Affine forward variance models

Abstract

We introduce the class of affine forward variance (AFV) models of which both the conventional Heston model and the rough Heston model are special cases. We show that AFV models can be characterized by the affine form of their cumulant generating function, which can be obtained as solution of a convolution Riccati equation. We further introduce the class of affine forward order flow intensity (AFI) models, which are structurally similar to AFV models, but driven by jump processes, and which include Hawkes-type models. We show that the cumulant generating function of an AFI model satisfies a generalized convolution Riccati equation and that a high-frequency limit of AFI models converges in distribution to the AFV model.

MKR gratefully acknowledges financial support from DFG grants ZUK 64 and KE 1736/1-1. We thank Masaaki Fukasawa and two anonymous referees for their insightful comments.

1 Introduction

The class of affine processes, introduced in [5], consists of all continuous-time Markov processes taking values in , whose log-characteristic function depends in an affine way on the initial state vector of the process. Affine processes have proved particularly convenient for financial modeling, typically giving rise to models with tractable formulae for the values of financial claims; the perennially popular Heston model [15] is just one (and perhaps the most famous) example of such a model.

In this paper, we introduce the class of affine forward variance (AFV) models of which classical Markovian affine stochastic volatility models turn out to be a special case. By writing our model in forward variance form, we are able to provide a unique characterization of a much wider class of affine stochastic volatility models, which includes non-Markovian models, such as the rough Heston model of [7] or, more generally, stochastic volatility models driven by affine Volterra processes in the sense of [1]. Our contribution is to provide necessary and sufficient conditions for a (non-Markovian) stochastic volatility model to be affine, thus adding a reverse direction to the results of [1], and with a simpler proof111Some of these simplifications are due to the fact that we limit ourselves to the (real-valued) moment generating function, as opposed to the (complex-valued) characteristic function, studied in [7]. In essence, the rough Heston model is – up to a choice of kernel – the only stochastic volatility model with an affine moment generating function.

Inspired by the original derivation [7] of the rough Heston model as a limit of simple pure jump models of order flow, we further introduce the class of affine forward order flow intensity (AFI) models. These model are structurally similar to affine forward variance models and generalize the simple order flow model of [7], by allowing arbitrary order size distributions and more general decay of the self-excitation of order flow. We define a high-frequency limit in which such models give rise to continuous affine forward variance models. In so doing, we generalize and simplify previous such derivations. Moreover, there is a clear structural analogy between the results we prove for AFV and AFI models, adding insight to and generalizing the connection between microstructural models of order flow and stochastic volatility models first brought to light in [16] and [17].

Our paper proceeds as follows. In Section 2, we introduce the class of affine forward variance models and show that a forward variance model has an affine cumulant generating function (CGF) if and only if it can be written in a very specific form. We further show that the CGF can be obtained as the unique global solution of a convolution Riccati equation closely related to the Volterra-Riccati equations of [1]. In Section 3, we introduce the class of AFI models, showing that the CGF of such models solves a generalized convolution Riccati equation. In Section 4, we show that AFI models become AFV models in a high-frequency limit, where order arrivals are extremely frequent and order sizes extremely small.

2 Affine forward variance models

2.1 Forward variance models

Let a probability space with right-continuous filtration and two independent, adapted Brownian motions and be given. The filtration generated by only is denoted by . Our starting point is a generic stochastic volatility model , where spot volatility is modeled by a -adapted continuous, integrable, and non-negative process and the price process by

| (2.1) |

for some correlation parameter . Crucially, we do not assume that is an Ito-process or even a semi-martingale. Instead, we focus on the family (indexed by ) of forward variance processes

| (2.2) |

which are, by definition, -adapted martingales with terminal values . By the martingale representation theorem, there exists, for each , a predictable process with a.s., such that

| (2.3) |

We refer to (2.1) together with (2.3) as stochastic volatility model in forward variance form, or simply as forward variance model. It is often convenient to use the log-price instead of and we note that it follows from (2.1) that satisfies the SDE

| (2.4) |

We also refer to together with the family of processes as forward variance model and denote it by . Moreover, we use the following convention:

which is consistent with (2.2) and allows to extend (2.3) to all .

Finally we introduce the following assumptions on the integrands :

Assumption 2.1.

-

(a)

For -almost all it holds that is non-negative, decreasing and continuous on .

-

(b)

For any the integrability condition

(2.5) holds almost surely.

We will show that in the class of affine forward variance models, the integrand must factor as , where is a deterministic function. To describe the admissible functions we introduce the following:

Definition 2.2.

For , an -kernel is a function which is continuous on and satisfies for all .

Remark 2.3.

- (a)

-

(b)

By (2.1) is a non-negative local martingale and therefore a supermartingale, such that . This implies by Jensen’s inequality that the moments are finite for all ; a fact that will be used subsequently.

2.2 A characterization of affine forward variance models

Definition 2.4.

We say that a forward variance model has an affine cumulant generating function determined by , if its conditional cumulant generating function is of the form

| (2.6) |

for all , and where is -valued and continuous on for all and .

Remark 2.5.

Alternatively, we could consider (2.6) with imaginary parameter for , i.e. an affine log-characteristic function as in [7]. This is of particular interest for applications of Fourier pricing to the model . To show results on distributional convergence, which will be the subject of Section 4, using the cumulant generating function is sufficient and it will turn out that restricting to real parameters simplifies many of the mathematical arguments.

Convolution integrals, as in the exponent of (2.6), will appear frequently in the following calculations and so it is natural to introduce the convolution operation . For functions with multiple arguments or subscripts, we use the convention that convolution acts on the first argument, excluding subscripts. Other arguments or subscripts are passed on to the result. With this convention (2.6) can be written succinctly as

| (2.7) |

The following result gives a characterization of all forward variance models with affine CGF. Its proof is given in Section 2.4 with some parts relegated to Appendix B.

thm 2.6.

Remark 2.7.

We introduce the useful notion of a -resolvent kernel:

lem 2.8.

Let and let be an -kernel. Then for any , there exists a unique -kernel , such that

| (2.12) |

If is convex, then the assertion also holds for . We call the -resolvent of .

Proof.

If it clear that , and the Lemma becomes trivial. In all other cases is the so-called ‘resolvent of the second kind’ (see [13]) of , and the properties of follow directly from Thm. 2.3.1 (existence and uniqueness), Thm. 2.3.5 (local -integrability), Prop. 9.5.7 (continuity), Prop. 9.8.1 (positivity for and Prop. 9.8.8 (positivity under log-convexity for ); all in [13]. ∎

Upon taking Laplace transforms of , the resolvent equation (2.12) becomes

| (2.13) |

which can be useful for determining explicitly from a given .

Remark 2.9 (Relation to affine Volterra processes).

Note that the instantaneous variance process of an AFV model can be written as

| (2.14) |

which shows that is an affine Volterra process in the sense of [1]. We emphasize, that the representation (2.14) is not unique. Indeed, let and let be the -resolvent of . Then, using e.g. [1, Lem. 2.5], it follows that

| (2.15) |

with , and a mean-reverting drift-term appears. Conversely, if a process of the form (2.15) is given, and if has a -resolvent , then the forward variance is of the form

with , cf. [1, Lem. 2.5].

2.3 Two examples: Heston and rough Heston models

Example 2.10 (The Heston model).

The Heston model [15] is given by

| (2.16a) | ||||

| (2.16b) | ||||

A simple calculation shows that

Hence,

and it follows that the Heston model can be written as an affine forward variance model with kernel

and initial forward variance

Note that is the -resolvent of the constant kernel , in accordance with Remark 2.9. To obtain the Riccati ODEs for the Heston model in the usual form (see e.g. [18]), let be a -function such that

By partial integration we obtain

Inserting into the convolution Riccati equation (2.9) yields

in accordance with [18]. Furthermore, it is straightforward to show that

with .

Example 2.11 (The rough Heston model).

In the rough Heston model, introduced in [7], (2.16b) is replaced by

| (2.17) |

where is related to the ‘roughness’ of the paths of . Note that this is an affine Volterra process (2.15) with power-law kernel . In [8] it is shown that the forward variance in the rough Heston model satisfies

with the kernel

and where denotes the generalized Mittag-Leffler function (cf. [9], [19, Sec. 1.2]).222Alternatively, one can check that the Laplace transforms and satisfy the relation (2.13) with . Thus, the rough Heston model is an affine forward variance model in the sense of Theorem 2.6. The initial forward variance is given by (cf. [8, Prop. 3.1])

To obtain the fractional Riccati equation (cf. [7, Eq. (24)]) for the rough Heston model set

By [7, Lem. A.2] satisfies

where denotes the Riemann-Liouville fractional derivative of order . Inserting into the convolution Riccati equation (2.9) yields

in accordance with [7, Eq (24)]. Denote by the Riemann-Liouville fractional integral of order and write for the function of constant value one. The exponent in (2.6) can be transformed as follows:

which is the same as [7, Eq (23)].

2.4 Proving the characterization result

To prepare for the proof of Theorem 2.6, we introduce the following notation: Given a family of continuous functions from to , we set

| (2.18) | ||||

| (2.19) |

If has an affine CGF determined by then it follows from (2.6) that is a martingale. Conversely, if is a martingale, then (2.6) follows by taking conditional expectations. Hence, the affine property of can be characterized in terms of the martingale property of . In order to apply Itô’s formula to we represent as an Itô process. The calculation is analogous to the drift computation in the Heath-Jarrow-Morton-model (cf. [10, Ch. 6]) and uses the stochastic Fubini theorem to interchange stochastic integral and Lebesgue integral.

lem 2.12.

Proof.

Fix and . Following [10, p. 94] closely, we compute

To justify the application of the stochastic Fubini theorem in the form of [21, Thm. 2.2], we have to check whether

is finite for all . Since is continuous, there is a finite constant . Using Assumption 2.1 we find that

for all and the application of the stochastic Fubini theorem was justified.

lem 2.13.

Proof.

Fix and set , with given by (2.10). It is easy to check that satisfies all conditions of Corollary A.7, i.e., that

-

•

is a finite, strictly convex function on and satisfies ;

-

•

has a single root in .

Thus, we conclude from Corollary A.7 the existence of a unique global continuous solution to (2.9) for all . Moreover, for all by estimate (A.11). Adding the boundary cases is trivial: Observe that is a constant global solution of (2.9) for , which must be unique by [13, Thm. 13.1.2]. Also the representation as follows directly from Corollary A.7. ∎

We are now prepared to prove the first part of Theorem 2.6.

Theorem 2.6, ‘if’ part..

Let and fix some . By Lemma 2.13, the convolution Riccati equation (2.9) associated to this kernel has a unique global continuous -valued solution . Using this solution we define the processes and as in (2.18) and (2.19). Applying Lemma 2.12, we see that equation (2.20) for can be simplified due to the factorization of to

Inserting into (2.21) we obtain

| (2.23) |

Since solves the convolution Riccati equation (2.9) the -term vanishes and we have shown that is a local martingale. It remains to show that is a true martingale. To this end, observe that

| (2.24) |

for all . But is a supermartingale, such that

Setting this is the -criterion for uniform integrability of . We conclude that is a true martingale, and hence that

| (2.25) |

showing (2.6) for all . Adding the boundary cases is trivial. Since in these cases, (2.25) follows immediately. ∎

For the reverse implication of Theorem 2.6 we distinguish the cases and . The proof follows the same structure in both cases, but needs some additional technical arguments, which are relegated to Appendix B.

Theorem 2.6, ‘only if’ part in the case ..

By assumption, the forward variance model has an affine CGF in the sense of Definition 2.4. Using the associated function , we define the processes and as in (2.18) and (2.19). Observe that due to (2.6), has to be a martingale. In addition, note that Assumption 2.1, together with yields that

for all . Applying Lemma 2.12 and using the fact that is a martingale, we see that the -term in (2.21) has to vanish, i.e. that

| (2.26) |

up to a -nullset. This is a quadratic equation in the variable , and due to the assumption it possesses a unique negative solution

Inserting the definition of from (2.20) and setting we obtain

| (2.27) |

This is a Volterra integral equation of the first kind (cf. [13, Sec. 5.5]) for the unknown function . From (2.26) it can easily be seen that . Therefore, by [13, Ex. 5.25], see also [12, Thm. 1], there exists a (locally finite Borel) measure – the resolvent of the first kind333Not to be confused with the -resolvent of Lemma 2.8. of – such that for all . Convolving (2.27) with , the unique solution of (2.27) can be expressed as, cf. [13, Thm. 5.3],

| (2.28) |

Denoting the last factor by and taking into account Assumption 2.1 the desired decomposition (2.8) follows. ∎

3 Affine forward order flow intensity models

We now introduce a class of models for market order flow, which are structurally similar to forward variance models. These models consist of a log-price and a forward intensity process , which models the expectation (at time ) of the future intensity of order flow (at time ). The forward intensity has a role similar to the forward variance, and we call the resulting model an affine forward order flow intensity (AFI) model.444The strong empirical correlation between order volume (as a proxy for intensity) and return variance is well-documented in the literature (see e.g. [11]). Therefore the parallels between AFV and AFI models should not come as a complete surprise. The AFI model is driven purely by the arrival of market orders, which are represented by two pure-jump semimartingales of finite activity and with common intensity . As in (2.2), we assume that and are connected by

The driving processes jump only upwards and represent the arrival of buy and sell orders respectively. Their jump height distributions are given by two probability measures on for buy and for sell orders. We assume that ; in particular, also the first moments

exist. In addition, we assume that the order flow processes are self-exciting, in the sense that each arriving order positively impacts the intensity process. This impact can be asymmetric, i.e. the degree of self-excitement may be different for buy- and sell-orders. Together this leads to the specification of the AFI model as

| (3.1a) | ||||

| (3.1b) | ||||

where is an -kernel in the sense of Definition 2.2, are positive constants, is determined by the martingale condition on and denote the compensated order flow processes, i.e. . Setting

| (3.2) |

and denoting by the compensated counterpart of , we can rewrite (3.1) as

We proceed to discuss the jump processes and the compensators of their random jump measures in more detail. The random jumps of are compensated by

where represents jump size. While and are independent, given , it is important to note that and are not. Instead, they move by simultaneous jumps. Thus, the predictable compensator of the jump measure of is given by

Note that the measure of joint jump heights is concentrated on the line segments and due to the simultaneity of jumps. In addition, we define

| (3.3) |

and calculate

Applying Itô’s formula for jump processes to it is easy to see that the martingale condition implies that

The following theorem is the analogue of Theorem 2.6 and shows the structural similarity between affine forward variance models and AFI models.

thm 3.1.

Proof.

Essentially, we proceed as in the ‘if’-part of the proof of Theorem 2.6. Let be defined as in (2.18) and set . Applying the same argument as in the proof of Lemma 2.12, but replacing Brownian motion by the pure-jump-martingale we obtain

where

Applying the Itô-formula with jumps to we obtain

and compensating the jumps yields

| (3.6) |

where ‘loc. mg.’ denotes a local martingale part that we need not compute explicitly. We see that the -terms vanish, if

i.e. if the generalized convolution Riccati equation (3.4) has a solution for .

To show that there exists a unique global continuous solution of (3.4), we proceed as in the proof of Lemma 2.13, i.e., we set and show that satisfies the conditions of Corollary A.7. In particular, for all ,

-

•

is a finite, strictly convex function on and satisfies ;

-

•

has a single root in .

Indeed, note that strict convexity is inherited from , cf. (3.3). In addition, convexity of the exponential function implies, for , that

and hence that

Finally, the existence of the root follows from the fact that

which implies that . In summary, satisfies all conditions of Cor. A.7 and we conclude the existence of a unique global solution of the Riccati equation for all . Moreover, for all by estimate (A.11). We can add the boundary cases , observing that they yield the constant global solution , which must be unique by [13, Thm. 13.1.2]. From (3) we conclude that is a local martingale. By the same arguments as in (2.24) and (2.25) it follows that is a true martingale, and hence that has an affine CGF. ∎

Example 3.2 (The bivariate Hawkes process of [7]).

Consider (3.1a), driven by a bivariate Hawkes process with unit jump size (i.e., , common kernel , and common intensity , given by

as in [7, Sec. 2]. Set and let be the -resolvent of in the sense of (2.12). In terms of , the Hawkes intensity has the martingale representation (cf. [2, Eq. (45)])

with the last integral now driven by a compensated jump processes. Taking conditional expectations and using the martingale property of yields

and hence

which shows that the model can be cast as AFI model with kernel . For concrete specifications of , we can take Laplace transforms and use the relation (2.13) to determine the corresponding . Consider, for example

| (3.7) |

For this we obtain from (2.13) the -resolvent

i.e., the kernel of the Heston model in forward variance form; see Example 2.10. Furthermore, the Hawkes kernel

| (3.8) |

has Laplace transform (cf. [14, Eq. (7.5)]). Thus its -resolvent is

| (3.9) |

the kernel of the rough Heston model in forward variance form; see Example 2.11.

4 High-frequency limit of the AFI model

We proceed to show that the AFV model is the high-frequency limit of the AFI model. This limit is closely related to the limits of ‘nearly unstable’ Hawkes processes considered in [16, 17, 7], see Example 4.4 below.

4.1 A first convergence result

Our starting point is the AFI model (3.1a). We assume that buy/sell order size distributions are normalized in the sense that

| (4.1) |

and we denote by

| (4.2) |

the variance of buy orders relative to sell orders. We introduce a small parameter and rescale (3.1) as

| (4.3a) | ||||

| (4.3b) | ||||

where are pure jump semimartingales, independent given their common intensity and with jump height distribution

Moreover, the kernels are scaled as

Thus, as , the frequency of jumps increases proportional to , while the size of jumps shrinks proportional to . The initial conditions of (4.3) are given by and . Under the given scaling, the quantities from (3.3) and below transform as

and we write

lem 4.1.

Given and the jump height distributions , define and by

| (4.4) |

Then

with as in (2.10). Moreover, also the partial derivatives with respect to and converge, i.e.

Proof.

We can write

| (4.5) |

where

Expanding in powers of yields

Hence, using (4.1) and (4.2), it follows that

where exchanging limit and integral is justified by dominated convergence and the integrability condition .

To show the convergence of partial derivatives, we take partial derivatives in (4.5) to obtain

Since is convex, its difference quotients converge monotonically, and monotone convergence can be used to exchange derivative and integral. Expanding in powers of , a direct calculation yields the desired limit. The proof for the -derivative is analogous. ∎

Remark 4.2.

Equation (4.4) gives important insights on the dependence of the leverage parameter on the micro-structural parameters (asymmetry of order sizes) and (asymmetry of self-excitement). Consider first the case of symmetric order size distributions as in [6]. In this case

which only takes values within , with boundaries attained in the limiting cases . When also asymmetry of order sizes is allowed, then can be represented as a scalar product of unit length vectors

which confirms that . In addition, the boundary cases can be attained when the vectors are of opposing resp. of the same direction, i.e., when and .

prop 4.3.

Proof.

By Theorem 3.1, in the CGF (2.6) of is the unique global solution of the generalized convolution Riccati equation (3.4) and hence satisfies

| (4.7) |

Note that is jointly continuous in all variables, and by Lemma 4.1 converges to as . By Corollary A.7, equation (4.7) can be transformed into a non-linear Volterra equation of type (A.6), whose solution depends jointly continuous on by [13, Thm. 13.1.1]. We conclude that converges, uniformly for in compacts, to as , where is the unique solution (cf. Theorem 2.6) of

Using Theorems 2.6 and 3.1, we conclude that

as , i.e., the moment generating function of converges to the moment generating function of on . By [4, Prob. 30.4], convergence of moment generating functions on a (non-empty) interval implies the convergence in distribution in (4.6). ∎

The following example shows that the scaling in (4.3) is related to the ‘nearly unstable’ limit of Hawkes models in [7].

Example 4.4 (Nearly unstable limit of bivariate Hawkes processes).

We continue Example 3.2 and consider the bivariate Hawkes process from [7] with Mittag-Leffler kernel (3.8). Introduce a small parameter and scale the kernel as

In terms of its Laplace transform, this scaling becomes . In particular, we have

i.e. as the stability condition of the Hawkes process approaches the critical value (hence ‘nearly unstable’). From (2.13), the Laplace transform of the resolvent kernel can be determined as

and thus the resolvent kernel is given by

Together with square-root scaling of the jump size we are exactly in the setting of (4.3) and conclude from Proposition 4.3 that the (univariate) marginal distributions of converge to those of the corresponding AFV model, i.e. the rough Heston model (cf. Example 2.11). Theorem 4.10 below strengthens this result to convergence of all finite-dimensional marginal distributions.

4.2 The joint moment generating function

In this subsection, we derive results on the joint moment generating function of log-price and forward variance and of the finite-dimensional marginal distributions of .

Assumption 4.5.

We assume that is either an AFV model or an AFI model, and we write for the corresponding function or . In addition we denote, for any , by the unique root where

Note that the function has already been studied in the context of affine stochastic volatility models in [18, Lem. 3.2ff]. In particular, we note that and are convex functions for and continuously differentiable on the interior of their domain.

prop 4.6.

Let be an AFV or an AFI model and let and be defined as in Assumption 4.5. Let , , and let be a piecewise continuous -valued function on , such that . Then

| (4.8) |

where is the unique continuous solution of the (generalized) convolution Riccati equation

| (4.9) | ||||

| with initial condition | ||||

| (4.10) | ||||

Remark 4.7.

Note that the expression (4.8) for the joint moment generating function does not correspond to the exponential-affine transform formula (4.6) of [1]. Specifically, constant in (4.8) would give the joint moment generation function of and the forward variance swap . In contrast, constant in (4.6) of [1] would give the the joint moment generation function of and quadratic variation .

Proof.

The existence of a unique, -valued solution to (4.9) with initial condition (4.10) follows from an application of Corollary A.8 with . In the proofs of Theorem 2.6 and Theorem 3.1, we have already established that satisfies the necessary conditions to apply the corollary. Next, we define and specialize to the forward variance case. By Lemma 2.12, it holds that

and that is a local martingale on if

Setting this is exactly (4.9). We conclude that is a local martingale on , and – repeating the argument following (2.24) – even a true martingale. Using the initial condition (4.10), we observe that

showing (2.6). The proof in the AFI case is analogous with the following modifications: has to be substituted by the pure-jump martingale and by the intensity . Itô’s formula for jump processes can then be applied as in the proof of Theorem 3.1. ∎

prop 4.8.

Let be an AFV or an AFI model and let and be defined as in Assumption 4.5. Let and be such that . Then, for all ,

| (4.11) |

where the functions are defined by backward recursion as the solutions of the convolution Riccati equations

| (4.12) | ||||

| with initial conditions | ||||

| (4.13) | ||||

Remark 4.9.

Proof.

We show the result by backward induction on : For the proposition is equivalent to Theorem 2.6, when is an AFV model, and to Theorem 3.1, when is an AFI model. Setting , we obtain from (A.15) in Corollary A.8 that

| (4.14) |

For the induction step assume that (4.11) has been shown for a certain and that (4.14) holds with replaced by . Writing

and applying the tower law of conditional expectations, we have

Since

we may apply Proposition 4.6 with and obtain (4.11) with as solution of (4.12) with initial condition (4.13). Finally, (4.14) holds with replaced by , using the estimate (A.15) from Corollary A.8. ∎

4.3 Convergence of finite-dimensional marginal distributions

thm 4.10.

Proof.

By Lemma 4.1 converges to and the same holds true for the partial derivatives with respect to and . Therefore, by the implicit function theorem, also and converge to and as for all . Moreover, since the are convex functions of , the convergence is uniform on compacts (cf. [20, Thm. 10.8]). The limit can be calculated explicitly and is given by

It is easy to see that is decreasing on and increasing on , where

We conclude that there is and a closed interval with non-empty interior, such that and are decreasing on for all . Introduce the set

and note that also is closed with non-empty interior. In addition, for all and , and the same holds for . From Proposition 4.8 we conclude that the joint moment generating function of the increments is of the form

for any and , where satisfies the iterated Riccati convolution equations (4.12) with . By Corollary A.8 each of these equations can be transformed into a non-linear Volterra equation, whose solution depends continuously on by [13, Thm. 13.1.1]. In addition, Lemma 4.1 yields the convergence . Hence we conclude – as in the proof of Proposition 4.3 – that converges, uniformly for in compacts, to as , where is the unique solution of the iterated Riccati convolution equations (4.12) with . Consider now the joint moment generating function of the increments of the AFV model with parameter and kernel . The convergence together with Proposition 4.8 yields

for all . By [4, Thm. 29.4 and Prob. 30.4] convergence of the moment generating function on a set with non-empty interior implies convergence in distribution, and (4.15) follows. ∎

Appendix A Some results on Volterra equations with convex non-linearity

We show some results on Volterra equations with convex non-linearity, of the type appearing in Theorem 2.6 and 3.1. On the non-linearity we impose the following assumptions:

Assumption A.1.

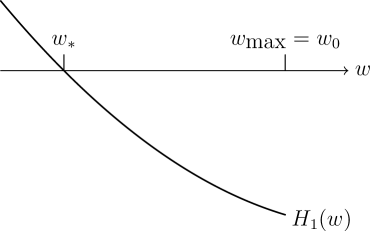

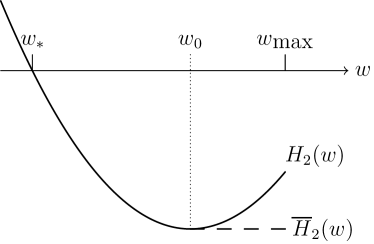

The function is continuously differentiable and convex with a unique root in . Moreover, and .

For a function satisfying Assumption A.1, we set

if the minimum is not unique (i.e., if has a flat part), then shall denote the leftmost minimizer. Note that either

-

•

, in which case is strictly decreasing on ; or

-

•

, in which case is strictly decreasing on and increasing on .

In any case, holds true. Also the following definition will be useful:

Definition A.2.

Let be a function satisfying Assumption A.1. The decreasing envelope of is defined as

| (A.1) |

Clearly also satisfies Assumption A.1, but is in addition decreasing and satisfies . Both Assumption A.1 and Definition A.2 are illustrated in Figure 1.

lem A.3.

Let be a convex function that satisfies Assumption A.1; in particular it has a root . Then

-

(a)

For any the function

(A.2) maps onto ; is strictly decreasing, and has an inverse , which maps onto .

-

(b)

For any the function

(A.3) maps onto ; is strictly increasing, and has an inverse , which maps onto .

Remark A.4.

Proof.

To show (a), note that the integrand is strictly positive on . It follows that is strictly decreasing and maps into . It remains to show that range of this map covers all of . To this end, observe that by convexity we have

| (A.5) |

and . Thus, we obtain

The proof of (b) is analogous; only the different sign of on has to be taken into account. ∎

thm A.5.

Let be an -kernel in the sense of Definition 2.2 and let be a convex function that satisfies Assumption A.1; in particular is its unique root in . For any continuous function consider the non-linear Volterra equation

| (A.6) |

- (a)

-

(b)

If then is the unique global solution of (A.6)

- (c)

In addition, case (a) can be extended to the following more general statement:

- (a’)

Remark A.6.

Clearly, if is decreasing (and hence ), cases (a) and (a’) coincide. In the general case (a) gives better bounds on than (a’), but is more restrictive in its assumption on the function .

Before proving the theorem, we add two Corollaries that are used in the proofs of Theorems 2.6, 3.1 and 4.10.

cor A.7.

Under the assumptions of Theorem A.5, consider the non-linear integral equation

| (A.10) |

-

(a)

If is increasing with values in then (A.10) has a unique global solution which satisfies

(A.11) -

(b)

If then is the unique global solution of (A.10).

-

(c)

If is decreasing with values in then (A.10) has a unique global solution which satisfies

(A.12)

In addition, case (a) can be extended to:

-

(a’)

If is increasing with values in then (A.10) has a unique global solution which satisfies

(A.13)

In any of the above cases, , where is the solution of (A.6).

cor A.8.

We start with the proof of Theorem A.5, which closely follow the account of Lakshmikantham’s comparison method in [3, Sec. II.7].

Proof of Theorem A.5.

Clearly, can be extended to a continuous function on all of and thus it follows from [13, Thm. 12.1.1] that (A.6) has a local continuous solution on an interval with . In addition, can be chosen maximal, in the sense that the solution cannot be continued beyond .

Case (a): By assumption, is increasing and takes values in . Set

| (A.16) |

and note that . From (A.6) it is clear that

| (A.17) |

i.e. the lower bound in (A.16) is always hit before the upper bound . In addition, using that the kernel is decreasing, we obtain that

| (A.18) |

for all . The function , which we have just defined, satisfies

| (A.19) | ||||

| (A.20) |

and the differential inequality

| (A.21) |

Here, we have used (A.18) and the fact that is decreasing on . Together with the initial estimate (A.20), a standard comparison principle for differential inequalities (cf. [22, II.§9]) yields

| (A.22) | ||||

| where | ||||

| (A.23) | ||||

We claim that the differential equation (A.23) is solved by

| (A.24) |

Indeed, applying to both sides of (A.24) yields

Taking -derivatives, we obtain

which is equivalent to (A.23). From (A.18), (A.19) and (A.22) we obtain the bound

| (A.25) |

for all . This implies that

| (A.26) |

which, in light of (A.16), means that , i.e. we have shown the bounds (A.7) to hold for all . However, by [13, Thm. 12.1.1] whenever . We conclude that , and hence that is a global solution of (A.6). Uniqueness follows from [13, Thm. 13.1.2].

Case (b): By assumption, . Since it is clear that is a global solution of (A.6). Uniqueness follows from [13, Thm. 13.1.2].

Case (c): By assumption, is decreasing and takes values in . This case can be handled analogous to case (a) with the following adaptations: The inequality signs in equations (A.17) – (A.22) have to be reversed. In (A.24) has to be substituted by and also in (A.25) and (A.26) the inequalities have to be reversed.

Case (a’): The proof of Case (a) applies, except for the following modification: (A.21) holds only when , since is decreasing only on . However, when , we can use the trivial estimate

which can be combined with (A.21) into

where is the decreasing envelope of from Definition A.2. The remaining proof of Case (a) applies after substituting by and by . ∎

Proof of Corollary A.7.

Let be the global solution of (A.6). Applying to both sides of (A.6), we see that is a global solution of (A.10). Next, we show uniqueness. To this end, assume that is a local solution of (A.10) on , different from and define

Clearly, on , and hence is a local solution of (A.6). By [13, Thm. 13.1.2], this solution is unique, and we conclude that , and hence also . Finally, applying – which is decreasing on – to the inequalities (A.7) and (A.8) yields (A.11) and (A.12). In case (a’) monotonicity of is lost, but for all yields (A.13). ∎

Proof of Corollary A.8.

Set

and note that is increasing with values in . Consider the non-linear Volterra equation

| (A.27) |

which has a unique global solution by Theorem A.5.(a) or (a’). For set

For we have

showing that is a global solution of (A.14). From cases (a) or (a’) of Theorem A.5, we obtain the bound

as claimed. To show uniqueness, assume that is a solution of (A.14), different from . Setting

we see that is a solution of (A.27) and conclude from Theorem A.5 that and hence also . ∎

Appendix B Theorem 2.6 in the case

We provide the remaining part of the proof of Theorem 2.6 in the case . Our starting point is the quadratic equation (2.26), which has been obtained without any assumption on the sign of . In the case , additional arguments are needed, since this equation may have two negative solutions.

Theorem 2.6, ‘only if’ part in the case ..

On the set we set

for . Note that by Assumption 2.1 must be a decreasing -kernel for a.e. . Since (2.8) holds trivially if is a -nullset, we may, without loss of generality, assume that is not a nullset and consider only in the remainder of the proof. Inserting into (2.20) yields

Plugging into (2.26) and eliminating gives

| (B.1) |

with is a quadratic equation in the variable with two solutions

| (B.2) |

both of which may be negative. However, using continuity of and evaluating (B.1) at yields that . Inserting into (B.2) and using this initially selects the solution and shows that

where is the first collision time of and , i.e. ,

On the interval we can proceed as in the case of and obtain that

| (B.3) |

where is the resolvent of the first kind of . Therefore, to complete the proof it suffices to show that can be made arbitrarily large by choosing a suitable . To this end, note that (B.1) is a convolution Riccati equation for with the kernel , i.e.,

Applying Lemma 2.13 we obtain that is its unique continuous solution, which, by Corollary A.7, can be written as , where solves

| (B.4) |

Moreover, the collision time can be represented in terms of as

| (B.5) |

By convexity, we can estimate from below as . Hence, from (B.4) we obtain the estimate

| (B.6) |

Let be the -resolvent of , and note that is again an -kernel (in particular non-negative) by Lemma 2.8. By the generalized Gronwall Lemma of [13, Lem. 9.8.2] it follows that , where solves the linear Volterra equation

Moreover, using [13, Thm. 2.3.5], we can express in terms of the -resolvent and obtain for all . Combining with (B.5), we finally obtain

Sending the right-hand side can be made arbitrarily large and we conclude that , which together with (B.3) completes the proof. ∎

References

- [1] Eduardo Abi Jaber, Martin Larsson, and Sergio Pulido. Affine Volterra processes. arXiv:1708.08796, 2017.

- [2] Emmanuel Bacry, Iacopo Mastromatteo, and Jean-François Muzy. Hawkes processes in finance. Market Microstructure and Liquidity, 1(01), 2015.

- [3] Drumi D Bainov and Pavel S Simeonov. Integral inequalities and applications, volume 57. Springer Science & Business Media, 2013.

- [4] Patrick Billingsley. Probability and measure. John Wiley & Sons, 2nd edition edition, 1986.

- [5] Darrell Duffie, Damir Filipović, and Walter Schachermayer. Affine processes and applications in finance. Annals of applied probability, pages 984–1053, 2003.

- [6] Omar El Euch, Masaaki Fukasawa, and Mathieu Rosenbaum. The microstructural foundations of leverage effect and rough volatility. Finance and Stochastics, 22(2):241–280, 2018.

- [7] Omar El Euch and Mathieu Rosenbaum. The characteristic function of rough Heston models. Mathematical Finance, forthcoming, 2018.

- [8] Omar El Euch and Mathieu Rosenbaum. Perfect hedging in rough Heston models. The Annals of Applied Probability, 28(6):3813–3856, 2018.

- [9] Arthur Erdélyi, Wilhelm Magnus, Fritz Oberhettinger, and Francesco G Tricomi. Higher transcendental functions, Vol. III, based on notes left by Harry Bateman, reprint of the 1955 original. Robert E. Krieger Publishing Co., Inc., Melbourne, Fla, 1981.

- [10] D. Filipovic. Term-Structure Models. Springer, 2009.

- [11] A Ronald Gallant, Peter E Rossi, and George Tauchen. Stock prices and volume. The Review of Financial Studies, 5(2):199–242, 1992.

- [12] Gustaf Gripenberg. On Volterra equations of the first kind. Integral Equations and Operator Theory, 3(4):473–488, 1980.

- [13] Gustaf Gripenberg, Stig-Olof Londen, and Olof Staffans. Volterra integral and functional equations, volume 34. Cambridge University Press, 1990.

- [14] Hans J Haubold, Arak M Mathai, and Ram K Saxena. Mittag-Leffler functions and their applications. Journal of Applied Mathematics, 2011.

- [15] Steven L Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. The Review of Financial Studies, 6(2):327–343, 1993.

- [16] Thibault Jaisson and Mathieu Rosenbaum. Limit theorems for nearly unstable Hawkes processes. The Annals of Applied Probability, 25(2):600–631, 2015.

- [17] Thibault Jaisson and Mathieu Rosenbaum. Rough fractional diffusions as scaling limits of nearly unstable heavy tailed Hawkes processes. The Annals of Applied Probability, 26(5):2860–2882, 2016.

- [18] Martin Keller-Ressel. Moment explosions and long-term behavior of affine stochastic volatility models. Mathematical Finance, 21(1):73–98, 2011.

- [19] Igor Podlubny. Fractional differential equations, volume 198 of Mathematics in Science and Engineering. Academic press, 1998.

- [20] R. Tyrrell Rockafellar. Convex Analysis. Princeton University Press, 1970.

- [21] Mark Veraar. The stochastic Fubini theorem revisited. Stochastics, 84(4):543–551, 2012.

- [22] Wolfgang Walter. Ordinary Differential Equations. Springer, 6th edition, 1996.