Quantitative Predictions

in Quantum Decision Theory

Abstract

Quantum Decision Theory, advanced earlier by the authors, and illustrated for lotteries with gains, is generalized to the games containing lotteries with gains as well as losses. The mathematical structure of the approach is based on the theory of quantum measurements, which makes this approach relevant both for the description of decision making of humans and the creation of artificial quantum intelligence. General rules are formulated allowing for the explicit calculation of quantum probabilities representing the fraction of decision makers preferring the considered prospects. This provides a method to quantitatively predict decision-maker choices, including the cases of games with high uncertainty for which the classical expected utility theory fails. The approach is applied to experimental results obtained on a set of lottery gambles with gains and losses. Our predictions, involving no fitting parameters, are in very good agreement with experimental data. The use of quantum decision making in game theory is described. A principal scheme of creating quantum artificial intelligence is suggested.

Index Terms:

Quantum decision theory, decision making, choice between lotteries, attraction index, quantitative predictions, game theory, artificial intelligenceI Introduction

Classical decision making, based on expected utility theory [1], is known to fail in many cases when decisions are made under risk and uncertainty. Numerous variants of so-called non-expected utility theories have been suggested to replace expected utility theory by using other more complicated functionals. The long list of such non-expected utility models can be found in the review articles [2, 3, 4]. The non-expected utility theories are, by construction, descriptive. By introducing several fitting parameters, such theories can be calibrated to some given set of empirical data. However, it is often possible to have different theories fitting the same set of experiments equally well, so that it is difficult to distinguish which of the models is better [5]. Moreover, on the basis of such theories, it is impossible to account for the known paradoxes arising in classical decision making and to make convincing out-of-sample predictions of new sets of empirical data. The non-expected utility theories have been thoroughly analyzed in numerous publications confirming the descriptive nature of these theories and their inability to perform useful predictions (see, e.g., [6, 7, 8, 9, 10]). Thus, Birnbaum [6, 7] carefully studied the so-called rank dependent utility theory and cumulative prospect theory, concluding that, even with fitting parameters, these theories are not able to get rid of paradoxes and moreover create new paradoxes. Safra and Segal [8] state that none of the non-expected utility theories can explain all main paradoxes but, on the contrary, distorting the structure of expected utility theory, the non-expected utility theories result in several non-expected inconsistencies. Al-Najjar and Weinstein [9, 10] present a detailed analysis of non-expected utility theories, coming to the conclusion that any variation of expected utility theory ”ends up creating more paradoxes and inconsistences than it resolves”.

The same conclusions apply to the so-called stochastic decision theories [11, 12, 13] that are based on underlying deterministic theories, decorating them with the probability of making errors in the choice. Introducing such probabilities, caused by decision-maker errors, into the log-likelihood functional adds several more parameters in the calibration exercise that improve the description of the given set of data. But such a stochastic decoration does not change the structure of the underlying deterministic theory and does not make predictions possible.

Clearly, the possibility of making predictions can be strongly hindered by the presence of unknown or poorly formulated conditions accompanying decision making. For instance, there can exist an unknown stochastic environment [14] or a varying context [15]. It may also happen that the provided information is imprecise and only partially reliable [16] or preference relations are incomplete [17] requiring the use of fuzzy logic [18]. In such situations, any prediction is likely to be only partial and often merely qualitative.

But even when the posed problem is well defined, suggesting, e.g., a choice between explicitly presented lotteries, quantitative predictions as a rule are impossible. In particular, the non-expected utility theories mentioned above have been developed exactly for such seemingly simple choice between well defined lotteries. And, as is discussed above, in many cases, the given lotteries, although being explicitly formulated, contain uncertainty not allowing for predictions. It is important to also stress that, in some cases of well defined lotteries, predictions based on utility theory are qualitatively wrong, as has been demonstrated by Kahneman and Tversky [19].

In the present paper, we consider the situation when decision making consists in the choice between well defined lotteries. We develop an approach allowing for quantitative predictions in arbitrary cases, including those where utility theory fails, being unable to provide even qualitatively correct conclusions. It is important to emphasize that quantitative predictions in our approach can be realized without any fitting parameters. So, our approach is not a descriptive, but rather a normative, or prescriptive theory.

Our approach is based on Quantum Decision Theory (QDT), which we developed earlier [20, 21, 22, 23, 24, 25, 26]. There have been other attempts to apply quantum techniques to cognitive sciences, as is discussed in the books [27, 28, 29, 30] and review articles [31, 32, 33, 34]. However, these attempts were based on constructing some models for describing particular effects, with the use of several fitting parameters for each case. Our approach of QDT is essentially different from all those models in the following facets. First, QDT is formulated as a general theory applicable to any variant of decision making, but not as a special model for a particular case. Second, the mathematical structure of QDT is common for both decision theory as well as for quantum measurements, which has been achieved by generalizing the von Neumann [35] theory of quantum measurements to the treatment of inconclusive measurements and composite events represented by noncommutative operators [36, 37, 38, 39]. The third unique feature of QDT is the possibility to develop quantitative predictions without any fitting parameters, as has been shown for some simple choices in decision making [40].

The predictions concern the fractions of decision makers choosing the corresponding lotteries. In QDT, such fractions are predicted by their corresponding behavioral quantum probabilities, as follows from the frequentist interpretation of probabilities and the assumption that the population of decision makers are, to a first approximation, representative of a homogenous group of individuals making probabilistic choices. The scheme for calculating the quantum probabilities is based on our previous demonstration that it consists of two terms, called utility and attraction factors. The utility factor derives from the utility of each lottery, being defined on prescribed rational grounds. The attraction factor represents the irrational side of a choice. The value of the attraction factor for a single decision maker and for a given choice is random. However, for a society of decision makers, one can derive the quarter law, which estimates the non-informative prior for the absolute value of the average attraction factor as equal to . In simple cases, the signs of the attraction factors can be prescribed by the principle of ambiguity aversion. In more complicated situations, a criterion has been suggested [40] and applied to lotteries with gains.

Here, we extend Ref. [40] by considering lotteries with both gains and losses, and not just gains. We also improve on the quarter law based on the non-informative prior, by including available information on the level of ambiguity characterizing a given set of games, thus providing the potential for improved predictions. Moreover, we consider the cases for which our previously proposed criterion defining the signs of attraction factors does not allow for unique conclusions. We present a generalization of the criterion for the sign of the attraction factors that addresses these limitations and also applies to lotteries with losses.

The possibility of mathematically formalizing all steps of a decision process, allowing for quantitative predictions, is important, not merely for decision theory, but also for the problem of creating an artificial quantum intelligence that could function only if all operations are explicitly formalized in mathematical terms. We have previously mentioned [41] that QDT can provide such a basis for creating artificial quantum intelligence, since the QDT mathematical foundation is formulated in the same way as the theory of quantum measurements.

In the present paper, we overcome the limitations of our previous publication [40] by generalizing QDT along the following directions.

(i) A general method for defining utility factors is advanced, valid for lotteries with losses as well as for lotteries with gains, or mixed-type lotteries.

(ii) A criterion is formulated for the quantitative classification of attraction factors for all kinds of lotteries, whether with gains or with losses. In the case of games with two lotteries, this criterion uniquely prescribes the signs of attraction factors.

(iii) The quarter law is generalized by taking into account the ambiguity level for a given set of games. This defines the typical absolute value of the attraction factor more accurately than the quarter law following from non-informative prior.

(iv) A method for estimating attraction factors for games with multiple lotteries is described.

(v) The value of our theory is illustrated by comparing its prediction with empirical results obtained on a set of games containing lotteries with gains and with losses, for which expected utility theory fails. Our approach results in quantitative predictions, without fitting parameters, which are in very good agreement with empirical data.

(vi) It is shown how the QDT can be applied to game theory. An application is illustrated by the prisoner dilemma.

(vii) The general principles for creating artificial quantum intelligence are suggested. It is emphasized that artificial intelligence, mimicking the functioning of human consciousness, should be quantum.

II Scheme of Quantum Decision Theory

In the present section, we briefly sketch the basic scheme of QDT in order to remind the reader about the definition of quantum probability used in decision theory. The technical details have been thoroughly expounded in the previous articles [20, 21, 22, 23, 24, 25, 26], which allows us to just recall here the basic notions.

As is mentioned in the Introduction, the mathematical scheme is equally applicable to quantum decision theory as well as to the theory of quantum measurements [36, 37, 38, 39]. An event can mean either the result of an estimation in the process of measurements, or a decision in decision making. In both the cases, there exist simple events that are operationally testable, that is, clearly observable, and inconclusive events that are either non-observable or even not well specified. The typical example in quantum measurements is the double-slit experiment, where the final registration of a particle by a detector is an operationally testable event, while the passage through one of the slits is not observable. In decision making, a straightforward example would be the choice between lotteries under uncertainty. The final choice of a lottery is an operationally testable event, while the deliberations on real or imaginary uncertainties in the formulation of the lotteries or in hesitations of the decision-maker can be treated as inconclusive events.

We consider a set of events labelled by an index . Each event is put into correspondence with a state of a Hilbert space , with the family of states forming an orthonormalized basis:

| (1) |

There also exists another set of events , labelled by an index , with each event being in correspondence with a state of a Hilbert space , the family of the states forming an orthonormalized basis:

| (2) |

A pair of events from different sets forms a composite event represented by a tensor-product state ,

| (3) |

in the Hilbert space

| (4) |

An event is called operationally testable if and only if it induces a projector on the space . The event set is assumed to consist of operationally testable events.

A different situation occurs when we have an inconclusive event being a set

| (5) |

of events associated with amplitudes that are random complex numbers. An inconclusive event corresponds to a state in the space , such that

| (6) |

The states are not orthonormalized, because of which the operator is not a projector.

A composite event is termed a prospect. Of major interest are the prospects composed of an operationally testable event and an inconclusive event:

| (7) |

A prospect corresponds to a prospect state in the space ,

| (8) |

and induces a prospect operator

| (9) |

The prospect states are not orthonormalized and the prospect operator is not a projector. The given set of prospects forms a lattice

| (10) |

whose ordering is characterized by prospect probabilities to be defined below. The assembly of prospect operators composes a positive operator-valued measure. By its role, this set is analogous to the algebra of local observables in quantum theory.

The strategic state of a decision maker in decision theory, or statistical operator of a system in physics, is a semipositive trace-one operator defined on the space . The prospect probability is the expectation value of the prospect operator:

| (11) |

with the trace over the space . To form a probability measure, the prospect probabilities are normalized,

| (12) |

Taking the trace in (11), it is possible to separate out positive-defined terms from sign-undefined terms, which respectively, are

| (13) |

Then the prospect probability reads as

| (14) |

The appearance of a sign-undefined term is typical for quantum theory, describing the effects of interference and coherence.

Note that the decision-maker strategic state has to be characterized by a statistical operator and not just by a wave function since, in real life, any decision maker is not an isolated object but a member of a society [38, 40].

An important role in quantum theory is played by the quantum-classical correspondence principle [42, 43], according to which classical theory has to be a particular case of quantum theory. In the present consideration, this is to be understood as the reduction of quantum probability to classical probability under the decaying quantum term:

| (15) |

In quantum physics, this is also called decoherence, when quantum measurements are reduced to classical measurements. The positive-definite term , playing the role of classical probability, is to be normalized,

| (16) |

From conditions (12) and (16) it follows

| (17) |

which is called the alternation law.

In decision theory, the classical part describes the utility of the prospect , which is defined on rational grounds. In that sense, a prospect is more useful than if and only if

| (18) |

The quantum part characterizes the attractiveness of the prospect, which is based on irrational subconscious factors. Hence a prospect is more attractive than if and only if

| (19) |

And the prospect probability (14) defines the summary preferability of the prospect, taking into account both its utility and attractiveness. So, a prospect is preferable to if and only if

| (20) |

The structure of the quantum probability (14), consisting of two parts, one showing the utility of a prospect and the other characterizing its attractiveness, is representative of real-life decision making, where both these constituents are typically present. Quantum probability, taking into account the rationally defined utility as well as such an irrational behavioral feature as attractiveness, can be termed as behavioral probability.

It is worth stressing that QDT is an intrinsically probabilistic theory. This is different from stochastic decision theories, where the choice is assumed to be deterministic, while randomness arises due to errors in decision making. The probabilistic nature of QDT is not caused by errors in decision making, but it is due to the natural state of a decision maker, described by a kind of statistical operator. Upon the reduction of QDT to a classical decision theory, it reduces to a probabilistic variant of the latter, since decisions under uncertainty are necessarily probabilistic [44]. As mentioned above, the description of a decision maker strategic state by a statistical operator, and not by a wave function, emphasizes the fact that any decision maker is not an absolutely isolated object but rather a member of a society, who is subjected to social interactions [38, 40, 45]. When comparing theoretical predictions with empirical data, it follows from the logical structure of QDT that one has to compare the theoretically calculated probability (14) with the fraction of decision makers preferring the considered prospect.

III General Definition of Utility Factors

In this section, we describe the general method for defining utility factors for a given set of lotteries containing both gains as well as losses.

Let a set of payoffs be given

| (21) |

in which payoffs can represent either gains or losses, being, respectively positive or negative. The probability distribution over a payoff set is a lottery

| (22) |

with the normalization condition

| (23) |

The lotteries are enumerated by the index . Under a utility function , the expected utility of lottery is

| (24) |

Utility functions for gains and losses can be of different signs. Therefore, the expected utility can also be either positive or negative. When it is negative, one often uses the notation of the lottery cost

An expected utility is positive, when in its payoffs gains prevail. And it is negative, when losses overwhelm gains.

As has been explained in Ref. [40], the choice between the given lotteries in any game is always accompanied by uncertainty related to the decision-maker hesitations with respect to the formulation of the game rules, understanding of the problem, and his/her ability to decide what he/she considers the correct choice. All these hesitations form an inconclusive event denoted above as . Therefore a choice of a lottery is actually a composite event, or a prospect

| (25) |

Here we denote the action of a lottery choice and a lottery by the same latter , which should not lead to confusion. The utility factor characterizes the utility of choosing a lottery . Since QDT postulates that the choice is probabilistic, it is possible to define the average quantity over the set of lotteries,

| (26) |

playing the role of a normalization condition for random expected utilities [46].

The utility factor represents a classical probability distribution and can be found from the conditional minimization of Kullback-Leibler information [47, 48]. The use of the Kullback-Leibler information for defining such a probability distribution is justified by the Shore-Jonson theorem [49] stating that there exists only one distribution satisfying consistency conditions, and this distribution is uniquely defined by the minimum of the Kullback-Leibler information, under given constraints. The role of the constraints here are played by the normalization conditions (16) and (26). Then the information functional reads as

| (27) |

where is a prior distribution, , and and are Lagrange multipliers.

As boundary conditions, it is natural to require that the utility factor of a lottery with asymptotically large expected utility would tend to unity,

| (28) |

while the utility factor of a lottery with asymptotically large cost, would go to zero,

| (29) |

Also, the utility factors, as their name implies, have to increase together with the related expected utilities,

| (30) |

Minimizing the information functional (27) results in the utility factors

| (31) |

with a non-negative parameter .

If one assumes that the prior distribution is uniform, such that , then one comes to the utility factors of the logit form. However, the uniform distribution does not satisfy the boundary conditions (28) to (29). Therefore a more accurate assumption, taking into account the boundary conditions, should be based on the Luce choice axiom [50, 51]. According to this axiom, if an -th object, from the given set of objects, is scaled by a quantity , then the probability of its choice is

| (32) |

In our case, the considered objects are lotteries and they are scaled by their expected utilities. So, for the non-negative utilities, we can set

| (33) |

while for negative utilities,

| (34) |

Expression (34) is chosen in order to comply with Luce’s axiom together with the ranking of preferences with respect to losses.

Generally, utilities can be measured in some units, say, in monetary units . Then we could use dimensionless scales defined as and for gains and losses, respectively. Obviously, expression (32) is invariant with respect to units in which is measured. Therefore, for simplicity of notation, we assume that utilities are dimensionless.

Thus, the utility factor (31), with prior (32), is

| (35) |

In particular, when gains prevail, so that all expected utilities are non-negative, then

| (36) |

While, when losses prevail, and all expected utilities are negative, then

| (37) |

In the mixed case, where the utility signs can be both positive and negative, one has to employ the general form (35).

The parameter characterizes the belief of the decision maker with respect to whether the problem is correctly posed. Under strong belief, one gets

| (40) |

which recovers the classical utility theory with the deterministic choice of a lottery with the largest expected utility. In the opposite case of weak belief, when uncertainty is strong, one has

| (41) |

To explicitly illustrate the forms of the utility factors, let us consider the often met situation of two lotteries under strong uncertainty, thus, considering the binary prospect lattice

| (42) |

with zero belief parameter. Then, if in both the lotteries gains prevail, we have

| (43) |

When losses are prevailing in the two lotteries, then

| (44) |

And if one expected utility is positive, say that of the first lottery, while the other utility is negative, then the utility factor for the first lottery is

| (45) |

respectively, .

In this way, the utility factors are explicitly defined for any combination of lotteries in the given game, with the payoff sets containing gains as well losses.

IV Classification of Lotteries by Attraction Indices

We now give a prescription for defining the attraction factors. By its definition, an attraction factor quantifies how each of the given lotteries is more or less attractive. The attractiveness of a lottery is composed of two factors, possible gain and its probability. It is clear that a lottery is more attractive, when it suggests a larger gain and/or this gain is more probable. In other words, a more attractive lottery is more predictable and promises a larger profit. On the contrary, a lottery suggesting a smaller gain or a larger loss and/or higher probability of the loss, is less attractive. A less certain lottery is less attractive, since it is less predictable, which is named as uncertainty aversion or ambiguity aversion. Below we give an explicit mathematical formulation of these ideas.

Let us introduce, for a lottery , the notation for the minimal gain

| (46) |

and for the minimal loss

| (47) |

These quantities characterize possible gains and losses in the given lotteries.

But payoffs are not the only features that attract the attention of decision makers. In experimental neuroscience, it has been discovered that, during the act of choosing, the main and foremost attention of decision makers is directed to the payoff probabilities [52]. We capture this empirical observation by considering different weights related to payoffs and to their probabilities in the characterization of the lottery attractiveness. Specifically, the weight of a payoff should be much smaller than the weight of its probability . We quantitatively formulate this by choosing weights proportional respectively to for the payoff versus for its probability. The later term is motivated by the decimal number system. This leads us to defining the lottery attractiveness

| (48) |

And the related relative quantity can be termed the attraction index

| (49) |

The latter satisfies the normalization condition

| (50) |

The notion of the lottery attraction index makes it straightforward to classify all lotteries from the considered game onto more or less attractive. Thus a lottery is more attractive than , hence

| (51) |

when the attraction index of the first lottery is larger than that of the second,

| (52) |

In the marginal case, when , the first lottery is more attractive if the probability of its minimal gain is smaller than that of the second lottery,

| (53) |

For short, this will be denoted as . And in the other marginal case, where , the first lottery is more attractive if the probability of its minimal loss is larger than that of the second,

| (54) |

This, for short, will be denoted as .

The criterion allows us to arrange all the given lotteries with respect to the level of their attractiveness.

For the particular case of a binary prospect lattice (42), the alternation property (17) reads as

| (55) |

Therefore the attraction factors have different signs,

| (56) |

The sign of each of the attraction factors is prescribed by the sign of the difference

| (57) |

If is positive, then the attraction factor of the first prospect is positive and that of the second is negative. On the contrary, if is negative, then the attraction factor of the first lottery is negative and that of the second is positive. In the marginal case, when , we shall use the notations accepted above and explained below (Eqs. (53) and (54)): If the first lottery is more attractive, we shall write , while when the second lottery is more attractive, this will be denoted as .

V Typical Values of Attraction Factors

The criterion of the previous section allows us to classify all the lotteries of the considered game onto more or less attractive. But we also need to define the amplitudes of the attraction factors. According to QDT, these values are probabilistic variables, characterizing irrational subjective features of each decision maker. For different subjects, they may be different. They can also be different for the same subject at different times [13]. Different game setups also influence the values of the attraction factors [53]. However, for a probabilistic quantity, it is possible to define its average or typical value.

V-A General considerations

We consider games, enumerated by , with lotteries in each, enumerated by . And let the choice be made by a society of decision makers, numbered by . In a -th game, decision makers make a choice between prospects . The typical value of the attraction factor is defined as the average

| (58) |

Denoting the mean value of the attraction factor for a prospect , as

| (59) |

we can write

| (60) |

For a large value of the product , the distribution of the attraction factors can be characterized by a probability distribution , which, in view of property (17), is normalized as

| (61) |

The average absolute value of the attraction factor can be represented by the integral

| (62) |

This defines the typical value of the attraction factor that characterizes the level of deviation from rationality in decision making [54].

If there is no information on the properties and specifics of the given set of lotteries in the suggested games, then one should resort to a non-informative prior, assuming a uniform distribution satisfying normalization (61), which gives . Substituting the uniform distribution into the typical value of the attraction factor (62) yields , which was named the “quarter law” in the earlier paper [40].

However, it is possible to find a more precise typical value by taking into account the available information on the given lotteries. For example, it is straightforward to estimate the level of uncertainty of the lottery set.

V-B Choice between two prospects

When choosing between two lotteries with rather differing utilities, the choice looks quite easy - the lottery with the largest utility is preferred. But when two lotteries have very close utilities, choosing becomes difficult. The closeness of the lotteries, corresponding to two prospects and , can be quantified by the relative difference

| (63) |

When the choice is between just two prospects, whose utility factors are normalized according to condition (16), hence when , then the relative difference simplifies to

| (64) |

There have been many discussions concerning choices between similar alternatives with close utilities or close probabilities, such that the choice becomes hard to make [55, 56, 57, 58]. We refer to such situations as “irresolute”. One of the major problems is how to quantify the similarity or closeness of the choices. Several variants of measuring the distance between the alternatives and have been suggested, including the linear distance , as well as different nonlinear distances , with . We propose that the value of that serves as an upper threshold, below which the lotteries are irresolute, should not depend on the exponent used in the definition of the distance. Therefore, in order for the exponent not to influence the boundary value, one has to require the invariance of the distance with respect to the exponent at the threshold, so that the critical threshold value should obey the equality: for any . The latter reads explicitly as

where is measured in percents. This equation is valid for arbitrary only for . Hence the critical boundary value equals . Thus the lotteries, for which the irresoluteness criterion

| (65) |

is valid, are to be treated as close, or similar, and the choice between them, as irresolute.

The next question is how the irresoluteness in the choice influences the typical attraction factor. Suppose that the fraction of irresolute games equals . Then the following properties of the distribution over admissible attraction factors should hold.

In the presence of irresolute games for which the irresoluteness criterion holds true, the probability that the attraction factor is zero is asymptotically small,

| (66) |

In other words, this condition means that, on the manifold of all possible games, absolutely rational games form a set of zero measure.

If not all games are irresolute , the probability of the maximal absolute value of the attraction factor is asymptotically small,

| (67) |

That is, on the manifold of all possible games, absolutely irrational games compose a set of zero measure.

Often employed as a prior distribution in standard inference tasks [59, 60, 61], the simplest distribution that obeys the two conditions (66) and (67) is the beta distribution that, under normalization (61), reads

| (68) |

Using this distribution, expression (62) gives the typical attraction factor value

| (69) |

Note that the average of given by (69) over the two boundary values and gives

thus recovering the non-informative quarter law.

This expression (69) can be used for predicting the results of decision making. For example, in the case of a binary prospect lattice, the difference in the attraction indices (57) defines the signs of the attraction factors, making it possible to prescribe the attraction factors and to the considered prospects.

V-C Choice between more than two prospects

When there are more than two prospects in the considered game, we propose the following procedure to estimate the attraction factors. Using the classification of the prospects by the attraction indices, as is described in the previous section, it is straightforward to arrange the prospects in descending order of attractiveness,

| (70) |

Let the maximal attraction factor be denoted as

| (71) |

Given the unknown values of the attraction factors, the non-informative prior assumes that they are uniformly distributed and at the same time they must obey the ordering constraint (70). Then, the joint cumulative distribution of the attraction factors is given by

| (72) |

where the series of inequalities ensure the ordering. It is then straightforward to show that the average values of the are equidistant, i.e. the difference between any two neighboring factors, on average, is independent of , so that

| (73) |

Taking their average values as determining their typical values, we omit the symbol representing the average operator and use the previous equation to represent the -th attraction factor as

| (74) |

From the alternation property (17), it follows that

| (75) |

The total number of lotteries can be either even or odd, leading to slightly different forms for the following expressions.

And the definition of the typical value (60) gives

| (79) |

Then the maximal attraction factor (75) becomes

| (83) |

Therefore formula (74) yields the expressions for all attraction factors

| (87) |

Let us denote the set of all attraction factors in the considered game as

If there are only two lotteries, then we have

and the attraction-factor set is

In the case of three lotteries,

and the attraction factor set reads as

In that way, all attraction factors can be defined.

VI Quantitative Predictions in Decision Making

In order to illustrate how the suggested theory makes it possible to give quantitative predictions, without any fitting parameters, let us consider the set of experiments performed by Kahneman and Tversky [19]. This collection of games, including both gains and losses, is a classical example showing the inability of standard utility theory to provide even qualitatively correct predictions as a result of the confusion caused by very close or coinciding expected utilities. Let us emphasize that the choice of these games has been done by Kahneman and Tversky [19] in order to stress that standard decision making cannot be applied for these games. This is why it is logical to consider the same games and to show that the use of QDT does allow us not only to qualitatively explain the correct choice, but also that QDT provides quantitative predictions for such difficult cases.

In the set of games described below, each game consists of two lotteries , with . The number of decision makers is about .

Recall that, as is explained in Sec. III, the choice between lotteries corresponds to the choice between prospects (25) including the action of selecting a lottery under a set of inconclusive events representing hesitations and irrational feelings. Therefore the choice, under uncertainty, between lotteries is equivalent to the choice between prospects . The choice under uncertainty for the case of a binary lattice can be characterized by the utility factors (43) to (45). We take the linear utility function, whose convenience is in the independence of the utility factors from the monetary units used in the lottery payoffs. The attraction factors are calculated by following the recipes described in Sec. IV and Sec. V.

We compare the prospect probabilities , theoretically predicted by QDT, with the empirically observed fractions [19]

of the decision makers choosing the prospect , with respect to the total number of decision makers taking part in the experiments.

VI-A Lotteries with gains

Game 1. The lotteries are

For this game, we shall show explicitly the related calculations, while omitting the intermediate arithmetics in the following cases.

The utilities of these lotteries are

Their sum is

The utility factors are close to each other,

For the lottery attractiveness (48), we find

which gives

The attraction indices (49) become

Then the attraction difference (57) is

The negative attraction difference tells us that the first lottery is less attractive, , which suggests that the second lottery is preferable, . The experimental results confirm this, displaying the fractions of decision makers choosing the respective lotteries as

Thus, although the first lottery is more useful, having a larger utility factor, it is less attractive, which makes it less preferable.

Game 2. The lotteries are

The following procedure is the same as in the first game. Calculating the utility factors

we again see that the lottery utilities are close to each other, so it is difficult to make the choice. For the lottery attractiveness, we have

giving the attraction indices

and the attraction difference

Now the latter is positive, showing that the first lottery is more attractive, , which suggests that the first lottery is preferable, . The experimental data for the related fractions are

in agreement with the expectation that the first lottery is preferable.

Game 3. The lotteries are

We calculate in the prescribed way the utility factors

lottery attractiveness,

and the attraction indices

The negative attraction difference

implies that the first lottery is less attractive, , which tells us that the second lottery should be preferable, . Again this is in agreement with the experimental results

The first lottery is less preferable, despite it is more useful, having a larger utility factor.

Game 4. The lotteries are

Calculating the utility factors

lottery attractiveness

and the attraction indices

we find the positive attraction difference

Hence the first lottery is more attractive , which suggests that the first lottery is preferable, . The experimental data

confirm this expectation.

Game 5. The lotteries are

The utility factors

turn out to be equal, which makes it impossible to decide in the frame of classical decision theory based on expected utilities. Then we calculate the lottery attractiveness

and the related attraction indices

The negative attraction difference

means that the first lottery is less attractive, , thence the second lottery is expected to be preferable, . This is confirmed by the empirical data

Game 6. The lotteries are

Again their utility factors are equal to each other,

The lottery attractiveness values

yield the attraction indices

whose positive attraction difference

implies that the first lottery is more attractive, , which suggests that the first lottery should be preferable, . The experimental results are

in agreement with the expectation.

Game 7. The lotteries are

Their equal utility factors,

do not allow us to make a choice based on their utility. We calculate the lottery attractiveness

and the attraction indices

Here the attraction difference is zero, , with the attraction indices being positive. Therefore, we resort to criterion (53), for which the minimal gains are . We find that

According to definitions (53) and (54), the marginal case, when and , is denoted as . This proposes that the first lottery is less attractive, according to the negative sign

Thus we find that , which suggests that the second lottery is preferable, . The experimental results give

VI-B Lotteries with losses

In the previous seven games, the lotteries with gains were considered. We now turn to lotteries with losses.

Game 8. The lotteries are

Following the same general procedure, we find the utility factors

lottery attractiveness

and the attraction indices

The positive attraction difference

means that the first lottery is more attractive, , because of which, we expect that the first lottery is preferable, . The experiments give

confirming that the first lottery is preferable, although its utility factor is smaller.

Game 9. The lotteries are

With the utility factors

lottery attractiveness

and the attraction indices

the attraction difference is negative,

Thence the first lottery is less attractive, , and we expect that the second lottery is preferable, . The empirical data are

Game 10. The lotteries are

The utility factors are equal,

hence both lotteries are equally useful. But the lottery attractiveness is different,

yielding the attraction indices

The negative attraction difference

signifies that the first lottery is less attractive, , which hints that the second lottery is preferable, . The experimental results are

Game 11. The lotteries are

The utility factors are again equal to each other,

which makes it impossible to employ the classical utility theory. But the lottery attractiveness

and the attraction indices

show that the attraction difference is positive,

Therefore the first lottery is more attractive, , which suggests that the first lottery is preferable, . The experimental data are

Game 12. The lotteries are

Again the equal utility factors,

do not allow for the choice based on the lottery utilities. But calculating the lottery attractiveness

and the attraction indices

we see that the attraction difference is positive,

This means that the first lottery is more attractive, , thence the first lottery is expected to be preferable, . The empirical results are

Game 13. The lotteries are

The utility factors are again equal,

For the lottery attractiveness

the attraction indices are also equal,

Getting the zero attraction difference, , with negative attraction indices, we have to involve criterion (54). The minimal losses are

And we find

Consequently, the first lottery is more attractive, which can be denoted as

The stronger attractiveness of the first lottery, when , suggests that the first lottery should be preferable, . The experimental data are

Game 14. The lotteries are

Although the utility factors are equal,

but the lottery attractiveness

defines different attraction indices

The negative attraction difference

implies that the first lottery is less attractive, . Then the second lottery is expected to be preferable, . The experimental results

confirm this expectation.

VI-C Empirical test of quantitative predictions of empirical choice frequencies

| 1 | 0.501 | 0.4 | 0.405 | -0.19 | 0.23 | 0.18 | -0.32 | 0.05 |

|---|---|---|---|---|---|---|---|---|

| 2 | 0.503 | 1.2 | 0.759 | 0.52 | 0.78 | 0.83 | 0.33 | 0.05 |

| 3 | 0.516 | 6.4 | 0.457 | -0.09 | 0.24 | 0.20 | -0.32 | 0.04 |

| 4 | 0.516 | 6.4 | 0.543 | 0.09 | 0.79 | 0.65 | 0.13 | 0.14 |

| 5 | 0.5 | 0 | 0.415 | -0.17 | 0.23 | 0.14 | -0.36 | 0.09 |

| 6 | 0.5 | 0 | 0.666 | 0.33 | 0.77 | 0.73 | 0.23 | 0.04 |

| 7 | 0.5 | 0 | 0.5 | -0 | 0.23 | 0.18 | -0.32 | 0.05 |

| 8 | 0.484 | 6.4 | -0.457 | 0.09 | 0.76 | 0.92 | 0.44 | 0.16 |

| 9 | 0.484 | 6.4 | -0.543 | -0.09 | 0.21 | 0.42 | -0.06 | 0.21 |

| 10 | 0.5 | 0 | -0.585 | -0.17 | 0.23 | 0.08 | -0.42 | 0.15 |

| 11 | 0.5 | 0 | -0.048 | 0.90 | 0.77 | 0.70 | 0.20 | 0.07 |

| 12 | 0.5 | 0 | -0.378 | 0.23 | 0.77 | 0.69 | 0.19 | 0.08 |

| 13 | 0.5 | 0 | -0.5 | +0 | 0.77 | 0.70 | 0.20 | 0.07 |

| 14 | 0.5 | 0 | -0.99 | -0.98 | 0.23 | 0.17 | -0.33 | 0.06 |

As is explained at the beginning of Sec. VI, the considered lotteries have been selected by Kahneman and Tversky [19] in order to demonstrate the failure of standard utility theory. All these lotteries exhibit close or even equal expected utilities, which makes the choice between them difficult or even undecided in the frame of utility theory. The majority of the lotteries are irresolute in the sense of criterion (65). But we show that in the frame of QDT, this set of lotteries is treatable.

Among the considered games, the choice is irresolute in games according to rule (65), leading to the fraction of irresolute games. Therefore the typical attraction factor (69) is predicted to be

| (88) |

Then the quantitative predictions for each of the games are determined by the formulas

| (89) |

These predictions are compared with the empirical results from Ref. [19] in Table 1. For each game, we show the utility factor defined by equations (43) or (44), the utility difference (64) providing a classification of the game irresoluteness, the attraction index (49), the attraction difference (57), and the predicted probability , which is compared with the experimentally observed fraction of decision makers preferring prospect . We also report the empirically observed attraction factor defined by

and the error of our theoretical prediction, as compared to the empirical data,

The results for , , , , and are not shown, since they are straightforwardly connected by the appropriate normalization conditions.

The median (resp. average) error is (resp. ). which are within the statistical accuracy of the experiment.

VII Quantum Decision Making in Game Theory

We have shown that Quantum Decision Theory (QDT) provides the basis for an accurate description of human decision making. Since decision making is also the basis of game theory, it is important to delineate the relation of QDT to game theory.

Quantum game theory, originated by Meyer [62] considers game theory from the perspective of quantum algorithms. There exist several good reviews on quantum game theory [63, 64, 65, 66]). Generally, quantum game theory, merging game theory and quantum mechanics, suggests two perspectives, with the common factor between the two perspectives being quantum information. In one perspective, players are not assumed to be quantum devices, although their conscious processes are described by quantum techniques taking into account the dual nature of consciousness, consisting of rational as well as irrational components. In this approach, games are treated as representing realistic situations in human decision making. From the other side, quantum mechanics as such can be treated as a collection of quantum games, which sheds insights into the nature of quantum algorithms. The discussion of these two perspectives can be found in Refs. [67, 68]. The relation of our Quantum Decision Theory to game theory is explained below in more details.

VII-A Reformulation of games into lottery sets

In the previous sections, it has been shown how QDT is applied to the choice between several lotteries. To follow the same way, we need to reformulate a game into a lottery set, after which we can directly employ the same QDT decision-making approach. For illustration, let us consider the typical structure of a two-by-two game. That is, we consider two players, each of which can accomplish two actions, say and . Then there are four strategies

where the action corresponds to the first player and , to the second player. The game is characterized by eight payoffs , with . The standard form of a payoff matrix is shown in Table II.

As has been explained above, the use of QDT is senseful only when there exists uncertainty in decision making. But, when all actions are absolutely certain, being uniquely defined, the QDT reduces to classical decision making, in agreement with the quantum-classical correspondence principle (15). This implies that QDT should be applied to mixed games, where actions are taken in the presence of uncertainty. For this purpose, we introduce a probability measure , with the usual properties

The notation defines a probability that the -th player takes the action .

The characteristic feature of games is that the payoffs of one player depend on the action of the other player, accomplished with the related probability. For example, the payoff of the first player, taking an action , is conditioned by the other player action , accomplished with the probability . Then the mixed game, corresponding to the matrix in Table II, can be reformulated as the choice between lotteries. Thus, the first player has to choose between two lotteries

that is, the first player has to decide between the actions and , whose payoffs depend on the actions of the second player. Respectively, the second player chooses between the lotteries

Introducing the payoff utility of a strategy for the -th player,

it is straightforward to define the lottery expected utilities, for the first player,

and for the second player

where .

After the game is reformulated into the approach of choosing between lotteries, which is usual for decision theory, it is possible to resort to QDT as we illustrate in the next subsection.

| player 1 player 2 | ||

|---|---|---|

VII-B Quantum decision making in the prisoner dilemma problem

For concreteness, let us consider the prisoner dilemma that is a canonical example of a game analyzed in game theory. Numerous other games enjoy the same structure as the prisoner dilemma. Here the action corresponds to keeping silence, not betraying the other prisoner, while denotes the action of betraying the other prisoner.

To apply QDT, we need the variant of the prisoner dilemma, where two players make decisions under uncertainty, without knowing the choice of the other agent, as has been treated in Ref. [19]. In that setup, the -th player, taking an action is not aware of the action accomplished by the other player. The admissible set of actions of the other player is an inconclusive event

in agreement with definition (5).

In order to avoid excessive notations, let us denote the choice of a lottery by the same symbol. Then the prospect of choosing this lottery by the -th player, under the unknown choice of the other player, is

| (90) |

Following the techniques of Sec. II, we get the prospect probabilities

| (91) |

Since we aim at analyzing the prisoner dilemma, we should keep in mind that this game is symmetric, such that the payoffs of the same strategies are the same for both players:

where the values are assumed to be non-negative.

For generality, we may interpret the strategy payoffs as utilities, so that

It is assumed that each player knows nothing about the choice of the other player, who can take any of the two actions with no informative prior, that is, with equal probability . Then the expected utilities of the lotteries to be chosen by the players are

Because of the symmetry, it is sufficient to consider just one of the players. Thus, the utility factors for the -th player, according to QDT, are

The specific feature of the prisoner dilemma is that the relations between payoffs are such that

From this, it immediately follows that

hence for each prisoner it is more useful to betray the other. This strategy is the Nash equilibrium in the classical prisoner dilemma.

However, in QDT, we have to consider not merely the utility, but the whole prospect probability (91). As is explained above, a more useful prospect may turn out to be not the most attractive. In the prisoner dilemma, each prisoner takes a decision “betray or not betray” under the uncertainty of what has been decided by the other prisoner. According to the principle of uncertainty and risk aversion [22, 23, 40], in the choice under uncertainty, decision makers are more inclined to be passive, not acting. In the present case, this means that not betraying is a more attractive action, hence

As is explained in Sec. V, under a complete ignorance of the actions of the other player, the attraction factors can be evaluated by employing the method of non-informative priors, yielding the quarter law, telling that the absolute values of the attraction factors are equal to . This tells us that the prospect probabilities are given by the expressions

The first of these is the probability for the prospect of not betraying, while the second one is the probability for the prospect of betraying.

Generally, the utility factors are influenced by the related payoff strategies. The typical values of utilities can be found by measuring the fraction of decision makers, taking the related decisions, when knowing the actions chosen by the other player, as has been done by Kahneman and Tversky [19], who found the fractions corresponding to and . A more detailed discussion of this has been given in Ref. [40].

Summarizing, we find that QDT predicts the prospect probabilities

Thence, despite the fact that the utility of not betraying is very small with the utility factor , the probability of not betraying is larger, being . This difference is predicted by QDT. The empirical data, observed by Kahneman and Tversky [19], when each of the players decides under uncertainty, are the fractions

which is in remarkable agreement with the prediction of QDT.

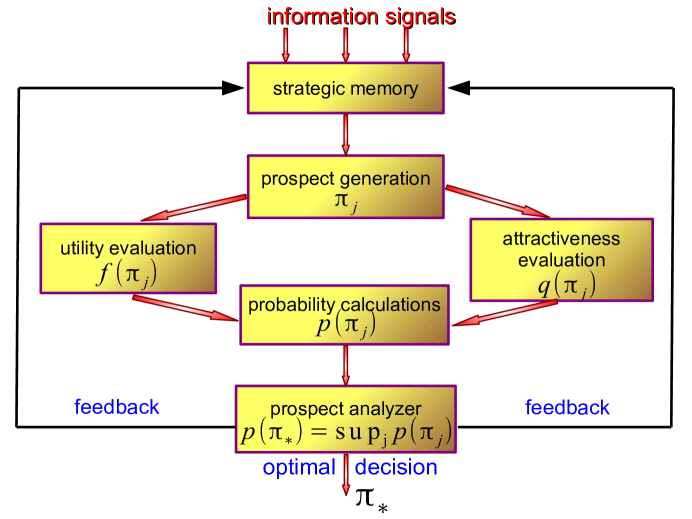

VIII Prolegomena to Artificial Quantum Intelligence

As is emphasized in the Introduction, the developed QDT theory not only provides a good description of human decision making, allowing for quantitative predictions, but also can serve as a basic scheme for creating artificial intelligence [69]. Actually, as has been shown above, realistic human decision making can be interpreted as being characterized by quantum rules. This is not because humans are quantum objects, but because the process of making decisions is dual, including both a rational evaluation of utility as well as subconscious evaluation of attractiveness. The dual nature of the decision process is effectively taken into account by the mathematics of quantum theory. Since artificial intelligence is assumed to mimic human mental processes, it has to function similarly to human decision making. That is, an artificial intelligence has to necessarily employ a type of quantum decision making. It is in that sense that an artificial intelligence is to be quantum.

Artificial intelligence is not the same as just a powerful computer, as one often assumes, but it is a rather different device functioning as a human brain, hence taking into account the dual nature of decision processes. A principal scheme of an artificial intelligence, functioning according to Quantum Decision Theory, is shown in Fig. 1.

IX Conclusion

We have suggested a formulation providing quantitative predictions for the fraction of decision makers choosing a given prospect among a set of alternatives. This formulation has the virtue of being parameter-free. The approach is based on Quantum Decision Theory (QDT) developed earlier by the authors. In the present paper, the theory has been generalized in several important aspects that are crucial for the development of such quantitative predictions:

(i) A general method for defining utility factors is advanced, valid for lotteries with losses as well as for lotteries with gains.

(ii) A criterion is formulated for the quantitative classification of attraction factors for all kinds of lotteries, whether with gains or with losses. In the case of games with two lotteries, this criterion uniquely prescribes the signs of attraction factors.

(iii) The quarter law is generalized by taking into account the irresoluteness of a given set of games. This defines the typical absolute value of the attraction factor more accurately than the quarter law based on a non-informative prior.

(iv) A method for estimating attraction factors for games with multiple (more than two) lotteries is described.

(v) The theory is illustrated by a set of games containing lotteries with gains and with losses, for which expected utility theory fails, while our approach results in quantitative predictions, without fitting parameters, being in very good agreement with empirical data.

(vi) It is demonstrated how games considered in game theory can be reformulated as sets of lotteries. This opens up the possibility of employing the techniques of QDT for mixed games containing uncertainty.

(vii) The mathematical formalization of all steps of decision making provided by our approach is important not only for accurate quantitative predictions of decision making by humans, but it can serve as a guiding scheme for creating artificial intelligence [41]. For this, it is necessary, first of all, to understand the basic structure of human decision making. As we have shown, our suggested approach captures the main features of decision making by humans, and gives rather accurate quantitative predictions. We suggest that the structure of artificial intelligence has to include the basic features of the developed QDT approach. A principal scheme of artificial quantum intelligence is proposed.

The theory described in the present paper is only a first step in the full mathematical formalization of the decision making process. Actually, what we have described is a one-step decision making. In multistep decision making, because of additional information acquired by agents, the choice can change [70]. To characterize the sequence of decisions taken by decision makers who are the members of a society, it is necessary to generalize the approach by taking into account dynamical effects influencing the temporal evolution of decisions due to the exchange of information among social decision makers. First attempts of generalizing QDT to account for temporal effects, caused by the amount of information among social decision makers, have been considered in Refs. [26, 40], where it was assumed that all decision makers in a society simultaneously get the same information. A more realistic situation of decision makers exchanging information with each other and varying their decisions accordingly will be presented in a following paper.

Acknowledgment

The authors are grateful for discussions to E.P. Yukalova. Financial support from the ETH Zürich Risk Center is appreciated.

References

- [1] J von Neumann and O. Morgenstern, Theory of Games and Economic Behavior. Princeton: Princeton University, 1953.

- [2] M.J. Machina, “Non-expected utility theory”, in New Palgrave Dictionary of Economics, S.N. Durlauf and L.E. Blume, Eds. New York: Macmillan, 2008.

- [3] M.J. Machina, “Risk, ambiguity, and the rank-dependence axioms,” Am. Econ. Rev., vol. 99, pp. 385–92, 2009.

- [4] A. Baillon, O. L’Haridon, and L. Placido, “Ambiguity models and the Machina paradoxes,” Am. Econ. Rev., vol. 101, pp. 1547–1560, 2011.

- [5] L.M. Bernstein, G. Chapman, C. Christensen, and A. Elstein, “Models of choice between multioutcome lotteries,” J. Behav. Decis. Mak., vol. 10, pp. 93–115, 1997.

- [6] M.H. Birnbaum, “Test of rank-dependent utility and cumulative prospect theory in gambles represented by natural frequences,” Org. Behav. Human Decis. Process., vol. 95, pp. 40–65, 2004.

- [7] M.H. Birnbaum, “Evidence against prospect theories in gambles with positive, negative, and mixed consequences,” J. Econ. Psychol., vol. 27, pp. 737–761, 2006.

- [8] Z. Safra and U. Segal, “Calibration results for nonexpected utility theories”, Econometrica, vol. 76, pp. 1143–1166, 2008.

- [9] N.I. Al-Najjar and J. Weinstein, “The ambiguity aversion literature: A critical assessment,” Econ. Philos., vol. 25, pp. 249–284, 2009.

- [10] N.I. Al-Najjar and J. Weinstein, “Rejoinder: The ambiguity aversion literature: A critical assessment”, Econ. Philos., vol. 25, pp. 357–369, 2009.

- [11] J.D. Hey, “Experimental investigations of errors in decision making under risk,” Eur. Econ. Rev., vol. 39, pp. 633–640, 1995.

- [12] T.P. Ballinger and N.T. Wilcox, “Decisions, errors and heterogeneity,” Econ. J.. vol. 107, pp. 1090–1105, 1997.

- [13] P.R. Blavatskyy and G. Pogrebna, “Models of stochastic choice and decision theories: why both are important for analyzing decisions,” J. Appl. Econometr., vol. 25, pp. 963–986, 2010.

- [14] D. Dong, C. Chen, H. Li, and T.J. Tarn, “Quantum reinforcement learning,” IEEE Trans. Syst. Man Cybern. B Cybern., vol. 38, pp. 1207–1220, 2008.

- [15] S. Andraszewicz, J. Rieskamp, and B. Scheibehenne, “How outcome dependences affect decisions under risk,” Decision, vol. 2, pp. 127–144, 2015.

- [16] R.A. Aliev, W. Pedrycz, V. Kreinovich, and O.H. Huseynov, “The general theory of decisions,” Inf. Sci., vol. 327, pp. 125–148, 2016.

- [17] R. Ureña, F. Chiclana, J.A. Morente-Molinera, and E. Herrera-Viedma, “Managing incomplete preference relations in decision making: a review and future trends,” Inf. Sci., vol. 301, pp. 14–32, 2015.

- [18] L.A. Zadeh, “Fuzzy sets,” Inf. Control, vol. 8, pp. 338–353, 1965.

- [19] D. Kahneman and A. Tversky, “Prospect theory: An analysis of decision under risk,” Econometrica, vol. 47, pp. 263–292, 1979.

- [20] V.I. Yukalov and D. Sornette, “Quantum decision theory as quantum theory of measurement,” Phys. Lett. A, vol. 372, pp. 6867–6871, 2008.

- [21] V.I. Yukalov and D. Sornette, “Physics of risk and uncertainty in quantum decision making,” Eur. Phys. J. B, vol. 71, pp. 533–548, 2009.

- [22] V.I. Yukalov and D. Sornette, “Mathematical structure of quantum decision theory,” Adv. Compl. Syst., vol. 13, pp. 659–698, 2010.

- [23] V.I. Yukalov and D. Sornette, “Decision theory with prospect interference and entanglement,” Theory Decis., vol. 70, pp. 283–328, 2011.

- [24] V.I. Yukalov and D. Sornette, “Conditions for quantum interference in cognitive sciences,” Top. Cogn. Sci., vol. 6, pp. 79–90, 2014.

- [25] V.I. Yukalov and D. Sornette, “Self-organization in complex systems as decision making,” Adv. Compl. Syst., vol. 17, p. 1450016, 2014.

- [26] V.I. Yukalov and D. Sornette, “Role of information in decision making of social agents,” Int. J. Inf. Technol. Decis. Mak., vol. 14, pp. 1129–1166, 2015.

- [27] A. Khrennikov, Ubiquitous Quantum Structure. Berlin: Springer, 2010.

- [28] J.R. Busemeyer and P. Bruza, Quantum Models of Cognition and Decision. Cambridge: Cambridge University, 2012.

- [29] E. Haven and A. Khrennikov, Quantum Social Science. Cambridge: Cambridge University, 2013.

- [30] F. Bagarello, Quantum Dynamics for Classical Systems. Hoboken: Wiley, 2013.

- [31] V.I. Yukalov and D. Sornette, “Processing information in quantum decision theory,” Entropy, vol. 11, pp. 1073–1120, 2009.

- [32] P. Agrawal and R. Sharda, “Quantum Mechanics and Human Decision Making”, Oper. Res., vol. 61, pp. 1–16, 2013.

- [33] D. Sornette, “Physics and financial economics (1776-2014): puzzles, Ising and agent-based models,” Rep. Prog. Phys., vol. 77, p. 062001, 2014.

- [34] M. Ashtiani and M.A. Azgomi, “A survey of quantum-like approaches to decision making and cognition,” Math. Soc. Sci., vol. 75, pp. 49–50, 2015.

- [35] J. von Neumann, Mathematical Foundations of Quantum Mechanics. Princeton: Princeton University, 1955.

- [36] V.I. Yukalov and D. Sornette, “Quantum probabilities of composite events in quantum measurements with multimode states,” Laser Phys., vol. 23, 105502, 2013.

- [37] V.I. Yukalov and D. Sornette, “Positive operator-valued measures in quantum decision theory,” Lect. Notes Comput. Sci., vol. 8951, pp. 146–161, 2015.

- [38] V.I. Yukalov and D. Sornette, “Quantum probability and quantum decision making,” Philos. Trans. Roy. Soc. A, vol. 374, p. 20150100, 2016.

- [39] V.I. Yukalov and D. Sornette, “Inconclusive quantum measurements and decisions under uncertainty,” Front. Phys., vol. 4, p. 12, 2016.

- [40] V.I. Yukalov and D. Sornette, “Manipulating decision making of typical agents,” IEEE Trans. Syst. Man Cybern. Syst., vol. 44, pp. 1155–1168, 2014.

- [41] V.I. Yukalov and D. Sornette, “Scheme of thinking quantum systems,” Laser Phys. Lett., vol. 6, pp. 833–839, 2009.

- [42] N. Bohr, Atomic Physics and Human Knowledge. New York: Wiley, 1958.

- [43] N. Bohr, Collected Works. The Correspondence Principle, Vol. 3. Amsterdam: North-Holland, 1976.

- [44] P. Guo, “One-shot decision theory,” IEEE Trans. Syst. Man Cybern. A, vol. 41, pp. 917–926, 2011.

- [45] W.A. Brock and S.N. Durlauf, “Discrete choice with social interactions,” Rev. Econ. Stud., vol. 68, pp. 235–260, 2001.

- [46] F. Gul, P. Natenzon, and W. Pesendorfer, “Random choice as behavioral optimization,” Econometrica, vol. 82, pp. 1873–1912, 2014.

- [47] S. Kullback and R.A. Leibler, “On information and sufficiency,” Ann. Math. Stat., vol. 22, pp. 79–86, 1951.

- [48] S. Kullback, Information Theory and Statistics. New York: Wiley, 1959.

- [49] J.E. Shore and R.W. Johnson, “Axiomatic derivation of the principle of maximum entropy and the principle of minimum cross-entropy,” IEEE Trans. Inf. Theory, vol. 26, pp. 26–37, 1980.

- [50] R.D. Luce, “A probabilistic theory of utility,” Econometrica, vol. 26, pp. 193–224, 1958.

- [51] R.D. Luce, Individual Choice Behavior: A Theoretical Analysis. New York: Wiley, 1959.

- [52] B.E. Kim, D. Seligman, and J.W. Kable, “Preference reversals in decision making under risk are accompanied by changes in attention to different attributes,” Front. Neurosci., vol. 6, p. 109, 2012.

- [53] C.A Holt and S.K. Laury, “Risk aversion and incentive effects,” Am. Econ. Rev., vol. 92, pp. 1644–1655, 2002.

- [54] V.I. Yukalov and D. Sornette, “Preference reversal in quantum decision theory,” Front. Psychol., vol. 6, p. 01538, 2015.

- [55] L.L. Thurstone, “A law of comparative judgment,” Psychol. Rev., vol. 34, pp. 273–286, 1927.

- [56] D.H. Krantz, “Rational distance functions for multidimensional scaling;” J. Math. Psychol., vol. 4, pp. 226–245, 1967.

- [57] D.L. Rumhelhart and J.G. Greeno, “Similarity between stimuli: an experimental test of the Luce and Restle choice models,” J. Math. Psychol., vol. 8, pp. 370–381, 1971.

- [58] P.L. Lorentziadis, “Preference under rsik in the presence of indistinguishable probabilities,” Oper. Res., vol. 13, pp. 429–446, 2013.

- [59] L. Devroye, Non-Uniform Random Variate Generation. New York: Springer, 1986.

- [60] D.J.C. MacKay, Information Theory, Inference, and Learning. Cambridge: Cambridge University, 2003.

- [61] T.M. Cover and J.A. Thomas, Elements of Information Theory. Hoboken: Wiley, 2006.

- [62] D.A. Meyer, “Quantum Strategies,” Phys. Rev. Lett., vol. 82, pp. 1052–1055, 1999.

- [63] J. Eisert and M. Wilkens, “Quantum games,” J. Mod. Opt., vol. 47. pp. 2543–2556, 2000.

- [64] E.W. Piotrowski and J. Sladkowski, “An invitation to quantum game theory,” Int. J. Theor. Phys., vol. 42, pp. 1089–1099, 2003.

- [65] S.E. Landsburg, “Quantum game theory,” Am. Math. Soc., vol. 51, pp. 394–399, 2004.

- [66] H. Guo, J. Zhang, and G.J. Koehler, “A survey of quantum games,” Dec. Support. Syst., vol. 46, pp. 318–332, 2008.

- [67] F.S. Khan and S.J.D. Phoenix, “Gaming the quantum,” Quant. Inf. Comput., vol. 13, pp. 231–244, 2013.

- [68] F.S. Khan and S.J.D. Phoenix, “Mini-maximizing two-qubit quantum computations,” Quant. Inf. Process., vol. 12, pp. 3807–3819, 2013.

- [69] M. Hutter, Universal Artificial Intelligence. Berlin: Springer, 2005.

- [70] C. Charness, E. Karni, and D. Levin, “On the conjunction fallacy in probability judgment: new experimental evidence regarding Linda,” Games Econ. Behav., vol. 68, pp. 551–566, 2010.

![[Uncaptioned image]](/html/1802.06348/assets/x2.png) |

Vyacheslav Yukalov received the M.Sc. degree in theoretical physics and Ph.D. degree in theoretical and mathematical physics from the Physics Faculty of the Moscow State University, Moscow, Russia, in 1970 and 1974, respectively. He has also received the Dr.Hab. degree in theoretical physics from the University of Poznan, Poznan, Poland, and the Dr.Sci. degree in physics and mathematics, from the Higher Attestation Committee of Russia. He was a Graduate Assistant at the Moscow State University from 1970 to 1973, before becoming an Assistant Professor, Senior Lecturer, and an Associate Professor at the Moscow Engineering Physics Institute, Moscow, Russia, from 1973 to 1984. Since 1984, he has been a Senior Scientist and Department Head at the Joint Institute for Nuclear Research in Dubna, Russia, where he currently holds the position of a Leading Scientist. He has authored about 450 papers in refereed journals and four books. He is also an Editor of five books and special issues. His current research interests include decision theory, quantum theory, dynamical theory, complex systems, nonlinear and coherent phenomena, self-organization, and development of mathematical methods. Prof. Yukalov is a member of the American Physical Society, American Mathematical Society, European Physical Society, International Association of Mathematical Physics, and the Oxford University Society. His scientific awards include the Research Fellowship of the British Council, Great Britain, from 1980 to 1981, Senior Fellowship of the Western University, Canada, in 1988, First Prize of the Joint Institute for Nuclear Research, Russia, in 2000, Science Prize of the Academic Publishing Company, Russia, in 2002, Senior Fellowship of the German Academic Exchange Program, Germany, in 2003, the Mercator Professorship of the German Research Foundation, Germany, from 2004 to 2005, and the Risk-Center Professorship of ETH Zürich, in 2015-2016. |

![[Uncaptioned image]](/html/1802.06348/assets/x3.png) |

Didier Sornette is professor of Entrepreneurial Risks in the department of Management, Technology and Economics at the Swiss Federal Institute of Technology (ETH Zurich), a professor of finance at the Swiss Finance Institute, and is associate member of the department of Physics and of the department of Earth Sciences at ETH Zurich. He uses rigorous data-driven mathematical statistical analysis combined with nonlinear multi-variable dynamical models including positive and negative feedbacks to study the predictability and control of crises and extreme events in complex systems, with applications to financial bubbles and crashes, earthquake physics and geophysics, the dynamics of success on social networks and the complex system approach to medicine (immune system, epilepsy and so on) towards the diagnostic of systemic instabilities. He directs the Financial Crisis Observatory that now operationally diagnoses financial bubbles in real-time ex-ante worldwide through a daily scanning of more than 25000 assets. |