Calibration for Weak Variance-Alpha-Gamma Processes111This research was partially supported by ARC grant DP160104037.

Abstract

The weak variance-alpha-gamma process is a multivariate Lévy process constructed by weakly subordinating Brownian motion, possibly with correlated components with an alpha-gamma subordinator. It generalises the variance-alpha-gamma process of Semeraro constructed by traditional subordination. We compare three calibration methods for the weak variance-alpha-gamma process, method of moments, maximum likelihood estimation (MLE) and digital moment estimation (DME). We derive a condition for Fourier invertibility needed to apply MLE and show in our simulations that MLE produces a better fit when this condition holds, while DME produces a better fit when it is violated. We also find that the weak variance-alpha-gamma process exhibits a wider range of dependence and produces a significantly better fit than the variance-alpha-gamma process on an S&P500-FTSE100 data set, and that DME produces the best fit in this situation.

2000 MSC Subject Classifications: Primary: 60G51

Secondary: 62F10, 60E10

Keywords: Brownian Motion, Gamma Process, Lévy Process, Subordination, Variance-Gamma, Variance-Alpha-Gamma, Self-Decomposability, Log-Return, Method of Moments, Maximum Likelihood Estimation, Digital Moment Estimation.

1 Introduction

The subordination of Brownian motion has important applications in mathematical finance, and acts as a time change that models the flow of information, measuring time in volume of trade, as opposed to real time. This idea was initiated by Madan and Seneta in [27] who introduced the variance-gamma () process for modelling stock prices, where the subordinate is Brownian motion and the subordinator is a gamma process.

Subordination can be applied to model dependence in multivariate price processes. The multivariate process in [27] uses -dimensional Brownian motion as its subordinate and a univariate gamma process as its subordinator, which gives it a restrictive dependence structure, where components cannot have idiosyncratic time changes and must have equal kurtosis when there is no skewness. Models based on linear combinations of independent Lévy processes [19, 23] also do not account for both common and idiosyncratic time changes. These deficiencies are addressed by the use of an alpha-gamma subordinator, resulting in the variance-alpha-gamma () process which was introduced by Semeraro in [34] and also studied in [18, 22]. However, in this case, the Brownian motion subordinate must have independent components, which also restricts the dependence structure.

To be precise, let , where be independent -dimensional processes, where is Brownian motion and is a subordinator. Subordination is the operation that produces the process defined by . Subordination in the case when has indistinguishable components has been studied in [4, 33], and when has independent components in [3]. In these cases, which we refer to as traditional subordination, is a Lévy process, otherwise it may not be (see [10], their Proposition 3.9). We refer the reader to [9] for a thorough discussion of traditional subordination and its applications.

In [10], we introduced the weak subordination of and , an operation that extends traditional subordination and always produces a Lévy process . Then the weak variance-alpha-gamma () process can be constructed using weak subordination instead of traditional subordination, while allowing for the Brownian motion to have possibly correlated components. The process exhibits a wider range of dependence while remaining parsimoniously parametrised, each component has both common and idiosyncratic time changes, it has marginals with independent levels of kurtosis, and the jump measure has full support.

Weak subordination also has applied in quantitative finance. In [29], various marginal consistent dependence models have been constructed by weak subordination. In [25], log return modelling based on the process was applied in instantaneous portfolio theory. In [28], weak subordination using subordinators with arbitrary marginal components and dependence specified by a Lévy copula was studied in the context of financial information flows.

Maximum likelihood estimation (MLE) has been used to fit financial data to a univariate process in [26, 16], to a bivariate process in [17], to a process in [29], and to a factor-based subordinated Brownian motion in [21, 29, 35], a generalisation of the process. Since the density function of the and distribution is not explicitly known but its characteristic function is, the density function is computed using Fourier inversion.

In this paper, we derive a sufficient condition in terms of the parameters for Fourier invertibility, a problem that to our knowledge is not addressed in the existing literature. Then we compare MLE with method of moments (MOM) and digital moment estimation (DME) from [24]. Using simulations we find that MLE produces a better fit when the Fourier invertibility condition is satisfied but that DME is better when it is violated. In addition, we fit both the and model to an S&P500-FTSE100 data set and show that the weak model has a significantly better fit, and that DME is the better method in this situation. Finally, using a condition for the self-decomposability of the process from [11], we find that the log returns are self-decomposable.

This paper is structured as follows. In Section 2, we review the definition and properties of the process, and other preliminaries. In Section 3, we derive a condition for Fourier invertibility. In Section 4, we apply MOM, MLE, DME to simulated and real data, and discuss our findings. In Section 5, we conclude the paper.

2 Weak Variance-Alpha-Gamma Process

Let be -dimensional Euclidean space whose elements are row vectors with canonical basis . Let denote the Euclidean product, denote the Euclidean norm, and let . For -dimensional processes and , indicates that and are identical in law, that is their systems of finite dimensional distributions are equal.

A overview of Lévy processes and weak subordination is given in the appendix. Throughout, refers to an -dimensional Brownian motion with linear drift and covariance matrix Cov, .

An -dimensional subordinator is an -dimensional Lévy process with nondecreasing components, and its Lévy measure is denoted by .

Gamma subordinator. For , a univariate subordinator is a gamma subordinator if its marginal , ,

is gamma distributed with shape parameter and rate parameter . If , we refer to as a standard gamma subordinator, in short, .

Alpha-gamma subordinator. Assume . Let and be independent gamma subordinators such that , , where , , , . A process is an alpha-gamma () subordinator [34] with parameters if . An alpha-gamma subordinator has correlated components with marginals , .

Variance-gamma process. Let , and be a covariance matrix. A process is a variance-gamma process [27] with parameters if , where .

The characteristic exponent of is (see [9], their Formula (2.9))

| (2.1) |

where is the principal branch of the logarithm.

Strong variance-alpha-gamma process. Assume . Let and be a diagonal matrix. A process is a (strong) variance-alpha-gamma () process [22, 34] with parameters if .

In [10], the weak process was formulate using weak subordination, allowing to have dependent components while remaining a Lévy process.

Weak variance-alpha-gamma process. Assume . Let and be an arbitrary covariance matrix. The process is a weak variance-alpha-gamma process [10] with parameters if , where denotes the weak subordination operation (see the appendix).

Next, we gather various known results about the process that will be useful later on. The notation is defined in (A.1) and self-decomposability is defined in the appendix.

Proposition 2.1.

Let and .

-

(i)

is an -dimensional Lévy process with Lévy exponent

(2.2) -

(ii)

Let , , be independent. Then .

-

(iii)

For any , .

-

(iv)

For , has marginal distribution .

-

(v)

If is diagonal, then .

-

(vi)

For , .

-

(vii)

If is invertible, then is self-decomposable if and only if .

The process exhibits a wider range of dependence than the process. For example, it has an additional covariance term from Proposition 2.1 (vi).

3 Fourier Invertibility

Let and and , , where is the identity function. The density function of , , which is needed for MLE, exists because has an absolutely continuous distribution for. However, it is not explicitly known, so it is computed using Fourier inversion as

| (3.1) |

where , , and from (2.2), provided . If , we say that is Fourier invertible and we give a condition for this in terms of an inequality relating the parameters.

Lemma 3.1.

Let , , , , , , . For all and , if , then .

Proof.

Lemma 3.2.

Let , and assume that is invertible. Let . If , then .

Proof.

Since variance-gamma processes are weakly subordinated processes (see (A.3)), we can apply Lemma 3.1, which means that we can assume . For , by (2.1), has characteristic function

Using the Cholesky decomposition, , where is a lower triangular matrix with positive elements on the diagonal. Let . Making the transformation , noting that exists, and hence the transformation is injective, we have

| (3.2) |

Using the polar decomposition (see Corollary B.7.7 in [32]) on the RHS of (3.2), we have if and only if

which is equivalent to . ∎

Proposition 3.1.

Let and , . Assume that is invertible. For , if

| (3.3) |

then .

Proof.

Remark 3.1.

Note that this condition for a distribution to be Fourier invertible is identical to the condition for its density function having no singularity in [20], which is .

4 Calibration

We now specialise to the case of . Let , , . Let be a bivariate price process

| (4.1) |

For equally spaced discrete observations with sampling interval , the log returns are

and are iid. We call this the model. If , we called it the model as reduces to a process by Proposition 2.1 (v).

4.1 Simulation method

The result in Proposition 2.1 (ii) can be used to simulate in terms of and processes.

For the sampling intervals and sample size , we make 100 simulations of , and estimate the parameters from the observations with true parameters , , , , .

4.2 Calibration methods

We estimate the parameters from the observations using method of moments (MOM), which is quick and easy to implement, maximum likelihood estimation (MLE) from Michaelsen & Szimayer [29], which may be expected as being asymptotically optimal under the model, and a modification of digital moment estimation (DME) from Madan [24], which is more robust to model misspecification.

Method of moments. The initial values of , , are obtained by least squares on the first four central moments , , , with the corresponding sample moments. The initial values of the joint parameters are obtained by least squares on , , with the corresponding sample moments, with excluded when fitting the model. Using these initial values, least squares is solved over all parameters. Note that this last step has no effect when these moments can be matched exactly.

Moment formulas can be found in [29].

Maximum likelihood estimation.

The density function of is not explicitly known so it is numerically computed using Fourier inversion by (3.1). The numerical optimisation needed to implement MLE requires initial values. The first initial values can be obtained by MOM. Using the first initial values, MLE is applied to each marginal observations to obtain the second initial values of , , and to the bivariate observations to obtain the second initial values of . Finally, using the second initial values, MLE is applied on all parameters. For the model, we apply the above method with the constraint .

Digital moment estimation.

Let , let be the vector of 10 equally spaced points from 0.05 to 0.95, and let be the empirical quantiles of the observations at the probabilities . Let , where , (see Proposition 2.1 (iv)), and is the corresponding empirical probability. Marginal parameters are estimated by minimizing the error .

With the estimated marginal parameters, let , , where , , and is the corresponding empirical probability. Since is computationally expensive to calculate directly, it is estimated by the empirical probability over 10000 simulations. The joint parameters , are estimated by minimizing the LOESS smooth [14] of the error . The predictor variables for the LOESS smooth are 100 equally spaced points on the feasible set of . For the model, we apply the above method with the constraint .

4.3 Goodness of fit statistics

To assess the overall goodness of fit of each parameter estimation method, as opposed to assessing individual parameters, we consider 3 goodness of fit statistics, the negative log-likelihood (), a chi-squared () statistic, and a Kolmogorov-Smirnov (KS) statistic.

To compute , we apply the Rosenblatt transform [31] of the fitted distribution to the observations, which has a uniform distribution on if the fitted distribution coincides with the true distribution, and then we compute the statistic for a test of uniformity over an equally spaced partition of into 100 cells. Since computing and requires Fourier inversion, it may not be possible to compute these statistics accurately when the Fourier invertibility condition does not hold, so they are not displayed in Table 2.

Therefore, we also consider the 2-dimensional, two-sample Kolmogorov-Smirnov statistic introduce by Peacock in [30], and computed using the method of [36]. This is the statistic for testing equality of the fitted distribution and the true distribution based on a sample from the respective distributions, and therefore does not require the density function or Fourier inversion. When applied to real data in Subsection 4.6, we take the average of the KS statistics computed from the observations and 100 samples from the fitted distribution. When applied to simulated data in Subsection 4.5, the KS statistic is computed from the observations and a sample from the fitted distribution. All 3 goodness of fit statistics were averaged over the 100 simulations.

4.4 Quantile choice for DME

Different choices of quantiles for DME are possible. Let be the vector of 10 equally spaced points from 0.05 to 0.95, be the vector of 10 equally spaced points from 0.01 to 0.99, be the vector of 10 equally spaced points from 0.1 to 0.9, be the vector of 20 equally spaced points from 0.05 to 0.95. For sampling interval , Table 1 shows the goodness of fit for 4 choices of quantiles. We find as yielding the lowest RMSE for most variables and the lowest goodness of fit statistics. However, given that the results are so similar, these quantile choices make only a small difference to the overall goodness of fit.

| Parameter | True value | ||||

|---|---|---|---|---|---|

| KS |

4.5 Simulated data results

For the sampling interval , the Fourier invertibility condition is satisfied as the LHS of (3.3) is . The calibration results for the model with is shown in Table 2. Here, we find that MLE gives the best fit with the lowest statistic. The KS statistic for MLE and DME are approximately equal.

| Parameter | True value | MOM | MLE | DME |

| KS |

For the sampling interval , the Fourier invertibility condition is violated as the LHS of (3.3) is . The corresponding results are shown in Table 3. Here, we find that DME gives the best fit with the lowest KS statistic, however MLE still produces a good fit and does not break down. This suggests that the condition may not be necessary for the MLE to produce accurate parameter estimates. In both cases, , the RMSE and goodness of fit statistics are highest for MOM.

| Parameter | True value | MOM | MLE | DME |

|---|---|---|---|---|

| KS |

4.6 Real data results

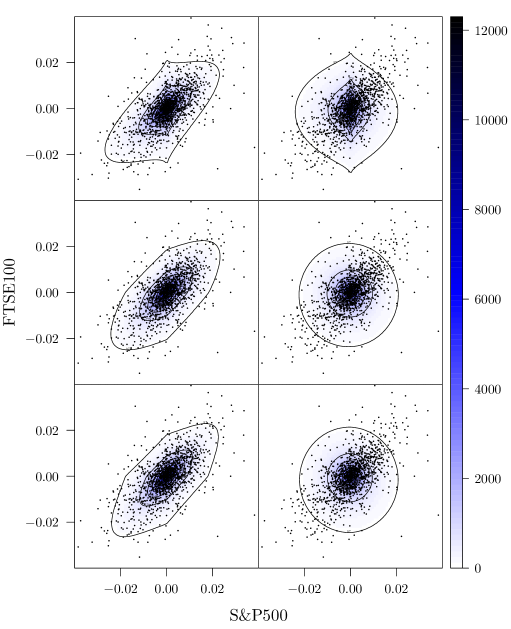

Next, we fit the and models to the S&P500 and FTSE100 indices as the bivariate price process (4.1) for a 5 year period from 14 February 2011 to 12 February 2016 with daily closing price observations taking . The estimated parameters, goodness of fit statistics and standard errors computed using 100 bootstrap samples are listed in Table 4. Contour plots of the fitted distributions and scatter plots of the bivariate log returns are shown in Figure 1.

| MOM | MLE | DME | ||||

| Parameter | ||||||

| KS | ||||||

Note that the Fourier invertibility condition is satisfied for all fitted models. Based on the , KS statistic and contour plots, the model produces a better fit than the model. In addition, for the model, DME gives a fit with a lower and KS statistic than MLE and MOM.

Assuming that the log returns satisfies the model, a likelihood ratio test can be used to test the hypothesis versus . The test statistic is asymptotically distributed with 1 degree of freedom. The -value is , so the model is rejected. Indeed, the model is not suited for modelling strong correlation since by Proposition 2.1 (vi), which is approximately 0 when is.

It has been suggested that log-returns should be self-decomposable [6, 7, 13]. Note that is very close to , which suggests that the log-returns process is indeed self-decomposable (see Proposition 2.1 (vii)). A likelihood ratio test can be used to test this hypothesis, versus . The test statistic is asymptotically distributed with 2 degrees of freedom. The -value is 0.128, so at a 5% significance level we cannot reject that is self-decomposable.

5 Conclusion

The process constructed by using weak subordination generalises the process, and we obtain a condition for Fourier invertibility in Theorem 3.1. We have shown that MOM, MLE and DME can be used to estimate the parameters of a process, and find that in our simulations MLE produces a better fit when the Fourier invertibility condition holds, while DME produces a better fit when it is violated. However, MLE may still produce good parameter estimates even when the Fourier invertibility condition is violated. In all cases, MOM produces the worst fit. We find that the process exhibits a wider range of dependence and produces a significantly better fit than the process when used to model the S&P500-FTSE100 data set, and that DME produces the best fit in this situation.

Appendix A Appendix

Lévy process. The reader is referred to the monographs [1, 5, 33] for necessary material on Lévy processes, to [2, 12, 15] for financial applications, while our notation follows [9, 10]. For , let and let denote the indicator function. Let be the Euclidean unit ball centred at the origin. The law of an -dimensional Lévy process is determined by its characteristic function , with

and Lévy exponent , where

, , is a covariance matrix, and is a nonnegative Borel measure on such that . We write provided is an -dimensional Lévy process with canonical triplet .

A subordinator is drift-less if its drift . All subordinators considered in this paper are drift-less.

An -dimensional random variable is self-decomposable if for any , there exists a random variable , independent of , such that . A Lévy process is self-decomposable if is.

Strongly subordinated Brownian motion. Let be a Brownian motion and be a drift-less subordinator. A process is the traditional or strong subordination of and if , .

Weakly subordinated Brownian motion. Let , and be a covariance matrix. Introduce the outer products and by

| (A.1) |

Let be an -dimensional Brownian motion and be an -dimensional drift-less subordinator. A Lévy process is called the weak subordination of and (see [10], their Proposition 3.1) if it has Lévy exponent

| (A.2) |

. Note that a more general definition of weak subordination and a proof of existence is given in [10].

Assume that independent and . If has indistinguishable components or has independent components, then

| (A.3) |

Otherwise may not a Lévy process, but always is (see [10], their Proposition 3.3 and 3.9).

Acknowledgement

B. Buchmann’s research was supported by ARC grant DP160104737. K. Lu’s research was supported by an Australian Government Research Training Program Scholarship.

References

- [1] Applebaum, D. (2009). Lévy Processes & Stochastic Calculus. Cambridge Studies in Advanced Mathematics, 116, 2nd ed, Cambridge University Press, Cambridge. MR2512800

- [2] Ballotta, L. & Bonfiglioli. E. (2016). Multivariate asset models using Lévy processes and applications. European J. Finance 22, 1320–1350.

- [3] Barndorff-Nielsen, O.E., Pedersen, J. & Sato, K. (2001). Multivariate subordination, self-decomposability and stability. Adv. in Appl. Probab. 33, 160–187. MR1825321

- [4] Barndorff-Nielsen, O.E. & Shiryaev, A. (2010). Change of Time and Change of Measure. World Scientific Publishing Co. Pte. Ltd., Hackensack, NJ. MR2779876

- [5] Bertoin, J. (1996). Lévy Processes. Cambridge University Press, Cambridge. MR1406564

- [6] Bingham, N.H. (2006). Lévy processes and self-decomposability in finance. Probability and Mathematical Statistics 26, 131–142.

- [7] Bingham, N.H. & Kiesel, R. (2002). Semi-parametric modelling in finance: Theoretical foundations. Quantitative Finance 2, 241–250.

- [8] Bogachev, V. I. (2007). Measure theory (Vol. 1). Springer Science & Business Media.

- [9] Buchmann, B., Kaehler, B., Maller, R., Szimayer, A. (2017). Multivariate subordination using generalised gamma convolutions with applications to variance gamma processes & option pricing. Stochastic Process. Appl. 127, 2208-–2242.

- [10] Buchmann, B., Lu, K., Madan, D. (2017). Weak subordination of multivariate Lévy processes and variance generalised gamma convolutions. To appear in Bernoulli. Available at https://arxiv.org/abs/1609.04481

- [11] Buchmann, B., Lu, K., Madan, D. (2017). Self-decomposability of variance generalised gamma convolutions Preprint. Australian National University and University of Maryland. Available at https://arxiv.org/abs/1712.03640

- [12] Cariboni, J. & Schoutens, W. (2009). Lévy Processes in Credit Risk. Wiley, New York.

- [13] Carr, P., Geman, H., Madan, D.B. & Yor, M. (2007). Self-decomposability and option pricing. Mathematical Finance 17, 31–57.

- [14] Cleveland, W.S., Grosse, E. & Shyu, W.M. (1991). Local Regression Models. Chapter 8, Statistical Models in S, editors Chambers, J.M. & Hastie, T.J., Chapman & Hall/CRC, Boca Raton.

- [15] Cont, R. & Tankov, P. (2004). Financial Modelling with Jump Processes, Chapman & Hall. London, New York, Washington D.C. MR2042661.

- [16] Finlay, E., & Seneta, E. (2008). Stationary-increment Variance-Gamma and models: Simulation and parameter estimation. Int. Stat. Rev. 76, 167–186. MR2492088.

- [17] Fung, T., & Seneta, E. (2010). Modelling and estimation for bivariate financial returns. International statistical review 78, 117–133.

- [18] Guillaume, F. (2013). The VG model for multivariate asset pricing: calibration and extension. Rev. Deriv. Res. 16, 25–52.

- [19] Kawai, R. (2009). A multivariate Lévy process model with linear correlation. Quantitative Finance 9, 597–606.

- [20] Küchler, U. & Tappe, S. (2008). On the shapes of bilateral Gamma densities. Statistics & Probability Letters 78, 2478–2484.

- [21] Luciano, E., Marena, M., & Semeraro, P. (2016). Dependence calibration and portfolio fit with factor-based subordinators. Quantitative Finance 16, 1037–1052.

- [22] Luciano, E. & Semeraro, P. (2010). Multivariate time changes for Lévy asset models: Characterization and calibration. J. Comput. Appl. Math. 233, 1937–1953. MR2564029

- [23] Madan, D.B. (2011). Joint risk-neutral laws and hedging. IIE Transactions 43, 840–850.

- [24] Madan, D.B. (2015). Estimating parametric models of probability distributions. Methodol. Comput. Appl. Probab. 17, 823–831. MR3377863

- [25] Madan, D.B. (2018). Instantaneous portfolio theory. Quantitative Finance. Available at https://doi.org/10.1080/14697688.2017.1420210

- [26] Madan, D.B., Carr, P.P., & Chang, E.C. (1998). The variance gamma process and option pricing. Review of Finance 2, 79–105.

- [27] Madan, D.B. & Seneta, E. (1990). The variance gamma (v.g.). model for share market returns. Journal of Business 63, 511–524.

- [28] Michaelsen, M. (2018). Information flow dependence in financial markets. Preprint. Universität Hamburg. Available at https://ssrn.com/abstract=3051180

- [29] Michaelsen, M. & Szimayer, A. (2018). Marginal consistent dependence modelling using weak subordination for Brownian motions. Quantitative Finance. Available at https://doi.org/10.1080/14697688.2018.1439182

- [30] Peacock, J.A. (1983). Two-dimensional goodness-of-fit testing in astronomy. Mon. Not. R. astr. Soc. 202, 615–627.

- [31] Rosenblatt, M. (1952). Remarks on a multivariate transformation. Ann. Math. Statist. 23, 470–472. MR0049525

- [32] Sasvári. Z. (2013). Multivariate Characteristic and Correlation Functions. Walter de Gruyter, Berlin, 2013. MR3059796

- [33] Sato, K. (1999). Lévy Processes and Infinitely Divisible Distributions. Cambridge University Press, Cambridge. MR3185174

- [34] Semeraro, P. (2008). A multivariate variance gamma model for financial applications. Journal of Theoretical and Applied Finance 11, 1–18. MR2398464

- [35] J. Wang. (2009). The Multivariate Variance Gamma Process and Its Applications in Multi-asset Option Pricing. PhD Thesis, University of Maryland.

- [36] Xiao, Y. (2017). A fast algorithm for two-dimensional Kolmogorov-Smirnov two sample tests. Computational Statistics & Data Analysis 105, 53–58.