client2vec: Towards Systematic Baselines for Banking Applications

Abstract

The workflow of data scientists normally involves potentially inefficient processes such as data mining, feature engineering and model selection. Recent research has focused on automating this workflow, partly or in its entirety, to improve productivity. We choose the former approach and in this paper share our experience in designing the client2vec: an internal library to rapidly build baselines for banking applications. Client2vec uses marginalized stacked denoising autoencoders on current account transactions data to create vector embeddings which represent the behaviors of our clients. These representations can then be used in, and optimized against, a variety of tasks such as client segmentation, profiling and targeting. Here we detail how we selected the algorithmic machinery of client2vec and the data it works on and present experimental results on several business cases.

1 Introduction

Data science processes such as data exploration, manual feature engineering,

validating hypotheses and constructing baselines can become convoluted, and often call for empirical and domain knowledge. Being a data science company, one of our concerns at BBVA D&A is to provide our data scientists with tools to improve these workflows, in the spirit of works such as [11, 15, 37, 22, 6, 27].

Most data analytics and commercial campaigns in retail banking revolve around the concept of behavioral similarity, for instance: studies and campaigns on client retention; product recommendations; web applications where our clients can compare their expenses with those of similar people in order to better manage their own finances; data-integrity tools.

The analytic work behind each of these products normally requires the construction of a set of customer attributes and a model, both typically tailored to the problem of interest.

We aim to systematize this process in order to encourage model and code reuse, reduce project feasibility assessment times and promote homogeneous practices.

Our contribution to this end is client2vec: a library to speed up the construction of informative baselines for behavior-centric banking applications. In particular, client2vec focuses on behaviors which can be extracted from account transactions data by encoding that information into vector form (client embedding). These embeddings make it possible to quantify how similar two customers are and, when input into clustering or regression algorithms, outperform the sociodemographic customer attributes traditionally used for customer segmentation or marketing campaigns. We pursued a solution with minimal computational and preprocessing requirements that could run even on simple infrastructures. This is not damaging: baselines need to provide an informative starting point rather than an off-the-shelf solution, and client2vec helps generating them in few minutes, with few lines of code. Additionally, client2vec offers our data scientists the possibility to optimize the embeddings against the business problem at hand. For instance, the embedding may be tuned to optimize the average precision for the task of retrieving suitable targets for a campaign.

This paper describes our experience and what we learned while building client2vec; it is organized as follows:

in Section 2 we go through the principles we built client2vec on; in Section 3 we mention relevant related work, from both the application and the algorithmic perspectives; in Section 4 we describe the structure of the account transactions data we used; in Section 5 we dig deeper into the algorithms we studied when developing our library, why we chose them and how we trained them; finally, in Section 6 we present experiments in the tasks of client segmentation, reconstruction of missing expenses and retrieval of targets for a commercial campaign.

2 Our approach

We built client2vec following an analogy with unsupervised word embeddings [28, 10, 9, 38], whereby account transactions can be seen as words, clients as documents (bags or sequence of words) and the behavior of a client as the summary of a document. Just like word or document embeddings, client embeddings should exhibit the fundamental property that neighboring points in the space of embeddings correspond to clients with similar behaviors.

We thus identified two possible paths: one is to extract vector representations of transactions and compose them into client embeddings, as done with word embeddings to extract phrase or document embeddings via averaging or more sophisticated techniques [38]; the other is to embed clients straight away. We explored the former option by applying the famed word2vec algorithm [28] to our data and then pooling the embeddings of individual transactions into client representations with a variety of methods. For the latter approach, which is the one currently employed by client2vec, we built client embeddings via a marginalized stacked denoising autoencoder (mSDA) [9]. For comparison and benchmarking purposes, we also tested the embedding comprising the raw transactional data of a client and the one produced by sociodemographic variables.

Embeddings are then turned into actionable baselines by casting business problems as nearest neighbor regressions. This builds on successful works in computer vision[39, 18, 36] which adopt the principle of the unreasonable effectiveness of data [17]. As we will show, such an approach produces effective baselines in a variety of scenarios.

3 Related work

The need for automation has been noticed by the wider data science community. The AutoML Challenge proposed contestants to solve classification and regression tasks without human intervention [16]. Projects like the Automatic Statistician111https://www.automaticstatistician.com/, which aims at developing an “artificial intelligence for data science”, for instance apply automatic, efficient exploration of the space of models for non-parametric regression by composing kernel structures [11] or matrix decomposition by organizing and exploring models in a context-free grammar [15]. Other strategies involve using Gaussian Processes for hyperparameter search [37] and autonomous feature engineering from raw data [22]. Along the same lines, automation may concern data cleaning [6] or even summarizing data and models with natural language [27]. A de facto standard for the rapid construction of baselines is the class of gradient boosting methods 222https://github.com/dmlc/xgboost/tree/master/demo#machine-learning-challenge-winning-solutions, accessed 2018-02-09. [14]. However, we seek a method that can produce an unsupervised embedding of a client that be semantically interpretable, with neighboring points representing behaviorally similar clients, and that we can reliably employ in tasks as diverse as retrieval or clustering, as we do in Section 6.

Consequently, we rather draw inspiration from the straightforward, successful application of textual embeddings produced by models like word2vec [28] or Glove [32] to data science problems such as predicting the outcome of soccer matches from Tumblr hashtags [34] or improving the accessibility of the information in medical corpora [29]. More interestingly, mechanisms for embedding words are applicable to any indexable entity and such models have been extended to embed data other than text. This includes embedding nodes in a graph [35], items in recommender systems [1], Pinterest’s pins [25] and even twitter users [4], where different embeddings of the same entity are mixed using a form of canonical correlation analysis.

One drawback of these embedding methods is that they lack a formalism to embed sets or sequences of items, rather than the items themselves. On sequential data, methods such as RNNs offer in most cases state-of-the-art performance [24]. However, these models are unsuitable to our use case: they are usually data-hungry and computationally burdensome, hence inadequate to rapidly and systematically build baselines. Autoencoders, on the other hand, have been shown to be effective at creating unsupervised embeddings of formal representations of sets (e.g. bag-of-items) [2, 9, Sec. 7] and have thus found application, for instance, in embedding patient data [30]. The latter work, in particular, leverages stacked denoising autoencoders (SDAs) and offers a very similar scenario to the ones we consider in our applications. We chose however to focus on mSDAs to reduce the computational cost associated with SDAs, Section 5.4.

4 Account transactions Data

Current account transactions include movements like direct debits, commission fees, coupons of financial products or debit card expenses. Said movements normally have an associated description, either in formatted or free text, and a movement code whose descriptivity is out of our control and ranges from the extremely general (a money transfer of any kind) to the very specific (the purchase of tickets of a given airline). The taxonomy of transactions is further enriched by assigning movement codes to one of 70 categories, e.g. Utilities or Car insurance. This operation is carried out by an internal tool employing search and NLP algorithms. Together with new structure, by miscategorizing some movements this procedure can also introduce noise, to which the algorithms we tested showed good resilience.

We chose to focus client2vec on an aggregation of current account data by client, year and transaction category. This aggregation can easily be applied to most commercial cases of interest, is readily available within BBVA and preserves enough information within a fairly succinct dataset. Past applications within BBVA include segmentation, campaigns, recommendations and automated finance management. Specifically, for a year worth of data, we aggregate each client into a vector of 70 numbers, one per category, as depicted in Figure 1. Unless otherwise specified, this is the data format that we will refer to throughout the rest of the paper.

5 Tools and Methodology

As we remarked, at the core of the baselines client2vec allows to build, is an encoding of the raw transactions data. When building the client2vec library, we then had to compare various embedding strategies against relevant use cases. In this section we detail said strategies, motivate their choice and outline the training methodology we used in our experiments.

5.1 Sociodemographic variables

The obvious fundamental benchmark to which we compared all methods are sociodemographic variables: age, gender, income range, postcode, city and province. Such variables are typically considered by banks, retailers and other organizations for purposes like segmentations or campaigns. All of these variables are categorical, even the income, having been binned in several ranges. As such, we one-hot encode them and then reduce the dimensionality of the vector thus obtained in order to measure the Euclidean distance between two sociodemographic representations.

5.2 Raw transactions

The simplest behavioral embedding of a client could be expressed as , where is the aggregated expense of that customer in the th category. This corresponds to one row of the table in Figure 1, possibly normalized (typically such that ) or binarized. This embedding helps us demonstrate that it is not only the use of transactional data instead of sociodemographic variables that can enhance the performance in certain banking applications, but also the representation algorithms applied on the data.

Following the analogy with NLP: if an individual account operation in a certain category is interpreted as a “word”, we can think of the raw transactions embedding as one-hot encodings (when binarized), or as “bag of words” (when continuous).

5.3 Embedding via word2vec

Word2vec [28] is a family of embeddings of words in documents, which express each word token with a dense vector. These vectors result from the intermediate encoding of a 2-layer network trained to reconstruct the linguistic context of each token and exhibit strong semantic properties, e.g. two nearby vectors refer to words that may share the same topic or even be synonyms.

In order to apply word2vec to account transactions it was key to transform our transactions data into sequences of meaningful tokens that word2vec could process. Indeed, concepts like “words” and “contexts” do not arise naturally in financial transactions. Moreover, we need them to reflect the different nature of each movement which the mere value of the transaction fails to capture: 1000€ spent on restaurants and 1000€ spent on pension plans likely point towards two different behavioral profiles.

5.3.1 Transactions quantization

To introduce a word-like entity we created a suitable quantization of our data. First, percentiles are computed for all transactions of our dataset in each category, i.e. computing percentiles for all the columns of the table in Figure 1. The percentiles are then used to define bins for the transactions of each category. Each bin is labeled with a word composed by the category identifier and the bin’s boundaries

. For example, referring to Figure 1, CAT1_-50.20:-7.16 is a possible label of a bin containing the transactions in CAT1 of both clients 1 and N. Such words then correspond to expenses in a certain category and range. Finally, a quantized copy of the raw dataset is built by replacing individual transactions with the label of the bin they fall inside, hence yielding a finite set of repeating words that depend on the nature of the transaction. The dataset thus transformed assumes some of the structural features of natural text, such as a finite vocabulary and a sentence-like organization.

A limitation of this approach is that properties like syntactical structures or parts of speech are here completely absent. Although a definition of context as co-occurrence of bin labels still holds, it is however be much weaker than that existing in text since our data, in the aggregation we are using, lacks a form of ordering. We found out that this severely hinders the performance of word2vec embeddings, which encouraged us to explore the alternative offered by mSDAs, Section 5.4.

5.3.2 From transactions to clients

Applying word2vec on the quantized dataset will yield transaction embeddings, which we then need to compose into client embeddings. Strategies such as concatenation or mean-pooling have been proposed in the context of computational linguistics [3, 23]. While intuitive and computationally inexpensive, they present weaknesses such as overly increasing the dimensionality of the representation or losing all information about word order. The computer vision community also extensively investigated the problem of pooling local representations [7, 31] leveraging ideas such as Fisher kernels [20, 33], max-pooling [7] or geometric approaches such as VLAD [21]. The latter, in particular, if applied to textual data, would amount to computing cluster centroids for the word vectors and subsequently concatenating the differences between each word vector and the corresponding centroid for all the words in a sentence. Considering that the centroids can be seen as “representative” words, VLAD allows to embed a sentence by its proximity to representative concepts.

This makes sense even in the context of transaction embeddings, where we’d like a client embedding to capture the salient behavioural characteristics of an individual. We therefore composed our low-level transaction embeddings obtained through word2vec with mean-pooling as well as VLAD.

5.4 Embeddings via mSDAs

As anticipated in Sections 3 and 5.3.1, after observing the inconsistent performance of word2vec-based embeddings, following the line of work of [30] we turned our attention to autoencoders. In particular, we chose to employ a marginalized stacked denoising autoencoder [9] which offers several advantages: ease of implementation and deployment; modest computational cost; excellent performance in domain adaptation tasks; and a natural manifold-learning interpretation explaining why neighboring embeddings represent clients with similar behaviors [9, 40]. We see all of these as valuable properties in a baseline.

MSDAs’ starting architecture is that of denoising autoencoders (DAs) [40], which are trained to minimize a reconstruction error such as the squared error used for continuous-valued data. In DAs the input is first corrupted with noise, yielding a which is then encoded as and finally decoded back to , as usual with weight matrices , , biases , and squashing nonlinearity . Denoising autoencoders can be stacked, yielding increasingly richer representations of the input data [40, 41].

The aim of this architecture is to let the autoencoder learn the statistical dependencies among the variables in , as that will allow it to reconstruct the value of a variable given the others. This is the information which an autoencoder encodes in the embeddings it produces. Therefore, two clients whose embeddings are close together don’t necessarily have the same expenses, but rather expenses with similar statistical dependencies. Following the manifold-learning and the generative-model interpretations of DAs [40] we can then think of the autoencoder as a way to learn a manifold on which neighboring points are mapped back to behaviorally similar client by the decoding function . Furthermore, the good performance shown by autoencoders in transfer learning and domain adaptation [9, 43, 42] suggests a statistical robustness suitable to build versatile baselines.

The change introduced by mSDAs is to marginalize out the noise distribution and train the autoencoder as if it had observed infinitely many noisy variations of the training set. The marginalized autoencoder is then modeled as a single reconstruction matrix , with the dimension of the input. Following [9], when the number of noisy observations goes to infinity, can be written as

| (1) |

where is the cross-correlation matrix between clean and noisy data, is the precision matrix for the noisy observations, and the expectation is taken over the noise distribution. By rewriting (1) as it is possible to interpret the weights in as follows: higher weights indicate which features in the data carry most information when reconstructing a target feature.

This construction of the autoencoder saves us from specifying the dimension of the intermediate encoding, while we use the the “reconstructed” version as the representation of which, in the non-stacked case, has the same dimension of . Such embedding therefore has the following interpretation: each entry holds the most likely reconstruction value for that variable. In the context of our data, this means that each entry holds the most likely average transaction value in the corresponding category, given all the other transactions of that client.

A limitation and at once an advantage of mSDAs is that their implementation boils down to solving the system of linear equations specified in (1), yielding a complexity of , that is cubic in the number of features 444Notice however that the model can be adapted to deal with high-dimensional data [9].. Nevertheless, we did not experience any performance issue on the datasets we consider in Section 6. These sets reflect those normally used for some commercial applications within BBVA, containing between 120K and 300K clients, each represented with 70 to 700 features. MSDAs are therefore an appropriate choice for our use cases, easy to implement, hassle-free to deploy and fast to train and tune due to their small numbers of hyperparameters. Indeed, the only model-related hyperparameters in our training are the probability for the Bernoulli masking noise and the number of stacked layers. One may also treat the choice of the nonlinearity as a hyperparameter, but we chose to keep a for all our models.

Finally, in terms of preprocessing, mSDAs’ requirements are also minimal: we can use the raw transactions table with just a few adjustments such as binarizing, -normalizing, log-normalizing, max-normalizing or rescaling from to . These are also treated as hyperparameters and optimized for each individual use case the mSDA is being employed on.

5.5 Model selection

We treat the preprocessing options for mSDAs listed above like hyperparameters to optimize at train time. Likewise, the hyperparameters for the word2vec benchmark are the word-embedding dimension and the context window size [28], while for the raw transaction embeddings we only choose whether to -normalize, log-normalize or binarize. The optimization is carried out separately for each use case we consider.

6 Experiments and Results

In this section we report the experiments we ran to check which of the client representation methods was the most versatile.

In particular, we first evaluated the embeddings against two base use cases: client segmentation and the reconstruction of the presence of transactions in a left-out category. The former also provided us with a qualitative description of how mSDA-based embeddings can extract meaninfgul behavioral patterns from transactional data. From these experiments it became apparent that mSDAs were offering the best representations, so we finally tested them on a commercial case of campaign targeting.

Observe that the use cases we are considering may be better tackled with more sophisticated machinery, e.g. advanced clustering techniques [12] in Sections 6.1 and 6.2 or recommender systems [5] in Sections 6.3 and 6.4. However, our aim is not to provide a state-of-the-art solution to these use cases, but rather to employ them as tests to select a good embedding for client2vec and, finally, to show the potential of the baselines thus obtained. All the experiments have been carried out on anonymized data and with sensitive information removed or adequately tokenized.

6.1 Clustering of clients

One of the most immediate use cases for a client embedding is generating a segmentation of the client base. One example of such segmentation arises in the functionality “Compare yourself” of our banking app 555www.bbva.es/eng/general/bconomy/pedro/index.jsp, accessed 2018-02-09.. Here, customers can compare their own expenses in certain categories against those of their sociodemographic segment, which is defined by 4 variables (age, income, gender and postcode). Note that these attributes have been selected and constructed by manual adjustment over time. For instance, an attribute like “income” is prone to be built progressively by trial and error as there are many non-deterministic signals of income in our data, which a data scientist might only discover progressively.

Our proposal for this first use case is to plug the embeddings we’re testing into a clustering algorithm and compare the homogeneity of the values of a left-out target category in the resulting clusters. This approach fits the interpretation of mSDAs highlighted in Section 5.4.

6.1.1 Setup and evaluation

We use a dataset with a year worth of data for 120k clients. For each target category and embedding , calling the expense of client in category we use the vector

of remaining attributes to compute an embedding . That is, each time we leave out one target category for evaluation purposes. The embeddings thus obtained are clustered via K-means in 300 clusters, a number comparable to that of the sociodemographic segments. While better clustering algorithms are available [12], K-means is a common first choice in the phase of baseline construction.

Call the set of transaction categories, the set of clusters produced for category by the embedding , the set of customers whose embedding is in , and the corresponding values in the left-out category. We define the dispersion of by the median spread within each cluster , with the spread being the standard deviation . By repeating this for all , we can evaluate embeddings by the average dispersion across all categories:

| (2) |

The rationale is that if customers are really similar within a cluster, this similarity should generalize to the unseen category and produce a low dispersion.

6.1.2 Results

Table 1 shows the results of the experiment: the nominal values of and variation relative to the sociodemographic embedding baseline. Simply moving away from the use of sociodemographic variables already produces a significant improvement, but within the embeddings built on transactional data the one offering the best performance is that produced by an mSDA.

To us, this is a critical implication in terms of data science productivity: for this use case, a baseline requiring one call to the client2vec library to obtain client embeddings, plus K-Means, yields more homogeneous customer segments than those of hand-crafted, domain-specific attributes. To complement these quantitative results, the next section will provide a qualitative assessment of whether mSDAs really identify customers with similar behavior.

| Method | Relative | Nominal | |

|---|---|---|---|

| Sociodemographic | +0.0 | 266e-5 | |

| Transactions | +58.66 | 110e-5 | |

| mSDA | +61.62 | 102e-5 | |

| word2vec + Avg | +48.19 | 137e-5 | |

| word2vec + VLAD | +50.59 | 131e-5 |

6.2 Case study: the typical traveler

We consider the case of clients that have travel-related expenses, and conjecture that a typical traveler should also have expenses in the Hotels category. This mining experiment further illustrates the benefits of transactional embeddings over sociodemographic variables.

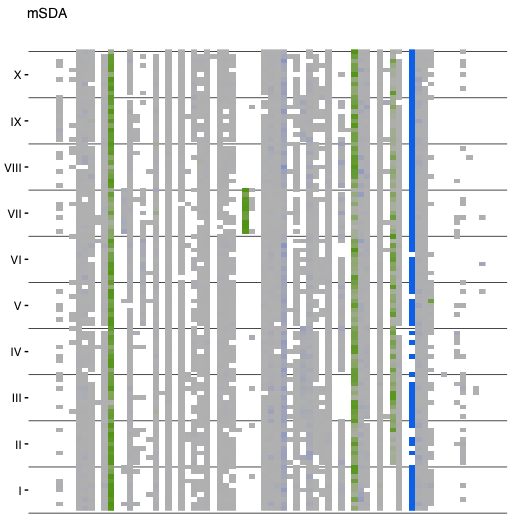

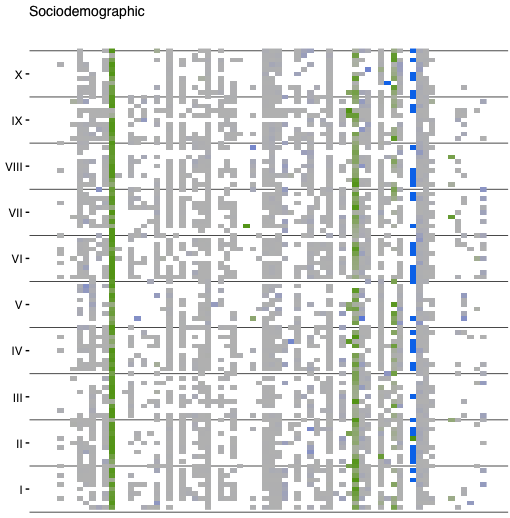

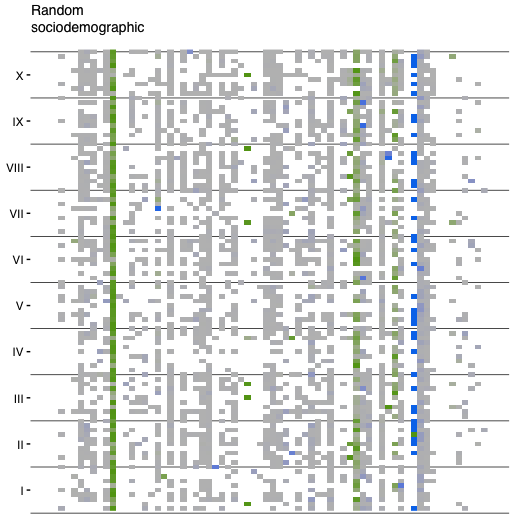

We proceed as in Section 6.1, using Hotels as target category. In addition to mSDAs and sociodemographic variables, here we also consider embeddings obtained by assigning a person to a random sociodemographic segment, e.g. by randomly changing their income or age ranges. We aim to extract different definitions of typical travelers according to different embeddings. To do so, in each embedding space we look at the 10 most central clients in each of the 10 densest clusters. The clients considered in different embedding spaces may differ. The proximity of a client to their cluster’s centroid represents the typicality of that client within the cluster, while cluster density is a measure of feature uniformity of the a cluster. Looking at different dense clusters, finally, prevents us from focusing exclusively on a single behavioral pattern or sociodemographic segment.

Figure 2 compares the transaction patterns of these typical clients. Each matrix corresponds to a different embedding. The Roman-numbered blocks of rows correspond to clusters, rows to clients and columns to transaction categories. Green dots correspond to incoming transactions (e.g. salary payments), while grey dots to outgoing ones. The blue column corresponds to expenses in the Hotels category.

The figure highlights how typical clients in the space of mSDA embeddings actually have very similar expense patterns (solid blocks of grey).

Furthermore, most of them have expenses in the Hotels category, confirming our initial hypothesis. Interestingly, even the clients not having an expense in Hotels roughly follow the grouping in clusters, being present mostly in clusters II and IV.

All this structural information is lost with the sociodemographic embedding, where the spending behavior appears fragmented and uncorrelated to the cluster structure. In fact, these patterns are virtually indistinguishable from those extracted with random sociodemographic segments. This suggests that sociodemographic variables capture close to no information about people’s spending habits.

6.3 Missing category prediction

Another measure of the effectiveness of a client embedding is being able to reconstruct whether a person had an expense in a target category. As some categories can be interpreted as families of products or services, e.g. Saving products, Bars and restaurants or Sports clubs, this use case can be seen as an approximation of product propensity prediction. In fact, it paves the way to the more commercially relevant experiment described in Section 6.4, in which we’ll look for clients that should have an expense in a category, but don’t.

6.3.1 Setup and evaluation

Here too we use a small dataset of 120K clients, splitting it in 100K customers as the training set, 10K as a validation set and 10K as the test set. We follow the notation of Section 6.1 and define

| (3) |

which indicates whether client has a transaction in the target category . To estimate it, we perform nearest neighbor regression in the embedding space. Call

| (4) |

where the neighbors are defined by a dot-product similarity in the space of the embedding . With this set we estimate

| (5) |

obtaining a preference score for the event that client had an expense in category . Drawing from the information retrieval methodology, we evaluate our predictions by average precision (AP) and precision at 100 (P@100), which for clarity we recall here. For a target category , we compute:

| (6) |

where the sum is taken over the set of all clients ordered by decreasing values of and is the precision computed on those clients with score higher than .

The P@100 is just the precision computed for the top-100 ranked predictions. The results discussed below are taken averaging the AP for 15 representative categories that bear commercial relevance for the bank or the client, e.g. Expense in groceries or Contributions to saving products.

6.3.2 Results

We evaluate results as in Section 6.1, but in the case of raw transactions and mSDA we look at both continuous and binarized transactions separately. Notice that in applications this preprocessing option would be optimized as a hyperparameter. We choose not to do this here to show that mSDAs are all but unaffected by such a relevant change, while the raw transactions embedding greatly benefits from it.

The results are presented in Table 2. Here mSDA embeddings still maintain an advantage over the alternatives, although to a lesser extent than in the segmentation use case. Here too, however, the improvement over sociodemographic variables is significant, being above 54 Notice also the poor performance of word2vec-based methods, which had offered much better results in Table 1. This is probably to be attributed to the lack of temporal information in our dataset and the coarseness of transaction categories, which make the concept of a local context of a word somewhat weak, if not ill-posed, as we remarked in Section 4. As a result, on tasks more complex than clustering, the performance of word2vec embeddings may be hindered.

Interestingly, the performance of the raw transactions embedding greatly benefits from the change from binary to continuous data while mSDAs seem to be left largely unaffected - in fact, their performance deteriorates a little. We conjecture that this may indicate that the autoencoder doesn’t need the information provided by the average transaction values when simply predicting whether an expense occurred, being the correlations among the variables in binary input data just as informative to that end. On the other hand, building exclusively on the transaction values, the raw transactions embedding is affected by the extreme coarseness of the binarized data.

| Method | AP | P@100 |

|---|---|---|

| Sociodemographic | 0.378 | 0.533 |

| Transactions (bin) | 0.324 | 0.466 |

| mSDA (bin) | 0.584 | 0.771 |

| Transactions (cont) | 0.558 | 0.704 |

| mSDA (cont) | 0.579 | 0.770 |

| word2vec + Avg | 0.269 | 0.359 |

| word2vec + VLAD | 0.274 | 0.380 |

6.4 Campaign targeting

In the experiments above we’ve seen how mSDAs achieved a consistently better performance in clustering and regression contexts, suggesting this is the first off-the-shelf embedding our colleagues should try from our library when starting to investigate a new mining task or commercial application. To reinforce this point, in this section we show how mSDA-based embeddings can be employed to create, with minimal effort, a commercially valuable method to retrieve sensitive targets for a commercial campaign. Application of non-trivial data-analytic methods for segmentation and targeting is not new, but effective methods like the one proposed in [19] usually entail a significant technical debt in development and maintenance, which becomes negligible with our library.

This experiment provides additional evidence that embeddings on transactional data have the potential to speed up data mining and analysis and even produce readily consumable solutions which can then be iterated upon, if needed.

6.4.1 Car and motorcycle insurance

One of the transaction categories we use in our data is that of a payment towards a car or motorcycle insurance, which creates a dataset of behaviors of the people who purchased that product (our positive samples). For this experiment we are using a richer dataset than the ones considered before, namely losing the category-wise aggregation in favour of movement-descriptor level data. Notice that this is a further simplification of the preprocessing we apply. We cast our search for similar clients as an IR problem [13, 26], and in particular we consider a randomly sampled set of seed positive clients, also referred to as query clients, who have a car insurance with BBVA, and a database of clients where only 7000 individuals also have the same car insurance.

We proceed precisely as in Section 6.3 by embedding via mSDA and then predicting using a set of nearest neighbors computed with dot-product similarity. The choice of is essentially business-dependent: the more neighbors we consider for each query, the more sensitive targets for our campaign we’re likely to retrieve. However, as it is to be expected, beyond a certain threshold for the precision of this method will start deteriorating. In fact, it can be reasonably argued that using a small will produce only a very restricted target set, given that the query customers supposedly share similar properties, hence they may also share their nearest neighbors - especially with a randomly sampled . In practice, that is certainly the case, but at the end of this section we will show that, in this instance, it is possible to achieve a satisfactory trade-off between diversity and precision.

Following Section 6.3, we evaluate the efficacy of our approach using the mean average precision at (MAP@), which we define below 666 is the same variable defining the number of neighbors.. We use the definition in (4), assuming here that is the mSDA embedding and that the neighborhood is computed within alone. We then define

| (7) |

where is the average precision defined in (6) computed on the set of neighbors of . The difference here is that we replace the indicator of (3) by the value , defined as follows. Given a subset of movement descriptors and a vector of a client’s transactions aggregated by movement descriptor,

defines the relevance (positivity) of . That is, is a true positive, hence relevant to the retrieval task, if it has a transaction for any of the movement descriptors in . The extension of the estimator in (5) as naturally follows. The APs are then averaged over the queries to compute the MAP@.

| Method | MAP@50 | @2E4 | @5E4 | @9E4 |

|---|---|---|---|---|

| mSDA + dot | 0.000 | 0.061 | 0.055 | 0.045 |

| Random | 0.000 | 0.024 | 0.023 | 0.023 |

We evaluate the MAP@ for various values of . The scores in Table 3

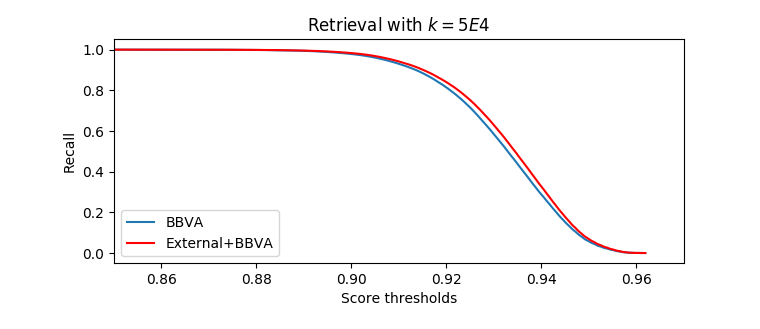

show that mSDA embeddings target customers more efficiently than random search, although the scores are nominally not far apart. We initially attributed this to the small fraction of relevant customers or to a weak correlation between insurance-related expenses and the other transactions. However, by looking at the blue recall curve of the retrieval problem with depicted in Figure 3, we realize that we are indeed retrieving a lot of relevant clients, thus indicating that we must be introducing many false positives.

Commercially, this is not an unwelcome outcome: we may be retrieving the real targets of an effective campaign, that is those customers that do have a car insurance, only with a different company. This information is not immediately evident from our data which doesn’t usually detail the insurance company or the kind of insurance (house, car, health etc.). Through some mining, however, we detected an exception to this rule by a descriptor specifying that some transactions referred to a car policy sold by a specific Spanish insurer, which allowed us to verify the positivity of some of those supposed false positives. This is equivalent to identifying a new set to define the positive labels (hence the relevance) of the database clients, consequently improving the MAPs as per Table 4.

| Method | MAP@50 | @2E4 | @5E4 | @9E4 |

|---|---|---|---|---|

| mSDA + dot | 0.289 | 0.108 | 0.072 | 0.054 |

| Random | 0.068 | 0.035 | 0.035 | 0.035 |

The red curve in Figure 3 is the recall for this new relevance criterion. Notice that the difference with the BBVA-only insurance recall is minimal. That is, the increase in MAP can be traced back to an increase in precision, but the recall graph suggests there may still be “false” positives we are mislabeling in our ground truth.

In order to spot them, we hypothesize the algorithm is retrieving all clients with car-related expenses, e.g. Highway toll, Automobile repair shops, Petrol, whom we thus label manually as positives. Customers with transactions in these categories are highly likely to own a car, which means they likely have a car insurance with a different company. The MAPs for this case are reported in Table 5, showing a substantial improvement on all values of .

| Method | MAP@50 | @2E4 | @5E4 | @9E4 |

|---|---|---|---|---|

| mSDA + dot | 0.897 | 0.776 | 0.670 | 0.536 |

| Random | 0.068 | 0.035 | 0.035 | 0.035 |

Finally, we conclude the section by arguing that restricting the retrieval to some of the values of which we have considered allows us to hit a sweetspot between diversity and precision. Call the number of distinct database clients retrieved for a certain and

| (8) |

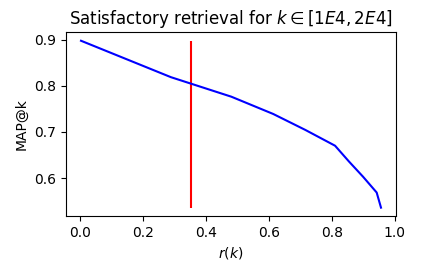

the fraction of distinct database clients retrieved when using neighbors. In Figure 4 we have plotted the values of the MAP@ against the corresponding and we have also highlighted the proportion of positive database clients. A high MAP at that , which is achieved for , indicates that both recall and precision are sufficiently high to be retrieving a large number of all the relevant clients.

This sweetspot of diversity and precison may not always be achievable, in which case it is advisable to step back and consider solutions like curating the query set or investigating whether the embedding is failing to capture the information we’d like it to leverage for our application (one may then resort to additional techniques like metric learning) or, like in the case described in this section, it is capturing way more than we initially expected. This latter point, in particular, demonstrates how client2vec can offer a quick and powerful starting point for data mining and advanced analytics, as well as off-the-shelf production-ready solutions.

7 Conclusions

We started the work which led to this study as an attempt to develop an internal tool that could catalyze the data-driven decision making for BBVA. We described how we worked towards a solution that was simple to use, fast to deploy and integrate in our colleagues’ processes and that required minimal preprocessing. Along the way, we learned that composing transactional embeddings extracted with word2vec into customer embeddings doesn’t always offer an acceptable performance, while mSDAs help us capture a good deal of behavioral information. Furthermore, we highlighted how this information can be extracted even from simple, coarse transactional data. We plan to keep expanding the client2vec library by adding new representations as new use cases arise, as well as by proactively exploring algorithms that fit its philosophy of simplicity, such as the nonlinear extension of mSDA proposed in [8] or metric learning to further boost the performance mSDA embeddings in client targeting. We also intend to start leveraging temporal information about the transactions of a client.

8 Acknowledgements

We would like to thank the whole team at BBVA D&A for guiding, inspiring and counseling us. Our thanks also go to the Smart Decision Making and Personal Finance Management teams at BBVA, whose products, data and business cases helped make this research possible.

References

- [1] O. Barkan and N. Koenigstein. Item2vec: Neural item embedding for collaborative filtering. In IEEE Workshop on MLSP. IEEE.

- [2] Y. Bengio, A. Courville, and P. Vincent. Representation learning: A review and new perspectives. IEEE Trans. PAMI, 2013.

- [3] Y. Bengio, R. Ducharme, P. Vincent, and C. Jauvin. A neural probabilistic language model. JMLR, 2003.

- [4] A. Benton, R. Arora, and M. Dredze. Learning multiview embeddings of twitter users. In ACL, 2016.

- [5] J. Bobadilla, F. Ortega, A. Hernando, and A. Gutiérrez. Recommender systems survey. Knowledge-based systems, 2013.

- [6] R. Boselli, M. Cesarini, F. Mercorio, and M. Mezzanzanica. An AI planning system for data cleaning. In ECML / PKDD, 2017.

- [7] Y.-L. Boureau, J. Ponce, and Y. LeCun. A theoretical analysis of feature pooling in visual recognition. In ICML, 2010.

- [8] M. Chen, K. Weinberger, F. Sha, and Y. Bengio. Marginalized denoising auto-encoders for nonlinear representations. In ICML, pages 1476–1484, 2014.

- [9] M. Chen, Z. Xu, K. Q. Weinberger, and F. Sha. Marginalized denoising autoencoders for domain adaptation. In ICML, 2012.

- [10] P. S. Dhillon, J. Rodu, D. P. Foster, and L. H. Ungar. Two step CCA: a new spectral method for estimating vector models of words. In ICML, 2012.

- [11] D. Duvenaud, J. R. Lloyd, R. Grosse, J. B. Tenenbaum, and Z. Ghahramani. Structure discovery in nonparametric regression through compositional kernel search. In ICML, 2013.

- [12] M. Filippone, F. Camastra, F. Masulli, and S. Rovetta. A survey of kernel and spectral methods for clustering. Pattern recognition, 2008.

- [13] W. B. Frakes and R. Baeza-Yates. Information retrieval: data structures and algorithms. Prentice Hall, 1992.

- [14] J. H. Friedman. Greedy function approximation: a gradient boosting machine. Annals of statistics, 2001.

- [15] R. Grosse, R. Salakhutdinov, W. Freeman, and J. Tenenbaum. Exploiting compositionality to explore a large space of model structures. In UAI, 2012.

- [16] I. Guyon, K. Bennett, G. Cawley, H. J. Escalante, S. Escalera, T. K. Ho, N. Macia, B. Ray, M. Saeed, A. Statnikov, et al. Design of the 2015 chalearn automl challenge. In IJCNN, 2015.

- [17] A. Halevy, P. Norvig, and F. Pereira. The unreasonable effectiveness of data. IEEE Intelligent Systems, 2009.

- [18] J. Hays and A. A. Efros. Im2gps: estimating geographic information from a single image. In CVPR, 2008.

- [19] N.-C. Hsieh and K.-C. Chu. Enhancing consumer behavior analysis by data mining techniques. International Journal of Information and Management Sciences, 2009.

- [20] T. Jaakkola and D. Haussler. Exploiting generative models in discriminative classifiers. In NIPS, 1999.

- [21] H. Jégou, M. Douze, C. Schmid, and P. Pérez. Aggregating local descriptors into a compact image representation. In CVPR, 2010.

- [22] J. M. Kanter and K. Veeramachaneni. Deep feature synthesis: Towards automating data science endeavors. In IEEE Int. Conf. on DSAA, 2015.

- [23] Q. Le and T. Mikolov. Distributed representations of sentences and documents. In ICML, 2014.

- [24] Z. C. Lipton, J. Berkowitz, and C. Elkan. A critical review of recurrent neural networks for sequence learning. arXiv preprint arXiv:1506.00019, 2015.

- [25] D. C. Liu, S. Rogers, R. Shiau, D. Kislyuk, K. C. Ma, Z. Zhong, J. Liu, and Y. Jing. Related pins at pinterest: The evolution of a real-world recommender system. In WWW, 2017.

- [26] T.-Y. Liu et al. Learning to rank for information retrieval. Foundations and Trends® in Information Retrieval, 2009.

- [27] J. R. Lloyd, D. Duvenaud, R. Grosse, J. B. Tenenbaum, and Z. Ghahramani. Automatic construction and Natural-Language description of nonparametric regression models. In AAAI, 2014.

- [28] T. Mikolov, I. Sutskever, K. Chen, G. S. Corrado, and J. Dean. Distributed representations of words and phrases and their compositionality. In NIPS, 2013.

- [29] J. A. Minarro-Giménez, O. Marin-Alonso, and M. Samwald. Exploring the application of deep learning techniques on medical text corpora. Studies in health technology and informatics, 2014.

- [30] R. Miotto, L. Li, B. A. Kidd, and J. T. Dudley. Deep patient: An unsupervised representation to predict the future of patients from the electronic health records. Scientific reports, 6, 2016.

- [31] N. Murray and F. Perronnin. Generalized max pooling. In CVPR, 2014.

- [32] J. Pennington, R. Socher, and C. Manning. Glove: Global vectors for word representation. In EMNLP, 2014.

- [33] F. Perronnin and C. Dance. Fisher kernels on visual vocabularies for image categorization. In CVPR, 2007.

- [34] V. Radosavljevic, M. Grbovic, N. Djuric, and N. Bhamidipati. Large-scale world cup 2014 outcome prediction based on tumblr posts. In KDD Workshop on Large-Scale Sports Analytics, 2014.

- [35] L. F. Ribeiro, P. H. Saverese, and D. R. Figueiredo. Struc2vec: Learning node representations from structural identity. In KDD, 2017.

- [36] J. A. Rodriguez-Serrano, D. Larlus, and Z. Dai. Data-driven detection of prominent objects. IEEE Trans. on PAMI.

- [37] J. Snoek, H. Larochelle, and R. P. Adams. Practical bayesian optimization of machine learning algorithms. In NIPS, 2012.

- [38] R. Socher, C. C. Lin, C. Manning, and A. Y. Ng. Parsing natural scenes and natural language with recursive neural networks. In ICML, 2011.

- [39] A. Torralba, R. Fergus, and W. T. Freeman. 80 million tiny images: A large data set for nonparametric object and scene recognition. IEEE Trans. PAMI, 2008.

- [40] P. Vincent, H. Larochelle, Y. Bengio, and P.-A. Manzagol. Extracting and composing robust features with denoising autoencoders. In ICML, 2008.

- [41] P. Vincent, H. Larochelle, I. Lajoie, Y. Bengio, and P.-A. Manzagol. Stacked denoising autoencoders: Learning useful representations in a deep network with a local denoising criterion. JMLR, 2010.

- [42] F. Zhuang, X. Cheng, P. Luo, S. J. Pan, and Q. He. Supervised representation learning: Transfer learning with deep autoencoders. In IJCAI, 2015.

- [43] F. Zhuang, X. Cheng, S. J. Pan, W. Yu, Q. He, and Z. Shi. Transfer learning with multiple sources via consensus regularized autoencoders. In ECML / PKDD, 2014.