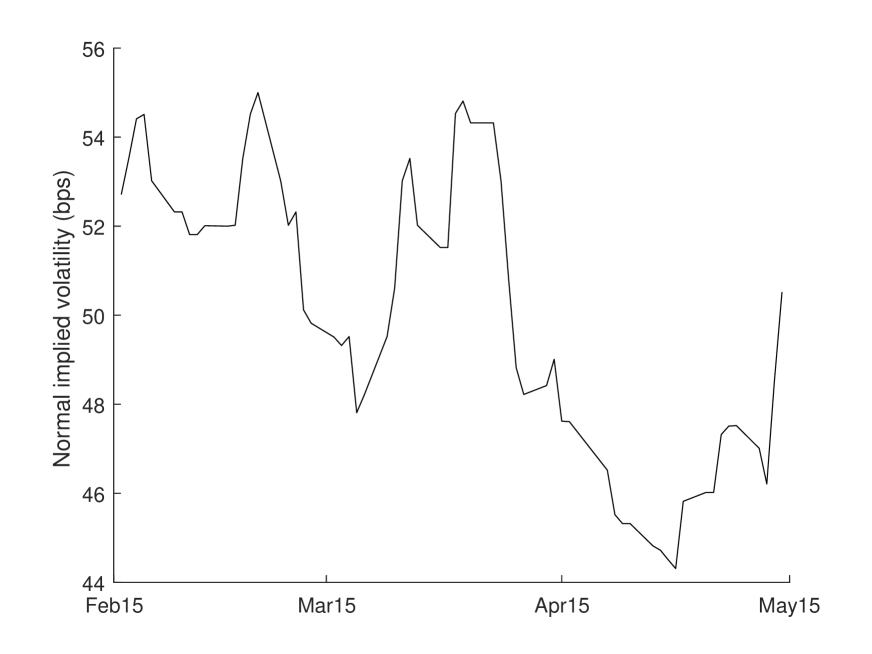

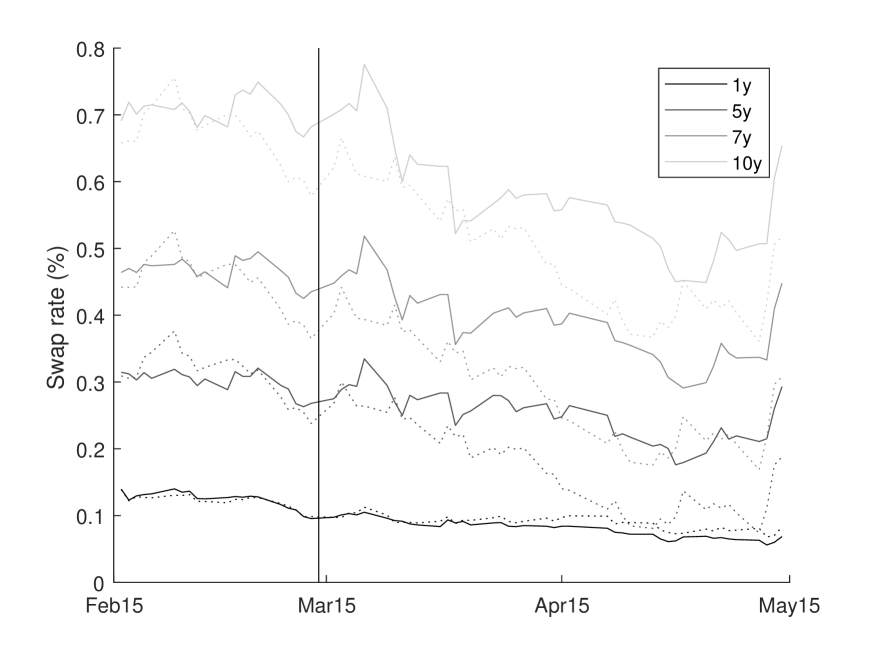

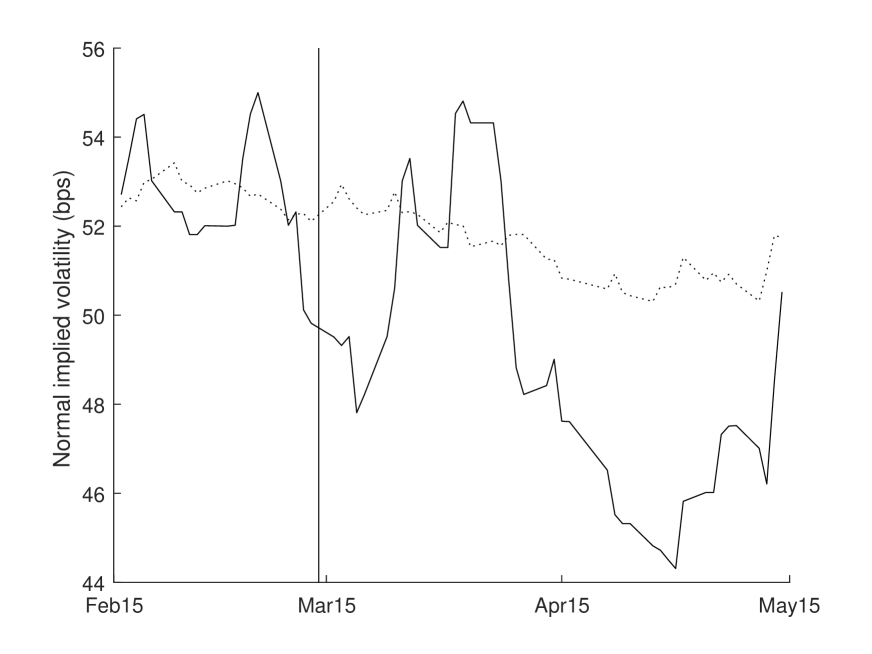

The term structure of interest rates is calibrated to European spot-starting swap contracts referencing the six month Euro Interbank Offered Rate (Euribor) with tenors of 1, 2, 3, 4, 5, 7, and 10 years. Figure 1(c) plots the par swap rates of swaps with tenors of 1, 5, 7, and 10 years. In addition, we also include ATM swaptions with time to maturity equal to 3 months and underlying swap with tenor 10 years. These are among the most liquid fixed-income instruments in the European market. The swaptions are quoted in terms of normal implied volatility and are plotted in Figure 1(d).

5.2 Model specification

We propose a parsimonious four-factor LJD specification without jumps for

| (27) |

with , , and . By Proposition 4.1, takes values in . Since we only include options with ATM strike in the calibration, we choose not to include any jumps in the dynamics in order to keep the number of parameters small. We define the cumulative dividend process as

so that and are driving the term structure of dividends. The corresponding instantaneous dividend rate becomes

Using Proposition 4.2, we guarantee by requiring . In order to further reduce the number of parameters, we set , so that and no longer enters in the dynamics of . We can thus normalize .

The discount factor process is defined as

so that and are driving the term structure of interest rates. The corresponding short rate becomes

which is unbounded from below and bounded above by .141414In the more general polynomial framework described in Section 2, it is possible to lower bound the short rate. For example, one can use compactly supported polynomial processes, similarly as in Ackerer and Filipović (2020). Dividing by a positive constant does not affect model prices, so for identification purposes we normalize .151515For a constant , the dynamics of is given by with . The dynamics of is therefore of the same form as that of .

The matrix is upper triangular and given by

The diagonal elements, which coincide with the eigenvalues, of are all positive by assumption. We can therefore interpret as the asymptotic zero-coupon bond yield and as the asymptotic risk-neutral expected dividend growth rate. Using Propositions 2.3 and 4.3, we introduce the following constraint on the model parameters in order to guarantee a finite stock price:

The parameter controls the correlation between interest rates and dividends. Specifically, the instantaneous correlation between the dividend rate and the short rate is given by

| (28) |

where denotes the quadratic covariation. The minus sign in front of appears because the Brownian motion drives the discount factor, which is negatively related to the short rate.

We set for parsimony, so that the stock price is equal to the present value of all future dividends, i.e., .

5.3 Calibration

We minimize the sum of squared differences between the model and market prices using the Nelder-Mead simplex algorithm. The parameters to be optimized are , , , , , , , , and . We propose an efficient way to filter out the latent factors , and on every day of the sample. For a given set of parameters, the dividend futures price (7) is a linear function of . We solve for through a linear least-squares regression from the dividend futures prices. The discounted swap value in (10) is a linear function of the latent factors and .161616Since we are using par swap rates, the value of the swap is equal to zero by definition. Applying Itô’s lemma to , it follows that the discounted stock price given by (8) and (12) is a linear combination of , , , , and . Since we already solved from the dividend futures prices, becomes a linear function of and . We solve and through a weighted linear least-squares regression from the swap rates and the stock price. We assign a relatively large weight to the stock price to make sure it is accurately matched by the model.

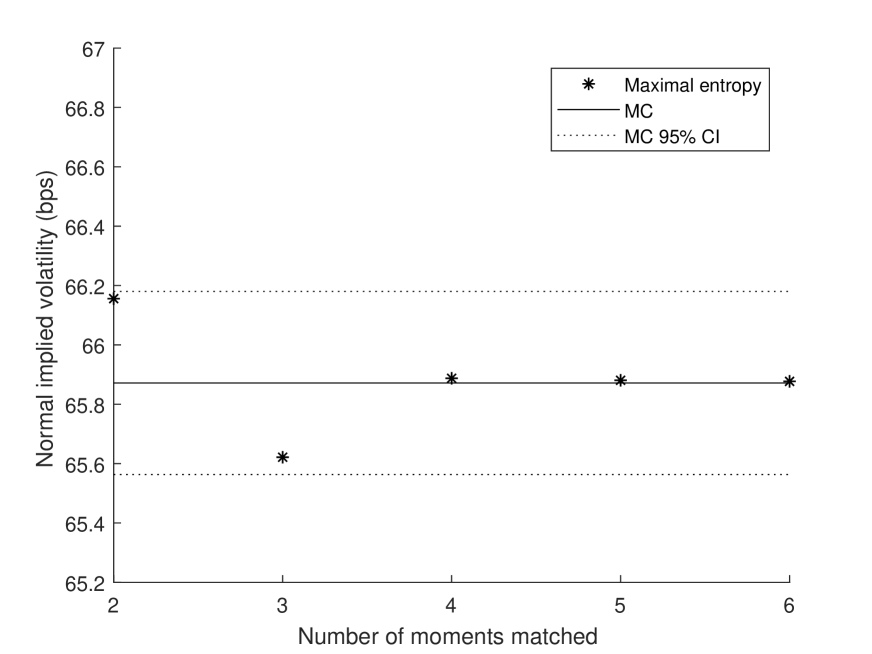

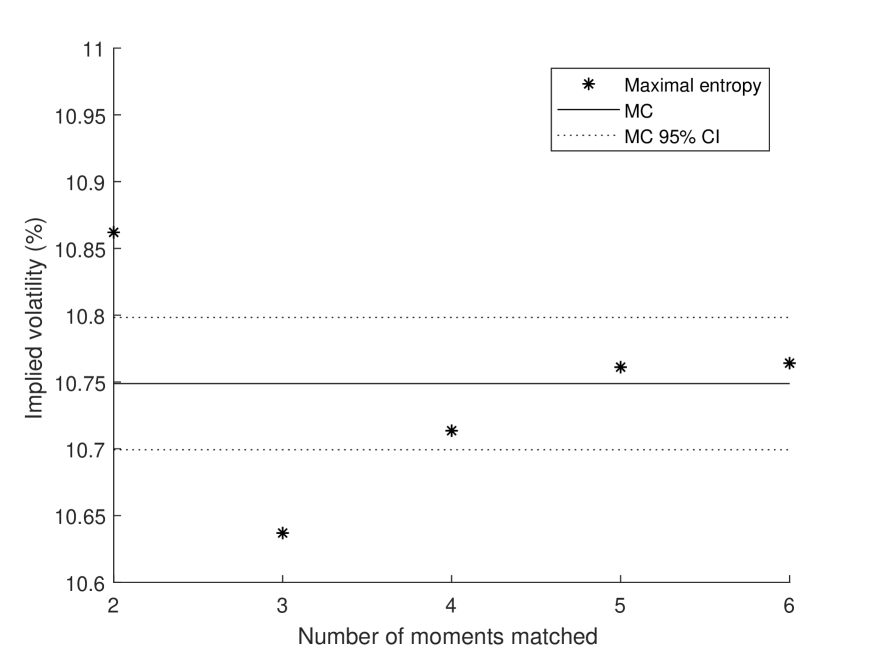

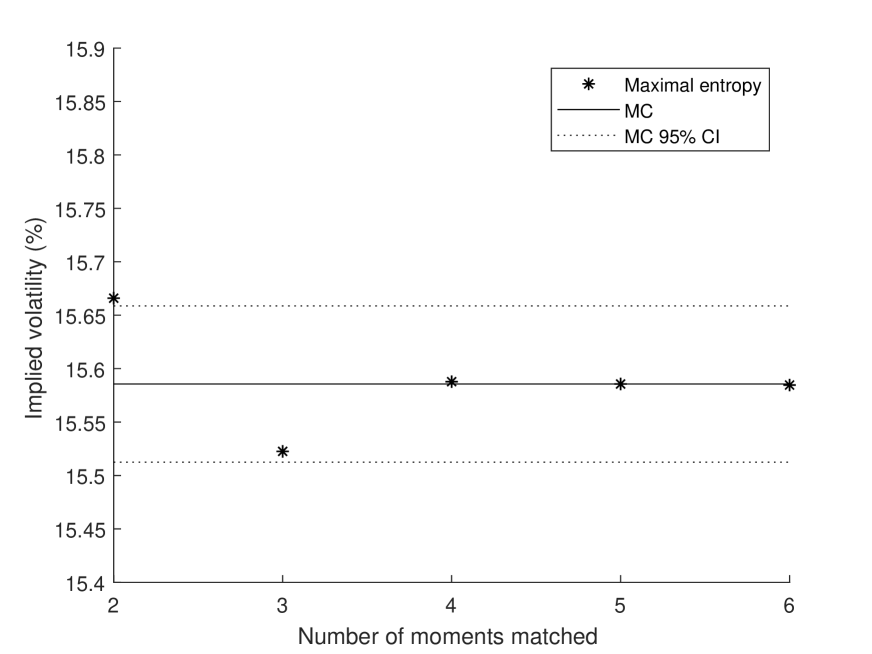

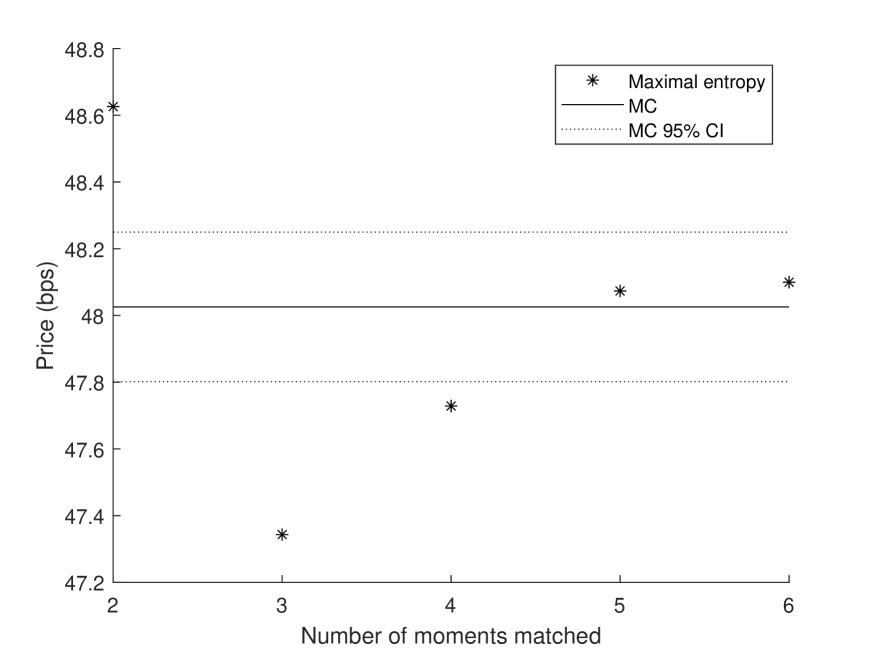

Although the option pricing technique described in Seciton 3.1 works in theory for any finite number of moment constraints, there is a computational cost associated with computing the moments on the one hand, and solving the Lagrange multipliers on the other hand. In the calibration, we use moments up to order four to price swaptions, dividend options, and stock options. The number of moments needed for an accurate option price depends on the specific form of the payoff function and on the model parameters. As an example, Figure 2 shows prices of a swaption, dividend option, stock option, and a hybrid option as described in Section 3.3 for different number of moments matched and a realistic set of parameters. For the hybrid option, we set , , and the spread such that the option is ATM. The swaption, dividend option, and stock option have the same characteristics as the ones used in the calibration. As a benchmark, we perform a Monte-Carlo simulation of the model. We discretize (27) at a weekly frequency with a simple Euler scheme and simulate trajectories.171717In addition, we also use the corresponding forward contracts as control variates. This variance reduction technique reduces the variance of the Monte-Carlo estimator approximately by a factor 4. We observe that using four to five moments produces a price approximation that is very close to the Monte-Carlo benchmark

We calibrate the model consecutively to one month of daily data from February, March, and April 2015. Table 1 shows the absolute pricing errors in the second, third, and fifth column, respectively. Considering the relatively small number of parameters, the fit is remarkably good. Dividend futures have a mean absolute relative error less than 1% with few exceptions. The mean absolute error of the swap rates is in the order of basis points for all tenors and all three months. The model only contains two volatility parameters ( and ), but nonetheless produces a relatively good fit with option prices on average. The Eurostoxx 50 index level is matched almost perfectly, thanks to the relatively large weight in the weighted least-squares regression to filter out the latent factors. The fourth and sixth column of Table 1 show out-of-sample pricing errors. Specifically, in the fourth (sixth) column we compute the pricing errors in March (April) using the parameters calibrated on February (March) data. The only degrees of freedom in this out-of-sample exercise are the values of the latent factors, which we filter out as explained before. The loss in pricing accuracy out-of-sample is modest, which speaks for the robustness of the model.

Table 2 shows the calibrated parameters. The parameters are comparable for the three calibration months, which is in line with the good out-of-sample performance. The parameter , which is the yield of the zero-coupon bond with infinite maturity, is decreasing in the subsequent calibrations, reflecting the decrease in interest rates over the sample period. The parameter , which is the asymptotic risk-neutral expected growth rate of the dividends, is always substantially lower than , as required for the stock price to be finite. The term structure of dividend futures is downward sloping over the entire sample period. This is reflected in the calibration by a small value for , which is the long-term mean of the process driving the dividends. Remarkably, is positive for all three months, close to the upper bound of one. In view of (28), this indicates a highly negative correlation between interest rates and dividends. This negative correlation is a central ingredient in our model, since it increases the volatility of the stock price relative to the dividends and interest rates. This allows to reconcile the relatively large implied volatility of stock options with the relatively small implied volatility of dividend options. From Figure 1(b) we can see that the difference between the dividend and stock option implied volatility was smaller in March than in February and April. This translates in a smaller calibrated in March compared to February and April.

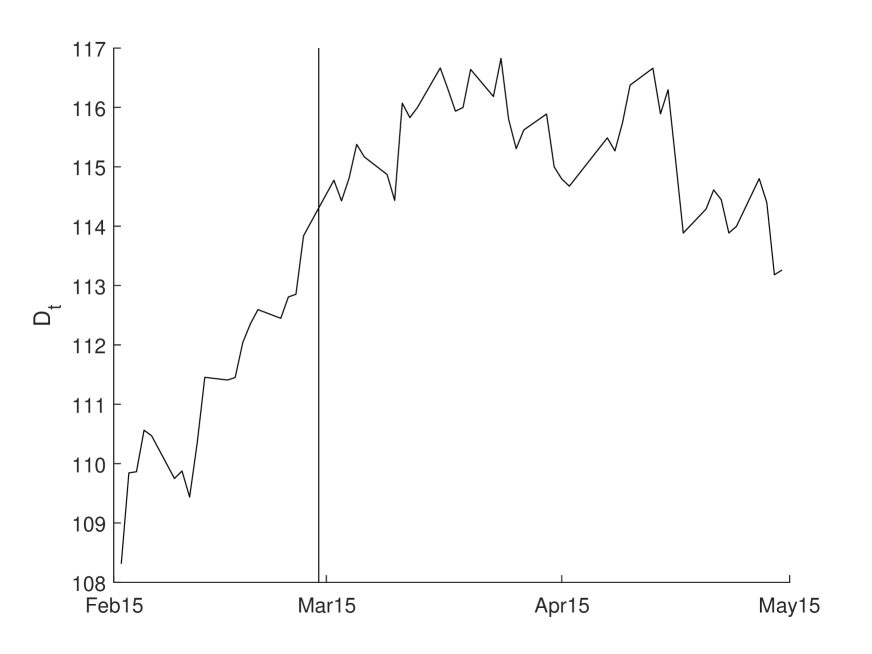

In Figure 3 we use the February parameters to plot the model prices together with the market prices over the full sample period. The February to March (March to April) regions of the plots are therefore a visualization of the second and fourth (fourth and sixth) column in Table 1. The goodness of fit deteriorates as we move away from the calibration window, which is to be expected. Note that the model is capable of capturing the level of implied volatilities of the stock and dividend options, but it fails to capture the variation over time. This is caused by the volatility structure of the model, where the relative volatility of the dividend factor is constant. Enriching the model specification with more factors can help to address this problem, however we leave this for future research. Figure 4 plots the filtered values of and using the parameters calibrated on February data. The plot looks similar when using the March or April parameters.

Figure 5 plots the stock duration using the February parameters. The stock duration is quite stable over time with an average around 23 years. Dechow et al. (2004) and Weber (2018) construct a stock duration measure based on balance sheet data and find an average duration of approximately 15 and 19 years, respectively, for a large cross-section of stocks. The plot looks similar when using the March or April parameters.

Table 3 contains computation times for calculating option prices. The bulk of the computation times is due to the computation of the moments of in (17). The number of stochastic factors that drive a derivative’s payoff and the degree of moments that have to be matched therefore strongly affect the computation time. We observe that all timings of the maximum entropy method are well below the time it took to run the benchmark Monte-Carlo simulation. The pricing of swaptions is much faster than the pricing of dividend and stock options, especially as the number of moments increases. This is because the discounted swaption payoff only depends on on the 2-dimensional process , while the discounted payoff of the dividend and stock option depends on the entire 4-dimensional process . In addition, the discounted payoff of the dividend and stock option is quadratic in the factors. Therefore, in order to compute moments up to degree of the discounted payoff, we need to compute moments up to degree of the factors. The computation of the dividend option is further complicated by the path-dependent nature of its payoff. Indeed, the dividend option payoff depends on the realization of the factors at and . In order to compute the moments of , we have to apply the moment formula twice. Hence, it involves computing a matrix exponential twice, which causes an additional computation time compared to the stock option.

6 Extensions

6.1 Seasonality

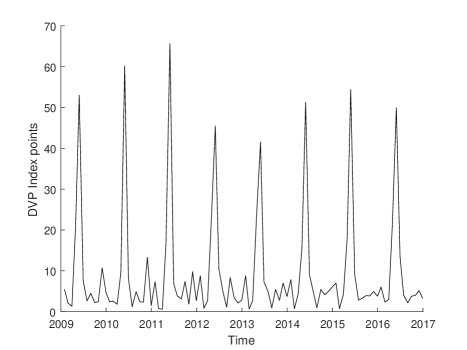

It is well known that some stock markets exhibit a strongly seasonal pattern in the payment of dividends. For example, Figure 6 shows that the constituents of the Euro Stoxx 50 pay a large fraction of their dividends between April and June each year.181818See e.g. Marchioro (2016) for a study of dividend seasonality in other markets. The easiest way to incorporate seasonality in our framework is to introduce a deterministic function of time and redefine the cumulative dividend process as:

| (29) |

The function therefore adds a deterministic shift to the instantaneous dividend rate:

| (30) |

In addition to incorporating seasonality, can also be chosen such that the observed dividend futures prices are perfectly matched. In Appendix A we show how the bootstrapping method of Filipović and Willems (2018) can be used to find such a function. We do not lose any tractability with the specification in (29), since the moments of can still easily be computed.

Alternatively, we could also introduce time dependence in the specification of . Doing so in general comes at the cost of losing tractability, because we leave the class of polynomial jump-diffusions. However, it is possible to introduce a specific type of time dependence such that we do stay in the class of polynomial jump-diffusions. Define as a vector of sine and cosine functions whose frequencies are integer multiples of (so that they all have period one)

The superposition

is a flexible function for modeling annually repeating cycles and is a standard choice for pricing commodity derivatives (see e.g. Sørensen (2002)). In fact, from Fourier analysis we know that any smooth periodic function can be expressed as a sum of sine and cosine waves. Remark now that is the solution of the following linear ordinary differential equation

The function can therefore be seen as a (deterministic) process of the form in (1) and can be added to the factor process. For example, the specification for in (27) could be replaced by

where the first factor mean-reverts around the second, and the second mean-reverts around a time-dependent mean. The process does not belong to the class of polynomial jump-diffusions, however the augmented process does.

In the calibration exercise in Section 5, we did not include any seasonal behavior in the dividends because the instruments used in the estimation are not directly affected by seasonality. Indeed, all the dividend derivatives used in the calibration reference the total amount of dividends paid in a full calendar year. The timing of the dividend payments within the year does therefore not play any role. In theory, the stock price should inherit the seasonal pattern from the dividend payments, since it drops by exactly the amount of dividends paid out. In practice, however, these price drops are obscured by the volatility of the stock price since the dividend payments typically represent only a small fraction of the total stock price. Dividend seasonality only plays a role for pricing claims on dividends realized over a time period different from an integer number of calendar years.

6.2 Dividend forwards

Dividend forwards, also known as dividend swaps, are the OTC equivalent of the exchange traded dividend futures. The buyer of a dividend forward receives at a future date the dividends realized over a certain time period against a fixed payment. Dividend forwards differ from dividend futures because they are not marked to market on a daily basis. The dividend forward price , , is defined as the fixed payment that makes the forward have zero initial value

If interest rates and dividends are independent, then we have . However, if there is a positive (negative) dependence between interest rates and dividends, then there is a convexity adjustment and the dividend forward price will be smaller (larger) than the dividend futures price. The following proposition derives the dividend forward price in the polynomial framework.

Proposition 6.1.

The dividend forward price is given by

where are the unique coordinate vectors satisfying

7 Conclusion

We have introduced an integrated framework designed to jointly price the term structures of dividends and interest rates. The uncertainty in the economy is modeled with a multivariate polynomial jump-diffusion. The model is tractable because we can calculate all conditional moments of the factor process in closed form. In particular, we have derived closed form formulas for prices of bonds, dividend futures, and the dividend paying stock. Option prices are obtained by integrating the discounted payoff function with respect to a moment matched density function that maximizes the Boltzmann-Shannon entropy. We have introduced the LJD model, characterized by a martingale part that loads linearly on the factors. The LJD model allows for a flexible dependence structure between the factors, which offers a valuable alternative to non-negative affine jump-diffusion models. We have assumed that dividends are paid out continuously and ignored the possibility of default. These assumptions are justified when considering derivatives on a stock index, but become questionable for derivatives on a single stock. An interesting future research direction is therefore to extend our framework with discrete dividend payments and default risk.

Appendix A Bootstrapping an additive seasonality function

In this section we explain how to bootstrap a smooth curve of (unobserved) futures prices corresponding to the instantaneous dividend rate . The curve should perfectly reproduce observed dividend futures prices and in addition incorporate a seasonality effect. Once we have this function, we define the function as

so that the specification in (29) perfectly reproduces observed futures contracts and incorporates seasonality.

Suppose for notational simplicity that today is time and we observe the futures prices of the dividends realized over one calendar year , . Divide the calendar year in buckets and assign a seasonal weight to each bucket, with . These seasonal weights can for example be estimated from a time series of dividend payments. We search for the twice continuously differentiable curve that has maximal smoothness subject to the pricing and seasonality constraints:

This can be cast in an appropriate Hilbert space as a convex variational optimization problem with linear constraints. In particular, it has a unique solution that can be solved in closed form using similar techniques as presented in Filipović and Willems (2018). By discretizing the optimization problem, a non-negativity constraint on can be added as well.

Appendix B Proofs

This section contains all the proofs of the propositions in the paper.

B.1 Proof of Proposition 2.2

Using the moment formula (3) we have for

Differentiating with respect to gives

The result now follows from

B.2 Proof of Proposition 2.3

Plugging in the specifications for and in (11) gives:

Since is a polynomial process, we can find a closed form expression for the expectation inside the integral:

The fundamental stock price therefore becomes:

where we have used the fact that the eigenvalues of the matrix have negative real parts.

B.3 Proof of Proposition 2.4

The market is arbitrage free if and only if the deflated gains process

| (31) |

is a non-negative local martingale.

If is of the form in (13), then we have

which is clearly a non-negative local martingale and therefore the market is arbitrage free.

Conversely, suppose that the market is arbitrage free and hence (31) holds. As a direct consequence, the process

must be a local martingale. To show nonnegativity, note that a local martingale bounded from below is a supermartingale, so that we have for all

where we have used the limited liability of the stock in the last inequality.

B.4 Proof of Proposition 2.6

B.5 Proof of Proposition 4.1

We start by showing that there exists a unique strong solution to (21) with values in . Due to the global Lipschitz continuity of the coefficients, the SDE in (21) has a unique strong solution in for every , see Theorem III.2.32 in Jacod and Shiryaev (2003). It remains to show that is -valued for all if . First, we prove the statement for the diffusive case.

Lemma B.1.

Consider the SDE

| (32) |

for some -dimensional Brownian motion and as assumed in Proposition 4.1. If , then for all .

Proof.

Replace in the drift of (32) by componentwise and consider the SDE

| (33) |

with . The function componentwise is still Lipschitz continuous, so that there exists a unique solution to (33). Now consider the SDE

| (34) |

with . Its unique solution is the -valued process given by

By assumption, we have that the drift function of (33) is always greater than or equal to the drift function of (34):

By the comparison theorem from (Geiß and Manthey, 1994, Theorem 1.2) we have almost surely

Hence, and therefore also solves the SDE (32). By uniqueness we conclude that for all , which proves the claim. ∎

Define as the th jump time of and . We argue by induction and assume that for some . Since the process is right-continuous, we have the following diffusive dynamics for the process on the interval

with and . The stopping time is a.s. finite and therefore the process defines a -dimensional Brownian motion with respect to its natural filtration, see Theorem 6.16 in Karatzas and Shreve (1991). By Lemma B.1 we have for all . As a consequence, we have for all . The jump size at time satisfies

where the are i.i.d. random variables with distribution . Rearranging terms gives . By induction we conclude that for , . The claim now follows because for a.s.

Next, we prove that is a polynomial jump-diffusion. The action of the generator of on a function is given by

| (35) |

where denotes the support of and we assume that is such that the integrals are finite. Now suppose that and assume without loss of generality that is a monomial with , . We now apply the generator to this function. It follows immediately that the first two terms in (35) are again a polynomial of degree or less. Indeed, the gradient (hessian) in the second (first) term lowers the degree by one (two), while the remaining factors augment the degree by at most one (two). The third term in (35) becomes (we slightly abuse the notation to represent both a multi-index and a vector):

| (36) |

where the logarithm is applied componentwise. Hence, we conclude that maps polynomials to polynomials of the same degree or less.

B.6 Proof of Proposition 4.2

This proof is similar to the one of Theorem 5 in Filipović et al. (2017). From (5) we have that if and only if

| (37) |

provided it is finite. Using (2) we have

| (38) |

Using the assumption for (cfr., Proposition 4.1), we have for all that

| (39) |

Combining (38) with (39) gives

| (40) |

If , then the fraction on the right-hand side of (40) can be seen as a convex combination of

with coefficients . As a consequence, we have in this case

If , then using the assumption (cfr., Proposition 4.1) we get

B.7 Proof of Proposition 4.3

Suppose first that is lower triangular. In order to get a specific idea what the matrix looks like, we start by fixing a monomial basis for using the graded lexicographic ordering of monomials:

| (41) |

It follows by inspection of (35) and (36) that, thanks to the triangular structure of , the matrix is lower triangular with respect to this basis. Indeed, the first and third term in (35) only contribute to the diagonal elements of , while the second term contributes to the lower triangular part (including the diagonal). The eigenvalues of are therefore given by its diagonal elements.

Each element in the monomial basis can be expressed as as , for some with . In order to find the diagonal elements of , we need to find the coefficient of the polynomial associated with the basis element . It follows from (35) and (36) that this coefficient is given by

The restriction allows to summarize all diagonal elements, and hence the eigenvalues, of as follows

Note that a change of basis will lead to a different matrix , however its eigenvalues are unaffected. The choice of the basis in (41) is therefore without loss of generality.

If is upper triangular, we consider a different ordering for the monomial basis:

The result now follows from the same arguments as in the lower triangular case.

B.8 Proof of Proposition 6.1

References

- Ackerer and Filipović (2020) Ackerer, D. and D. Filipović (2020). Linear credit risk models. Finance and Stochastics 24(1), 169–214.

- Ackerer et al. (2018) Ackerer, D., D. Filipović, and S. Pulido (2018). The Jacobi stochastic volatility model. Finance and Stochastics 22(3), 667–700.

- Agmon et al. (1979) Agmon, N., Y. Alhassid, and R. D. Levine (1979). An algorithm for finding the distribution of maximal entropy. Journal of Computational Physics 30(2), 250–258.

- Al-Mohy and Higham (2011) Al-Mohy, A. H. and N. J. Higham (2011). Computing the action of the matrix exponential, with an application to exponential integrators. SIAM Journal on Scientific Computing 33(2), 488–511.

- Avellaneda (1998) Avellaneda, M. (1998). Minimum-relative-entropy calibration of asset-pricing models. International Journal of Theoretical and Applied Finance 1(04), 447–472.

- Barone-Adesi et al. (2005) Barone-Adesi, G., H. Rasmussen, and C. Ravanelli (2005). An option pricing formula for the GARCH diffusion model. Computational Statistics & Data Analysis 49(2), 287–310.

- Bekaert and Grenadier (1999) Bekaert, G. and S. R. Grenadier (1999). Stock and bond pricing in an affine economy. Technical report, National Bureau of Economic Research.

- Bernhart and Mai (2015) Bernhart, G. and J.-F. Mai (2015). Consistent modeling of discrete cash dividends. Journal of Derivatives 22(3), 9–19.

- Black (1976) Black, F. (1976). The pricing of commodity contracts. Journal of Financial Economics 3(1-2), 167–179.

- Bos et al. (2003) Bos, M., A. Shepeleva, and A. Gairat (2003). Dealing with discrete dividends. Risk 16(9), 109–112.

- Bos and Vandermark (2002) Bos, M. and S. Vandermark (2002). Finessing fixed dividends. Risk 15(1), 157–158.

- Brennan (1998) Brennan, M. J. (1998). Stripping the S&P 500 index. Financial Analysts Journal 54(1), 12–22.

- Brennan and Schwartz (1979) Brennan, M. J. and E. S. Schwartz (1979). A continuous time approach to the pricing of bonds. Journal of Banking & Finance 3(2), 133–155.

- Buchen and Kelly (1996) Buchen, P. W. and M. Kelly (1996). The maximum entropy distribution of an asset inferred from option prices. Journal of Financial and Quantitative Analysis 31(1), 143–159.

- Buehler (2010) Buehler, H. (2010). Volatility and dividends–Volatility modelling with cash dividends and simple credit risk. Working Paper.

- Buehler (2015) Buehler, H. (2015). Volatility and dividends II–Consistent cash dividends. Working Paper.

- Buehler et al. (2010) Buehler, H., A. S. Dhouibi, and D. Sluys (2010). Stochastic proportional dividends. Working Paper.

- Chance et al. (2002) Chance, D. M., R. Kumar, and D. R. Rich (2002). European option pricing with discrete stochastic dividends. Journal of Derivatives 9(3), 39–45.

- Collin-Dufresne and Goldstein (2002a) Collin-Dufresne, P. and R. S. Goldstein (2002a). Do bonds span the fixed income markets? Theory and evidence for unspanned stochastic volatility. Journal of Finance 57(4), 1685–1730.

- Collin-Dufresne and Goldstein (2002b) Collin-Dufresne, P. and R. S. Goldstein (2002b). Pricing swaptions within an affine framework. Journal of Derivatives 10(1), 9–26.

- Corrado and Su (1996a) Corrado, C. J. and T. Su (1996a). Skewness and kurtosis in S&P 500 index returns implied by option prices. Journal of Financial Research 19(2), 175–192.

- Corrado and Su (1996b) Corrado, C. J. and T. Su (1996b). S&P 500 index option tests of Jarrow and Rudd’s approximate option valuation formula. Journal of Futures Markets 16(6), 611–629.

- Cox and Hobson (2005) Cox, A. M. and D. G. Hobson (2005). Local martingales, bubbles and option prices. Finance and Stochastics 9(4), 477–492.

- d’Addona and Kind (2006) d’Addona, S. and A. H. Kind (2006). International stock–bond correlations in a simple affine asset pricing model. Journal of Banking and Finance 30(10), 2747–2765.

- Dechow et al. (2004) Dechow, P. M., R. G. Sloan, and M. T. Soliman (2004). Implied equity duration: A new measure of equity risk. Review of Accounting Studies 9(2-3), 197–228.

- Duffie et al. (2003) Duffie, D., D. Filipović, and W. Schachermayer (2003). Affine processes and applications in finance. Ann. Appl. Probab. 13(3), 984–1053.

- Filipović and Larsson (2020) Filipović, D. and M. Larsson (2020). Polynomial jump-diffusion models. Stochastic Systems 10(1), 71 – 97.

- Filipović et al. (2017) Filipović, D., M. Larsson, and A. B. Trolle (2017). Linear-rational term structure models. Journal of Finance 72, 655–704.

- Filipović and Willems (2018) Filipović, D. and S. Willems (2018). Exact smooth term structure estimation. SIAM Journal on Financial Mathematics 9(3), 907–929.

- Fusai and Tagliani (2002) Fusai, G. and A. Tagliani (2002). An accurate valuation of Asian options using moments. International Journal of Theoretical and Applied Finance 5(02), 147–169.

- Geiß and Manthey (1994) Geiß, C. and R. Manthey (1994). Comparison theorems for stochastic differential equations in finite and infinite dimensions. Stochastic Processes and their Applications 53(1), 23–35.

- Geske (1978) Geske, R. (1978). The pricing of options with stochastic dividend yield. Journal of Finance 33(2), 617–625.

- Guennoun and Henry-Labordère (2017) Guennoun, H. and P. Henry-Labordère (2017). Equity modeling with stochastic dividends. Working Paper.

- Holly et al. (2011) Holly, A., A. Monfort, and M. Rockinger (2011). Fourth order pseudo maximum likelihood methods. Journal of Econometrics 162(2), 278–293.

- Jackwerth and Rubinstein (1996) Jackwerth, J. C. and M. Rubinstein (1996). Recovering probability distributions from option prices. Journal of Finance 51(5), 1611–1631.

- Jacod and Shiryaev (2003) Jacod, J. and A. Shiryaev (2003). Limit Theorems for Stochastic Processes, Volume 2. Springer-Verlag.

- Jarrow and Rudd (1982) Jarrow, R. and A. Rudd (1982). Approximate option valuation for arbitrary stochastic processes. Journal of Financial Economics 10(3), 347–369.

- Jarrow et al. (2007) Jarrow, R. A., P. Protter, and K. Shimbo (2007). Asset price bubbles in complete markets. Advances in Mathematical Finance, 97–121.

- Jaynes (1957) Jaynes, E. T. (1957). Information theory and statistical mechanics. Physical Review 106(4), 620.

- Jondeau and Rockinger (2001) Jondeau, E. and M. Rockinger (2001). Gram–Charlier densities. Journal of Economic Dynamics and Control 25(10), 1457–1483.

- Karatzas and Shreve (1991) Karatzas, I. and S. Shreve (1991). Brownian Motion and Stochastic Calculus (2nd ed.). Springer-Verlag.

- Kim (1995) Kim, I.-M. (1995). An alternative approach to dividend adjustments in option pricing models. Journal of Financial Engineering 4, 351–373.

- Korn and Rogers (2005) Korn, R. and L. G. Rogers (2005). Stocks paying discrete dividends: modeling and option pricing. Journal of Derivatives 13(2), 44–48.

- Kragt et al. (2020) Kragt, J., F. De Jong, and J. Driessen (2020). The dividend term structure. Journal of Financial and Quantitative Analysis 55(3), 829–867.

- Lasserre et al. (2006) Lasserre, J.-B., T. Prieto-Rumeau, and M. Zervos (2006). Pricing a class of exotic options via moments and SDP relaxations. Mathematical Finance 16(3), 469–494.

- Lemke and Werner (2009) Lemke, W. and T. Werner (2009). The term structure of equity premia in an affine arbitrage free model of bond and stock market dynamics. Technical report, ECB Working Paper.

- Lettau and Wachter (2007) Lettau, M. and J. A. Wachter (2007). Why is long-horizon equity less risky? A duration-based explanation of the value premium. Journal of Finance 62(1), 55–92.

- Lettau and Wachter (2011) Lettau, M. and J. A. Wachter (2011). The term structures of equity and interest rates. Journal of Financial Economics 101(1), 90–113.

- Linetsky (2004) Linetsky, V. (2004). Spectral expansions for Asian (average price) options. Operations Research 52(6), 856–867.

- Lioui (2006) Lioui, A. (2006). Black-Scholes-Merton revisited under stochastic dividend yields. Journal of Futures Markets 26(7), 703–732.

- Mamaysky et al. (2002) Mamaysky, H. et al. (2002). On the joint pricing of stocks and bonds: Theory and evidence. Technical report, Yale School of Management.

- Marchioro (2016) Marchioro, M. (2016). Seasonality of dividend point indexes. Statpro Quantitative Research Series.

- Mead and Papanicolaou (1984) Mead, L. R. and N. Papanicolaou (1984). Maximum entropy in the problem of moments. Journal of Mathematical Physics 25(8), 2404–2417.

- Merton (1973) Merton, R. C. (1973). Theory of rational option pricing. Bell Journal of Economics 4(1), 141–183.

- Nelson (1990) Nelson, D. B. (1990). ARCH models as diffusion approximations. Journal of Econometrics 45(1), 7–38.

- Overhaus et al. (2007) Overhaus, M., A. Bermúdez, H. Buehler, A. Ferraris, C. Jordinson, and A. Lamnouar (2007). Equity Hybrid Derivatives. John Wiley & Sons.

- Pilipović (1997) Pilipović, D. (1997). Energy Risk: Valuing and Managing Energy Derivatives. McGraw-Hill.

- Rockinger and Jondeau (2002) Rockinger, M. and E. Jondeau (2002). Entropy densities with an application to autoregressive conditional skewness and kurtosis. Journal of Econometrics 106(1), 119–142.

- Rompolis (2010) Rompolis, L. S. (2010). Retrieving risk neutral densities from european option prices based on the principle of maximum entropy. Journal of Empirical Finance 17(5), 918–937.

- Sørensen (2002) Sørensen, C. (2002). Modeling seasonality in agricultural commodity futures. Journal of Futures Markets 22(5), 393–426.

- Suzuki (2014) Suzuki, M. (2014). Measuring the fundamental value of a stock index through dividend future prices. Working Paper.

- Tunaru (2018) Tunaru, R. S. (2018). Dividend derivatives. Quantitative Finance 18(1), 63–81.

- Vellekoop and Nieuwenhuis (2006) Vellekoop, M. H. and J. W. Nieuwenhuis (2006). Efficient pricing of derivatives on assets with discrete dividends. Applied Mathematical Finance 13(3), 265–284.

- Weber (2018) Weber, M. (2018). Cash flow duration and the term structure of equity returns. Journal of Financial Economics 128(3), 486–503.

- Willems (2019a) Willems, S. (2019a). Asian option pricing with orthogonal polynomials. Quantitative Finance 19(4), 605–618.

- Willems (2019b) Willems, S. (2019b). Linear stochastic dividend model. Working Paper.

- Yan (2014) Yan, W. (2014). Estimating a unified framework of co-pricing stocks and bonds. Working Paper.

| February | March | March (oos) | April | April (oos) | |

|---|---|---|---|---|---|

| Dividend futures (ARE in %) | |||||

| 1y | 0.602 | 1.460 | 1.156 | 1.770 | 0.821 |

| 2y | 0.982 | 0.743 | 0.949 | 0.941 | 2.344 |

| 3y | 0.577 | 0.898 | 1.013 | 0.704 | 1.488 |

| 4y | 0.434 | 0.437 | 0.456 | 0.784 | 0.926 |

| 5y | 0.549 | 0.466 | 0.434 | 0.506 | 0.343 |

| 7y | 1.052 | 0.884 | 1.140 | 0.784 | 2.467 |

| 9y | 0.901 | 0.738 | 0.843 | 1.129 | 3.819 |

| Interest rate swaps (AE in %) | |||||

| 1y | 0.003 | 0.004 | 0.005 | 0.005 | 0.004 |

| 2y | 0.021 | 0.032 | 0.011 | 0.037 | 0.011 |

| 3y | 0.028 | 0.038 | 0.017 | 0.047 | 0.007 |

| 4y | 0.025 | 0.029 | 0.032 | 0.042 | 0.020 |

| 5y | 0.021 | 0.025 | 0.047 | 0.026 | 0.040 |

| 7y | 0.029 | 0.030 | 0.067 | 0.028 | 0.069 |

| 10y | 0.044 | 0.043 | 0.061 | 0.063 | 0.073 |

| Dividend option (AE in %) | 0.407 | 0.871 | 0.912 | 0.365 | 0.531 |

| Swaption (AE in bps) | 1.063 | 2.092 | 2.331 | 1.142 | 3.516 |

| Stock option (AE in %) | 1.868 | 0.932 | 3.482 | 1.089 | 1.129 |

| Index level (ARE in %) | 0.038 | 0.028 | 0.065 | 0.023 | 0.059 |

| Parameter | February | March | April |

|---|---|---|---|

| 0.0045 | 0.0043 | 0.0016 | |

| 0.018 | 0.018 | 0.022 | |

| 0.0013 | 0.0015 | 0.0015 | |

| 3.1e-04 | 2.7e-04 | 2.4e-04 | |

| 0.17 | 0.16 | 0.22 | |

| 0.053 | 0.047 | 0.035 | |

| 0.12 | 0.10 | 0.11 | |

| 0.34 | 0.32 | 0.45 | |

| 0.97 | 0.80 | 0.99 |

| MC | ||||||

|---|---|---|---|---|---|---|

| Swaption | 0.02 | 0.02 | 0.02 | 0.02 | 0.02 | 1.01 |

| Dividend option | 0.03 | 0.06 | 0.14 | 0.41 | 1.24 | 25.88 |

| Stock option | 0.02 | 0.03 | 0.06 | 0.07 | 0.11 | 3.49 |