rcss : Subgradient and duality approach for dynamic programming

Abstract.

This short paper gives an introduction to the rcss package. The R package rcss provides users with a tool to approximate the value functions in the Bellman recursion using convex piecewise linear functions formed using operations on tangents. A pathwise method is then used to gauge the quality of the numerical results.

Keywords. Convexity, Dynamic programming, Duality, Subgradient

1. Introduction

Sequential decision making is often addressed under the framework of Markov Decision Processes/Dynamic Programming. However, deriving analytical solutions for even some of the simplest decision processes may be too cumbersome [13, 1, 12]. The use of numerical approximations may be far more practical given the rapid improvements in everyday computational power. The ability to gauge the quality of these approximations is also of significant practical importance. This paper will describe the implementation of fast and accurate algorithms to address these issues for Markov decision processes within a finite time setting, finite action set, convex reward functions and whose Markov processes follow linear dynamics. Under certain conditions, [5] showed that these value function approximations enjoy uniform convergence on compact sets. The package rcss represents a R implementation of these methods and has already been used to address problems such as pricing financial options [7], natural resource extraction [6], battery management [9], optimal portfolio liquidation [8] and optimal asset allocation under hidden state dynamics [10]. One of the major benefits of implementing these methods in R [14] is that the results can be analysed using the vast number of statistical tools avaliable in this language. The R package can be found here: https://github.com/YeeJeremy/rcss and the manual is listed at https://github.com/YeeJeremy/RPackageManuals/blob/master/rcss-manual.pdf.

2. Problem Setting

Suppose that state space is the product of a finite set and an open convex set . At each decision time , an action is chosen by the agent and the dynamic choice of these actions influences the evolution of the Markov process where is the set of sample paths. The discrete component is assumed to be a controlled Markov chain with transition probabilities , where is the probability of transitioning from to after applying action . The second component evolves in a linear fashion given by where are matrix-valued random variables refered to as disturbances. The matrix entries in these disturbances are assumed to be integrable. At each time the decision rule is given by a mapping , prescribing at time an action for a given state . A sequence of decision rules is called a policy. For each policy , associate it with a so-called policy value defined as the total expected reward

where and are convex functions in the second argument for . These functions represent the scrap and reward in the decision problem, respectively. A policy is called optimal if it maximizes the total expected reward over all policies . To obtain such policy, one introduces for the so-called Bellman operator

acting on all functions where the expectation is defined. Consider the Bellman recursion, also referred to as backward induction:

A recursive solution to the Bellman recursion above are called value functions and they determine an optimal policy via

for .

3. Numerical Approach

Since the reward and scrap functions are convex in the continuous variable, the value functions are also convex due to the linear state dynamics and so can be approximated by convex piecewise linear functions. For this, introduce the so-called subgradient envelope of a convex function on a grid with points i.e. by

which is a maximum of the tangents of on all grid points . Using the subgradient envelope operator, define the double-modified Bellman operator as

where the probability weights corresponds to the distribution sampling of each disturbance . The corresponding backward induction

for and yields the so-called double-modified value functions . If the disturbance sampling is constructed using local averages on a partition of the disturbance space or using random Monte Carlo sampling, it can be shown that the double-modified value functions converge uniformly to the true value functions on compact sets if the grid becomes dense in . Now, to gauge the quality of the approximations from the above, we construct two random variables whose expectaions bound the true value function i.e.

| (1) |

This process exhibits a helpful self-tuning property. The the closer the value function approximations to optimality, the tighter the bounds in Equation 1 and the lower the standard errors of the bound estimates.

The R package rcss represents these convex piecewise linear functions as matrices and offers several options to use nearest neighbour algorithms (from [11]) to reduce the computational cost of the above methods. Most of the computational work is done in C++ via Rcpp [3] and is parallezied using OpenMp [2]. The following sections will demonstrate some real world applications of this R package.

4. Example: Bermuda Put

Optimal switching problems naturally arise in the valuation of financial contracts. A simple example is given by the Bermudan Put option. This option gives its owner the right but not an obligation to choose a time to exercise the option in order to receive a payment which depends on the price of the underlying asset at the exercise time. The so-called fair price of the Bermudan option is related to the solution of an optimal stopping problem (see [4]). Here, the asset price process at time steps is modelled as a sampled geometric Brownian motion

where are independent random variables following a log-normal distribution. The fair price of such option with strike price , interest rate and maturity date , is given by the solution to the optimal stopping problem

A transformation of the state space is required to be able representing the reward functions in a convenient way for the rcss package to process, thus we introduce an augmentation with 1 via

then it becomes possible to represent the evolution as the linear state dynamics

with independent and identically distributed matrix-valued random variables given by

This switching system is defined by two positions and two actions . Here, the positions ‘exercised’ and ‘not exercised’ are represented by , respectively, and the actions ‘don’t exercise’ and ‘exercise’ are denoted by and respectively. With this interpretation, the position change is given by deterministic transitions to specified states

deterministically determined by the target positions

while the rewards at time and are defined as

for all , , .

4.1. Code Example

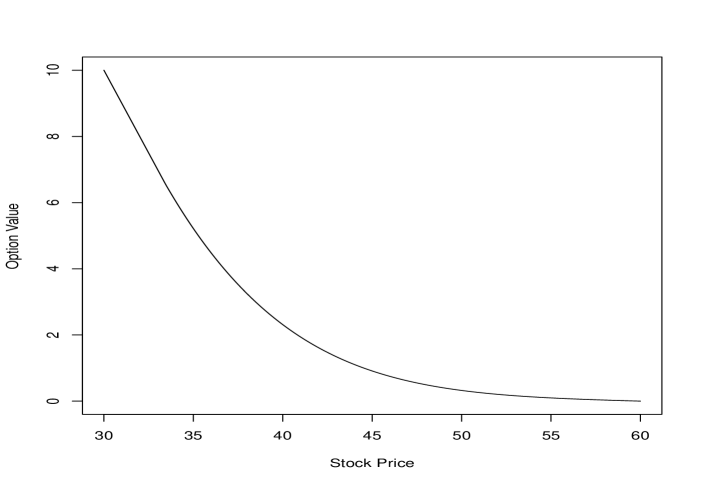

As a demonstration, let us consider a Bermuda put option with strike price 40 that expires in 1 year. The put option is exercisable at 51 evenly spaced time points in the year, which includes the start and end of the year. The following code approximates the value functions in the Bellman recursion. On a Linux Ubuntu 16.04 with Intel i5-5300U CPU @2.30GHz and 16GB of RAM, the following code takes around 0.2 cpu second and around 0.05 real world seconds.

The matrix grid represents our choice of grid points where each row represents a point. The 3-dimensional array disturb represents our sampling of the disturbances where disturb[,,i] gives the i-th sample. Here, we use local averages on a component partition of the disturbance space. The 5-dimensional array reward represents the subgradient approximation with reward[,,a,p,t] representing . The object bellman is a list containing the approximations of the value functions and expected value functions for all positions and decision epochs. Please refer to the package manual for the format of the inputs and outputs. To obtain the value function of the Bermuda put option, simply run the plot command below.

The following code then computes the lower and upper bound estimates for the value of the option when . On our machine, the following takes around cpu seconds and around real world seconds to run.

The above code takes the exact reward and scrap functions as inputs. The function FastPathPolicy computes the candidate optimal policy. The object bounds is a list containing the primals and duals for each sample path and each position at each decision time . Again, please refer to the package manual for the format of the inputs and outputs. If the price of the underlying asset is , the confidence interval for the option price is given by the following.

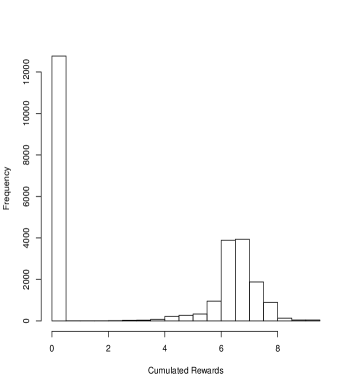

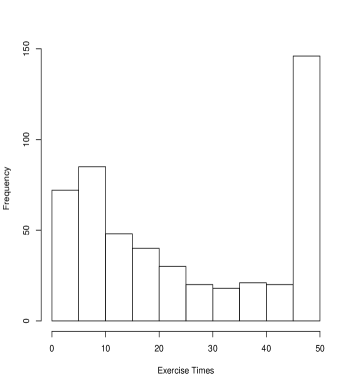

The package ’rcss’ also allows the user to test the prescribed policy from the Bellman recursion on any supplied set of sample paths. The resulting ouput can then be further studied with time series analysis or other statistical work. In the following code, we will use the previously generated sample paths to backtest our policy and generate histograms.

Figure 2 contains the histograms for the cumulated rewards and exercise times. Let us emphasise the usefulness of such scenario generation. Given an approximately optimal policy and backtesting, one can perform statistical analysis on the backtested values to obtain practical insights such as for risk analysis purposes.

5. Example: Swing Option

Let us now consider the swing option which is a financial contract popular in the energy business. In the simplest form, it gives the owner the right to obtain a certain commodity (such as gas or electricity) at a pre-specified price and volume at a number of exercise times which can be freely chosen by the contract owner. Let us consider a specific case of such contract, referred to as a unit-time refraction period swing option. In this contract, there is a limit to exercise only one right at any time. Given the discounted commodity price , the so-called fair price of a swing option with rights is given by the supremum

over all stopping times with values in . In order to represent this control problem as a switching system, we use the position set to describe the number of exercise rights remaining. That is stands for the situation when there are rights remaining to be exercised. The action set represents the choice between exercising () or not exercising (). The control matrices are given for exercise action

and for not-exercise action as

for all . In the case of the swing option, the transition between and occurs deterministically, since once the controller decides to exercise the right, the number of rights remaining is diminished by one. The deterministic control of the discrete component is easier to describe in therm of the matrix where stands for the discrete component which is reached from by the action . For the case of the swing option this matrix is

Having modelled the discounted commodity price process as an exponential mean-reverting process with a reversion parameter , long run mean and volatility , we obtain the logarithm of the discounted price process as

A further transformation of the state space is required before linear state dynamics can be achieved. If we introduce an augmentation with 1 via

then it becomes possible to represent the evolution as the linear state dynamics

with independent and identically distributed matrix-valued random variables given by

The reward and scrap values are given by

| (2) |

for and

| (3) |

respectively for all and .

5.1. Code Example

In this example, consider a swing option with rights exercisable on time points. As before, we begin by performing the value function approximation. On our machine, the following code takes around cpu seconds or around real world seconds to run.

After obtaining these function approximations, the following code computes the confidence intervals for the value of a swing option with remaining rights. The code below takes approximately cpu seconds or real world seconds to run.

6. Conclusion

This paper gives a demonstration of the R package rcss in solving optimal switching problems. The problem setting discussed in this paper is broad and can be used to model a wide range of problems. Using nearest neighbour algorithms, the package rcss is able to solve some real world problems in an accurate and quick manner.

References

- [1] N. Bauerle and U. Rieder, Markov decision processes with applications to finance, Springer, Heidelberg, 2011.

- [2] L. Dagum and R. Menon, Openmp: an industry standard api for shared-memory programming, IEEE Computational Science & Engineering 5 (1998), no. 1, 46–55.

- [3] D. Eddelbuettel and R. Francois, Rcpp: Seamless R and C++ integration, Journal of Statistical Software 40 (2011), no. 8, 1–18.

- [4] P. Glasserman, Monte Carlo methods in financial engineering, Springer, 2003.

- [5] J. Hinz, Optimal stochastic switching under convexity assumptions, SIAM Journal on Control and Optimization 52 (2014), no. 1, 164–188.

- [6] J. Hinz, T. Tarnopolskaya, and J. Yee, Commodity resource valuation and extraction: A pathwise programming approach, Preprint (Preprint).

- [7] J. Hinz and N. Yap, Algorithms for optimal control of stochastic switching systems, Theory of Probability and its Applications 60 (2015), no. 4, 770–800.

- [8] J. Hinz and J. Yee, An algorithmic approach to optimal asset liquidation problems, Asia-Pacific Financial Markets 24 (2017), no. 2, 109–129.

- [9] by same author, Optimal forward trading and battery control under renewable electricity generation, Journal of Banking & Finance InPress (2017).

- [10] by same author, Stochastic switching for partially observable dynamics and optimal asset allocation, International Journal of Control 90 (2017), no. 3, 553–565.

- [11] M. Muja and D. Lowe, Flann - fast library for approximate nearest neighbors, 2016, Version 1.9.1.

- [12] H. Pham, Continuous-time stochastic control and optimization with financial applications, vol. 61, Springer Science & Business Media, 2009.

- [13] W. Powell, Approximate dynamic programming: Solving the curses of dimensionality, Wiley, Hoboken, New Jersey, 2007.

- [14] R Core Team, R: A language and environment for statistical computing, R Foundation for Statistical Computing, 2013, ISBN 3-900051-07-0.