A McKean–Vlasov equation with positive feedback and blow-ups

Abstract

We study a McKean–Vlasov equation arising from a mean-field model of a particle system with positive feedback. As particles hit a barrier they cause the other particles to jump in the direction of the barrier and this feedback mechanism leads to the possibility that the system can exhibit contagious blow-ups. Using a fixed-point argument we construct a differentiable solution up to a first explosion time. Our main contribution is a proof of uniqueness in the class of càdlàg functions, which confirms the validity of related propagation-of-chaos results in the literature. We extend the allowed initial conditions to include densities with any power law decay at the boundary, and connect the exponent of decay with the growth exponent of the solution in small time in a precise way. This takes us asymptotically close to the control on initial conditions required for a global solution theory. A novel minimality result and trapping technique are introduced to prove uniqueness.

1 Introduction

This paper concerns a McKean–Vlasov problem, formulated probabilistically as

| (1.1) |

where is a constant, is a standard Brownian motion and is an independent random variable distributed on the positive half-line. We denote the law of by . A solution to this problem is a deterministic and initially zero càdlàg function that is increasing and for which (1.1) holds for any Brownian motion . Viewing (1.1) as an SDE in , notice that there is no distinction to be made between strong and weak notions of solution: knowing fixes the law of and, together with any Brownian motion, fixes a pathwise construction of . When , the equations have a positive feedback effect and this is the case we consider here — the situation for is classical and existence and uniqueness of smooth solutions is known [2, 3, 4].

Our motivation for studying (1.1) comes from mathematical finance, where it can be used as a simple model for contagion in large financial networks or large portfolios of defaultable entities. To illustrate how (1.1) may emerge in this context, consider a large system of banks. Following the structural approach to credit risk, we say that the ’th bank defaults when its asset value, , hits a default barrier, . This gives rise to the notion of distance-to-default, for which a simple model could be of the form

where are i.i.d. copies of and are independent Brownian motions. Next, we can introduce an element of contagion with a model in which the default of one bank causes the other banks to lose a proportion of their assets. For large , we have , so the new asset values, , are then defined by

where for . After taking logarithms, it follows that the new distances-to-default, , satisfy

| (1.2) |

for . If we let , then the same arguments as in [6] show that we can recover solutions to (1.1) — with the corresponding drift and volatility — as topological limit points of the particle system (1.2), and these solutions are global: they exist for all . As regards the form of (1.2), we will concentrate the analysis in this paper on the simplest case (1.1) and then we devote the final Section 6 to a discussion of more general coefficients.

The first version of the problem (1.1) appeared in the mathematical neuroscience literature as a mean-field limit of a large network of electrically coupled neurons [2, 3, 5, 6]. In this setting, each neuron is identified with an electrical potential (given by an SDE) and when it reaches a threshold voltage, the neuron fires an electrical signal to the other neurons, which then become excited to higher voltage levels. After reaching the threshold, the neuron is instantaneously reset to a predetermined value and it then continues to evolve according to this rule indefinitely. Therefore, the model is different to our setting as we do not reset the mean-field particle in (1.1), however, the essential mathematical difficulties from the positive feedback remain common to both models. With regard to the financial framework introduced above, we note that a similar model for default contagion (with constant drift and volatility) was recently proposed in [14].

Mathematically, the McKean–Vlasov problem (1.1) can be recast in a number of ways. We denote the law of killed at the origin by and set , for suitable test functions . Then a simple application of Itô’s formula gives the nonlinear PDE

| (1.3) |

for with and . Writing for the density of (which exists by Proposition 2.1), we can formally integrate by parts in (1.3) to find the Dirichlet problem

| (1.4) |

In other words, the law of solves the heat equation with a drift term proportional to the flux across the Dirichlet boundary at zero — the latter being a highly singular nonlocal nonlinearity. Setting in (1.4), the equations for and can be viewed as a Stefan problem with supercooling on the semi-infinite strip . From this point of view, it is known that may explode in finite time as has been analysed (on a finite strip) in the series of papers [8, 9, 10, 13].

A third characterisation of (1.1) is as the solution to the integral equation

| (1.5) |

where is the c.d.f. of the Normal distribution. This is a Volterra integral equation of the first kind, and a derivation can be obtained by following [15]. The formulation that is most helpful here is to view the problem as a fixed point of the map defined by

| (1.6) |

that is, a solution to . We will use this map in stating and proving our main theorems. The key is to find a suitable space on which stabilises and to show that it is contractive (Theorems 1.6 & 1.7). Note that [5, 14] also take this approach to the problem, but our techniques differ in that they are entirely probabilistic and do not rely on PDE estimates.

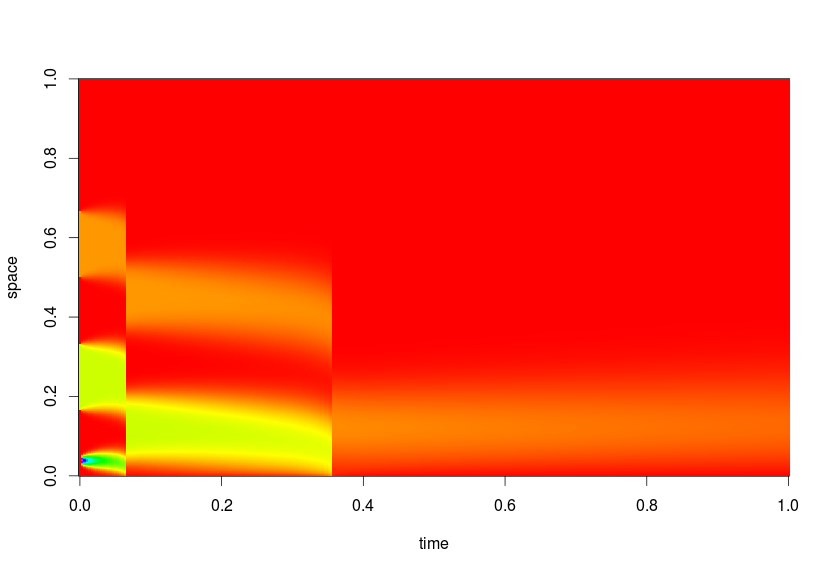

A very interesting feature of the problem (1.1) is that it exhibits a phase transition in the continuity of solutions as the feedback strength, , increases. The methods of [5], for the neuroscience version of the problem, show that for sufficiently small (and with ) there is a unique solution to (1.1) in the class of continuously differentiable functions. On the other hand, the extremely simple proof below (modified from [2]) shows that (1.1) cannot have a continuous solution for values of that are sufficiently large. When this is the case, the positive feedback becomes too great and at some point in time the loss process, , undergoes a jump discontinuity, which we call a blow-up. In other words, in an infinitesimal period of time, a macroscopic proportion of the mass in the PDE (1.3) is lost at the boundary — i.e. the system blows up (see Figure 1.1). It is intriguing that this result can be proved so simply and with no technical estimates, although of course the threshold obtained below is not sharp and the proof does not reveal anything about the nature of the blow-ups.

Theorem 1.1 (Blow-up for large ).

Let . If , then any solution to (1.1) cannot be continuous for all times.

Proof.

For a contradiction, suppose solves (1.1) and is continuous. Stopping at , we then get

Taking expectations and rearranging,

where we note that a.s. and , since Brownian motion hits every level with probability 1. As is continuous and increasing, the integral can be computed exactly, so we get

which is the required contradiction. ∎

From Theorem 1.1 it is clear that, in general, we cannot restrict our search to solutions of (1.1) that are continuous and so we must allow càdlàg solutions. If a solution has a jump of size at time , then the instantaneous loss must equal the mass of absorbed at the boundary after a translation by , that is:

| (1.7) |

see Figure 1.2. Unfortunately, this equation alone is not sufficient to determine the jump sizes of a discontinuous solution. In particular, is always a solution, but in general this is an invalid jump size by Theorem 1.1. To continue the solution after a blow-up, we must decide how to choose the jump size from the solution set of (1.7). In [6] the authors introduce the term physical solution for a solution, , that satisfies

| (1.8) |

for all . The next result justifies that this is a natural condition, as it is the smallest possible choice of jump size that admits càdlàg solutions (see Section 2 for a proof and further discussion).

Proposition 1.2 (Physical solutions have minimal jumps).

Suppose is any càdlàg process satisfying (1.1). Then

for every . In particular, if the right-hand side is non-zero for some , then has a blow-up at time .

It is helpful to consider the density function, , of in light of Proposition 1.2. If, at some time , is greater than or equal to the critical value of on a non-zero interval about the origin, then a blow-up in is forced to occur at that time.

In [6] it is shown that there exist (global) physical solutions to the neuroscience version of equation (1.1), for any , albeit with an initial measure that vanishes in a neighbourhood of zero. Those solutions arise as topological limit points of a corresponding finite particle system analogous to (1.2). Consequently, the authors are unable to establish regularity results on the solutions. The main advantage of a fixed point argument is that solutions are guaranteed to have known regularity, at least on a small time interval.

Our motivation in this paper is to make progress towards the following conjecture:

Conjecture 1.3 (Global uniqueness).

Currently, we are far from proving Conjecture 1.3, and the major obstruction concerns the initial conditions. To see why, notice that after a jump has taken place, we must, in general, restart the system from an initial law that has a density which does not vanish at the origin (see Figure 1.2, as well as Proposition 2.1 concerning the existence of a density for at all times). In fact, without further analysis, all we can say about the measure after a blow-up at time is that

Therefore, to attack Conjecture 1.3 it is necessary to make progress towards the following simpler goal:

Conjecture 1.4 (Uniqueness for non-vanishing initial laws).

Suppose has a density and satisfies . Then the solution, L, to (1.1) is unique and up to a small time, and it satisfies as .

Initial conditions that do not vanish at the origin are currently outside the scope of known results, and the results that do exist only tackle the uniqueness in a too restrictive class of candidate solutions. In the literature, the closest to Conjecture 1.4 is [14, Thm. 2.6] which is established for a slight variant of our problem: Given an initial density with , it gives existence and uniqueness up to the first time the -norm of explodes in the class of candidate solutions for which for some . Here denotes the usual Sobolev space with one weak derivative in . We note that these conditions on imply that it decays like near the origin, so it is far from what is needed in order to proceed to a global uniqueness theory. The aforementioned was preceded by [5, Thm. 4.1], which gives existence and uniqueness on a small time interval in the class of solutions, starting from an initial density that decays like as . The connection between the boundary decay of the initial condition and the short-time regularity of solutions will feature prominently in our results below.

Moreover, the existing results in the literature leave open the question of whether there is (short-time) uniqueness in the wider class of càdlàg solutions. This is more than just a technical curiosity: Indeed, the physical and financial motivations for (1.1) derive from the corresponding particle system, as presented in (1.2), but the requisite regularity of its limit points is not known and could be difficult to verify a priori — all we know is that they are càdlàg. Thus, it obstructs the full convergence in law of the finite system (i.e. the propagation of chaos).

1.1 Main results

Our contribution here is to construct an solution to (1.1) up to the first time its norm explodes, and to show that it is the unique solution on this time interval amongst all possible càdlàg solutions (Theorem 1.8). We allow initial densities with any power law decay at the origin, that is, decay of order as for some . To be precise, we consider initial conditions, , that have a bounded initial density, , for which we can find constants such that

| (1.9) |

A key observation is that it is only the values of , and that determine the behaviour of solutions in short time (Theorem 1.7). The reason for assuming an initial density is that this state is reached after any non-zero period of time anyway (Proposition 2.1). Below, we state our main results chronologically to make it clear how they are connected.

First we introduce the following subsets of :

Definition 1.5.

For , and , let denote the subset of given by

Our first argument is to show that, on these sets, is an -contraction. The proof follows by comparing the first hitting times of a single Brownian motion driven by two different drift functions (Proposition 3.1), which is a coupling of the processes in (1.6) to the same Brownian motion . As a by-product of this method we can deduce that differentiable solutions are minimal in the class of potential càdlàg solutions, which is an important ingredient in the main uniqueness result (Theorem 1.8). The power of the technique lies in the ability to estimate the positive part of the difference , for two solutions and , assuming only the regularity properties of and not .

Theorem 1.6 (Contraction and minimality).

For any and , there exists such that for all

Moreover, if there exists a solution to (1.1) for some , and and another solution that is càdlàg, then for all .

To construct a fixed point solution, we find choices of the parameters , and such that the map stabilises on the set . An interesting product of our technique is that we are able to recover the exact regularity of the solutions at time zero from the decay of the initial condition near the Dirichlet boundary. Thus, the main factor in the short-time growth of solutions is the behaviour of the heat equation with absorbing boundary conditions and not the feedback effect in the model. This should be an indication that something new is required to tackle Conjecture 1.3. Crucially, we rely on Girsanov’s Theorem to control , for which we require . Notice, however, that if as in the hypothesis of Conjecture 1.3, then we must have (by comparison with the case ), and so we can no longer expect this approach to be viable.

Theorem 1.7 (Stability and fixed point).

There exists a constant depending only on , and such that for all there exists for which

Hence has a fixed point, , in and this solution is unique in the class of candidate solutions in .

This short-time fixed point construction can be extended by observing that if is in the space , then, by appealing to Girsanov’s Theorem, we can show that the density must have decay of order near the Dirichlet boundary. In other words, we can recover the regularity of the initial condition at time , and so exactly the same argument can be applied to the system restarted from time . Consequently, we can extend the solution constructed in Theorem 1.7 onto another small non-zero time interval and iterate this procedure, so long as the solution we obtain is in . The catch that prevents this procedure from giving a differentiable solution for all times (recall that this would contradict Theorem 1.1) is that we lose control of the constants in the relevant subsets. Hence the construction only applies up to the first time the -norm of the solution explodes. Trivially, this occurs no later than the first jump, however, the mathematical challenge in attempting to restart the problem after an explosion time seems no less difficult than Conjecture 1.4.

Theorem 1.8 (Uniqueness up to explosion).

The analogous result for the McKean–Vlasov problem corresponding to (1.2) is presented in Section 6. The first step towards uniqueness is given by Theorem 1.6: The differentiable solution constructed in the first part of Theorem 1.8 is minimal, so it must be a lower bound of any generic candidate càdlàg solution, at least in small time. To obtain an upper bound, we introduce a family of processes in which we kill a small proportion, , of the initial condition at time zero. In Section 5 we show that these modified solutions cannot overlap and so they bound the generic solutions from above. By returning to the contraction argument in Theorem 1.6, we show that these modified solutions converge to the differentiable solution as the amount of deleted mass, , tends to zero. Thus, the envelope of solutions shrinks to zero size and this forces uniqueness of solutions. The power of this method is that it circumvents the need to have quantitative information about the generic candidate càdlàg solutions.

Remark 1.9 (Propagation of chaos).

Theorem 1.8 resolves ambiguity about the validity of the propagation of chaos. By following the methods in [6], it can be shown that the particle system in (1.2) has limit points that converge in law (with respect to a suitable topology) to a càdlàg solution of (1.1). Now that we have uniqueness amongst general càdlàg solutions, we can conclude that this is in fact full convergence, up to the first explosion time, and not just subsequential convergence.

Overview of the paper

In Section 2 we motivate and explain the physical condition (1.8) and prove that it is necessary in order to have a càdlàg solution. In Section 3 we prove Theorem 1.6 via a comparison argument. In Section 4 we prove Theorem 1.7 by finding a space on which the map stabilises. In Section 5 we prove Theorem 1.8 by extending the fixed point argument up to the explosion time and introducing the -deleted solutions used to bound candidate solutions. In Section 6 we show how our arguments can be extended to incorporate more general drift and diffusion coefficients.

2 Minimal jumps and -fragility — proof of Proposition 1.2

Our aims in this section are twofold: Firstly, we prove that the physical jump condition in (1.8) yields the solution with the smallest possible jump size (at any given instance) and, secondly, we provide some intuition for this behaviour.

We begin by observing that regardless of the initial condition, at any time , the measure will have a density.

Proposition 2.1 (Existence of a density process).

Let be the law of a solution, , to (1.1). For all , is absolutely continuous with respect to the Lebesgue measure and therefore has a density function, . Moreover, if has a density , then .

Proof.

By omitting the killing at zero, we have the upper bound

where is the Brownian transition kernel. Hence , so the first claim follows from the Radon–Nikodym Theorem. If has a density in , then we get

since . This proves the second claim. ∎

As remarked in Section 1, equation (1.7) alone is insufficient to determine the jump size at a given time. Not only is zero always a solution of that equation, but there may indeed be many other solutions that differ from the physical solution given by (1.8).

Example 2.2.

An alternative way to view (1.8), which better motivates Proposition 1.2, is the notion of fragility. To state a proper definition, consider first the sequence

| (2.1) |

for a given measure and constants and . Notice that is increasing in and in . Hence we can deduce that the limit exists and is an increasing function of . Therefore, we can sensibly define:

Definition 2.3 (-fragility).

The measure, , is said to be -fragile if

To see why -fragility is related to physical solutions, consider starting the heat equation from an initial law . In small time, we will immediately lose mass at the boundary, say an amount. To approximate the contagious system in (1.1), we must then shift the measure down towards the origin by an amount . If we apply this to , we obtain a loss of , which we can then further shift our initial condition by, and so on, hence obtaining in the limit. If this terminal quantity does not shrink to zero with , we should not expect the solution to (1.1) to be right-continuous at : An infinitesimal loss of mass starts a cascade of losses summing to a non-zero amount. Indeed, this is a heuristic version of the argument presented in the proof of Proposition 1.2 below. For now, we notice that there is, in fact, an exact correspondence between and the physical jump condition.

Proposition 2.4.

For any atomless measure on the positive half-line and we have

Proof.

Write and .

Suppose . Then we can find such that . By taking the limit as in (2) we get

where the inequality is due to the definition of , but this is clearly a contradiction.

Suppose . By definition of , we can find a sequence as such that

Fix any such and take , then we have

Since we may now repeat the argument to get

and so on. Proceeding inductively, we conclude that , so taking gives , which is a contradiction. ∎

Example 2.5.

Returning to the density from Example 2.2, set for . Then for all , so we get

Thereafter, , so and, since , it follows that remains equal to for all . Consequently, we have for all , and hence , which indeed agrees with the physical jump condition.

Remark 2.6 (Restarting solutions at a non-zero time).

To prove Proposition 1.2 it will be sufficient to take in the statement of the result, since we can always restart the system at a time , taking as our new time origin. This might be confusing at first glance as we specified in our definition of a solution to (1.1). To be clear, if we want to solve (1.1) from a time onwards, and we have a solution up to time , then we can solve the problem

for , where is the density for the problem at time . Indeed, this is exactly the same formulation as (1.1), except the initial condition is a sub-probability density. We then have that

is an extension of for , which solves (1.1). Therefore, restarting the system at a non-zero time is just a matter of normalising the initial condition.

Proof of Proposition 1.2.

For a contradiction, suppose that is a càdlàg process satisfying (1.1) for which the inequality in Proposition 1.2 is violated. As noted in Remark 2.6, it suffices to assume that this occurs at , and this implies that and as . By definition of we have

Thus, if is a decreasing differentiable function, then

Using this lower bound, it holds for any that

Here is the Normal c.d.f. and we shall also need the Normal p.d.f., . Observe that the function

satisfies

| (2.2) |

Now let . Since we are assuming , we have for all sufficiently small, and hence

Using and , we can rearrange this inequality to find that

In other words, for all sufficiently small, we have

but this is our required contradiction: By (2.2) is strictly decreasing and if then we can certainly find sufficiently small so that . ∎

3 Contractivity of and minimality of differentiable solutions — proof of Theorem 1.6

The main objective in this section is to prove Theorem 1.6, which states that differentiable solutions are minimal and that is contractive on . The key technique is the following comparison result, which is obtained by coupling two outputs, and , of the map (1.6) to the same driving Brownian motion.

Proposition 3.1 (Comparison).

Let and be two increasing and initially zero càdlàg functions and be defined as in (1.6) for model parameters and . Suppose that is continuous on . Then

where and is the Normal c.d.f.

Proof.

It is no loss of generality to take a Brownian motion, , and initial value, , such that (1.6) holds with this and this for both and , that is

where we denote the respective hitting times of zero by and .

By conditioning on the value of we have

| (3.1) | ||||

where in the final line we have discarded the contribution on . Since is increasing and we can further bound (3.1) by

On the event we have , so

and thus we have

Since the right-hand side is positive, we can replace the left-hand side by its maximum with zero, so the proof is complete. ∎

When is differentiable with power law control on its derivative near zero, then we are able to use this derivative to get a more direct bound.

Corollary 3.2.

Suppose that for some , and (recall Definition 1.5). Then there exists , independent of and , such that

where is any càdlàg function that is increasing and initially zero.

Proof.

We begin by noticing that is bounded above on by the linear function

Therefore, by Proposition 3.1,

The result follows since , by definition of . ∎

It is now a straightforward task to prove Theorem 1.6.

Proof of Theorem 1.6.

With and fixed as in the statement of the result, take , where we will show how to take sufficiently small (and independent of and ) so that we have the result. With as in Corollary 3.2 and the symmetry in , we have

for , where is a constant independent of , and . Consequently, it suffices to take such that .

For the second half of the result, take now fixed as in the statement. By the same estimate as above applied to Corollary 3.2, we have

where is any time with . Therefore, taking such that forces

that is for .

By returning to Corollary 3.2, and repeating the same estimate again, we can deduce that

for any . Thus, by taking sufficiently close to , we can again force

Continuing to repeat this argument, we obtain a sequence of times . If , then the argument also applies at time and so can be restarted. Furthermore, if this procedure ever terminates at a time strictly less than , then the argument can be restarted (by left continuity) for a non-zero time, thus contradicting the termination. Hence we conclude that we have uniqueness up to the time . ∎

4 Stability of and the fixed-point argument — proof of Theorem 1.7

Here we show that we can choose parameters such that maps into itself. From this and Theorem 1.6, we are then able to conclude the existence of a solution in short time by the Banach fixed point theorem. We will also carefully track the contribution to the regularity of the solution near time zero due to the decay of the initial density near the Dirichlet boundary. To this end, we will see that the exponent in Theorem 1.7 comes directly from Lemma 4.2 below.

Lemma 4.1.

With and above

where

Proof.

Fix and take to be the solution to the backward heat equation on the positive half-line with Dirichlet boundary condition:

That is, let

By applying Itô’s formula to we obtain

Since , integrating in time and taking expectation gives

where the endpoints take the values

It remains to notice that

∎

Our strategy is to apply the method of difference quotients [7, Sect. 5.8.2, Thm. 3] using Lemma 4.1. With fixed, the starting point is to write

| (4.1) |

In order to estimate these three integrals we must make use of the assumption (1.9) on the behaviour of near the origin. Recall that we have constants such that

Lemma 4.2 ().

There exists and such that

for all and .

Remark 4.3 (Constants).

In the proof below we will allow the constants to increase as necessary, but we will pay close attention to ensure that does not depend on (whereas does).

Proof of Lemma 4.2.

By the fundamental theorem of calculus, and properties of , we have

Splitting the -integral and using the bound on gives

Note that the final term is a bounded function of and , so by taking sufficiently small we can conclude the result. ∎

In order to control from equation (4) we need to make some assumptions on the regularity of . Provided is in , we have that is absolutely continuous with respect to Brownian motion, and so we can proceed as below with a change of measure.

Lemma 4.4 (A Girsanov argument).

Let be measurable and bounded and assume that for some . Then for all and

where is a standard Brownian motion started from and .

Proof.

Let denote the Radon–Nikodym derivative

for . Under , is a standard Brownian motion by Girsanov’s Theorem. Therefore, applying Hölder’s inequality gives

where . Finally, it is a simple calculation to see that

and this completes the proof. ∎

Corollary 4.5.

Suppose satisfies the conditions of Lemma 4.4 and fix . Then there is a constant depending only on and such that, for all and ,

Proof.

We first prove the bound for Brownian motion, and then we appeal to the previous lemma for the full result. From the assumption (1.9) we can certainly find a constant such that for all , and so

where from here on we absorb the relevant numerical constants into . Using the estimate

together with the substitution gives

| (4.2) |

Now notice that for generic we have the inequality

Hence it holds for , and that

Combining this inequality with , for a constant depending only on , allows us to bound the inner integral in (4.2) by

Setting this into (4.2) and making the change of variables we obtain

Finally, the result for in place of follows by invoking Lemma 4.4. ∎

Lemma 4.6 ().

If , then there exist constants , and (depending on ) such that

Remark 4.7.

Formally, the integrand in converges to a Dirac mass at zero, evaluated at and multiplied by . We expect such an expression to vanish since implies . While this argument is not rigorous, it suggests why and hence why this term will not contribute to the bound on in the proof of Theorem 1.7.

Proof of Lemma 4.6.

We begin by applying the bound to get

Taking and in Corollary 4.5, and bounding with the worst-case exponents, gives

where and are constants depending on . The result is now complete by choosing and so that (possible since ) and (take sufficiently close to 1 and maintain constant ratio ). ∎

The third term, , is not so simple to control.

Lemma 4.8 ().

If and then there exist constants , and (depending only on and ) such that

Proof.

We begin by applying the fundamental theorem of calculus to see that

and therefore

Taking an expectation and using Corollary 4.5 gives

| (4.3) |

where depends only on and the choice of and .

By applying the bound (4.3) to the expression for , we get

where is defined to be

| (4.4) |

for a constant , provided and . To keep the above exponents bigger than , we need to select and so that , whereby we obtain

where we have absorbed numerical constants into . Since , we can take sufficiently close to 1 so that we have the required exponent. The proof is then complete by noting that

∎

Proposition 4.9 (Stability of ).

There exists a constant depending only on and such that for every there exists for which

where also depends on the model parameters.

Proof.

Take and as in the conclusion of Lemma 4.2. We will decrease the value of throughout the proof, but this is the in the statement of the result.

With Proposition 4.9 now in place, it remains to show that we can find a fixed point and deduce that it lives in one of the sets .

Proof of Theorem 1.7.

Take , and as in the conclusion of Proposition 4.9. Take sufficiently small so that the first half of Theorem 1.6 holds. Define the sequence

By the Banach fixed point theorem, we know that there exists a limit point in , as , and that . So solves (1.1) on .

To see , notice that, since is bounded by 1, dominated convergence gives

| (4.6) |

Proposition 4.9 ensures , so we have the estimate

Using this in (4.6) yields

and hence the method of difference quotients [7, Sect. 5.8.2, Thm. 3] gives that is in . Moreover, it holds pointwise almost everywhere in that

so sending gives that , as required.

The uniqueness statement follows immediately by applying the second half of Theorem 1.6. ∎

5 Bootstrapping and full uniqueness up to explosion time — proof of Theorem 1.8

Here we show how the solutions from the fixed point argument in the previous section can be extended up to the first time their norm explodes. (Trivially, this time occurs before or at the first jump time.) The key to this bootstrapping method is to notice that if , for some , then necessarily (Lemma 5.1). Not only does this show that cannot be a jump time, it also allows us to apply the fixed point argument once more, thus extending the solution to for some (Corollary 5.2). The first half of Theorem 1.8 then follows by iterating this argument (Corollary 5.3).

After the above, we proceed to prove the second half of Theorem 1.8. The idea is to consider modified initial conditions for which a fixed portion of the initial density is erased and added to the initial value of the loss process (Definition 5.4). An argument that shows solutions cannot overlap (Lemma 5.6) then allows us to trap any general càdlàg solution of (1.1) between the modified solutions and the minimal differentiable solution. The proof concludes by showing that the size of this trapping envelope shrinks to zero as the size of the initial modification is taken to zero (Lemma 5.7), thus forcing the minimal solution and the general càdlàg solution to be equal (see Figure 5.2).

5.1 Bootstrap

Lemma 5.1 (Recovery of initial exponents).

Proof.

Note that there exists a limit , since must be increasing. Therefore, there exists a left limit density (recall Proposition 2.1).

Fix . Our strategy is to apply Hunt’s switching identity [1, Thm. II.1.5]. Define the dual process

for . Then we have

for all non-negative measurable functions and . (Note that, since and by the hypotheses, we have continuity of ). By taking and an arbitrary non-negative measurable function, we can conclude that

| (5.1) |

for almost every .

Since , is just a Brownian motion with a drift. Therefore we can apply Lemma 4.4 with in place of and to get

for any , where is a Brownian motion and depends on , and and is independent of . (We have absorbed the exponential factor into .) By the assumption that , and increasing as needed, we deduce that

Provided we take such that , we can apply Jensen’s inequality to get

Putting this into (5.1) gives the required bound near zero at time . Proposition 2.1 gives , so we have the required boundedness away from the origin too. Since the constants obtained above are independent of , we can find , and such that

for all and . By sending , we have the result. ∎

The implication of Lemma 5.1 is that at the end of the fixed-point argument from Section 4 we can restart the argument with new initial conditions that have the same power law decay. As a result we can push our construction of solutions by a further non-zero amount of time. Notice, however, that we lose control of the exact constant that we had in Theorem 1.7 and hence the proceeding results are qualitative, not quantitative.

Corollary 5.2 (Extending solutions).

Proof.

Since we have , Lemma 5.1 implies that satisfies the condition (1.9), for some constants , and (that are possibly different to those for ). Therefore, by Theorem 1.7 there exists and such that we can find solving

| (5.2) |

for (recall Remark 2.6). It follows that, if we define and

then extends and solves (1.1) for all with the required derivative control. ∎

Corollary 5.3 (Bootstrap to explosion time).

Proof.

By repeating Corollary 5.2, we can find an infinite sequence of times over which we can successively extend . If is such that , then we are done. Otherwise, by the left continuity of , we can restart the argument from by applying Corollary 5.2. This procedure cannot terminate at a time for which , or else it can be restarted, hence we conclude the result. ∎

5.2 Monotonicity and trapping

Our main technical construction will be a solution to (1.1) for which we delete a portion of the initial condition near the boundary and add that mass to the loss at time zero, before finally shifting the density towards zero accordingly.

Definition 5.4 (-deleted solutions).

Suppose has a density and let . Define the McKean–Vlasov problem

| (5.3) |

where solutions, , are taken to be càdlàg.

It is not immediately clear that we can solve the above problem for , however, careful inspection of the initial loss reveals that we can.

Lemma 5.5 (-deleted solutions exist).

Proof.

We begin by noting that, for , we have

Hence we can certainly take sufficiently small so that

This guarantees that , and so we can rewrite (5.3) as

| (5.4) |

see Figure 5.1. As noted in Remark 2.6, we can solve to find , since vanishes on , so we certainly have the control in (1.9) for some choice of constants. Furthermore, we have

so we can find constants such that (1.9) holds for uniformly in . Since the arguments in Section 4 for proving Theorem 1.7 depend only on the constants in (1.9), we can conclude that the parameters of obtained in Theorem 1.7 are constant across the class of initial densities , for . Hence we have the result. ∎

The solutions in Lemma 5.5 are useful because we have the following two comparison results, which say that the -deleted solutions dominate and converge to the traditional solutions of (1.1) — see Figure 5.2.

Lemma 5.6 (Monotonicity).

Proof.

By construction, the result is true at time . For a contradiction, let be the first time at which . Couple both solutions to the same Brownian motion:

for , so that taking the difference gives

Therefore, from the definition of , we get

| (5.5) |

Now fix any such that . Then we have

| (5.6) |

By Girsanov’s Theorem, is absolutely continuous with respect to Brownian motion, and the infimum of Brownian motion has a density, therefore the probability on the right-hand side of (5.6) is non-zero. Hence , which is the required contradiction. ∎

Lemma 5.7 (Convergence).

Suppose there exist constants , , and such that for all . Then there exists such that

Proof.

We know from Lemma 5.6 that on . By following the argument in Section 3 for the proof of Theorem 1.6, and coupling and to the same Brownian motion, we have

where is a constant independent of , increasing from line to line as necessary. Therefore, taking a supremum over and taking sufficiently small, we have

which completes the proof. ∎

We are now in a position to complete the proof of the main uniqueness theorem. As already indicated, the idea is to trap a general candidate solution from below by the differentiable solution from Corollary 5.3 and from above by the -deleted solutions, and then to shrink the resulting envelope to zero using the uniform control in Lemma 5.7

Proof of Theorem 1.8.

Take the bootstrapped solution, , from Corollary 5.3. We will be done if we can show that there is not a solution to (1.1) on that is distinct from , for any . So for a contradiction, suppose that is such a solution and let be the first discontinuity of .

By Lemma 5.5 we can find , and a family satisfying the hypotheses of Lemma 5.7. By decreasing so that , Lemma 5.6 and Theorem 1.6 guarantee

By taking from the conclusion of Lemma 5.7 and sending , we conclude that on .

This argument can now be restarted from time and iterated as in the proof of Corollary 5.3, hence we conclude that up to the minimum of and . If , then we are done, so suppose . By left-continuity, we have that , and, since does not have a jump at time , the physical jump condition (1.7) gives

This contradicts being a jump time of and so it completes the proof. ∎

6 Extensions to more general coefficients

In this section we consider some simple extensions of (1.1) that incorporate more general drift and diffusion coefficients. The aim is to outline how the analysis can be reduced to that of the previous sections and thus we will only provide sketches of the proofs.

To be specific, we consider the McKean–Vlasov problem

| (6.1) |

where is a Brownian motion and the independent initial condition, , is given by , which is assumed to satisfy (1.9) and taken to be sub-Gaussian. In terms of the coefficients, we assume that is Lipschitz in space with and we impose the non-degeneracy condition for all . Furthermore, we impose an upper bound for positive (this is only used in Section 6.3 and it could be omitted if we could ensure in Section 6.1).

The above setup includes the financial model (1.2). Moreover, it e.g. allows for a Brownian motion with an Ornstein–Uhlenbeck type drift modelling the attraction to a ‘resting state’ — as in the original neuroscience model [5]. This could also be of interest in the financial framework, for example to include a target leverage ratio or to model some notion of ‘flocking to default’ as in [11].

Theorem 6.1 (Existence and uniqueness up to explosion).

Let the above assumptions be in place. Then there exists a solution to (6.1) up to time

such that, for some , it holds for every that for some . Furthermore, this solution is unique in the class of candidate solutions with in .

As for (1.1), the notions of weak and strong uniqueness for (6.1), regarded as an SDE in , are equivalent: taking the difference of two solutions with the same and cancels all terms apart from the drift, whereby strong uniqueness is immediate from the Lipschitz property of . In essence, the main point in the proof of Theorem 6.1 is to have good control on the boundary decay of the relevant transition densities akin to the classical Dirichlet heat kernel estimates.

When there is no spatial dependence in the drift — as in (1.2) — we can do better with essentially no extra work. Specifically, we can directly replicate the monotonicity and trapping arguments from Section 5.2, which gives uniqueness amongst generic càdlàg solutions.

Theorem 6.2 (Generic uniqueness).

The remainder of this section concerns the proofs of Theorems 6.1 and 6.2, however, we will only show how to reduce the analysis to that of Sections 3, 4 and 5. The proof of Theorem 6.1 is split into three succinct parts: first we discuss the stability of the fixed point map (Section 6.1), then we revisit the bootstrapping of short-time existence (Section 6.2), and finally we extend the contractivity arguments (Section 6.3). Last, the proof of Theorem 6.2 is outlined in Section 6.4.

6.1 Stability of the fixed point map

Let denote the fixed point map for (6.1) defined by analogy with (1.6). Then we need to ensure that Proposition 4.9, concerning the stability of , also holds true in this more general setting.

To this end, the starting point is still the expression for from Lemma 4.1, which remains valid with given by (6.1). Next, we can observe that the Girsanov argument from Lemma 4.4 will now take the form

with

where is a standard Brownian motion and is an independent random variable distributed according to . Indeed, we can simply consider the Radon–Nikodym derivative

and otherwise repeat the arguments from the proof of Lemma 4.4. From here, we can apply [12, Thm. 2.7] to see that the absorbed process has a transition density which satisfies the Dirichlet heat kernel type estimate

| (6.2) |

for some constants and only depending on , where the latter can be taken sufficiently small such that .

Remark 6.3.

The estimate (6.2) is derived in [12, Sec. 6] by first showing that

where is the Green’s function for as a terminal-boundary value problem on with . This follows from ideas closely related to those in Lemma 4.1 and the estimate then comes from a careful change of measure in the second term to remove the drift of .

With a view towards Section 6.2, fix any and set , where is the decay exponent of the initial condition. Then the power law decay of near the boundary, cf. (6.2), implies that we can replicate the arguments from Section 4 with in place of the Dirichlet heat kernel, . In this way Proposition 4.9 remains true only with in place of .

6.2 Density bounds for bootstrapping

Let denote the law of killed at the origin. In order to allow bootstrapping of our short-time results, we need to establish analogoues of Lemma 5.1 and Corollary 5.2.

First, referring to (6.2) as above, we can argue by analogy with Proposition 2.1 to see that has a density, . Moreover, these same arguments show that is bounded with .

Now suppose , for some , and fix . As in Section 5, we can then define, for all , the dual process

where and is a Brownian motion. As in the proof of Lemma 5.1, it follows from Hunt’s switching identity that

Thus, by the same Girsanov argument as in the extension of Lemma 4.4 above, it holds for any that

| (6.3) |

where

and is the first hitting time of zero by . As for , the absorbed process has a transition density , so we get

| (6.4) |

Appealing again to [12], we see that satisfies precisely the same bound as (6.2). Now observe that for and recall that . Using this and the order boundary decay of the second term in (6.2), as applied to , it follows easily from (6.3) and (6.4) that

for any such that . Taking close enough to so that (with fixed in Section 6.1) we can conclude that satisfies condition (1.9) for every with as the decay exponent. Given this, we immediately obtain the desired analogues of Lemma 5.1 and Corollary 5.2.

6.3 Contractivity of the fixed point map

In this subsection we finally show that remains an contraction, by extending the first part of Theorem 1.6, and then we complete the proof of Theorem 6.1.

With as in the statement of Theorem 1.6, consider for the corresponding processes and given by

coupled through the same Brownian motion and initial condition. Let and denote the respective hitting times of zero.

Since is increasing, and recalling also the upper bound on for , it holds for all that

| (6.5) |

Moreover, by the Lipschitzness of the drift we have

so Grönwall’s lemma yields

Therefore, on the event it holds for all that

| (6.6) |

Using (6.5) and (6.6), and arguing as in (3.1), we deduce that

for , where a simple time-change shows that is given explicitly by

with . Noting that and using the bound , it is straightforward to verify that

Thus, it holds for all that

From here we can repeat the proof of Theorem 1.6 to get contractivity of and by Section 6.1 we have stability. Thus, the short-time version of Theorem 6.1 holds by the same arguments as in the proof of Theorem 1.7. Finally, Section 6.2 allows us to bootstrap this result up to the explosion time and so the full Theorem 6.1 follows.

6.4 Minimality, monotonicity and trapping

In this final subsection we consider the special case and sketch the remaining steps towards the proof of Theorem 6.2.

Proceeding as in Section 6.3, the Grönwall argument is now no longer needed and instead we immediately get on . Therefore, the ensuing arguments yield

and hence the exact same reasoning as in the second part of Theorem 1.6 ensures that any differentiable solution is minimal.

In terms of the monotonicity and trapping procedure, the only change in Lemma 5.6 is that equation (5.6) now reads as

| (6.7) |

Consequently, the proof of Lemma 5.6 goes through by absolute continuity with respect to the time-changed Brownian motion . Furthermore, the proof of Lemma 5.7 follows immediately by applying the same reasoning as in Section 6.3. Given this, the proof of Theorem 6.2 can be finished in precisely the same way as the second part of Theorem 1.8.

Acknowledgements.

The research of A. Søjmark was partially supported by the EPSRC award EP/L015811/1. We are grateful for the careful reading and suggested improvements from an anonymous referee.

References

- [1] J. Bertoin. Lévy processes. Cambridge University Press, Cambridge, 1996

- [2] M.J. Cáceres, J.A. Carrillo and B. Perthame. Analysis of non-linear noisy integrate & fire neuron models: blow-up and steady states. J. Math. Neurosci., 1(7), 2011.

- [3] J.A. Carrillo, M.D.M. González, M.P. Gualdani and M.E. Schonbek. Classical solutions for a nonlinear Fokker–Planck equation arising in computational neuroscience. Comm. Partial Differential Equations, 38: 385–409, 2013.

- [4] J.A. Carrillo, B. Perthame, D. Salort and D. Smets. Qualitative Properties of Solutions for the Noisy Integrate & Fire model in Computational Neuroscience. Nonlinearity, 28(9): 3365, 2015.

- [5] F. Delarue, J. Inglis, S. Rubenthaler and E. Tanré. Global solvability of a networked integrate-and-fire model of McKean–Vlasov type, Ann. Appl. Probab. 25(4):2096–2133, 2015.

- [6] F. Delarue, J. Inglis, S. Rubenthaler and E. Tanré. Particle systems with singular mean-field self-excitation. Application to neuronal networks, Stochastic Process. Appl. 125(6): 2451–2492, 2015.

- [7] L.C. Evans. Partial Differential Equations. Graduate studies in mathematics. American Mathematical Society, 2010.

- [8] A. Fasano and M. Primicerio. A critical case for the solvability of Stefan-like problems, Math. Methods Appl. Sci., 5: 84–96, 1983.

- [9] A. Fasano, M. Primicerio, S.D. Howison and J.R. Ockendon. On the singularities of one dimensional Stefan problems with supercooling. In: Mathematical Models for Phase Change Problems, Ed. J.F. Rodrigues, International Series of Numerical Mathematics 88, Birkhäuser Verlag, Basel, 1989.

- [10] A. Fasano, M. Primicerio, S.D. Howison and J.R. Ockendon. Some remarks on the regularization of supercooled one-phase Stefan problems in one dimension, Quart. Appl. Math., 47: 153–168, 1990.

- [11] J.-P. Fouque and L.-H. Sun. Systemic risk illustrated. In: Handbook on Systemic Risk, Eds. J.-P. Fouque and J. Langsam, Cambridge University Press, New York, 2013.

- [12] B. Hambly and A. Søjmark. An SPDE model for systemic risk with endogenous contagion. arXiv:1801.10088, 2018.

- [13] M.A. Herrero and J.J.L. Velázquez Singularity formation in the one-dimensional supercooled Stefan problem, European J. Appl. Math., 7: 119–150, 1996.

- [14] S. Nadtochiy and M. Shkolnikov. Particle systems with singular interaction through hitting times: Application in systemic risk modeling. arXiv:1705.00961, 2017.

- [15] G. Peskir. On Integral Equations Arising in the First-Passage Problem for Brownian Motion, J. Integral Equations Appl. 14(4): 397–423, 2002.