Testing a Goodwin model with general capital accumulation rate

Abstract

We perform econometric tests on a modified Goodwin model where the capital accumulation rate is constant but not necessarily equal to one as in the original model (Goodwin, 1967). In addition to this modification, we find that addressing the methodological and reporting issues in Harvie (2000) leads to remarkably better results, with near perfect agreement between the estimates of equilibrium employment rates and the corresponding empirical averages, as well as significantly improved estimates of equilibrium wage shares. Despite its simplicity and obvious limitations, the performance of the modified Goodwin model implied by our results show that it can be used as a starting point for more sophisticated models for endogenous growth cycles.

Keywords: Goodwin model, endogenous cycles, parameter estimation, employment rate, income shares.

JEL Classification Numbers: C13, E11, E32.

1 Introduction

Compared with the large literature dedicated to theoretical aspects of the Goodwin model and its extensions111The seminal paper is Goodwin (1967). Desai (1973) introduced three extensions of the model to incorporate inflation, expected inflation and variable capacity utilization. In a series of papers (van der Ploeg, 1984, 1985, 1987), van der Ploeg introduced the impact of savings by households, substitutability between labor and capital and cost minimizing impact of technical change. There has also been numerous works aimed at understanding the impact of government policy within the framework of the Goodwin model (see Wolfstetter, 1982; Takeuchi and Yamamura, 2004; Asada, 2006; Yoshida and Asada, 2007; Costa Lima et al., 2014). They address problems such as choice of policy (Keynesian versus Classical), role of policy lag and types of debt. Recently Nguyen Huu and Costa-Lima (2014) introduced a stochastic version of the Goodwin model with Brownian noise in the productivity factor, empirical studies of such models have attracted relatively little interest. A well-known exception is Harvie (2000), where the Goodwin model is put to test using data for 10 OECD countries from 1959 to 1994, with largely negative conclusions. Regrettably, the work presented in Harvie (2000) contained a serious mistake, as well as several smaller problems with its methodology and data construction, that call its conclusion into question. The purpose of the present paper 222A previous version of this work circulated with the title ‘Econometric Estimation of Goodwin Growth Models’. The key difference in this version is the capital accumulation rate introduced in Section 2.1. The results obtained in the previous version for the original Goodwin model, namely corresponding to , are now presented in an online appendix to this paper, which also contains results for the related Desai and van der Ploeg models and can be found at www.math.mcmaster.ca/grasselli/appendix-Goodwin is to address these issues and reevaluate the empirical validity of the Goodwin model. We begin with a brief overview of related empirical studies of the Goodwin and similar models.

One of the first studies that tried to analyze the Goodwin model in the context of real data was Atkinson (1969), with an emphasis on finding the typical time scale of long-run steady state and cyclical models. Atkinson uses the then recently proposed Goodwin model as an example of growth model with cycles and proceeds to calculate its period using several alternative values for the underlying parameters. Although not an econometric study, it made attempts to compare periods for trade cycles in postwar United States with those obtained for the Goodwin model. It also inspired the approached later adopted in Harvie (2000), namely to test the Goodwin model by estimating the underlying parameters separately from the model and comparing the resulting equilibrium values (and period) with the corresponding empirical averages. A major breakthrough in the area came with Desai (1984), where the foundation on how to estimate such dynamic models was laid using data for the United Kingdom for the period 1855 to 1965. By testing generalized models having the Goodwin model as a special case, Desai largely rejected the empirical validity of many assumptions in the Goodwin model. Following Desai, Harvie (2000) tested the Goodwin model in 10 OECD countries from 1959 to 1994 by comparing the estimated equilibrium wage shares and employment rates with the empirical average values. Although he observed qualitative evidence of the cyclical relationship as proposed by Goodwin, there was poor quantitative evidence of the Goodwin model being close to reality. Unfortunately there were several problems with the data construction in this paper, in addition to the mistake described in detail in Section 2.2, that compromised the validity of most of its results. In this regard, Mohun and Veneziani (2006) have discussed the appropriate data for econometric estimation for the Goodwin model and the problems with Harvie’s estimations. Although they did not do econometric estimation, they compared the qualitative cycles and trends for non-farm payroll data for US using two different datasets. Interestingly, they attribute most of the problematic results reported in Harvie (2000), such as the unrealistically high estimates for the parameters in the Philips curve, to structural change in the data over the period. As we explain in Section 2.2, however, most of these problems disappear once the mistake in Harvie (2000) is corrected.333For example, the correct parameters in the Philips curve can be obtained by simply dividing the parameters reported in Harvie (2000) by a factor of 100. In addition, as shown in Section 3, we do not find evidence for structural break in the relationships used to estimate the underlying parameters of the model. Garcia-Molina and Medina (2010) extended the work done in Harvie (2000) for 67 developed and developing countries. These countries could be divided into three groups, one which depicted Goodwin cycles, the second with movement in opposite direction as predicted by Goodwin due to demand-pushed cycles, and a third without any cyclical movement.

Other approaches have been used to test the Goodwin model. For example, Goldstein (1999) used multivariate vector auto regression (VAR) specification to understand dynamic interaction between unemployment and profit share of income. He also extended the model to include structural shifts in it. As another example, Dibeh et al. (2007) used the Bayesian inference method to directly estimate the parameters of the differential equations in the Goodwin model, rather than looking at the underlying structural equations like Harvie (2000). They also modify the classic Goodwin model by introducing a sinusoidal wave to act as exogenous periodic variation. Although the estimates are very close to real data, they do not comment on the theoretical properties such as structural stability of the new stochastic system. Flaschel (2009) extended the literature by analyzing the wage share-employment rate relationship using modern econometric techniques. He used a Hodrick-Prescott filter to decompose the state variables into trend and cycles for the US economy. He found considerable evidence of the closed Goodwin cycles that is more prominent than looking at raw data. Further he used a non-parametric bivariate P-spline regression to understand the relationship between wage share and employment rate and the dynamics of unemployment-inflation rate. An important contribution in this study is the separation of long phase cycles and business cycles through this method. Tarassow (2010) used bivariate VAR model for quantifying the relationship between wage share and employment rate in the US economy. The core of the paper is the implementation of impulse response functions and variance decomposition of forecast error to understand the propagation of shocks in one variable to the other using both the raw data and HP filtered data. Massy et al. (2013) introduced multiple sine-cosine terms to the state equations in the Goodwin model in order to better explain the fluctuations in real data for 16 countries. Although addition of harmonics definitely improved the fit, there is no discussion on the theoretical properties or the impact on structural stability of the model. Recently Moura Jr. and Ribeiro (2013) took a non-conventional route to estimate the Goodwin model, as well as an extension proposed by Desai et al. (2006), using data for the Brazilian economy from 1981-2009. The novelty of their approach lies in the data construction for wage share and employment rate. They use the Gompertz-Pareto distribution on individual income database for Brazil to find the wage share and profit share. Moreover since the methodology to calculate unemployment changed over the years, they redefined unemployment as a state when the average individual income is equal to or below 20% of the national minimum salary. Using these two new data series, they estimate classic Goodwin and its extension. Although there is clear evidence of qualitative cycles, they do not find quantitative evidence to support the Goodwin model or its extension.

Our own approach is much closer to that of Desai (1984) and Harvie (2000), but with the aim to, first of all, address the problems in Harvie (2000), then extend the study to a broader and more systematic dataset, and finally perform empirical tests of an extension of the Goodwin model. For this, we first update the data used in Harvie (2000) to cover a longer period from 1960 to 2010 and redefine some of the key variables taking into account the criticisms raised, among others, in Mohun and Veneziani (2006). Next we introduce what turns out to be a crucial modification in the original Goodwin model, namely allowing the ratio of investment to profit to be given by a parameter , which should then be estimated from the data along with the other parameters in the model, rather than assumed to be identically equal to one as in the original Goodwin model.444We are indebted to an anonymous referee for suggesting this modification.

We then perform an empirical test of the Goodwin model in Section 2 along the lines suggested in Harvie (2000), namely by estimating the underlying parameters of the model and comparing the resulting estimates for the equilibrium values of employment rate and wage share with the corresponding empirical means over the period. This includes a careful analysis of stationarity of the underlying time series and stability of the estimated parameters. We find a marked improvement over the results reported in Harvie (2000). For example, the estimates for equilibrium employment rate are remarkably close to the empirical means, with an average relative error of just 0.53% across all countries, ranging from a minimum relative error of 0.1% in Germany and to a maximum of 1.15% in Canada and Finland. By comparison, the estimates for equilibrium employment rate in Harvie (2000) were not even inside the range of observed data, resulting in an average relative error of 9.09% across all countries. As we mention in Section 2.2 and discuss in detail in Grasselli and Maheshwari (2017), most of this improvement in the estimated employment rates can be attributed to correcting the reporting mistake in Harvie (2000). Our results for wage shares, on the other hand, are also significantly better than those of Harvie (2000), even though they were not affected by the same mistake. The improvement in this case is largely attributable to the introduction of the capital accumulation rate , which Harvie (2000) implicitly assumes to be equal to one, in accordance with the original Goodwin model, but we estimate from the data. As a result, our estimated equilibrium wage shares lie well within the range of observed values for all countries and have an average relative error of 2.54% when compared to empirical means, ranging from a minimum relative error of 0.26% for Germany to a maximum of 5.83% for the UK. By comparison, the estimated equilibrium wage shares estimated in Harvie (2000) for the original Goodwin model are outside the range of observed value for all countries and have an average relative error of 38%, ranging from a minimum relative error of 22.6% for Norway to a maximum of 103% for Greece.555As explained in Section 2.3, we use the same number of countries as Harvie (2000), but replace Greece with Denmark, whose economic fundamentals are closer to the other countries in the sample. Excluding Greece, the average relative error in the estimated equilibrium wage share in Harvie (2000) is still 30.8%.

More importantly, the introduction of the capital accumulation rate also leads to improved performance for the simulated trajectories of the modified Goodwin model obtained from the estimated parameters. We show this in Section 4 by means of the Theil statistics, where we compute the root-mean-square errors between for employment rates and wage shares using all observed points and the corresponding simulated trajectories. We find that the errors are again smaller for employment rates than for wages shares, which also show a larger component of systematic errors.

2 A modified Goodwin model

This section explains theoretical setup of the original Goodwin model as proposed in Goodwin (1967) and the modification adopted in this paper. This is followed by an explanation of the corresponding econometric setup presented in Harvie (2000) and a description of the data and summary statistics.

2.1 Model Setup

The Goodwin model starts by assuming a Leontieff production function with full capital utilization, that is,

| (1) |

where is real output, is real capital stock, is the employed labor force, is labor productivity and is a constant capital-to-output ratio. It also assumes exponential growth function for both productivity and total labour force of the form

| (2) | ||||

| (3) |

where and are constant growth rates. Finally, the version of the Goodwin model adopted in this paper is based on the following two behavioural relationships:

| (4) | ||||

| (5) |

where and are constants. The first relationship above says that the growth in real wage rate

| (6) |

where denotes the real wage bill in the economy, depends on the employment rate

| (7) |

through a linear Phillips curve . The second relationship, namely equation (5) above, says that a constant fraction of total profits

| (8) |

from production are reinvested in the accumulation of capital, which in turn depreciates at a constant rate . The remainder fraction of profits are distributed as dividends to the household sector, which is assumed to have no savings, so that all wages and dividends are spent on consumption.

Using these assumptions and defining as the wage share of output in the economy, one can derive the following set of equations to describe the relationship of wage share and employment rate:

| (9) | ||||

| (10) |

The solution of these system of differential equations is a closed orbit around the non-hyperbolic equilibrium point

| (11) | ||||

| (12) |

with period given by

| (13) |

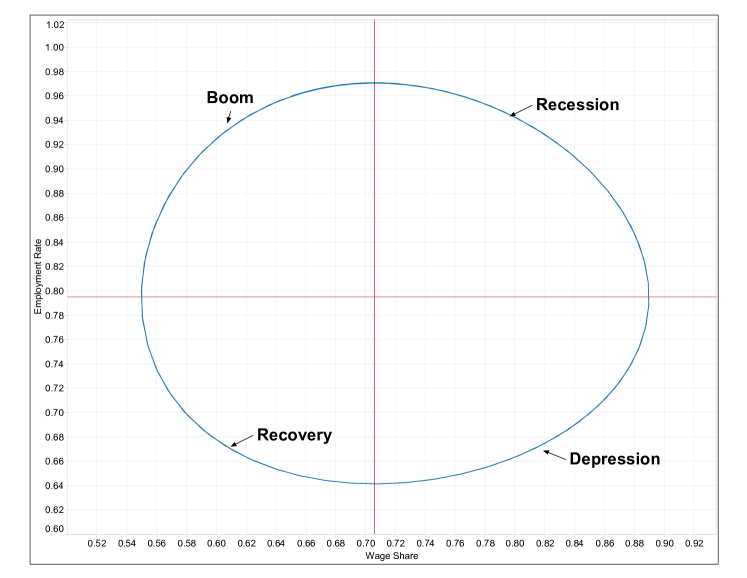

and is illustrated in Figure 1. In the original Goodwin model proposed in Goodwin (1967), investment was assumed to be always equal to profits, that is to say, in (5). To the best of our knowledge, the more general form in (5), with a constant not necessarily equal one, was first proposed in Ryzhenkov (2009) in the context of a more complicated three-dimensional model for the wage share, employment rate, and a variable capital-to-output ratio.

[ Insert Figure 1 here ]

2.2 Econometric setup

The test of the Goodwin model proposed by Harvie (2000) consists of comparing the econometric-estimate predictors for the equilibrium point , which can be obtained from (11)-(12) by substituting the econometric estimates for the underlying parameters in the model, with the empirical average of the observed employment rates and wage shares through the data sample.

Before describing our results, we take a slight detour to discuss some of the methodological and reporting issues in Harvie (2000). To start with, Harvie (2000) had a transcription mistake in the reported estimated parameters for the Phillips curve: the coefficients for the employment rate in Table A2.3 of Harvie (2000) are incorrect.666We thank David Harvie for informing us through private communication that the coefficients of the employment rate were supposed to be in percentages but mistakenly used as numbers. For example, the estimated coefficient for the employment rate for Australia is reported as in Table A2.3 when it should have been . This mistake propagated further, leading to inappropriate equilibrium estimates of employment rate in Table 2 of Harvie (2000). The mistakenly large estimates of the parameters in the Phillips curve effectively killed the impact of productivity growth on employment rate and led to estimates of employment rate that were downward biased, with over 10% absolute error for some countries. For example, if the correct coefficients from Table A2.3 had been used, the estimate for the equilibrium employment rate for UK would have been 0.96, while Harvie (2000) reported it as 0.85. The estimate of period of the Goodwin cycle is also incorrect due to same problem and consequent miscalculation. The correct period of the Goodwin cycles should have been between 10 to 22 years for the data used in Harvie (2000), but it was reported to be between one and two years for all the countries. The mistake and its consequences, as well as the correct values for the parameters, equilibrium points, and periods are discussed in detail in Grasselli and Maheshwari (2017).

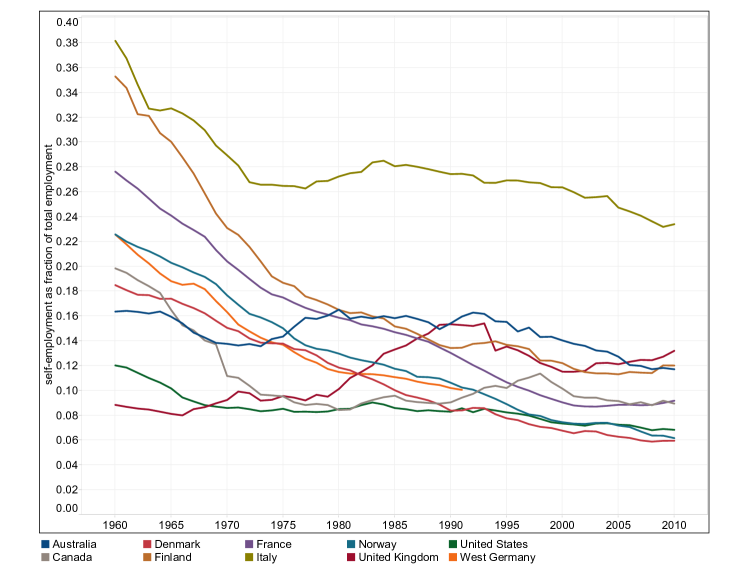

Secondly, the definition of wage share in his study does not segregate the income of the self employed into labor and capital income. Including proprietor’s income as part of ‘net operating surplus’ is a gross underestimation of the wage share. As can be seen in Figure 2, the fraction of the labor force that was self employed in the sample countries during the period of study can be quite high. As of 2010, while Italy has around a quarter of its population as self employed, three of the other 8 countries have over 10% of total employment as self employed. This effect was more prominent in early part of the data, when 8 of the 10 countries had over 15% of total employment as self employed. Including their total income as part of profits is therefore inappropriate.

[ Insert Figure 2 here ]

Finally, the methodology in Harvie (2000) was inconsistent in defining the total income of the economy. When defining wage share, Harvie (2000) used (Compensation of Employees + Net Operating Surplus) as a proxy for total income, leaving out consumption of fixed capital and taxes on production and imports from the GDP, whereas when defining productivity and in the derivation of equilibrium values it used GDP as a proxy for total income. In the results that follow, we address these problems with the methodology in Harvie (2000).

2.3 Data Construction and Sources

We use data from the AMECO database777AMECO is the annual macro-economic database of the European Commission’s Directorate General for Economic and Financial Affairs (DG ECFIN). We used the data provided in tabular form at http://knoema.com/ECAMECODB2014Mar/annual-macro-economic-database-march-2014 from 1960 to 2010 for Australia, Canada, Denmark, Finland, France, Italy, Norway, UK and US. For Germany, we use data from 1960 to 1990 only, to avoid dealing with the jumps that occur in all variables because of unification. These are the same countries analyzed in Harvie (2000), except that we replaced Greece by Denmark, which has economic fundamentals that are closer to the other countries in the sample.

We define output as GDP at factor cost, that is, net of taxes and subsidies on production and imports, and use a GDP deflator to obtain real income as

| (14) |

This is because the Goodwin model does not consider either taxes or subsidies explicitly, which are included in measures of GDP at producers’s price.

For the estimation of the Goodwin model, we have to separate income into wages and profits. Wages can be gauged from the ‘Compensation of Employees’ variable in the database, but this does not include the income of the self employed, which can be significantly high. Since we can not find segregation of proprietors income into labor and capital, we follow Klump et al. (2007) and use compensation per employee as proxy for labor income of the self employed. Thus the real wage bill in the economy is given by

| (15) |

and gross real profits are defined as . We next define total employment as

| (16) |

and total labor force as

| (17) |

For variables using real capital stock , we use the total net capital stock (at 2005 prices) from the database, which include both private and government fixed assets, and divide it by real output to obtain the capital-to-output ratio . Similarly, the return on capital can then be defined as

| (18) |

For depreciation rate , we use the definition from the manual of AMECO database, that is,

| (19) |

Similarly, for the accumulation rate we use

| (20) |

2.4 Summary Statistics

Table 1 summarizes the data for wage share and employment rate for the 10 countries we analyze. The average wage share for the period varied between 61.48% for Norway to 71.47% for UK, whereas the average employment rate varied between 92.80% for Italy to 97.31% for Norway. Norway is a curious case with highest average employment rate (and least variability) and lowest average wage share (and highest variability). Finland is the only country with over 4% standard deviation in the employment rate, mostly attributable to a slump in the Finnish economy during the early 1990s, when the employment rate dropped by over 12% in four years and the wage share continued to decline throughout the decade. On the other hand, the United States has one of the most stable wage share and employment rate when compared with any of its European counterpart.

[ Insert Table 1 here ]

3 Estimation results

The estimate of the equilibrium employment rate in equation (11) depends on the estimation of Phillips curve , that is to say the parameters and , and the productivity growth rate , whereas the estimate of the equilibrium wage share in equation (12) depends on , , , and . We can estimate the parameters for productivity growth rate and population growth rate using the log-regression of the variables on the time trend, that is,

| (21) | ||||

| (22) |

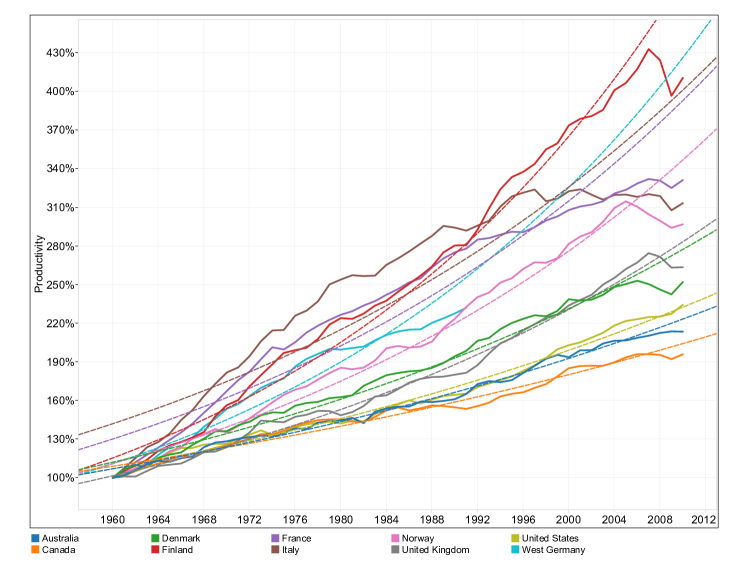

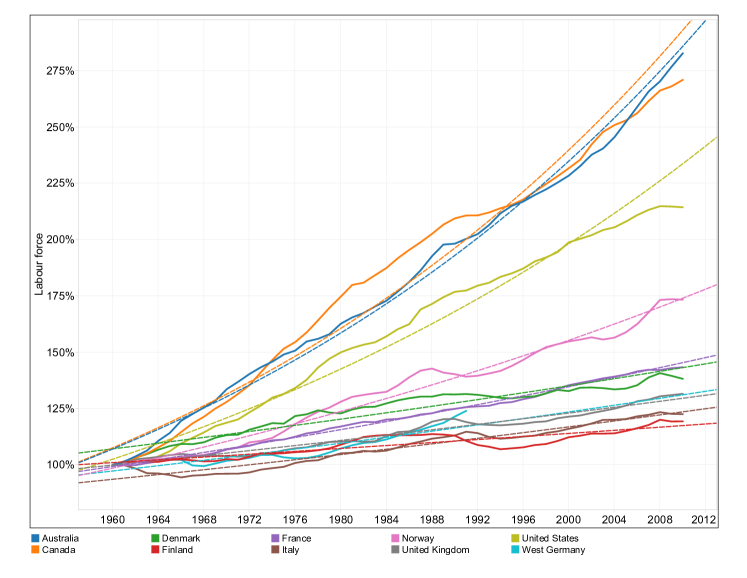

Table 5 presents the estimates of the parameters in equation (21) for different countries. The productivity growth rate varies from 1.3% for Canada to 2.9% for Finland, with all the European countries exhibiting a higher productivity growth rates than the three non-European ones. Similarly, Table 6 shows the parameters estimate for equation (22). Here Australia and Canada top the list with roughly 2% growth rate of labor force followed by US with 1.65%. All the European economies considered, except Norway, face the problem of ageing population with the growth rate less than 1%. Figure 6 also gives a graphical interpretation of labour force growth and productivity growth rate.

The estimate for the Phillips curve is more involved. Following Harvie (2000), we first approximate the term by and replace (4) with

| (23) |

for the discrete-time variables and

| (24) |

which is itself an approximation for . Harvie (2000) then proposes to estimate an autoregressive distributed lag (ARDL) model of the form

| (25) |

and assumes stationarity of the variables to obtain estimates and for the long-run coefficients from the estimates of the ARDL(p,q) model above (see Harvie (2000, footnote 1, page 356)). This is problematic, since there is no guarantee that the variables at hand are indeed stationary. Table 7 shows the results of the augmented Dickey-Fuller test (ADF test) to check for unit root for real wage growth, employment rate, productivity growth, inflation and nominal wage growth for the 10 countries in the study. At a broad level we can say that real wage growth and productivity growth are stationary whereas the employment rate, inflation and nominal wage growth are non-stationary for most of the countries.

Because real wage growth and employment rate have different order of integration (the former is stationary, the latter is not), we can not use standard time series models to estimate the parameters in (23). Instead, we shall use the bounds-testing procedure proposed by Pesaran et al. (2001), which allows us to test for the existence of linear long-run relationship when variables have different order of integration. We start by formulating an unrestricted error correction model (ECM) of the form

| (26) |

where the lag is determined using a Bayesian Information Criterion. As it happens, the optimal lag turns out to be zero for all countries, so that the effective unrestricted error correction model is given by

| (27) |

We first perform a Ljung-Box Q test to check for no serial correlation in the errors for equation (27), as this is a necessary condition for the bounds-testing procedure of Pesaran et al. (2001) to apply. We observe in Table 8 that the p-values for the alternative hypothesis that the errors are AR(m) for are greater than 10% for all countries, thus implying no serial correlation.

We proceed by testing the hypothesis in (27) against the alternative hypothesis that is not true. We do this because, as in conventional co-integration tests, the absence of a long-run equilibrium relationship between the variables and is equivalent to , so a rejection of implies a long-run relationship. The technical complication associated with an arbitrary mix of stationary and non-stationary variables is that exact critical values for a conventional F-test are not available in this case. The essence of the approach proposed in Pesaran et al. (2001) consisted in providing bounds on the critical values for the asymptotic distribution of the F-statistic instead, with the lower bounds corresponding to the case where all variables are and the upper bound corresponding to the case where all variables are . The lower and upper bounds provided in Narayan (2005) for 50 observations at 1%, 5% and 10% levels are (7.560, 8.685), (5.220, 6.070) and (4.190, 4.940), respectively. Table 9 shows the computed F-statistic for the joint restriction , which lie above the upper bound at the 1% significance level for all the countries except Germany, where it is above the upper bound at the 10% significance level. We thus reject the null hypothesis of absence of co-integration for all countries.

Having established that the variables show co-integration, we can now meaningfully estimate a long-run “levels model” of the form

| (28) |

Table 10 shows the estimates for (28) where we can see that all countries have negative intercept and positive slope. Thus employment has significantly positive impact at 10% level of significance for all the countries except Canada, with the coefficient ranging from 11% for Canada to 75% for Germany. Italy has a higher coefficient 98% but it may be plagued by bias due to auto-correlation in the errors. We also perform a test of serial correlation in the long-run model (28). The last five columns in Table 10 show the p-values for the alternative hypothesis that the errors are AR(m) for and suggests that the model is appropriate for all the countries except Italy, where errors are serially correlated at the 5% level of significance.

As a final check, we estimate the coefficients of a restricted error correction model of the form

| (29) |

where is a conventional “error-correction term” obtained as the estimated residual series from the long-run relationship (28), that is,

| (30) |

where and are the estimated coefficients in (28). If the model is correct, the coefficient of the lagged error terms should be negative and significant, as can be seen in Table 11. Model diagnostic tests for no-autocorrelation and homoscedasticity are accepted for all countries except Italy.

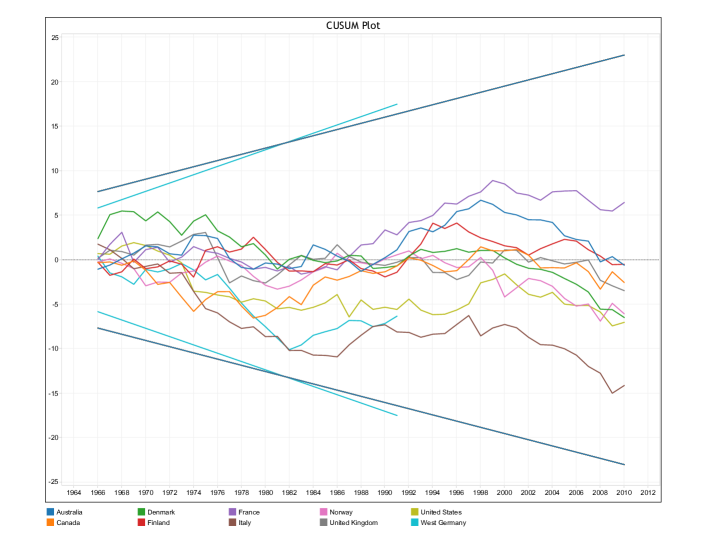

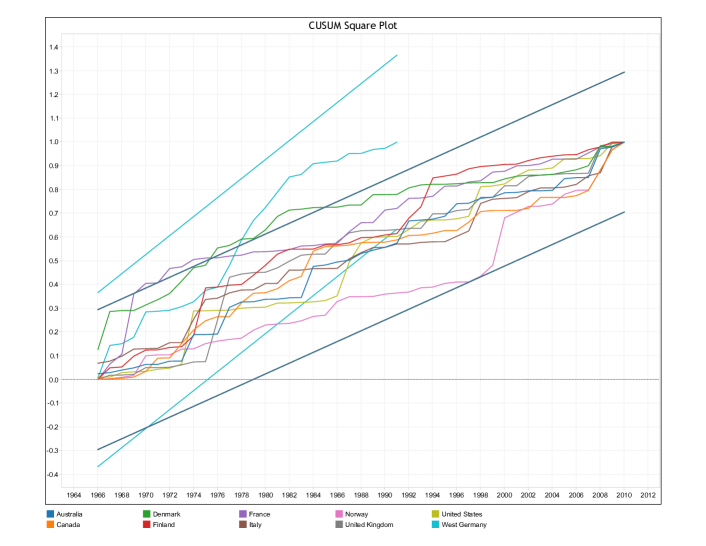

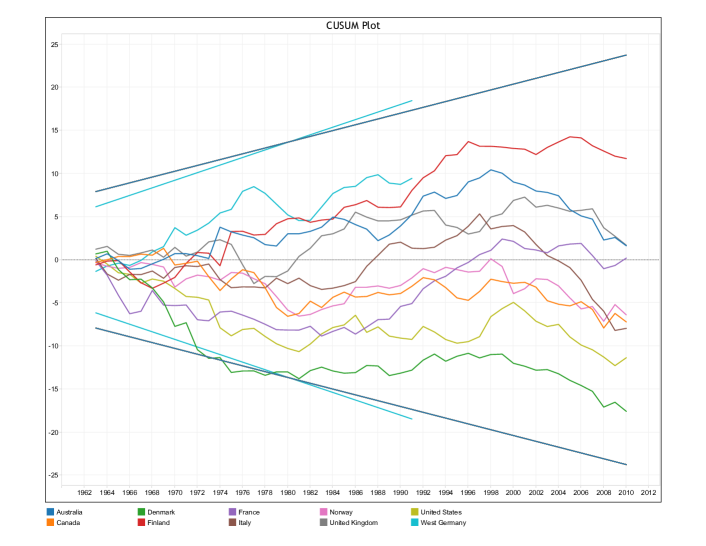

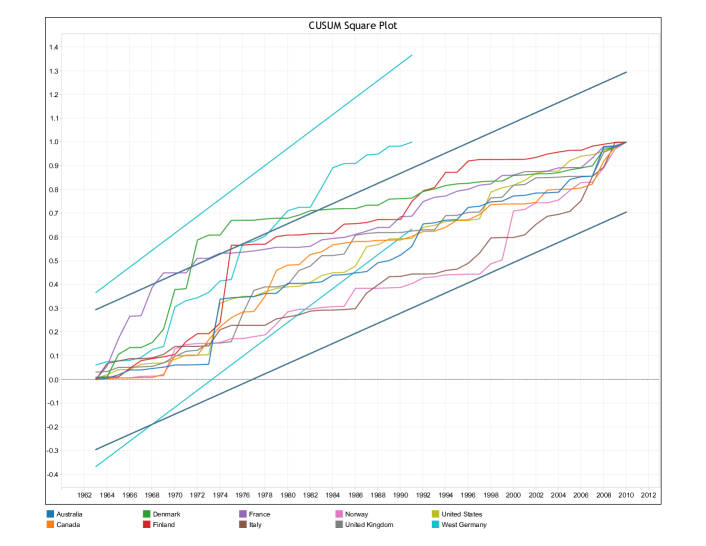

Before computing the equilibrium values arising from the estimated parameters, we check for structural change in the underlying relationship by testing the null hypothesis that the regression coefficients in equations (27) and (28) are constant over time. Figure 7 shows the result of the CUSUM (cumulative sum of recursive residuals) and CUSUMSQ (cumulative sum of recursive squared residuals) tests for the coefficients of (27). We can see fluctuations well within the 99% confidence interval for all countries for the CUSUM test and for all countries except France and Denmark (note that the tests for Germany have different bands because of the smaller number of observations). Very similar results are shown in Figure 8 for the same tests for the coefficients of the long-run model in equation (28). We therefore accept the null hypothesis of constant parameters in equations (27) and (28) throughout the period.

Having ruled out structural breaks in the underlying relationship, we follow Harvie (2000) and obtain the econometric-estimate predictors for the Goodwin equilibrium values and period by substituting these parameter estimates into equations (11)-(13), that is,

| (31) | ||||

| (32) | ||||

| (33) |

These equilibrium estimates for the Goodwin model are presented in Table 2. In this table, the parameter estimates and for the productivity and population growth rate are taken from Tables 5 and 6 respectively. The estimate for the depreciation parameter is the average of the historical depreciation calculated using equation (20). Similarly, the estimate for capital-to-output ratio and capital accumulation rate are the historical averages of the ratios of real capital stock to real output and real investment to real profits, respectively. The estimates and for the parameters of the linear Phillips curve are taken from Table 10.

[ Insert Table 2 here ]

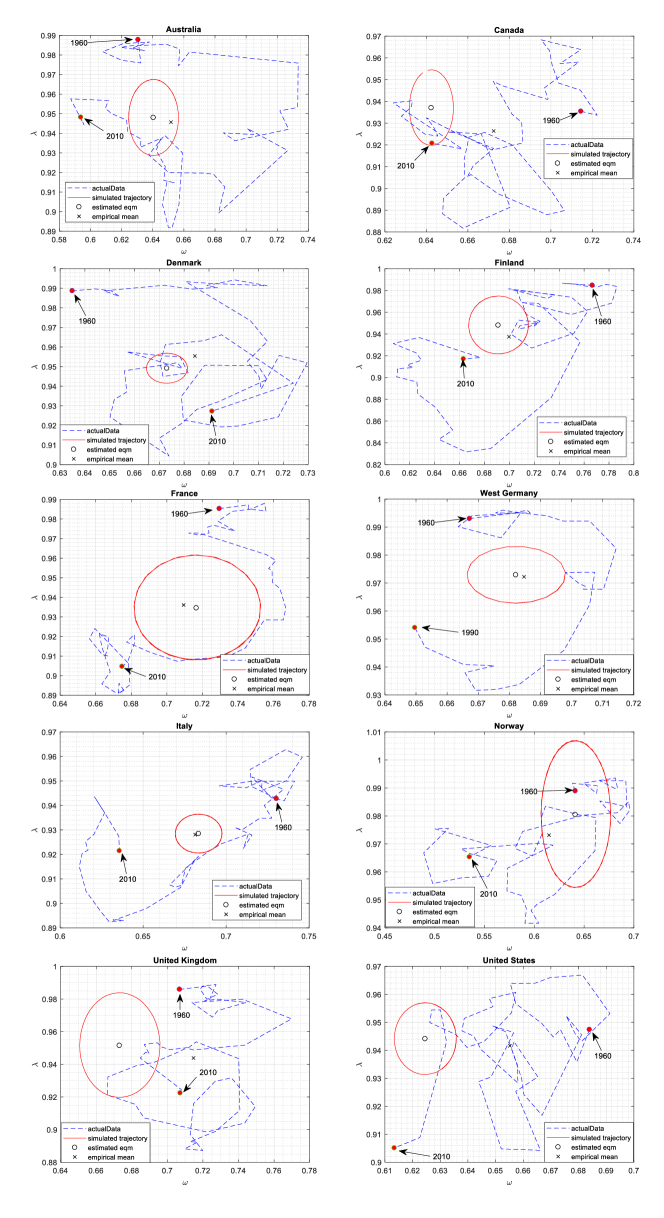

As we can see in Figure 3, the estimates for the equilibrium wage share and employment rate are well within the range of observed values. Table 3 shows the absolute and relative errors for the estimated when compared with the corresponding empirical means over the period. Starting with the employment rate, we see that the absolute difference between the empirical mean reported in Table 1 and the estimated equilibrium value reported in Table 2 is less than 1% for all the countries except Canada and Finland, where the differences are 1.07% and 1.05%, respectively. The relative error for the employment rate ranges from 0.05% for Italy to 1.15% for Canada and averages to 0.53% over the countries in the sample. Compared with the estimated values in Harvie (2000), which were not even inside the range of observed data and had an average relative error of 9.09%, this is a motivating improvement. As mentioned in Section 1, the reason for the high errors in the estimates for equilibrium employment rates reported in Harvie (2000) was the transcription mistake explained in Section 2.2. When correcting for this mistake, as shown in Grasselli and Maheshwari (2017) the average relative error in equilibrium employment rate is reduced from 9.09% to 0.60%, which is comparable with the average relative error of 0.53% obtained here.

Moving on to the wage share, we see from Table 3 that the absolute difference between the empirical mean reported in Table 1 and the estimated equilibrium value reported in Table 2 is less than 3% for all the countries except the UK and the US, where the differences are 4.2% and 3.1%, respectively. The relative error for the wage share ranges from 0.26% for Germany to 5.83% for the UK and averages to 2.54% over the countries in the sample. This is a remarkable improvement in performance when compared with the estimated values in Harvie (2000), which were outside the range of observed data and had an average relative error of nearly 40%, ranging from 22% for the UK to more than 100% for Greece. Even excluding Greece, which is not part of our dataset, the average relative error for the estimated wage share in Harvie (2000) is more than 30%. The improvement in estimates for equilibrium wage share, however, have nothing to do with the transcription mistake in Harvie (2000), since the parameters affected by the mistake only enter in the calculation of the equilibrium employment rate. The improved estimates can be attributed instead to two different factors: (i) a more accurate measurement of the wage share that takes into account self-employment as explained in Section 2.3 and (ii) the introduction of the investment-to-output ratio in (5). As can be seen in expression (32), a lower estimate leads to a lower equilibrium wage share. We see from Table 2 that the estimates are significantly lower one, which is the value implicitly assumed in the original Goodwin model analyzed in Harvie (2000).

[ Insert Figure 3 here ]

4 Simulated Trajectories

Our approach thus far has concentrated on the measure of performance suggested in Harvie (2000) for the Goodwin model, namely the comparison between the estimated equilibrium values for wage share and employment rate and their corresponding empirical means for the period in the sample. An alternative measure consists of analyzing the errors in the actual trajectories, rather than equilibrium values only. In other words, we can simulate the trajectories of the modified Goodwin model implied by the estimated parameters in Table 2 and compute the difference between each observed wage share and employment rate pair and the corresponding pair on the simulated trajectory. Since there is a closed orbit associated with each initial condition, we repeat this procedure using each observed data pair as a candidate initial condition. For each country, we then select the initial condition that minimizes the mean squared error. Finally, we decompose this mean squared error in order to better understand the sources of error. The results are presented in Table 4.

[ Insert Table 4 here ]

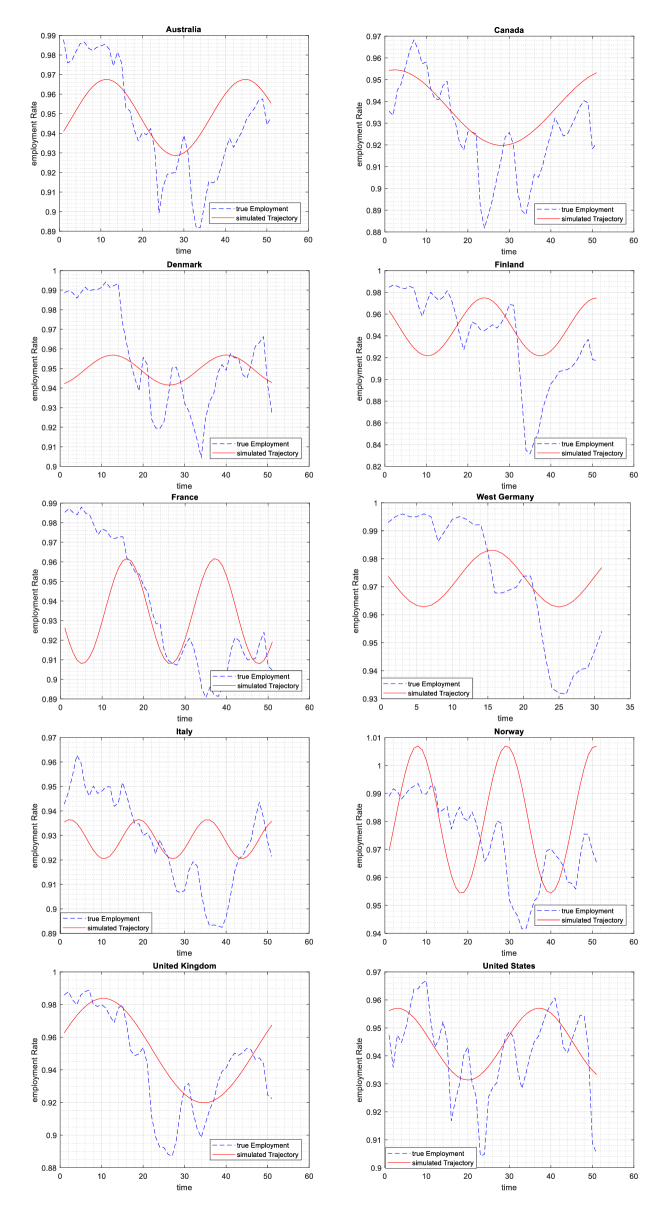

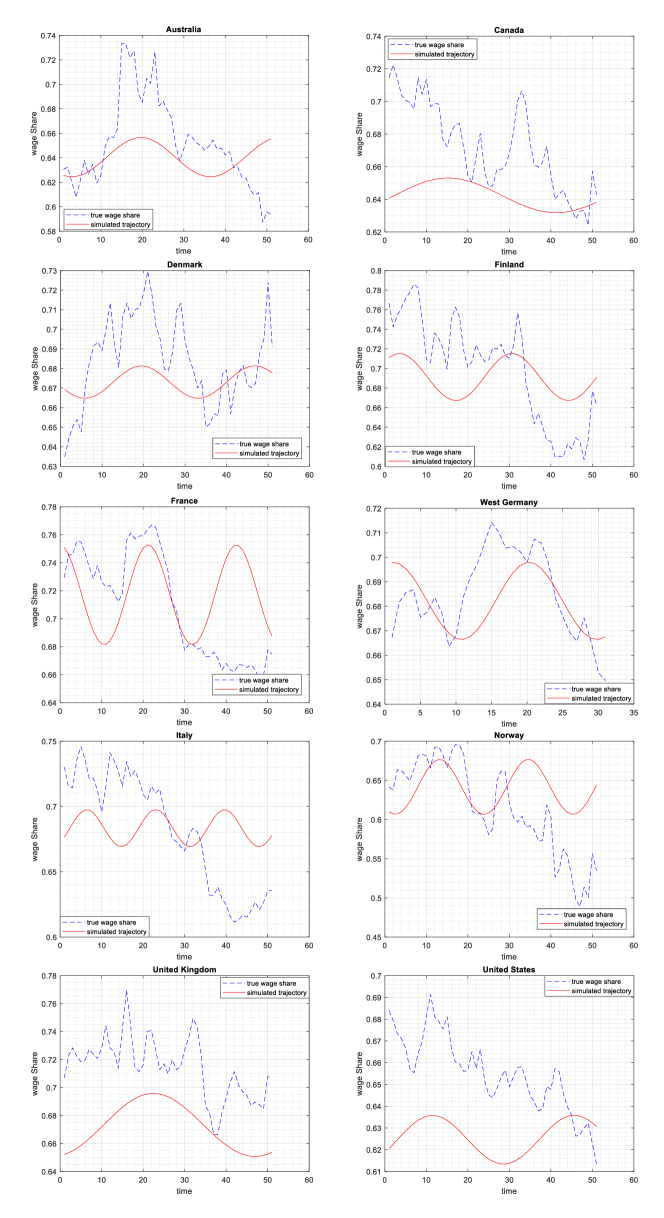

The first column of Table 4 shows the root-mean-square error (RMSE) for employment rate as a fraction of the mean employment rate over the period. We see that this ranges from 1.4% for the US to 4.5% for Finland, with an average of 2.6% across all countries. The next three columns shows the decomposition of the mean squared error (MSE) into a bias, variance, and covariance proportions. The bias proportion indicates how far the mean of the simulated trajectory is from the mean of the observed data, whereas the variance proportion indicates how far the variance of the simulated trajectory is from the variance of the observed data. Together, they measure the proportion of the MSE that is attributed to systematic errors. Accordingly, the covariance proportion measures the remaining unsystematic errors. We see from Table 4 that the bias proportion and the variance proportion contribute on average to 9.5% and 29% of the MSE for employment rate, respectively, so that the covariance proportion is the largest one and contributes on average to 61.5% of the MSE. This is a positive result, but masks large differences between the countries. For example, whereas France is a model case where both the bias (1.5%) and the variance (11.7%) are low, there are examples such as Canada, with a high bias (38.2%) and low variance (9.8%) contributions and other such as Germany, with very low bias (0.2%) but high variance (51.8%) contributions. These differences can be seen in Figure 4, which shows both the observed data and simulated trajectories for the modified Goodwin model.

The last four columns in Table 4 show the corresponding results for the wage share. Consistently with the results in Section 3, where we found that the errors in equilibrium wage share were systematically higher than the ones for employment rate, we see that the RMSE for the simulated wage share as a fraction of the mean wage share for the period is also higher than the ones for employment rate, averaging at 5.8% over all countries. We also see that the average bias (27.9%) and variance (31%) contributions for the MSE in wage share are higher than the corresponding proportions for the employment rate. In other words, not only the MSE are higher for wage share than for employment rate, but they contain a much larger proportion of systematic error. This can be seen in Figure 5, where the agreement between observed and simulated values for wage shares is generally worse than that for employment rate shown in Figure 4. In particular, the Goodwin model is clearly unable to match the decreasing trend in wage share observed in most countries, most notably the US, even though it captures the cyclical fluctuations reasonably well.

5 Concluding remarks

The Goodwin model is a popular gateway to a large literature on endogenous growth cycles, as it serves as the starting point to much more complex models, such as the model proposed in Keen (1995) and its many extensions. Any hope of empirical validation of the extended models, therefore, necessarily needs to be based on a somewhat decent performance of the basic model. The tests performed in Harvie (2000), however, seemed to have dealt these endeavours a fatal blow by showing that the basic Goodwin model was not remotely descriptive of the cycles observed in real data for OECD countries in the second half of the last century.

The main contribution of this paper is to dispense once and for all with this notion. We show that a simple modification of the Goodwin model, namely the introduction of a parameter representing a constant capital accumulation rate, leads to remarkable improvements in performance when compared with the results reported in Harvie (2000). In particular, the estimates for show that it is generally much smaller than one, which corresponds to the implicit assumption in the original Goodwin model. Since a lower value for leads to a lower equilibrium wage share, our estimates for equilibrium wage share are systematically lower than the ones in Harvie (2000) and much closer to the empirical means.

We move beyond a simple comparison between equilibrium values and empirical means and analyze the performance of the simulated trajectories for the modified Goodwin mode. We find that both the simulated employment rates and wage shares lie comfortably within the range of observable values, with the single exception of the simulated wage shares for the UK, which lie below the observed values for the entire period. Moreover, the simulated trajectories are not too far from observed values. For example, the root-mean-square errors for employment rates ranges from 1.4% (US) to 4.5% (Finland) of the mean employment rate, whereas the root-mean-square errors for wage shares ranges from 2.3% (Germany) to 9.3% (Norway) of the mean wage share. Furthermore, we observe that the contribution of unsystematic errors to the mean squared error is on average much larger for employment rates (61.5%) than for wage shares (41.1%).

Nevertheless, even in the modified Goodwin analyzed here has clear and severe limitations. As it is quite apparent, the patterns for observed data shown in Figure 3 do not even remotely resemble the closed orbits predicted by the model, even though the quantitative errors are not as bad as previously believed. In other words, the model is unable to capture more complicated dynamics for employment rates and wage shares, such as the sub-cycles that can be seen for many countries, or the clear downward trend for wage share.

Our results suggest, however, that endogenous growth cycle models based on extensions of the Goodwin model deserve much more empirical explorations. In particular, models incorporating more realistic banking and financial sectors, such as the extension proposed in Keen (1995) and analyzed in Grasselli and Costa Lima (2012) have the potential to improve the estimates of the equilibrium wage share even further, given the more flexible investment behaviour assumed for firms. In addition, models exhibiting a larger variety of dynamic behaviour, such as limit cycles or multiple equilibria, might provide even more accurate descriptions of the type of economic variables treated here.

References

- Asada (2006) Asada, T., 2006. Stabilization policy in a Keynes-Goodwin model with debt accumulation. Structural Change and Economic Dynamics, vol. 17, no. 4, 466 – 485.

- Atkinson (1969) Atkinson, A.B., 1969. The timescale of economic models: How long is the long run? The Review of Economic Studies, vol. 36, no. 2, 137–152.

- Costa Lima et al. (2014) Costa Lima, B., Grasselli, M., Wang, X.S., and Wu, J., 2014. Destabilizing a stable crisis: Employment persistence and government intervention in macroeconomics. Structural Change and Economic Dynamics, vol. 30, 30 – 51.

- Desai (1973) Desai, M., 1973. Growth cycles and inflation in a model of the class struggle. Journal of Economic Theory, vol. 6, no. 6, 527–545.

- Desai (1984) Desai, M., 1984. An econometric model of the share of wages in national income: UK 1855–1965. In Nonlinear Models of Fluctuating Growth: An International Symposium Siena, Italy, March 24–27, 1983, editors R.M. Goodwin, M. Krüger, and A. Vercelli. Springer Berlin Heidelberg, Berlin, Heidelberg, 253–277.

- Desai et al. (2006) Desai, M., Henry, B., Mosley, A., and Pemberton, M., 2006. A clarification of the Goodwin model of the growth cycle. Journal of Economic Dynamics and Control, vol. 30, no. 12, 2661–2670.

- Dibeh et al. (2007) Dibeh, G., Luchinsky, D., Luchinskaya, D., and Smelyanskiy, V., 2007. A Bayesian estimation of a stochastic predator-prey model of economic fluctuations. In Noise and Stochastics in Complex Systems and Finance, editor J.K.S.B.R.N. Mantegna, vol. 6601 of SPIE Proceedings. 10.

- Flaschel (2009) Flaschel, P., 2009. The Goodwin distributive cycle after fifteen years of new observations. In Topics in Classical Micro- and Macroeconomics. Springer Berlin Heidelberg, 465–480.

- Garcia-Molina and Medina (2010) Garcia-Molina, M. and Medina, E., 2010. Are there Goodwin employment-distribution cycles? International empirical evidence. Cuadernos de Economia, vol. 29, 1–29.

- Goldstein (1999) Goldstein, J.P., 1999. Predator-prey model estimates of the cyclical profit squeeze. Metroeconomica, vol. 50, no. 2, 139–173.

- Goodwin (1967) Goodwin, R.M., 1967. A growth cycle. In Socialism, Capitalism and Economic Growth, editor C.H. Feinstein. Cambridge University Press, London, 54–58.

- Grasselli and Costa Lima (2012) Grasselli, M.R. and Costa Lima, B., 2012. An analysis of the Keen model for credit expansion, asset price bubbles and financial fragility. Mathematics and Financial Economics, vol. 6, no. 3, 191–210.

- Grasselli and Maheshwari (2017) Grasselli, M.R. and Maheshwari, A., 2017. A comment on ‘Testing Goodwin: growth cycles in ten OECD countries’. To appear in Cambridge Journal of Economics, doi: 10.1093/cje/bex018.

- Harvie (2000) Harvie, D., 2000. Testing Goodwin: Growth cycles in ten OECD countries. Cambridge Journal of Economics, vol. 24, no. 3, 349–76.

- Keen (1995) Keen, S., 1995. Finance and economic breakdown: Modeling Minsky’s “Financial Instability Hypothesis”. Journal of Post Keynesian Economics, vol. 17, no. 4, 607–635.

- Klump et al. (2007) Klump, R., McAdam, P., and Willman, A., 2007. Factor substitution and factor augmenting technical progress in the U.S. Review of Economics and Statistics, vol. 89, 183–192.

- Massy et al. (2013) Massy, I., Avila, A., and Garcia-Molina, M., 2013. Quantitative evidence of Goodwin’s non-linear growth cycles. Applied Mathematical Sciences, vol. 7, 1409–1417.

- Mohun and Veneziani (2006) Mohun, S. and Veneziani, R., 2006. Goodwin cycles and the U.S. economy, 1948-2004. MPRA paper, University Library of Munich, Germany.

- Moura Jr. and Ribeiro (2013) Moura Jr., N. and Ribeiro, M.B., 2013. Testing the Goodwin growth-cycle macroeconomic dynamics in Brazil. Physica A: Statistical Mechanics and its Applications, vol. 392, no. 9, 2088 – 2103.

- Narayan (2005) Narayan, P.K., 2005. The saving and investment nexus for China: evidence from cointegration tests. Applied Economics, vol. 37, no. 17, 1979–1990.

- Nguyen Huu and Costa-Lima (2014) Nguyen Huu, A. and Costa-Lima, B., 2014. Orbits in a stochastic Goodwin–Lotka–Volterra model. Journal of Mathematical Analysis and Applications, vol. 419, no. 1, 48–67.

- Pesaran et al. (2001) Pesaran, M.H., Shin, Y., and Smith, R.J., 2001. Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, vol. 16, no. 3, 289–326.

- Ryzhenkov (2009) Ryzhenkov, A.V., 2009. A Goodwinian model with direct and roundabout returns to scale (an application to Italy). Metroeconomica, vol. 60, no. 3, 343–399.

- Takeuchi and Yamamura (2004) Takeuchi, Y. and Yamamura, T., 2004. Stability analysis of the Kaldor model with time delays: monetary policy and government budget constraint. Nonlinear Analysis: Real World Applications, vol. 5, no. 2, 277 – 308.

- Tarassow (2010) Tarassow, A., 2010. The empirical relevance of Goodwin’s business cycle model for the US economy. MPRA Paper 21012, University Library of Munich, Germany.

- van der Ploeg (1984) van der Ploeg, F., 1984. Implications of workers’ savings for economic growth and the class struggle. In Nonlinear Models of Fluctuating Growth: An International Symposium Siena, Italy, March 24–27, 1983, editors R.M. Goodwin, M. Krüger, and A. Vercelli. Springer Berlin Heidelberg, Berlin, Heidelberg, 1–13.

- van der Ploeg (1985) van der Ploeg, F., 1985. Classical growth cycles. Metroeconomica, vol. 37, no. 2, 221–230.

- van der Ploeg (1987) van der Ploeg, F., 1987. Growth cycles, induced technical change, and perpetual conflict over the distribution of income. Journal of Macroeconomics, vol. 9, 1–12.

- Wolfstetter (1982) Wolfstetter, E., 1982. Fiscal policy and the classical growth cycle. Zeitschrift für Nationalökonomie, vol. 42, no. 4, 375–393.

- Yoshida and Asada (2007) Yoshida, H. and Asada, T., 2007. Dynamic analysis of policy lag in a Keynes-Goodwin model: Stability, instability, cycles and chaos. Journal of Economic Behavior & Organization, vol. 62, no. 3, 441 – 469.

Appendix A Auxiliary Tables

Appendix B Auxiliary Figures

| Wage Share | Employment Rate | |||

|---|---|---|---|---|

| Country | mean | std | mean | std |

| Australia | 0.6517 | 0.0366 | 0.9457 | 0.0282 |

| Canada | 0.6724 | 0.0268 | 0.9264 | 0.0214 |

| Denmark | 0.6843 | 0.0228 | 0.9554 | 0.0258 |

| Finland | 0.6997 | 0.0539 | 0.9375 | 0.0418 |

| France | 0.7094 | 0.0379 | 0.9361 | 0.0329 |

| Germany | 0.6838 | 0.0180 | 0.9719 | 0.0230 |

| Italy | 0.6814 | 0.0440 | 0.9280 | 0.0193 |

| Norway | 0.6148 | 0.0592 | 0.9731 | 0.0151 |

| United Kingdom | 0.7147 | 0.0215 | 0.9438 | 0.0311 |

| United States | 0.6552 | 0.0172 | 0.9416 | 0.0155 |

| Country | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Australia | 0.015 | 0.020 | 0.052 | 2.881 | -0.215 | 0.242 | 0.694 | 0.6404 | 0.9480 | 33.41 |

| Canada | 0.013 | 0.020 | 0.043 | 2.864 | -0.095 | 0.115 | 0.605 | 0.6424 | 0.9371 | 51.94 |

| Denmark | 0.018 | 0.006 | 0.050 | 2.842 | -0.330 | 0.367 | 0.640 | 0.6730 | 0.9492 | 27.34 |

| Finland | 0.029 | 0.003 | 0.052 | 3.314 | -0.258 | 0.303 | 0.898 | 0.6910 | 0.9480 | 27.10 |

| France | 0.022 | 0.008 | 0.038 | 3.326 | -0.491 | 0.549 | 0.792 | 0.7165 | 0.9346 | 21.25 |

| Germany | 0.028 | 0.006 | 0.036 | 3.367 | -0.705 | 0.753 | 0.735 | 0.6821 | 0.9729 | 19.03 |

| Italy | 0.021 | 0.006 | 0.047 | 3.206 | -0.891 | 0.982 | 0.738 | 0.6833 | 0.9285 | 16.59 |

| Norway | 0.023 | 0.011 | 0.047 | 3.208 | -0.574 | 0.609 | 0.722 | 0.6411 | 0.9804 | 21.41 |

| UK | 0.021 | 0.005 | 0.037 | 3.053 | -0.108 | 0.135 | 0.588 | 0.6731 | 0.9515 | 48.73 |

| US | 0.016 | 0.016 | 0.052 | 2.725 | -0.227 | 0.257 | 0.610 | 0.6245 | 0.9441 | 34.13 |

| Employment rate | Wage share | |||

|---|---|---|---|---|

| Australia | 0.0023 | 0.24% | 0.011 | 1.74% |

| Canada | 0.0107 | 1.15% | 0.030 | 4.47% |

| Denmark | 0.0062 | 0.65% | 0.011 | 1.65% |

| Finland | 0.0105 | 1.12% | 0.009 | 1.24% |

| France | 0.0015 | 0.16% | 0.007 | 1.01% |

| Germany | 0.0010 | 0.10% | 0.002 | 0.26% |

| Italy | 0.0005 | 0.05% | 0.002 | 0.28% |

| Norway | 0.0073 | 0.75% | 0.026 | 4.28% |

| United Kingdom | 0.0077 | 0.82% | 0.042 | 5.83% |

| United States | 0.0025 | 0.27% | 0.031 | 4.68% |

| Average | 0.0050 | 0.53% | 0.017 | 2.54% |

| Employment rate | Wage share | |||||||

|---|---|---|---|---|---|---|---|---|

| Australia | 0.025 | 6.6% | 39.2% | 54.3% | 0.055 | 12.8% | 50.4% | 36.8% |

| Canada | 0.018 | 38.2% | 9.8% | 52.0% | 0.059 | 61.6% | 18.9% | 19.4% |

| Denmark | 0.026 | 5.2% | 65.7% | 29.1% | 0.034 | 23.9% | 50.8% | 25.3% |

| Finland | 0.045 | 4.6% | 29.1% | 66.4% | 0.069 | 3.8% | 57.7% | 38.5% |

| France | 0.042 | 1.5% | 11.7% | 86.8% | 0.058 | 3.6% | 9.7% | 86.7% |

| Germany | 0.023 | 0.2% | 51.8% | 48.0% | 0.023 | 4.1% | 13.6% | 82.3% |

| Italy | 0.021 | 0.1% | 45.1% | 54.8% | 0.064 | 0.2% | 58.8% | 41.1% |

| Norway | 0.023 | 16.1% | 0.01% | 83.9% | 0.093 | 15.5% | 41.0% | 43.5% |

| United Kingdom | 0.023 | 14.0% | 14.81% | 71.2% | 0.069 | 83.4% | 1.2% | 15.4% |

| United States | 0.014 | 8.2% | 23.30% | 68.5% | 0.054 | 70.4% | 7.6% | 22.0% |

| Average | 0.026 | 9.5% | 29.0% | 61.5% | 0.058 | 27.9% | 31.0% | 41.1% |

| Country | Australia | Canada | Denmark | Finland | France | Germany | Italy | Norway | UK | US |

| - | - | - | - | - | - | - | - | - | - | |

| Rsquare | 0.988 | 0.968 | 0.976 | 0.975 | 0.906 | 0.937 | 0.829 | 0.978 | 0.990 | 0.986 |

| adjRsquare | 0.987 | 0.967 | 0.975 | 0.975 | 0.904 | 0.935 | 0.825 | 0.978 | 0.990 | 0.985 |

| Fstat | ||||||||||

| LBQstat | ||||||||||

| JBStat | 2.60 | 1.29 | 5.59 | 4.84 | 2.56 | 5.63 | 0.70 | 1.91 | ||

| ARCHstat |

| Country | Australia | Canada | Denmark | Finland | France | Germany | Italy | Norway | UK | US |

| Rsquare | 0.989 | 0.965 | 0.900 | 0.786 | 0.995 | 0.822 | 0.938 | 0.978 | 0.963 | 0.979 |

| adjRsquare | 0.989 | 0.964 | 0.898 | 0.782 | 0.995 | 0.816 | 0.937 | 0.977 | 0.963 | 0.978 |

| Fstat | ||||||||||

| LBQstat | ||||||||||

| JBStat | 4.21 | 4.45 | 1.72 | 0.92 | 1.75 | 1.33 | 2.88 | 3.17 | 1.76 | |

| ARCHstat |

| Country | real wage growth | employment rate | productivity growth | inflation | nominal wage growth |

| Australia | 0.001 | 0.449 | 0.001 | 0.260 | 0.153 |

| Canada | 0.001 | 0.510 | 0.001 | 0.140 | 0.220 |

| Denmark | 0.404 | 0.535 | 0.001 | 0.410 | 0.200 |

| Finland | 0.001 | 0.073 | 0.001 | 0.160 | 0.424 |

| France | 0.063 | 0.655 | 0.050 | 0.695 | 0.675 |

| Germany | 0.147 | 0.432 | 0.046 | 0.157 | 0.256 |

| Italy | 0.073 | 0.341 | 0.013 | 0.607 | 0.530 |

| Norway | 0.001 | 0.549 | 0.002 | 0.001 | 0.114 |

| UK | 0.001 | 0.293 | 0.001 | 0.223 | 0.138 |

| US | 0.001 | 0.402 | 0.001 | 0.438 | 0.096 |

| Country | lag 1 | lag 2 | lag 3 | lag 4 | lag 5 |

|---|---|---|---|---|---|

| Australia | 0.967 | 0.926 | 0.938 | 0.948 | 0.970 |

| Canada | 0.912 | 0.242 | 0.358 | 0.520 | 0.664 |

| Denmark | 0.742 | 0.946 | 0.279 | 0.334 | 0.463 |

| Finland | 0.714 | 0.841 | 0.432 | 0.594 | 0.732 |

| France | 0.555 | 0.838 | 0.859 | 0.508 | 0.453 |

| Germany | 0.795 | 0.603 | 0.786 | 0.525 | 0.282 |

| Italy | 0.313 | 0.594 | 0.719 | 0.827 | 0.872 |

| Norway | 0.940 | 0.935 | 0.795 | 0.846 | 0.922 |

| UK | 0.948 | 0.997 | 0.869 | 0.323 | 0.425 |

| US | 0.687 | 0.642 | 0.794 | 0.598 | 0.298 |

| Country | Australia | Canada | Denmark | Finland | France | Italy | Norway | UK | US | Germany |

| F statistics | 15.548 | 17.154 | 33.071 | 21.107 | 12.574 | 8.519 | 21.421 | 13.830 | 8.019 | 5.651 |

| Country | Variable | AdjR2 | lag 1 | lag 2 | lag 3 | lag 4 | lag 5 | ||

| Australia | Coeff | -0.215 | 0.242 | 0.086 | |||||

| pValue | 0.031 | 0.022 | 0.155 | 0.363 | 0.560 | 0.646 | 0.743 | ||

| Canada | Coeff | -0.095 | 0.115 | 0.010 | |||||

| pValue | 0.283 | 0.230 | 0.407 | 0.173 | 0.196 | 0.307 | 0.438 | ||

| Denmark | Coeff | -0.330 | 0.367 | 0.216 | |||||

| pValue | 0.001 | 0.000 | 0.397 | 0.298 | 0.061 | 0.109 | 0.181 | ||

| Finland | Coeff | -0.258 | 0.303 | 0.274 | |||||

| pValue | 0.000 | 0.000 | 0.493 | 0.571 | 0.174 | 0.284 | 0.393 | ||

| France | Coeff | -0.491 | 0.549 | 0.755 | |||||

| pValue | 0.000 | 0.000 | 0.090 | 0.237 | 0.406 | 0.210 | 0.311 | ||

| Germany | Coeff | -0.699 | 0.747 | 0.673 | |||||

| pValue | 0.000 | 0.000 | 0.287 | 0.342 | 0.483 | 0.576 | 0.276 | ||

| Italy | Coeff | -0.891 | 0.982 | 0.507 | |||||

| pValue | 0.000 | 0.000 | 0.015 | 0.010 | 0.011 | 0.021 | 0.035 | ||

| Norway | Coeff | -0.574 | 0.609 | 0.039 | |||||

| pValue | 0.100 | 0.090 | 0.868 | 0.852 | 0.745 | 0.800 | 0.891 | ||

| UK | Coeff | -0.108 | 0.135 | 0.045 | |||||

| pValue | 0.131 | 0.076 | 0.085 | 0.168 | 0.289 | 0.078 | 0.097 | ||

| US | Coeff | -0.227 | 0.257 | 0.086 | |||||

| pValue | 0.031 | 0.022 | 0.057 | 0.134 | 0.224 | 0.358 | 0.322 |

| Country | Variable | AdjR2 | |||

|---|---|---|---|---|---|

| Australia | Coeff | 0.000 | 0.023 | -0.826 | 0.390 |

| pValue | 0.944 | 0.941 | 0.000 | ||

| Canada | Coeff | 0.000 | 0.034 | -0.873 | 0.425 |

| pValue | 0.859 | 0.884 | 0.000 | ||

| Denmark | Coeff | -0.001 | 0.343 | -1.097 | 0.586 |

| pValue | 0.654 | 0.176 | 0.000 | ||

| Finland | Coeff | 0.000 | 0.375 | -0.953 | 0.473 |

| pValue | 0.888 | 0.076 | 0.000 | ||

| France | Coeff | -0.001 | 0.103 | -0.679 | 0.330 |

| pValue | 0.436 | 0.663 | 0.000 | ||

| Germany | Coeff | -0.001 | 0.192 | -0.766 | 0.237 |

| pValue | 0.777 | 0.676 | 0.003 | ||

| Italy | Coeff | -0.001 | -0.263 | -0.580 | 0.245 |

| pValue | 0.754 | 0.570 | 0.000 | ||

| Norway | Coeff | 0.000 | 0.902 | -0.983 | 0.469 |

| pValue | 0.963 | 0.388 | 0.000 | ||

| UK | Coeff | 0.000 | 0.278 | -0.762 | 0.355 |

| pValue | 0.981 | 0.279 | 0.000 | ||

| US | Coeff | 0.000 | -0.249 | -0.583 | 0.279 |

| pValue | 0.841 | 0.175 | 0.000 |