Asymptotic Correlation Structure of Discounted Incurred But Not Reported Claims under Fractional Poisson Arrival Process

Abstract

This paper studies the joint moments of a compound discounted renewal process observed at different times with each arrival removed from the system after a random delay. This process can be used to describe the aggregate (discounted) Incurred But Not Reported claims in insurance and also the total number of customers in an infinite server queue. It is shown that the joint moments can be obtained recursively in terms of the renewal density, from which the covariance and correlation structures are derived. In particular, the fractional Poisson process defined via the renewal approach is also considered. Furthermore, the asymptotic behaviour of covariance and correlation coefficient of the aforementioned quantities is analyzed as the time horizon goes to infinity. Special attention is paid to the cases of exponential and Pareto delays. Some numerical examples in relation to our theoretical results are also presented.

Keywords: Applied probability; Fractional Poisson process; Incurred But Not Reported (IBNR) claims; Infinite server queues; Correlation.

1 Introduction

To model Incurred But Not Reported (IBNR) claims in insurance, in this paper it is first assumed that the claim arrivals follow a renewal process and the reporting delay for each claim is arbitrary. It is known (e.g. Willmot (1990), Mikosch (2009) and Ross (2014)) that unreported claims in actuarial science can be connected to quantities considered in other fields such as the number of customers or particles in a system with an infinite server queue structure (i.e. customers are served immediately upon their arrivals by one of those many servers). There is a vast literature on systems involving infinite server queues. See e.g. Brown and Ross (1969), Keilson and Seidmann (1988), Liu et al. (1990), and Keilson and Servi (1994) for some classical results; and Ridder (2009), Pang and Whitt (2012), Blom and Mandjes (2013), Jansen et al. (2016), Moiseev and Nazarov (2016), and Blom et al. (2017) for some recent development of the subject. As mentioned in Mikosch (2009, Section 8.2.4), the counting process of the IBNR claims can be viewed as a generating model for the activities of processing packets in a large data network. In this case, the number of active sources at time is the subject of interest of that model. Aggregate IBNR claim process is also related to the cumulative shock model with delayed termination (e.g. Finkelstein and Cha (2013, Section 4.4)), where the reporting time of a claim (i.e. the claim arrival time plus its reporting lag) corresponds to the time of the effective event which terminates fault. Interested readers are also referred to Blanchet and Lam (2013) for the application of infinite serve queues in large insurance portfolios. See also Badescu et al. (2016a,b) for the theoretical properties and parameter estimations of a marked Cox model for IBNR claims.

In the analysis of such stochastic models, the knowledge of correlation structure of the underlying arrival process is often useful to understand the joint behaviour of the process of our interest observed at different times. Indeed, the correlation between two instants and when can be used to assess if the process has a long memory, i.e. if the state of the process at a given time has significant impact on its state at a much later time, and can serve to quantify such impact. This kind of information can be of paramount importance for decision making. In particular, the notion of long-range dependence appears when the correlation function exhibits the form of power-law decay. This definition arises in different fields such as finance, data network, and earthquake modelling. From a statistical point of view, the theoretical results allow the possibility of fitting a model to physical phenomena where long-range dependence or short-range dependence is practically observed, as explained in e.g. in Mikosch (2009, Section 8.2.4). In this paper, we shall focus on studying the covariance and correlation structures of compound renewal sums at different times (in the presence of a random delay in realization) as well as their asymptotic behaviours. To this end, the related joint moments are first derived, which may be of interest in its own right as they can in principle be used in moment-based approximations. It should be also noted that the joint moments and covariance structure of the aggregate discounted claims without any reporting delay were studied by Léveillé and Adékambi (2010, 2012) and Léveillé and Hamel (2013).

To model the long-range dependence property for the renewal process governing the claim arrival process, a fractional generalization of the Poisson process, known as the fractional Poisson process, will be utilized. It is known that there are different ways to define the fractional Poisson process such as using time-changed processes (e.g. Leonenko et al. (2014)). Here we adopt the definition obtained by a renewal-type treatment (e.g. Mainardi et al. (2004), and Meerschaert et al. (2011)), where the fractional Poisson process is viewed as a renewal process with Mittag-Leffler interarrival times. Consequently, the interarrival times are heavy-tailed and have infinite mean (e.g. Repin and Saichev (2000)) as opposed to the light-tailed exponential interarrival times with finite mean in the Poisson process. The fractional Poisson process is an interesting choice in the context of actuarial science, and in particular it can be used to model the arrival of claims caused by rare and extreme events such as storms and high-magnitude earthquakes in line with the discussions in e.g. Benson et al. (2007) and Biard and Saussereau (2014). Indeed, Benson et al. (2007) commented that the use of this type of renewal process is a critical extension from the Poisson assumption because the application of a Poisson model for a geologic process with heavy-tailed waiting times between events will result in a significant misrepresentation of the associated risk. Our analysis will shed light on how this heavy-tail feature impacts the long-term correlation of the IBNR process.

In what follows, we shall define the model in the context of actuarial science. It is assumed that the claim counting process is a renewal process with the sequence of arrival times where for . Here is the set of positive integers, and represents the sequence of interarrival times that are independent and identically distributed (iid) with cumulative distribution function (cdf) and probability density function (pdf) . We adopt the usual convention that . Therefore, the claim count is defined by with . The renewal function of the claim counting process shall be denoted by , where is the -th fold convolution of the cdf with itself and is its pdf. Let us introduce as the sequence of claim amounts which are also assumed to be iid. Denoting as the time-lag (or reporting delay) corresponding to the -th claim arrival, the time-lags are assumed to form an iid sequence with common cdf and pdf . It is assumed that the claim counting process (or the interarrival times ), the claim amounts and the delays are mutually independent. Such independence assumption is standard in the actuarial literature (see e.g. Karlsson (1974) and Willmot (1990)), and we refer interested readers to Landriault et al. (2017) for some discussions on possible dependence assumptions on the triplet . For later use, the generic random variables of , and are denoted by , and respectively. It will be seen that the moments of the claim amount are sufficient for our analysis, and therefore we define and for convenience.

The total discounted IBNR claim process is now defined by

| (1.1) |

where is a constant force of interest. We shall adopt the convention that whenever . For notational simplicity, we let when . Note that, although the model is explained in an actuarial setting, it can be applied to a queueing context via a switch of terminology by changing ‘claim arrival’ and ‘reporting delay’ to ‘customer arrival’ and ‘service time’ respectively. In particular, if the distribution of is assumed to be a point mass at one, then can be interpreted as the total number of customers at time in a queue. (In such case, the assumption of independence between and means that the service offered to customers does not depend on their arrival times, which is a standard assumption in queue.) Consequently, our formulation under an actuarial context is more general than a queue, as (i) insurance companies possibly take into account the effect of interest (allowing for ) when discounting claims; and (ii) actuaries associate a loss amount to each claim event when calculating or estimating outstanding claims. In this paper, we are interested in the covariance and correlation structures of and for , which are defined as and respectively.

Concerning the renewal process for claim arrivals, in most of our analysis it is essential to know explicitly the renewal density for . The class of fractional Poisson processes turns out to be a good candidate thanks to its nice renewal density (see (4.1)). Certainly, some results will be simplified for the Poisson process as does not depend on .

2 Outline of results and long-range dependence of IBNR process

In order to have a global overview of the paper, our main contributions are presented here. In Section 3, the marginal moments of and the joint moments of and for are derived in Theorems 1 and 2 using renewal arguments, and consequently the covariance is studied in Corollary 1 and Theorem 3. Section 4 is devoted to the asymptotic behaviours (as ) of the mean, variance and covariance in the case of fractional Poisson arrival process. To obtain simpler formulas, distributional assumptions on the random delays are made, where exact and asymptotic results are provided in Propositions 2-4 for the exponential case, and asymptotics in Propositions 5-7 for the Pareto case. We remark that the focus of the paper is to analyze the properties of the IBNR process and to provide probabilistic interpretations. Immediate practical applications of the results, including statistical estimation and fitting with a data set, are outside the scope of this paper and will be topics for future research. For legibility purpose, the asymptotic results obtained in the paper are summarized as follows when claims occur according to a fractional Poisson process with index . The notation means that as for some constant that possibly depends on but not on . Moreover, means that the delay is exponentially distributed with mean whereas means that the survival function of is given by (4.27). We remark that the multiplicative constants are omitted in the summary below not only for the sake of brevity but also for the fact that the asymptotic correlation up to a multiplicative factor will be sufficient for determining whether a process possesses short-range or long-range dependence (see Definition 2). Nonetheless, the exact expressions for these multiplicative constants are given by (4.14), (4.19), (4.26), (4.32), (4.35) and (4.45) in the aforementioned propositions and can be computed or approximated (see Section 5).

| (2.10) | |||||

We emphasize that our contributions are not only to actuarial science but also to queueing theory. In the queueing literature, only few papers have dealt with fractional Poisson arrivals because the techniques are usually very specific to fractional calculus. See e.g. Orsingher and Polito (2011) for a particular queue with a birth and death structure modelled by fractional Poisson arrivals, which is one of the rare papers on the subject. However, there are no results in the literature concerning infinite server queues where the arrivals are modelled by a fractional Poisson process, to the best of our knowledge. The result (LABEL:tableau_recap1) and the tables in (2.10) enable us to give some qualitative insight on whether the IBNR process (or the queue as a special case) exhibits long-range dependence under the fractional Poisson setting. The behaviour will turn out to be different depending on the distribution of the delays, as displayed in (2.11)-(2.19) thereafter. The choice of the delays, namely exponential and Pareto, is motivated by the fact that these are representatives of light-tailed and heavy-tailed distributions respectively. These distributions were also chosen for technical purpose, and we however believe that this will shed light on whether behaviours resembling those in (2.11)-(2.19) are valid more generally for wider classes of light-tailed and heavy-tailed distributions in future research. Interested readers are also referred to Resnick and Rootzen (2000) for an infinite server queue with heavy-tailed service time and Poisson arrivals, where heavy-tailed service time was argued to be a good candidate for modelling the transfer of huge files across the World Wide Web. In the following, we first state the notion of long-range dependence defined by Maheshwari and Vellaisamy (2016, Section 2.2).

Definition 1

(Long-range dependence in Maheshwari and Vellaisamy (2016)) Let be a stochastic process. Suppose that the correlation function satisfies, for all ,

for some and . If , then is said to possess long-range dependence property. On the other hand, if , then has short-range dependence.

From Leonenko et al. (2014, p.10), it is known that the fractional Poisson process with index has long-range dependence property. However, the above Definition 1 only includes processes where the correlation function exhibits power decay (and it excludes the cases where the correlation decreases exponentially or follows other decay law). According to Mikosch (2009, p.283), one also has the following more general definition of long-range dependence, which is adapted to stochastic processes that are not necessarily stationary.

Definition 2

(General notion of long-range dependence) Let be a stochastic process. Then is said to possess long-range dependence property if one has for all that

On the other hand, has short-range dependence if, for all ,

For convenience, from now on long-range dependence and short-range dependence will be abbreviated as LRD and SRD respectively. It is instructive to note that if a process has the LRD (resp. SRD) property under Definition 1, then it also has the LRD (resp. SRD) property under Definition 2. In the upcoming discussion, Definition 2 will be adopted. In the case where the delays follow exponential distribution, one sees from (LABEL:tableau_recap1) that

| (2.11) |

and therefore has SRD. When the delays are distributed, the asymptotic behaviour of the correlation can be readily obtained using (2.10), resulting in the following table.

| (2.15) |

The above results can be compared to the situation where arrivals occur according to a Poisson process (i.e. ). We only look at the discount-free case (i.e. ) as follows. When , we use the covariance in (3.8) along with the variance in (3.11) to easily check that in the Poisson case, and therefore the process has SRD. This is consistent with the fractional Poisson case (i.e. ) described in (2.11). In contrast, when , we omit the details and state that (3.8) implies in the Poisson case. Moreover, one can use (3.11) with the help of L’Hôpital’s rule to verify that if ; if ; and if , and consequently the following table is constructed.

| (2.19) |

Comparing (2) and (2.19), it is interesting to note that is SRD in the Poisson case but LRD in the fractional Poisson case when the Pareto delay parameter is such that . For other values of the dependence property in both cases are in agreement.

These correlation behaviours can be further interpreted as follows. When the delay distribution is exponential which is light-tailed, a claim that has occurred but has not been reported at time is likely to be reported by time when grows large, regardless of whether the claim arrives according to a Poisson or a fractional Poisson process. This explains the SRD property. On the other hand, switching from exponential to Pareto delay which is heavy-tailed, an unreported claim at time is more likely to remain unreported at time (for large ) because . Here means that for large enough, which is a generalization of the classical stochastic order for random variables (see e.g. Shaked and Shanthikumar (2007, Chapter 1)). Consequently, the process may have a tendency to be LRD. Note that increasing the Pareto shape parameter leads to stochastically smaller delay (in the sense that for ), which explains the observation from (2) and (2.19) that the asymptotic correlation between and decreases faster (as a function of ) as increases, and eventually switches from LRD to SRD once exceeds a certain threshold. In particular, for Poisson claim arrivals (see (2.19)), it is noticed that is LRD if and only if , i.e. when the Pareto delay has infinite mean. For fractional Poisson claim arrivals with index , the interarrival times are heavy-tailed (see (4.2)) and have infinite mean, and hence it is natural that there is a competition between the index for the interarrival time and the Pareto parameter , and the threshold in this case is given by as in (2).

Remark 1

Instead of analyzing the behaviour of as (for fixed ), it will also be interesting to study as both and tend to infinity. For example, one may replace and by and respectively and look at , and our exact results (e.g. Corollary 1 and Equation (4)) are still valid, from which asymptotics as (for fixed ) may be obtained. However, we leave this as future research because it is the asymptotics of as that help us determine whether the IBNR process is SRD or LRD.

3 General results

In this section, general recursive formulas for the joint moments of the total discounted IBNR claims and are derived without any specific distributional assumptions on the interarrival times , the reporting delays or the claim amounts (recall that the moments of the claim amounts suffice in all the analysis). Our results can be conveniently expressed in terms of the Dickson-Hipp (D-H) operator (see Dickson and Hipp (2001)). For any integrable real function (with non-negative domain), the D-H operator is defined by with both and non-negative. We begin by looking at the expectation in the following proposition.

Proposition 1

For a renewal claim arrival process, the mean of the total discounted IBNR claims until time is given by

| (3.1) |

In particular, when this reduces to

| (3.2) |

Proof: By taking expectation on (1.1) with the use of independence assumptions, one finds

which simplifies to give (3.1). Then (3.2) follows immediately as .

This direct technique applied in Proposition 1, however, is not very helpful to derive the expression for higher-order moments. For higher moments, it is useful to employ the conditioning technique based on the first claim arrival time . It is thus convenient to define the new notation

Conditioning on , we note that is also a discounted IBNR claim that has the same distribution as . Then may be expressed in terms of as

| (3.3) |

Subsequently, recursive formula for the marginal moments of , namely , can be derived for via a binomial expansion in Theorem 1. We remark that the same result can also be obtained by considering the moment generating function of followed by differentiation: such a technique was used by Woo (2016) who considered the joint moments of discounted compound renewal sums for dependent business lines (or different types of dependent claims) evaluated at the same time point . However, our technique of using a binomial expansion is easily applicable in the present context for the joint moments of the discounted IBNR process (for a single line of business) evaluated at different time points and , namely and , as in the proof of Theorem 2.

Theorem 1

For and , a recursive formula for evaluating is given by

| (3.4) |

where the starting value is .

Proof: See Appendix A.1.

Theorem 2

For and , the joint moments of and can be calculated recursively as

| (3.5) |

and this requires the application of Theorem 1 as a starting point.

Proof: See Appendix A.2.

Furthermore, from Theorems 1 and 2, the covariance formula for and is readily available as given below.

Corollary 1

For a renewal claim arrival process, the covariance of the total discounted IBNR claims at the time points and (where ) is given by

| (3.6) |

If there is no discounting (i.e. ), this reduces to

| (3.7) |

Furthermore, for a Poisson process with rate (i.e. ), it is simplified to

| (3.8) |

which is consistent with the covariance expression in Blom et al. (2014, Section 4).

The following corollary is immediately obtainable by letting in Corollary 1.

Corollary 2

For a renewal claim arrival process, the variance of the total discounted IBNR claims at time is given by

| (3.9) |

When , this reduces to

| (3.10) |

Furthermore, for a Poisson arrival process with rate , it is simplified to

| (3.11) |

Note that as , where .

Theorem 3

When and , the limit of is given by

| (3.12) |

Proof: First, we use the result which is obtainable by applying the Smith’s Renewal Theorem to (3.2) as

By taking the limit with the help of dominated convergence, the first term on the right-hand side of (1) in Corollary 1 becomes

where the second term in the integration converges to . This can be cancelled out with the third term in (1). Then, the desired result (3.12) follows.

The result in Theorem 3 shows that, provided that the delay time is integrable, the IBNR claims are asymptotically uncorrelated, i.e. on a first approximation, one has as . More information on the speed of convergence of the covariance towards will be given in the forthcoming Propositions 4 and 7 when additional distributional assumptions are made. In fact, one of the obstacles in the proofs in those propositions is to be able to provide a second order approximation for the joint moment as , in order to get some information on the rate of decrease of .

4 Fractional Poisson Process

In this section, we consider the fractional Poisson process for the claim counting process , so that the renewal function and renewal density are given by, for ,

| (4.1) |

where is the (ordinary) Gamma function defined by for , and and are parameters such that and . From Equation (28) of Laskin (2003), its variance is given by

where is the Beta function. Therefore, the variance is increasing in time according to a power law when . If , this process becomes the ordinary Poisson process with rate . From Repin and Saichev (2000), the asymptotic behaviour for the survival function of the interarrival times satisfies (when )

| (4.2) |

where is some constant. For the estimation of the parameters and of a fractional Poisson process, interested readers are referred to Cahoy et al. (2010), who first derived the estimators by matching the first two moments of the log of the interarrival time and then proved their asymptotic normality.

In the sequel, two different distributional assumptions for the random delay variable , namely exponential and Pareto, will be considered in detail. To proceed with our analysis, we first recall the definitions and properties of some special functions.

-

(i)

The Gaussian (or ordinary) hypergeometric function is defined as the power series (for )

(4.3) where for is the Pochhammer symbol with . Its integral representation is given by

(4.4) provided that the right-hand side converges. We also have the relationship between hypergeometric function and incomplete Beta function given by

(4.5) Another important identity for the Gaussian hypergeometric function is

(4.6) -

(ii)

The confluent hypergeometric function of the first kind or the Kummer’s function introduced by Kummer (1837) (see e.g. Abramowitz and Stegun (1972, Chapter 13)) is defined by

(4.7) and its integral representation is

(4.8) We also have the transform relation between two Kummer’s functions as

(4.9) The Kummer’s function satisfies

(4.10) See Equation (13.1.4) on p.504 of Abramowitz and Stegun (1972).

4.1 Exponential delay

In this section, it is assumed that for , where is the exponential parameter for the delay so that and .

Expectation of total discounted IBNR process. We first establish an expression for and provide its asymptotic behaviour as .

Proposition 2

With exponential delay in a fractional Poisson claim arrival process, the mean of the total discounted IBNR claims when is given by, for ,

| (4.11) |

and for ,

| (4.12) |

where is the renewal function given in (4.1) for the fractional Poisson process. In addition, the corresponding asymptotic behaviours are

| (4.13) |

and

| (4.14) |

respectively.

Proof: First, we note that for exponential delay, one has . In particular, when . Hence, , and as a result of Proposition 1 we have the relation

| (4.15) |

In other words, it is immediate to obtain the mean in the presence of discounting from the mean without discounting.

When , we have from Proposition 1 that . Then, with the fractional Poisson process for claim arrivals, substitution of its renewal density (4.1) followed by a change of variable yields

| (4.16) |

Utilizing the Kummer’s function in (4.8), the above expectation may be neatly expressed as (4.11). Consequently, using the relation (4.15), we easily obtain (4.12).

Example 1

(Poisson process) For notational convenience, we denote the present value of a -year continuous annuity payable at rate $1 per year as . When the claims arrive according to a Poisson process with rate , from Proposition 1 we have and thus from (4.15). Of course, the same results are obtainable by setting in Proposition 2, since when the fractional Poisson process is just a Poisson process. In particular, noting that from (4.7), the result follows from (4.11) for . Also, asymptotic behaviours are given as

Variance of total discounted IBNR process. Next, from (3.9), we find the variance of and its asymptotic result in the following proposition.

Proposition 3

With exponential delay in a fractional Poisson claim arrival process, the variance of the total discounted IBNR claims when is given by

| (4.17) |

where

| (4.18) |

In addition, the asymptotic behaviour when is

| (4.19) |

Proof: The three terms on the right-hand side of (3.9) are expressed as follows. The first term can be calculated by using (4.12), and (4.1) as

| (4.20) |

Using the infinite series representation of the Kummer’s function in (4.7) with a change of variable from to , the integral term above can be expressed as

| (4.21) |

where is defined in (4.18) and the last equality is due to the Kummer’s transformation (4.9). From (3.1) together with (4.1) and (4.12), the sum of the remaining two terms in (3.9) is given by

| (4.22) |

To obtain the asymptotic formula (4.19) as , we focus on the first term of in (3) (or (3)) and would like to show that

| (4.23) |

for some constant . Note that (4.10) implies

In order to apply such an asymptotic result, we need to check the validity of interchanging limit and infinite summation on the left-hand side of (A.57). It can be proved that the related sequence is uniformly bounded (which gives a sufficient condition). This part of the proof is not trivial and is provided in Part 1 of the ‘Supplementary materials’. We can now evaluate the limit on the left-hand side of (A.57) by interchanging the order of limit and infinite summation followed by substitution of (4.18), and this gives rise to

Hence, we identify in (A.57) so that (3) asymptotically behaves like . Combining (3) and (3) with asymptotic results of (3) and (4.14) yields (4.19).

Covariance of total discounted IBNR processes. We finish this section by studying the covariance of and and its asymptotic behaviour as .

Proposition 4

With exponential delay in a fractional Poisson claim arrival process, the covariance of the total discounted IBNR claims and for is given by

| (4.24) |

where

| (4.25) |

In addition, the asymptotic behaviour when is

| (4.26) |

Proof: See Appendix A.3.

4.2 Pareto delay

This section considers a heavy-tailed distribution for random delay. In particular, it is assumed that follows a Pareto distribution with tail

| (4.27) |

where are the parameters. In this case, when . However, if then has infinite mean, and consequently is not a directly Riemann integrable function and the Smith’s Renewal Theorem is no longer applicable. In the rest of this section, it is assumed that . The proofs of all three propositions require the next lemma.

Lemma 1

Define, for ,

| (4.28) |

where and . The above integral satisfies, as ,

| (4.29) |

for some constant . In particular, when , finer asymptotic results can be given by, as ,

| (4.30) |

for some constants and .

Proof: See Part 2 of the ‘Supplementary materials’.

Expectation of total IBNR process. We have the following proposition for the mean of .

Proposition 5

With Pareto delay in a fractional Poisson claim arrival process, the mean of the total IBNR claims when is given by

| (4.31) |

Its asymptotic behaviour is, as ,

| (4.32) |

Proof: Substitution of (4.1) and (4.27) into (3.2) yields

from which (4.31) follows by a change of variable from to .

Regarding the asymptotic behaviour, we separate the analysis into three cases as follows.

Case 1. : The integral in (4.31) can be expressed in terms of the incomplete Beta function (4.5), i.e.

As , one finds the first asymptotic result in (4.32).

Remark 2

Consider the fractional Poisson claim arrival process with . One particular consequence of the asymptotic results (4.32) in Proposition 5 is that

The above result can be intuitively understood in the following way. Since the interarrival time and the delay exhibit power decay according to (4.2) and (4.27), one checks easily that

Hence, if then delays are too long and cannot make up for the faster arriving claims, which justifies why the expected value of IBNR claims tends to infinity as time goes by.

Variance of total IBNR process. The upcoming Proposition 6 is concerned with the asymptotic behaviour of . We first introduce the following lemma in preparation for its proof.

Lemma 2

Let be a continuous function, and define the integral, for ,

| (4.33) |

where is fixed. It is assumed that and so that the integral must converge. We have the asymptotic result, as ,

| (4.34) |

Proof: See Part 3 of the ‘Supplementary materials’.

Proposition 6

With Pareto delay in a fractional Poisson claim arrival process, the asymptotic behaviour of the variance of the total IBNR claims when is, as ,

| (4.35) |

where is given by (4.28).

Proof: Recall that the variance of is given by (3.10). Application of (4.1), (4.27) and (4.31) yields that its first term equals

| (4.36) |

To analyze the asymptotic behaviour of , we mainly focus on the term (6). The analysis is separated into three cases as follows.

Case 1. : With the help of (4.5) and (4.3), (6) can be rewritten as

| (4.37) | |||

| (4.38) |

where the last two lines are due to a change of variable from to together with (4.4). Note that the second and the third terms in (3.10) are equivalent to and respectively, and their asymptotics are given by (4.32) as

| (4.39) |

This case can be further subdivided into two cases.

Case 1a. : Now, we shall proceed to prove that (4.38) is asymptotically proportional to as . To see this, we let

| (4.40) |

and look at

| (4.41) | ||||

| (4.42) |

See (A.4) in Appendix A.4 for the calculation of the limit using the uniform convergence of the series on . Combining (4.39) and (4.42), the first two results of (4.35) and part of the third result when follow.

Case 1b. : The integral in (4.37) of the same form as (4.33) and thus, a direct application of (4.34) with , , , , and yields, as ,

where . Because the assumption implies as , combining with the results in (4.39) we observe that the second term in (3.10) dominates the asymptotic behaviour which is proportional to . Therefore, the part of the third result of (4.35) when follows.

Case 2. : In this case, we can re-express the integral in (6) in terms of (4.28) as

| (4.43) |

It is shown in Appendix A.4 that

| (4.44) |

5 Numerical Examples

This section is dedicated to numerical illustrations of the theoretical results regarding some exact and asymptotic expressions of the mean, variance, covariance and correlation of IBNR processes for fractional Poisson claim arrivals with exponential and Pareto delay distributions. In all examples, it is assumed that the first two moments of the claim amount are and respectively (so that and the coefficient of variation of indicates claim with high variability). In addition, the parameter of the fractional Poisson process is assumed to be , and except for Example 5 we assume a force of interest of .

Example 2

(Impact of parameters of delay distribution) In this example, the underlying claim arrival process is assumed to have fractional Poisson parameter , and both and delays will be considered under various choices of parameters. We first calculate the asymptotic mean and variance of the IBNR claims by plugging in a large (where ) into our asymptotic expressions. The results are listed in Table 2 and Table 2. The corresponding exact values, whenever they can be calculated explicitly using our theoretical results, are quoted in parenthesis. The asymptotic and the exact values are very close in each case. Table 2 shows that decreases as increases for exponential delays. Intuitively, this is due to the fact that for (where means that usual stochastic ordering for all ), as stochastically smaller delays imply that incurred claims are reported quicker and there are less IBNR claims. Similarly, when one switches to Pareto delay, the monotonicity of in and can be explained by the stochastic orderings for and for . Note that the values of in Table 2 show the same pattern as those in Table 2. Moreover, the values of and in Table 2 are of small magnitude for exponential delays, and this is consistent with the implication of the summary in (LABEL:tableau_recap1) that and tend to zero as tends to infinity. However, for Pareto delays, the magnitude of and is large when but is small when . Such an observation is consistent with (2.10) which indicates that both and tend to infinity or zero depending on whether or (recall that is fixed at ). See also Remark 2.

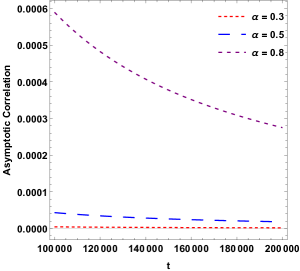

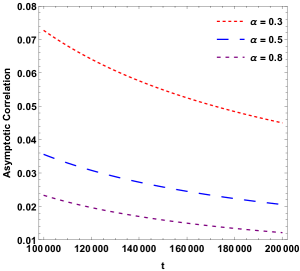

Next, the asymptotic covariance and correlation between and are provided in Table 3 and Table 4 respectively. In each table, we consider two scenarios with different initial time but the same time frame . Specifically, in Case 1 we assume and while in Case 2 we let and . Although the asymptotic covariances in Table 3 show similar pattern to those in Table 2 and Table 2 concerning means and variances, it is important to note that the covariance should always tend to zero as tends to infinity according to (LABEL:tableau_recap1) and (2.10). The high values of the covariance for Pareto delays when are attributed to the fact that the proportionality constant is large in these cases (see (4.45)). In calculating the asymptotic correlation in Table 4, we are dividing the results in Table 3 by the square root of the product of the asymptotic variances and because both and are large. It is observed that correlation decreases when increases for delay or when increases for delay. However, the behaviour of the correlation in response to a change in for delay depends on the fixed value of . In particular, the correlation decreases in when but increases in when . For both exponential and Pareto delays, the correlation increases as the initial time increases (while keeping the time frame fixed).

| Exponential | Pareto | ||||

| 0.100726 | 0.2 | 171.345 | 196.824 | 226.091 | |

| (0.100730) | (171.339) | (196.812) | (226.068) | ||

| 0.2 | 0.050363 | 0.4 | 18.4377 | 24.3287 | 32.1020 |

| (0.050364) | (18.4294) | (24.3120) | (32.0685) | ||

| 0.5 | 0.020145 | 1.0 | 0.057982 | 0.115965 | 0.231930 |

| (0.020145) | (0.066325) | (0.125668) | (0.237372) | ||

| 1.0 | 0.010073 | 1.2 | 0.025181 | 0.050363 | 0.100726 |

| (0.010073) | (0.023468) | (0.046426) | (0.091681) | ||

| 2.0 | 0.005036 | 1.4 | 0.012591 | 0.025181 | 0.050363 |

| (0.005036) | (0.012545) | (0.025060) | (0.050041) | ||

| Exponential | Pareto | ||||

| 0.1 | 1.004398 | 0.2 | 14,755.3 | 19,469.8 | 25,690.5 |

| (0.994294) | |||||

| 0.2 | 0.399871 | 0.4 | 210.101 | 365.806 | 636.906 |

| (0.397343) | |||||

| 0.5 | 0.126382 | 1.0 | 0.231930 | 0.463859 | 0.927718 |

| (0.125977) | |||||

| 1.0 | 0.055399 | 1.2 | 0.120935 | 0.262715 | 0.588618 |

| (0.055298) | |||||

| 2.0 | 0.025129 | 1.4 | 0.061263 | 0.133768 | 0.301616 |

| (0.025104) | |||||

| Exponential | Pareto | ||||||||

| Case 1: | Case 1: | Case 1: | Case 2: | ||||||

| 0.1 | 0.2 | 2,131.32 | 2,786.52 | 3,646.48 | 4,112.99 | 5,389.03 | 7,066.23 | ||

| 0.2 | 0.4 | 45.4345 | 73.6313 | 120.865 | 73.4282 | 119.888 | 198.112 | ||

| 0.5 | 1.0 | ||||||||

| 1.0 | 1.2 | ||||||||

| 2.0 | 1.4 | ||||||||

| Exponential | Pareto | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Case 1: | Case 2: | Case 1: | Case 2: | ||||||

| 0.1 | 0.2 | ||||||||

| 0.2 | 0.4 | ||||||||

| 0.5 | 1.0 | ||||||||

| 1.0 | 1.2 | ||||||||

| 2.0 | 1.4 | ||||||||

Example 3

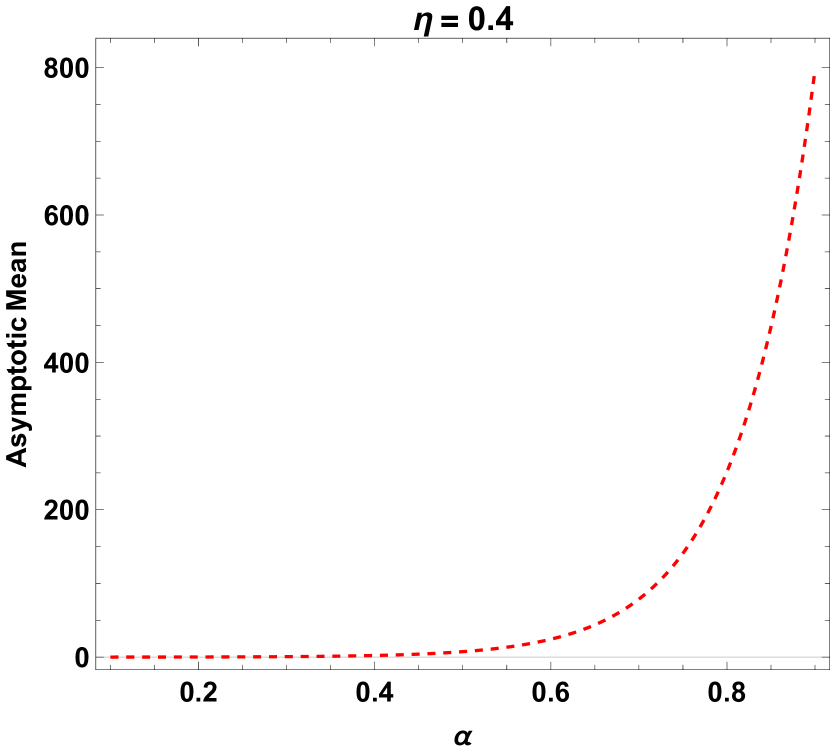

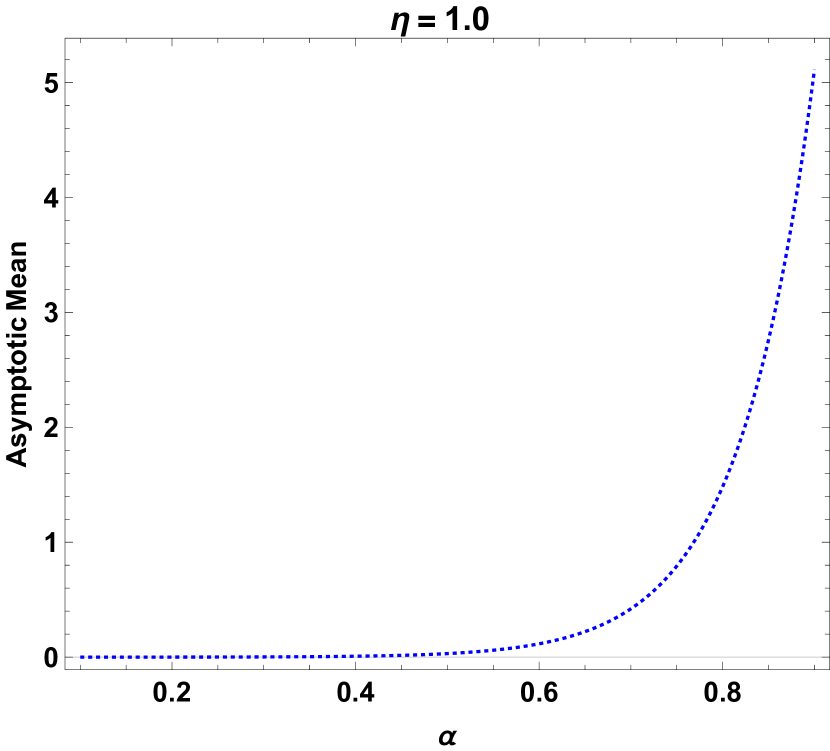

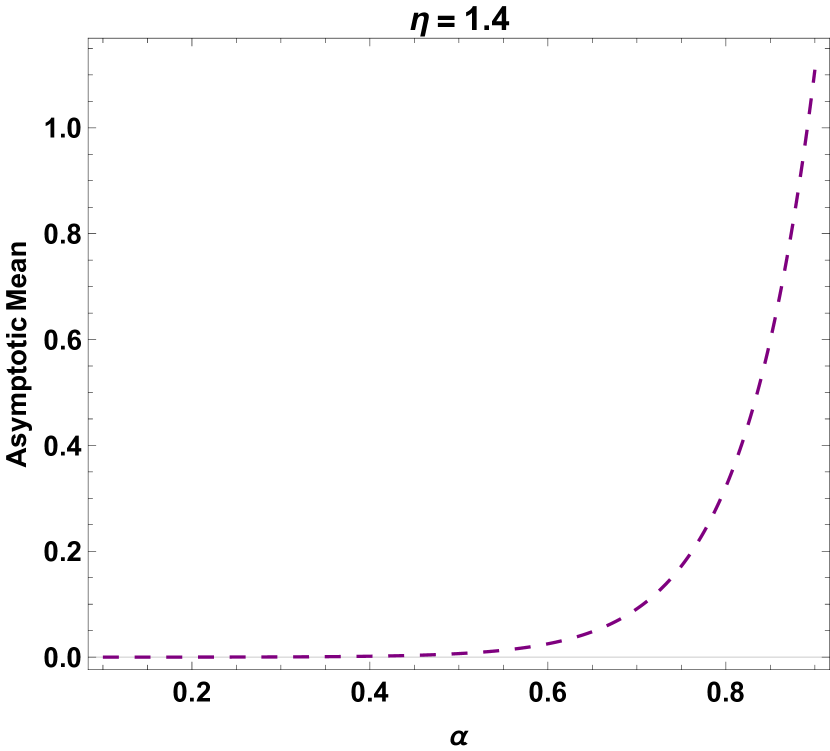

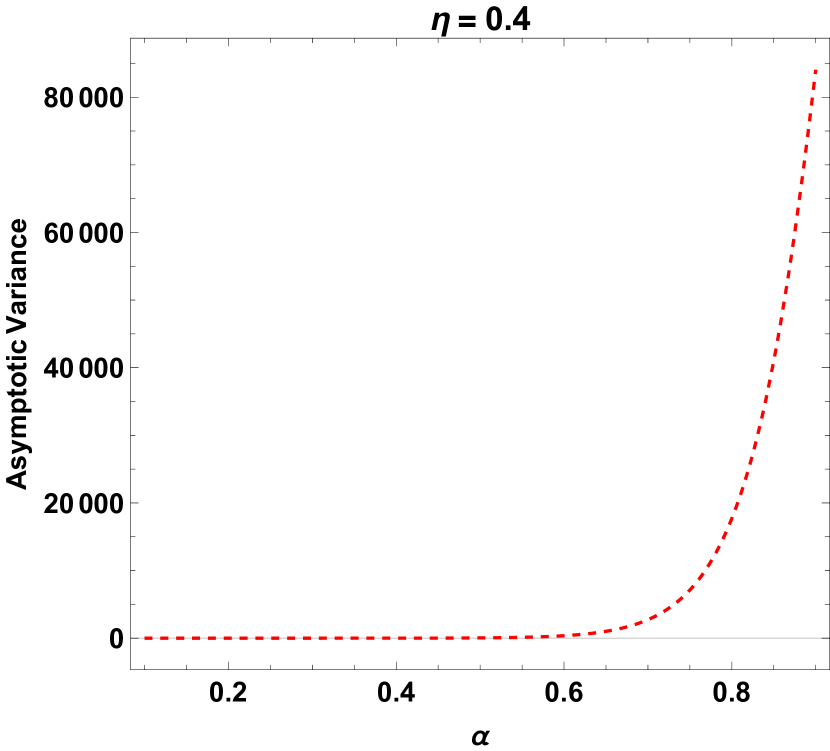

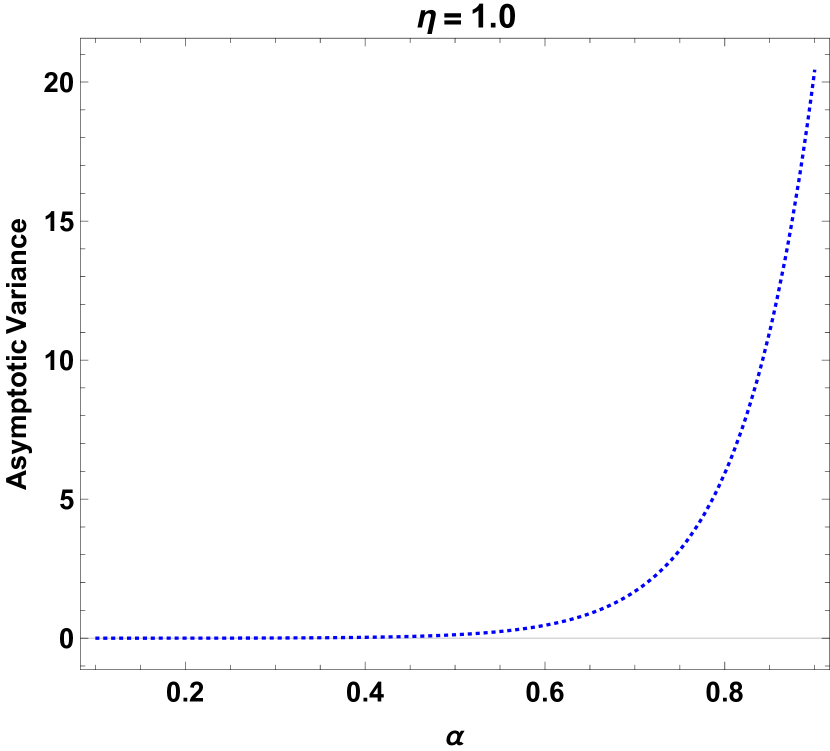

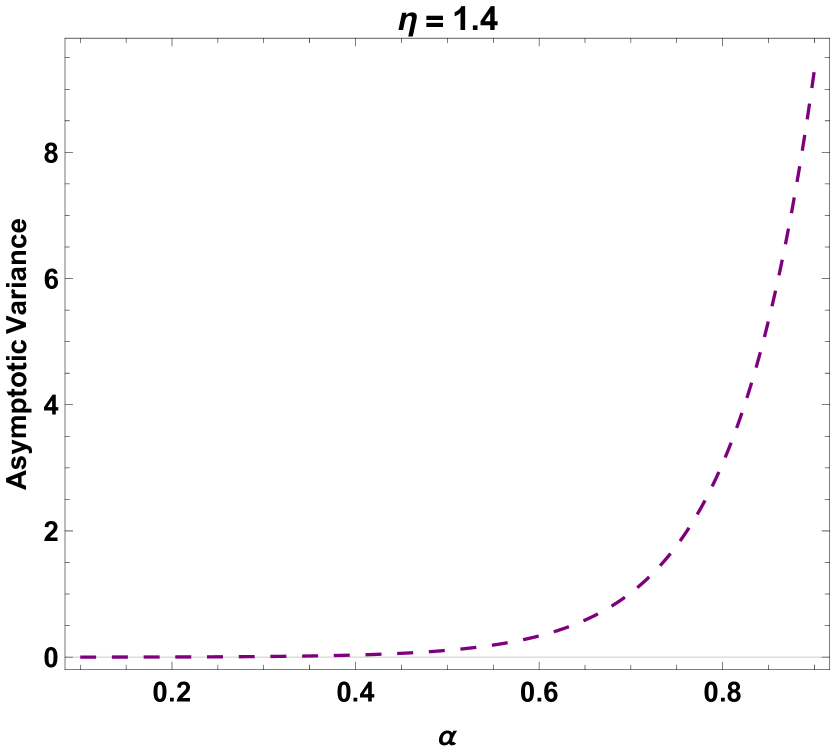

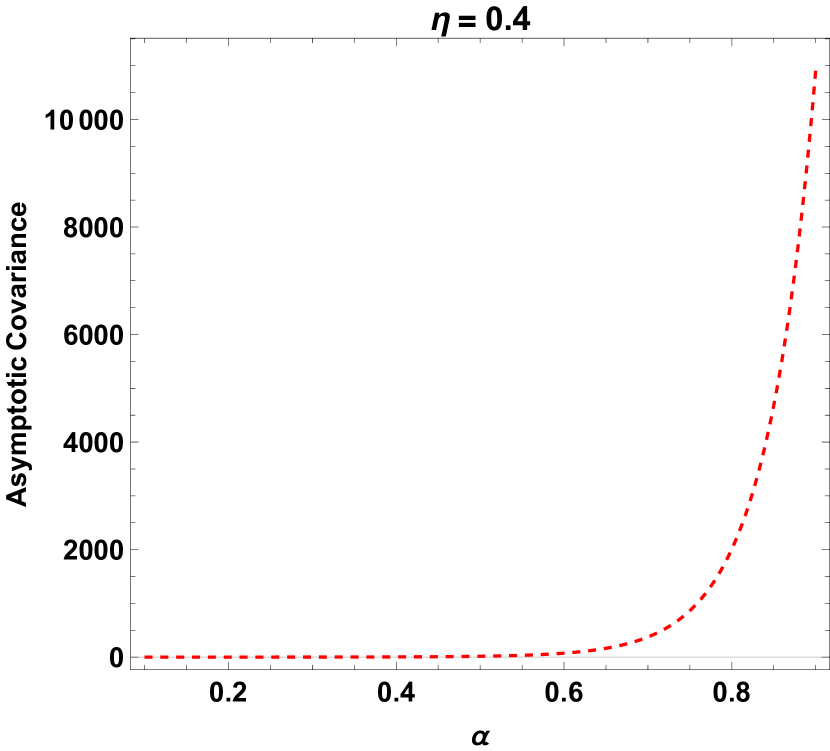

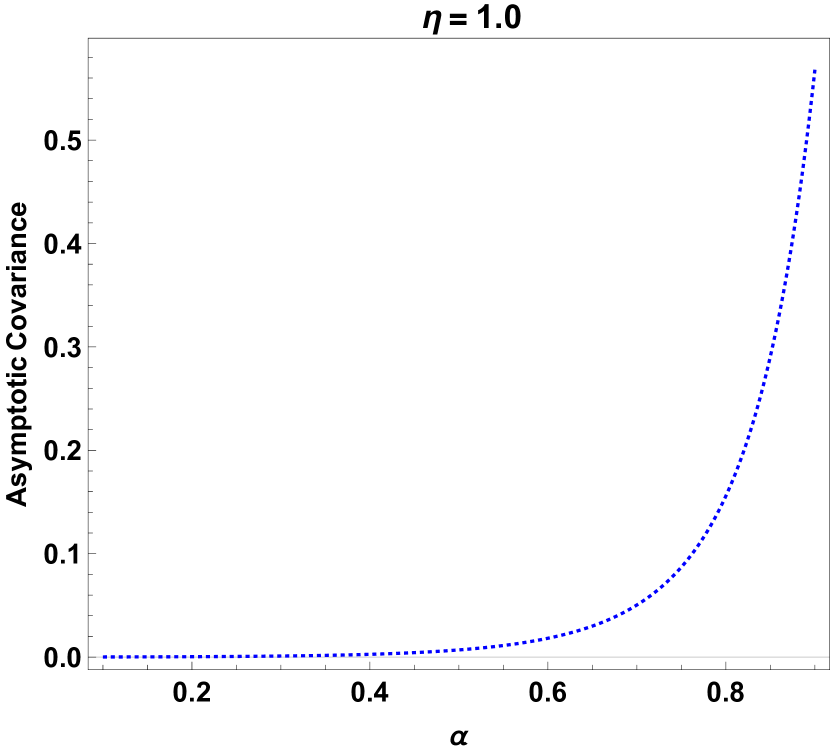

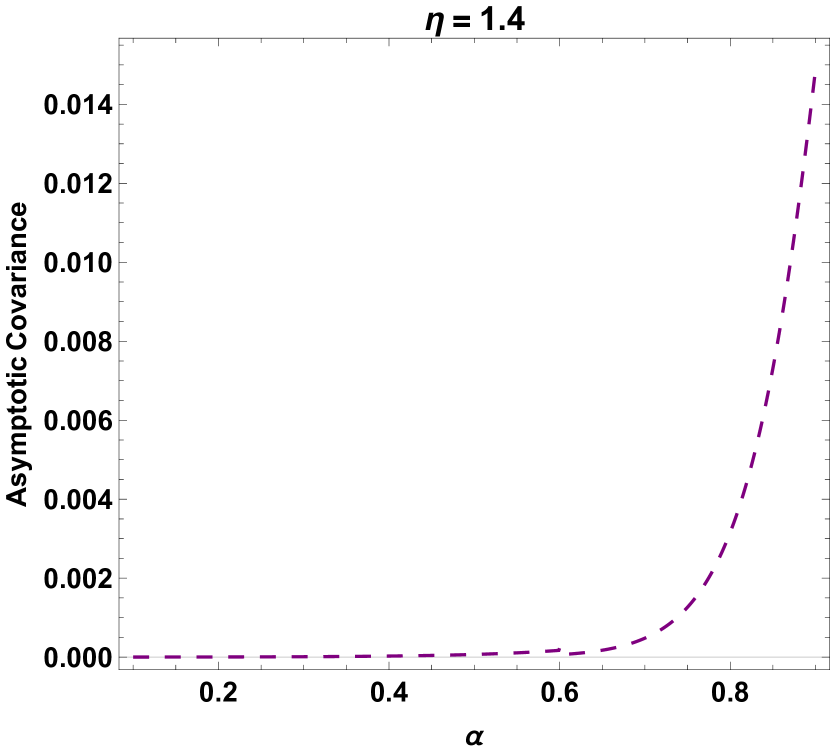

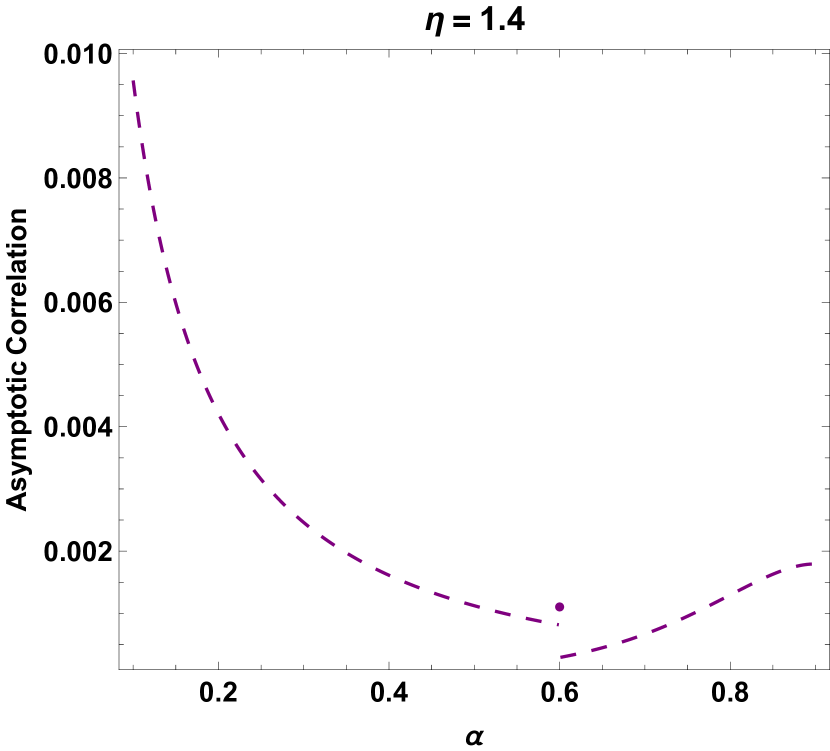

(Impact of fractional Poisson parameter ) In this example, the effect of (where ) on the asymptotics of the IBNR claims is examined. We focus on the case of Pareto delays with (and additionally for covariance and correlation). Moreover, we let and consider three scenarios where . The results are given in Figures 1-4. For each fixed , the asymptotic mean in Figure 1 is increasing in . Intuitively, as increases, the interarrival times of the claims becomes less heavy-tailed (see (4.2)) so that claims arrive more frequently, thereby increasing the IBNR claims. It is also noted that the asymptotic mean is continuous in , as evident from each of the three pieces in (4.32). The asymptotic variance in Figure 2 and the asymptotic covariance in Figure 3 show similar trend at a first glance. However, we remark that for the case (which corresponds to the first subfigure of Figure 2) there is indeed a discontinuity at , which can hardly be seen due to the scale of the plot. Such a curve is plotted using the first three pieces of (4.35). In contrast, the second and third subfigures of Figure 2 for the cases and are continuous in and are plotted using the fourth and fifth pieces of (4.35). Similarly, the first two subfigures of Figure 3 concerning the covariance are continuous in and are both plotted using the first piece of (4.45), but the third subfigure is discontinuous at and is plotted using all three pieces of (4.45). The aforementioned discontinuities explain those observed in the first and third subfigures of Figure 4.

Example 4

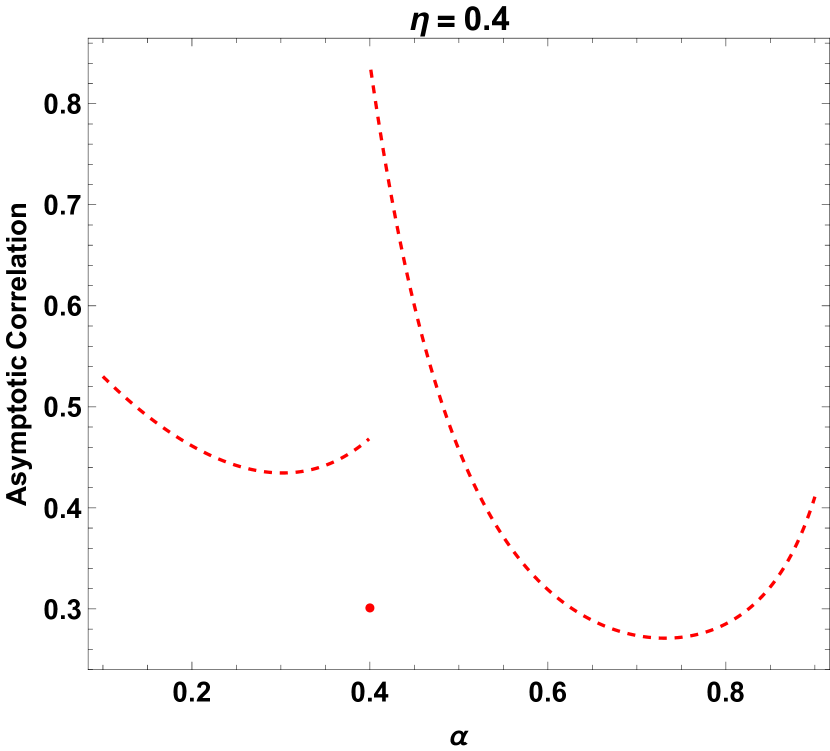

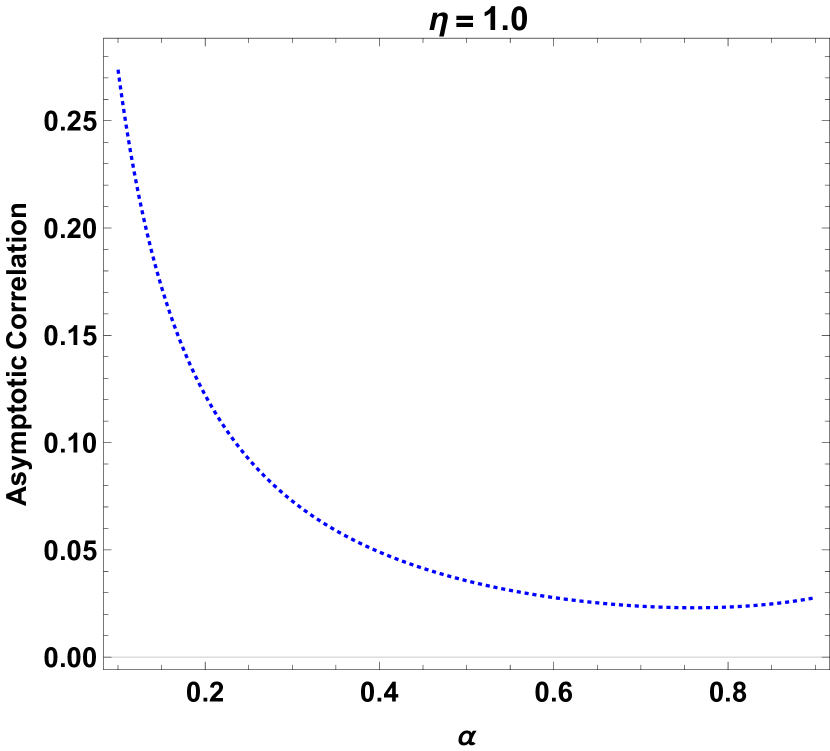

(Change of correlation over time ) In this example, we fix the initial time , we examine how the asymtotic correlation between and changes when increases from to . The results for are plotted in Figure 5 for both and delays. The correlation always decreases in because an IBNR claim at time is more likely to be reported by time as increases. For exponential delays (where the IBNR process is always SRD), the correlation increases as the fractional Poisson parameter increases. This can be explained by (2.11) where the correlation is always asymptotically proportional to which is increasing in . Note that the proportionality constant also depends on , but one expects that the effect of a change in on dominates for large . On the other hand, the correlation under Pareto delays decreases in when increases from 0.3 through 0.5 to 0.8 in this example. However, one should note from Example 3 that in general the asymptotic correlation is not necessarily monotone in (see Figure 4).

Example 5

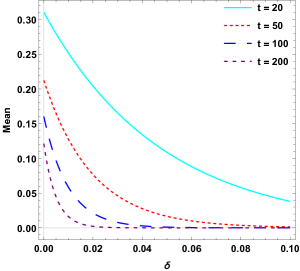

(Impact of force of interest ) This final example briefly illustrates the effect of on the exact values of mean and variance of the IBNR claims for exponential delays with parameter . We let and consider four time values in Figure 6. It can be seen that both and quickly approaches zero as increases due to heavier discounting. Such an effect is more pronounced for a larger value of , which is expected because of the presence of and in the asymptotic formulas for the mean and variance respectively (see (LABEL:tableau_recap1)).

Acknowledgements

The authors would like to thank the anonymous reviewers for helpful comments and suggestions which greatly improved an earlier version of the paper as well as Dr. Olde Daalhuis for insightful discussions concerning Part 1 of the supplementary materials in relation to the proof of Proposition 3. Landy Rabehasaina and Jae-Kyung Woo gratefully acknowledge the support from the Joint Research Scheme France/Hong Kong Procore Hubert Curien grant No 35296 and F-HKU710/15T and the UNSW Business School 2018 International Research Collaboration Travel Funds.

References

- [1] Abramowitz, M. and Stegun, I.A., eds. 1972. Handbook of Mathematical Functions with Formulas, Graphs, and Mathematical Tables. Applied Mathematics Series 55, Dover Publications.

- [2] Badescu, A.L., Lin, X.S., and Tang, D. 2016a. A marked Cox model for the number of IBNR claims: Theory. Insurance: Mathematics and Economics 69: 29-37.

- [3] Badescu, A.L., Lin, X.S., and Tang, D. 2016b. A marked Cox model for the number of IBNR claims: Estimation and application. Preprint available at SSRN at https://papers.ssrn.com/sol3/papers.cfm?abstractid=2747223.

- [4] Benson, D.A., Schumer, R. and Meerschaert, M.M. 2007. Recurrence of extreme events with power-law interarrival times. Geophysical Research Letters 34(16): L16404.

- [5] Biard, R. and Saussereau, B. 2014. Fractional Poisson process: Long-range dependence and applications in ruin theory. Journal of Applied Probability 51: 727-740. (Correction available in 2016 Journal of Applied Probability 53: 1271-1272.)

- [6] Blanchet, J. and Lam, H. 2013. A heavy traffic approach to modeling large life insurance portfolios. Insurance: Mathematics and Economics 53: 237-251.

- [7] Blom, J. and Mandjes, M. 2013. A large-deviations analysis of Markov-modulated infinite-server queues. Operations Research Letters 41: 220-225.

- [8] Blom, J., De Turck, K. and Mandjes, M. 2017. Refined large deviations asymptotics for Markov-modulated infinite-server systems. European Journal of Operational Research 259: 1036-1044.

- [9] Blom, J., Kella, O. Mandjes, M. and Thorsdottir, H. 2014. Markov-modulated infinite-server queues with general service times. Queueing Systems 76: 403-424.

- [10] Brown, M. and Ross, S.M. 1969. Some results for infinite server queues. Journal of Applied Probability 6: 604-611.

- [11] Cahoy, D.O., Uchaikin, V.V. and Woyczynski, W.A. 2010. Parameter estimation for fractional Poisson processes. Journal of Statistical Planning and Inference 140: 3106-3120.

- [12] Dickson, D.C.M. and Hipp, C. 2001. On the time to ruin for Erlang(2) risk processes. Insurance: Mathematics and Economics 29: 333-344.

- [13] Finkelstein, M. and Cha, J.H. 2013. Stochastic Modeling for Reliability, Springer series in reliability engineering. London: Springer-Verlag.

- [14] Jansen, H.M., Mandjes, M.R.H., De Turck, K. and Wittevrongel, S. 2016. A large deviations principle for infinite-server queues in a random environment. Queueing Systems 82: 199-235.

- [15] Karlsson, J.E. 1974. A stochastic model for time lag in reporting of claims. Journal of Applied Probability 11: 382-387.

- [16] Keilson, J. and Seidmann, A. 1988. with batch arrivals. Operations Research Letters 7: 219-222.

- [17] Keilson, J. and Servi, L.D. 1994. Networks of non-homogeneous systems. Journal of Applied Probability 31A: 157-168.

- [18] Kummer, E.E. 1837. De integralibus quibusdam definitis et seriebus infinitis. Journal für die reine und angewandte Mathematik (in Latin) 17: 228-242.

- [19] Landriault, L., Willmot, G.E. and Xu, D. 2017. Analysis of IBNR claims in renewal insurance models. Scandinavian Actuarial Journal 7: 628-650.

- [20] Laskin, N. 2003. Fractional Poisson process. Communications in Nonlinear Science and Numerical Simulation 8: 201-213.

- [21] Leonenko, N.N., Meerschaert, M.M., Schilling, R.L. and Sikorskii, A. 2014. Correlation structure of time-changed Lévy processes. Communications in Applied and Industrial Mathematics 6, e-483.

- [22] Léveillé, G. and Adékambi, F. 2010. Covariance of discounted compound renewal sums with a stochastic interest rate. Scandinavian Actuarial Journal 1: 1-20.

- [23] Léveillé, G. and Adékambi, F. 2012. Joint moments of discounted compound renewal sums. Scandinavian Actuarial Journal 1: 40-55.

- [24] Léveillé, G. and Hamel, E. 2013. A compound renewal model for medical malpractice insurance. European Actuarial Journal 3: 471-490.

- [25] Liu, L., Kashyap, B.R.K. and Templeton, J.G.C. 1990. On the system. Journal of Applied Probability 27: 671-683.

- [26] Maheshwari, A. and Vellaisamy, P. 2016. On the long-range dependence of fractional Poisson and negative binomial processes. Journal of Applied Probability 53: 989-1000.

- [27] Mainardi, F., Gorenflo, R. and Scalas, E. 2004. A fractional generalization of the Poisson Processes. Vietnam Journal of Mathematics 32: 53-64.

- [28] Meerschaert, M.M., Nane, E. and Vellaisamy, P. 2011. The fractional Poisson process and the inverse stable subordinator. Electronic Journal of Probability 16: 1600-1620.

- [29] Mikosch, T. 2009. Non-Life Insurance Mathematics: An Introduction with the Poisson Process. 2nd ed. Springer.

- [30] Moiseev, A. and Nazarov, A. 2016. Queueing network MAP - with high-rate arrivals. European Journal of Operational Research 254: 161-168.

- [31] Olver, F.W.J., Olde Daalhuis, A.B., Lozier, D.W., Schneider, B.I., Boisvert, R.F., Clark, C.W., Miller, B.R. and Saunders, B.V. (Editors.) 2016. NIST Digital Library of Mathematical Functions. http://dlmf.nist.gov/, Release 1.0.14 of 2016-12-21.

- [32] Orsingher, O. and Polito, F. 2011. On a fractional linear birth-death process. Bernoulli 17: 114-137.

- [33] Pang, G. and Whitt, W. 2012. Infinite-server queues with batch arrivals and dependent service times. Probability in the Engineering and Informational Sciences 26: 197-220.

- [34] Repin, O.N. and Saichev, A.I. 2000. Fractional Poisson law. Radiophysics and Quantum Electronics 43: 738-741.

- [35] Resnick, S. and Rootzen, H. 2000. Self-similar communication models and very heavy tails. Annals of Applied Probability 10: 753-778.

- [36] Ridder, A. 2009. Importance sampling algorithms for first passage time probabilities in the infinite server queue. European Journal of Operational Research 199: 176-186.

- [37] Ross, S. 2014. Introduction to Probability Models, 11th ed. Academic Press.

- [38] Shaked M. and Shanthikumar G. 2007. Stochastic Orders, Springer series in statistics.

- [39] Woo, J.-K. 2016. On multivariate discounted compound renewal sums with time-dependent claims in the presence of reporting/payment delays. Insurance: Mathematics and Economics 70: 354-363.

- [40] Willmot, G.E. 1990. A queueing theoretic approach to the analysis of the claims payment process. Transactions of Society of Actuaries 42: 447-497.

Appendix A

A.1 Proof of Theorem 1

We begin by utilizing (3.3) to expand (for and ) into a binomial sum as

Conditioning on , its expectation is given by

| (A.1) |

For convenience, for we define and , where

Further define the convolution operator as for where and have positive domain. Via multiplication of (A.1) by , one obtains

for , which is a renewal equation satisfied by . Therefore, its solution is given by

| (A.2) |

where the last line follows from the representation of the renewal function. Dividing both sides by yields the desired result (3.4).

A.2 Proof of Theorem 2

First, from (3.3) with the application of binomial expansion it follows that, for and ,

Taking expectations on the both sides of above equation via conditioning on results in

| (A.3) |

where the notation of D-H operator has been used.

Similar to the arguments used in the proof of Theorem 1, we proceed by defining and for and fixed . Replacing by in (A.2) and multiplying both sides by , we arrive at the renewal equation

| (A.4) |

for , where with

Analogous to (A.2), the solution of (A.4) is

which is identical to (2) upon dividing by and then replacing with .

A.3 Proof of Proposition 4

1. Proving the exact formula (4). We start by proving (4). First, plugging (4.12), and (4.1) into the first term on the right-hand side of (1) yields

| (A.5) |

Again, with the application of (4.7) followed by changing a variable to , we find that the integral in (A.3) can be expressed as

| (A.6) |

where and are given by (4.18) and (4.25) respectively. Similarly, the third term of (1) can be represented as

| (A.7) |

where the last equality is due to (3). Lastly, using (3.1) and the fact that , we observe that the second term in (1) is simply

| (A.8) |

which corresponds to the second term on the right-hand side of (4) thanks to (4.12). It is also clear that the last terms in (1) and (4) are identical again because of (4.12). Therefore, combining this with (A.3)-(A.3) yields (4).

2. Proving the asymptotic formula (4.26). We now proceed to prove the asymptotic result (4.26). From (A.3) and (A.8), it is noted that the third and the second terms of (1) are and respectively. In what follows, it will be shown that these two terms are asymptotically dominated by the first and the last terms of (1). Using (3.1), (4.15) and , the sum of the first and the last terms of (1) can be expressed as

| (A.9) |

In view of the integrand above, one needs to first study the asymptotics of as for all (where is fixed). By applying (4.16), we rewrite as, for ,

| (A.10) |

where

| (A.11) | ||||

| (A.12) |

will be analyzed separately.

Term . Performing the change of variable to the term in (A.11) yields

| (A.13) |

with the obvious definitions of and . We first look at . Note that is decreasing in . Therefore, for large enough such that , one has that, for ,

| (A.14) |

which is integrable with respect to on . For all , and tend to and respectively as . Then, by dominated convergence we arrive at

| (A.15) |

As for , changing variable leads to

which can be upper bounded as

| (A.16) |

which tends to as . Combining with (A.3), we conclude that the limit of (A.13) is given by

| (A.17) |

Note that the inequality (A.3) implies the uniform upper bound where for all and . Moreover, because is bounded on , (A.16) also means that for all and where is some constant. As a result, we arrive at the upper bound

| (A.18) |

where .

Term . Concerning in (A.12), we first consider, by a change of variable ,

| (A.19) |

where and have obvious definitions. Note that can be rewritten as

| (A.20) |

Applying similar arguments used for analyzing and gives rise to

by dominated convergence, and

| (A.21) |

which tends to as . Consequently, (A.19) converges to as , and then one uses (A.20) to evaluate

| (A.22) |

In addition, for all and , one may check that where while (A.21) implies that for some constant . Coupled with the fact that for and large enough (say ) where is some constant, we can upper bound (A.20) as

| (A.23) |

where .

The result. Plugging (A.17) and (A.22) into (A.10) yields the asymptotic equivalent, for all ,

| (A.24) |

We shall now establish an equivalent for the integral term in (A.3) and consider

| (A.25) |

Utilizing the definition (A.10) together with the bounds (A.18) and (A.23), it is clear that

Taking limit as on both sides of (A.25) along with the use of dominated convergence and (A.24), it is easy to see that

| (A.26) |

It now remains to conclude how the asymptotic formula (4.26) is obtained. Recall that the second and the third terms of (1) are respectively and . These are negligible compared to the sum of the first and the last terms, namely (A.3), which is because of (A.26). Applying (A.3) and (A.26) again yields the result (4.26).

A.4 Proof of auxiliary results for Proposition 6

1. Proving (4.42) when . To begin, we shall show that with given by (4.40) is uniformly convergent. It is first observed that

| (A.27) |

Utilizing the identity (4.6) which requires (i.e. as assumed), one can write

Then, via application of (4.3) and (4.6) (requiring , i.e. which is satisfied), we can sum ’s as

| (A.28) |

Hence, uniform convergence is proved. Then, further using the definitions of and in (4.40) and (A.27), we can now evaluate the limit on the right-hand side of (4.41) as

| (A.29) |

from which (4.42) follows. Note that is continuous at when (i.e. in our case), and (A.4) has been applied.

2. Proving (4.44) when . Via a change of variable with in (4.43), i.e. , so that implies , and , we obtain

| (A.30) |

Based on the fact that as , we shall establish the limit of as . It is first noted that for all , increases towards as . In order to determine the limit of , we shall use the asymptotic result of as in Lemma 1. In what follows, we focus on the case as the argument will be similar when . We shall need the following lemma.

Lemma 3

Given . For every one has the limiting result

which is a convergent integral for and .

Proof: We distinguish two cases according to the sign of .

Case 1. : Because increases towards as , the result follows by monotone convergence.

Case 2. : For all and , it is clear that

Since is finite, application of the dominated convergence theorem yields the result.

From (4.29), one has that there exists such that

This implies that we can first fix a , and then there exists large enough such that

| (A.31) |

For example, one may pick such that , i.e. .

Next, due to (A.30), we turn our attention the asymptotic behaviour of

| (A.32) |

where and have obvious definitions, and is fixed. Starting with the term , it is noted that is upper bounded by for all and and the integral is finite. Application of the dominated convergence theorem gives rise to

| (A.33) |

As for , using (A.31) one has the upper bound

Thus, it follows from Lemma 3 that

which is equivalent to

| (A.34) |

thanks to (A.32). Let us now observe that, by the triangular inequality,

and therefore, with the help of (A.34) and (A.33) we arrive at

| (A.35) |

While the first integral on the right-hand side is clearly finite, the second integral is also convergent thanks to the estimate (4.29). Since is arbitrary, we can let in the above inequality, ending with the right-hand side converging to . We thus obtain (4.44) for .

Finally, we remark that the procedure to derive (4.44) in the case is similar. The splitting of (A.32) into and can still be adopted but the major difference is that (A.31) needs to be modified using the second case of (4.29). The limit (A.33) is still valid, and one can obtain a similar upper bound to (A.4) which converges to . The details are omitted.

A.5 Proof of Proposition 7

Recall that is fixed such that . As in the proof of Proposition 4 for the case of exponential delays, to analyze the asymptotic behaviour of as we shall look at the terms appearing in the general expression (1). We can write for , where

| (A.36) | ||||

| (A.37) | ||||

| (A.38) |

The following is dedicated to obtaining the asymptotics for , and as .

Term . Substituting the renewal density (4.1) and the Pareto survival function (4.27) into (A.36) followed by some simple manipulations, we arrive at the two sided bounds

By squeezing principle one obtains the asymptotic behaviour

| (A.39) |

Term . Utilizing (3.2), one sees that in (A.38) can be written as

| (A.41) |

In order to derive the asymptotics for as , we proceed by studying the asymptotic behaviour of for all and then apply dominated convergence. Let us first define, for ,

which is decreasing in . By changing variable , we get that

| (A.42) |

where is defined in (4.28) (with the definition extended to allow for as well). Hence, one has thanks to (4.31). Defining

| (A.43) |

for , we can write

and then in (A.41) can be decomposed as where

| (A.44) | ||||

| (A.45) |

The terms and are studied separately as follows.

Term of . We shall first proceed to prove the auxiliary result

| (A.46) |

Note that the limiting behaviour of as depends on the value of . It will be seen that L’Hôpital’s rule can be applied when where the limit on the left-hand side of (A.46) is of the indeterminate form or . This involves differentiating in (A.43) with respect to , yielding

| (A.47) |

where the derivative of in (A.5) is given by

Four cases are considered as follows.

Case 1. : Utilizing (4.29) in Lemma 1, it is not difficult to see that as , and consequently one has the expansion

| (A.48) |

The first term on the right-hand side of (A.47) thus satisfies the asymptotic formula

Since and as , the second term on the right-hand side of (A.47) can again be estimated using (A.5) via

Plugging the above two estimates into (A.47) yields, for all ,

| (A.49) |

This is further split into two cases as follows.

Case 1a. : In view of the expression on the right-hand side of (A.49), it is noted that as , asserting that as . As a result, the left-hand side of (A.46) is in the form , and application of L’Hôpital’s rule yields

| (A.50) |

Case 1b. : Using the finer asymptotic result (4.30), one finds that (A.5) with can be expressed as

for some constant . Further expanding at and , we obtain

| (A.51) |

where the last line follows from the assumption . By noting that (again because of )

replacing by in (A.5) gives rise to

In view of the definition (A.43), taking difference of the above equation with (A.5) results in as , i.e. the left-hand side of (A.46) is in the form . Consequently, the L’Hôpital’s rule can be applied as in (A.50), and further use of (A.49) leads to (A.46).

Case 2. : In this case, it is clear that as . Therefore, it is clear from (A.5) and (A.43) that as , implying that the left-hand side of (A.46) is . Note that (A.5) is now replaced by , and one can check that the arguments leading to (A.49) and (A.46) still hold.

Case 3. : According to (4.29) in Lemma 1, one has as for some constant . With some simple algebra it can be shown that (A.5) is replaced by as where is a constant. Note that the first term is the dominant one, and the procedure leading to (A.49) is still valid. It remains to show that as so that L’Hôpital’s rule in (A.50) can be applied and (A.46) holds true. To see this, we substitute the above estimation of into (A.5) (under ) so that, similar to (A.5),

for some constant . One also has the same equation but with replaced by , and therefore taking difference results in

Case 4. : This final case is different from the previous ones in the sense that in the denominator on the left-hand side of (A.46) equals to one. We shall proceed directly to calculate the limit as follows. First, application of the finer asymptotic result (4.30) to (A.5) with yields, for some constant ,

| (A.52) |

We further expand each term in the square bracket as

Therefore, (A.5) is reduced to

where and are constants. The equation is also valid when is replaced by , and therefore taking difference results in

which is (A.46).

Having proved (A.46) for , we are ready to conclude on . For all and , two observations are made as follows. First, it is clear that . Second, the fact that is decreasing in implies , which is upper bounded as it is continuous and convergent to a finite limit as thanks to (A.46). Using the definition (A.44), we can thus apply the dominated convergence theorem to obtain

| (A.53) |

Term of . Note that defined in (A.45) is identical to zero if , and therefore it is sufficient to focus on the case . For all and , one obtains easily that as . Moreover, one has the inequality which is an upper bounded quantity. The dominated convergence theorem thus yields from (A.45) the equivalent

| (A.54) |

An asymptotic formula of will follow once we find one for . Recall that (A.5) implies as , where is asymptotically equivalent to (resp. ) when (resp. ) according to (4.29) in Lemma 1, and tends to when . Consolidating these results with (A.54), we arrive at the asymptotic behaviour for given by, as ,

| (A.55) |

Asymptotics for . We can now gather the asymptotic results (A.53) and (A.55) to give the asymptotics for as . First, if , then only matters as equals zero. Second, if , then asymptotically dominates . Third, if , then both and asymptotically behave like and therefore . These are all summed up to yield

| (A.56) |

The result. From (A.39) and (A.40), it is clear that and are both asymptotically proportional to as . By comparing with (A.56), one sees that is dominated by when , so that . If , then , and all asymptotically behave like , and one has . Finally, is the dominant term when . All these results are summarized in (4.45).

Supplementary materials

Part 1: Proving the validity of interchanging limit and infinite summation in Equation (4.23) in Proposition 3

In the proof of Proposition 3 , we have determined the constant in Equation (4.23), namely

| (A.57) |

(where is defined in (4.18)) by assuming that the limit and the infinite summation on the left-hand side can be interchanged. Here we shall prove that this is valid. Setting

| (A.58) |

the left-hand side of (A.57) equals . To interchange the order of limit and infinite summation, a sufficient condition is that the series converges uniformly on . According to the Weierstrass M-test, uniform convergence of can be proved by finding a sequence such that

| (A.59) |

and

| (A.60) |

Upper bounding by a well defined is, in view of (A.58), only possible if one is able to provide some fine asymptotics for the Kummer’s function as (see (4.10)). We need some precise information on the term , and in particular it is important to analyze how depends on the parameter since varies with . Refined expansions are only available in the literature for the Tricomi’s functions (to the best of our knowledge) but not for . Hence, we will use those expansions coupled with the identity (see Olver et al. (2006, Equation (13.2.41)))

| (A.61) |

where is the Tricomi’s function (or the confluent hypergeometric function of the second kind). We recall that is a multivalued complex function, and hence the term , multiplied by , changes its argument by and then changes the value of the term .

We first decompose (A.58) into two parts as

| (A.62) |

where

| (A.63) | ||||

| (A.64) |

In the above definitions, is a constant that will be chosen ‘large enough’ later on. In other words, we break down into two terms and according to whether grows slower or faster than towards , and the terms and will be studied separately.

Term . First, we look at the term . Using (4.18) and (4.8), (A.63) can be rewritten as

| (A.65) |

It can be readily checked that (as a function of for ) achieves maximum at . Therefore, one has that Further noting that (A.65) can be upper bounded as

| (A.66) |

which does not depend on . Utilizing the Stirling’s formula

| (A.67) |

one observes that

| (A.68) |

and therefore

Then, we apply the ratio test to check that

and thus

| (A.69) |

Term . Next, applying (A.61) and (4.18) in (A.64), we further decompose as

| (A.70) |

where

| (A.71) |

and

| (A.72) |

To upper bound the above two functions, we can make use of Olver et al. (2006, Chapter 13.7(ii)) regarding bounds on . In particular, we shall put , or , and into their Equation (13.7.4). It is noted that the bounds are of slightly different forms depending on the way tends to infinity. In particular, we will use their result by putting (i.e. is real), which tends to as .

Term of . For the term , applying Olver et al. (2006, Chapter 13.7(ii)) with , and , we have that

| (A.73) |

where

| (A.74) |

We note that the above inequality corresponds to the term that belongs to region in Olver et al. (2006, Chapter 13.7(ii)), and therefore it is valid only when . The intermediate functions , and are given by their Equations (13.7.8) and (13.7.9) as , , and

Recall that is to be chosen ‘large enough’. Here we shall choose for some that we, at this point, impose strictly larger than (so that the constraint in (A.74) is satisfied) to arrive at the inequalities ,

| (A.75) |

and

| (A.76) |

where and are non-negative constants. A crucial point concerning these two constants is that they only depend on (that is to be fixed later on) and are always finite under . Incorporating the inequalities (A.75) and (A.76) into (A.74) leads to

| (A.77) |

where . With (A.73) and (Part 1: Proving the validity of interchanging limit and infinite summation in Equation (4.23) in Proposition 3 ), we obtain the upper bound

| (A.78) |

where .

Next, noting that (as a function of ) is decreasing on , we have

Consequently,

Then, with the help of (A.78), in (A.71) can be upper bounded as, for ,

| (A.79) |

Using (A.68) with , it is noted that

and thus for ,

As a result, application of ratio test gives, for ,

where the second last inequality follows from the fact that (as a function of ) is decreasing on . Hence,

| (A.80) |

Term of . Lastly, we consider the term in (A.72). Applying again Olver et al. (2006, Chapter 13.7(ii)) with , and implies

| (A.81) |

The term in the above Tricomi’s function this time tends to regardless of whether one chooses to multiply by or . Even though the value of is different depending on whether we choose the argument or , the upcoming bounds (Part 1: Proving the validity of interchanging limit and infinite summation in Equation (4.23) in Proposition 3 ) and (A.84) are the same as they only involve the modulus of . Hence, we choose to keep the notation for presentation purpose. Thus, the error term in (A.81) satisfies the inequality

| (A.82) |

for . Note that, contrary to (A.74), the above inequality corresponds this time to which belongs to region in Olver et al. (2006, Chapter 13.7(ii)), and hence it is valid for . The functions , and are given by their Equations (13.7.8) and (13.7.9) as ,

and

where and are non-negative constants. By substituting the above results into (A.82), we arrive at

| (A.83) |

where . Using (Part 1: Proving the validity of interchanging limit and infinite summation in Equation (4.23) in Proposition 3 ), an upper bound for (A.81) is given by

| (A.84) |

where .

Now, we can get from (A.72) and (A.84) the upper bound, for ,

| (A.85) |

Utilizing the Stirling’s formula (A.67) and the equivalent for Gamma function (see Abramowitz and Stegun (1972, Equation (6.1.37), p.257), namely

we obtain the asymptotic relationship

Thus, for ,

Consequently, the ratio test verifies that, for ,

and hence,

| (A.86) |

Verifying (A.59) and (A.60). Combining (A.62), (A.70), (Part 1: Proving the validity of interchanging limit and infinite summation in Equation (4.23) in Proposition 3 ), (Part 1: Proving the validity of interchanging limit and infinite summation in Equation (4.23) in Proposition 3 ) and (Part 1: Proving the validity of interchanging limit and infinite summation in Equation (4.23) in Proposition 3 ), it is clear that by choosing in (A.63) and (A.64), we have

i.e. the upper bound (A.59) is obtained by defining the sequence via . Then, the condition (A.60) is satisfied thanks to (A.69), (A.80) and (A.86).

Part 2: Proof of Lemma 1

First, we split defined in (4.28) into two parts as

| (A.87) |

where the first integral is always finite. Therefore, we focus on the divergent second integral and distinguish between the cases and for ease of presentation.

Case 1. : Performing integration by parts, one obtains

| (A.88) |

The analysis is further separated into three cases as follows.

Case 1a. : In this case, and therefore the integral is convergent as is bounded on . Incorporating such an observation into (A.88), it is clear that

| (A.89) |

for some constant . Further expanding , we obtain

| (A.90) | ||||

| (A.91) |

where the last line is due to . Combining (A.87), (A.89) and (A.91) yields the first asymptotic result in (4.30).

Case 1b. : Equation (A.88) is still valid, but the integral on the right-hand side can easily shown to be divergent at . Integration by parts gives

| (A.92) |

where the integral converges as because is finite. Incorporating (A.88) and (A.92) into (A.87) and utilizing the expansion at and , one finds (for some constant )

which simplifies to the second asymptotic formula in (4.30) because .

Case 1c. : The integral on the right-hand side of (A.88) satisfies

By applying the expansion (A.90) (which is also valid for ) and the above result to (A.88), one proves the first result in (4.29) when .

It is instructive to note that the proven result (4.30) also asserts that the first asymptotic formula in (4.29) is also valid when .

Part 3: Proof of Lemma 2

Performing a change of variable (i.e. ) in (4.33) yields

| (A.93) |

To analyze the asymptotic behaviour of as (so that ), we shall study the integral, for small ,

| (A.94) |

where

| (A.95) |

It is clear that converges to as by dominated convergence (as is bounded on and and is finite). For , a change of variable (i.e. with ) results in

| (A.96) |

We need to consider two cases as follows.

Case 1. : We rewrite (A.96) as

| (A.97) |

where . It can be seen that is bounded by some constant for all and a small enough . Besides, one has that is finite. Hence, by the dominated convergence theorem we obtain

Consequently, (A.97) (or (A.96)) behaves asymptotically as

| (A.98) |

Case 2. : By the change of variable (i.e. with ), (A.96) becomes

| (A.99) |

For and small enough (less than ), it is observed that both and are upper bounded by some constant. Therefore, one checks easily that

Hence, by the dominated convergence theorem together with the fact that as , one finds that the asymptotic behaviour of (A.99) (or (A.96) with ) is given by

| (A.100) |