Rational Models for Inflation-Linked Derivatives

Abstract

We construct models for the pricing and risk management of inflation-linked derivatives. The models are rational in the sense that linear payoffs written on the consumer price index have prices that are rational functions of the state variables. The nominal pricing kernel is constructed in a multiplicative manner that allows for closed-form pricing of vanilla inflation products suchlike zero-coupon swaps, year-on-year swaps, caps and floors, and the exotic limited-price-index swap. We study the conditions necessary for the multiplicative nominal pricing kernel to give rise to short rate models for the nominal interest rate process. The proposed class of pricing kernel models retains the attractive features of a nominal multi-curve interest rate model, such as closed-form pricing of nominal swaptions, and it isolates the so-called inflation convexity-adjustment term arising from the covariance between the underlying stochastic drivers. We conclude with examples of how the model can be calibrated to EUR data.111The authors are grateful to L. P. Hughston and to participants of the JAFEE 2016 Conference (Tokyo, August 2016), the CFE 2016 Congress (Sevilla, December 2016), 2016 QMF Conference (Sydney, December 2016), and of the London Mathematical Finance Seminar held at King’s College London (30 November 2017) for comments and suggestions. The authors especially acknowledge high-quality feedback provided by two anonymous reviewers.

Keywords:

Inflation-linked derivatives, rational term structure models, convexity adjustment, calibration, pricing kernels, year-on-year swap, limited price index.

AMS subject classification: 60J25, 60H30, 91G20, 91G30.

1 Introduction

The inflation market has grown in the aftermath of the 2008 financial crisis. Central banks have been conducting aggressive quantitative easing to keep inflation off the cliff of deflation, and the ensuing fears have driven hedging needs. As a consequence, the market for trading inflation has soared to the point where standard inflation derivatives are now cleared on the London Clearing House (LCH) in numbers exceeding 100 bn EUR measured by notional outstanding value in early 2017. As this number only counts linear derivatives, the total market size is likely much larger. Among the products cleared one finds the Year-on-Year swap (YoY swap), swapping annual inflation against a fixed strike, and the Zero-Coupon swap (ZC swap), which swaps cumulative inflation against a fixed strike at maturity.

Among the OTC-traded nonlinear derivatives, the most important is arguably the YoY cap/floor, which is in principle a portfolio of calls (caplets) or puts (floorlets) with equal strike on YoY inflation. Another significant derivative is the ZC cap/floor, which is simply a call/put on the ZC swap rate. The derivatives market is dwarfed in size by the market for inflation-linked bonds. These bonds are typically government-issued debt where the principal is linked to the consumer price index (CPI) or similar. The bonds often have an embedded YoY floor protecting the principal from being adjusted downwards by deflation. Limited Price Index (LPI) products come with both a lower and upper bound on the principal adjustment creating a path-dependent collar on inflation. Despite its exotic nature LPIs have been in high demand by pension funds. All products should ideally be priced in a consistent manner using a tractable arbitrage-free model. Cap/floor products display volatility skews and non-flat term structures of volatility, both of which the model also should be able to capture. Besides, the model should yield closed-form solutions for the price of the most traded derivatives, here the YoY and the ZC cap/floor.

(Hughston,, 1998) develops a general arbitrage-free theory of interest rates and inflation in the case where the consumer price index and the real and nominal interest rate systems are jointly driven by a multi-dimensional Brownian motion. This approach is based on a foreign exchange analogy in which the CPI is treated as a foreign exchange rate, and the “real” interest rate system is treated as if it were the foreign interest rate system associated with the foreign currency. The often-cited work by (Jarrow and Yildirim,, 2003) makes use of such a setup. They consider a three-factor model (i.e., driven by three Brownian motions) in which the CPI is modelled as a geometric Brownian motion, with deterministic time-dependent volatility and the two interest rate systems are treated as extended Vasicek-type (or Hull-White) models. Similar to (Jarrow and Yildirim,, 2003), (Dodgson and Kainth,, 2006) use a short-rate approach where the nominal and the inflation rates are both modelled by Hull-White processes while discarding the idea of a real economy. A GBM-based model for the CPI provides the baseline framework for how one might understand implied volatility in such a market, but any GBM model for the CPI does not, by construction, reproduce volatility smiles.

Further development of inflation models has paralleled that of interest rates models. For example inflation counterparts to the nominal LIBOR Market Model, see for example (Brigo and Mercurio,, 2007), have been studied in (Belgrade et al.,, 2004), (Mercurio,, 2005), and (Mercurio and Moreni,, 2006). While these models can reproduce smiles—augmented with stochastic volatility or jumps—they rely on numerically intensive algorithms or approximations for the pricing of ZC cap/floors, in particular. One may say similarly of the models by (Kenyon,, 2008), (Gretarsson et al.,, 2012), and (Mercurio and Moreni,, 2009) who in a similar manner use forward inflation, or in the case of (Hinnerich,, 2008) the forward inflation swap rate, as the model primitive. (Waldenberger,, 2017) builds an inflation counterpart to the nominal model of (Grbac et al.,, 2015) and (Keller-Ressel et al.,, 2013). One also finds (Ribeiro,, 2013) in the local volatility context, (Kruse,, 2011) extending the GBM methodology with (Heston,, 1993) stochastic volatility, and (Singor et al.,, 2013) adding stochastic volatility to the (Jarrow and Yildirim,, 2003) model. Our work is inspired by the approach to nominal term structure of interest rates based on the so-called rational models. This choice is motivated by the success of the rational model framework as documented in the comprehensive empirical study of (Filipović et al.,, 2017) who demonstrate that linear-rational models perform as well or better than similar affine term structure models. Furthermore, the rational model framework has been extended to model multiple nominal curves and credit risk in (Crépey et al.,, 2016) and (Macrina and Mahomed,, 2018); it is this approach we follow. This framework allows for analytical expressions for swaptions, which is not the case for affine term structure models. In this paper, we demonstrate how rational models for inflation are constructed, which retain the tractability of the nominal counterpart and can price, in closed-form, all the relevant derivatives suchlike YoY and ZC cap/floors and LPI swaps.

In Section 2, we first present the model in full generality. Following Döberlein and Schweizer, (2001), we study the conditions for a short rate model representation to be obtained. In Section 3 we derive option pricing formulae under different assumptions in the driving process, and in Section 4 we end with an example that shows how the model can be simultaneously calibrated to inflation derivatives and a multiple-curve nominal interest rate market.

2 Rational term structures

We adopt the pricing kernel approach, which was pioneered by (Constantinides,, 1992), (Flesaker and Hughston, 1996a, ), (Flesaker and Hughston, 1996b, ) and (Rogers,, 1997)—for a good summary see (Hunt and Kennedy,, 2004) and, for a more recent account, (Grbac and Runggaldier,, 2015). (Macrina and Mahomed,, 2018) propose pricing kernel models to construct so-called curve-conversion factor processes, which link distinct yield-curves in a consistent arbitrage-free manner, and which give rise to the across-curve pricing formula for consistent valuation and hedging of financial instruments across curves. Applications include the pricing of inflation-linked and hybrid fixed-income securities. A property of the pricing kernel approach is the ease with which the pricing and hedging of multiple currencies can be handled. This is the property one benefits from when considering inflation-linked pricing, and nominal and real economies are introduced in analogy to domestic and foreign economies. Compared to the classical approach, in order to allow for negative short rates, we relax the paradigm and consider general semimartingale dynamics for the pricing kernels. The approach taken next is one where the existence of a pricing kernel model is postulated and its dynamics are modelled. It is via the pricing kernel that no-arbitrage price processes of tradable assets are generated by imposing that the asset price process, when multiplied by the pricing kernel process, be a martingale with respect to the probability measure the pricing kernel dynamics are produced. This no-arbitrage notion is one presented in textbooks suchlike, e.g., Hunt and Kennedy, (2004) and Björk, (2009).

2.1 General model

We model a financial market by a filtered probability space , where denotes the real probability measure and the market filtration satisfying the usual conditions. A finite time horizon is considered, i.e., a time line , throughout.

Definition 2.1 (Pricing kernel).

We call a stochastic process with a pricing kernel if it is a strictly positive, càdlàg, semimartingale such that has finite expectation for all .

Let where is a probability measure on . Let be the (nominal) pricing kernel process. If we consider some claim , then by standard no-arbitrage theory, see e.g. (Hunt and Kennedy,, 2004), the process , defined by

| (2.1) |

is an arbitrage-free price process. The notation is short-hand for . Following (Nguyen and Seifried,, 2015)[Proposition 2.2], we have:

Proposition 2.2.

Consider assets with price processes satisfying Eq. (2.1), i.e., such that is a -martingale for . Assume the asset with strictly positive price process is traded. Then, the market is free of arbitrage.

Proof.

By Eq. (2.1), the process is a strictly positive martingale with . A measure may be defined by on any finite interval, and by the Bayes’ rule one obtains

for . Thus, is a risk-neutral measure associated with the numeraire . The existence of a pricing kernel, here the process , guarantees absence of arbitrage, also in the case of uncountably many assets. Here we refer to the no-arbitrage notion of “no asymptotic free lunch with vanishing risk” (NAFLVR) developed in (Cuchiero et al.,, 2016). ∎

We are agnostic as to how the asset with price process is chosen; for example it may be a zero-coupon bond. From formula (2.1) it follows that, for , the nominal zero-coupon bond price system,

| (2.2) |

is free of arbitrage opportunities. Assuming that is differentiable in , the short rate process may be obtained by the well-known relation This tells that determines simultaneously the inter-temporal risk-adjustment and the discounting rate.

The goal is to produce models, which facilitate the pricing of inflation-linked derivatives. To this end, we equip the framework with a real-market analogous to the foreign economy in the foreign-exchange analogy. If we assume that is a pricing kernel for the real market, then the foreign-exchange analogy establishes the relationship

| (2.3) |

where denotes the CPI process that acts as an exchange rate from the nominal to the real economy, see, e.g. (Björk,, 2009, Proposition 17.11).

As in (Flesaker and Hughston, 1996a, ), (Flesaker and Hughston, 1996b, ), (Rutkowski,, 1997) and (Rogers,, 1997), we introduce an extra degree of flexibility and model prices with respect to an auxiliary measure . This extra degree of freedom allows for simplified calculations or more tractable modelling under the -measure while desirable statistical properties may still be captured under the -measure. In fact it is also possible to build in terminal distributions or “views” under , in the spirit of (Black and Litterman,, 1992), and as explicitly obtained in (Macrina,, 2014). This is a feature expected by practitioners of inflation-linked trading, motivated by the fact that inflation is an area that often receives significant attention from monetary policymakers and is subject to so-called “forward guidance”. With regard to how to induce the measure change for such a purpose, we refer to (Hoyle et al.,, 2011), (Macrina,, 2014) for the multivariate generalisation, and (Crépey et al.,, 2016) for an application in a multi-curve term structure setup. We shall model the Radon-Nikodym process with as a strictly positive, càdlàg martingale and fix some time . Then, for , defines an equivalent measure. By setting , with no loss of generality, we can express the fundamental pricing equation (2.1) under by the Bayes formula:

| (2.4) |

for and . That is, is the nominal pricing kernel under the -measure. Similarly, the relationship introduces the real pricing kernel under . It follows that, under , and are strictly positive, semimartingales, see (Jacod and Shiryaev,, 2003)[III Theorem 3.13], and that for all .

Modelling convention. Let for , for modelling convenience. From the relation (2.3), it then follows . We model and , where , as strictly positive semimartingales under such that and have finite expectation for .

Definition 2.3 (Real-kernel spread model).

Let the triplet be such that , and are strictly-positive, càdlàg, and . Furthermore assume and are semimartingales and that is a martingale. Denote by the measure induced by . Assume that and have finite expectation for all under . We call such a triplet a real-kernel spread model (RSM).

Often, the pricing of inflation-linked instruments is performed under either the nominal risk-neutral measure or the real risk-neutral measure . In the general setting presented so far, one is not necessarily in a position to get consistent prices under these measures. In Section 2.2, we treat this issue in the context of some well-known models, which use from the outset a risk-neutral measure. In Section 2.3 we proceed to the pricing of primary inflation-linked securities in the backdrop of a more specific model class. In Section 2.4 we discuss the change to risk-neutral measures in the same model class.

2.2 Comparison with other models

In this section, we discuss other models and in a few cases show that our specification can be regarded as a generalisation. The comparisons shall help to understand our modelling approach in that they show how our model ingredients would look in known models.

In the case of equity pricing, the benchmark model is the geometric Brownian motion specification of (Black and Scholes,, 1973). In this sense, the most natural translation of this to inflation modelling is done by (Korn and Kruse,, 2004) specifying the inflation index under the nominal risk-neutral measure by

where and are the deterministic nominal and real interest rates and is a Brownian motion. Black-Scholes-type pricing formulae are derived for ZC caps with payoff function , and (Rubinstein,, 1991) derives a pricing formula of a similar type for YoY caplets with payoff function . We refer to (Kruse,, 2011) for the exact formulae. The formulae for the ZC cap and YoY caplet as functions of the volatility parameter can be inverted to implied volatilities as it is commonly done for equity options. This will be relevant in Section 4 when we calibrate some specific rational pricing models.

(Jarrow and Yildirim,, 2003) produce an important generalisation that allows for the pricing of inflation-linked securities with stochastic interest rates. In practice, the popular model specification is to assume that the nominal and the real interest rates have Hull-White dynamics. Under the nominal risk-neutral measure, such a model specification takes the form

where , and are dependent Brownian motions, and where and are functions chosen to fit the term-structure of interest rates, see (Brigo and Mercurio,, 2007)[Chapter 15] and (Hull and White,, 1990).

Proposition 2.4.

Proof.

The measure change to is given in (Jarrow and Yildirim,, 2003)[Footnote 5], the measure change to is similar and, in the Black-Scholes case, the results are standard. ∎

The choice above is not unique. One could, e.g., set and change the other processes accordingly, which would amount to specifying and matching the models under , instead.

2.3 Primary inflation-linked instruments

We now proceed to the pricing of the primary inflation-linked products, suchlike the ZC swap and the YoY swap, which serve as the fundamental hedging instruments against inflation risk and the swap rates as underlying of exotic inflation-linked derivatives. To this end, we propose a specific class of rational pricing kernels:

Definition 2.5 (Rational pricing kernel system).

Let be a measure equivalent to induced by a Radon-Nikodym process . Let and be positive martingales under with . Let have finite expectation under for all . Let the real pricing kernel be given by where is a strictly positive deterministic function with , and where is a deterministic function that satisfies . Furthermore, let where is a strictly positive deterministic function with , and set We call thus specified a rational pricing kernel system (RPKS).

By Ito’s lemma, and are strictly positive semimartingales. An RPKS is in particular an RSM-triplet and therefore, by Section 2.1, it produces a nominal and a real market, both free of arbitrage opportunities. The martingale () generates the randomness in the real market, while the joint law of () and () generates the randomness in the nominal market. All derivations throughout will be obtained under the assumption of having an RPKS.

Proposition 2.6 (Affine payoffs evaluated in an RPKS).

Assume an RPKS. The price process of a contract with payoff function , for , at the fixed date is given by

| (2.5) |

where, for , , , , . If , i.e. the payoff is linear in , the price process is a rational function of and .

Proof.

It follows by the -pricing equation (2.4). ∎

The price process of the nominal ZC bond follows from Eq. (2.5) for and . We have,

| (2.6) |

with and given in Proposition 2.6. It then follows that the initial nominal term structure , , is given by In particular, the parameter function appearing in both, the price processes of the nominal ZC bond and the contract (2.5), can thus be used for calibrating to the market-observed prices , , according to We note that should not belong to , one can calculate its value in all relevant time points and use a -interpolation, and nevertheless produce the same price for any financial product whose payoff only depends on state variables at those times.

The most basic inflation-linked product is the ZC swap, which gives exposure to the CPI value at the swap maturity for an annualised fixed payment. Its price process can be written in the form

| (2.7) |

where is the price of an inflation-linked ZC bond at . ZC swaps are highly liquid for several maturities and therefore it is reasonable to consider an actual term-structure of ZC swaps and aim at constructing models able to calibrate to the relevant market data in a parsimonious manner. By Eq. (2.7), given a nominal term-structure, a ZC swap term-structure is equivalent to an inflation-linked ZC bond term-structure, and fitting either is equivalent. The price of an inflation-linked ZC bond within an RPKS follows directly from Proposition 2.6:

with and given in Proposition 2.6. We see that by matching the degree of freedom to the initial term structure of inflation-linked bonds as implied from the market, i.e. , the model replicates the term structure of ZC swaps. For ZC swaps, a de-annualised fair rate is quoted, namely a number such that for the initial value of the swap is zero. Given , the initial term structure is implied from the ZC swap market fair rates via The price process of a real ZC bond is

| (2.8) |

with and as in Proposition 2.6. In accordance with the foreign-exchange analogy, it holds that

Next, we consider the Year-on-Year swap (YoY swap) which exchanges yearly percentage increments of CPI against a fixed rate. The YoY swap can be decomposed into swaplets, so we consider first the price at time of a such over the period . By the pricing relation (2.4) we have

| (2.9) |

with and as in Proposition 2.6. For YoY swaps the fair rate is quoted in financial markets such that . The price of the swap is , from which the fair rate can be extracted:

| (2.10) |

If independence between and is assumed, the YoY swap rate at time becomes

Thus, if the independence assumption is imposed, the swap rate is completely determined by the inflation-linked and nominal term structures and hence can be expressed in a model-independent fashion. The difference between the market-observed swap rate and the above expression is often referred to as the convexity correction for the YoY swap of length .

2.4 On short-rate representation

In the following section, we study the question of the existence of a classical savings accounts in an RPKS, which is related to the work of Döberlein and Schweizer, (2001). We shall see that the obtained class of nominal pricing kernels can rarely be represented in terms of a short rate model. We study the reasons behind the lack of such a property. If it is possible to decompose a pricing kernel into

| (2.11) |

where is a short rate process and is the corresponding numeraire measure, then the prices obtained in either model would be equal, i.e. the same prices could instead have been obtained using a short rate approach. To investigate whether a decomposition like (2.11) exists, some technical material is needed.

We recall that a special semimartingale is a process with a unique decomposition , where is predictable and of finite variation, is a local martingale and . The decomposition is called the canonical (additive) decomposition. We recall (Jacod and Shiryaev,, 2003, II Theorem 8.21)

Theorem 2.7.

Let be a semimartingale with , such that and are strictly positive. Then, is a special semimartingale if and only if it admits a multiplicative decomposition

| (2.12) |

where is a strictly positive and càdlàg -local martingale, is a positive, predictable process with locally finite variation, and . When the decomposition exists, it is unique and is given by

where and are the processes in its canonical additive decomposition.

Comparing Eq. (2.11) and Eq. (2.12) in Theorem 2.7 we see that a number of conditions need to be satisfied for a short rate representation to be available. The pricing kernel has to satisfy the assumptions of Theorem 2.7, has to be a true martingale and act as a measure change, needs to have the specific form in (2.11) and finally the resulting ZC bond prices need to be sufficiently differentiable. More precisely, following (Döberlein and Schweizer,, 2001, Theorem 5 and Proposition 12), when (2.12) exists for a pricing kernel, one calls an implied savings account. When in addition is satisfied, where is adapted and , then the forward and short rates exist, that is, (2.11) holds, and is termed a classical savings account.

Our first endeavour is to characterise the real-economy risk-neutral measure . In the case that the short-rate process exists, we denote it by . If in addition is absolutely integrable, then the discount factor exists, and we define

We introduce the process , given by

and note that , for all . Next, we denote by the stochastic exponential and define

| (2.13) |

which is strictly positive for all .

Lemma 2.8.

Assume an RPKS. Then has a savings account if and only if in (2.13) is an -martingale. In this case, , and the savings account is classical with short rate process given by

| (2.14) |

Proof.

We now examine the nominal market processes; this endeavour is slightly more elaborate. In the case that the nominal short-rate process and the associated discount factor exist, we write

We furthermore define

and , which is differentiable in in the case that the nominal short rate exists in an RPKS. In the case that , we define the stochastic exponential We note that , i.e. for all . We define the “pseudo short-rate”

| (2.16) |

Lemma 2.9.

Assume an RPKS and that exists. Consider the “pseudo short-rate” (2.16). Then has a classical savings account with short rate , given by

| (2.17) |

if and only if and is an -martingale.

Proof.

Lemma 2.9 is a weaker result than Lemma 2.8, since is not necessarily a local martingale. The result is still interesting because is the most tempting candidate for a short-rate process in a discount factor emerging from a nominal pricing kernel. Lemma 2.9 shows that, in general, we cannot expect to have a classical savings account with short rate . This rules out though neither the existence of a savings account nor a classical savings account with a different “short-rate”. To apply the theory we need to be a special semimartingale.

Lemma 2.10.

Assume an RPKS and that is a special semimartingale. Then the canonical additive decomposition is given by where

| (2.19) | |||||

The multiplicative decomposition is where

moreover, a savings account exists if and only if is a martingale.

Proof.

When there are no simultanous jumps in and the situation is simpler:

Corollary 2.11.

Assume an RPKS, and that a.s. Then is a special semimartingale and the canonical decomposition is given by where

and where

and a savings account exists if and only if is a martingale. If additionally is absolutely continuous, write and define for . Then,

and, if , then a classical savings account exists.

Proof.

By assumption, we have that and thus the decomposition above has a predictable bounded variation part. By change of variables, . That is, by (Döberlein and Schweizer,, 2001, Proposition 12), integrability implies existence of a classical savings account. ∎

A simple example where the first condition is satisfied is if or is continuous. If both and are Ito processes then is absolutely continuous.

Finally we present a lemma giving a condition in an RPKS to check whether is special, this will be particularly simple to check in the following setting.

Lemma 2.12.

Assume an RPKS and that and are locally square-integrable. Then is a special semimartingale.

3 Construction of the exponential-rational class

Our next goal is to derive explicit price formulae for financial derivatives based on the ZC and the YoY swap rates, and for the so-called limited price-index (LPI) swap. For its flexibility, tractability and good calibration properties, we choose to work with a sub-class among the rational pricing kernel systems, namely the exponential-rational pricing kernels. We next construct this class.

Definition 3.13 (Exponential-rational pricing kernels).

Assume an RPKS and let be a d-dimensional stochastic process. Assume that and in Definition 2.5 are on the form and . We call this class the exponential-rational pricing kernel models. If is an additive process, we call this class the additive exponential-rational pricing kernel models.

Remember that an RPKS requires that and are martingales, that has finite expectation for all and that , it is implicit that and in Definition 3.13 are chosen such that this is satisfied.

Definition 3.14 (Additive process).

Let be a d-dimensional stochastic process. Following (Sato,, 1999, Definition 1.6), we say is additive if it has a.s. càdlàg paths, , and

-

1.

Independent increments: for any , , the random variables are independent,

-

2.

Stochastic continuity: for any and , .

In the remainder of the paper, the derivations will be based on exponential-rational pricing kernel models. The additive exponential-rational pricing kernel models will be given particular attention, so we now recall some facts about additive processes and provide some examples. The independent increments property gives a Lévy-Khintchine representation

where the Lévy-Khintchine triplet (,,) is unique and satisfies a number of conditions (see (Sato,, 1999, Chapter 2)). The Lévy-Khintchine triplet also determines the sample path properties of by the Lévy-Ito decomposition (see (Sato,, 1999)[Chapter 4]). Next, we consider examples of how additive processes can be obtained.

Example 3.15 (Time change).

Let be a continuous, increasing process with . For , define pathwise for a Lévy process. Then inherits the independent increments of and is therefore additive. A particular simple case is obtained by letting be deterministic. Then, we may write where is the characteristic exponent of in .

Example 3.16 (Stacking independent additive processes).

Let be one-dimensional additive processes with characteristic exponents . Then is an N-dimensional additive process with characteristic exponent where . Furthermore, for is a one-dimensional additive process with characteristic exponent .

A fact about additive processes is that they are convenient to construct martingales. Define

| (3.20) |

then for it holds that and the Laplace exponent is well-defined, see Sato, (1999)[Theorem 25.17]. It follows from the independent increments property that for , one has

| (3.21) |

is a martingale. We can build exponential martingales by taking an additive process and let the drift absorb the mean in (3.21). This produces the condition that, if

| (3.22) |

then is a martingale. Eq. (3.20) is useful for additive-exponential rational models. Recall Definition 2.5, Eq. (3.20) shows that has finite expectation for all if . Similarly, recalling Lemma 2.12, and are locally square-integrable if and .

We proceed to calculate a number of expressions needed in both the previous and next sections. First, for and ,

where we define the forward Laplace exponent . For the YoY swap (2.9) we also need

where is assumed. We notice that the sign, and to some extent the magnitude of the covariance, depends on the non-linearity of . For the subsequent derivation of Fourier-inversion formulae, we will also need the multiperiod generalized characteristic function.

Lemma 3.17.

Let be an additive process. Assume , set and define

Set and for . Assume that for . Then,

| (3.23) |

which is well-defined and finite.

Proof.

The statement follows from iterated expectation and the independent increments property. ∎

We next build on the ideas of the Examples 3.15 and 3.16 with two concrete specifications for the additive exponential-rational pricing kernel models. Very similar models will be calibrated in Section 4.

Specification 3.18 (Time-changed Lévy).

Let be a Lévy process satisfying the condition . Let be given points such that both coordinates are increasing and let be a continuous, non-decreasing interpolation. Then interpolates the given points. This property can be utilised for, e.g., fitting a term-structure of at-the-money implied volatilities. Building on this motivation, we let

Let and denote the Lévy-Khintchine triplets of and . Then has the Lévy-Khintchine triplet

where and . By choosing the drifts and according to (3.22) we can turn and into martingales. This construction generalises to higher dimensions in a straightforward way.

Specification 3.19 (Time-changed Wiener process).

3.1 Option pricing

By use of the exponential-rational pricing kernel models, tractable expressions can be derived for inflation-linked derivatives, such as the YoY floor and the ZC floor. Under the stronger assumption of additive exponential-rational pricing kernel models, we can find a similarly tractable formula for the LPI swap.

3.1.1 Year-on-Year floors

The payoff of the YoY floor can be written in terms of a series of floorlets. A floorlet has payoff function paid at time , typically is quoted with . In practice it is often observed that to ensure that there is a reliable observation of CPI available at maturity. We want our framework to be able to accommodate this feature. The next theorem is a pricing formula for the YoY floorlet.

Theorem 3.20.

Assume an exponential-rational pricing kernel model. Let , and where , , and . Let and assume that

| (3.24) |

Let and consider

by Eq. (2.4), the price of the YoY floorlet. Then we have:

| (3.25) |

where and . If , then .

Proof.

By the pricing formula (2.4) the price at any time is

We can directly apply Lemma A.33, found in the appendix, to get (3.25). Note that if then a part of is measurable. The formula for follows by observing that the payoff function is -measurable and recalling Eq. (2.2) combined with the relation (2.4). ∎

A point to note about (3.25) is the quadratic convergence of the numerator in the integral, which makes the formula particularly tractable. In the case that we use an additive exponential-rational pricing kernel model, follows from an application of Lemma 3.17, and the integrability (3.24) is satisfied if . Note that the difference between a YoY caplet and floorlet is a YoY swaplet, potentially with time-lag. The price is

| (3.26) |

where and are given in Theorem 3.20. This can be used in conjunction with Theorem 3.20 to get the price of a caplet or used directly to price the time-lagged swaplet.

3.1.2 Zero-Coupon floors

Next we focus on the pricing of the ZC floor, which together with the ZC cap and YoY caps and floors, are the most liquidly traded inflation-linked derivatives. The structure of this section closely follows the previous one, since the calculations are similar. The payoff at time of the ZC floor can be written in the form with akin to the YoY floor. Typically, the strike quoted is , where .

Theorem 3.21.

Assume an exponential-rational pricing kernel model. Let , and , where

and . Assume and

| (3.27) |

Consider and let

be the price at time of a ZC floor. Then we have

where and . If , then .

Proof.

Exactly as for the YoY case, see Theorem 3.20. ∎

If we assume the additive exponential-rational pricing kernel, follows directly from (3.23), and the assumption (3.27) is satisfied if . Analogous to the YoY cap we have the time-lagged ZC swap has price

| (3.28) |

where and are given in Theorem 3.21. Which can also be used to obtain the price of ZC caps.

3.1.3 Limited price index swap

The tractability of the model specification we have used so far allows to find semi-closed-form price formulae for the exotic limited price index (LPI) swap. This, contrary to the previous theorems, does rely on the assumption that the driving stochastic process is additive. The LPI is defined by

where and is a periodic fixed date, typically yearly. The contracts have maturities up to 30 years. Similar to the ZC swap, the LPI swap has payoff . We will consider the payoff to be settled at the fixed time . The pricing relation (2.4) gives the swap price at time :

where is the price process of the LPI-linked ZC bond. We therefore need to derive the price at time of the LPI-linked ZC bond.

Theorem 3.22.

Assume an additive exponential-rational pricing kernel model. Assume, without loss of generality, that . Let, for ,

and be such that

Then,

where

Furthermore, for

where , and

Proof.

First we write

Note that is -measurable and independent of . Using the tower property and the independent increments property we have:

| (3.29) | ||||

All the expectations can be calculated by Lemma A.32, in the appendix, to obtain

The remaining remaining expectations are calculated in the same way. ∎

We note that each is calculated like a ZC floor or YoY caplet, i.e. the evaluation is no more complicated than for a YoY cap. To price multiple LPI-linked ZC bonds, the shorter maturity bond prices can be found from the factors needed for the longer maturity ones.

3.2 Gaussian formulae

In this section we derive the results equivalent to Theorems 3.20, 3.21 and 3.22 under the assumption of the model in Specification 3.19. The results will be Black-Scholes-style formulae.

Proposition 3.23.

Proof.

Using the independent increments property

Now we apply Lemma A.35 to each term to obtain the result. ∎

The case where is derived similarly, see Proposition 3.25. The price formula for the ZC floor is derived analogously.

Proposition 3.24.

Proof.

Using the properties of the conditional expectation and the independence of the increments, we may write

Now applying Lemma A.34 to each term yields the result. ∎

The formula for the price process of the LPI-linked ZC bond follows in the same way.

Proposition 3.25 (Limited price index bond).

3.3 Nominal products

An important nominal linear interest rate derivative is the swap which pays the difference between a fixed rate and a floating rate. Loosely speaking we refer to this rate as the LIBOR. Suppose we have a sequence of time points , and let . A payer’s swap pays at each , where is the LIBOR spot rate. We assume for ease of exposition that payments on the fixed leg and floating leg both occur at time . It follows that the price of the swap at time is given by

| (3.30) |

Definition 3.26 (Single-curve setup).

If LIBOR rates are spanned by a single system of nominal bonds for all tenors, we say that we are in the single-curve setup.

We refer to (Grbac and Runggaldier,, 2015) for an overview of single- and multi-curve interest rate models. Within the single-curve setup, we have the no-arbitrage relation

It follows that

and thus the swap price is given by

| (3.31) |

3.3.1 Swaptions

A swaption is an option to enter a swap at some future time. If we let this point in time be and denote the maturity of the underlying swap by , the swaption price at is given by Eq. (2.4) and we have

| (3.32) |

where is the notional.

Proposition 3.27.

Assume an additive exponential-rational pricing kernel model and assume the single curve setup. Let , as in (3.32), be the swaption price at time . Let denote the payment dates of the underlying swap. Set

If and , then , and if and , then

If , define , and . Let if and if . Assume that . Then

where and .

Proof.

From the nominal bond pricing formula (2.6) we have that

Then, inserting this into the swap formula (3.31), we obtain

We may write

| (3.33) |

Collecting terms and using the fact that for any , we arrive at

If and , then

| (3.34) |

where we recall that . The result follows from Lemma A.31. If and , then

| (3.35) |

and the result follows from Lemma A.32. The two remaining cases are straightforward. ∎

The independent increments property of is only used to obtain Eq. (3.33).

3.3.2 Multi-curve interest rate setting

We can, at a relatively low cost, allow our model to incorporate multi-curve-features. This is done by modelling (3.30) as a rational function of state variables not fully spanned by the ones driving the nominal bonds. We model the forward LIBOR by

(Crépey et al.,, 2016) propose the following definition, which we shall adopt.

Definition 3.29 (Rational multi-curve setup).

Let

| (3.36) |

where is an -martingale with , and where and are deterministic functions.

We consider where is chosen such that is a martingale. This is analogous to how and are modelled. Adding a multi-curve dimension to the nominal markets has no effect on any of the formulae derived for the inflation products. It does though impact the swaption formula.

Proposition 3.30.

Assume an additive exponential-rational pricing kernel model and the multi-curve setup. Consider a swaption with maturity written on a swap with payments dates . The swaption price at is given by

| (3.37) |

where is the distribution of and

Furthermore,

Proof.

We note that, analogous to the single-curve setup, the independent increments of are only used to evaluate . In our applications, since is bi-variate, we may apply the two-dimensional cosine method of (Ruijter and Oosterlee,, 2012). The most immediate method for handling (3.37) in higher dimensions is in the style of (Singleton and Umantsev,, 2002), where with being exact. If , this leads to a one-dimensional integral, see (Kim,, 2014) and (Cuchiero et al.,, 2019). If the inversion formula becomes a two-dimensional (Hurd and Zhou,, 2010)-type formula.

4 Calibration examples

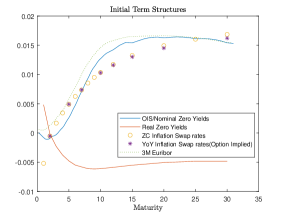

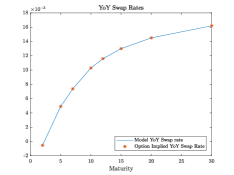

In this section, we show the calibration properties of the models on real data. We consider EUR data from Bloomberg from 1 January 2015. The necessary data consists of OIS zero-yields constructed from EONIA overnight indexed swaps, LIBOR discrete curves based on EURIBOR and a term structure of ZC forward rates, as well as YoY cap and floor prices and EURIBOR swaptions. There is no LPI traded on EUR data. The OIS and EURIBOR curves are constructed directly in the Bloomberg system. We then set the nominal curve equal to the OIS curve, and the initial real (or equivalently the initial inflation-linked) curve is implied from the OIS curve and zero-coupon inflation forward rate using the methodology described in Section 2.3. The prices for YoY caps and floors are available to us for maturities 2, 5, 7, 10, 12, 15, 20 and 30 years. The strikes for the floors range from -1% to 3% and caplets from 1% to 6%. Quotes for YoY swap rates are not available to us, but the overlap in strikes for YoY caps and floors allows us to use put-call (cap-floor) parity to imply YoY swap rates consistent with the option prices.

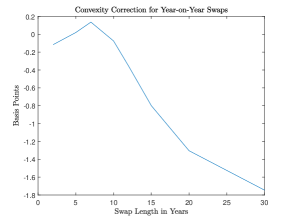

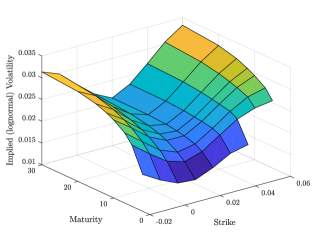

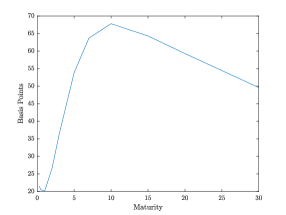

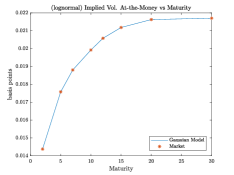

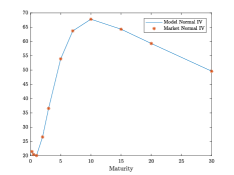

In Figure 1, all the curves are plotted on the left-hand side. The real curve is plotted as zero-coupon rates, and we note that on this day, there is a consistently negative real curve with a widening gap to the nominal as the maturity increases. The 3m EURIBOR and OIS curve are plotted as discrete forward rates with 3m increments to be directly comparable, and we can note a significant spread between the two curves in the short and most liquid end of the maturity spectrum, which warrants the use of a multi-curve model to price nominal products. Finally, we observe that the option-implied YoY swap rates are close to the ZC swap rates. This relation implies only small levels of the convexity correction as seen directly in the right-hand-side of Figure 1 where the convexity correction, as described in Section 2.3, is plotted for different swap lengths. An implied lognormal volatility surface is constructed from the prices of these options (selecting out-of-the-money options where available) using a geometric Brownian motion model for the CPI index as described in Section 2.2. Two of the prices for the two year maturity are identically zero and are thus removed from the dataset. We find the at-the-money implied volatility of the YoY cap using the piecewise constant hermite interpolation. The surface is plotted in the left hand side of Figure 2, and one can see a significant volatility smile, but also volatility levels that are quite low, around only 1.5-3%. Finally we consider a EURIBOR term structure of swaptions with maturities ranging from 3m, 6m, 1Y, 2Y, 3Y, 5Y, 7Y, 10Y, 15Y, 20Y to 30Y. Since the focus of the paper is on the inflation component we limit our modelling to one curve—the 3m tenor curve. We thus calibrate only to swaptions with a one-year underlying swap length, since this swaption, by EUR market convention, contains payments involving only 3m EURIBOR. We refer to (Crépey et al.,, 2016) for a more extensive calibration involving matching the volatility of both the 3m and 6m EURIBOR curves in a rational model resembling this one, but without the inflation component. Due to the lognormal assumption for swap rates precluding negative interest, rates it is now customary to quote swaption prices in normal or Bachelier implied volatility as opposed to lognormal. This is done on the right panel in Figure 2. The data is from 1 January 2015, and we calibrate directly to these volatilities.

Very similar to Specification 3.18, our model setup is the following:

where for are deterministic martingalizing functions and thus the model is a two factor model. We assume that is a two-dimensional Lévy process with independent marginals and that is a deterministic time-change. The two independent Lévy processes are defined by their Laplace exponents

at . Thus we are in the additive exponential-rational pricing kernel setup with

We set , and . This means that the parameter determines the dependence between the and and it furthermore means that the randomness in is merely a (log)-linear transformation of the randomness in . As in (3.21), when we can solve for the martingalizing drifts to obtain

We set the deterministic time-change , where is a piecewise constant function

Here , is the set of maturities quoted in the YoY option market. We calibrate the constants starting from the smallest to the largest maturity by matching to the YoY cap/floor volatility surface allowing a perfect fit to at least one strike per maturity. The dependence structure between the and component is fully determined by the parameter thus reducing the model to a two-factor setup where the calculated expressions for YoY caplets, YoY swap prices and swaption prices can be applied directly without approximation.

The nominal and the real curve are fitted by construction, but fitting the term-structure of YoY swap rates is less straightforward, since the swap rate depends on the full parameter set of the model, see Eq. (2.10). We choose to calibrate the function to this term structure. There is enough flexibility in the function to fit the YoY swap rates without error, but direct calibration results in a quite volatile function which is hardly desirable. Therefore we instead fit an eight-knot Hermite polynomial with a non-smoothness penalty – a similar choice is made in (Gretarsson et al.,, 2012) – and we find that the loss of accuracy when doing this is insignificant. The flexible shape means that the correlation parameter and volatility parameter in practice cannot be identified simultaneously with from the YoY swap curve. We solve this issue by simply fixing the and the parameters before calibration. In practice one needs only to avoid setting these parameters too low because the convexity correction becomes zero, by construction, if or . In both of our calibration examples we fix these values at and .

Since swap rates are determined not only by the function, but the full parameter set of the model, one cannot calibrate independently of and the parameters determining the process. On the other hand, YoY cap and floor prices are primarily affected by the component and thus not very sensitive to the changes in values of unless the correlation between and is very high, which means this dual identification problem is in fact easily solved in practice. The overall calibration algorithm can be reduced to:

-

1.

Set , and calibrate and the parameters of determining the law of to YoY cap/floor implied volatilities.

-

2.

Calibrate to the curve of YoY swap rates rates using least squares minimization with a penalty for .

-

3.

Repeat Step 1 using instead the updated values of .

-

4.

Calibrate to swaption prices.

The swaption calibration is done by calibrating the function sequentially. This means that the parameter, which also determines overall variance cannot be calibrated at the same time and we therefore fix it at below. We parametrise the function by setting . The function is then piecewise constant in relation to the swaption maturities we can observe, i.e.

with .

Gaussian example

We first assume that and are independent standard Brownian motions with Laplace exponent at , i.e. in the spirit of Specification 3.19. We would not expect a Gaussian or log-normal model to be well suited to reproduce implied volatility smiles, but we nevertheless believe that a Gaussian setup is illustrative as a benchmark case of study.

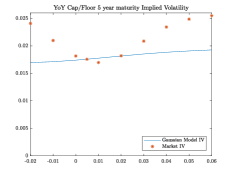

As discussed above, we first fix the and , and then proceed with the calibration algorithm described above. In Step 1 we choose to calibrate to at-the-money implied volatility. This is done sequentially starting with calibrating to the two-year YoY implied volatility and to the five-year YoY implied volatility, and so forth. We note that the value of affects not just the two-year maturity but all YoY option maturities (larger than two years) since we are calibrating directly to caps, which have annual payments every year until maturity. Thus the sequential nature of the calibration of these parameters is key. The result of this calibration can be seen in Figure 3 where we plot at-the-money implied volatility from the market. We furthermore plot an example of the model smile in the for a fixed maturity of five years. While the model smile is not completely flat, the Gaussian structure is, by construction, not suited for smile fitting. Finally the YoY swap rates are fitted without error by adjusting the function. YoY swap rates requires only mild adjustment of the function away from its default value of one.222 All parameter values are available upon request.

When fitting to swaptions we fix as explained above. Then we sequentially fit the function directly to swaption normal implied volatility starting from the three-month maturity up to the thirty-year maturity. The model is made to fit at-the-money, swaptions only, and the results are plotted in the lower right quadrant of Figure 3.

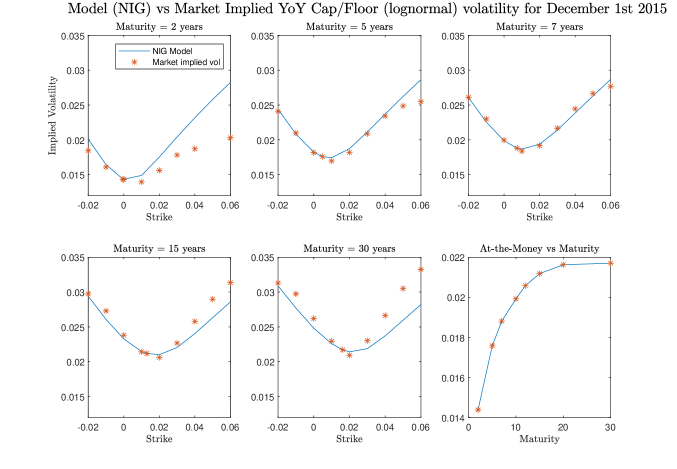

NIG example

To produce a model more in line with the volatility smile, we instead assume that are independent Normal Inverse Gaussian (NIG) processes, see for example (Barndorff-Nielsen,, 1998). We have that the Laplace exponent at is given by

expressed in terms of the parametrisation as where and Since we want to control variance primarily using the time-change , we set so that and both have variance of 1. Since we are only calibrating to the YoY cap/floor smile the full distribution of both marginals in is not identified by the data. For simplicity, we also set and . As in the Gaussian case we prefix and . In the NIG case we split Step 1 in the calibration process by first fixing the rate of time at a constant, i.e. , and then calibrate to the whole YoY cap/floor implied volatility surface using the lsqnonlin algorithm in Matlab. Thereafter, the individual are calibrated sequentially such that the model fits the at-the-money implied volatilities without error. The rest of the algorithm is followed exactly like in the Gaussian case.

The fit to YoY swap rates is indistinguishable from the graph in Figure 3 and is not plotted again. We set and fit the function to the same dataset of swaptions on one-year underlying swaps. The resulting fit is again indistinguishable from the fit in Figure 3 and the calibrated function is available upon request. In Figure 4, we plot model vs market volatility smiles for select maturities. We have only used one time-dependent scaling, so the model fits the at-the-money level without error. The remaining option prices are in principle fitted using only two parameters and . Thus we would not expect a perfect fit for all maturities. In general, any Lévy process is well known to exhibit a flattening smile as maturities are increased which often results in a slightly too steep smile in the short end and too flat in the long end. These problems could be resolved by introducing further time-inhomogeneity or by applying stochastic time-changes, but with the virtue of model simplicity taken into account, we view the calibrated setup as satisfactory.

5 Conclusions

This paper focuses primarily on the theoretical development of stochastic, rational term-structure models using pricing kernels suitable for the pricing of nominal and inflation-linked financial instruments. We demonstrate how this model class can be constructed with a view towards calibration to market data. We furthermore show how the models extend the classical short rate approach to inflation modelling. We expect future research to be focused more on the numerics of risk management within the model as well as calibration to a broader set of market instruments such as joint calibration of year-on-year and zero-coupon caps, as well as including time-series information in the calibration problem.

Appendix

Appendix A Lemmas

This section contains a number of lemmas used for the derivation of the formulae for option pricing.

Lemma A.31.

Let be the moment generating function of , a random vector with conditional distribution . Assume , and . Then,

We omit the proof of this lemma since it is standard.

Lemma A.32.

Let be the moment generating function of , a random vector with conditional distribution . Assume , and . Then,

Lemma A.33.

Let be the conditional moment generating function of , a random vector with conditional distribution . Assume and that Then

Proof.

Lemma A.34.

Let and with and assume that . Then

where , , and .

Proof.

By conditional of normals . Noting that , the tower property yields

as sought. ∎

Proof.

As Lemma A.34. ∎

References

- Barndorff-Nielsen, (1998) Barndorff-Nielsen, O. E. (1998). Processes of normal inverse Gaussian type. Finance and Stochastics, 2(1):41–68. https://doi.org/10.1007/s007800050032.

- Belgrade et al., (2004) Belgrade, N., Benhamou, E., and Koehler, E. (2004). A market model for inflation. Working Paper. http://dx.doi.org/10.2139/ssrn.576081.

- Björk, (2009) Björk, T. (2009). Arbitrage Theory in Continuous Time. Oxford University Press.

- Black and Litterman, (1992) Black, F. and Litterman, R. (1992). Global portfolio optimization. Financial Analysts Journal, 48(5):28–43. https://doi.org/10.2469/faj.v48.n5.28.

- Black and Scholes, (1973) Black, F. and Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy, 81(3):637–654. http://dx.doi.org/10.1086/260062.

- Brigo and Mercurio, (2007) Brigo, D. and Mercurio, F. (2007). Interest Rate Models – Theory and Practice: With Smile, Inflation and Credit. Springer-Verlag Berlin Heidelberg.

- Constantinides, (1992) Constantinides, G. M. (1992). A theory of the nominal term structure of interest rates. The Review of Financial Studies, 5(4):531–552. https://doi.org/10.1093/rfs/5.4.531.

- Crépey et al., (2016) Crépey, S., Macrina, A., Nguyen, T. M., and Skovmand, D. (2016). Rational multi-curve models with counterparty-risk valuation adjustments. Quantitative Finance, 16(6):847–866. https://doi.org/10.1080/14697688.2015.1095348.

- Cuchiero et al., (2019) Cuchiero, C., Fontana, C., and Gnoatto, A. (2019). Affine multiple yield curve models. Mathematical Finance, 29(2):568–611.

- Cuchiero et al., (2016) Cuchiero, C., Klein, I., and Teichmann, J. (2016). A new perspective on the fundamental theorem of asset pricing for large financial markets. Theory of Probability & Its Applications , 60(4):561–579.

- Dodgson and Kainth, (2006) Dodgson, M. and Kainth, D. (2006). Inflation-linked derivatives. Royal Bank of Scotland Risk Training Course, Market Risk Group.

- Döberlein and Schweizer, (2001) Döberlein, F. and Schweizer, M. (2001). On savings accounts in semimartingale term structure models. Stochastic Analysis and Applications, 19(4):605–626.

- Filipović et al., (2017) Filipović, D., Larsson, M., and Trolle, A. B. (2017). Linear-rational term structure models. The Journal of Finance, 72(2):655–704. https://doi.org/10.1111/jofi.12488.

- (14) Flesaker, B. and Hughston, L. (1996a). Positive interest. Risk, 9(1):46–49.

- (15) Flesaker, B. and Hughston, L. (1996b). Positive interest: Foreign exchange. In Vasicek and Beyond. Risk Publication.

- Grbac et al., (2015) Grbac, Z., Papapantoleon, A., Schoenmakers, J., and Skovmand, D. (2015). Affine LIBOR models with multiple curves: Theory, examples and calibration. SIAM Journal on Financial Mathematics, 6(1):984–1025. https://doi.org/10.1137/15M1011731.

- Grbac and Runggaldier, (2015) Grbac, Z. and Runggaldier, W. (2015). Interest Rate Modeling: Post-Crisis Challenges and Approaches. Springer.

- Gretarsson et al., (2012) Gretarsson, H., Ribeiro, D., and Trovato, M. (2012). Quadratic gaussian inflation. Risk, 25(9):86.

- Heston, (1993) Heston, S. L. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options. The Review of Financial Studies, 6(2):327–343. https://doi.org/10.1093/rfs/6.2.327.

- Hinnerich, (2008) Hinnerich, M. (2008). Inflation-indexed swaps and swaptions. Journal of Banking & Finance, 32(11):2293–2306. https://doi.org/10.1016/j.jbankfin.2007.04.033.

- Hoyle et al., (2011) Hoyle, E., Hughston, L. P., and Macrina, A. (2011). Lévy random bridges and the modelling of financial information. Stochastic Processes and their Applications, 121(4):856–884. https://doi.org/10.1016/j.spa.2010.12.003.

- Hughston, (1998) Hughston, L. (1998). Inflation derivatives. Merrill Lynch and King’s College London Working Paper.

- Hull and White, (1990) Hull, J. and White, A. (1990). Pricing interest-rate-derivative securities. The Review of Financial Studies, 3(4):573–592. https://doi.org/10.1093/rfs/3.4.573.

- Hunt and Kennedy, (2004) Hunt, P. and Kennedy, J. (2004). Financial Derivatives in Theory and Practice. Wiley.

- Hurd and Zhou, (2010) Hurd, T. R. and Zhou, Z. (2010). A Fourier transform method for spread option pricing. SIAM Journal on Financial Mathematics, 1(1):142–157. https://doi.org/10.1137/090750421.

- Jacod and Shiryaev, (2003) Jacod, J. and Shiryaev, A. N. (2003). Limit Theorems for Stochastic Processes. Springer-Verlag Berlin Heidelberg.

- Jarrow and Yildirim, (2003) Jarrow, R. and Yildirim, Y. (2003). Pricing treasury inflation protected securities and related derivatives using an HJM model. Journal of Financial and Quantitative Analysis, 38(2):337–358. https://doi.org/10.2307/4126754.

- Keller-Ressel et al., (2013) Keller-Ressel, M., Papapantoleon, A., and Teichmann, J. (2013). The affine LIBOR models. Mathematical Finance, 23(4):627–658. https://doi.org/10.1111/j.1467-9965.2012.00531.x.

- Kenyon, (2008) Kenyon, C. (2008). Inflation is normal. Risk.

- Kim, (2014) Kim, D. H. (2014). Swaption pricing in affine and other models. Mathematical Finance, 24(4):790–820. https://doi.org/10.1111/mafi.12014.

- Korn and Kruse, (2004) Korn, R. and Kruse, S. (2004). Einfache verfahren zur bewertung von inflationsgekoppelten finanzprodukten. Blätter der DGVFM, 26(3):351–367. https://doi.org/10.1007/BF02808386.

- Kruse, (2011) Kruse, S. (2011). On the pricing of inflation-indexed caps. European Actuarial Journal, 1(2):379–393.

- Macrina, (2014) Macrina, A. (2014). Heat kernel models for asset pricing. International Journal of Theoretical and Applied Finance, 17(07):1450048. https://doi.org/10.1142/S0219024914500484.

- Macrina and Mahomed, (2018) Macrina, A. and Mahomed, O. (2018). Consistent valuation across curves using pricing kernels. Risks, 6(1):18.

- Mercurio, (2005) Mercurio, F. (2005). Pricing inflation-indexed derivatives. Quantitative Finance, 5(3):289–302. https://doi.org/10.1080/14697680500148851.

- Mercurio and Moreni, (2006) Mercurio, F. and Moreni, N. (2006). Inflation with a smile. Risk, 19(3):70–75.

- Mercurio and Moreni, (2009) Mercurio, F. and Moreni, N. (2009). A multi-factor SABR model for forward inflation rates. http://dx.doi.org/10.2139/ssrn.1337811.

- Nguyen and Seifried, (2015) Nguyen, T. A. and Seifried, F. T. (2015). The multi-curve potential model. International Journal of Theoretical and Applied Finance, 18(07):1550049.

- Ribeiro, (2013) Ribeiro, D. (2013). A local volatility model to price and calibrate year-on-year and zero-coupon inflation options. http://dx.doi.org/10.2139/ssrn.2290730.

- Rogers, (1997) Rogers, L. (1997). The potential approach to the term structure of interest rates and foreign exchange rates. Mathematical Finance, 7(2):157–176. https://doi.org/10.1111/1467-9965.00029.

- Rubinstein, (1991) Rubinstein, M. (1991). Pay now, choose later. Risk, 4(2):13.

- Ruijter and Oosterlee, (2012) Ruijter, M. J. and Oosterlee, C. W. (2012). Two-dimensional Fourier cosine series expansion method for pricing financial options. SIAM Journal on Scientific Computing, 34(5):B642–B671. https://doi.org/10.1137/120862053.

- Rutkowski, (1997) Rutkowski, M. (1997). A note on the Flesaker-Hughston model of the term structure of interest rates. Applied Mathematical Finance, 4(3):151–163. https://doi.org/10.1080/135048697334782.

- Sato, (1999) Sato, K.-i. (1999). Lévy Processes and Infinitely Divisible Distributions. Cambridge University Press.

- Singleton and Umantsev, (2002) Singleton, K. J. and Umantsev, L. (2002). Pricing coupon-bond options and swaptions in affine term structure models. Mathematical Finance, 12(4):427–446. https://doi.org/10.1111/j.1467-9965.2002.tb00132.x.

- Singor et al., (2013) Singor, S. N., Grzelak, L. A., Van Bragt, D. D., and Oosterlee, C. W. (2013). Pricing inflation products with stochastic volatility and stochastic interest rates. Insurance: Mathematics and Economics, 52(2):286–299. https://doi.org/10.1016/j.insmatheco.2013.01.003.

- Waldenberger, (2017) Waldenberger, S. (2017). The affine inflation market models. Applied Mathematical Finance, pages 1–21. https://doi.org/10.1080/1350486X.2017.1378582.