The QLBS Q-Learner Goes NuQLear:

Fitted Q Iteration, Inverse RL, and Option Portfolios

Igor Halperin

NYU Tandon School of Engineering

e-mail:

Abstract:

The QLBS model is a discrete-time option hedging and pricing model that is based on Dynamic Programming (DP) and Reinforcement Learning (RL). It combines the famous Q-Learning method for RL with the Black-Scholes (-Merton) model’s idea of reducing the problem of option pricing and hedging to the problem of optimal rebalancing of a dynamic replicating portfolio for the option, which is made of a stock and cash. Here we expand on several NuQLear (Numerical Q-Learning) topics with the QLBS model. First, we investigate the performance of Fitted Q Iteration for a RL (data-driven) solution to the model, and benchmark it versus a DP (model-based) solution, as well as versus the BSM model. Second, we develop an Inverse Reinforcement Learning (IRL) setting for the model, where we only observe prices and actions (re-hedges) taken by a trader, but not rewards. Third, we outline how the QLBS model can be used for pricing portfolios of options, rather than a single option in isolation, thus providing its own, data-driven and model independent solution to the (in)famous volatility smile problem of the Black-Scholes model.

1 Introduction

In Ref. [1], we presented the QLBS model - a discrete-time option hedging and pricing model rooted in Dynamic Programming (DP) and Reinforcement Learning (RL). It combines the famous Q-Learning method for RL [2, 3] with the Black-Scholes (-Merton) model’s idea of reducing the problem of option pricing and hedging to the problem of optimal rebalancing of a dynamic replicating portfolio for an option, which is made of a stock and cash [4, 5].

In a nutshell, the celebrated Black-Scholes-Merton (BSM) model, also known as the Black-Scholes (BS) model [4, 5], shows that even though the option price can (and will) change in the future because it depends on a future stock price which is also unknown, a unique fair option price can be found by using the principle of one price for identical goods, alongside with the method of pricing by replication. This assumes a continuous re-hedging and a special (lognormal) choice of stock price dynamics. However, such apparent uniqueness of option prices also means that, under these assumptions, options are completely redundant, as they can be always perfectly replicated by a simple portfolio made of a stock and cash.

As argued in more details in [1], an apparent redundancy of options in the BSM model is due to the fact that the latter model is formulated in the continuous time limit , where hedges are rebalanced continuously, and at zero cost. In such academic limit, an option becomes risk-free, and hence completely redundant, as it is just equal, at any time , to a dynamic portfolio of a stock and cash. In any other case, i.e. when a time step , risk in an option position cannot be completely eliminated, but at best can be minimized by a proper choice in an offsetting position in a stock that underlies the option, i.e. by an optimal hedge.

But in the real life, re-balancing of option hedges always happens with some finite frequency , e.g. daily, monthly, etc. Therefore, keeping a time-step finite while controlling risk in an option position is critical for keeping realism in any option pricing model. While the classical BSM model gives rise to elegant closed-form expressions for option prices and hedges in the mathematical limit , it makes its theoretical ”risk-neutral” option prices and hedges quite problematic in practice, even as a ”zero-order” approximation to the real world.

Indeed, as financial markets are precisely in the business of trading risk, any meaningful ”zero-order” approximation should account for risk inherently present in financial options and other derivative instruments. One could argue that using an equilibrium ”risk-neutral” framework for option pricing and hedging in a risky option trading business is akin to explaining a biological system starting with equilibrium thermodynamics. While it would be absurd to describe life as a ”correction” to non-life (which is the only possible state with equilibrium thermodynamics), various volatility smile models developed in continuous-time Mathematical Finance do essentially the same thing for financial risk in option pricing111”Economics ended up with the theory of rational expectations, which maintains that there is a single optimum view of the future, that which corresponds to it, and eventually all the market participants will converge around that view. This postulate is absurd, but it is needed in order to allow economic theory to model itself on Newtonian Physics.” (G. Soros). I thank Vivek Kapoor for this reference..

Indeed, to adjust model-based ”risk-neutral” option prices to market prices of risky options, traditional local and/or stochastic volatility models (see e.g. [6]) come to the altar of Athena to ask her to breathe life into a clay volatility surface that was just designed to be flat (dead) in the original BSM model! This is because the latter model rests on two critical assumptions: 1) continuous re-hedging is possible, which produces an equilibrium ”risk-neutral” option price, and 2) the world is log-normal with a fixed volatility which means a flat volatility surface as a function of option strike and maturity. Because both these assumptions are violated in practice, the original BSM model contradicts data, which makes it some way in between of a pure mathematical model, and a technical tool to quote market option prices as BS implied volatilities, and risk-manage options using their sensitivities with respect to the stock volatility (”vega”-sensitivity), and other BS sensitivity parameters (”the Greeks”). A mismatch with the market data is ”fixed” by switching to local or stochastic volatility models that ”match the market” much better than the original BSM model.

But this smacks of a ”scientific” Cargo cult, with PDEs and GPUs replacing straw airplanes and wooden rifles. No matter how well stochastic volatility models fit market prices, they entirely miss the first question that needs an answer for trading, namely the question of expected risk in any given option contract. Their straight-face answer to such basic question would be ”Right now, you have no risk in this option, sir!”

Needless to say, in physics a quantum model that tweaked the Planck constant to achieve consistency with data would be deemed nonsensical, as the Planck constant is a constant that cannot change, thus any ”sensitivity with respect to ” would be meaningless (but see [7]).

Yet, a likely questionable adjustment to the original BSM model via promoting a model constant (volatility) to a variable (local or stochastic volatility), to reconcile the model with market data, has become a market standard since 1974. The main reason for this is a common belief that advantages of analytical tractability of the classical BSM model in the continuous-time limit outweigh its main drawbacks such as inconsistency with data, thus calling for ”fixes” in the original model, such as introduction of non-constant volatilities.

However, this only brings a theoretical (and practical!) nightmare on the modeling side, when the financial risk, unceremoniously thrown away in the classical BSM model and other continuous-time models of Mathematical Finance but present in the market data, tries to make it back to the game, via mismatches between the model and market behavior. This results in what was colorfully described as ”Greek tragedies” for practitioners by Satyajit Das [8].

The main issue with these Mathematical Finance models is that they lump together two different problems with the original BSM model: (i) the absence of risk in the limit , and (ii) differences between real-world stock price dynamics and lognormal dynamics assumed in the BSM model. On the contrary, the QLBS model tackles these two problems sequentially.

It starts with a discrete-time version of the BSM model, and re-states the problem of optimal option hedging and pricing as a problem of risk minimization by hedging in a sequential Markov Decision Process (MDP). When transition probabilities and a reward function are known, such model can be solved by means of DP. This produces a semi-analytical solution for the option price and hedge, which only involves matrix linear algebra for a numerical implementation [1].

On the other hand, we might know only the general structure of a MDP model, but not its specifications such as transition probability and reward function. In this case, we should solve a Bellman optimality equation for such MDP model relying only on samples of data. This is a setting of Reinforcement Learning, see e.g. a book by Satton and Barto [9].

It turns out that in such data-driven and model-free setting, the QLBS model can be solved (also semi-analytically) by the celebrated Q-Learning method of Watkins [2, 3]. In recognition of the fact that Q-Learning produces both the optimal price and optimal hedge in such time-discretized (and distribution-free) version of the BS model, we called the model developed in Ref. [1] the QLBS model.

While Ref. [1] focused on Mathematical Q-Learning (”MaQLear”) for the QLBS model, here we expand on several topics with a Numerical Q-Learning (”NuQLear”) analysis of the model. First, we investigate the performance of Fitted Q Iteration (FQI) for a RL (data-driven) solution to the model, and benchmark it versus a DP (model-based) solution, as well as versus the BSM model. Second, we extend the model to a setting of Inverse Reinforcement Learning (IRL), where we only observe prices and actions (re-hedges) taken by a trader, but not rewards. Third, we outline how the QLBS model can be used for pricing portfolios of options, rather than a single option in isolation. This requires mutual consistency of pricing of different options in a portfolio. We show how the QLBS model addresses this problem, i.e. solves the (in)famous volatility smile problem of the Black-Scholes model.

The paper is organized as follows. In Sect. 2, we give a summary of the QLBS model, and present both a DP-based and RL-based solutions for the model. An IRL formulation for the model is developed in Sect. 3. ”NuQLear” experiments are presented in Sect. 4. Sect. 5 outlines option hedging and pricing in the QLBS model in a multi-asset (portfolio) setting. Finally, we conclude in Sect. 6.

2 The QLBS model

The QLBS model starts with a discrete-time version of the BSM model, where we take the view of a seller of a European option (e.g. a put option) with maturity and a terminal payoff of at maturity, that depends on a final stock price at that time. To hedge the option, the seller use the proceeds of the sale to set up a replicating (hedge) portfolio made of the stock and a risk-free bank deposit . The value of the hedge portfolio at any time is

| (1) |

where is a position in the stock at time , taken to hedge risk in the option. As at the option position should be closed, we set , which produces a terminal condition at :

| (2) |

Instead of (non-stationary) stock price , we prefer to use time-homogeneous variables as state variables in the model, where and are related as follows:

| (3) |

2.1 Optimal value function

As was shown in [1], the problem of optimal option hedging and pricing in such discrete-time setting can be formulated as a problem of Stochastic Optimal Control (SOC) where a value function to be maximized is given by the following expression:

| (4) |

where is a Markowitz-like risk aversion parameter [10], means an information set of all Monte Carlo (or real) paths of the stock at time , and the upper-script stands for a policy that maps the time and the current state into an action :

| (5) |

As shown in [1], the value function (4) satisfies the following Bellman equation:

| (6) |

where the one-step time-dependent random reward is defined as follows:

| (7) | |||||

where , where is the sample mean of all values of , and similarly for . For , we have where is determined by the terminal condition (2).

An optimal policy is determined as a policy that maximizes the value function :

| (8) |

The optimal value function corresponding to the optimal policy satisfies the Bellman optimality equation

| (9) |

Once it is solved, the (ask) option price is minus the optimal value function: .

If the system dynamics are known, the Bellman optimality equation can be solved using methods of Dynamic Programming such as Value Iteration. If, on the other hand, dynamics are unknown and the optimal policy should be computed using samples, which is a setting of Reinforcement Learning, then a formalism based on an action-value function, to be presented next, provides a better framework for Value Iteration methods.

2.2 Action-value function

The action-value function, or Q-function, is defined by an expectation of the same expression as in the definition of the value function (4), but conditioned on both the current state and the initial action , while following a policy afterwards:

| (10) | |||

The Bellman equation for the Q-function reads [1]

| (11) |

An optimal action-value function is obtained when (10) is evaluated with an optimal policy :

| (12) |

The optimal value- and state-value functions are connected by the following equations

| (13) | |||

The Bellman Optimality equation for the action-value function is obtained by substituting the first of Eqs.(13) into the second one:

| (14) |

with a terminal condition at given by

| (15) |

where is determined by the terminal condition (2). A ”greedy” policy that is used in the QLBS model always seeks an action that maximizes the action-value function in the current state:

| (16) |

2.3 DP solution for the optimal Q-function

If transition probabilities to compute the expectation in the right-hand side of the Bellman optimality equation (14) are known, then the Bellman equation (14) can be solved, jointly with the optimal policy (16), using backward recursion starting from and the terminal condition (15). This can be used for benchmarking in our test environment where we do know these probabilities, and know the rewards function (7).

Substituting the one-step reward (7) into the Bellman optimality equation (14) we find that is quadratic in the action variable :

| (17) | |||||

As is a quadratic function of , the optimal action (i.e. the hedge) that maximizes is computed analytically:

| (18) |

Plugging Eq.(18) back into Eq.(17), we obtain an explicit recursive formula for the optimal action-value function:

| (19) |

where is defined in Eq.(18).

In practice, the backward recursion expressed by Eqs.(19) and (18) is solved in a Monte Carlo setting, where we assume to have access to simulated (or real) paths for the state variable [1]. In addition, we assume that we have chosen a set of basis functions .

We can then expand the optimal action (hedge) and optimal Q-function in basis functions, with time-dependent coefficients:

| (20) |

Coefficients and are computed recursively backward in time for . The results are given by the following expressions:

| (21) |

where

| (22) |

and

| (23) |

where

| (24) |

Equations (21) and (23), computed jointly and recursively for , provide a practical implementation of the DP-based solution to the QLBS model using expansions in basis functions. This approach can be used to find optimal price and optimal hedge when the dynamics are known. For more details, see Ref. [1].

2.4 RL solution for QLBS: Fitted Q Iteration

Reinforcement Learning (RL) solves the same problem as Dynamic Programming (DP), i.e. it finds an optimal policy. But unlike DP, RL does not assume that transition probabilities and reward function are known. Instead, it relies on samples to find an optimal policy.

Our setting assumes a batch-mode learning, when we only have access to some historically collected data. The data available is given by a set of trajectories for the underlying stock (expressed as a function of using Eq.(3)), hedge position , instantaneous reward , and the next-time value :

| (25) |

We assume that such dataset is available either as a simulated data, or as a real historical stock price data, combined with real trading data or artificial data that would track the performance of a hypothetical stock-and-cash replicating portfolio for a given option.

We use a popular batch-model Q-Learning method called Fitted Q Iteration (FQI) [11, 12]. A starting point in this method is a choice of a parametric family of models for quantities of interest, namely optimal action and optimal action-value function. We use linear architectures where functions sought are linear in adjustable parameters that are next optimized to find the optimal action and action-value function.

We use the same set of basis functions as we used above in Sect. 2.3 . As the optimal Q-function is a quadratic function of , we can represent it as an expansion in basis functions, with time-dependent coefficients parametrized by a matrix :

| (32) | |||||

| (33) |

Eq.(32) is further re-arranged to convert it into a product of a parameter vector and a vector that depends on both the state and the action:

| (34) | |||||

Here stands for an element-wise (Hadamard) product of two matrices. The vector of time-dependent parameters is obtained by concatenating columns of matrix , and similarly, stands for a vector obtained by concatenating columns of the outer product of vectors and .

Coefficients can then be computed recursively backward in time for [1]:

| (35) |

where

| (36) |

To perform the maximization step in the second equation in (2.4) analytically, note that because coefficients and hence vectors (see Eq.(32)) are known from the previous step, we have

| (37) |

It is important to stress here that while this is a quadratic expression in , it would be completely wrong to use a point of its maximum as a function of as such optimal value in Eq.(37). This would amount to using the same dataset to estimate both the optimal action and the optimal Q-function, leading to an overestimation of in Eq.(2.4), due to Jensen’s inequality and convexity of the function. The correct way to use Eq.(37) is to plug there a value of computed using the analytical solution Eq.(18), applied at the previous time step. Due to availability of the analytical optimal action (18), a potential overestimation problem, a classical problem of Q-Learning that is sometimes addressed using such methods as Double Q-Learning [13], is avoided in the QLBS model, leading to numerically stable results.

3 Inverse Reinforcement Learning in QLBS

Inverse Reinforcement Learning (IRL) provides a very interesting and useful extension of the (direct) RL paradigm. In the context of batch-mode learning used in this paper, a setting of IRL is nearly identical to the setting of RL (see Eq.(25)), except that there is no information about rewards:

| (38) |

The objective of IRL is typically two-fold: (i) find rewards that would be most consistent with observed states and action, and (ii) (the same as in RL) find the optimal policy and action-value function. One can distinguish between on-policy IRL and off-policy IRL. In the former case, we know that observed actions were optimal actions. In the latter case, observed actions may not necessarily follow an optimal policy, and can be sub-optimal or noisy.

In general, IRL is a harder problem than RL. Indeed, not only we have to find optimal policy from data, which is the same task as in RL, but we also have to do it without observing rewards. Furthermore, the other task of IRL is to find a (the?) reward function corresponding to an observed sequence of states and actions. Note that situations with missing reward information are probably encountered more frequently in potential applications of RL/IRL than observable rewards. In particular, this is typically the case when RL methods are applied to study human behavior, see e.g. [14]. IRL is also widely used in robotics as a useful alternative to direct RL methods via training robots by demonstrations, see e.g. [15].

It appears that IRL offers a very attractive, at least conceptually, approach for many financial applications that consider rational agents involved in a sequential decision process, where no information about rewards received by an agent is available to a researcher. Some examples of such (semi- ?) rational agents would be loan or mortgage borrowers, deposit or saving account holders, credit card holders, consumers of utilities such as cloud computing, mobile data, electricity, etc.

In the context of trading applications, such IRL setting may arise when a trader wants to learn a strategy of a counterparty. She observes counterparty’s actions in their bilateral trades, but not counterparty’s rewards. Clearly, if she reverse-engineered most likely counterparty’s rewards from observed actions to find counterparty’s objective (strategy), she could use it to design her own strategy. This is a typical IRL problem.

While typically IRL is a harder problem than RL, and both are computationally hard, in the QLBS model both are about equally easy, due to a quadratic form of both the reward function (7) and action-value function (17). Moreover, the general IRL setting, where only states and actions, but not rewards, are observed in a dataset, is exactly in between of our two previous settings: a DP setting where we only observe states, and a RL setting where we observe states, actions, and rewards.

The main difference is that in the DP setting we know model dynamics, including in particular the risk aversion parameter , while in the setting of RL or IRL is unknown. Therefore, we will first assume that is known, and outline how IRL should proceed with the QLBS model, and then we will discuss ways to estimate from data.

In the IRL setting, once we have observed states and actions , rewards corresponding to these actions can be obtained, if is known, in the same way they were computed in Eq.(7). The only difference is that while in the DP solution of Sec. 2.3 we computed rewards (7) for optimal actions (18), in the IRL setting we would use observed actions to plug into Eq.(7) to compute the corresponding rewards. After that, the algorithm proceeds in the same way as the FQI solution of Sect. 2.4, using these computed rewards instead of observed rewards in Eq.(2.4). Clearly, this produces identical RL and IRL solutions of the QLBS model, as long as implied in observed rewards in the RL case is the same used in Eq.(7) by the IRL solution.

This means that the first problem of IRL, i.e. finding a reward function, amounts for the QLBS model to finding just one parameter using Eq.(7). This can be done using an approach that we present next.

3.1 Maximum Entropy IRL

A simple method to estimate the one-step reward function (7) by estimating its parameter is based on a highly tractable version of a popular Maximum Entropy (MaxEnt) IRL method [16] that was developed in [17] in a different context.

We start with writing expected rewards corresponding to Eq.(7) as follows

| (39) |

where, omitting for brevity the dependence on , we defined

| (40) |

The MaxEnt method of [17] assumes that one-step probabilities of observing different actions in data are described by an exponential model

| (41) |

where is a normalization factor.

Thus, by combining an exponential distribution of the MaxEnt method with the quadratic expected reward (39), we ended up with a Gaussian action distribution (41) for IRL in QLBS. Clearly this is very good news given the amount of tractability of Gaussian distributions. Using Eq.(41), the log-likelihood of observing data is (omitting a constant factor in the second expression)

| (42) |

where with stands for expressions (40) evaluated on the -th path. As this is a concave function of , its unique maximum can be easily found numerically using standard optimization packages.

Note that optimization in Eq.(42) refers to one particular value of , therefore this calculation can be repeated independently for different times , producing a curve that could be viewed as a term structure of implied risk aversion parameter.

It can also be noticed that while Eq.(41) describes a probabilistic Gaussian policy (action probability), in Sect. 2.4 we used the deterministic ”greedy” policy (16). Therefore, if we used a value of estimated with Eq.(42) in the IRL algorithm described above, this may not produce the same result as the RL approach of Sect. 2.4. Policy assumptions can be made more consistent between the RL and IRL approaches if instead of Q-Learning (in the form of Fitted Q Iteration) that we used in Sect. 2.4, we switched to G-Learning [18] that replaces the ”greedy max” term in Eq.(2.4) with a ”soft-greedy max” term for a G-function:

| (43) |

where is an ”inverse temperature” parameter of G-Learning [18]. We leave G-Learning in the QLBS model for a future research.

4 NuQLear experiments

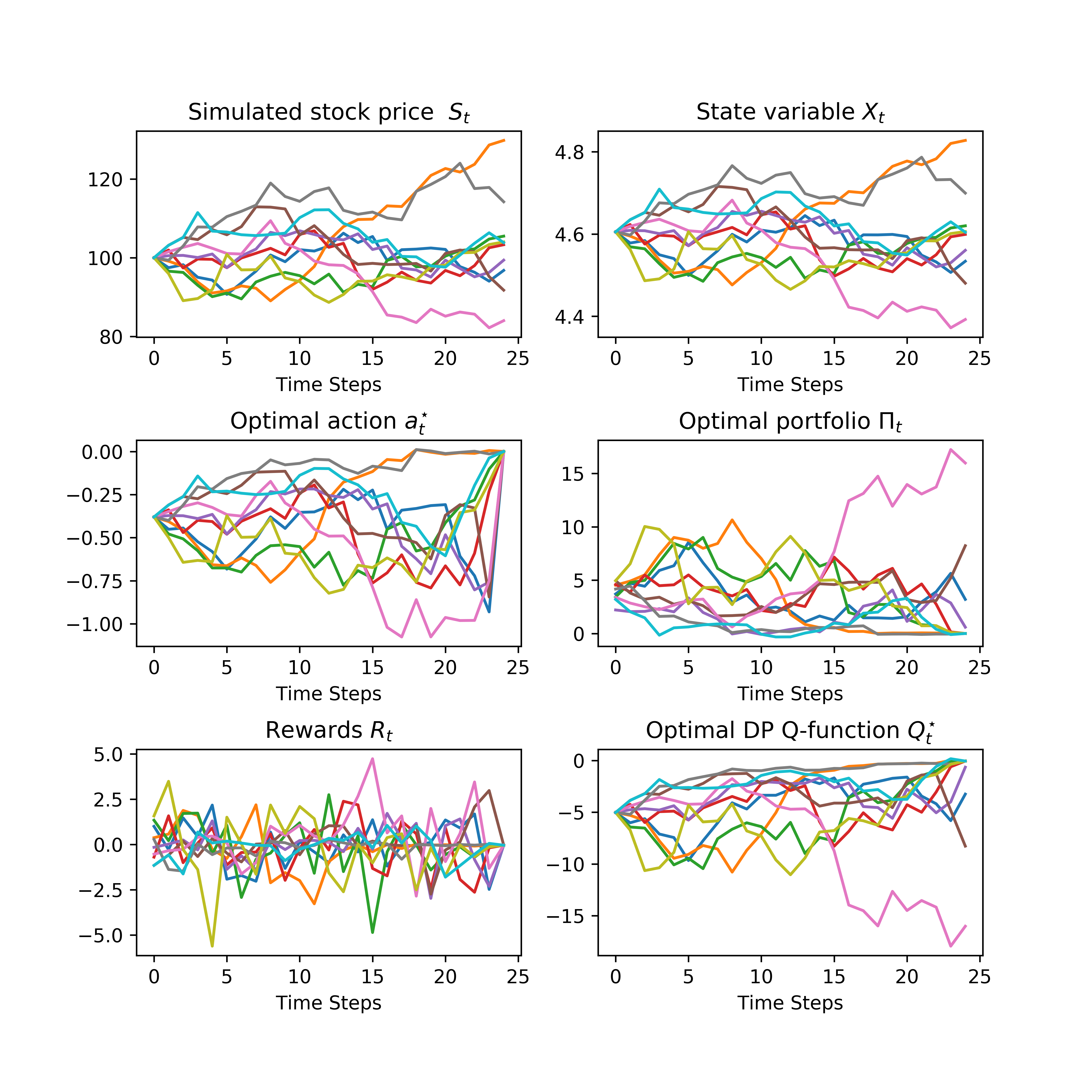

We illustrate the numerical performance of the model in different settings (DP, RL, IRL) using simulated stock price histories with the initial stock price , stock drift , and volatility . Option maturity is year, and a risk-free rate is . We consider an ATM (”at-the-money”) European put option with strike . Re-hedges are done bi-weekly (i.e. ). We use Monte Carlo scenarios for a path of the stock, and report results obtained with two MC runs, where the error reported is equal to one standard deviation calculated from these runs. In our experiments, we use pure risk-based hedges, i.e. omit the second term in Eq.(18) to facilitate comparison with the BSM model.

We use 12 basis functions chosen to be cubic B-splines on a range of values of between the smallest and largest values observed in a dataset.

4.1 DP solution

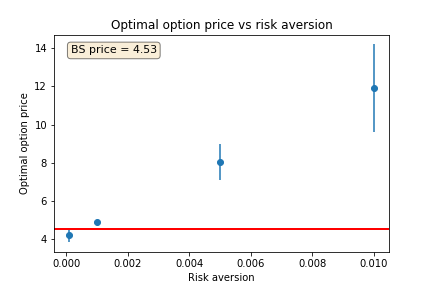

In our experiments below, we pick the Markowitz risk aversion parameter . This provides a visible difference of QLBS prices from BS prices, while being not too far away from BS prices. The dependence of the ATM option price on is shown in Fig. 1.

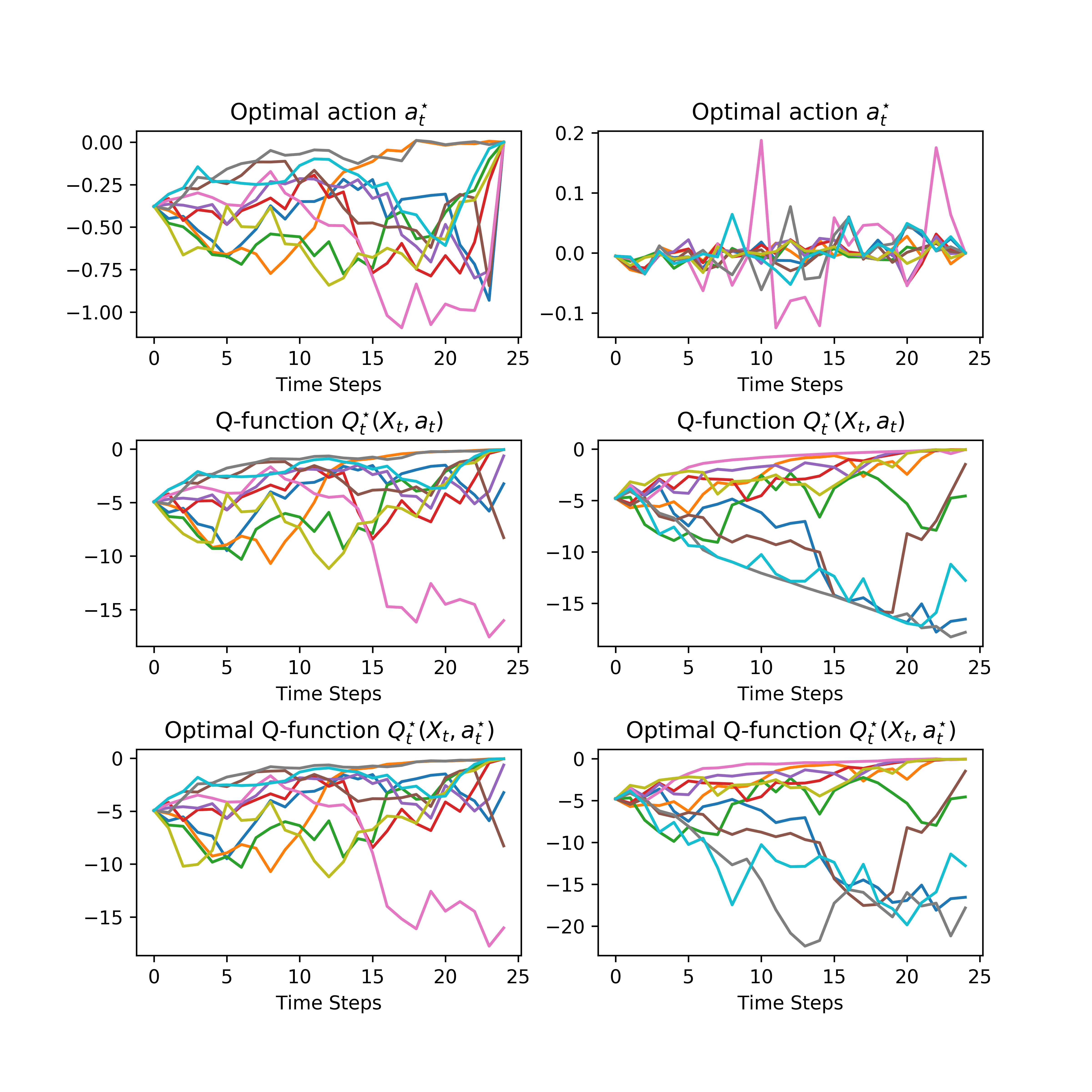

Simulated path and solutions for optimal hedges, portfolio values, and Q-function values corresponding to the DP solution of Sect. 2.3 are illustrated in Fig. 2. In the numerical implementation of matrix inversion in Eqs.(21) and (23), we used a regularization by adding a unit matrix with a regularization parameter of .

The resulting QLBS ATM put option price is (based on two MC runs), while the BS price is 4.53.

4.2 On-policy RL/IRL solutions

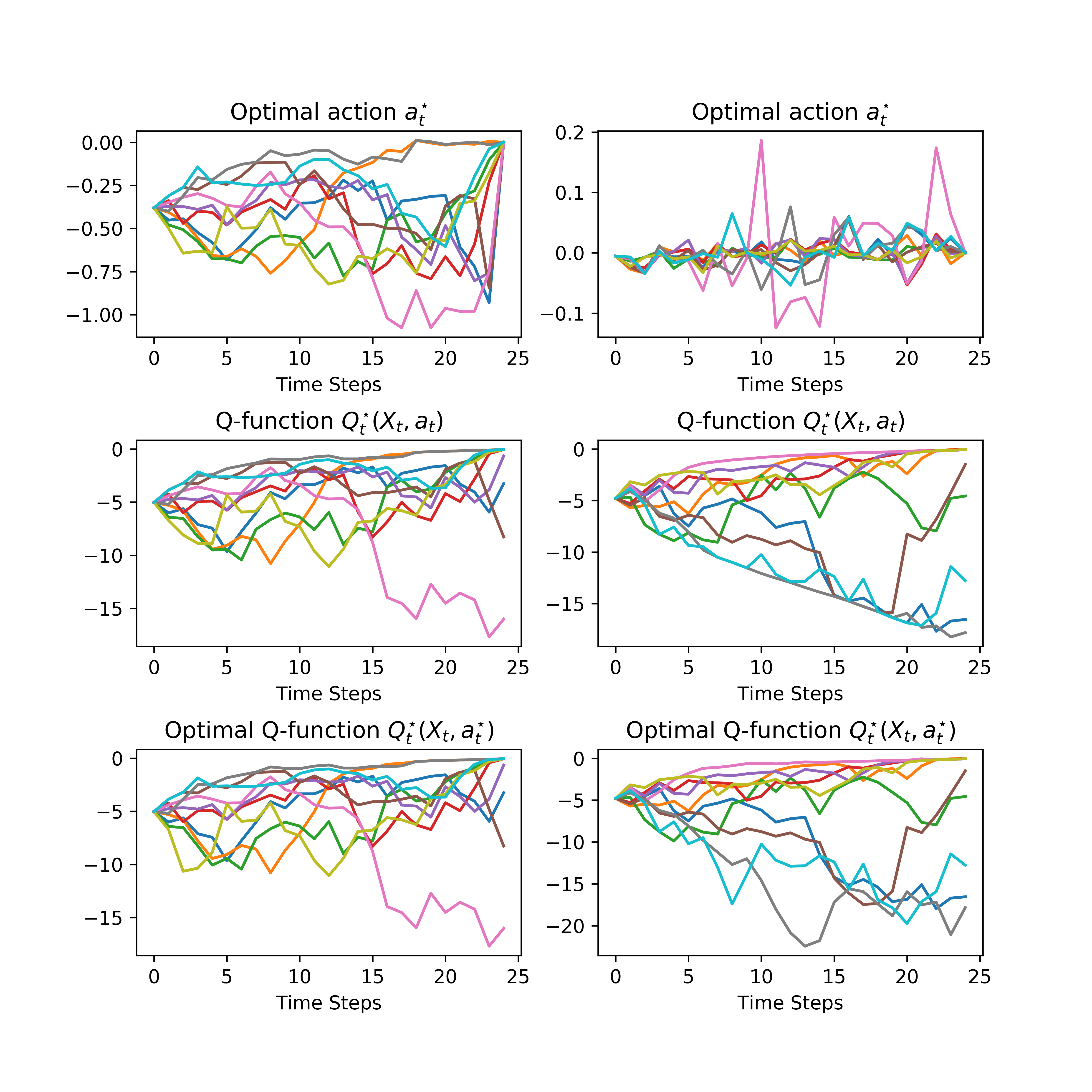

We first report results obtained with on-policy learning. In this case, optimal actions and rewards computed as a part of a DP solution are used as inputs to the Fitted Q Iteration algorithm Sect. 2.4 and the IRL method of Sect. 3, in addition to the paths of the underlying stock. Results of two MC runs with Fitted Q Iteration algorithm of Sect. 2.4 are shown in Fig. 3. Similarly to the DP solution, we add a unit matrix with a regularization parameter of to invert matrix in Eq.(35). Note that because here we deal with on-policy learning, the resulting optimal Q-function and its optimal value are virtually identical in the graph.

The resulting QLBS RL put price is which is identical to the DP value. As expected, the IRL method of Sect. 3 produces the same result.

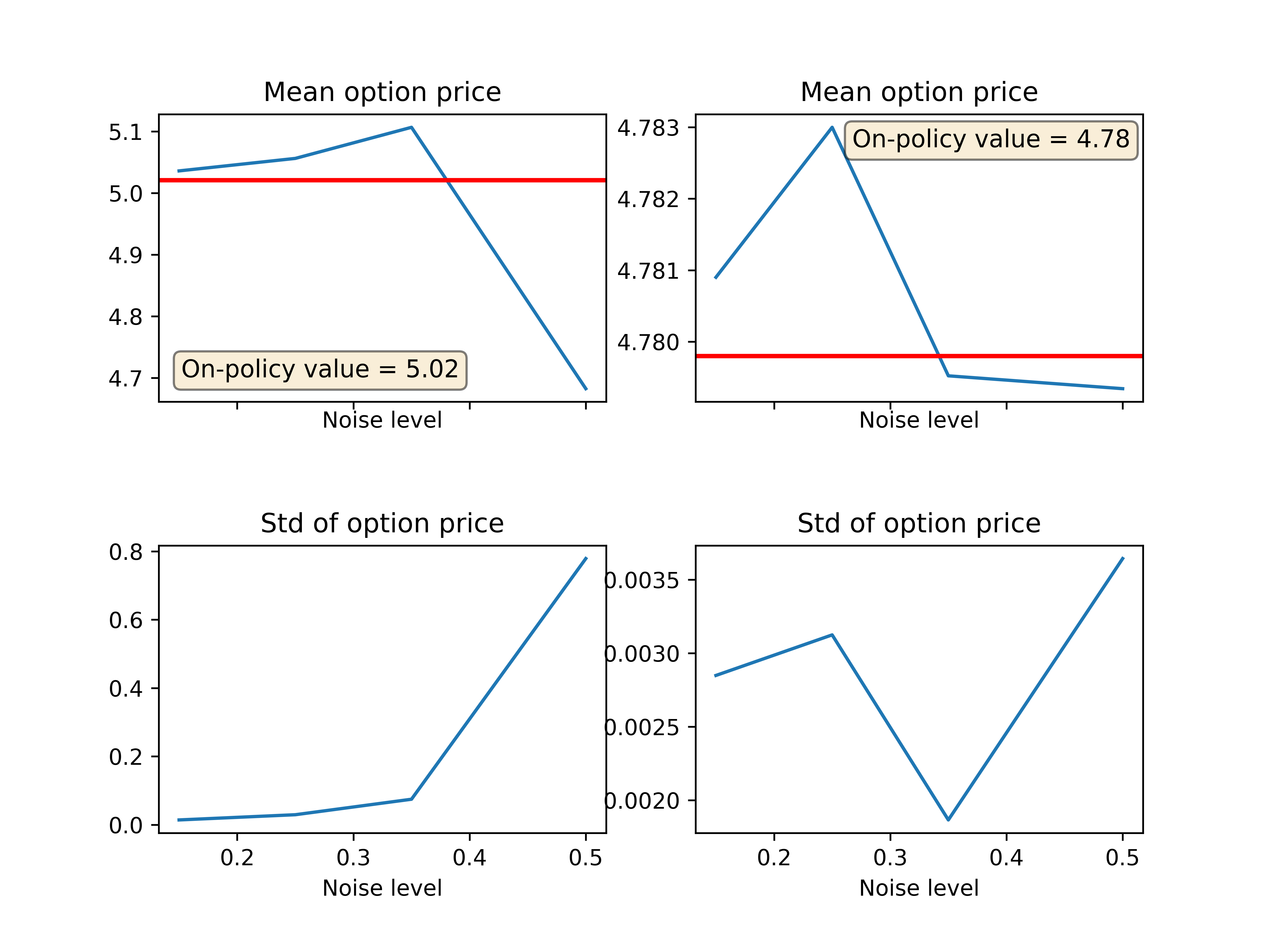

4.3 Off-policy RL solution

In the next set of experiments we deal with off-policy learning. To make off-policy data, we multiply, at each time step, optimal hedges computed by the DP solution of the model by a random uniform number in the interval where is a parameter controlling the noise level in the data. We will consider the values of to test the noise tolerance of our algorithms. Rewards corresponding to these sub-optimal actions are obtained using Eq.(7). In Fig. 4 we show results obtained for off-policy learning with 5 different scenarios of sub-optimal actions. Note that while some non-monotonicity in these graphs is due to a low number of scenarios, we note that the impact of sub-optimality of actions in recorded data is rather mild, at least for a moderate level of noise in actions. This is as expected as long as Fitted Q Iteration is an off-policy algorithm. This implies that when dataset is large enough, the QLBS model can learn even from data with purely random actions, and, in particular, learn the BSM model itself, if the world is lognormal [1].

Results of two MC runs for off-policy learning with the noise parameter with Fitted Q Iteration algorithm are shown in Fig. 5.

5 Option portfolios

While above and in [1] we looked at the problem of hedging and pricing of a single European option by an option seller that does not have any pre-existing option portfolio, here we outline a simple generalization to the case when the option seller does have such pre-existing option portfolio, or alternatively if she wants to sell a few options simultaneously222The context of this section was previously presented in a separate note ”Relative Option Pricing in the QLBS Model” (https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3090608)..

In this case, she needs to worry about consistency of pricing and hedging of all options in her new portfolio. In other words, she has to solve the dreaded volatility smile problem for her particular portfolio. Here we will show how she can do it in a worry-free way using the QLBS model.

Assume the option seller has a pre-existing portfolio of options with market prices . All these options reference an underlying state vector (market) which can be high-dimensional such that each particular option with references only one or a few components of market state .

Alternatively, we can add vanilla option prices as components of the market state . In this case, our dynamic replicating portfolio would include vanilla options, along with underlying stocks. Such hedging portfolio would provide a dynamic generalization of static option hedging for exotics introduced by Carr et. al. [19].

We assume that we have a historical dataset that includes observations of trajectories of tuples of vector-valued market factors, actions (hedges), and rewards (compare with Eq.(25)):

| (44) |

Now assume the option seller wants to add to this pre-existing portfolio another (exotic) option (or alternatively, she wants to sell a portfolio of options ). Depending on whether the exotic option was traded before in the market or not, there are two possible scenarios. We will look at them one by one.

In the first case, the exotic option was previously traded in the market (by the seller herself, or by someone else). As long as its deltas and related P&L impacts marked by a trading desk are available, we can simply extend vectors of actions and rewards in Eq.(44), and then proceed with the FQI algorithm of Sect. 2.4 (or with the IRL algorithm of Sect. 3, if rewards are not available). The outputs of the algorithm will be optimal price of the whole option portfolio, plus optimal hedges for all options in the portfolio. Note that as long as FQI is an off-policy algorithm, it is quite forgiving to human or model errors: deltas in the data should not even be perfectly mutually consistent (see single-option examples in the previous section). But of course, the more consistency in the data, the less data is needed to learn an optimal portfolio price .

Once the optimal time-zero value of the total portfolio is computed, a market-consistent price for the exotic option is simply given by a subtraction:

| (45) |

Note that by construction, the price is consistent with all option prices and all their hedges, to the extent they are consistent between themselves (again, this is because Q-Learning is an off-policy algorithm).

Now consider a different case, when the exotic option was not previously traded in the market, and therefore there are no available historical hedges for this option. This can be handled by the QLBS model in essentially the same way as in the previous case. Again, because Q-Learning is an off-policy algorithm, it means that a delta and a reward of a proxy option (that was traded before) to could be used in the scheme just described in lieu of their actual values for option . Consistently with a common sense, this will just slow down the learning, so that more data would be needed to compute the optimal price and hedge for the exotic . On the other hand, the closer the traded proxy to the actual exotic the option seller wants to hedge and price, the more it helps the algorithm on the data demand side. Finally, when rewards for the are not available, we can use the IRL methods of Sect. 3.

6 Summary

In this paper, we have provided further extensions of the QLBS model developed in [1] for RL-based, data-driven and model-independent option pricing, including some topics for ”NuQLear” (Numerical Q-Learning) experimentations with the model. In particular, we have checked the convergence of the DP and RL solutions of the model to the BSM results in the limit .

We looked into both on-policy and off-policy RL for option pricing, and showed that Fitted Q Iteration (FQI) provides a reasonable level of noise tolerance with respect to possible sub-optimality of observed actions in our model, which is in agreement with general properties of Q-Learning being an off-policy algorithm. This makes the QLBS model capable of learning to hedge and price even when traders’ actions (re-hedges) are sub-optimal or not mutually consistent for different time steps, or, in a portfolio context, between different options.

We formulated an Inverse Reinforcement Learning (IRL) approach for the QLBS model, and showed that when the Markowitz risk aversion parameter is known, the IRL and RL algorithms produce identical results, by construction. On the other hand, when is unknown, it can be separately estimated using Maximum Entropy (MaxEnt) IRL [16] applied to one-step transitions as in [17]. While this does not guarantee identical results between the RL and IRL solutions of the QLBS model, this can be assured again by using G-Learning [18] instead of Q-Learning in the RL solution of the model.

Finally, we outlined how the QLBS model can be used in the context of option portfolios. By relying on Q-Learning and Fitted Q Iteration, which are model-free methods, the QLBS model provides its own, data-driven and model independent solution to the (in)famous volatility smile problem of the Black-Scholes model. While fitting the volatility smile and pricing options consistently with the smile is the main objective of Mathematical Finance option pricing models, this is just a by-product for the QLBS model. This is because the latter is distribution-free, and is therefore capable of adjusting to any smile (a set of market quotes for vanilla options). As was emphasized in the Introduction and in [1], the main difference between all continuous-time option pricing models of Mathematical Finance (including the BSM model and its various local and stochastic volatility extensions, jump-diffusion models, etc.) and the QLBS model is that while the former try to ”match the market”, they remain clueless about the expected risk in option positions, while the QLBS model makes the risk-return analysis of option replicating portfolios the main focus of option hedging and pricing, similarly to how such analysis is applied for stocks in the classical Markowitz portfolio theory [10].

References

- [1] I. Halperin, ”QLBS: Q-Learner in the Black-Scholes (-Merton) Worlds”, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3087076 (2017).

- [2] C.J. Watkins, Learning from Delayed Rewards. Ph.D. Thesis, Kings College, Cambridge, England, May 1989.

- [3] C.J. Watkins and P. Dayan, ”Q-Learning”, Machine Learning, 8(3-4), 179-192, 1992.

- [4] F. Black and M. Scholes, ”The Pricing of Options and Corporate Liabilities”, Journal of Political Economy, Vol. 81(3), 637-654, 1973.

- [5] R. Merton, ”Theory of Rational Option Pricing”, Bell Journal of Economics and Management Science, Vol.4(1), 141-183, 1974.

- [6] P. Wilmott, Derivatives: The Theory and Practive of Financial Engineering, Wiley 1998.

- [7] R.J. Scherrer, ”Time Variation of a Fundamental Dimensionless Constant”, http://lanl.arxiv.org/pdf/0903.5321.

- [8] S. Das, Traders, Guns, and Money, Prentice Hall (2006).

- [9] R. S. Sutton and A. G. Barto, Reinforcement Learning: An Introduction, A Bradford Book (1998).

- [10] H. Markowitz, Portfolio Selection: Efficient Diversification of Investment, John Wiley, 1959.

- [11] D. Ernst, P. Geurts, and L. Wehenkel, ”Tree-Based Batch Model Reinforcement Learning”, Journal of Machine Learning Research, 6, 405-556, 2005.

- [12] S.A. Murphy, ”A Generalization Error for Q-Learning”, Journal of Machine Learning Research, 6, 1073-1097, 2005.

- [13] H. van Hasselt, ”Double Q-Learning”, Advances in Neural Information Processing Systems, 2010 (http://papers.nips.cc/paper/3964-double-q-learning.pdf).

- [14] S. Liu, M. Araujo, E. Brunskill, R. Rosetti, J. Barros, and R. Krishnan, ”Undestanding Sequential Decisions via Inverse Reinforcement Learning”, 2013 IEEE 14th International Conference on Mobile Data Management.

- [15] J. Kober, J. A. Bagnell, and J. Peters, ”Reinforcement Learning in Robotics: a Survey”, International Journal of Robotic Research, vol. 32, no. 11 (2013), pp. 1238-1278.

- [16] B.D. Ziebart, A. Maas, J.A. Bagnell, and A.K. Dey, ”Maximum Entropy Inverse Reinforcement Learning” (2008), AAAI, p. 1433-1438 (2008).

- [17] I. Halperin, ”Inverse Reinforcement Learning for Marketing” , https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3087057 (2017).

- [18] R. Fox, A. Pakman, and N. Tishby, ”Taming the Noise in Reinforcement Learning via Soft Updates”, https://arxiv.org/pdf/1512.08562.pdf (2015).

- [19] P. Carr, K. Ellis, V. Gupta, ”Static Hedging of Exotic Options”, Journal of Finance, 53, 3 (1998), pp. 1165-1190.