Nonparametric method for sparse conditional density estimation in moderately large dimensions

Abstract: In this paper, we consider the problem of estimating a conditional density in moderately large dimensions. Much more informative than regression functions, conditional densities are of main interest in recent methods, particularly in the Bayesian framework (studying the posterior distribution, finding its modes…). Considering a recently studied family of kernel estimators, we select a pointwise multivariate bandwidth by revisiting the greedy algorithm Rodeo (Regularisation Of Derivative Expectation Operator). The method addresses several issues: being greedy and computationally efficient by an iterative procedure, avoiding the curse of high dimensionality under some suitably defined sparsity conditions by early variable selection during the procedure, converging at a quasi-optimal minimax rate.

Keywords: conditional density, high dimension, minimax rates, kernel density estimators, greedy algorithm, sparsity, nonparametric inference.

1 Introduction

1.1 Motivations

In this paper, we consider the problem of the conditional density estimation.

We observe a -sample of a couple , in which is the vector of interest while gathers auxiliary variables. We denote the joint dimension. In particular we are interested in the inference of the -dimensional conditional density of conditionally to .

There is a growing demand for methods of conditional density estimation in a wide spectrum of applications such as Economy[Hall et al., 2004], Cosmology [Izbicki and Lee, 2016], Medicine [Takeuchi et al., 2009], Actuaries [Efromovich, 2010b ], Meteorology [Jeon and Taylor, 2012] among others. It can be explained by the double role of the conditional density estimation: deriving the underlying distribution of a dataset and determining the impact of the vector of auxiliary variables on the vector of interest .

In this aspect, the conditional density estimation is richer than both the unconditional density estimation and the regression problem.

In particular, in the regression framework, only the conditional mean are estimated instead of the full conditional density, which can be especially poorly informative in case of an asymmetric or multi-modal conditional density.

Conversely, from the conditional density estimators, one can, e.g., derive the conditional quantiles [Takeuchi et al., 2006] or give accurate predictive intervals [Fernández-Soto et al., 2002].

Furthermore, since the posterior distribution in the Bayesian framework is actually a conditional density, the present paper also offers an alternative method to the ABC methodology (for Approximate Bayesian Computation) [Beaumont et al., 2002 ; Marin et al., 2012 ; Biau et al., 2015] in the case of an intractable-yet-simulable model.

The challenging issue in conditional density estimation is to circumvent the ”curse of dimensionality”.

The problem

is twofold: theoretical and practical.

In theory, it is stigmatized by the minimax approach, stating that in a -dimensional space the best convergence rate for the pointwise risk over a -regular class of functions is : in particular, the larger is , the slower is the rate.

In practice, the larger the dimension is, the larger the sample size is needed to control the estimation error.

In order to maintain reasonable running times in moderately large dimensions, methods have to be designed especially greedy.

Furthermore, one interesting question is how to retrieve the eventual relevant components in case of sparsity structure on the conditional density

. For example, if we have at disposal plenty of auxiliary variables without any indication on their dependency with our vector of interest , the ideal procedure will take in input the whole dataset and still achieve a running time and a minimax rate as fast as if only the relevant components were given and considered for the estimation. More precisely, two goals are simultaneously addressed : converging at rate with the relevant dimension, i.e. the number of components that influence the conditional density , and

detect the irrelevant components at an early stage of the procedure in order to afterwards only work on the relevant data and thus speed up the running time.

1.2 Existing methodologies

Several nonparametric methods have been proposed to estimate conditional densities: kernel density estimators [Rosenblatt, 1969 ; Hyndman et al., 1996 ; Bertin et al., 2016] and various methodologies for the selection of the associated bandwidth [Bashtannyk and Hyndman, 2001 ; Fan and Yim, 2004 ; Hall et al., 2004]; local polynomial estimators [Fan et al., 1996 ; Hyndman and Yao, 2002]; projection series estimators [Efromovich, 1999; 2007]; piecewise constant estimator [Györfi and Kohler, 2007 ; Sart, 2017]; copula [Faugeras, 2009].

But while most of the aforementioned works are only defined for bivariate data or at least when either or is univariate, they are also computationally intractable as soon as .

It is in particular the case for the kernel density methodologies (Hall, Racine ,Li 2004, Bertin et al. 2016): they achieve the optimal minimax rate, and even the detection of the relevant components, thanks to an adequate choice of the bandwidth (for the two aforementioned methods by cross validation and Goldenshluger-Lepski methodology), but the computational cost of these bandwidth selections is prohibitive even for moderate sizes of and . To the best of our knowledge, only two kernel density methods have been proposed to

handle large datasets.

[Holmes et al., 2010] propose a fast method of approximated cross-validation, based on a dual-tree speed-up, but they do not establish any rate of convergence and only show the consistency of their method.

For scalar , [Fan et al., 2009] proposed to perform a prior step of dimension reduction on to bypass the curse of dimensionality, then they estimate the bivariate approximated conditional density by kernel estimators. But the proved convergence rate is not the optimal minimax rate for the estimation of a bivariate function of assumed regularity . Moreover, the step of dimension reduction restricts the dependency of to a linear combination of its components, which may induce a significant loss of information.

Projection series methods for scalar have also been proposed.

[Efromovich, 2010a ] extends his previous work [Efromovich, 2007]

to a multivariate . Theoretically the method achieves an oracle inequality, thus the optimal minimax rate. Moreover it performs an automatic dimension reduction on when there exists a smaller intrinsic dimension.

To our knowledge, it is the only method which addresses datasets of dimension larger than with reasonable running times and does not pay its numerical performance with non optimal minimax rates. However the computation cost is prohibitive when both and are large.

More recently, Izbicki and Lee have proposed two methodologies using orthogonal series estimators [Izbicki and Lee, 2016; 2017].

The first method is particularly fast and can handle very large (with more than covariates). Moreover the convergence rate adapts to an eventual smaller unknown intrinsic dimension of the support of the conditional density. The second method originally proposes to convert successful high dimensional regression methods into the conditional density estimation, interpreting the coefficients of the orthogonal series estimator as regression functions, which allows to adapt to all kind of figures (mixed data, smaller intrinsic dimension, relevant variables) in function of the regression method. However both methods converge slower than the optimal minimax rate. Moreover their optimal tunings depend in fact on the unknown intrinsic dimension.

For multivariate and , [Otneim and Tjøstheim, 2017] propose a new semiparametric method, called Locally Gaussian Density Estimator: they rewrite the conditional density as a product of a function depending on the marginal distribution functions (easily estimated since univariate, then plug-in), and a term which measures the dependency between the components, which is approximated by a centred Gaussian whose covariance is parametrically estimated. Numerically, the methodology seems robust to addition of covariates of independent of , but it is not proved. Moreover they only establish the asymptotic normality of their method.

1.3 Our strategy and contributions

The challenge in this paper is to handle large datasets, thus we assume at our disposal a sample of large size and of moderately large dimension. Then our work is motivated by the following three objectives:

-

(i)

achieving the optimal minimax rate (up to a logarithm term);

-

(ii)

being greedy, meaning that the procedure must have reasonable running times for large and moderately large dimensions, in particular when ;

-

(iii)

adapting to a potential sparsity structure of . More precisely, in the case where locally depends only on a number of its components, can be seen as the local relevant dimension. Then the desired convergence rate has to adapt to the unknown relevant dimension : under this sparsity assumption, the benchmark for the estimation of a -regular function is to achieve a convergence rate of the order , which is the optimal minimax rate if the relevant components were given by an oracle.

Our strategy is based on kernel density estimators. The considered family has been recently introduced and studied in [Bertin et al., 2016]. This family is especially designed for conditional densities and

is better adapted for the objective (iii) than the intensively studied estimator built as the ratio of a kernel estimator of the joint density over one of the marginal density of . For example, a relevant component for the joint density and the marginal density of may be irrelevant for the conditional density and it is the case if a component of is independent of . Note though that many more cases of irrelevance exist since we define the relevance as a local property.

The main issue with kernel density estimators is the selection of the bandwidth , and in our case, we also want to complete the objective (ii), since the pre-existing methodologies of bandwidth selection does not satisfy this restriction and thus cannot handle large datasets. In this paper, it is performed by an algorithm we call CDRodeo, which is derived from the algorithm Rodeo [Lafferty and Wasserman, 2008 ; Liu et al., 2007], which has respectively been applied for the regression and the unconditional density estimation. The greediness of the algorithm allows us to address datasets of large sizes while keeping a reasonable running time (see Section 3.5 for further details). We give a simulated example with a sample of size and of dimension in Section 4. Moreover, Rodeo-type algorithms ensure an early detection of irrelevant component, and thus achieve the objective (iii) while improving the objective (ii).

From the theoretical point of view, if the regularity of is known, our method achieves an optimal minimax rate (up to a logarithmic factor), which is adaptive to the unknown sparsity of . The last property is mostly due to the Rodeo-type procedures. The improvement of our method in comparison to the paper [Liu et al., 2007] which estimates the unconditional density with Rodeo is twofold.

First, our result is extended to any regularity , whereas [Liu et al., 2007] fixed .

Secondly, our notion of relevance is both less restrictive and more natural. In [Liu et al., 2007], they studied the -risk of their estimator, therefore they have to consider a notion of global relevance, whereas we consider a pointwise approach, which allows us to define a local property of relevance, which can be applied to a broader class of functions. Moreover, their notion of relevance is not intrinsic to the unknown density, but in fact depends on a tuning of the method, a prior chosen baseline density which has no connexion with the density, which limits the interpretation of the relevance.

1.4 Overview

Our paper is organized as follows. We introduce the CDRodeo method in Section 2. The theoretical results are in Section 3, in which we specify the assumptions and the tunings of the procedure from which are derived the convergence rate and the complexity cost of the method. A numerical example is presented in Section 4. The proofs are in the last section.

2 CDRodeo method

Let be a sample of a couple of multivariate random vectors: for ,

with valued in and in . We denote the joint dimension.

We assume that the marginal distribution of and the conditional distribution of given are absolutely continuous with respect to the Lebesgue measure, and we define such as for any , is the conditional density of conditionally to . We denote the marginal density of .

Our method estimates pointwisely : let us fix the point of interest.

Kernel estimators.

Our method is based on kernel density estimators. More specifically, we consider the family proposed in [Bertin et al., 2016], which is especially designed for the conditional density estimation. Let be a kernel function, ie: , then for any bandwidth , the estimator of is defined by:

| (1) |

where is an estimator of , built from another sample of . We denote by the sample size of . The choices of and are specified later (see section 3.2).

Bandwidth selection.

In kernel density estimation, selecting the bandwidth is a critical choice which can be viewed as a bias-variance trade-off. In [Bertin et al., 2016], it is performed by the Goldenshluger-Lepski methodology (see [Goldenshluger and Lepski, 2011]) and requires an optimization over an exhaustive grid of couples of bandwidths, which leads to intractable running time when the dimension exceeds (and large dataset).

That is why we focus in a method which excludes optimization over an exhaustive grid of bandwidths to rather propose a greedy algorithm derived from the algorithm Rodeo.

First introduced in the regression framework [Wasserman and Lafferty, 2006 ; Lafferty and Wasserman, 2008], a variation of Rodeo was proposed in [Liu et al., 2007] for the density estimation. Our method we called CDRodeo (for Conditional Density Rodeo) addresses the more general problem of conditional density estimation.

Like Rodeo (which means Regularisation Of Derivative Expectation Operator), the CDRodeo algorithm generates an iterative path of decreasing bandwidths, based on tests on the partial derivatives of the estimator with respect to the components of the bandwidth.

Note that the greediness of the procedure leans on the selection of this path of bandwidths, which enables us to address high dimensional problems of functional inference.

Let us be more precise: we take a kernel of class and consider the statistics for and , defined by:

is easily computable, since it can be expressed by:

| (2) |

where is the function defined by:

| (3) |

-

1.

Input: the point of interest , the data , the bandwidth decreasing factor, the bandwidth initialization value, a parameter .

-

2.

Initialization:

-

(a)

Initialize the bandwidth: for , .

-

(b)

Activate all the variables: .

-

(a)

-

3.

While () & ():

-

for all :

-

(a)

Update and .

-

(b)

If : update .

else: remove from .

-

(a)

-

-

4.

Output: (and ).

The details of the CDRodeo procedure are described in Algorithm 1 and can be summed up in one sentence: for a well-chosen threshold (specified in Section 3.3), the algorithm performs at each iteration the test to determine if the component of the current bandwidth must be shrunk or not. It can be interpreted by the following principle: the bandwidth of a kernel estimator quantifies within which distance of the point of interest and at which degree an observation helps in the estimation. Heuristically, the larger the variation of is, the smaller the bandwidth is required for an accurate estimation. The statistics are used as a proxy of to quantify the variation of in the direction . Note in particular that since the partial derivatives vanish for irrelevant components, this bandwidth selection leads to an implicit variable selection, and thus to avoid the curse of dimensionality under sparsity assumptions.

3 Theoretical results

This section gathers the theoretical results of our method.

3.1 Assumptions

We consider a compactly supported kernel. For any bandwidth , we define the neighbourhood of (typically, or , and or ) as follows:

Then we denote the CDRodeo initial bandwidth and for short, .

We also introduce the notation for the supremum norm over a set .

The following first assumption ensures a certain amount of observations in the neighbourhood of our point of interest .

Assumption 1 ( bounded away of ).

We assume .

Note that if the neighbourhood does not contain any observation , the estimation of the conditional distribution of given the event is obviously intractable.

The second assumption specifies the notions of ”sparse function” and ”relevant component”, under which the curse of high dimensionality can be avoided.

Assumption 2 (Sparsity condition).

There exists a subset such that for any fixed , the function is constant on .

In other words, if we denote the cardinal of , Assumption 2 means that locally depends on only of its variables. We call relevant any component in .

The notion of relevant component depends on the point where is estimated. For example, a component which behaves as in the conditional density is only relevant in the neighbourhood of and .

Note that this local property addresses a broader class of functions, which extends the application field of Theorem 2 and improves the convergence rate of the method.

Finally, the conditional density is required to be regular enough.

Assumption 3 (Regularity of ).

There exists a known integer such that is of class on and such that for all .

3.2 Conditions on the estimator of

Given the definition of the estimator (1), we need an estimator of .

If is known.

We take . This case is not completely obvious. In particular, it tackles the case of unconditional density estimation, if we set by convention and .

If is unknown.

We need an estimator which satisfies the following two conditions:

-

(i)

a positive lower bound:

-

(ii)

a concentration inequality in local sup norm: there exists a constant such that:

The following proposition proves these conditions are feasible. Furthermore, the provided estimator of (see the proof in Section 5.3.1) is easily implementable and does not need any optimisation.

3.3 CDRodeo parameters choice.

Kernel .

We choose the kernel function of class , with compact support and of order , i.e.: for , , and .

Note that considering a compactly supported kernel is fundamental for the local approach. In particular, it relaxes the assumptions by restricting them to a neighbourhood of .

Taking a kernel of order is usual for the control of the bias of the estimator.

Parameter .

Let be the decreasing factor of the bandwidth. The larger , the more accurate the procedure, but the longer the computational time. From the theoretical point of view, it remains of little importance, as it only affects the constant terms. In practice, we set it close to .

Bandwidth initialization.

We recall that we set (and the initial bandwidth as ).

Threshold .

For any bandwidth and for , we set the threshold as follows:

| (4) |

with (where is defined in (3)) and . The expression is obtained by using concentration inequalities on . For the proof, the parameter has to be tuned such that:

| (5) |

which is satisfied for large enough. The influence of this parameter is discussed in the next section, once the theoretical results are stated.

Hereafter, unless otherwise specified, the parameters are chosen as described in this section.

3.4 Mains results

Let us denote the bandwidth selected by CDRodeo.

In Theorem 2, we introduce a set of bandwidths which contains with high probability, which leads to an upper bound of the pointwise estimation error with high probability.

In 3, we deduce the convergence rate of CDRodeo from Theorem 2.

More precisely, in Theorem 2, we determine lower and upper bounds (with high probability) for the stopping iteration of each bandwidth component. We set:

| (6) |

and

| (7) |

where

Then we define the set of bandwidths by:

Theorem 2.

Assume that satisfies Conditions (i) and (ii) of section 3.2 and Assumptions 1, 3 and 2 are satisfied. Then, the bandwidth selected by CDRodeo belongs to with high probability. More precisely, for any and for large enough:

| (8) |

Moreover, with probability larger than , the CDRodeo estimator verifies:

| (9) |

with

Corollary 3.

Under the assumptions of Theorem 2, for any :

3 presents a generalization of the previous works on Rodeo [Lafferty and Wasserman, 2008] and [Liu et al., 2007] whose results are restricted to the regularity and to simpler problems, namely regression and density estimation.

We compare the convergence rate of CDRodeo with the optimal minimax rate. In particular, our benchmark is the pointwise minimax rate, which is of order , for the problem of -regular -dimensional density estimation, obtained by [Donoho and Low, 1992].

Without sparsity structure (), CDRodeo achieves the optimal minimax rate, up to a logarithmic factor.

The exponent of this factor depends on the parameter . For the proofs, we need in order to satisfy (5), but if an upper bound (or a pre-estimator) of were known, we could obtain the similar result with and a modified constant term. Note that the logarithmic factor is a small price to pay for a computationally-tractable procedure for high-dimensional functional inference, in particular see section 3.5 for the computational gain of our procedure.

Under sparsity assumptions, we avoid the curse of high dimensionality and our procedure achieves the desired rate (up to a logarithmic term), which is optimal if the relevant components were known. Note that some additional logarithmic factors could be unavoidable due to the unknown sparsity structure, which needs to be estimated. Identifying the exact order of the logarithm term in the optimal minimax rate for the sparse case remains an open challenging question.

3.5 Complexity

We now discuss the complexity of CDRodeo

without taking into account the pre-computation cost of at the points , (used for computing the ), but a fast procedure for is required, to avoid losing CDRodeo computational advantages.

For CDRodeo, the main cost lies in the computation of the ’s along the path of bandwidths.

The condition restricts to at most updates of the bandwidth across all components, leading to a worst-case complexity of order .

But as shown in Theorem 2, with high probability, , in which only the relevant components are active after the first iteration. In first iteration, the ’s computation costs operations, while the product kernel enables us to compute the ’s in following iteration with only operations, which leads to the complexity .

In order to grasp the advantage of CDRodeo greediness, we compare its complexity with optimization over an exhaustive bandwidth grid with values for each component of the bandwidth (which is often the case in others methods: Cross validation, Lepski methods…): for each bandwidth of -sized grid, the computation of a statistic from the -sized dataset needs at least operation, which leads to a complexity of order . Using the parameters used in the simulated example in section 4 (, , , ), the ratio of complexities is , and even without sparsity structure: . It means that CDRodeo run is a billion times faster on this data set.

4 Simulations

In this section, we test the practical performances of our method. In particular, we study CDRodeo on a 5-dimensional example. The major purpose of this section is to assess if the numerical performances of our procedure. Let us describe the example. We set and and simulate an i.i.d sample with the following distribution: for any :

-

-

the first component of follows a uniform distribution on ,

-

-

the other components , , are independent standard normal and are independent of ,

-

-

is independent of , and and the conditional distribution of given is exponential with survival parameter .

The estimated conditional density function is then defined by:

This example enables us to test several criteria: sparsity detection, behaviour when fonctions are not continuous, bimodality estimation, robustness when takes small values.

In the following simulations, if not stated explicitly otherwise, Rodeo is run with sample size , product Gaussian kernel, initial bandwidth value , bandwidth decreasing factor and parameter and .

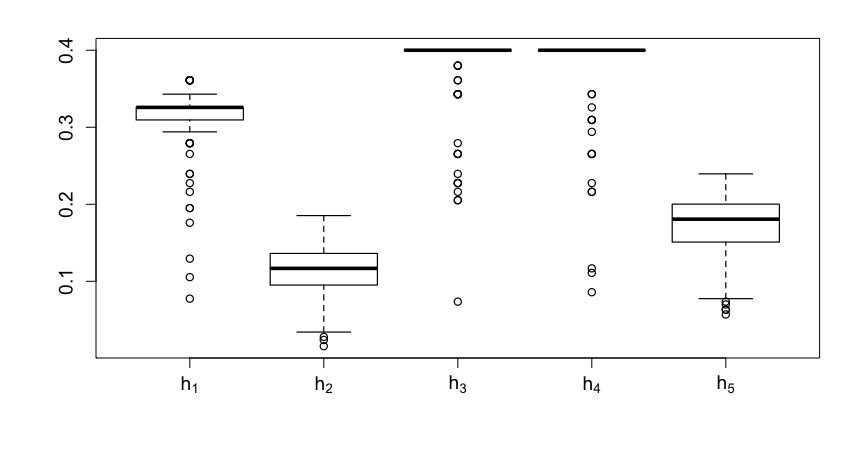

Figure 1 illustrates CDRodeo bandwidth selection. In which, the boxplots of each selected bandwidth component are built from 200 runs of CDRodeo at the point . This figure reflects the specificity of CDRodeo to capture the relevance degree of each component, and

one could compare it with variable selection (as done in [Lafferty and Wasserman, 2008]).

The components and are irrelevant and for this point of interest, the components and are clearly relevant while the component is barely relevant as is constant in the direction in near neighbourhood of . As expected, the irrelevant and are mostly deactivated at the first iteration, while the relevant and are systematically shrunk. The relevance degree of is also well detected as the values of are smaller than , but significantly larger than and .

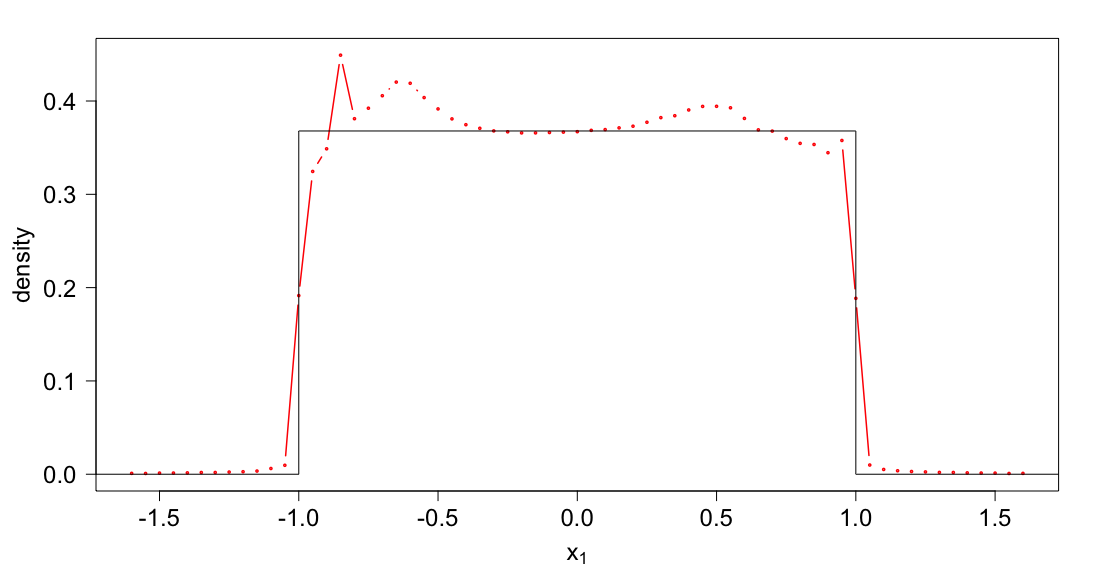

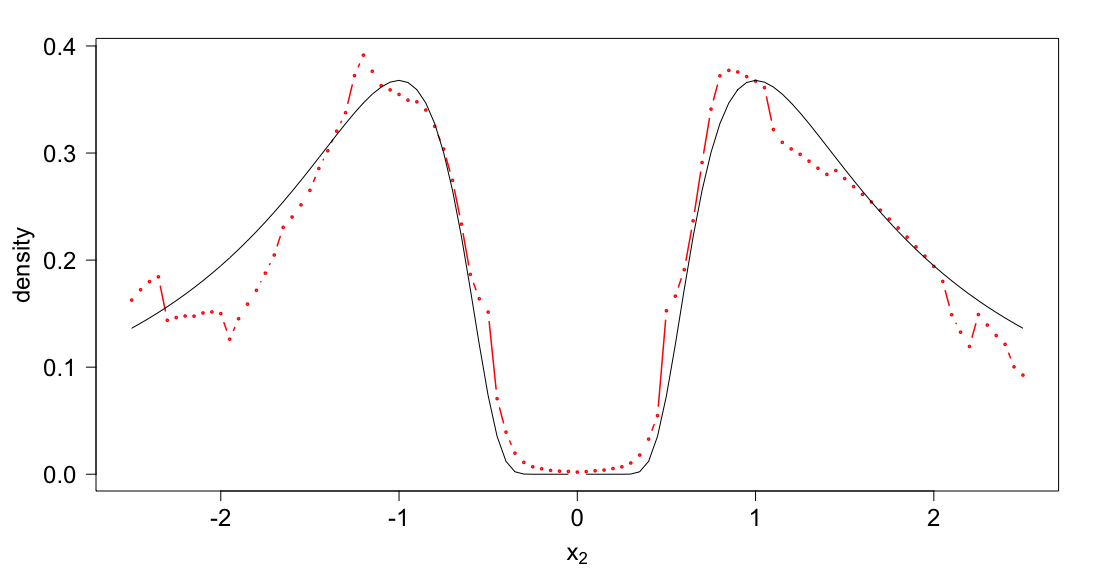

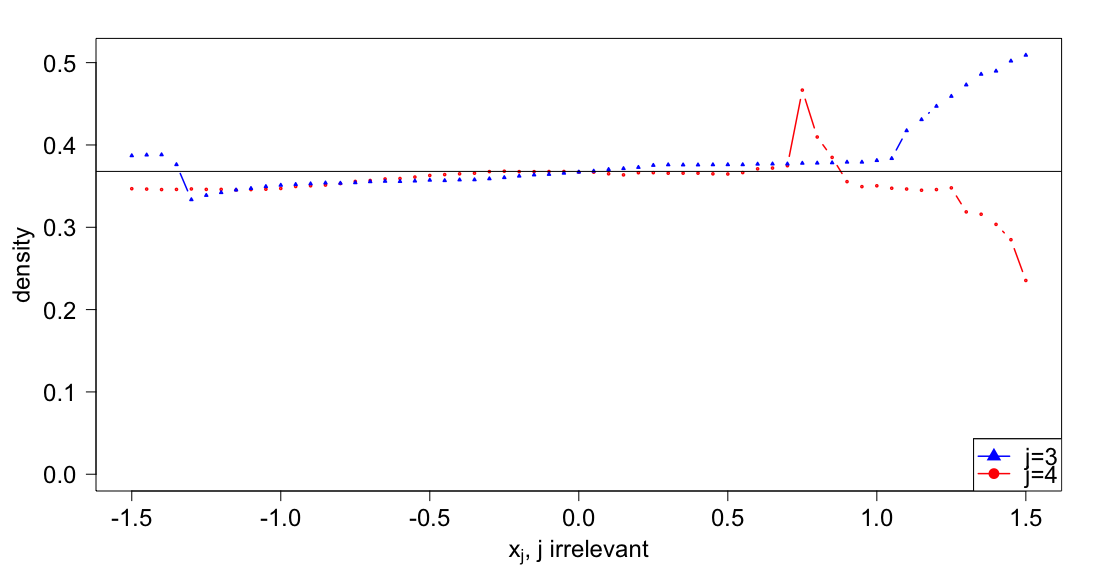

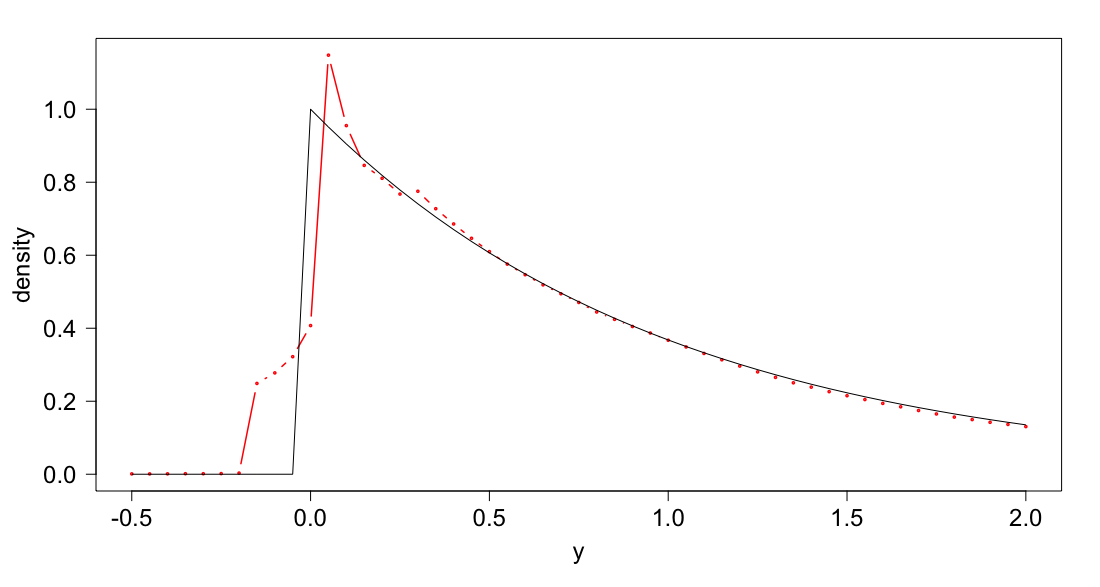

Figure 2 gives CDRodeo estimation of from one -sample. The function is well estimated. In particular, irrevance, jumps and bi-modality are features which are well detected by our method. As expected, main estimation errors are made on points of discontinuity for and or at the boundaries for , and . Note that the values are particularly small at the boundaries of the plots in function of , leading to lack of observations for the estimation. Note however that null value for does not deteriorate the estimation (cf top left plot), since the estimate of vanishes automatically when there is no observation near the point of interest.

Running time.

The simulations are implemented in R on a Macintosh laptop with a GHz Intel Core i7 processor. In the Figure Figure 1, the runs of CDRodeo take seconds (around minutes), or seconds per run.

5 Proofs

We first give the outlines of the proofs in Section 5.1. To facilitate the lecture of the proof, we have divided the proofs of the main results (Proposition 1, Theorem 2 and 3) into intermediate results which are stated in Section 5.2 and proved in Section 5.4. The proof of the main results are in Section 5.3.

5.1 Outlines of the proofs

We first prove Proposition 1 by constructing an estimator of with the wanted properties. In this proof, we use some usual properties of a kernel density estimator (control of the bias, concentration inequality), which are gathered in Lemma 4.

Theorem 2 states two results: the bandwidth selection (8) and the estimation error of the procedure (9).

For the proof of the bandwidth selection (8), Proposition 8 mades explicit the highly probable behaviour of CDRodeo along a run, and thus the final selected bandwidth. In particular, the proof leans on an analysis of , which is made in two steps. We first consider , a simpler version of in which we substitute the estimator of by itself, and we detail its behaviour in Lemma 6. Then we control the difference (see in 1. of Lemma 7) to ensure behaves like .

To control the estimation error of the procedure (9), we similarly analyse in two parts: in Lemma 5, we describe the behaviour of , the simpler version of in which we substitute the estimator of by itself, and in 2. of Lemma 7, we bound the difference . Then the bandwidth selection (8) leads to the upper bound with high probability of the estimation error of (9).

Finally, we obtain the expected error of stated in 3 by controlling the error on the residual event.

5.2 Intermediate results

For any bandwidth , we define the kernel density estimator by: for any ,

| (10) |

where a kernel which is compactly supported, of class ,

of order where we recall that is defined by .

We also introduce the neighbourhood

| (11) |

Lemma 4 ( behaviour).

We assume is on with , then for any bandwidth ,

-

1.

if we denote , then

-

2.

If the condition

is satisfied, then for and for any :

Lemma 5 ( behaviour).

For any bandwidth , and any , let us denote . Then, if is chosen as in section 3.3, under Assumptions 3, 2 and 1,

-

1.

Let . Then

Besides, if we denote the bias of , then:

with .

-

2.

Let , where with . If Cond(): is satisfied, then:

-

3.

Let . Then

with .

Lemma 6 ( behaviour).

For any and any bandwidth , we define , and . If is chosen as in section 3.3, and under Assumptions 1, 3 and 2,

-

1.

Under Assumptions 1, 3 and 2, for :

whereas, for , for large enough,

(12) where .

Besides, let . Then :(13) - 2.

- 3.

Lemma 7.

For any and any component , we denote and . Under Assumptions 2, 3 and 1, if the conditions on are satisfied (see section 3.2), then,

-

1.

for :

-

2.

for :

We introduce the notation , , the state of the bandwidth at iteration if . In particular for a fixed , is identical for any . Then we consider the event:

where we denote .

Proposition 8 (CDRodeo behaviour).

Under Assumptions 1, 3 and 2, on , .

In other words, when happens:

-

1.

non relevant components are deactivated during the iteration ;

-

2.

at the end of the iteration , the active components are exactly the relevant ones;

-

3.

CDRodeo stops at last at the iteration .

Moreover, for any :

The following lemma give a technical result to canonically obtain an upper bound of the bias of a kernel estimator. Let us denote the multiplication terms by terms of two vectors.

Lemma 9.

Let and a bandwidth . For , let be a continuous function with compact support and with at least zero moments, ie: for ,

Let a function of class on . Then:

| (14) |

where

with the notations and (where is the canonical basis of ), and

Finally, we recall (without proof) the classical Bernstein’s Inequality and Taylor’s theorem with integral remainder.

Lemma 10 (Bernstein’s inequality).

Let be independent random variables almost surely uniformly bounded by a positive constant and such that for , . Then for any ,

Note that this version is a simple consequence of Birgé and Massart (p.366 of [Birgé and Massart, 1998]).

Lemma 11 (Taylor’s theorem).

Let be a function of class . Then we have:

5.3 Proofs of Proposition 1, Theorem 2 and 3

5.3.1 Proof of Proposition 1

We construct in two steps: we first construct an estimator which satisfies

| (15) |

then we show that if we set , satisfies Conditions (i) and (ii) for large enough.

We take as the kernel density estimator defined in(10), with a kernel that is compactly supported, of class , of order .

and a bandwidth specified later.Let us control the bias .

We define . In particular, is of class and has zero moments.

Therefore we can apply Lemma 4 :

where .

Therefore, since

we have for any threshold :

| (16) |

Therefore, we have reduced the problem to a local concentration inequality of in sup norm. In order to move from a supremum on to a maximum on a finite set of elements of , let us construct a -net of . We denote such that:

We set the smallest integer such that i.e.:

then we introduce the notation , for a multi-index defined, such that the component of is:

Then

is a -net of , in the meaning that for any , there exists such that .

Therefore to obtain the desired concentration inequality, we only need to obtain the concentration inequality for each point of and to control the following supremum

For this purpose, we obtain (from Taylor’s Inequality): for any ,

Therefore, for any :

Since is a -net of :

Thus:

And so:

We denote . Then:

Then the inequality (16) becomes: for any threshold ,

| (17) |

We want to apply 2. of Lemma 4. Therefore we fix the following settings:

-

•

-

•

, where is the threshold in 2. of Lemma 4;

-

•

.

For short, we denote , so:

In particular, since we take and we assume , then . Hence we obtain for large enough:

and also, since :

Thus:

and the inequality (17) becomes:

| (18) |

We verify that is satisfied for large enough:

Then we can apply 2. of Lemma 4,

Thus the inequality (18) becomes:

| (19) |

Let us control :

Then for large enough:

Therefore:

Since , we have obtained the desired concentration inequality (15) with .

Now we consider . By construction, satisfies Condition (i).

Let us show it also satisfies Condition (ii), i.e.:

We write:

Since , , we obtain from the previously proved concentration inequality (15):

5.3.2 Proof of Theorem 2

We introduce and denote . On , belongs to (cf Proposition 8). Thus:

| (20) |

For any , we denote and , and we decompose the loss as follows:

| (21) |

Using Lemma 7, since :

| (22) |

Moreover, by Lemma 5, since :

| (23) | ||||

| (24) |

And, also:

| (25) |

To conclude,

with for large enough (ie: ),

It remains to give an upper bound on . For any :

using Lemma 5, since for any , Cond() is satisfied. Moreover:

for large enough. Hence:

for large enough, since is finite.

5.3.3 Proof of 3

We consider the event for which we proved in Theorem 2:

for any . For short, we denote for any bandwidth . Then we decompose as follows:

By definition of , we immediately obtain:

| (26) |

For the second term, we first bound a.s. In CDRodeo procedure, the loop stops when the current bandwidth becomes too small: . So the final bandwidth satisfies:

Since ,

Hence:

Therefore, for any , using :

| (27) |

for any (since ).

We conclude by combining (26) and (27):

| (28) |

5.4 Proof of Proposition 8 and the lemmas

5.4.1 Proof of Proposition 8

First, note that the final state of the bandwidth determines exactly at which iteration each component has been deactivated: for a fixed bandwidth ,

if , we denote such as for , . In particular, is the iteration of deactivation of the component .

We introduce the notation , , the state of the bandwidth at iteration if .

It implies that is exactly defined by:

for .

Notice that for a fixed , is identical for any : by definition of , if , else .

We recall the definition

For any component and any bandwidth , we decompose as follows:

| (29) |

- 1.

-

2.

Let us show that implies that the relevant components remain active until iteration .

It suffices to prove , for any and any bandwidth , . (Indeed, by induction: , and since the irrelevant components deactivate at the iteration 0, if the current bandwidth at the iteration is , then the fact that all the relevant components remain active for this bandwidth implies that the bandwidth at iteration is ).Let us fix , and we denote . Using the decomposition (29), we obtain the following lower bound:

Then, combining:

we obtain:

Now let us show:

First, if is large enough (ie ), thenThen it suffices to prove:

i.e.:

It is ensured for , by definition of in (6):

(30) Therefore, on , the component remains active until the iteration .

-

3.

Let us now prove that on , each relevant component deactivates at last at iteration . In particular, by definition of , belongs to on .

Assume happens.

We fix . It suffices to prove that if is still active at iteration , then on happens, it deactivates at the end of this iteration. We assume is still active and we denote the state of the bandwidth at iteration .By the first point, for any , .

Given the second point, each relevant component was still active at the beginning of the iteration , ie: for any , .

Moreover, since is still active, . Let us prove that: . Using the decomposition (29):Using the points 1. and 2. of Lemma 6 and 1. Lemma 7, since :

Given the specific form of :

Moreover, for large enough:

Therefore:

In other words, when happens, any active component at iteration deactivates.

So we have proved that on , .

It remains to show that holds with high probability.

By choice of :

We want to apply 2. and 3. of Lemma 6 for any and any with . These bandwidths satisfy:

which ensures that for large enough, and hold for any and any . Note in particular that ).

Therefore, for any component ,

and for any and any ,

To conclude, note that is finite, so for any :

by definition .

5.4.2 Proof of Lemma 4

-

1.

We control the bias . We write for any :

The kernel is of order and is assumed of class on , with in particular , then we can apply Lemma 9 with the settings , , , , and for , . We obtain:

(31) with

Let us control . First we write:

Therefore:

Hence:

Then:

(32) Besides, is of order and and so:

Therefore the terms vanish in the equation (31), and with the upper bound of (32), we obtain:

with .

- 2.

5.4.3 Proof of Lemma 5

-

1.

We recall the notation for the multiplication terms by terms of two vectors. Then:

Now let us give an upper bound on the bias of :

since . Then we apply the Lemma 9 with the settings , , , , and . We obtain:

where

Notice that for , for any , thus and vanish. Therefore:

Now let us give an equivalent of the bias. First, using Assumption 3, for any , we can define the modulus of continuity of on by:

Then we decompose as follows:

with such that:

(33) since

- 2.

- 3.

5.4.4 Proof of Lemma 6

-

1.

First, we write more explicitly: for any bandwidth , any observation and any direction ,

where we recall is the function .

Note then that the support of is included in the support of , and by integration by part, we obtain for any :(37) In particular, since is of order , for , and .

We recall the notation for the multiplication terms by terms of two vectors. Using Assumption 2, if , for any . Thus we obtain:Therefore for .

Now, we deal with the case . Let us fix . We denote (with the canonic basis of ). Then we write:Then for fixed , denoting , we apply Lemma 9 with the settings , , , , , , then

(38) where

(39) (40) Now let us determine an equivalent of . For this purpose, let us introduce the modulus of continuity of on (which is well defined by Assumption 3):

Then we write:

(41) with

In particular:

(42) Now let us bound defined in (39). First, we bound , defined in (40):

which lead to:

(43) Finally, notice that by continuity of (Assumption 3), since :

-

2.

We first bound a.s. and its variance.

(44) For the variance:

(45) We apply Bernstein’s inequality (cf Lemma 10) to :

Let us compare the rates:

So, if is satisfied:

- 3.

5.4.5 Proof of Lemma 7

-

1.

We decompose as follows:

Using when :

(46) First we deal with . By definition of :

(47) Now let us give an upper bound of . Using Lemma 6,

- 2.

5.4.6 Proof of Lemma 9

We first denote

Then we obtain by integration by parts:

| (48) |

For any , we denote and for , (where is the canonical basis of ). Then, we write:

| (49) |

Then we apply Taylor’s theorem (cf Lemma 11) to the functions , :

where we denote for short:

| (50) |

We introduce the notation

and for any , we denote the vector without its variable, then (48) becomes:

Since has at least zero moments, the terms with vanish, leading to:

| (51) |

with .

Acknowledgement.

The author is extremely grateful to Claire Lacour and Vincent Rivoirard for suggesting me to study this problem, for the stimulating discussions, the helpful advices and the careful proofreading.

References

- Bashtannyk and Hyndman, [2001] Bashtannyk, D. M. and Hyndman, R. J. (2001). Bandwidth selection for kernel conditional density estimation. Comput. Statist. Data Anal., 36(3):279–298.

- Beaumont et al., [2002] Beaumont, M., Zhang, W., and Balding, D. (2002). Approximate bayesian computation in population genetics. Genetics, 162(4):2025–2035.

- Bertin et al., [2016] Bertin, K., Lacour, C., and Rivoirard, V. (2016). Adaptive pointwise estimation of conditional density function. Ann. Inst. H. Poincaré Probab. Statist., 52(2):939–980.

- Biau et al., [2015] Biau, G., Cérou, F., and Guyader, A. (2015). New insights into approximate bayesian computation. Ann. Inst. H. Poincaré Probab. Statist., 51(1):376–403.

- Birgé and Massart, [1998] Birgé, L. and Massart, P. (1998). Minimum contrast estimators on sieves: exponential bounds and rates of convergence. Bernoulli, 4(3):329–375.

- Donoho and Low, [1992] Donoho, D. L. and Low, M. G. (1992). Renormalization exponents and optimal pointwise rates of convergence. Ann. Statist., 20(2):944–970.

- Efromovich, [1999] Efromovich, S. (1999). Nonparametric Curve Estimation: Methods, Theory and Applications. Springer Science & Business Media.

- Efromovich, [2007] Efromovich, S. (2007). Conditional density estimation in a regression setting. Ann. Statist., 35(6):2504–2535.

- [9] Efromovich, S. (2010a). Dimension reduction and adaptation in conditional density estimation. Journal of the American Statistical Association, 105(490):761–774.

- [10] Efromovich, S. (2010b). Oracle inequality for conditional density estimation and an actuarial example. Ann. Inst. Statist. Math., 62(2):249–275.

- Fan et al., [1996] Fan, J., Yao, Q., and Tong, H. (1996). Estimation of conditional densities and sensitivity measures in nonlinear dynamical systems. Biometrika, 83(1):189–206.

- Fan and Yim, [2004] Fan, J. and Yim, T. H. (2004). A crossvalidation method for estimating conditional densities. Biometrika, 91(4):819–834.

- Fan et al., [2009] Fan, J.-q., Peng, L., Yao, Q.-w., and Zhang, W.-y. (2009). Approximating conditional density functions using dimension reduction. Acta Mathematicae Applicatae Sinica, English Series, 25(3):445–456.

- Faugeras, [2009] Faugeras, O. P. (2009). A quantile-copula approach to conditional density estimation. J. Multivariate Anal., 100(9):2083–2099.

- Fernández-Soto et al., [2002] Fernández-Soto, A., Lanzetta, K., Chen, H.-W., Levine, B., and Yahata, N. (2002). Error analysis of the photometric redshift technique. Monthly Notices of the Royal Astronomical Society, 330(4):889–894.

- Goldenshluger and Lepski, [2011] Goldenshluger, A. and Lepski, O. (2011). Bandwidth selection in kernel density estimation: oracle inequalities and adaptive minimax optimality. Ann. Statist., 39(3):1608–1632.

- Györfi and Kohler, [2007] Györfi, L. and Kohler, M. (2007). Nonparametric estimation of conditional distributions. IEEE Trans. Inform. Theory, 53(5):1872–1879.

- Hall et al., [2004] Hall, P., Racine, J., and Li, Q. (2004). Cross-validation and the estimation of conditional probability densities. J. Amer. Statist. Assoc., 99(468):1015–1026.

- Holmes et al., [2010] Holmes, M. P., Gray, A. G., and Isbell, C. L. (2010). Fast kernel conditional density estimation: A dual-tree monte carlo approach. Computational Statistics & Data Analysis, 54(7):1707 – 1718.

- Hyndman et al., [1996] Hyndman, R. J., Bashtannyk, D. M., and Grunwald, G. K. (1996). Estimating and visualizing conditional densities. J. Comput. Graph. Statist., 5(4):315–336.

- Hyndman and Yao, [2002] Hyndman, R. J. and Yao, Q. (2002). Nonparametric estimation and symmetry tests for conditional density functions. J. Nonparametr. Stat., 14(3):259–278.

- Izbicki and Lee, [2016] Izbicki, R. and Lee, A. B. (2016). Nonparametric conditional density estimation in a high-dimensional regression setting. Journal of Computational and Graphical Statistics, 25(4):1297–1316.

- Izbicki and Lee, [2017] Izbicki, R. and Lee, A. B. (2017). Converting high-dimensional regression to high-dimensional conditional density estimation. Electron. J. Statist., 11(2):2800–2831.

- Jeon and Taylor, [2012] Jeon, J. and Taylor, J. W. (2012). Using conditional kernel density estimation for wind power density forecasting. J. Amer. Statist. Assoc., 107(497):66–79.

- Lafferty and Wasserman, [2008] Lafferty, J. and Wasserman, L. (2008). Rodeo: Sparse, greedy nonparametric regression. Ann. Statist., 36(1):28–63.

- Liu et al., [2007] Liu, H., Lafferty, J. D., and Wasserman, L. A. (2007). Sparse nonparametric density estimation in high dimensions using the rodeo. In International Conference on Artificial Intelligence and Statistics, pages 283–290.

- Marin et al., [2012] Marin, J.-M., Pudlo, P., Robert, C. P., and Ryder, R. (2012). Approximate bayesian computation methods. Statistics and Computing, 22(6):1167–1180.

- Otneim and Tjøstheim, [2017] Otneim, H. and Tjøstheim, D. (2017). Conditional density estimation using the local gaussian correlation. Statistics and Computing, pages 1–19.

- Rosenblatt, [1969] Rosenblatt, M. (1969). Conditional probability density and regression estimators. In Multivariate Analysis, II (Proc. Second Internat. Sympos., Dayton, Ohio, 1968), pages 25–31. Academic Press, New York.

- Sart, [2017] Sart, M. (2017). Estimating the conditional density by histogram type estimators and model selection. ESAIM: Probability and Statistics, 21:34–55.

- Takeuchi et al., [2006] Takeuchi, I., Le, Q. V., Sears, T. D., and Smola, A. J. (2006). Nonparametric quantile estimation. Journal of Machine Learning Research, 7(Jul):1231–1264.

- Takeuchi et al., [2009] Takeuchi, I., Nomura, K., and Kanamori, T. (2009). Nonparametric conditional density estimation using piecewise-linear solution path of kernel quantile regression. Neural Comput., 21(2):533–559.

- Wasserman and Lafferty, [2006] Wasserman, L. and Lafferty, J. D. (2006). Rodeo: Sparse nonparametric regression in high dimensions. In Advances in Neural Information Processing Systems, pages 707–714.