Numerical inverse Laplace transform for convection-diffusion equations

Abstract

In this paper a novel contour integral method is proposed for linear convection-diffusion equations. The method is based on the inversion of the Laplace transform and makes use of a contour given by an elliptic arc joined symmetrically to two half-lines. The trapezoidal rule is the chosen integration method for the numerical inversion of the Laplace transform, due to its well-known fast convergence properties when applied to analytic functions. Error estimates are provided as well as careful indications about the choice of several involved parameters. The method selects the elliptic arc in the integration contour by an algorithmic strategy based on the computation of pseudospectral level sets of the discretized differential operator. In this sense the method is general and can be applied to any linear convection-diffusion equation without knowing any a priori information about its pseudospectral geometry. Numerical experiments performed on the Black–Scholes () and Heston () equations show that the method is competitive with other contour integral methods available in the literature.

Keywords: Contour integral methods, pseudospectra, Laplace transform, numerical inversion of Laplace transform, trapezoidal rule, quadrature for analytic functions.

AMS subject classifications: 65L05, 65R10, 65J10,65M20, 91-08

1 Introduction

We consider the time discretization of Initial Value Problems for linear systems of ODEs:

| (1) |

for , a discrete version of an elliptic operator and a source term including possibly boundary contributions. The solution will thus be a time-dependent vector, of dimension equal to the number of degrees of freedom in the spatial semi-discretization of the reference problem. We are particularly interested in equations arising in mathematical finance, such as Black–Scholes, Heston or Heston-Hull-White equations [2, 5, 6].

Classical methods to approximate the solution to (1) include Runge-Kutta and multistep integrators. Also splitting schemes, like ADI methods have been proposed to solve the continuous reference problem, see for example [7, 8, 9, 10] for Heston equation. All these methods are of time-stepping type and thus, in order to approximate the solution at a certain time , approximations at certain smaller times must be previously computed. For large times or high accuracy requirements this procedure can be extremely demanding in terms of time and computational cost. An alternative to time-stepping methods to compute the solution at (few) given times, large or not, can be derived based on the Laplace transform and its numerical inversion. This approach has been successfully developed in [4, 13, 14, 16] for linear evolutionary problems governed by a sectorial operator, this is, assuming that in (1) has bounded resolvent outside a certain acute sector in the left-half of the complex plane. The magnitude of the resolvent norm deeply impacts on the rate of convergence of the method. For this reason, the integration contour must be chosen accordingly to the pseudospectral geometry of . In particular, if is non normal the pseudospectral geometry of can be difficult to estimate [18]. The spatial discretization of a convection-diffusion operator typically leads to a non normal matrix [11, 20]. In the present paper we propose a novel contour integral method for (1), which includes a preliminary study of the pseudospectral level curves of .

In the present paper we assume that the Laplace transform of the source term exists, is available, and admits a bounded analytic extension to a big region of the complex plane outside the spectrum of . The case of more general sources is out of the scope of the present manuscript but has been considered in the literature [16]. Under these hypotheses, we can apply the (unilateral) Laplace transform to both the sides of the system in (1), which leads to the following algebraic equation for :

| (2) |

where and stands for the identity matrix. The inversion formula for the Laplace transform provides the following representation of the unknown function :

| (3) |

where is a deformation of a Bromwich contour, which can be taken as an open regular curve running from to and such that all singularities of are to its left. Thus, must leave to its left the eigenvalues of and all possible singularities of . The discretization of (3) by some quadrature rule will provide an approximation of , for a given . Assuming that the Laplace transform can be analytically extended to the left half of the complex plane and that this extension is properly bounded with respect to , several authors have proposed different contour profiles and parametrizations for . Probably the first relevant related reference is [17], where the author analyzes a cotangent mapping with horizontal asymptotes and the classical trapezoidal rule for the inversion of scalar Laplace transforms. Much more recently, the cotangent contour have been investigated and improved [3]. Alternatively hyperbolic contours have been considered in [4, 13, 14, 16], with a focus on evolutionary problems governed by sectorial operators. In [20] a parabolic profile for is chosen. In all these references, the resulting scheme converges with spectral accuracy with different rates of convergence according to the particular application and the range of times at which the inverse Laplace transform is required. An application of the parabolic contour is studied in [11] to solve precisely Black–Scholes and Heston equations. These methods require in practice some a priori knowledge of the pseudospectral geometry of . In particular, in [11, 20] a critical parabola bounding the resolvent norm of the (continuous) differential operator under consideration is used. This information is available only for few operators. For more complicated equations, such as Heston’s equation, the critical parabola is only guessed. Also in [14] a preliminary information about the pseudospectral behaviour is needed in order to efficiently set the sector of the complex plane outside which the resolvent norm is analytic and bounded by some suitable constant. In the present work we present a method that combines a preliminary numerical investigation of the pseudospectral level sets of with the efficient inversion of the Laplace transform. This feature makes the applicability of our method much wider.

Our error analysis will show that in (3) can be replaced by a finite open arc of an ellipse. In [15] the behaviour of the resolvent norm of some simple convection-diffusion operator is studied and it is shown that there exists a parabola containing the portion of the complex plane where this norm grows unboundedly, being this the starting point in [11, 20]. But if a spatial semi-discretization is applied, the differential operator is approximated by a matrix , which has a finite spectrum and closed curves surrounding the eigenvalues as pseudospectral level curves, see [15, Figures 5, 6]. Moreover, since the exponential factor in (3) drags down the norm of the integrand function as moves to the left, we are interested in observing the pseudospectral behaviour of only in a vertical strip of the complex plane. For these reasons we found that an open arc of an ellipse is a good candidate to efficiently bound the resolvent norm of in a region of interest. Moreover, the choice of an elliptic profile has never been investigated in the literature, and its performance turns out to be competitive w.r.t. other methods. Our final selection of the integration profile relies both on the computation of some pseudospectral level curves associated to and on the optimization of the error bounds which we derive for our quadrature. Our method is strongly based on the theoretical error estimate of the trapezoidal rule when applied to exponentially decaying analytic integrands [1, 12, 19].

Apart from being able to deal with more general problems than those considered in [11, 14, 20], our new method enjoys the following important advantages:

-

•

it is able to approximate the solution of (1) uniformly for belonging to large time windows.

-

•

round-off errors are controlled in a robust and systematic way.

-

•

it is highly parallellizable.

-

•

it provides an approximation of the solution to (1) at a desired time (or time window) without computing any history.

-

•

its performance is not affected by the lack of regularity (in space) of the initial data in (1).

-

•

it provides an approximation within a prescribed target accuracy by dynamically increasing the number of quadrature points on the integration contour, without changing the integration profile and taking advantage of previous computations.

The article is organized as follows. In Section 2 we review the error estimate for the trapezoidal rule when applied to exponentially decaying integrands. In Section 3 our new method is fully described and analyzed. In Section 4 we provide details about the practical implementation and the computational cost. In Section 5, after a first illustrative application of the method to a canonical convection-diffusion equation, we test the method on Black-Scholes and Heston equations. We compare our new method with the methods in [11] and [14] in Section 6. Finally, in Section 7 we extend our algorithm to approximate the solution for in a time window by using a unique integration contour.

The new integration contour

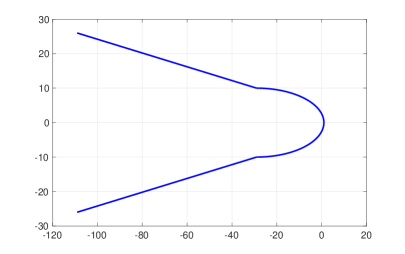

We propose a contour in (3) which is the union of two half-lines connected with an open arc of an ellipse as shown in Figure 1.

In particular is defined as , with

| (4) |

where, for constant parameters to be determined,

parameterizes the elliptic arc and

parameterize the half-lines.

We recall that the constants in the parametrization must be chosen so that the resulting contour leaves to its left the spectrum of and the singularities of . There is quite some freedom in the choice of the two half-lines, as along as their real part goes to minus infinity as . Actually, the contribution of the half-lines to the contour integral is expected to be small and will be neglected in practice, as we explain in Subsection 3.3.

2 Preliminaries about the trapezoidal rule

We will apply the classical trapezoidal rule to approximate (3), after parametrization by (4). The resulting integral will be of the form

| (5) |

with satisfying the properties listed in Assumption 1.

Assumption 1.

The complex extension of the integrand function in (5) satisfies the following properties:

For some

-

1.

() is analytic and bounded inside the strip ;

-

2.

inside the strip ;

-

3.

() and such that one has that

-

4.

For the same of the previous point, such that

-

5.

such that , one has , for a certain .

Under these hypotheses it is possible to prove the following Theorem

Theorem 1.

Proof.

The proof is a variant of the one in [1, Appendix].

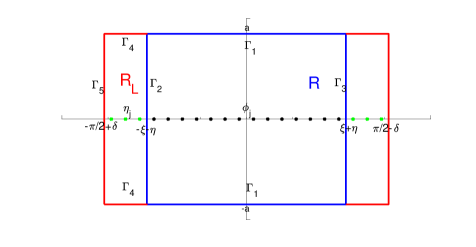

We consider the rectangle and call the union of its horizontal sides, and its vertical left and right sides, respectively (see Figure 2).

Consider the integral

We have

| (8) |

On the one hand, for ,

it follows

On the other hand, define

One has

The function

satisfies by the residue Theorem

Observe that

Let us consider

We estimate

| (9) |

We estimate the integrals over . Take the rectangle and call its left vertical side and the union of its horizontal sides. We define as in the statement of the Theorem, so that is the largest segment with length an even multiple of . We have that

with , . In other words is the error of the same trapezoidal quadrature rule applied on the integral on the interval with the same spacing . In this way, we get

On the one hand, we estimate (with )

| (10) |

On the other hand, we estimate

and

so that

| (11) |

We finally obtain

| (12) |

3 A new method

The only portion of the integration contour as defined in (4) that we will use in practice is the half ellipse. As already done in [13, 14, 11], this elliptical profile is selected through the construction of a suitable conformal mapping . In particular we want it to map horizontal segments onto ellipses in the complex plane (we will use the right half of these ellipses). Thus we set

| (13) |

We ask (13) to be holomorphic and impose the Cauchy-Riemann equations, getting that has to be constant and

| (14) | |||

where are constants. The resulting mapping turns out to be entire, since the partial derivatives of both the real and the imaginary parts are everywhere continuous. It is thus invertible and the complex derivative cannot be zero.

The core idea of using the mapping (13) is to let vary in the segment , for a suitable , while the integrand function

| (15) |

stays bounded for every , , . In particular, we will use the mapping (13) to efficiently bound the exponential term and the norm of the resolvent . We are doing this by constructing two external half ellipses delimiting the part of the complex plane where the integrand is bounded. The mapping (13) is asked to map the segments onto this two curves. Then, we will use as integration profile the one corresponding to the image of the real segment . In formulas, the actual profile of integration that we use is parameterized as

| (16) |

Let us focus first on the resolvent. We will construct an ellipse in the complex plane such that the resolvent norm is bounded on its right half. In particular, satisfies the following properties

Assumption 2.

We assume that an ellipse of center and right intersection with the real axis is given in such a way that:

-

1.

its right half, that from now on we call leaves to its left the spectrum of , , and the set of the singularities of the function ;

-

2.

, being the working precision;

-

3.

there exists s. t. for all ;

-

4.

there exists s. t. , for all .

For instance we can choose , and .

is uniquely defined by and a further point , . The construction of , as explained in Subsection 4.1, takes as input parameters the values and returns a value , which is computed accordingly to the pseudospectral geometry of the operator .

In general, an ellipse satisfying Assumption 2 for a given operator and vector is not known a priori. Assume that a closed curve surrounding the spectrum of and the possible singularities of is known. Moreover , we assume that encloses the portion of the complex plane where the resolvent norm is large. Based on , a general algorithmic strategy for computing numerically is proposed in Section 4.1. Since for a general matrix we do not have any information about its pseudospectral geometry, we approximate by using eigtool [21]. The construction is general and it does not require any a priori information about the spectral behaviour of . Moreover, for the applications under consideration we show that a low resolution when approximating might be enough for our purposes, see Section 4.2. Notice that, if more information about the pseudospectral behaviour of is available, the use of eigtool can be avoided.

Once is given, we want (13) to map the segment , for an to be fixed, onto . Imposing the ellipse to be centered at and to pass through the points , we get

| (17) |

where

Solving (17) for we get

| (18) | |||||

| (19) | |||||

which only depend on the real parameter .

3.1 Quadrature error estimates for the new integration contour

Assume we are interested in approximating the unknown function up to a certain precision that we call . Because of the presence of the exponential, we expect the integrand function (15) to become smaller in modulus as moves from the right to the left on the profile of integration. For this reason, we would like to truncate the integral once the function reaches the value . The motivation for fixing as in point (2) of Assumption 2 is that we are assuming that the center of the half ellipse (that is also the center of the integration ellipse ) is negative enough to make the integrand function close to the working precision at . In this way, for every greater than the working precision, we can efficiently use the half ellipse of integration in order to recover approximations of the solution of order . In practice, we assume that there exists a truncation parameter , defined as

| (20) |

The integrand we want to approximate is

In other words, we are neglecting not only the two half-lines of profile (4), but also the contribution to the integral coming from the portions of ellipse parametrized in the intervals and as on these intervals the modulus of the integrand function is expected to be lower than the precision , because of the rapidly decaying behaviour of the exponential. Applying trapezoidal quadrature rule to , we get the sum

We remark that, since the profile of integration is symmetric w.r.t. the real axis, the quadrature sum can be simplified to

| (21) |

From Theorem 1 we get the following result.

Theorem 2.

Assume that the function (15) is analytic and bounded on the rectangle for a certain , with and given by (18), (19), (3). Assume moreover that the ellipse of integration has foci on the real axis. Set

| (22) | |||

| (23) | |||

| (24) |

Finally, we assume that the integrand function for all . Then the quadrature error can be estimated by

| (25) |

with and given by (7) (with ).

Proof.

The result follows immediately from Theorem 1 with . Following the notation of Theorem 1, we set and . In particular, we observe that satisfies Assumption 1. Now, let us estimate for . We have

We observe that, from the hypothesis that both the foci are real, the horizontal semi-axis of the ellipse is longer than the vertical one, and so . Then is positive and so is (as from its definition in (19)). So, it is straightforward to prove that the maximum of the exponential is attained for . Indeed consider the function . Its derivative is and it is positive if and only if

Recalling (18), (19) this reads as

yhere . Then, is increasing if and only if and, since , attains its maximum for . ∎

Remark 1.

In considering the term

| (26) |

we have that and then for growing. Moreover, as from equation (3), is chosen in order to have smaller than the working precision. In the end, we expect to be much smaller than , at least for big enough. In practice, is very small (and negligible) also for very small values of . To show this, we report in the following tables the size of the error B (26) that we observe in the numerical experiments displayed in Section 5. The term , which is computed for , is much smaller than the accuracy in every case.

Remark 2.

It is possible to select a positive and consider the trapezoidal rule with a quadrature step for some natural number , and to change the proof of Theorem 1 in order to make as defined in (26), by evaluating the modulus of the integrand function along boundary of the rectangle .

In this way, the double exponential appearing in (26) vanishes because of the multiplication by and the term is even smaller. This change will made the length of the interval used to select the quadrature step dependent on the number of the nodes and so, it won’t be possible any more to double this number saving the information computed on the previous nodes.

3.2 Selection of the optimal integration contour

Once is fixed, the profile of integration is uniquely defined by equations (18), (19), (3). To complete our construction, we need to ask the exponential part in the integrand to be bounded on the external half ellipse . We have

Then, setting , being , we get that

| (27) |

and, recalling equations (18), (19), (3), we get

| (28) |

The term is made dependent on so that it is not fixed a priori but it results from the optimization process of the parameter . The construction summarized by the equations (18), (19), (3), (28) is still theoretical. In order to have it working, we need to find a parameter (and consequently the truncation parameter as defined in (20)) giving us the actual rate of convergence of the quadrature rule. We notice that the profile of integration is given once is fixed by formulas (18), (19). The tool we use to make the selection is the estimate (25). In order to simplify this estimate, we identify a leading term and neglect all the remaining ones, whose contribution is expected to be smaller. First of all, we notice that we expect (defined in (22), (23)): this is due to the rapid decaying property of the exponential part in the integrand function and, in practice, it holds in most cases. Moreover, we assume (where is the one in (24)), since the exponential is larger for parametrized in than the one in . In the end, we neglect the contribution of the term of order (), and the one of the term (26) that is expected to be small (see Remark 1). Finally we simplify the error estimate (25) to

| (29) |

Recalling (23), we roughly estimate . Since we are interested in the order of magnitude of the estimate is enough precise for our purposes. In the end, within the accuracy, the quadrature error is

| (30) |

Assuming we seek approximation of with a prescribed precision , we impose (30) to equal the precision. Solving for , we compute

| (31) |

as the (theoretical) minimum number of quadrature nodes letting us reach the fixed accuracy. We aim to minimize in order to make the convergence as fast as possible. The minimization of the function in (31) appears to be technically complicated since it depends on two variables () and the truncation parameter depends on the profile of integration by the nonlinear constraint (20). For this reason, recalling that , we estimate

| (32) |

The best that we can do to minimize is to minimize the function

| (33) |

We fix an upper bound and we seek minimizers of in the interval . In the numerical experiments we use . Once the minimizer value has been computed, it defines uniquely the profile of integration by formulas (16), (18), (19), (3). Recall that is a function of by formula (28).

3.3 Truncation error

The profile (4) that we use to apply the Bromwich inversion formula is never used in practice: we just use a “small” portion of the ellipse contained in it. How much this portion is “small” depends on the fixed precision . In practice, we disregard all the points of (4) whose contribution is estimated to be smaller than . We resume the global error analysis in the following

Theorem 3.

Consider the integration profile defined in (4), where the elliptical part is constructed as in Section 3.2. We denote as in (4), the parametrization of the two half lines making part of , whose slope is assumed to be such that encloses all the singularities of the integrand function. Moreover, assume that

In the end, we assume that all the hypotheses of Theorem 2 are satisfied. Then, the total error of our approximation of (3) is given by

where is bounded by (25) and the truncation error is bounded by

and does not depend on .

Proof.

Recall that we are approximating the following integral

with defined by (4). First of all, we estimate the contribution of the two half-lines parameterized by the mappings and . Choosing as in (4), we have

| (34) |

with our choice in (17). An analogous bound follows for . We notice that the same estimate is not valid if we choose the two half-lines to be vertical.

Next we notice that the only portion of the ellipse that we approximate by using the quadrature formula (21) is the one parameterized on the interval . We estimate now the contribution of the other two intervals , . Recalling that we assume and for all as in Theorem 2, we have

and analogously for the integral on . In the end the error

where is defined in (21), is estimated by Theorem 2. The thesis then follows. ∎

3.4 Stability of the method

One of the most attractive features of the method is its stability. In particular, we are able to compute the stability constant of the method.

In practice, we approximate the exact solution by the linear combination

| (35) |

where and is the error in the numerical solution of the linear system

| (36) |

for our quadrature nodes. We assume that the quadrature nodes , the parametrization and its derivative are computed exactly. We state the following result.

Proposition 1.

Proof.

The actual error in our computation is given by

We can estimate it in the following way

with and as in Theorem 3 and

Recalling that the integration contour is parameterized as , with positive and we have

where . ∎

Remark 3.

Given an integration contour , depending on the working precision, it is possible to compute the maximal precision we can get along . First we compute the condition number of the matrix , for a set of . Then we use this information to estimate the numerical error introduced when solving (36). At this point the computation of (37) is straightforward. We can incorporate this feasibility check in our algorithm, asking the user, in case the required precision is too high, to adjust the parameter by choosing a larger value.

3.5 The approximation of the integrand tail

Once the integration contour is computed, we need to approximate the truncation parameter as defined in (20). Let us recast (20) into the system

| (38) | |||

| (39) |

Observe that, once the profile of integration is fixed, considering its parametrization , from (38) one has

| (40) |

We suggest Algorithm 1 to compute iteratively (where is the precision we ask for the constant ).

In all the numerical tests we observe that Algorithm 1 converges quickly to the sought values of . We fix and in at most iterations Algorithm 1 approximates the constant with a precision approximately equal to .

Remark 4.

The sequence resulting from Algorithm 1 can be seen as a fixed point iteration method. Concerning the convergence of Algorithm 1, assume that a pair exists such that

| (41) |

where

| (42) |

Assume further that (42) is differentiable and there exists a constant such that

| (43) | |||

| (44) |

being an interval containing , being solution to system (38), (39) and all the points , , with as defined in Algorithm 1. Then both the sequences , converge and in particular

4 Practical implementation

4.1 Construction of the inner ellipse

In the described method, it is crucial to construct properly the inner ellipse . It is conceived to bound the resolvent norm and it must be adjusted in order to leave to its left all the possible singularities of the vector . Let us focus, for the moment, on the resolvent norm: should be far enough from the spectrum of but, if it’s too far, it will produce a slowdown of the rate of convergence of the numerical scheme. For this reason, we decided to construct the ellipse by a procedure based on the computation of some pseudospectral level curve associated to the matrix . In particular, we approximate these curves using eigtool [21]. If some theoretical information about these curves is already known, we can skip the computation by eigtool and directly construct from it. First of all, we define the region were we need to “place” our ellipse. This region is defined as , where are real parameters to be chosen. This choice is partially heuristic and we ask the user to make a selection of these two values. We suggest the following criteria:

-

(i)

choice of : once the time is fixed, we need to have smaller than the working precision. This is due to the fact that we use as the center of the ellipse and, having in mind formula (34), we need to be sure that the contribution of the two lines of the profile (4) is negligible. In our experiments we choose .

-

(ii)

choice of : this point is going to be the right intersection of our half ellipse with the real axis. We can choose as the rightmost intersection of the pseudospectral boundary with the real axis taking, for example, . In case has some singularity to the right of this point, we need to move as to be sure that all these singularities are to the left of the half ellipse. In our examples has a singularity in the origin. For this reason we take as a small positive number. Several values of are tested in the numerical examples.

Now we need to estimate the resolvent norm in the strip . We do this by computing some suitable pseudospectral level curve of the matrix . We recall that, given , the pseudospectral level curve of is defined as

| (45) |

Moreover, we call weighted pseudospectral level curve the set of points

| (46) |

Let us fix two positive values (we use as bounding constants). We define as the weighted pseudospectral level curve and the pseudospectral level curve. We compute , in the strip . We notice that both , are symmetric w.r.t. the real axis (and then we can just compute the two curves in the upper complex plane). For using our algorithm, we need the two level curves to be defined in the whole strip . For this reason, if it happens that for some there is no such that is on the curve, we set and we add the point to the curve. After that, we define

| (47) |

We call critical curve. The meaning of the computation of is the following: we approximate in order to have a bound of and then of the integrand function (15), while on we require that the norm of the resolvent is not too high in order to ensure that the condition number of the system (2) on the points of the curve (and then of the ellipse ) is not too big to cause a loss of accuracy. Defining as in (47) will ensure that both the conditions are satisfied. From a practical point of view, we computed the value of the resolvent norm on a grid in the strip using the Matlab code eigtool, [21]. It is straightforward to compute an approximation of , , and then from it. In particular we end up with a set of points approximating the upper part of the critical curve . The ellipse should be chosen in order to approximate in the sharpest way the curve . Moreover, since it may happen that the grid chosen by eigtool is too coarse, the critical curve may not capture some of the eigenvalues of (in the case where the pseudospectral level curve near those ones are very small closed curves surrounding the eigenvalues). In addition, we have to consider also the possible singularities of (that we assume to form a finite set). We call , , the eigenvalues of and , , the singularities of . Now define

The ellipse has to be chosen in order to enclose all the points of . In this way, the two conditions (3), (4) of Assumption 2 will be satisfied with and . We recall that, the ellipse is completely defined by its center (that we choose as ), and two other points: the point and any other point , that we used in the equations (17), (27). We can always take since the curve is symmetric w.r.t. the real axis. The basic idea of the construction of is to start with a large ellipse (a circle) and then shrink it as much as possible so that all the points of lay below the upper arc of . The construction we suggest is the following:

-

(i)

We start considering a circle centered at with radius .

-

(ii)

If all the points of are inside the circle, we try to shrink the curve. To do this, we consider a partition of the interval , say with , . We consider the ellipse centered at , passing through the point and having right focus at . Then, we check, from the right to the left if all the points of are enclosed by . If there is a point that is outside , we go back to the circle of the previous case and we choose it as . In particular we set and as the corresponding imaginary part on the circle. In our experiments we set .

-

(iii)

If, on the contrary, all the points of are inside , we go on choosing a more elliptical curve having right focus at and then we check the position of w.r.t. the new . We stop when the curve excepts some points of , choosing the previously computed as and the point on it as we did in the previous case.

-

(iv)

If the last computed ellipse , the one with right focus at is still large enough to enclose , we set as the point on corresponding to .

-

(v)

If in the very first point the circle already excepts some points of , we choose among them the point with higher (in modulus), imaginary part, say it is the point and we set for a small . The curve is the one centered at , and passing through . We can adjust the value of in order to ensure that is all inside .

In Figure 4, we show how the algorithm works on a particular matrix coming from the spatial discretization of the Heston operator

(that we will use in Section 5). The green line is a 100 points approximation of the critical curve in the region defined by , while the blue dots are the eigenvalues of the matrix in the same strip of the complex plane. Top left: the blue line is the first guess for the ellipse (a circle). Top right: the guesses for are plotted in blue (where each ellipse has right focus , a point of the partition of the interval ). Bottom left: in addition to the previous guesses, also the first ellipse excepting some of the eigenvalues of and crossing the curve is plotted (it corresponds to the index ). Bottom right: is drown in red (and it is chosen as the ellipse corresponding to ) and the point is marked with a black cross

4.2 Computational cost

The method consists in two main parts: the precomputing part, where we construct the ellipse , see Section 4.1, and compute the actual ellipse of integration (Section 3.1) and the computing part, where the quadrature formula (21) is applied to get the approximation of the unknown function . The precomputing part is essential in order to make the algorithm general, since by means of it all the pseudospectral information about the discrete operator is approximated and, then, used to set the optimal profile of integration. In particular, in this part the software eigtool is employed. This software allows to compute an approximation of the resolvent norm at the points of a rectangular grid in the complex plane. As a byproduct, eigtool also computes the eigenvalues of . In the Table 1, we report the time employed by eigtool in computing the approximations for both Black-Scholes and Heston operator (the software is run on a laptop with a 2,4 GHz Intel Core i5 processor, using Matlab R2016b). In each case, we report the region of the complex plane (Box) where we seek the approximation. For Black-Scholes (size ), the number of points defining the rectangular grid is set to , while it is set to in the case of Heston equation (size ).

| Black-Scholes | Heston | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

The computation of the pseudospectral information is used to compute the critical curve (47). The ellipse is selected by the algorithm explained in Section 4.1. We remark that the use of eigtool produces a larger computational cost w.r.t. other methods [11, 13, 14, 20]. However, we remark that these methods can be efficiently applied only if some pseudospectral information on is already known. The choice of an algorithmic approach to investigate the behaviour of makes our method ready to be used for every system of ODEs of the form (1). In the case is normal or some curve bounding the region where the resolvent norm of grows unboundedly is already known, the use of eigtool can be avoided.

For the computation of the truncation parameter , we apply Algorithm 1. Every iteration of this procedure requires the evaluation of the function

The cost of this evaluation depends on the size of . We observe that for every iteration of Algorithm 1 the linear system

| (48) |

is solved for .

Concerning the integration part, i.e., the computation of the quadrature sum (21), the execution time depends on the size of the matrix and the number of quadrature nodes that are used to get the desired accuracy. In order to save time, it is possible to precompute in parallel the integrand function at the quadrature nodes. Assuming the critical curve already computed by eigtool, in Tables 2, 3 we report the time needed to select the profile , to approximate the truncation parameter by Algorithm 1 of Section 3.2 and to apply the quadrature sum (21) for nodes. In all cases the resolution of the system (48) is done using the backslash command of Matlab. We also report the total number of solved linear systems.

| Select. | Algorithm 1 | Numerical quadrature | # Solved linear systems | |

|---|---|---|---|---|

| iterations | ||||

| iterations |

| Select. | Algorithm 1 | Numerical quadrature | # Solved linear systems | |

|---|---|---|---|---|

| iterations | ||||

| iterations |

We notice that it is possible to save the computation done for when approximating the solution on nodes (taking an extra node between each pair of consecutive points). In this way the execution time is halved doubling the number of nodes.

An extra computational cost is needed for the feasibility check: it is possible, indeed, to approximate the stability constant of the method by computing the condition number of the system (36) for a set of points on the integration ellipse , as explained in Section 3.4. However, this feasibility check can be skipped and it is not necessary in order to run the algorithm even if it is useful to make a forecast on the maximal precision attainable on the computed and to check whether the chosen tolerance is too sharp w.r.t. the working precision. It is worth noticing that the execution time needed to run eigtool strongly depends on the fixed number of grid points. How to set this number? Numerical experiments suggest that we need a very low resolution of the computed pseudospectral level curves and the algorithm is robust w.r.t. the choice of . For example, for the Black-Scholes case, with , , we seek approximations of the resolvent norm in the box . Then, we compute a reference solution corresponding to and we measure the error w.r.t. this approximation of the solutions computed using . We also report the time employed by eigtool to perform the approximation. The results are listed in Table 4.

4.3 Summary of the method

The main parts of our method are: construction of the inner ellipse , selection of the optimal integration contour , truncation of the profile . In the end, the trapezoidal quadrature rule is applied to the selected portion of ellipse to get the sought approximation of the solution to (1). For the sake of clarity, we briefly list the sequential steps which are needed to implement the method:

- 1.

-

2.

Computation of the inner ellipse . As explained in Section 4.1, the user is asked to choose the values of (respectively the center of and its right intersection with the real axis). This choice is partially heuristic but it is guided by (i), (ii) on Page 4.1. The procedure of Section 4.1 returns a point which defines uniquely the profile , together with . The construction uses eigtool for the computation of the pseudospectral sets (as defined in (45), (46)). In all the numerical experiments we found that the choice , was effective.

-

3.

Computation of the integration profile as explained in Section 3.2. In particular, the ellipse of integration is parameterized as

with coefficients depending on just one free parameter by formulas (18), (19), (3). In order to find the optimal profile of integration we minimize the scalar function of in (33);

- 4.

-

5.

Apply quadrature formula (21) to get the sought approximation of .

5 Numerical results

In this section, we collect some numerical results of our method. We first consider a canonical convection-diffusion equation, used as an academic test. We then test our approach with the Black-Scholes and Heston equations. The Black-Scholes model here is the same as the one considered in [11], while for the Heston model we consider a slightly different boundary condition from that in [11], following [7]. The function (33) is minimized by means of the built-in Matlab function fminbnd. In all the examples, we construct the inner ellipse as explained in Subsection 4.1 taking , .

5.1 A canonical convection-diffusion operator

As a first illustration of our method we apply it, as in [20], to

| (49) |

with initial and boundary conditions

| (50) |

We consider and following the following steps, according to Section 4.3:

- •

-

•

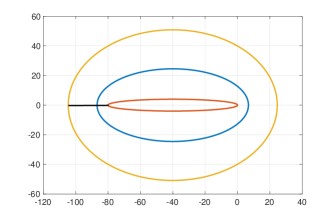

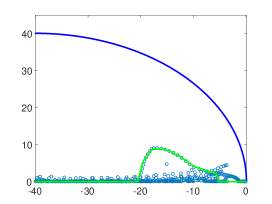

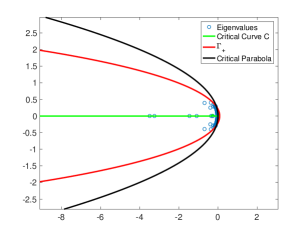

Computation of the inner ellipse : following (i), (ii) of page 4.1, we choose and . We remark that in this case the vector in (1) is constant and then has a singularity in the origin. For this reason, we must select . The procedure of Section 4.1 gives back the point . The ellipse is plotted in Figure 5 together with the critical parabola recovered in [20] (). The green line is the one called in Section 4.1 and it is computed by eigtool.

-

•

Computation of the integration profile: once the parameters are fixed, we minimize the function (33). It reaches its minimum at . The minimization is done numerically using the built-in Matlab function fminbnd.

- •

-

•

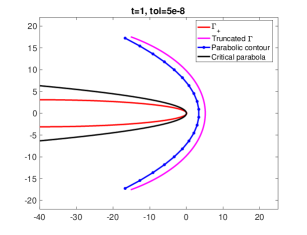

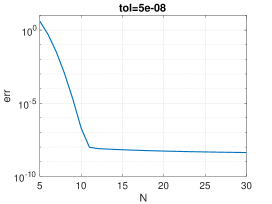

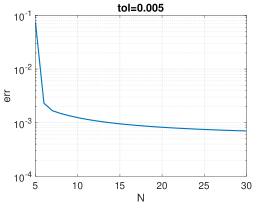

We apply quadrature formula (21). We apply it on nodes, for . We compare the resulting approximation of with the one computed by direct evaluation of the exponential matrix (expm function in Matlab). The results are plotted in Figure 5.

Figure 5: Top Left: comparison between and the theoretical critical parabola used in [20]. Top Right: plot of and truncated . In green the critical parabola and in blue the parabolic profile selected for by the method [11]. Bottom: Error VS number of nodes.

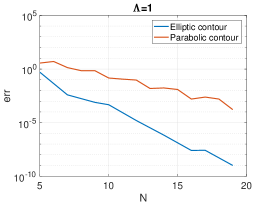

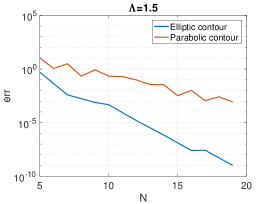

5.2 Black-Scholes equation

The well known (deterministic) Black-Scholes equation [2] has the following form

| (51) |

for given, where the unknown function stands for the fair price of the option when the corresponding asset price at time is and is the maturity time of the option. Moreover, , are given constants (representing the interest rate and the volatility respectively). In practice, for the sake of numerical approximation, we consider a bounded spatial domain, considering

for a sufficiently large . We take (51) together with the following conditions, typical for the European option call

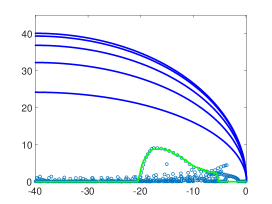

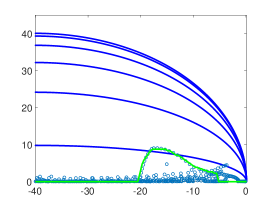

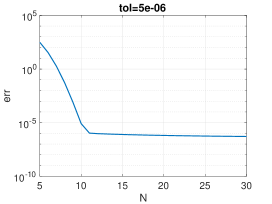

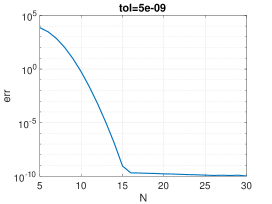

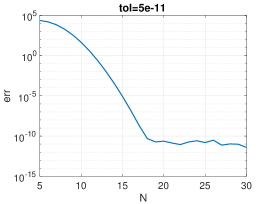

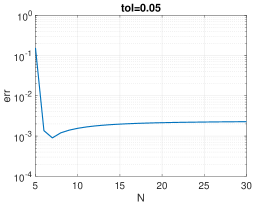

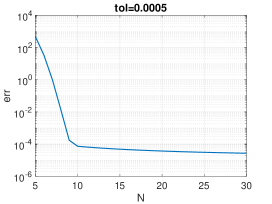

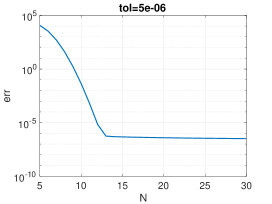

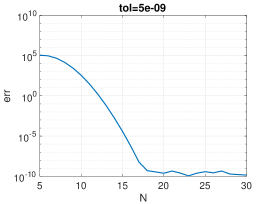

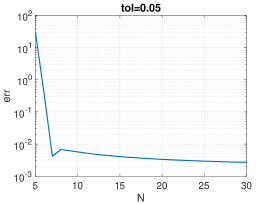

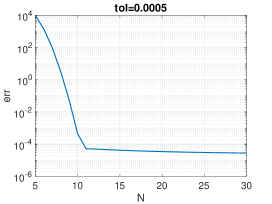

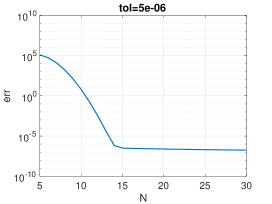

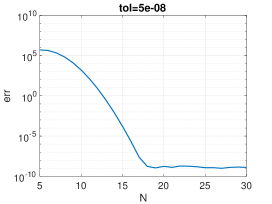

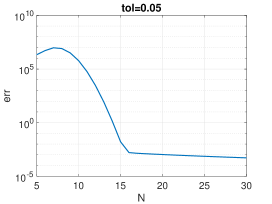

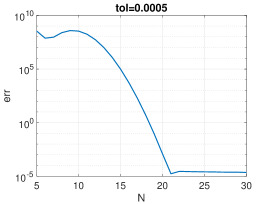

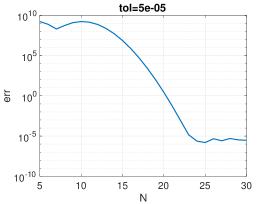

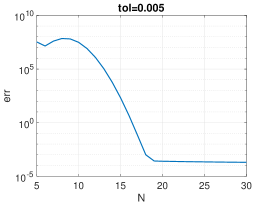

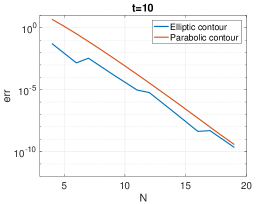

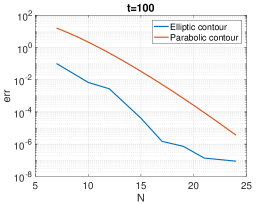

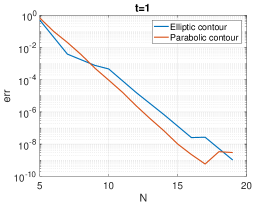

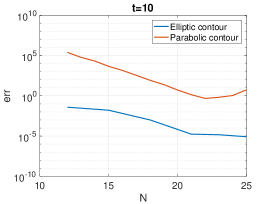

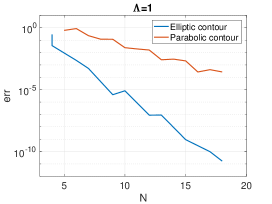

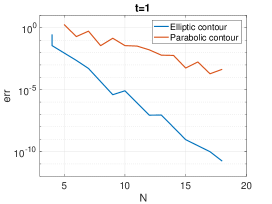

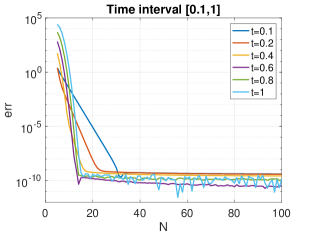

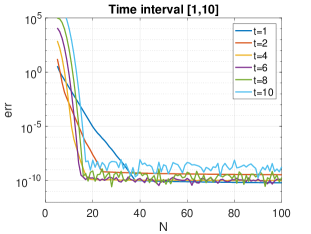

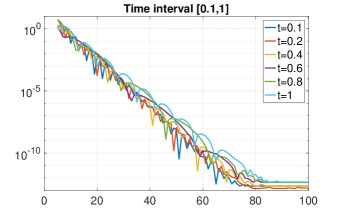

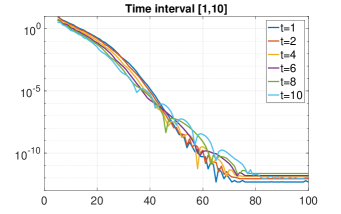

Following the same strategy adopted in [11], we discretize in space on a uniform space grid of points in , for , using the classical centered finite difference scheme. We choose , and . We plot the error for a selection of tolerances for the cases (Fig. 6) and (Fig. 7)

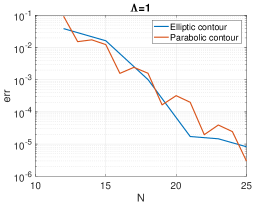

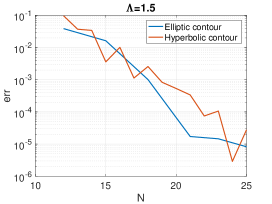

5.3 Heston equation

The Heston equation [5] is

| (52) |

The unknown function represents the price of an European option when at time the corresponding asset price is equal to and its variance is . We consider the equation on the unbounded domain

where the time is fixed. The parameters , and are given. Moreover, equation (52) is usually considered under the condition that is known as Feller condition. We take equation (52) together with the initial condition

where is fixed a priori (and represents the strike price of the option), and boundary conditions

For the numerical solution of (52), we need to choose a bounded domain of integration. In particular we fix two positive constants and we let the two variables vary in the set

On the new boundary, we need to add two more conditions (specific for the European call option)

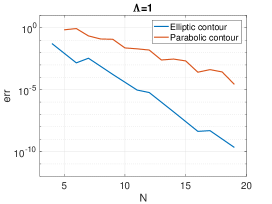

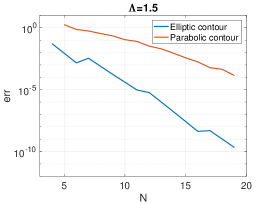

The spatial discretization we adopted is the one introduced in [7]. We take . We plot the error for a selection of tolerances for the cases (Fig. 8) and (Fig. 9).

6 Comparison with other methods

6.1 Comparison with parabolic contours

A direct comparison with the method in [11] is not possible, since our algorithm works with the goal of a fixed accuracy while the one reported in [11] aims to reduce the error as grows. Anyway, for the sake of comparison, we can run our algorithm as follows:

-

-

for a set of target precisions ( for example), we run our algorithm;

-

-

for each tolerance we save the smallest number of quadrature nodes for which is reached;

-

-

for each tolerance we save the corresponding error .

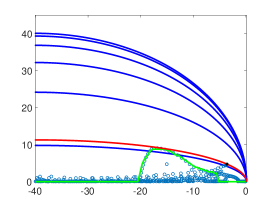

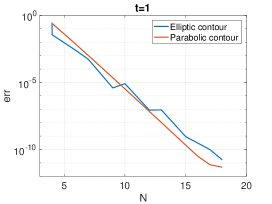

Once we get the array , we can compare it with the corresponding error coming from the method of [11]. We make our experiments both for Black-Sholes and for Heston equation, for a selection of times . In Figure 10 the comparison for Black-Scholes is depicted

For the comparison in the case of Heston equation, we recall that the boundary condition considered in [11] is slightly different from (5.3). However the spectrum of the discrete operator is quite similar, and thus we implement the method in [11] using the same inner parabola. Qualitatively, the numerical results we get for are the same as the one in [11]. The comparison is showed in Figure 11

6.2 Comparison with hyperbolic contours

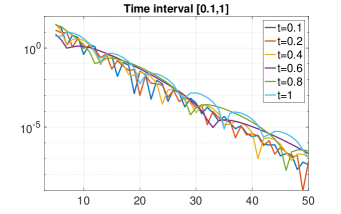

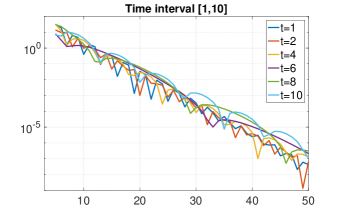

By using the same startegy as the previous subsection, we build the array . We compare these results with the method in [14] for both the cases of Black-Scholes and Heston equations. We set , as geometric parameters to bound the resolvent norm, as explained in [14]. This choice turns out to be effective and the method seems to converge. However, in [14] no optimality criteria are given to select and they necessarily depend on the spectral geometry of . Since [14] works on time intervals of the form , we provide a comparison for a selection of time ratios and for the times . The results are reported in Figures 12, 13, 14 and 15

7 Extension to the case of time intervals

We notice that the most expensive computation when evaluating (15) is the inversion of the matrix at the quadrature nodes. This inversion does not involve the time that appears only in the exponential part. For this reason, a great improvement to the efficiency of the method comes from the possibility of using a unique integration contour for a whole time interval . In this Section we suggest a strategy for computing a unique profile of integration, uniquely defined by the parameter by (16), (18), (19), (3). By doing that, for a general time , we just need to compute the corresponding truncation parameter and the constant in (38), (39). We would like to get an uniform error estimate like (29) for the whole interval . Recalling (30) and the fact that , we estimate

| (54) |

Using estimate (54), we recover the (theoretical) value of quadrature nodes sufficient to reach a prescribed precision . In particular, we get

| (55) |

Fix . We construct as explained in Section 4.1 for the time (lower time of the interval). The choice of the smaller time reflects in the setting of the center of the integration ellipse as explained in (i) of page 4.1. In this way, we expect the contribution of the two half-lines in (4) to be negligible for all the times . Application of the construction of Section 4.1 gives the parameters defining uniquely . At this point, we minimize the function

| (56) |

where is given by (28). We end up with the optimal defining uniquely the profile of integration by (16), (18), (19), (3). We will use this profile for every time .

Even if the profile of integration is the same for all times, when changes we need to truncate it in a different point. For a general we can compute the corresponding values using Algorithm 1 of Section 3.5. In case we need to evaluate our integral for many times , Algorithm 1 can be too expensive. Indeed, every iteration of this method requires the evaluation of the resolvent function. To save computational cost, we do as follows:

-

•

we compute the pairs and corresponding to the times ;

- •

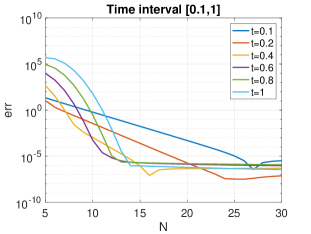

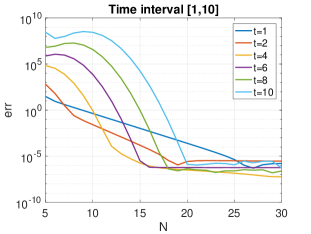

We show some numerical experiments for both Black-Scholes and Heston equation. Since the case of very large times is not really interesting (because the solution rapidly becomes stationary), we consider the case of intervals of the form with . In particular, we make the experiments on the intervals , . In this way, we approximate the solution on the whole time interval and the computation is competitive with respect to the classical PDEs integrators. In the plots 16, 17, we show the numerical results for Black-Scholes and Heston equations. The target tolerance we choose is for Black–Scholes and for Heston. We also fix for Black–Scholes and for Heston.

A slowdown of the convergence rate as decreases is observed. This is due to the fact that is decreasing w.r.t. time and the rate of convergence is . It is interesting to compare those performances with the one obtained by [14] since this method is also conceived to work on time intervals. In Figures 18, 19 the results are plotted (in both cases we take )

8 Conclusions

In this paper we have proposed a new method for the numerical inversion of the Laplace transform of functions with specific properties arising in the space-time approximation of linear convection-diffusion equations.

Our method is based on a preliminary investigation of some pseudospectral level sets of . In this way, the method can be directly applied to any linear system of ODEs with constant coefficient matrix and no other a priori information about the discrete operator is needed. This first step is not considered sistematically in [11, 13, 14, 20]. In our applications, the computation of the pseudospectral level curves is performed by eigtool. The computational cost of the approximation made by using eigtool is reported in Subsection 4.2, where we also show that a low resolution in this approximation might be enough to construct a good integration contour.

We recap the main advantages of our method:

-

(i)

It is designed in order to achieve a prescribed precision as fast as possible.

-

(ii)

It is stable: adding quadrature nodes never deteriorates the quality of the approximation. As shown in [14] and [20], this can be a delicate issue in the numerical inversion of the Laplace transform.

The stability constant of the method can be computed to carry out an a priori feasibility check to detect if the prescribed accuracy is too high.

-

(iii)

It is easily adapted to approximate the solution to (1) on relatively large time intervals of the form , with .

-

(iv)

Once the target accuracy and the time are fixed, our algorithm selects the profile of integration independently of the number of quadrature nodes. Thus, the cost of adding quadrature nodes to reach the target accuracy is low in comparison to the algorithms in [11, 14], where the integration contour does depend on the number of quadrature nodes.

Future research will be devoted to reduce the dependance on eigtool, which can be prohibitively expensive for large matrices arising from the spatial discretization of 2D and, specially, 3D convection-diffusion equations. The resolution of the linear systems with non-normal matrices should also be more carefully studied.

Acknowledgments

The authors thank K. J. in ’t Hout for providing the codes implementing the method in [7]. NG and MLF thank INdAM GNCS for financial support. MLF also acknowledges the support of the Spanish grant MTM2016-75465 and the Ramón y Cajal program of the Ministerio de Economia y Competitividad, Spain.

References

- [1] L. Banjai, M. López-Férnandez, A. Schädle, Fast and oblivious algorithms for dissipative and two-dimensional wave equations, Siam J. Numer. Anal., Vol. 55, pp. 621-639, 2017.

- [2] F. Black, M. Scholes, The pricing of options and corporate liabilities, J. Polit. Econ., Vol. 81, pp. 637-654, 1973.

- [3] B. Dingfelder, J. A. C. Weideman, An improved Talbot method for numerical Laplace transform inversion, Numer. Algorithms, Vol. 68, pp. 167-183, 2015.

- [4] I. P. Gavrilyuk, V. L. Makarov, Exponentially convergent parallel discretization methods for the first order evolution equations, Comput. Methods Appl. Math., Vol. 1, Number 4, pp. 333-355, 2001.

- [5] S. L. Heston, A closed-form solution for options with stochastic volatility with applications to bond and currency options, Rev. Finan. Stud., Vol. 6, pp. 327-343, 1993.

- [6] J. C. Hull, Options, Futures and Other Derivatives, 6th ed., Prentice Hall, New Jersey, 2006.

- [7] K. J. in ’T Hout, S. Foulon, ADI diference schemes for option pricing in the Heston model with correlation, Int. J. Numer. Anal. Model., Vol. 7, Number 2, pp. 303-320, 2010.

- [8] K. J. in ’t Hout, ADI schemes in the numerical solution of the Heston PDE, Numerical Analysis and Applied Mathematics, eds. T. E. Simos et.al., AIP Conf. Proc: 936, 2007.

- [9] K. J. in ’t Hout, B. D. Welfert, Stability of ADI schemes applied to convection-diffusion equations with mixed derivative terms, Appl. Numer. Math. Vol. 57, pp. 19-35, 2007.

- [10] K. J. in ’t Hout, B. D. Welfert, Unconditional stability of second -order ADI schemes applied to multi-dimensional diffusion equations with mixed derivative terms, Appl. Numer. Math., Vol. 59, pp. 677-692, 2009.

- [11] K. J. in ’t Hout, J. A. C. Weideman, A contour integral method for the BlackScholes and Heston Equations, SIAM J. Sci. Comput., Vol. 33, Num. 2, pp. 763-785, 2011.

- [12] M. Javed, L. N. Trefethen. A trapezoidal rule error bound unifying the Euler-Maclaurin formula and geometric convergence for periodic functions. Proc. R. Soc. Lond. Ser. A Math. Phys. Eng. Sci., 470(2161):20130571, 9, 2014.

- [13] M. López-Férnandez, C. Palencia, On the numerical inversion of the Laplace transform of certain holomorphic mappings, Appl. Numer. Math., Vol. 51, pp. 289-303, 2004.

- [14] M. López-Férnandez, C.Palencia, A. Schädle, A spectral order method for inverting sectorial Laplace transform, SIAM J. Numer. Anal., Vol. 44, Num. 3, pp. 1332–1350, 2006.

- [15] S. C. Reddy, L. N. Trefethen, Pseudospectra of the convection-diffusion operator, SIAM J. Appl. Math., Vol. 54, pp. 1634-1649, 1994.

- [16] D. Sheen, I. Sloan, V. Thomée, A parallel method for time discretization of parabolic equations based on Laplace transformation and quadrature, IMA J. Numer. Anal., Vol. 23, pp. 269-299, 2003.

- [17] A. Talbot, The Accurate Numerical Inversion of Laplace Transforms, IMA J. Appl. Math., Vol. 23, pp. 97-120, 1979.

- [18] L. N. Trefethen, M. Embree, Spectra and Pseudospectra: The Behaviour of Nonnormal Matrices and Operators. Princeton, NJ: Princeton University Press, 2005.

- [19] L. N. Trefethen, J. A. C. Weideman, The Exponentially Convergent Trapezoidal Rule, SIAM Rev., Vol. 56, Number 3, pp. 385-458, 2014.

- [20] J. A. C. Weideman, Improved contour integral methods for parabolic PDEs, IMA J. Numer. Anal., Vol. 30, pp. 334-350, 2010.

- [21] Thomas G. Wright. EigTool. http://www.comlab.ox.ac.uk/pseudospectra/eigtool/, 2002.