Diffusion Approximation of a Risk Model with Non-Stationary Hawkes Arrivals of Claims

Abstract

We consider a classical risk process with arrival of claims following a non-stationary Hawkes process. We study the asymptotic regime when the premium rate and the baseline intensity of the claims arrival process are large, and claim size is small. The main goal of the article is to establish a diffusion approximation by verifying a functional central limit theorem and to compute the ruin probability in finite-time horizon. Numerical results will also be given.

MSC2010: primary 91B30; secondary 60F17, 60G55.

Keywords: diffusion approximation, risk process, finite-horizon ruin probability, Hawkes processes.

1 Introduction

In risk theory of insurance and finance literature, ruin is the most important event. The theoretical foundation of ruin theory, known as the Cramér-Lundberg model or classical risk process was introduced by Lundberg [22]. In this paper we consider a classical risk process with the wealth at time given by

| (1.1) |

where are i.i.d. claims with the first two moments being finite, and independent of the claims arrival process which follows a non-stationary Hawkes process with the intensity (1.2), and is the constant premium rate that the insurance company receives, and is the initial wealth of the insurance company.

In the classical risk model in [22], is assumed to follow a Poisson process, which has independent and stationary time increments. In this paper, we assume that the arrival process follows a non-stationary Hawkes process, which has the clustering and self-exciting features and the time increments are dependent. A linear Hawkes process which was first introduced by A.G. Hawkes in 1971 [17, 18] is a simple point process . In this paper, we consider the non-stationary Hawkes process. The stochastic intensity of at time is given by

| (1.2) |

where are the occurrences of the points before time , and and we always assume that . We use the notation to denote the number of points in the interval . When , the non-stationary Hawkes process becomes a Poisson process with rate . A commonly used nontrivial example of is an exponential function, i.e., for , where . In this special case, the process is Markovian. In the literature, the parameter is called the baseline intensity, and is called the exciting function or sometimes referred to as the kernel function. The linear Hawkes process exhibits both self–exciting (i.e., the occurrence of an event increases the probabilities of future events) and clustering properties. Hence it is very appealing in point process modeling and it has wide application in various domains, including neuroscience [20, 24, 26], seismology [23], genome analysis [15, 25], social network [3, 5], finance (see the recent survey paper [1] and the references therein) and others.

A main topic in the mathematical finance or insurance literature, inspired by the early contributions of Lundberg [22] and Cramér [6], is the computation of the ruin probability over both finite-time and infinite-time horizon. In fact, exact formulas for both finite-time and infinite-time ruin probability are known only for few special models. Therefore, asymptotic methods have been developed to derive expansions of the ruin probability as the initial capital or reserve increases to infinity. In this paper, we focus on computing the ruin probability over finite-time horizon.

Non-stationary Hawkes Process has wide application in insurance [28, 32]. By applying the techniques of large deviations, the asymptotics of the ruin probabilities for risk processes in insurance were studied in Stabile and Torrisi [28] for the light-tailed claims and in Zhu [32] for the heavy-tailed claims. However, these two papers focus on asymptotic regimes for large initial wealth. Our paper assumes baseline intensity for Hawkes Process, which can be used to study catastrophic events. Similar regime has been studied by Gao and Zhu [11], where they use large initial intensity for Markovian case. Our paper studies different asymptotic regime that is when the baseline intensity of arrival process is large. We apply functional central limit theorem to obtain approximations and use that to study finite time ruin probability. The limit theorems have also been studied for an extension of linear Hawkes processes and Cox-Ingersoll-Ross processes in Zhu [33], which has applications in short interest rate models in finance.

A diffusion approximation is constructed for an insurance risk model which was considered by Embrechts and Schmidli [10], where the company is allowed to borrow money if needed and to invest money for large surpluses. Moreover, diffusion approximations of the risk reserve process were first studied by Iglehart [19] and subsequently by Grandell [14], Harrison [16], Schmidli [27], and Bauerle [2] by using the machinery of weak convergence.

The main goal of this article is to develop diffusion approximations for the wealth process which was introduced in (1.1) under the regime when the premium rate and the baseline intensity of the claims arrival process are large, and claim size is small. Furthermore, employing approximations of risk processes, we obtain formulas for ruin probabilities in finite horizon. Finally, we give the numerical illustrations for the results.

The rest of the paper is organized as the follows. In Section 2, we state the main results on the functional central limit theorem for aggregate claims process and hence also the wealth process, where the claims arrive according to a non-stationary Hawkes process. In Section 3, we obtain the finite-horizon ruin probability asymptotic for diffusion approximation with large initial wealth. Finally, in Section 4, we give some examples for numerical results. The proofs of the main result are given in the Appendix.

2 Functional Central Limit Theorem for Aggregate Claims Process

In this section, we study approximations for the aggregate claims process with a large baseline intensity. More precisely, we consider

| (2.1) |

so that the claim sizes are scaled by a factor and are i.i.d. with first two moments being finite, and we define , ., and for some constant . We assume the claims arrival process has intensity given by (1.2). We write to emphasize that the baseline intensity of this Hawkes process is . Our goal is to establish a functional central limit theorem for the process in the asymptotic regime .

In the classical risk model when the claims arrival process follows a standard Poisson process with constant intensity , this is the standard diffusion approximation that is used in the insurance literature.

Proposition 1.

We first present the mean and variance of the arrival process .

-

(a)

,

-

(b)

,

where

| (2.2) |

and satisfies the integral equation:

| (2.3) |

We now present a result on the functional central limit theorem (FCLT) for the aggregate claims process, and hence also the wealth process, where the claims arrive according to a non-stationary Hawkes process. Write as the space of càdlàg processes on that are equipped with Skorohod topology (see, e.g., Billingsley [4]).

Let us denote the aggregate claims process as:

| (2.4) |

Theorem 2.

Assume that is a decreasing function and . As ,

weakly in , where is a mean-zero almost surely continuous Gaussian process with the covariance function, ,

| (2.5) |

As a result,

| (2.6) |

weakly in .

The key in the observation is that can be written as an integral of a centered Gaussian process plus an independent Brownian motion:

Proposition 3.

It holds in distribution that

| (2.7) |

where is a centered Gaussian process with for any ,

| (2.8) |

and is a standard Brownian motion independent of .

Remark 4.

We first briefly explain why we obtain a Gaussian limit . By the immigration–birth representation of Hawkes processes (see, e.g., [18]), we know that for a Hawkes process with a baseline intensity and an exciting function , we can decompose it as the sum of independent Hawkes process, each having a baseline intensity one and an exciting function . Then one expects by central limit theorem type of arguments, will be asymptotically Gaussian when we send to infinity.

Remark 5.

We next discuss the variance function of in (2.5). In general, the variance function of in (2.5) is semi-explicit and we can compute it by first numerically solving and via the integral equation (2.2) and (2.3). In the special case when where , the variance function of is explicit. To see this, we first deduce from (2.2) and (2.3) that

| (2.9) |

and

| (2.10) |

Then from Proposition 1, we get

| (2.11) |

and

| (2.12) |

Let in (2.5), we get:

| (2.13) |

Remark 6.

Furthermore we are able to calculate the covariance of . Please see the derivation in appendix. For ,

| (2.14) |

where are constants and

In this special case, we notice that the variance function of , is nonlinear in in general. This is very different from the case when is a Poisson process (i.e., ) where becomes a standard Brownian motion.

3 Ruin Probability for the Diffusion Approximation

In this section, we focus on developing the asymptotic estimates for the finite-horizon ruin probabilities. In the large baseline intensity limit, the ruin probability becomes:

| (3.1) |

for the finite-horizon case.

From the fact that

| (3.2) |

weakly in in Theorem 2, it suffices to study (3.1) as the large baseline intensity approximation to get the finite-horizon ruin probabilities for .

Next, let us consider the exact asymptotics for the finite-time ruin probability with large initial wealth. We rely on the results in [8].

Let be the standard deviation function of . Let us consider . We know that

| (3.3) |

which is increasing in with unique maximum achieved at . We can compute that

| (3.4) |

as . For any ,

| (3.5) |

We can further compute that

| (3.6) | ||||

as , and .

The Assumption A1 is thus satisfied in [8] for . The Assumption A2 trivially holds in [8] for , see proof of Theorem 2 in appendix.

By Theorem 3.1. [8], we have

| (3.7) |

as , where

and

,

where

| (3.8) |

where is a fractional Brownian motion with Hurst index and and .

In our setting, , and is a standard Brownian motion.

4 Numerical Studies

In this section we study several numerical illustrations for the theoretical results of this article. For , we can simulate the Gaussian process , and numerically compute the ruin probability for the finite-horizon case.

4.1 Jump size as exponential distribution

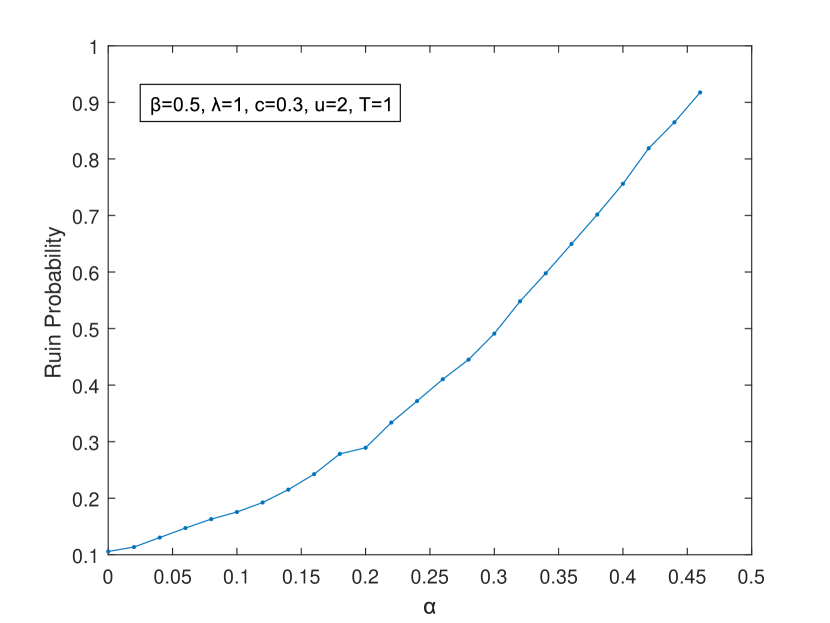

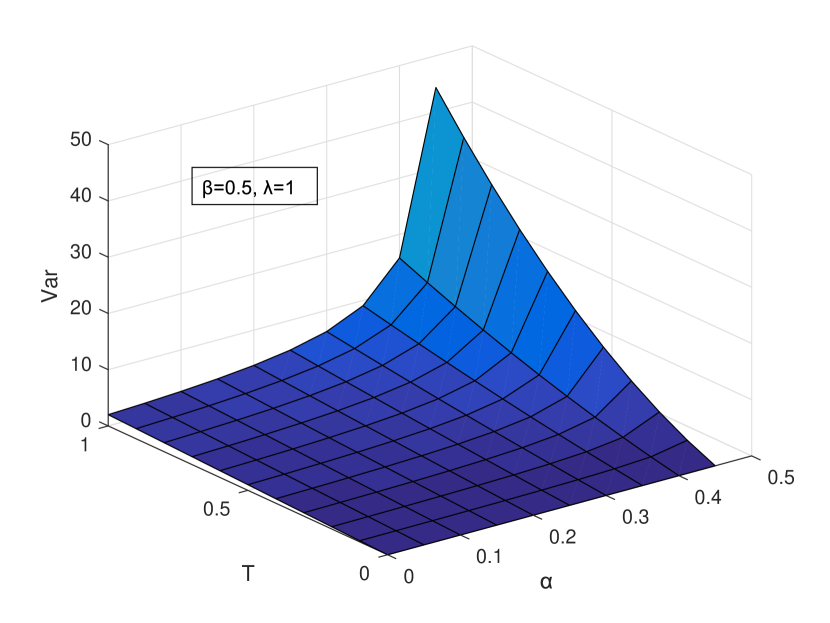

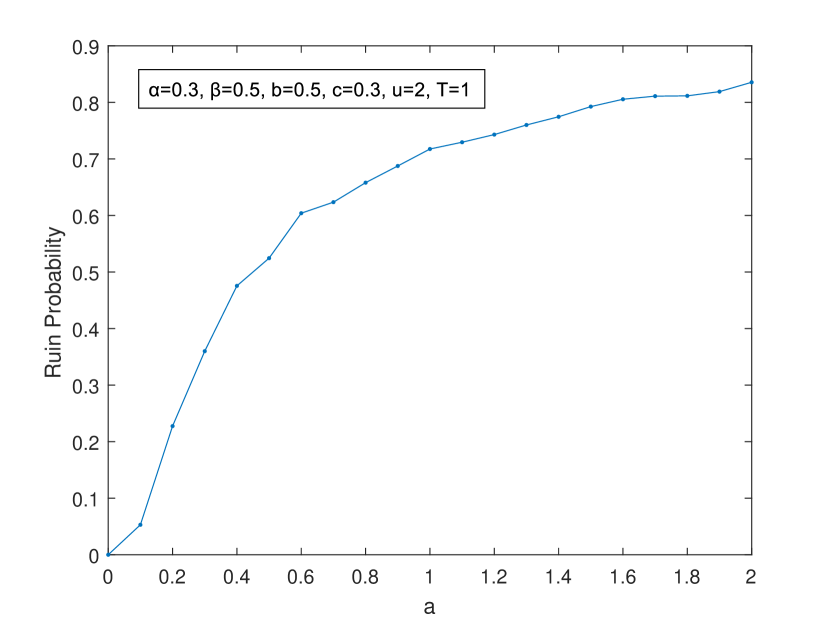

Here suppose follows an i.i.d. exponential distribution with intensity , i.e. , we computed the ruin probability with different parameters We recall that in Remark 6, we assume so that the covariance function of is explicit.

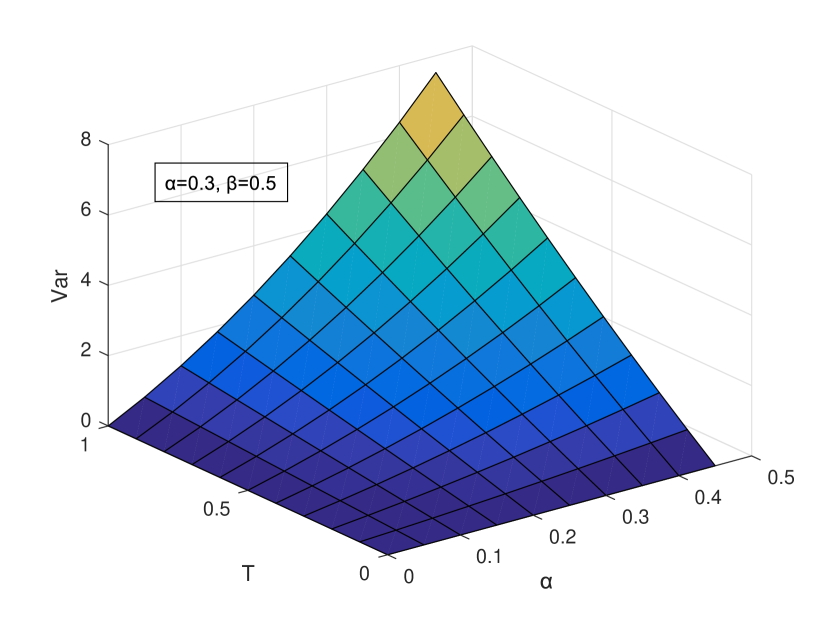

From Figure 1(a) we can see that with other parameters fixed, the ruin probability is an increasing function of . To explain, we plotted the variance of shown in (5), as a function of and . In Figure 1(b), the variance increases as increases. Intuitively, as the variance of increases, the probability that exceed a certain range increases. So the ruin probability increases.

Then we plot the ruin probability as a function of the intensity of the jump . And also, we can infer this from the plot of versus :

4.2 Jump size as Gamma distribution

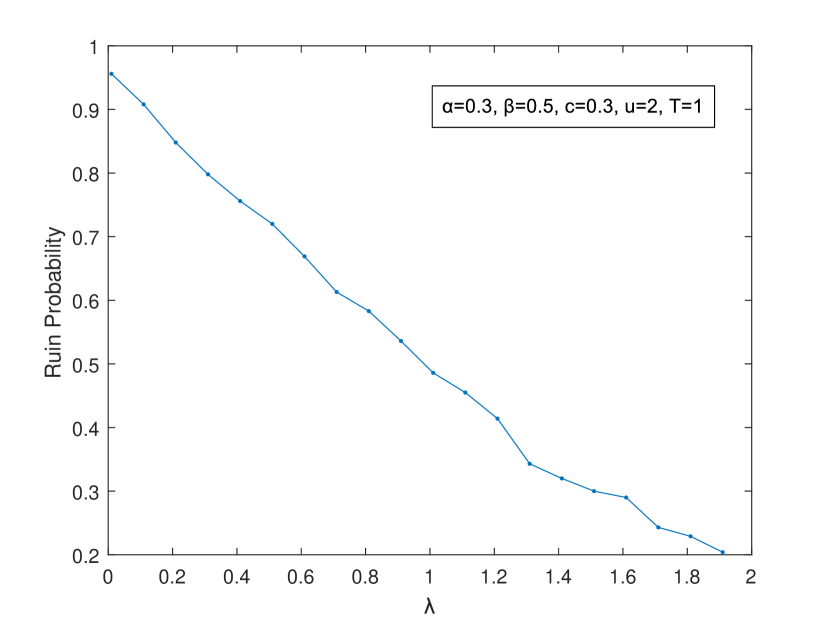

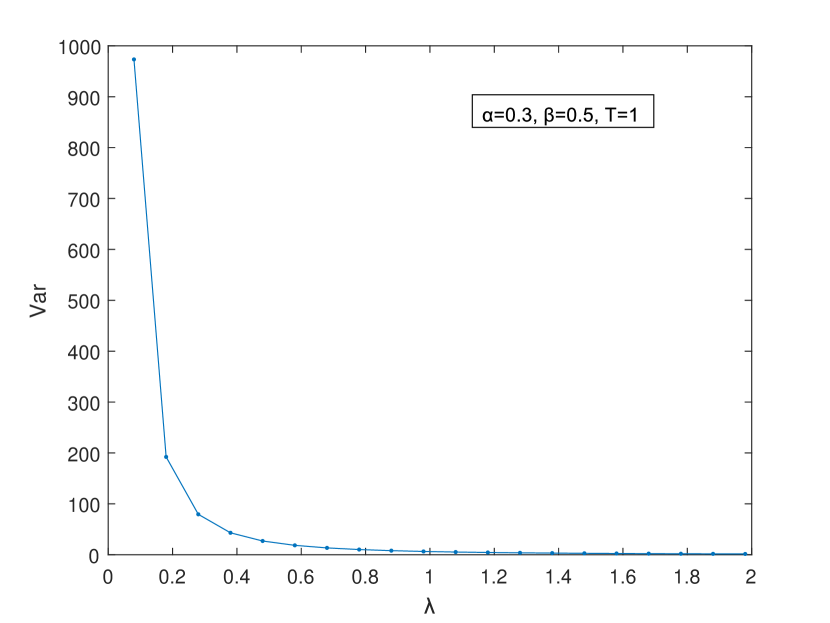

Assume the jump size follows Gamma distribution with shape and rate , i.e. . Let’s see how the ruin probability changes as change.

We can see that the ruin probability is an increasing function of , and this can be explained by the in Figure 3(b), the variance increases as increases.

5 Appendix

5.1 Proof of Proposition 1

Proof.

By the result of the moment generating function of obtained in Zhu [30], we have, for any and ,

| (5.1) |

where the function is the unique solution to the integral equation

| (5.2) |

We first compute the first two moments of . By differentiating the moment generating function of with respect to in (5.1), we get

| (5.3) |

and by differentiating with respect to again, we get

| (5.4) |

By differentiating both sides of (5.2) w.r.t. , we get

| (5.5) |

By differentiating again w.r.t. , we get

5.2 Proof of Theorem 2

Proof.

For the sake of simplicity, we assume that The argument to go from to non-integer-valued follows the same argument as in Gao and Zhu [12] . By immigration birth representation, we can decompose as the sum of independent and identically distributed (i.i.d) Hawkes processes , each distributed as a Hawkes process with base intensity (the superscript 1 in ) and the exciting function . For notational simplicity, we use for . As a result, we can decompose as the sum of i.i.d. compound Hawkes processes and let us write .

Therefore,

Let . Then, are i.i.d. random elements of with and for any (This is a well-known fact for Hawkes processes. See e.g. [31]). Similarly, we define .

By Hahn’s theorem (see e.g. Theorem 7.2.1. in [29]), we have as

| (5.7) |

weakly in , where is a mean-zero almost surely continuous Gaussian process with the covariance function of provided that the following conditions are satisfied: For every , there exist continuous nondecreasing real-valued functions and on with numbers and such that

| (5.8) |

and

| (5.9) |

for all with .

First, notice that

| (5.10) |

By using the tower property,

| (5.11) |

The first inequality in (5.11) holds because

We deduce that (5.8) is satisfied with for some constant and .

The last two inequality holds because and . Also, we can conclude from the proof of Theorem 1 of [12], . Note that above are all constants. So we deduce that (5.9) is satisfied with for some constant and . Thus we have verified (5.7).

Finally, let us identify the variance and covariance function of the Gaussian limit , for any ,

| (5.12) |

∎

5.3 Derivation of the result in (3.6)

as , and .

5.4 Derivation of the results in Remark 5 and 6

To compute , we have:

and

| (5.13) |

Here , so (5.13) can be written as:

| (5.14) |

In the special case when , is Markovian and we can get the explicit formula.

We have , so

In (5.14),

| (5.15) |

Here , . Also we have:

and

Solving it, we get:

| (5.16) |

Moreover, we have

and

Hence we have:

| (5.17) |

Next, we need to figure out by using the infinitesimal generator as following:

| (5.18) |

Let then we have

and hence, we have

By differentiation, we get:

Solving it, we get

| (5.19) |

Substitute into (5.15), we get:

| (5.21) |

where are constants and

Hence, we have:

| (5.22) |

According to (5.14), we have

| (5.23) |

Thus, we can compute that as following:

| (5.25) |

In (LABEL:covgg), setting , we obtain the variance of :

| (5.26) |

Acknowledgements

Youngsoo Seol is grateful to the support from the Dong-A University

research grant.

References

- [1] Bacry, E., Mastromatteo, I., and Muzy, J. F. (2015). Hawkes processes in finance. Market Microstructure and Liquidity, 1, 1-59.

- [2] Bäuerle, N. (2004). Approximation of optimal reinsurance and dividend payout policies. Math. Finance, 14, 99-113.

- [3] Blundell, C., Beck, J., and Heller, K. A. (2012). Modelling reciprocating relationships with Hawkes processes. In Advances in Neural Information Processing Systems. 2600-2608.

- [4] Billingsley, P. (1999). Convergence of Probability Measures, 2nd edition. Wiley–Interscience, New York.

- [5] Crane, R. and D. Sornette. (2008). Robust dynamic classes revealed by measuring the response function of a social system. Proc. Nat. Acad. Sci. USA, 105, 15649.

- [6] Cramér, H. On the mathematical theory of risk. Skandia Jubilee Volume, (1930) Stockholm. Reprinted in: MartinL¡§of, A. (Ed.) Cram¢¥er, H. (1994) Collected Works. Springer, Berlin.

- [7] Dȩbicki, K. (2002). Ruin probability for Gaussian integrated processes. Stochastic Process. Appl., 98, 151-174.

- [8] Dȩbicki, K., Hashorva, E., Ji L. and Z. Tan. (2014). Finite-time ruin probability of aggregate Gaussian processes. Markov Process. Related Fields, 20, 435-450.

- [9] Dieker, A. B. (2005). Extremes of Gaussian processes over an infinite horizon. Stochastic Process. Appl., 115, 207-248.

- [10] Embrechts P, Schmidli H. (1994). Ruin estimation for a general insurance risk model. Adv. Appl. Probab., 26(2), 404-422.

- [11] Gao, X. and Zhu, L. (2018). Large deviations and applications for Markovian Hawkes processes with a large initial intensity. Bernoulli, 24, 2875-2905.

- [12] Gao, X. and Zhu, L. (2018). Functional central limit theorem for stationary Hawkes processes and its application to infinite-server queues. Queueing system, 60, 161-206.

- [13] Gao, X. Zhou, X. and Zhu, L. (2018). Transform analysis for Hawkes processes with applications in dark pool trading. Quantitative Finance, 2, 265-282.

- [14] Grandell,J. (1977). A class of approximations of ruin probabilities. Scand. Actuar. J., 37-52.

- [15] Gusto, G., and Schbath, S. (2005). FADO: a statistical method to detect favored or avoided distances between occurrences of motifs using the Hawkes’ model. Stat. Appl. Genet. Mol. Biol., 4(1).

- [16] Harrison,J.M. (1977). Ruin problems with compounding assets. Stochastic Process. Appl., 5, 67-79.

- [17] Hawkes, A. G. (1971). Spectra of some self-exciting and mutually exciting point processes. Biometrika 58, 83-90.

- [18] Hawkes, A.G. (1971). Point spectra of some mutually exciting point processes. J. Roy. Statist. Soc. Ser. B Stat. Methodol., pp.438-443.

- [19] Iglehart, D. L. (1969). Diffusion approximations in collective risk theory. J. Appl. Prob. ,6, 285-292.

- [20] Johnson, D. H. (1996). Point process models of single-neuron discharges. J. Comput. Neurosci., 3(4), 275-299.

- [21] Karabash, D. and Zhu, L. (2015). Limit theorems for marked Hawkes processes with application to a risk model. Stochastic Models, 31, 433-451.

- [22] Lundberg, F. (1903). Approximerad framställning av sannolikhetsfunktionen. Aterförsäkring av kollektivrisker. Akad. Afhandling. Almqvist och Wiksell, Uppsala.

- [23] Ogata, Y. (1988). Statistical models for earthquake occurrences and residual analysis for point processes. J. Amer. Stat. Assoc., 83(401), 9-27.

- [24] Pernice, V., Staude B., Carndanobile, S. and S. Rotter. (2012). How structure determines correlations in neuronal networks. PLoS Comput. Biol., 85:031916.

- [25] Reynaud-Bouret, P., and Schbath, S. (2010). Adaptive estimation for Hawkes processes; application to genome analysis. Ann. Statist., 38(5), 2781-2822.

- [26] Reynaud-Bouret, P., Rivoirard, V., and Tuleau-Malot, C. (2013). Inference of functional connectivity in neurosciences via Hawkes processes. In 1st IEEE Global Conference on Signal and Information Processing.

- [27] Schmidli,H. (1994). Diffusion approximations for a risk process with the possibility of borrowing and investment. Comm. Stat. Stoch. Models, 10,365-388.

- [28] Stabile, G. and G. L. Torrisi. (2010). Risk processes with non-stationary Hawkes arrivals. Methodol. Comput. Appl. Prob. ,12, 415-429.

- [29] Whitt, W. (2002). Stochastic-process limits: an introduction to stochastic-process limits and their application to queues. Springer Science and Business Media.

- [30] Zhu, L. (2013). Moderate deviations for Hawkes processes. Stat. and Prob. Letters, 83 885-890.

- [31] Zhu, L. (2013). Central limit theorem for nonlinear Hawkes processes. J. Appl. Prob., 50 760-771.

- [32] Zhu, L. (2013). Ruin probabilities for risk processes with non-stationary arrivals and subexponential claims. Insurance Math. Econom., 53(3), 544-550.

- [33] Zhu, L. (2014). Limit theorems for a Cox-Ingersoll-Ross process with Hawkes jumps. J. Appl. Prob., 51 699-712.