Replica Approach for Minimal Investment Risk with Cost

Takashi Shinzato

shinzato@eng.tamagawa.ac.jp

Department of Management Science

Department of Management Science College of Engineering College of Engineering

Tamagawa University

Tamagawa University

Machida

Machida Tokyo Tokyo 1948610 1948610 Japan

(Received February 8, 2018; accepted *** 1, 2018)

Japan

(Received February 8, 2018; accepted *** 1, 2018)

Abstract

In the present work, the optimal portfolio minimizing the investment risk with cost is discussed analytically, where this objective function is constructed in terms of two negative aspects of investment, the risk and cost. We note the mathematical similarity between the Hamiltonian in the mean-variance model and the Hamiltonians in

the Hopfield model and the Sherrington–Kirkpatrick model and show that we can analyze this portfolio optimization problem by using replica analysis,

and derive the minimal investment risk with cost and the investment concentration of the optimal portfolio. Furthermore, we validate our proposed method through numerical simulations.

The portfolio optimization problem is one of the most actively researched topics

in mathematical finance, coming from the theory of diversification investment

management put forth by Markowitz in his pioneer works in 1952 and 1959 [1, 2].

In mathematical finance, (especially operations research),

investment optimality in some practical situations has been discussed

[3, 4, 5],

but only analysis of an annealed disordered system in the literature of spin glass has been discussed for the portfolio optimization problem, whereas analysis of the quenching system

which is desired by rational investors has been given little attention.

Recently, however,

such analysis of the quenched disordered system desired by rational investors

in the context of diversified investment

has started to be investigated using the analytical approaches developed in statistical mechanical informatics

and econophysics [6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23].

For instance, Ciliberti et al. examined

the investment risk of the absolute deviation model and

the expected shortfall model

in the portfolio optimization problem

with a budget constraint by using replica analysis.

Specifically, they analyzed

the typical behavior of the ground state in the limit of absolute zero temperature (the optimal solution of the portfolio optimization problem)

[6, 7].

Pafka et al.

compared

the eigenvalue distribution of the variance-covariance matrix derived from practical data

with

the eigenvalue distribution of the

variance-covariance matrix

defined by novel variables mapped by Cholesky decomposition and

discussed three types of investment risks in diversification investment

[8].

Kondor et al. evaluated

the relationship between noise and estimated error of each optimal portfolio with respect to several risk models:

the mean-variance model,

the absolute deviation model,

the expected shortfall model, and

the max-loss model [9].

Caccioli et al.

used replica analysis to determine whether the optimal solution of

the expected shortfall model with

ridge regression

is stable [10].

Furthermore,

Shinzato et al.

replaced the portfolio optimization problem including a budget constraint with an inference problem using the Boltzmann distribution

and derived analytically the trial distribution which can approximate the Boltzmann distribution based on the Kullback–Leibler information criterion using a belief propagation method.

They also derived the faster solver algorithm for the optimal solution

using the trial distribution [11].

As described above, various investment models have been examined using replica analysis and a belief propagation method

in these previous studies[12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23],

but in recent years, attention has been given to the mathematical similarity between

the Hopfield model and the most representative investment models, that is mean-variance model.

For instance,

Shinzato showed with the Chernoff inequality and replica analysis that the investment risk of the mean-variance model and the investment concentration of the

optimal

portfolio satisfy the self-averaging property

[12].

In addition, Shinzato analyzed the minimization problem of

investment risk with constraints of budget and

investment concentration by using replica analysis,

comparing the results with those of a previous work[12],

as well as analyzing the influence of the investment concentration constraint on the optimal portfolio[13].

Moreover, Shinzato

further investigated

the maximization problem of

investment concentration with constraints of budget and

investment risk in a previous work[13]

and the corresponding minimization problem as a counterpart, and

derived the mathematical structures of the two optimal portfolios of

the primal–dual optimization problems[14].

Further, Tada et al. resolved the

primal–dual optimization problems by using

Stieltjes transformation of

the asymptotical eigenvalue distribution of the Wishart matrix

in order to validate

the findings in previous works[13, 14]

where the analysis used replica analysis[15].

That is, they

reexamined

the minimization problem of investment risk with

constraints of budget and investment concentration (and the corresponding maximization problem)

and the maximization problem of

investment concentration with

constraints of budget and investment risk (and the corresponding minimization problem)

without using replica analysis or the replica symmetry ansatz.

In addition, Shinzato considered the minimization problem of investment risk with constraints of budget and expected return, and the maximization problem of expected return with constraints of budget and investment risk as a primal–dual optimization problem, analyzing

them by using replica analysis and reexamining the relationship between the two optimal portfolios[16].

Varga-Haszonits et al.

generalized

the minimization problem of investment risk

with

constraints of budget and expected return that was considered in the work by Shinzato[16]

and analyzed the stability

of the replica symmetry solution[17].

Shinzato examined the minimization problem of investment risk with constraints of budget and expected return by using replica analysis and derived a macroscopic theory like the Pythagorean theorem of the Sharpe ratio and opportunity loss

[18].

In addition,

Shinzato analyzed the minimization problem of investment risk with a budget constraint when the variance of the asset return is not unique using replica analysis and a belief propagation method and calculated the minimum investment risk per asset and the investment concentration of the optimal portfolio[19].

Furthermore,

using the asymptotic eigenvalue distribution of the Wishart matrix, Shinzato in a previous work[20]

reexamined

the minimization problem of investment risk per asset with

constraints of budget and investment concentration of the optimal portfolio handled in

the earlier work [19].

As a related case,

Shinzato examined the

minimization problem of

investment risk with a budget constraint

when

the return is characterized by a single-factor model

by using replica analysis and

succeeded in quantifying the influence of common factors included in the minimal investment risk

[21].

Moreover,

Shinzato examined the minimization problem of

investment risk with constraints of budget and

short-selling by using replica analysis when the asset

returns are independently and identically distributed, and

confirmed that the minimal investment risk per asset based

on the replica symmetric ansatz has a first-order phase transition[22].

Following Shinzato’s results, Kondor et al. examined the problem of the minimization of

a specific type of risk function with constraints of budget and short-selling

by using replica analysis for the case that each asset return is not necessarily distributed identically for all assets, and clarified that their minimal risk function has a first-order phase transition

[23].

As described above, at various investment opportunities, objective criteria (such as investment risk, purchase cost, expected return, and investment concentration) that rational investors hope to know have been examined using the approaches of a quenched disordered system (e.g., replica analysis and a belief propagation method).

However, it is also known that rational investors do not directly use only these objective criteria, but rather investment activities are carried out based on each investor’s utility function [24, 25].

Such a utility function is based on investment preferences (namely,

risk averse/risk neutral/risk loving) of each investor, and furthermore, the utility function involves a combination of investment risk, purchase cost, and expected return.

Among the previous cross-disciplinary research, few studies discussed the utility function, so it has been difficult to build a theory that appropriately supports investment decisions by rational investors.

Therefore,

in order to provide a seamless connection between

the analytical approach discussed in previous works[6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23]

and the analysis of utility functions, that is,

as a first step of an analysis of utility functions,

we examine the minimization problem of

a loss function defined by two objective criteria under a budget constraint

by using replica analysis.

In particular,

we assume

the utility function of the

rational investors whose hope is to reduce

two negative aspects of

investment, the investment risk (fluctuation risk of the held asset occurring during the investment period) and purchasing (or selling) cost (cost incurred in investing).

The remainder of the paper is organized as follow.

In the next section,

the portfolio optimization problem with a budget constraint

for minimizing the loss function defined by the investment risk and purchasing cost (which we refer to hereafter as the investment risk with cost) is formulated.

Section 3

demonstrates that

the computation complexity for

finding the optimal portfolio minimizing the

investment risk with cost

is increasing with the number of assets

by an analysis of this portfolio optimization problem with the Lagrange multiplier method,

and therefore that it is difficult to evaluate this problem in practical situations.

In section 4,

with the aim of avoiding this computational difficulty when using the Lagrange multiplier method,

we assess the minimal investment risk with cost per asset

and its investment concentration

by using replica analysis.

Further, we

compare the findings obtained by our proposed method with the minimal expected investment risk with cost

and its investment concentration derived from the analytical procedure in previous work.

In section 5,

the effectiveness of our proposed method is

verified by numerical simulations.

The final section is devoted to summarizing the present study and discussing future research.

2 Model Setting

In the present work,

we consider

the portfolio optimization

problem

with a budget constraint

in which one invests in assets at each of periods

in a stable investment market with no restrictions on short-selling

and show the properties of the optimal portfolio minimizing the

objective function defined by the two loss functions capturing the negative aspects of investment, investment risk and purchasing cost.

First,

the portfolio of asset is ,

and the portfolio of all assets is .

The notation indicates the transpose of a vector or matrix and, using the same setting as in previous works

[6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23]

, the budget constraint of the portfolio is defined as

(1)

In addition,

the return of asset

at period is represented by ,

and is independently distributed according to some distribution with mean and variance . Moreover,

purchasing cost per portfolio of asset at

the first period of investment is . Using this notation,

the investment risk and total purchasing cost are giving by

(2)

(3)

Since the first term of the first line in Eq. (2), , describes

the total return at period

and the second term represents its expectation, the investment risk is defined by

the sum of

the squared of differences between

the total return at each period, , and

the expected total return . Further, for the sake of simplicity,

here the modified return is used;

note that the mean

and the variance of the modified return are and , respectively.

Eq. (3)

represents the total purchasing cost.

Based on the above model setting, as the objective function,

using the cost tolerance , the investment risk plus the total purchasing cost at the first period of investment

is represented as (and is what we are calling the investment risk with cost), and is expressed as

(4)

where

the variance-covariance matrix (that is, the Wishart matrix) defined by the modified return ,

,

and cost vector

are

used in Eq. (4). Specifically,

the th component of Wishart matrix is .

Moreover, using return matrix

,

is also defined.

From the definition of the investment risk with cost in Eq. (4),

cost tolerance

is the tolerance degree of the investor with respect to the added cost.

One point should be noticed here.

The investment risk with cost discussed in this work, , is

regarded as the Hamiltonian in this investment system, which allows us

to apply

several analytical approaches developed

in spin glass theory

to analyze

the typical behaviors of the optimal portfolio of this portfolio optimization problem multidirectionally.

The reason for this is that, given

Ising spins

and extremal magnetic field

,

square symmetric matrix

represents Hebb’s law in the case of the Hopfield model and/or the RKKY interaction matrix in the case of the Sherrington-Kirkpatrick (SK) model.

The Hamiltonian of the Hopfield or SK model

is defined by

(5)

where the notation means the sum over all pairs satisfying .

Comparing

Eqs. (4)

and (5),

it is easily seen that they are mathematically similar with respect to these two models. Moreover,

Wishart matrix defined in Eq. (4)

is related to Hebb’s law in the Hopfield model and

the aim of both problems is to minimize the Hamiltonian. Therefore,

using replica analysis and belief propagation developed in

fields engaged in cross-disciplinary research such as spin glass theory and statistical mechanical informatics,

we can analyze the portfolio optimization problem and

derive several novel

insights for

diversification investment theory.

That is,

the optimal portfolio minimizing the

Hamiltonian constructed from RKKY interaction terms only (i.e., )

by using the analytical approach for a quenched disordered system

has been investigated in

previous works, where it has been shown that it is difficult to

analyze the quenched disordered system

(i.e., the rational investors can be regarded as in spin glass theory)

by using the analytical approach developed in operations research (i.e., the approach for an annealed disordered system).

[6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23].

As the natural extension of

previous works[12, 13, 14],

we here add terms of external magnetic fields to investment risk, that is,

the total cost,

in order to attempt to construct and

analyze a utility function

and thereby create a

macroscopic theory, which would enrich the theory of optimal investment risk.

Under the above assumptions, in the limit of a large number of assets ,

the minimal investment risk with cost per asset

is

(6)

where

the feasible subset of portfolio ,

and

the vector of ones

are used.

From a previous work[12],

this minimal investment risk with cost

satisfies the property

of self-averaging.

Moreover,

from the definition of

Eq. (6),

the minimal investment risk with cost is related to the analysis of a quenched disordered system.

On the other hand, from the literature of operations research,

the

minimal expected investment risk with cost per asset

is

(7)

where

is the configuration average of the function .

Equation

(7) shows that this description is related to

the analysis of an annealed disordered system.

Therefore,

the goal of the present work

is also to derive and examine the

optimal investment strategy of the portfolio optimization problem

with rational investors,

so we will discuss in Eq. (6) in detail, but not in Eq. (7).

3 Lagrange Multiplier Method

Here, given return matrix

and using the Lagrange multiplier method,

the minimal investment risk with cost per asset and

its investment concentration are analytically evaluated.

Lagrange function

for the minimization problem of the investment risk with cost in

Eq. (4), under the budget constraint in Eq. (1),

is defined by

(8)

where auxiliary variable is the

Lagrange multiplier variable with respect to

the budget constraint in Eq. (1).

The extremum of

satisfies

and ,

so the minimal investment risk with cost per asset is

(9)

Moreover, the investment concentration of

the optimal portfolio

is

(10)

In the evaluation of

the minimal investment risk with cost per asset

and

the investment concentration of the optimal portfolio ,

we

need to

assess

six moments,

,

,

,

and

,

,

, and also the inverse matrices and .

However, computing these inverse matrices accurately requires an computation.

Thus, we have the problem that

as the number of assets

becomes larger, of course, so does the

computation complexity.

As the number of assets is typically to ,

it is not easy to assess directly either

in Eq. (9)

or in Eq. (10).

In the following section, therefore, we avoid

the computation of the inverse of the Wishart matrix

and propose a method for effectively analyzing

the minimal investment risk with cost and

the investment concentration of the optimal solution.

4 Replica Analysis

Here, following previous works[6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23],

we consider

the minimal investment risk with cost per asset

and its investment concentration

in terms of replica analysis. First,

in Eq. (4)

is regarded as the Hamiltonian of this

investment system.

The partition function of

the investment market (at inverse temperature ),

, is defined by

(11)

where

is

the subspace of feasible

portfolios in Eq. (1).

Furthermore,

using this description of the partition,

from the identity function

(12)

it is known that

the typical behavior of the minimal investment risk with

cost per asset can be evaluated[23].

Similar to in this previous work,

in order to assess the

configuration average of the logarithm of the partition function

, we

need to analyze

the th moment at . That is,

is expanded, where

and are order parameters (with auxiliary parameters ). Then

the set of order parameters is

.

Moreover,

the notation

means

the extremum of with respect to , and

the period ratio is

and , as above.

Note that

the

order parameters here are defined by

(14)

(15)

In addition,

(16)

is used.

In the evaluation

of

Eq. (4),

as the

replica symmetry solution,

(19)

(22)

(25)

(28)

(29)

are set. From this,

using replica trick

,

(30)

is obtained, where the novel set of order parameters is used.

From these terms in the extremum, the order parameters are

(31)

(32)

(33)

(34)

(35)

(36)

(37)

(38)

(39)

where

(40)

(41)

(42)

(43)

From these and the identity in

Eq. (12), ,

the minimal investment risk with cost per asset is

(44)

Further,

Eq. (32) gives the extremal investment concentration .

In the next section, we will discuss numerical experiments conducted in order to

validate our proposed method. Before then, we should make some comments.

First, a previous work[19]

has already discussed the portfolio optimization problem

in the situation that cost when investing is ignored,

giving the minimal investment risk per asset and

its investment concentration as follows:

(45)

(46)

This corresponds to the case of our results.

Next, for the portfolio optimization problem which minimizes the purchasing cost

when ignoring investment risk, the purchasing cost is defined as

(47)

and the minimal cost per asset is

(48)

Then, from the relationship and

using Eq. (44), the minimal cost per asset is obtained as .

This result is supported by the fact that

there does not exist, for example, a minimum of the function of

with the two constraint conditions . These comments indicate that the findings obtained by the proposed method are

consistent with the well-known properties of the optimal solution of the portfolio optimization problem.

Lastly,

the minimal expected investment risk with cost

and its investment concentration

evaluated using the previous analytical procedure (the approach of an annealed disordered system) of operations research

are as follows:

(49)

As an interpretation of this finding,

since, for example, the function is

monotonically increasing in , compared with Eqs. (44)

and (49),

(51)

is obtained. That is, in the literature of

minimization of investment risk with cost,

it has been verified that the minimal investment risk with cost

does not correspond to the minimal expected investment risk with cost ;

and similarly,

the investment concentration of the optimal

is not equal to

the investment concentration of the solution derived in operations research

.

5 Numerical Experiments

In this section,

using numerical experiments,

a verification of the result based on replica analysis

in the preceding section is performed. First,

if the purchasing cost and the variance of return

do not depend on each other,

then the second term of in Eq. (44) and

in Eq. (41) reduce to

and

.

However, since this model setting is similar to that of a previous work[19],

in this paper, we consider the case that and are correlated.

Here,

we assume that

the mean of return , , is equal to

the purchasing cost , that is,

.

Moreover, we assume that

the second moment of return

is randomly proportional to

the square of mean , that is, .

In this setting, the variance of return is

. Note that

is the random coefficient and does not depend on .

For the concrete setting of the numerical experiments,

we assume that

are independently distributed with

the bounded Pareto distributions whose density functions are denoted by

(54)

(57)

where are the upper and lower bounds of

, and

are the powers characterizing the

bounded Pareto distributions.

We here

do not evaluate analytically

the inverse matrix in Eqs. (9) and (10) in order to

assess the optimal portfolio.

Instead, in the following steps, we derive the optimal portfolio numerically by using the steepest descent method

and assess the minimal investment risk with cost and its investment concentration .

Step 1. (Initial setting)

Assign and randomly according to the density function in Eq. (54), , and

that in Eq. (57), .

In particular, random variables

are independently and identically distributed according to

the uniform distribution on , so that

and

.

Step 2. (Initial setting)

For asset ,

the returns of assets are

independently and identically distributed with

and

.

Moreover, the modified return is

.

Thus,

the

return matrix

is assigned.

Step 3. (Initial setting)

Using the modified return in

Step 2,

(58)

Step 4. (Initial setting)

Set the initial portfolio

and

Lagrange coefficient as

and and the initial of cost tolerance

as .

Step 5. (Optimization)

Using the portfolio at iteration step ,

,

and Lagrange coefficient ,

update (the portfolio at iteration step )

and the Lagrange coefficient

(using the steepest descent method for in Eq. (8)) as follows:

(59)

(60)

where are the learning rates of the steepest descent method.

Step 6. (Optimization)

Compute the difference between and

,

(61)

Step 7. (Optimization)

If ,

then update and go back to Step 5. If ,

then, regarding and

as the approximations of the optimal

portfolio

and Lagrange coefficient , evaluate

the minimal investment risk with cost per asset

and its investment concentration

,

and go to Step 8.

Step 8. (Optimization)

If , then update

and go back to Step 5.

If , then stop the steepest descent algorithm.

Note that

we do not use either the replica symmetry ansatz and a calculation of an inverse matrix

in this algorithm. Moreover, using this steepest descent method algorithm times,

with respect to the return matrix assigned in the initial setting of the th trial,

, which is used to assess

the minimal investment risk with cost and its investment concentration

and

the sample averages of the minimal investment risk with cost per asset and

the investment concentration of the optimal portfolio are

(62)

(63)

where and are the results of th trial.

For the numerical simulations,

, and the parameters of the bounded

Pareto distribution are .

Further, defines the range of cost tolerance and its increment,

the learning rates of the steepest descent method are ,

and the constant of

the stopping condition is .

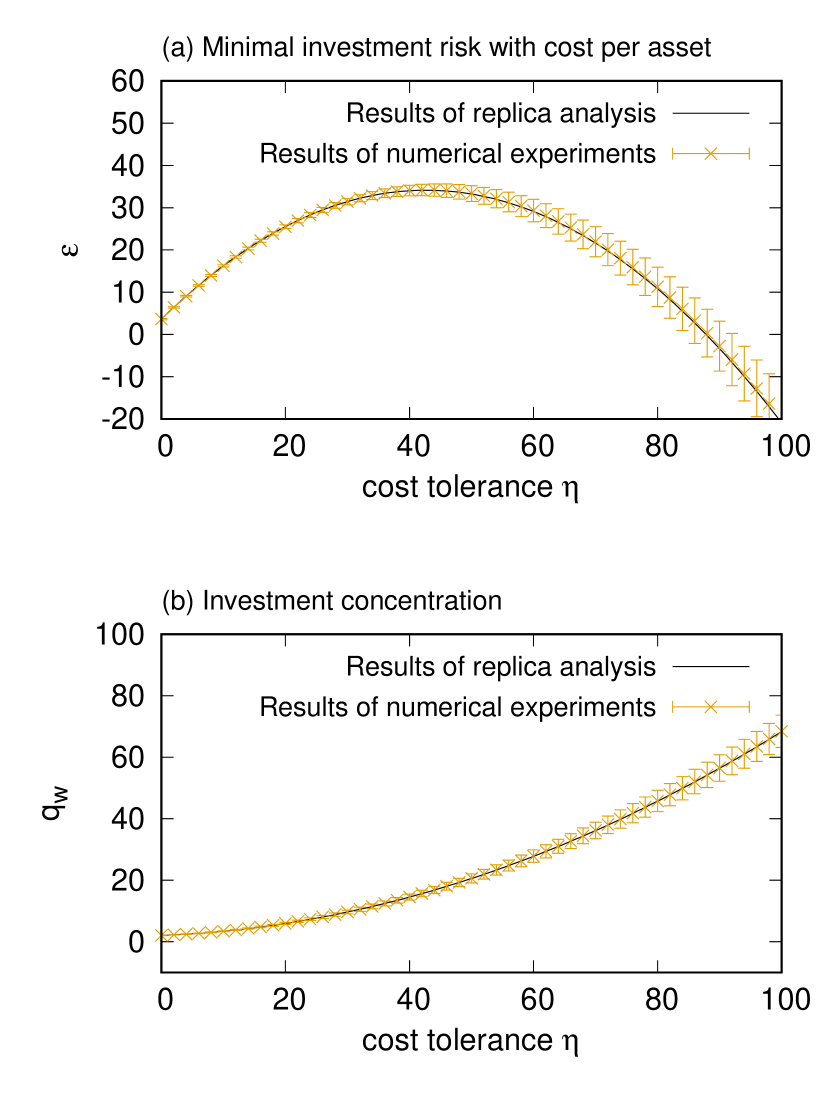

Finally, the total number of trials is . The

numerical results estimated by this steepest

descent method with these numerical settings (orange crosses with

error bars)

and those based on replica analysis (black solid lines)

are shown in Fig. 1.

As shown, the results derived by using replica analysis

and the numerical results

are consistent with each other, which verifies

the validity of our proposed method based on replica analysis.

In addition,

from Eqs. (51), (32), and (LABEL:eq42),

the analytical approach developed in operations research in previous works

is difficult to use to examine

the minimization problem of

the investment risk with cost under a budget constraint, that is,

it is disclosed that the analytical approach developed in operations research

cannot examine

the properties of the minimal investment risk with cost and

the investment concentration of the optimal portfolio.

Figure 1:

Results of the replica analysis and the numerical experiments ().

The horizontal axis indicates the cost tolerance , and the vertical axes show

(a) the minimal investment risk with cost per asset , and (b) the investment

concentration .

The black solid lines indicate the results of

the replica analysis for (a)

Eq. (44) and (b) Eq. (32). The orange crosses with

error bars indicate the results of the numerical simulations.

6 Conclusion

In this

work, we have investigated using replica analysis

the

minimization problem of the investment risk with cost which is

defined by two types of loss in investment, the risk and cost.

Concretely, based on mathematical similarity,

we regarded the investment risk with cost

as the Hamiltonian of this investment system, and further,

since

this system is mathematically analogous to

the Hamiltonians of the Hopfield model and the SK model,

we recognized that we could analyze the portfolio optimization problem using replica analysis.

Similar to in previous works[6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23],

we were able to

examine

the minimal investment risk with cost and the investment concentration of

the optimal portfolio minimizing

the investment risk with cost thoroughly based on the replica symmetry ansatz.

In addition,

we showed

that the minimal investment risk with cost

and its investment concentration which are evaluated by the

approach of a quenched disordered system

are in no way consistent with

the minimal expected investment risk with cost

and the investment concentration minimizing the expected investment risk with cost

which are evaluated by

the approach developed in operations research (that is, the approach of an annealed disordered system).

Using the results of numerical simulations,

we verified the validity of our proposed method based on replica analysis. Namely,

we showed that the properties of the minimal investment risk with cost

and its investment concentration,

which are not easily analyzed by the analytical approach

developed in operations research,

are revealed by the quenched disordered approach.

In this paper, we assumed that,

with respect to the cost per unit portfolio,

purchasing cost is equal to selling cost;

however, as

future research, we also need to considered the case that

purchasing cost (the cost on ) and

selling cost (the cost on ) are distinct.

For this purpose, as a generalization, we need to consider the portfolio optimization problem for the case that

the cost needs to be represents as a piecewise linear

or nonlinear function; for example, we can change in Eq. (3) to

.

Moreover,

in order to construct a macroscopic relation of the diversification investment theory,

we need to derive a relation

between the macroscopic variables like the Pythagorean theorem of the Sharpe ratio and

the relation of loss opportunity

[18, 19, 20]. Further,

so as to examine the properties of the utility function

of the optimal portfolio, we need to investigate

several performance indicators rather than merging risk and cost

(see appendix B).

Acknowledgements

The author is grateful for detailed discussions with

K. Kobayashi, H. Yamamoto, and D. Tada.

This work was supported in part by

Grants-in-Aid Nos. 15K20999, 17K01260, and 17K01249; Research Project of the Institute of Economic Research Foundation at Kyoto University; and Research Project

No. 4 of the Kampo Foundation.

Appendix A Moments

In this appendix,

using replica analysis,

we will calculate the six moments in the argument of Lagrange multiplier’s method,

,

,

,

,

, and

. First, the following partition is applied:

where . Further, we analyze

For this purpose, we define

(66)

Thus, and are given by

(67)

(68)

The second derivatives of and with respect to

allow the six moments to be analyzed exactly.

Moreover, in a similar way to that used in a previous work[16],

since the logarithm of the partition function maintains the property of self-averaging,

using replica analysis and the replica symmetric ansatz,

(69)

is assessed as follows.

From the extremum of the order parameters when ,

we analytically derive , and . Substituting these into Eq. (69),

(70)

and

(71)

where have already been substituted. From this,

we can evaluate the second derivatives of and with respect to

analytically as

(72)

(73)

(74)

(75)

Next,

using the result of Eq. (9) in the case of a finite number of assets ,

in the thermodynamical limit of , these should

maintain the self-averaging property,

so we substitute the results in Eqs. (72) to (74) into

(9),

(78)

which is consistent with the result based on replica analysis in

Eq. (44). Similarly, if the results

from Eqs. (72) to (LABEL:eq-a14) are substituted into

Eq. (10), then it is also verified that this result corresponds to that based on replica analysis in

Eq. (32).

Appendix B Investment risk with return and cost

Since the model handled in this paper

is mathematically analogous to both the Hopfield model and the SK model, we have focused on the minimization problem of the investment risk with cost.

Here, however, let us consider the minimization problem of

the investment risk with return, which has been widely investigated

in operations research. First, the expected return of the portfolio is

defined as follows:

(79)

where is the mean of return of asset , that is, . In

this setting, the investment risk with return is

(80)

where is the mixing degree of return. From this,

when

in the main manuscript is replaced by ,

the minimal investment risk with return

per asset is based on

Eq. (44). Then,

(81)

where

(82)

In addition, we can also consider the minimization problem of

the investment risk

with

both return and cost added, that is,

the investment risk

with return and cost, as follows:

(83)

Then the minimal investment risk with return and cost per asset

can be calculated as

where

in Eq. (4) is replaced by

. This shows that

we can analyze a utility function which comprises risk, return, and cost. Note that the utility function

depends on the preferences of each investor; that is,

the utility function is a subjective criterion based on each individual’s needs

of what the important factors are for the investor to decide to invest.

As individual terms in the utility function,

it is well known that the utility function

may include risk, return, and cost (that is,

the mixing degree of return and cost tolerance

differ between investors). As mentioned in the main manuscript, investment

theory should be deepened in order to meet the needs of each investor and

an optimal investment strategy should be proposed for the rational investor.

References

[1]

H. M. Markowitz: The Journal of Finance 7 (1952) 77.

[2]

H. M. Markowitz: Portfolio Selection: Efficient Diversification of

Investments (Yale University Press, 1959).

[3]

H. Konno and H. Yamazaki: Management Science 37 (1991) 519.

[4]

R. T. Rockafellar and S. Uryasev: Journal of Risk 2 (2000) 21.

[5]

A. F. Perold: Manage. Sci. 30 (1984) 1143.

[6]

S. Ciliberti and M. Mzard: The European Physical Journal B

57 (2007) 175.

[7]

S. Ciliberti, I. Kondor, and M. Mzard: Quantitative Finance

7 (2007) 389.

[8]

S. Pafka and I. Kondor: Physica A: Statistical Mechanics and its Applications

319 (2003) 487 .

[9]

I. Kondor, S. Pafka, and G. Nagy: Journal of Banking & Finance 31

(2007) 1545 .

[10]

F. Caccioli, S. Still, M. Marsili, and I. Kondor: The European Journal of

Finance 19 (2013) 554.

[11]

T. Shinzato and M. Yasuda: PLOS ONE 10 (2015) 1.

[12]

T. Shinzato: PLOS ONE 10 (2015) 1.

[13]

T. Shinzato: Journal of Statistical Mechanics: Theory and Experiment 2017 (2017) 023301.

[14]

T. Shinzato: Physica A: Statistical Mechanics and its Applications 490 (2018) 986 .

[15]

D. Tada, H. Yamamoto, and T. Shinzato: Journal of the Physical Society of Japan

86 (2017) 124804.

[16]

T. Shinzato: Phys. Rev. E 94 (2016) 052307.

[17]

I. Varga-Haszonits, F. Caccioli, and I. Kondor: Journal of Statistical

Mechanics: Theory and Experiment 2016 (2016) 123404.

[18]

T. Shinzato: ArXiv e-prints (2017).

[19]

T. Shinzato: Phys. Rev. E 94 (2016) 062102.

[20]

T. Shinzato: ArXiv e-prints (2016).

[21]

T. Shinzato: Journal of the Physical Society of Japan 86 (2017)

063802.

[22]

T. Shinzato: IEICE technical report 110 (2011) 23.

[23]

I. Kondor, G. Papp, and F. Caccioli: Journal of Statistical Mechanics: Theory

and Experiment 2017 (2017) 123402.

[24]

D. G. Luenberger: Investment Science (Oxford University Press, 1998).

[25]

Z. Bodie, A. Kane, and A. Marcus: Investments (The McGraw-Hill/Irwin

series in finance, insurance and real estate. McGraw-Hill Education, 2014),

The McGraw-Hill/Irwin series in finance, insurance and real estate.