1 Introduction

The Markov regime switching model has been a popular framework for empirical work in economics and finance. Following the seminal contribution by Hamilton (1989), it has been used in numerous empirical studies to model, for example, the business cycle (Hamilton, 2005; Morley and Piger, 2012), stock market volatility (Hamilton and Susmel, 1994), international equity markets (Ang and Bekaert, 2002; Okimoto, 2008), monetary policy (Schorfheide, 2005; Sims and Zha, 2006; Bianchi, 2013), and economic growth (Kahn and Rich, 2007). Comprehensive theoretical accounts and surveys of applications are provided by Hamilton (2008, 2016) and Ang and Timmermann (2012).

The number of regimes is an important parameter in applications of Markov regime switching models. Despite its importance, however, testing for the number of regimes in Markov regime switching models has been an unsolved problem because the standard asymptotic analysis of the likelihood ratio test statistic (LRTS) breaks down because of problems such as unidentifiable parameters, the true parameter being on the boundary of the parameter space, and the degeneracy of the Fisher information matrix. Testing the number of regimes for Markov regime switching models with normal density, which are popular in empirical applications, poses a further difficulty because normal density has the undesirable mathematical property that the second-order derivative with respect to the mean parameter is linearly dependent on the first derivative with respect to the variance parameter, leading to further singularity.

This paper proposes the likelihood ratio test of the null hypothesis of regimes against the alternative hypothesis of regimes for any and derives its asymptotic distribution. To the best of our knowledge, the asymptotic distribution of the LRTS has not been derived for testing the null hypothesis of regimes with . To test the null hypothesis of no regime switching, namely , Hansen (1992) derives an upper bound of the asymptotic distribution of the LRTS, and Garcia (1998) also studies this problem. Carrasco et al. (2014) propose an information matrix-type test for parameter constancy in general dynamic models including regime switching models. Cho and White (2007) derive the asymptotic distribution of the quasi-LRTS for testing the single regime against two regimes by rewriting the model as a two-component mixture model, thereby ignoring the temporal dependence of the regimes. Qu and Zhuo (2017) extend the analysis of Cho and White (2007) and derive the asymptotic distribution of the LRTS that properly takes into account the temporal dependence of the regimes under some restrictions on the transition probabilities of latent regimes. Marmer (2008) and Dufour and Luger (2017) develop tests for the null hypothesis of no regime switching by using different approaches from the LRTS. The studies discussed above focus on testing the single regime against two regimes. To the best of our knowledge, however, the asymptotic distribution of the LRTS for testing the null hypothesis of regimes with remains unknown.

Several papers in the literature consider tests when some parameters are not identified under the null hypothesis. These include Davies (1977, 1987), Andrews and Ploberger (1994, 1995), Hansen (1996a), Andrews (2001), and Liu and Shao (2003), among others. Estimation and testing with a degenerate Fisher information matrix are investigated in an iid setting by Chesher (1984), Lee and Chesher (1986), Rotnitzky et al. (2000), and Gu et al. (2017), among others. Chen et al. (2014) examine uniform inference on the mixing probability in mixture models.

To facilitate the analysis herein, we develop a version of Le Cam’s differentiable in quadratic mean (DQM) expansion that expands the likelihood ratio under the loss of identifiability, while adopting the reparameterization and higher-order expansion of Kasahara and Shimotsu (2015). In an iid setting, Liu and Shao (2003) develop a DQM expansion under the loss of identifiability in terms of the generalized score function. We extend Liu and Shao (2003) to accommodate dependent and heterogeneous data as well as modify them to fit our context of parametric regime switching models. Using a DQM-type expansion has an advantage over the “classical” approach based on the Taylor expansion up to the Hessian term because deriving a higher-order expansion becomes tedious as the order of expansion increases in a Markov regime switching model. Furthermore, regime switching models with normal components are not covered by Liu and Shao (2003) because their Theorem 4.1 assumes that the generalized score function is obtained by expanding the likelihood ratio twice, whereas our Section 6.2 shows that the score function is a function of the fourth derivative of the likelihood ratio in the normal case.

Our approach follows Douc et al. (2004) [DMR hereafter], who derive the asymptotic distribution of the maximum likelihood estimator (MLE) of regime switching models. We express the higher-order derivatives of the period density ratios in terms of the conditional expectation of the derivatives of the period complete-data log-density, i.e., the log-density when the state variable is observable, by applying the missing information principle (Woodbury, 1971; Louis, 1982) and extending the analysis of DMR. We then show that these derivatives of the period density ratios can be approximated by a stationary, ergodic, and square integrable martingale difference sequence by conditioning on the infinite past, and this approximation is shown to satisfy the regularity conditions for our DQM expansion.

We first derive the asymptotic null distribution of the LRTS for testing against . When the regime-specific density is not normal, the log-likelihood function is locally approximated by a quadratic function of the second-order polynomials of the reparameterized parameters. When the density is normal, the degree of deficiency of the Fisher information matrix and required order of expansion depend on the value of the unidentified parameter; in particular, when the latent regime variables are serially uncorrelated, the model reduces to a finite mixture normal model in which the fourth-order DQM expansion is necessary to derive a quadratic approximation of the log-likelihood function. We expand the log-likelihood with respect to the judiciously chosen polynomials of the reparameterized parameters—which involves the fourth-order polynomials—to obtain a uniform approximation of the log-likelihood function in quadratic form and derive the asymptotic null distribution of the LRTS by maximizing the quadratic form under a set of cone constraints building on the results of Andrews (1999, 2001).

To derive the asymptotic null distribution of the LRTS for testing against for , we partition a set of parameters that describes the true null model in the alternative model into subsets, each of which corresponds to a specific way of generating the null model. We show that the asymptotic distribution of the LRTS is characterized by the maximum of the random variables, each of which represents the LRTS for testing each of the subsets.

We also derive the asymptotic distribution of the LRTS under local alternatives. Carrasco et al. (2014) show that the contiguous local alternatives of their tests are of order , where is the sample size. In a related problem of testing the number of components in finite mixture normal regression models, Kasahara and Shimotsu (2015) show that the contiguous local alternatives are of order (see also Chen and Li, 2009; Chen et al., 2012; Ho and Nguyen, 2016). We show that the value of the unidentified parameter affects the convergence rate of the contiguous local alternatives. When the regime-specific density is normal, some contiguous local alternatives are of the order , and the LRT is shown to have non-trivial power against them. The tests of Carrasco et al. (2014) do not have power against such alternatives, whereas the test of Qu and Zhuo (2017) rules out such alternatives because of their restriction on the parameter space.

The asymptotic validity of the parametric bootstrap is also established both under the null hypothesis and under local alternatives. The simulations show that our bootstrap LRT has good finite sample properties. Our results also imply that the bootstrap LRT is valid for testing the number of hidden states in hidden Markov models because this paper’s model includes the hidden Markov model as a special case. Although several papers have analyzed the asymptotic property of the MLE of the hidden Markov model, the asymptotic distribution of the LRTS for testing the number of hidden states has been an open question.

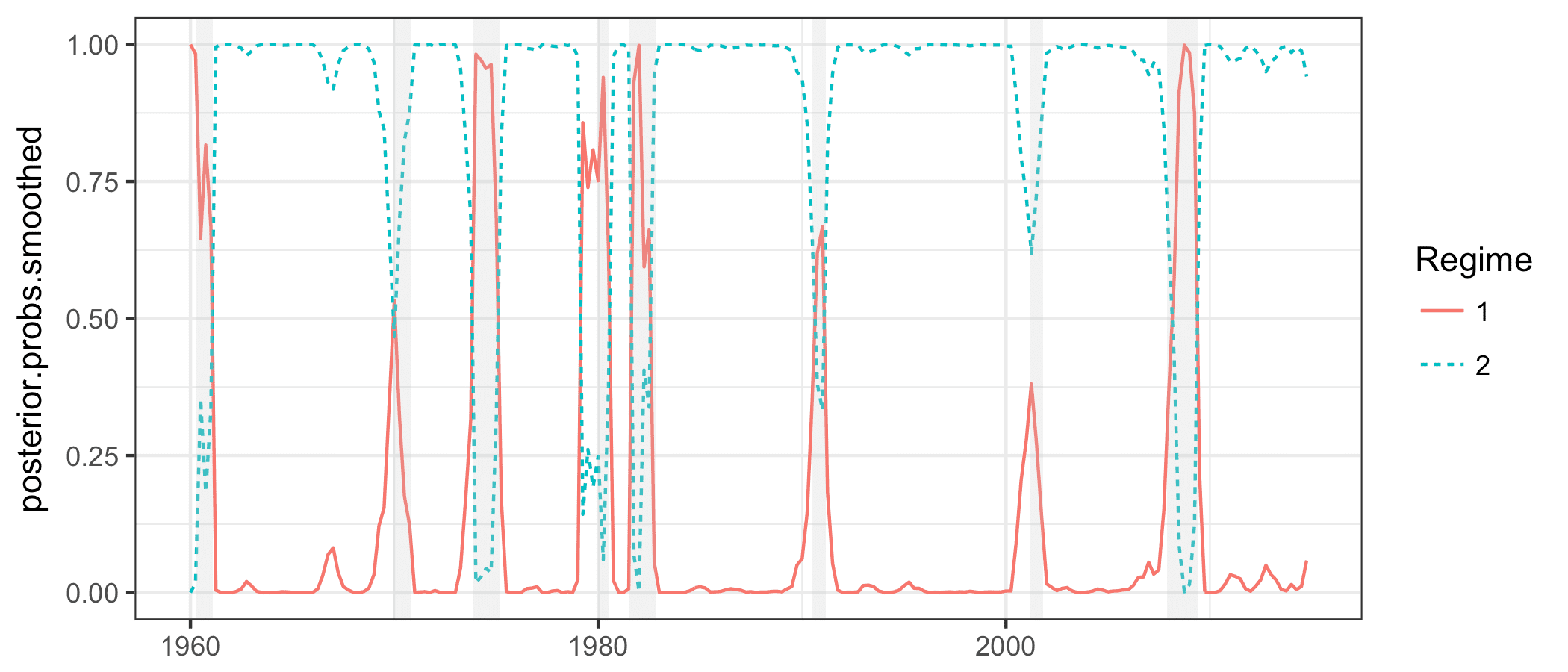

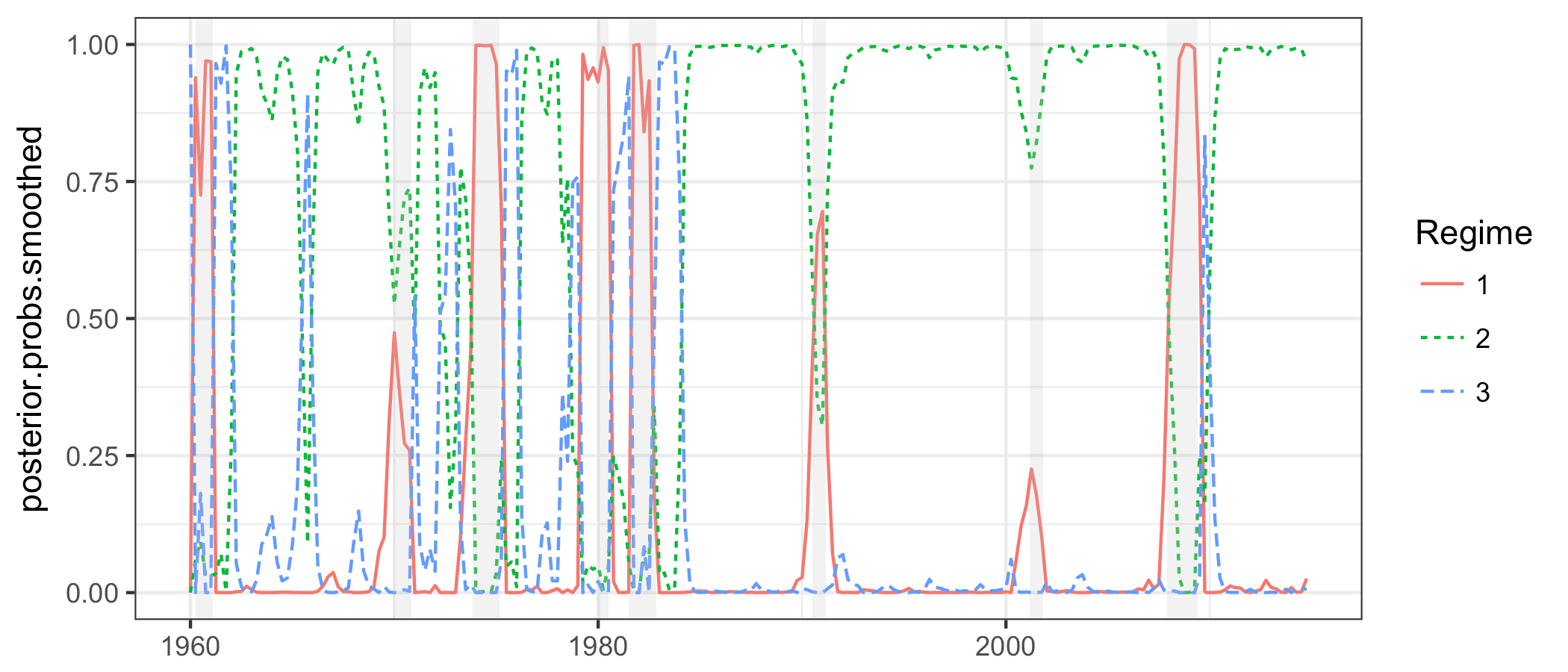

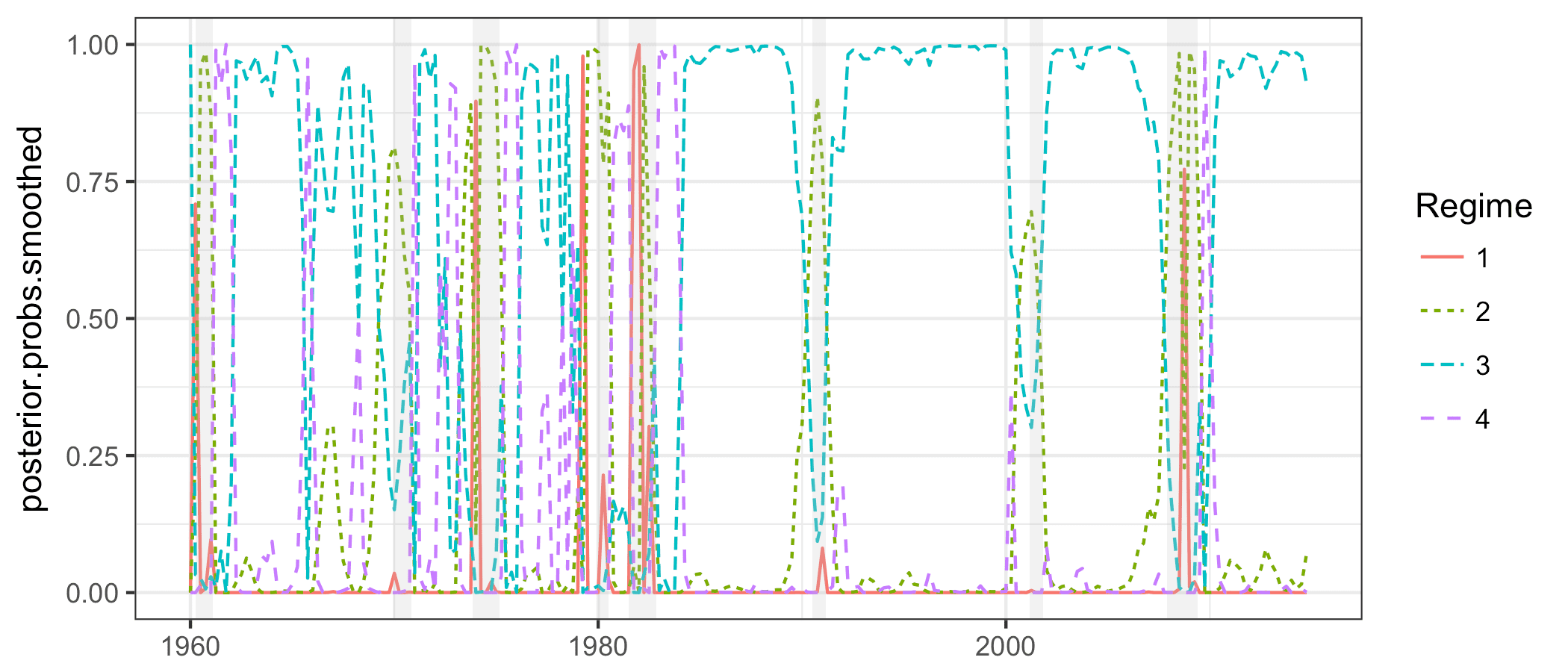

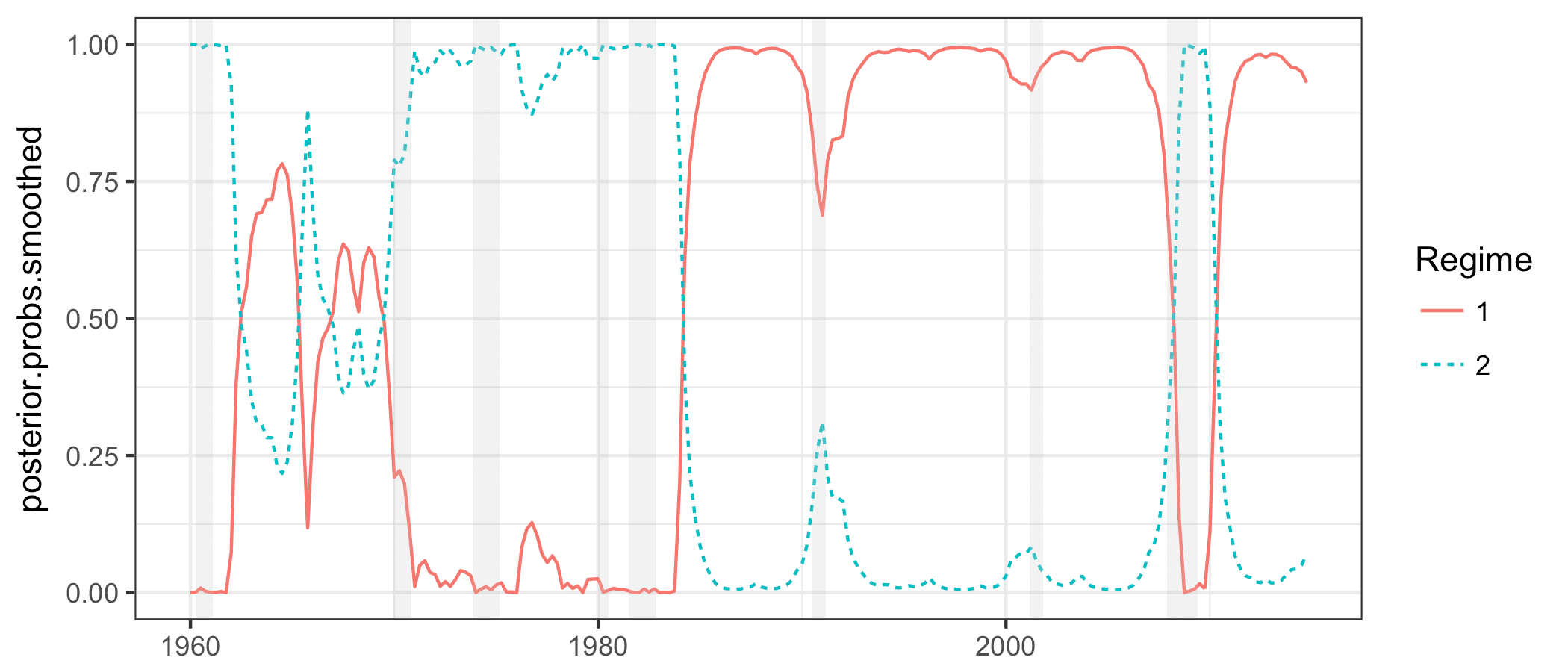

The remainder of this paper is organized as follows. After introducing the notation and assumptions in Section 2, we discuss the degeneracy of the Fisher information matrix and loss of identifiability in regime switching models in Section 3. Section 4 establishes the DQM-type expansion. Section 5 presents the uniform convergence of the derivatives of the density ratios. Sections 6 and 7 derive the asymptotic null distribution of the LRTS. Section 8 derives the asymptotic distribution under local alternatives. Section 9 establishes the consistency of the parametric bootstrap. Section 10 reports the results from the simulations and an empirical application, using U.S. GDP per capita quarterly growth rate data. Section 11 collects the proofs and auxiliary results.

2 Notation and assumptions

Let denote “equals by definition.” Let denote the weak convergence of a sequence of stochastic processes indexed by for some space . For a matrix , let and be the smallest and largest eigenvalues of , respectively. For a -dimensional vector and a matrix , define and . For a vector and a function , let , and let denote a collection of derivatives of the form . Let denote an indicator function that takes the value 1 when is true and 0 otherwise. denotes a generic non-negative finite constant whose value may change from one expression to another. Let and . Let denote the largest integer less than or equal to , and define . Given a sequence , let . For a sequence indexed by and , we write if, for any , there exist and such that for all , and we write if, for any , there exist and such that for all . Loosely speaking, and mean that and when is sufficiently small, respectively. All limits are taken as unless stated otherwise. The proofs of all the propositions and lemmas are presented in the appendix.

Consider the Markov regime switching process defined by a discrete-time stochastic process , where takes values in a set with and , and let denote the associated Borel -field. For a stochastic process and , define . Denote for a fixed integer and . Here, is an observable variable, is an unobservable state variable, is the lagged ’s used as a covariate, and is a weakly exogenous covariate. DMR’s model does not include .

Assumption 1.

(a) is a first-order Markov chain with the state space . (b) For each , is independent of given . (c) For each , is conditionally independent of given . (d) is conditionally independent of given . (e) is a strictly stationary ergodic process.

When is absent, DMR provide a sufficient condition for the ergodicity of in their Assumption (A2). We assume the ergodicity of for brevity.

The unobservable Markov chain is called the regime. The integer represents the number of regimes specified in the model. The parameter belongs to , a compact subset of . contains the parameter of the transition probability of , which we denote by . Let for and , and is determined by . contains the parameter of the conditional density of given , which is given by . Here, is the structural parameter that does not vary across regimes, is the regime-specific parameter that varies across regimes, and is the conditional density of given when .

Let

|

|

|

|

|

|

|

|

We assume , and the true parameter value is denoted by .

We make the following assumptions that correspond to (A1)–(A3) in DMR.

Assumption 2.

(a) and

for each . (b) For all , , and , and . (c) and , where .

As discussed on p. 2260 of DMR, Assumption 2(a) implies that the Markov chain has a unique invariant distribution and is uniformly ergodic for all . For notational brevity, we drop the subscript from , , , etc., unless it is important to clarify the specific value of . Assumptions 1(b) and (c) imply that is a Markov chain on given , and is conditionally independent of given . Consequently, Lemma 1, Corollary 1, and Lemma 9 of DMR go through even in the presence of . Because is stationary, we can and will extend to a stationary process with doubly infinite time. We denote the probability measure and associated expectation of under stationarity by and , respectively.

Under Assumptions 1(a)–(d), the density of given , and is given by

|

|

|

(1) |

Define the conditional log-likelihood function and stationary log-likelihood function as

|

|

|

|

|

|

|

|

where we use the fact that and , which follows from Assumption 1. Note that

|

|

|

|

|

|

and . Let . Lemma 11(a) in the appendix shows that, for all probability measures and on and all ,

|

|

|

(2) |

Consequently, goes to zero at an exponential rate as . Therefore, as shown in the following proposition, the difference between and is bounded by a deterministic constant, and the maximum of and the maximum of are asymptotically equivalent.

Proposition 1.

Under Assumptions 1 and 2, for all ,

|

|

|

As discussed on p. 2263 of DMR, the stationary density is not available in closed form for some models with autoregression. For this reason, we consider the log-likelihood function when the initial distribution of follows some distribution

and .

Define the MLE, , by the maximizer of the log-likelihood:

|

|

|

(3) |

where is given in (1). We define the number of regimes by the smallest number such that the data density admits the representation (3). Our objective is to test against .

4 Quadratic expansion under the loss of identifiability

When testing the number of regimes by the LRT, a part of is not identified under the null hypothesis. Let denote the part of that is not identified under the null, and split as . For example, in testing against , we have and . We denote the conditional log-likelihood function as and use and interchangeably.

Denote the true parameter value of by , and denote the set of corresponding to the null hypothesis by .

Let be a continuous function of such that if and only if . For , define the neighborhood of by

|

|

|

When the MLE is consistent, the asymptotic distribution of the LRTS is determined by the local properties of the likelihood functions in .

We establish a general quadratic expansion of the log-likelihood function defined in (3) around that expresses as a quadratic function of . Once we derive a quadratic expansion, the asymptotic distribution of the LRTS can be characterized by taking its supremum with respect to under an appropriate constraint and using the results of Andrews (1999, 2001).

Denote the conditional density ratio by

|

|

|

(4) |

so that . We assume that can be expanded around as follows. With a slight abuse of the notation, let and recall .

Assumption 3.

For all , admits an expansion

|

|

|

(5) |

where satisfies if and satisfy, for some , , , and , (a) , (b) with , (c) , (d) , (e) for , (f) , (g) .

We first establish an expansion of in the neighborhood of for any .

Proposition 2.

Suppose that Assumptions 3 (a)–(f) hold. Then, for any ,

|

|

|

The following proposition expands in for some . This proposition is useful for deriving the asymptotic distribution of the LRTS because a consistent MLE is in by definition. Let .

Proposition 3.

Suppose that Assumption 3 holds. Then, for any , (a) , and (b) for any ,

|

|

|

The following corollary of Propositions 2 and 3 shows that defined in (3) admits a similar expansion to for all . Consequently, the asymptotic distribution of the LRTS does not depend on , and may be maximized in while fixing or jointly in and . Let and , which includes a consistent MLE with any .

Corollary 1.

(a) Under the assumptions of Proposition 2, we have

for any .

(b) Under the assumptions of Proposition 3, for any and , and .

5 Uniform convergence of the derivatives of the log-density and density ratios

In this section, we establish approximations that enable us to apply the results in Section 4 to the log-likelihood function of regime switching models. Because of the presence of singularity, the expansion (5) of the density ratio involves the higher-order derivatives of the density ratios with . Note that can be expressed in terms of the derivatives of log-densities, . We show that these derivatives are approximated by their stationary counterpart that condition on the infinite past in place of . Consequently, the sequence is approximated by a stationary martingale difference sequence.

For and , let

|

|

|

(6) |

denote the stationary density of associated with conditional on , where is drawn from its true conditional stationary distribution . Let denote the associated conditional density of given .

Define the density ratio as . For , , , and , define the derivatives of the log-densities and density ratios by, with suppressing the subscript from for brevity,

|

|

|

|

|

|

The following assumption corresponds to (A6)–(A8) in DMR and is tailored to our setting where some elements of are not identified and is finite. Note that Assumptions (A6) and (A7) in DMR pertaining to hold in our case because the ’s are bounded away from 0 and 1. Let . satisfies Assumption 4(b) in general when is sufficiently small.

Assumption 4.

There exists a positive real such that on the following conditions hold: (a) For all , is six times continuously differentiable on . (b) for and with , where and for some and . (c) For almost all , and, for almost all , for , there exist functions in such that for all .

The following proposition shows that and are -Cauchy sequences that converge to -a.s. and in uniformly in and .

Proposition 4.

Under Assumptions 1, 2, and 4, for , there exist random variables and such that, for all and ,

|

|

|

|

|

|

|

|

|

|

|

|

where , , , , , and . (d) Uniformly in and , and converge -a.s. and in to as .

As shown by the following proposition, we may prove the uniform convergence of the derivatives of the density ratios by expressing them as polynomials of the derivatives of the log-density and applying Proposition 4 and Hölder’s inequality.

Proposition 5.

Under Assumptions 1, 2, and 4, for , there exist random variables and such that, for all and ,

|

|

|

|

|

|

|

|

|

|

|

|

(d) Uniformly in and , and converge -a.s. and in to as . (e) -a.s.

When we apply the results in Section 4 to regime switching models, corresponds to on the left-hand side of (5), and in (5) is a function of the ’s. Proposition 5 and the dominated convergence theorem for conditional expectations (Durrett, 2010, Theorem 5.5.9) imply that for all . Therefore, is a stationary, ergodic, and square integrable martingale difference sequence, and satisfies Assumption 3(a)(b)(g).

6 Testing homogeneity

Before developing the LRT of components, we analyze a simpler case of testing the null hypothesis against when the data are from . We assume that the parameter space for takes the form for a small . Denote the true parameter in the one-regime model by . The two-regime model gives rise to the true density if the parameter lies in a subset of the parameter space

|

|

|

Note that is not identified under .

Let denote the two-regime log-likelihood for a given initial distribution , and let denote the MLE of given , where is suppressed from because does not matter asymptotically. Let denote the one-regime MLE that maximizes the one-regime log-likelihood function under the constraint .

We introduce the following assumption for the consistency of and . Assumption 5(b) corresponds to Assumption (A4) of DMR. Assumption 5(c) is a standard identification condition for the one-regime model. Assumption 5(d) implies that the Kullback–Leibler divergence between and is 0 if and only if .

Assumption 5.

(a) and are compact, and is in the interior of . (b) For all and all , is continuous in . (c) If , then . (d) for all if and only if .

The following proposition shows the consistency of the MLEs of and .

Proposition 6.

Suppose that Assumptions 1, 2, and 5 hold. Then, under the null hypothesis of , and .

Let denote the LRTS for testing against . Following the notation of Section 4, we split into , where is the part of not identified under the null hypothesis; the elements of are delineated later. In the current setting, corresponds to . Define and . The parameter spaces for and under restriction are given by and , respectively. Because the mapping from to is one-to-one, we reparameterize as , and let . Henceforth, we suppress for notational brevity and write, for example, as and as when doing so does not cause confusion.

We derive the asymptotic distribution of the LRTS by applying Corollary 1 to and representing and in (5) in terms of , , and its derivatives; involves higher-order derivatives, and consists of the functions of the polynomials of (reparameterized) . Section 6.1 analyzes the case when the regime-specific distribution of is not normal with unknown variance. Section 6.2 analyzes the case when the regime-specific distribution is normal with regime-specific and unknown variance. Section 6.3 handles the normal distribution where the variance is unknown and common across regimes. Note that because and are independent when , we have

|

|

|

(7) |

Define , so that .

6.1 Non-normal distribution

When we apply Corollary 1 to regime switching models, is a function of

’s with defined in (6). In order to express in terms of via the Louis information principle (Lemma 1 in the appendix), we first derive the derivatives of the complete data conditional density .

Consider the following reparameterization. Let

|

|

|

(8) |

Let and . Under the null hypothesis of one regime, the true value of is given by . Henceforth, we suppress the subscript from . Using this definition of , let . By using reparameterization (8) and noting that , we have and

|

|

|

(9) |

Henceforth, let , , , and denote , , , and , respectively, and similarly for ,, , and .

Expanding twice with respect to and evaluating at gives

|

|

|

|

(10) |

|

|

|

|

Recall . Observe that satisfies

|

|

|

|

(11) |

|

|

|

|

where the first three results follow from the property of a Bernoulli random variable, and the last result follows from Hamilton (1994, p. 684). Then, it follows from (7) and (11) that

|

|

|

|

(12) |

From Lemma 1, , and the definition of in (6), we obtain

|

|

|

|

Applying (10), (12), and to the right-hand side gives

|

|

|

(13) |

Similarly, it follows from Lemma 1, (10), (12), (13), and that

|

|

|

(14) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(15) |

Because the first-order derivative with respect to is identically equal to zero in (13),

the unique elements of and constitute the generalized score in Corollary 1. This score is approximated by a stationary martingale difference sequence, where the approximation error satisfies Assumption 3.

We collect some notations. Recall and . For a vector and a matrix , define the vectors and as

|

|

|

|

(16) |

|

|

|

|

Noting that for , define, with ,

|

|

|

|

(17) |

and with

|

|

|

(18) |

Here, in (17) depends on but not on and corresponds to in Corollary 1.

The following proposition shows that the log-likelihood function is approximated by a quadratic function of . Let . Let and , where we suppress the subscript from .

We use this definition of through Sections 6.1–6.3. As shown in Sections 6.2 and 6.3, Assumption 6 does not hold for regime switching models with a normal distribution.

Assumption 6.

for , where is given in (17).

Proposition 7.

Suppose Assumptions 1, 2, 4, 5, and 6 hold. Then, under the null hypothesis of , (a) ; and (b) for any ,

|

|

|

(19) |

We proceed to derive the asymptotic distribution of the LRTS. With defined in (17), define

|

|

|

|

(20) |

|

|

|

|

where

is a -vector mean zero Gaussian process indexed by with . Define the set of admissible values of when by . Define by

|

|

|

(21) |

The following proposition establishes the asymptotic null distribution of the LRTS.

Proposition 8.

Suppose Assumptions 1, 2, 4, 5, and 6 hold. Then, under the null hypothesis of , .

In Proposition 8, the LRTS and its asymptotic distribution depend on the choice of because . It is possible to develop a version of the EM test

(Chen and Li, 2009; Chen et al., 2012; Kasahara and Shimotsu, 2015) in this context that does not impose an explicit restriction on the parameter space for and ; however, we leave such an extension to future research.

6.2 Heteroscedastic normal distribution

Suppose that in the -th regime follows a normal distribution with regime-specific intercept and variance . We split into , and write the density of the -th regime as

|

|

|

(22) |

for some function . In many applications, is a linear function of and , e.g., . Consider the following reparameterization introduced in Kasahara and Shimotsu (2015) ( in Kasahara and Shimotsu corresponds to here):

|

|

|

(23) |

where , , , and , so that . Collect the reparameterized parameters, except for , into one vector . As in Section 6.1, we suppress the subscript from . Let the reparameterized density be

|

|

|

(24) |

Let , where and . Because the likelihood function of a normal mixture model is unbounded when (Hartigan, 1985), we impose for a small in . We proceed to derive the derivatives of evaluated at . , , and are the same as those given in (10) except for and that those with respect to are multiplied by . The higher-order derivatives of with respect to are derived by following Kasahara and Shimotsu (2015).

From Lemma 6 and the fact that normal density satisfies

|

|

|

|

(25) |

|

|

|

|

we have

|

|

|

(26) |

where

|

|

|

|

|

|

|

|

It follows from , (11), and elementary calculation that

|

|

|

|

(27) |

|

|

|

|

|

|

|

|

with . Hence, and are linearly dependent.

We proceed to derive a representation of in terms of . Repeating the calculation leading to (13)–(15) and using (27) gives the following. First, (13) and (14) still hold; second, the elements of except for the -th element are given by (15) after adjusting that the derivative with respect to must be multiplied by 2 (e.g., and ); third,

|

|

|

(28) |

When , is a non-degenerate random variable as in the non-normal case. When , however, becomes identically equal to 0, and indeed the first non-zero derivative with respect to is the fourth derivative.

Because of this degeneracy, we derive the asymptotic distribution of the LRTS by expanding four times. It is not correct, however, to simply approximate by a quadratic function of (and other terms) when and a quadratic function of when . This results in discontinuity at and fails to provide a valid uniform approximation. We establish a uniform approximation by expanding four times but expressing in terms of , , and other terms.

For , define . Then, we can write (28) as

|

|

|

(29) |

Note that satisfies and is non-degenerate even when . Define as in (16) but replacing with . Collect the relevant parameters as

|

|

|

(30) |

where

|

|

|

(31) |

with . Recall . Similarly to (18), define the elements of the generalized score by

|

|

|

(32) |

Define the generalized score as

|

|

|

(33) |

The following proposition establishes a uniform approximation of the log-likelihood ratio.

Assumption 7.

(a) for , where is given in (33). (b) .

Proposition 9.

Suppose Assumptions 1, 2, 4, 5, and 7 hold and the density of the -th regime is given by (22). Then, under the null hypothesis of , (a) ; and (b) for any ,

|

|

|

(34) |

The asymptotic null distribution of the LRTS is characterized by the supremum of , where and are defined analogously to those in (20) but with defined in (33), and the supremum is taken with respect to and under the constraint implied by the limit of the set of possible values of as . This constraint is given by the union of and , where , , and

|

|

|

|

(35) |

|

|

|

|

|

|

|

|

|

|

|

|

Note that depends on , whereas does not depend on . Heuristically, and correspond to the limits of the set of possible values of when and , respectively. When , we have because . Further, the set of possible values of converges to because can be arbitrarily small. Consequently, the limit of is characterized by .

Define and as in (20) but with defined in (33). Let and denote and evaluated at . Define and by

|

|

|

|

(36) |

|

|

|

|

The following proposition establishes the asymptotic null distribution of the LRTS.

Proposition 10.

Suppose that the assumptions in Proposition 9 hold. Then, under the null hypothesis of , .

6.3 Homoscedastic normal distribution

Suppose that in the -th regime follows a normal distribution with the regime-specific intercept but with common variance . We split and into and , and write the density of the -th regime as

|

|

|

(37) |

for some function . Consider the following reparameterization:

|

|

|

(38) |

where and . Collect the reparameterized parameters, except for , into one vector . Suppressing from , let the reparameterized density be

|

|

|

(39) |

Let ; then, the first and second derivatives of with respect to and are the same as those given in (10) except for . We derive the higher-order derivatives of with respect to . From Lemmas 6 and (25), we obtain

|

|

|

|

(40) |

|

|

|

|

where , , , , and

.

It follows from , (11), and elementary calculation that

|

|

|

|

(41) |

|

|

|

|

Repeating the calculation leading to (13)–(15) and using (41) gives the following. First, (13) and (14) still hold; second, the elements of are given by (15) except for the -th element; third, is given by (28). Further, Lemma 8 in the appendix shows that when , and . Because when and , we expand four times and express it in terms of , , , and other terms to establish a uniform approximation.

Collect the relevant parameters as

|

|

|

(42) |

Define the generalized score as

|

|

|

(43) |

where is defined as in (29), for , and

and are defined as in (32) but using the density (37) in place of (22).

Define, with and ,

|

|

|

|

(44) |

|

|

|

|

|

|

|

|

The following two propositions correspond to Propositions 9 and 10, establishing a uniform approximation of the log-likelihood ratio and asymptotic distribution of the LRTS.

Assumption 8.

for , where is given in (43).

Proposition 11.

Suppose Assumptions 1, 2, 4, 5, and 8 hold and the density of the -th regime is given by (37). Then, statements (a) and (b) of Proposition 9 hold.

Proposition 12.

Suppose that the assumptions in Proposition 11 hold. Then, under the null hypothesis of , , where and are defined as in (36) but in terms of constructed with defined in (43) and and defined in (LABEL:Lambda-lambda-homo).

7 Testing against for

In this section, we derive the asymptotic distribution of the LRTS for testing the null hypothesis of regimes against the alternative of regimes for general . We suppress the covariate unless confusion might arise.

Let denote the parameter of the -regime model, where contains for and , and . We assume and for identification.

The true -regime conditional density of given and is

|

|

|

(45) |

where with .

Let the conditional density of of an -regime model be

|

|

|

(46) |

where is defined similarly to with and . We assume that for some .

Write the null hypothesis as with

|

|

|

Define the set of values of that yields the true density (45) under as . Under , the -regime model (46) generates the true -regime density (45) if and the transition matrix of reduces to that of the true -regime model.

We reparameterize the transition probability of by writing as , where is point identified under , while is not point identified under . The transition probability of under equals the transition probability of under if and only if . The detailed derivation including the definition of is provided in Section 11.2.5 in the appendix.

Define the subset of that corresponds to as

|

|

|

|

|

|

|

|

then, holds.

For , let denote the -regime log-likelihood for a given initial distribution . We treat as fixed. Let and . The following proposition shows that the MLE is consistent in the sense that the distance between and tends to 0 in probability. The proof of Proposition 13 is essentially the same as the proof of Proposition 6 and hence is omitted.

Assumption 9.

(a) and are compact, and is in the interior of . (b) For all and all , is continuous in . (c) for all if and only if . (d) for all if and only if .

Proposition 13.

Suppose Assumptions 1, 2, and 9 hold. Then, under the null hypothesis of , and .

Let denote the LRTS for testing against .

We proceed to derive the asymptotic distribution of the LRTS by analyzing the behavior of the LRTS when for each . Define . Observe that if , then follows a two-state Markov chain on whose transition probability is characterized by and . Collect reparameterized into , where does not affect the transition probability of when . See Section 11.2.5 in the appendix for the detailed derivation.

Define ; then, we can write and as and . Because provides no information for distinguishing between and if , we can write and as

|

|

|

(47) |

7.1 Non-normal distribution

For non-normal component distributions, consider the following reparameterization similar to (8):

|

|

|

Collect the reparameterized identified parameters into one vector , where , so that the reparameterized -regime log-likelihood function is . Let denote the value of under . Define the reparameterized conditional density of as

|

|

|

|

where . Let denote . It follows from (47) and the law of iterated expectations that

|

|

|

|

(48) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where the second equality holds because if , and the last equality holds because, conditional on , is a two-state stationary Markov process with parameter .

Let , , and denote , , and . Let denote the derivative of evaluated at , and define and similarly. Repeating a derivation similar to (10)–(15) but using (48) in place of (12), we obtain

|

|

|

|

(49) |

|

|

|

|

|

|

|

|

|

|

|

(50) |

|

|

|

|

|

|

(51) |

Define , define as in (17) by replacing with , and let

|

|

|

(52) |

and , where is defined similarly to (18) as

|

|

|

|

(53) |

|

|

|

|

Similarly to (20), define

|

|

|

|

(54) |

|

|

|

|

|

|

|

|

where is an -vector mean zero Gaussian process with

. Note that corresponds to the residuals from projecting on . Define by

|

|

|

The following proposition gives the asymptotic null distribution of the LRTS. Under the stated assumptions, the log-likelihood function permits a quadratic approximation in the neighborhood of similar to the one in Proposition 7. Define . Under , for any , for , and uniformly in and ,

|

|

|

where and . Consequently, the LRTS is asymptotically distributed as the maximum of the random variables, each of which represents the asymptotic distribution of the LRTS that tests . Denote the parameter space for by , and let .

Assumption 10.

for , where is given in (52).

Proposition 14.

Suppose Assumptions 1, 2, 4, 9, and 10 hold. Then, under , .

7.2 Heteroscedastic normal distribution

As in Section 6.2, we assume that in the -th regime follows a normal distribution with the regime-specific intercept and variance of which density is given by (22). Consider the following reparameterization similar to (23):

|

|

|

where , , , and . As in Section 7.1, we collect the reparameterized identified parameters into , where and . Similar to (24), define the reparameterized conditional density of as

|

|

|

|

|

|

|

|

Let , , , and denote , , , and . From (26) and a derivation similar to (48), we obtain the following result that corresponds to (27) in testing homogeneity:

|

|

|

|

(55) |

|

|

|

|

|

|

|

|

Repeating the calculation leading to (49)–(51) and using (55) gives the following. First, (49) and (50) still hold; second, the elements of except for the -th element are given by (51) while adjusting the derivative with respect to by multiplying by 2; third,

|

|

|

For , define . Similarly to (32), define the elements of the generalized score as

|

|

|

|

(56) |

|

|

|

|

Similarly to (33), define as in (52) by redefining in (52) as

|

|

|

(57) |

Define and as in (54) with defined in (57). Let and denote and evaluated at . Define as in (LABEL:Lambda-lambda), and define as in (LABEL:Lambda-lambda) by replacing with . Similar to (36), define and by and , where and .

The following proposition establishes the asymptotic null distribution of the LRTS. As in the non-normal case, the LRTS is asymptotically distributed as the maximum of the random variables.

Assumption 11.

Assumption 10 holds when is given in (57).

Proposition 15.

Suppose Assumptions 1, 2, 4, 9, and 11 hold and the component density of the -th regime is given by (22). Then, under ,

.

7.3 Homoscedastic normal distribution

As in Section 6.3, we assume that in the -th regime follows a normal distribution with the regime-specific intercept and common variance whose density is given by (37).

The asymptotic distribution of the LRTS is derived by using a reparameterization

|

|

|

similar to (38) and following the derivation in Sections 6.3 and 7.2. For brevity, we omit the details of the derivation. Define as in (53), and denote each element of as

|

|

|

Similarly to (43), define as in (52) by redefining in (52) as

|

|

|

(58) |

where for .

The following proposition establishes the asymptotic null distribution of the LRTS.

Assumption 12.

Assumption 10 holds when is given in (58).

Proposition 16.

Suppose Assumptions 1, 2, 4, 9, and 12 hold and the component density of the -th regime is given by (37). Then, under , , where and are defined as in Proposition 15 but in terms of constructed with given in (58) and and defined as in (LABEL:Lambda-lambda-homo) but replacing with .