Efficient kernel-based variable selection with sparsistency

Abstract

Sparse learning is central to high-dimensional data analysis, and various methods have been developed. Ideally, a sparse learning method shall be methodologically flexible, computationally efficient, and with theoretical guarantee, yet most existing methods need to compromise some of these properties to attain the other ones. In this article, a three-step sparse learning method is developed, involving kernel-based estimation of the regression function and its gradient functions as well as a hard thresholding. Its key advantage is that it assumes no explicit model assumption, admits general predictor effects, allows for efficient computation, and attains desirable asymptotic sparsistency. The proposed method can be adapted to any reproducing kernel Hilbert space (RKHS) with different kernel functions, and its computational cost is only linear in the data dimension. The asymptotic sparsistency of the proposed method is established for general RKHS under mild conditions. Numerical experiments also support that the proposed method compares favorably against its competitors in both simulated and real examples.

Key Words and Phrases: Gradient learning, hard thresholding, ridge regression, RKHS, nonparametric sparse learning

1 Introduction

sparse learning has attracted tremendous interests from both researchers and practitioners, due to the availability of large number of variables in many real applications. In such scenarios, identifying the truly informative variables for the objective of analysis has become a key factor to facilitate statistical modeling and analysis. Ideally, a sparse learning method shall be flexible, efficient, and with theoretical guarantee. To be more specific, the method shall not assume restrictive model assumptions, so that it is applicable to data with complex structures; its implementation shall be computationally efficient and able to take advantage of high performance computing platform; it shall have theoretical guarantee on its asymptotic consistency in identifying the truly informative variables.

In literature, many sparse learning methods have been developed in the regularization framework assuming certain working model set. The most popular working model set is to assume a linear model, where the sparse learning task simplifies to identifying nonzero coefficients. Under the linear model assumption, the regularization framework consists of a least square loss function for the linear model as well as a sparsity-inducing regularization term. Various regularization terms have been considered, including the least absolute shrinkage and selection operator (Lasso; [34]), the smoothly clipped absolute deviation (SCAD; [7]), the adaptive Lasso [44], the minimax concave penalty (MCP; [41]), the truncated -penalty (TLP; [25]), the -penalty [26], and so on. These methods have also been extended to the nonparametric models to relax the linear model assumption. For example, under the additive model assumption, a number of sparse learning methods have been developed [27, 14], where each component function depends on one variable only. Further, a component selection and smoothing operator method (COSSO; [17]) is proposed to allow higher-order interaction components in the additive model. Yet the higher-order additive models need to enumerate all the interaction components, which may explode in an exponential order of the number of variables. These nonparametric sparse learning methods, although more flexible than the linear model, still require some explicit working model sets.

More recently, attempts have been made to develop nonparametric sparse learning methods to circumvent the dependency on restrictive model assumptions. Particularly, sparse learning is formulated in a dimension reduction framework in Li et al. [16] and Bondell and Li [3] via searching for the sparse basis of the central dimension reduction space. Fukumizu and Leng [10] developed a gradient-based dimension reduction method that can be extended to nonparametric sparse learning. A novel measurement-error-model-based sparse learning method is developed in Stefanski et al. [30] and Wu and Stefanski [38] for nonparametric kernel regression models, and some gradient learning methods [22, 39] are proposed to conduct sparse learning in a flexible RKHS [35]. Also, a flexible knock-off filter framework [1] and a recursive feature elimination method by using kernel ridge regression are proposed [5], which show substantial advantage than most existing methods, yet their lack of selection consistency or computational efficiency remain as some of their main obstacles. Specifically, it is also interesting to point out that most existing gradient-based methods [22, 39] aim to directly estimate the gradient functions in a regularization framework with some well-designed penalty terms, and thus they may not be applicable to analyze data with high dimension due to their expensive computational cost.

Another popular line of research on high-dimensional data is variable screening, which screens out uninformative variables by examining the marginal relationship between the response and each variable. The marginal relationship can be measured by various criteria, including the Pearson’s correlation [8], the empirical functional norm [6], the distance correlation [33], and a quantile-adaptive procedure [13]. All these methods are computationally very efficient, and attain the sure screening property, meaning that all the truly informative variables are retained after screening with probability tending to one. This is a desirable property, yet slightly weaker than the asymptotic consistency in sparse learning. Another potential weakness of the marginal screening methods is that they may ignore those marginally unimportant but jointly important variables [13]. To remedy this limitation, some recent work [12, 37] has been done to conduct sure screening for variables with interaction effects.

In this article, we propose an efficient kernel-based sparse learning method, which is methodologically flexible, computationally efficient, and able to achieve the asymptotic consistency without requiring any explicit model assumption. The method consists of three simple steps, involving kernel-based estimation of the regression function and its gradient functions as well as a hard thresholding. It first fits a kernel ridge regression model in a flexible RKHS to obtain an estimated regression function, then estimates its gradient functions along each variable by taking advantage of the derivative reproducing property [43], and finally hard-thresholds the empirical norm of each gradient function to identify the truly informative variables. This method is flexible in that it can be adapted to any RKHS with different kernel functions, to accommodate prior information about the true regression function. The proposed method also enables efficient estimation of the gradient functions in two steps by using the derivative property in RKHS, which significantly reduces the computational cost and allows for diverging dimension. Its computational cost is only linear in the data dimension, and thus computationally efficient to analyze dataset with large dimensions. For example, the simulated examples with variables can be efficiently analyzed on a standard multi-core PC. More importantly, asymptotic consistency can be established for the proposed method without requiring any explicit model assumptions. It is clear that the proposed method is advantageous than the existing methods, as it achieves methodological flexibility, numerical efficiency and asymptotic consistency. To our knowledge, this method is the first one that can achieve these three desirable properties at the same time.

The rest of the article is organized as follows. In Section 2, we present the proposed general kernel-based sparse learning method as well as its computational scheme. In Section 3, the asymptotic consistency of the proposed method is established. Two theoretical examples are provided in In Section 4. In Section 5, the proposed method is extended to select truly informative interaction terms. The numerical experiments on the simulated and real examples are contained in Section 6, followed by a concluding summary in Section 7. All the necessary lemmas and technical proofs are given in Appendix and supplementary materials.

2 Proposed method

2.1 Regression in RKHS

Suppose a random sample are independent copies of , drawn from some unknown distribution with supported on a compact metric space and . Consider a general regression setting,

where is a random error with and , and thus with denoting the conditional distribution of given . It is also assumed that , where is a RKHS induced by some pre-specified kernel function . For each , denote , and the reproducing property of RKHS implies that for any , where is the inner product in .

The RKHS enjoys a number of desirable properties making it particularly suitable for general nonparametric models, including its approximation ability, its functional complexity and derivative reproducing property. To be precise, many popularly used kernels, including Gaussian kernel and Laplace kernel, are universal [31], meaning that their induced RKHS’s are dense in the continuous function space under the infinity norm. This universal approximation property ensures that the kernel-based methods can yield nonparametric estimates with small approximation error in estimating any continuous target function. On the other hand, to characterize statistical properties for nonparametric models, the notion of functional complexity appearing in empirical process are widely employed for theoretical analysis, such as various covering numbers, VC dimension and Rademacher complexity [2]. The RKHS has a very interesting and surprising property that for a unit ball of the RKHS, its Rademacher complexity [2] can be bounded as , where denotes the global Rademacher complexity. In other words, the functional complexity of the bounded ball in the RKHS is less affected by the dimension of variables, and thus a small variance estimator without sacrificing approximation ability for nonparametric estimation can be obtained by kernel-based methods. In addition, in the literature of nonparametric statistics, estimating the gradient function of the target function is generally hard. However, the derivative of any function in a smooth RKHS also has the reproducing property, implying that kernel-based methods have simultaneous convergence behavior in both the function itself and its gradient function with the same rate of convergence under the sup norm.

2.2 Gradient-based sparse learning

In sparse modeling, it is generally believed that only depends on a small number of variables, while others are uninformative. Unlike model-based settings, sparse learning for a general regression model is challenging due to the lack of explicit regression parameters. Here we measure the importance of variables in a regression function by examining the corresponding gradient functions. It is crucial to observe that if a variable is deemed uninformative, the corresponding gradient function

should be exactly zero almost surely. Thus the true active set can be defined as

where with the marginal distribution .

The proposed general sparse learning method is presented in Algorithm 1.

We now give details of each step in Algorithm 1. To obtain in Step 1, we employ the kernel ridge regression model,

| (1) |

where the first term, denoted as , is an empirical version of , and is the associated RKHS-norm of . By the representer theorem [35], the minimizer of (1) must have the form

where and . Then the optimization task in (1) can be solved analytically, with

| (2) |

where , and + denotes the Moore-Penrose generalized inverse of a matrix. When is invertible, (2) simplifies to .

Next, to obtain in Step 2, it follows from Lemma 1 in the supplementary material that for any ,

where . This implies that the gradient function of any can be bounded by its -norm up to some constant. In other words, if we want to estimate within the smooth RKHS, it suffices to estimate itself without loss of information. Consequently, if is obtained in Step 1, can be estimated as for each , where .

In Step 3, it is difficult to evaluate directly, as is usually unknown in practice. We then adopt the empirical norm of as a practical measure,

The estimated active set can be set as for some pre-specified . It is clear that our method can be regarded as a nonparametric joint screening method, which can correctly identify all the truly informative variables acting on the response with a general effect, including those marginally noninformative but jointly informative ones.

The proposed method presented in Algorithm 1 is general in that it can be adapted to any smooth RKHS with different kernel functions, where the choice of kernel function depends on prior knowledge about . For instance, if is known as linear or polynomial function in advance, the RKHS induced by the linear or polynomial kernel can be used. If no prior information about is available, the RKHS induced by the Gaussian kernel can be used, which is known to be universal in the sense that any continuous function can be well approximated by some function in the induced RKHS under the infinity norm [31]. In practice, unless some reliable prior information about is known, it is recommended to consider the RKHS induced by the Gaussian kernel due to its capacity and flexibility.

Remark 1: The proposed method is computationally efficient, whose computational cost is about . The complexity comes from inverting an matrix in (2), and the complexity comes from calculating for . This complexity is particularly attractive in the large--small- scenario, where the computational complexity becomes linear in and parallelization can be employed to further speed up the computation. In some other scenarios with large , the complexity can be too demanding. Some possible improvements are available to alleviate the computational burden by some low rank approximation, such as the random sketch method in Yang et al. [40]. Its computational complexity can be reduced to , where is the sketch dimension to be determined as in [40]. More importantly, the random sketch method is proved to be fast and minimax optimal for fitting the kernel ridge regression.

Remark 2: The estimated regression function is merely an intermediate step for estimating the gradient functions, which is a consistent estimate but converges to the true regression function at some rather slow rate due to the inclusion of the noise variables. We also want to emphasize that the data is only used once to estimate the representer coefficients in (2), and then the estimated gradient function can be estimated directly by using the derivative reproducing property in RKHS by Lemma 1 in the supplementary material.

2.3 Tuning

The proposed method presented in Algorithm 1 consists of two tuning parameters, the ridge parameter and the thresholding parameter . Based on our limited numerical experience, the proposed method performs well and stable when the ridge parameter is sufficiently small in various scenarios. Similar observation on the choice of ridge parameter has also been made in [37]. Therefore, we set and focus on the choice of in all the simulated experiments.

To optimize the selection performance of the proposed method, we employ the stability-based criterion [32] to select the value of . Its key idea is to measure the stability of sparse learning by randomly splitting the training sample into two parts and comparing the disagreement between the two estimated active sets. Specifically, given a thresholding value , we randomly split the training sample into two parts and . Then the proposed method is applied to and and obtains two estimated active sets and , respectively. The disagreement between and is measured by Cohen’s kappa coefficient

where and with and denotes the set cardinality.

The procedure is repeated for times and the estimated sparse learning stability is measured as

Finally, the thresholding parameter is set as , where is some given percentage. In all the simulated experiments, we set as suggested in [32], and the performance of the resultant tuning criterion appears to be satisfactory.

3 Asymptotic sparsistency

Now we establish the asymptotic consistency of the proposed method. First, we introduce an integral operator , given by

for any . Note that if the corresponding RKHS is separable, by the spectral theorem we have

where is an orthonormal basis of , is the eigenvalue of the integral operator , and is the inner product in . By Mercer’s theorem, under some regularity conditions, the eigen-expansion of the kernel function is Therefore, the RKHS-norm of any can be written as

which implies the decay rate of fully characterizes the complexity of the RKHS, and is closely related with various entropy numbers [31].

We denote the cardinality of the true active set as , and both and are allowed to diverge with . The following technical assumptions are made.

Assumption 1: Suppose that is in the range of the -th power of , denoted as , for some positive constant .

Assumption 2: There exist some constants and such that , and , for any

Assumption 3: The distribution of has a -exponential tail with some function ; that is, there exists some constant such that for any .

In Assumption 1, the operator on is self-adjoint and semi-positive definite, and thus its fractional operator is well defined. Furthermore, the range of is contained in if [29], and thus Assumption 1 implies that there exists some function such that , ensuring strong estimation consistency under the RKHS-norm. Similar assumptions are also imposed in [19]. Assumption 2 assumes the boundedness of the kernel function and its gradient functions, and is satisfied by many popular kernels, including the Gaussian kernel and the Sobolev kernel [29, 22, 39] with the compact support condition. Note that the compact support condition is commonly used in machine learning literature [19, 22, 5, 18] for mathematical simplicity, and it may be relaxed by allowing the support to expand with sample size, which leads to some additional treatment in the asymptotic analysis. Assumption 3 characterizes the tail behaviour of the error distribution, which relaxes the commonly-used bounded in machine learning literature [29, 22, 18]. It is general and satisfied by a variety of distributions [37, 42]. For example, if follows a sub-Gaussian distribution or any bounded distribution, Assumption 3 is satisfied with ; if follows a sub-exponential distribution, Assumption 3 is satisfied with for some constant .

Theorem 1.

Suppose Assumptions 1–3 are satisfied. Then with probability at least , there holds

| (3) |

Additionally, let , then with probability at least , there holds

| (4) |

where and denotes the inverse function of .

Theorem 1 establishes the convergence rate of the difference between the estimated regression function and the true regression function in terms of the RKHS-norm. Note that similar results have been established in learning theory literature [28, 29]. Yet these results assume that the response to be uniformly bounded above, which can be too restrictive in practice. Theorem 1 relaxes the restrictive boundness condition by characterizing the tail behaviour of the error term. Theorem 1 also shows that converges to with high probability, which is crucial to establish the asymptotic sparsistency. Note that is spelled out precisely for the subsequent analysis of the asymptotic sparsistency and its dependency on . Note that the convergence result still holds even when diverges with , and the quantities and in (3) and (4) may depend on through , and thus may also diverges with . Yet such dependencies are generally difficult to quantify explicitly in a fully general case [10].

Remark 3: The rate of convergence in Theorem 1 can be strengthened to obtain an optimal strong convergence rate in a minimax sense as in [9]. Yet it requires the random error follows a sub-Gaussian distribution and the decay rate of ’s eigenvalues has an upper bound of polynomial order; that is, for some positive constant and . Then the rate of convergence in (4) can be further improved.

Assumption 4: There exists some positive constant such that

Assumption 4 requires the true gradient function contains sufficient information about the truly informative variables. Unlike most nonparametric models, we measure the significance of each gradient function to distinguish the informative and uninformative variables without any explicit model specification. Note that the required minimal signal strength in Assumption 4 is much tighter than that in many nonparametric sparse learning methods [14, 39], which often require the signal to be bounded away from zero.

Now we establish the asymptotic sparsistency of the proposed sparse learning method.

Theorem 2.

Suppose the assumptions of Theorem 1 and Assumption 4 are satisfied. Let , then we have

Theorem 2 shows that the selected active set can exactly recover the true active set with probability tending to 1. This result is particularly interesting given the fact that it is established for any RKHS with different kernel functions. A direct application of the proposed method and Theorem 2 is to conduct nonparametric sparse learning with sparsistency [33, 13, 39]. If no prior knowledge about the true regression function is available, the proposed method can be applied with a RKHS associated with the Gaussian kernel. Asymptotic sparsistency can be established following Theorem 2 provided that is contained in the RKHS associated with the Gaussian kernel. This RKHS is fairly large as the Gaussian kernel is known to be universal in the sense that any continuous function can be well approximated by some function in the induced RKHS under the infinity norm [31]. The above theoretical results can be further refined when belongs to some specific RKHS, and some theoretical examples are provided in Section 4.

4 Theoretical examples

This section provides some theoretical examples to illustrate the proposed method with the linear and quadratic kernels. Moreover, we also discuss some possible treatments to improve the theoretical results with some additional technical assumptions.

4.1 Linear kernel

Variable selection for linear model is of great interest in statistical literature due to its simplicity and interpretability. Particularly, the true regression function is assumed to be a linear function, , and the true active set is defined as . We also centralize the response and each variable, so that can be discarded from the linear model for simplicity.

We now apply the general results in Section 3 to establish the sparsistency of the proposed algorithm under the linear model. We first scale the original data as and , and let be the RKHS induced by the scaled linear kernel . Then the true regression function can be rewritten as . With the scaled data, the ridge regression formula in (1) becomes

| (5) |

By the representer theorem, the solution of (5) is

| (6) |

where and . It is equivalent to the standard formula for the ridge regression according to the Sherman-Morrison-Woodbury formula [37]. If we let , the estimate in (6) is exactly the same as the HOLP estimate in [37]. In other words, the HOLP method can be regarded as a special case of our proposed algorithm with the RKHS induced by the linear kernel.

Corollary 1.

Suppose that Assumptions S1 in the supplementary material is met. Let , then for any , there exists some positive constant such that, with probability at least , there holds

Additionally, suppose that Assumption S2 in the supplementary material is met. If let , then we have

where and are provided in Assumption S2.

Note that Corollary 1 holds when diverges at order Particularly, when is sufficiently small, can diverge at the polynomial rate . This result is comparable with that in Shao and Deng [23] under the finite second moment error assumption. The strong convergence rate obtained in Corollary 1 is also comparable with that in Theorem 2 of [23], and similar result holds for the required minimal signal strength.

Remark 4: Note that the proposed algorithm requires , and thus needs to be bounded, which implies that should be fixed in the linear case. Interestingly, if we take and all the technical assumptions stated in [37] are met, including that follows a spherically symmetric distribution and the noise has q-exponential tail, we can directly apply the theoretical results of the HOLP method to establish a similar selection consistency in Corollary 1. As a direct consequence, and are allowed to diverge at some exponential and polynomial rate of , respectively.

4.2 Quadratic kernel

Variable selection for quadratic model is of great interest in statistical literature [12, 15, 24], where the true regression function is assumed to be , where ’s are the true interaction coefficients and implies that and have an interaction effect. The true active set is defined as

which contains variables contributing to through either the main factors or the interaction terms. For simplicity, we denote , and with and Then, we scale the original data as and , and let be the RKHS induced by a scaled quadratic kernel . The true regression model can be rewritten as . Note that the quadratic model can be transformed into a linear form, then the established results in Section 4.1 can be directly applied. Specifically, with the scaled data, the ridge regression formula in (1) becomes

| (7) |

Then the estimated active set is defined as with some pre-specified thresholding value .

With some slight modification of the proof of Corollary 1, we obtain the following convergence results for the scaled quadratic kernel.

Corollary 2.

Suppose that Assumptions S3 in the supplementary material is met. Let , then for any , there exists some positive constant such that, with probability at least , there holds

Additionally, suppose that Assumption S4 in the supplementary material is met. if let , then we have

where and are provided in Assumption S4.

Note that the treatment in this subsection can be further extended to the polynomial regression model with degree by using the scaled polynomial kernel , and similar theoretical results can be established for the proposed algorithm with the scaled polynomial kernel.

5 An extension: interaction selection

We now extend the proposed method to identify the truly informative interaction effects. In literature, a number of attempts have been made to identify the true interaction effects in both parametric and nonparametric regression models [17, 4, 20, 12, 11]. Yet, most existing methods require some pre-specified working models and some of them are computationally demanding. For example, the COSSO method [17] and the SpIn method [20] assume a second-order additive structure and need to enumerate two-way interaction terms in the model, making their methods feasible only when is relatively small. By contrast, our method can be extended directly and provide an efficient alternative for interaction selection without explicit model assumption.

Following the idea in Section 2, the true interaction effects can be defined as those with nonzero second-order gradient function . Specifically, given the true active set , we denote

which contains the variables that contribute to the interaction effects in . Further, let , which contains the variables that contribute to the main effects of only.

Therefore, the main goal of interaction selection is to correctly estimate both and . First, let be a forth-order differentiable kernel function, then it follows from Lemma 1 in the supplementary material that for any ,

where . Then, given from (1), its second-order gradient function is

where . Its empirical norm is . With some pre-defined thresholding value , the estimated and are set as

respectively. The following technical assumption is made to establish the interaction selection consistency for the proposed method.

Assumption 5: There exists some constant such that for any and .

Assumption 5 can be regarded as the extension of Assumptions 2 by requiring the boundedness of the second-order gradients of .

Theorem 3.

Suppose the assumptions of Theorem 2 and Assumption 5 are met. Let . Then with probability at least , there holds

where .

Theorem 3 shows that converges to with high probability, which is crucial to establish the interaction selection consistency.

Assumption 6: There exists some positive constant such that .

Assumption 6 can be regarded as the extension of Assumption 3 by requiring the true second-order gradient functions have sufficient information about the interaction effects.

Theorem 4.

Suppose the assumptions of Theorem 3 as well as Assumption 6 are met. By taking , we have

Theorem 4 shows that the proposed interaction selection method can exactly detect the interaction structure with probability tending to 1. Note that this result is established without requiring the strong heredity assumption, which is often assumed by the existing parametric interaction selection methods [4, 12]. It is also clear that the proposed method can be extended to detect higher-order interaction effects, which is of particular interest in some real applications [21].

6 Numerical experiments

In this section, the numerical performance of the proposed method is examined, and compared against some existing methods, including the distance correlation learning [33] and the quantile-adaptive screening [13]. As these two methods are designed for screening only, they are also truncated by some thresholding values to conduct sparse learning. For simplicity, we denote these three methods as GM, DC-t and QaSIS-t, respectively. Note that the computational cost of most existing gradient-based methods [22, 39] can be very expensive, and thus they are not included in the numerical comparison with large dimension.

In all the simulation examples, no prior knowledge about the true regression function is assumed, and the Gaussian kernel is used to induce the RKHS, where is set as the median of all the pairwise distances among the training sample. For the proposed method, we set the ridge parameter in all simulated examples, and use the stability criterion in Section 2.3 to conduct a grid search for the optimal thresholding parameter , where the grid is set as .

6.1 Simulated examples

Two simulated examples are examined under various scenarios.

Example 1: We first generate with , where and are independently drawn from . The response is generated as where , with , , and ’s are independently drawn from . Clearly, the first variables are truly informative.

Example 2: The generating scheme is similar to Example 1, except that and are independently drawn from and . The first variables are truly informative.

For each example, we consider scenarios with and . For each scenario, and are examined. When , the variables are completely independent, whereas when , correlation structure are added among the variables. Each scenario is replicated times. The averaged signal-to-noise ratios (SNR) of the simulated examples under different scenarios are summarized in Table 1. The averaged performance measures are summarized in Tables 2 and 3, where Size is the averaged number of selected informative variables, TP is the number of truly informative variables selected, FP is the number of truly uninformative variables selected, C, U, O are the times of correct-fitting, under-fitting, and over-fitting, respectively.

| Tables 1 – 3 about here |

Clearly, the SNRs of the simulated examples are comparable to those in [17, 14]. It is evident that GM outperforms the other methods in both examples. In Example 1, GM is able to identify all the truly informative variables in most replications. However, the other two methods tend to miss some truly informative variables, probably due to the interaction effect between and . In Example 2, with a three-way interaction term involved in , GM is still able to identify all the truly informative variables with high accuracy, but the other two methods tend to underfit by missing some truly informative variables in the interaction term. It is also interesting to notice that GM tends to overselect variables in some cases, which is generally less severe than under-selecting truly informative variables.

Note that if we do not threshold DC and QaSIS, they tend to overfit almost in every replication as both screening methods tend to keep a substantial amount of uninformative variables to attain the sure screening property. Furthermore, when the correlation structure with is considered, identifying the truly informative variables becomes more difficult, and both DC-t and QaSIS-t become unstable, yet GM still outperforms these two competitors and can exactly identify all the truly informative variables in most replications.

6.2 Supermarket dataset

We now apply the proposed method to a supermarket dataset in Wang [36]. The dataset is collected from a major supermarket located in northern China, consisting of daily sale records of products on days. In this dataset, the response is the number of customers on each day, and the variables are the daily sale volumes of each product. The primary interest is to identify the products whose sale volumes are related with the number of customers, and then to design sale strategies based on those products. The dataset is pre-processed so that both the response and predictors have zero mean and unit variance.

In addition to GM, DC-t and QaSIS-t, we also include the comparisons with SCAD [7] and MCP [41]. As the truly informative variables are unknown for the supermarket dataset, we report the prediction performance of each method. Specifically, the supermarket dataset is randomly split into two parts, with 164 observations for testing and the remaining for training. We first apply each method to the full dataset to select the informative variables, and then refit a kernel ridge regression model for the nonparametric methods and a linear ridge regression for the parametric methods with the selected variables on the training set. The prediction performance of each ridge regression model is measured on the testing set. The procedure is replicated 1000 times, and the number of selected variables, the averaged prediction errors and the out of sample the are summarized in Table 4.

| Table 4 is about here |

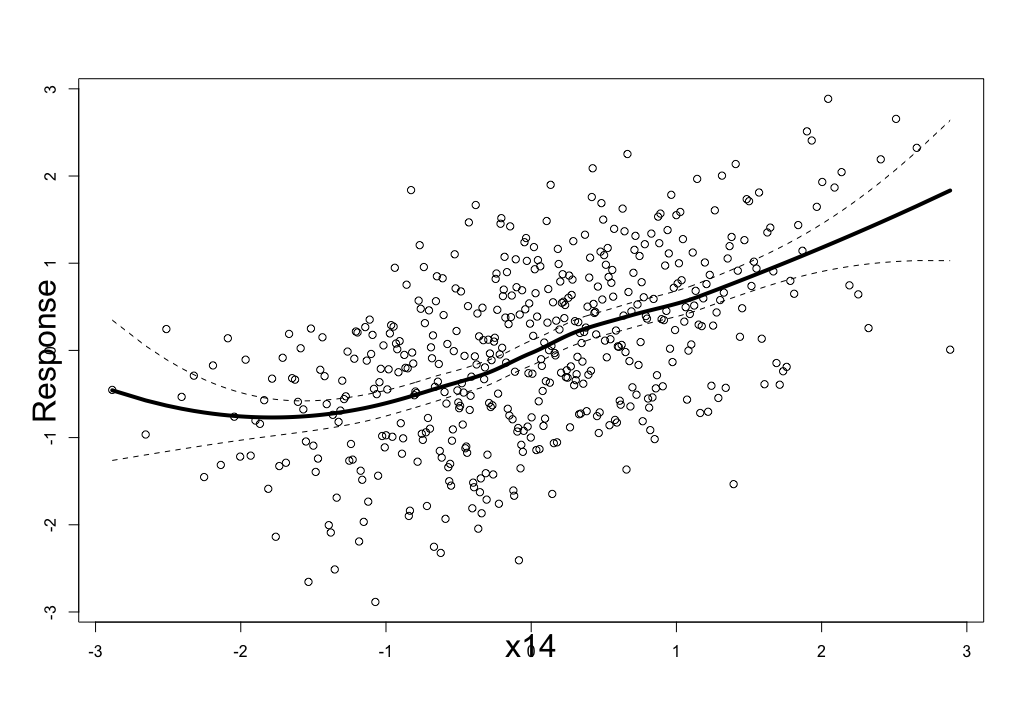

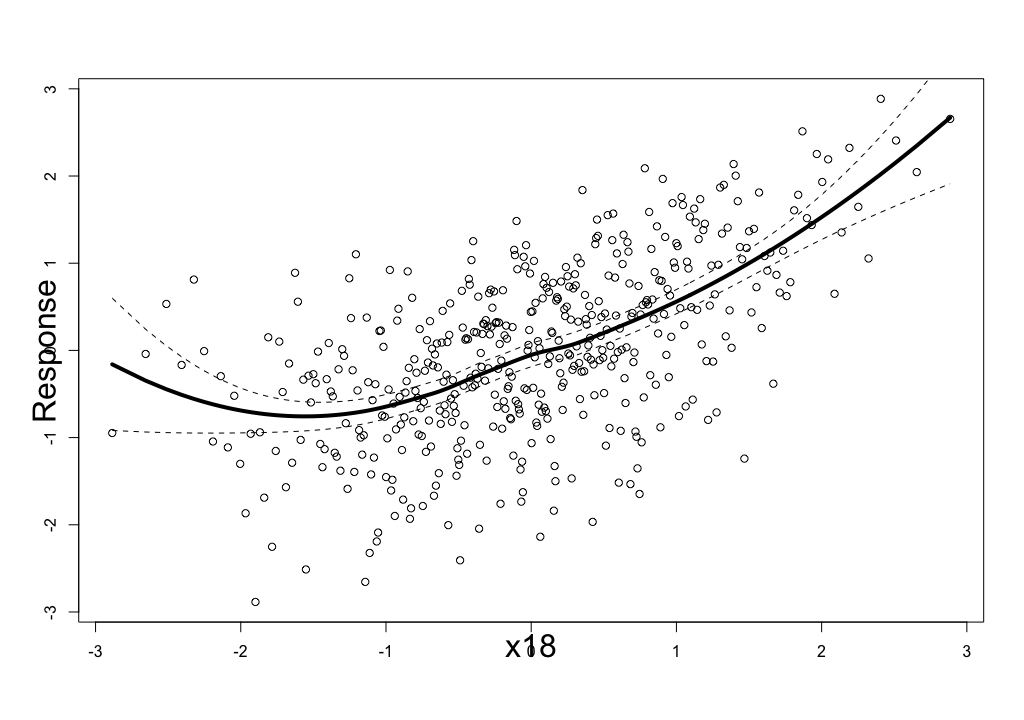

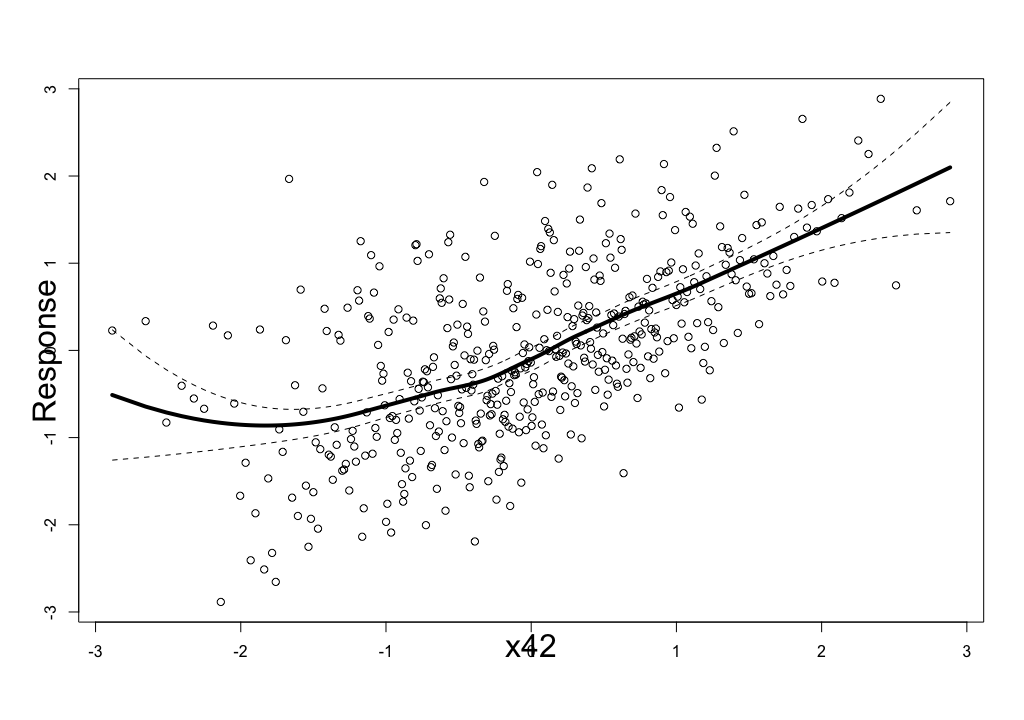

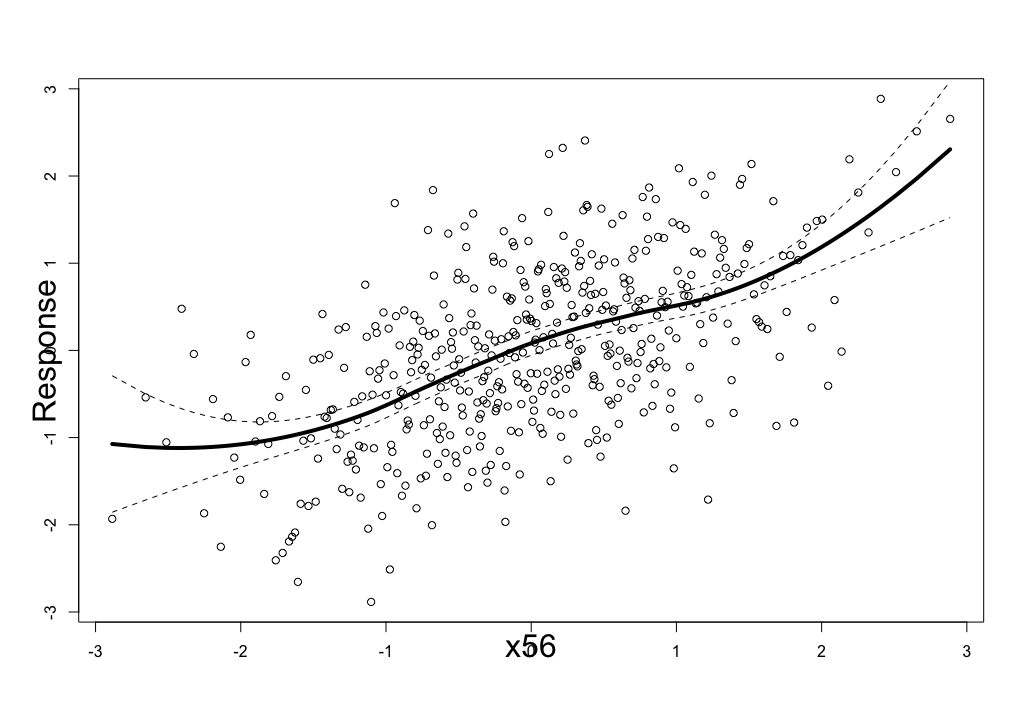

As Table 4 shows, GM selects 10 variables, whereas DC-t and QaSIS-t select 7 variables and SCAD and MCP select 59 and 28 variables, respectively. The average prediction error of GM is smaller than that of the other four methods, implying that DC-t and QaSIS-t may miss some truly informative variables that deteriorate their prediction accuracy, and SCAD and MCP may include too many noise variables. Precisely, among the 10 selected variables by GM, and are missed by both DC-t and QaSIS-t. The scatter plots of the response against these five variables are presented in Figure 1.

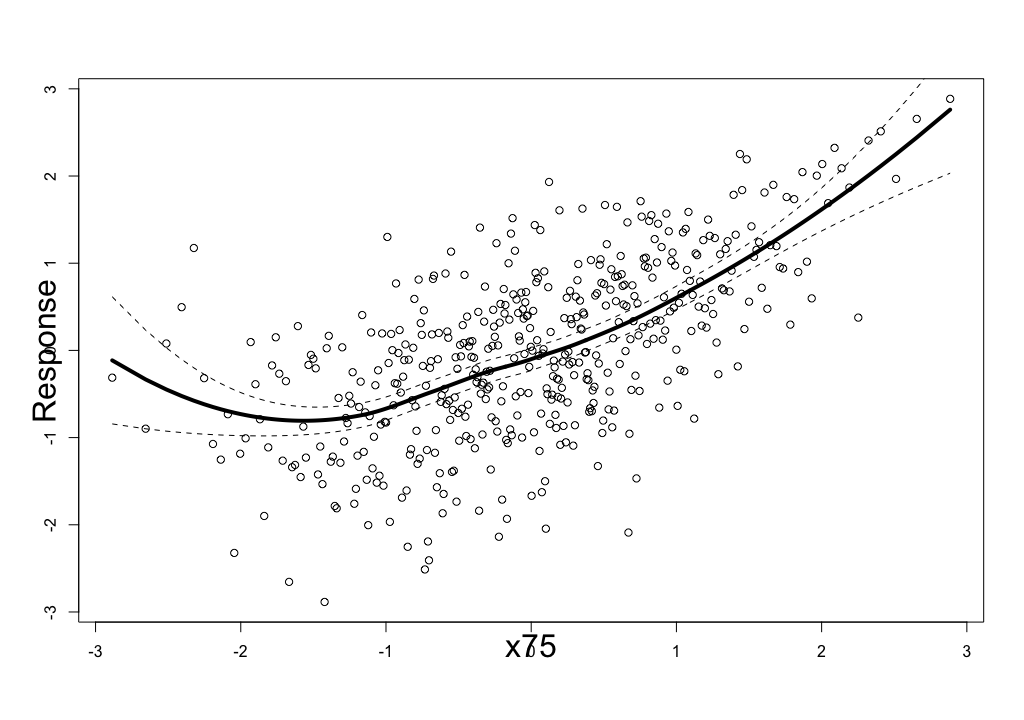

| Figure 1 is about here |

It is evident that the response and these variables have shown some clear relationship, which supports the advantage of GM in identifying the truly informative variables.

7 Summary

This article proposes a novel gradient-based sparse learning method, which can simultaneously enjoy methodological flexibility, numerical efficiency and asymptotic consistency. It provides a novel and promising way to conduct sparse learning for nonparametric models. The proposed method is simple and efficient in that the kernel ridge regression has analytic solution and the estimated gradient functions can be directly computed by using the derivative reproducing property [43]. It can be easily scaled up to analyze datasets with huge dimensions. The theoretical results are established without requiring any restrictive model assumption, which justifies the robustness of the proposed method to the underlying data distribution.

One interesting future work is to consider a more general scenario with out of the specified RKHS , such as a non-differentiable . One possible remedial route is to consider the true active set , where measures the largest possible change of along , and denotes all variables except for . Then the equivalence between and the gradients of some intermediate function is to be examined in order to bridge the gap between and . Another interesting future work is to extend the proposed method to deal with mixed-type predictors, and can also be used to measure the significance of each variable.

Supplementary materials

Proofs of Theorems 3 and 4, some necessary lemmas and their proofs as well as verification of the theoretical examples are provided in the supplementary materials.

Acknowledgment

Xin He’s research was supported in part by NSFC-11901375 and Shanghai Pujiang Program 2019PJC051. Junhui Wang’s research was supported in part by HK RGC Grants GRF-11303918 and GRF-11300919. Shaogao Lv’s research was partially supported by NSFC-11871277. The authors also thank the associate editor and two anonymous referees for their constructive suggestions.

Appendix: technical proof

Proof of Theorem 1. For simplicity, we denote two events

and denotes the complement of . Then can be decomposed as

For , by Assumption 3, we have

| (8) |

By Assumption 1 and (8), for any , with probability at least , there holds

implying that .

For , note that

We first bound following the similar treatment as in Smale and Zhou [28]. Suppose are the normalized eigenpairs of the integral operator , we have

and

when . Thus by Assumption 1, there exists some function such that . Directly calculation yields to

Therefore, the RKHS-norm of can be bounded as

| (9) |

It then follows from Proposition 1 in the supplemental material that

Combining the upper bounds of and yields that . Thus, with probability at least , there holds

Now we turn to establish the weak convergence rate of in estimating . We first introduce some notations. Define the sample operators for gradients and their adjoint operators as

respectively. And the integral operators for gradients and are defined as

Note that and are the Hilbert-Schimdt operators by Propositions and of Rosasco et al. [22], then we have

Furthermore, we denote as a Hilbert space with all the Hilbert-Schmidt operators on , which endows with a norm such that for any .

With these operators, simple algebra yields that

where the last inequality follows from the Cauthy-Schwartz inequality. It then suffices to bound the terms in the upper bound of separately. Note that is a bounded quantity, and it follows from Assumption 2 and Rosasco et al. [22] that . Hence, we have

where . When is sufficiently small, the upper bound can be simplified to

where is bounded in the first half of the proof. Furthermore, for any , by the concentration inequalities for [22], we have

for any . Therefore, with probability at least , there holds

Combining all the upper bounds above, we have with probability at least , there holds

This implies the desired results immediately with .

Proof of Theorem 2. We first show that in probability. If not, suppose there exists some but , and thus . By Assumption 4, we have with probability that

which contradicts with Theorem 1. This implies that with probability at least .

Next, we show that in probability. If not, suppose there exists some but , which implies but , and then with probability at least , there holds

This contradicts with Theorem 1 again, and thus with probability at least . Combining these two results yields the desired sparsistency.

References

- [1] R. Barber and E. Cands. Controlling the false discovery rate via knockoffs. Annals of Statistics, 43:2055–2085, 2015.

- [2] P. Bartlett and S. Mendelson. Rademacher and gaussian complexities: risk bounds and structural results. Journal of Machine Learning Research, 3:463–482, 2002.

- [3] H. Bondell and L. Li. Shrinkage inverse regression estimation for model free variable selection. Journal of the Royal Statistical Society, Series B, 71:287–299, 2009.

- [4] N. Choi, W. Li, and J. Zhu. Variable selection with the strong heredity constraint and its oracle property. Journal of the American Statistical Association, 105:354–364, 2010.

- [5] S. Dasgupta, Y. Goldberg, and M. Kosorok. Feature elimination in kernel machines in moderately high dimensions. Annals of Statistics, 47:497–526, 2019.

- [6] J. Fan, Y. Feng, and R. Song. Nonparametric independence screening in sparse ultrahigh dimensional additive models. Journal of the American Statistical Association, 106:544–557, 2011.

- [7] J. Fan and R. Li. Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American Statistical Association, 96:1348–1360, 2001.

- [8] J. Fan and J. Lv. Sure independence screening for ultrahigh dimensional feature space (with discussion). Journal of the Royal Statistical Society, Series B, 70:849–911, 2008.

- [9] S. Fischer and I. Steinwart. Sobolev norm learning rates for regularized least square algorithm. Manuscript, 2019.

- [10] K. Fukumizu and C. Leng. Gradient-based kernel dimension reduction for regression. Journal of the American Statistical Association, 109:359–370, 2014.

- [11] N. Hao, Y. Feng, and H. Zhang. Model selection for high dimensional quadratic regression via regularization. Journal of the American Statistical Association, 113:615–625, 2018.

- [12] N. Hao and H. Zhang. Interaction screening for ultra-high dimensional data. Journal of the American Statistical Association, 109:1285–1301, 2014.

- [13] X. He, L. Wang, and H. Hong. Quantile-adaptive model-free variable screening for high-dimensional heterogeneous data. Annals of Statistics, 41:342–369, 2013.

- [14] J. Huang, J. Horowitz, and F. Wei. Variable selection in nonparametric additive models. Annals of Statistics, 38:2282–2313, 2010.

- [15] Y. Kong, D. Li, Y. Fan, and J. Lv. Interaction pursuit in high-dimensional multi-response regression via distance correlation. Annals of Statistics, 45:897–922, 2017.

- [16] B. Li, H. Zha, and F. Chiaromonte. Contour regression: a general approach to dimension reduction. Annals of Statistics, 33:1580–1616, 2005.

- [17] Y. Lin and H. Zhang. Component selection and smoothing in multivariate nonparametric regression. Annal of Statistics, 34:2272–2297, 2006.

- [18] S. Lv, H. Lin, H. Lian, and J. Huang. Oracle inequalities for sparse additive quantile regression in reproducing kernel hilbert space. Annals of Statistics, 2:781–813, 2018.

- [19] S. Mendelson and J. Neeman. Regularization in kernel learning. Annal of Statistics, 38:526–565, 2010.

- [20] P. Radchenko and G. James. Variable selection using adaptive nonlinear interaction structures in high dimensions. Journal of the American Statistical Association, 105:1541–1553, 2010.

- [21] M. Ritchie, L. Hahn, N. Roodi, L. Bailey, W. Dupont, F. Parl, and J. Moore. Multifactor-dimensionality reduction reveals high-order interactions among estrogen-metabolism genes in sporadic breast cancer. The American Journal of Human Genetics, 69:138–147, 2001.

- [22] L. Rosasco, S. Villa, S. Mosci, M. Santoro, and A. Verri. Nonparametric sparsity and regularization. Journal of Machine Learning Research, 14:1665–1714, 2013.

- [23] J. Shao and X. Deng. Estimation in high-dimensional linear models with deterministic design matrices. Annals of Statistics, 40:1821–1831, 2012.

- [24] Y. She, Z. Wang, and H. Jiang. Group regularized estimation under structural hierarchy. Journal of the American Statistical Association, in press, 2018.

- [25] X. Shen, W. Pan, and Y. Zhu. Likelihood-based selection and sharp parameter estimation. Journal of the American Statistical Association, 107:223–232, 2012.

- [26] X. Shen, W. Pan, Y. Zhu, and Z. Zhou. On constrained and regularized high-dimensional regression. Annals of the Institute of Statistical Mathematics, 65:807–832, 2013.

- [27] T. Shively, R. Kohn, and S. Wood. Variable selection and function estimation in additive non-parametric regression using a data-based prior. Journal of the American Statistical Association, 94:777–794, 1999.

- [28] S. Smale and D. Zhou. Shannon sampling ii: connections to learning theory. Applied and Computational Harmonic Analysis, 19:285–302, 2005.

- [29] S. Smale and D. Zhou. Learning theory estimates via integral operators and their approximations. Constructive Approximation, 26:153–172, 2007.

- [30] L. Stefanski, Y. Wu, and K. White. Variable selection in nonparametric classification via measurement error model selection likelihoods. Journal of the American Statistical Association, 109:574–589, 2014.

- [31] I. Steinwart and A. Christmann. Support Vector Machine. Springer, 2008.

- [32] W. Sun, J. Wang, and Y. Fang. Consistent selection of tuning parameters via variable selection stability. Journal of Machine Learning Research, 14:3419–3440, 2013.

- [33] G. Szekely, M. Rizzo, and N. Bakirov. Measuring and testing dependence by correlation of distances. Annals of Statistics, 35:2769–2794, 2007.

- [34] R. Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society, Series B, 58:267–288, 1996.

- [35] G. Wahba. Support vector machines, reproducing kernel hilbert spaces, and randomized gacv. Advances in kernel methods: support vector learning, pages 69–88, MIT Press, 1998.

- [36] H. Wang. Forward regression for ultra-high dimensional variable screening. Journal of the American Statistical Association, 104:1512–1524, 2009.

- [37] X. Wang and C. Leng. High dimensional ordinary least squares projection for screening variables. Journal of the Royal Statistical Society, Series B, 78:589–611, 2016.

- [38] Y. Wu and L. Stefanski. Automatic structure recovery for additive models. Biometrika, 102:381–395, 2015.

- [39] L. Yang, S. Lv, and J. Wang. Model-free variable selection in reproducing kernel hilbert space. Journal of Machine Learning Research, 17:1–24, 2016.

- [40] Y. Yang, M. Pilanci, and M. Wainwright. Randomized sketches for kernels: fast and optimal nonparametic regression. Annals of Statistics, 45:991–1023, 2017.

- [41] C. Zhang. Nearly unbiased variable selection under minimax concave penalty. Annals of Statistics, 38:894–942, 2010.

- [42] C. Zhang, Y. Liu, and Y. Wu. On quantile regression in reproducing kernel hilbert spaces with data sparsity constraint. Journal of Machine Learning Research, 17:1–45, 2016.

- [43] D. Zhou. Derivative reproducing properties for kernel methods in learning theory. Journal of Computational and Applied Mathematics, 220:456–463, 2007.

- [44] H. Zou. The adaptive lasso and its oracle properties. Journal of the American Statistical Association, 101:1418–1429, 2006.

| Example 1 | 5.00 | 3.87 | 5.06 | 3.87 |

|---|---|---|---|---|

| Example 2 | 3.58 | 4.23 | 3.55 | 4.20 |

| Method | Size | TP | FP | C | U | O | |

|---|---|---|---|---|---|---|---|

| (400,500,0) | GM | 5.00 | 5.00 | 0.00 | 50 | 0 | 0 |

| QaSIS-t | 4.28 | 4.28 | 0.00 | 22 | 28 | 0 | |

| DC-t | 4.80 | 4.80 | 0.00 | 40 | 10 | 0 | |

| (400,1000,0) | GM | 4.98 | 4.98 | 0.00 | 49 | 1 | 0 |

| QaSIS-t | 4.32 | 4.32 | 0.00 | 21 | 29 | 0 | |

| DC-t | 4.78 | 4.78 | 0.00 | 39 | 11 | 0 | |

| (500,10000,0) | GM | 5.00 | 5.00 | 0.00 | 50 | 0 | 0 |

| QaSIS-t | 4.28 | 4.28 | 0.00 | 24 | 26 | 0 | |

| DC-t | 4.68 | 4.68 | 0.00 | 36 | 0 | 14 | |

| (500,50000,0) | GM | 5.06 | 4.98 | 0.08 | 45 | 1 | 4 |

| QaSIS-t | 4.08 | 4.08 | 0.00 | 18 | 32 | 0 | |

| DC-t | 4.48 | 4.48 | 0.00 | 28 | 22 | 0 | |

| (500, 100000,0) | GM | 5.18 | 5.00 | 0.18 | 43 | 0 | 7 |

| QaSIS-t | 3.98 | 3.98 | 0.00 | 8 | 42 | 0 | |

| DC-t | 4.52 | 4.52 | 0.00 | 28 | 22 | 0 | |

| (400,500,1) | GM | 4.98 | 4.98 | 0.00 | 49 | 1 | 0 |

| QaSIS-t | 2.80 | 2.72 | 0.08 | 0 | 50 | 0 | |

| DC-t | 2.94 | 2.94 | 0.00 | 0 | 50 | 0 | |

| (400,1000,1) | GM | 4.96 | 4.96 | 0.00 | 48 | 2 | 0 |

| QaSIS-t | 2.34 | 2.26 | 0.08 | 0 | 50 | 0 | |

| DC-t | 2.96 | 2.96 | 0.00 | 0 | 50 | 0 | |

| (500,10000,1) | GM | 4.94 | 4.94 | 0.00 | 47 | 3 | 0 |

| QaSIS-t | 2.38 | 2.28 | 0.10 | 0 | 50 | 0 | |

| DC-t | 3.08 | 3.08 | 0.00 | 0 | 50 | 0 | |

| (500,50000,1) | GM | 4.96 | 4.92 | 0.04 | 44 | 4 | 2 |

| QaSIS-t | 2.42 | 2.36 | 0.08 | 0 | 50 | 0 | |

| DC-t | 2.94 | 2.94 | 0.00 | 0 | 50 | 0 | |

| (500, 100000, 1) | GM | 4.94 | 4.92 | 0.02 | 46 | 3 | 1 |

| QaSIS-t | 10.26 | 2.46 | 7.80 | 0 | 50 | 0 | |

| DC-t | 3.12 | 3.12 | 0.00 | 0 | 50 | 0 |

| Method | Size | TP | FP | C | U | O | |

|---|---|---|---|---|---|---|---|

| (400,500,0) | GM | 5.00 | 5.00 | 0.00 | 50 | 0 | 0 |

| QaSIS-t | 4.26 | 4.26 | 0.00 | 22 | 28 | 0 | |

| DC-t | 4.92 | 4.92 | 0.00 | 48 | 2 | 0 | |

| (400,1000,0) | GM | 5.14 | 5.00 | 0.14 | 44 | 0 | 6 |

| QaSIS-t | 4.04 | 4.04 | 0.00 | 20 | 30 | 0 | |

| DC-t | 4.96 | 4.96 | 0.00 | 48 | 2 | 0 | |

| (500,10000,0) | GM | 5.10 | 5.00 | 0.10 | 45 | 0 | 5 |

| QaSIS-t | 3.82 | 3.82 | 0.00 | 13 | 37 | 0 | |

| DC-t | 4.92 | 4.92 | 0.00 | 46 | 4 | 0 | |

| (500,50000,0) | GM | 5.40 | 5.00 | 0.40 | 37 | 0 | 13 |

| QaSIS-t | 3.04 | 3.04 | 0.00 | 8 | 42 | 0 | |

| DC-t | 4.66 | 4.66 | 0.00 | 38 | 12 | 0 | |

| (500, 100000,0) | GM | 5.32 | 5.00 | 0.32 | 41 | 0 | 9 |

| QaSIS-t | 3.02 | 3.02 | 0.00 | 5 | 45 | 0 | |

| DC-t | 4.66 | 4.66 | 0.00 | 34 | 16 | 0 | |

| (400,500,1) | GM | 5.00 | 4.98 | 0.02 | 48 | 1 | 1 |

| QaSIS-t | 5.78 | 2.90 | 2.88 | 3 | 38 | 9 | |

| DC-t | 31.30 | 4.00 | 27.30 | 1 | 0 | 49 | |

| (400,1000,1) | GM | 5.10 | 5.00 | 0.10 | 45 | 0 | 5 |

| QaSIS-t | 7.78 | 2.22 | 5.56 | 1 | 42 | 7 | |

| DC-t | 38.74 | 5.00 | 33.74 | 2 | 0 | 48 | |

| (500,10000,1) | GM | 5.10 | 4.96 | 0.14 | 42 | 2 | 6 |

| QaSIS-t | 12.94 | 2.08 | 10.86 | 0 | 45 | 5 | |

| DC-t | 74.98 | 5.00 | 69.98 | 0 | 0 | 50 | |

| (500,50000,1) | GM | 5.16 | 4.98 | 0.18 | 43 | 1 | 6 |

| QaSIS-t | 32.52 | 2.08 | 30.44 | 0 | 42 | 8 | |

| DC-t | 79.62 | 5.00 | 74.62 | 0 | 1 | 49 | |

| (500, 100000,1) | GM | 5.10 | 4.96 | 0.14 | 44 | 2 | 4 |

| QaSIS-t | 42.32 | 2.54 | 39.78 | 0 | 44 | 6 | |

| DC-t | 79.94 | 4.88 | 75.06 | 0 | 6 | 44 |

| Dataset | Method | Size | Testing error (Std) | Out of sample |

|---|---|---|---|---|

| GM | 10 | 0.1369 (0.0005) | 0.8631 | |

| QaSIS-t | 7 | 0.1674 (0.0006) | 0.8326 | |

| DC-t | 7 | 0.1713(0.0006) | 0.8287 | |

| SCAD | 59 | 0.1872 (0.0006) | 0.8128 | |

| MCP | 28 | 0.2040 (0.0006) | 0.7960 |