Moment Explosions in the Rough Heston Model

Abstract.

We show that the moment explosion time in the rough Heston model [El Euch, Rosenbaum 2016, arxiv:1609.02108] is finite if and only if it is finite for the classical Heston model. Upper and lower bounds for the explosion time are established, as well as an algorithm to compute the explosion time (under some restrictions). We show that the critical moments are finite for all maturities. For negative correlation, we apply our algorithm for the moment explosion time to compute the lower critical moment.

2010 Mathematics Subject Classification:

91G20,45D051. Introduction

It has long been known that the marginal distributions of a realistic asset price model should not feature tails that are too thin (as, e.g., in the Black-Scholes model). In many models that have been proposed, the tails are of power law type. Consequently, not all moments of the asset price are finite. Existence of the moments has been thoroughly investigated for classical models; in particular, we mention here Keller-Ressel’s work [20] on affine stochastic volatility models. Precise information on the critical moments – the exponents where the stock price ceases to be integrable, depending on maturity – is of interest for several reasons. It allows to approximate the wing behavior of the volatility smile, to assess the convergence rate of some numerical procedures, and to identify models that would assign infinite prices to certain financial products. We refer to [3, 20] and the article Moment Explosions in [8] for further details and references on these motivations. Moreover, when using the Fourier representation to price options, choosing a good integration path (equivalently, a good damping parameter) to avoid highly oscillatory integrands requires knowing the strip of analyticity of the characteristic function. Its boundaries are described by the critical moments [24, 26].

In recent years, attention has shifted in financial modeling from the classical (jump-)diffusion and Lévy models to rough volatility models. Since the pioneering work by Gatheral et al. [15], the literature on these non-Markovian stochastic volatility models, inspired by fractional Brownian motion, has grown rapidly. We refer, e.g., to Bayer et al. [4] for many references. In the present paper we provide some results on the explosion time and the critical moments of the rough Heston model. While there are several “rough” variants of the Heston model, we work with the one proposed by El Euch and Rosenbaum [9]. The dynamics of this model are given by

where and are correlated Brownian motions, , and are positive parameters. The smoothness parameter is in . (For , the model clearly reduces to the classical Heston model.) Besides having a microstructural foundation, this model features a characteristic function that can be evaluated numerically in an efficient way, by solving a fractional Riccati equation (equivalently, a non-linear Volterra integral equation; see Section 2). Its tractability makes the rough Heston model attractive for practical implementation, and at the same time facilitates our analysis.

We first analyze the explosion time, i.e., the maturity at which a fixed moment explodes. While the explosion time of the classical Heston model has an explicit formula, for rough Heston we arrive at a well-known hard problem: Computing the explosion time of the solution of a non-linear Volterra integral equation (VIE) of the second kind. There is no general algorithm known, and in most cases that have been studied in the literature, only bounds are available. See Roberts [30] for an overview. Using the specific structure of our case, we show that the explosion time is finite if and only if it is finite for the classical Heston model, and we provide a lower and an upper bound (Sections 3–5). As a byproduct, the validity of the fractional Riccati equation, respectively the VIE, for all moments is established, which culminates in Section 6. In Section 7 we derive an algorithm to compute the explosion time, under some restrictions on the parameters. The critical moments are finite for all maturities (Section 8) and can be computed by numerical root finding (Section 9). Our approach has two limitations: First, to compute the critical moments, maturity must not be too high. Second, our algorithm can compute the upper critical moment only for , and the lower critical moment for . As the latter is the more important case in practice, we focus on the left wing of implied volatility when recalling the relation between critical moments and strike asymptotics (Lee’s moment formula; see Section 10).

Corollary 3.1 in [10] is related to our results. For each maturity, it gives explicit lower and upper bounds for the critical moments. Inverting them yields a lower bound for the explosion time; the latter is not comparable to our bounds.

2. Preliminaries

El Euch and Rosenbaum [9] established a semi-explicit representation of the moment generating function (mgf) of the log-price in the rough Heston model. The mgf is given by

| (2.1) |

where satisfies a fractional Riccati differential equation (see below). The constraint from [9] was removed recently in [10]. The paper [2] contains an alternative derivation of the fractional Riccati equation, and [1] has more general results, embedding the rough Heston model into the new class of affine Volterra processes. Recall the following definition (see e.g. [21]):

Definition 2.1.

The (left-sided) Riemann-Liouville fractional integral of order of a function is given by

| (2.2) |

whenever the integral exists, and the (left-sided) Riemann-Liouville fractional derivative of order of is given by

| (2.3) |

whenever this expression exists.

(The fractional derivative can be defined for as well, but this is not needed in our context.) The function from (2.1) is the unique continuous solution of the fractional Riccati initial value problem

| (2.4) | ||||

| (2.5) |

where is defined as

| (2.6) |

with coefficients

For , this becomes a standard Riccati differential equation, which admits a well-known explicit solution [14, Chapter 2]. The roots of are located at the points with

| (2.7) | ||||

| (2.8) |

The following result, relating fractional differential equations and Volterra integral equations, is a special case of Theorem 3.10 in [21].

Theorem 2.2.

Let , and suppose that and . Then satisfies the fractional differential equation

if and only if it satisfies the Volterra integral equation (VIE)

Using Theorem 2.2, the Riccati differential equation (2.4) with initial value (2.5) can be transformed into the non-linear Volterra integral equation

This integral equation was used in [9] to compute numerically. The function

solves

| (2.9) |

with non-linearity

| (2.10) |

where and are defined in (2.7) and (2.8). Equation (2.9) is a nonlinear Volterra integral equation with weakly singular kernel; it will be used to analyze the blow-up behavior of (and thus of ) in Section 3. We quote the following standard existence and uniqueness result for equations of this kind.

Theorem 2.3.

Let , , and suppose that is locally Lipschitz continuous. Then there is such that the Volterra integral equation

has a unique continuous solution on , and there is no continuous solution on any larger right-open interval .

Proof.

In [9], the fractional Riccati equation was established for , whereas we are interested in . The justification of (2.4)–(2.5), and thus of (2.9), for hinges on a result from [10] and the analytic dependence of on . See Sections 5 and 6 for details. We write

| (2.11) |

for the moment explosion time in the rough Heston model. In the classical case (), the explicit expression

| (2.12) | ||||

| (2.13) |

has been found by Andersen and Piterbarg [3] (see also [20]). It is a consequence of the explicit characteristic function, which is not available for the rough Heston model. We distinguish between the following cases for :

-

(A)

,

-

(B)

, and

-

(C)

, and

-

(D)

As several of our results deal with and satisfying case (A), we explicitly note

Note that cases (A) and (B) combined are exactly the cases in which the moment explosion time in the classical Heston model is finite, by (2.13). We can now state our first main result.

Theorem 2.4.

For , the moment explosion time of the rough Heston model is finite if and only if satisfies (A) or (B). This is equivalent to (explosion time of the classical Heston model) being finite.

The proof of Theorem 2.4 consists of two main parts. First, Propositions 3.2, 3.4, 3.6, and 3.7 discuss the blow-up behavior of the solution of (2.9) in cases (A)-(D), and Lemma 3.8 shows that blow-up of leads (unsurprisingly) to blow-up of the right-hand side of (2.1). Second, we show in Section 5 that the explosion time of (the solution of (2.9)) agrees with (the explosion time of the rough Heston model) for all . As mentioned after Theorem 2.3, this is not obvious from the results in the existing literature.

3. Explosion time of the Volterra integral equation

We begin by citing a result from Brunner and Yang [7] which characterizes the blow-up behavior of non-linear Volterra integral equations defined by positive and increasing functions. We note that some arguments in our subsequent proofs (from Proposition 3.2 onwards) are similar to arguments used in [7]. Alternatively, it should be possible to extend the arguments in Appendix A of [16]; there, is in .

Proposition 3.1.

Assume that is continuous and the following conditions hold:

-

(G1)

and is strictly increasing,

-

(G2)

,

-

(P)

is a positive, non-decreasing, continuous function,

-

(K)

is locally integrable and is a non-decreasing function.

Furthermore, assume and with and . Then the solution of the Volterra integral equation

blows up in finite time if and only if

| (3.1) |

for all .

Proof.

This is a special case of Corollary 2.22 in Brunner and Yang [7], with not depending on time. ∎

In case (A), all assumptions of Proposition 3.1 are satisfied and only the integrability condition (3.1) has to be checked to determine whether the solution of (2.9) blows up in finite time.

Proposition 3.2.

Proof.

Fix such that and . Note that in this case. (Here and in the following, we will often suppress in the notation.) If we write the Volterra integral equation (2.9) in the form

with non-linearity and , using (2.10) and (7.3), then the conditions and guarantee that and are positive and strictly increasing on with . Hence, the solution is positive for positive values, and . (Positivity follows from Lemma 2.4 in [7], or from Lemma 3.2.11 in [6].) It is easy to check that all the assumptions (G1), (G2), (P) and (K) of Proposition 3.1 are satisfied. Moreover, and

for all . By Proposition 3.1, the solution blows up in finite time. ∎

In case (B), Proposition 3.1 cannot be applied directly to the solution of (2.9). Hence, the Volterra integral equation has to be modified in order to satisfy the assumptions of Proposition 3.1 in a way that is still a subsolution of the modified equation, i.e. satisfies (2.9) with “” instead of “”. First, we provide a comparison lemma for solutions and subsolutions.

Lemma 3.3.

Let be a strictly increasing, continuous function and . Suppose that is the unique continuous solution of the Volterra integral equation

where satisfies condition (K) from Proposition 3.1. If is a continuous subsolution,

then holds for all .

Proof.

For any define for . From the positivity of , it follows that and

Since , it follows that . We want to show on the whole interval . Therefore, suppose that exists such that for all and . However, because is strictly increasing, we have

which is a contradiction. Hence, the inequality holds for all . Since was arbitrary, the result follows easily. ∎

Proposition 3.4.

Proof.

Fix such that , and . Note that in this case, the non-linearity is obviously positive by (2.10). However, is strictly decreasing on . To deal with this problem, let and define the modified non-linearity as

| (3.2) |

Then is a positive, strictly increasing, Lipschitz continuous function that starts at and . Let be the unique continuous solution (recall Theorem 2.3) of the Volterra integral equation

| (3.3) |

with and . Note that the second equality in (3.3) follows from (7.3). Due to the positivity of and on , the solution is positive on as well. The functions , and satisfy the assumptions (G1), (G2), (P) and (K) in Proposition 3.1. Furthermore, and satisfies (3.1). By Proposition 3.1, blows up in finite time. Because satisfies (2.9) and , it follows that is a subsolution of the modified Volterra integral equation, i.e.,

Now, Lemma 3.3 implies . Consequently, blows up as well. ∎

Cases (C) and (D) are the cases where the solution of (2.9) does not blow up in finite time. In fact, does not blow up at all, as we will see. The following lemma provides the key argument for both cases.

Lemma 3.5.

Let be a Lipschitz continuous function that is positive on and on for an . Then the unique continuous solution of the Volterra integral equation

satisfies for all .

Proof.

The non-negativity of implies . Suppose exists such that . By the continuity of , there exists that satisfies and for all . From on , we have

Since is non-negative and is decreasing,

which is a contradiction. Therefore, satisfies for all . ∎

Proposition 3.6.

Proof.

Fix such that , and . Note that the inequality implies . Moreover, from (2.10), it follows that is the smallest positive root of . Define the non-linearity as

Then is a non-negative, Lipschitz continuous function that starts at . Therefore, Lemma 3.5 yields that the unique continuous solution of

is bounded with for all . Since on , the function solves the original Volterra integral equation

and from the uniqueness of the solution we obtain . ∎

Proposition 3.7.

Proof.

Fix such that , which is equivalent to . Note that implies . Moreover, from (2.10), it follows that is the smallest positive root of . Define , which satisfies

| (3.4) |

If we define the non-linearity as

then is a non-negative, Lipschitz continuous function that starts at . With Lemma 3.5 we obtain that the unique continuous solution of

is bounded with for all . Furthermore, solves (3.4) because for all . The uniqueness of the solution yields

Hence, the solution is bounded with . ∎

We have shown that (A) and (B) are exactly the cases in which the solution of the Volterra integral equation (2.9), and thus the solution of the fractional Riccati differential equation (2.4) with initial value (2.5), blows up in finite time. The following lemma shows that blow-up of is equivalent to blow-up of the right-hand side of (2.1).

Lemma 3.8.

If is a non-negative, continuous function that blows up in finite time with explosion time , then blows up in finite time as well, with the same explosion time . If is a bounded continuous function, then does not blow up in finite time.

Proof.

First, suppose that the non-negative, continuous function explodes at and let . Then we can find such that for all . Hence,

for all . For the second assertion, suppose that is continuous and bounded with . Then we have

for all . ∎

4. Bounds for the explosion time

We now establish lower and upper bounds for , valid whenever it is finite (cases (A) and (B)). We denote by the explosion time of the solution of (2.9). As we will see later, it agrees with , and so both bounds of this section hold for the explosion time of the rough Heston model. We prove them first, because we will apply the lower bound in the proof of .

Theorem 4.1.

Proof.

Fix satisfying the requirements of case (A) or (B). It follows from Propositions 3.2 and 3.4 that in either case the solution is non-negative, starts at and . For any choose

with and . Using the inequality for , the non-negativity of and that is strictly increasing on , we have for

Thus, we obtain for

Finally,

Maximization over , then , and the substitution yield the inequality (4.1). ∎

For , the right-hand side of (4.1) simplifies to

| (4.2) |

In case (A), the lower bound (4.1) is sharp in the limit : We have then, and therefore (4.2) is exactly the moment explosion time (2.12) of the classical Heston model.

Another lower bound for can be obtained from Corollary 3.1 in [10]. Numerical examples show that it is not comparable to the bound from our Theorem 4.1.

Theorem 4.2.

Proof.

Fix satisfying the requirements of case (A) or (B). From Propositions 3.2 and 3.4, in either case the solution is positive on , starts at and . For any choose

| (4.4) |

with and . Define in case (A) and from (3.2) in case (B). Since and is positive and strictly increasing, we have for

Thus, we obtain for

Therefore,

Note that from the definition of , it depends on and . The fact that is only zero at implies that as . Taking the limit , then minimizing over and substitution yields

In case (A), we are finished. In case (B), we have . Then the dominated convergence theorem for yields the inequality (4.3). ∎

5. Explosion time in the rough Heston model

In Section 3, we established that the right-hand side of (2.1), defined using the solution of the VIE (2.9), explodes if and only if satisfies the conditions of cases (A) or (B). As before, we write for the explosion time of . Recall that denotes the explosion time of the rough Heston model, as defined in (2.11). The goal of the present section is to show that , and that (2.1) holds for all and . The following result from [10] was already mentioned at the end of the introduction.

Lemma 5.1 (Corollary 3.1 in [10]).

For each , there is an open interval such that (2.1) holds for all from that interval.

Lemma 5.2.

The solution of the Volterra integral equation (2.9) is differentiable w.r.t. , and its derivative satisfies

| (5.1) |

Proof.

Lemma 5.3.

-

(i)

In case (A) we have for and for .

-

(ii)

If satisfies case (B), then the same holds if is sufficiently small.

Proof.

We only discuss the case , because is analogous.

(i) Note that (5.1) is a “linear VIE” that can be written as

| (5.2) |

where we define

| (5.3) | ||||

| (5.4) |

to bring the notation close to that of Section 6.1.2 in [5]. Clearly, (5.2) is not really a linear VIE, because the unknown function appears in and . But as our aim is not to solve it, but to control the sign of , this viewpoint is good enough.

As we are in case (A), we get from and that . Furthermore, we have , and therefore

since and by Proposition 3.2. From this we obtain , and hence for all . By Theorem 6.1.2 of Brunner [5], we can express the solution of (5.1) with the resolvent kernel ,

| (5.5) |

The resolvent kernel has the explicit representation (see [5])

| (5.6) |

where

| (5.7) |

From this representation of the resolvent kernel, and the fact that (5.4) is non-negative in case (A), it is obvious that . Since we thus conclude from (5.5) that for all .

(ii) Recall that we assume that , because is analogous. We have to show that

| (5.8) |

satisfies . We use the following facts: for large, for large, and explodes as . Thus, from (5.3) satisfies

| (5.9) |

and satisfies . We can therefore pick such that

For and any satisfying , we have

Using this observation in (5.7), we see from a straightforward induction proof that

The same then holds for the resolvent kernel (5.6),

| (5.10) |

By (5.5), we obtain

| (5.11) |

Now note that

| (5.12) |

where the right-hand side is positive. Indeed, (5.12) follows from (5.9) and (5.10), as on the left-hand side of (5.12) is . Thus, letting , we find that the negative terms on the right-hand side of (5.11) dominate. This completes the proof. ∎

Lemma 5.4.

Let and . Then is analytic at .

Proof.

According to Section 3.1.1 in [6], the solution can be constructed by successive iteration and continuation. We just show that the first iteration step leads to an analytic function, because the finitely many further steps needed to arrive at arbitrary can be dealt with analogously. Define the iterates and

On a sufficiently small time interval, converges uniformly to , and the solution can then be continued by solving an updated integral equation and so on (see [6]), until we hit . Now fix and as in the statement of the lemma. For a sufficiently small open complex neighborhood , it is easy to see that holds for . Define

Then there is such that, for arbitrary and ,

By the definition of , a trivial inductive proof then shows that

| (5.13) |

By a standard result on parameter integrals (Theorem IV.5.8 in [11]), the bound (5.13) implies that each function is analytic in . From the bounds in Section 3.1.1 of [6], it is very easy to see that the convergence is locally uniform w.r.t. for fixed . It is well known (see Theorem 3.5.1 in [18]) that this implies that the limit function is analytic. ∎

Lemma 5.5.

The function increases for and decreases for .

Proof.

Recall that in cases (C) and (D), which include . For case (A), the assertion follows from part (i) of Lemma 5.3. So let satisfy case (B), where again we assume w.l.o.g. that . Suppose that does not increase. Then we can pick such that any left neighborhood of contains a point with . From the continuity of (see Lemma 5.4), part (ii) of Lemma 5.3, and the continuity of from (5.8), there are satisfying and such that in the rectangle

Then, implies that

| (5.14) |

because the inequality shows that must explode at least as fast as . But (5.14) is a contradiction to . ∎

Proof.

We assume that , as is handled analogously. By Lemma 5.5, increases. In this proof, we write for the right-hand side of (2.1), and for the mgf. Now fix and such that has positive distance from the graph of the increasing function . Clearly, it suffices to consider pairs with this property. By Lemma 5.1, there are such that

| (5.15) |

We now show that (5.15) extends to by analytic continuation. From general results on characteristic functions (Theorems II.5a and II.5b in [34]), is analytic in a vertical strip of the complex plane, and has a singularity at . If we suppose that , then Lemma 5.4 leads to a contradiction: The left-hand side of (5.15) would then be analytic at , and the right-hand side singular. This shows that (5.15) can be extended to the left up to by analytic continuation. ∎

The following theorem completes the proof of Theorem 2.4.

Theorem 5.7.

Let . Then , and (2.1) holds for .

Proof.

For later use (Section 9), we give the following alternative argument:

Another proof that .

Let us suppose that there is with . From Theorem 4.1, it is easy to see that the continuous function tends to as approaches the region where . Thus, there is with .

We have seen in Lemma 5.4 that is analytic for any fixed . But it is also analytic w.r.t. for fixed : From Theorem 1 in Lubich [27], itself based on earlier work by Miller and Feldstein [28], it follows that is analytic on the whole interval . By Hartogs’s theorem (Theorem 1.2.5 in [22]), we conclude that the bivariate function is continuous. Thus, the blow-up of at implies that

| (5.16) |

(Again, we write for the right-hand side of (2.1) and for the mgf.) By Lemma 5.6, also blows up there, and thus has a singularity at . Since , we conclude from Corollary II.1b in [34] that . As is a martingale, this implies that for all . In particular, it contradicts . ∎

6. Validity of the fractional Riccati equation for complex

Although the focus of this paper is on real , the mgf needs to be evaluated at complex arguments when used for option pricing. The following result fully justifies using the fractional Riccati equation (2.4), respectively the VIE (2.9), to do so. As above, we write for the moment explosion time of , and for the explosion time of the VIE (2.9).

Theorem 6.1.

Let . Then , and (2.1) holds for .

Lemma 6.2.

Let . Then .

Proof.

Proof of Theorem 6.1.

The first statement is clear from . Now let be arbitrary. As above, we write for the mgf and for the right-hand side of (2.1). By Theorem 5.7, we have for in the real interval

The function is analytic on the strip

| (6.1) |

By the same argument as in Lemma 5.4, the function is analytic on the set , which contains the strip (6.1) by Lemma 6.2. Therefore, and agree on (6.1) by analytic continuation. This implies the assertion. ∎

7. Computing the explosion time

Recall that, for fixed , the explosion time of the rough Heston model is the blow-up time of , where solves the fractional Riccati initial value problem (2.4)–(2.5). We know from Theorem 2.4 that exactly in the cases (A) and (B), defined in Section 2. We now develop a method (Algorithm 7.5) to compute for satisfying the conditions of case (A). In case (B), a lower bound can be computed, which is sometimes sharper than the explicit bound (4.1). The function satisfies the fractional Riccati equation

| (7.1) |

where and , with initial condition . (Recall that we often suppress the dependence on in the notation.) We try a fractional power series ansatz

| (7.2) |

with unknown coefficients .

Lemma 7.1.

(see e.g. [21]) Let . The fractional integral and derivative of power functions are given by

| (7.3) | ||||

| (7.4) |

By (7.3), the fractional power series (7.2) (formally) satisfies the initial condition (2.5). Inserting (7.2) into (7.1) and using (7.4), we obtain

| (7.5) |

where

Note that is an increasing sequence; this follows easily from the fact that is convex (see Example 11.14 in [32]). By Stirling’s formula, for . From (7.5), we obtain a convolution recurrence for :

| (7.6) | ||||

| (7.7) |

The function can thus be expressed as , where

Lemma 7.2.

Let , satisfying case (A) (recall the definition in Section 2). Then is analytic at zero, with a positive and finite radius of convergence .

Proof.

To see that the radius of convergence is positive, we show that there is such that

| (7.8) |

(Adding the factor to this geometric bound facilitates the inductive proof.) We have

Choose such that the left-hand side is for all , and such that for all . The latter is possible because . Fix a number with and such that holds for . Let and assume, inductively, that holds for . From the recurrence (7.7), we then obtain

Since is a strictly convex function of on with minimum at , it is easy to see that

where the last equality follows from the well-known representation of the beta function in terms of the gamma function (see 12.41 in [33]). We conclude

This completes the inductive proof of (7.8).

The finiteness of the radius of convergence will follow from the existence of a number such that

| (7.9) |

To this end, define

By Stirling’s formula, we have as , and so eventually increases. Let be such that increases for , and define

This number satisfies for by definition. Let us fix some and assume, inductively, that holds for . By (7.7)

Thus, (7.9) is proved by induction. ∎

From the estimates in Lemma 7.2, it is clear that termwise fractional derivation of the series (7.2) is allowed, and so the right-hand side of (7.2) really represents the solution of (7.1) with initial condition , as long as satisfies . We proceed to show how the explosion time can be computed from the coefficients . The essential fact is that there is no gap between and . For this, we require the following classical result from complex analysis ([29], p. 235).

Theorem 7.3 (Pringsheim’s theorem, 1894).

Suppose that the power series has positive finite radius of convergence , and that all the coefficients are non-negative real numbers. Then has a singularity at .

Theorem 7.4.

Proof.

Note that, in case (B), we can argue similarly as in the preceding proof. However, the coefficients are no longer positive, and so Pringsheim’s theorem is not applicable. Then, the inequality need not be an equality. Still, we can compute a lower bound for the explosion time:

| (7.11) |

Now assume that we are in case (A) again. We now discuss how to speed up the convergence in (7.10). Roberts and Olmstead [31] studied the blow-up behavior of solutions of nonlinear Volterra integral equations with (asymptotically) fractional kernel. Their arguments hinge on the asymptotic behavior of the nonlinearity for large argument. In particular, in our situation, with from (2.10) satisfying for , formula (3.2) in [31] yields

| (7.12) |

We write for two reasons: First, our integral equation (2.9) does not quite satisfy the technical assumptions in [31]. Second, not all steps in [31] are rigorous. We proceed, heuristically, to infer refined asymptotics of from (7.12). Define

a power series with radius of convergence , by the definition of in Lemma 7.2. Its asymptotics for can be derived from (7.12). Recall that the explosion time and the radius of convergence of are related by .

The method of singularity analysis (see Section VI in [12]) allows to transfer the asymptotics of to asymptotics of its Taylor coefficients . Sweeping some analytic conditions under the rug, we arrive at

and thus

| (7.13) |

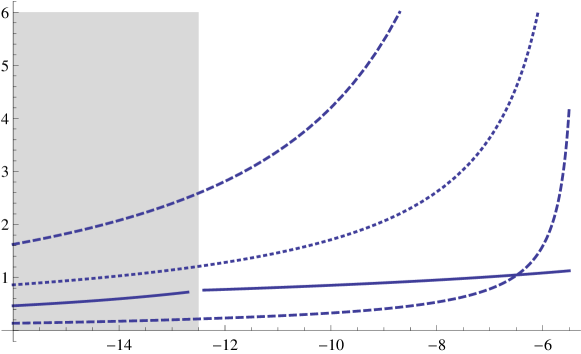

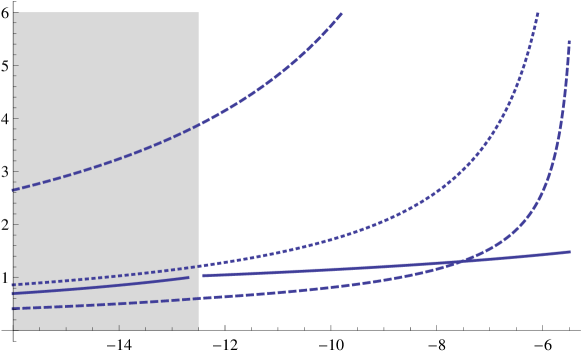

Numerical tests confirm (7.13), and we have little doubt that it is true (in case (A)). Summing up, can be computed by the following algorithm, which converges much faster than the simpler approximation :

Algorithm 7.5.

Let be a real number satisfying case (A).

-

•

Fix (e.g. ),

-

•

compute by the recursion (7.7),

-

•

compute the approximation

(7.14) for the explosion time.

We stress that, while the arguments leading to (7.13) are heuristic, we have rigorously shown in Theorem 7.4 that is the of the left-hand side of (7.14). The heuristic part is that the subexponential factor improves the relative error of the approximation from to . Note that our approach to compute the blow-up time can of course be extended to more general fractional Riccati equations. Finally, as mentioned above (see (7.11)), we can compute a lower bound for if it is finite, but is outside of case (A):

Algorithm 7.6.

Let be a real number satisfying case (B).

-

•

Fix (e.g. ),

-

•

compute by the recursion (7.7),

-

•

compute the approximate lower bound

of the explosion time.

Remark 7.7.

As for the applicability of Algorithm 7.5, suppose that (with analogous comments applying to the less common case ). From (2.7), we have for , and so we are in case (A) for large enough . More precisely, case (A) corresponds to the interval . For from that interval, the explosion time can be computed by Algorithm 7.5. To the right of , there is a (possibly empty) interval corresponding to case (B), where is still finite, but Algorithm 7.5 cannot be applied. Still, a lower bound can be computed by (7.11), and we have the bounds from Theorems 4.1 and 4.2, which can be easily evaluated numerically. Proceeding further to the right on the -axis, we encounter an interval containing , on which (cases (C) and (D)). Afterwards, becomes finite again, but these belong to case (B), leaving us with bounds for only.

To conclude this section, we note that can be approximated by replacing the coefficients in (7.2) by the right-hand side of (7.13). Let us write for the latter. Retaining the first exact coefficients, this leads to the approximation

| (7.15) |

where denotes the polylogarithm. While this approximation seems to be very accurate even for small (see [17]), it is limited to real satisfying case (A), and thus not applicable to option pricing.

8. Finiteness of the critical moments

While we have analyzed the explosion time of the rough Heston model so far, in most applications of moment explosions (see the introduction), the critical moments

| (8.1) |

are of interest. Using the upper bound for the moment explosion time in Theorem 4.2, we will now show the finiteness of the critical moments for every maturity . Computing and is discussed in Section 9.

Theorem 8.1.

In the rough Heston model the critical moments and are finite for every .

Proof.

Only the finiteness of is proven, as the proof for is very similar. Denote the upper bound of in (4.3) by for all in the cases (A) and (B). First, we show that for sufficiently large , we are always in case (A) or (B), depending on the sign of the correlation parameter . From (2.7) and (2.8), it is easy to see that

| (8.2) |

where . Thus, eventually for sufficiently large . In the next step, we show that the upper bound converges to as . Indeed, in case (A) the integral in (4.3) satisfies

for some , using the monotonicity , the inequality and as .

If we are eventually in case (B) as , then and holds for all sufficiently large . Note that in this case attains its global minimum at and the minimum value is . Thus, the integral in (4.3) satisfies

for some , using the monotonicity , the inequality on and (8.2).

Altogether, we have . Since , the same is true for the moment explosion time , i.e. . Now let be arbitrary. Then there exists such that for all . This inequality implies for all , and therefore . ∎

From the preceding proof, it easily follows that and are of order as . This is consistent with the classical Heston model (), where the decay order is , by inverting (2.13).

9. Computing the critical moments

We first collect some simple facts that apparently have not been made explicit in the literature on moment explosions. Moment explosion time and critical moments are defined as in (2.11) resp. (8.1).

Lemma 9.1.

Let be a positive stochastic process. Its moment explosion time is denoted by , , and its critical moments by and , .

-

(i)

increases for , and decreases for .

-

(ii)

If is a martingale, then decreases, and increases.

-

(iii)

Suppose that is a martingale. If decreases strictly on the interval

then on . Analogously, if increases strictly on the interval

then on .

Proof.

(i) As , we may assume that ( is analogous). The assertion follows from Jensen’s inequality, since is convex for .

(ii) We just consider . Since is a martingale, we have . For any number and , we have

by the conditional Jensen inequality. This shows the assertion.

(iii) We just prove the first statement. Note that (i) implies that is an interval. Now suppose for contradiction that satisfies

This means that there is satisfying . Hence, , contradicting the strict decrease of . Finally, suppose for contradiction that satisfies . Then there is such that . For arbitrary , we get

This implies , again contradicting the strict decrease of . ∎

If the assumptions of part (iii) hold, then we can compute the critical moments from the explosion time, by numerically solving the equations resp. . Note, however, that strict monotonicity may fail for reasonable stochastic volatility models. In the -model [25], the explicit characteristic function shows that the critical moments do not depend on maturity (for positive maturity), and the explosion time assumes only the values zero and infinity.

In the classical Heston model, on the other hand, it easily follows from (2.13) that (recall that the index denotes ) is a strictly monotonic function of : On the set where it is finite, strictly increases for negative , and strictly decreases for positive . By part (iii) of Lemma 9.1, this implies that we have

| (9.1) |

Thus, although the critical moments do not admit an explicit expression, they can be computed using (2.13) and (9.1), by numerical root finding with an appropriate starting value.

While we have no doubt that strict monotonicity of the explosion time extends to the rough Heston model, this seems not easy to verify. If we accept it as given, then the lower critical moment can be computed for from

Again, we focus on the lower critical moment, because then we can apply Algorithm 7.5 to compute for . Recall that this algorithm works only for , which amounts to case (A). Thus, must not be too large in (9), namely such that satisfies case (A). (Usually, this requirement is not too prohibitive.)

To provide some indication for the strict monotonicity of , recall that according to Lemma 5.3, (see Section 2) decreases strictly w.r.t. , if satisfies case (A). It is then plausible (although not proven) that the strictly smaller function explodes at a larger time than , where . As another indication, the bounds in Theorems 4.1 and 4.2 are strictly monotonous, as seen by differentiating them w.r.t. .

Even in case strict monotonicity should not hold, we certainly have

| (9.2) | ||||

| (9.3) |

for all , which suffices for numerical computations (under the above restriction on ). The validity of (9.2) and (9.3) is clear from (5.16): If is constant on some interval, lying to the left of zero, say, then the mgf blows up as approaches the interval’s right endpoint from the right.

10. Application to asymptotics

In the introduction we mentioned several potential applications of our work. In this section, we give some details on one of them: Knowing the critical moments gives first order asymptotics for the implied volatility for large and small strikes. We write for the implied volatility, where is the log-moneyness. According to Lee’s moment formula [23], the left wing of implied volatility satisfies

| (10.1) |

We focus on negative log-moneyness, because then the slope depends on the lower critical moment, which Algorithm 7.5 computes in the important case . As in any model with finite critical moments, the marginal densities of the rough Heston model have power-law tails. More precisely, if we write for the density of , then

and

| (10.2) |

Our approach (see Section 9) allows to evaluate the right-hand sides of (10.1) and (10.2) numerically for the rough Heston model, if is not too large.

In [13], (10.1)–(10.2) were considerably sharpened for the classical Heston model. We expect that such a refined smile expansion can be done for rough Heston, too, with density asymptotics of the form

where the depend on and . In the classical Heston model, the factor becomes in line with [13]. Extending the analysis of [13] to will require a detailed study of the blow-up behavior of the Volterra integral equation (2.9). Among other things, (a special case of) the heuristic analysis in [31], which we already mentioned in Section 7, would have to be made rigorous, and extended to ensure uniformity w.r.t. the parameter . We postpone this to future work. Note that the approximation (7.15) might be useful in this context.

References

- [1] E. Abi Jaber, M. Larsson, and S. Pulido, Affine Volterra processes. Preprint, arxiv:1708.08796, 2017.

- [2] E. Alos, J. Gatheral, and R. Radoicic, Exponentiation of conditional expectations under stochastic volatility. Preprint, https://ssrn.com/abstract=2983180, 2017.

- [3] L. B. G. Andersen and V. V. Piterbarg, Moment explosions in stochastic volatility models, Finance Stoch., 11 (2007), pp. 29–50.

- [4] C. Bayer, P. K. Friz, P. Gassiat, J. Martin, and B. Stemper, A regularity structure for rough volatility. Preprint, arXiv:1710.07481, 2017.

- [5] H. Brunner, Collocation methods for Volterra integral and related functional differential equations, vol. 15 of Cambridge Monographs on Applied and Computational Mathematics, Cambridge University Press, Cambridge, 2004.

- [6] , Volterra integral equations, vol. 30 of Cambridge Monographs on Applied and Computational Mathematics, Cambridge University Press, Cambridge, 2017.

- [7] H. Brunner and Z. W. Yang, Blow-up behavior of Hammerstein-type Volterra integral equations, J. Integral Equations Appl., 24 (2012), pp. 487–512.

- [8] R. Cont, Encyclopedia of Quantitative Finance, John Wiley and Sons, 2014.

- [9] O. El Euch and M. Rosenbaum, The characteristic function of rough Heston models. Preprint, arxiv:1609.02108, 2016.

- [10] , Perfect hedging in rough Heston models. Preprint, arxiv:1703.05049, 2017.

- [11] J. Elstrodt, Maß- und Integrationstheorie, Springer-Lehrbuch, Springer-Verlag, Berlin, sixth ed., 2009.

- [12] P. Flajolet and R. Sedgewick, Analytic Combinatorics, Cambridge University Press, Cambridge, 2009.

- [13] P. Friz, S. Gerhold, A. Gulisashvili, and S. Sturm, On refined volatility smile expansion in the Heston model, Quantitative Finance, 11 (2011), pp. 1151–1164.

- [14] J. Gatheral, The Volatility Surface, A Practitioner’s Guide, Wiley, 2006.

- [15] J. Gatheral, T. Jaisson, and M. Rosenbaum, Volatility is rough. Preprint, arXiv:1410.3394, 2014.

- [16] J. Gatheral and M. Keller-Ressel, Affine forward variance models. Preprint, arxiv:1801.06416, 2018.

- [17] C. Gerstenecker, Moment Explosion Time in the Rough Heston Model, Master’s thesis, TU Wien, 2018.

- [18] R. E. Greene and S. G. Krantz, Function theory of one complex variable, vol. 40 of Graduate Studies in Mathematics, American Mathematical Society, Providence, RI, third ed., 2006.

- [19] G. Gripenberg, S.-O. Londen, and O. Staffans, Volterra integral and functional equations, vol. 34, Cambridge University Press, Cambridge, 1990.

- [20] M. Keller-Ressel, Moment explosions and long-term behavior of affine stochastic volatility models, Math. Finance, 21 (2011), pp. 73–98.

- [21] A. A. Kilbas, H. M. Srivastava, and J. J. Trujillo, Theory and applications of fractional differential equations, vol. 204 of North-Holland Mathematics Studies, Elsevier Science B.V., Amsterdam, 2006.

- [22] S. G. Krantz, Function theory of several complex variables, Wadsworth & Brooks/Cole Advanced Books & Software, Pacific Grove, CA, second ed., 1992.

- [23] R. W. Lee, The moment formula for implied volatility at extreme strikes, Math. Finance, 14 (2004), pp. 469–480.

- [24] , Option pricing by transform methods: Extensions, unification, and error control, Journal of Computational Finance, 7 (2004), pp. 51–86.

- [25] A. L. Lewis, Option valuation under stochastic volatility, Finance Press, Newport Beach, CA, 2000.

- [26] R. Lord and C. Kahl, Optimal Fourier inversion in semi-analytical option pricing. Tinbergen Institute Discussion Papers 06-066/2, Tinbergen Institute, 2007.

- [27] C. Lubich, Runge-Kutta theory for Volterra and Abel integral equations of the second kind, Math. Comp., 41 (1983), pp. 87–102.

- [28] R. K. Miller and A. Feldstein, Smoothness of solutions of Volterra integral equations with weakly singular kernels, SIAM J. Math. Anal., 2 (1971), pp. 242–258.

- [29] R. Remmert, Theory of complex functions, vol. 122 of Graduate Texts in Mathematics, Springer-Verlag, New York, 1991.

- [30] C. A. Roberts, Analysis of explosion for nonlinear Volterra equations, J. Comput. Appl. Math., 97 (1998), pp. 153–166.

- [31] C. A. Roberts and W. E. Olmstead, Growth rates for blow-up solutions of nonlinear Volterra equations, Quart. Appl. Math., 54 (1996), pp. 153–159.

- [32] R. L. Schilling, Measures, integrals and martingales, Cambridge University Press, New York, 2005.

- [33] E. T. Whittaker and G. N. Watson, A course of modern analysis, Cambridge Mathematical Library, Cambridge University Press, Cambridge, 1996. Reprint of the fourth (1927) edition.

- [34] D. Widder, The Laplace transform, Princeton mathematical series, Princeton University Press, Princeton, 1941.