∎

22email: aaron.kim@stonybrook.edu

First Passage Time for Tempered Stable Process and Its Application to Perpetual American Option and Barrier Option Pricing

Abstract

In this paper, we will discuss an approximation of the characteristic function of the first passage time for a Lévy process using the martingale approach. The characteristic function of the first passage time of the tempered stable process is provided explicitly or by an indirect numerical method. This will be applied to the perpetual American option pricing and the barrier option pricing. Numerical illustrations are provided for the calibrated parameters using the market call and put prices. JEL Classification : G13, C21, C42

Keywords:

Lévy process tempered stable process first passage time barrier option pricing perpetual American option pricing1 Introduction

Since Black and Scholes (1973) have introduced the no-arbitrage option pricing model and formula, the Black-Scholes (BS) model became the most popular model in finance. Moreover, pricing path dependent exotic options, including American perpetual option and barrier options, is an important topic in finance. After the Black-Monday stock market crash in 1987, the volatility smile effect in option market have been observed and many scientists have introduced many advanced models to describe the smile effect. The Lévy process option pricing models (or simply Lévy models), based on tempered stable (TS) processes, including normal tempered stable (NTS) and CGMY processes, are popular models to explain the volatility smile effect in European call and put prices (See Barndorff-Nielsen and Levendorskii (2001), Barndorff-Nielsen and Shephard (2001), Carr et al. (2002), Boyarchenko and Levendorskiĭ (2000), Koponen (1995), and Rachev et al. (2011)).

The distribution of the first passage time for the arithmetic Brownian motion is an essential topic to calculate those path dependent option prices. We have the distribution of the first passage time of Brownian motion in literature including Barndorff-Nielsen (1977). Sequentially the distribution of first passage time on Lévy process has been studied by Hurd and Kuznetsov (2009), Rogers (2000) and others.

The perpetual American option and barrier option pricing also not only studied on BS model but also studied on Lévy models. Gerber and Shiu (1994) discussed the perpetual American option pricing formula on the BS model with the martingale approach, and Boyarchenko and Levendorskiĭ (2002b) found perpetual American option pricing formula using the Wiener–Hopf factorization on the Lévy model. The barrier option price formula under the BS model is provided in literature including Hull (2015). Additionally, Boyarchenko and Levendorskiĭ (2002c) presented the barrier option pricing method on Lévy model. The partial integro-differential equation method has been very popularly used for barrier option pricing (See Chandra and Mukherjee (2016) and Cont and Tankov (2004)) on Lévy model. Recently, Boguslavskaya (2014) discussed barrier option pricing method using A transform.

In this paper, we will discuss the characteristic function of the first passage time of a subclass of Lévy process containing Brownian Motion and TS processes (NTS or CGMY process) using the martingale approach. Since the martingale approach does not works for the process with jumps, we will use a continuous approximation of the Lévy process. After then we find an approximation form of the characteristic function for the first passage time of Lévy process. In some special cases, we will see the closed form of characteristic function. If the closed form solution is not allowed then the numerical method can be used to find it. The characteristic function of the first passage time will be applied to find perpetual American option prices and barrier option prices. The numerical methods and performance for pricing perpetual American option and barrier option will be discussed with empirical market data.

The remainder of this paper is organized as follows. The characteristic function of the first passage time for some Lévy process using the martingale method is deduced in Section 2. The approximation case for the Lévy process with jumps also discussed in the section. The perpetual American option pricing and the barrier option pricing is discussed in Section 3, together with numerical illustrations. Section 3 summarizes the main findings. In the appendix, we explain how pricing formulas of perpetual American option and barrier call and put options are obtained.

2 Characteristic function of the first passage time

Let be a Lévy process. Suppose that is the characteristic function (ch.F) of and is the Lévy symbol of that is given by so that (see Applebaum (2004)). Let be a level. We define a first passage time for the Lévy process to touch the level as follows:

| (1) |

Lemma 1

Suppose is a continuous Lévy process. For all , if there exist a complex function such that , is well defined, and

| (2) |

then the ch.F of equals to

| (3) |

Proof

Remark 2.1

Applying Lemma 1, we can obtain the probability density function (pdf) of by the inverse Fourier transform as follows:

| (5) |

Example 1 (Brownian Motion)

Let where is Brownian motion, , and . Since the ch.F of is

The equation (2) is equal to

and satisfying the equation is

For the condition , we have

Hence the ch.F of the first passage time for is

which is well known ch.F of inverse Gaussian distribution.

We cannot use Lemma 1 for the Lévy process with jumps, since is not true in general. To escape the problem, we define continuous approximation process for the Lévy process as

where is a partition of a real interval as

We refer to as the continuously approximated process of .We have characteristic function of as follows:

where

We use numerical approximation of , then we have

After then we use Lemma 1 for with approximated ch.F of . That is if satisfy (2), then the first passage time of has an approximation of the characteristic function as

2.1 Cases of NTS Process and Normal Inverse Gaussian Process

Let , , , and . Consider a pure jump Lévy process whose ch.F is equal to

The process is referred to as the the NTS process with parameters , , , , and denoted by , , , , . The NTS process has finite exponential moments for a closed interval, That is, if

If , , , , with , then the process is referred to as the the normal inverse Gaussian (NIG) process with parameters , , , and denoted by , , , . The ch.F of the NIG process is equal to

If , , , , where and with then and for all . In this case, the process is referred to as the standard NTS process with parameters , , and denoted by , , . With the same argument, , , , where and with , then and for all . In this case, the process is referred to as the standard NIG process with parameters , and denoted by , .

By applying Lemma 1 to the process , , , , we find satisfying (2) that is

or

Finally, we obtain the solution

Since NIG process is a pure jump Lévy process, we cannot use Lemma 1 directly. Instead, we use a continuously approximated process of the process for a partition . Satisfying the condition for all , we have the ch.F of the first passage time for process as

where

and

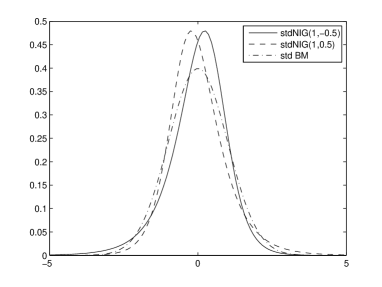

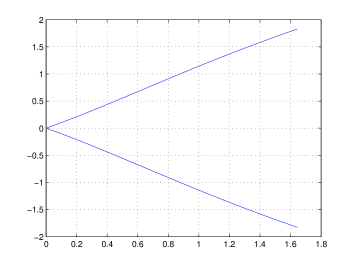

For the numerical illustration, we present the pdf’s of the standard NIG distributions and the first passage time of the standard NIG process in Figure 1. To draw figure, we use the fast Fourier transform method for the equation (5) with the ch.F of the first passage time.

Let , and with parameter and , and let be the standard Brownian motion. We consider continuously approximated processes and for and , respectively. In the both left and right plates, the solid curve is for , the dashed curve is for and the dash-dot curve is for . The left plate, we show that the pdf’s of (solid) and (dashed), that are skewed left, and skewed right, respectively. The pdf of (dash-dot) is a standard normal pdf, which is symmetric. Let , and be the first passage time of , , and , respectively, for the level . In the right plate, we presented the pdf’s of (solid), (dashed) and (dash-dot). Since the distribution of () is skewed left (right) while the distribution of is symmetric, the mod of () is located a little right (left) of the mod of .

By applying Lemma 1 to the process , , , , , we find satisfying (2) that is

| (6) |

which has no explicit solution, but we can find the solution numerically. Moreover, the NTS process is also a pure jump Lévy process, we find the ch.F of the first passage time using the continuously approximated process of the NTS process.

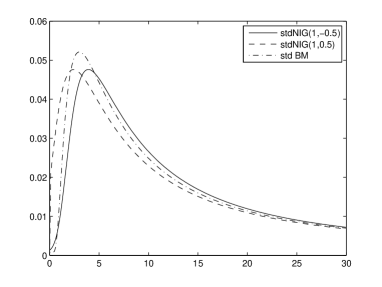

For the numerical illustration, we present the function , ch.F’s, and pdf’s of the standard NTS distributions and the pdf of the first passage time of the standard NTS process in Figure 2. We consider two standard NTS processes and with parameters , and , and the level . The upper left and right plates are ’s for and , respectively, which satisfy (6). The middle left and right plates are the for the stdNTS and stdNTS, respectively. Pdf’s of and are the dashed and solid curves, respectively, on the bottom left plate.

Let and be continuously approximated process with respect to and . Pdf’s of the first passage time of and are numerically approximated as the dashed and solid curves, respectively, on the bottom right plate. Dash-dot curves of bottom left and right plates are pdf of standard normal distribution and pdf of the first passage time of the standard Brownian motion, respectively. For the same arguments as standard NIG case, we have mode of the dashed and solid curves are located left and right of the dash-dot curve, respectively in the bottom right plate.

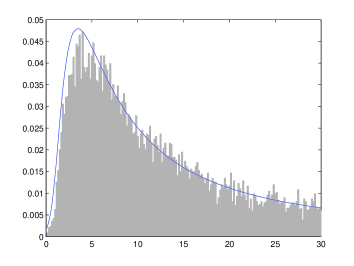

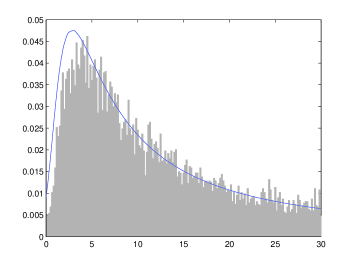

Finally, the pdf obtained by the characteristic function is compared with the first passage time distribution of simulated sample paths. We denote the pdf’s of and as and , respectively. We generate 20,000 sample paths of stdNTS, using inverse transform method explained in Rachev et al. (2011). That is with time step year fraction for . Then we obtain 30 years sample path. Setting as above example, We find the set of the first hitting time as

We present the relative histogram for and on the left plate of Figure 3. We do the same test for stdNTS, and present the relative histogram for the simulation based first passage time of stdNTS and on the right plate of Figure 3.

2.2 Case of CGMY Process

Let , , and . The pure jump Lévy process whose ch.F is equal to

is referred to as CGMY tempered stable process (See Carr et al. (2002)) or CGMY process with parameters , , , , ,and denoted by , , , , . The CGMY process has finite exponential moments for a closed interval, That is, if . If , , , , where and then and for all . In this case, the process is referred to as the standard CGMY process with parameters , , and denoted by , , .

For given , we find satisfying (2) that is

| (7) | ||||

which has no explicit solution. As the NTS process case in (6), we are also able to find the solution of (7) numerically, and ch.F is as the equation in Lemma 1.

For the numerical illustration, we consider two standard CGMY processes stdCGMY( , , ) and stdCGMY(, , ), and the level . Also we take and which are continuously approximated process of and , respectively. We present the function , ch.F’s, and pdf’s of the standard CGMY distributions and the pdf of the first passage time of the standard CGMY process in Figure 4. The upper left and right plates are the for stdCGMY(, , ) and stdCGMY(, , ), respectively. The middle left and right plates are the chF’s for stdCGMY(, , ) and stdCGMY(, , ), respectively. Pdf’s of stdCGMY(, , ) and stdCGMY(, , ) are the dashed and solid curves, respectively, on the bottom left plate. Pdf’s of the first passage times of and are the dashed and solid curves, respectively, on the bottom right plate. Dash-dot curves of bottom left and right plates are pdf of standard normal distribution and pdf of the first passage time of the standard Brownian motion, respectively. For the same arguments as standard NIG case, we have mode of the dashed and solid curves are located left and right of the dash-dot curve, respectively in the bottom right plate.

We can do the same simulation experiment for the stdCGMY(, , ) and stdCGMY( , , ) as the standard NTS case in the previous section. We omit to show the result since the result of CGMY simulation cases are very similar as of the NTS simulation cases.

3 Application to Exotic Option Pricing and Numerical Illustration

Let and be a Lévy process and its continuously approximated process, respectively, and suppose that there is an closed interval containing 0 such that for any . We assume that there exist satisfying the condition of Lemma 1 for , and is the first hitting time given by (1).

Let and be the risk free rate of return and the continuous dividend rate of a given underlying asset, respectively. The underlying asset price process is assumed as

All of the market models in this paper are based on the risk-neutral world which has no-arbitrage. So we assume that the discount price process with is martingale. In this case, we referred to the risk-neutral price model as Lévy market model.

The class of TS process is a subclass of Lévy process including NTS and CGMY process. The Lévy process option pricing models (i.e. Lévymodel) with TS processes are often used for the option pricing theory. The model can capture the volatility smile effect of option market by describing fattails and skewness of risk-neutral measure (See Boyarchenko and Levendorskiĭ (2002a), Cont and Tankov (2004), Schoutens (2003), and Rachev et al. (2011)).

NTS Market model

In the Lévy market model, suppose is the NTS process with parameters , , , , , where

then the discount process is martingale, since

In this case, we say that the underlying asset price process follows the NTS market model. In particular, if we say that it follows NIG market model.

CGMY Market model

In the Lévy market model, suppose is the CGMY process with parameters , where

then the discount process is martingale for the same argument of the NTS market model case. In this case, we say that the underlying asset price process follows the CGMY market model.

Model calibration

We calibrate parameters of the three TS (NIG, NTS and CGMY) market models by using the S&P 500 index call and put options. We obtain the S&P 500 index call and put price from OptionMetricsTM provided by Wharton Research Data Services. The parameters are calibrated by the least square curve fit and the call and put option prices of NTS, NIG, and CGMY models are calculated by Fast Fourier Transform method by Lewis (2001) and Carr and Madan (1999). For the benchmark, we calibrate the BS model (Black and Scholes (1973)) parameter which is referred to as volatility.

In this calibration, we use the option prices of October 8, 2014 on which underlying S&P 500 index was , risk-neutral interest rate was , and dividend rate for S&P 500 index was . We select calls and puts with moneyness (= (strike price) / (current underlying price)) in between 0.9 and 1.1, and having time to maturities, 7 days, 32 days or 52 days. We calibrate parameters for call prices and put prices separately. The calibrated parameters are presented in Table 1. In the table, we provide three error estimators together: the average absolute error (AAE), the average absolute error as a percentage of the mean price (APE), and the root-mean-square error (RMSE),111See Schoutens (2003) for additional details. defined as follows:

where and are model prices and observed market prices of options, , and is the number of observed call option prices. As reported many literature including Carr et al. (2002), Schoutens (2003), and Rachev et al. (2011), the NIG, NTS, and CGMY market models have better calibration performance than the BS model, that is, the three error estimators for those three Lévy market models are remarkably smaller than the three error estimator for the BS model.

Approximation for Characteristic function of

As we discussed in Section 2, the characteristic function of is numerically approximated as for NTS and CGMY market model. With this approximation we discuss pricing Perpetual American Call and Put, and pricing Barrier Option in the following subsections. In the following market, we assume that priving process of stock price process is the continuously approximated process for NTS (including NIG) and CGMY processes.

3.1 Application to Perpetual American Call and Put

We consider a perpetual American call and put options with strike price . The perpetual call price is equal to

where

and is the value satisfying (2) and (3) for and . The perpetual put price is equal to

where

and is the value satisfying (2) and (3) for and . More details for the perpetual American call and put prices are presented in Appendix.

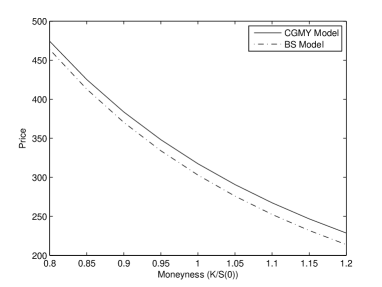

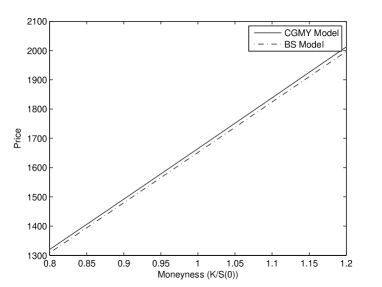

Using the perpetual call/put formula above, we calculate prices of the perpetual American call and put options for the NIG, NTS and CGMY market models using the calibrated parameters on October 8, 2014 presented in Table 1. We also use the underlying price, risk-neutral rate of return, and dividend rate from the data on October 8, 2014. Since perpetual call and put prices for NIG, NTS and CGMY market models are very similar, we present only prices (solid curves) under the CGMY market model in Figure 5. for the benchmark, we calculate perpetual American option prices (dash-dot curves) using BS model. In this context, the left plate of the figure is perpetual call prices and tie right plate is the perpetual put prices for moneyness from 0.8 to 1.2. We find that BS prices are more or less smaller than CGMY prices.

3.2 Application to Barrier Option Pricing

The barrier option is one of the most popular exotic option. Barrier options are classified by the knock-in barrier option, and the knock-out barrier option. The knock-in barrier option is activated when the underlying asset price hit a given barrier level. The knock-out barrier option is alive until the underlying price hit the barrier level, but once the underlying price hit the barrier level, the price of the option becomes zero. The knock-in barrier option is divided by the up-and-in barrier option and the down-and-in barrier option. If the barrier level is upper (lower) than the current underlying prices, then the knock-in barrier option is referred to as the up-and-in (down-and-in) barrier option. The knock-out barrier option is also divided by the up-and-out barrier option and the down-and-out barrier option. If the barrier level is upper (lower) than the current underlying prices, then the knock-out barrier option is referred to as the up-and-out (down-and-out) barrier option222See Hull (2015) for more details..

In this section, we discuss pricing of European style barrier call and put options. Let be the barrier level, be the strike price of call and put, and be the time to maturity. Suppose that the current underlying asset price is , and let . Then we have the down-and-in and down-and-out options if and the up-and-in and up-and-out options if . Let and be the risk free rate of return and the continuous dividend rate of a given underlying asset, respectively.

The down-and-in call (), up-and-in put () are priced by

and

and the up-and-in call () and down-and-in put () are priced by

and

where

Since knock-out call(put) option price can be calculated by the vanilla call(put) price minus knock-in call(put) price, we do not consider the knock-out call and put options in this section. More Details and proofs for the barrier option pricing are explained in Appendix.

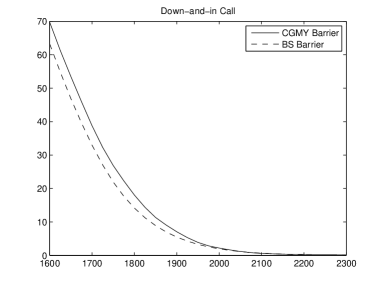

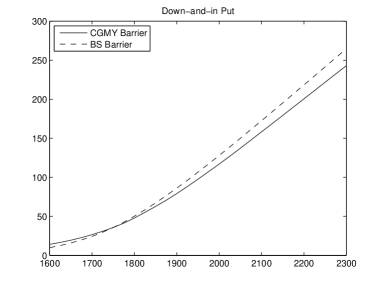

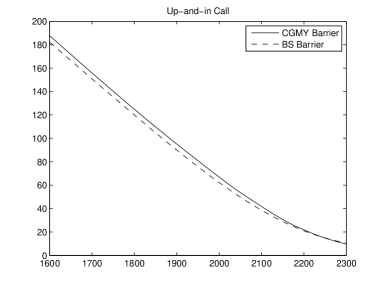

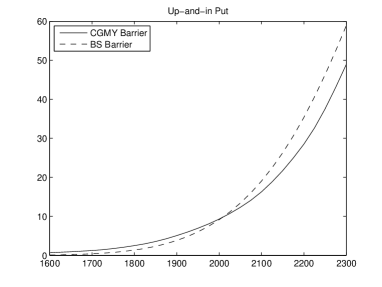

Notably, we calculate those four knock-in option prices numerically. We use the estimated parameters in Table 1 for call and put prices of October 8, 2014, on which underlying S&P 500 index was , risk-neutral interest rate was , and dividend rate for S&P 500 index was . We assume that the time to maturity is = 1 year and we select strike prices between 1600 and 2300, that is, . Since the barrier option prices under NIG and NTS market models are not remarkably different from the prices under the CGMY market models, we just show the barrier option prices under CGMY market model. For the benchmark, we compare the CGMY prices to the barrier option prices based on BS model.

In Figure 6, the down-and-in call and put option prices are presented in the left and right plates, respectively, for the barrier level is 1750. The barrier option on the CGMY model is typically greater than the price on BS model, since the CGMY distribution is skewed left and the CGMY distribution has fatter tails than Gaussian distribution. because of the left skewness of the CGMY distribution, the probability that the knock-in option be alive is larger than the case of BS model. In Figure 7, the up-and-in call and put option prices are presented in the left and right plates, respectively, for the barrier level is 2200. That being the case, the BS barrier option prices are different from CGMY barrier option prices.

In addition, we implement the four barrier option pricing formula using the fast Fourier transform algorithm. To accomplish this numerical calculation, we use MatlabTM 2015a on a PC equipped with Intel CORE i7TM processor (3.00GHz Dual core) and MS WindowsTM 10 operating system. It took 59.9 seconds to obtain the down-and-in call option prices, and took 67.6 seconds to obtain down-and-in put option prices. It took 69.3 seconds to obtain down-and-in call option prices, and took 61.4 seconds to obtain down-and-in put option prices.

4 Conclusion

In this paper, we found an approximation of the characteristic function of the first passage time for a Lévy process using the martingale approach and the continuously approximated process. More precisely, we found approximations of ch.F’s and pdf’s of the first passage time of three TS processes (NIG, NTS, and CGMY processes), explicitly or numerically. It was applied to price the perpetual American option and the barrier option. Numerical illustrations were provided together, for the calibrated parameters using the market call and put prices. We obtained one tractable method to find those exotic options under the TS market model. The result can be used for analyzing default probability in credit risk management also.

Acknowledgment I am grateful to Professor Kyuong Jin Choi, in Haskayne School of Business, University of Calgary, who gave the motivation to complete of this research. Also, all remaining errors are entirely my own.

References

- Applebaum [2004] D. Applebaum. Lévy process and stochastic calculus. Cambridge Univ. Press, New York, 2004.

- Barndorff-Nielsen [1977] O. Barndorff-Nielsen. Exponentially decreasing distributions for the logarithm of particle size. Proceedings of the Royal Society of London A: Mathematical, Physical and Engineering Sciences, 353(1674):401–419, 1977. ISSN 0080-4630. doi: 10.1098/rspa.1977.0041. URL http://rspa.royalsocietypublishing.org/content/353/1674/401.

- Barndorff-Nielsen and Levendorskii [2001] O. E. Barndorff-Nielsen and S. Levendorskii. Feller processes of normal inverse gaussian type. Quantitative Finance, 1:318 – 331, 2001.

- Barndorff-Nielsen and Shephard [2001] O. E. Barndorff-Nielsen and N. Shephard. Normal modified stable processes. Economics Series Working Papers from University of Oxford, Department of Economics, 72, 2001.

- Black and Scholes [1973] F. Black and M. Scholes. The pricing of options and corporate liabilities. The Journal of Political Economy, 81(3):637–654, 1973.

- Boguslavskaya [2014] E. Boguslavskaya. Solving optimal stopping problems for Lévy processes in infinite horizon via -transform. ArXiv e-prints, March 2014.

- Boyarchenko and Levendorskiĭ [2000] S. I. Boyarchenko and S. Z. Levendorskiĭ. Option pricing for truncated Lévy processes. International Journal of Theoretical and Applied Finance, 3:549–552, 2000.

- Boyarchenko and Levendorskiĭ [2002a] S. I. Boyarchenko and S. Z. Levendorskiĭ. Non-Gaussian Merton-Black-Scholes Theory. World Scientific, 2002a.

- Boyarchenko and Levendorskiĭ [2002b] S. I. Boyarchenko and S. Z. Levendorskiĭ. Perpetual american options under Lévy processes. SIAM Journal on Control and Optimization, 40(6):1663–1696, 2002b.

- Boyarchenko and Levendorskiĭ [2002c] S. I. Boyarchenko and S. Z. Levendorskiĭ. Barrier options and touch-and-out options under regular l vy processes of exponential type. The Annals of Applied Probability, 12(4):1261–1298, 2002c.

- Carr and Madan [1999] P. Carr and D. Madan. Option valuation using the fast fourier transform. Journal of Computational Finance, 2(4):61–73, 1999.

- Carr et al. [2002] P. Carr, H. Geman, D. Madan, and M. Yor. The fine structure of asset returns: An empirical investigation. Journal of Business, 75(2):305–332, 2002.

- Chandra and Mukherjee [2016] S. R. Chandra and D Mukherjee. Barrier option under l vy model : A pide and mellin transform approach. Mathematics, 4(1), 2016.

- Cont and Tankov [2004] R. Cont and P. Tankov. Financial Modelling with Jump Processes. Chapman & Hall / CRC, 2004.

- Gerber and Shiu [1994] H. U. Gerber and E. S. W. Shiu. Martingale approach to pricing perpetual american options. Astin Bulletin, 24:195–220, 1994.

- Hull [2015] J. C. Hull. Options, Futures and Other Derivatives. Prentice-Hall, 9th edition, 2015.

- Hurd and Kuznetsov [2009] T. R. Hurd and A. Kuznetsov. On the first passage time for brownian motion subordinated by a Lévy process. Journal of Applied Probability, 46(1):181–198, 03 2009. doi: 10.1239/jap/1238592124.

- Koponen [1995] I. Koponen. Analytic approach to the problem of convergence of truncated Lévy flights towards the gaussian stochastic process. Physical Review E, 52:1197–1199, 1995.

- Lewis [2001] A. L. Lewis. A simple option formula for general jump-diffusion and other exponential Lévy processes. avaible from http://www.optioncity.net, 2001.

- Rachev et al. [2011] S. T. Rachev, Y. S. Kim, M. L. Bianch, and F. J. Fabozzi. Financial Models with Lévy Processes and Volatility Clustering. John Wiley & Sons, 2011.

- Rogers [2000] L. C. G. Rogers. Evaluating first-passage probabilities for spectrally one-sided l vy processes. Journal of Applied Probability, 37(4):1173–1180, 12 2000. doi: 10.1239/jap/1014843099.

- Schoutens [2003] W. Schoutens. Lévy Processes in Finance. Wiley, 2003.

| Call/Put | Model | Parameters | AAE | APE | RMSE |

| Call | BS | 3.3619 | 0.1042 | 4.1806 | |

| NIG | , , | 2.4056 | 0.0746 | 2.8746 | |

| NTS | , , | 2.3939 | 0.0742 | 2.8637 | |

| , | |||||

| CGMY | , , | 2.4107 | 0.0747 | 2.8810 | |

| , | |||||

| Put | BS | 3.5132 | 0.1507 | 4.3561 | |

| NIG | , , | 1.3995 | 0.0600 | 1.6910 | |

| NTS | , , | 1.3920 | 0.0597 | 1.6846 | |

| , | |||||

| CGMY | , , | 1.4006 | 0.0601 | 1.6957 | |

| , |

Appendix

As appendix, we discuss perpetual American option pricing and barrier option pricing under the Lévy market model.

Perpetual American Option

The perpetual call and put option price on Lévy model can be obtained by the martingale method introduced in Gerber and Shiu [1994]. In this section, we just follow the martingale method for the Lévy market price model. We consider a perpetual American call option with strike price . If the option holder exercise the call at a time , then the holder obtain where . Let be a real number with . The holder will exercise the call when the asset price first become greater than or equal to the level . We define the first passage time

where . Then the current value of the perpetual American call is

Let

which is the Laplace transform of . Applying Lemma 1, we can obtain the Laplace transform as

where is the value satisfying (2) and (3) for and . Hence we have

By solving

we find the optimal value

Hence, we obtain the maximum value

If then the call is immediately exercised so we have price . Therefore the perpetual call price is equal to

We consider a perpetual American put option with strike price . If the option holder exercise the put at a time , then the holder obtain . Let be a real number with . The holder will exercise the put when the asset price first become less than or equal to the level . We define the first passage time

where . Then the current value of the put is

which is the Laplace transform of . For the same arguments as the call option case, we find the optimal value

where is the value satisfying (2) and (3) for and . Hence the perpetual put price is equal to

Barrier Option

Let be the payoff function of European options. For example, the European call and put options with strike price are given by and , respectively. The knock-in barrier option with the barrier level , time to maturity is priced by the following equation

where . Note that for the down-and-in barrier option and for the up-and-in barrier option. Since we have

the knock-out barrier option price can be obtained by the following equation

where . Note that for the down-and-out barrier option and for the up-and-out barrier option.

Case 1:

If then the barrier option price is the same as option prices without the barrier:

For example (1) up-and-in call option with , we have , and (2) down-and-in put option with , we have .

Case 2:

If , we have

where is the pdf of . Since we have and

the becomes

| (8) |

By European option pricing formula using Fourier transform (See Carr and Madan [1999], Lewis [2001] and Rachev et al. [2011]), we have

where for complex number and is a real constant such that and are well defined for all . Hence we have

Let

then

European call and put options

For the call option payoff , we have

and for the put option payoff , we have

The down-and-in call option price () and up-and-in put option price () are always in Case 2. Therefore, we have their prices as

and

For the up-and-in call option price () and the down-and-in put option price (), we consider Case 1, and finally obtain

and

The up-and-out and down-and-out calls corresponding to the up-and-in and down-and-in calls above are priced by , and , respectively, where is the vanilla call option price with strike price , and time to maturity . The up-and-out and down-and-out puts corresponding to the up-and-in and down-and-in puts above are priced by , and , respectively, where is the vanilla put option price with strike price , and time to maturity .