Urn model for products’ shares in international trade

Abstract

International trade fluxes evolve as countries revise their portfolios of trade products towards economic development. Accordingly products’ shares in international trade vary with time, reflecting the transfer of capital between distinct industrial sectors. Here we analyze the share of hundreds of product categories in world trade for four decades and find a scaling law obeyed by the annual variation of product share, which informs us of how capital flows and interacts over the product space. A model of stochastic transfer of capital between products based on the observed scaling relation is proposed and shown to reproduce exactly the empirical share distribution. The model allows analytic solutions as well as numerical simulations, which predict a pseudo-condensation of capital onto few product categories and when it will occur. At the individual level, our model finds certain products unpredictable, the excess or deficient growth of which with respect to the model prediction is shown to be correlated with the nature of goods.

I Introduction

Finite and uneven distribution of resources and capabilities for production lead a huge volume of products and capital to be exchanged across countries. The organization of such international trade has long been studied to elucidate the impact of the international relations, geography and sociocultural factors on trade fluxes Tinbergen (1962), as represented by e.g., the gravity model Anderson (2010); Barigozzi et al. (2010), as well as the topology of the trade network of countries Serrano and Boguñá (2003); Garlaschelli and Loffredo (2004).

The fluctuation of trade volumes of various products also carries valuable information on human economic activities. As a country’s portfolio of exports is crucial for both its immediate success in the global market and long-term development Hidalgo et al. (2007); Hidalgo and Hausmann (2009); Hausmann and Hidalgo (2011); Tacchella et al. (2012), political and economic agents often shift their investment strategy from one product to another, which affect the market share of related products. Aggregated together, a huge number of such strategy shifts across countries, time, and products cause fluctuations of products’ shares, which can provide a clue for understanding a principle of capital management towards best benefiting from producing and exporting selected goods.

Here we report our finding of a scaling behavior of the annual variation of trade products’ shares in international trade. It is shown to imply that capital invested for various product categories, identified here with their shares, tends to move to and from popular products, the probability of which is quadratically proportional to their current shares. A stochastic model of such biquadratic transfer of discretized capital among products is proposed, which reproduces the empirical distribution and evolution of product share, confirming that the shifts of investment strategy are made mostly referring to the current shares of products. Random transfer models have been similarly proposed to explain the distribution of wealth among individuals or countries Yakovenko and Rosser Jr (2009); Bouchaud and Mézard (2000). The functional form of the transfer rate determines whether the system is either in the fluid phase or the condensate phase with the biquadratic one at the boundary. Analytic solutions and simulation results reveal the possibility of condensation of capital onto few key products and predict its time scale. Therefore the studied model can be used as a framework helping understand and analyze the overwhelming complexity of international trade.

II Distribution and annual variation of product share

We analyze the NBER-UN dataset Feenstra et al. (2005), which contains trade volumes of product types based on the Standard International Trade Classification (SITC Rev. 2) and consistently reported over the period 1962-2000. A single datum is the amount of trade (in nominal dollars) from country to country in product category in the year . We investigate product share

| (1) |

which is the fraction of the total amount of money involved in trade worldwide that is exchanged with product , and thus represents the popularity of this product in the global economy. While the total trade volume grows exponentially, we are here interested in the investment-strategy shifts among various product categories, which are entirely contained in the dynamics of .

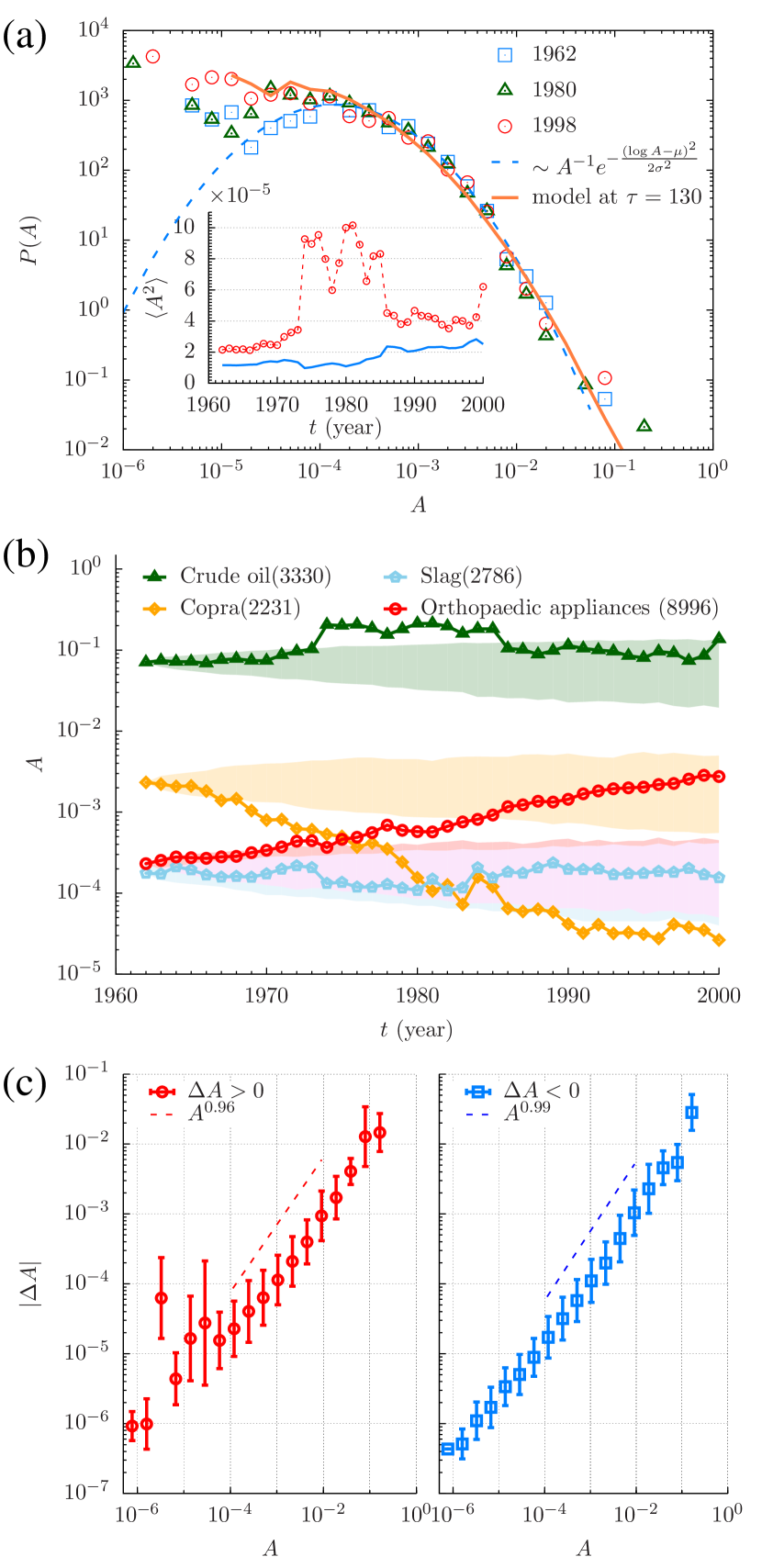

Remarkably a small number of products occupy a large fraction of total trade Mantegna and Stanley (1995). Crude oil (SITC 3330) is the category with the largest share, retaining close to of all trade for the whole period. By contrast, the share for e.g. the category of slag and similar waste (SITC 2786) never exceeds . The general shape of the probability density function of product share is close to a lognormal function as shown in Fig. 1 (a) or a stretched-exponential function Clauset et al. (2009); Alstott et al. (2014).

Many products’ share exhibits significant variation over time, as in the case of orthopedic appliances (8996) and copra (2231) which display steady growth and decline respectively over orders of magnitude in their shares [Fig. 1 (b)]. We find that the annual variation of the share of an individual product category , when averaged over gains () or losses (), is found to be proportional to the current share as

| (2) |

with [Fig. 1 (c)]. For so small as , the gain of product share shows fluctuations. The linear scaling in Eq. (2) appears also in other economic time series Gibrat (1931); Mantegna and Stanley (1995). Considering as approximating the time average of in the period between and and as the standard deviation in the same period, we find Eq. (2) represent the fluctuation scaling with , which has been investigated for diverse complex systems de Menezes and Barabási (2004); Eisler et al. (2008); Kendal and Jørgensen (2011) under such names as Gibrat’s law Gibrat (1931) or Taylor’s law Taylor (1961). Though simple, Eq. (2) has far-reaching implications for the underlying dynamics of capital invested for product categories, which we address in the next sections.

III Urn model

Differentiated evolution of individual product share arise from a huge number of microscopic changes of investment made by companies and countries, which can be modeled as independent trajectories subject to non-gaussian stochasticity Mantegna and Stanley (1995) or as emerging from exchange between individuals Yakovenko and Rosser Jr (2009); Bouchaud and Mézard (2000). We take the latter approach to understand the origin of the empirical features of product share presented in Sec. II.

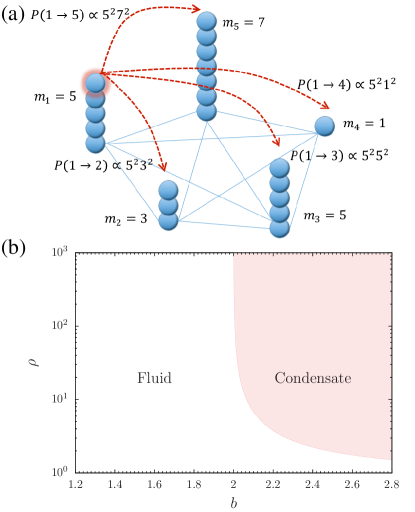

As the first step of modeling the kinetics of product share, we discretize the product share by introducing a unit share , representing the amount available for a single strategic change. Then we find the continuous share discretized to particles, resulting in a total of particles distributed over urns or sites (products). Transferring a particle from a site to another represents the flow of capital between them caused by the change of investment strategy of microscopic agents on a short time scale. We assume that those share particles hop from a site to another stochastically and independently. Such a particle-hopping model can be classified as the urn model Godreche and Luck (2002); Evans and Hanney (2005) in which a site sends one of its particles to another site with rate varying with both the departure and destination site [Fig. 2 (a)].

III.1 Biquadratic transfer rate

The transfer rate can be determined to satisfy Eq. (2). A sequence of particle jumps in or out of a site sums up to increase or decrease the number of particles at by as in random walks Hughes (1995). Therefore the linear scaling in Eq. (2) can be reproduced if a site is selected times per unit time. This reasoning leads us to the transfer rate being biquadratic in the numbers of particles at and . That is, in

| (3) |

If , sites are uniformly selected, the number of particles at a site follows the Boltzmann distribution in the stationary state with the particle density Yakovenko and Rosser Jr (2009). If , sites are given unequal chances for particle hopping. If we consider particle hopping as occurring due to attraction between particles and assume that is proportional to the sum of those attractions between all pairs of particles at site and , we find that individual particles attract one another with equal strength for . The quadratic scaling , reproducing the linear scaling in Eq. (2), implies inhomogeneous interaction between particles; the interaction between a particle at site and another at is proportional to . It should be mentioned that a site having only one particle is not allowed to send a particle elsewhere, i.e., if , since our study is restricted to the products maintaining non-zero share in the studied period.

III.2 Stationary-state distribution and phase diagram

To see how particles are distributed under Eq. (3), let us consider the evolution of the probability of finding a particle configuration with time Evans and Hanney (2005):

| (4) |

where is identical to except at sites and such that . In the stationary state , the detailed balance condition (and equivalently ) is satisfied if is the multiplication of a function of and a function of Evans and Hanney (2005), which is approximately true in the stationary state of our model; the denominator of Eq. (3) saturates in the long time limit as confirmed in Fig. 3 (b). Inserting Eq. (3) in the detailed-balance condition, one finds that takes a factorized form

| (5) |

with the Riemann zeta function and the partition function. While many properties of the factorized states in Eq. (5) have been investigated Burda et al. (2002); Majumdar et al. (2005); Evans et al. (2006), we have seen that the case of is the model for the kinetics of product share in international trade, the properties of which are not fully understood.

Of main interest is the particle-number distribution at a single site, which is obtained from the whole particle configuration probability as by using Eq. (5) Evans and Hanney (2005)

| (6) |

The particle-number distribution behaves as for small while the contribution of in Eq. (6) may not be negligible for large. When the particle density is small, the latter contribution takes the form with depending on via the relation . corresponds to the negative chemical potential Evans et al. (2006), and decreases with increasing . For , there exists the critical density such that the relation can be satisfied by with only for :

| (7) |

If , develops additionally a bump in the region indicating that most particles occupy a single site, which may be called condensation Evans et al. (2006). For and finite, is free from such a bump in the limit . Therefore two phases, fluid and condensate phase, can be defined depending on whether such condensation occurs or not in the stationary state, which leads to the phase diagram in the plane [Fig. 2 (b)].

IV Urn model with for product share kinetics

The phase diagram in Fig. 2 (b) indicates that is a critical value: Condensate emerges for finite particle density only when is larger than . Given that the kinetics of product share in international trade is described by the model with , one can expect that there will be no condensation in international trade. However in reality is large but finite and then a bump may appear in even with for sufficiently large, which is called pseudo-condensate Evans et al. (2006). In this section, we bring the urn model with as close as possible to the real trade by fitting the model parameters, mainly the particle density and the time scale, to address the model’s power of explaining the international trade in the past and predicting its future.

IV.1 Time scale corresponding to one year

Let denote the time interval in the model corresponding to one year in the real world. For the time interval , a site is selected times for gaining or losing a particle with the rate in Eq. (3) and , which either increases or decreases by Hughes (1995)

| (8) |

Identifying Eq. (2) with (8) under the relation , we find that yielding . We use the rescaled time

| (9) |

such that the increase of by corresponds to one year in reality.

IV.2 Fitting the simulated second moment to data

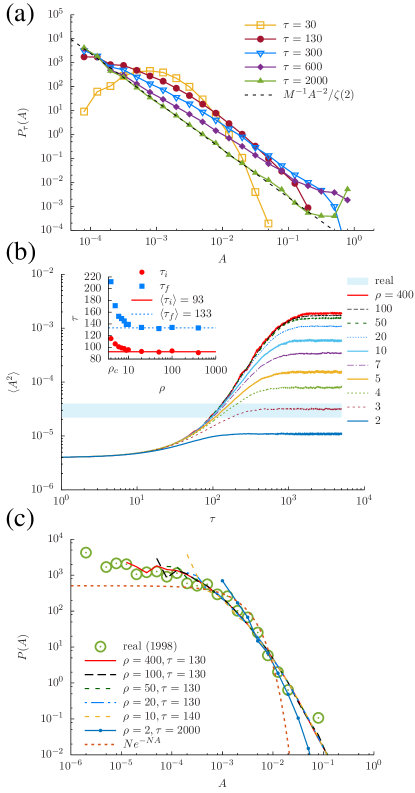

The comparison of the particle-number distribution in the model, varying with the particle density , and the empirical share distribution may help us to estimate . We perform simulations of the model with sites and different particle densities set to be integers. Particles are uniformly distributed over all sites initially at , yielding . As the stochastic transfers of particles are repeated, the particle-number distribution gets broadened as shown in Fig. 3 (a). The second moment increases with the rescaled time and saturates in the late-time regime as shown in Fig. 3 (b). The empirical value of increases steadily from to for the period 1962-2000 except for the jumps related to oil crises in the middle of the period, which disappear if crude oil (SITC 3330) is excluded [Fig. 1 (a)]. Interestingly, the simulated values of overlap with the empirical values at as long as [Fig. 3 (b)]. This time interval is in quite good agreement with the real time interval, 38 years from 1962 to 2000. For , the overlap period varies with or does not even exist e.g., for or . Based on these results, we estimate the particle density to be .

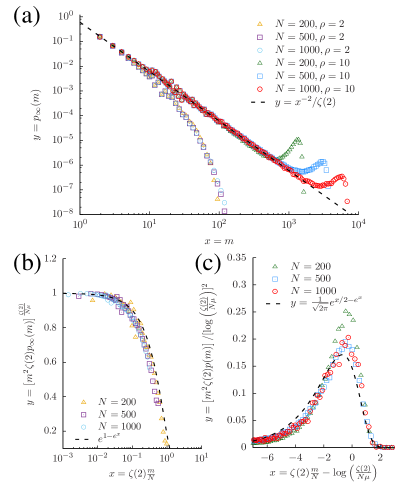

IV.3 Share distribution and condensation

For all , the simulated share distributions, in the period match excellently the empirical share distributions as shown in Fig. 3 (c). The simulated with decays faster, failing to fit into the empirical distributions even in the long-time limit.

Given such excellent agreement between the empirical data and the simulation results in the period , one may wonder what will happen in the late-time regime in the simulations. It can hint at the future of international trade. While the broadening of the simulated distribution in the early-time regime does not depend on the particle density, in the late-time regime varies significantly with . The analytic solution for in the stationary state, derived in Appendix A, shows that similarly to , a critical density exists for and large but finite such that in Eq. (6) behaves as a function of differently depending on whether is larger than or not. Consequently, for , has an exponential-decay factor

| (10) |

with . In contrast, for , it has a bump, in addition to the power-law decay form small , as

| (11) |

for finite, indicating the emergence of a pseudo-condensate Evans et al. (2006): Most particles gather at a single site. Given , the estimated particle density is above the critical density [Appendix A] suggesting that the kinetics of product share will enter the pseudo-condensate phase in the long-time limit: The share distribution is expected to get broadened and end up with a power-law decay plus a bump near as an example in Fig. 3 (a) for .

The time scale for such condensation phenomena can be predicted by our simulation results. saturates around for [Fig. 3 (b)], which suggest that the stationary-state distribution displaying a bump will appear in years.

The predictions of the capital condensation in the product space and its time scale demonstrate that our model can be a framework for analyzing the evolution of the share distribution at present and in the future. Its limitations is, however, worthy to note. Most of all, we considered a fixed number, 508, of products traded consistently over the studied period 1962-2000. But in reality, new and old products may enter and leave the space of products, which can make big effects. For instance, the critical density will be larger with larger , possibly occurring by the rise of new industries. It might pull the international trade out of the pseudo-condensate phase. Also, annual gains show large fluctuations for products having small share . Allowing larger chance of gain to small-share, probably new, products might help prevent the condensation of share onto top popular products.

V Probabilistic prediction for individual products

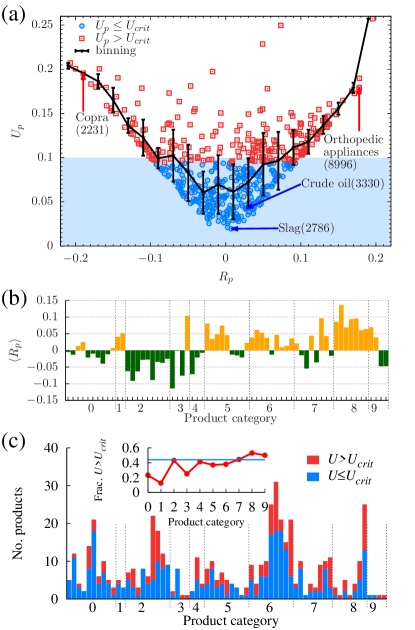

Our model can make a probabilistic prediction also for individual products’ share. We investigate how well the model can predict the growth rates of share for each product . We choose ’s rather than the share ’s since an exceptional variation of the growth rate at a certain time may cause a cascade of shifts in the share for like the upper shift of share for oil in Fig. 1 (b). Running simulations with the empirical values at , , as the initial configuration at , we obtain simulated growth rates for all products over the rescaled time period with and the number of simulation runs.

From the rank of the empirical growth rate among its simulated values ’s, we compute the excess growth rate

| (12) |

which represents how much the share of product grows faster (slower) than the median of the simulated growth rates. The excess growth rates for a product will be uniformly distributed between and if simulations yield a good probabilistic prediction for the empirical growth rates ’s of the product Marhuenda et al. (2005); it should not be possible to discern empirical values from the simulated ones. Let us sort ’s such that . If ’s are uniformly distributed between and , then we expect that ’s will increase linearly with such that . Deviations from this expectation can quantify the non-uniformity of ’s and the failure of the model to predict the growth rates ’ of product Marhuenda et al. (2005). Therefore we define the unpredictability of product by

| (13) |

where the ’s are sorted such that for all and . of numbers from the uniform distribution may be larger than with probability . Therefore we consider products with as unpredictable Marhuenda et al. (2005).

We find that 284 products () are predictable while the remaining 224 () are unpredictable by the model simulations with . The number of predictable products was smaller for other selected values of . More products are classified as predictable if the model prediction is made for a shorter period than years. Most of the unpredictable products display large positive or negative excess growth rate (Fig. 4 (a)). Interestingly, such deviations are correlated with the nature of the products, as identified in the SITC framework: Growth rates for raw materials and agricultural commodities tend to be smaller than the predicted growth rates, showing the mean excess growth rate negative, while manufactured and especially high-end products such as medical appliances have positive. Figure 4 (b) shows the mean excess growth rates of 66 product categories based on the first two digits of SITC. Chemicals (SITC codes beginning with 5), manufactured goods (6 and 8) and machinery (7) have grown faster than the model prediction while the growth of the share of crude materials (2) was slower than the prediction. The fraction of unpredictable products is larger among manufactured goods than among raw materials (Fig. 4 (c)).

Some products show small but large owing to large fluctuations ; the offer and demand for such products tends to be highly variable or historically determined e.g. railways, warships, and uranium. Thus, our predictability metric captures the fact that some products are more (or less) variable than expected, even if their trend is predicted.

VI Summary and discussion

In this paper we presented a stochastic particle model for the kinetics of products’ shares in international trade, in which sites represent product categories and particles represent a unit of share. From the empirical scaling behavior of the annual variations of product share, the probability of a site to send a particle to another site is set to be proportional to the square of the number of particles at the two sites. Products’ shares are related to the capital invested in those product categories, and therefore such biquadratic transfer rate illuminates a fundamental nature of capital in its activity and interaction.

If the preference to popular products is weaker than that represented by the biquadratic rate, the stationary state will lie in the fluid phase, having no condensation as long as the particle density is finite. Therefore capital in international trade may be considered as being at the edge of the fluid phase. Comparing with the empirical data, we found that the period 1962-2000 covered in the dataset corresponds to a transient period in the model. We were able to determine the time scale and the range of the particle density with which the model predictions match the empirical annual variation and distribution of product share. The estimated particle density turns out to be larger than the critical density, suggesting that a large fraction of trade volumes will concentrate on few product categories in the future. The model simulations show how the share distribution will change with time and predict the time scale of such condensation by using the estimated parameters. The model also makes baseline predictions for the evolution of various industrial sectors, and by comparison, allows us to find other factors such as intrinsic economic fitness Safarzyńska and van den Bergh (2010) at work in addition to the endogenous dynamics represented by our model.

While our model can serve as a simple framework for analyzing the kinetics of capital in the space of products, it could be extended by allowing for the birth and death of product categories, leading to expansion or contraction of the product space. Also intrinsic fitness of products can be considered. Another natural development would be to assume that capital transfers occur on a network of products linked through heterogeneously weighted development pathways Hidalgo et al. (2007); Hidalgo and Hausmann (2009); Hausmann and Hidalgo (2011).

Acknowledgements.

This work was supported by the National Research Foundation of Korea (NRF) grants funded by the Korean Government (No. 2013R1A1A201068845 and No. 2016R1A2B4013204).Appendix A Derivation of the single-site distribution in the stationary state of the urn model with

In Eq. (5), the factorized form of the configuration probability with leads us to find that the grand partition function is given by with the generating function of represented as , where is the poly-logarithm function . This series converges for and expanded around as Robinson (1951)

| (14) |

The partition function can be recovered from the grand partition function by , where the contour is within the radius of convergence, Evans and Hanney (2005). Using Eq. (14), one finds that the dominant contribution is made around with

| (15) |

and thus the integral is approximated in the limit , , and finite by employing the steepest descent path with running from to as

| (16) |

Using Eq. (16) into Eq. (6), we find that

| (17) |

For defined in Eq. (16), when is large, the contribution near to is dominant, allowing us to approximate it as

| (18) |

According to our numerical computation, this approximation is good even for . For , we consider the path surrounding the branch cut of , with and such that , which leads us to

| (19) |

Different behaviors of for and in Eqs. (18) and (19) give rise to different behaviors of depending on and as shown in Fig. 5 (a). In case , corresponding to the low-density regime with the critical density defined by

| (20) |

both functions in Eq. (17) behave as Eq. (18). Therefore the particle-number distribution behaves as

| (21) |

which is confirmed by the simulation results for various ’s and [Fig. 5 (b)]. One finds that in the regime , has the exponential-decaying term as in Eq. (10).

If or , the function in the denominator in Eq. (17) behaves as Eq. (19). In the regime with , the function in the numerator in Eq. (17) behaves also as Eq. (19) and we find that the ratio of the two functions is close to , leading to . In the large- region where , the function in the numerator in Eq. (17) behaves as Eq. (18), leading to

| (22) |

with . The function takes a bell-shape around such that it takes a form around which leads to Eq. (11). The scaled plots of in the regime where is finite in Fig. 5 (c) confirm Eq. (22).

References

- Tinbergen (1962) J. Tinbergen, Shaping the world economy (New York: Twentieth Century Fund, 1962).

- Anderson (2010) J. E. Anderson, The gravity model, Tech. Rep. (National Bureau of Economic Research, 2010).

- Barigozzi et al. (2010) M. Barigozzi, G. Fagiolo, and D. Garlaschelli, Phys. Rev. E 81, 046104 (2010).

- Serrano and Boguñá (2003) M. A. Serrano and M. Boguñá, Phys. Rev. E 68, 015101 (2003).

- Garlaschelli and Loffredo (2004) D. Garlaschelli and M. I. Loffredo, Phys. Rev. Lett. 93, 188701 (2004).

- Hidalgo et al. (2007) C. A. Hidalgo, B. Klinger, A.-L. Barabási, and R. Hausmann, Science 317, 482 (2007).

- Hidalgo and Hausmann (2009) C. A. Hidalgo and R. Hausmann, Proc. Natl. Acad. Sci. U.S.A. 106, 10570 (2009).

- Hausmann and Hidalgo (2011) R. Hausmann and C. A. Hidalgo, J. Econ. Growth 16, 309 (2011).

- Tacchella et al. (2012) A. Tacchella, M. Cristelli, G. Caldarelli, A. Gabrielli, and L. Pietronero, Sci. Rep. 2, 723 (2012).

- Yakovenko and Rosser Jr (2009) V. M. Yakovenko and J. B. Rosser Jr, Rev. Mod. Phys. 81, 1703 (2009).

- Bouchaud and Mézard (2000) J.-P. Bouchaud and M. Mézard, Phys. A 282, 536 (2000).

- Clauset et al. (2009) A. Clauset, C. Shalizi, and M. Newman, SIAM Rev. 51, 661 (2009), http://dx.doi.org/10.1137/070710111 .

- Alstott et al. (2014) J. Alstott, E. Bullmore, and D. Plenz, PLOS ONE 9, e85777 (2014).

- Feenstra et al. (2005) R. C. Feenstra, R. E. Lipsey, H. Deng, A. C. Ma, and H. Mo, World trade flows: 1962-2000, Tech. Rep. (National Bureau of Economic Research, 2005).

- Mantegna and Stanley (1995) R. N. Mantegna and H. E. Stanley, Nature 376, 46 (1995).

- Gibrat (1931) R. Gibrat, Les inégalités économiques (Librarie du Recueil Sirey, Paris, 1931).

- de Menezes and Barabási (2004) M. A. de Menezes and A.-L. Barabási, Phys. Rev. Lett. 92, 028701 (2004).

- Eisler et al. (2008) Z. Eisler, I. Bartos, and J. Kertész, Adv. Phys. 57, 89 (2008).

- Kendal and Jørgensen (2011) W. S. Kendal and B. Jørgensen, Phys. Rev. E 83, 066115 (2011).

- Taylor (1961) L. R. Taylor, Nature 189, 732 EP (1961).

- Godreche and Luck (2002) C. Godreche and J. Luck, J. Phys. Condens. Matter 14, 1601 (2002).

- Evans and Hanney (2005) M. R. Evans and T. Hanney, J. Phys. A Math. Gen. 38, R195 (2005).

- Hughes (1995) B. Hughes, Random Walks and Random Environments (Oxford Univ. Press, Clarendon, 1995).

- Burda et al. (2002) Z. Burda, D. Johnston, J. Jurkiewicz, M. Kamiński, M. A. Nowak, G. Papp, and I. Zahed, Phys. Rev. E 65, 026102 (2002).

- Majumdar et al. (2005) S. N. Majumdar, M. R. Evans, and R. K. P. Zia, Phys. Rev. Lett. 94, 180601 (2005).

- Evans et al. (2006) M. Evans, S. Majumdar, and R. Zia, J. Stat. Phys. 123, 357 (2006).

- Marhuenda et al. (2005) Y. Marhuenda, D. Morales, and M. Pardo, Statistics 39, 315 (2005).

- Safarzyńska and van den Bergh (2010) K. Safarzyńska and J. C. van den Bergh, J. Evol. Econ. 20, 329 (2010).

- Robinson (1951) J. E. Robinson, Phys. Rev. 83, 678 (1951).