Asian Option Pricing with Orthogonal Polynomials111I thank Damien Ackerer, Damir Filipović, participants at the 9th International Workshop on Applied Probability in Budapest, and two anonymous referees for helpful comments. The research leading to these results has received funding from the European Research Council under the European Union’s Seventh Framework Programme (FP/2007-2013) / ERC Grant Agreement n. 307465-POLYTE.

forthcoming in Quantitative Finance)

Abstract

In this paper we derive a series expansion for the price of a continuously sampled arithmetic Asian option in the Black-Scholes setting. The expansion is based on polynomials that are orthogonal with respect to the log-normal distribution. All terms in the series are fully explicit and no numerical integration nor any special functions are involved. We provide sufficient conditions to guarantee convergence of the series. The moment indeterminacy of the log-normal distribution introduces an asymptotic bias in the series, however we show numerically that the bias can safely be ignored in practice.

JEL Classification: C32, G13

Keywords: Asian option, option pricing, orthogonal polynomials

1 Introduction

An Asian option is a derivative contract with payoff contingent on the average value of the underlying asset over a certain time period. Valuation of these contracts is not straightforward because of the path-dependent nature of the payoff. Even in the standard Black and Scholes (1973) setting the distribution of the (arithmetic) average stock price is not known. In this paper we derive a series expansion for the Asian option price in the Black-Scholes setting using polynomials that are orthogonal with respect to the log-normal distribution. The terms in the series are fully explicit since all the moments of the average price are known. We prove that the series does not diverge by showing that the tails of the average price distribution are dominated by the tails of a log-normal distribution. As a consequence of the well known moment indeterminacy of the log-normal distribution (see e.g., Heyde (1963)), it is not theoretically guaranteed that the series converges to the true price. We show numerically that this asymptotic bias is small for standard parameterizations and the real approximation challenge lies in controlling the error coming from truncating the series after a finite number of terms.

There exists a vast literature on the problem of Asian option pricing. We give a brief overview which is by no means exhaustive. One approach is to approximate the unknown distribution of the average price with a more tractable one. Turnbull and Wakeman (1991), Levy (1992), Ritchken et al. (1993), Li and Chen (2016) use an Edgeworth expansion around a log-normal reference distribution to approximate the distribution of the arithmetic average of the geometric Brownian motion. Ju (2002) and Sun et al. (2013) use a Taylor series approach to approximate the unknown average distribution from a log-normal. Milevsky and Posner (1998) use a moment matched inverse gamma distribution as approximation. Their choice is motivated by the fact that the infinite horizon average stock price has an inverse gamma distribution. More recently, Aprahamian and Maddah (2015) use a moment matched compound gamma distribution. Although these type of approximations lead to analytic option price formulas, their main drawback is the lack of reliable error estimates. A second strand of the literature focuses on Monte-Carlo and PDE methods. Kemna and Vorst (1990) propose to use the continuously sampled geometric option price as a control variate and show that it leads to a significant variance reduction. Fu et al. (1999) argue that this is a biased control variate, but interestingly the bias approximately offsets the bias coming from discretely computing the continuous average in the simulation. Lapeyre et al. (2001) perform a numerical comparison of different Monte-Carlo schemes. Rogers and Shi (1995), Zvan et al. (1996), Vecer (2001, 2002), Marcozzi (2003) solve the pricing PDE numerically. Another approach is to derive bounds on the Asian option price, see e.g. Curran (1994), Rogers and Shi (1995), Thompson (2002), and Vanmaele et al. (2006). Finally, there are several papers that derive exact representations of the Asian option price. Yor (1992) expresses the option price as a triple integral, to be evaluated numerically. Geman and Yor (1993) derive the Laplace transform of the option price. Numerical inversion of this Laplace transform is however a delicate task, see e.g. Eydeland and Geman (1995), Fu et al. (1999), Shaw (2002). Carverhill and Clewlow (1990) relate the density of the discrete arithmetic average to an iterative convolution of densities, which is approximated numerically through the Fast Fourier Transform algorithm. Later extensions and improvements of the convolution approach include Benhamou (2002), Fusai and Meucci (2008), Černỳ and Kyriakou (2011), and Fusai et al. (2011). Dufresne (2000) derives a series representation using Laguerre orthogonal polynomials. Linetsky (2004) derives a series representation using spectral expansions involving Whittaker functions.

The approach taken in this paper is closely related to Dufresne (2000) in the sense that both are based on orthogonal polynomial expansions. The Laguerre series expansion can be shown to diverge when directly expanding the density of the average price, which is related to the fact that the tails of the average price distribution are heavier than those of the Gamma distribution. As a workaround, Dufresne (2000) proposes to work with the reciprocal of the average, for which the Laguerre series does converge. The main downside of this approach is that the moments of the reciprocal average are not available in closed form and need to be calculated through numerical integration, which introduces a high computational cost and additional numerical errors. Asmussen et al. (2016) use a different workaround and expand an exponentially tilted transformation of the density of a sum of log-normal random variables using a Laguerre series. They show that the exponential tilting transformation guarantees the expansion to converge. However, a similar problem as in Dufresne (2000) arises: the moments of the exponentially tilted density are not available in closed form and have to be computed numerically. In contrast, our approach is fully explicit and does not involve any numerical integration, which makes it very fast.

Truncating our series after only one term is equivalent to pricing the option under the assumption that the average price is log-normally distributed. The remaining terms in the series can therefore be thought of as corrections to the log-normal distribution. This has a very similar flavour to approaches using an Edgeworth expansion around the log-normal distribution (cfr. Jarrow and Rudd (1982) and Turnbull and Wakeman (1991)). The key difference with our approach is that the Edgeworth expansion can easily diverge because it lacks a proper theoretical framework. In contrast, the series we present in this paper is guaranteed to converge, possibly with a small asymptotic bias. A thorough study of the approximation error reveals that the asymptotic bias is positively related to the volatility of the stock price process and the option expiry. We use the integration by parts formula from Malliavin calculus to derive an upper bound on the approximation error.

The remaining of this paper is structured as follows. Section 2 casts the problem and derives useful properties about the distribution of the arithmetic average. Section 3 describes the density expansion used to approximate the option price. In Section 4 we investigate the approximation error. Section 5 illustrates the method with numerical examples. Section 6 concludes. All proofs can be found in Appendix C.

2 The distribution of the arithmetic average

We fix a stochastic basis satisfying the usual conditions and let be the risk-neutral probability measure. We consider the Black-Scholes setup where the underlying stock price follows a geometric Brownian motion:

where is the short-rate, the volatility of the asset, and a standard Brownian motion. For notational convenience we assume , which is without loss of generality. We define the average price process as

The price at time 0 of an Asian option with continuous arithmetic averaging, strike , and expiry is given by

The option price can not be computed explicitly since we do not know the distribution of . However, we can derive useful results about its distribution.

We start by computing all the moments of . Using the time-reversal property of a Brownian motion, we have the following identity in law (cfr. Dufresne (1990), Carmona et al. (1997), Donati-Martin et al. (2001), Linetsky (2004)):

Lemma 2.1.

The random variable has the same distribution as the solution at time of the following SDE

| (2.1) |

Since the SDE in (2.1) defines a polynomial diffusion (see e.g., Filipović and Larsson (2016)), we can compute all the moments of its solution at a given time in closed form. By the identity in law of Lemma 2.1 we therefore also have all of the moments of in closed form:

Proposition 2.2.

If we denote by , , then we have

where is the following lower bidiagonal matrix

| (2.2) |

Given that the matrix exponential is a standard built-in function in most scientific computing packages, the above moment formula is very easy to implement. There also exist efficient numerical methods to directly compute the action of the matrix exponential, see e.g. Al-Mohy and Higham (2011) and Caliari et al. (2014). An equivalent, but more cumbersome to implement, representation of the moments can be found in Geman and Yor (1993).

The following proposition shows that admits a smooth density function whose tails are dominated by the tails of a log-normal density function:

Proposition 2.3.

-

1.

The random variable admits an infinitely differentiable density function .

-

2.

The density function has the following asymptotic properties:

3 Polynomial expansion

Following a similar structure as Ackerer et al. (2017) and Ackerer and Filipović (2017), we use in this section the density expansion approach described by Filipović et al. (2013) to approximate the Asian option price. Define the weighted Hilbert space as the set of measurable functions on with finite -norm defined as

| (3.1) |

for some constants , . The weight function is the density function of a log-normal distribution. The corresponding scalar product between two functions is defined as

Since the measures associated with the densities and are equivalent, we can define the likelihood ratio function such that

Using Proposition 2.3 we now have the following result:

Proposition 3.1.

If , then , i.e.

Denote by the set of polynomials on and by the subset of polynomials on of degree at most . Since the log-normal distribution has finite moments of any degree, we have for all . Let form an orthonormal polynomial basis for . Such a basis can, for example, be constructed numerically from the monomial basis using a Cholesky decomposition. Indeed, define the Hankel moment matrix as

| (3.2) |

which is positive definite by construction. If we denote by the unique Cholesky decomposition of , then

forms an orthonormal polynomial basis for . Alternative approaches to build an orthonormal basis are, for example, the three-term recurrence relation (see Lemma A.1 for details) or the analytical expressions for the orthonormal polynomials derived in Theorem 1.1 of Asmussen et al. (2016).

Remark 3.2.

The matrix defined in (3.2) can in practice be non-positive definite due to rounding errors. This problem becomes increasingly important for large and/or large because the elements in grow very fast. Similarly, the moments of can also grow very large, which causes rounding errors in finite precision arithmetic. In Appendix A we describe a convenient scaling technique that solves these problems in many cases.

Define the discounted payoff function . Since for all , we immediately have that . Denote by the closure of in . We define the projected option price , where denotes the orthogonal projection of onto in . Elementary functional analysis gives

| (3.3) |

where we define the likelihood coefficients and payoff coefficients . Truncating the series in (3.3) after a finite number of terms finally gives the following approximation for the Asian option price:

| (3.4) |

The likelihood coefficients are available in closed form using the moments of in Proposition 2.2:

The payoff coefficients can also be derived explicitly, as shown in the following proposition.

Proposition 3.3.

Let be the standard normal cumulative distribution function. The payoff coefficients are given by

with

| (3.5) |

Equivalently, we could also derive the approximation (3.4) by projecting , instead of , on the set of polynomials. This leads to the interpretation of (3.4) as the option price one obtains when approximating the true density by

| (3.6) |

The function integrates to one by construction

where the last equality follows from the fact that integrates to one. However, it is not a true probability density function since it is not guaranteed to be non-negative.

4 Approximation error

The error introduced by the the approximation in (3.4) can be decomposed as

The second term is guaranteed to converge to zero as . In order for the first term to vanish, we need and/or . It is well known (see e.g., Heyde (1963)) that the log-normal distribution is not determined by its moments. As a consequence, the set of polynomials does not lie dense in : . Hence, the fact that is not sufficient to guarantee that the first term in the error decomposition is zero. One of the goals of this paper is to quantify the importance of the first error term. In this section we therefore investigate the error associated with projecting and on the set of polynomials.

The -distances of and to their respective orthogonal projections on are given by

The -norm of the payoff function can be derived explicitly following very similar steps as in the proof of Proposition 3.3:

where , and are defined in (3.5). Hence, we can explicitly evaluate .

The computation of is more difficult since depends on the unknown density . The following lemma uses the integration by parts formula from Malliavin calculus to derive a representation of in terms of an expectation, which can be evaluated by Monte-Carlo simulation:

Lemma 4.1.

For any we have

| (4.1) |

where is any deterministic finite-valued function.

Remark 4.2.

The purpose of the function is to guarantee that the simulated actually goes to zero for . Indeed, if we set , then can be different from zero due to the Monte-Carlo error, which can lead to numerical problems when evaluating . This can be avoided by, for example, using the indicator function , for some .

As a direct consequence of (4.1) we get the following expression for the -norm of the likelihood ratio.

Corollary 4.3.

The -norm of is given by

where the random variable is independent from all other random variables and has the same distribution as .

This allows us to get an estimate for by simulating the random vector . In Appendix B we describe how to use the known density function of the geometric average as a powerful control variate to significantly reduce the variance in the Monte-Carlo simulation.

Using the Cauchy-Schwarz inequality we also have the following upper bound on the approximation error in terms of the projection errors and .

Proposition 4.4.

For any we have

| (4.2) |

This upper bound will therefore be small if and/or are well approximated by a polynomial in . Computing the upper bound involves a Monte-Carlo simulation to compute , which makes it impractical to use as a decision rule for . This bound should be seen as a more conservative estimate of the approximation error compared to direct simulation of the option price.

5 Numerical examples

In this section we compute Asian option prices using the series expansion in (3.4). The orthonormal basis is constructed using the scaling technique described in Appendix A. We set so that Proposition 3.1 is satisfied and choose so that the first moment of matches the first moment of . As a consequence, we always have

Remark 5.1.

Choosing and so that the first two moments of are matched is typically not possible due to the restriction in Proposition 3.1. A similar problem arises in the Jacobi stochastic volatility model of Ackerer et al. (2017), where options are priced using a polynomial expansion with a normal density as weight function. Ackerer and Filipović (2017) address this problem by using a mixture of two normal densities as weight function. Specifying as a mixture of normal densities would not work in our setting since in this case .333 Instead of approximating the distribution of , it is tempting to approximate the distribution of and rewrite the discounted payoff function accordingly. In this case, one can show that specifying as a normal density function gives a series approximation that converges to the true price. The catch is that we do not know the moments of , only those of , and hence the terms in the series can not be computed explicitly. Instead, we can use a mixture of two log-normal densities:

where is the mixture weight, and and are log-normal density functions with mean parameters , and volatility parameters , respectively. In order for Proposition 3.1 to apply, it suffices to choose . The remaining parameters can then be chosen freely and used for higher order moment matching.

We consider a set of seven parameterizations that has been used as a set of test cases in, among others, Eydeland and Geman (1995), Fu et al. (1999), Dufresne (2000), and Linetsky (2004). The first columns of Table 1 contain the parameter values of the seven cases. The cases are ordered in increasing size of . Remark that for all cases, however we normalize the initial stock price to one and scale the strike and option price accordingly. The columns LNS10, LNS15, LNS20 (Log-Normal Series) contain the option price approximations using (3.4) for , respectively. The columns LS (Laguerre Series) and EE (Eigenvalue Expansion) correspond to the series expansions of Dufresne (2000) and Linetsky (2004), respectively. The column VEC shows the prices produced by the PDE method of Vecer (2001, 2002) using a grid with 400 space points and 200 time points.444This grid choice corresponds to the one used in Vecer (2001). By significantly increasing the number of space points in the grid, the PDE method can achieve the same accuracy as Linetsky (2004). However, doing so makes the method very slow. The last column contains the 95% confidence intervals of a Monte-Carlo simulation using the geometric Asian option price as a control variate, cfr. Kemna and Vorst (1990). We simulate price trajectories with a time step of and approximate the continuous average with a discrete average.

[Table 1 around here]

For the first three cases we find virtually identical prices as Linetsky (2004), which is one of the most accurate benchmarks available in the literature. Remarkably, our method does not face any problems with the very low volatility in case 1. Many other existing method have serious difficulty with this parameterization. Indeed, the series of Dufresne (2000) does not even come close to the true price, while Linetsky (2004) requires 400 terms to obtain an accurate result. The price of Vecer (2001, 2002) is close to the true price, but still outside of the 95% Monte-Carlo confidence interval. Methods based on numerical inversion of the Laplace transform of Geman and Yor (1993) also struggle with low volatility because they involve numerical integration of highly oscillating integrands (see e.g., Fu et al. (1999)). When using exact arithmetic for case 1, our series with 20+1 terms agrees with the 400 term series of Linetsky (2004) to eight decimal places. When using double precision arithmetic, which was used for all numerical results in this section, the price agrees to four decimal places due to rounding errors. For cases 4 to 7, the LNS prices are slightly different from the EE benchmark. However, they are still very close and with the exception of case 4, they are all within the 95% confidence interval of the Monte-Carlo simulation.

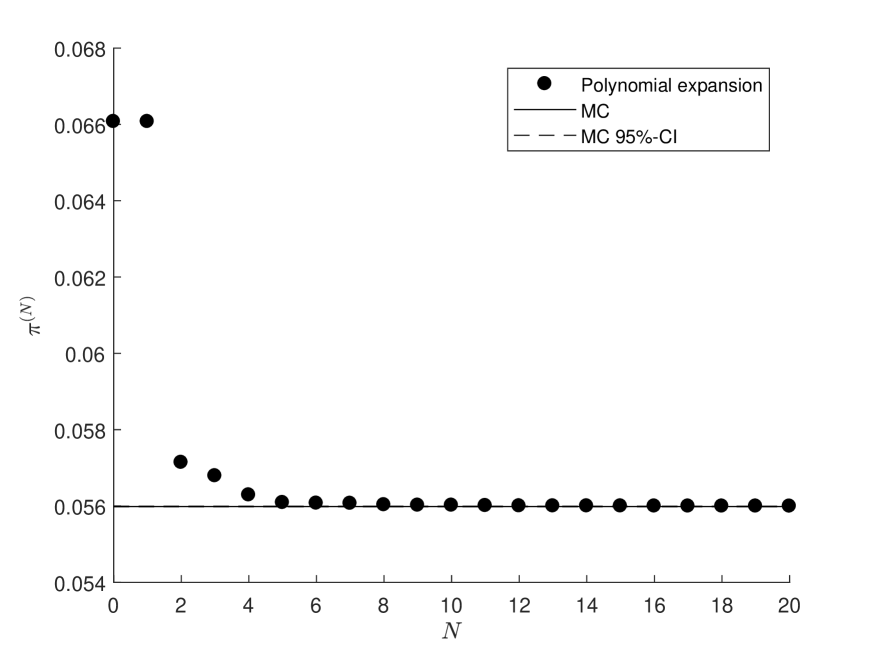

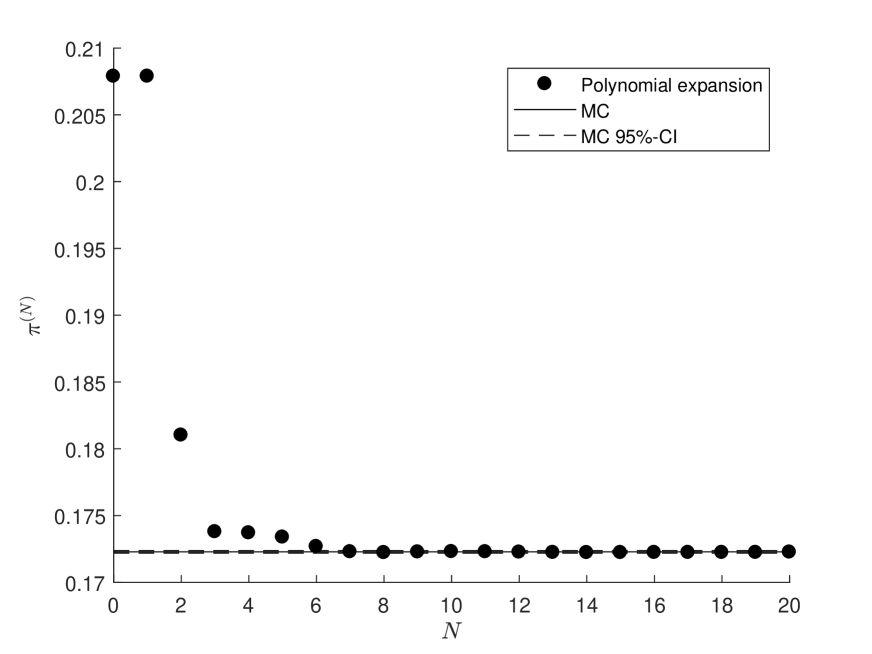

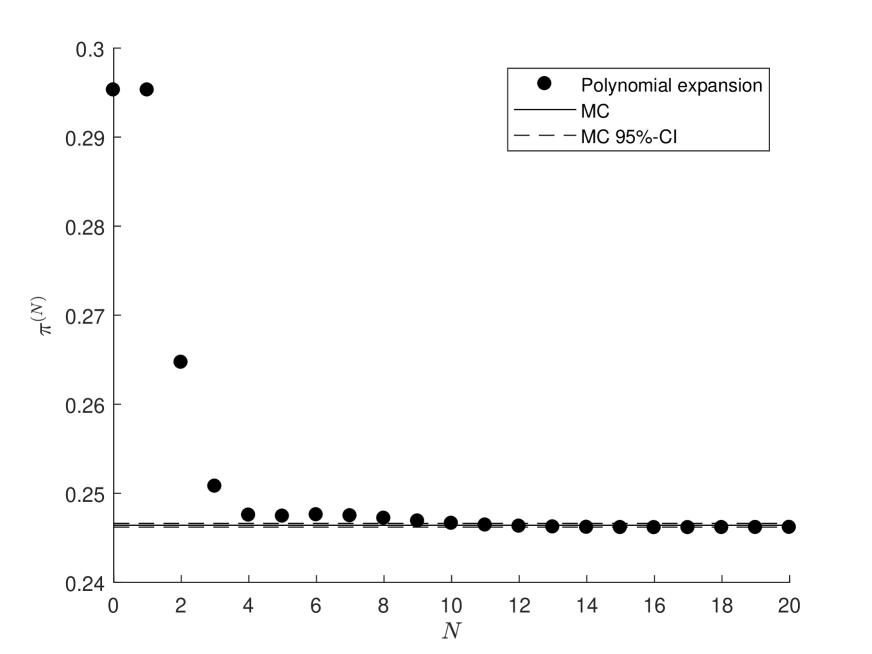

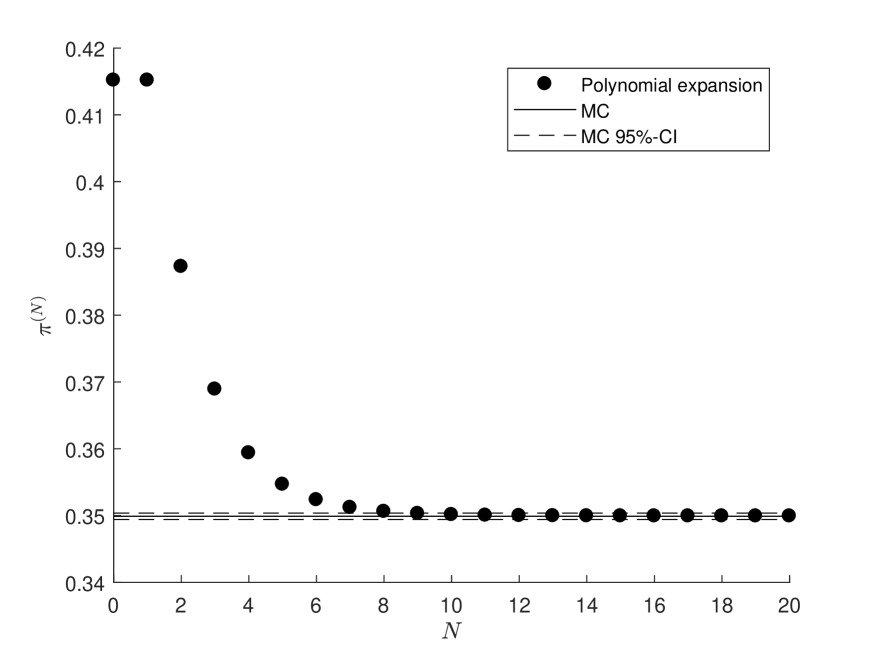

[Figure 1 around here]

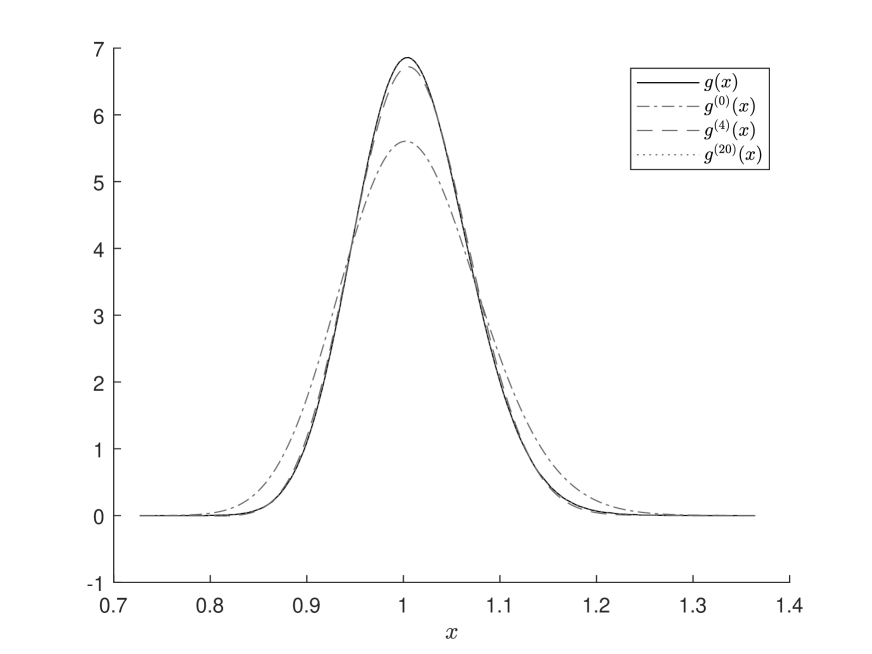

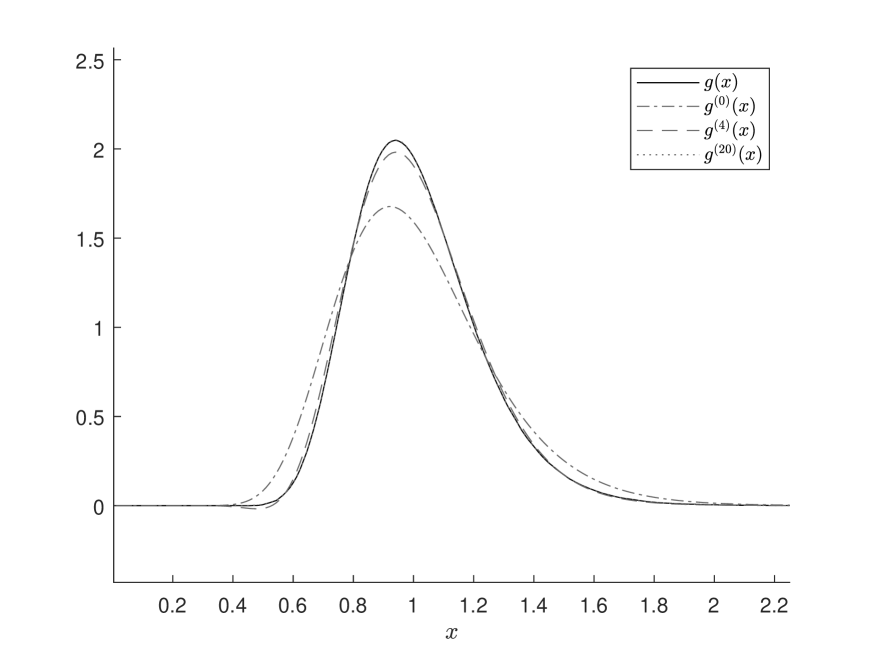

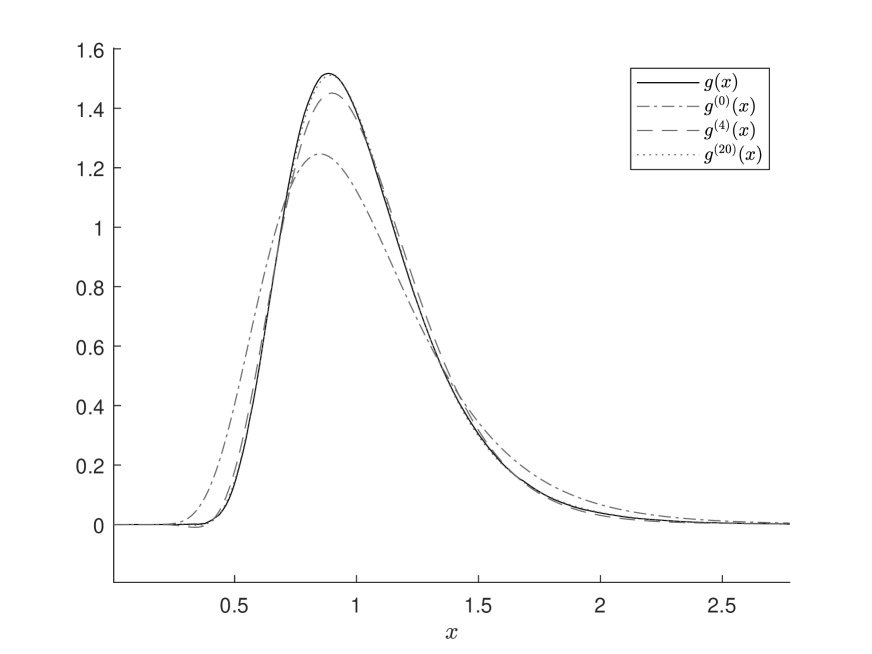

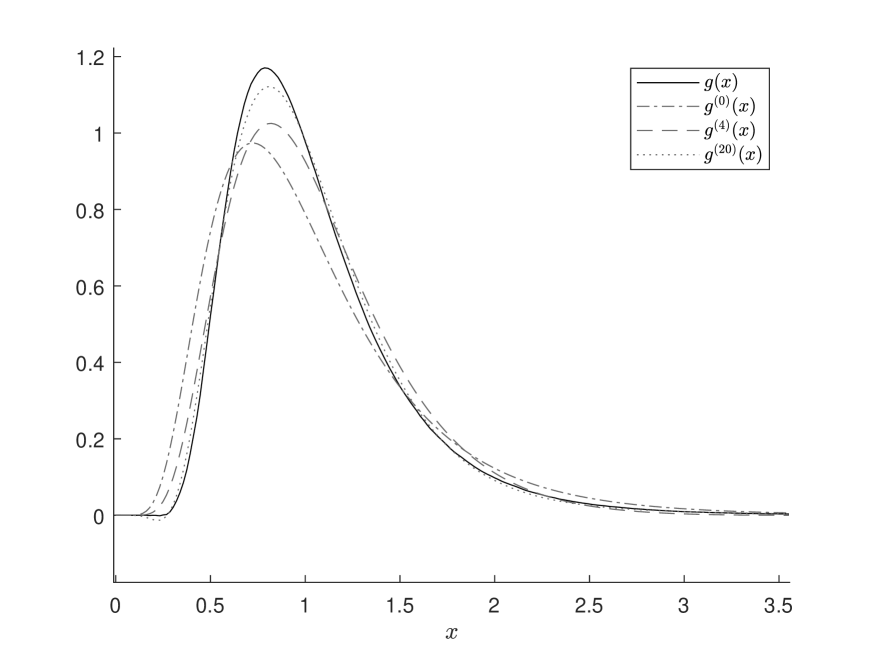

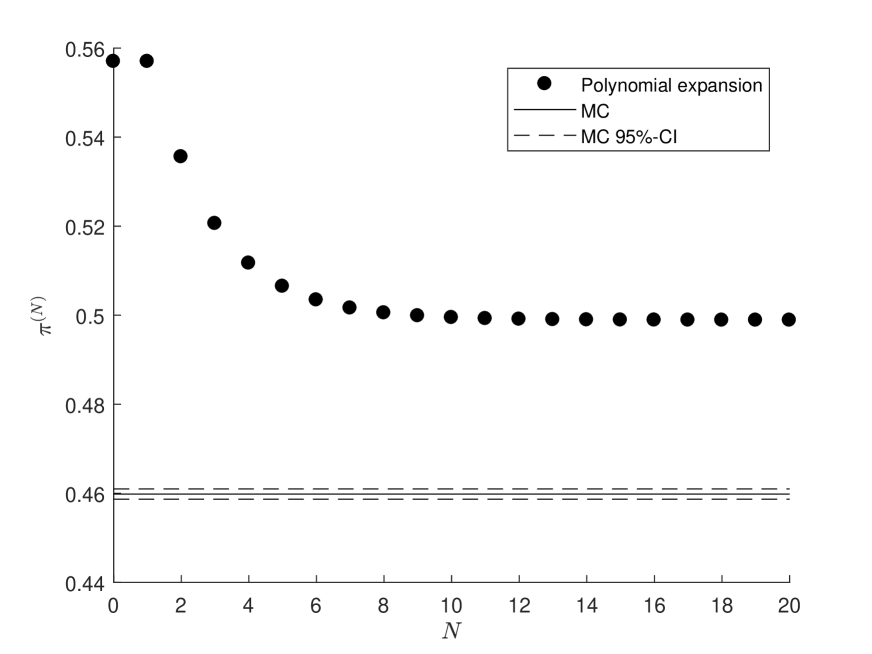

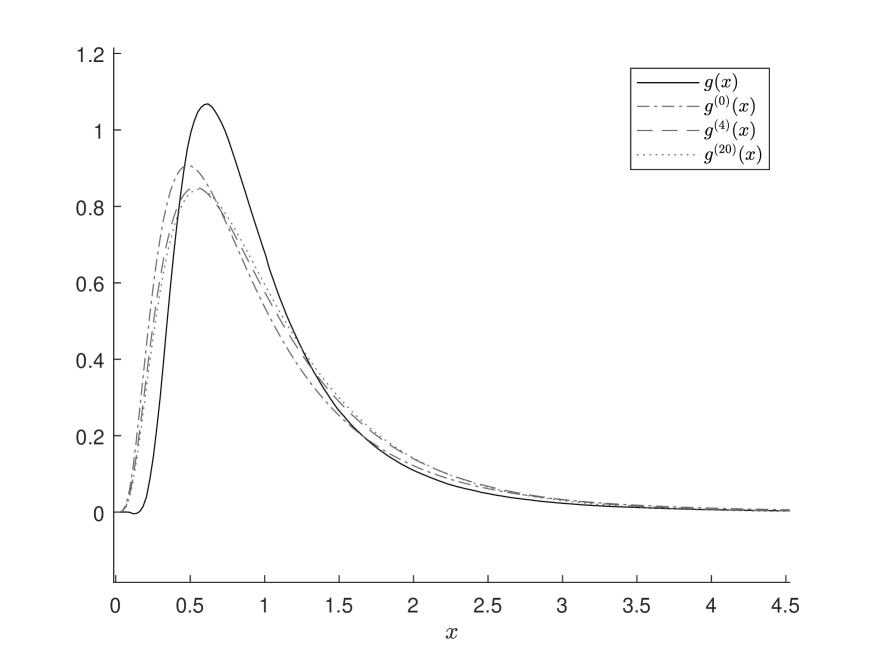

Figure 1 plots the LNS price approximations for ranging from 0 to 20, together with the Monte-Carlo price and the corresponding 95% confidence intervals as a benchmark.555Figure 1 and 2 only show cases 1, 3, 5, and 7. The plots for the other cases look very similar and are available upon request. We observe that the series converges very fast in all cases. In fact, truncating the series at would give almost identical results. In theory, can be chosen arbitrarily large, however in finite precision arithmetic it is inevitable that rounding errors start playing a role at some point. Remark that the prices for and are identical, which is a consequence of the fact that the auxiliary distribution matches the first moment of . Figure 2 plots the simulated true density and the approximating densities , , and defined in (3.6). The true density was simulated using (B.2) in Appendix B, which is an extension of (4.1) using the density of the geometric average as a powerful control variate. Note that , since . We can see that the approximating densities approach the true density as we include more terms in the expansion. In Figure 2(a) and 2(b) the approximation is virtually indistinguishable from the true density. However, in Figure 2(c) and 2(d) there remains a noticeable difference between and . This is consistent with the pricing errors we observed earlier in Table 1.

[Figure 2 around here]

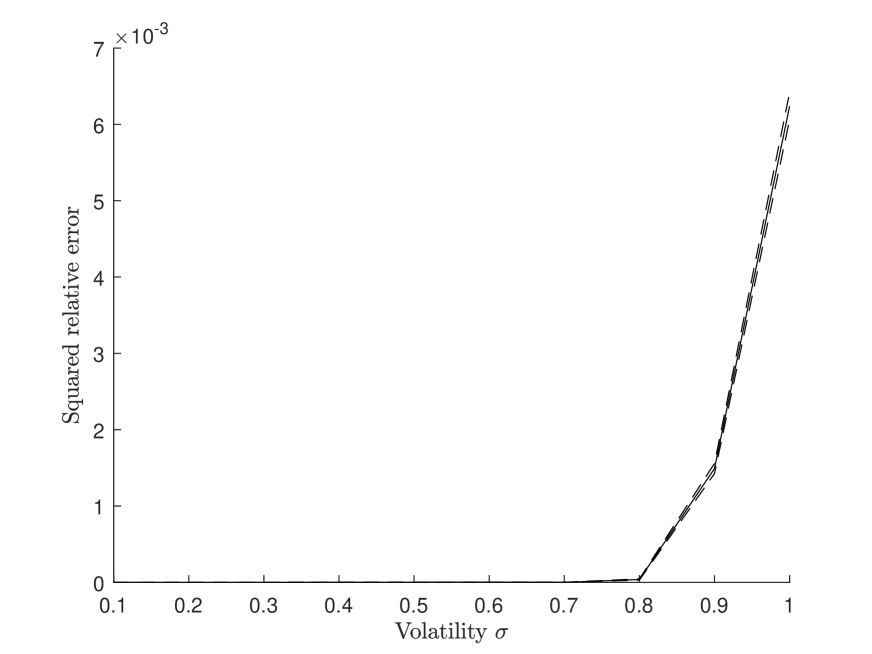

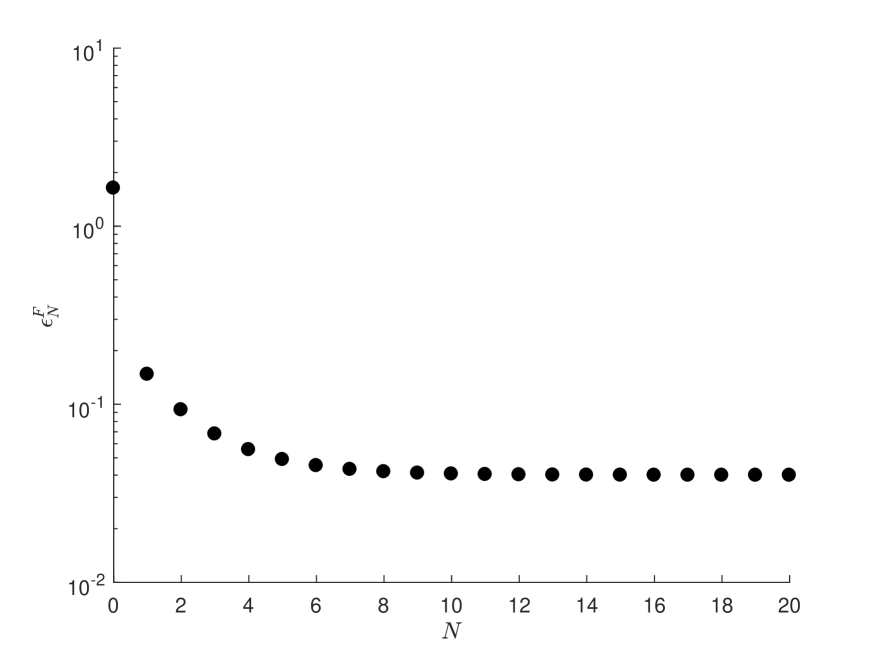

The above results indicate that for not too high, the LNS provides a very accurate approximation of the option price. This is not entirely surprising since determines the volatility parameter of the auxiliary log-normal density , and hence how fast the tails of go to zero. Loosely speaking, when is small, projecting the payoff or likelihood ratio function on the set of polynomials in is almost like approximating a continuous function on a compact interval by polynomials. However, when becomes larger, the tails of decay slowly and it becomes increasingly difficult to approximate a function with a polynomial in . In other words, for larger values of , the moment indeterminacy of the log-normal distribution starts playing a more prominent role. A natural question is therefore whether this poses a problem for option pricing purposes. In Figure 3(a) we fix and plot for a range of values for the squared relative error

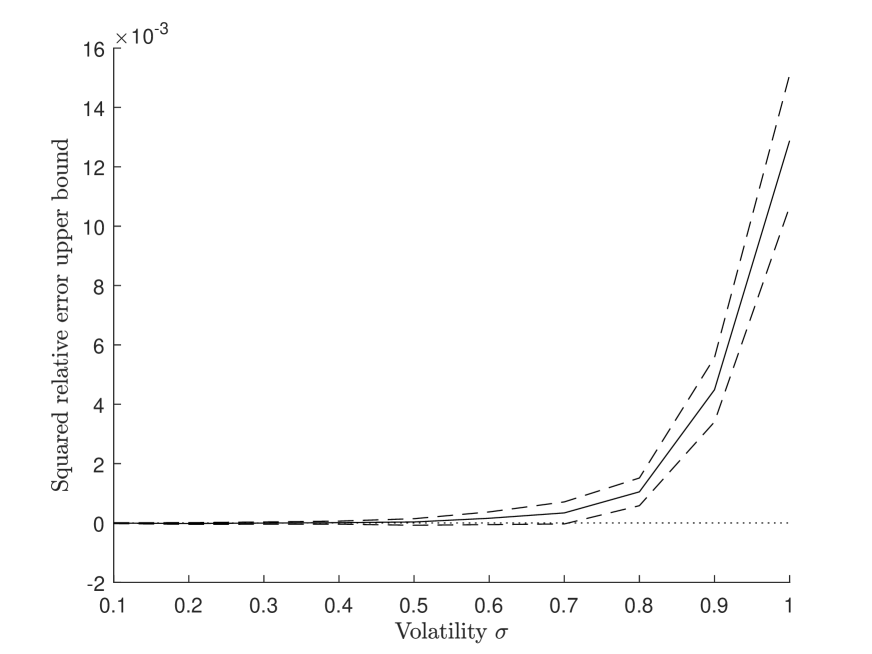

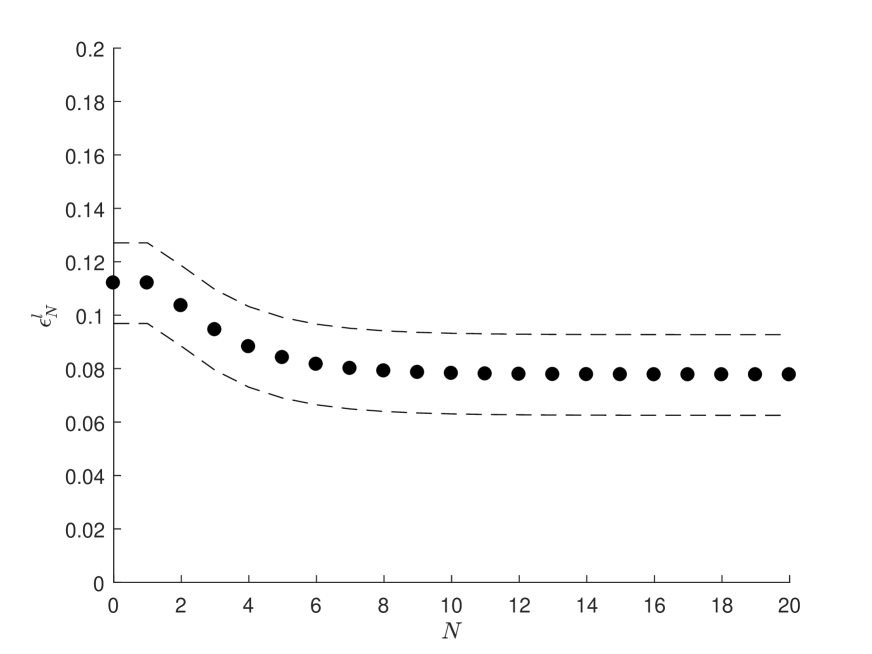

where denotes the Monte-Carlo price estimate. The error starts to becomes noticeable around , where . For higher values of the error increases sharply. In Figure 3(b) we plot a more conservative estimate of the squared relative error using the upper bound in (4.2). This plot shows that the upper bound is only significantly different from zero for larger than approximately . Figure 4 gives a more detailed insight in the extreme case of . Although the LNS series converges relatively fast, it is clear from Figure 4(a) that it does not converge to the true price. The reason, as already mentioned before, is that the payoff and likelihood ratio functions are not accurately approximated by polynomials in the -norm, as indicated by the projection errors in Figure 4(c) and 4(d). We would obtain similar results by keeping fixed and varying the maturity , since the crucial parameter for the asymptotic pricing error is . As a rule of thumb, we suggest to use the LNS method when .

The main advantage of the method proposed in this paper is the ease of of its implementation and the computation speed. All terms in the series are fully explicit and involve only simple linear algebra operations. Table 2 shows the computation times of the LNS with , as well as the computation times of the benchmark methods.666For the LS, all symbolic calculations related to the moments of the reciprocal of the average have been pre-computed using Matlab’s Symbolic Math Toolbox. We use 15+1 terms in the series, a higher number of terms leads to severe rounding problems in double precision arithmetic. For the EE, the integral representation (16) in Linetsky (2004) has been implemented instead of the series representation (15). The implementation of the series representation involves partial derivatives of the Whittaker function with respect to its indices. These derivatives are not available in Matlab’s Symbolic Math Toolbox and numerical finite difference approximations did not give accurate results. All numerical integrations are performed using Matlab’s built-in function integral. For case 1, the numerical integration in the EE did not finish in a reasonable amount of time. For the VEC method, we use Prof. Jan Vecer’s Matlab implementation, which can be downloaded at http://www.stat.columbia.edu/~vecer/asiancontinuous.m. All computations are performed on a desktop computer with an Intel Xeon 3.50GHz CPU. The LNS computation times are all in the order of miliseconds. Although the EE is very accurate, it comes at the cost of long computation times (in the order of several seconds) caused by the expensive evaluations of the Whittaker function. The LS does not require calls to special functions, however the method is slowed down by the numerical integration involved in computing the moments of the reciprocal of the average. The implementation of both the EE and LS require the use of software that can handle symbolic mathematics, in contrast to the implementation of the LNS. The VEC method is the fastest among the benchmarks considered in this paper, but still an order of magnitude slower than the LNS.

[Table 2 around here]

6 Conclusion

We have presented a series expansion for the continuously sampled arithmetic Asian option using polynomials that are orthogonal with respect to the log-normal distribution. The terms in the series are fully explicit and do not require any numerical integration or special functions, which makes the method very fast. We have shown that the series does not diverge if the volatility of the auxiliary log-normal distribution is sufficiently high. However, the series is not guaranteed to converge to the true price. We have investigated this asymptotic bias numerically and found that its magnitude is related to the size of .

There are several extensions to our method. First of all, we can handle discretely monitored Asian options using exactly the same setup, but replacing the moments of the continuous average with those of the discrete average. The latter are easily computed using iterated expectations. Secondly, we only look at fixed-strike Asian options in this paper. Since the process is jointly a polynomial diffusion, we can compute all of its mixed moments. Our method can then be extended to price floating-strike Asian options by using a bivariate log-normal as auxiliary distribution. Finally, we can define the auxiliary density as a mixture of log-normal densities, as studied in Ackerer and Filipović (2017). Using a mixture allows to match higher order moments, which can lead to a faster convergence of the approximating series.

References

- Ackerer and Filipović (2017) Ackerer, D. and D. Filipović (2017). Option pricing with orthogonal polynomial expansions. Working paper.

- Ackerer et al. (2017) Ackerer, D., D. Filipović, and S. Pulido (2017). The Jacobi stochastic volatility model. Finance and Stochastics, 1–34.

- Al-Mohy and Higham (2011) Al-Mohy, A. H. and N. J. Higham (2011). Computing the action of the matrix exponential, with an application to exponential integrators. SIAM Journal on Scientific Computing 33(2), 488–511.

- Aprahamian and Maddah (2015) Aprahamian, H. and B. Maddah (2015). Pricing Asian options via compound gamma and orthogonal polynomials. Applied Mathematics and Computation 264, 21–43.

- Asmussen et al. (2016) Asmussen, S., P.-O. Goffard, and P. J. Laub (2016). Orthonormal polynomial expansions and lognormal sum densities. arXiv preprint arXiv:1601.01763.

- Bally (2003) Bally, V. (2003). An elementary introduction to Malliavin calculus. Ph. D. thesis, INRIA.

- Benhamou (2002) Benhamou, E. (2002). Fast Fourier transform for discrete Asian options. Journal of Computational Finance 6(1), 49–68.

- Björck and Pereyra (1970) Björck, k. and V. Pereyra (1970). Solution of Vandermonde systems of equations. Mathematics of Computation 24(112), 893–903.

- Black and Scholes (1973) Black, F. and M. Scholes (1973). The pricing of options and corporate liabilities. Journal of Political Economy 81(3), 637–654.

- Caliari et al. (2014) Caliari, M., P. Kandolf, A. Ostermann, and S. Rainer (2014). Comparison of software for computing the action of the matrix exponential. BIT Numerical Mathematics 54(1), 113–128.

- Carmona et al. (1997) Carmona, P., F. Petit, and M. Yor (1997). On the distribution and asymptotic results for exponential functionals of Lévy processes. Exponential functionals and principal values related to Brownian motion, 73–121.

- Carverhill and Clewlow (1990) Carverhill, A. and L. Clewlow (1990). Valuing average rate (Asian) options. Risk 3(4), 25–29.

- Černỳ and Kyriakou (2011) Černỳ, A. and I. Kyriakou (2011). An improved convolution algorithm for discretely sampled Asian options. Quantitative Finance 11(3), 381–389.

- Curran (1994) Curran, M. (1994). Valuing Asian and portfolio options by conditioning on the geometric mean price. Management science 40(12), 1705–1711.

- Donati-Martin et al. (2001) Donati-Martin, C., R. Ghomrasni, and M. Yor (2001). On certain Markov processes attached to exponential functionals of Brownian motion; applications to Asian options. Revista Matematica Iberoamericana 17(1), 179.

- Dufresne (1990) Dufresne, D. (1990). The distribution of a perpetuity, with applications to risk theory and pension funding. Scandinavian Actuarial Journal 1990(1), 39–79.

- Dufresne (2000) Dufresne, D. (2000). Laguerre series for Asian and other options. Mathematical Finance 10(4), 407–428.

- Eydeland and Geman (1995) Eydeland, A. and H. Geman (1995). Domino effect: Inverting the Laplace transform. Risk 8(4), 65–67.

- Filipović and Larsson (2016) Filipović, D. and M. Larsson (2016). Polynomial diffusions and applications in finance. Finance and Stochastics 20(4), 931–972.

- Filipović et al. (2013) Filipović, D., E. Mayerhofer, and P. Schneider (2013). Density approximations for multivariate affine jump-diffusion processes. Journal of Econometrics 176(2), 93–111.

- Fournié et al. (1999) Fournié, E., J.-M. Lasry, J. Lebuchoux, P.-L. Lions, and N. Touzi (1999). Applications of Malliavin calculus to Monte Carlo methods in finance. Finance and Stochastics 3(4), 391–412.

- Fu et al. (1999) Fu, M. C., D. B. Madan, and T. Wang (1999). Pricing continuous Asian options: a comparison of Monte Carlo and Laplace transform inversion methods. Journal of Computational Finance 2(2), 49–74.

- Fusai et al. (2011) Fusai, G., D. Marazzina, and M. Marena (2011). Pricing discretely monitored asian options by maturity randomization. SIAM Journal on Financial Mathematics 2(1), 383–403.

- Fusai and Meucci (2008) Fusai, G. and A. Meucci (2008). Pricing discretely monitored Asian options under Lévy processes. Journal of Banking & Finance 32(10), 2076–2088.

- Gautschi (2004) Gautschi, W. (2004). Orthogonal Polynomials: Computation and Approximation. Oxford University Press.

- Geman and Yor (1993) Geman, H. and M. Yor (1993). Bessel processes, Asian options, and perpetuities. Mathematical Finance 3(4), 349–375.

- Heyde (1963) Heyde, C. (1963). On a property of the lognormal distribution. In Selected Works of CC Heyde. Springer Science & Business Media.

- Jarrow and Rudd (1982) Jarrow, R. and A. Rudd (1982). Approximate option valuation for arbitrary stochastic processes. Journal of Financial Economics 10(3), 347–369.

- Ju (2002) Ju, N. (2002). Pricing Asian and basket options via Taylor expansion. Journal of Computational Finance 5(3), 79–103.

- Kemna and Vorst (1990) Kemna, A. G. and A. Vorst (1990). A pricing method for options based on average asset values. Journal of Banking & Finance 14(1), 113–129.

- Lapeyre et al. (2001) Lapeyre, B., E. Temam, et al. (2001). Competitive Monte Carlo methods for the pricing of Asian options. Journal of Computational Finance 5(1), 39–58.

- Levy (1992) Levy, E. (1992). Pricing European average rate currency options. Journal of International Money and Finance 11(5), 474–491.

- Li and Chen (2016) Li, W. and S. Chen (2016). Pricing and hedging of arithmetic Asian options via the Edgeworth series expansion approach. The Journal of Finance and Data Science 2(1), 1–25.

- Linetsky (2004) Linetsky, V. (2004). Spectral expansions for Asian (average price) options. Operations Research 52(6), 856–867.

- Marcozzi (2003) Marcozzi, M. D. (2003). On the valuation of Asian options by variational methods. SIAM Journal on Scientific Computing 24(4), 1124–1140.

- Milevsky and Posner (1998) Milevsky, M. A. and S. E. Posner (1998). Asian options, the sum of lognormals, and the reciprocal gamma distribution. Journal of Financial and Quantitative Analysis 33(3), 409–422.

- Nualart (2006) Nualart, D. (2006). The Malliavin Calculus and Related Topics. Springer.

- Ritchken et al. (1993) Ritchken, P., L. Sankarasubramanian, and A. M. Vijh (1993). The valuation of path dependent contracts on the average. Management Science 39(10), 1202–1213.

- Rogers and Shi (1995) Rogers, L. C. G. and Z. Shi (1995). The value of an Asian option. Journal of Applied Probability 32(4), 1077–1088.

- Shaw (2002) Shaw, W. (2002). Pricing Asian options by contour integration, including asymptotic methods for low volatility. Working paper.

- Sun et al. (2013) Sun, J., L. Chen, and S. Li (2013). A quasi-analytical pricing model for arithmetic Asian options. Journal of Futures Markets 33(12), 1143–1166.

- Thompson (2002) Thompson, G. (2002). Fast narrow bounds on the value of Asian options. Technical report, Judge Institute of Management Studies.

- Turnbull and Wakeman (1991) Turnbull, S. M. and L. M. Wakeman (1991). A quick algorithm for pricing European average options. Journal of Financial and Quantitative Analysis 26(3), 377–389.

- Turner (1966) Turner, L. R. (1966). Inverse of the Vandermonde matrix with applications.

- Vanmaele et al. (2006) Vanmaele, M., G. Deelstra, J. Liinev, J. Dhaene, and M. J. Goovaerts (2006). Bounds for the price of discrete arithmetic Asian options. Journal of Computational and Applied Mathematics 185(1), 51–90.

- Vecer (2001) Vecer, J. (2001). A new PDE approach for pricing arithmetic average Asian options. Journal of Computational Finance 4(4), 105–113.

- Vecer (2002) Vecer, J. (2002). Unified pricing of Asian options. Risk 15(6), 113–116.

- Yor (1992) Yor, M. (1992). On some exponential functionals of Brownian motion. Advances in Applied Probability 24(3), 509–531.

- Zvan et al. (1996) Zvan, R., P. A. Forsyth, and K. R. Vetzal (1996). Robust numerical methods for PDE models of Asian options. Technical report, University of Waterloo, Faculty of Mathematics.

Appendix A Scaling with auxiliary moments

In this appendix we show how to avoid rounding errors by scaling the problem using the moments of the auxiliary density .

Using we get from (3.4):

Define as the diagonal matrix with the moments of on its diagonal:

We can now write

| (A.1) |

where we have defined the matrices , and the vector as

for . The components of and grow much slower for increasing as their counterparts and , respectively. The vector corresponds to the moments of divided by the moments corresponding to . Since both moments grow approximately at the same rate, this vector will have components around one. This scaling is important since for large the raw moments of are enormous. This was causing trouble for example in Dufresne (2000). We therefore circumvent the numerical inaccuracies coming from the explosive moment behavior by directly computing the relative moments.

The likelihood and payoff coefficients can be computed by performing a Cholesky decomposition on instead of :

where is the Cholesky decomposition of .

Remark that to compute the option price in (A.1), we do not necessarily need to do a Cholesky decomposition. Indeed, we only need to invert the matrix . Doing a Cholesky decomposition is one way to solve a linear system, but there are other possibilities. In particular, remark that is a Vandermonde matrix and its inverse can be computed analytically (see e.g. Turner (1966)). There also exist specific numerical methods to solve linear Vandermonde systems, see e.g. Björck and Pereyra (1970). However, we have not found any significant differences between the Cholesky method and alternative matrix inversion techniques for the examples considered in this paper.

For very large values of , even the matrix might become ill conditioned. In this case it is advisable to construct the orthonormal basis using the three-term recurrence relation:

Lemma A.1.

The polynomials , , defined recursively by

with

satisfy

Proof.

Straightforward application of the moment-generating function of the normal distribution and Theorem 1.29 in Gautschi (2004). ∎

The above recursion suffers from rounding errors in double precision arithmetic for small , but is very accurate for large .

Appendix B Control variate for simulating

In order to increase the efficiency of the Monte-Carlo simulation of , we describe in this appendix how to use the density of the geometric average as a control variate. This idea is inspired by Kemna and Vorst (1990), who report a very substantial variance reduction when using the geometric Asian option price as a control variate in the simulation of the arithmetic Asian option price. Denote by the geometrical price average. It is not difficult to see that is normally distributed with mean and variance . Hence, is log-normally distributed and we know its density function, which we denote by , explicitly. Similarly as in Lemma 4.1, we can also express as an expectation:

Lemma B.1.

For any

| (B.1) |

where is any deterministic finite-valued function.

We now propose the following estimator for the density of the arithmetic average:

| (B.2) |

for some deterministic finite-valued functions and . Given the typically high correlation between the geometric and arithmetic average, the above estimator has a significantly smaller variance than the estimator in (4.1). In numerical examples the functions and are chosen as follows:

where and denote the first moments of and , respectively.

Finally, we use (B.2) to express as an expectation that can be evaluated using Monte-Carlo simulation:

| (B.3) |

where the random variable is independent from all other random variables and has the same distribution as . In numerical examples we find a variance reduction of roughly a factor ten.

Appendix C Proofs

This appendix contains all the proofs.

C.1 Proof of Lemma 2.1

Using the time-reversal property of a Brownian motion, we have the following identity in law for fixed :

Applying Itô’s lemma to gives

C.2 Proof of Proposition 2.2

Applying the infinitesimal generator corresponding to the diffusion in (2.1) to a monomial gives:

Hence, we have componentwise, where is defined as

C.3 Proof of Proposition 2.3

-

1.

We will show that the solution at time of the SDE in (2.1) admits a smooth density function. The claim then follows by the identity in law.

Define the volatility and drift functions and . Hörmander’s condition (see for example Section 2.3.2 in Nualart (2006)) becomes in this case:

Hörmander’s condition is satisfied since for we have . Since and are infinitely differentiable functions with bounded partial derivatives of all orders, we conclude by Theorem 2.3.3 in Nualart (2006) that , and therefore , admits a smooth density function.

-

2.

We start from the following two observations:

where . Using the fact that the exponential is an increasing function, we get

Applying the rule of l’Hôpital gives

Hence we have show that for .

Since the exponential is a convex function, we have that the arithmetic average is always bounded below by the geometric average:

It is not difficult to see that is normally distributed with mean and variance . By similar arguments as before we therefore have

C.4 Proof of Proposition 3.1

We can write the squared norm of as

| (C.1) |

for some . The second term is finite since the function is continuous over the compact interval . From Proposition 2.3 we have

For the log-normal density we have

Since by assumption, we are guaranteed that the first and last term in (C.1) are finite for a sufficiently small (resp. large) choice of (resp. ).

C.5 Proof of Proposition 3.3

The payoff coefficients can be written as

with

Completing the square in the exponent gives

where is defined in (3.5). We finally get

C.6 Proof of Lemma 4.1

This proof is based on Malliavin calculus techniques, we refer to Nualart (2006) for an overview of standard results in this area. A similar approach is taken by Fournié et al. (1999) to compute the Greeks of an Asian option by Monte-Carlo simulation.

Denote by , the Malliavin derivative operator. By Theorem 2.2.1 in (Nualart, 2006) we have for and

Denote by

the Skorohod integral and by the corresponding domain. The Skorohod integral is defined as the adjoint operator of the Malliavin derivative and can be shown to extend the Itô integral to non-adapted processes. In particular, we have immediately that and

| (C.2) |

For we have and

Using the duality relationship between the Skorohod integral and the Malliavin derivative we get

| (C.3) |

By Lemma 1 in Bally (2003) (see also Proposition 2.1.1 in Nualart (2006) for a similar approach) we obtain the following representation of the density function of :777Informally speaking one applies a regularization argument in order to use (C.3) for the (shifted) Heaviside function .

| (C.4) |

Interchanging the order of integration gives

which gives Plugging this into (C.4) gives

We use Proposition 1.3.3 in Nualart (2006) to factor out the random variable from the Skorohod integral:

where we used (C.2) in the last equation. Using the chain rule for the Malliavin derivative we get

Putting everything back together we finally get:

Since the Skorohod integral has zero expectation we also have

for any deterministic finite-valued function .

C.7 Proof of Corollary 4.3

The result follows immediately from (4.1) and

C.8 Proof of Proposition 4.4

Using the Cauchy-Schwarz inequality and the orthonormality of the polynomials we get

C.9 Proof of Lemma B.1

Applying the Malliavin derivative to gives

Similarly as in the proof of Lemma 4.1 we can write

| (C.5) |

Using Proposition 1.3.3 in Nualart (2006) to factor out the random variable from the Skorohod integral gives

Plugging this back into (C.5) finally gives

Since the Skorohod integral has zero expectation we also have

for any deterministic finite-valued function .

| Case | LNS10 | LNS15 | LNS20 | LS | EE | VEC | MC 95% CI | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | .02 | .10 | 1 | 2.0 | .05601 | .05600 | .05599 | .0197 | .05599 | .05595 | [.05598 | , | .05599] |

| 2 | .18 | .30 | 1 | 2.0 | .2185 | .2184 | .2184 | .2184 | .2184 | .2184 | [.2183 | , | .2185] |

| 3 | .0125 | .25 | 2 | 2.0 | .1723 | .1722 | .1722 | .1723 | .1723 | .1723 | [.1722 | , | .1724] |

| 4 | .05 | .50 | 1 | 1.9 | .1930 | .1927 | .1928 | .1932 | .1932 | .1932 | [.1929 | , | .1933] |

| 5 | .05 | .50 | 1 | 2.0 | .2466 | .2461 | .2461 | .2464 | .2464 | .2464 | [.2461 | , | .2466] |

| 6 | .05 | .50 | 1 | 2.1 | .3068 | .3062 | .3061 | .3062 | .3062 | .3062 | [.3060 | , | .3065] |

| 7 | .05 | .50 | 2 | 2.0 | .3501 | .3499 | .3499 | .3501 | .3501 | .3500 | [.3494 | , | .3504] |

| Case | LNS10 | LNS15 | LNS20 | LS | EE | VEC | MC | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | .02 | .10 | 1 | 2.0 | .006 | .008 | .009 | .930 | - | .277 | 6.344 |

| 2 | .18 | .30 | 1 | 2.0 | .002 | .002 | .003 | .666 | 2.901 | .345 | 5.518 |

| 3 | .0125 | .25 | 2 | 2.0 | .002 | .002 | .002 | .635 | 3.505 | .374 | 12.138 |

| 4 | .05 | .50 | 1 | 1.9 | .001 | .002 | .003 | .785 | 3.172 | .404 | 6.819 |

| 5 | .05 | .50 | 1 | 2.0 | .001 | .002 | .002 | .701 | 2.768 | .404 | 5.432 |

| 6 | .05 | .50 | 1 | 2.1 | .001 | .001 | .002 | .687 | 2.719 | .398 | 5.452 |

| 7 | .05 | .50 | 2 | 2.0 | .002 | .002 | .004 | .594 | 2.202 | .438 | 11.699 |