∎

22email: kaercher@aices.rwth-aachen.de 33institutetext: Sébastien Boyaval 44institutetext: Laboratoire d’hydraulique Saint-Venant (Ecole des Ponts ParisTech – EDF R& D – CEREMA) Université Paris-Est, 6 quai Watier, 78401 Chatou Cedex, France and INRIA Paris (team Matherials)

44email: sebastien.boyaval@enpc.fr 55institutetext: Martin A. Grepl 66institutetext: Numerical Mathematics (IGPM), RWTH Aachen University, Templergraben 55, 52056 Aachen, Germany

66email: grepl@rwth-aachen.de 77institutetext: Karen Veroy 88institutetext: Aachen Institute for Advanced Study in Computational Engineering Science (AICES)

and Faculty of Civil Engineering, RWTH Aachen University, Schinkelstraße 2, 52062 Aachen

88email: veroy@aices.rwth-aachen.de

Reduced basis approximation and a posteriori error bounds for 4D-Var data assimilation††thanks: This work was supported by the Excellence Initiative of the German federal and state governments and the German Research Foundation through Grant GSC 111.

Abstract

We propose a certified reduced basis approach for the strong- and weak-constraint four-dimensional variational (4D-Var) data assimilation problem for a parametrized PDE model. While the standard strong-constraint 4D-Var approach uses the given observational data to estimate only the unknown initial condition of the model, the weak-constraint 4D-Var formulation additionally provides an estimate for the model error and thus can deal with imperfect models. Since the model error is a distributed function in both space and time, the 4D-Var formulation leads to a large-scale optimization problem for every given parameter instance of the PDE model. To solve the problem efficiently, various reduced order approaches have therefore been proposed in the recent past. Here, we employ the reduced basis method to generate reduced order approximations for the state, adjoint, initial condition, and model error. Our main contribution is the development of efficiently computable a posteriori upper bounds for the error of the reduced basis approximation with respect to the underlying high-dimensional 4D-Var problem. Numerical results are conducted to test the validity of our approach.

Keywords:

Variational data assimilation 4D-Var Strong-constraint 4D-Var Weak-constraint 4D-Var Reduced-order modelsReduced basis method A posteriori error estimation PDE-constrained optimization Parameter estimation1 Introduction

The goal of four-dimensional variational (4D-Var) data assimilation is to estimate unknown control variables of a dynamical system — classically the initial condition of the system — that provide the best fit of the system outputs with observation data over a specific time interval Courtier1997 ; DT1986 ; Lorenc1981 ; Lorenc1986 ; Sasaki1970 . The use of 4D-Var data assimilation is prevalent in oceanography Bennett1993 and meteorology Lynch2015 , where the dynamical system is described by partial differential equations (PDEs); see the recent texts LSZ2015 ; RC2015 and references therein for variational data assimilation in general.

We consider two variants of the 4D-Var problem. In the traditional strong-constraint 4D-Var formulation, the model is assumed to be “perfect” and only the initial conditions serve as the (unknown) control variable. The weak-constraint 4D-Var formulation additionally accounts for an imperfect model in the traditional formulation by introducing and finding a forcing term to account for the model error. In the weak-constraint case, the unknown initial condition and unknown model-error forcing term thus serve as control variables; for various weak-constraint formulations see e.g. Tremolet2006 .

The 4D-Var problem is usually cast as an optimization problem and has very close connections to optimal control theory VH2006 . A cost functional is introduced consisting of two terms in the classical strong-constraint formulation: the first term penalizes the misfit between the (unknown) initial condition and its prior background information and the second term penalizes the distance between the predicted system outputs and the observation data. In the weak-constraint case, another term is added which penalizes the model-error forcing. The optimal estimate of the initial condition is then found by minimizing the cost functional subject to the governing equations of the dynamical system, i.e., the PDE. After discretization of the PDE using classical techniques such as finite elements or volumes, the 4D-Var problem results in a large-scale optimization problem which is typically very expensive to solve due to the high-dimensional state and control variable spaces and the associated computation of the cost functional, gradient, and possibly Hessian. Note that in the discretized weak-constraint formulation, the model-error forcing is also assumed to be spatially distributed and thus has approximately the same dimension as the state and initial condition. To lower the tremendous computational cost for solving the problem, an incremental approach has been proposed in CTH1994 .

Another possibility to speed-up the solution process are reduced-order approaches which have been proposed successfully for the strong-constraint 4D-Var formulation in, for example, CZN+2007 ; DN2008 ; DAS2010 ; HK2006 ; RDB+2005 ; VH2006 . There are two kinds of 4D-Var reduced-order approaches in the literature: In the first approach HK2006 ; RDB+2005 ; VH2006 , a reduced basis space is introduced, e.g. using empirical orthogonal functions, only for the control variable (initial condition). By limiting the search space to the reduced space, the optimization cost per iteration decreases and the convergence improves (at least during the first few iterations). In the second approach CZN+2007 ; DN2008 ; DAS2010 , a reduced-order model for the system dynamics using proper orthogonal decomposition (POD) is additionally introduced. This leads to an additional speed-up and significant overall computational savings compared to reducing only the control space. All of these approaches also consider adapting the basis during the optimization. However, to the best of our knowledge, a posteriori error bounds to assess the sub-optimality of the reduced-order 4D-Var solutions have not yet been developed.

In this paper, we develop efficiently evaluable a posteriori error bounds for reduced order solutions of the strong- and weak-constraint 4D-Var data assimilation problem. We consider the standard quadratic 4D-Var cost functional constrained by parametrized linear parabolic PDEs involving noisy observations in time. Our final goal is not only to recover the “usual” 4D-Var control variables, i.e. the initial condition and model-error forcing, but also the model parameters. A preliminary improvement of the model itself before estimating the state can result in an improved state estimate, see e.g. the application in Habert2016 . We thus obtain a bilevel optimization problem where the outer optimization stage is performed over the model parameters after an inner optimization stage identical to the standard 4D-Var setting, i.e., an optimization over control variables for given fixed model parameters. In this paper, we focus mainly on the inner optimization stage and propose a posteriori error bounds for the control variable. Our main contributions are as follows:

-

•

In Section 3, we consider the strong-constraint 4D-Var formulation. We employ the reduced basis method to generate reduced order approximations for the solution of the parametrized 4D-Var problem, i.e., the state, adjoint, and control variables (i.e., the initial condition). We then propose an a posteriori error bound for the control variable that allows us to assess the error between the reduced-order 4D-Var solution and 4D-Var solution of the underlying high-dimensional FE approximation.

-

•

In Section 4, we extend the reduced basis approximation and a posteriori error estimation procedure from the strong- to the weak-constraint case. For simplicity of exposition, we consider the model-error forcing as the only unknown control variable in this section.

-

•

In Section 5, we combine the results from the two previous sections and consider problems with unknown initial condition and model-error forcing.

With the assumption of affine parameter dependence, the reduced-order 4D-Var problems and the a posteriori error bounds can be efficiently evaluated using an offline-online computational decomposition. Problems involving material parameters often naturally satisfy an affine parameter dependence, and even geometric parameters can often be treated after introducing suitable affine mappings onto a reference domain RHP2008 . Furthermore, the dimension reduction as well as the a posteriori error bound formulation presented in this paper still hold even for non-affine problems. However, for non-affine problems the computations can no longer be decomposed into offline-online stages, and the online computational efficiency thus suffers. To address this issue, the non-affine case can be treated using the Empirical Interpolation Method (EIM) which replaces the non-affine terms using an affine approximation and thus allows to regain the online-computational efficiency; we refer the interested reader e.g. to BMN+2004 ; GMN+2007 ; MNP+2007 .

We present numerical results for the strong- and weak-constraint setting in Section 6. We consider the dispersion of a pollutant governed by a convection-diffusion equation with a Taylor-Green vortex velocity field. Our goal is to recover the initial condition (in the strong-constraint case) or the model-error forcing (in the weak-constraint case) given noisy measurements of the pollutant concentration at five spatial locations over time.

We note that there is a close connection between the 4D-Var problem formulation and optimal control and that a posteriori error bounds for reduced order solutions to optimal control problems have been developed previously. However, rigorous and efficiently evaluable error bounds have been proposed mainly for elliptic problems KG2012 ; Kaercher2017 ; NRM+2012 , whereas error bounds for parabolic optimal control problems are either not rigorous Dede2010 or not (online-)efficient TV2009 . The only exception for parabolic problems is KG2014 , which only considers scalar time-dependent controls and is based on a pertubation argument, often resulting in a more conservative error bound Kaercher2017 .

Finally, we note that the reduced basis method has already been used in a parameterized-background data-weak approach to variational data assimilation in MPP+2015 ; MPP+2015a . However, this previous work considers the elliptic case and presents a relaxation of the 3D-Var setting, whereas we consider the time-dependent case using the classical 4D-Var formulation. Before introducing some preliminary definitions and assumptions in the following section, we do note that although we consider the 4D-Var problem here, our approach directly applies to the 3D-Var setting since the two are formally similar Lynch2015 .

2 Preliminaries

In this section, we introduce the necessary ingredients and definitions for the subsequent discussion. The 4D-Var problem is usually cast in a fully discrete setting; we thus directly consider a spatial finite element (FE) and temporal finite difference (FD) discretization using the weak variational formulation. We summarize the continuous formulation of the 4D-Var problem in Appendix A.

Let with be a Hilbert space of functions over the bounded Lipschitz domain , , with boundary . The inner product and induced norm associated with are given by and , respectively. We assume that the norm is equivalent to the -norm and denote the dual space of by . We also introduce the Hilbert space for the control, , together with its inner product , induced norm , and associated dual space . Furthermore, let be a prescribed -dimensional compact set in which our -tuple input parameter resides.

We divide the time interval with fixed final time into subintervals of equal length and define , and . We also introduce two conforming finite element approximation spaces and of typically large dimension and ; note that and shall inherit the inner product and norm from and , respectively. We shall assume that the spaces and the number of timesteps are large enough – i.e. and are sufficiently rich and the time-discretization sufficiently fine – such that the FE-FD approximation guarantees a desired accuracy over the whole parameter domain .

We next introduce the (for the sake of simplicity) parameter-independent bilinear forms for all and . We assume that is continuous, i.e.

| (1) |

We also introduce the parameter-dependent bilinear form , which we assume to be continuous, coercive,

| (2) |

and affinely parameter-dependent,

| (3) |

for some (preferably) small integer . Here, the coefficient functions are continuous and depend on , but the continuous bilinear forms do not depend on .

We also require the continuous linear functional and the continuous and linear (observation) operator , where is a suitable Hilbert space of observations with inner product and norm . Although a more general setting is possible, we consider here the observation space and the observation operator given by , where are linear output functionals. The continuity constant of the operator is given by

| (4) |

For the development of the a posteriori error bounds we assume that we have access to a positive lower bound for the coercivity constant defined in (2) such that

| (5) |

We note that is used in the a posteriori error bound formulation to replace the actual coercivity constants. Whereas the constants and are parameter-independent and can thus be computed once offline, we require that the coercivity lower can be efficiently evaluated online, i.e., the computational cost is independent of the FE dimension . Various recipes exist to obtain such bounds HRS+2007 ; RHP2008 .

3 Strong-constraint 4D-Var

In this section, we consider the strong-constraint 4D-Var data assimilation problem. The extension to the weak-constraint case is considered in Section 4.

3.1 Problem statement

For a given parameter , the classical 4D-Var problem can be stated as the minimization problem

| (6) |

with initial condition for all and cost functional given by

| (7) |

Here, is the background state (also referred to as the prior), i.e., the best estimate of the true initial condition prior to measurements being available, and , , is the given data, e.g., observed outputs. The first term in the cost functional penalizes the deviation of the initial condition from the background state, the second term penalizes the deviation of the predicted outputs from the given data/observed outputs. The relative weight of both terms is affected by the choice of the and inner products. Note that we use for the unknown control/initial condition to signify the similarity to optimal control and the notation to indicate the implicit dependence of the cost functional on the parameter through the state . However, to simplify the notation we often do not explicitly state the dependence of the state and control on the parameter, i.e., we use and instead of and , respectively.

We would like to point out that the first term in (7) represents a Tichonov regularization of the cost functional and that the regularization parameter is “hidden” in the choice of the inner product. We refer to Engl1996 for regularization of inverse problems in general and to Puel2009 for Tichonov regularization in data assimilation. Furthermore, we note that the choice of the norm for the data misfit term depends on the characteristics of the noise and is inspired by Gaussian noise in this paper. Different noise characteristics may require a different choice of norm; we refer e.g. to Rao2017 for a discussion using and Huber norms instead of the norm. The approach presented in the following is restricted to the case of Gaussian noise.

Employing a Lagrangian approach, we obtain the associated necessary, and in our setting sufficient, first-order optimality conditions: Given , the optimal solution satisfies

| (8a) | |||||

| (8b) | |||||

| (8c) | |||||

| (8d) | |||||

where the final condition of the adjoint is given by . Concerning the existence and uniqueness of the 4D-Var problem specifically and of saddle point problems in general we refer to Broecker2017 and BGL2005a .

3.1.1 Algebraic Formulation

The 4D-Var problem is usually stated using an algebraic formulation Ide1997 . We thus briefly outline the algebraic equivalent of (LABEL:fe_strong) by introducing a basis for the finite element spaces and such that and , respectively. We express the state, adjoint, and control, respectively, as

and denote the corresponding coefficient vectors by , , and We thus obtain the algebraic formulation of the classical 4D-Var minimization problem

| (9) |

Here, , , , and are the usual finite element mass matrix, stiffness matrix, load vector, and state-to-output matrix with entries , , , and , respectively. The matrix is given by . Furthermore, the matrices with entries and with entries can be identified as the inverses of the background and observation error covariance matrices, respectively. Here, denotes the th unit vector in .

The derivation and algebraic formulation of the optimality system (8) is standard and thus omitted for brevity. Further, in our problem setting the first-discretize-then-optimize and first-optimize-then-discretize strategies lead to the same algebraic formulation of the first-order optimality system. For more details on these two approaches, we refer to HPU+2009 and for time-dependent problems specifically to SW2013 .

3.2 Reduced basis approximation

We first assume that we are given the reduced basis spaces for the state and adjoint, and for the control. Here, is the number of iterations of the POD-Greedy sampling procedure to construct the spaces and discussed in Section 4.4. Note that the dimensions and of the reduced basis spaces depend on but are in general not equal to . Furthermore, the basis functions of and are orthogonalized with respect to the and inner product, respectively.

We next replace the finite element approximation of the PDE constraint in the 4D-Var problem statement (LABEL:fe_strong) with its reduced basis approximation. For a given parameter , the reduced-order 4D-Var data assimilation problem can thus be stated as

| (10) |

with initial condition for all .

We can again employ a Lagrangian approach to obtain the reduced-order optimality system: Given any , the optimal solution satisfies

| (11a) | |||||

| (11b) | |||||

| (11c) | |||||

| (11d) | |||||

where the final condition of the adjoint is given by . The reduced-order optimality system can be solved efficiently using an offline-online computational procedure which is briefly discussed in Section 3.4.

Note that we use a single reduced basis ansatz and test space for the state and adjoint equations for two reasons: first, a single space for state and adjoint guarantees the stability of the reduced-order optimality system GV2011a ; and second, the reduced-order optimality system (11) reflects the reduced-order 4D-Var problem (LABEL:rb_strong) only if the spaces of the state and adjoint equations are identical. Since the state and adjoint solutions need to be well-approximated using the single space , we combine both snapshots of the state and adjoint equations into the reduced basis space .

We also note that the dynamics of the state and adjoint are often different, and thus separate spaces for the state and adjoint would be beneficial concerning the computational efficiency, i.e. the dimension of the state/adjoint reduced basis space and thus the overall dimension of the reduced-order optimality system would be considerably smaller. However, this requires a Petrov-Galerkin projection for the state and adjoint with associated detriment concerning the stability.

3.3 A posteriori error estimation

We turn to the a posteriori error estimation procedure. Although we consider a parametrized problem here, we note that the error bounds proposed below can also be used in the non-parametrized reduced-order setting and are independent of how the reduced-order spaces are constructed, i.e., the bound directly applies to reduced-order approaches where the spaces are constructed e.g. using empirical orthogonal functions, POD, or dual-weighted POD DN2008 .

As mentioned above, our main goal is to rigorously bound the error in the optimal control, . This will allow us to confirm the fidelity of the reduced-order 4D-Var solution efficiently during the online stage. Our a posteriori error bounds are also crucial in the construction of the reduced basis spaces by the POD-Greedy algorithm (see Section 3.5).

To begin, we require the residuals

| (12) | ||||

| (13) | ||||

| (14) |

We also define

| (15) |

and the errors , , and . Note that we use and as a shorthand notation for and , respectively. We can now state our main result:

Proposition 1

Let and be the optimal solutions of the full-order and reduced-order 4D-Var problems, (LABEL:fe_strong) and (LABEL:rb_strong), respectively. The error satisfies

| (16) |

where and are given by

| (17) | ||||

| (18) |

Proof

We start from the error-residual equations obtained from (8) and the definitions of the residuals

| (19) | ||||

| (20) | ||||

| (21) |

where and . We first choose in (19) and take the sum from to to get

| (22) |

Similarly, choosing in (20) and summing from to we obtain

| (23) |

Finally, from (21) with we have

| (24) |

By adding equations (23) and (24), and then subtracting (22) we get

| (25) |

Since , and , the left-hand side of (25) reduces to and we thus obtain

| (26) |

From the proof for the spatio-temporal energy norm bound in GP2005 ; KG2014 we know that

| (27) |

We need an analogous result for the adjoint. To this end, we first choose in (20) to obtain

| (28) |

We next note from the Cauchy-Schwarz inequality and Young’s inequality that

| (29) |

and also that

| (30) |

where we also used the definition of the constant . Finally, again from Young’s inequality we obtain

| (31) |

By summing two times (28) from to and invoking (29), (30), and (31), we obtain

| (32) |

and hence

| (33) |

Using the inequalities (27) and (33) in (26), invoking the definitions (15), and noting that , it follows that

| (34) |

We now use Young’s inequality to bound

| (35) |

and thereby eliminate the second term on the left-hand side of the inequality (34) to obtain

| (36) |

Using the definitions of and in (17) and (18), respectively, (36) simplifies to

| (37) |

We obtain the desired result by bounding the error by the larger root of the quadratic inequality.

3.4 Computational Procedure

We briefly comment on the computational procedure to solve the reduced-order 4D-Var problem and to evaluate the error bound. Given the affine parameter dependence, the offline-online decomposition for the reduced basis approximation is already quite standard in the reduced basis literature RHP2008 ; for the parabolic case considered in this paper, we also specifically refer to GP2005 ; KG2014 . The evaluation of the a posteriori error bounds requires the following ingredients:

-

•

the dual norm of the residuals , , and ;

-

•

the coercivity lower bound and the constant .

For the construction of the coercivity lower bound, , various recipes exist HRS+2007 ; PRV+2002 ; VRP2002 . The specific choices for our numerical tests are stated in Section 6. The constant is parameter-independent and can be computed by solving a generalized eigenproblem. The offline-online evaluation of the dual norms of the residuals is standard and hence omitted RHP2008 . For a summary of the computational cost in the parabolic optimal control context, we refer to KG2014 .

We solve the full-order and reduced-order 4D-Var problems with a preconditioned Newton-CG method on the “reduced” cost functional , i.e., we eliminate the PDE-constraint in the minimization problem. The control mass matrix is used as a preconditioner. We present results for the number of CG iterations in Section 6. Overall, the online computational cost to solve the reduced-order 4D-Var problem and to evaluate the a posteriori error bound depends only on the reduced basis dimensions and , but is independent of .

3.5 Greedy Algorithm

To construct the reduced basis spaces and , we use the POD-Greedy sampling procedure in Algorithm 1. Here, is a finite but suitably large training sample, is the initial parameter value, the maximum number of greedy iterations, and a prescribed error tolerance. We also define the relative error bound . Furthermore, for a given time history , the operator returns the largest POD-mode with respect to the inner product (normalized with respect to the -norm), and denotes the -orthogonal projection of onto the reduced basis space .

In steps 6 and 7 of Algorithm 1 we expand the reduced basis space with the largest POD mode of both the state and the adjoint solution. Note that we apply the POD in these two steps to the time history of the optimal state and adjoint projection errors, i.e., and , and not to the solutions , and , itself.111For the first iteration of the algorithm we define , and hence and . This ensures that the POD modes are already orthogonal with respect to the inner product and that we add only new information to which is not yet captured in the reduced basis.

In step 8 we expand the reduced basis space with the optimal control at . Due to the time-dependence of the state and adjoint, it is possible that a specific parameter is picked several times by the greedy search in step 9. Before expanding , we thus need to check if the new snapshot is already contained in the reduced basis space , and consequently discard linearly dependent snapshots. By construction, we thus have and (although it is theoretically possible that , we did not observe this case in the numerical results). Finally, we note that information from the data assimilation cost functional enters through the adjoint equation and the adjoint snapshots into .

4 Weak-constraint 4D-Var

We next consider the weak-constraint 4D-Var data assimilation problem, thus accounting for possible model errors in the dynamical system. For simplicity, we assume in this section that the initial condition is known and that we are only interested in bounding the model error. We consider the combined problem (unknown initial condition and model error) in the next section.

4.1 Problem statement

To emphasize the relation between the weak-constraint 4D-Var problem and the optimal control setting, we denote in this section the model error by . However, the model error is now time-dependent, i.e., , and appears in every time step of the dynamical system. For a given parameter , the weak-constraint 4D-Var problem is then given by the minimization problem

| (38) |

with initial condition for all and cost functional given by

| (39) |

We note that the cost functional now contains the contribution of the model error as a sum over all time steps. In the optimal control setting, denotes the desired optimal control. In the data assimilation setting, however, is usually set to zero since the model error is generally assumed to be unbiased LSZ2015 . We also note that a constant (known) bias can be taken into account by adjusting the right-hand side . Similar to the strong-constraint formulation, , , are the observed outputs.

We again obtain the associated necessary and sufficient first-order optimality conditions using a Lagrangian approach: Given , the optimal solution satisfies

| (40a) | |||||

| (40b) | |||||

| (40c) | |||||

| (40d) | |||||

where the final condition of the adjoint is given by . We note that the adjoint equation of the weak-constraint formulation (40c) is identical to the adjoint of the strong constraint formulation (8c).

4.2 Reduced basis approximation

We again assume that we are given the reduced basis spaces for the state and adjoint and for the control. Whereas the construction of the space directly follows from the discussion in Section 3.5 for the strong-constraint case, the construction of needs to be adjusted to account for the time-dependence of the model error. We briefly outline the procedure in Section 4.4.

For a given parameter , we can now state the weak-constraint reduced-order 4D-Var data assimilation problem as follows

| (41) |

with initial condition for all . The reduced-order optimality system directly follows from (40) and is thus omitted.

4.3 A posteriori error estimation

We first introduce the residuals for the weak-constraint case

| (42) | ||||

| (43) | ||||

| (44) |

Since the adjoint equations (40c) and (8c) are identical, the adjoint residual is actually equivalent to the strong-constraint case, i.e., . Similar to (15), we introduce the sums from to of the dual norms of the residuals as

| (45) |

and the time-dependent model error . We may now state our main result:

Proposition 2

Let and , , be the optimal solutions of the full-order and reduced-order 4D-Var problems (LABEL:fe_weak) and (LABEL:rb_weak), respectively. The error satisfies

| (46) |

where and are given by

| (47) | ||||

| (48) |

Proof

The proof follows partly from the proof of Proposition 1; we thus stress the differences and refer to the previous proof whenever possible. We again start from the error-residual equations which are now given by

| , | (49) | ||||

| (50) | |||||

| (51) | |||||

where and , since we guarantee that . We now choose in (49), in (50), and in (21), sum all equations from from to and combine them following the proof of Proposition 1 to obtain

| (52) |

We next bound the primal error. Since the primal equation contains the model error on the right-hand side, we need to extend the proof from GP2005 for the spatio-temporal energy norm bound to include the extra term on the right-hand side. The derivation is similar to the one for the bound of the adjoint in the proof of Proposition 1 (cf. (28) – (33)), but instead of bounding the inner product using Cauchy-Schwarz and the constant , we invoke the continuity of the bilinear form . We can thus derive the bound

| (53) |

Furthermore, since the adjoint of the strong- and weak-constraint case are equivalent, we can directly use the bound (33). Using the inequalities (53) and (33) in (52), invoking the definitions (45), and noting that , it follows that

| (54) |

We again use Young’s inequality to bound

| (55) |

and thereby eliminate the second term on the left-hand side of (54) to obtain

| (56) |

Using the definitions of and in (47) and (48), respectively, we obtain

| (57) |

The desired result follows again by using the larger root of the quadratic inequality as a bound for the error.

The offline-online computational procedure in the weak-constraint case is analogous to the strong-constraint case discussed in Section 3.4 and therefore omitted. Note that we additionally require the constant now, which is parameter-independent and can be computed by solving a generalized eigenproblem (similar to ). For the Newton-CG method, we use the block-diagonal matrix as a preconditioner.

4.4 Greedy Algorithm

The POD-Greedy sampling procedure to construct the reduced basis spaces and in the weak-constraint case is very similar to the strong-constraint case. We summarize the procedure in Algorithm 2 and only comment on the differences.

First, since we assume in this section that the initial condition is known, we initialize the reduced basis space with . Second, we additionally require the operator , which returns the largest POD mode with respect to the inner product (and normalized with respect to the -norm). Also, denotes the -orthogonal projection of onto the reduced basis space and denotes the time history of the optimal model-error forcing. Since the model-error forcing is time-dependent, we simply replace step 8 in Algorithm 1 with a POD-step and add only the largest POD mode to . We note that the POD modes are orthogonal with respect to the inner product and that we now usually have and (due to the initial condition), i.e., the reduced basis space is enriched in every greedy step. Again, it is theoretically possible that and , although we did not observe this case in the numerical results.

5 Combined 4D-Var formulation

We now combine the results from the previous two sections and consider the classical 4D-Var data assimilation problem including model error.

5.1 Problem statement

For a given parameter , we now consider the minimization problem

| (58) |

with initial condition for all and cost functional given by

| (59) |

In addition to the error between the predicted and observed outputs, the cost functional now contains the deviation of the initial condition from the background state, as well as the model error for all time steps. As mentioned earlier, in the data assimilation context we usually have and , i.e. the background state is nonzero whereas the model error is assumed to have zero mean.

The associated necessary and sufficient first-order optimality conditions are thus: Given , the optimal solution satisfies

| (60a) | |||||

| (60b) | |||||

| (60c) | |||||

| (60d) | |||||

| (60e) | |||||

where the final condition of the adjoint is given by .

5.2 Reduced basis approximation and error estimation

The reduced-order problem follows directly from (LABEL:fe_comb) and (59) by restricting the state, adjoint, and control spaces to their respective reduced basis spaces. We again introduce an integrated space for the state and adjoint, and two separate spaces for the “control,” i.e., for the initial condition and for the model error . The greedy procedure to generate these spaces simply combines the algorithms introduced in Sections 3.5 and 4.4.

For any given , we can now state the reduced-order minimization problem as follows

| (61) |

with initial condition for all . The reduced-order optimality system directly follows from (60) and is thus omitted.

The a posteriori error bound result is a combination of the strong- and weak-constraint case. In addition to the residuals of the state , adjoint , and model error defined in (42), (43), and (44), we also require the residual

| (62) |

The a posteriori error bound is given in the following proposition.

Proposition 3

Let and be the optimal solutions of the full-order and reduced-order 4D-Var problems (LABEL:fe_comb) and (LABEL:rb_comb), respectively. The error satisfies

| (63) |

where and are given by

| (64) |

and

| (65) |

6 Numerical results

6.1 Problem description

We consider the dispersion of a pollutant governed by a convection-diffusion equation with a Taylor-Green vortex velocity field. The concentration of the pollutant is measured at five spatial locations over time. The computational domain is and we assume homogeneous Dirichlet boundary conditions on the lower boundary and homogeneous Neumann boundary conditions on the remaining boundary . The Péclet number serves as our parameter, i.e., we have . The bilinear form is thus given by

| (66) |

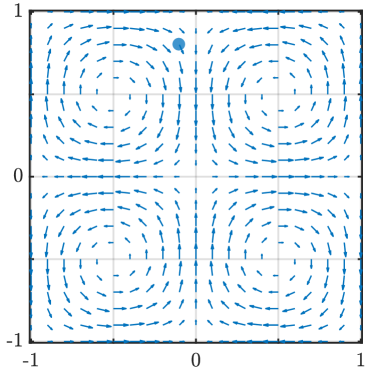

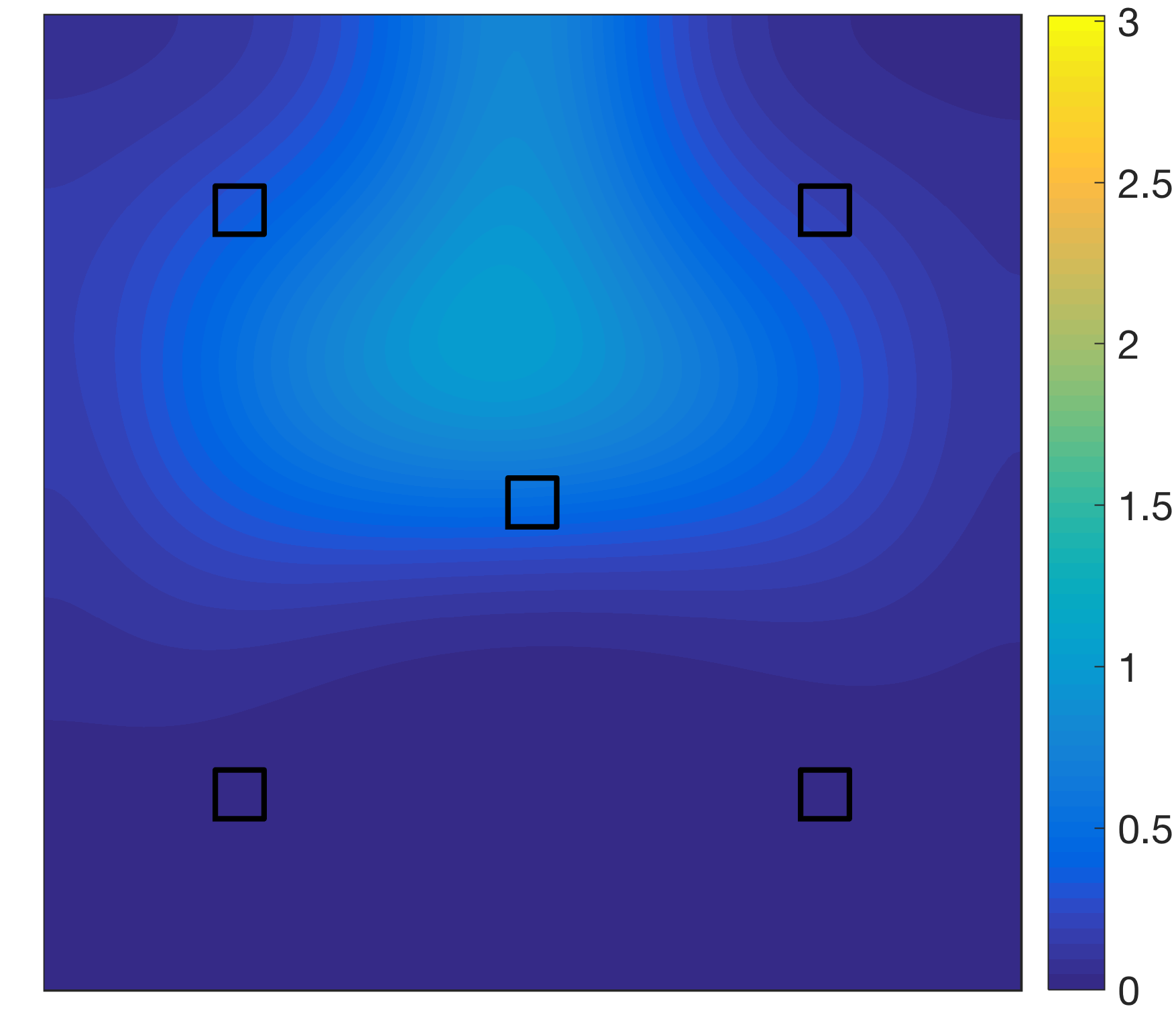

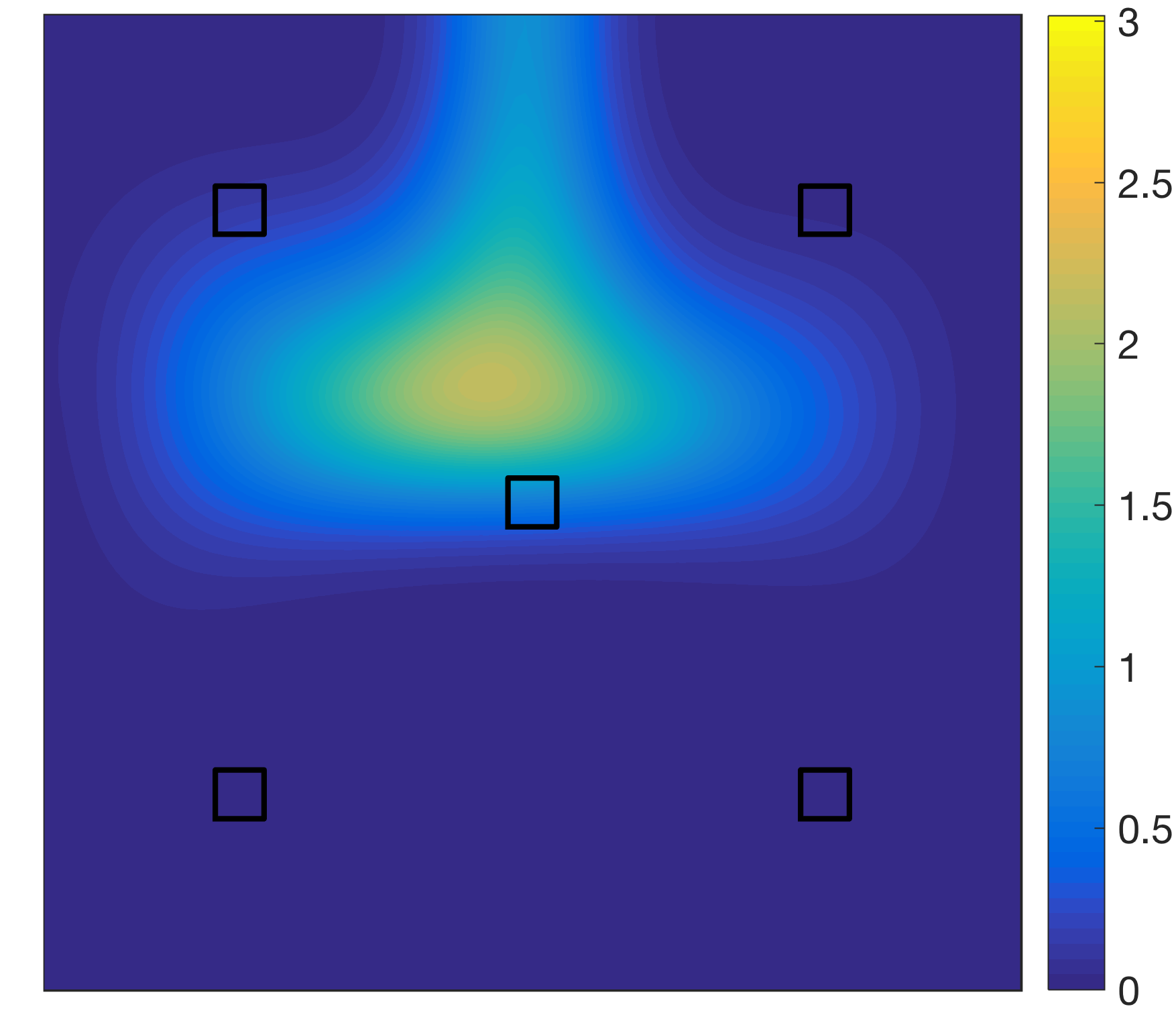

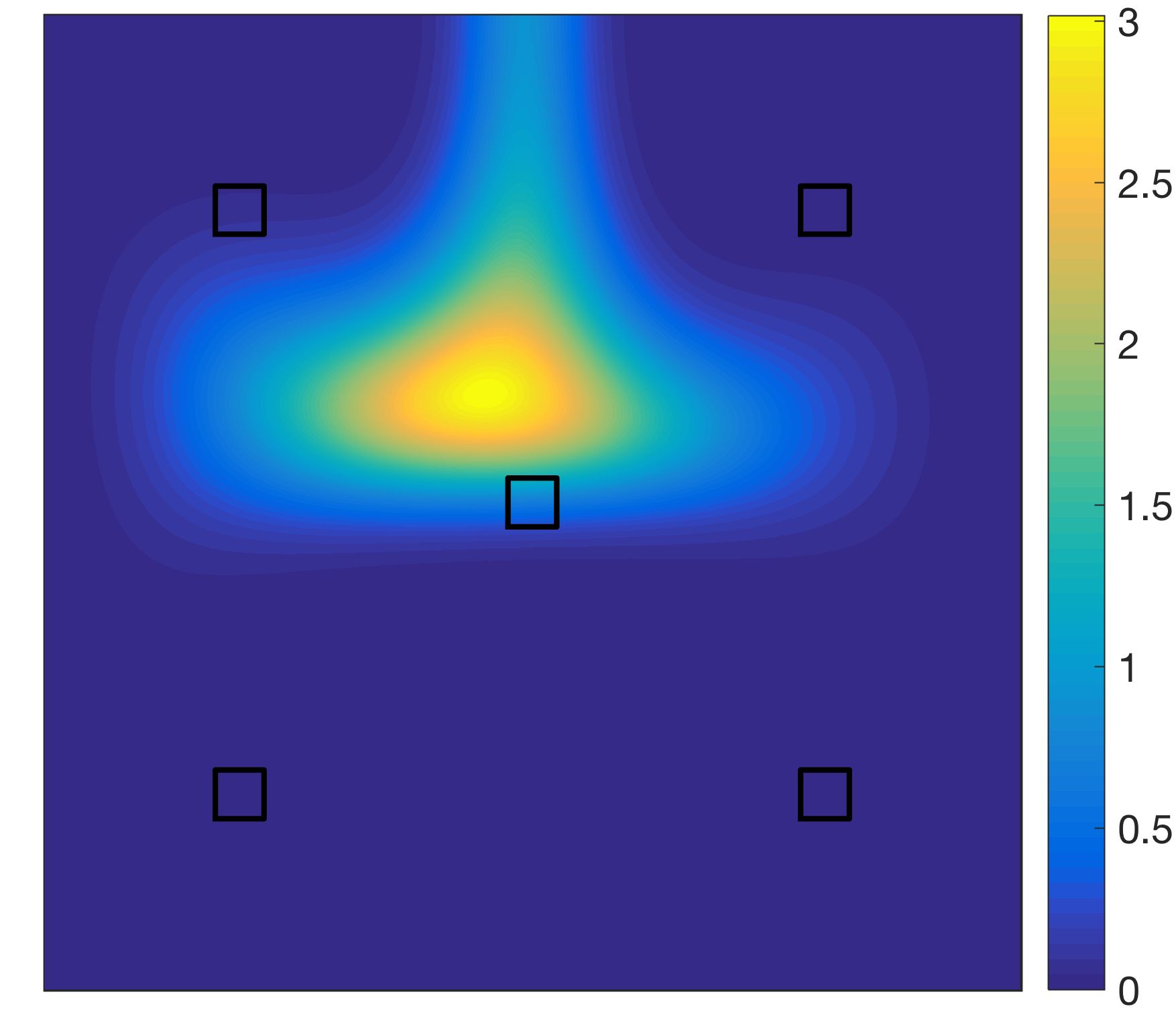

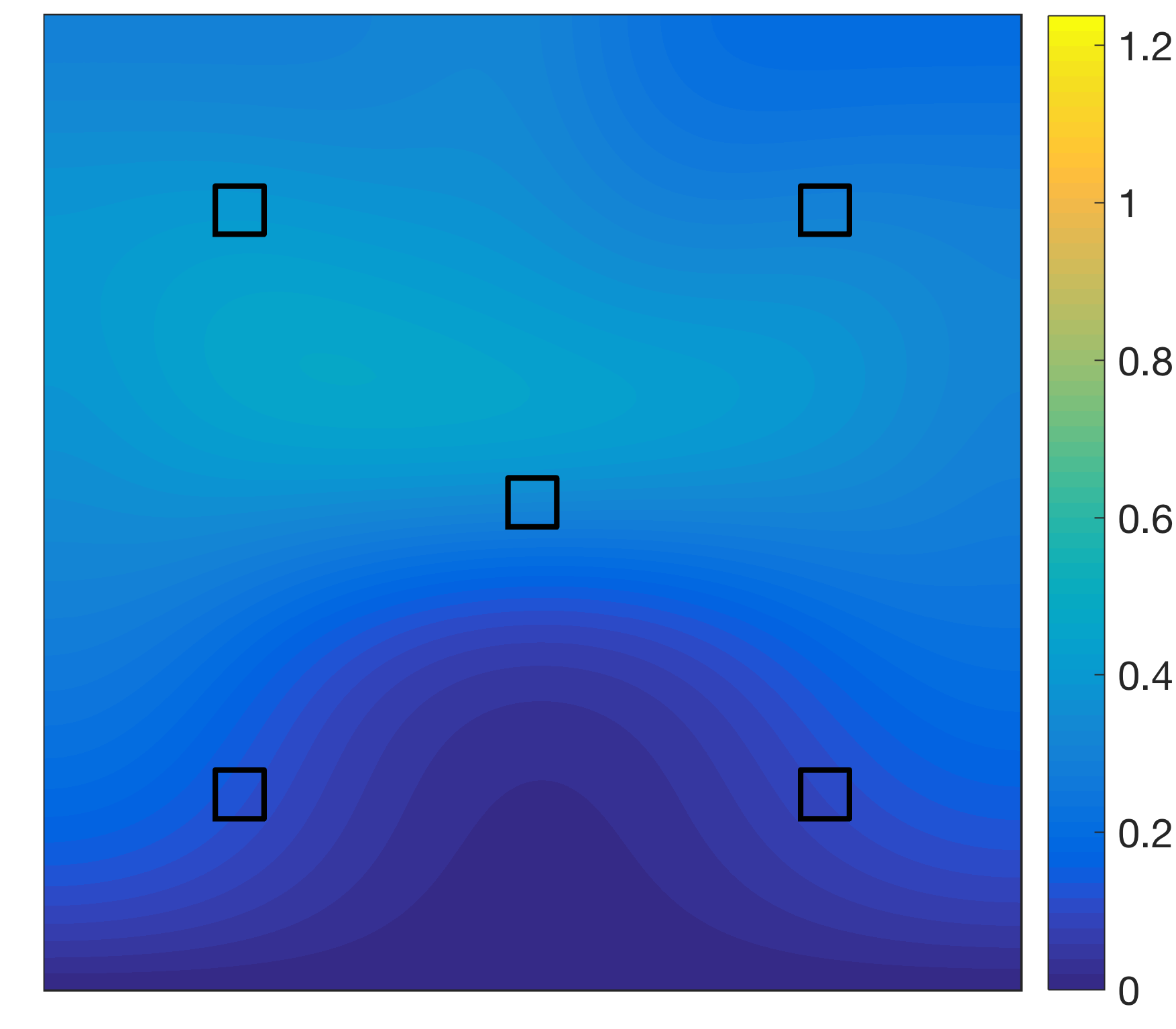

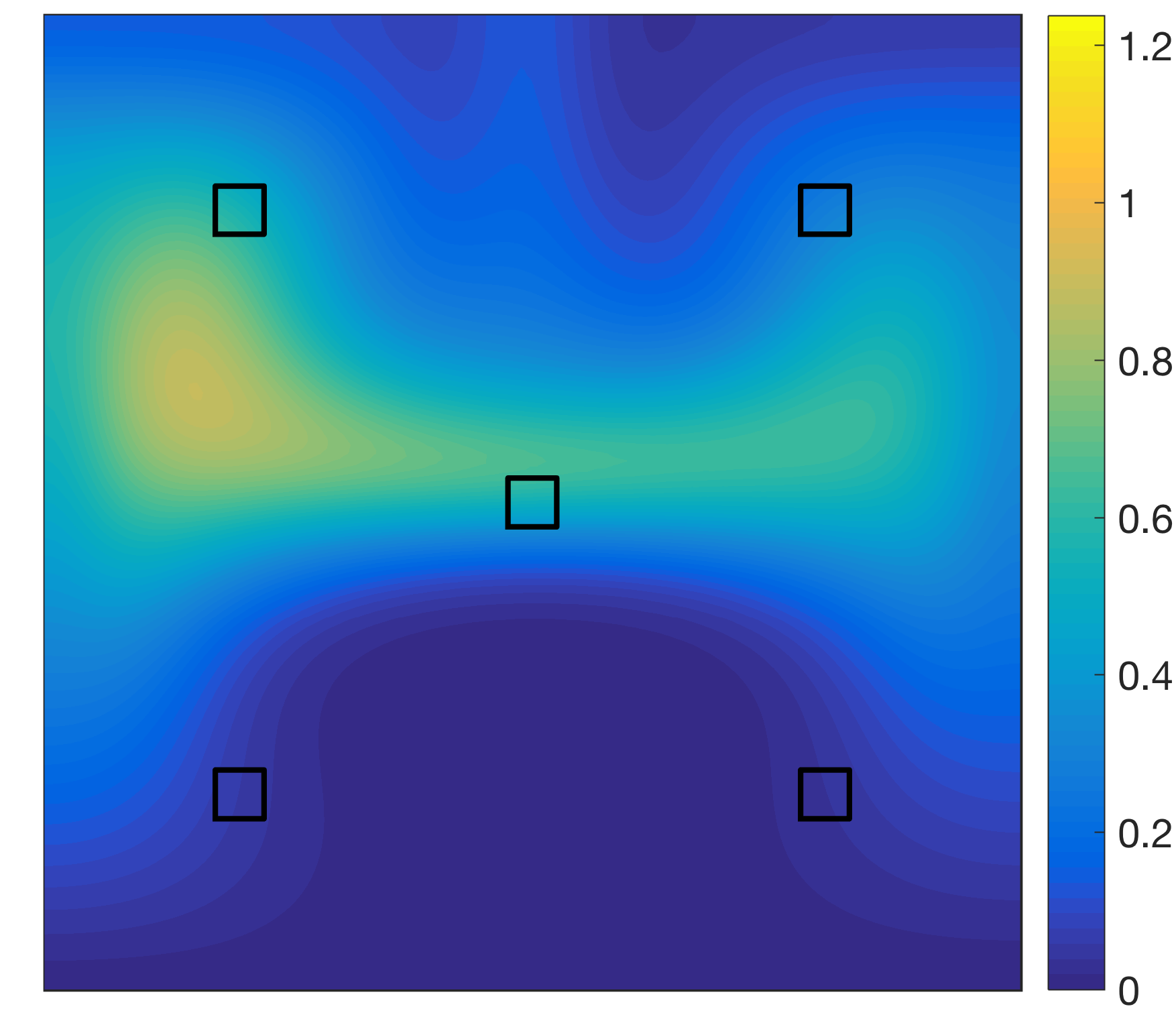

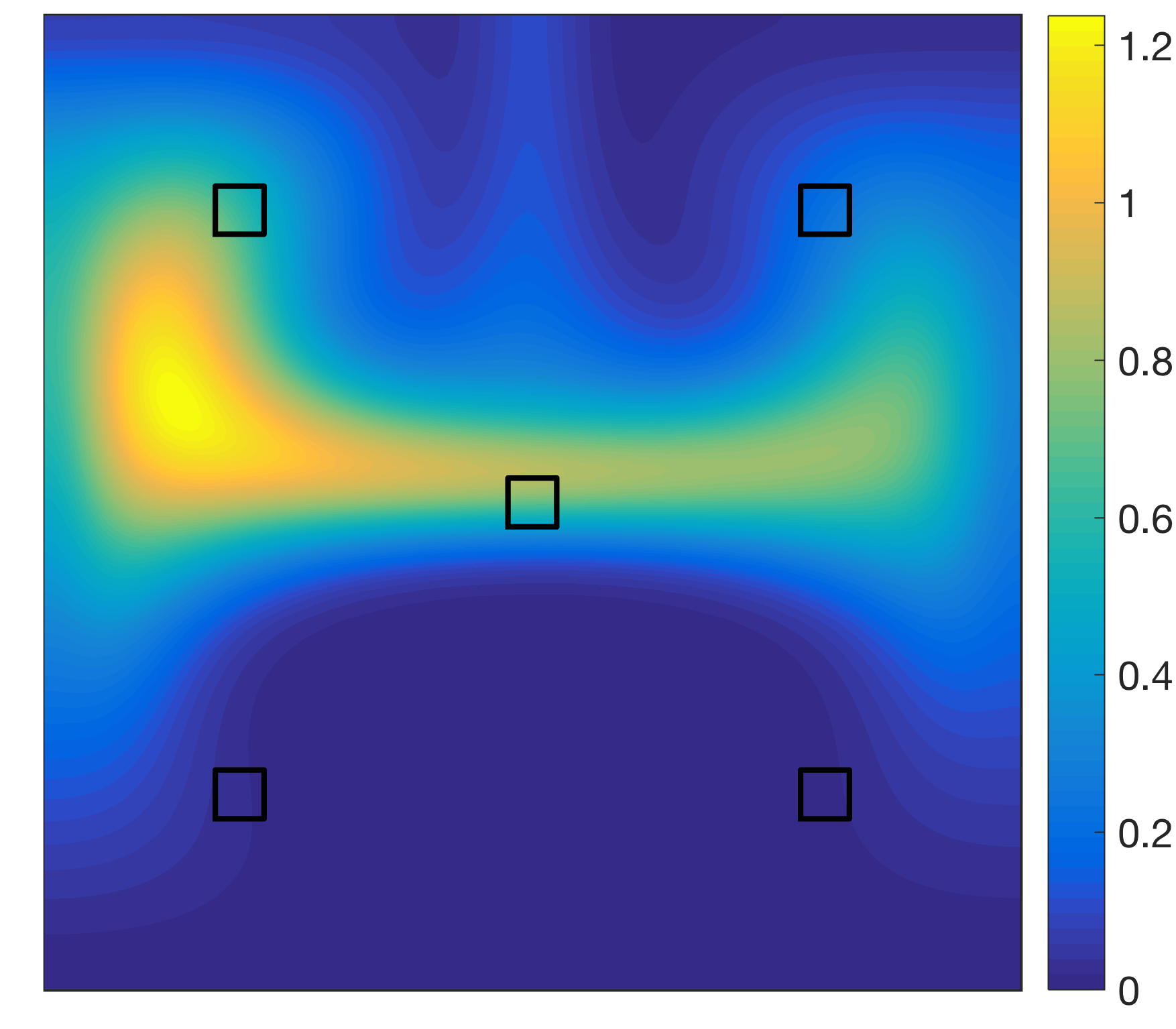

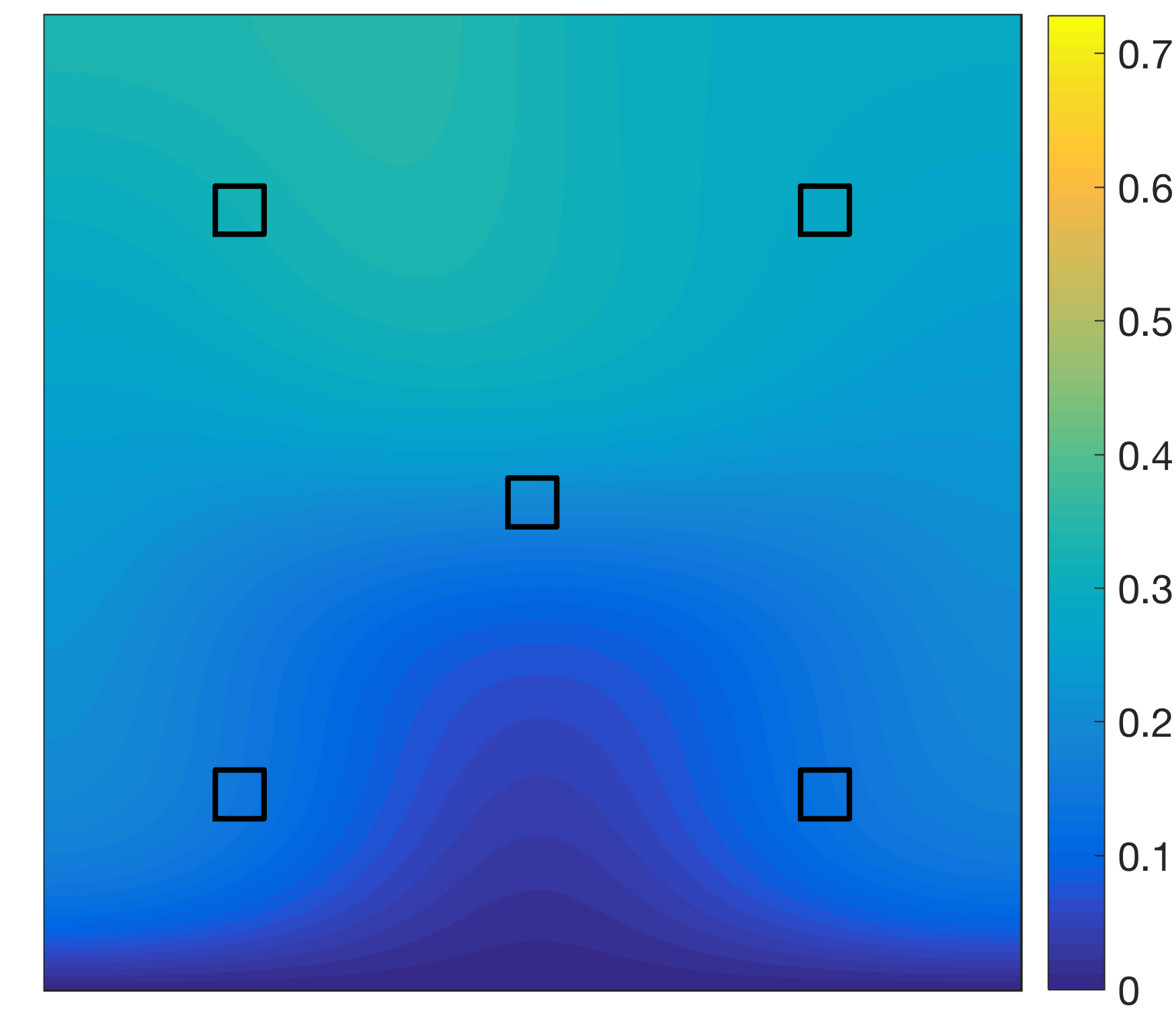

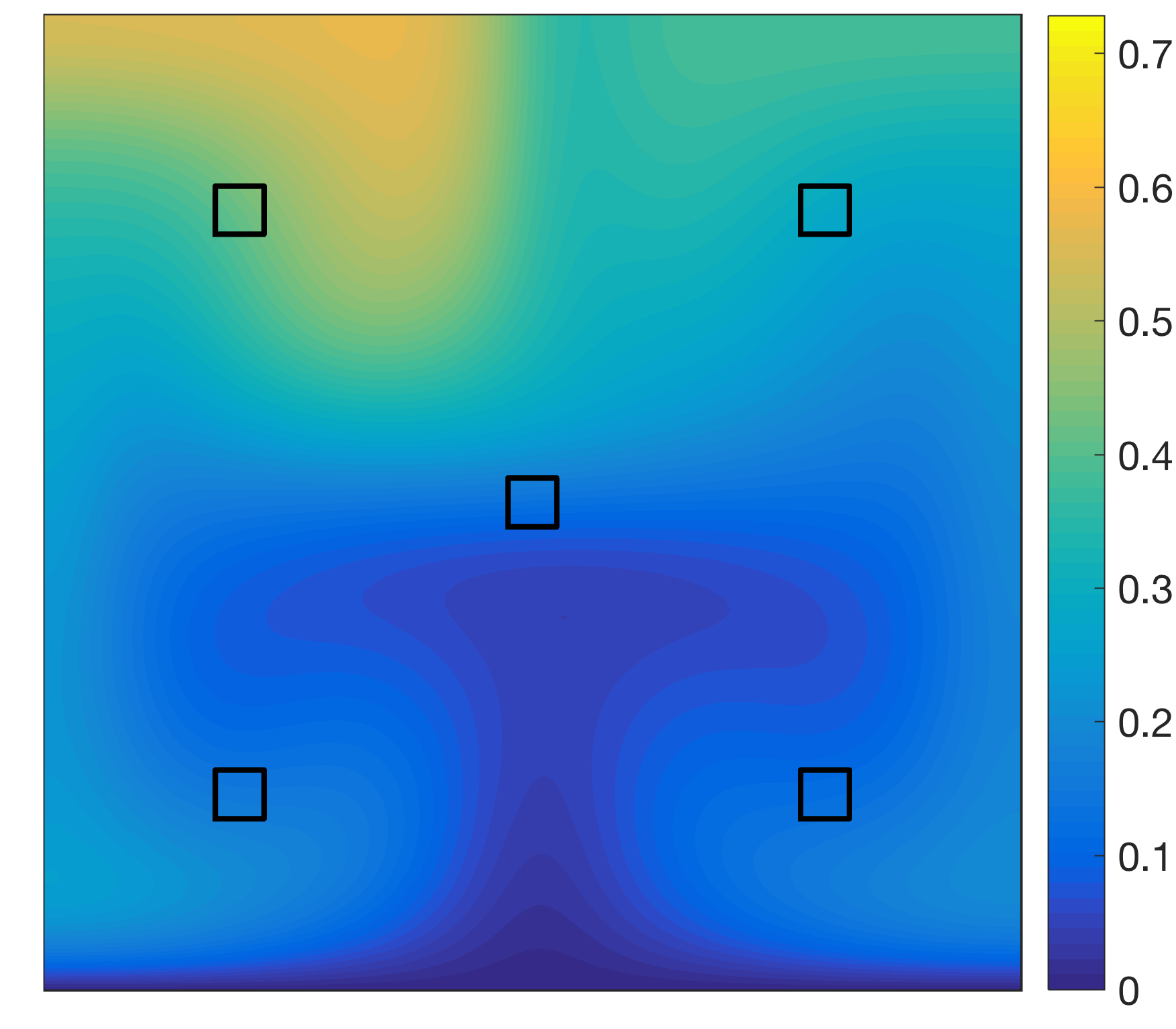

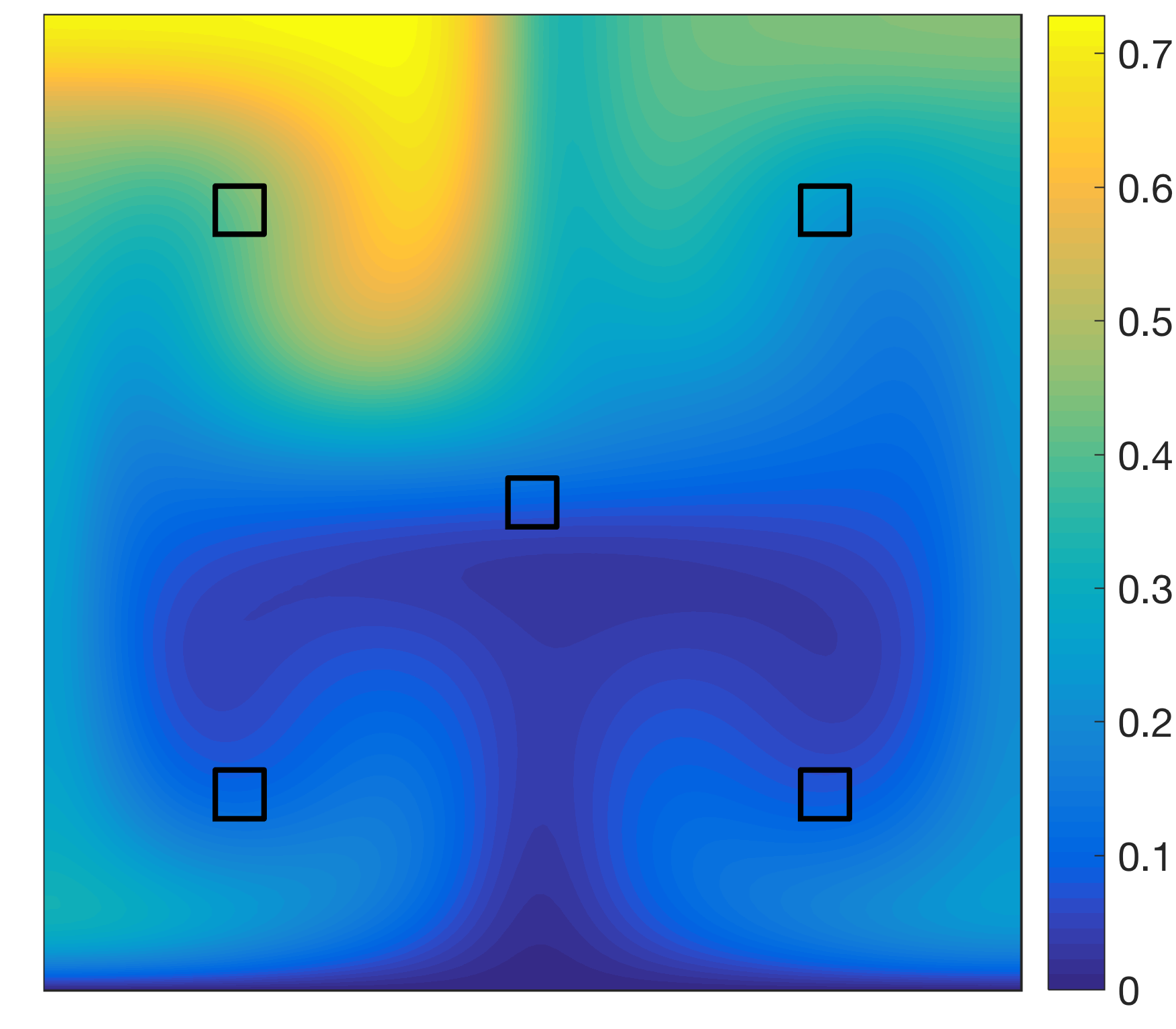

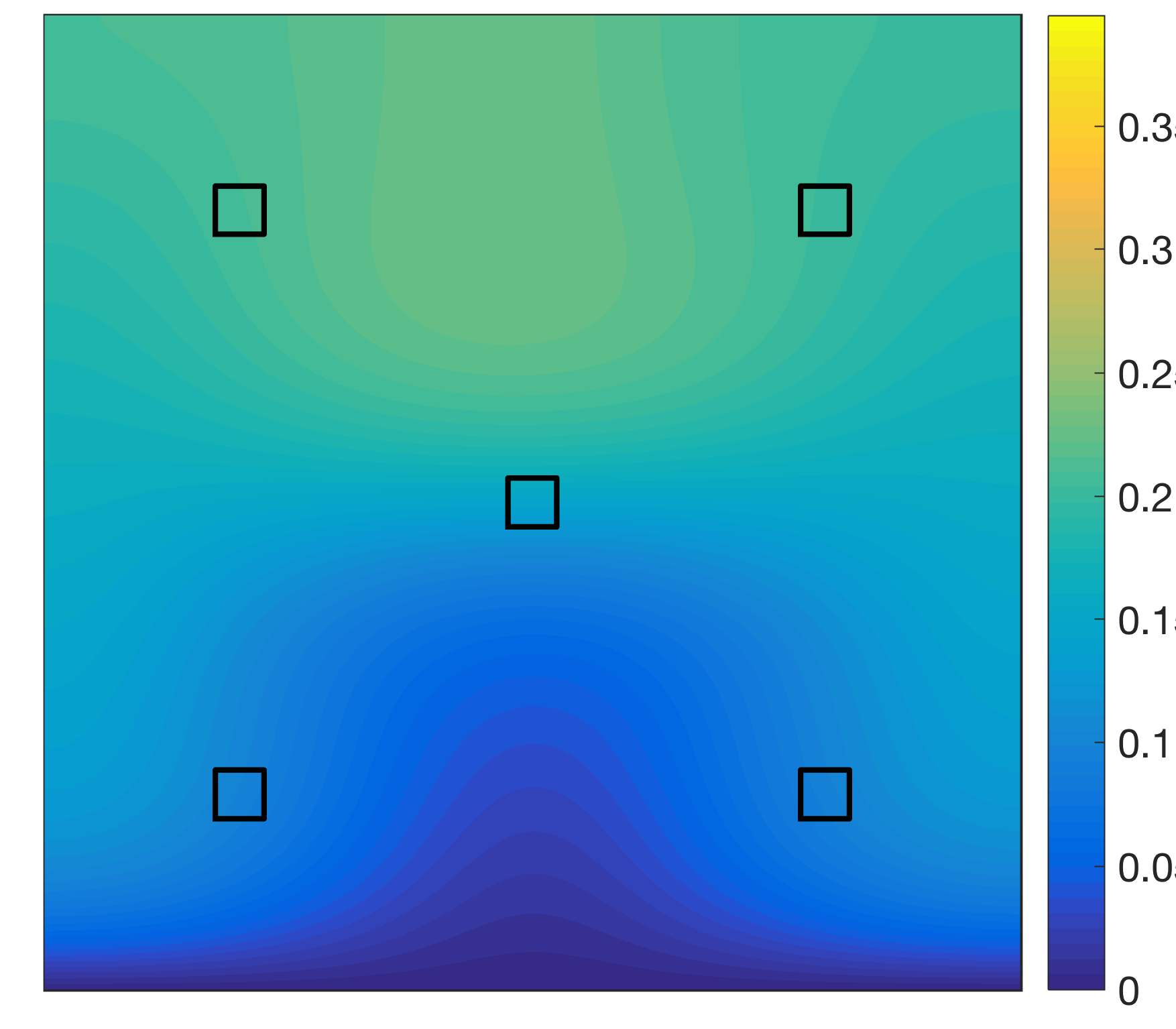

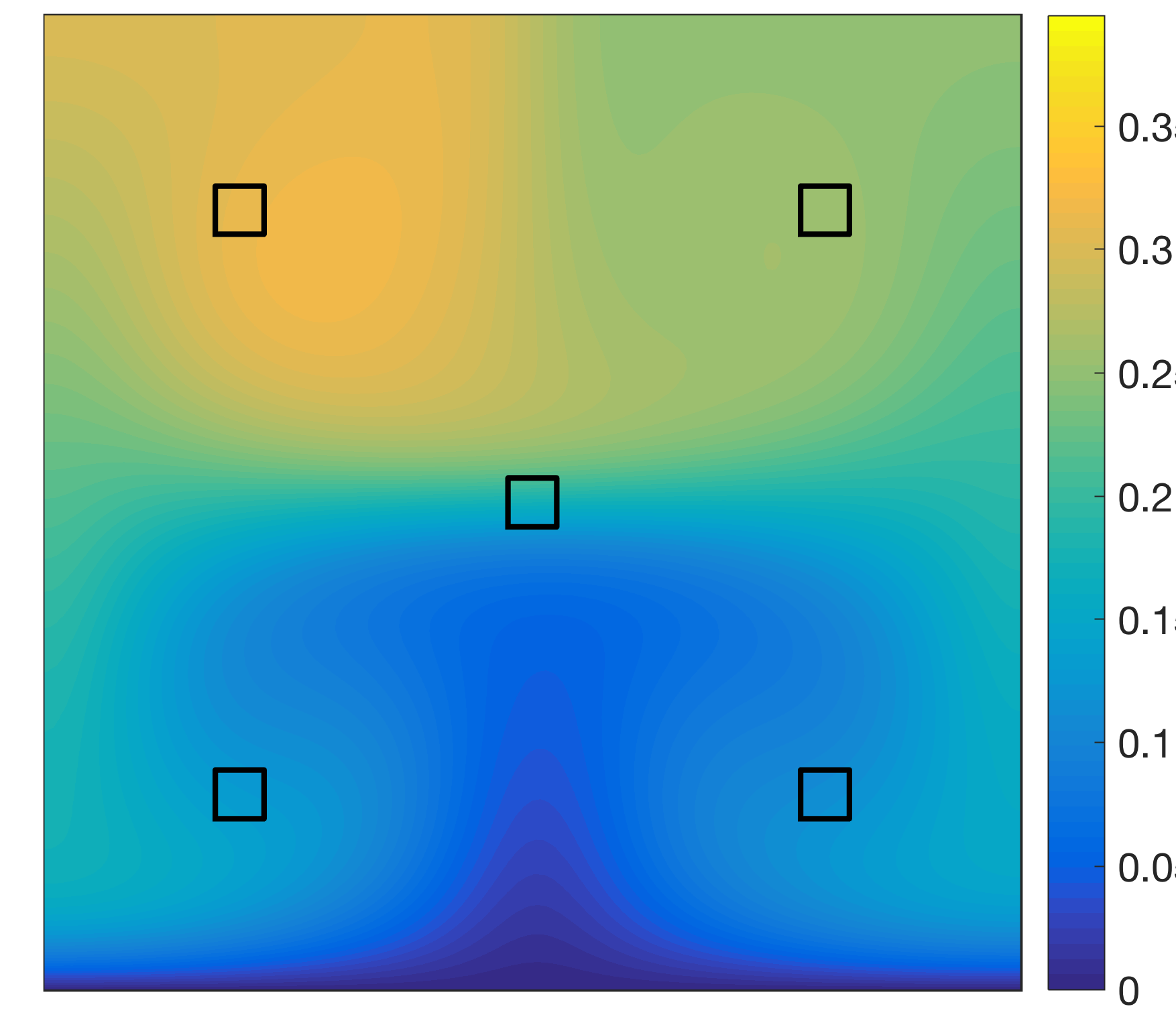

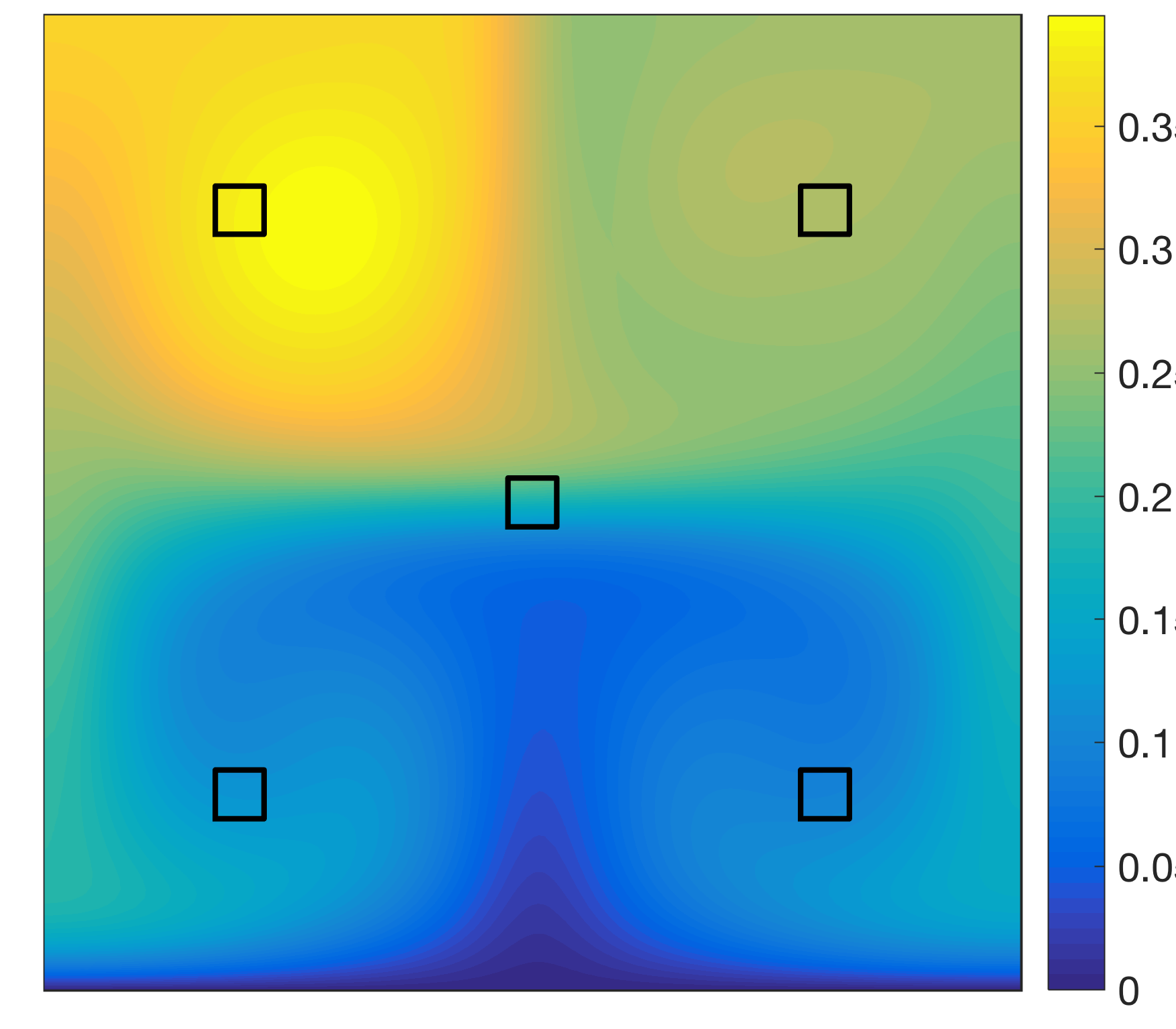

and the velocity field is . The domain with measurement sites as well as the velocity field are sketched in Figure 1. Our model problem is motivated by the source reconstruction of a (possibly) accidental release of an agent, where the velocity field is known Krysta2006 ; Krysta2007 . Although we consider a fixed velocity field here, our problem formulation also directly applies to (affinely) parametrized velocity fields.

We do not consider an additional forcing term and thus set . The inner product on is defined as for the reference parameter . Since is divergence-free and on , one can show that is coercive and that the symmetric part of is given by . Hence we can use the min-theta approach to construct a coercivity lower bound: . For details, we refer to Appendix B.3 of Kaercher2016 .

We choose the time interval and a time step size resulting in time steps. For the space discretization we introduce a spatial mesh with an element size of and corresponding linear finite element approximation spaces with degrees of freedom. We assume that the (unknown true) initial condition is given by a spatial Gaussian function with mean and covariance matrix , where and is the identity matrix (the center of the Gaussian is shown as a blue dot in Figure 1). The average concentration over the measurement domains shown in Figure 1 serve as our five outputs , . We then generate noisy measurements by adding white noise to the outputs computed from the full-order model for the (unknown true) parameter with initial condition such that , where is a vector containing uncorrelated Gaussian noise in each entry, i.e, . The inverse observation covariance matrix is given by . In practice, the choice 10 produces acceptable results for the 4D Var problem (a thorough discussion of the impact of Tychonov regularization on 4D-Var is beyond the scope of this paper, we refer to Puel2009 for more details). In the strong-constraint case, we assume an optimal prior and set the prior mean to be equal to the true initial condition. In the weak-constraint case, we set to account for the model-error forcing and i.e. the model-error forcing is assumed to be unbiased and have zero mean. In both cases, the inverse prior covariance matrix is given by the mass matrix.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

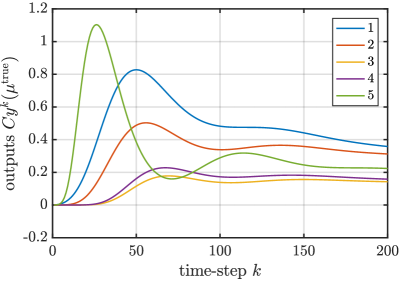

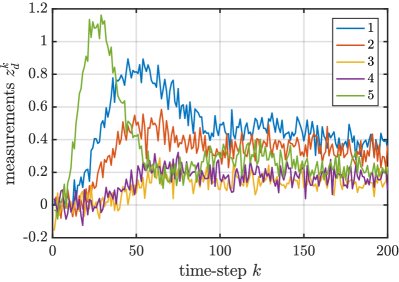

A preconditioned Newton-CG method takes between seconds for (requiring 31 CG iterations) and seconds for (requiring 56 CG iterations) to solve the full-order strong-constraint 4D-Var problem. For the weak-constraint case, the solution time ranges from seconds (, 81 CG iterations) to seconds (, 137 CG iterations). In Figure 2, we plot the concentration of the pollutant for three different parameter values and various timesteps. The influence of the Taylor-Green vortex and the Péclet number on the solutions is clearly visible. In Figure 3 on the left, we plot the five true outputs over time (the numbering and color of the curves refer to the sketch in Figure 1). The corresponding noisy measurements used for the data assimilation are shown on the right. We note that all computations were performed in Matlab on a computer with 2.6 GHz Intel Core i7 processor and 16 GB of RAM.

6.2 Reduced-order 4D-Var approach

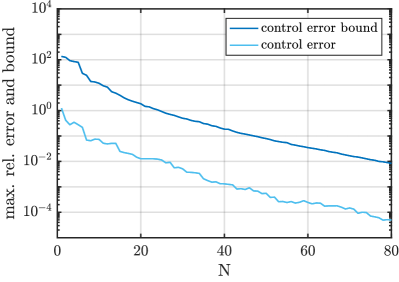

We consider the strong- and weak-constraint 4D-Var data assimilation problem separately and present results for the performance of the reduced-order approach for each setting. We thus build different reduced basis spaces for the strong- and weak-constraint case by employing the Greedy sampling procedure described in Section 3.5 and 4.4, respectively. For both, we choose and a training set consisting of 40 equidistant parameters over the parameter domain . We also prescribe the number of Greedy iterations to (strong) and (weak) resulting in a relative error bound tolerance of approximately .

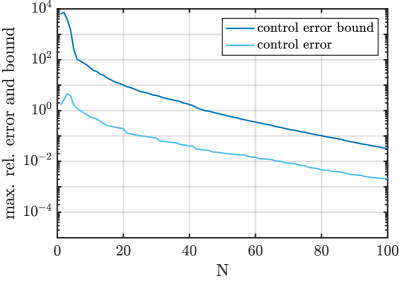

In Figure 4 we plot the maximum relative error and error bound over a test sample consisting of 20 randomly chosen parameters in versus the number of Greedy iterations . The relative error and bound are defined as and in the strong-constraint case, and by and in the weak-constraint case. We observe that the error and bound converge at the same rate and that the effectivities, i.e., the ratio of the bound and the error, thus remain almost constant over . The mean effectivities over the test sample for are in the strong-constraint case and in the weak-constraint case. We note that maximum dimensions of the reduced basis state/adjoint and control spaces are and (strong-constraint), and and (weak-constraint). Especially in the strong-constraint case, we thus obtain a considerable reduction in the dimension of the control space from to . This will also be reflected in the required number of CG iterations to solve the reduced-order 4D-Var problem (see below).

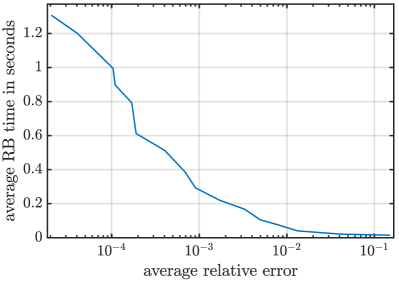

We next report on the online computational times of our reduced-order approach. Similar to the full-order approach, the reduced-order solution times also depend on (smaller for and higher for ) and of course also strongly on . We first consider the strong-constraint case: the solution times for the reduced-order 4D-Var problem range from milliseconds to seconds, the evaluation of the a posteriori error bound takes between and milliseconds. We note that the computation of the error bound is much faster than the solution of the 4D-Var problem itself. Furthermore, we note that the computational time to evaluate the error bound only depends on and not on (i.e., evaluating the bound for fixed at or takes the same time). The overall online speed-up for thus ranges from approximately to .

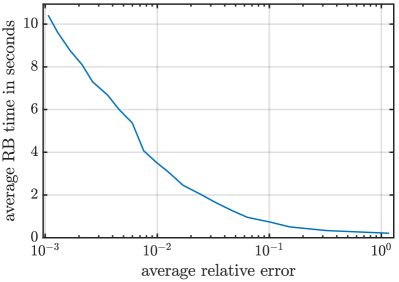

In the weak-constraint case, the solution times for the reduced-order 4D-Var problem range from milliseconds to seconds, the evaluation of the a posteriori error bound takes between and milliseconds. Again, the evaluation of the error bound is much faster than the solution of the 4D-Var problem itself. The online speed-up for is now approximately .

In order to illustrate the connection between the approximation error and the online solution time, we plot the average online solution time of the reduced-order 4D-Var problem versus the average relative error over the test sample in Figure 5. Recall that the full-order solution takes approximately seconds for the strong-constraint case and seconds for the weak-constraint case.

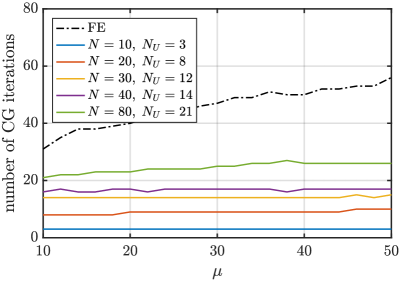

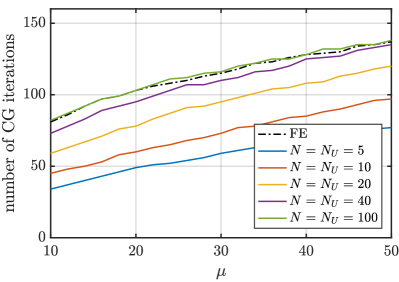

We next show results for the number of CG iterations required to solve the reduced-order 4D-Var problem. In Figure 6, we plot the number of CG iterations as a function of the parameter for various values of and on the left for the strong-constraint case and on the right for the weak-constraint case. In the same plots, we also show the number of CG iterations required to solve the full-order problem. We observe a different behavior in the strong- and weak-constraint case. We first note that in the weak-constraint case the number of reduced-order CG iterations converges to the number of full-order CG iterations with increasing . However, in the strong-constraint case the number of reduced-order CG iterations is bounded by , which is significantly smaller than . The number of reduced-order CG iterations are thus almost constant over for given and are considerably smaller than the number of full-order CG iterations even for .

Finally, we consider the outer minimization problem and try to estimate the unknown true parameter which lead to the noisy measurements. To this end, we define the “optimal” parameters and which minimize the full-order and reduced-order cost functionals

| (67) |

respectively. We compute the optimal estimated parameters and using the Matlab routine fminbnd, which only needs evaluations of the full-order and reduced-order cost functional. We also define the maximum relative cost functional error and parameter error . We present these errors for the strong- and weak-constraint case as a function of in Table 1. We observe that in both cases the cost functional error and parameter error converge very fast, i.e., the reduced-order approach allows us to recover the optimal parameter . We also note that the (full-order) optimal parameter is close to the true parameter in the strong-constraint case ( vs. ), but that this is not true in the weak-constraint case ( vs. ). Since with increasing , this is of course also true for — and the best we can expect of — the reduced-order optimal parameters.

| N | (strong) | (strong) | (weak) | (weak) |

|---|---|---|---|---|

| 10 | 3.12e-01 | 4.18e-01 | 2.44e-01 | 6.02e-02 |

| 20 | 7.36e-03 | 1.30e-01 | 1.70e-02 | 9.33e-03 |

| 30 | 8.22e-04 | 1.42e-03 | 3.51e-03 | 1.70e-04 |

| 40 | 1.24e-04 | 4.99e-04 | 6.37e-04 | 3.26e-04 |

| 50 | 1.14e-05 | 2.98e-05 | 2.05e-04 | 3.53e-05 |

| 60 | 4.36e-06 | 1.27e-05 | 9.70e-05 | 3.90e-05 |

| 70 | 3.92e-07 | 4.18e-06 | 3.58e-05 | 1.93e-05 |

| 80 | 8.76e-08 | 9.71e-08 | 1.05e-05 | 4.12e-06 |

| 90 | - | - | 4.17e-06 | 2.51e-06 |

| 100 | - | - | 1.94e-06 | 3.09e-06 |

7 Conclusion

In this paper, we considered the strong- and weak-constraint 4D-Var data assimilation problem. We presented a reduced-order approach to the 4D-Var problem based on the reduced basis method and proposed rigorous and efficiently evaluable a posteriori error bounds for the optimal control, i.e., the initial condition in the strong-constraint setting and the model-error forcing in the weak-constraint setting. For both instances we showed numerical results confirming the validity of the proposed approach. We also presented theoretical results for the combined case with unknown initial condition and model-error forcing.

We note that although we consider a parametrized problem here, the error bounds can also be used in the non-parametrized reduced-order setting and are independent of how the reduced-order spaces are constructed. The bound thus directly applies to reduced-order approaches where the spaces are constructed, e.g., using empirical orthogonal functions, POD, or dual-weighted POD DN2008 . We also believe that the error bounds can be gainfully applied in a multi-fidelity approach to solve the 4D-Var problem, e.g., in a trust-region approach as proposed in CNF2011 ; DNZ+2013 .

Although we also presented results for the error in the cost functional and for estimating the unknown model parameter, we currently cannot provide rigorous and sharp a posteriori error bounds for these quantities. Furthermore, we only considered a fixed setting for the noise level and regularization parameter here, a detailed analysis of the influence of these parameters on the performance of the reduced order model has not been performed. These are topics of current and future research in our groups.

Appendix A Continuous 4D-Var Formulation

The strong-constraint 4D-Var problem for a linear parabolic PDE on , with a Lipschitz domain,

| (68) |

classically rewrites as the optimal control problem:

with a lower semi-continuous cost functional

| (69) |

on the tensor-product of and . If the observation operator has a unique continuation in , is coercive and strictly convex. Then, if so the set of admissible states is non-empty, there exists a unique solution, see e.g. Fursikov2000 . To characterize and compute the solution, one can use duality techniques following PBG+1964 or ET1976 . On introducing a Lagrange multiplier , for the constraint, it is classical that the solution should satisfy MS2002

| (70a) | ||||

| (70b) | ||||

| (70c) | ||||

| (70d) | ||||

| (70e) | ||||

which is a well-posed saddle-point problem, well-approximated by the discretization (8) EG2010 , again on the condition that the observation operator has a unique continuation in . Note that first adequately discretizing then leads to exactly the same discrete Euler-Lagrange equations as (8).

The weak-constraint 4D-Var problem is also classical, see e.g. Fursikov2000 . The optimal control problem becomes

for

| (71) |

with the lower semi-continuous cost functional

| (72) |

on the tensor-product of and ; the saddle-point becomes

| (73a) | ||||

| (73b) | ||||

| (73c) | ||||

while existence and uniqueness of a soluion still hold under the same conditions.

References

- (1) Barrault, M., Maday, Y., Nguyen, N.C., Patera, A.T.: An ‘empirical interpolation’ method: application to efficient reduced-basis discretization of partial differential equations. Comptes Rendus de l’Académie des Sciences Paris 339(9), 667–672 (2004). DOI 10.1016/j.crma.2004.08.006.

- (2) Bennett, A.F.: Inverse Methods in Physical Oceanography. Cambridge University Press (1993)

- (3) Benzi, M., Golub, G.H., Liesen, J.: Numerical solution of saddle point problems. Acta Numerica 14, 1?137 (2005). DOI 10.1017/S0962492904000212

- (4) Bröcker, J.: Existence and uniqueness for four-dimensional variational data assimilation in discrete time. SIAM Journal on Applied Dynamical Systems 16(1), 361–374 (2017). DOI 10.1137/16M1068918.

- (5) Cao, Y., Zhu, J., Navon, I.M., Luo, Z.: A reduced-order approach to four-dimensional variational data assimilation using proper orthogonal decomposition. International Journal for Numerical Methods in Fluids 53(10), 1571–1583 (2007). DOI 10.1002/fld.1365.

- (6) Chen, X., Navon, I.M., Fang, F.: A dual-weighted trust-region adaptive POD 4D-Var applied to a finite-element shallow-water equations model. International Journal for Numerical Methods in Fluids 65(5), 520–541 (2011). DOI 10.1002/fld.2198.

- (7) Courtier, P.: Dual formulation of four-dimensional variational assimilation. Quarterly Journal of the Royal Meteorological Society 123(544), 2449–2461 (1997). DOI 10.1002/qj.49712354414.

- (8) Courtier, P., Thépaut, J.N., Hollingsworth, A.: A strategy for operational implementation of 4D-Var, using an incremental approach. Quarterly Journal of the Royal Meteorological Society 120(519), 1367–1387 (1994). DOI 10.1002/qj.49712051912.

- (9) Daescu, D.N., Navon, I.M.: A dual-weighted approach to order reduction in 4DVAR data assimilation. Monthly Weather Review 136(3), 1026–1041 (2008). DOI 10.1175/2007MWR2102.1.

- (10) Dedè, L.: Reduced basis method and a posteriori error estimation for parametrized linear-quadratic optimal control problems. SIAM J. Sci. Comput. 32(2), 997–1019 (2010)

- (11) Dimitriu, G., Apreutesei, N., Ştefănescu, R.: Numerical Simulations with Data Assimilation Using an Adaptive POD Procedure, pp. 165–172. Springer Berlin Heidelberg, Berlin, Heidelberg (2010). DOI 10.1007/978-3-642-12535-5_18.

- (12) Du, J., Navon, I., Zhu, J., Fang, F., Alekseev, A.: Reduced order modeling based on POD of a parabolized Navier-Stokes equations model II: Trust region POD 4D VAR data assimilation. Computers & Mathematics with Applications 65(3), 380–394 (2013). DOI 10.1016/j.camwa.2012.06.001.

- (13) Ekeland, I., Temam, R.: Convex Analysis and Variational Problems. Studies in mathematics and its applications. Elsevier (1976)

- (14) Engl, H.W., Hanke, M., Neubauer, A.: Regularization of Inverse Problems. Kluwer Academic Publishers (1996)

- (15) Ern, A., Guermond, J.L.: Theory and Practice of Finite Elements. Applied Mathematical Sciences. Springer (2010)

- (16) Fursikov, A.V.: Optimal control of distributed systems. Theory and applications, vol. 187. American Mathematical Society, Providence, RI (2000)

- (17) Gerner, A.L., Veroy, K.: Certified reduced basis methods for parametrized saddle point problems. SIAM Journal on Scientific Computing 34(5), A2812–A2836 (2012). DOI 10.1137/110854084.

- (18) Grepl, M.A., Maday, Y., Nguyen, N.C., Patera, A.T.: Efficient reduced-basis treatment of nonaffine and nonlinear partial differential equations. ESAIM: Mathematical Modelling and Numerical Analysis 41(3), 575–605 (2007)

- (19) Grepl, M.A., Patera, A.T.: A posteriori error bounds for reduced-basis approximations of parametrized parabolic partial differential equations. ESAIM: Math. Model. Num. 39(1), 157–181 (2005). DOI 10.1051/m2an:2005006.

- (20) Habert, J., Ricci, S., Pape, E.L., Thual, O., Piacentini, A., Goutal, N., Jonville, G., Rochoux, M.: Reduction of the uncertainties in the water level-discharge relation of a 1d hydraulic model in the context of operational flood forecasting. Journal of Hydrology 532(Supplement C), 52 – 64 (2016). DOI 10.1016/j.jhydrol.2015.11.023.

- (21) Hinze, M., Pinnau, R., Ulbrich, M., Ulbrich, S.: Optimization with PDE Constraints, Mathematical Modelling: Theory and Applications, vol. 23. Springer (2009)

- (22) Hoteit, I., Köhl, A.: Efficiency of reduced-order, time-dependent adjoint data assimilation approaches. Journal of Oceanography 62(4), 539–550 (2006). DOI 10.1007/s10872-006-0074-2.

- (23) Huynh, D.B.P., Rozza, G., Sen, S., Patera, A.T.: A successive constraint linear optimization method for lower bounds of parametric coercivity and inf-sup stability constants. Comptes Rendus de l’Académie des Sciences Paris 345(8), 473–478 (2007). DOI 10.1016/j.crma.2007.09.019.

- (24) Ide, K., Courtier, P., Ghil, M., Lorenc, A.: Unified notation for data assimilation: operational, sequential and variational. J. Meteorol. Soc. Jpn. 75, 181–189 (1997)

- (25) Kärcher, M.: Certified reduced basis methods for parametrized pde-constrained optimization problems. Ph.D. thesis, RWTH Aachen University 2017

- (26) Kärcher, M., Grepl, M.A.: A certified reduced basis method for parametrized elliptic optimal control problems. ESAIM: Contr. Optim. Ca. 20(2), 416–441 (2013). DOI 10.1051/cocv/2013069

- (27) Kärcher, M., Grepl, M.A.: A posteriori error estimation for reduced order solutions of parametrized parabolic optimal control problems. ESAIM: M2AN 48(6), 1615–1638 (2014). DOI 10.1051/m2an/2014012.

- (28) Kärcher, M., Tokoutsi, Z., Grepl, M.A., Veroy, K.: Certified reduced basis methods for parametrized elliptic optimal control problems with distributed controls. Journal of Scientific Computing (2017). DOI 10.1007/s10915-017-0539-z.

- (29) Krysta, M., Bocquet, M.: Source reconstruction of an accidental radionuclide release at European scale. Quarterly Journal of the Royal Meteorological Society 133(623), 529–544 (2007). DOI 10.1002/qj.3.

- (30) Krysta, M., Bocquet, M., Sportisse, B., Isnard, O.: Data assimilation for short-range dispersion of radionuclides: An application to wind tunnel data. Atmospheric Environment 40(38), 7267–7279 (2006). DOI 10.1016/j.atmosenv.2006.06.043.

- (31) Law, K., Stuart, A., Zygalakis, K.: Data Assimilation. Springer (2015)

- (32) Le Dimet, F.X., Talagrand, O.: Variational algorithms for analysis and assimilation of meteorological observations: theoretical aspects. Tellus A 38A(2), 97–110 (1986). DOI 10.1111/j.1600-0870.1986.tb00459.x.

- (33) Lorenc, A.C.: A global three-dimensional multivariate statistical interpolation scheme. Monthly Weather Review 109(4), 701–721 (1981). DOI 10.1175/1520-0493(1981)1090701:AGTDMS2.0.CO;2.

- (34) Lorenc, A.C.: Analysis methods for numerical weather prediction. Quarterly Journal of the Royal Meteorological Society 112(474), 1177–1194 (1986). DOI 10.1002/qj.49711247414.

- (35) Lynch, P.: The Princeton Companion to Applied Mathematics, chap. Numerical Weather Prediction, pp. 705–712. Princeton University Press (2015)

- (36) Maday, Y., Nguyen, N.C., Patera, A.T., Pau, G.S.H.: A general, multipurpose interpolation procedure: the magic points. Communications on Pure and Applied Analysis (CPAA) 8, 383 – 404 (2007). DOI 10.3934/cpaa.2009.8.383

- (37) Maday, Y., Patera, A.T., Penn, J.D., Yano, M.: A parameterized-background data-weak approach to variational data assimilation: formulation, analysis, and application to acoustics. International Journal for Numerical Methods in Engineering 102(5), 933–965 (2015). DOI 10.1002/nme.4747.

- (38) Maday, Y., Patera, A.T., Penn, J.D., Yano, M.: PBDW state estimation: noisy observations; configuration-adaptive background spaces; physical interpretations. ESAIM: Proc. 50, 144–168 (2015). DOI 10.1051/proc/201550008.

- (39) Marchuk, G., Shutyaev, V.: Solvability and numerical algorithms for a class of variational data assimilation problems. ESAIM, Control Optim. Calc. Var. 8, 873–883 (2002). DOI 10.1051/cocv:2002044

- (40) Negri, F., Rozza, G., Manzoni, A., Quarteroni, A.: Reduced basis method for parametrized elliptic optimal control problems. SIAM J. Sci. Comput. 35(5), A2316–A2340 (2013)

- (41) Pontryagin, L., Boltyanskij, V., Gamkrelidze, R., Mishchenko, E.: The mathematical theory of optimal processes; translated from the Russian by D.E. Brown. . Macmillan (1964)

- (42) Prud’homme, C., Rovas, D.V., Veroy, K., Machiels, L., Maday, Y., Patera, A.T., Turinici, G.: Reliable real-time solution of parametrized partial differential equations: Reduced-basis output bound methods. J. Fluid. Eng. 124(1), 70–80 (2002). DOI 10.1115/1.1448332.

- (43) Puel, J.P.: A nonstandard approach to a data assimilation problem and Tychonov regularization revisited. SIAM Journal on Control and Optimization 48(2), 1089–1111 (2009). DOI 10.1137/060670961.

- (44) Rao, V., Sandu, A., Ng, M., Nino-Ruiz, E.D.: Robust data assimilation using and Huber norms. SIAM Journal on Scientific Computing 39(3), B548–B570 (2017). DOI 10.1137/15M1045910.

- (45) Reich, S., Cotter, C.: Probabilistic Forecasting and Bayesian Data Assimilation. Cambridge University Press (2015)

- (46) Robert, C., Durbiano, S., Blayo, E., Verron, J., Blum, J., Dimet, F.X.L.: A reduced-order strategy for 4D-Var data assimilation. Journal of Marine Systems 57(1-2), 70–82 (2005). DOI 10.1016/j.jmarsys.2005.04.003.

- (47) Rozza, G., Huynh, D.B.P., Patera, A.T.: Reduced basis approximation and a posteriori error estimation for affinely parametrized elliptic coercive partial differential equations. Archives of Computational Methods in Engineering 15(3), 229–275 (2008). DOI 10.1007/s11831-008-9019-9.

- (48) Sasaki, Y.: Some basic formalisms in numerical variational analysis. Monthly Weather Review 98(12), 875–883 (1970). DOI 10.1175/1520-0493(1970)0980875:SBFINV2.3.CO;2.

- (49) Stoll, M., Wathen, A.: All-at-once solution of time-dependent Stokes control. Journal of Computational Physics 232(1), 498–515 (2013). DOI 10.1016/j.jcp.2012.08.039.

- (50) Trémolet, Y.: Accounting for an imperfect model in 4D-Var. Quarterly Journal of the Royal Meteorological Society 132(621), 2483–2504 (2006). DOI 10.1256/qj.05.224.

- (51) Tröltzsch, F., Volkwein, S.: POD a-posteriori error estimates for linear-quadratic optimal control problems. Comput. Optim. Appl. 44, 83–115 (2009). DOI 10.1007/s10589-008-9224-3.

- (52) Vermeulen, P.T.M., Heemink, A.W.: Model-reduced variational data assimilation. Monthly Weather Review 134(10), 2888–2899 (2006). DOI 10.1175/MWR3209.1.

- (53) Veroy, K., Rovas, D.V., Patera, A.T.: A posteriori error estimation for reduced-basis approximation of parametrized elliptic coercive partial differential equations: “convex inverse” bound conditioners. ESAIM: Contr. Optim. Ca. 8, 1007–1028 (2002). DOI 10.1051/cocv:2002041. Special Volume: A tribute to J. L. Lions