Short- to Mid-term Day-Ahead Electricity Price Forecasting Using Futures

Abstract

Due to the liberalization of markets, the change in the energy mix and the surrounding energy laws, electricity research is a dynamically altering field with steadily changing challenges. One challenge especially for investment decisions is to provide reliable short to mid-term forecasts despite high variation in the time series of electricity prices. This paper tackles this issue in a promising and novel approach. By combining the precision of econometric autoregressive models in the short-run with the expectations of market participants reflected in future prices for the short- and mid-run we show that the forecasting performance can be vastly increased while maintaining hourly precision. We investigate the day-ahead electricity price of the EPEX Spot for Germany and Austria and setup a model which incorporates the Phelix future of the EEX for Germany and Austria. The model can be considered as an AR24-X model with one distinct model for each hour of the day. We are able to show that future data contains relevant price information for future time periods of the day-ahead electricity price. We show that relying only on deterministic external regressors can provide stability for forecast horizons of multiple weeks. By implementing a fast and efficient lasso estimation approach we demonstrate that our model can outperform several other models in the literature.

keywords:

Electricity price , Mid-term , Future Data , Forecasting , AR , Lasso1 Introduction

Modeling and forecasting electricity prices have become an important and broad part of economic research during the last decades. The specifics of electricity prices, also known as stylized facts as well as the due to new laws rapidly changing market conditions especially in Europe and Germany have promoted this development. Moreover, the data transparency has tremendously increased during the last years, either by law or by negotiated agreement data for e.g. electricity consumption, production, prices and even planned capacities can be downloaded via different sources like ENTSO-E or the exchanges themselves. The electricity exchanges also expanded their product portfolio by launching new electricity related products like new block products, derivatives or complete new spot auctions as e.g. the EXAA GreenPower auction. Even though these changes will provide the informed decision maker with more valid options, it also increases the complexity of the decision making process.

One of the research approaches which tries to incorporate the changing market conditions is the econometric perspective, which in general constructs models which aim to capture the underlying behavior of the electricity price time series and can provide forecasts afterwards. These forecasts can help market participants in their decision making for e.g. investment decisions. Moreover, forecasts offer different utility dependent on their forecasting horizon. Forecasts of only a few days in advance can help electricity companies to adjust their production planning. For instance, if an owner of a pumped-storage hydroelectricity plant has information on extremely low prices in the future they can easily schedule their generation of electricity by releasing their water reservoir now and refill it later when the electricity price is low. Medium- or long-term forecasts can help market participants to identify investment opportunities in the long-run, e.g. when the decision of the construction of a new wind power plant is considered, as they need to have reliable information on future cash-flows for their product. This is especially important in Germany, as the market premium which producers of renewable energy receive is calculated according to the attachment 1 of §23a EEG (“Erneuerbare-Energien-Gesetz”) by using, among others, the average monthly spot prices of the EPEX SE.

Econometric models usually use the intertemporal correlation structure of day-ahead electricity prices and combine them with external fundamental or stylized facts related regressors to provide good forecasts , see for instance Weron, (2014) for an extensive review of different models . However, these models usually struggle when it comes to mid- or even long-term horizon forecasting. The reason for that is mainly, that every non-deterministic regressor like electricity load, wind- and solar power production, water reservoir levels or fuel prices have to be forecasted as well. This means that the forecaster has not only the task to come up with a good model for the electricity price but also for the regressors, even though both time series may come from very different disciplines of research. Moreover, due to their autoregressive structure every error in forecasting of one of the series will have an impact on any consecutive forecasting time point, depending on the magnitude of the intertemporal correlation of the time series itself and especially the residuals. Some authors therefore try to either use already forecasted regressors or only lags of external regressors (e.g. Bunn et al., (2016) or Hagfors et al., (2016)). This in turn leads to a situation where the forecasting horizon is restricted to the lowest used lag of the external regressors. When the day-ahead price of electricity is concerned, this means that due to the usual hourly resolution, forecasting e.g. four weeks leads to points in time which have to be forecasted. Simple autoregressive models also converge quickly to their mean, which make them incapable of forecasting longer forecasting horizons (Keles et al., , 2012).

Therefore, we want to setup a model, which is capable of generating reliable short to mid-term forecasts of up to four weeks by using regressors, which provide a preferably long deterministic structure, which means that we do not have to forecast them for as long as possible. For this we have decided to use the EPEX day-ahead electricity spot price of Germany and Austria and combine it with the EEX Phelix futures which have a cash settlement based on the average EPEX spot price for different time horizons. As the literature is not consentaneous on the distinction between short-term, mid-term and long-term, we decided to declare the forecasting horizon we use as short- to mid-term. Our forecasting horizon comprises 1 to 28 days. In the next paragraphs, whenever we list a paper according to their forecasting horizon, we follow their own definition of the term.

The literature on mid- to long-term electricity price forecasting is very scarce (Yan and Chowdhury, , 2013). This holds especially true for econometric modeling. Maciejowska and Weron, (2016) for instance utilize an autoregressive modeling approach to forecast the UK electricity price for up to 45 days. The authors compare the difference in forecasting accuracy of, among others, AR-models with hourly precision and AR-models which only use the daily average. They find that in the mid-term simpler models without hourly resolution seem to be superior against more complex models which keep the complex hourly structure, while in the short-term this the relation is the other way round. Moreover, they also find that including regressors did not always lead to better forecasts, the inclusion of prices for instance weakened the accuracy in general due to problems with forecasting this time series.

In the study of Ziel and Steinert, (2017) the authors apply an econometric autoregressive approach towards the sale and purchase curves of the EPEX day-ahead electricity price. By a simulation study they can replicate the market situation and provide mid- to long-term probabilistic forecasts for the electricity price as well as all other related components . For their study they use the auction bids as well as external regressors like wind and solar power. By evaluating coverage probabilities they are able to compare their probabilistic forecasting values with the real electricity price time series and state that given the long horizon the models tends to have promising results.

Other approaches for mid- and long-term forecasting originate from other fields of electricity price research, e.g. heuristics as in Yan and Chowdhury, (2015) or fundamental models like in Bello et al., (2016, 2017).

Nevertheless the relationship between spot and future products is an extensive field of research in finance and in energy economics as well. However, the typical relationship of futures can be described by the difference in expectation about spot prices and the price of a future, which in commodities research is due to the participants necessity of getting a premium for storing a specific asset(Weron and Zator, , 2014). But as electricity prices cannot be stored easily, this relationship tends to be more complex. The basic relationship is typically described as follows: (see e.g. Benth et al., (2008))

| (1) |

where is the expected electricity price of delivery period based on the information set at time for . represents the before mentioned risk premium and the price of the future in for period with the electricity price as underlying. Usually the delivery period is an interval with . However, in practice futures are often quoted with a corresponding maturity. For instance, the Phelix Day Base Future with maturity 2 refers to a delivery period of all 24 hours of the day starting with the first hour of the day 2 days after the product was traded. This is known as Musiela parameterization (Musiela, , 1993) and formally describes a future product as the price of the future product in , with the corresponding delivery period starting in . Thus it holds for the time to maturity that . If the delivery period is an interval , then we have with . In the modeling section we consider the Musiela parametrization as well, as was also done for instance in Barndorff-Nielsen et al., (2014), Carmona and Coulon, (2014) or Benth and Paraschiv, (2017).

To display the direct relationship of future products to expected prices, it helps to rearrange equation (1) to :

| (2) |

It can be seen that there is a direct theoretical link between the expectation for electricity prices in the future, which can be e.g. generated by econometric modeling, and the price of the corresponding future product. Assuming that the risk premium is 0, we could easily obtain future electricity prices by taking a look at the future products. However, several authors have found various results concerning the risk premium, usually stating that there is a negative or positive risk premium present, usually determined by a complex set of variables see e.g. Redl and Bunn, (2013) or Aoude et al., (2016). Given historical information on day-ahead electricity prices and futures as well as other relevant information concerning the risk premia it is possible to construct and forecast the hourly price forward curve. This was done with real data for the German and Austrian electricity market for instance by Caldana et al., (2017). Even though the authors had to forecast electricity spot prices as well, the focus of their study was to get realistic approximations for the hourly price forward curve. Paraschiv et al., (2015) utilized the estimated hourly price forward curves to simulate realistic hourly day-ahead spot price behavior for the German/Austrian market. They also conduct a forecasting study with two different time points with two different forecasting horizons each. They show that their combined regime-switching approach yielded better results than a combined ARIMA benchmark when the mean absolute percentage error (MAPE) is considered. Due to the nature of their approach and the fact that they have a similar forecasting horizon as we do, we will compare our models later on in detail. However, our model will differ in the sense that we focus on capturing the day-ahead price movements only by using the observable historic futures, for which we do not necessarily need the full hourly price forward curve. Nevertheless, the possible dependency of day-ahead electricity prices on future products is rather complex and needs a specific modeling approach.

We will therefore setup a model which will use future products observable at a time point to forecast hourly day-ahead prices of up to four weeks with an econometric modeling. Our model does not need to explicitly create hourly price forward curves but instead will model the impact of future product prices directly towards the day-ahead electricity prices. Together with additional known regressors like the weekday or the seasons of the year we make sure that every of our external regressors is deterministic throughout the whole forecasting period. Such an approach, which can capture the information of different future products, might therefore tackle the issue of stacking errors of forecasted regressors. From a finance perspective this coincides with simply utilizing the market expectations for futures to improve our forecasts. Assuming that we have a different and especially worse information set than active traders, e.g. about actual outages or maintenances of power plants, this is a promising approach to improve forecasts. Therefore, we structured our paper as follows. The next section will describe in detail how to merge both quite different market structures into one model. We will propose a model with an efficient estimation and regressor selection algorithm to gain high forecasting precision. In Section 3 we will execute a thorough forecasting study to analyze our findings minutely. The last section will conclude by summarizing our results and pointing out the drawbacks of our study as well as suggestions for future research.

2 Data and model setup

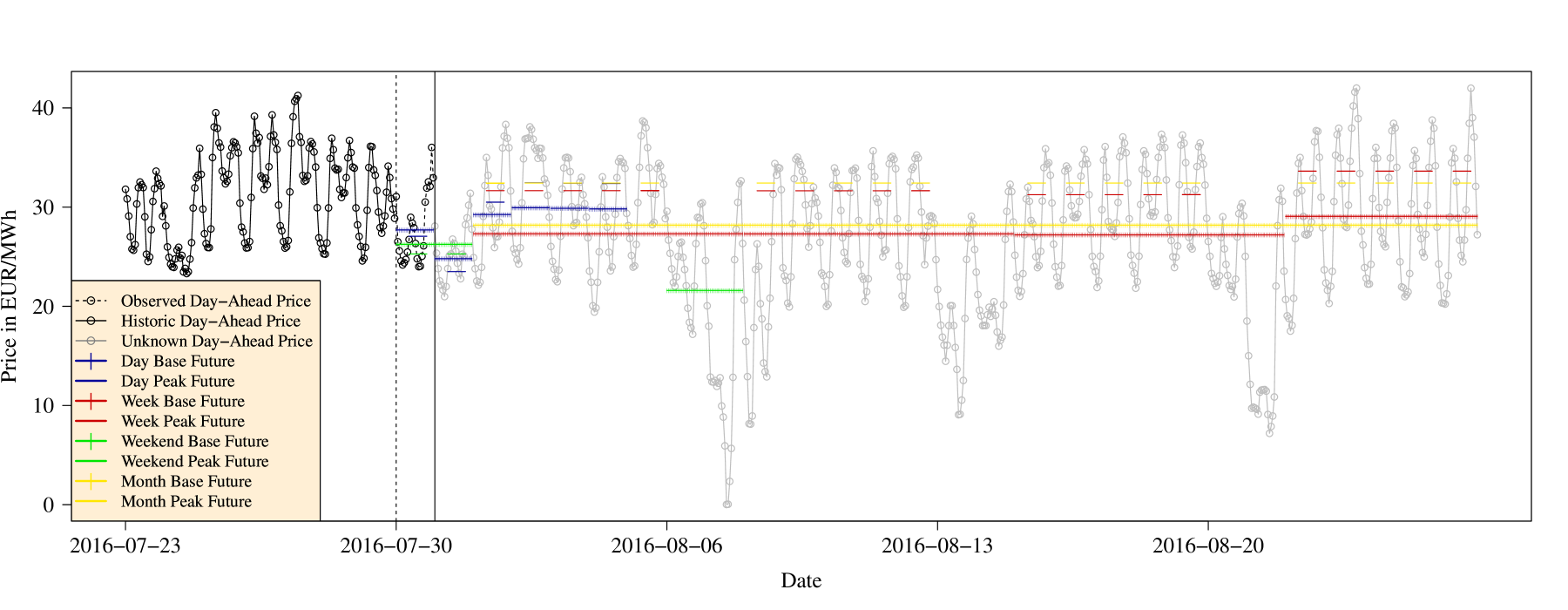

Figure 1 shows the complexity of the different future products and the day-ahead electricity price. We selected the future products, which we utilized in this paper and plotted their settlement price of the 29.07.2016 corresponding to the time frame they were traded for. For instance, as the 29.07.2016 was a Friday, the weekend base future with maturity one depicted as green line referred to the day-ahead electricity price of all hours of the weekend, e.g. the 30.07. and 31.07. The futures are based on end-of-day prices, meaning that because of the market structure of the spot products, the day-ahead electricity prices for the 30.07. were actually observable. This situation is depicted by the two different vertical lines . Based on the observable day-ahead prices, the traders had to determine prices for different future periods by making predictions for the future electricity price, which is depicted as grey line.

It can be easily seen that the traded future products of the 29.07. contained a great amount of information for the next several days, but due to week and month future also some information regarding the next four weeks. This is remarkable, as all this information is deterministic and therefore a model which incorporates futures as regressors would not have the need to forecast these regressors as well.

As mentioned in the previous section econometric models usually tend to have superior forecasting ability in the short-run with hourly precision, but struggle to make promising forecasts when forecasting horizons of weeks are considered. On the other hand future data provide deterministic long-term forecasts for horizons up to years but lack in accuracy when hourly or even to some extent even daily data is considered.

Hence, we are going to combine the precision of these econometric models with the power of the long-term price information of futures. We will setup an econometric model with a forecasting horizon of up to four weeks for the day-ahead electricity price of Germany and Austria while still preserving hourly precision.

Our model will therefore consist of three parts: the autoregressive time-series of day-ahead prices of the EPEX Spot for Germany and Austria, specifically selected future Phelix data for Germany and Austria provided by the EEX and day of the week dummy variables. Starting with the 01.05.2016 we will create a forecast for up to four weeks for every day of one year, which will result in 365 forecasts each with a time horizon of up to 28 days. Every day where an estimation and forecasting is done will only use observations from the previous 365 days, meaning that we will utilize a rolling window for the estimation.

We will use the EEX end-of-day data from the Phelix Base Day, Phelix Base Week, Phelix Base Weekend and Phelix Base Month products and their peak counterparts. We generally selected the different products and maturities to match our forecasting horizon. As second criterion we only incorporated products which were traded on business days for at least 75% of the time. This was used as some products, for instance the weekend peak future from maturity 8 to 12 seem to have very little trades during our investigated time period. Third, for products with more than 10 different traded maturities, we decided to investigate only the most up-to-date maturities for which the delivery period of the product corresponded to time of the day-ahead product. For instance, the month future for the next month has maturities from 3 to 31, but only the maturity 3 contains the most recent information about the price for the next month. A more detailed discussion of the update scheme will be provided after the model is fully introduced.

It is important to notice that these datasets only update once a day, as we use end-of-day data. Also the delivery period of these products are defined by their specific type, e.g. the Phelix Base Week will deliver 1 MW/h for every hour of the specified week for the traded price via cash settlement.

Another issue occurs when trading times are considered. The future products are traded from 08:00 to 18:00 but as we use the end-of-day data our datapoints will always represent the price of 18:00. The day-ahead auction for the spot closes 12:00 and sets the prices for the following day. Given that situation the day-ahead prices can only be dependent on the future end-of-day prices of two days before the day for which they were traded. Unlike the day-ahead electricity the future products are only traded on business days, so there is no price available on weekends or public holidays. However, our model accounts for all these facts. In the following description of the model parts we will mention the specific adjustments to overcome these issues.

The full model is defined as follows:

| (3) |

The model represents an AR24-X model , where X stands for the external regressors, e.g. futures, weekday dummies and periodic B-splines. It contains the regressor coefficients as well as an error term . The model treats the day-ahead electricity price for every hour of the day as a separate time series. This is useful especially as future data is usually not available in hourly precision but can be e.g. for the day-base-future in daily precision. As the day-ahead prices for each hour now also exhibits daily precision the variations of both time series occur within the same time period. We will refer to model (3) as Future-Model.

Every hourly price of a day in the dataset is dependent on the previous days of itself as well as on the 23 other hours of a day and their previous lags to model the autocorrelation structure. A detailed example for the dependency structure is presented in Figure 2, which should be kept in mind when reading the following technical descriptions of the future product dependency.

The variables and represent the the prices of the Phelix base and peak day futures respectively for maturity of 2 up to 6 days, based on the end-of-day price of the day two days before the actual observed day-ahead price. The price of 30.09.2016 e.g. is explained by all future maturities as end-of-day data of the 28.09.2016 as can be obtained from Figure 2. Higher maturities starting from up to 7 days in the future were not included as during the sample period no or just little trading occurred for these maturities. Additionally, the earlier prices of these maturities are considered as well. This guarantees that at least for one week we can use deterministic values, as for instance the day-base future with maturity 4 traded on Monday has now influence on the day-ahead price of Friday by the variable , e.g. the maturity 4 base day-future price with lag 2. Notice that in this example the day-future with maturity 4 traded on Monday represents the price an investor had to pay on Monday to buy 1 MW/h of electricity for every hour on Friday. If the exchange was closed due to a public holiday or weekend we simply replaced the not available value with the most recent value for that maturity, of usually one or two days before that day.

The data is also dependent one the last observable value of and of the base and peak week future respectively, as traded on the antecedent week for the actual week. The last observable week future price for the current week is usually the one on the Friday of the last week, but can be some days before that when public holidays occurred. So the day-ahead price for every hour of, for instance, the 22.10.2016, which is a Saturday, is dependent on the end-of-day price of the week-future of 14.10.2016, which is a Friday. The reason for the inclusion of this value is that traders may use this value as an orientation for the mean price of the upcoming week. It is also a day of the week to which the traded week future at the 14.10.2016 corresponded to. Moreover, we included all traded maturities on Friday for the next four weeks, which are represented by the index set as well as their historic values with up to lags. This guarantees that we have deterministic values for up to four weeks, as represents the value for the current week as traded on a Friday four weeks ago. Higher lags and maturities were dropped as they would exceed our planned forecasting horizon.

Furthermore, we included the base and peak futures for the weekend and respectively. This product is traded only with maturities up to 12 days, which means that it only provides deterministic values up to the weekend of the following week. For our model we used every tradeable maturity, from 1 to 5 days-ahead for the current weekend and from 8 to 12 days-ahead for the following weekend. These maturities are represented by the index set . As the maturities 8 to 12 for the weekend peak future were traded very rarely or even never, we excluded these five time series from our model and labeled their corresponding set of maturities . For the used weekend series we rearranged the prices so that for every day of the business week, e.g. Monday to Friday, every series becomes 0. The weekend days received the observable prices of every maturity traded during the week. This means that for instance the day-ahead prices for every hour of Sunday are dependent on the weekend base future price for maturity 1, which is always traded on a Friday, but also for maturity 2, which is always traded on a Thursday and so on. Note that the price for Saturday cannot be dependent on the price for maturity 1, as we used end-of-day data for the future, which results in that price being not possible to observe for investors. Hence, this specific price is set to 0 as well.

The last future product we included is the month base and peak future and respectively. The value of the month future was calculated as the last traded and observable month future price of the last month for the current month. Note that the last observable price is not necessarily the one at the last day of the month, as due to weekends and public holidays the last day of a month may not be a trading day. In this case we instead took the first observable price before that day. The month future price was kept fixed over the whole month and changes only after a new month occurs. Due to our forecasting horizon we decided to not include any historic values of this product.

Finally, we also introduced seven dummy variables which represent the day of the week (DoW) and are set to 1 if a specific weekday occurs and are 0 otherwise. To account for public holidays we regarded each public holiday as a Sunday. In addition to the weekday effects we also added the typical seasonal structure of electricity prices by adding a periodic cubic B-spline for each of the four season of the year. This regressor is a smooth cubic function which peaks at the the middle of a season and smoothly diminishes into the next season until it reaches the value of 0 for all other dates until the same season is about to start again. For details on the construction of periodic B-splines we refer the reader to Ziel et al., (2016).

As already mentioned the rather complex dependency structure of the day-ahead price towards the future products is illustrated for an interesting set of days from 30.09.2016 to 02.10.2016 in Figure 2.111For simplification, we present the dependency structure only towards base future products and leave out the peak products. However, the only difference in the dependency structure between those two is that the maturity 8 to 12 weekend products were omitted for peak products. These days show an interesting behavior as the include not only the phase in from a business day to the weekend but also the transition from one month to another. The different cells in the figure represent the day a specific product was traded, which is also the day for which the end-of-day value of that product was used as a regressor for the day-ahead-price of the day which can be obtained from the respective caption. For instance, for the day ahead-prices of 30.09.2016, which was a Friday, we can see that the base week future with maturitiy 3 (M3) traded at the 23.09. was used as a regressor. Moreover, it is shown that e.g. the base weekend future was set to 0 for that day, as Friday is not a day of the weekend. It is also identifiable, that for the base day future the values for 24.09. and 25.09. were not observable, as this was a weekend where the exchange was closed. Therefore the most recent values were used, which was in this case the value of the 23.09. which is a Friday. By comparing the different dates in the cells between the three presented days, one can retrace the distinct updating schemes as explained in the paragraphs before.

Overall, our model consists of 323 possible parameters. 168 of them emerge from the 24 hours and their 7 lags. The day of the week dummies together with periodic B-splines account for 11 parameters. The remaining 144 considered parameters coming from the future products are summarized in Table 1.

| Day Base | Day Peak | Week Base | Week Peak | Weekend Base | Weekend Peak | Month Base | Month Peak | |

| Current Values | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 |

| Historic Values | 7 | 7 | 3 | 3 | 1 | 1 | 0 | 0 |

| Number of Maturities | 5 | 5 | 4 | 4 | 10 | 5 | 1 | 1 |

| Overall # of parameters | (1+7)5=40 | (1+7)5=40 | (1+3)4=16 | (1+3)4=16 | (1+1)10=20 | (1+1)5=10 | (1+0)1=1 | (1+0)1=1 |

As our observation window has only 365 points in time for every hour and 323 possible parameters, we need an efficient and sparse method to estimate and possibly eliminate some of the regressors driven by an algorithm. Hence, we decided to use the lasso estimator of Tibshirani, (1996) in combination with a coordinate-descent estimation approach as included in the R-package glmnet by Friedman et al., (2016). For more insights into the lasso procedure and its properties, see e.g. Hastie et al., (2015).

As the lasso estimator is a penalized least square estimator, we need to rewrite equation (3). Furthermore, in order to successfully execute the lasso algorithm the variables need to be standardized, so that they have a variance of 1. The final lasso-suited ordinary least squares representation of (3) is therefore:

| (4) |

where the -symbol represents the scaled versions of the respective data vector. With representation (4) we can estimate the scaled parameter vectors given all observable days by using the lasso estimator :

| (5) |

where is a penalty parameter, is the amount of observations used and the number of possible parameters.

As estimation algorithm we use the coordinate descent approach of Friedman et al., (2007) especially as it provides a fast estimation technique. Given a possible parameter set estimated by the coordinate descent approach. We select the best fitting tuning parameter on an exponential grid ( with equidistant) by evaluating the Bayesian information criterion (BIC) which is regarded as conservative and therefore sparse model selection criterion. Using the BIC criterion will therefore induce a high probability that a large amount of the possible regressors will be removed by setting their equivalent to 0, so that the final models for every hour are very unlikely to exhibit all parameters. To keep track of the included regressors we will show an overview about how often they were actually used in the following section.

Using this complex approach of modeling the data allows us to incorporate information in the day-ahead prices, which are not represented in the models which use the hourly price forward curves. Given the future price information of a specific day it is possible to create the hourly price forward curve (HPFC) as an risk-neutral approximation for the real day-ahead prices of the upcoming days. In order to get the real prices under the assumption that investors are risk-averse it is possible to model the differences of the hourly price forward curve to the real day-ahead prices as a risk premium. This was done for instance by Paraschiv et al., (2015). They use the future base prices of a specific day to create the HPFC in order to get information of the day-ahead prices of the future. To create realistic day-ahead prices under risk-averse evaluation they additionally model the difference between the two as risk premium using a regime switching time series approach. In this sense they are not only able to track the movements of the risk premium, but also to guarantee price spikes when they simulate prices with their model. As the time horizon of the future base products is relatively high, they can even carry out a forecasting analysis for two different starting time points in 2012 for up to one month.

Our approach is comparable to the model of Paraschiv et al., (2015) as we use a similar set of input parameters to estimate day-ahead prices of the future. However, there is a substantial difference in our approaches, as in addition to the futures of one day, we also utilize the futures of days before today as lagged data. This has the advantage that we can use the historic expectations of investors who, for instance, have bought three days ago a day base future with maturity in four days. Such investors are obliged to pay or receive the settlement price determined by the future product. If these traders are active on the day-ahead exchange as well, they are likely to remember the price they had agreed on several days ago when they contracted the future product and may therefore influence the day-ahead price accordingly.

Our approach would therefore roughly correspond to a HPFC-model which uses the HPFC of today and the past HPFCs as well as direct input to day-ahead prices. As we do not model HPFC directly, our model does not has to be in line with theory about risk averse investors and their required risk premia. Nevertheless, if the assumptions of the theory leading to equation (2) are correct, HPFC-approaches and our approach model the same variable, i.e. . If we further assume that the risk premium is exactly 0, then our model would also model the HPFC in a comparable fashion as Caldana et al., (2017), who also utilize a function of day-ahead prices with e.g. seasonal and weekly patterns to create HPFC.

However, even though our regressors can be motivated by the theory of HPFC, we do not necessarily require the underlying assumptions of that theory to hold. Our model is only associated with the assumptions of plain time-series analysis. The reason for that is that our model has the sole purpose of forecasting day-ahead prices, which is also not necessarily the same as explaining the underlying data, see for instance Shmueli et al., (2010) for a thorough analysis of that common misconception. This insight leads to another important difference in our modeling approaches, as we utilize the advantages of machine learning for parameter selection, as done by the estimation algorithm of Friedman et al., (2007) for the lasso-selection problem we use. Therefore we can simply add more regressors, e.g. deterministic information on the weekday or previous lags of the price.

However, our approach has the drawback compared to the approach of Paraschiv et al., (2015), that due to the lack of a financial theory for our model we cannot determine the risk premium which risk averse investors require.

3 Forecasting, results and simulation

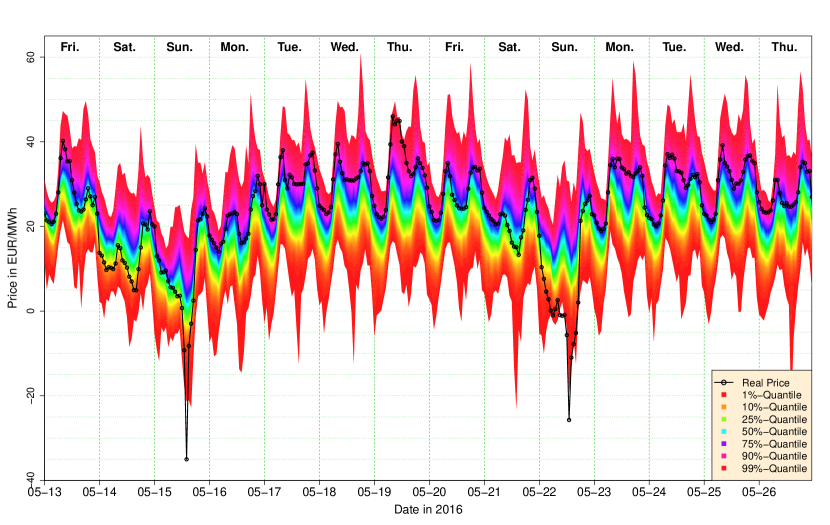

We design a rolling window out-of-sample forecasting study for forecasting evaluation. Note that in contrast to an expanding window study only a rolling window study allows for proper forecasting evaluation in the context of the Diebold-Mariano test that we utilize here, for more details see Diebold, (2015). In our study we consider an in-sample length of days. Moreover, we use rollowing windows. We denote as the last in-sample day of the first rolling window. Hence, we define the estimated error of model (3) as days and hours ahead forecasting error of the -th rolling window. Note that is an estimated error of , but is estimated by multiple models as the forecasting windows overlap within the rolling window study. Figure 3 illustrates this design of the forecasting study. Reddish colors symbolize data which was observed until the start of the forecasting period. Greenish colors stand for data which originates from the future. The greenish area consists of the forecasting period and the remaining data for estimation and covers one year, e.g. days. For from 1 to 3 it can be seen that the rolling estimation window shifts for one day for each . This is done until , e.g. the whole greenish area of is covered. The dashed lines show the range of the forecasting period of and helps to determine the structure of the rolling process. It can be obtained that the day of the last forecasting period of corresponds to the day of the next to last day of the forecasting period of and so on.

After estimating the coefficients of model (3) we can simply construct a forecast by iteratively estimating , where represents the index set of days given the starting weekday which has to be forecasted and of is 28 . However, some of the future products are only observable for some of the days of the prediction horizon. E.g. the day base future with maturity 2 is only observable for the day-ahead price in two days. As forecasting these future products would lead to a situation where we would still had to face the problem as described earlier, we estimate the coefficients in model (3) repeatedly for each day of our 28 days long forecasting horizon, but exclude all regressors which were not observable for that time. This has the advantage that we will only use true observable and therefore deterministic regressors, which makes the model fair and applicable for practical uses. The disadvantage is that we have to carry out 28 out model estimations per shift in the rolling estimation window, which coincides with demanding CPU-times.

For model comparison we decided to use two different and commonly used measures, the MAE (Mean Absolute Error) and the MMAE (Mean Mean Absolute Error). These two are defined as follows:

| (6) | ||||

| (7) | ||||

| (8) |

with as smallest integer and mod as modulo operator.

Given the forecasts of our rolling estimation window, which included forecasts for every day of the months from May 2016 to April 2017 , we can compute the which represents the Mean Absolute Error for every day and every corresponding hour of the day . As we forecasted four weeks the can be calculated for up to hours. Given a we can easily transform it to the notation, which is convenient to calculate the . The is a less volatile measure than the as it represents the error the model has made up to a certain forecasting horizon in opposition to the which provides the error for a specific forecasting horizon.

For model comparison we introduce three extremely competitive benchmarks, two VAR-HoW(p) with AIC-selection based on the paper of Ziel et al., (2015) and the AR24(p) with lasso and BIC-selection as it was selected as most competitive model in Ziel, (2016). They are defined as follows:

| (9) | |||||

| (10) |

For the VAR-HoW(p) models the was treated as one hourly time-series, i.e. . The first one of the VAR-HoW(p) models represents a univariate model with , which we refer to as AR-HoW(p) from now on. The second one is a 3-dimensional model for the electricity price, electricity load and renewable energy production from wind and solar energy, so with as load and as renewable energy production. This model will be referred to as VAR-X(p). Note that the univariate and bivariate models were competitive benchmarks in Ziel et al., (2015) for the same forecasting horizon. The univariate AR-HoW(p) model in a slightly modified version turned out to be a strong competitor in the paper of Ziel and Weron, (2016).

The VAR-HoW(p) extends the standard VAR(p) framework by a weekly seasonal component, so that the resulting process is non-stationary. The seasonal regressor HoW which stands for Hour of the Week represents a deterministic dummy variable which becomes 1 when a specific hour of the week is present. As a week has hours in total this results in 168 regressors added for each dimension of the VAR-HoW(p). The estimation of this model was done in a two-step-approach by first estimating the model via Ordinary-Least-Squares and then an AIC-selected VAR() by solving the multivariate Yule-Walker-Equations on where is selected out of . Note that .

Our last benchmark is the AR24(p). It corresponds to our main model (3) but considers no future data. It is also estimated in the same way as our main model. With that benchmark we want to isolate the impact of the futures data towards our model.

The MMAE is a very good measure to break down different models to one number. This can be done by choosing the highest possible , e.g. the mean over all forecasting errors up to hours in the future. After estimating and forecasting the day-ahead electricity price for each model, we start with the presentation of the MMAE for a forecasting horizon of hours. It is displayed in Table 2.

| Future-Model | AR24(p) | AR-HoW(p) | VAR-X(p) | |

| 7.19 | 8.56 | 8.26 | 8.49 |

In this first overview we can see that the proposed future-based model is superior considering the whole forecasting period. The number 7.19 means that a market participant who used this model faced an absolute error of 7.19 EUR/MWh on average, when the participant forecasted 672 hours or four weeks at once.

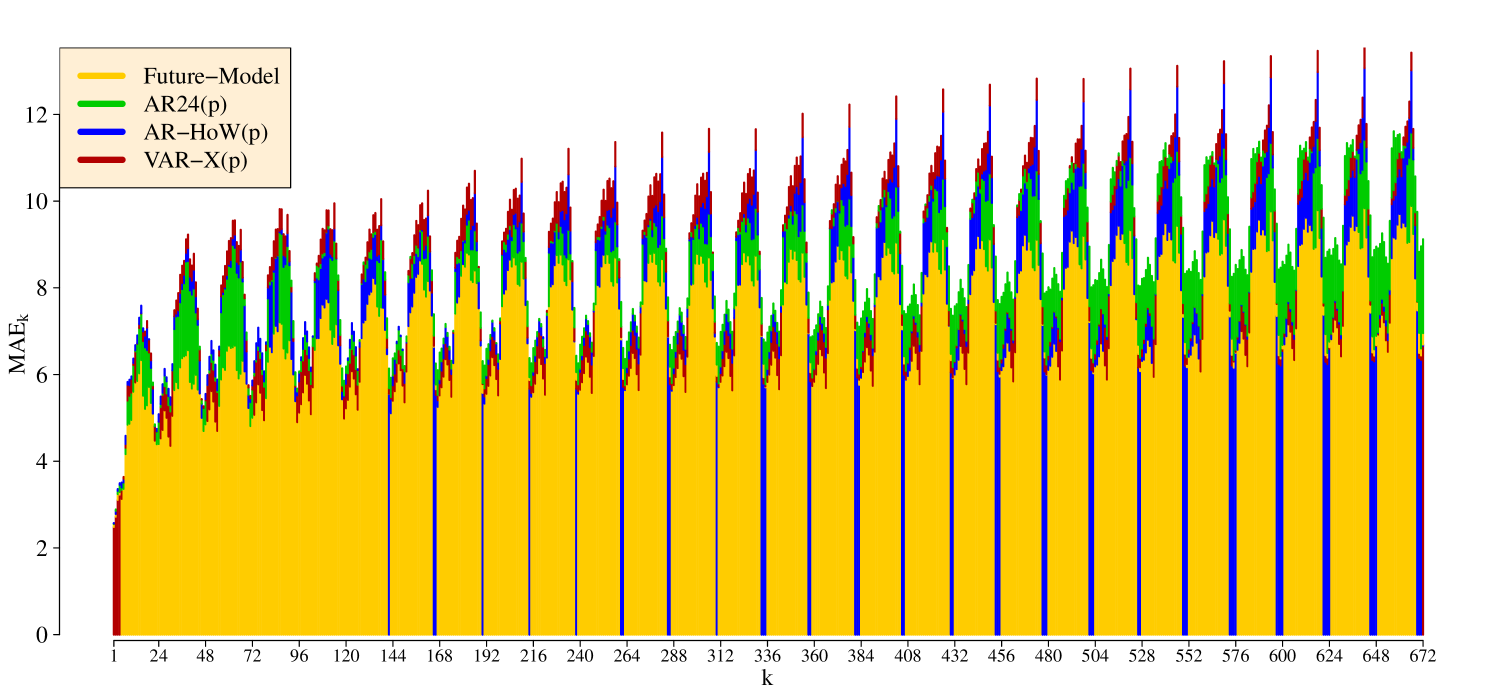

Much more detailed and difficult to illustrate is the as we have to compare four different models over 672 points in time, resulting in different values. Hence, we decided to use a stacked bar chart over all 672 hours which shows the for each model. This is shown in Figure 4.

Every model received its individual color, as shown in the legend in the top-left corner of the figure. The stacked bars are always ordered from the best to the worst model, so that the viewer can easily spot the best model over the time. The difference of the next best model to the actual model is then stacked on the existing bar and given its individual color. This is done for every bar and every benchmark model so it is also possible to spot the worst model very quickly. Hence, it can be seen that the Future-Model which has the color yellow seems to outperform every other model over the majority of time. Almost each of the benchmark models is however for some hours in the future the best model. We can also see that the VAR-X(p) with color red is very often the worst model for peak hours. This is especially fascinating given the fact that for the first fours hours the VAR-X(p) is in fact the best model. The diminishing forecasting power of the model is very likely due to the fact that for this type of model the regressors, e.g. load and especially renewables have to be forecasted as well. But as these forecasts are barely accurate for renewables for such a long time frame they add uncertainty to the overall precision of the price model. Interestingly, it can be obtained that every model independent of being univariate or multivariate, in the sense that it models every hour separately, tends to have extremely volatile behaviour. The night hours seem to exhibit much lower than the daytime hours. A possible reason for that could be the influence of renewables, as these hours are prone for unexpected variability of sunlight and the resulting solar power. As expected, the also seems to increase over time, but reaches a convergence point after approximately one week , especially when the Future-Model is considered. The best model during the first 24 hours of the forecasting horizon exhibits extremely low values, always below a of 7 EUR/MWh.

However, as there are still some hours where other model outshine the Future-Model we want to further investigate the differences between these models and determine which is the overall best model by using statistical theory. Therefore we employed a multivariate Diebold-Mariano-Test (DM-Test) for every day of the first four forecasting weeks. The DM-Test is a quite commonly used test in electricity price forecasting, it was recently used for instance in Bordignon et al., (2013) or Nan et al., (2014).

Our DM-test is based on the -norm of the estimated daily residuals of two forecasts, say and . It utilizes the loss functions and to compute the loss differences

The key idea is now to check if is significantly different from zero or not. If is significantly smaller than zero with respect to a certain significance level then the forecast is significantly better than forecast for the forecasting day . The DM-statistic for forecasting day is defined as

where and with its standard deviation. The latter one we estimate by the sample standard deviation of the corresponding process. Note that under the null hypothesis of the test () the DM-statistic is asymptotic normal.

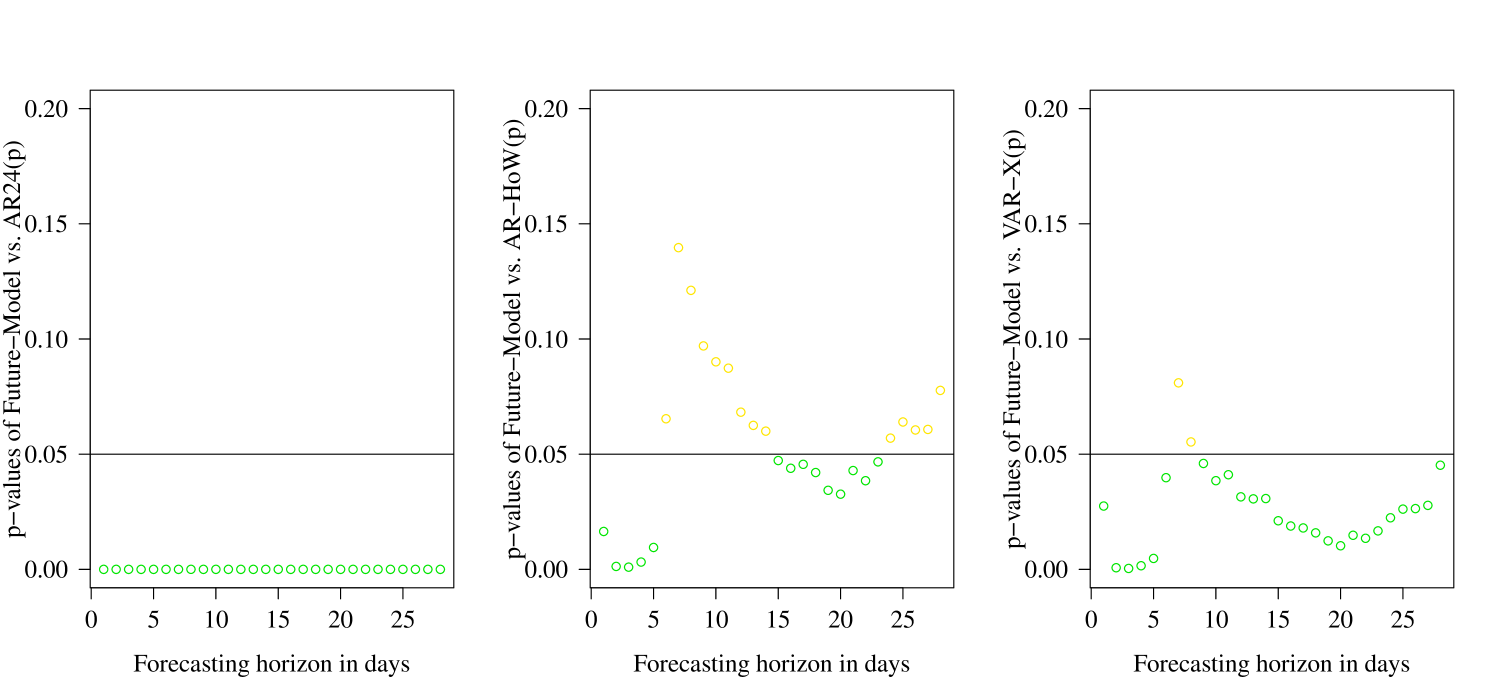

We applied the DM-Test for all competitors of our model, the AR24(p), the AR-HoW(p) and the VAR-X(p) . The results are illustrated in figure 5.

The figure depicts the p-values of the DM-Test for the Future-Model against all tested benchmark models. For every day of the first four weeks, e.g. 28 days, a multivariate DM-test was executed. The horizontal line in every chart represents an arbitrarily chosen five percent error probability for our test. If one of the dots lays above the straight line, we can conclude that based on our level of confidence we cannot say that our model performed significantly better for that specific time horizon. The figure indicates that for all investigated days the AR24(p) benchmark could not perform significantly better than our model. As the AR24(p) model is the same model as ours but without the futures, we can conclude that adding future products provided an increasing in forecasting performance. Even though overall the Future-Model performed better than the AR-HoW(p) and VAR-X(p) benchmark models, we cannot statistically proof that for every day of the forecasting. For the VAR-X(p) benchmark our model is significantly better for every day except for day seven and eight. Comparing our results with the AR-HoW(p) our models performs significantly better during 50 percent of all days. It can be obtained that especially during the first days our model exhibits great model performance, while the following days the performance seems to not become significant anymore. However, after day 14 the performance seems to stabilize again and the model becomes significantly better. Please note that our model not being significantly better does not mean that the benchmark models performed better. Also all these evaluations are heavily dependent on the chosen significance level. For a ten percent significance level for instance our model would be significantly better for almost every hour and model. But as these level choices, especially given a multiple testing problem, are overall debatable we will base our evaluation only for one significance level and provide the p-values in Figure 5 at the ordinate. Nevertheless, comparing simply the performance of models does not provide detailed insight to the reasons of why the Future-Model lead to superior forecasting performance. Hence, we would like to analyse the final model structure of our Future-Model throughout the whole forecasting period.

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | 19 | 20 | 21 | 22 | 23 | 24 | ||

| Day-Ahead Price | H1 lag 1 | 0.00 | 0.00 | 0.03 | 1.06 | 4.67 | 0.10 | 0.00 | 3.15 | 0.74 | 0.07 | 0.00 | 0.08 | 0.00 | 0.03 | 0.17 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.25 | 0.08 | 0.00 | 0.06 |

| H2 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 7.06 | 17.42 | 4.76 | 12.99 | 11.73 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.23 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.02 | |

| H3 lag 1 | 0.24 | 10.15 | 0.79 | 0.25 | 0.15 | 1.25 | 36.39 | 26.35 | 13.20 | 0.01 | 0.00 | 0.00 | 0.00 | 0.01 | 0.14 | 0.00 | 0.00 | 0.14 | 0.13 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| H4 lag 1 | 4.73 | 26.36 | 49.18 | 31.10 | 16.87 | 2.70 | 0.00 | 3.60 | 0.01 | 0.05 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.01 | 0.00 | 0.10 | 0.06 | 7.21 | 3.01 | 0.00 | 0.07 | 1.35 | |

| H5 lag 1 | 0.02 | 11.46 | 16.47 | 53.13 | 46.14 | 44.43 | 34.71 | 42.34 | 1.09 | 0.29 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.08 | 0.09 | 0.38 | 0.23 | 0.25 | 0.11 | 0.15 | 0.31 | |

| H6 lag 1 | 2.11 | 6.93 | 24.06 | 36.27 | 65.57 | 55.80 | 25.10 | 1.09 | 0.15 | 0.00 | 0.08 | 0.51 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.14 | 0.00 | 0.02 | 0.11 | 0.00 | 0.06 | 1.54 | |

| H7 lag 1 | 0.46 | 11.06 | 36.54 | 75.46 | 91.40 | 51.44 | 35.35 | 33.89 | 30.73 | 0.97 | 0.15 | 3.53 | 0.88 | 0.03 | 0.05 | 0.68 | 0.25 | 0.22 | 0.05 | 0.10 | 0.04 | 0.00 | 0.01 | 0.32 | |

| H8 lag 1 | 30.12 | 54.19 | 32.67 | 27.86 | 31.46 | 2.93 | 0.00 | 2.37 | 0.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.10 | 1.26 | 0.06 | 0.00 | 0.00 | 0.06 | 0.37 | |

| H9 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.34 | 2.19 | |

| H10 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 1.03 | 0.19 | 2.78 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.01 | 0.00 | 0.31 | 1.79 | |

| H11 lag 1 | 0.00 | 0.00 | 0.00 | 0.18 | 0.26 | 0.26 | 1.16 | 0.04 | 3.79 | 0.00 | 0.49 | 1.97 | 0.47 | 0.00 | 0.00 | 0.03 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.01 | |

| H12 lag 1 | 0.00 | 0.00 | 0.01 | 0.00 | 0.00 | 0.01 | 0.43 | 1.13 | 9.14 | 51.36 | 77.26 | 87.22 | 82.92 | 42.93 | 22.53 | 22.10 | 15.89 | 0.16 | 0.33 | 0.08 | 0.00 | 0.00 | 0.00 | 0.34 | |

| H13 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.01 | 0.00 | 2.05 | 0.00 | 0.00 | 0.34 | 35.29 | 40.14 | 78.51 | 87.65 | 62.39 | 4.58 | 0.99 | 0.02 | 1.13 | 0.00 | 0.00 | 0.00 | 0.00 | 0.03 | |

| H14 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.22 | 2.02 | 2.01 | 1.23 | 1.73 | 2.05 | 1.56 | 0.06 | 0.08 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| H15 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 4.73 | 0.35 | 0.08 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.38 | 0.05 | 0.00 | 0.01 | |

| H16 lag 1 | 0.00 | 1.13 | 0.00 | 4.73 | 11.70 | 0.81 | 0.00 | 0.00 | 0.00 | 0.10 | 0.47 | 1.00 | 5.93 | 19.70 | 34.80 | 15.90 | 12.74 | 0.00 | 0.00 | 0.00 | 0.07 | 0.00 | 0.00 | 0.00 | |

| H17 lag 1 | 0.00 | 0.43 | 0.00 | 0.07 | 0.00 | 0.00 | 0.30 | 0.01 | 0.01 | 2.09 | 11.62 | 2.45 | 1.94 | 3.27 | 18.99 | 14.74 | 3.78 | 0.14 | 0.00 | 0.00 | 0.66 | 3.34 | 0.29 | 1.31 | |

| H18 lag 1 | 0.00 | 19.78 | 0.21 | 12.17 | 31.42 | 0.30 | 0.00 | 2.89 | 19.93 | 58.77 | 57.65 | 75.62 | 72.71 | 76.84 | 79.48 | 90.77 | 94.16 | 99.57 | 32.46 | 2.31 | 0.01 | 0.15 | 0.17 | 0.70 | |

| H19 lag 1 | 0.00 | 0.21 | 0.01 | 0.68 | 2.03 | 0.00 | 0.03 | 3.13 | 2.82 | 6.30 | 22.54 | 21.55 | 14.02 | 7.49 | 5.40 | 10.88 | 33.18 | 73.00 | 77.70 | 0.33 | 0.11 | 0.29 | 0.81 | 0.29 | |

| H20 lag 1 | 44.62 | 96.54 | 85.84 | 80.20 | 79.89 | 93.22 | 89.75 | 98.16 | 99.06 | 99.02 | 99.02 | 94.09 | 86.20 | 85.42 | 74.66 | 63.36 | 53.19 | 47.44 | 90.29 | 95.04 | 3.29 | 0.00 | 0.00 | 0.00 | |

| H21 lag 1 | 67.79 | 44.75 | 29.10 | 27.11 | 18.62 | 47.75 | 79.13 | 76.14 | 82.89 | 87.82 | 18.92 | 4.27 | 5.86 | 0.79 | 1.90 | 1.98 | 8.37 | 2.38 | 7.17 | 74.83 | 85.70 | 3.87 | 0.23 | 1.01 | |

| H22 lag 1 | 41.55 | 4.20 | 0.07 | 1.41 | 8.30 | 38.20 | 50.10 | 5.81 | 0.89 | 1.15 | 0.01 | 0.00 | 0.00 | 0.00 | 0.17 | 1.12 | 1.75 | 1.35 | 16.40 | 19.70 | 92.15 | 99.96 | 38.60 | 36.42 | |

| H23 lag 1 | 43.25 | 6.96 | 0.42 | 0.19 | 0.34 | 8.42 | 15.27 | 36.87 | 55.98 | 61.84 | 62.14 | 71.89 | 70.59 | 52.12 | 54.43 | 33.87 | 32.44 | 20.20 | 11.97 | 19.82 | 27.69 | 41.93 | 80.81 | 54.08 | |

| H24 lag 1 | 100 | 100 | 100 | 100 | 100 | 100 | 99.57 | 69.77 | 61.17 | 55.86 | 63.00 | 63.88 | 55.58 | 58.25 | 49.36 | 79.69 | 78.43 | 47.57 | 12.26 | 40.96 | 37.40 | 43.45 | 50.73 | 79.28 | |

| H1 lag 7 | 0.23 | 0.00 | 0.00 | 0.10 | 0.43 | 0.33 | 5.00 | 2.93 | 0.18 | 0.66 | 4.35 | 3.10 | 1.93 | 5.02 | 4.12 | 0.04 | 0.22 | 0.23 | 9.36 | 1.78 | 0.67 | 3.25 | 5.91 | 3.70 | |

| H2 lag 7 | 0.24 | 0.00 | 0.00 | 0.00 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.19 | 0.06 | 0.00 | 0.00 | 0.47 | 0.64 | 0.02 | 0.07 | 0.00 | 0.07 | 0.02 | 0.02 | 0.00 | 0.00 | 0.00 | |

| H3 lag 7 | 0.00 | 0.00 | 0.00 | 0.00 | 0.02 | 0.00 | 0.00 | 1.02 | 0.20 | 0.06 | 0.00 | 0.00 | 0.09 | 0.24 | 0.45 | 0.06 | 0.01 | 0.15 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.21 | |

| H4 lag 7 | 0.00 | 0.00 | 0.00 | 0.00 | 0.29 | 0.07 | 0.04 | 0.36 | 0.41 | 0.45 | 1.89 | 1.82 | 1.25 | 0.40 | 0.81 | 0.04 | 0.11 | 5.01 | 0.00 | 0.03 | 0.25 | 0.05 | 0.00 | 0.20 | |

| H5 lag 7 | 1.91 | 0.02 | 0.02 | 2.14 | 0.75 | 0.15 | 0.01 | 0.01 | 0.15 | 0.04 | 1.74 | 4.83 | 2.15 | 1.78 | 0.00 | 0.85 | 1.78 | 11.80 | 1.17 | 6.31 | 3.17 | 1.20 | 14.74 | 10.39 | |

| H6 lag 7 | 0.00 | 0.34 | 0.00 | 0.00 | 0.02 | 0.03 | 0.03 | 0.17 | 0.19 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.17 | 1.10 | 0.54 | 1.17 | 3.83 | 3.96 | 2.23 | |

| H7 lag 7 | 0.79 | 2.05 | 1.50 | 20.22 | 27.34 | 56.96 | 63.08 | 49.00 | 56.24 | 20.83 | 9.90 | 8.86 | 3.79 | 1.24 | 0.06 | 6.16 | 8.20 | 13.04 | 7.91 | 31.76 | 23.49 | 6.05 | 0.86 | 1.42 | |

| H8 lag 7 | 0.00 | 0.61 | 0.14 | 0.76 | 22.57 | 21.27 | 39.03 | 22.23 | 16.48 | 14.11 | 8.13 | 5.99 | 3.15 | 3.09 | 2.38 | 9.05 | 9.67 | 5.31 | 10.72 | 28.99 | 24.29 | 0.64 | 0.04 | 0.00 | |

| H9 lag 7 | 2.58 | 0.83 | 0.71 | 3.54 | 8.15 | 16.83 | 0.58 | 22.35 | 35.76 | 56.49 | 38.34 | 29.84 | 22.96 | 8.79 | 3.68 | 10.52 | 5.71 | 0.07 | 4.66 | 5.37 | 7.40 | 0.94 | 1.64 | 2.06 | |

| H10 lag 7 | 0.00 | 0.00 | 0.00 | 0.01 | 0.13 | 0.29 | 0.00 | 0.00 | 0.12 | 4.36 | 10.95 | 8.79 | 2.59 | 6.45 | 0.00 | 0.55 | 0.19 | 0.63 | 0.33 | 3.95 | 2.25 | 0.00 | 0.03 | 0.00 | |

| H11 lag 7 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.07 | 0.00 | 0.00 | 0.00 | 7.61 | 16.23 | 16.87 | 22.14 | 17.92 | 4.66 | 26.92 | 26.09 | 16.62 | 27.30 | 14.98 | 0.07 | 0.00 | 0.01 | 0.00 | |

| H12 lag 7 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.59 | 0.00 | 0.00 | 17.93 | 15.23 | 3.36 | 4.37 | 9.45 | 0.00 | 2.62 | 4.62 | 10.47 | 11.98 | 5.17 | 0.00 | 0.00 | 0.00 | 0.00 | |

| H13 lag 7 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.13 | 0.28 | 0.00 | 0.57 | 0.49 | 0.17 | 0.40 | 0.00 | 2.47 | 0.05 | 0.07 | 0.00 | 0.00 | 0.00 | 0.24 | 0.00 | 0.01 | 0.02 | |

| H14 lag 7 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.26 | 0.03 | 0.09 | 1.25 | 0.00 | 0.00 | 0.00 | 0.00 | 16.00 | 0.14 | 0.00 | 0.00 | 0.00 | 0.00 | 0.04 | 0.01 | 0.02 | 0.45 | |

| H15 lag 7 | 0.00 | 0.00 | 0.00 | 0.00 | 0.10 | 0.09 | 0.00 | 0.24 | 1.59 | 25.13 | 27.08 | 17.15 | 6.81 | 49.87 | 57.33 | 4.35 | 1.26 | 0.02 | 0.00 | 0.00 | 0.01 | 0.02 | 0.00 | 0.38 | |

| H16 lag 7 | 0.00 | 4.76 | 0.00 | 0.00 | 9.01 | 0.00 | 0.37 | 2.21 | 4.80 | 10.77 | 6.39 | 5.93 | 5.20 | 16.13 | 22.96 | 24.72 | 25.16 | 30.40 | 14.51 | 0.02 | 0.00 | 0.00 | 0.00 | 0.02 | |

| H17 lag 7 | 0.01 | 0.00 | 0.00 | 0.00 | 1.59 | 0.00 | 0.00 | 0.00 | 0.05 | 0.28 | 10.97 | 17.96 | 16.60 | 14.03 | 32.09 | 35.24 | 26.14 | 33.30 | 6.46 | 0.14 | 0.00 | 0.00 | 0.38 | 0.01 | |

| H18 lag 7 | 0.00 | 0.00 | 0.01 | 0.02 | 0.00 | 0.00 | 0.19 | 0.54 | 0.88 | 21.71 | 24.89 | 27.44 | 35.73 | 26.57 | 2.03 | 54.40 | 56.91 | 70.36 | 48.50 | 3.43 | 0.27 | 1.13 | 1.59 | 2.20 | |

| H19 lag 7 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.01 | 8.83 | 8.83 | 0.88 | 0.77 | 0.37 | 0.50 | 0.00 | 0.00 | 0.18 | 0.67 | 0.16 | 40.20 | 6.93 | 0.02 | 0.03 | 0.38 | 0.01 | |

| H20 lag 7 | 0.24 | 0.00 | 0.01 | 0.00 | 6.48 | 31.59 | 9.34 | 0.02 | 0.45 | 0.67 | 3.05 | 4.65 | 1.76 | 0.20 | 0.02 | 0.23 | 0.01 | 0.00 | 0.00 | 37.94 | 0.00 | 0.00 | 0.10 | 0.00 | |

| H21 lag 7 | 0.00 | 0.00 | 0.00 | 0.00 | 0.01 | 0.97 | 43.46 | 35.91 | 32.61 | 4.43 | 0.68 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | 0.02 | 0.00 | 0.00 | 3.80 | 51.62 | 2.65 | 0.65 | 0.71 | |

| H22 lag 7 | 0.16 | 0.00 | 0.00 | 0.00 | 0.09 | 0.05 | 0.12 | 0.29 | 3.95 | 0.03 | 0.00 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.11 | 0.00 | 0.06 | 19.21 | 84.25 | 23.83 | 9.33 | |

| H23 lag 7 | 0.09 | 9.66 | 15.77 | 1.13 | 0.02 | 0.00 | 0.05 | 0.00 | 0.00 | 0.08 | 0.19 | 0.46 | 0.01 | 0.05 | 0.00 | 0.00 | 0.00 | 0.56 | 0.22 | 0.01 | 0.00 | 0.07 | 28.86 | 18.50 | |

| H24 lag 7 | 0.00 | 0.61 | 0.23 | 0.08 | 0.00 | 0.00 | 0.13 | 0.16 | 0.14 | 0.46 | 1.42 | 1.22 | 0.39 | 1.11 | 1.22 | 1.59 | 3.06 | 8.47 | 0.88 | 0.01 | 0.00 | 0.00 | 0.00 | 0.04 | |

| Day Base Future | M2 lag 7 | 0.00 | 0.00 | 0.00 | 0.10 | 0.10 | 0.00 | 0.24 | 0.82 | 0.07 | 0.14 | 0.34 | 1.20 | 0.07 | 0.00 | 0.00 | 0.14 | 0.00 | 0.00 | 0.21 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| M2 lag 6 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.04 | 0.00 | 0.00 | 0.04 | 0.20 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M2 lag 5 | 0.00 | 0.00 | 0.00 | 0.09 | 0.73 | 4.84 | 4.57 | 18.68 | 33.01 | 39.27 | 14.70 | 13.61 | 0.00 | 0.00 | 0.00 | 0.00 | 0.09 | 0.50 | 0.00 | 3.84 | 0.00 | 0.00 | 0.05 | 1.46 | |

| M2 lag 4 | 0.00 | 0.00 | 0.05 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.05 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.11 | 0.44 | 0.00 | 0.00 | |

| M2 lag 3 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.16 | 0.34 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.14 | 0.00 | |

| M2 lag 2 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.09 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M2 lag 1 | 0.00 | 0.14 | 0.14 | 0.14 | 0.27 | 0.00 | 0.00 | 0.00 | 0.27 | 0.00 | 0.00 | 0.14 | 0.00 | 0.00 | 0.00 | 1.23 | 2.88 | 0.00 | 0.00 | 0.14 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M2 lag 0 | 18.90 | 74.79 | 73.97 | 76.16 | 100 | 97.26 | 60.00 | 44.11 | 38.90 | 12.88 | 6.03 | 3.56 | 16.71 | 19.73 | 8.49 | 27.67 | 27.67 | 4.38 | 20.27 | 67.67 | 58.63 | 44.93 | 47.95 | 83.56 | |

| M3 lag 7 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.10 | 1.34 | 1.16 | 0.38 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M3 lag 6 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.04 | 0.16 | 0.08 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.04 | 0.00 | 0.00 | 0.00 | |

| M3 lag 5 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.32 | 1.05 | 0.64 | 0.23 | 0.14 | |

| M3 lag 4 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.22 | 0.27 | 0.00 | 0.27 | 0.11 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.05 | 0.66 | 0.55 | |

| M3 lag 3 | 0.00 | 0.00 | 0.00 | 0.07 | 0.27 | 0.07 | 0.27 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.07 | 0.00 | 0.00 | 0.00 | |

| M3 lag 2 | 9.32 | 3.20 | 1.00 | 1.10 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.09 | 1.19 | 0.00 | 0.00 | 0.09 | 0.55 | 0.00 | 0.18 | 0.09 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M3 lag 1 | 43.29 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 99.32 | 67.40 | 31.10 | 13.42 | 22.19 | 7.53 | 2.05 | 13.84 | 18.49 | 2.47 | 0.14 | 80.68 | 86.58 | 33.70 | 9.73 | 12.88 | |

| M3 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.27 | 34.52 | 53.97 | 87.12 | 40.00 | 12.33 | 0.27 | 3.29 | 0.82 | 2.47 | 0.55 | 32.05 | 28.77 | 40.82 | 45.21 | 100 | 100 | 80.00 | 88.22 | 97.81 | |

| M4 lag 7 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 5.34 | 0.24 | 0.03 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M4 lag 6 | 0.00 | 0.00 | 0.00 | 0.04 | 0.04 | 0.00 | 2.31 | 1.14 | 0.59 | 4.03 | 1.41 | 0.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.31 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M4 lag 5 | 0.00 | 0.00 | 0.00 | 0.14 | 0.05 | 0.00 | 0.00 | 3.61 | 0.18 | 0.00 | 0.00 | 0.50 | 0.00 | 0.00 | 0.09 | 0.46 | 0.46 | 0.00 | 0.00 | 0.46 | 0.46 | 2.56 | 0.00 | 0.59 | |

| M4 lag 4 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.55 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.27 | 0.11 | 0.60 | 1.81 | 0.71 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M4 lag 3 | 2.12 | 3.56 | 1.30 | 8.77 | 19.18 | 3.97 | 0.34 | 0.00 | 0.00 | 0.00 | 0.00 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.27 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M4 lag 2 | 0.09 | 25.84 | 30.32 | 33.42 | 36.44 | 53.52 | 86.48 | 67.95 | 92.69 | 23.56 | 3.56 | 0.91 | 1.92 | 0.82 | 0.64 | 3.01 | 3.01 | 1.00 | 5.39 | 52.33 | 39.45 | 25.21 | 2.56 | 16.26 | |

| M4 lag 1 | 0.00 | 0.14 | 0.14 | 0.00 | 0.00 | 0.82 | 9.04 | 1.10 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.27 | 0.00 | 0.14 | 2.88 | 65.07 | 80.14 | 98.36 | 88.90 | 90.82 | |

| M4 lag 0 | 20.55 | 24.11 | 34.52 | 29.32 | 35.34 | 23.29 | 10.68 | 4.66 | 21.92 | 14.25 | 0.27 | 1.37 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.10 | 1.37 | 15.34 | 0.00 | 1.92 | 0.00 | 5.21 | |

| M5 lag 7 | 0.00 | 6.13 | 0.07 | 0.24 | 0.03 | 0.00 | 0.00 | 0.00 | 0.03 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.07 | 0.00 | 0.00 | 0.10 | 0.00 | 0.00 | 0.00 | |

| M5 lag 6 | 0.00 | 0.00 | 0.27 | 0.00 | 0.00 | 0.00 | 0.00 | 0.04 | 0.12 | 0.39 | 0.04 | 0.31 | 0.00 | 0.00 | 0.00 | 0.04 | 0.00 | 0.00 | 0.08 | 0.08 | 0.20 | 0.12 | 0.00 | 0.55 | |

| M5 lag 5 | 0.00 | 0.00 | 0.00 | 0.23 | 2.33 | 4.57 | 25.43 | 11.74 | 13.88 | 0.00 | 0.00 | 0.00 | 0.05 | 0.41 | 0.23 | 4.57 | 7.58 | 0.37 | 1.51 | 0.14 | 0.09 | 0.09 | 0.00 | 0.41 | |

| M5 lag 4 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.16 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.33 | 0.00 | 0.05 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M5 lag 3 | 94.38 | 90.82 | 67.47 | 47.95 | 55.75 | 50.75 | 47.67 | 31.30 | 47.33 | 48.15 | 16.85 | 15.21 | 18.42 | 29.32 | 38.36 | 34.86 | 14.93 | 4.73 | 12.33 | 46.44 | 72.33 | 37.81 | 7.05 | 21.64 | |

| M5 lag 2 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 | 9.77 | 0.18 | 0.64 | 0.37 | 0.82 | 1.92 | 0.09 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 11.87 | 70.59 | 73.24 | 75.07 | 72.05 | 69.50 | |

| M5 lag 1 | 0.41 | 4.93 | 3.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.41 | 1.37 | 0.00 | 0.27 | 0.00 | 0.00 | 0.00 | 0.14 | 0.00 | 0.00 | 4.52 | 5.07 | 1.64 | 2.47 | 0.41 | 16.58 | |

| M5 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.82 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 24.93 | 23.56 | 15.34 | 22.19 | 27.67 | |

| M6 lag 7 | 0.00 | 1.20 | 1.13 | 0.82 | 0.07 | 0.21 | 0.07 | 0.07 | 0.34 | 0.89 | 2.43 | 2.02 | 2.19 | 1.44 | 0.31 | 0.65 | 0.10 | 0.27 | 0.00 | 0.14 | 0.38 | 0.17 | 0.51 | 0.00 | |

| M6 lag 6 | 0.00 | 4.07 | 7.32 | 5.21 | 6.42 | 5.95 | 5.95 | 8.18 | 9.32 | 7.71 | 7.05 | 5.56 | 3.87 | 0.27 | 0.04 | 0.00 | 0.00 | 0.78 | 0.47 | 1.41 | 3.44 | 0.00 | 0.00 | 0.00 | |

| M6 lag 5 | 0.14 | 0.05 | 0.00 | 0.27 | 0.27 | 0.87 | 3.93 | 1.74 | 3.24 | 1.28 | 1.19 | 0.87 | 0.78 | 0.14 | 0.00 | 0.00 | 0.00 | 0.05 | 0.27 | 7.03 | 4.89 | 0.00 | 0.14 | 0.18 | |

| M6 lag 4 | 6.96 | 2.19 | 0.88 | 1.48 | 6.68 | 12.99 | 10.63 | 22.79 | 26.68 | 11.78 | 5.48 | 10.47 | 10.03 | 0.99 | 0.00 | 1.04 | 0.77 | 3.84 | 2.52 | 40.77 | 28.71 | 34.08 | 22.74 | 26.30 | |

| M6 lag 3 | 0.00 | 0.00 | 0.00 | 0.00 | 1.51 | 1.78 | 3.63 | 16.44 | 21.51 | 1.71 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.14 | 30.68 | 60.41 | 62.26 | 54.18 | 56.64 | 53.56 | |

| M6 lag 2 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.37 | 2.83 | 0.55 | 1.74 | 0.09 | 0.00 | 0.73 | 0.09 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 11.32 | 41.28 | 38.63 | 53.42 | 50.41 | 46.03 | |

| M6 lag 1 | 0.00 | 0.00 | 0.00 | 0.14 | 0.55 | 0.14 | 2.19 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 21.37 | 85.75 | 58.90 | 55.07 | 55.21 | 59.45 | |

| M6 lag 0 | 0.00 | 0.55 | 0.00 | 0.27 | 0.55 | 1.37 | 1.10 | 0.00 | 0.55 | 1.10 | 0.27 | 1.37 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 7.95 | 15.89 | 1.10 | 0.82 | 15.89 | |

| Day Peak Future | M2 lag 7 | 0.00 | 0.07 | 0.03 | 0.14 | 0.00 | 0.00 | 0.24 | 2.12 | 1.47 | 0.72 | 0.07 | 0.27 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.07 | 0.21 | 0.07 | 0.72 | 0.21 | 0.00 | 0.03 |

| M2 lag 6 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.20 | 0.00 | 0.00 | 0.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.47 | 0.04 | 0.27 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M2 lag 5 | 0.00 | 0.00 | 0.55 | 0.00 | 0.00 | 0.00 | 0.23 | 12.92 | 11.64 | 16.94 | 32.83 | 43.88 | 38.31 | 32.10 | 17.49 | 38.31 | 31.60 | 33.88 | 17.76 | 0.05 | 0.27 | 0.78 | 1.64 | 4.06 | |

| M2 lag 4 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.59 | 0.00 | 0.00 | 0.00 | 0.33 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.88 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M2 lag 3 | 0.00 | 0.00 | 0.00 | 0.48 | 2.26 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.14 | 0.00 | 0.07 | 0.00 | 0.00 | 0.07 | 0.55 | 0.07 | 0.00 | 0.00 | 0.00 | 0.62 | 0.48 | 2.53 | |

| M2 lag 2 | 0.00 | 0.00 | 0.18 | 0.91 | 5.66 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M2 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.10 | 1.23 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.14 | 0.00 | 0.00 | 0.00 | |

| M2 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 24.38 | 53.42 | 68.77 | 86.58 | 81.37 | 84.66 | 55.34 | 69.04 | 94.52 | 98.36 | 77.53 | 23.84 | 0.55 | 0.00 | 0.00 | 0.00 | |

| M3 lag 7 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.03 | 0.48 | 0.03 | 0.00 | 0.14 | 0.03 | 0.14 | 0.17 | 0.00 | 0.14 | 0.31 | 0.82 | 5.62 | 3.77 | 0.21 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M3 lag 6 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.04 | 1.60 | 0.90 | 0.20 | 0.16 | 0.04 | 0.20 | 0.08 | 0.00 | 0.16 | 1.06 | 0.74 | 3.29 | 4.19 | 0.00 | 0.31 | 2.62 | 0.78 | 10.18 | |

| M3 lag 5 | 0.00 | 0.00 | 0.00 | 0.00 | 0.91 | 0.05 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.10 | 2.01 | 0.05 | 0.41 | |

| M3 lag 4 | 0.00 | 0.00 | 0.00 | 0.00 | 2.68 | 0.33 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.05 | 0.38 | 0.00 | 0.00 | 0.00 | 0.16 | 12.93 | 0.55 | 5.32 | |

| M3 lag 3 | 0.00 | 0.00 | 0.00 | 0.07 | 0.00 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.34 | 2.60 | 0.27 | 0.89 | |

| M3 lag 2 | 0.00 | 0.18 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.09 | 0.09 | 0.00 | 1.19 | 13.97 | 5.75 | 0.18 | 0.73 | |

| M3 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 4.66 | 29.73 | 99.86 | 100 | 100 | 99.73 | 100 | 100 | 99.32 | 95.07 | 98.77 | 100 | 32.88 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M3 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 4.66 | 16.99 | 38.36 | 23.29 | 21.37 | 10.96 | 48.77 | 62.74 | 69.86 | 77.26 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M4 lag 7 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.88 | 0.00 | 0.38 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.24 | 0.24 | 0.03 | 0.00 | 0.00 | 0.03 | 0.03 | |

| M4 lag 6 | 0.00 | 0.00 | 0.00 | 0.00 | 0.55 | 0.12 | 3.84 | 1.57 | 1.25 | 0.00 | 1.10 | 0.16 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.08 | 0.00 | 0.00 | 0.27 | 0.51 | 0.08 | 1.33 | |

| M4 lag 5 | 0.00 | 0.00 | 0.00 | 0.09 | 0.32 | 0.23 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.41 | 3.42 | 0.18 | 1.42 | |

| M4 lag 4 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.05 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.44 | 0.05 | 0.00 | 0.27 | 0.38 | 0.00 | 0.00 | 0.00 | 0.71 | 0.00 | 0.00 | 0.00 | |

| M4 lag 3 | 0.00 | 0.00 | 0.00 | 0.00 | 0.62 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.58 | 0.00 | 0.07 | 0.41 | |

| M4 lag 2 | 0.00 | 0.18 | 0.00 | 0.46 | 0.55 | 0.00 | 0.00 | 0.00 | 28.77 | 80.64 | 61.37 | 74.61 | 86.58 | 92.88 | 94.43 | 94.52 | 94.06 | 74.79 | 54.98 | 19.63 | 0.09 | 0.00 | 0.09 | 0.00 | |

| M4 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 9.73 | 4.66 | 1.51 | 0.00 | 10.55 | 20.96 | 46.99 | 61.23 | 0.55 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M4 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 19.18 | 10.96 | 5.21 | 1.10 | 31.78 | 45.21 | 47.40 | 26.85 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M5 lag 7 | 0.00 | 0.00 | 0.00 | 0.00 | 0.03 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M5 lag 6 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.04 | 0.00 | 0.00 | 0.00 | 0.04 | 0.12 | |

| M5 lag 5 | 0.00 | 0.00 | 0.00 | 0.09 | 0.05 | 0.05 | 0.14 | 0.00 | 0.05 | 0.05 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.50 | 3.20 | 13.42 | 2.56 | 4.75 | |

| M5 lag 4 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M5 lag 3 | 0.00 | 0.21 | 0.00 | 0.68 | 6.23 | 6.71 | 3.22 | 5.89 | 24.45 | 70.82 | 96.10 | 95.75 | 97.47 | 97.53 | 88.90 | 98.42 | 98.63 | 99.79 | 85.48 | 59.86 | 0.55 | 0.00 | 0.00 | 0.00 | |

| M5 lag 2 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.55 | 0.00 | 0.18 | 0.82 | 5.84 | 56.71 | 16.07 | 0.18 | 0.00 | 0.91 | 17.44 | 49.50 | 56.07 | 0.64 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M5 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.41 | 0.14 | 0.00 | 0.00 | 1.64 | 10.68 | 58.08 | 65.75 | 5.07 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M5 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 2.74 | 1.64 | 19.45 | 1.92 | 0.00 | 0.00 | 6.03 | 11.51 | 27.95 | 22.47 | 20.55 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M6 lag 7 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.45 | 2.43 | 5.41 | 6.16 | 7.50 | 5.58 | 6.06 | 0.14 | 5.68 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M6 lag 6 | 0.00 | 0.00 | 0.00 | 0.00 | 0.04 | 0.20 | 0.00 | 0.00 | 0.16 | 5.87 | 10.37 | 13.39 | 20.82 | 13.58 | 11.19 | 8.81 | 12.37 | 3.25 | 4.50 | 0.23 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M6 lag 5 | 0.00 | 0.00 | 0.00 | 0.14 | 2.69 | 0.27 | 0.00 | 0.14 | 0.18 | 9.82 | 13.38 | 10.46 | 15.11 | 15.07 | 15.34 | 15.34 | 15.66 | 13.15 | 13.93 | 2.37 | 0.09 | 0.00 | 0.00 | 0.00 | |

| M6 lag 4 | 1.48 | 0.05 | 0.00 | 0.05 | 0.71 | 1.92 | 5.48 | 13.42 | 26.79 | 27.07 | 29.48 | 33.92 | 49.53 | 33.10 | 24.88 | 48.38 | 61.10 | 71.84 | 52.93 | 6.90 | 0.22 | 0.00 | 0.00 | 0.00 | |

| M6 lag 3 | 0.00 | 0.00 | 0.00 | 0.00 | 0.75 | 0.41 | 0.00 | 0.00 | 0.00 | 8.49 | 5.75 | 10.14 | 0.00 | 0.00 | 0.00 | 0.00 | 0.07 | 40.41 | 42.47 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M6 lag 2 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 | 0.00 | 0.09 | 0.64 | 0.09 | 0.00 | 0.00 | 0.00 | 1.19 | 34.52 | 28.86 | 2.47 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M6 lag 1 | 0.00 | 0.14 | 0.00 | 0.00 | 1.10 | 0.27 | 7.67 | 1.92 | 0.14 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.55 | 72.05 | 60.68 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M6 lag 0 | 0.00 | 0.00 | 0.00 | 0.55 | 3.84 | 1.37 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.92 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 7.40 | 20.55 | 21.10 | 0.55 | 0.00 | 0.00 | 0.00 |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | 19 | 20 | 21 | 22 | 23 | 24 | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Week Base Future | M3 lag 3 | 8.41 | 3.01 | 22.50 | 52.24 | 21.80 | 0.31 | 0.20 | 6.16 | 5.42 | 1.84 | 0.24 | 0.47 | 0.05 | 0.01 | 0.00 | 0.15 | 0.01 | 1.33 | 0.78 | 5.49 | 6.08 | 9.69 | 47.02 | 3.61 |

| M3 lag 2 | 0.18 | 32.42 | 55.06 | 57.32 | 52.86 | 22.03 | 15.23 | 40.89 | 30.64 | 13.89 | 6.72 | 9.68 | 1.04 | 0.84 | 0.30 | 0.02 | 0.00 | 0.55 | 0.47 | 0.00 | 0.02 | 0.00 | 1.92 | 1.08 | |

| M3 lag 1 | 0.20 | 0.22 | 0.57 | 0.17 | 0.15 | 0.00 | 0.00 | 0.00 | 0.02 | 0.00 | 0.00 | 0.47 | 0.00 | 0.02 | 0.05 | 0.02 | 0.10 | 0.05 | 0.00 | 1.02 | 6.26 | 0.62 | 4.04 | 7.00 | |

| M3 lag 0 | 0.89 | 0.00 | 0.14 | 1.65 | 6.18 | 17.23 | 18.94 | 30.20 | 29.92 | 23.68 | 10.57 | 9.13 | 4.53 | 4.60 | 4.19 | 7.82 | 11.53 | 15.44 | 15.03 | 33.15 | 26.22 | 13.32 | 12.77 | 14.89 | |

| M10 lag 3 | 7.02 | 45.08 | 30.99 | 21.73 | 18.12 | 13.86 | 1.90 | 4.76 | 0.49 | 0.14 | 0.00 | 0.00 | 0.08 | 0.00 | 0.00 | 0.54 | 9.07 | 4.23 | 8.73 | 9.09 | 17.99 | 30.54 | 34.64 | 16.56 | |

| M10 lag 2 | 0.00 | 4.57 | 17.36 | 0.37 | 0.62 | 0.26 | 0.00 | 0.00 | 0.00 | 0.00 | 0.26 | 0.44 | 0.62 | 0.00 | 0.15 | 0.00 | 0.00 | 0.30 | 4.42 | 3.67 | 5.86 | 5.36 | 3.90 | 0.14 | |

| M10 lag 1 | 0.37 | 0.00 | 0.00 | 0.00 | 0.00 | 2.72 | 1.74 | 4.11 | 5.18 | 6.66 | 3.91 | 2.79 | 2.74 | 0.42 | 0.00 | 1.79 | 4.49 | 25.62 | 45.49 | 47.83 | 42.97 | 21.81 | 35.34 | 22.61 | |

| M10 lag 0 | 1.51 | 0.00 | 0.00 | 0.00 | 0.00 | 2.75 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.07 | 0.48 | 1.78 | 3.09 | 7.21 | 2.68 | 14.62 | 13.38 | 30.40 | |

| M17 lag 3 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.02 | 0.00 | 0.10 | 0.00 | 0.22 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.15 | 0.00 | 0.01 | 0.01 | 0.47 | 0.01 | |

| M17 lag 2 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 3.58 | 6.05 | 8.18 | 10.81 | 9.61 | 7.80 | 7.22 | 6.09 | 3.82 | 7.23 | 10.55 | 22.13 | 30.20 | 33.53 | 36.10 | 11.30 | 23.30 | 11.30 | |

| M17 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.15 | 0.00 | 0.02 | 0.40 | 8.18 | 4.91 | 3.29 | 0.50 | 0.00 | 0.00 | 0.10 | 2.97 | 38.43 | 43.74 | 53.76 | 58.35 | 56.33 | 62.89 | 54.79 | |

| M17 lag 0 | 0.00 | 0.34 | 1.30 | 0.69 | 0.00 | 0.00 | 0.00 | 0.27 | 0.00 | 0.00 | 0.07 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.14 | 0.21 | 11.26 | 34.11 | 44.54 | 34.73 | 2.68 | |

| M24 lag 3 | 0.88 | 0.00 | 0.00 | 0.00 | 0.00 | 13.60 | 2.13 | 15.94 | 41.12 | 44.52 | 36.14 | 37.02 | 43.24 | 52.99 | 52.31 | 54.92 | 56.24 | 39.15 | 53.34 | 55.32 | 48.67 | 37.90 | 31.14 | 29.51 | |

| M24 lag 2 | 0.20 | 0.00 | 0.49 | 2.89 | 0.26 | 17.69 | 0.37 | 0.00 | 0.11 | 3.20 | 2.53 | 1.63 | 0.55 | 0.00 | 0.00 | 0.00 | 0.00 | 0.73 | 7.16 | 15.64 | 27.07 | 42.01 | 31.31 | 42.88 | |

| M24 lag 1 | 0.00 | 0.07 | 7.53 | 13.96 | 13.56 | 3.27 | 0.30 | 0.15 | 0.00 | 1.02 | 0.20 | 0.05 | 0.00 | 0.00 | 0.00 | 0.00 | 0.07 | 0.02 | 0.55 | 0.10 | 0.50 | 2.04 | 2.54 | 0.00 | |

| M24 lag 0 | 0.00 | 0.34 | 2.26 | 11.60 | 23.34 | 14.21 | 4.74 | 1.65 | 5.90 | 0.14 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | 0.07 | 0.21 | 0.00 | 0.55 | 0.41 | 10.43 | 0.82 | 4.87 | 0.41 | |

| Week Peak Future | M3 lag 3 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 6.57 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.05 | 0.00 | 0.01 | 1.55 | 3.95 | 14.33 | 38.99 | 49.08 | 38.93 | 43.59 | 38.66 | 45.09 |

| M3 lag 2 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.05 | 1.87 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.03 | 0.02 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.17 | 0.12 | |

| M3 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.50 | 1.42 | 0.15 | 0.52 | 0.90 | 0.37 | 0.17 | 0.00 | 0.00 | 0.12 | 0.15 | 0.00 | 0.00 | 0.00 | 0.35 | 0.00 | 0.00 | 0.00 | |

| M3 lag 0 | 0.00 | 0.14 | 1.51 | 0.89 | 12.77 | 10.57 | 28.41 | 94.30 | 98.01 | 99.93 | 97.94 | 65.68 | 41.11 | 38.23 | 35.07 | 37.89 | 37.06 | 48.52 | 32.53 | 37.27 | 31.98 | 13.18 | 0.14 | 2.68 | |

| M10 lag 3 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 13.91 | 10.36 | 1.69 | 0.00 | 1.24 | 1.44 | 5.37 | 3.85 | 1.38 | 1.56 | 4.42 | 9.53 | 1.26 | 4.10 | 11.08 | 9.82 | 3.49 | 0.18 | 2.30 | |

| M10 lag 2 | 0.00 | 0.00 | 0.00 | 0.11 | 1.07 | 2.66 | 17.36 | 0.02 | 0.44 | 0.15 | 0.14 | 1.48 | 1.32 | 1.02 | 0.20 | 0.12 | 0.05 | 0.12 | 3.17 | 2.82 | 6.94 | 2.62 | 0.00 | 0.00 | |

| M10 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 8.47 | 21.78 | 39.83 | 55.33 | 47.88 | 44.44 | 43.84 | 43.42 | 31.43 | 32.38 | 29.41 | 41.20 | 42.77 | 43.64 | 28.27 | 30.86 | 10.14 | 1.25 | 0.00 | 0.00 | |

| M10 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 2.88 | 0.07 | 0.07 | 0.41 | 0.07 | 0.21 | 0.14 | 0.00 | 0.07 | 1.99 | 0.89 | 0.07 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.14 | |

| M17 lag 3 | 0.00 | 0.00 | 0.08 | 0.23 | 9.13 | 3.77 | 1.29 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.01 | 0.04 | 0.00 | 0.00 | 0.03 | 0.00 | 0.33 | 3.15 | 0.00 | 0.00 | |

| M17 lag 2 | 0.00 | 1.60 | 0.85 | 0.11 | 6.18 | 23.42 | 59.78 | 34.73 | 33.84 | 44.13 | 45.49 | 51.52 | 45.73 | 41.51 | 43.60 | 42.13 | 39.07 | 24.44 | 21.20 | 22.87 | 19.80 | 0.00 | 0.00 | 0.00 | |

| M17 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.05 | 0.00 | 0.17 | 0.47 | 0.55 | 0.67 | 3.44 | 8.10 | 14.08 | 20.64 | 36.96 | 22.81 | 16.55 | 1.45 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M17 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.07 | 4.12 | 21.69 | 29.31 | 29.51 | 20.45 | 1.30 | 4.46 | 0.27 | 2.75 | 0.07 | 5.15 | 18.87 | 0.55 | 0.00 | 0.00 | |

| M24 lag 3 | 0.00 | 3.68 | 0.77 | 0.00 | 7.14 | 29.22 | 79.91 | 79.29 | 56.56 | 32.00 | 30.50 | 27.48 | 29.57 | 49.74 | 53.83 | 52.49 | 47.53 | 49.28 | 50.38 | 33.96 | 17.13 | 4.13 | 0.00 | 0.00 | |

| M24 lag 2 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 12.05 | 9.00 | 0.65 | 1.43 | 3.46 | 8.62 | 3.88 | 7.37 | 3.50 | 5.88 | 13.95 | 28.22 | 26.68 | 17.94 | 2.04 | 2.80 | 0.26 | 0.00 | 0.00 | |

| M24 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.12 | 6.46 | 20.61 | 36.22 | 25.90 | 15.65 | 1.35 | 0.30 | 0.02 | 27.34 | 10.14 | 4.31 | 9.15 | 1.60 | 0.00 | 0.00 | |

| M24 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.34 | 0.00 | 0.00 | 0.00 | 0.00 | 0.14 | 0.00 | 0.21 | 2.81 | 0.00 | 0.00 | 0.00 | |

| Weekend Base Future | M1 lag 1 | 1.48 | 0.77 | 0.11 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.16 | 0.00 | 0.38 | 0.11 | 0.27 | 0.00 | 0.05 | 0.00 |

| M1 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M2 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.91 | 0.00 | 0.00 | 0.00 | 0.14 | 0.00 | 0.46 | 0.05 | 0.14 | 0.78 | 1.28 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M2 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.64 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.91 | 3.82 | 15.29 | |

| M3 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.43 | 0.00 | 0.98 | 0.00 | 0.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M3 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.64 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.32 | 0.32 | 3.51 | |

| M4 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.03 | 0.48 | 0.03 | 1.44 | 0.65 | 1.16 | 1.34 | 1.82 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M4 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.19 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.96 | 0.38 | 4.41 | |

| M5 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.06 | 0.00 | 0.00 | 0.06 | 0.03 | 0.21 | 0.18 | 0.33 | 0.21 | 2.56 | 0.88 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M5 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.77 | |

| M8 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.02 | 0.16 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.05 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.09 | 0.00 | 0.00 | 0.00 | 0.00 | 0.02 | 0.00 | |

| M8 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| M9 lag 1 | 0.00 | 1.37 | 8.95 | 12.56 | 18.31 | 24.44 | 35.56 | 23.00 | 8.36 | 8.64 | 4.99 | 4.51 | 1.52 | 0.72 | 0.21 | 1.52 | 7.31 | 4.55 | 0.63 | 0.06 | 2.36 | 0.88 | 0.91 | 1.85 | |

| M9 lag 0 | 0.00 | 0.00 | 0.00 | 0.00 | 7.16 | 14.74 | 22.22 | 6.11 | 0.18 | 0.00 | 1.00 | 0.87 | 11.31 | 8.03 | 8.67 | 14.60 | 6.25 | 0.00 | 0.05 | 0.00 | 0.59 | 7.98 | 0.14 | 0.50 | |

| M10 lag 1 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.27 | 6.07 | 2.48 | 0.39 | 0.37 | 0.31 | 8.82 | 15.14 | 16.22 | 16.85 | 15.57 | 0.67 | 0.33 | 0.16 | 0.84 | 1.62 | 0.61 | 0.37 | |

| M10 lag 0 | 0.00 | 0.00 | 0.63 | 2.70 | 4.81 | 10.88 | 14.51 | 9.94 | 0.94 | 0.00 | 0.00 | 0.00 | 0.35 | 1.06 | 0.98 | 6.38 | 0.90 | 0.16 | 0.04 | 0.47 | 6.77 | 13.73 | 4.15 | 4.38 | |