Robust Inference for Seemingly Unrelated Regression Models

Abstract

Seemingly unrelated regression models generalize linear regression models by considering multiple regression equations that are linked by contemporaneously correlated disturbances. Robust inference for seemingly unrelated regression models is considered. MM-estimators are introduced to obtain estimators that have both a high breakdown point and a high normal efficiency. A fast and robust bootstrap procedure is developed to obtain robust inference for these estimators. Confidence intervals for the model parameters as well as hypothesis tests for linear restrictions of the regression coefficients in seemingly unrelated regression models are constructed. Moreover, in order to evaluate the need for a seemingly unrelated regression model, a robust procedure is proposed to test for the presence of correlation among the disturbances. The performance of the fast and robust bootstrap inference is evaluated empirically in simulation studies and illustrated on real data.

Abstract

In the supplementary material we introduce functionals corresponding to MM-estimators and discuss important properties of these MM-functionals such as equivariance, influence function and asymptotic variance. Also influence functions and asymptotic distributions are derived for the proposed robust test statistics. Power curves are included for a situation which is less deviating from diagonality than the equicorrelation matrix. Furthermore, we construct bootstrap confidence intervals based on fast and robust bootstrap and evaluate their performance in a simulation study. In addition, we illustrate these confidence intervals on Grunfeld data. The appendix also contains expressions for the partial derivatives required in the fast and robust bootstrap procedure, a verification of the consistency conditions for the robust test on regression coefficients, and the proofs of the theorems.

KEYWORDS: Diagonality test; Fast and robust bootstrap; MM-estimator; Robust testing

© 2018. This manuscript version is made available under the CC-BY-NC-ND 4.0 license http://creativecommons.org/licenses/by-nc-nd/4.0/

1. Introduction

Many scientists have investigated statistical problems involving multiple linear regression equations. Unconsidered factors in these equations can lead to highly correlated disturbances. In such cases, estimating the regression parameters equation-by-equation by, e.g., least squares is not likely to yield efficient estimates. Therefore, seemingly unrelated regression (SUR) models have been developed. SUR models take the underlying covariance structure of the error terms across equations into account. Applications in econometrics and related fields include demand and supply models (Kotakou,, 2011; Martin et al.,, 2007), capital asset pricing models (Hodgson et al.,, 2002; Pástor and Stambaugh,, 2002), chain ladder models (Hubert et al.,, 2017; Zhang,, 2010), vector autoregressive models (Wang,, 2010), household consumption and expenditure models (Kuson et al.,, 2012; Lar et al.,, 2011), environmental sciences (Olaolu et al.,, 2011; Zaman et al.,, 2011), natural sciences (Cadavez and Henningsen,, 2012; Hasenauer et al.,, 1998) and many more.

A SUR model, introduced by Zellner, (1962), consists of dependent linear regression equations, also called blocks. Denote the th block in matrix form by

where contains the observed values of the response variable and is an matrix containing the values of input variables. Note that the number of predictors does not need to be the same for all blocks. The vector contains the unknown regression coefficients for the th block and constitutes its error term. The error term is assumed to have and where is the unknown variance of the errors in the th block, and represents the identity matrix of size . In the SUR model blocks are connected by the assumption of contemporaneous correlation. That is, the th element of the error term of block may be correlated with the th element of the error term of block . With and observation numbers and and block numbers, the covariance structure of the disturbances can be summarized as

Note that each regression equation in a SUR model is a linear regression model in its own right. The different blocks may seem to be unrelated at first sight, but are actually related through their error terms.

The regression equations in a SUR model can be combined into two equivalent single matrix form equations. Let bdiag denote the operator that constructs a block diagonal matrix from its arguments. Moreover, let denote the Kronecker product and let be a symmetric matrix with elements . First, the SUR model can be rewritten as a single linear regression model

where , a block diagonal matrix with , and . For the error term it then holds that . Secondly, the SUR model can be represented as a multivariate linear regression model

where , , and . Equivalently, we can write the error matrix as with which satisfies . Hence, the covariance of the error matrix is given by .

It is well-known that ordinary least squares which ignores the correlation patterns across blocks may yield inefficient estimators. Generalized least squares (GLS) is a modification of least squares that can deal with any type of correlation, including contemporaneous correlation. For the SUR model, the GLS estimator takes the form

| (1) |

GLS coincides with the separate least squares estimates if for , or if . GLS is more efficient than least squares estimator (Zellner,, 1962), but in most situations the covariance needed in GLS is unknown. Feasible generalized least squares (FGLS) estimates the elements of by where is the residual vector of the th block obtained from ordinary least squares and then replaces in GLS by the resulting estimator . The finite-sample efficiency of FGLS is smaller than for GLS, although the asymptotic efficiency of both methods is identical. Note that FGLS can be repeated iteratively.

Alternatively, maximum likelihood estimators (MLE) can be considered (see Srivastava and Giles,, 1987). Assuming that the disturbances are normally distributed, the log-likelihood of the SUR model is given by

| (2) |

Maximizing this log-likelihood with respect to yields the estimators which are the solutions of the following equations

| (3) |

with the block diagonal form of . Hence, the maximum likelihood estimators correspond to the fully iterated FGLS estimators.

It is well-known that outliers in the data (observations which deviate from the majority of the data) can severely influence classical estimators such as LS, MLE and their modifications. Hence, FGLS and MLE are expected to yield non-robust estimates. Robust M-estimators for the SUR model have been proposed, but these estimators lack affine equivariance (Koenker and Portnoy,, 1990). Bilodeau and Duchesne, (2000) have introduced robust and affine equivariant S-estimators. Recently, Hubert et al., (2017) developed an efficient algorithm for these estimators. Despite its remarkable robustness properties, S-estimators can have a low efficiency, which makes them less suitable for inference. Therefore, we introduce MM-estimators for the SUR model which can combine high robustness with a high efficiency. To obtain efficient and powerful robust tests, we also introduce an efficient MM-estimator of the error scale based on the residuals of the MM-estimates.

Asymptotic theory can be used to draw inference corresponding to the MM-estimates in the SUR model. However, these asymptotic results rely on assumptions that are hard to verify in practice. The bootstrap (Efron,, 1979) offers an alternative approach that does not require strict assumptions. However, the standard bootstrap lacks speed and robustness. Therefore, the fast and robust bootstrap (FRB) procedure of Salibian-Barrera and Zamar, (2002) is adapted to the SUR setting. The FRB can be used to construct confidence intervals (Salibian-Barrera et al.,, 2006; Salibian-Barrera and Zamar,, 2002) as well as to develop hypothesis tests (Salibian-Barrera,, 2005; Salibian-Barrera et al.,, 2016; Van Aelst and Willems,, 2011). In particular, one of our main goals is to develop a robust test for diagonality of the covariance matrix to evaluate the need for using a SUR model.

To set the scene, MM-estimators for the SUR model are introduced in Section 2 as an extension of S-estimators. Section 3 focuses on the fast and robust bootstrap procedure to develop robust inference. In Section 4 the MM-estimator of scale is introduced and hypothesis tests concerning the regression coefficients are studied. In Section 5 we investigate a robust procedure to test for diagonality of the covariance matrix , i.e., to test whether a SUR model is really needed. The finite-sample performance of the FRB inference procedures is investigated by simulation in Section 6. Section 7 illustrates the robust inference on a real data example from economics and Section 8 concludes. The supplementary material includes properties of MM-estimators and the proposed test statistics, and contains some extra results on robust confidence intervals.

2. Robust Estimators for the SUR Model

2.1 S-estimators

We first introduce S-estimators for the SUR model as proposed by Bilodeau and Duchesne, (2000). Consider so-called -functions which satisfy the following conditions:

-

(C1)

is symmetric, twice continuously differentiable and satisfies

-

(C2)

is strictly increasing on and constant on for some .

The most popular family of -functions is the class of Tukey bisquare -functions given by where is a tuning parameter.

Definition 1.

Let for and let be a -function with parameter in (C2). Then, the S-estimators of the SUR model are the solutions that minimize subject to the condition

where the minimization is over all and with PDS the set of positive definite and symmetric matrices of dimension . The determinant of is denoted by and represents the th row of the residual matrix .

The constant can be chosen as to obtain a consistent estimator at an assumed error distribution . Usually, the errors are assumed to follow a normal distribution with mean zero and then we can take . As before, the regression coefficient estimates in the matrix can also be collected in the vector .

The first-order conditions corresponding to the above minimization problem yield the following fixed-point equations for S-estimators

| (4) |

with diagonal matrix where , and . Note the similarities with the GLS in (1) and the MLE in (3). The factor can be interpreted as the weight that the estimator gives to the th observation. A small (large) residual distance leads to a large (small) weight . The smaller the weight of an observation, the smaller its contribution to the SUR fit. To compute the S-estimates efficiently, Hubert et al., (2017) developed the fastSUR algorithm based on the ideas of Salibian-Barrera and Yohai, (2006).

The breakdown point of an estimator is the smallest fraction of the data that needs to be contaminated in order to drive the bias of the estimator to infinity. S-estimators with a bounded loss function, as we consider here, have a positive breakdown point (Lopuhaä and Rousseeuw,, 1991; Van Aelst and Willems,, 2005). Their asymptotic breakdown point equals . The constant has been fixed to guarantee consistency, but the parameter can be tuned to obtain any desired breakdown point . Hence, S-estimators can attain the maximal breakdown point of . S-estimators with a smaller value of downweight observations more heavily and correspond to a higher breakdown point.

S-estimators satisfy the first-order conditions of M-estimators (see Huber and Ronchetti,, 2009), so they are asymptotically normal. However, the choice of the tuning parameter involves a trade-off between breakdown point (robustness) and efficiency at the central model (Bilodeau and Duchesne,, 2000). For this reason, S-estimators are less adequate for robust inference. MM-estimators (Yohai,, 1987) avoid this trade-off by computing an efficient M-estimator starting from a highly robust S-estimator (see, e.g., Kudraszow and Maronna,, 2011; Tatsuoka and Tyler,, 2000; Van Aelst and Willems,, 2013). We now introduce MM-estimators for the SUR model.

2.2 MM-estimators

Let denote the S-estimator of covariance in Definition 1. Decompose into a scale component and a shape matrix such that with .

Definition 2.

Let for and let be a -function with parameter in (C2). Given the S-scale , MM-estimators of the SUR model minimize

over all and with . The MM-estimator for covariance is defined as .

As before, the MM-estimator of the regression coefficients can also be written in vector form . Similarly as for S-estimators, the first-order conditions corresponding to the above minimization problem yield a set of fixed-point equations:

| (5) |

with where , and . Starting from the initial S-estimates, the MM-estimates are calculated easily by iterating these estimating equations until convergence.

MM-estimators inherit the breakdown point of the initial S-estimators. Hence, they can attain the maximal breakdown point if initial high-breakdown point S-estimators are used. Moreover, since MM-estimators also satisfy the first-order conditions of M-estimators, they are asymptotically normal. In the supplementary material it is shown that the asymptotic efficiency of does not depend on the -function of the initial S-estimator. Therefore, the breakdown point and the efficiency of MM-estimators can be tuned independently. That is, the tuning constant in can be chosen to obtain an S-scale estimator with maximal breakdown point, while the constant in is tuned to attain a desired efficiency, e.g., , at the central model with normal errors. Note that while MM-estimators have maximal breakdown point, there is some loss of robustness because the bias due to contamination is generally higher as compared to S-estimators (see, e.g., Berrendero et al.,, 2007).

3. Fast and Robust Bootstrap

The asymptotic distribution of MM-estimators can be used to obtain inference for the parameters in the SUR model based on their MM-estimates. However, these asymptotic results are only reasonable for sufficiently large samples and rely on the assumption of elliptically symmetric errors which does not necessarily hold in practice. The bootstrap offers an alternative approach that requires less assumptions. Unfortunately, for robust estimators the standard bootstrap procedure lacks speed and robustness. The standard bootstrap is computer intensive because many bootstrap replicates are needed and the fastSUR algorithm is itself already computationally intensive. Moreover, classical bootstrap does not yield robust inference results. Indeed, due to the resampling with replacement, the proportion of outlying observations varies among bootstrap samples. Some bootstrap samples thus contain a majority of outliers, resulting in breakdown of the estimator. These estimates affect the bootstrap distribution leading to unreliable inference. Therefore, we use the fast and robust bootstrap introduced by Salibian-Barrera and Zamar, (2002) and generalized in e.g., Salibian-Barrera et al., (2006) and Peremans et al., (2017).

Consider an estimator of a parameter that satisfies the fixed-point equations where the function depends on the given sample. For a bootstrap sample it equivalently holds that . Now, consider as a first-step approximation of the bootstrap estimate . These first-step approximations underestimate the variability of the bootstrap distribution since the starting value is the same for all bootstrap approximations. To remedy this deficiency a linear correction factor can be derived from a Taylor expansion of . This yields the fast and robust bootstrap (FRB) estimator, given by

with the gradient of evaluated at . Consistency of has been discussed in detail by Salibian-Barrera and Zamar, (2002); Salibian-Barrera et al., (2006). The FRB estimator is computationally much more efficient because the first-step approximations are easy to compute and the linear correction term needs to be calculated only once, since it depends only on the original sample. Moreover, for a robust estimator the fixed-point equations usually correspond to a weighted version of the corresponding equations for the non-robust MLE or generalized least squares estimator. The weights in the equations downweight outlying observations. In such case, the FRB estimator is robust because no matter how many times an outlying observation appears in a bootstrap sample, it receives the same low weight as in the original sample since the weights depend on the estimate corresponding to the original sample.

To apply the FRB to the S and MM-estimators for the SUR model, we rewrite the estimating equations of S-estimators in (4) as

where , . Similarly, we rewrite the estimating equations (5) of MM-estimators as

where , , and for an matrix . Now, let be the vector which combines the S and MM-estimates for the SUR model and let

| (6) |

Then, we have that . Expressions for the partial derivatives in can be found in the supplementary material.

Based on the FRB estimates confidence intervals for the model parameters can be constructed by using standard bootstrap techniques. This is shown in more detail in the supplementary material. In the next sections we construct robust test procedures for the SUR model and show how FRB can be used to estimate their null distribution.

4. Robust Tests for the Regression Parameters

Consider the following general null and alternative hypothesis with respect to the regression parameters in the SUR model

| (7) |

for some and . Here represents the number of linear restrictions on the regression parameters under the null hypothesis. For example, for and the null hypothesis simplifies to . Note that the null hypothesis can restrict regression parameters of different blocks, e.g., .

For maximum likelihood estimation, the standard test statistic is the well-known likelihood-ratio statistic. With the log-likelihood in (2) it is given by

where is the MLE in the full model and the MLE in the restricted model under the null hypothesis. Under the null hypothesis the test statistic is asymptotically chi-squared distributed with degrees of freedom. See, e.g., Henningsen and Hamann, (2007) for more details on standard test statistics (such as Wald and F-statistics) in SUR models.

A robust likelihood-ratio type test statistic corresponding to MM-estimators can be obtained by using the plug-in principle. Let denote the unrestricted scatter MM-estimator and the restricted MM-estimator. Then, the robust likelihood-ratio statistic becomes

| (8) |

with and the scale S-estimators of the full and null model, respectively. Similarly to , the test statistic is nonnegative, since by definition of the S-estimators.

The test statistic in (8) only depends on S-scale estimators. Hence, the low efficiency of S-estimators may affect the efficiency of tests based on . In the linear regression context, Van Aelst et al., (2013) recently introduced an efficient MM-scale estimator corresponding to regression MM-estimators. Analogously, we propose to update the S-estimator of scale in the SUR model by a more efficient M-scale , defined as

Similarly to , the constant can be chosen as to obtain a consistent estimator at the assumed error distribution , e.g., . The likelihood-ratio type test statistic corresponding to this MM-scale estimator is then defined as

| (9) |

Results on the asymptotic distribution and influence function of these test statistics are provided in the supplementary material. Since the asymptotic distribution is only useful for sufficiently large samples, we consider FRB as an alternative to estimate the null distribution of the test statistics. However, since likelihood-ratio type test statistics converge at a higher rate than the estimators themselves, a standard application of FRB leads to an inconsistent estimate of the null distribution of the test statistic (Van Aelst and Willems,, 2011). To overcome this issue, the test statistic in (8) is rewritten as

| (10) |

where and are the S-estimators in the full and null model respectively and where is the multivariate M-estimator of scale corresponding to a given and with . That is, is the solution of

| (11) |

Similarly, the MM-based test statistic in (9) is rewritten as

| (12) |

where

| (13) |

Let contain the S and MM-estimators of the regression coefficients and error shape matrices for the full model and let contain the corresponding estimators for the reduced model. Denote , then both test statistics can be written in the general form

where the dot in the subscript can be either S or MM and the function is determined by (10)-(11) or (12)-(13), respectively. The FRB approximation for the null distribution of this test statistic then consists of the values

where are the FRB approximations for the regression and shape estimates in the bootstrap samples. It can be checked that the function satisfies the condition

| (14) |

so the partial derivatives of vanish asymptotically. This condition guarantees that the FRB procedure consistently estimates the null distribution of the test statistic, as shown in Van Aelst and Willems, (2011). Note that the FRB procedure for hypothesis tests is computationally less efficient than for the construction of confidence intervals (see supplementary material) because the S-scales of the full and null model have to be computed by an iterative procedure for each of the bootstrap samples. However, the increase in computation time is almost negligible compared to the time needed by the standard (non-robust) bootstrap for these robust estimators.

Bootstrapping a test statistic to estimate its null distribution requires that the bootstrap samples follow the null hypothesis, even when this hypothesis does not hold in the original data. Therefore, we first construct null data that approximately satisfy the null hypothesis, regardless of the hypothesis that holds in the original data. According to Salibian-Barrera et al., (2016), for the linear constraints in (7) null data for can be constructed as

with the residuals in the full model. Bootstrap samples are now generated by sampling with replacement from the null data . Let denote the MM-estimates for the null data in the full model and let denote the MM-estimates for the null data in the restricted model. Due to affine equivariance we have that , so these estimates can be obtained without extra computations. However, the estimates for the reduced model cannot be derived from equivariance properties and need to be computed from the transformed data. Similarly, null data can be constructed for . Finally, when FRB recalculated values of the test statistic have been calculated based on the null data, then the corresponding FRB p-value is given by

| (15) |

where is the value of the test statistic at the original sample.

5. Robust Test for Diagonality of the Covariance Matrix

The key feature of the SUR model is the existence of contemporaneous correlation, corresponding to a non-diagonal covariance matrix . If the covariance matrix is diagonal the SUR model simplifies to unrelated regression models. Therefore, by testing for diagonality of the necessity of a SUR model is evaluated.

Consider the following hypotheses

| (16) |

A popular diagonality test for the standard SUR model is the Breusch-Pagan test (Breusch and Pagan,, 1980) which is based on the Lagrange multiplier idea (Baltagi,, 2008). It measures the total sum of squared correlations:

with the elements of the sample correlation matrix of the residual vectors , . Here, each is the residual vector corresponding to a single-equation LS fit in block . Under the null hypothesis is asymptotically chi-squared distributed with degrees of freedom. Evidently, the LS based Breusch-Pagan test is vulnerable to outliers in the data. Therefore, we introduce robust Breusch-Pagan type tests.

Contrary to the classical estimators, the S and MM-estimators in a SUR model do not simplify to their univariate analogues under the null hypothesis. However, to calculate the restricted estimates the S and MM-estimators and corresponding fastSUR algorithm can be adapted such that the equations for the off-diagonal elements of the covariance matrix are excluded. For example, in case of MM-estimators the estimating equations become

for and with where . The restricted covariance matrix estimates and under then become diagonal matrices as needed. Since the tuning constants of the -functions are kept fixed, the reduced estimators also have the same breakdown-point and efficiency level as their counterparts in the full model. Moreover, the multivariate structure is not lost, i.e., we still obtain a single weight for each observation across all blocks.

Based on the restricted estimators, we now estimate the correlation between the errors of block and as

with . Based on these correlation estimates we propose a robust Breusch-Pagan test statistic:

| (17) |

Note that is nonnegative. Similarly, a robust Breusch-Pagan test based on S-estimators, denoted by , can be defined as well, but it will not benefit from the gain in efficiency of MM-estimators.

From their asymptotic chi-squared distribution (see the supplementary material) non-robust p-values may be derived. Alternatively, FRB can again be used to estimate the null distribution of the test statistics. Note that the robust Breusch-Pagan test statistic only requires the estimates in the restricted model as can be expected for a Lagrange multiplier test. Let denote the vector that collects all S and MM-estimators in the restricted model. Based on the FRB approximations , bootstrap replications for the null distribution of can be generated as

with

where , and similarly for . It is straightforward to check that the consistency condition in (14) holds under for these test statistics, where is now defined through (17). Hence, the FRB procedure consistently estimates the null distribution of the test statistics.

To make sure that the bootstrap samples satisfy the null hypothesis, we generate bootstrap samples from the following transformed data

with the residuals in the full model. The residuals of the full SUR model are possibly correlated across blocks. By transforming these residuals with , this correlation is removed and it can be expected that for the transformed data

| (18) |

regardless of the hypothesis that holds in the original data. Note that in the SUR model we cannot rely on equivariance properties to obtain the identity matrix exactly because the model is only affine equivariant for transformations within blocks. However, extensive empirical investigation confirmed that (18) holds for the transformed data, and the corresponding value of the test statistic indeed becomes approximately zero. Similarly, null data can be created for as well.

6. Finite-Sample Performance

We now investigate by simulation the performance of FRB tests based on the robust likelihood-ratio test statistics and and the robust Breusch-Pagan statistics and . The tests are performed at the significance level. We study both the efficiency of the tests under the null hypothesis and the power under the alternative as well as their robustness.

In the SUR model, bootstrap samples can be obtained by either case (row) resampling from the original sample or by resampling the -dimensional residuals , . While the results in the previous sections hold for both types of bootstrapping, in this paper we use case resampling which is a more nonparametric approach than the model based error resampling.

Consider first the following hypothesis test in a SUR model:

| (19) |

To investigate the efficiency of the test procedures, data are simulated under the null hypothesis. Observations are generated according to a SUR model with three blocks () and two predictors (as well as an intercept) in each block. Hence, there are regression coefficients in the model. The predictor variables are generated independently from a standard normal distribution. The -dimensional vector of regression coefficients equals such that the null hypothesis holds. The covariance matrix is taken to be a correlation matrix with all correlations equal to 0.5. The multivariate errors are generated from either or (a multivariate elliptical t-distribution with mean zero and scatter ) with 3 degrees of freedom. To investigate the robustness of the procedure we also considered contaminated data. We have generated the worst possible type of outliers, namely bad leverage points, by replacing in each block all the regressors of the first 10% or 30% of the observations by uniform values between -10 and -5 and by adding to each of the corresponding original responses a value that is normally distributed with mean 20 and variance 1.

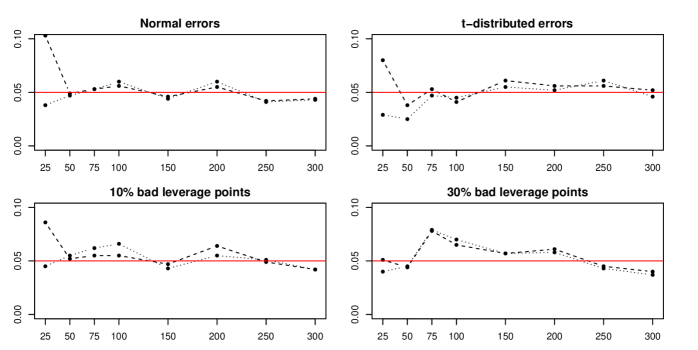

Robust S-estimators and MM-estimators with maximal breakdown point of 50% are computed. The MM-estimator is tuned to have 90% efficiency. The null distribution of both and are estimated by FRB as explained in Section 4, using bootstrap samples. The corresponding p-values are obtained as in (15). For each simulation setting 1000 random samples are generated for sample sizes and 300 (recall that represents the number of observations per block). Figure 1 shows the empirical level of the two tests for both clean and contaminated data.

It can be seen that the empirical levels are close to the 5% nominal level in most cases. The difference between and is mainly seen when the sample size is small. Indeed, for , the test using performs better than when is used. Note that outliers in the data only have a limited effect on the rejection rates, showing robustness of the level of the FRB tests.

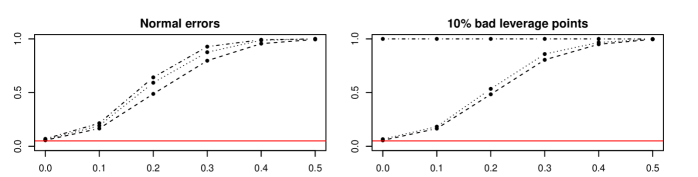

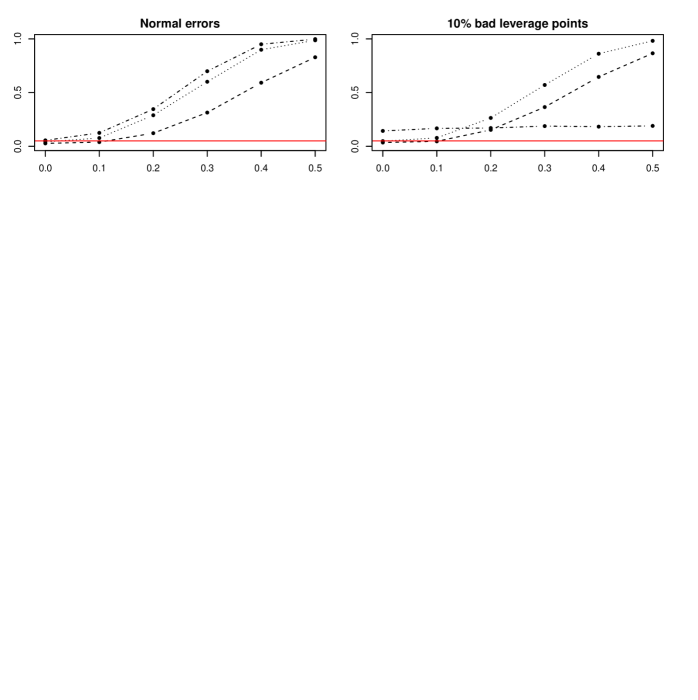

To investigate the power of the robust tests, we have simulated data sets under the alternative hypothesis. In Figure 2 we show the power of the tests for samples of size with where ranges from 0 to 0.5 with step length 0.1.

From the left plot we see that the power increases quickly when becomes larger. The power of the robust tests is only slightly lower than for the classical test in the non-contaminated setting. Moreover, the power of the test is (slightly) higher than for the test. The plot on the right shows that the classical test completely fails if the data is contaminated with 10% of bad leverage points. On the other hand, the robust tests are not affected much by the contamination and yield similar power curves as in the case without contamination.

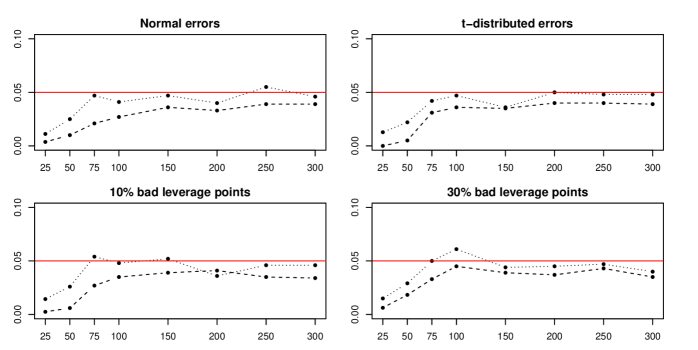

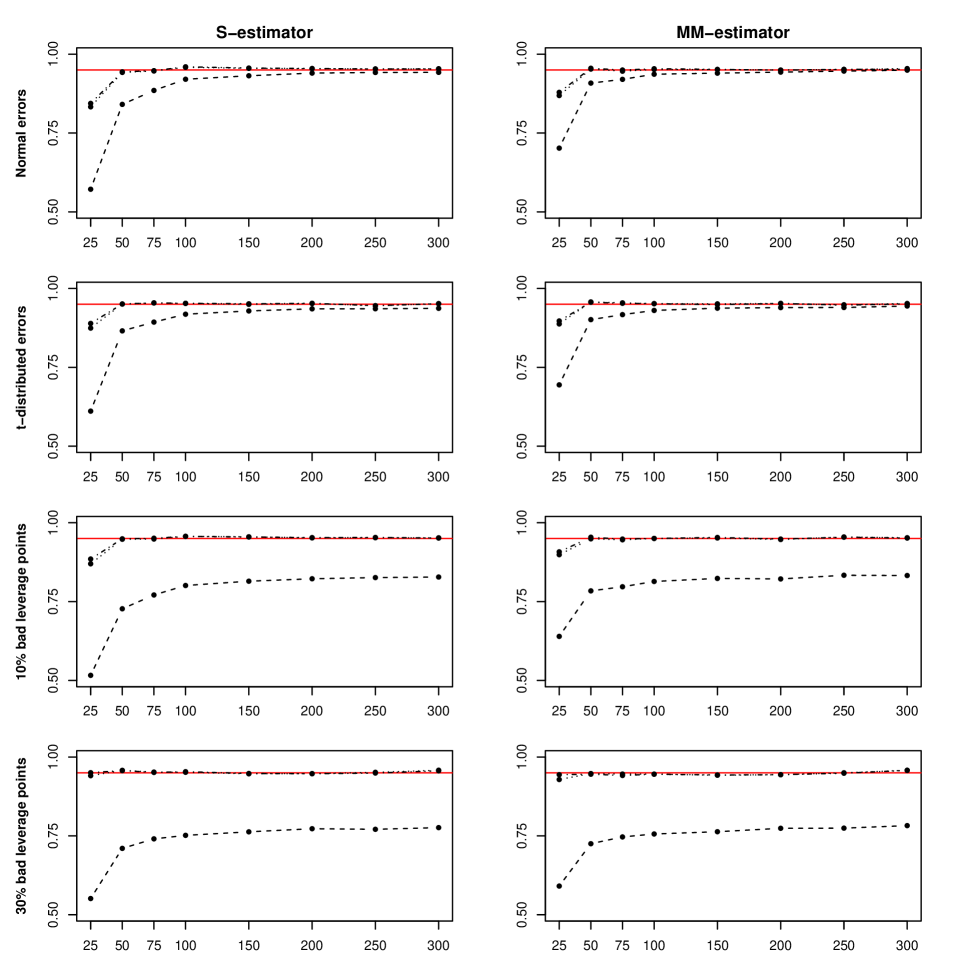

Let us now consider the test for diagonality of the covariance matrix in (16). First, data are generated under the null hypothesis, i.e., data are simulated as in the previous section, but the multivariate errors are generated from either or from with the identity matrix. The LM test statistic corresponding to both S and MM-estimators is computed. As before, 1000 data sets were generated for each setting. In Figure 3 the rejection rates are plotted as a function of sample size for the four cases considered (normal errors, t-distributed errors, 10% contamination and 30% contamination).

The rejection rates in the different cases behave similar. The lower efficiency of S-estimators becomes apparent as the empirical levels of are lower in all (but one) cases. For small sample sizes the nominal level is clearly underestimated, but for MM-estimation the nominal level is already reached for . The efficiency of the tests is not much affected by heavy tailed errors or contamination which confirms their robustness under the null hypothesis.

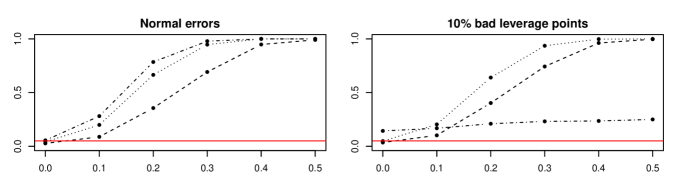

To investigate the power of the test procedures, data were simulated under the alternative hypothesis as well. To this end, was set equal to an equicorrelation matrix with correlation taking values from 0 to 0.5 with step length 0.1 for the case .

The left plot in Figure 4 shows the resulting power curves of the classical and robust Breusch-Pagan tests. We see that the test based on MM-estimators performs almost as well as the classical Breusch-Pagan test. For the empirical level of reaches almost one. The test based on S-estimators performs less well in this setting with blocks. However, we have noted that the performance of increases with the number of blocks in the SUR model. For larger block sizes the difference with becomes negligible. The right plot in Figure 4 shows that the classical Breusch-Pagan test cannot handle contamination, resulting in a drastic loss of power. On the other hand, the power of the robust tests is not affected much by the bad leverage points, resulting in power curves that are similar to the uncontaminated case. This setting where is an equicorrelation matrix can be considered to be a strong deviation from diagonality because the deviation is present in all covariance elements. Therefore, we also investigated the power of the diagonality test for other structures of . It turns out that the comparison between the three tests remains the same for other settings. The power curves for the case where only one covariance deviates from zero are given in the supplementary material.

7. Example: Grunfeld Data

As an illustration we consider the well-known Grunfeld data (see, e.g., Bilodeau and Duchesne, (2000)). This dataset contains information on the annual gross investment of 10 large U.S. corporations for the period 1935-1954. The recorded response is the annual gross investment of each corporation (Investment). Two predictor variables have been measured as well, which are the value of outstanding shares at the beginning of the year (Shares) and the beginning-of-year real capital stock (Capital). One may expect that within the same year the activities of one corporation can affect the others. Hence, the SUR model seems to be appropriate. Unfortunately, the classical and robust estimators of the covariance matrix become singular when all 10 companies are considered. Therefore, we only focus on the measurements of three U.S. corporations: General Electric (GE), Westinghouse (W) and Diamond Match (DM). General Electric and Westinghouse are active in the same field of industry and thus their activities can highly influence each other. Since the interest is in modeling dependencies between the corporations within the same year, a SUR model with three blocks is considered. The model is given by

| (20) |

with for and .

We consider inference corresponding to the standard MLE and robust MM-estimators. MM-estimates are obtained with 50% breakdown point and a normal efficiency of 90%. For the MLE, inference is obtained by using asymptotic results and standard bootstrap. For MM-estimators, robust inference is based on the asymptotic results as well as on FRB using bootstrap samples generated by case resampling. Given the small sample size, we may expect that the bootstrap inference is more reliable than the asymptotic inference according the simulation results in the previous section.

Table 1 contains the estimates for the regression coefficients and corresponding standard errors (between brackets) based on bootstrap for the SUR model in (20).

| Corporation | MLE | MM-estimator | ||||

|---|---|---|---|---|---|---|

| Intercept | Shares | Capital | Intercept | Shares | Capital | |

| GE | -42.270 | 0.049 | 0.122 | -30.661 | 0.033 | 0.152 |

| (27.559) | (0.016) | (0.034) | (26.679) | (0.014) | (0.026) | |

| W | -3.684 | 0.067 | 0.018 | -6.320 | 0.059 | 0.117 |

| (8.293) | (0.016) | (0.074) | (10.779) | (0.022) | (0.102) | |

| DM | -0.716 | 0.016 | 0.453 | -0.855 | 0.002 | 0.614 |

| (1.394) | (0.022) | (0.144) | (0.608) | (0.009) | (0.093) | |

We can clearly see that there are differences between the estimates of both procedures. Focusing on the slope estimates, we see that the MM-estimator yields larger effects of Capital (beginning-of-year real capital stock) and smaller effects of Shares (value of outstanding shares at beginning of the year) on annual gross investments than the MLE. The largest differences can be seen in the estimates , , and and their standard errors. The estimates for the scatter matrix and corresponding correlation matrix are given by

and

respectively. The robust covariance estimates are generally smaller than the classical estimates. Both estimators find large correlations between the errors of the different blocks. The largest correlation occurs between the first two blocks, which correspond to the equations of General Electric and Westinghouse.

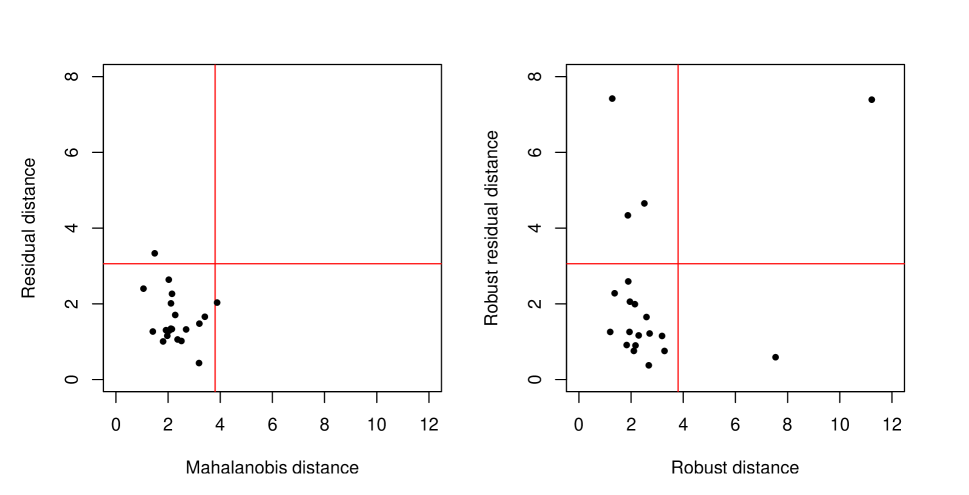

Since there are several differences between the non-robust MLE and the robust MM-estimates, we investigate the data for the presence of outliers. Outliers can be detected by constructing a multivariate diagnostic plot as in Hubert et al., (2017). This plot displays the residual distances of the observations versus the robust distance of its predictors. Based on the SUR estimates the residual distances are computed as

Similarly, to measure how far an observations lies from the majority in the predictor space, robust distances can be calculated as

with the th row of and where and are MM-estimates of the location and scatter of (Tatsuoka and Tyler,, 2000). Note that contributions of intercept terms have been removed from so that only the actual predictors are taken into account. For non-outlying observations with normal errors, the squared residual distances are asymptotically chi-squared distributed with degrees of freedom as usual. Therefore, a horizontal line at cut-off value (the square root of the 0.975 quantile of a chi-squared distribution with degrees of freedom) is added to the plot to flag outliers. Observations that exceed this cut-off are considered to be outliers. Similarly, if the predictors of the regular observations are approximately normally distributed, then asymptotically the squared robust distances are approximately chi-squared distributed with degrees of freedom. Therefore, we add a vertical line to the plot at cut-off value to identify outliers in the predictor space, i.e., leverage points. An observation is called a vertical outlier if its residual distance exceeds the cut-off but it is not outlying in the predictor space. If the observation is also outlying in the predictor space, it is called a bad leverage point. Observations with small residual distance which are outlying in the predictor space are called good leverage points because they still follow the SUR model. Similarly, a diagnostic plot can be constructed based on the initial S-estimates for the SUR model or even based on the MLE, although the latter will not reliably identify outliers due to the non-robustness of the estimates.

Multivariate diagnostic plots corresponding to our analysis of the Grunfeld data are shown in Figure 5, based on both the MLE and MM-estimates.

The diagnostic plot corresponding to the classical non-robust estimates does not reveal any clear outliers. It seems that all observations follow the SUR model. However, outliers may have affected the estimates to the extent that the outliers are masked. Therefore, we consider the robust diagnostic plot corresponding to the MM-estimates. This plot indeed shows a different picture. Three vertical outliers and one bad leverage point are identified, as well as one good leverage point. The three vertical outliers correspond to the years 1946, 1947 and 1948, while the bad leverage point corresponds to the year 1954. Further exploration of the data indicates that the three vertical outliers are mainly due to exceptionally high investments in those three post World War II years. For the final year 1954, the measurements for all variables are rather extreme, most likely due to the postwar booming economy, which explains why this year is flagged as a bad leverage point in the robust analysis. These four outliers may potentially influence the inference results based on MLE, leading to misleading conclusions. To verify the effect of the outliers on the MLE estimates of the parameters, we also calculated the MLE estimates based on the data without the outliers. The results (not shown) confirmed that the outliers and especially the bad leverage point affect the MLE estimates, because without these outliers the MLE estimates highly resemble the MM-estimates in Table 1.

The large correlation estimates between the errors of the different blocks already suggested that these correlations should not be ignored, and thus that the SUR model is indispensable. We can now formally test whether it is indeed necessary to use the SUR model. Therefore, we apply the diagonality test in Section 5 to test the hypotheses in (16). Table 2 shows the results for the Breusch-Pagan test as well as our robust Breusch-Pagan test. The table contains the values of both test statistics, as well as the corresponding asymptotic p-values and bootstrap p-values. The proportionality constant for the asymptotic chi-squared distribution is estimated by using the empirical distribution to calculate the expected value.

| Estimator | LM | AS p-value | B p-value |

|---|---|---|---|

| MLE | 23.482 | 0.001 | 0.003 |

| MM | 14.825 | 0.003 | 0.019 |

We immediately see that at the significance level, the null hypothesis of diagonality is rejected in all cases. Hence, the outliers in this example do not affect the MLE estimates in such a way that the covariance structure of the SUR model is completely hidden.

From an econometric point of view it can now be interesting to investigate whether the predictors Shares and Capital have the same effect on investments for the two energy companies General Electric and Westinghouse. Hence, we test

| (21) |

Table 3 contains the values of the likelihood-ratio statistics and corresponding asymptotic and bootstrap p-values.

| Estimator | AS p-value | B p-value | |

|---|---|---|---|

| MLE | 6.728 | 0.035 | 0.168 |

| MM | 7.255 | 0.057 | 0.086 |

If we consider a significance level, then the conclusion is not completely clear for the MLE. The commonly used asymptotic p-value does reject the null hypothesis, but based on the bootstrap p-value we cannot reject the null hypothesis anymore. On the other hand, the robust test yields asymptotic and bootstrap p-values that lie closer together and which do not reject the null hypothesis. Hence, the presence of outliers does not affect the outcome of the robust hypothesis test while it seems to have caused instability for the classical test based on the MLE. Indeed, if we remove the bad leverage point, then the asymptotic p-value corresponding to the MLE already increases to which is in line with the p-value based on the MM-estimator for the full data set.

8. Conclusion

In this paper we have introduced MM-estimators for the SUR model as an extension of S-estimators. MM-estimators combine high robustness (breakdown point) with high efficiency at the central model. Based on these MM-estimators robust inference for the SUR model has been developed based on the FRB principle. We considered likelihood ratio type statistics to test the existence of linear restrictions among the regression coefficients. While MM-estimators update the S-estimates of the regression coefficients and shape matrix, they do not automatically update the S-scale estimate. However, it turns out that more accurate and powerful tests are obtained if a more efficient MM-scale estimator is used.

An important question is whether it is necessary to use a joint SUR model rather than individual linear regression models for each of the blocks. To evaluate the need for a SUR model we proposed a robust alternative for the well-known Breusch-Pagan test. The FRB was used again to obtain a highly reliable test for diagonality of the covariance matrix, i.e., for existence of contemporaneous correlation among the errors in the different blocks of the SUR model.

Acknowledgments

This research has been partially supported by grant C16/15/068 of International Funds KU Leuven and the CRoNoS COST Action IC1408. The computational resources and services used in this work were provided by the VSC (Flemish Supercomputer Center), funded by the Research Foundation - Flanders (FWO) and the Flemish Government - department EWI.

Supplementary Material

In the supplementary material we introduce functionals corresponding to MM-estimators and discuss important properties of these MM-functionals such as equivariance, influence function and asymptotic variance. Also influence functions and asymptotic distributions are derived for the proposed robust test statistics. Power curves are included for a situation which is less deviating from diagonality than the equicorrelation matrix. Furthermore, we construct bootstrap confidence intervals based on FRB and evaluate their performance in a simulation study. In addition, we illustrate these confidence intervals on Grunfeld data. The appendix also contains expressions for the partial derivatives required in the FRB procedure, a verification of the consistency conditions for the robust test on regression coefficients, and the proofs of the theorems.

References

- Baltagi, (2008) Baltagi, B. (2008). Econometrics. Springer Texts in Business and Economics. Springer Berlin Heidelberg.

- Berrendero et al., (2007) Berrendero, J., Mendes, B., and Tyler, D. (2007). On the maximum bias functions of MM-estimates and constrained M-estimates of regression. The Annals of Statistics, 35(1):13–40.

- Bilodeau and Duchesne, (2000) Bilodeau, M. and Duchesne, P. (2000). Robust estimation of the SUR model. The Canadian Journal of Statistics, 28:277–288.

- Breusch and Pagan, (1980) Breusch, T. S. and Pagan, A. R. (1980). The Lagrange Multiplier Test and its Applications to Model Specification in Econometrics. The Review of Economic Studies, 47(1):239–253.

- Cadavez and Henningsen, (2012) Cadavez, V. A. P. and Henningsen, A. (2012). The Use of Seemingly Unrelated Regression (SUR) to Predict the Carcass Composition of Lambs. Meat Science, 92:548–553.

- Croux et al., (2008) Croux, C., Filzmoser, P., and Joossens, K. (2008). Classification efficiencies for robust linear discriminant analysis. Statistica Sinica, 18:581–599.

- Davison and Hinkley, (1997) Davison, A. and Hinkley, D. (1997). Bootstrap Methods and Their Application. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press.

- Efron, (1979) Efron, B. (1979). Bootstrap methods: Another look at the jackknife. The Annals of Statistics, 7(1):1–26.

- Efron, (1987) Efron, B. (1987). Better Bootstrap Confidence Intervals. Journal of the American Statistical Association, 82(397):171–185.

- Hampel et al., (1986) Hampel, F. R., Ronchetti, E. M., Rousseeuw, P. J., and Stahel, W. A. (1986). Robust Statistics: The Approach Based on Influence Functions. Wiley.

- Hasenauer et al., (1998) Hasenauer, H., Monserud, R. A., and Gregoire, T. G. (1998). Using simultaneous regression techniques with individual-tree growth models. Forest Science, 44(1):87–95.

- Henningsen and Hamann, (2007) Henningsen, A. and Hamann, J. D. (2007). systemfit: A Package for Estimating Systems of Simultaneous Equations in R. Journal of Statistical Software, 23(4):1–40.

- Heritier and Ronchetti, (1994) Heritier, S. and Ronchetti, E. (1994). Robust bounded-influence tests in general parametric models. Journal of the American Statistical Association, 89:897–904.

- Hodgson et al., (2002) Hodgson, D. J., Linton, O., and Vorkink, K. (2002). Testing the capital asset pricing model efficiently under elliptical symmetry: A semiparametric approach. Journal of Applied Econometrics, 17(6):617–639.

- Huber and Ronchetti, (2009) Huber, P. J. and Ronchetti, E. M. (2009). Robust Statistics, 2nd edition. Wiley, New York.

- Hubert et al., (2017) Hubert, M., Verdonck, T., and Yorulmaz, O. (2017). Fast robust SUR with economical and actuarial applications. Statistical Analysis and Data Mining, 10(2):77–88.

- Koenker and Portnoy, (1990) Koenker, R. and Portnoy, S. (1990). M-estimation of multivariate regressions. Journal of the American Statistical Association, 85:1060–1068.

- Kotakou, (2011) Kotakou, C. A. (2011). Panel Data Estimation Methods on Supply and Demand Elasticities: The Case of Cotton in Greece. Journal of Agricultural and Applied Economics, 43(1).

- Kudraszow and Maronna, (2011) Kudraszow, N. L. and Maronna, R. A. (2011). Estimates of MM type for the multivariate linear model. Journal of Multivariate Analysis, 102(9):1280–1292.

- Kuson et al., (2012) Kuson, S., Sriboonchitta, S., and Calkins, P. (2012). The determinants of household expenditures in Savannakhet, Lao PDR: A Seemingly Unrelated Regression analysis. The Empirical Econometrics and Quantitative Economics Letters, 1(4):39–60.

- Lar et al., (2011) Lar, N., Calkins, P., Leeahtam, P., Wiboonpongse, A., Phuangsaichai, S., and Nimanussornkul, C. (2011). Determinants of Food, Health and Transportation Consumption in Mawlamyine, Myanmar: Seemingly Unrelated Regression Analysis. International Journal of Intelligent Technologies & Applied Statistics, 4(2):165–189.

- Lopuhaä, (1989) Lopuhaä, H. P. (1989). On the relation between -estimators and -estimators of multivariate location and covariance. The Annals of Statistics, 17(4):1662–1683.

- Lopuhaä, (1999) Lopuhaä, H. P. (1999). Asymptotics of reweighted estimators of multivariate location and scatter. The Annels of Statistics, 27(5):1638–1665.

- Lopuhaä and Rousseeuw, (1991) Lopuhaä, H. P. and Rousseeuw, P. J. (1991). Breakdown points of affine equivariant estimators of multivariate location and covariance matrices. The Annals of Statistics, 19:229–248.

- Martin et al., (2007) Martin, S., Rice, N., Jacobs, R., and Smith, P. (2007). The market for elective surgery: Joint estimation of supply and demand. Journal of Health Economics, 26(2):263–285.

- Olaolu et al., (2011) Olaolu, M., Ajayi, A., and Akinnagbe, O. (2011). Impact of National Fadama Development Project II on Rice farmers profitability in Kogi State, Nigeria. Journal of Agricultural Extension, 15(1):64–74.

- Pástor and Stambaugh, (2002) Pástor, L. and Stambaugh, R. F. (2002). Mutual fund performance and seemingly unrelated assets. Journal of Financial Economics, 63(3):315–349.

- Peremans et al., (2017) Peremans, K., Segaert, P., Van Aelst, S., and Verdonck, T. (2017). Robust bootstrap procedures for the chain-ladder method. Scandinavian Actuarial Journal.

- Salibian-Barrera, (2005) Salibian-Barrera, M. (2005). Estimating the p-values of robust tests for the linear model. Journal of Statistical Planning and Inference, 128(1):241–257.

- Salibian-Barrera et al., (2006) Salibian-Barrera, M., Van Aelst, S., and Willems, G. (2006). Principal Components Analysis Based on Multivariate MM-estimators with Fast and Robust Bootstrap. Journal of the American Statistical Association, 101(475):1198–1211.

- Salibian-Barrera et al., (2016) Salibian-Barrera, M., Van Aelst, S., and Yohai, V. J. (2016). Robust tests for linear regression models based on -estimates. Computational Statistics & Data Analysis, 93:436–455.

- Salibian-Barrera and Yohai, (2006) Salibian-Barrera, M. and Yohai, V. J. (2006). A fast algorithm for S-regression estimates. Journal of Computational and Graphical Statistics, 15(2):414–427.

- Salibian-Barrera and Zamar, (2002) Salibian-Barrera, M. and Zamar, R. H. (2002). Bootrapping robust estimates of regression. The Annals of Statistics, 30(2):556–582.

- Srivastava and Giles, (1987) Srivastava, V. K. and Giles, D. E. A. (1987). Seemingly Unrelated Regression Equations Models: Estimation and Inference. Statistics: A Series of Textbooks and Monographs. Taylor & Francis.

- Tatsuoka and Tyler, (2000) Tatsuoka, K. S. and Tyler, D. E. (2000). On the uniqueness of S-functionals and M-functionals under nonelliptical distributions. The Annels of Statistics, 28(4):1219–1243.

- Van Aelst and Willems, (2005) Van Aelst, S. and Willems, G. (2005). Multivariate regression S-estimators for robust estimation and inference. Statistica Sinica, 15:981–1001.

- Van Aelst and Willems, (2011) Van Aelst, S. and Willems, G. (2011). Robust and Efficient One-Way MANOVA Tests. Journal of the American Statistical Association, 106(494):706–718.

- Van Aelst and Willems, (2013) Van Aelst, S. and Willems, G. (2013). Fast and robust bootstrap for multivariate inference: the R package FRB. Journal of Statistical Software, 53(3):1–32.

- Van Aelst et al., (2013) Van Aelst, S., Willems, G., and Zamar, R. (2013). Robust and efficient estimation of the residual scale in linear regression. Journal of Multivariate Analysis, 116:278–296.

- Wang, (2010) Wang, H. (2010). Sparse Seemingly Unrelated Regression Modelling: Applications in Finance and Econometrics. Computational Statistics & Data Analysis, 54(11):2866–2877.

- Yohai, (1987) Yohai, V. J. (1987). High breakdown point and high efficiency robust estimates for regression. The Annals of Statistics, 15:642–656.

- Zaman et al., (2011) Zaman, K., Khan, H., Khan, M. M., Saleem, Z., and Nawaz, M. (2011). The impact of population on environmental degradation in South Asia: application of seemingly unrelated regression equation model. Environmental Economics, 2(2).

- Zellner, (1962) Zellner, A. (1962). An Efficient Method of Estimating Seemingly Unrelated Regressions and Tests for Aggregation Bias. Journal of the American Statistical Association, 57(298):348–368.

- Zhang, (2010) Zhang, Y. (2010). A general multivariate chain ladder model. Insurance: Mathematics and Economics, 46(3):588–599.

Robust Inference for Seemingly Unrelated Regression Models: Supplementary Material

Kris Peremans and Stefan Van Aelst

Department of Mathematics, KU Leuven, 3001 Leuven, Belgium

KEYWORDS: Asymptotic normal efficiency; Influence function; Fast and robust bootstrap; Robust confidence interval

9. Properties of MM-estimators

We investigate the properties of MM-estimators in more detail. To this end, we first introduce MM-functionals corresponding to the MM-estimators introduced in the manuscript. We state equivariance properties of these MM-functionals and investigate their robustness and efficiency by deriving their influence function and asymptotic variance. We present results for both the estimator of the regression coefficients and the estimator of the scatter .

9.1 Functionals

Functional versions of S and MM-estimators for the SUR model can be defined as follows.

Definition 3.

Let be the distribution function of and let be a -function as before. Then, the S-functionals of the SUR model are the solutions that minimize subject to the condition

over all and with .

To define the MM-functionals, we again decompose the scatter matrix functional into a scale and a shape component, i.e., such that .

Definition 4.

Let be the distribution function of and let be a -function as before. Given the S-scale functional , the MM-functionals of the SUR model minimize

over all and with . The MM-functional for covariance is defined as .

Note that the S and MM-estimators can be obtained by the choice , the empirical distribution function corresponding to the data.

9.2 Equivariance

Similarly as for S-estimators (Bilodeau and Duchesne,, 2000), it can easily be shown that the MM-functionals in the SUR model are equivariant under affine transformations of the regressors, regression transformations and blockwise scale transformations of the responses.

For ease of notation, let us write the MM-functionals as and with with . Then, the MM-functionals satisfy the following equivariance properties:

-

(a)

Affine equivariance of regressors:

with where the blocks are of size .

-

(b)

Regression equivariance:

for any .

-

(c)

Scale equivariance of responses:

for any diagonal matrix with diagonal matrix in which each diagonal element of is repeated times.

9.3 Influence Function

We now derive the influence functions of the MM-functionals introduced above. Since MM-functionals reduce to S-functionals when , we only have to consider influence functions for MM-functionals. While the breakdown point is a global measure of robustness, the influence function is a local measure of robustness. The influence function of a functional measures the effect on of an infinitesimal amount of contamination at a point . Consider the contaminated distribution

with the point mass distribution at and . Then, the influence function of is defined as

To derive the influence function, we consider the SUR model

where the -dimensional vector has distribution and is independent of the -dimensional error variable . We assume that follows a unimodal elliptically symmetric distribution with density

where and the function has a strictly negative derivative. The error distribution is thus symmetric around the origin. Let denote the resulting distribution of . The following theorem gives the influence functions of the regression and scatter MM-functionals for model distributions .

Theorem 1.

If has model distribution as defined above, then the influence functions of the MM-estimators for the SUR model are given by

| (22) |

and

with and where we use the notation for and . With the constants are given by

| (23) | ||||

| (24) | ||||

| (25) |

Note that the influence function of the regression functional is bounded in but unbounded in . Hence, contamination in the direction of the response has a bounded influence on . The effect becomes zero for far away outliers because the weight function becomes zero for large values of its argument. On the other hand, contamination in the predictor space can have an infinitely large effect on the estimator, but only if the corresponding residual is sufficiently small. This means that the point is a good leverage point since it does not deviate from the SUR model. Moreover, the influence function of the scatter functional only depends on and is bounded. Hence, contamination in the predictor space does not affect the scatter functional while the effect of contamination in the response remains bounded.

9.4 Asymptotic Variance

Following Hampel et al., (1986), the asymptotic variance of a functional is obtained by

By using the expressions for the influence functions in Theorem 1 we immediately obtain the asymptotic variances of the MM-estimators for the SUR model in Theorem 2 below. We use the notation for the commutation matrix of size such that for any matrix . Note that vec denotes the vector operator, stacking all columns of its matrix argument into one vector.

Theorem 2.

In case of S-estimators (), these expressions correspond to the asymptotic variances of S-estimators in Bilodeau and Duchesne, (2000). Moreover, the asymptotic variance of the scatter coincides with that in Lopuhaä, (1989) and Salibian-Barrera et al., (2006).

The asymptotic relative efficiency (ARE) for the regression coefficients , relative to the MLE , becomes

Note that the ARE does not depend on the number of predictors in the SUR model nor on the distribution of , but only depends on the number of blocks in the model and the distribution of the errors. Moreover, it can immediately be seen that the ARE of the MM-estimator does not depend on the initial loss function for the S-estimator, but only depends on the loss function . Hence, the constant in can indeed be tuned to guarantee a desired efficiency at the central model, independently of the breakdown point which is determined by the constant in .

10. Asymptotic Results of the Proposed Test Statistics

Furthermore, we present some asymptotic results of the robust test statistics and (see Sections 4 and 5 of the manuscript respectively).

10.1 Robust Tests for the Regression Parameters

Under the null hypothesis in (7) the asymptotic distributions of the test statistics and are proportional to a chi-squared distribution with degrees of freedom. Denote

for and with . Remark that the constants , and are already defined in (23), (25) and (27) respectively. Then, we have the following result.

Theorem 3.

Let have model distribution . Under the null hypothesis it holds that

and

These asymptotic null distributions can be used to obtain p-values corresponding to the test statistics in the finite-sample case. However, this standard approach requires a sufficiently large sample size and also accurate estimates of the expectations in the proportionality factors to obtain reliable results.

Robustness of these test statistics is investigated through their influence functions. The (first-order) influence function of these test statistics equals zero. Therefore, we consider their second-order influence function (Croux et al.,, 2008), which is defined as

Boundedness of this influence function guarantees stability of the asymptotic level and power of the asymptotic test in presence of contamination (Heritier and Ronchetti,, 1994). The next theorem yields the second-order influence functions of and at model distribution under the null hypothesis .

Theorem 4.

If has model distribution and if is true, then the second-order influence functions of and are given by

and

The second-order influence functions in Theorem 4 are unbounded in but bounded in . The redescending nature of the functions and guarantees that contamination in the response does not affect the test statistics when becomes large. Hence, only good leverage points can have a large effect on the test statistics. Since and the constants and are always positive, the impact of contamination is larger for than for . The increased efficiency of MM-estimators thus implies some loss in robustness.

10.2 Robust Test for Diagonality of the Covariance Matrix

The following theorem shows that under the null hypothesis in (16) the asymptotic distribution of the robust test statistics and is proportional to a chi-squared distribution.

Theorem 5.

Let have model distribution . Assume that is a diagonal matrix. Then, it holds that

and

To investigate the robustness of the resulting tests, we again derive the second-order influence function of the test statistics under the null hypothesis.

Theorem 6.

If has model distribution and if is a diagonal matrix, then the second-order influence function of and are given by

and

This theorem shows that leverage points do not influence the test statistic and that large response outliers have zero influence as well. The boundedness of the second-order influence functions ensures the stability of the asymptotic level and power of these diagonality tests (Heritier and Ronchetti,, 1994).

11. Finite-Sample Performance of diagonality test (continued)

In Section 6 of the manuscript we have investigated the power of the diagonality test for the situation where is an equicorrelation matrix with correlation ranging from 0 to 0.5 with step length 0.1. While for this setting the deviation from diagonality was present in all covariance elements, we now consider a situation that is less diverging from diagonality. In particular, we consider the same simulation setting as in the final paragraph of Section 6 but now set equal to

where takes values from 0 to 0.5 with step length 0.1. For data simulated under this alternative hypothesis, the resulting power curves are shown in Figure 6.

The left plot corresponds to the situation with normal errors without outliers. The right panel shows the power curves in case 10% contamination is added to the data as in Section 6 of the manuscript. Compared to the equicorrelation setting considered in the manuscript, all power curves increase at a slower pace because we are now considering a difficult case where only one correlation is responsible for the deviation from diagonality. However, when comparing the classical and robust Breusch-Pagan tests, the same conclusions can be drawn as in the manuscript. In absence of contamination the test based on MM-estimators performs almost as well as the classical test. Moreover, in contrast to the classical test its performance is not much affected in the presence of bad leverage points.

12. Robust Confidence Intervals

The results in Theorem 2 can be used to construct confidence intervals for the parameters in the SUR model based on their MM-estimates. For example, a confidence interval for a regression parameter can be obtained as

| (28) |

with the quantile of the standard normal distribution and an estimate of the asymptotic variance in (26) based on the empirical distribution corresponding to the data.

Alternatively, regular bootstrap confidence intervals are constructed as follows. Let be a set of parameter estimates based on bootstrap samples. Then a percentile confidence interval for is obtained as

where denotes the order statistics corresponding to the bootstrap estimates. Basic percentile (BP) confidence intervals select and . To improve the accuracy of the confidence intervals, the bias-corrected and accelerated (BCa) method (Efron,, 1987) can be used to determine the confidence levels and . See, e.g., Davison and Hinkley, (1997) for more details on percentile methods.

As explained in Section 3 of the manuscript, confidence intervals based on standard bootstrap are not attractive because they are not robust. Therefore, we propose to construct bootstrap confidence intervals based on the FRB estimates. For example, a FRB percentile confidence interval for is computed as

| (29) |

where is a set of FRB bootstrap replicates.

13. Finite-Sample Performance for Confidence Intervals

The performance of confidence intervals obtained by FRB based on robust S and MM-estimators for the SUR model is investigated by simulation. We focus on intervals for the regression coefficients with 95% confidence level. The performance is measured by their coverage and their average length.

We consider the same simulation setting as in Section 6 of the manuscript. Robust S-estimators and MM-estimators are computed with maximal breakdown point of 50% and the MM-estimator has 90% efficiency. bootstrap samples are generated for the FRB. Three different confidence intervals are calculated for the slopes in the model: asymptotic confidence intervals (AS) given by (28), and BP and BCa confidence intervals according to (29) based on FRB. For each simulation setting the coverage is estimated by the fraction of the confidence intervals that contains the true value of the parameter. The reported coverage and average lengths of the confidence intervals are the average results for all slopes in the model. In Figure 7 the coverage is depicted as a function of sample size, while the average interval lengths are given in Tables 4 and 5 for data with normal errors, containing 0% or 10% of contamination, respectively.

| Estimator | Type | Sample size | |||||||

|---|---|---|---|---|---|---|---|---|---|

| 25 | 50 | 75 | 100 | 150 | 200 | 250 | 300 | ||

| AS | 0.467 | 0.470 | 0.406 | 0.359 | 0.298 | 0.260 | 0.234 | 0.214 | |

| S | BP | 1.315 | 0.786 | 0.538 | 0.437 | 0.336 | 0.283 | 0.250 | 0.226 |

| BCa | 1.319 | 0.787 | 0.539 | 0.438 | 0.338 | 0.284 | 0.251 | 0.227 | |

| AS | 0.533 | 0.458 | 0.380 | 0.331 | 0.272 | 0.236 | 0.212 | 0.194 | |

| MM | BP | 1.064 | 0.572 | 0.431 | 0.362 | 0.288 | 0.245 | 0.218 | 0.198 |

| BCa | 1.126 | 0.573 | 0.433 | 0.364 | 0.289 | 0.246 | 0.219 | 0.199 | |

| Estimator | Type | Sample size | |||||||

|---|---|---|---|---|---|---|---|---|---|

| 25 | 50 | 75 | 100 | 150 | 200 | 250 | 300 | ||

| AS | 0.387 | 0.349 | 0.298 | 0.261 | 0.216 | 0.188 | 0.169 | 0.155 | |

| S | BP | 1.506 | 0.751 | 0.526 | 0.430 | 0.334 | 0.282 | 0.250 | 0.226 |

| BCa | 1.543 | 0.754 | 0.528 | 0.432 | 0.336 | 0.283 | 0.251 | 0.227 | |

| AS | 0.426 | 0.340 | 0.283 | 0.246 | 0.202 | 0.175 | 0.157 | 0.144 | |

| MM | BP | 1.084 | 0.587 | 0.444 | 0.374 | 0.297 | 0.254 | 0.226 | 0.205 |

| BCa | 1.108 | 0.590 | 0.446 | 0.376 | 0.298 | 0.255 | 0.227 | 0.206 | |

From Figure 7 we can see that the coverage for S and MM-estimators is very similar for all settings. These results clearly show that the FRB confidence intervals reach the nominal 95% coverage level much sooner (for already) then the asymptotic confidence intervals, which for still haven’t completely reached the nominal level. Moreover, there is almost no difference between the two types of FRB percentile confidence intervals. Hence, the more complex BCa intervals do not seem to offer any gain over the more simple basic percentile intervals in this case. For the situations with normal and t-distributed errors, the coverage converges to the nominal level for all three methods. On the other hand, for data contaminated with 10% or 30% bad leverage points in each block, the asymptotic confidence intervals fail to get close to 95% coverage while the FRB confidence intervals still reach the nominal level quickly. This clearly shows the robustness of the FRB based confidence intervals.

Using MM-estimators does not yield confidence intervals with better coverage compared to S-estimators. However, as can be seen from Table 4 and 5, confidence intervals based on MM-estimators are generally shorter than those based on S-estimators. The increased efficiency of the MM-estimators thus leads to more informative confidence intervals. These tables also show that the asymptotic confidence intervals are much shorter than the FRB intervals in all cases. However, these intervals are too short, resulting in (severe) under-coverage as seen in Figure 7. Note that in terms of average length there is again little difference between the BCa and BP confidence intervals. Finally, by comparing the two tables it can be seen that 10% of bad leverage points does not affect the average length of the FRB confidence intervals much in this setting.

Similarly as for the regression coefficients, confidence intervals for the elements of the scatter matrix or shape matrix and scale can be constructed. For the shape matrix, the behavior of the confidence intervals is the same as for the regression coefficients. For the scale and the elements of the scatter matrix the performance is generally worse in presence of contamination. The reason is that the scale S-estimator is not redescending and thus contamination has a persistent effect on the scale estimate which also affects the confidence intervals.

In summary, we can conclude that asymptotic confidence intervals only yield reliable results for clean data with large sample size while FRB confidence intervals remain reliable for contaminated data and smaller sample sizes. Moreover, MM-estimators yield more informative inference than S-estimators.

14. Example: Grunfeld Data (Continued)

As in Section 7 of the manuscript we use the Grunfeld data and consider a SUR model with three blocks corresponding to the U.S. corporations General Electric (GE), Westinghouse (W), and Diamond Match (DM). The SUR model is given in (20). As before, the MM-estimates are calculated with 50% breakdown point and a normal efficiency of 90%. The robust coefficient estimates (and their bootstrap standard errors) are presented in Table 1 of the manuscript.

We consider the construction of confidence intervals corresponding to the robust MM-estimators. Confidence intervals are computed based on asymptotic results and the fast and robust bootstrap. For the FRB bootstrap samples are generated using case resampling.

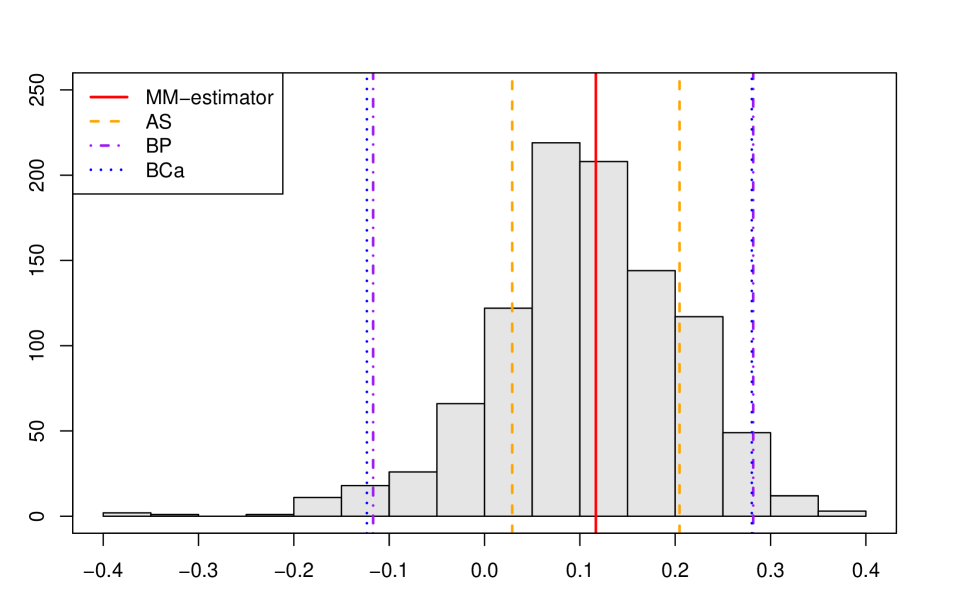

We now compare inference results for regression coefficients in the SUR model. As an example, we first focus on , the slope for predictor Capital in the regression equation for Westinghouse. A histogram of the FRB replications of is presented in Figure 8.

The solid (red) vertical line corresponds to the MM-estimate of this coefficient as reported in Table 1. The dashed (orange) lines represent the asymptotic confidence interval based on the MM-estimate as given by (28). The dash-dotted (purple) and dotted (blue) lines represent the BP and BCa confidence intervals as given by (29), respectively. It can immediately be seen that the asymptotic confidence interval which relies on the assumption that the distribution of is a normal distribution is much narrower than the other two. However, from the histogram of the FRB replications it is clear that the bootstrap distribution is skewed, which indicates that the normality assumption is not realistic. The two bootstrap confidence intervals do not rely on the normality assumption and they can also better resist the effect of outliers, which makes them more reliable in this case. When checking significance of this regression coefficient, the bootstrap confidence intervals yield a different conclusion than the asymptotic confidence interval. Indeed, both bootstrap percentile confidence intervals contain zero, implying that the coefficient is non-significant, but based on the asymptotic confidence interval the coefficient would be considered significant. However, as seen in the simulations, the asymptotic confidence interval is most likely too small, leading to under-coverage and too optimistic conclusions.

The three confidence intervals for each of the regression coefficients are reported in Table 6.

| Corporation | Coefficient | AS | BP | BCa | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| lower | upper | lower | upper | lower | upper | ||||||||

| GE | -68. | 941 | 7. | 619 | -84. | 541 | 21. | 659 | -89. | 872 | 17. | 221 | |

| 0. | 015 | 0. | 051 | 0. | 010 | 0. | 069 | 0. | 012 | 0. | 071 | ||

| 0. | 117 | 0. | 187 | 0. | 083 | 0. | 184 | 0. | 096 | 0. | 186 | ||

| W | -19. | 106 | 6. | 465 | -25. | 379 | 18. | 015 | -34. | 574 | 10. | 736 | |

| 0. | 035 | 0. | 082 | 0. | 017 | 0. | 105 | 0. | 027 | 0. | 121 | ||

| 0. | 029 | 0. | 204 | -0. | 117 | 0. | 282 | -0. | 123 | 0. | 280 | ||

| DM | -2. | 253 | 0. | 543 | -2. | 187 | 0. | 110 | -2. | 167 | 0. | 170 | |

| -0. | 016 | 0. | 020 | -0. | 011 | 0. | 021 | -0. | 013 | 0. | 019 | ||

| 0. | 554 | 0. | 674 | 0. | 411 | 0. | 773 | 0. | 390 | 0. | 757 | ||

As already seen in the simulations, both percentile confidence intervals are very similar, while the asymptotic confidence intervals are generally much shorter. This illustrates again that asymptotic confidence intervals may lead to unreliable conclusions.

Appendix

Partial derivatives of . In order to apply the fast and robust bootstrap procedure the partial derivatives need to be computed. The Jacobian of given in equation (6) has the following form

Note that the two upper rows in this gradient correspond to the estimating equations of the MM-estimator, while the two bottom rows correspond to those of the S-estimator. The expressions for the S-estimator are omitted because these are similar to the derivatives for the MM-estimator. Consider the matrices

where the vector is repeated times. The vector has length and is defined as with the 1 at the th entry of the vector. Write and , that is, and contain the information of the th observation across all blocks. Introduce the following notation as well:

Straightforward derivations then lead to the following expressions:

Consistency condition of and . Consider the function of defined through equations (10) and (11) (a similar derivation holds for ). In order for the partial derivatives of to vanish it is sufficient to show that the partial derivatives of converge to zero for . Differentiating (32) with respect to leads to

Rearranging terms and evaluating the inner derivative we obtain

which is exactly zero for due to the estimating equations of .

Differentiating (32) with respect to leads to

The right hand-side of this equality can be simplified to

By evaluating the previous line at and using the estimating equations for , it can be shown that the right hand-side reduces to zero.

Proof of Theorem 1. Let have model distribution with the distribution of and the elliptically symmetric distribution of . Let us denote to simplify the notation. The influence function of is obtained by differentiating the estimating equations for w.r.t. and evaluating the result at . The derivation of these equations is similar as in the finite-sample case. For a general distribution function of , the estimating equations of the MM-functionals and are given by

where and . We thus have

which can be rewritten as

Applying the chain rule and using the estimating equation at yields

The second term simplifies to . Differentiation of the first term and symmetry of yields

Computing the inner derivatives and simplifying the result leads to

| (30) |

Splitting the first integral into a and a component yields

Using symmetry and results in (Lopuhaä,, 1999) this can be rewritten as

Combining both integrals in (30) now yields

Rearranging terms leads to the result in (22). ∎

Proof of Theorem 2. Consider with model distribution . The asymptotic variance of is given by

Using the expression for the influence function in (22), we obtain

Splitting the remaining integral yields

which by symmetry can be rewritten as

Combining the results yields (26). For a general distribution this result is obtained by using the affine equivariance property. ∎

To proof Theorem 3, we need the following lemma.

Lemma 1.

Under and the conditions of Theorem 3, it holds that

| (31) |

Proof of Lemma 1. We prove the lemma for the simple case , that is, and . First, application of the delta method yields the following first-order approximation

where , and . If we replace with its true value , we obtain an asymptotic equivalent expression. A similar expression is true for . Decompose with and similarly for and other variables. Then a first-order approximation for is given by

with , since under it holds that .

In this simple case it is easy to show that the th component of the right hand-side of equation (31) is equal to . Therefore, we only need to prove the lemma for the remaining components. Denote as the elimination matrix, i.e., . Then, using the first-order approximations we obtain

Considering the general expression for the inverse of a block matrix, the terms between brackets reduce to

Consequently, we have that

In the last line we recognize the first-order approximation of . Hence,