High Dimensional Elliptical Sliced Inverse Regression in non-Gaussian Distributions

Abstract

Sliced inverse regression (SIR) is the most widely-used sufficient dimension reduction method due to its simplicity, generality and computational efficiency. However, when the distribution of the covariates deviates from the multivariate normal distribution, the estimation efficiency of SIR is rather low. In this paper, we propose a robust alternative to SIR - called elliptical sliced inverse regression (ESIR) for analysing high dimensional, elliptically distributed data. There are wide range of applications of the elliptically distributed data, especially in finance and economics where the distribution of the data is often heavy-tailed. To tackle the heavy-tailed elliptically distributed covariates, we novelly utilize the multivariate Kendall’s tau matrix in a framework of so-called generalized eigenvector problem for sufficient dimension reduction. Methodologically, we present a practical algorithm for our method. Theoretically, we investigate the asymptotic behavior of the ESIR estimator and obtain the corresponding convergence rate under high dimensional setting. Quantities of simulation results show that ESIR significantly improves the estimation efficiency in heavy-tailed scenarios. A stock exchange data analysis also demonstrates the effectiveness of our method. Moreover, ESIR can be easily extended to most other sufficient dimension reduction methods.

Keywords: Multivariate Kendall’s tau; Sliced inverse regression; Elliptical distribution; Convergence rate; Central subspace; Sufficient dimension reduction.

MSC2010 subject classifications: Primary 62H86; secondary 62G20

1 Introduction

In the regression model, let denote the response variable and denote the covariates. If there exist orthogonal vectors with unit norm such that

| (1.1) |

where represents independence, the column space of the matrix is defined as a dimension reduction subspace by Cook (1994) and Cook (1998). The intersection of all the dimension reduction subspaces is still a dimension reduction subspace and is called the central subspace (Cook (1994), Cook (1996)). Various methods have been proposed to estimate the central subspace in the literature, which are together referred as sufficient dimension reduction methods. Among them, sliced inverse regression (SIR, Li (1991)) is the earliest and most popular method owning to its simplicity, generality and efficiency for computation. Li (1991) proved the consistency of SIR for fixed setting. Hsing and Carroll (1992) considered the case where each slice only contained two data points and gave the asymptotic normality results for the SIR estimator. Following their work, Zhu and Ng (1995) derived the asymptotic properties of the sliced estimator for general cases. Zhu and Fang (1996) proposed another version of SIR based on the kernel technique and obtained its asymptotic results. All the results summarized above are constricted to fixed context. Zhu, Miao and Peng (2006) studied the asymptotic behaviors of the SIR for diverging with . A recent work given by Lin, Zhao and Liu (2017) treated the asymptotic performance of the SIR estimator from a different perspective. Instead of SIR, other methods designed for the estimation of the central subspace have also been investigated, including but not limited to sliced average variance estimator (SAVE) proposed by Cook and Weisberg (1991) and Cook (2000), principal Hessian directions (PHD, Li (1992), Cook (1998)), parametric inverse regression (PIR) suggested by Bura and Cook (2001a) and Bura and Cook (2001b), minimum average variance estimator (MAVE, Xia et al., (2002)), contour regression (Li, Zha and Chiaromonte (2005)), inverse regression estimator (Cook and Ni (2005)), the hybrid methods which combined SIR and SAVE in a convex way (Zhu, Ohtaki and Li (2006)), principal fitted components (Cook (2007)), directional reduction (DR, Li and Wang (2007)), likelihood acquired directions (Cook and Forzani (2009)), semiparametric dimension reduction methods (Ma and Zhu (2012)), and direction estimation via distance covariance (Sheng and Yin (2013), Sheng and Yin (2016)).

Due to the simplicity and computational efficiency of its algorithm, SIR is the most widely used and most studied method in practice and in the literature. However, although it only requires the linearity condition (Li (1991)) to have the consistency of the SIR estimator, the SIR performs much worse when the distribution of deviates from the normal case. This phenomenon can be seen quite clearly from our simulations. The fact is that the more the deviates form the multivariate normal distribution, the worse the performance of the SIR gets. In principal component analysis (PCA), which is a unsupervised version of dimension reduction, the deviation from normal assumption is also a serious problem. That is, this kind of deviation may lead to the PCA’s inconsistency (Johnstone and Lu (2009), Han and Liu (2016)) when the dimension of is growing with the sample size . Aware of this inconsistency problem, Han and Liu (2016) proposed a new kind of PCA method based on the Kendall’s tau matrix for elliptically distributed , called elliptical component analysis (ECA). They proved that the ECA method is consistent for both sparse and non-sparse settings. In this paper, we novelly extend their idea from unsupervised learning to supervised learning via a generalized eigenvector problem (Li (2007), Chen, Zou and Cook (2010)). Consequently, our method can address the problem of low efficiency of SIR in non-normal settings. Furthermore, our method is theoretically sound since the elliptical distribution family naturally satisfies the so-called linearity condition (Li (1991)) and the merits of the introduction of the Kendall’s tau matrix for elliptically distributed are then well kept in the sufficient dimension reduction.

The essential reason why we are concerned about the elliptical family comes from the wide range of application of the elliptically distributed data, especially in finance and economics where the distribution of the data often possesses high kurtosis and heavy tailed pattern. For example, Han and Liu (2016) studied a high dimensional non-Gaussian heavy-tailed data set on functional magnetic resonance imaging in their paper. Fan, Liu and Wang (2015) considered the problem of covariance matrix estimation based on large factor model for elliptical data. The proof of the consistency of the SIR in Lin, Zhao and Liu (2017) was based on the assumption that follows a sub-Gaussian distribution. In this paper, we go further steps to investigate the elliptical family of the covariates. To tackle the heavy-tailed problem, we propose a new SIR method called elliptical sliced inverse regression estimator (ESIR) and study both its basic properties and high dimensional properties.

Note that Li (1991) had a remark for the robust versions of SIR (Remark 4.4). Li (1991) did not think this issue was crucial and suggested the influential design points be down-weighted or be screened out in the observational study. However, things are different in our paper where the focus is on the elliptical distributions with heavy tails. It’s not a problem of experimental design, because the data points are not under control. Besides, screening out those “bad” points seems not appropriate. On one hand, the number of those “bad” points can be very large due to the heavy tails and removing them from the sample would worsen the estimation efficiency. On the other hand, heavy tails of the data are exactly what we care about (especially in finance and economics) and ignoring this feature could lead to misleading conclusion. To sum up, we believe that it’s of great importance to do some in-deep research to address the common heavy-tailed issue.

In the second part of the paper, we construct the convergence rate of the ESIR estimator under the high dimensional setting. Specifically, we allow all of the dimension of the covariates , the number of the slices and the number of the data points in each slice to grow with the sample size at a proper rate. This kind of study is of vital importance due to the escalating of computing power bringing us a large quantity of high dimensional data sets in various fields, as pointed out by Zhu, Miao and Peng (2006).

The rest of the article is organized as follows. In the next section, some background knowledge is given about the elliptical distribution and the Kendall’s tau matrix. In Section 3, we propose the ESIR estimator, its basic properties and the ESIR algorithm. Consistency and convergence rate of the ESIR estimator for high dimensional are demonstrated in Section 4. We present large numbers of simulation results to compare the estimation efficiency of ESIR with the original SIR and to investigate the influence of , and on the estimation accuracy in Section 5. Section 6 concludes the paper and the last section reports the technical proofs of the theorems.

2 Background

2.1 Elliptical distribution

Let and with full rank (we only consider the full rank case in this paper). If

where is a nonnegative continuous scalar random variable, is a deterministic matrix with and is a uniform random vector on the unit sphere, we say follows an elliptical distribution, i.e. , . Here, means that the random vectors and follow the same distribution. Throughout the article, without loss of generality we assume to guarantee . The marginal and conditional distributions of an elliptical distribution still belong to the elliptical family and the independent sum of elliptical distributions is also elliptically distributed. Special cases of elliptical distribution include multivariate normal distribution, multivariate t-distribution, symmetric multivariate stable distribution, symmetric multivariate Laplace distribution and multivariate logistic distribution, etc.

Compared with the Gaussian or sub-Gaussian family, the elliptical family enables us to model complex data more flexibly. First of all, the elliptical family includes kinds of heavy-tailed distributions, while the Gaussian is characterized with exponential tail bounds. What’s more, we can use elliptical family to describe tail dependence between variables (Hult and Lindskog (2002), Han and Liu (2016)). Thus, elliptical family can be used to model complex data sets such as the financial data, genomic data and bio-imaging data and so on.

2.2 Multivariate Kendall’s tau

Let be an independent copy of a random vector . We introduce the population multivariate Kendall’s tau matrix (Han and Liu (2016)):

Let be independent replicates of . The sample version of the Kendall’s tau matrix is defined as

It is easy to derive that , and and are both positive definite.The sample Kendall’s tau matrix is a second-order U-statistic with good properties, that is, the spectral norm of the kernel of the U-statistic

is bounded by which makes enjoy some good theoretical properties. Furthermore, the convergence of to doesn’t rely on the generating variable thanks to the distribution free property of the kernel(Han and Liu (2016)).

Although the multivariate Kendall’s tau matrix is not identical or proportional to the covariance matrix of , under some conditions they share the same eigenspace, see Marden (1999), Croux, Ollila and Oja (2002), Oja (2010) and Han and Liu (2016). Moreover, by simple calculation we find that is a weighted version of the sample covariance matrix , that is

| (2.1) |

while

3 Elliptical sliced inverse regression

3.1 Sliced inverse regression

In this section, we give a rough overview of the SIR method. The model below is used to explore the theoretical properties of the SIR:

| (3.1) |

where are unknown dimensional row vectors, is independent of the covariates and is an arbitrary unknown function defined on . The linear space generated by ’s is called the efficient dimension reduction (e.d.r.) space and any linear combination of the ’s is referred as an e.d.r. direction. Li (1991) demonstrated that if was standardized by to have zero mean and identity covariance matrix, the inverse regression curve would be contained in the e.d.r. space. Accordingly, the principal component analysis method is applied to the estimated covariance matrix of the inverse regression curve. Hence, the leading vectors of the estimated covariance matrix can then be transformed to estimate the e.d.r. directions. In fact, Li (1991) showed that each would converge to an e.d.r. direction at rate of when stayed fixed.

The key condition for the SIR method is referred as the linearity condition, i.e. , for any , for some constants . To satisfy this condition, the distribution of the covariates is required to be elliptically symmetric. Such distributions include the normal distribution and the general symmetric elliptical distributions.

3.2 Elliptical sliced inverse regression

We construct our basic theorem for elliptical sliced inverse regression (ESIR) in this part. Here, “E” represents our focus on the heavy-tailed symmetric elliptical family.

Theorem 1.

Proof.

Following the conclusion of Theorem 3.1 in Li (1991), if we can prove that the linear space spanned by is the same as the space spanned by , we are done.

For any vector , let , then the span of can be written as and

where the first equality comes from the spectral decomposition of , the second one is established by the property that (see Marden (1999), Croux, Ollila and Oja (2002) ,Oja (2010) and Han and Liu (2016) for details), the third equality is given by Proposition 2.1 of Han and Liu (2016) and . The last equality verifies our guess. ∎

Theorem 1 is very similar to Theorem 3.1 of Li (1991). It’s not surprising in view of the close relationship between and in Section 2. Worth noting that we only assume that follows an elliptical distribution and we don’t pose any distribution restriction on while Bura and Forzani (2015) and Bura, Duarte and Forzani (2016) required be elliptically distributed and multivariate exponentially distributed respectively.

Let , where is the population Kendall’s tau matrix defined above in Section 2. Then, (3.1) can be rewritten as

| (3.2) |

where . Following the usage in Li (1991), we call the vector linearly generated by these ’s as the standardized e.d.r direction. For this new version of standardized covariates, we have the following corollary.

Corollary 1.

We then can easily derive that is degenerate in directions which are orthogonal to ’s. Thus, by Lemma 1 in the Appendix, we conclude that

| (3.3) |

is also degenerate in those directions mentioned above. Thus, the eigenvectors associated with the largest eigenvalues of are the standardized e.d.r. directions . We then transform to by for the original e.d.r. directions.

Given Corollary 1 and Lemma 1 in the Appendix, we construct the operating scheme for elliptical sliced inverse regression:

1. For each , we calculate a new standardized form of : , where and denote the sample Kendall’s tau matrix and the sample mean of respectively.

2. Divide the range of into “equal” slices, . Here, “equal” means that the number of the data points falling in each slice is equal to .

3. In each slice, compute the sample mean of : .

4. Form the Kendall’s tau matrix for :

| (3.4) |

then compute the eigenvalues and eigenvectors of .

5. Denote the largest eigenvectors of be . We transform them back to the original version by , that is, .

In this algorithm, we enforce the number of the data points in each slice to be fixed to so that we don’t need any weighting adjustment for the calculation of . In addition, the data points in the last slice may be not exactly which exerts little influence asymptotically. Our algorithm is essentially a generalized eigenvector problem. Please see more details in Li (2007) and Chen, Zou and Cook (2010). Of note, like SIR, the ESIR may not recover all the e.d.r. directions. One may refer to other dimension reduction methods like SAVE and DR to address such problems.

4 Asymptotic properties of elliptical slice inverse regression with diverging number of covariates

In this paper, we assume the data points stay the same in different slice, and the number of the slices and are both allowed to grow with the sample size . During the process of the proof, we use original rather than its standardization. The conclusion can then be directly extended to the standardized version.

Denote the inverse regression curve by and decompose as:

where with and and for the sample version,

and

where and and are the concomitants (Yang (1977)) of . For each slice, denote

Here, and . Of note, all the notations given above depend on . Under several mild conditions, we establish the consistency and convergence rate of the ESIR estimator in the following theorem.

Theorem 2.

Assume the following conditions hold:

(1). and for some constant , where .

(2). There exist some positive constants and such that

(3). The inverse regression curve is -stable regarding and . See more details in Lin, Zhao and Liu (2017).

Let be n independent samples of and suppose where . We have

The second part of Condition (1) is similar to that of Hsing and Carroll (1992), Zhu and Ng (1995) and Zhu, Miao and Peng (2006), which only requires rather than in their articles. The reason why we have a much milder condition here may originate from the first part of this condition, i.e. , is restricted to be elliptically distributed. Condition (2) is similar to Condition (A3) of Lin, Zhao and Liu (2017), where they imposed the boundary condition on the eigenvalues of while we assume the boundary property holds for . This extension is reasonable due to the connection between and . The last condition is exactly the same as the second part of Condition (A4) in Lin, Zhao and Liu (2017) and we put a remark (Remark 2) in Section 7 for this condition.

Theorem 2 shows that the effect of on the convergence rate is two-sided. Hence, we’d better choose a moderate size for the number of the slices, not too big or too small. What’s more, the growing rate of with respect to is roughly , noting that . Therefore, we only require to diverge to infinity with and satisfying to make an consistent estimator of .

Corollary 2.

Under conditions of Theorem 2, if the eigenvalues of is bounded away from zero and infinity and , with probability converging to we obtain

5 Numerical examples

We report several numerical results in this section, including different model designs for simulation data and a real data analysis of the Istanbul stock exchange data. The squared multiple correlation coefficient (Li (1991), Zhu, Miao and Peng (2006)) is used to measure the distance between the ESIR estimator and the central subspace for and their average to measure the distance between the space formed by all the ’s and the central subspace (Li (1991), Zhu, Miao and Peng (2006)). is calculated by

for any vector . Thus, a bigger squared multiple correlation coefficient indicates more estimation efficiency.

5.1 Single index model

Three types of single index models are considered under multivariate normal distribution and other five frequently used elliptical distributions in this part, including the multivariate Laplace distribution, multivariate symmetric logistic distribution, multivariate Student’ t distribution with degrees of freedom and and the multivariate Cauchy distribution.

Model (A1):

Model (A2):

Model (A3):

Model (A1) and (A2) come from Li (1991) and Model (A3) is stimulated by Example 3 of Zhu, Miao and Peng (2006). In all the above three models, , , and where and is the generating variable. We change the distribution of among the elliptical distributions mentioned above by adjusting the distribution of the generating variable . For multivariate logistic distribution, we choose the dependence parameter to be to indicate weak dependence among elements of . The sample size , the number of predictors and the number of the slices are chosen to be , and respectively. Table 1 reports the means and standard deviations (in parentheses) of after replicates under different simulation schemes.

Distr of normal Laplace logistic t () t () Cauchy Model (A1) SIR 0.95 0.88 0.90 0.71 0.37 0.10 (0.02) (0.07) (0.05) (0.19) (0.25) (0.12) ESIR 0.95 0.88 0.97 0.84 0.60 0.47 (0.02) (0.08) (0.00) (0.09) (0.30) (0.33) Model (A2) SIR 1.00 0.97 1.00 0.77 0.42 0.18 (0.00) (0.02) (0.00) (0.23) (0.28) (0.16) ESIR 1.00 0.98 0.97 0.93 0.81 0.48 (0.00) (0.01) (0.00) (0.05) (0.18) (0.36) Model (A3) SIR 0.91 0.82 0.90 0.66 0.34 0.16 (0.04) (0.12) (0.06) (0.25) (0.27) (0.15) ESIR 0.90 0.80 0.97 0.73 0.49 0.40 (0.05) (0.13) (0.01) (0.20) (0.30) (0.34)

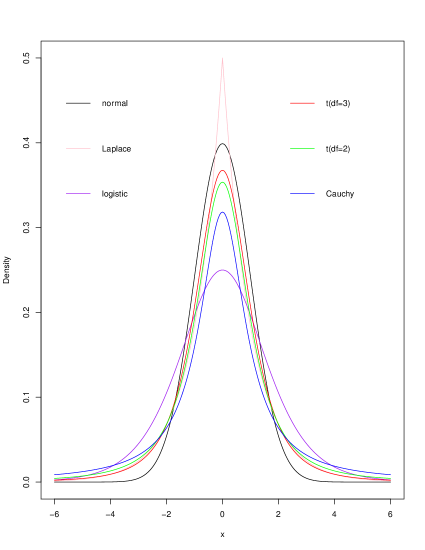

As can be seen from Table 1, the ESIR method outperforms the SIR method in almost all the simulation schemes. Furthermore, the efficiency gain is more significant when the tail of the distribution of tends to become heavier, which can be easily seen from the simulation results for , and Cauchy () distributed covariates where a smaller degree of Student’s t distribution indicates a heavier tail. For multivariate normal distribution and Laplace distribution, our ESIR estimator performs nearly as well as the SIR. Of note, the tail of the Laplace distribution is very close to that of normal distribution. See Figure 1 for the tails of the marginal distributions of .

5.2 Other models

Four models are considered in this section under case for six different elliptical distributions of . Unless otherwise noted, the simulation parameters used here are the same as those used in the first part for the single index model.

Model (B2):

Here, we reset , with , and .

Model (B3):

where the simulation parameters for this model are the same as model (B2). Both of Model (B2) and (B3) stem from Example 2 and 3 of Zhu, Miao and Peng (2006).

Model (B4):

where and . This model stems from Example 3 of Chen, Cook and Zou (2015). The distribution of deviates a little bit from the elliptical distribution. That is, let where , where with for and where .

Distr of normal logistic EC1 Model (B1) SIR 0.96 0.88 0.92 0.91 0.20 0.56 0.22 0.19 0.21 (0.02) (0.06) (0.04) (0.18) (0.18) (0.15) ESIR 0.94 0.76 0.85 0.99 0.18 0.59 0.89 0.84 0.87 (0.03) (0.16) (0.00) (0.17) (0.20) (0.24) Model (B2) SIR 0.99 0.81 0.90 0.99 0.71 0.85 0.48 0.44 0.46 (0.01) (0.22) (0.01) (0.27) (0.23) (0.26) ESIR 0.99 0.62 0.81 1.00 0.74 0.87 0.94 0.85 0.90 (0.01) (0.31) (0.00) (0.24) (0.13) (0.24) Model (B3) SIR 1.00 0.93 0.97 1.00 0.26 0.63 0.38 0.42 0.40 (0.00) (0.05) (0.00) (0.26) (0.21) (0.29) ESIR 1.00 0.78 0.89 1.00 0.23 0.62 0.88 0.87 0.88 (0.00) (0.20) (0.00) (0.24) (0.23) (0.20) Model (B4) SIR 0.97 0.66 0.82 1.00 0.67 0.84 0.43 0.42 0.43 (0.01) (0.20) (0.00) (0.21) (0.15) (0.07) ESIR 0.97 0.69 0.83 1.00 0.90 0.95 0.92 0.81 0.87 (0.01) (0.16) (0.00) (0.03) (0.17) (0.28)

Distr of t() t() Cauchy (t()) Model (B1) SIR 0.89 0.72 0.81 0.77 0.48 0.63 0.25 0.21 0.23 (0.10) (0.15) (0.16) (0.20) (0.21) (0.15) ESIR 0.93 0.54 0.74 0.90 0.49 0.70 0.79 0.66 0.73 (0.05) (0.24) (0.07) (0.27) (0.26) (0.28) Model (B2) SIR 0.98 0.42 0.70 0.90 0.36 0.63 0.67 0.33 0.50 (0.02) (0.32) (0.13) (0.27) (0.23) (0.22) ESIR 0.98 0.32 0.65 0.98 0.37 0.68 0.95 0.67 0.81 (0.02) (0.28) (0.03) (0.30) (0.09) (0.33) Model (B3) SIR 0.96 0.73 0.85 0.85 0.47 0.66 0.40 0.41 0.41 (0.05) (0.25) (0.15) (0.28) (0.27) (0.27) ESIR 0.99 0.59 0.79 0.95 0.47 0.71 0.86 0.68 0.77 (0.01) (0.30) (0.06) (0.31) (0.20) (0.28) Model (B4) SIR 0.93 0.33 0.63 0.85 0.22 0.54 0.62 0.12 0.37 (0.07) (0.24) (0.14) (0.20) (0.19) (0.13) ESIR 0.91 0.40 0.66 0.87 0.34 0.61 0.86 0.56 0.71 (0.05) (0.25) (0.10) (0.25) (0.15) (0.32)

In these cases, we include another elliptical distribution and remove the Laplace distribution, because the result of Laplace distribution is quite similar to that of normal distribution. Define with where F indicates F distribution. Here does not have finite mean. This distribution was also used in Han and Liu (2016). Table 2 and 3 exhibit a little bit difference from that of single index models. That is, while the first leading eigenvector or direction presents almost the same efficiency improvement as in the single index case, the second estimated direction performs not so well as the SIR estimator under several simulation settings. However, one can find that when the tail of the distribution gets heavier, the ESIR estimation for the second e.d.r. direction inclines to become more accurate. From a comprehensive point of view, the ESIR estimation efficiency is comparable or better than that of the SIR method. The robustness of ESIR is well demonstrated in Table 3, i.e. , when the tail of the distribution of the covariates goes heavier (from t(3) to t(1)), the performance of our proposed ESIR method is getting better.

To examine the influence of , and on the estimation efficiency of the ESIR estimator, we consider the combinations of , and in Model (B1) for Cauchy distributed covariates. Simulation results are presented in Table 4 after replicates.

H 5 10 20 40 p 5 10 30 5 10 30 5 10 30 5 10 30 SIR 0.47 0.24 0.12 0.47 0.27 0.12 0.46 0.24 0.10 0.41 0.24 0.09 0.42 0.21 0.08 0.41 0.22 0.07 0.42 0.24 0.08 0.41 0.17 0.08 ESIR 0.86 0.82 0.74 0.83 0.77 0.73 0.87 0.76 0.69 0.82 0.74 0.67 0.62 0.60 0.56 0.68 0.60 0.59 0.70 0.66 0.54 0.75 0.64 0.58 SIR 0.52 0.29 0.13 0.44 0.28 0.13 0.48 0.32 0.10 0.43 0.25 0.10 0.37 0.25 0.08 0.44 0.21 0.09 0.43 0.21 0.07 0.40 0.17 0.09 ESIR 0.87 0.78 0.70 0.86 0.75 0.63 0.85 0.79 0.72 0.87 0.74 0.68 0.66 0.56 0.49 0.67 0.58 0.57 0.66 0.62 0.54 0.65 0.66 0.56 SIR 0.48 0.29 0.11 0.48 0.28 0.10 0.48 0.26 0.12 0.43 0.25 0.09 0.40 0.21 0.08 0.42 0.22 0.06 0.39 0.19 0.07 0.39 0.20 0.07 ESIR 0.87 0.80 0.76 0.91 0.73 0.72 0.92 0.86 0.67 0.88 0.77 0.67 0.68 0.58 0.56 0.70 0.60 0.64 0.71 0.64 0.58 0.71 0.65 0.63

In this setting, we avoid reporting the stand deviations and the averages of and to improve the clarity of the simulation results. From Table 4, we find that when and stay fixed, the larger causes and to become smaller as high dimension reduces the estimation efficiency of both SIR and ESIR. However, our ESIR method is not so sensitive to dimensionality as SIR. Looking at the rows of Table 4, and regarding the ESIR method decrease much slower when gets larger. Secondly, when gets larger, both SIR and ESIR tend to perform better which fits our expectation. Lastly, the number of slices doesn’t have any significant impact on the estimation of both methods. It’s not surprising because Zhu and Ng (1995) and Zhu, Miao and Peng (2006) also found such a phenomenon in their simulation studies for SIR method. We don’t present simulation results for other distributions or other models here as they are quite similar to those of Table 4.

5.3 Real data analysis

In this part, we exploit the Istanbul stock exchange data set

(http://archive.ics.uci.edu/ml/datasets/ISTANBUL+STOCK+EXCHANGE) to demonstrate the superiority of ESIR in contrast with SIR when the explaining variables are characterized by non-Gaussian and heavy-tailed features. There are variables in the data sets from Jan 5, 2009 to Feb 22, 2011 (536 rows in all): Istanbul stock exchange national 100 index (ISE), Standard Poole 500 return index (SP), Stock market return index of Germany (DAX), Stock market return index of UK (FTSE), Stock market return index of Japan (NIKKEI), Stock market return index of Brazil (BOVESPA), MSCI European index (EU) and MSCI emerging markets index (EM). We choose EM as the response variable and the other variables as the covariates to formulate a regression problem.

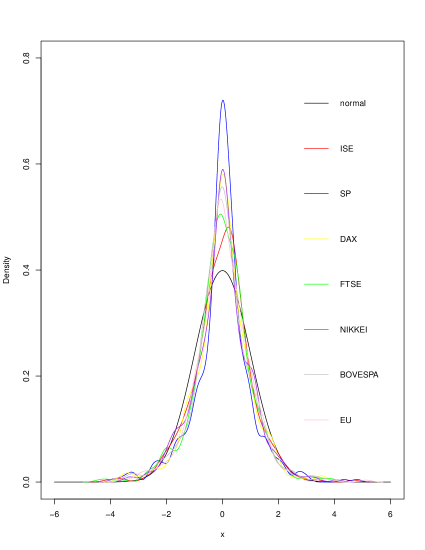

Firstly, we explore the marginal distributions of the independent variables. Two normality tests, Shapiro-Wilk test and Kolmogorov-Smirnovare test, are conducted to check the non-Gaussian feature of these variables. Table 5 summarizes the Shapiro-Wilk statistics and Kolmogorov-Smirnovare statistics. We find that the covariates are all considered as non-Gaussian distributed at the significance level of except that the conclusion on the variable ISE is questionable. We then plot the empirical densities of the standardized covariates against the stand normal distribution to illustrate the heavy-tailed pattern. Figure 2 exhibits this heavy-tailed character pretty clearly. It can also be seen from this figure that all the independent variables are symmetric about . Thus, we can readily apply our ESIR method to this data set.

Shapiro-Wilk Kolmogorov-Smirnov ISE SP DAX FTSE NIKKEI BOVESPA EU

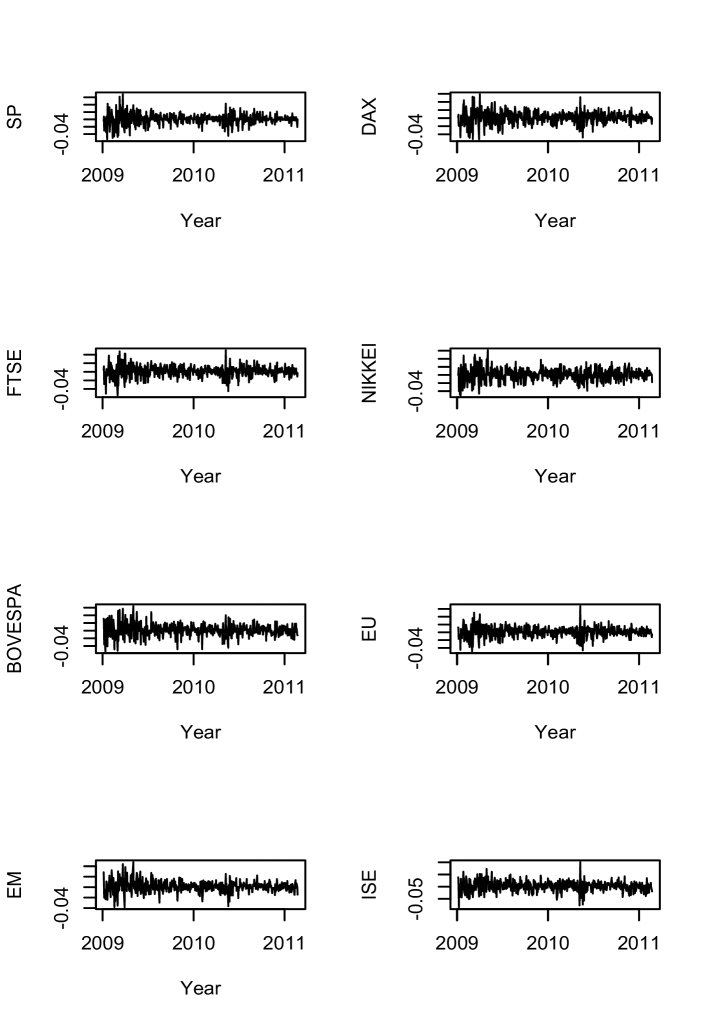

To determine the dimension of the central subspace, we apply the widely-used marginal dimension test with the number of slices being . The test result suggests that would be a proper choice. Therefore, we set the dimension of the central subspace to be and the number of slices . After estimating the e.d.r. directions, we get two new factors: and , then use them and , , and as explanatory variables to fit . The adjusted R-squared and F statistics are then exploited to compare the performances of ESIR and SIR. We first try samples of the whole time period (in fact, we used the first samples for computational convenience) and extend to investigate three shorter periods which simultaneously appear to possess significant heavy tails (see Figure 3). The results are presented in Table 6. Obviously, our method outperforms the SIR in all the four periods with significantly larger values of both R-squared and F statistics. This finding is complied with the simulation results above. It can be conjectured that the ESIR method would work better for individual asset returns and more risky financial derivatives.

Time period Adjusted F statistic SIR ESIR SIR ESIR 2009.01.05-2009.03.13 0.69 0.71 241.30 264.40 2009.03.30-2009.06.10 0.60 0.73 159.60 291.90 2010.04.27-2010.07.06 0.64 0.71 187.70 266.30 2009.01.05-2011.01.04 0.56 0.71 137.10 267.60

6 Discussion

In this paper, we propose the elliptically sliced inverse regression method for sufficient dimension reduction, which is a robust alternative to SIR for analysing high dimensional, elliptically distributed data. The main idea is to introduce the multivariate Kendall’s tau matrix in a generalized eigenvector problem to cope with the heavy-tailed elliptically distributed covariates. We then present the main theorem to demonstrate the rationality of the ESIR estimator and give a practical algorithm for the ESIR method. The asymptotic behavior of the ESIR estimator is studied and the corresponding convergence rate is obtained in high dimensional setting. Simulation results demonstrate that ESIR significantly improves the estimation efficiency for the central subspace under the setting of elliptically distributed covariates. Moreover, our method can be easily extended to most other sufficient dimension reduction methods such as SAVE, directional reduction (DR, Li and Wang (2007)) and principal fitted components (PFC, Cook and Forzani (2009)) etc. Please refers to Li (2007) and Chen, Zou and Cook (2010) for generalized eigenvector problem. Lastly, our method is of vital importance for analyzing heavy-tailed financial, genomic and bioimaging data. Of note, we do not spend energy on ascertaining the dimension of the central subspace in this paper and leave it for further study.

7 Proofs

7.1 Lemma 1

Lemma 1.

Assume and , where is the matrix of the eigenvectors and with being the corresponding eigenvalues. Letting denote the population Kendall’s tau matrix of the vector , by Proposition of Marden (1999) we have

where is a diagonal matrix containing the eigenvalues of .

Proof.

The proof for this Lemma is mainly based on the results of Marden (1999). For any , we have the decomposition below:

| (7.1) |

where is some orthogonal matrix, is coordinatewise symmetric about 0, that is

| (7.2) |

for any matrix with and and is some centering vector. We assume that exists, and without loss of generality, that with for . Thus, we obtain , where with .

7.2 Proof of Theorem 2

Proof.

where and for .

For the first part , by Theorem 3.1 of Han and Liu (2016), if , we can easily obtain

where . The last equality is ensured by Condition (2).

For the second part , if Condition (3) stands, from Remark 1 and 2 in Lin, Zhao and Liu (2017), we get

| (7.5) |

Using the relationship of and in Section 2 and the second part of Condition (1), we obtain

For the third part , elementary probability theory tells us that the elements of converge to those of at the rate of . Thus, and . Now we introduce some notation for easy presentation: and . Then we only need to consider the term below:

Condition (1) implies that . Then, and . Thus, . In view of , we obtain

∎

Remark 1.

Although Han and Liu (2016) required in their Theorem 3.1, one can easily find that it is not a necessary condition by reviewing their proof, which means in our paper that we don’t need any restriction on the distribution of for the consistency. That’s a quite good property, because it is not trivial to test the distribution of .

Remark 2.

The convergence rate for the second part does not seem quite apparent. In fact, there is an underling assumption. That is, we believe that the weights plugged into (2.1) would not change the decreasing rate of (7.5), which is a power of . This speculation is tenable, because the weights take effects as the reciprocal of the distance. This assumption could be further demonstrated by the following finding:

7.3 Proof of Corollary 2

Proof.

From Theorem 3.2 of Han and Liu (2016) in combination with that the eigenvalues of are bounded away from zero and infinity, we have , where the last equality can be demonstrated by

Moreover, in view of Condition (2) in Theorem 2, we can easily get . Together with the result of Theorem 2 about , we complete the proof.

∎

References

- Bura and Cook (2001a) Bura, E. and Cook, R. D. (2001a). Extending sliced inverse regression: the weighted Chi-squared test. Journal of the American Statistical Association, 96, 996–1003.

- Bura and Cook (2001b) Bura, E. and Cook, R. D. (2001b). Estimating the structural dimension of regressions via parametric inverse regression. Journal of the Royal Statistical Society, B, 63, 393–410.

- Bura and Forzani (2015) Bura, E. and Forzani, L. (2015). Sufficient reductions in regressions with elliptically contoured inverse predictors. Journal of the American Statistical Association, 110, 420–434.

- Bura, Duarte and Forzani (2016) Bura, E., Duarte, S. and Forzani, L. (2016). Sufficient reductions in regressions with exponential family inverse predictors. Journal of the American Statistical Association, 111, 1313–1329.

- Chen, Cook and Zou (2015) Chen, X., Cook, R. D. and Zou, C. L. (2015). Diagnostic studies in sufficient dimension reduction. Biometrika, 102, 545–558.

- Chen, Zou and Cook (2010) Chen, X., Zou, C. L. and Cook, R. D. (2010). Coordinate-independent sparse sufficient dimension reduction and variable selection. The Annals of Statistics, 38, 3696–3723.

- Cook (1994) Cook, R. D. (1994). On the interpretation of regression plots. Journal of the American Statistical Association, 89, 177–189.

- Cook (1996) Cook, R. D. (1996). Graphics for regressions with a binary response. Journal of the American Statistical Association, 91, 983–992.

- Cook (1998) Cook, R. D. (1998). Regression Graphics: Ideas for Studying Regressions through Graphics. Wiley, New York.

- Cook (2000) Cook, R. D. (2000). SAVE: a method for dimension reduction and graphics in regression. Communications in Statistics, Part A, Theory and Methods, 29, 2109–2121.

- Cook (2007) Cook, R. D. (2007). Fisher Lecture: Dimension deduction in regression (with Discussion). Statistical Science, 22, 1–26.

- Cook and Forzani (2009) Cook, R. D. and Forzani, L. (2009). Likelihood-based sufficient dimension reduction. Journal of the American Statistical Association, 104, 197–208.

- Cook and Ni (2005) Cook, R. D. and Ni, L. (2005). Sufficient dimension reduction via inverse regression: A minimum discrepancy approach. Journal of the American Statistical Association, 100, 410–428.

- Cook and Weisberg (1991) Cook, R. D. and Weisberg, S. (1991). Comment on sliced inverse regression for dimension reduction by K. C. Li. Journal of the American Statistical Association, 86, 328–332.

- Croux, Ollila and Oja (2002) Croux, C., Ollila, E., and Oja, H. (2002). Sign and rank covariance matrices: statistical properties and application to principal components analysis. In Statistics for Industry and Technology, pages 257–69. Birkhauser.

- Fan, Liu and Wang (2015) Fan, J., Liu, H. and Wang, W. (2015). Large covariance estimation through elliptical factor models. arXiv preprint arXiv:1507.08377.

- Han and Liu (2016) Han, F. and Liu, H. (2016). ECA: high dimensional elliptical component analysis in non-Gaussian distributions. Journal of the American Statistical Association, DOI: 10.1080/01621459.2016.1246366.

- Hsing and Carroll (1992) Hsing, T. and Carroll, R. J. (1992). An asymptotic theory for sliced inverse regression. The Annals of Statistics, 20, 1040–1061.

- Hult and Lindskog (2002) Hult, H., and Lindskog, F. (2002). Multivariate extremes, aggregation and dependence in elliptical distributions. Advances in Applied probability, 34, 587–608.

- Jing, Shao and Wang (2003) Jing, B. Y., Shao, Q. M. and Wang, Q. (2003). Self-normalized cramer-type large deviations for independent random variables. The Annals of Probability, 31, 2167–2215.

- Johnstone and Lu (2009) Johnstone, I. and Lu, A. (2009). On consistency and sparsity for principal components analysis in high dimensions. Journal of the American Statistical Association, 104, 682–693.

- Li and Wang (2007) Li, B. and Wang, S. L. (2007). On directional regression for dimension reduction. Journal of the American Statistical Association, 102, 997–1008.

- Li, Zha and Chiaromonte (2005) Li, B., Zha, H. and Chiaromonte, F. (2005). Contour regression: A general approach to dimension reduction. The Annals of Statistics, 33, 1580–1616.

- Li (1991) Li, K. C. (1991). Sliced inverse regression for dimension reduction. Journal of the American Statistical Association, 86, 316–342.

- Li (1992) Li, K. C. (1992). On principal Hessian directions for data visualization and dimension reduction: Another application of Stein s lemma. Journal of the American Statistical Association, 87, 1025 C-1039.

- Li (2007) Li, L. (2007). Sparse sufficient dimension reduction. Biometrika, 94, 603–613.

- Lin, Zhao and Liu (2017) Lin Q., Zhao Z. and Liu J. S. On consistency and sparsity of sliced inverse regression in high dimensions, The Annals of Statistics(accepted), arXiv:1507.03895.

- Marden (1999) Marden, J. (1999). Some robust estimates of principal components. Statistics and Probability Letters, 43(4), 349–359.

- Ma and Zhu (2012) Ma, Y. and Zhu, L. (2012). A semiparametric approach to dimension reduction. Journal of the American Statistical Association, 107, 168–179.

- Oja (2010) Oja, H. (2010). Multivariate Nonparametric Methods with R: An Approach based on Spatial Signs and Ranks, volume 199. Springer, New York.

- Sheng and Yin (2013) Sheng, W. and Yin, X. (2013). Direction estimation in single-index models via distance covariance. Journal of Multivariate Analysis, 122, 148–161.

- Sheng and Yin (2016) Sheng, W. and Yin, X. (2016). Sufficient dimension reduction via distance covariance. Journal of Computational and Graphical Statistics 25, 91–104.

- Xia et al., (2002) Xia, Y., Tong, H., Li, W. K. and Zhu, L. (2002). An adaptive estimation of dimension reduction space (with Discussion). Journal of the Royal Statistical Society, B, 64, 363–410.

- Yang (1977) Yang, S. S. (1977). General distribution theory of the concomitants of order statistics. The Annals of Statistics, 5, 996–1002.

- Zhu and Fang (1996) Zhu, L. X. and Fang, K. T. (1996). Asymptotics for kernel estimate of sliced inverse regression. The Annals of Statistics, 24, 1055–1068.

- Zhu and Ng (1995) Zhu, L. X. and Ng, K. W. (1995). Asymptotics of sliced inverse regression. Statistica Sinica, 5, 727–736.

- Zhu, Miao and Peng (2006) Zhu, L. X., Miao, B. Q. and Peng, H. (2006). On sliced inverse regression with high-dimensional covariates. Journal of the American Statistical Association, 101, 630–643.

- Zhu, Ohtaki and Li (2006) Zhu, L. X., Ohtaki, M. and Li, Y. X. (2006). Extensions of sliced inverse regression Cbased algorithms. Technical report, University of Hong Kong, Dept. of Statistics and Actuarial Science.