Kinetic Theory for Finance Brownian Motion from Microscopic Dynamics

Abstract

Recent technological development has enabled researchers to study social phenomena scientifically in detail and financial markets has particularly attracted physicists since the Brownian motion has played the key role as in physics. In our previous report (arXiv:1703.06739; to appear in Phys. Rev. Lett.), we have presented a microscopic model of trend-following high-frequency traders (HFTs) and its theoretical relation to the dynamics of financial Brownian motion, directly supported by a data analysis of tracking trajectories of individual HFTs in a financial market. Here we show the mathematical foundation for the HFT model paralleling to the traditional kinetic theory in statistical physics. We first derive the time-evolution equation for the phase-space distribution for the HFT model exactly, which corresponds to the Liouville equation in conventional analytical mechanics. By a systematic reduction of the Liouville equation for the HFT model, the Bogoliubov-Born-Green-Kirkwood-Yvon hierarchal equations are derived for financial Brownian motion. We then derive the Boltzmann-like and Langevin-like equations for the order-book and the price dynamics by making the assumption of molecular chaos. The qualitative behavior of the model is asymptotically studied by solving the Boltzmann-like and Langevin-like equations for the large number of HFTs, which is numerically validated through the Monte-Carlo simulation. Our kinetic description highlights the parallel mathematical structure between the financial Brownian motion and the physical Brownian motion.

pacs:

??I Introduction

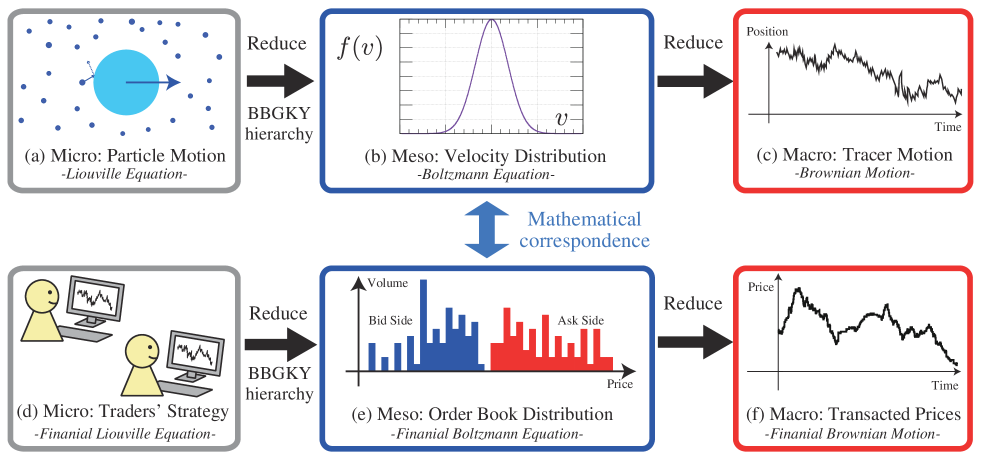

The goal of statistical physics is to reveal macroscopic behavior of physical systems from their microscopic setups, and has been partially achieved in equilibrium and nonequilibrium statistical mechanics KuboB . For example, kinetic theory has provided a mathematically rigid foundation for various non-equilibrium systems, such as dilute molecular gas, Brownian motion, granular gas, active matter, traffic flows, neural networks, and social dynamics Chapman1970 ; Broeck2004 ; Broeck2006 ; Brilliantov ; Bertin2006 ; Helbing ; Nishinari ; Prigogine ; Cai2004 ; Buice2013 ; Pareschi . The fundamental equations of kinetic theory (i.e., the Boltzmann and Langevin equations) were historically introduced on the basis of phenomenological arguments within the frameworks of non-linear master equations and stochastic processes Resibois1977 ; GardinerB . Furthermore, their systematic derivations were mathematically developed from analytical mechanics by Bogoliubov-Born-Green-Kirkwood-Yvon (BBGKY) and van Kampen Resibois1977 ; McDonald ; VanKampen ; Spohn1980 .

Inspired by these successes, physicists have attempted to apply statistical physic approaches even to social science beyond material science. In particular, financial markets have attracted physicists as an interdisciplinary area Mantegna1999 ; Slanina2014 since they exhibit quite similar phenomena to physics, represented by the Brownian motion. It is noteworthy that the concept of the Brownian motion was historically first invented by Bachelier in finance Bachelier1900 before the famous work by Einstein in physics Einstein1905 . After the work by Bachelier, various characters of Brownian motions in finance and their differences from physical Brownian motions have been found by both theoretical and data analyses. On the level of price time series, the power-law behavior of price movements has been reported empirically Mantegna1995 ; Lux1996 ; Plerou1999 ; Guillaume1997 ; Longin1996 . Such universal characters have been summarized as the stylized facts Slanina2014 and have been theoretically studied by time-series models Slanina2014 ; JDHamilton ; Engle1982 ; PUCK2006 and agent-based models Kyle1985 ; Takayasu1992 ; Bak1997 ; Lux1999 ; SatoTakayasu1998 ; Yamada2007 ; Yamada2009 ; Yamada2010 . In addition, characters of order books (i.e., current distributions of quoted prices) are studied by both empirical analysis and order-book models Slanina2014 ; Maslov2000 ; Daniels2003 ; Smith2003 ; Bouchaud2002 ; Farmer2005 ; Toth2011 ; Donier2015 . For example, the zero-intelligence order-book models Maslov2000 ; Daniels2003 ; Smith2003 ; Bouchaud2002 ; Farmer2005 ; Toth2011 ; Donier2015 have been investigated from various viewpoints, such as power-law price movement statistics Maslov2000 , order-book profile Bouchaud2002 , and market impact by large meta orders Toth2011 ; Donier2015 . The collective motion of the full order book was further found by analyzing the layered structure of the order book Yura2014 ; Kanazawa2017 , which was a key to generalize the fluctuation-dissipation relation to financial Brownian motion. To date, however, the modeling of individual traders’ dynamics based on direct microscopic evidence has not been fully studied, which was a crucial obstacle to apply the statistical mechanics from microscopic dynamics. To fully apply statistical mechanics to financial systems, it is expected necessary to establish the microscopic dynamical model of traders based on microscopic evidence and to develop a non-equilibrium statistical mechanics for such non-Hamiltonian many-body systems.

Recently, an extension of the kinetic framework for financial Brownian motion has been proposed by studying high-frequency data including traders identifiers (IDs) Kanazawa2017 . The dynamics of high-frequency traders (HFTs) were directly analyzed by tracking trajectories of the individuals, and a microscopic model of trend-following HFTs have been established showing agreeing with empirical analyses of microscopic trajectories. On the basis of the “equation of motions” for the HFTs, the Boltzmann-like and Langevin-like equations are finally derived for the mesoscopic and macroscopic dynamics, respectively. This framework is shown consistent with empirical findings, such as HFTs’ trend-following, average order book, price movement, and layered order-book structure. However, the mathematical argument therein was rather heuristic similarly to the original derivation of the conventional Boltzmann and Langevin equations. Considering the traditional stream of kinetic theory, a mathematical derivation beyond heuristics is necessary for the financial Brownian motion paralleling to the works by BBGKY and van Kampen.

In this paper, we show the mathematical foundation for the financial Brownian motion in the parallel mathematics in kinetic theory. For the trend-following HFT model Kanazawa2017 , we first define the phase space and the corresponding phase-space distribution (PSD) according to analytical mechanics McDonald ; Evans2008 . We then exactly derive the time-evolution equation for the PSD, which corresponds to the Liouville equation in analytical mechanics. The many-body dynamics for the PSD are reduced into few-body dynamics for reduced PSD according to the reduction method by BBGKY. By assuming the molecular chaos, we obtain the non-linear Boltzmann equation for the order-book profile and the master-Boltzmann equation for the market price dynamics. We also present their perturbative solutions for large number of HFTs to study the dynamical behavior of this system for all hierarchies. The validity of our framework is finally examined by Monte Carlo simulation.

This paper is organized as follows: In Sec. II, we briefly review the mathematical structure of the standard kinetic theory before proceeding to our work. In Sec. III, we describe the detail of the trend-following HFTs model as the microscopic setups. In Sec. IV, the microscopic dynamics of the model are exactly formulated in terms of the Liouville equation and the corresponding BBGKY hierarchal equation. In Sec. V, the financial Boltzmann equation is derived as the mesoscopic description of this financial system. In Sec. VI, the macroscopic behavior is analyzed by deriving the financial Langevin equation. In Sec. VII, implications of our theory are discussed for several related topics. We conclude this paper in Sec. VIII with some remarks.

II Brief Review of Conventional Kinetic Theory for Brownian Motion

Before proceeding to the core part of our work, we here briefly review the scenario of conventional kinetic theory for Brownian motion to convey our essential idea for generalization toward financial systems. Let us consider the Hamiltonian dynamics of gas particles of mass and a tracer particle of mass with the hard-core interaction in a hard-core box of volume (see Fig. 1a for a schematic). The momentum and position of the th gas particle are denoted by and for , and those of the tracer are denoted by and . The dynamics of this system are described by the equation of motions,

| (1) |

with interaction force between particles and for ( for and otherwise).

II.1 Liouville equation

In analytical mechanics, the phase space is defined as . The state of the system can be designated as the phase point defined by , and the corresponding PSD is denoted by . The time evolution of PSD is described by the Liouville equation,

| (2) |

with the Liouville operator 111In the presence of the hard-core interaction, the Liouville operator is non-local and is technically called the pseudo-Liouville operator Resibois1977 ; Ernst1969 ; Beijeren1979 ; KanazawaTheses . (see Refs. Resibois1977 ; McDonald ; Evans2008 ; Ernst1969 ; Beijeren1979 ; KanazawaTheses for the details). This equation is exactly equivalent to the equation of motions (1) mathematically, and is the fundamental equation for the microscopic description (Fig. 1a). This equation is however not analytically solvable as it fully addresses the original many-body dynamics without any approximation.

II.2 BBGKY hierarchy and Boltzmann equation

To focus on the one-body dynamics of a gas particle or the tracer, let us introduce the reduced PSDs,

On the assumption of binary interaction, we can exactly derive hierarchies of PSDs, such that

| (3) | ||||

| (4) |

with one-body Liouville operators and two-body collision operators . These equations are exact but not closed in terms of and .

To obtain analytical solutions, a further approximation is necessary. The standard approximation in kinetic theory is a mean-field approximation, called molecular chaos,

| (5) |

which is mathematically shown asymptotically exact for dilute gas in the thermodynamic limit (called the Boltzmann-Grad limit Cercignani1994 ). We then obtain the closed dynamical equation for as

| (6) |

which is the fundamental equation for the mesoscopic description (Fig. 1b). The steady solution for of the non-linear Boltzmann equation (6) is then given by the celebrated Maxwell-Boltzmann distribution.

II.3 Langevin equation

The stochastic dynamics for the macroscopic variables can be also obtained within kinetic theory. By applying molecular chaos for as

| (7) |

we obtain the master-Boltzmann equation (or the linear Boltzmann equation)

| (8) |

which belongs to the linear-master equations in the Markov process and describes the dynamics of the tracer particle. Equation (8) can be further approximated as the Fokker-Planck equation within the system size expansion VanKampen . One can thus deduce the Langevin equation for the tracer as the macroscopic description of the Brownian motion (Fig. 1c),

| (9) |

with viscous coefficient , temperature of the gas , and the white Gaussian noise with unit variance.

The above formulation shows the systematic connection from the microscopic Newtonian dynamics to the mesoscopic dynamics and macroscopic dynamics. This methodology is shown valid even for non-equilibrium systems when the gas is sufficiently dilute (see Refs. Broeck2004 ; Broeck2006 ; Brilliantov ; Bertin2006 ; Helbing ; Nishinari ; Prigogine ; Pareschi for its application to various nonequilibrium systems), and is one of the most successful formulations in statistical physics.

II.4 Idea to generalize kinetic theory toward finance

Here, let us remark our idea to generalize the framework toward financial Brownian motion. Financial markets have a quite similar hierarchal structure to the conventional Brownian motion (see Fig. 1d–f for a schematic): In the microscopic hierarchy, individual traders make decisions to buy or sell currencies at a certain price (Fig. 1d). In the mesoscopic hierarchy, the dynamics are coarse-grained into the order-book dynamics with removal of traders’ IDs (Fig. 1e). In the macroscopic hierarchy, the dynamics are reduced to the price dynamics (Fig. 1f). One can notice that these hierarchies directly correspond to those in kinetic theory; traders, order book, and price correspond to molecules, velocity distribution, and Brownian particle, respectively. In this sense, the financial markets have a similar hierarchal structure to that in kinetic theory. From the next section, we present a parallel mathematical framework for the description of financial markets from microscopic dynamics.

III Microscopic Setup

In this section, the dynamics of the trend-following HFT model in Ref. Kanazawa2017 is mathematically formulated within the many-body stochastic processes with collisions on the basis of microscopic empirical evidences.

III.1 Notation

We here briefly explain the notation in this paper. Any stochastic variable accompanies the hat symbol such as to stress its difference to non-stochastic real numbers such as . For example, the probability distribution function (PDF) of a stochastic variable at real time is denoted by with a non-stochastic real number (i.e., the probability of is given by ). The complementary cumulative distribution function (CDF) is also defined as . To simplify the notation, arguments in functions are sometimes abbreviated without mention if they are obvious. The ensemble average of any stochastic quantity is denoted by .

We next explain the terminology for the order book for the whole market (Fig. 2a). The highest bid (lowest ask) quoted price among all the traders is called the market best bid (ask) price (). The average of the market best bid and ask prices is called the market mid price . The difference between the market best bid and ask prices is called the market spread. The market transacted price means the price at which a transaction occurs in the market. In this paper, the market price (mathematically denoted by ) means the market transacted price for short.

As for a single trader, the highest bid (lowest ask) quoted price by a single trader is called the best bid (ask) price of the trader (denoted by () for the th trader). The average of the best bid and ask prices of the trader is called the mid price of the trader (denoted by ). Also, the difference between the best bid and ask prices of the trader is called the buy-sell spread of the trader (denoted by ), which is different from the market spread.

There are two types of time in this paper. One is the real time and the other is the tick time (Fig. 2b). The tick time is defined as a discrete time incremented by every market transaction and corresponds to the real time as a stochastic variable, such as . Here the square brackets for the function argument (e.g., ) means that the stochastic variable is measured according to the tick time (i.e., ), highlighting the differences to that measured according to the real time (e.g., with the round brackets).

III.2 Characters of real HFTs

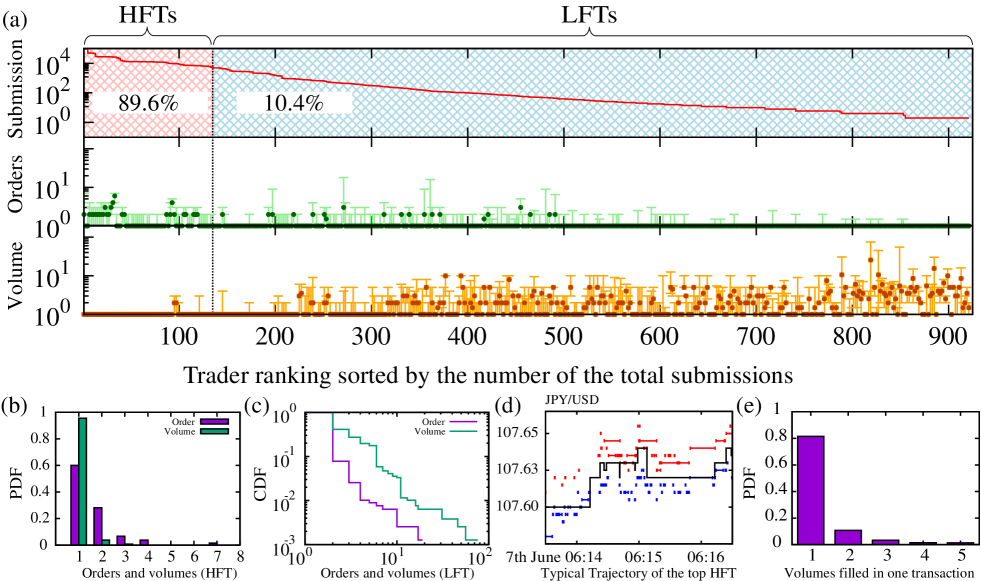

Here we describe the characters of real HFTs on the basis of high-frequency data analysis of a foreign exchange (FX) market. We analyzed the order-book data including anonymized trader IDs and anonymized bank codes in Electronic Broking Services (EBS) from the 5th 18:00 to the 10th 22:00 GMT June 2016. EBS is an interbank FX market and is one of the biggest financial platforms in the world. The minimum volume unit for transaction was one million US dollars (USD) for the FX market between the USD and the Japanese Yen (JPY). We particularly focus on HFTs, who frequently submit or cancel their orders according to algorithms. As reported in our previous work Kanazawa2017 , HFTs have several characters quite different from low frequency traders (LFTs). For this paper, an HFT is defined as a trader who submitted more than 2500 time during the week, similarly to a previous research EBS_Schmit . With this definition, the number of HFTs was 135 during this week, while the total number of traders submitting limit orders was 922 222 In Ref. Kanazawa2017 , 134 traders were defined as HFTs with one trader excluded whose order lifetime is extremely short., and 89.6% of all the orders in this market were submitted by the HFTs. Here we summarize the reported characters with several additional evidence:

-

(1).

Small number of live orders and volume: HFTs typically maintain a few live orders, less than ten (see Fig. 3a and b). Furthermore, a single order submitted by HFTs typically implies one unit volume of the currency. These characters are in contrast to those of LFTs, who sometimes submit a large amount of volumes by a single order (see Fig. 3a and c for the fat-tailed distributions of the number of orders or volumes for LFTs).

-

(2).

Liquidity providers: Typical HFTs plays the role of key liquidity providers (or market makers) and have the obligation to maintain continuous two-way quotes during their liquidity hours according to the EBS rulebook EBSRule (see Fig. 3d for a typical trajectory of the top HFT). The balance between the ask and bid order book is kept statistically symmetric to some extent, seemingly thanks to the liquidity providers.

-

(3).

Frequent price modification: Typical HFTs frequently modify their quoted prices by successive submission and cancellation of orders (see Fig. 3d for a typical trajectories of the top HFT). The lifetime of orders were typically within seconds for the top HFT, while the typical transaction interval was seconds in our dataset. In addition, 94.4% of the submissions by all the HFTs were canceled finally without transactions.

-

(4).

Trend-following property: HFTs tend to follow the market trends. We here denote the best bid and ask quoted price of the th trader and the market price at the tick time by , , and , respectively (see Fig. 2b). We also denote the mid quoted price of the the trader by . According to Ref. Kanazawa2017 , the future price movement of the th HFT statistically obeys

(10) conditionally on the historical price movement with characteristic constants and . The constant characterizes the strength of trend-following of the th trader, whereas characterizes the saturation threshold for the trader’s reaction to market trends. Here the ensemble average is taken for active traders on the condition that the previous price movement is given by with a non-stochastic real number . In the following, we introduce short hand notation for the conditional ensemble average as . In addition, the variance of the HFT’s future price movement is independent of historical market trends as

(11) with variance and constant independent of .

We also note that the one-to-one transaction is the basic interaction among traders in this market. The percentage of the one-to-one transaction was indeed 81.5% in our dataset (see Fig. 3e for more detailed evidence). On the basis of the above empirical results, the trend-following HFT model was proposed in Ref. Kanazawa2017 as the corresponding minimal microscopic model as reviewed in the next section.

III.3 Theoretical Model

On the basis of the above HFT’s characters, let us consider the microscopic model of HFTs according to Ref. Kanazawa2017 , within the framework of many-body stochastic systems with collisions.

III.3.1 State variables

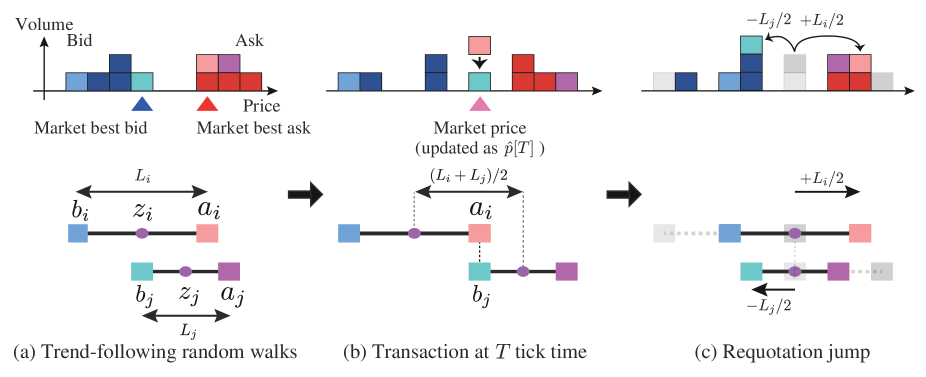

Let us consider a market composed of HFTs quoting both bid and ask prices and at all the time with the unit volume, where the index identifies the individual trader (). This assumption is consistent with the empirical HFT’s characters (1) and (2). For simplicity, the difference between the best bid and ask prices of a single trader (called buy-sell spread ) is assumed to be time-constant unique to the trader (see Fig. 4a):

| (12) |

On this assumption, the dynamics of individual HFTs are uniquely characterized by the mid price of HFTs as . The maximum and minimum values of the buy-sell spread among traders are denoted by and , respectively. According to Ref. Kanazawa2017 , the buy-sell distribution is directly measured to obey the -distribution, such that

| (13) |

with decay length and empirical exponent .

III.3.2 Trend-following random walks

HFTs have a tendency to maintain continuous two-sided quotes by frequently modifying their prices (i.e., successive cancellation and submission of limit orders), as required by the market rule EBSRule . This implies that the mid-price trajectory of an HFT can be modeled as a continuous random trajectory (i.e., the characters (2) and (3)). Remarkably, there is a mathematical theorem guaranteeing that the Itô processes (i.e., SDEs driven by the white Gaussian noise) are the only Markov processes with continuous sample trajectory GardinerB . As a minimal model satisfying all the characters of real HFTs (1)–11, the dynamics of the HFTs are modeled within the Itô processes as

| (14) |

in the absence of transactions (Fig. 4a) by taking into account the empirical trend-following properties 11. Here and are constants characterizing the strength and threshold of trend-following effect and is the white Gaussian noise with unit variance. The presence of the trend-following effect in Eq. (14) is the character of our HFT model, which induces the collective motion of limit orders Kanazawa2017 . The trend-following effect triggers translational motion of the full order book, which was crucial to reproduce the layered structure of the order book reported in Ref. Yura2014 .

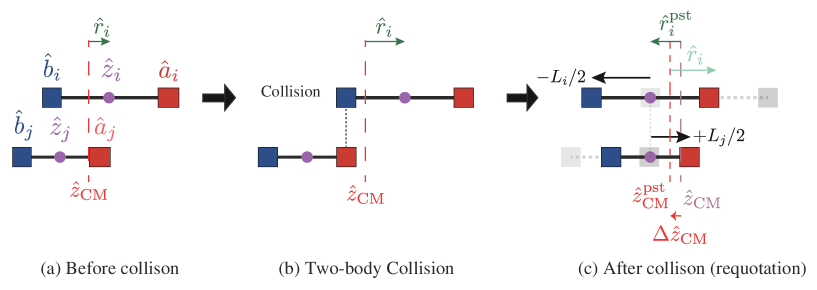

III.3.3 Transaction rule

When the best bid and ask prices coincide, there occurs an transaction (see Fig. 4b). The transaction condition (i.e., the condition of price matching) is mathematically given by

| (15) |

for . In the following, we assume that the index is an integer always different from another integer . At the instance of transaction , let us assume that the traders requote their prices simultaneously (see Fig. 4c) such that

| (16) |

where and are post-transactional bid and ask prices after transaction for between traders and , respectively. By introducing the mid-price of the individual traders as , the transaction rule is rewritten as

| (17) |

We here define the market price and the previous price movement at time . is the market price at the previous transaction; is the price movement by the previous transaction. They are updated after transactions under the following post-transaction rule (Fig. 4b and c):

| (18) |

with signature function defined by for and .

III.4 Complete model dynamics

We here specify the complete dynamics of the quoted prices within the framework of stochastic processes with collisions. When the previous price movement is , we assume that traders’ quoted prices are described by the trend-following random walks:

| (19) |

where is requotation jump term and is the th transaction time between traders and satisfying

| (20) |

The requotation jump corresponds to collisions in molecular kinetic theory. The price-matching condition (15) and the requotation rule (16) correspond to the contact condition and the momentum exchange rule in standard kinetic theory for hard-sphere gases, respectively. The summary of the model parameters is presented in the Table 1 with their dimensions. A sample trajectory of this model is depicted in Fig. 5a. We note that this model is a generalization of the previous theoretical model in Refs. Takayasu1992 ; SatoTakayasu1998 ; Yamada2007 ; Yamada2009 ; Yamada2010 on the basis of the above empirical facts (1)–11 on HFTs.

| Parameter | Meaning | Dimension |

|---|---|---|

| Number of traders | dimensionless | |

| Buy-sell spreads of traders | price | |

| Strength of trend-following | price/time | |

| Saturation for trend-following | price | |

| Variance of random noise | price2/time |

The dynamics of the price and the previous price movement can be specified within the framework of stochastic processes. Since and are updated at the instance of transactions, their dynamics synchronizes with collision time . Considering the transaction rule for prices (18), their concrete dynamical equations are thus given by

| (21) |

with the price after collision and the price movement after collision . In this paper, the Itô convention is used for the multiplication to -functions.

III.5 Slow variable

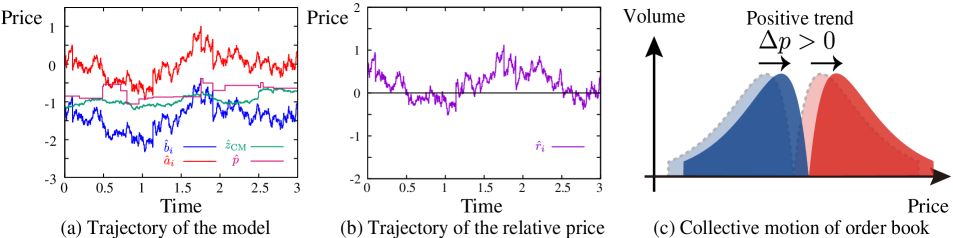

Introduction of slow variables is the key for reduction of the complex dynamics in general (e.g., the center of mass (CM) of the Brownian particle VanKampen and the slaving principles in synergetics HakenB ). Here we introduce the CM of the quoted prices as the slow variable of this system (Fig. 5a). The definition of the CM and its dynamics are given by

| (22) |

with . The CM characterizes the macroscopic dynamics of this system. As will be shown in Sec. VI.3.1, indeed, the diffusion coefficient of the CM turns out to be proportional to for the weak trend-following case, implying that the selection of is reasonable as a slow variable.

Another motivation to introduce the CM is to define the relative price from the CM such that

| (23) |

since the relative price has better mathematical characters than . For example, the relative price fluctuates around zero (see Fig. 5b for the dynamics in the comoving frame of CM) and has the stationary distribution, while the original variable diffuses to infinity for a long time and has no stationary distribution.

III.6 Difference to other order-book models

One of the unique characters of the HFT model is the collective motion of order book due to trend-following. As shown in Ref. Yura2014 , the order book has the layered structure in the sense that the difference in volumes of bid (ask) order book near best price has positive (negative) correlation with price movements. This implies that the order book exhibits the translational motion like inertia in physics (Fig. 5c), and thus movements of HFTs are not independent of each other like herding behavior. This collective motion has not been implemented in conventional order-book models, which are based on independent Poisson processes for order submission and cancellation, and is minimally implemented in our HFT model as trend-following for the consistency with the layered order-book structure Kanazawa2017 .

IV Main Result 1: Microscopic Description

As the main results of this paper, the analytical solutions to the trend-following HFT model are presented by developing the mathematical technique of kinetic theory. We first introduce the phase space for the HFT model in the standard manner of analytical mechanics, and derive the dynamical equation for the PSD, which we call the financial Liouville equation. We next derive the hierarchy for the reduced distributions similarly to the BBGKY hierarchy in molecular kinetic theory, which is the theoretical key to understand the financial system systematically as shown in Secs. V and VI.

IV.1 Phase space and phase-space distribution

Here first we introduce the phase space for the HFT model according to the standard manner of analytical mechanics. Let us introduce a vector , which corresponds to a phase point in the phase space as . Equations (19), (21), and (22) are the complete set of dynamical equations for the phase point, corresponding to the Newtonian equations of motions in conventional mechanics. Also, let us define the PSD function . Using the PSD, the probability is given by where the phase point exists at the time in the volume element .

IV.2 Financial Liouville Equation

As the first main result in this paper, we present the Liouville equation for the trend-following trader model (19)–(22) as the dynamical equation for the PSD. The dynamical equation for the PSD is given by

| (24) |

where the advective and diffusive Liovuille operator and the binary collision Liouville operator are defined by

| (25a) | ||||

| (25b) | ||||

Here we have introduced the symmetric absolute derivative for an arbitrary function and abbreviated derivatives and (see Appendix. A for the detailed derivation). We have also introduced a difference vector:

| (26) |

with movement of the CM . This is the first main result in this paper. The advective and diffusive Liovuille operator describes the continuous dynamics of the system in the absence of transactions, while the binary collision Liouville operator describes the discontinuous dynamics in the presence of transactions. Equation (24) formally corresponds to the Liouville equation (2) in molecular kinetic theory, and is called the financial Liouville equation in this paper. The financial Liouville equation completely characterizes the microscopic dynamics of all traders (Fig. 1d).

IV.3 Financial BBGKY Hierarchy

The financial Liouville equation (24) is exact but cannot be solved analytically. We therefore reduce Eq. (24) toward a simplified dynamical equation for a one-body distribution in the parallel method to molecular kinetic theory. According to the standard method in the kinetic theory, the Boltzmann equation, a closed dynamical equation for the one-body distribution, can be derived by systematically reducing the Liouville equation in the parallel method to BBGKY (see Sec. II.2). We here present the lowest-order equation of reduced distributions for the trend-following HFT model in the parallel calculation in kinetic theory. We first introduce the relative price from the CM as . We also define the one-body, two-body and three-body reduced distribution functions for the relative price:

| (27a) | |||

| (27b) | |||

We then obtain the lowest-order hierarchal equation for the one-body distribution as

| (28) |

with one-body, two-body, and three-body Liouville operators , , defined by

| (29a) | ||||

| (29b) | ||||

| (29c) | ||||

effective variance , and jump size ,

| (30) |

Here indirectly originates from the movement of the CM during requotation. The detailed derivation of Eq. (28) is described in Appendix. B. Equation (28) formally corresponds to the conventional BBGKY hierarchal equation (3) for the mesoscopic description. On the basis of Eq. (28), the Boltzmann-type closed equation for the one-body distribution is derived in the next section.

We also derive the hierarchal equation for the macroscopic dynamics. For the macroscopic variables , we here define the reduced distributions:

| (31) |

We then obtain the hierarchal equation for the macroscopic dynamics,

| (32) |

with advective and diffusive Liouville operator and collision Liouville operator between particles and :

| (33a) | ||||

| (33b) | ||||

Equation (32) formally corresponds to the lowest-order conventional BBGKY hierarchal equation (8) for the macroscopic description. Using this hierarchal equation (32), a closed master-Boltzmann equation is derived for the macroscopic variables in the next section.

The set of Eqs. (28) and (32) is the second main result in this paper. Equation (28) connects the microscopic description (Fig. 1d) to the mesoscopic description (Fig. 1e), and Eq. (32) connects the mesoscopic description (Fig. 1e) to the macroscopic description (Fig. 1f). Their detailed derivation is presented in Appendix. B. These equations are derived in a parallel calculation to the conventional BBGKY hierarchal equations (3) and (8), and are called the financial BBGKY hierarchal equations in this paper. Similarly to the conventional BBGKY hierarchal equations (3) and (8), our hierarchal equations (28) and (32) are exact but are not closed: the dynamics of low-order distributions are driven by those of higher-order distributions. Appropriate approximations are necessary to derive closed equations, such as the molecular chaos, which will be studied in the next section.

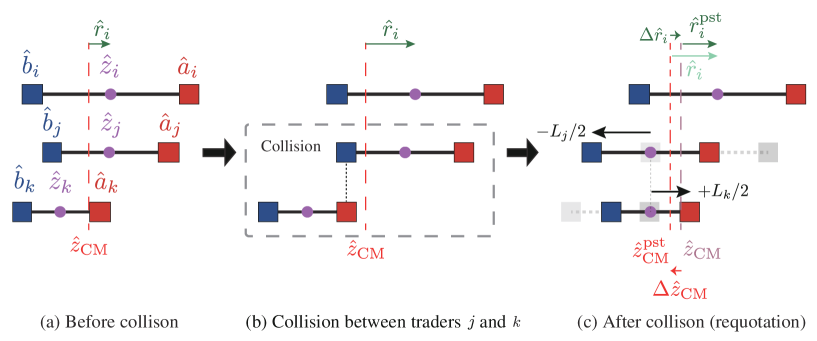

Remark on the three-body collision term.

We here remark the emergence of the three-body collision term in the BBGKY hierarchy (28), which is slightly different from the conventional BBGKY hierarchy (3). This term appears because our kinetic theory is formulated on the basis of the relative price . To understand this point, let us consider the movement of the relative price of the th trader during collision between traders and (see Fig. 7 for a schematic of three-body collision). While the mid price of the th trader does not move during the collision between traders and , the CM of this system moves through a distance of . The relative price thus moves indirectly through a distance of , which appears in the three-body collision operator (29c). This effect is intuitively small for the large limit and is finally shown irrelevant to the leading-order (LO) and next-leading-order (NLO) approximations as discussed later.

V Main Result 2: Mesoscopic description

From microscopic dynamics, we have derived the BBGKY hierarchal equation (28) for the mesoscopic description of the HFT model in a parallel manner to the conventional BBGKY hierarchal equation (3). Here we proceed to derive the closed mean-field model for the mesoscopic description, which will be finally shown useful to understand the order-book profile systematically.

V.1 Financial Boltzmann Equation

We here derive a closed equation for the one-body distribution function by assuming a mean-field approximation. The one-body and two-body distribution functions and are introduced conditional on the traders’ spreads and , satisfying and . Let us approximately truncate the two-body correlation as

| (34) |

which corresponds to molecular chaos (5), the standard approximation in the conventional kinetic theory. The validity of this approximation will be numerically evaluated in Sec. V.2. A closed mean-field equation for the one-body distribution is thus obtained as

| (35) |

with mean-field probability flux for . The systematic derivation of this equation is the third main result in this paper (see Appendix. C for the detail). Equation (35) is a closed equation for the one-body distribution function, and corresponds to the Boltzmann equation in molecular kinetic theory (see Fig. 1b). Equation (35) is therefore called the financial Boltzmann equation in this paper. Here the dummy variable () implies the transactions as a bidder (an asker), and the integrals on the right-hand side (rhs) correspond to the collision integrals in the standard Boltzmann equation (6). Remarkably, Eq. (35) is derived from a systematic calculation from the Liouville equation (24), whereas it was originally introduced with a rather heuristic discussion in our previous paper Kanazawa2017 .

V.2 Solution

Let us focus on the steady solution of Eq. (35). Equation (35) can be analytically solved for on an appropriate boundary condition (See Appendix. D for the detail) for the steady state. The LO steady solution is given by the tent function:

| (36) |

The average order-book profile for the ask side is given by the superposition of the tent function:

| (37) |

We note that the average order-book profile has a symmetry, such that for the average bid order-book . We also note that the NLO correction (98) can be obtained as shown in Appendix. E. Though the LO solution (36) is sufficient to understand the average order-book profile, the NLO solution (98) is necessary to understand the dynamics of the financial Langevin equation, as shown in Sec. VI.

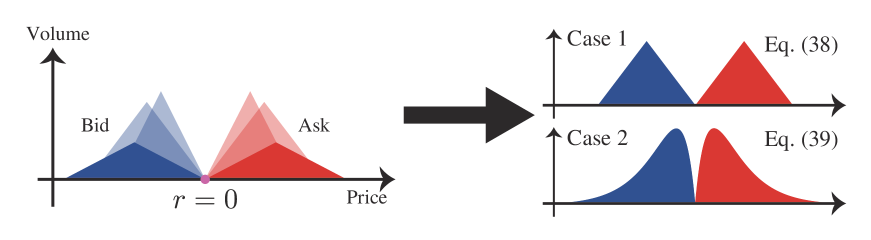

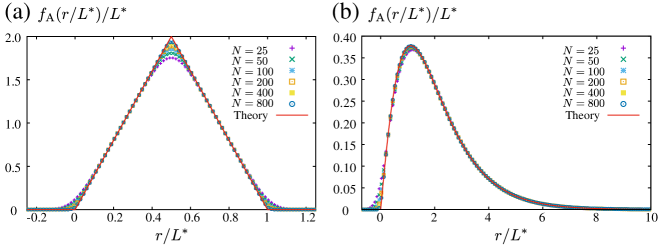

Numerical comparison 1: -distributed spread.

We here study the theoretical order-book profiles for two concrete examples with numerical validation (see Appendix. F for the detailed implementation). Let us first consider the case of a single spread . The corresponding average order-book profile is given by the tent function

| (38) |

We have numerically examined the validity of this formula in Fig. 9a, which shows the numerical agreement with our formula (38). The LO solution (38) works quite well for the description of the order-book profile, and the numerical convergence in Fig. 9a implies that Eq. (38) might be exactly valid for .

Numerical comparison 2: -distributed spread.

The formula (37) works well even for and when the integrals converge. As an example, let us consider the case where the spread obeys the -distribution

| (39) |

which was empirically validated through single-trajectory analysis of individual traders in our previous work Kanazawa2017 . We have numerically examined the validity of this formula in Fig. 9b, which shows the numerical agreement with our formula (39). The numerical convergence in Fig. 9b implies that the LO solution (39) might be also exact for .

VI Main Result 3: Macroscopic Description

In this section, we derive the stochastic equations for the macroscopic dynamics of this system from the BBGKY hierarchal equation (32) in the parallel method to the master-Boltzmann equation (8) for physical Brownian motions.

VI.1 Master-Boltzmann Equation for Financial Brownian Motion

On the basis of the financial BBGKY hierarchy (32) for the macroscopic dynamics, we derive a closed dynamical equation for the macroscopic variables . Here we first make the assumption of molecular chaos,

| (40) |

Using the NLO solution (98), we deduce a closed master-Boltzmann equation for the macroscopic dynamics (see Appendix. G for the detailed calculation):

| (41) |

where the mean-field collision Liouville operators for the macroscopic variables is defined by

| (42) |

with , Gaussian distribution , jump size distribution , and mean transaction interval defined by

| (43) |

by assuming is zero for . Note that Eq. (42) is a master equation (or the differential form of the Chapman-Kolmogorov equation GardinerB ) and is equivalent to a set of stochastic differential equations (SDEs) (see Eq. (103) in Appendix. G).

VI.2 Financial Langevin Equation

We have derived the stochastic dynamics for the three macroscopic variable as the master equation (42) (or equivalently SDEs (103)) in the continuous time . We next simplify the dynamics (42) of the three macroscopic variables into that of a single macroscopic variable in the tick time . In the tick time …., the dynamical equation for the price movement is given by

| (44) |

where is time interval between transaction, is the zigzag noise of order , and is a random noise of order (see Appendix. H for the detail). The systematic derivation of Eq. (44) is the fourth main result of this paper. Equation (44) corresponds to the conventional Langevin equation (9), and is thus called the financial Langevin equation in this paper.

Within the mean-field approximation, we can specify all the statistics of the random noise terms from analytics. The time interval is given by the exponential random number with mean interval ,

| (45) |

The zigzag noise is defined by the difference of two Gaussian random numbers as

| (46) |

where is a discrete-time white Gaussian noise with unit variance. The random noise term is specified as

| (47) |

where is a discrete-time white Gaussian noise with unit variance and is a discrete-time white noise term obeying with an -independent distribution .

We next discuss the interpretation of each term on the rhs of Eq. (44). The trend-following term induces the collective motion of the order book and thus keeps the price movement in the same direction for a certain time-interval similarly to the inertia in physics. On the other hand, the zigzag noise term exhibits one-tick negative autocorrelation, such that

| (48) |

and has the effect to change the price movement direction alternately. In this sense, the trend-following term and the zigzag noise have the opposite effect to each other; the balance between their strengths is crucial for the qualitative behavior of the market price dynamics. The random noise term originates from the slow dynamics of the CM: is the diffusion term of the CM during a transaction time-interval and is the movement term of the CM by requotation jumps of traders after transaction.

VI.3 Solution

The macroscopic dynamics of the price strongly depends on the balance between the strength of trend-following effect and that of the zigzag noise. Here we present the solutions of the financial Langevin equation depending on the strength of trend-following with the dimensional analysis. The price movement originating from trend-following behavior is estimated to be (of price dimension). On the other hand, the amplitude of the zigzag noise is estimated to be (of price dimension). Their balance is thus characterized by the dimensionless parameter defined by

| (49) |

Another dimensionless control parameter is the ratio between the average movement by the trend-following (of price dimension) and the saturation threshold against the market trend (of price dimension):

| (50) |

The set of dimensionless parameters governs the qualitative dynamics of the market price. For consistency with the empirical report Kanazawa2017 , we focus on the case of in this section, whereby the saturation of the hyperbolic function is valid. (see Sec. VII.9 for the discussion on the case with ). Here we introduce three classifications in terms of the strength of trend-following:

-

1.

Weak trend-following case:

-

2.

Strong trend-following case:

-

3.

Marginal trend-following case:

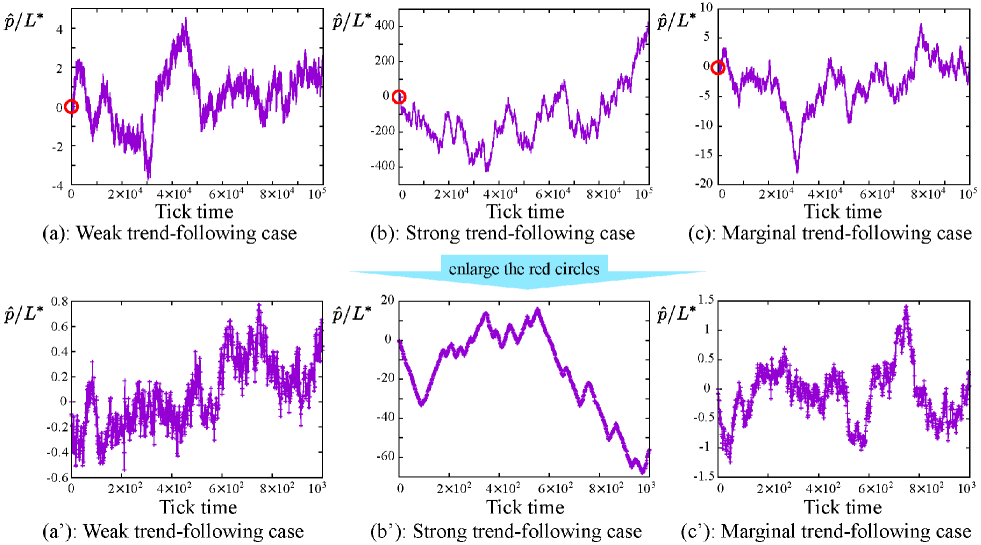

Sample trajectories are plotted in Fig. 10 to highlight the character of each case: For the weak trend-following case (Fig. 10a), the price tends to move upward and downward alternatively every tick because of the zigzag noise . For the strong trend-following case (Fig. 10b), the unidirectional movement of price is kept for a certain time period. For the marginal trend-following case (Fig. 10c), both zigzag and unidirectional movements randomly appear because both effects are in balance. As will be shown later in detail, the marginal case may be the most realistic, at least in our dataset. We next study these qualitative characters through statistical analysis of price time series within the mean-field approximation.

VI.3.1 Weak trend-following case

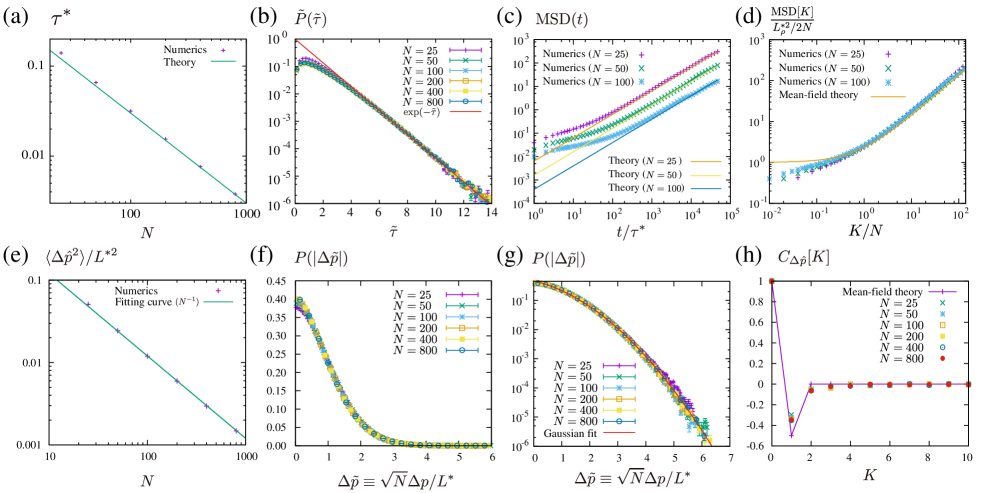

For the weak trend-following case , the trend-following effect is negligible compared with the zigzag noise: . The master equation (42) can then analytically solved in continuous time . By applying the system size expansion VanKampen (see Appendix. I for derivation), we obtain the diffusion equation for the CM

| (51) |

with the renormalized diffusion coefficient up to the order of and the second-order Kramers-Moyal coefficient . The diffusion constant decays for , which implies that the dynamics of the CM become slower as the number of the traders increases. Given that the dynamics of price coincides with that of the CM for a long timescale, the diffusion of the price is also shown normal for a long timescale with the same diffusion coefficient in the real time . The mean square displacement (MSD) based on real time is thus analytically obtained as

| (52) |

showing the normal diffusion for a long time.

We also study price movement at one-tick precision. For the weak trend-following case, the only relevant term in Eq. (44) is the zigzag noise for a short timescale. Price movement then obeys the Gaussian distribution

| (53) |

The autocorrelation function of the price movement is also given by

| (54) |

Interestingly, this property is consistent with an empirical fact that price movements typically exhibit zigzag behavior for a short timescale, which is reflected in the one-tick strong negative autocorrelation of the price movement.

Here we discuss the origin of the strong negative correlation in terms of price movement. Remarkably, only the random noise is dominant for long time whereas only the zigzag noise is dominant for a short timescale. For , indeed, we obtain

| (55) |

which implies that the contribution by the zigzag noise is negligible compared with that of the random noise (i.e., ). Considering that the random noise originates from the diffusion of the CM, Eq. (55) means that the macroscopic behavior of price is governed by the slow dynamics of the CM. Even though the price movement at one-tick precision is much larger than that of the CM, such movement is irrelevant to the macroscopic dynamics of the whole system. This is the origin of the strong negative correlation for price movement in this model with weak trend-following. To relieve such negative correlation, stronger trend-following is necessary to induce the collective motion of the order book as discussed in Ref. Kanazawa2017 . We note that similar slow diffusion is observed in the conventional zero-intelligence order-book models Maslov2000 ; Daniels2003 ; Smith2003 , with which the trend-following effect is not incorporated likewise.

We also note that the negative correlation (54) is also related to the slow diffusion of price for a short timescale. Indeed, the MSD is given by

| (56) |

within the mean-field approximation. This formula implies that the MSD is almost constant (i.e., no diffusion) for a short timescale while it is asymptotically linear (i.e., the normal diffusion) for a long timescale .

Numerical comparison.

Here we examine the validity of our formulas through comparison with numerical results for the -distributed spread (see Appendix. F for the implementation).

Transaction interval.

We first check the statistics of the time-interval between transactions . The mean transaction interval is numerically plotted in Fig. 11a, showing the quantitative agreement with the theoretical prediction (45) including the coefficient. We also numerically plotted the probability distribution of with scaling parameters for horizontal and vertical axes, qualitatively showing the exponential tail for large . Here, we have introduced a scaled transaction interval and plotted the scaled probability distribution in Fig. 11b

| (57) |

with scaling parameters for the horizontal and vertical axes and . The coefficients and were determined by the least-square method to fit the exponential tail for each . The numerical results imply the modification for the decay length , whereas the mean-field solution (45) predicts . This means that the mean-field solution (45) is not exact but is rather qualitatively correct for the probability distribution .

This factor modification can be roughly understood from the viewpoint of the order statistics, as discussed in Ref. Kanazawa2017 . The mean-field approximation predicts the exponential interval distribution (45), which means that the transaction obeys the exact Poisson process. As the numerics shows, however, the transaction obeys the Poisson process not exactly but only asymptotically. One candidate of its origin is that a transaction occurs as a pair of arrivals of both bid and ask quotes. Let us assume that the arrival of a bid (ask) quote at the transaction price obeys the Poisson statistics as . Any transaction is assumed to occurs when both bid and ask quotes arrive at the transaction price. We then make an approximation that and . On the basis of the orders statistics David2003 , we obtain

| (58) |

where the fitting parameter was determined by the consistency condition for the average interval as . We thus obtain the modification factor as an approximation.

We note that the transaction interval is not under the influence of the trend-following effect. The above statistical characters on transaction interval are therefore shared for any parameter set of .

MSD.

Our theoretical prediction on the MSD is numerically examined here for analyses based on both real time and tick time . We first numerically check the MSD (52) based on real time in Fig. 11c. This figure shows the quantitative agreement with our theoretical formula (52) without fitting parameters. We also check the MSD based on tick time in Fig. 11d, showing a quantitative agreement with the theoretical prediction (56) for . For small , the agreement is not perfect between the numerical data and the theoretical line, but the slowness of the diffusion is qualitatively observed as predicted in the mean-field solution (56).

Price movement.

The dependence of the variance of price movement is checked in Fig. 11e on the number of traders . We numerically obtained with modification factor and . Though there is a discrepancy in terms of the factor , the mean-field solution (53) qualitatively works well for the variance of price movement. We also checked the PDF of the scaled price movement (Fig. 11f and g for the peak and tail of PDF, respectively). In Fig. 11g, we also show a Gaussian-type fitting curve for the tail with parameters , , and . These figures suggests that the PDF of the price movement has the Gaussian tail, which is qualitatively consistent with the theoretical prediction (53) ( and ).

Autocorrelation.

The autocorrelation function is checked in Fig. 11h, which supports the qualitative consistency between the theory (55) and the numerical results in terms of the negative correlation at tick. This negative correlation implies that the price time series exhibits zigzag behavior in the absence of the trend-following effect. Indeed, the probability of is theoretically for the mean-field model (see Appendix. J), considerably higher than (i.e., the pure random walks). This result is also qualitatively consistent with the numerical result (around ) as shown in Table 2.

| Case | Same sign | Different sign |

|---|---|---|

| (a) Weak trend-following case | 0.389 | 0.611 |

| (b) Strong trend-following case | 0.949 | 0.051 |

| (c) Marginal trend-following case | 0.480 | 0.520 |

| (d) Real price time series | 0.479 | 0.521 |

VI.3.2 Strong trend-following case

The strong trend-following case is also analytically tractable, whereby the trend-following term is dominant such that . Here we assume that the saturation threshold is sufficiently small such that . This condition simplifies the analysis below because the hyperbolic function can be approximated as the signature function, such that . Price movement is then governed by the first term on the rhs of Eq. (44), which approximately leads the exponential distribution,

| (59) |

with decay length for . The decay length is given by the mean movement originating from the trend-following as within the mean-field approximation (45). By applying the improved mean-field approximation (58), more consistent coefficient is obtained with the numerical result below. The trend-following effect plays similar roles to momentum inertia in physics, which are reflected in the autocorrelation function and the MSD plot as shown numerically in the next paragraph.

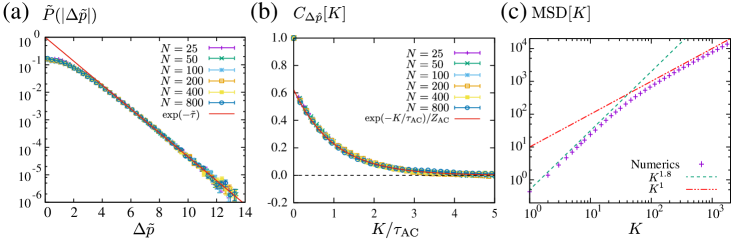

Numerical comparison.

Numerical characters are studied here for the strong trend-following case under the parameter set . We first study the price movement distribution . In Fig. 12a, the price movement distribution is plotted by scaling the horizontal and vertical axes,

| (60) |

qualitatively showing the exponential tail for the scaled price movement . Here the scaling parameters and were determined by the least square method for the tail. The mean-field solution (45) and the improved mean-field solution (58) predicts and , respectively. These theoretical predictions are qualitatively consistent with the numerical estimation .

We next study the autocorrelation function of the price difference based on tick time in Fig. 12b by scaling the horizontal line. For our parameter sets, the numerical result implies that the autocorrelation function can be written as

| (61) |

with fitting parameters and . This autocorrelation suggests that the strong trend-following keeps unidirectional price movements for a certain time-interval. Indeed, the probability of is much higher than under this condition as shown in Table 2. In addition, the numerical MSD plot in Fig. 12c shows the rapid diffusion (almost ballistic motion ) for a short time and the normal diffusion for a long time

VI.3.3 Marginal case

The most complex case is the marginal case , where both trend-following effect and zigzag noise contribute to the price movement as . While both trend-following term and random noise term are relevant on this condition, the main contribution to the price movement tail originates from the trend-following term because the former yields the exponential tail while the latter yields the Gaussian tail. We thus obtain the exponential tail (59) for the price movement for the marginal case. This theoretical conjecture is to be validated numerically below.

Numerical comparison.

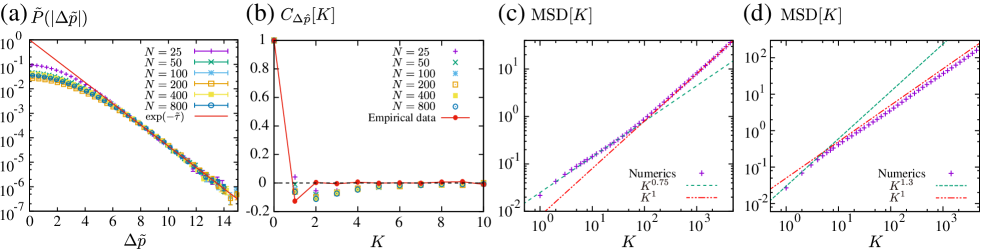

We studied the marginal case under the parameter set . In Fig. 13a, we plot the price movement distribution by scaling both horizontal and vertical axes as Eq. (60). We thus obtain the exponential-law tail (60) for the price movement qualitatively.

In Fig. 13b, we also studied the autocorrelation function on tick time through both numerical simulation (points) and empirical data analysis (solid line) of the real time series. This figure shows the slight negative correlation around , which was qualitatively consistent with the empirical result in our dataset. This result also implies that the price time series exhibits a slight zigzag behavior for a certain tick period. This theoretical implication was validated by analyzing the probability of as summarized in Table 2. The table 2 shows the quantitative consistency between the marginal trend-following case and the real price time series.

We also discuss the behavior of MSD in Fig. 13c and d, which shows both slow and rapid diffusions dependently on the parameters. For example, we set the parameters and for Fig. 13c and d, respectively. In Fig. 13c, the MSD plot exhibits a slightly slow diffusion for a short time and the normal diffusion for a long time. In Fig. 13d, on the other hand, the MSD plot exhibits a slightly rapid diffusion with the Hurst exponent for a short time and the normal diffusion for a long time. We thus conclude that our HFT model can reproduce a variety of diffusion by adjusting the trend-following parameters.

VII Discussion

We here discuss implications of our theory to understand various topics intensively.

VII.1 Comparison with real dataset

| Case | Prob. of diff. sign | |||

|---|---|---|---|---|

| (a) Weak trend-following case | Gaussian | Exponential | Strongly negative at | around |

| (b) Strong trend-following case | Exponential | Exponential | Strongly positive | less than |

| (c) Marginal trend-following case | Exponential | Exponential | Slightly negative around | around |

| (d) Empirical facts | Exponential | Exponential | Slightly negative around | around |

Here we provide a detailed comparison between empirical facts and the above theoretical predictions as follows: As for the order-book profile , the validity of the formula (39) was examined by analyzing daily average order-book in Ref. Kanazawa2017 . The exponential-tail for time interval distribution was studied in Ref. MTakayasu2002 by removing the non-stationary property of time series. The price movement was reported to obey the exponential-law in Ref. Kanazawa2017 by removing the non-stationary property of time series. The price time series tended to exhibit zigzag behaviors, which were reflected in the negative autocorrelation function around (see Fig. 13c) and the probability of (i.e., taking different signs) slightly over (see Table 2). All these characters are consistent with our theoretical prediction for the marginal trend-following case (see Table 3 for the summary of the comparison). The HFT model presented here can show precise agreements with these empirical facts. Considering that the market was stable in our dataset, we concluded that our HFT model can describe the FX market well, at least during the stable period. Description of unstable markets is out of scope of this paper and is a next interesting problem for future studies.

VII.2 Validity of Mean-Field Approximation

We have numerically validated the mean-field theory. The LO solution (36) quantitatively describes the order-book profile (37) with high precision and the NLO solution (98) qualitatively describes the price movement (44). Possible reasons are discussed here why the mean-field approximation works so well for the trend-following HFT model considering the common sense in physics.

The mean-field approximation is expected invalid for low-dimensional physical systems because two-body correlations do not disappear between colliding pairs for a long time. Colliding particles are not allowed to be separated far from each other because of the continuity of paths and the low-dimensional space geometry. For one-dimensional Hamiltonian systems with hard-core interactions, for example, any particle successively collides against the fixed neighboring particles and two-body correlations then remain forever. The mean-field approximation is therefore shown valid only for high-dimensional systems, at least for several concrete setups. From this viewpoint, the precise agreement is not trivial between the mean-field solution (37) and the numerical result.

In contrast, the continuity of the path is absent due to requotation jumps though our model is a one-dimensional system. The transaction rule (17) compulsorily separates the transaction pairs after their collision, because of which there is no restriction on the combination of possible transaction pairs. In the limit, in addition, transactions between the same pair traders becomes rare (i.e., the probability of successive transaction between the same pair decays as the order of ), which implies quick disappearance of the two-body correlation between transaction pairs for . This is our conjecture to validate the mean-field approximation for this model. If this conjecture is correct, kinetic-like descriptions may be valid for various agent-based systems, if agents are separated compulsorily to avoid successive interactions between the same pairs.

VII.3 Non-stationary property for price movements: power-law behavior

Financial markets are known to exhibit strong non-stationary properties statistically, such as the intraday activity patterns. Here we discuss the impact of such non-stationary properties on the price movements and its relation to the celebrated power-law behavior for a long time.

Our theoretical model implies that the exponential law (59) for the price movement as the basic statistical property. This property was shown consistent with the real price movement in Ref. Kanazawa2017 for a short time, by removing the non-stationary property in terms of the decay length . The decay length is related to the number of traders and the strength of trend-following , both of which are expected to have non-stationary properties. At least, indeed, the number of traders exhibits a trivial but strong non-stationary property with a correlation with the decay length.

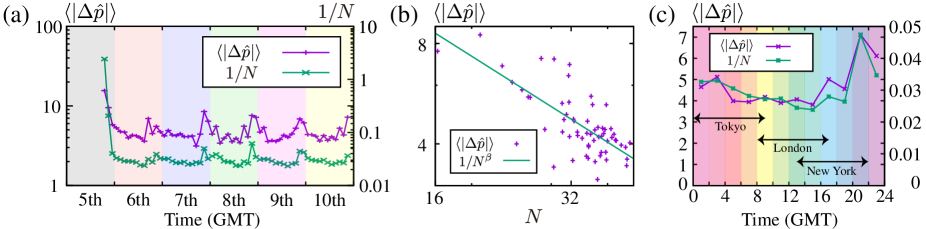

To illustrate this character, let us analyze the statistical relation between the mean absolute price movement and the number of HFTs in our dataset. We measured as a representative of the market volatility for a short time and studied its correlation with every two hours in Fig. 14a. Spearman’s rank correlation coefficient was between and . This result implies that the market volatility is relatively small when is large, which is qualitatively consistent with our theoretical prediction of (e.g., if parameters are time-constant other than ). The regression analysis between and implies as shown in Fig. 14b. We also note that both and had a tendency to become large during inactive hours of the EBS market (Fig. 14c).

The non-stationary property of the market volatility is related to the power-law behavior of the price movement for a long time. In Ref. Kanazawa2017 , the decay length is shown to have a power-law distribution , which implies the power-law price movement for a long time as the superposition of the short-time exponential distribution,

| (62) |

with the complementary cumulative price movement distribution and . This result is consistent with previous empirical researches Plerou1999 ; Lux1996 ; Guillaume1997 ; Longin1996 . We thus concluded that both exponential law and power-law can consistently coexist at least in our dataset.

We here note that the FX market in our dataset was rather stable without any external shocks. While the exponential-law was essential for a short time in our dataset, we do not deny the possibility that the power-law may be essential even for a short time for unstable markets under external shocks. We believe that that there would exist essentially different structures in unstable markets and it would be interesting to study the statistics of traders’ behavior in unstable markets under financial crisis for a future perspective.

VII.4 Non-stationary property for transaction interval: power-law behavior

As for the transaction interval, our theory predicts that the exponential-law (45) is essential rather than the power-law. This result is consistent with the previous report in Ref. MTakayasu2002 , showing that the exponential-law is essential for a short time but it superposition leads the power-law behavior of transaction interval for a long time.

VII.5 Non-stationary property for order-book dynamics: stability of the order-book profile

We have discussed that both price movement and transaction interval are quite sensitive to non-stationary properties of the market. On the other hand, the average order-book profile is relatively insensitive to such non-stationary properties, in contrast to the price movement and transaction interval. Indeed, the average order-book profile is independent of the trend-following property . In addition, the order-book profile shows a convergence for , such that is an -functions, which implies that large variation of does not have impact on the order-book profile.

Similar insensitivity does not exist for the price movement and transaction interval. Indeed, they exhibit the strong divergence for as and , which implies the huge impact of large variation of on their statistics.

In this sense, the average order-book profile is a stable quantity to measure under non-stationary processes, whereas the price movement and transaction interval are unstable quantities. Our theory provides the insight on the sensitivity of measured quantities to the non-stationary nature of the market. We believe that developing systematic methods to remove such non-stationary nature is the key to understand not only the origin of power-laws in finance but also the essence of market microstructure.

VII.6 More is different: vs.

One of the most interesting features in statistical physics lies in the fact that many-body systems can exhibits essentially different characters from few-body systems, such as the critical phenomena and collective motion. Though the current HFT model here does not exhibit critical phenomena, an essential difference can be shown between the cases of and . To illustrate this point, let us consider the case of without trend-following. Our theory is applicable to solve the case of exactly, which leads the same solution presented in Ref. Yamada2009 . The price movement is then predicted to obey the exponential-law even without trend-following, which is qualitatively different from the Gaussian-law for . This difference appears because the dynamics of the CM are not sufficiently slow for . For , indeed, one can show the absence of the zigzag noise term in the financial Langevin equation (44), which leads the dominance of the random exponential noise . For , on the other hand, the random noise is negligibly small due to the slow CM dynamics, and the trend-following effect becomes necessary to explain the exponential price movements statistics. The model presented here thus exhibits essentially different characters as the number of traders increases.

VII.7 Does the trend-following effect break the random walk hypothesis?

Seemingly, the trend-following effect is strongly contradictory to the conventional assumption of the random walk hypothesis. Our analysis however implies that the situation is not so simple: In the absence of the trend-following, the market price exhibits the strong zigzag behavior, which is far from the pure random walks. By adjusting the strength of trend-following appropriately (i.e., the marginal trend-following case), on the other hand, the zigzag behavior is somewhat relieved and the market price time series rather approaches the random walks. In this sense, the trend-following strategy might originate from the rational behavior of HFTs to equilibrate the strategies among traders. It would be interesting to pursue the origin of trend-following behavior from economical viewpoints as future studies.

We also note that the real price time series exhibits slightly zigzag behaviors (i.e., the negative autocorrelation and the tendency for price movement to take different sign), which are consistent with our HFT model for the marginal trend-following case. These different characters from the pure random walks have been well-known in finance and are obviously applicable to predict the direction of price movement in one-tick future. It is not easy however to make profits over the market spread (i.e., the difference between the market best bid and ask prices) by utilizing only these properties. While the real price time series slightly deviates from the pure random walks, it is not obvious whether these characters provide easy opportunities to statistically make profits. Making profits requires us to predict price movements beyond the market spread, which is out of scope of this paper but is an interesting topic for a future study.

VII.8 Possible generalization 1: multiple-tick trend-following random walks and the PUCK model

In this manuscript, we have addressed the trend-following HFT model with one-tick memory. It is straightforward to generalize the one-tick memory model toward a multiple-tick memory model, such that

| (63) |

where is the exponential moving average for the price movements with decay time and renormalization constant . In the authors’ view, this model is more realistic because such an exponential moving average is a popular strategy among HFTs according to a detailed regression analysis for trend-following Sueshige2018 . We then obtain a generalization of the financial Langevin equation as

| (64) |

The generalized financial Langevin equation (64) is equivalent to the potentials of unbalanced complex kinetics (PUCK) model PUCK2006 , which was previously introduced by time-series data analyses. Here we use an identity

| (65) |

for the exponential moving averages and , which leads the PUCK model

| (66) |

under a random potential . In this sense, our theory is straightforwardly applicable to a derivation of the PUCK model.

VII.9 Possible generalization 2: reduction to the random multiplicative processes

In Sec. VI.3, we assume both for analytical simplicity and for consistency with the empirical report Kanazawa2017 . Here we discuss the case with , whereby the hyperbolic trend-following reduces to the linear trend-following as . The financial Langevin equation (44) is thus replaced with a linear financial Langevin equation

| (67) |

By introducing the second-order difference , we obtain a similar equation to the conventional Langevin equation as

| (68) |

with a random frictional coefficient , consistently with the simplified discussion in the supplementary material of Ref. Kanazawa2017 . Since Eq. (68) belongs to the random multiplicative processes TakayasuPRL1997 , the price movement obeys the power-law statistics, consistently with the previous exact solution Yamada2009 for the two-body case .

VIII Conclusion

In this paper, we have presented a systematic solution for the trend-following trader model, which was empirically introduced in our previous work Kanazawa2017 . Starting from the microscopic dynamics of the individual traders, we have systematically reduced the multi-agent dynamics by generalizing the mathematical method developed in molecular kinetic theory. We first introduce the phase space for our model and derive the dynamical equation for the phase space distribution function, which corresponds to the Liouville equation in the conventional analytical mechanics. On the basis of the Liouville equation for the trend-following trader model, we derive a hierarchy of reduced distributions in the parallel method to the BBGKY hierarchy. By introducing the mean-filed approximation, corresponding to the assumption of molecular chaos, we derive the mean-field dynamical equation for the one-body distribution function, similarly to the Boltzmann equation. We then derive the analytic solution for the mean-field model, whose validity is numerically examined when the number of traders is sufficiently large. We also derive the financial Langevin equation, governing the macroscopic dynamics of the financial Brownian motion, and study the macroscopic properties of the market price movements.

Here we have clarified the power of the kinetic frameworks in describing financial markets from microscopic dynamics. In our conjecture, this success lies on the fact that the financial markets approximately satisfy the key assumptions of the binary interaction and molecular chaos (see Secs. III.2 and VII.2 for related discussions); the one-to-one transaction (i.e., the binary interaction) is the most basic interaction, and traders less likely transact with the same counterparty for . We believe that the financial market is one of the best subjects to apply the kinetic theory, besides traffic flow and wealth distribution Helbing ; Nishinari ; Prigogine ; Pareschi . We also believe that generalization of kinetic theories would be a key to clarify various social systems from microscopic dynamics, since we have access to various microscopic data these days.

Acknowledgements.

We have greatly acknowledged to T. Ito, M. Katori, H. Hayakawa, M. Oshikawa, F. van Wijland, S. Ogawa, K. Yamada, T. Ooshida, D. Yanagisawa, S. Ichiki, K. Tamura, and J. Ozaki for fruitful discussions. We also appreciate NEX for their provision of the EBS data on their foreign exchange platform. This work was supported by Japan Society for the Promotion of Science KAKENHI (Grand No. 16K16016 and No. 17J10781) and Japan Science and Technology Agency, Strategic International Collaborative Research Program.Appendix A Detailed Derivation of Financial Liouville Equation

We here derive the financial Liouville equation for the trend-following trader model. The dynamics of our model is given by

| (69) |

where we have introduce the colored Gaussian noise satisfying and . For the mathematical convenience below, we finally take the white noise limit : . We next consider the dynamics of the center of the mass :

| (70) |

Let next us consider the dynamics of an arbitrary function for . The time-evolution of is governed by the continuous movement by the continuous noise term and the discontinuous jumps by the deterministic transaction term . We then obtain

| (71) |

where we have introduced the difference vector induced by transactions defined by

| (72) |

with and . Let us decompose the sum of -functions here as

| (73) |

where we have used just before (or equivalently, just before ) by taking collision directions into account. We then take the ensemble average of both hand side of Eq. (71) with the aid of the Novikov’s theorem Novikov for an arbitrary functional

| (74) |

for the colored Gaussian noise . Here we remark the following two important relations for the -function for the phase space :

| (75) |

and

| (76) |

with the dummy variable

| (77) |

By substituting , we take the ensemble average for both hand-sides of Eq. (71) in the limit. We then obtain

| (78) |

with an abbreviation symbol . Here, let us pay attention to the signature of the derivatives. Considering for all and for , we obtain the signature of derivatives

| (79) |

Equation (78) can be simplified into Eq. (24) in terms of signatures by introducing the symmetric absolute derivative

| (80) |

Note that Eq. (24) is a partial integro-differential equation because of the transaction jumps, though the conventional Liouville equation is a partial differential equation. This implies that our financial Liouville equation (24) technically corresponds to the pseudo-Liouville equation Resibois1977 ; Ernst1969 ; Beijeren1979 ; KanazawaTheses rather than the Liouville equation.

Appendix B Detailed Derivation of Financial BBGKY Hierarchy

We here derive the lowest BBGKY hierarchal equation for the reduced distribution function (28), starting from the financial Liouville equation (24). We first introduce the relative price from the CM as . By making transformation , the financial Liouville equation can be rewritten as

| (81) | ||||

where we have used the chain rule for the variable transformation:

| (82) |

We have also introduced with

| (83) |

According to the definition of the one-body, two-body, and three-body reduced distributions (27), the lowest-order hierarchy is then derived as

| (84) |

with effective variance and jump size with , . Equation (28) is thus derived from Eq. (84) by introducing Liouville operators.

Appendix C Detailed Derivation of Financial Boltzmann Equation (35)

In this Appendix, we derive the financial Boltzmann equation (35) from the financial BBGKY hierarchy (28). To simplify the hierarchal equation (28), we use the symmetry among the traders in terms of the spread: when the the spreads are equal for both th and th traders, their one-body distributions are also equal, namely,

| (85) |

Furthermore, there are also symmetries for the two-body and three-body distributions such that

| (86) |

and

| (87) |

On the basis of these symmetries, we introduce the conditional distributions on spreads. We denote the minimum and the maximum spreads among traders by and , respectively. We also assume that the number of the traders is so large that we can approximately regard spreads as continuously distributed. In other words, the spread distribution is an approximately continuous function. We assume that for . The one-body and two-body distributions and are defined conditional on spreads and by

| (88) |

Here we make the following approximations for :

-

1.

The effective variance is approximated as the

(89) -

2.

The discrete sum is approximated as continuous integrals:

(90) -

3.

The relatively small displacement is negligible:

(91)

On the basis of these approximations, the lowest hierarchal equation (28) can be rewritten as

| (92) |

where correction terms of are ignored. We thus have obtained Eq. (92), which was derived in our previous paper Kanazawa2017 by a heuristic argument. The financial Boltzmann equation (35) is then derived by making the mean-field approximation (34) to Eq. (28). Note that the three-body correlation terms in Eq. (28) is finally irrelevant under these assumptions. The consistency of this assumption is examined using the NLO solution of Eq. (35) in Appendix. K.

Appendix D Boundary Condition

We here note the boundary condition for the financial Boltzmann equation (35). We introduce the cutoff for the boundaries at and assume the following four assumptions:

-

1.

Equation (35) is valid only for .

-

2.

The cutoff is taken sufficiently large: .

-

3.

The probability is zero beyond the boundary:

-

4.

The boundaries are the reflecting barriers, which ensure the conservation of the probability:

(93)

The probability conservation (93) can be mathematically proved in Appendix. L under this boundary condition. The cutoff parameter is finally taken infinity as , and the main results in this paper do not depend on .

We here also note another related technical issue for the mean-field solution (36). The large number limit is taken before the limit for the boundary . We also note that, when the limit for the maximum spread is taken, the limit is taken in the last order in this paper to conserve the second assumption . Equation (36) therefore technically implies

| (94) |

Appendix E Next-to-leading-order solution to the financial Boltzmann equation

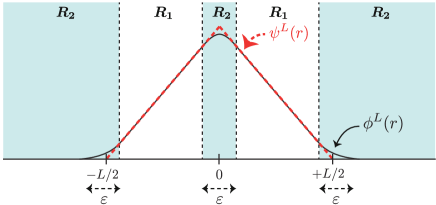

The LO solution for the financial Boltzmann equation (35) is given by the tent function (36). Here we consider the NLO solution in the steady state, where the edges of tent functions are smooth because of the finite-number effect of traders. We first derive the NLO solution by an intuitive asymptotic analysis, and will check that the solution satisfies the original financial Boltzmann equation (35) by direct substitution. We make the following three ansatzs (see Fig. 15 as a schematic): (i) There are two domains and . Here is the thickness of the boundary layers originating from the finite-number effect, with order as will be shown later. (ii) Out of the boundary layers , the deviation from the LO solution is negligible. (iii) In the boundary layers , the deviation from the LO solution is not negligible. On the basis of these ansatzs, for , we approximate

| (95) |

The financial Boltzmann equation (35) is then approximated for as

| (96) |

where we have ignored the inflow flux on the basis of the ansatz and we have introduced , , and . The general solution around is given by

| (97) |

with arbitrary coefficients and . Under the boundary condition , we obtain . Considering the asymptotic relation for , we obtain for the asymptotic connection to the LO solution in . We thus obtain the NLO solution around the boundary ,

| (98) |

which is consistent with the LO solution (36) for : .

We have obtained the NLO solution (98) rather intuitively, but we can check that the solution satisfies the original Boltzmann equation (35) up to the order of by direct substitution. Around , indeed, we obtain

| (99) |